Zai Lab: The Bridge to the Middle Kingdom

I. Introduction: The Arbitrage of Innovation

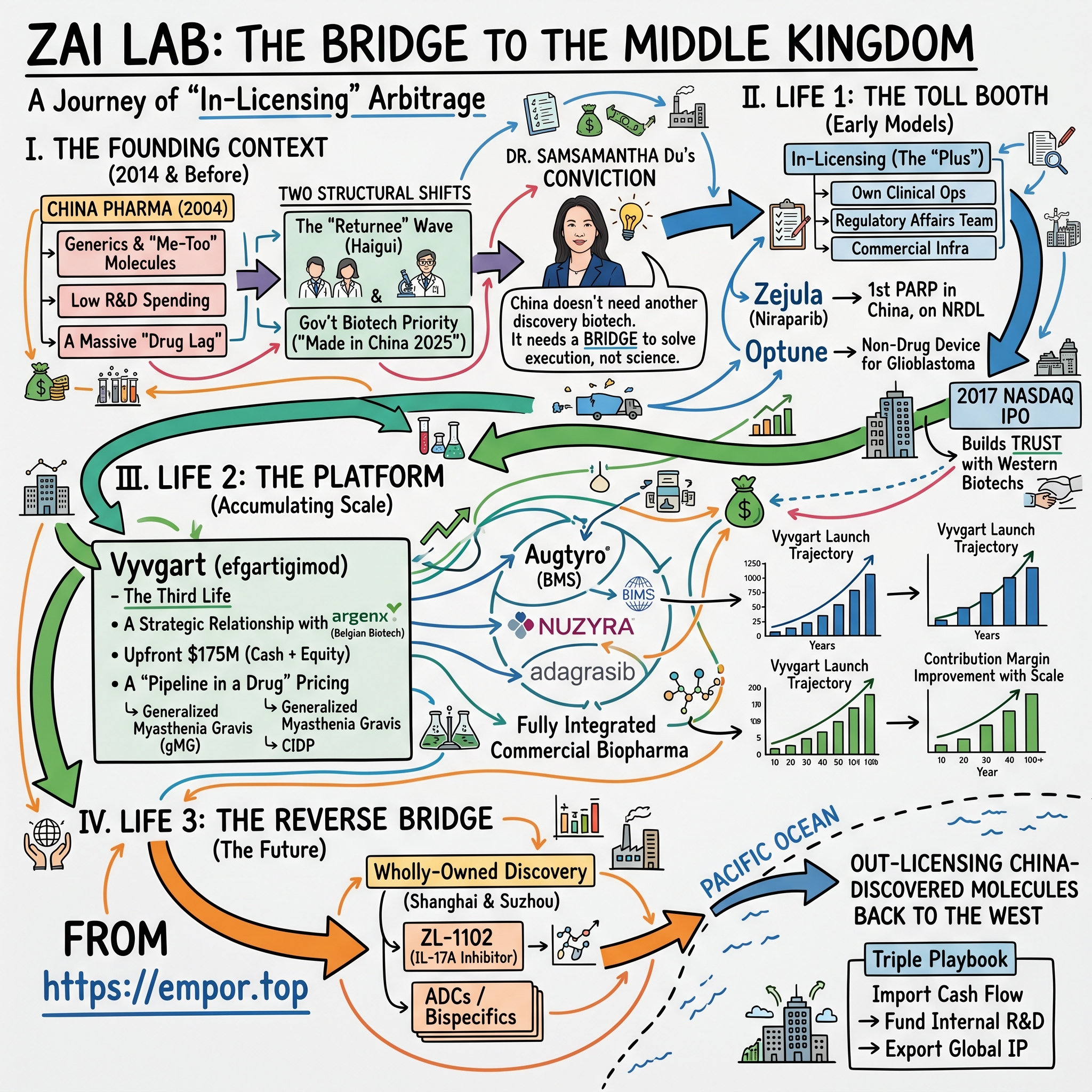

Picture a conference room on the 18th floor of a Pudong office tower in early 2014. Outside the window, the Lujiazui skyline glitters with the cranes of a country still building itself. Inside the room sits Dr. Samantha Du, 49 years old, holding a printout of the U.S. National Cancer Institute's pipeline. She has been circling drug names with a red pen — molecules that have already cleared Phase 2 in Boston or San Diego, but which Chinese cancer patients will not see for another half-decade. Possibly never. Around the table are two associates from Sequoia Capital China and one from Qiming Venture Partners. The pitch she is about to make sounds, on paper, almost insulting to the venture capital ear: she does not want to discover a drug. She does not want to invent a molecule. She wants to license other people's medicines.

What she is actually proposing, however, is one of the cleverest arbitrages in modern healthcare. The "Great Wall" of Chinese pharmaceutical regulation — the years-long delay between an FDA approval and a National Medical Products Administration approval, the duplicative bridging trials, the inscrutable politics of the National Reimbursement Drug List — is widely treated by Western biotechs as a barrier. Du sees it as a moat. If you can build the only credible vehicle that runs through the wall, you can charge a toll on every blockbuster that enters the world's second-largest healthcare market for the next thirty years.

That toll booth grew up. Today, in April 2026, Zai Lab Limited trades dual-listed on Nasdaq under the ticker ZLAB and on the Hong Kong Stock Exchange under 9688.HK. Its market capitalization sits in the low-to-mid single-digit billions of dollars — a number that has yo-yoed dramatically with the fortunes of Chinese biotech as an asset class, but which understates the strategic position the company has assembled. Zai is no longer just a toll booth. It is a fully integrated commercial-stage biopharma running a portfolio of in-licensed blockbusters — Vyvgart, Zejula, Optune, Augtyro, NUZYRA, VYVGART Hytrulo — alongside a quietly maturing pipeline of internally discovered molecules that the company increasingly intends to send back across the Pacific in the other direction.

The thesis of this episode is that the "in-licensing" model that Zai pioneered in China has gone through three distinct lives. Life one was the toll booth — collect a license, run a bridging trial, reap a royalty. Life two was the platform — accumulate enough commercial infrastructure that the marginal cost of adding the next drug approached zero. Life three, which is just beginning, is the reverse bridge — using the cash flows from imported drugs to fund original Chinese discovery, then out-licensing those discoveries to the West. This is the same arc, give or take a decade, that Korean conglomerates ran in consumer electronics, that Taiwanese firms ran in semiconductors, and that Chinese internet companies ran in mobile. It is, in a sense, the playbook of a developing economy growing up in real time.

Over the next two-and-change hours, the journey runs from a monsoon-season conversation in Shanghai to the boardroom of argenx in Ghent, through the bureaucratic labyrinth of the NMPA, into the world of myasthenia gravis and tumor-treating fields, and finally to a question every long-term investor in this name eventually has to answer: when the bridge is built, what is the toll worth?

II. The Founding Context: China's "Returnee" Wave

To understand why Zai Lab could exist, you have to understand why it could not have existed in 2004. A decade before Du's pitch meeting, the Chinese pharmaceutical industry was, to put it generously, an industrial archaeology site. There were roughly five thousand domestic drug manufacturers. The vast majority produced generics, and a depressingly large fraction produced what the industry euphemistically called "me-too" molecules — chemical close-cousins of Western originator drugs, manufactured under licensing arrangements that would not have survived a Hatch-Waxman challenge in the United States. Domestic R&D spending as a percentage of revenue at the largest Chinese pharma companies was in the low single digits. The original-research output of Chinese biology, despite a vast and growing PhD pool, was concentrated in academic labs whose translational-medicine infrastructure was nonexistent.

Layered on top was the China Food and Drug Administration, the NMPA's predecessor, which operated with a backlog measured in years. A drug approved by the FDA in 2010 might begin a Chinese clinical trial in 2013, complete it in 2017, and reach Chinese patients in 2019 — assuming everything went well, which it usually did not. The polite phrase for this was "drug lag." The impolite version, used quietly in oncology wards in Shanghai and Beijing, was that Chinese cancer patients were dying of yesterday's disease while the West was treating them with tomorrow's medicine.

Two structural shifts changed the air pressure in the room. The first was the so-called "returnee wave," or haigui — overseas-trained Chinese scientists, most of whom had spent fifteen or twenty years at Pfizer, Merck, Genentech, and Novartis, who began coming home in waves in the late 2000s and early 2010s. They brought with them the operating playbook of Western biotech: how to design a registrational trial, how to negotiate with regulators, how to write a CMC dossier that would actually be approved. The second shift was the Chinese government's growing and unmistakable signal that biotech was a strategic priority — language that would later crystallize into "Made in China 2025" but which, by 2014, was already shaping capital flows from the National Social Security Fund and from local government investment vehicles in Suzhou, Hangzhou, and Shanghai.

Samantha Du was the archetypal returnee — and arguably its most influential. Born in China, she had earned a PhD from the University of Cincinnati, joined Pfizer in 1995 in Connecticut, and risen through the ranks of business development. In 2001, she joined Hutchison MediPharma — better known later as HUTCHMED — as one of its founding scientists, helping to build what became, for a time, China's most credible domestic oncology pipeline. By 2014 she had served as venture partner at Sequoia Capital China, where she had a front-row seat to every Western biotech trying to figure out the China question. She was, to use a poker term, the player who had seen every hand in the deck.

The conviction that crystallized for her was simple. China did not need another discovery-stage biotech. There were already thousands of those, most of them subscale. What China needed was one company that could solve, end-to-end, the problem of taking a Western blockbuster from BLA approval through bridging trial through NMPA registration through National Reimbursement Drug List negotiation through hospital formulary listing through actual prescription by a Chinese oncologist. This was less a science problem than an operating problem — and, crucially, it was a problem that Western biotechs were uniquely poorly equipped to solve themselves.

Sequoia and Qiming wrote the seed checks. The pitch landed because the venture investors understood that Du was not selling a science risk; she was selling an execution risk that she was unusually well-positioned to underwrite. The mission statement that emerged, reportedly inscribed on the wall of the first Pudong office, was almost utilitarian: "Bringing the world's best medicines to China, faster." The unstated corollary was that this also meant bringing the world's best returns to Chinese biotech investors, faster.

The first molecule on the whiteboard was not a Zai discovery. It was a PARP inhibitor called niraparib, sitting inside a small Boston biotech called Tesaro. It would become Zejula. And it would teach Zai Lab how to walk.

III. The "VIP" Model and Early Inflections

Inside Zai's Shanghai headquarters, the model has a name that sounds slightly underwhelming until you appreciate what it actually is: VIP, for Variation on In-Licensing Plus. The "Plus," in Zai's framing, is the part Western analysts kept missing. Conventional in-licensing is a contract: a Western biotech sells the China rights to its drug to a local distributor, who handles registration and sales in exchange for a milestone-and-royalty arrangement. That is what Bayer and Pfizer have done with Chinese partners for thirty years. The arrangement is asset-light on both sides, and it produces predictably mediocre results, because neither party has skin in the long-term value of the asset.

What Zai did differently was treat the in-licensed asset as if it were a wholly-owned program. The company invested in its own clinical operations, its own regulatory affairs team, its own medical-affairs and commercial infrastructure. It paid larger upfront fees to its partners — sometimes startlingly larger — in exchange for broader rights, deeper data access, and longer commercial windows. And it negotiated the contracts so that Zai's economics scaled with the asset's success, not just with milestones. In effect, Zai became the China subsidiary that the Western biotech could never afford to build itself.

The first big bet was Tesaro's niraparib in 2016. Niraparib was a once-daily oral PARP inhibitor — a class of cancer drugs that exploits a vulnerability in tumors with defective DNA-repair machinery, particularly ovarian cancers carrying BRCA mutations. The science was elegant; the U.S. commercial opportunity was real but constrained by competition from AstraZeneca's olaparib. For Tesaro, which was burning cash and trying to fund a U.S. launch, the China rights were a nice-to-have; for Zai, they were the cornerstone of a franchise. The deal closed with Zai paying low-single-digit-millions upfront plus development and sales milestones, and royalties tiered into the high teens. By 2019, Zejula had received NMPA approval as the first PARP inhibitor approved in China for the maintenance treatment of recurrent ovarian cancer. By 2020, it had been added to the National Reimbursement Drug List, unlocking commercial volumes that would have been impossible in self-pay form.

The second early bet was even more interesting from a strategy standpoint. Optune, NovoCure's "tumor treating fields" device, was not a drug at all; it was a wearable medical device that delivered alternating electric fields through transducer arrays glued to a patient's shaved scalp, disrupting mitosis in glioblastoma cells. The science was unconventional, the device was bulky, and the U.S. commercial uptake had been slow because oncologists trained on chemotherapy were skeptical of physics. Zai signed for the greater China rights and, in doing so, quietly told the world that "in-licensing" at Zai was not just about pills. It was about any modality that could meaningfully change Chinese patient outcomes.

The inflection point was the September 2017 Nasdaq IPO. Zai priced 5.4 million American Depositary Shares at $18 apiece, raising approximately $172 million on a fully-diluted equity value of roughly $850 million. The first-day pop took the stock above $30, and within two years it would trade above $80. The IPO was significant for reasons that went beyond the cash. It was a signal — to U.S. biotech CEOs and business-development heads — that there was now a publicly-listed, SEC-reporting, Western-governance-standards Chinese biotech that they could partner with without taking on the perceived "China risk" that had spooked their boards for a decade. The "Bridge" narrative was, fundamentally, a marketing narrative aimed at solving the China discount on Western biotech transactions, and the IPO made it credible.

What Zai understood, and what its competitors did not, was that the scarcest resource in this business was not capital and not science. It was trust. Western biotech CEOs needed to believe that the China partner would not slow-walk the development program, would not divert clinical-trial data to the parent company's own discovery efforts, would not under-invest in commercialization in order to over-invest in the next deal. Zai's transparency, public-company governance, and bench of returnee executives with intact U.S. references made it the default choice. Once you are the default choice, every subsequent deal gets easier — and every subsequent deal makes you more of the default. This is, although the company would never put it this way, a network-effect business hiding inside a pharmaceutical balance sheet.

IV. Management Deep-Dive: The Du Doctrine

The cliché in biopharma is that the company is the founder, and in Zai Lab's case the cliché is unusually accurate. Samantha Du serves as Founder, Chief Executive Officer, and Chairwoman of the Board, an accumulation of titles that would normally raise governance flags but which, in Zai's case, reflects something closer to operational reality. She is the person U.S. biotech CEOs call when they want to know whether to do a China deal. She is also the person who decides which drugs Zai chases.

Du's biography reads as if it were optimized for the role she ended up filling. The Cincinnati PhD gave her American scientific credibility; the Pfizer years gave her business-development chops in a culture that rewarded transactional precision; the Hutchison MediPharma years gave her direct experience building a Chinese drug-development operation from a standing start; the Sequoia years gave her access to the global biotech deal flow and the venture-investor's instinct for triage. Her style, by all accounts of those who have negotiated against her, is meticulous, patient, and quietly competitive. She is known for asking exactly one more question than her counterparties expect.

The shareholding structure reflects a level of skin-in-the-game that has held up through one of the worst China-biotech bear markets on record. Du and her affiliated entities have remained the largest individual shareholder group, and the company has taken pains to structure executive compensation around development milestones, regulatory approvals, and sales ramp metrics — in other words, around speed-to-market. This matters more than it sounds. The classical biotech compensation problem is that scientific tenure is rewarded over commercial outcomes; at Zai, the incentive arrows all point at "get the drug to the patient and into the formulary."

The management bench around her tells the story of the company's evolution. The earliest hires were heavy on R&D and regulatory affairs — people who knew how to design a bridging trial and shepherd it through the NMPA. The middle wave brought in commercial leaders, many recruited from the Chinese subsidiaries of GSK, Roche, and Eli Lilly, with established hospital relationships and KOL networks. The most recent wave has tilted toward chief commercial officers, U.S.-listing-experience CFOs, and global-development heads — signaling, unmistakably, that Zai is no longer a deal-shop but an operating company. The transition from "we license drugs" to "we sell drugs" is, in retrospect, the single most important organizational shift Zai has made.

Governance straddles two cultures, which is harder than it sounds. The board includes Western biotech veterans whose intuitions on capital allocation and clinical strategy are calibrated to the Cambridge–San Francisco axis; it also includes investors and operators whose intuitions on hospital procurement, provincial reimbursement politics, and regulatory relationships are calibrated to Beijing and Shanghai. These two intuition sets do not always agree. The compensation for that friction is that, when they do converge on a decision, the decision tends to be more robust than either group would have produced alone.

The Du doctrine, distilled, has three pillars. First, speed beats originality in the early innings of a developing market — getting the eighth-best drug to market three years early is more valuable than getting the best drug to market three years late. Second, commercial infrastructure compounds — every new sales rep, every new hospital relationship, every new reimbursement-team negotiator increases the value of every future asset. Third, trust is the moat — a single botched partnership, a single allegation of data diversion, would unwind a decade of relationship-building, and so the marginal dollar of governance investment is almost always worth it. None of these pillars is glamorous. All of them, applied consistently for twelve years, are why Zai Lab exists in its current form.

It is also worth saying out loud what Du herself rarely says: she has built an organization that depends less and less on her personally over time, and that is the rarest and most valuable thing a founder-CEO can do. The Vyvgart launch, the largest commercial test in Zai's history to date, was executed by a commercial organization whose hospital coverage, reimbursement strategy, and patient-services infrastructure were operationally independent of any individual decision Du needed to make. The bridge has institutional engineering now.

V. M&A and Capital Deployment: The Benchmarking

If Zai's first life was Zejula and its second life was Optune, its third life — the one currently driving the equity story — is Vyvgart. The deal that brought it to China is the cleanest case study available of how the modern Zai allocates capital, and it deserves to be examined closely.

The asset is efgartigimod, branded Vyvgart in most of the world. It is a humanized IgG1 antibody fragment that binds the neonatal Fc receptor, accelerating the degradation of pathogenic IgG autoantibodies. Translated into English: it is a remarkably elegant treatment for a class of autoimmune diseases — generalized myasthenia gravis being the lead indication — in which the patient's immune system mistakenly produces antibodies that attack their own tissues. The drug essentially tells the body to throw the bad antibodies away faster. It was discovered by argenx, a Belgian biotech spun out of Ghent University, and it represented the company's first commercial-stage asset.

In January 2021, Zai Lab announced a strategic collaboration with argenx to develop and commercialize efgartigimod in greater China. The structure: an upfront payment of $75 million in cash, a $100 million equity investment by Zai into argenx common stock at a premium to market, plus tiered double-digit royalties on Chinese sales. The total upfront commitment, including the equity, was $175 million — an extraordinary number for a Chinese in-licensing deal at the time and roughly 3-4x the largest comparable Chinese in-licensing transactions of the prior cycle.

Standard biotech analyst reaction at the time was to ask whether Zai had overpaid. The market royalty for an autoimmune asset of this profile would conventionally clear at 10-15% on net sales, and Zai had paid a premium that compressed its forward economics. The counterargument, which has aged well, is that what Zai actually bought was not just one molecule but a strategic relationship. The argenx pipeline includes multiple follow-on indications for efgartigimod (chronic inflammatory demyelinating polyneuropathy, primary immune thrombocytopenia, others under study), a follow-on subcutaneous formulation (Vyvgart Hytrulo), and a deeper antibody platform with several next-generation candidates. By writing a check large enough to be argenx's most important Asian relationship, Zai positioned itself to be the natural partner for everything that came next from Ghent. That is "pipeline in a drug" pricing, and at scale it changes the IRR math considerably.

NMPA approval of Vyvgart for generalized myasthenia gravis came in 2023, followed by inclusion on the National Reimbursement Drug List in early 2024. The Chinese launch trajectory through 2024 and 2025 was, by Chinese standards for a specialty autoimmune drug, exceptional — outperforming the trajectory of analogous launches that had taken five to seven years to reach steady-state penetration. The follow-on indications, particularly CIDP, are now rolling through Chinese registration on a fast-follower timeline that the original deal structure made possible.

The same playbook has been re-run, with variations, in other deals. The collaboration with Bristol-Myers Squibb on Augtyro (repotrectinib), an ROS1/NTRK inhibitor for non-small-cell lung cancer with specific oncogenic fusions, gave Zai a beachhead in next-generation precision oncology. Earlier collaborations with Paratek brought NUZYRA, with Mirati brought adagrasib (since the BMS-Mirati transaction, repositioned within the BMS portfolio), and with various other Western partners brought a portfolio breadth that, by the mid-2020s, made Zai one of the most diversified specialty biopharmas operating in greater China.

The benchmarking question that matters more than any individual deal is: how much value does Zai create per dollar of upfront M&A spend, relative to alternative deployments of the same capital? Compared to the traditional Chinese pharma giants — Jiangsu Hengrui in particular — Zai's "value per head" on its in-licensing strategy has materially outperformed Hengrui's internal R&D spend, in the sense that Zai has gotten more revenue-generating assets to NMPA approval per dollar invested. The cost of this outperformance is dependence on Western originators; the benefit is shorter cycle times and lower scientific risk.

Equally important is what Zai did not do. The 2021 biotech bubble produced a parade of ambitious China in-licensing transactions at valuations that look, in retrospect, like they were priced for permanent zero interest rates. LianBio, Everest Medicines, and several other Zai-clones struck deals at upfront-and-equity packages that the subsequent bear market made impossible to support. LianBio ultimately wound down its operations and returned capital to shareholders. Zai was not immune to the 2022-2023 share-price drawdown — it lost more than 70% of its peak market capitalization — but it had retained sufficient cash discipline and license selectivity that the operating business never had to be restructured. The deals Zai did not do, in a vintage where bad deals were available cheaply, may matter more than the deals it did.

VI. "Hidden" Growth and the Internal Pivot

The narrative around Zai Lab as an in-licensing company is so dominant that it tends to obscure the second business growing inside the first one. By 2020, Zai had begun systematically investing in wholly-owned discovery — building an internal R&D engine in Shanghai and Suzhou whose output it could either commercialize itself in China or, more interestingly, license out to Western partners. The first widely-discussed example was ZL-1102, a humanized IL-17A inhibitor in development for chronic plaque psoriasis. ZL-1102 will not, by itself, transform the company's economics. It is significant for what it represents: the first asset for which Zai owns the global intellectual property.

The internal pipeline has expanded into oncology bispecifics, antibody-drug conjugates, and select autoimmune targets. The strategic logic is clear. A pure in-licensing company is structurally a price-taker — its margins are set by the upfront and royalty terms its Western partners demand, and its multiple is constrained by the perception that it does not own its own destiny. A company that mixes in-licensed and self-discovered assets in a portfolio escapes both constraints. The royalty-paying assets fund the discovery engine; the discovery engine produces optionality on global rights; the global-rights optionality re-rates the multiple.

The "reverse bridge" thesis has begun to show up in actual transactions across the Chinese biotech sector. Innovent, BeiGene, Hengrui, and a handful of others have begun out-licensing Chinese-discovered assets — particularly antibody-drug conjugates and bispecifics — to Western pharma and biotech at upfront economics that, in 2018, would have been considered fantasy. Zai's positioning here is more nascent than the leaders'. But the company's combination of Western-governance credibility, returnee-led R&D, and the existing deal-flow relationships that made it the bridge in the first place make it structurally well-positioned to participate as the reverse-direction flow of molecules accelerates.

The portfolio split, viewed by therapeutic area, tells the story of a company in transition. The oncology franchise — Zejula, Optune, Augtyro, NUZYRA — is the steady cash generator. It is unlikely to grow at headline-stealing rates from here, but it generates the contribution margin that funds everything else. The autoimmune and neurology franchise — anchored by Vyvgart, with KarXT-related opportunities being navigated through the BMS-Karuna transaction's complex partnership architecture — is the hyper-growth engine. The optionality value in this segment is significant: Vyvgart's ramp is still in early innings in China, the CIDP indication is just landing, and the broader FcRn-inhibition platform has multi-indication potential that argenx is actively expanding worldwide.

The Optune business deserves a separate paragraph, because it is structurally unlike everything else Zai sells. It is not a pill, not an antibody, not a small molecule. It is a wearable device that delivers electric fields, paired with a service business — patient training, transducer-array fitting, technical support, replacement logistics — that operates on something closer to a software-as-a-service economics than to traditional pharma. Average revenue per patient is high, but the business requires a physically present support organization in every major Chinese metropolitan area where glioblastoma patients are concentrated. It is a fascinating microcosm of what "biotech" can mean in the 2020s, and it gives Zai's commercial organization muscles that no traditional pharma organization develops.

A second-layer consideration worth naming briefly: the wholly-owned pipeline meaningfully changes the company's exposure to the geopolitical risk premium that has weighed on China-listed biotechs since 2022. A company that depends entirely on Western in-licensed assets is, in some sense, hostage to the willingness of Western boards to keep doing China deals. A company with its own discovery output is the seller, not just the buyer, in those conversations. That symmetry matters for long-term re-rating.

VII. The 7 Powers and Porter's Five Forces

It is fashionable in 2026 to apply Hamilton Helmer's 7 Powers framework to every business analysis, and most of the time the application is forced. Zai Lab is one of the cases where the framework genuinely earns its keep, because the company's competitive advantages do not come from any single source — they come from a stack of mutually reinforcing structural moats that took twelve years to assemble.

Cornered Resource. The cornered resource at Zai is not a molecule and not a patent; it is a combination of regulatory know-how and KOL relationships that takes a decade to build and cannot be cloned with money. The Chinese clinical trial system runs on relationships — with principal investigators at the top thirty academic medical centers, with NMPA reviewers whose scientific preferences are well-understood by the people who have submitted dozens of dossiers, with hospital pharmacy committees who decide which drugs make it onto formulary. Zai's regulatory affairs and medical-affairs teams have been doing this for a decade. A new entrant could hire individual people, but reproducing the institutional memory and the network density would take five years at minimum. This is a textbook cornered resource, and it is the single most underappreciated component of the moat.

Counter-Positioning. Zai's structural advantage against Big Pharma's China subsidiaries is that it does not have a global head office in New Jersey or Basel that needs to approve every Chinese commercial decision. Pfizer China, Roche China, Novartis China are good organizations, but they operate on a clock that includes board reviews, global brand-strategy meetings, and the political weight of being a multi-hundred-billion-dollar global enterprise that cannot move quickly without producing collateral effects elsewhere. Zai can decide on a Tuesday to reposition a Chinese reimbursement strategy and ship the change by Friday. This is not just a speed advantage; it is a structural feature of how the two organizations make decisions that the larger one cannot easily replicate.

Network Effects. The network effect is in deal flow. Every successful Western partnership Zai completes makes the next Western partnership easier — for Zai and harder for its competitors. Western biotech business-development teams are small and word-of-mouth-driven; the question they ask about a potential Chinese partner is "who did your last U.S. partner call as a reference?" Zai has been the answer for years now, and the asymmetry compounds. LianBio, Everest, and the wave of 2021 entrants ran into this network effect head-on and, in several cases, were unable to overcome it.

Scale Economies. The commercial infrastructure — sales reps, medical liaisons, patient-services organizations, reimbursement-team negotiators — is mostly fixed-cost relative to a single asset and mostly variable-cost relative to the portfolio. Each new in-licensed asset that lands on top of the existing infrastructure has a marginal commercialization cost that is materially below the standalone cost of building Chinese commercial infrastructure from scratch. This is why Zai's contribution margins on incremental drugs improve as the portfolio scales.

Switching Costs. Less central to the Zai story than the others, but present in the device business. Optune patients and their treatment centers, once trained on the device and its support workflow, do not casually switch to alternative therapies. The investment in patient education and physician familiarity creates real friction.

Branding and Process Power are present but secondary. The Zai brand inside the Chinese KOL community is a real asset; the process power around regulatory submissions and reimbursement negotiations is increasingly a real asset, but it is not yet at Toyota-Production-System levels of differentiation.

Now Porter's Five Forces, briefly. Threat of new entrants is moderated by the cornered-resource and network-effect arguments above; the LianBio cohort tested entry, and entry was harder than it looked. Bargaining power of buyers is the central existential question for the entire Chinese biopharma sector. The National Reimbursement Drug List is, in a meaningful sense, a single buyer for any drug that aspires to volume in China, and the NRDL price negotiations have repeatedly produced double-digit price cuts in exchange for inclusion. The NRDL is, as one analyst memorably described it, "the final boss" of Chinese pharma economics. Zai's response has been to focus on indications where the volume-times-price math works even after the NRDL haircut — autoimmune diseases like myasthenia gravis, where the patient population is large and the alternative of self-pay is unworkable, are particularly well-suited. Bargaining power of suppliers — that is, the Western originators — is real but bounded by the fact that originators need a credible Chinese partner more than they need any specific one. Threat of substitutes is the standard biopharma threat: cheaper generics, biosimilars, alternative modalities. Industry rivalry in China specifically is intense at the discovery-stage level and surprisingly limited at the in-licensing-and-commercialization level, because the network effects narrow the practical competitive set.

The synthesis is that Zai's moat is not a single feature; it is the interaction of five or six features, and that interaction is the thing that takes a long time to build and a long time to dismantle.

VIII. Playbook: Lessons for the Modern Investor

If you spend enough time studying companies like Zai Lab, certain lessons start to generalize beyond the specific business. The Zai playbook is a set of principles about how to build a value-capture vehicle in a market where you do not control the underlying technology, and the principles travel.

Lesson one: the "asset-light" frame is mostly a marketing exercise. It is fashionable to describe in-licensing businesses as "asset-light" because they do not own the molecules they sell. This is misleading. The physical distribution infrastructure required to commercialize a specialty drug in China — the sales force, the medical-affairs organization, the patient-services apparatus, the cold-chain logistics, the reimbursement-negotiation team — is enormously asset-intensive. The asset-lightness is on the discovery side; the commercial side is anything but. Investors who expect biopharma in-licensing models to scale like software should recalibrate. The unit economics improve with scale, but the absolute dollar investment required to reach scale is large and grows roughly linearly with portfolio breadth.

Lesson two: the platform reveals itself at the second drug. The first in-licensed drug at any China-bridge biotech looks like a one-asset business that is primarily a bet on that asset. The second in-licensed drug, deployed across the same commercial infrastructure, is when you discover whether the company is a portfolio operator or a single-asset story. The third drug is when you find out whether the platform compounds. By drug five or six, the marginal cost of adding a new asset has collapsed to a level that creates structural advantage over single-asset competitors. Zai is past this inflection. Most of its competitors are not.

Lesson three: geopolitics is a macro variable that requires explicit risk budgeting. The "dual-listing tightrope" — Nasdaq and Hong Kong — is not just a financing convenience. It is a hedge against the possibility that one or the other capital market becomes inaccessible for political reasons. The cost of the hedge is real: dual reporting, dual investor relations, dual audit committees, dual exposure to two different sets of regulatory expectations. The benefit of the hedge is asymmetric: in scenarios where U.S.-listed Chinese companies face delisting pressure under the Holding Foreign Companies Accountable Act or its successors, the Hong Kong listing is the safety net. Long-term investors in any U.S.-listed Chinese company should be modeling these scenarios explicitly rather than waving them off as tail risk.

Lesson four: when to buy versus when to build is a temperament question, not just a returns question. Zai's evolution from pure in-licensor to mixed in-licensor and original-discovery operator reflects a judgment that, at sufficient scale, the optionality value of owning your own pipeline begins to exceed the cost of the discovery infrastructure. This is a calculation that depends on cost of capital, on the maturity of the local discovery ecosystem, on the company's ability to attract scientific talent, and on the founders' tolerance for the longer cycle times of original research. Zai's answer has been to lean into the build side of the equation gradually rather than abruptly, which appears to be the right pace given how much capital was destroyed in the Chinese discovery-biotech sector during the 2022-2023 drawdown.

A myth worth fact-checking briefly: the conventional wisdom that "China biotech valuations cannot recover until U.S.-China relations normalize" is overstated. The 2022-2023 drawdown in Chinese biotech equities had multiple causes — interest-rate-driven multiple compression, NRDL-driven margin pressure, sector-specific concerns about clinical-trial data quality, and yes, geopolitical risk premia — but the fundamental cash flows of well-run companies in the sector continued to grow through the drawdown. The recovery, when it has come, has been driven by individual asset performance and out-licensing economics rather than by macro reconciliation. Investors who waited for a geopolitical all-clear missed the inflection.

A second-layer aside on capital allocation: the discipline Zai has shown around share repurchases, balance-sheet management, and the pace of new business-development transactions has improved materially since 2022. The company has trimmed cash burn, prioritized late-stage assets over speculative early-stage in-licensing, and has been openly communicative about its intent to reach operating profitability on a non-GAAP basis. This kind of discipline is rare in Chinese biotech and rare in the broader biopharma sector at companies of Zai's stage.

IX. Conclusion and the Bull versus Bear Case

The bear case on Zai Lab is articulable in three sentences. The NRDL price-cut cycle will continue to grind down the gross margins on every commercially successful drug, and the Chinese pharmaceutical market will increasingly resemble a high-volume, low-margin generics industry with specialty-pharmaceutical economics only available in narrow indications. The U.S.-China relationship will continue to deteriorate, raising the cost of capital and limiting the company's access to the U.S. equity market that is its largest source of long-term funding. The "reverse bridge" — out-licensing Chinese-discovered assets to the West — will face Western regulatory and political headwinds (the BIOSECURE Act and its successors are the cleanest example) that limit the addressable market for the company's discovery output.

Each of these is a real risk, and each deserves a serious answer. The NRDL haircut question is partially answered by therapeutic-area selection — autoimmune diseases like myasthenia gravis and CIDP are structurally less price-sensitive than oncology, because the patient base is large enough to drive volume but the disease severity is high enough to justify branded pricing. The geopolitical question is partially answered by the Hong Kong listing and by the company's increasing operational independence from U.S. capital markets — Zai has financing optionality that a single-listed company does not. The reverse-bridge question is partially answered by the empirical observation that, despite political headwinds, Chinese-originated assets continue to be licensed by Western pharmas at increasing valuations, because the underlying scientific output is too good to ignore.

The bull case is also articulable in three sentences. Vyvgart, with its follow-on indications and subcutaneous formulations, becomes the highest-selling immunology franchise in Chinese history, and the resulting cash flows fund the next decade of in-licensing and discovery without dilution. The platform — the commercial infrastructure, the regulatory know-how, the KOL network, the deal-flow brand — compounds to a position where Zai is the structural default partner for any Western biotech approaching the China market, and that position translates into pricing power on the upfront terms of new deals. The original-discovery pipeline matures into a franchise of wholly-owned global assets that out-license at economics comparable to BeiGene's recent transactions, re-rating the multiple from "Chinese in-licensor" to "global biopharma headquartered in Shanghai."

The truth, as usual, is probably between the cases, and the path between them depends on a small number of variables that long-term investors can actually track. The KPIs that matter most for this name are concentrated. First, Vyvgart net product sales in China, reported quarterly, with particular attention to the trajectory through year-three of launch — this is the single best leading indicator of whether the specialty-launch model is working at scale. Second, the cadence and economics of new in-licensing transactions, watched not for the upfront dollars but for the structural terms — broadening of rights, extension of follow-on indications, equity components — that signal Zai's ongoing competitive position with Western originators. Third, and increasingly, the out-licensing or partnering of internally discovered assets, which would be the clearest proof point that the reverse-bridge thesis is becoming reality rather than narrative.

A handful of regulatory and clinical milestones deserve attention. Vyvgart's CIDP launch trajectory through 2026 and 2027 will determine whether the franchise can grow into the multi-indication asset that the original deal economics depend on. The Augtyro launch in Chinese non-small-cell lung cancer — particularly in the ROS1-positive segment — will determine whether the BMS partnership reproduces the Vyvgart playbook in oncology. Updates from the wholly-owned pipeline, particularly any Phase 2 or Phase 3 data readouts on the bispecific and antibody-drug conjugate programs, will determine whether the discovery investment is producing globally competitive science.

Zooming out, the Zai Lab story is a mirror for China's broader industrial trajectory. The country's economy spent thirty years importing other people's intellectual property, learning to manufacture it at scale, and gradually building the indigenous capability to produce its own. The Zai playbook compresses that arc into a single twelve-year corporate history. Samantha Du's bet was, in essence, that the bridge metaphor was structurally correct — that the most valuable position in a developing market was not at either end of the bridge, but on the bridge itself, charging a toll on every molecule that crossed. That bet has aged remarkably well. The next decade will test whether the toll booth can also become a destination.

X. Epilogue and Further Reading

The most recent reporting cycle has continued to reflect the company's transition from R&D-heavy investment-mode to commercial-stage operating leverage. Vyvgart's Chinese ramp has been the dominant line item in revenue growth, with the oncology franchise providing baseline contribution and the device business providing optionality. Operating cash burn has narrowed materially from peak 2021 levels, and management has reiterated its intent to reach non-GAAP operating profitability on the published timeline.

The PDUFA-equivalent NMPA dates worth tracking through 2026 and 2027 cluster around the follow-on Vyvgart indications, additional Augtyro indications, and several wholly-owned program milestones whose timelines management updates on its quarterly calls. Investors should also watch for any further in-licensing transactions with the kind of "pipeline in a drug" structure that the argenx deal pioneered, as those will be the clearest signals of where Zai sees its next franchise opportunities.

A short reading list for those who want to go deeper:

- Zai Lab investor day presentations, particularly the 2023 and 2024 editions, in which the commercial-stage transition is laid out in management's own framing.

- The argenx-Zai Lab strategic collaboration agreement (publicly available in argenx's SEC filings as an 8-K exhibit), which is the cleanest publicly available example of the modern in-licensing structure.

- Samantha Du's profile in BioCentury and STAT News, both of which have run substantive feature pieces on the founding history and the bridge model.

- The NMPA reform papers from 2015, which are dry but essential reading for understanding why the regulatory window opened when it did.

- Hamilton Helmer's 7 Powers, applied here as the framework for the cornered-resource analysis but useful well beyond Zai.

The bridge is built. The question now is what crosses it next, in which direction, and at what toll.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube