Zebra Technologies: From Barcode Pioneer to Enterprise Intelligence Giant

I. The Nervous System You Never Knew Existed

Picture a Tuesday afternoon at any major distribution center in America. A worker picks up a rugged handheld device, scans a barcode on a pallet of incoming goods, and within milliseconds, a warehouse management system halfway across the country knows exactly what arrived, where it should go, and who needs it next.

The label on that pallet was printed by a Zebra printer. The scanner reading it was built by Zebra. The rugged mobile computer the worker holds runs Zebra software on Zebra hardware. The RFID tag embedded in the carton, silently broadcasting its identity to ceiling-mounted readers, communicates through Zebra infrastructure. From the moment that pallet was loaded onto a truck to the moment it reaches a store shelf or a customer's doorstep, Zebra technology has touched it at virtually every checkpoint along the way.

This is Zebra Technologies, and the odds are overwhelming that anyone reading this has interacted with its products today without knowing it. Over 80 percent of Fortune 500 companies rely on Zebra devices. Ninety-four percent of the Fortune 100 are customers. If a package arrived at your door, if a nurse scanned your hospital wristband, if a retail associate checked inventory on a handheld screen, Zebra technology almost certainly handled the transaction. The company operates through more than 10,000 channel partners across over 100 countries, yet most people outside the supply chain industry have never heard of it.

That anonymity is, in a way, the hallmark of a truly great infrastructure company. The best plumbing is the plumbing nobody thinks about.

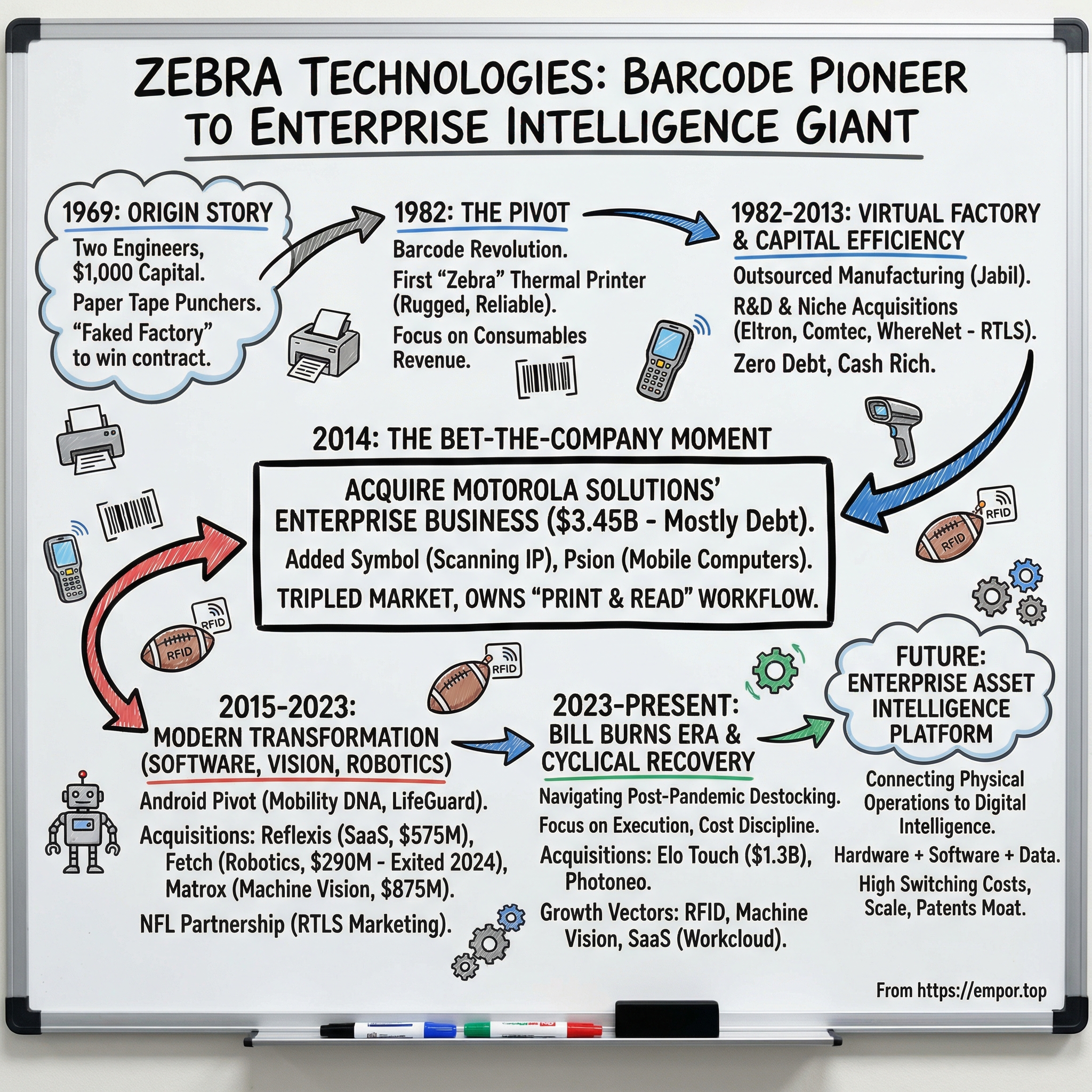

The central question this deep dive seeks to answer is deceptively simple: How did a company that started making paper tape punchers in 1969 with a thousand dollars in capital survive the death of its original industry, bet the entire company on a single leveraged acquisition, and emerge as a leader in enterprise robotics, machine vision, and AI-powered software?

The answer involves two engineers who faked a factory, a barcode printer named after a wild animal, a three-and-a-half-billion-dollar deal financed almost entirely with debt, and one of the most successful platform transitions in enterprise technology history. It is the story of infrastructure builders who understood, again and again, that the real money is not in the goods being shipped but in the invisible systems that make shipping possible.

Here is a roadmap of what lies ahead. The story begins with two engineers and a thousand dollars in 1969, moves through the barcode revolution and a brilliantly capital-efficient business model, reaches a climactic bet-the-company acquisition in 2014, transitions through a software and AI transformation, and arrives at the present day, where a new CEO is navigating recovery from a brutal cyclical downturn while repositioning the company for its next act. Along the way, there are lessons in M&A strategy, technology pivots, competitive moat construction, and the art of building invisible but essential infrastructure.

II. Two Engineers and a Pivot (1969-1982)

In 1969, two engineers named Edward Kaplan and Gerhard Cless each put up five hundred dollars and founded a company called Data Specialties Incorporated. The total investment was a thousand dollars. Their workspace was a cramped 1,320-square-foot office, and their product was electromechanical paper tape punching machines for the printing industry. These were precision devices that encoded data onto paper tape, a technology that was already mature and would soon become obsolete. But in the early 1970s, there was still a market for them, and Kaplan and Cless were gifted engineers who could build them better than almost anyone else.

The founding legend involves a moment of entrepreneurial audacity that would make any startup founder blush. When Bell & Howell, a major potential customer, wanted to visit Data Specialties' "factory" before awarding a contract, Kaplan and Cless faced a problem: they had no factory. What they had was a cramped office with a handful of assembled machines.

So they did what desperate founders do. They disassembled their already-finished machines and spread the components across every surface of the office. They hired temporary workers to sit at stations pretending to assemble products. They brought in a secretary. And they enlisted their wives to call the office phone every ten minutes, impersonating customers placing orders for machines that did not yet exist in volume.

Bell & Howell's inspectors walked through what appeared to be a bustling operation and awarded the contract. Data Specialties went on to capture roughly 50 percent of the paper tape punch market.

It is the kind of origin story that sounds apocryphal but appears consistently in company histories. And it reveals something important about the DNA of the organization: a willingness to operate at the edge of what is possible, to punch above their weight class, and to improvise solutions to seemingly impossible problems. These traits would define Zebra for the next five decades.

By the late 1970s, the crisis that would test these instincts arrived. Digital technology was rendering paper tape obsolete. The printing industry was moving to electronic composition systems. Data Specialties' core market was evaporating. Many companies in this position simply wind down. But Kaplan and Cless had an engineer's mentality: they looked for the next hard problem to solve rather than clinging to the old one.

What they found was barcode printing. The barcode itself had been invented in the 1950s and first scanned commercially at a grocery store in 1974, but on-demand barcode label printing was still in its infancy. Existing solutions were clunky, expensive, and unreliable. Kaplan and Cless recognized that as barcodes spread through retail, logistics, and manufacturing, someone would need to build the printers that generated them. Not the general-purpose office printers made by HP or Epson, but specialized thermal printers that could produce durable, scannable barcodes on demand in warehouses, factory floors, and shipping docks.

In 1982, at a trade show in Dallas, they unveiled their first barcode printer under the brand name "Zebra." The choice of name was clever: zebra stripes evoke barcodes, the visual connection was immediate and memorable. The printer itself was robust, reliable, and technologically superior to what competitors offered. It was purpose-built for industrial environments, designed to handle heat, dust, and the relentless pace of a production line.

In 1986, the company's identity had shifted so completely from paper tape to barcodes that Kaplan and Cless renamed the entire corporation Zebra Technologies. The old business was dead. The new one was just beginning to accelerate.

The timing of this pivot deserves emphasis. The mid-1980s were the dawn of the barcode era in logistics and manufacturing. Walmart had begun mandating barcodes from suppliers in 1983. The U.S. Department of Defense adopted a barcode standard called LOGMARS for tracking military supplies. Hospitals started using barcodes for patient identification and medication tracking. Each of these adoption waves meant more labels to print, and each label needed a specialized printer that could produce crisp, scannable codes on demand. Zebra was not just entering a new market; it was catching a wave that would grow for the next three decades.

What made Zebra's printers stand out was their thermal printing technology. Rather than using ink cartridges or toner, thermal printers use heat to create images on specially treated paper or ribbon. The result is labels that resist smudging, tolerate moisture, and remain scannable even after rough handling during shipping. For a warehouse receiving dock where packages get stacked, compressed, and tossed, ink-jet labels would smear within hours. Thermal labels endure. This technical advantage became the foundation of Zebra's entire business model, and it created a consumables revenue stream: every thermal printer required a steady supply of specialty labels and ribbon, generating recurring revenue long after the initial hardware sale.

This pivot, from a dying electromechanical niche to an emerging digital infrastructure market, established the pattern Zebra would repeat throughout its history. The company has never been sentimental about its legacy technology. When the world changes, Zebra changes with it.

III. The Barcode Revolution and the Virtual Factory (1982-2013)

The three decades between Zebra's barcode debut and its transformative 2014 acquisition represent a masterclass in capital-efficient growth. During this entire period, Zebra employed what insiders called the "Virtual Factory" model, and it was one of the most underappreciated strategic decisions in the company's history.

Rather than building its own manufacturing plants, Zebra outsourced production while keeping engineering and sales in-house. In practical terms, this meant Zebra designed the printers, developed the firmware, managed the customer relationships, and let contract manufacturers handle the physical assembly.

By the late 2000s, approximately 59 percent of production capacity was outsourced to Jabil Circuit, the contract electronics manufacturer. Around 40 percent of thermal printer final assembly flowed through Jabil's facilities. This was a deliberately radical approach for a hardware company in an era when most industrial manufacturers believed owning your factory was synonymous with controlling your quality.

Why does this matter? Because it made Zebra extraordinarily capital efficient. While competitors sank hundreds of millions into factory infrastructure, Zebra channeled its capital into R&D and acquisitions. The result was visible on the balance sheet: entering 2013, Zebra held $528.6 million in cash and investments with zero long-term debt. For a company generating roughly a billion dollars in annual revenue, this was a fortress balance sheet, one that would soon prove essential for the most consequential bet in the company's history.

But before that bet, Zebra spent two decades building its position through steady organic growth and targeted acquisitions. The company went public in 1991, listing on the NASDAQ under the ticker ZBRA. The IPO was not a Silicon Valley spectacle; it was the quiet listing of a profitable, growing industrial technology company. Zebra was never a "story stock." It made real products that generated real cash flow from day one as a public company.

The acquisition machine started running in the late 1990s. In 1998, Zebra merged with Eltron International, consolidating the desktop barcode printer market. Eltron was a strong competitor in the lower end of the thermal printer segment, and the merger gave Zebra dominance across the full product range, from compact desktop units to high-volume industrial printers.

Two years later, the acquisition of Comtec in 2000 pushed Zebra into mobile printing, adding portable printers that could travel with delivery drivers and field service technicians. These were not large-format industrial machines but compact, battery-powered units that could print receipts and labels from the back of a delivery truck or a utility worker's belt. It was a niche within a niche, but it demonstrated Zebra's instinct for finding specialized hardware problems that general-purpose printer companies would never bother to solve.

Perhaps the most prescient early acquisition came in 2007, when Zebra purchased WhereNet, a company specializing in Real-Time Location Systems. RTLS technology uses wireless signals to track the precise location of tagged assets within a defined space, like a factory floor or a hospital campus.

To understand RTLS in simple terms, imagine GPS but for indoor spaces. GPS works well outdoors, but inside a warehouse or hospital, satellite signals cannot penetrate walls and ceilings. RTLS uses a network of indoor receivers and small tags attached to assets, workers, or equipment to provide similar location tracking within buildings. At the time, RTLS seemed niche. In hindsight, it was an early signal of where Zebra's ambitions were heading: from simply printing labels to tracking the things those labels were attached to.

Through it all, Zebra cultivated a culture of hardware excellence. Its thermal printers became the gold standard in rugged, industrial-grade label printing. Zebra earned the reputation as the "Cisco of Printers" within the enterprise world, a somewhat unglamorous designation that masked a powerful competitive position. When a logistics company needed barcode printers that would run continuously in a hundred-degree warehouse without jamming, Zebra was the default choice. When a hospital needed wristband printers that met FDA requirements, Zebra was specified. The brand became synonymous with reliability in environments where failure was not an option.

By 2013, Zebra was a profitable, well-run company with roughly a billion dollars in revenue, zero debt, and dominant market share in enterprise printing. Anders Gustafsson, who had taken over as CEO in 2007, had professionalized the company's management and sharpened its strategic focus. The stock had been a solid if unspectacular performer. But Gustafsson and his board were looking at a market reality that concerned them: the thermal printing market was mature. Growth was steady but not spectacular. The addressable market for barcode printers, while defensible, was measured in the low single-digit billions. Zebra owned a commanding share of a limited pie.

The question facing the board was existential: should Zebra remain a well-run niche leader, compounding modestly and returning cash to shareholders? Or should it make a bold strategic leap into adjacent markets that would fundamentally reshape the company? The conservative path was the safer bet. The ambitious path involved borrowing more money than the company had ever seen. Gustafsson chose ambition, and the decision that followed would change the company forever.

IV. The Bet-the-Company Moment: Acquiring Motorola Solutions' Enterprise Business (2014)

On April 15, 2014, Zebra Technologies announced that it would acquire the Enterprise business of Motorola Solutions for $3.45 billion in cash.

To understand why this announcement sent shockwaves through the industry, consider the math: Zebra's entire market capitalization at the time was roughly equivalent to the purchase price. This was not a bolt-on acquisition. It was not even a large deal relative to the acquirer. It was a company swallowing something approximately its own size, financed almost entirely with borrowed money. In M&A parlance, this is what is called a "transformational acquisition," and most transformational acquisitions end badly. The history of corporate M&A is littered with companies that overreached and destroyed shareholder value. Think AOL-Time Warner, Sprint-Nextel, or HP-Autonomy.

Motorola Solutions had decided to focus exclusively on its public safety communications business, the radio systems used by police departments, fire stations, and emergency services. Its Enterprise division, which made barcode scanners, rugged mobile computers, and wireless networking equipment for warehouses and retail stores, was strategic non-core. Motorola wanted out. Zebra wanted in.

The financing structure tells the story of how bold this bet really was. Zebra put up $200 million from its cash reserves and borrowed $3.25 billion through a combination of bank credit facilities and debt securities. Morgan Stanley served as financial advisor and provided a fully underwritten financing commitment. A company that had operated with zero long-term debt for its entire public life was suddenly leveraged to the hilt. To put the risk in perspective, the debt-to-EBITDA ratio immediately after closing was north of 5x. In the world of leveraged finance, that is firmly in "high-yield" territory. If the integration stumbled, if customers defected, if the combined business failed to generate the expected cash flow, Zebra could have found itself in severe financial distress.

But Gustafsson and his team had done their homework. They understood the Motorola Enterprise business intimately because they had been competing against it for years. They knew the customers, the products, the margin structure, and the competitive dynamics. This was not a private equity firm buying a business it had studied for six months; this was an operator acquiring an adjacent business it had observed and competed against for decades. That operational familiarity reduced integration risk significantly.

What did Zebra get for $3.45 billion? Two crown jewels in particular. First, Symbol Technologies, one of the original inventors of handheld barcode scanning. Motorola had acquired Symbol in January 2007 for approximately $3.9 billion, getting the foundational patent portfolio for laser barcode scanning, 2D imaging, and RFID technology. These patents represented decades of innovation in automatic identification and data capture. Second, Psion, the British maker of rugged mobile computers and vehicle-mounted terminals, which Motorola had acquired in 2012 for $200 million. Psion's devices were the handheld computers used by warehouse workers, delivery drivers, and field technicians across the world.

The strategic logic was elegant. Zebra had always been on the "print" side of the barcode equation: it made the machines that generated the labels. The Motorola Enterprise business was on the "read" side: it made the devices that scanned and interpreted those labels.

By combining both sides, Zebra went from owning one piece of the automatic identification puzzle to owning the entire workflow. The company could now print a barcode, scan it, transmit the data, manage the device doing the scanning, and feed the information into enterprise systems. Think of it like a media company that previously only manufactured cameras suddenly also owning the televisions, the broadcast network, and the streaming platform. The total addressable market roughly tripled overnight.

The Motorola Enterprise business also came with approximately $2.5 billion in pro-forma annual revenue and deep, entrenched relationships with the world's largest retailers, logistics operators, and manufacturers. These were not relationships that could be built from scratch in anything less than a decade.

The deal also brought approximately 4,500 employees into Zebra, effectively doubling the headcount. The cultural integration challenge was significant. Zebra was lean, entrepreneurial, and accustomed to operating as an engineering-first organization with a relatively flat hierarchy. The Motorola Enterprise division carried the DNA of a large multinational corporation, with layers of management, formal processes, and a very different decision-making cadence. Merging these cultures was the kind of challenge that derails most acquisitions.

Zebra's leadership, however, executed the integration with discipline that surprised many skeptics. The company emphasized business continuity, adopted best practices from both organizations, and focused relentlessly on deleveraging the enormous debt load. By 2016 and 2017, the combined entity was operating as a unified company, and Zebra was actively paying down debt while growing the top line. Revenue jumped from approximately $1 billion pre-deal to roughly $3.5 billion on a pro-forma basis, and the company steadily improved margins as integration synergies materialized.

The deal closed on October 27, 2014, and the integration began immediately. Zebra's leadership team, led by Gustafsson, faced the classic post-merger challenge: how to capture synergies without disrupting the operations that made both businesses valuable. They took a pragmatic approach, keeping the best practices from both organizations while consolidating back-office functions and rationalizing product lines. The former Motorola Enterprise salesforce brought deep relationships with the world's largest retailers, logistics companies, and manufacturers. Zebra's engineering DNA brought product rigor and a culture of innovation at lower cost structures.

What made the integration particularly impressive was the speed of deleveraging. Zebra had taken on $3.25 billion in debt to complete the deal, a staggering sum for a company its size. Many investors expected a long, painful period of debt reduction that would constrain the business. Instead, the combined company's robust cash generation, driven by the integration of high-margin printing consumables with the higher-volume scanner and mobile computer business, allowed Zebra to pay down debt faster than expected. Each quarter, the leverage ratio improved, and by the late 2010s, the balance sheet was in a position of comfortable strength.

For investors who study M&A patterns, the Motorola Enterprise acquisition is a case study worth memorizing. Zebra went from being the best barcode printer company in the world to being the undisputed leader in the entire Automatic Identification and Data Capture market. It cemented a position that competitors would spend the next decade trying unsuccessfully to dislodge. The company that had once faked a factory to win a contract had just borrowed $3.25 billion to buy its way into an entirely new strategic orbit, and it worked.

V. The Modern Transformation: Software, Vision, and Robotics (2015-2023)

With the Motorola integration successfully completed, Zebra's leadership turned to a question that would define the company's next decade: what comes after hardware dominance? The answer, articulated as the "Enterprise Asset Intelligence" vision, was a strategic pivot from selling devices to selling outcomes. In plain terms, Zebra wanted to move up the value chain from hardware margins to software margins, from one-time device sales to recurring subscription revenue, from physical products to data-driven services.

But before the software pivot could gain traction, Zebra caught one of the most significant technology tailwinds in enterprise computing history: the Android transition.

To appreciate what happened, consider the state of enterprise mobility in 2014. Nearly every warehouse worker, delivery driver, and retail associate using a handheld computer was running some version of Microsoft Windows Mobile or Windows Embedded Compact (commonly known as Windows CE). These were ancient operating systems with tiny developer ecosystems, clunky user interfaces, and declining support from Microsoft. When Microsoft effectively killed Windows Mobile, the entire enterprise mobility market needed a new platform.

Zebra bet heavily on Android. This was not an obvious choice at the time. Android was associated with consumer smartphones and cheap tablets, not industrial devices built to survive a six-foot drop onto concrete, operate in subzero cold storage, or function reliably in a 120-degree Fahrenheit warehouse during a Texas summer.

Enterprise IT departments were skeptical, and for understandable reasons. Android's security reputation in the consumer world was poor. The fragmentation problem, with hundreds of device manufacturers running different versions of the operating system, was well known. And Google's commitment to long-term support for enterprise use cases was unproven. Windows CE might have been ancient and ugly, but it was a known quantity. Betting your warehouse operations on Android felt, to many IT directors, like replacing your reliable pickup truck with an untested sports car.

But Zebra saw what others missed. Android's massive developer ecosystem meant enterprises could build custom apps quickly using familiar tools and widely available programming talent. Its touch-based interface was intuitive for frontline workers who already used Android smartphones in their personal lives, dramatically reducing training time compared to the arcane menu structures of Windows CE devices.

Perhaps most importantly, Google's ongoing investment in Android, driven by the advertising revenue that depended on the platform's continued dominance, meant the underlying platform would keep improving for decades. Zebra was not just choosing an operating system; it was choosing to ride the most powerful mobile platform in the world, one backed by hundreds of billions in ecosystem investment that Zebra would never have to pay for directly.

The key to Zebra's Android strategy was its proprietary software layer called Mobility DNA. This suite of tools transformed stock Android into an enterprise-grade operating system with centralized device management, security hardening, and productivity features that did not exist on competing hardware. On top of that, Zebra introduced LifeGuard for Android, guaranteeing up to ten years of operating system and security updates for each device. Consumer Android phones typically get three to four years of updates. By extending the support window to a decade, Zebra aligned the software lifecycle with the hardware replacement cycle that enterprises actually operate on.

The Android transition did something else critically important: it created massive switching costs. Once an enterprise built custom Android apps using Zebra's Enterprise Mobility Development Kit, configured its device management infrastructure around Zebra's tools, and trained thousands of workers on Zebra devices, migrating to a competitor became operationally agonizing. This lock-in dynamic would become central to Zebra's competitive moat.

To understand the depth of these switching costs, consider a concrete example. A major logistics company deploying 50,000 Zebra mobile computers across hundreds of facilities has built dozens of custom Android applications using Zebra's EMDK. These apps are purpose-built for Zebra hardware features: specific scanning engine APIs, camera configurations, touch screen calibrations, and connectivity protocols. The IT department has invested months configuring Zebra's StageNow tool for automated device provisioning, so new devices can be configured and deployed in minutes rather than hours. Their mobile device management platform is integrated through Zebra's OEMConfig standards. Switching to a competitor's hardware would require rewriting every application, rebuilding the provisioning infrastructure, retraining the IT staff, and accepting a period of degraded performance during the transition. The direct cost of switching runs into the tens of millions of dollars, and the indirect cost, in terms of operational disruption during the transition, is incalculable. No CIO takes that risk unless absolutely forced to.

With the platform foundation firmly in place, Zebra launched an aggressive M&A campaign to build out the software, vision, and robotics capabilities that would define its future. Three acquisitions stood out for their strategic ambition and the valuation benchmarks they established.

In 2020, Zebra acquired Reflexis Systems for $575 million, roughly 8.7 times revenue. Reflexis made workforce management software used by major retailers like Target and McDonald's, the kind of applications that schedule employees, manage tasks, and optimize labor deployment. The strategic logic was straightforward: if Zebra devices were already in the hands of every frontline worker, the software those workers used to manage their shifts and tasks should also be a Zebra product. Reflexis brought high-margin, recurring SaaS revenue and deep stickiness with some of the world's largest retailers.

A year later, in 2021, Zebra acquired Fetch Robotics for $290 million. Zebra had already owned a 5 percent stake in Fetch and paid $290 million for the remaining 95 percent. At the time of acquisition, Fetch had annualized revenue of approximately $10 million, implying a staggering valuation of roughly 30 times sales. This was a strategic premium for entry into the Autonomous Mobile Robot market, where robots work alongside humans in warehouses to move goods, pick items, and transport materials. The thesis was that chronic labor shortages in logistics and warehousing would drive inexorable demand for automation.

In 2022, Zebra completed the acquisition of Matrox Imaging for $875 million, approximately 8.75 times revenue on roughly $100 million in annual sales. Matrox brought machine vision technology: cameras and software that can "see" defects on assembly lines, read labels and markings, and guide robotic arms. This pushed Zebra into the fixed industrial scanning and machine vision market, putting it in direct competition with established players like Cognex and Keyence.

Each of these acquisitions reflected a different strategic calculus. Reflexis at 8.7 times revenue represented a fair price for a proven SaaS business with blue-chip customers and predictable recurring revenue. Matrox at 8.75 times revenue was a reasonable multiple for a hardware-software hybrid with strong margins and deep technical moats. Fetch at 30 times revenue was the speculative bet, the one acquisition where Zebra paid a premium that only made sense if the AMR market exploded. As events would later demonstrate, not every strategic bet pays off at the price you paid.

Simultaneously, Zebra built one of the most visible marketing partnerships in enterprise technology through its collaboration with the National Football League. In 2014, Zebra installed its Real-Time Location System in two pilot stadiums, and by 2015, the deployment extended to all NFL venues. The system worked by embedding tiny active RFID tags, each about the size of a nickel and weighing just 3.3 grams, into the epaulets of every player's shoulder pads. Two tags per player communicated with Zebra receivers positioned throughout the stadium, capturing precise location measurements at sub-second intervals.

The NFL branded this capability "Next Gen Stats," and it quickly became a staple of television broadcasts. Viewers could see a receiver's top speed on a touchdown run, compare route patterns between players, and analyze defensive formations in ways that were previously impossible. Zebra and Wilson Sporting Goods jointly developed an RFID-embedded football, making it the official game ball of the NFL. Since that 2014 pilot, the system has monitored over 15,000 players across more than 550,000 plays, and the partnership, now in its twelfth year, has been renewed multiple times.

For Zebra, the NFL deal was not primarily about revenue. It was a marketing masterstroke. Every Sunday during football season, millions of viewers saw Zebra's tracking technology highlighted on national television. For a company that most people outside the supply chain industry had never heard of, this visibility was invaluable. It demonstrated the power of real-time location tracking in a context that was immediately understandable and emotionally engaging. When Zebra's sales team then walked into a warehouse or hospital and pitched the same RTLS technology for tracking assets, patients, or workers, the NFL reference point gave instant credibility.

VI. The Bill Burns Era: A New CEO Navigates the Storm (2023-Present)

In March 2023, one of the most significant leadership transitions in Zebra's history took place quietly, without the drama that often accompanies CEO changes at major public companies. Anders Gustafsson, who had served as CEO since 2007 and guided Zebra through its most transformative period including the Motorola acquisition and the Android transition, handed the reins to Bill Burns.

Gustafsson's tenure deserves acknowledgment before moving on. He took over a sub-billion-dollar printer company and left a diversified, five-billion-dollar-plus enterprise technology platform. Under his watch, Zebra executed the largest acquisition in the company's history, successfully transitioned its entire product line to Android, built a patent portfolio of over 5,300 patents, and expanded from barcode printing into scanning, mobile computing, RFID, machine vision, and workforce software. Few CEO tenures in industrial technology can match that record of strategic transformation.

Burns was not an outsider parachuted in by a restless board. He had served as Zebra's Chief Product and Solutions Officer, the executive responsible for the company's product roadmap, its "Enterprise Asset Intelligence" strategy, and the vision for how hardware, software, and data analytics would converge into an integrated platform.

In many ways, Burns was the architect of the strategy he was now being asked to execute as CEO. The board was betting on continuity and execution rather than disruption. It was a message to investors and employees alike: the strategy is right, and what matters now is disciplined execution.

His compensation structure reveals how the board thinks about alignment. Burns' pay is heavily weighted toward long-term incentives, particularly performance-vested restricted stock units tied to Zebra's total shareholder return relative to peers. He holds less than one percent of outstanding shares but is required to maintain stock ownership equal to six times his base salary. In practical terms, this means Burns has significant personal wealth tied to the stock price over multi-year horizons, exactly the kind of incentive alignment that long-term investors want to see.

Burns' leadership style differs from Gustafsson's in important ways. Where Gustafsson was the dealmaker and strategic visionary who engineered the Motorola acquisition and set the direction for the Android pivot, Burns is the product-and-engineering leader who understands the technology stack intimately. On earnings calls and at investor conferences, Burns speaks with the fluency of someone who has spent years in product development meetings, rattling off details about AI vision models, deep learning inference at the edge, and the technical architecture of RFID systems. He has described Zebra as having "probably 50 different projects across our portfolio" involving AI, spanning machine vision inspection, optical character recognition, navigation for autonomous vehicles, product recognition, and demand planning. This is not a CEO who delegates technology strategy; it is a CEO who lives it.

Burns inherited a company entering the teeth of the most severe cyclical downturn in its recent history. The years 2021 and 2022 had been extraordinary for Zebra, driven by pandemic-fueled demand for warehouse and logistics technology. E-commerce exploded, supply chains strained, and customers aggressively pulled forward device purchases. Revenue peaked at $5.78 billion in 2022.

Then the bullwhip snapped.

The term "bullwhip effect" describes what happens when small fluctuations in end-user demand get amplified as they move up the supply chain. Imagine a grocery store that normally orders 100 cases of soup per week. During a panic, it orders 300. The distributor, seeing triple demand, orders 500 from the manufacturer. The manufacturer ramps up production. Then the panic ends. The store goes back to 100, but the distributor has 400 cases in stock and orders nothing. The manufacturer sees orders drop to zero. This is the bullwhip, and it is exactly what happened to Zebra on a massive scale.

Customers who had over-ordered in 2021 and 2022 suddenly found themselves sitting on excess inventory of Zebra devices. Distributors were bloated with stock. New orders collapsed.

Full-year 2023 revenue plunged to $4.58 billion, a gut-wrenching 20.7 percent decline. Non-GAAP diluted earnings per share cratered to $1.71 for the full year 2023. Free cash flow turned negative, an outcome that would have been almost unimaginable two years earlier when cash was gushing in from pandemic-driven demand.

Burns' response was measured rather than panicked. He held the line on R&D investment, resisting the natural corporate impulse to slash research spending during a downturn. He maintained the company's strategic direction and focused on what he could control: cost discipline, capital allocation, and continuing to advance the software and AI roadmap.

His messaging to investors was consistent, almost monotonously so, which is exactly what you want from a CEO navigating a cyclical trough. The destocking was a temporary inventory cycle, not a structural deterioration in demand. The underlying drivers of Zebra's business, the digitization of frontline work, the automation of warehouses, the proliferation of RFID, were all intact and accelerating. He was asking investors to look through the cycle, not at it.

The recovery validated his patience.

Revenue climbed back to $4.98 billion in 2024, an 8.7 percent recovery. Then in 2025, the company posted $5.40 billion in revenue with non-GAAP diluted EPS of $15.84 and free cash flow of $831 million. The contrast with the negative free cash flow just two years earlier was stark.

When Zebra reported Q4 2025 results in February 2026, the stock surged over 14 percent in a single session as investors digested both the results and the bullish 2026 guidance calling for revenue growth of 9 to 13 percent and non-GAAP EPS of $17.70 to $18.30. The guidance implied that 2026 would be the year Zebra finally surpassed its pre-destocking peak in every financial metric. For investors who had held through the downturn, it was vindication. For those who had bought during the trough, it was a substantial return.

Burns also made a pivotal capital allocation decision that revealed his strategic pragmatism. In December 2024, Zebra announced it would exit its robotics automation business, the Fetch Robotics unit acquired just three years earlier for $290 million. The AMR business had never scaled to expectations. The specific market Fetch addressed was worth only a few hundred million dollars, and the competitive landscape, with well-funded players like Locus Robotics and Ocado-owned 6 River Systems, was brutal. Zebra took approximately $60 million in impairment charges and announced plans to wind down most of the robotics staff by end of 2025, with expected annual savings of $20 million.

Walking away from a $290 million acquisition after three years is painful. It is the kind of write-off that invites second-guessing from analysts and shareholders alike. But Burns reframed the decision as portfolio discipline rather than failure, and the logic was sound.

The AMR market, while growing, was fiercely competitive and fragmented. Locus Robotics had raised over a billion dollars in venture capital. 6 River Systems had the backing of first Shopify and then Ocado. Amazon had its own robotics division, Kiva Systems, which it had acquired back in 2012 and kept entirely for internal use. For Zebra, a company whose competitive advantages centered on ruggedized devices, software ecosystems, and deep enterprise relationships, warehouse robotics was a departure from its core strengths.

The capital and management attention freed up from robotics would be redirected toward higher-growth, higher-conviction opportunities in RFID, machine vision, and AI. On earnings calls, Burns projected "high double-digit" growth in RFID for 2026, with the technology expanding beyond its traditional apparel base into grocery, parcel logistics, government, quick-service restaurants, and healthcare.

The other major move under Burns was the acquisition of Elo Touch Solutions, which closed in September 2025 for $1.3 billion. Elo makes interactive touchscreens and point-of-sale systems, the customer-facing devices used in self-checkout kiosks, restaurant ordering systems, and retail displays. Walk into any fast-casual restaurant with a touchscreen ordering station, or use a self-checkout lane at a grocery store, and there is a good chance the screen was made by Elo. The company generates approximately $400 million in annual sales with a growth rate and EBITDA margin profile similar to Zebra's core business.

The strategic logic of the Elo deal illuminated Burns' vision for expanding Zebra's footprint. Historically, Zebra had been a "back-of-house" company: its devices lived in warehouses, stockrooms, loading docks, and behind retail counters. Elo moved Zebra to the "front-of-house," the customer-facing workflows where interactive technology meets the end consumer. The combined addressable market expansion was roughly $8 billion, and management projected $25 million in incremental annual EBITDA synergies by year three. In essence, Burns was building a company that touched every surface of physical commerce, from the moment goods arrive at a dock to the moment a consumer taps a touchscreen to pay.

VII. The Hidden Businesses: What Most Investors Miss

Ask a casual observer what Zebra Technologies does, and the answer will almost certainly be "barcode printers." That is like saying Apple makes personal computers. It is technically true and profoundly incomplete. Zebra's most exciting growth vectors are businesses that most investors either do not know exist or substantially underestimate.

Machine Vision and Fixed Industrial Scanning. Imagine a manufacturing assembly line producing thousands of electronic components per hour. At several points along the line, cameras examine each component, checking for microscopic defects: a solder joint that is slightly misaligned, a label that is crooked, a surface scratch invisible to the human eye.

If the camera detects a problem, the defective component is automatically rejected before it reaches the customer. No human eyes were involved. No quality inspector needed to squint under fluorescent lights for eight hours. The camera never gets tired, never blinks, never has a bad day. This is machine vision, and it is one of the fastest-growing segments in industrial technology.

For anyone unfamiliar with the technology, think of it as giving a factory the ability to see. Traditional barcode scanning is one-dimensional: you point a laser at a code and read the information encoded in the stripes. Machine vision is multidimensional: cameras capture full images, and software algorithms analyze those images for patterns, anomalies, measurements, and text. The applications range from inspecting pharmaceutical labels for accuracy to guiding robotic arms that pick items from conveyor belts to verifying that every component on a circuit board is correctly placed.

Zebra entered this market through a series of deliberate acquisitions. In May 2021, it acquired Adaptive Vision, a Polish company specializing in deep learning-based machine vision software. In June 2022 came the much larger Matrox Imaging deal, bringing platform-independent software, smart cameras, 3D sensors, and vision controllers. Then in 2025, the acquisition of Photoneo for approximately $65 million added advanced 3D vision capabilities. Zebra unified these capabilities under its Aurora software platform, which lets manufacturers configure, deploy, and manage both cameras and barcode scanners from a single interface.

The competitive landscape in machine vision is formidable. Cognex, the pure-play market leader, generated $915 million in revenue in 2024 with decades of customer relationships and certified reliability in demanding factory environments. Keyence, the Japanese giant, leverages a massive direct sales force and consistently delivers operating margins exceeding 50 percent, making it one of the most profitable industrial companies on earth. The global machine vision market was valued at roughly $20 billion in 2024 and is projected to reach nearly $70 billion by 2034.

Zebra's advantage against these incumbents is integration. Rather than selling standalone vision systems, Zebra can offer machine vision as part of a comprehensive enterprise ecosystem that includes mobile computing, scanning, RFID, and workforce software. For a plant manager already running on Zebra devices, adding Zebra vision cameras to the inspection line is a natural extension of an existing relationship. This bundle-and-cross-sell approach mirrors what enterprise software companies have done for decades, and it creates a powerful wedge into a market where Zebra is still a relative newcomer.

Zebra Workcloud: The SaaS Play. The second hidden business is Zebra Workcloud, the company's suite of enterprise software applications built primarily on the Reflexis acquisition. Workcloud is not a single product but a platform of interconnected modules: Inventory Visibility for accurate stock counts, Workforce Optimization for intelligent scheduling and demand forecasting, Task Management for execution tracking, Communication for secure enterprise collaboration, and Demand Intelligence for forecasting and analysis.

Think of it this way. Zebra's hardware is the hand that touches every item in a warehouse or store. Workcloud is the brain that decides what those hands should do and when. A retail store manager using Workcloud can see in real time which aisles need restocking, which employees are available and best qualified to do it, and whether customer traffic patterns suggest shifting staff to the checkout lanes. This kind of frontline orchestration was historically done with clipboards and walkie-talkies. Zebra is digitizing it.

The company does not separately disclose Workcloud revenue, which makes it difficult to track from the outside. This opacity is a source of frustration for investors who want to quantify the software transition. Without a clean revenue breakout, the market cannot easily assess how much of Zebra's value should be attributed to higher-multiple software revenue versus lower-multiple hardware revenue.

But the strategic importance is clear in management commentary and capital allocation decisions. The goal is to create an ecosystem where hardware sales pull through software subscriptions, converting one-time transactions into recurring revenue streams with higher margins and greater predictability. These subscriptions typically run on multi-year service agreements, adding durability to the revenue base. It is the classic "razor and blades" model applied to enterprise technology: sell the device, then sell the software that makes the device indispensable.

RFID: The Quiet Giant. If machine vision is the flashy growth story and Workcloud is the margin expansion story, RFID may be the most important growth vector of all. Radio-Frequency Identification technology allows items to be tracked without line-of-sight scanning. Instead of manually scanning each barcode one at a time, an RFID reader can identify hundreds of tagged items simultaneously just by being in the same room. A retail associate can count every garment in a store by walking the aisles with a handheld RFID reader, a task that would take hours with barcode scanning.

RFID adoption in retail apparel is already well established, with major chains using it for inventory accuracy and loss prevention. But Burns has articulated a vision for RFID expanding into entirely new categories: grocery and fresh food tracking, parcel logistics, government asset management, quick-service restaurant inventory, and healthcare supply chains. Each new category represents billions in additional addressable market. Burns projected high double-digit growth in RFID for 2026, making it one of the company's fastest-growing product lines.

The economics of RFID adoption are worth understanding because they explain why expansion beyond apparel feels inevitable rather than speculative. A single RFID tag costs a few cents. A handheld RFID reader costs several thousand dollars. The infrastructure of fixed RFID readers and antennas at dock doors and in stockrooms costs tens of thousands per location. But the return on investment is enormous. Retailers consistently report that RFID drives inventory accuracy from the low 60 percent range to above 95 percent. That improvement in accuracy translates directly into fewer stockouts, fewer markdowns, better labor productivity, and reduced shrinkage. For a grocery chain managing thousands of perishable SKUs with expiration dates, RFID could mean the difference between throwing away 10 percent of fresh produce and 3 percent. The financial case is overwhelming, and the only question is how quickly each new vertical reaches the adoption tipping point.

Zebra's position in this RFID expansion is particularly strong because it sells the entire ecosystem: the RFID printers that encode the tags, the handheld and fixed readers that capture the signals, the mobile computers that process the data, and the software that turns raw reads into actionable intelligence. No competitor offers this full-stack approach with the same depth and breadth.

VIII. Competitive Moats and Strategic Frameworks

Understanding why Zebra's competitive position is durable requires looking at the business through two complementary lenses: Michael Porter's Five Forces framework, which maps the industry structure, and Hamilton Helmer's Seven Powers framework, which identifies the specific sources of persistent competitive advantage.

Porter's Five Forces

Start with competitive rivalry. The enterprise AIDC market is not a free-for-all. It is essentially a duopoly between Zebra and Honeywell, with smaller players like Datalogic competing in niches.

Honeywell is the primary antagonist: a massive, diversified industrial conglomerate with deep pockets, extensive customer relationships, and a product line that directly overlaps with Zebra's in scanners, mobile computers, and printers. In machine vision, Cognex and Keyence add competitive intensity. But the duopoly structure means pricing is generally rational. Neither Zebra nor Honeywell has an incentive to start a destructive price war in a market where both earn healthy margins.

The threat of new entrants is low to moderate. Building ruggedized enterprise devices is genuinely hard. These are not consumer electronics with two-year life cycles. Zebra's mobile computers must survive being dropped repeatedly onto concrete, operate in temperatures ranging from negative 20 to 50 degrees Celsius, resist dust and water ingress, and run for ten years with continuous security updates.

The engineering requirements, combined with the certifications needed for specific industries like healthcare and hazardous environments, create meaningful barriers. However, there is a persistent low-end threat from consumer devices. An iPhone in a rugged case running a scanning app is not as capable as a purpose-built Zebra device, but for some applications, it is good enough. This is the classic innovator's dilemma pattern: the low-end disruption threat. It has existed for a decade without meaningfully eroding Zebra's position, partly because enterprise environments demand reliability, security, and manageability that consumer devices cannot provide. But it bears watching.

Supplier power is a genuine vulnerability. Zebra's mobile computers run on Qualcomm Snapdragon processors, and the Android operating system depends on Google's ongoing investment and support. During the 2021-2022 global chip shortage, Zebra experienced significant supply constraints as Qualcomm chips became scarce.

The company has limited ability to dual-source its processor platform because the entire software stack, including Mobility DNA and customer applications, is built on specific Qualcomm chip architectures. Additionally, Jabil Circuit handles approximately 59 percent of Zebra's manufacturing, creating concentration risk in production. These supplier dependencies are structural features of the business model, not bugs that management can easily fix.

Buyer power is moderate. Zebra's largest customers, companies like Amazon, Walmart, and FedEx, have enormous purchasing leverage and can extract volume discounts. But the switching costs described below limit how aggressively buyers can play vendors against each other. When your entire warehouse operation runs on Zebra infrastructure, threatening to switch to Honeywell is an empty gesture unless you are actually willing to endure the disruption.

Hamilton Helmer's Seven Powers

The most powerful of Helmer's seven sources of competitive advantage in Zebra's case is switching costs, and the depth of these switching costs is often underappreciated by investors who view Zebra as a commodity hardware company.

Consider what happens when a large enterprise decides to replace its Zebra mobile computers with a competitor's devices. Every custom Android application built using Zebra's Enterprise Mobility Development Kit must be rewritten or adapted. The device management infrastructure, configured around Zebra's OEMConfig and StageNow tools, must be rebuilt from scratch. Thousands of frontline workers must be retrained.

The integration between handheld devices and the warehouse management system, which has been tuned over years of operation to Zebra's specific hardware APIs and barcode formats, must be reconfigured and tested. Print management software configured for backward compatibility with Zebra printers will not work with competitor hardware out of the box. And the ten-year security update commitment from LifeGuard for Android cannot simply be replicated overnight.

This is not hypothetical. Zebra commands a 42.3 percent share of the global enterprise mobile computing market as of 2023. That share has remained remarkably stable because switching is, in the words of one industry analyst, "operational suicide." The switching costs are not just financial; they are organizational, technical, and temporal. No enterprise wants to risk disrupting its warehouse operations for six months while it migrates to a new device platform.

Scale economies provide the second major source of power. Zebra operates a global service and support network spanning over 100 countries, a repair and logistics infrastructure that smaller competitors simply cannot match. When a device breaks down in a warehouse in Sao Paulo or a hospital in Frankfurt, Zebra can dispatch a replacement or arrange a repair through local service capabilities. Building that kind of global service infrastructure from scratch would require years and hundreds of millions of dollars in investment.

The company's 10,000-plus channel partner ecosystem creates a distribution flywheel: more partners mean more reach, which drives more sales, which funds more R&D, which produces better products, which attracts more partners. Zebra has been described as the "main and arguably only must-carry brand" in the AIDC channel, the way Cisco is the default in networking equipment. For a value-added reseller specializing in warehouse technology, not carrying Zebra is like a car dealership not selling Toyotas. The brand is simply too important to the channel to ignore.

The third source of power is what Helmer calls a "cornered resource." Zebra's patent portfolio includes over 5,300 U.S. and international patents, many inherited from Symbol Technologies and augmented by a separate acquisition of more than 200 RFID patents from BTG for approximately $10 million.

This makes Zebra one of the largest RFID intellectual property holders in the world. These patents cover foundational technologies in barcode scanning, 2D imaging, and radio-frequency identification, the bedrock inventions upon which the entire AIDC industry was built. A new entrant would need to either license this IP or engineer around it, both of which are expensive and time-consuming. The patent portfolio functions as a legal moat that reinforces the operational moat created by switching costs and scale.

Network effects in the traditional sense are limited but growing. As the Workcloud software platform scales, the data generated by millions of Zebra devices across thousands of enterprises could create indirect network effects: more usage generates more data, which improves forecasting algorithms, which makes the platform more valuable, which drives more adoption. This flywheel is still early-stage but represents a potential source of increasing returns.

There is a fifth power worth noting: counter-positioning, which Helmer defines as the ability to adopt a new business model that incumbents cannot replicate without damaging their existing business. Zebra demonstrated this most clearly during the Android pivot. When Microsoft abandoned Windows Mobile, Zebra moved faster than any competitor to embrace Android for enterprise. Honeywell and other incumbents, which had invested heavily in Windows-based device ecosystems, were slower to transition because their existing customer base and engineering organizations were optimized for Windows. Zebra's willingness to go all-in on Android, building Mobility DNA and LifeGuard as competitive differentiators on a new platform, gave it a multi-year head start that translated into durable market share gains.

Finally, Zebra enjoys moderate branding power. In enterprise procurement, "Zebra" has become almost generic for rugged barcode printers and mobile computers, the way "Xerox" once meant photocopying and "Kleenex" means tissue. The company was ranked number one in its industry on Newsweek's list of America's Most Trusted Companies. This brand recognition, built over five decades of reliable products, provides a subtle but meaningful advantage in procurement decisions where specifying "Zebra" is the path of least resistance for IT departments.

The overall moat assessment suggests that Zebra's competitive position is strong but not invulnerable. Switching costs and scale economies are the primary moats, reinforced by a cornered resource in the patent portfolio and growing process power in M&A execution and supply chain management. The key question for investors is whether the emerging software and data businesses will add network effects to this moat profile, potentially creating a compounding advantage that is even harder to overcome.

IX. Financial Performance and Market Position

The financial story of Zebra over the past five years is a textbook case of cyclicality within a secular growth trend. Understanding where the company stands today requires separating the noise of the inventory cycle from the signal of long-term structural demand.

Revenue tells the cyclical story most clearly. From a pre-pandemic base of roughly $4.5 billion in 2020, Zebra surged to $5.63 billion in 2021 and peaked at $5.78 billion in 2022 as pandemic-driven demand for warehouse and logistics technology pulled forward multiple years of equipment purchases.

Then came the reckoning. Revenue plunged to $4.58 billion in 2023 as customers worked through bloated inventories and distributors destocked aggressively. The recovery began in 2024 with revenue of $4.98 billion and continued into 2025 at $5.40 billion. Management's 2026 guidance projects another step up to roughly $5.9 to $6.1 billion, which would represent a new all-time revenue high.

The earnings trajectory amplified the cyclical swings even more dramatically. Non-GAAP diluted EPS collapsed from peak levels to just $1.71 in 2023, then rebounded to roughly $10.25 in 2024 and $15.84 in 2025. The 2026 guidance of $17.70 to $18.30 would represent new all-time EPS highs, finally eclipsing the 2022 peak. These dramatic swings reflect the operating leverage inherent in a business with significant fixed costs in R&D and distribution: when revenue drops 20 percent, earnings drop far more because the cost base does not shrink proportionally.

The margin profile reveals the underlying quality of the business. Gross margins have typically ranged between 43 and 48 percent, reflecting the premium pricing Zebra commands for its ruggedized, enterprise-grade devices. The 2024 gross margin recovered to approximately 48.4 percent.

To put these margins in context, a typical consumer electronics company like Lenovo operates at gross margins in the low 20s. A diversified industrial like Honeywell runs in the mid-30s. Zebra's gross margins, nearly reaching 50 percent, reflect the pricing power that comes from selling mission-critical devices to customers with high switching costs. When a warehouse cannot operate without your scanners, you can charge a premium.

Adjusted EBITDA margins have stabilized around 22 percent through the recovery, suggesting the company has found a sustainable operating cadence. These are not software-like margins, but they are impressive for a hardware-centric business and continue to improve as the software mix grows.

Free cash flow is perhaps the most telling metric, and the one that best captures the underlying economics of the business.

In 2023, free cash flow was negative $91 million, a shocking figure for a company that had historically generated hundreds of millions in cash annually. The negative cash flow reflected not just the revenue decline but also the working capital impact of unwinding bloated inventory and managing elevated receivables during a period when customers were pushing back on payment terms.

By 2025, free cash flow had surged to $831 million, driven by $917 million in operating cash flow minus just $86 million in capital expenditures. That $86 million capex figure is worth pausing on. For a company generating $5.4 billion in revenue, spending less than $90 million on capital expenditures is remarkably low. It is a direct consequence of the capital-light model that Kaplan and Cless established in the 1970s, and it continues to generate disproportionate cash relative to the asset base. The company converts revenue to free cash flow at a rate that most hardware companies can only envy.

Capital allocation in 2025 reflected confidence in both internal capabilities and the stock's value. Zebra deployed capital across three priorities simultaneously.

First, $1.365 billion went to acquisitions, primarily the Elo Touch and Photoneo deals, expanding the company's addressable market and technical capabilities. Second, $587 million went to share repurchases, reducing the share count and concentrating ownership among remaining shareholders. Third, $328 million went to net debt reduction, strengthening the balance sheet for future strategic flexibility.

A new $1 billion share repurchase authorization was announced alongside Q4 2025 results, signaling management's belief that the stock remains attractively priced relative to the company's earnings power.

The "arms dealer" analogy is perhaps the most useful mental model for thinking about Zebra's market position. The company does not sell the goods that flow through global supply chains. It sells the infrastructure that makes those supply chains work: the printers that generate the labels, the scanners that read them, the mobile computers that direct the workers, the RFID systems that track the inventory, and increasingly the software that orchestrates the entire operation. When e-commerce volumes grow, Zebra benefits. When retailers invest in omnichannel fulfillment, Zebra benefits. When manufacturers automate quality inspection, Zebra benefits. The company is positioned at the intersection of nearly every secular trend in physical operations.

One financial nuance worth highlighting is the 2026 gross margin outlook. Management flagged an expected two-point gross margin headwind from rising memory component prices. This is a reminder that even with dominant market share, Zebra's hardware business faces input cost pressures that are largely outside its control. However, management indicated that targeted price increases, cost savings from exiting the robotics business, and improving software mix should more than offset this headwind. The ability to pass through input cost increases to customers without losing share is itself a signal of pricing power, one of the more tangible manifestations of the competitive moat described in the previous section.

X. The Playbook: Lessons for Infrastructure Builders

Zebra's history offers a remarkably clear playbook for how infrastructure companies can compound value over decades, and it revolves around three principles that any capital allocator should study.

The first lesson is knowing when to bet the company versus when to bolt on. The 2014 Motorola acquisition was a bet-the-company deal: $3.25 billion in debt for a company that had never borrowed, a purchase price equal to its own market cap, a target that would triple its revenue. Everything had to go right, and it did.

By contrast, the acquisitions that followed, Reflexis at $575 million, Fetch at $290 million, Matrox at $875 million, were all bolt-on deals that extended capabilities without threatening the balance sheet.

The strategic wisdom is in knowing which type of M&A is appropriate for each moment. You bet the company once, when the opportunity is transformative and the timing is right. You bolt on repeatedly, when the platform is established and you are filling capability gaps. Most companies get this wrong. They either play it too safe, making only small acquisitions that never change the competitive landscape, or they bet the company too often, eventually hitting a deal that breaks them. Zebra got the sequencing right.

The second lesson is surviving technology shifts through unsentimental reinvention. Zebra has now navigated four major technology transitions. From paper tape to barcodes in the early 1980s. From standalone printers to networked AIDC systems through the Motorola acquisition. From Windows Mobile to Android in the mid-2010s. And now from pure hardware to a hybrid hardware-software-AI platform. Each transition required abandoning products, capabilities, and sometimes entire business units that had been core to the company's identity. The willingness to exit the robotics business in 2024, just three years after acquiring Fetch for $290 million, demonstrated that this unsentimental DNA remains alive under new leadership.

The third lesson is the Android pivot itself, a case study in riding a consumer technology wave into the enterprise. When Microsoft abandoned Windows Mobile, Zebra did not try to build its own operating system or adopt a competing platform like iOS. It recognized that Android's consumer momentum would inevitably flow into the enterprise, and it positioned itself as the bridge between Google's consumer platform and the demanding requirements of industrial users. The Mobility DNA software layer and the LifeGuard security support program turned a commodity operating system into a proprietary ecosystem. Zebra took something freely available, Android, wrapped it in ten years of security support and enterprise-grade management tools, and created switching costs that competitors have struggled to replicate.

These three principles, transformative M&A at the right moment, unsentimental technology pivots, and riding consumer waves into the enterprise, form a playbook that is applicable far beyond barcode printing. Any company selling infrastructure to enterprises can study how Zebra executed each of these transitions and emerged stronger on the other side.

There is also a fourth, less obvious lesson: the power of the "virtual factory" in enabling strategic flexibility. Because Zebra never tied up capital in manufacturing infrastructure, it had the financial firepower to make the Motorola acquisition when the opportunity appeared. A company burdened with factory debt and ongoing capex commitments might not have had the balance sheet credibility to borrow $3.25 billion. Zebra's asset-light model was not just operationally efficient; it was strategically liberating. It gave the company optionality that competitors with capital-intensive manufacturing operations did not have. The lesson for other industrial companies is that being capital-light is not just about margins; it is about preserving the ability to act decisively when transformative opportunities arise.

A fifth lesson deserves mention: the importance of choosing battles. The Fetch Robotics acquisition was a strategic bet that did not pay off. But the way Zebra handled the exit, quickly, cleanly, and with honest communication to investors, matters just as much as the original decision. Many companies cling to failed acquisitions for years, hoping to justify the original price through incremental improvements that never materialize. Burns' willingness to take the impairment charge and move on within three years preserved capital, management attention, and organizational focus for the higher-conviction opportunities in RFID, machine vision, and AI. The lesson is not to avoid all risky bets. It is to recognize when a bet is not working and to exit before the opportunity cost compounds.

XI. The Bull and Bear Case

The Bull Case

The most compelling argument for Zebra centers on the intersection of three secular trends that show no signs of reversing.

First, labor shortages in warehousing, logistics, and manufacturing are structural, not cyclical. Demographic headwinds in developed economies mean fewer workers are available for the physically demanding jobs that constitute Zebra's end markets. In the United States alone, the warehouse and logistics sector faces a persistent shortfall of hundreds of thousands of workers. Every warehouse that cannot hire enough workers is a warehouse that needs more technology: faster scanners, smarter devices, machine vision for quality inspection, software to optimize the workers it does have.

This labor scarcity is Zebra's best friend, because it converts a discretionary technology upgrade into an operational necessity. A warehouse manager who might have delayed a device refresh for another year cannot delay it when there simply are not enough workers to operate without the productivity gains that new technology provides.

Second, supply chain complexity continues to increase. The proliferation of e-commerce, same-day delivery expectations, omnichannel fulfillment, and global sourcing means enterprises need more visibility into their operations, not less. RFID adoption is still in its early innings across most categories outside apparel. Burns' projection of high double-digit RFID growth in 2026 reflects genuine whitespace in grocery, logistics, healthcare, and government applications. Each new category that adopts RFID represents billions in incremental addressable market.

Third, and most important for valuation, is the potential for Zebra to re-rate from a cyclical hardware company to an industrial technology and software platform. Today, Zebra trades at multiples typical of industrial hardware businesses. But as the software and services mix grows through Workcloud, RFID subscriptions, and machine vision analytics, the recurring revenue base could become large enough to warrant a higher multiple.

The gap between how the market prices Zebra today and how it might price a version of Zebra with 30 or 40 percent recurring revenue is substantial. This re-rating is not guaranteed, but it is the core thesis for investors who believe Zebra is in the early stages of a multi-year transformation rather than the late stages of a hardware upgrade cycle.

The Bear Case

The bear case is grounded in three legitimate concerns that investors must weigh honestly.

Cyclicality remains the most immediate risk. The 2023 destocking episode demonstrated that Zebra's revenue can decline 20 percent in a single year when customers freeze hardware purchases. This is fundamentally a capex business. When the economy slows, when CFOs tighten budgets, when warehouse operators decide existing devices can last another year, Zebra's revenue drops before its costs do. The operating leverage that amplifies earnings on the way up works in reverse on the way down. Non-GAAP EPS fell by roughly two-thirds from peak to trough. For investors with short time horizons, this volatility is real and recurring.

Commoditization is the slow-burn threat. Today, Zebra's rugged mobile computers are engineering marvels designed for environments that would destroy a consumer smartphone. But what happens if low-cost manufacturers in Asia close the quality gap?

The rugged device market could follow the same trajectory as many other hardware categories, where "good enough" eventually disrupts "best in class." Think about what happened in the server market, where commodity x86 servers from Dell and HP gradually displaced proprietary systems from IBM and Sun Microsystems. The incumbents' products were technically superior, but the gap narrowed until the price differential could no longer be justified.

Zebra's switching costs and software ecosystem provide protection, but these defenses are not impregnable. If a Honeywell or a Chinese upstart can offer devices that integrate reasonably well with standard Android enterprise management tools at 60 percent of the price, some cost-sensitive customers will switch. The question is whether Zebra's software layer, Mobility DNA, LifeGuard, and Workcloud, can create enough differentiation to keep the competition at bay even as the hardware itself becomes more commoditized.

Honeywell itself is the third concern. Unlike Zebra, Honeywell is a massive, diversified industrial conglomerate with the financial capacity to invest aggressively in any business segment it chooses.

If Honeywell decides to wage a sustained competitive campaign for market share in enterprise mobility, whether through pricing, R&D investment, or acquisitions, it has resources that Zebra cannot match. The duopoly structure has been stable for years, but stability is not guaranteed. There are also periodic rumors about Honeywell potentially spinning off or restructuring its business units, which could create a more focused competitor in Zebra's core markets. A standalone Honeywell enterprise mobility company, unburdened by conglomerate overhead and fully focused on winning share, would be a significantly more dangerous competitor than the current business unit buried within a larger organization.

A fourth bear concern, often overlooked, is execution risk on the software transformation. Zebra has articulated a compelling vision for transitioning from hardware to a hardware-plus-software platform. But hardware companies attempting to become software companies have a mixed track record. The sales motion is different, the talent profile is different, the customer success model is different, and the organizational culture required to ship software on iterative release cycles clashes with the hardware culture of long development timelines and physical product launches. Zebra's ability to attract and retain top software talent, to sell subscriptions rather than boxes, and to build a SaaS customer success function from scratch, are all execution challenges that remain unproven at scale.

The KPIs That Matter

For investors looking to track Zebra's trajectory without drowning in quarterly noise, two metrics stand above all others.

The first is organic revenue growth, stripped of acquisitions and currency effects. This metric reveals whether the underlying demand for Zebra's products is expanding or contracting, independent of M&A activity. During the destocking, organic growth turned sharply negative. During the recovery, it turned positive.

The trend of this number over rolling four-quarter periods is the single best indicator of the health of the business. It cuts through the noise of acquisition-driven revenue bumps and currency fluctuations to reveal whether the core business is growing. When the Q4 2025 results showed organic net sales growth of 3.6 percent in the Connected Frontline segment, that was a meaningful signal that underlying demand was normalizing after the brutal destocking cycle.

The second is the software and services revenue mix as a percentage of total revenue. Zebra does not disclose this with the granularity investors would like, but directional commentary from management on Workcloud adoption, RFID attachment rates, and software subscription growth provides the signal.

If this mix is growing meaningfully, quarter over quarter, the company is successfully executing its transition from hardware vendor to platform company. If it stagnates or grows only through acquisition accounting, the re-rating thesis is at risk. Investors should listen carefully to earnings call commentary for specific software growth metrics, even if Zebra does not publish a clean breakout. The language management uses to describe software momentum, or the conspicuous absence of that language, is itself a data point.

XII. Epilogue: The Intel Inside of the Physical World

There is a phrase that Zebra's own marketing materials sometimes use: "the edge of the enterprise."

It refers to the physical locations where work actually happens, the warehouse floor, the delivery truck, the hospital room, the factory line, the retail aisle. Not the corporate headquarters. Not the cloud data center. Not the executive suite with its polished conference table and wall-mounted dashboards. The edge is where the messy, physical work of the global economy takes place, the noisy, temperature-variable, dust-filled spaces where goods are moved, patients are treated, and products are built.

Zebra Technologies has spent more than fifty years building the technology that makes these places function. From the paper tape punchers of the 1970s to the AI-powered machine vision systems of the 2020s, the company has reinvented itself repeatedly while maintaining a consistent strategic position: the invisible infrastructure layer that connects physical operations to digital intelligence.

The analogy to "Intel Inside" is apt. Intel's processors were invisible to end users but essential to every computer that ran. Zebra's devices are invisible to the consumer receiving a package but essential to every step of the journey that brought it to their door.

The difference is that Zebra's transformation is still in its middle chapters. The shift from hardware to software, from printing barcodes to seeing with machine vision, from tracking inventory to orchestrating entire frontline workforces, these transitions are underway but far from complete. The next five years will determine whether Zebra fully executes this metamorphosis or remains primarily a hardware company with software aspirations.

Whether Zebra successfully completes this transformation will depend on execution under Burns' leadership, on the pace of RFID adoption across new categories, on the machine vision business's ability to compete with entrenched incumbents, and on the disciplined capital allocation that has characterized the company's best decisions.