Yum! Brands: The Story of the Fast Food Empire

I. Introduction & Episode Setup

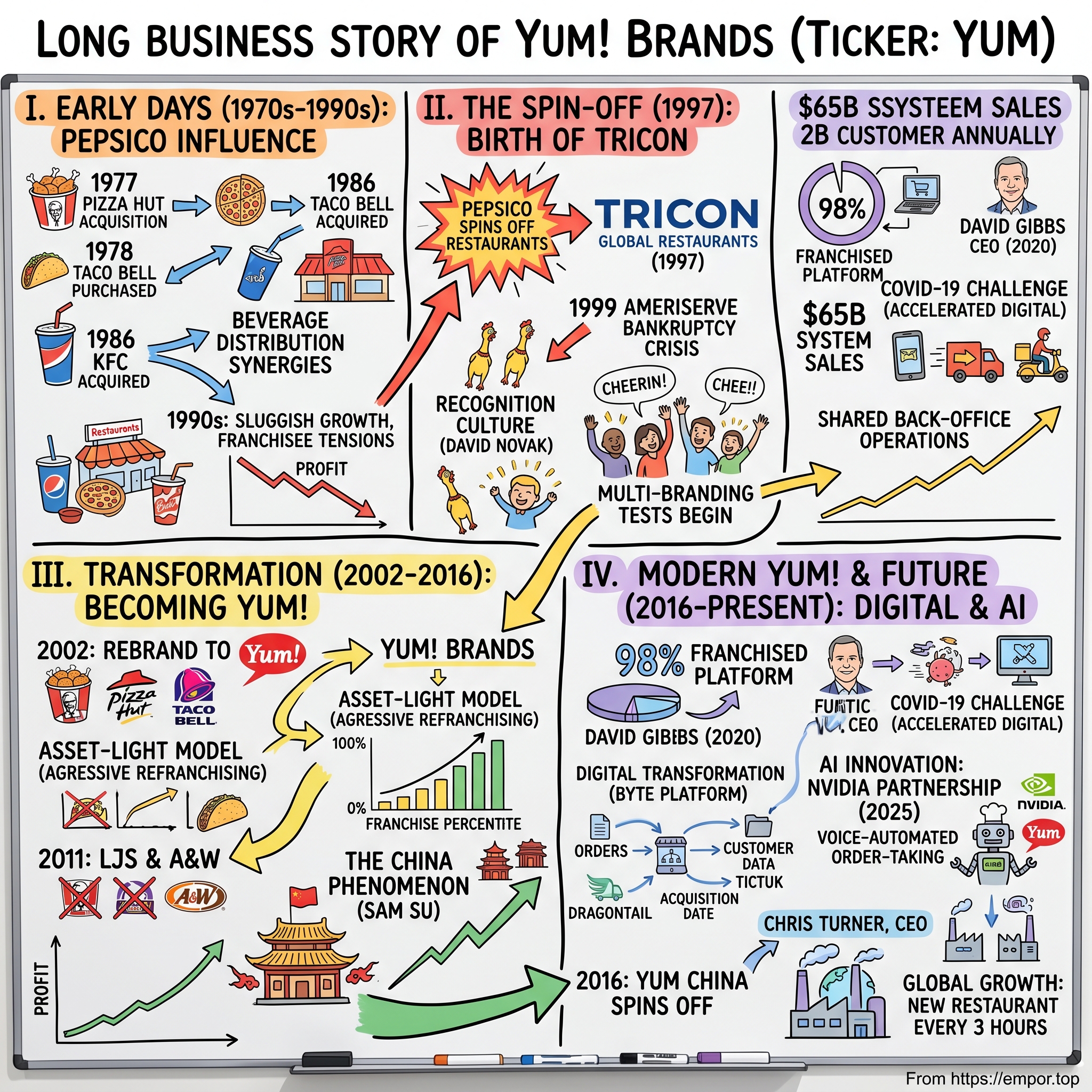

Picture this: It's 2:30 AM in Louisville, Kentucky, and the lights are still blazing at Yum! Brands headquarters. Not because of a crisis—but because somewhere in the world, it's lunchtime. At this very moment, a KFC is opening in Kazakhstan, a Pizza Hut delivery driver is navigating Bangkok traffic, and a Taco Bell in California is serving its late-night fourth meal crowd. Every three hours, a new Yum! restaurant opens somewhere on Earth. By the time you finish reading this sentence, the company has served roughly 10,000 customers.

This is the paradox of Yum! Brands: a company that operates more restaurants than McDonald's—over 61,000 locations across 155 countries—yet somehow flies under the radar of mainstream business consciousness. While McDonald's golden arches dominate skylines and business school case studies, Yum! has quietly built an empire that serves 2 billion customers annually, generating $65 billion in system sales. That's larger than the GDP of Luxembourg.

The journey from PepsiCo's experimental restaurant division to the world's largest restaurant company by unit count is a masterclass in portfolio management, franchise economics, and global expansion. It's a story of three iconic brands—KFC, Pizza Hut, and Taco Bell—that somehow found synergy despite serving completely different cuisines. It's about transforming from a capital-intensive operator to an asset-light franchising machine that generates predictable cash flows with 98% of locations franchised.

But more than anything, this is a story about timing and transformation. About recognizing when synergies become constraints (the PepsiCo spin-off), when growth requires geographic focus (the China phenomenon), and when technology shifts from nice-to-have to existential necessity (the digital revolution). It's about building a recognition culture that turned hourly workers into brand evangelists and franchisees into partners rather than adversaries.

The numbers tell one story: from $24 billion in system sales at the 2002 rebrand to $65 billion today, from 50% franchised to 98%, from minimal digital presence to AI-powered kitchens. But the real story lies in the decisions behind those numbers—the boardroom battles over the China spin-off, the calculated risks of refranchising during peak valuations, the pivot from competing with McDonald's to creating an entirely different playbook.

We'll explore how a company born from PepsiCo's desire for captive beverage distribution evolved into a franchise platform that some analysts now view as more tech company than restaurant operator. We'll examine the portfolio logic that led to acquiring Long John Silver's and A&W, only to divest them a decade later. We'll dive deep into the China story—how KFC became more popular than McDonald's in the world's most populous nation, and why spinning off that crown jewel might have been the smartest move Yum! ever made.

This is also a story about leadership transitions—from PepsiCo executives learning the restaurant business, to David Novak's transformational culture-building, to David Gibbs' financial engineering, and now Chris Turner's upcoming technology-focused tenure. Each leader faced their defining moment: Novak with the Ameriserve bankruptcy that nearly crippled the supply chain, Gibbs with COVID-19's existential threat to dine-in restaurants, and Turner inheriting a company at the intersection of AI disruption and labor automation.

The franchise model mastery alone deserves attention. While competitors struggled with franchisee relations, Yum! built a system where operators compete to open new locations. The company's capital allocation framework—balancing growth investment, dividends, and buybacks—has returned over $20 billion to shareholders since 2016 while still funding expansion and technology transformation.

As we unpack this story, we'll see how three seemingly disparate brands—southern fried chicken, Italian-American pizza, and Mexican-inspired fast food—became a coherent portfolio. How a company dismissed as PepsiCo's unwanted stepchild became a global powerhouse. And how the next chapter, featuring AI-powered kitchens and ghost restaurants, might represent the biggest transformation yet.

II. The PepsiCo Era: Building the Foundation (1977-1997)

The conference room at PepsiCo's Purchase, New York headquarters was thick with cigarette smoke—this was 1977, after all—as CEO Don Kendall stared at the proposal before him. Pizza Hut's co-founders, brothers Dan and Frank Carney, were ready to sell. The Wichita-based chain they'd started in 1958 with $600 borrowed from their mother had grown to 3,000 locations. But competition was intensifying, capital needs were mounting, and the Carneys wanted out. The price: $315 million, roughly $1.5 billion in today's dollars. For PepsiCo's leadership, this wasn't just about pizza. The company's history began in 1977, when PepsiCo entered the restaurant business by acquiring Pizza Hut from co-founders Dan and Frank Carney. The Carney brothers sold Pizza Hut to PepsiCo for $300 million—a significant premium for a chain that reached $436 million in sales that year. But Kendall saw something bigger: a captive distribution channel for Pepsi products in an era when Coca-Cola dominated fountain sales through McDonald's.

The logic seemed bulletproof. Restaurants generate massive beverage margins—a $0.10 cost becomes a $2.00 sale. Control the restaurant, control the beverage contract. Plus, from 1971 to 1977, Pizza Hut's profits grew an average of 40% per year. The quick-service restaurant industry was exploding, and PepsiCo wanted in.

Barely a year passed before PepsiCo doubled down. A year later, PepsiCo purchased Taco Bell from founder Glen Bell. Glen Bell had built his Mexican-inspired chain from a single hot dog stand in San Bernardino—yes, the same town where the McDonald brothers started—into a 868-location empire. The synergies seemed obvious: different dayparts (Pizza Hut peaked at dinner, Taco Bell at lunch), complementary real estate needs, and of course, more Pepsi fountains.

But the real prize came in 1986. In July 1986, R. J. Reynolds sold KFC to PepsiCo to pay off debt from its recent purchase of Nabisco. The tobacco giant needed cash after its leveraged buyout of the cookie maker, and PepsiCo paid $850 million for what was already an American icon. Colonel Harland Sanders had sold his company for $2 million in 1964; seven years later, the company was sold to Heublein for $280 million. Now PepsiCo was paying nearly a billion.

The irony wasn't lost on industry observers: at the time PepsiCo bought Kentucky Fried Chicken, the New York Times reported KFC was Coke's second-largest fountain account, behind McDonald's. Yet about 20% of KFC's stores served Pepsi products, and PepsiCo insisted the acquisition was about more than just beverage sales—it was about building a restaurant empire.

Through the late 1980s and early 1990s, PepsiCo went on an acquisition spree that would make private equity blush. In 1992, PepsiCo acquired California Pizza Kitchen. In 1993, it acquired Chevys Fresh Mex, D'Angelo Grilled Sandwiches, and the American division of Canadian chain East Side Mario's. The strategy was clear: dominate every segment of casual dining, from pizza to Mexican to Italian to sandwiches.

Wayne Calloway, who succeeded Kendall as CEO in 1986, pushed even harder into restaurants. His vision: PepsiCo would become the world's largest restaurant company, leveraging operational synergies across brands while guaranteeing Pepsi exclusivity. Multi-branding—putting a KFC and Taco Bell in the same location—would maximize real estate efficiency. Shared supply chains would drive down costs. The beverage tie-in was just gravy.

But cracks were emerging. Restaurant margins consistently lagged behind PepsiCo's core beverage and snack businesses. While Pepsi and Frito-Lay generated 15-20% operating margins, the restaurant division struggled to break 10%. Wall Street analysts increasingly questioned why a CPG company was running restaurants—businesses with fundamentally different economics, capital requirements, and operational complexity.

The franchisee relationships deteriorated throughout the 1990s. KFC franchisees, in particular, revolted against PepsiCo's corporate mandates. They resented being forced to sell Pepsi when many believed Coke would drive higher sales. They bristled at new product initiatives pushed from Purchase headquarters by executives who'd never worked a fryer. The relationship became so toxic that franchisees formed opposition groups and threatened legal action.KFC's international division saw significant growth during the 1990s, but domestic sales were sluggish due to intense competition and failed product launches. Relations between its parent company and franchisees had deteriorated—in August 1989, president John Cranor proposed amendments that would allow PepsiCo to take over weak franchises and increase royalty fees, sparking a lawsuit that wasn't resolved until 1996. The brand hadn't achieved its business plan and had no same-store sales growth for seven straight years, becoming "a graveyard for PepsiCo executives".

The mid-1990s brought a breaking point. Consumers were demanding healthier foods and fast foods were considered the worst of the worst—this was when Kentucky Fried Chicken rebranded as simply KFC. PepsiCo wasn't seeing the return on its assets from restaurants that it saw with its beverage and snack food divisions, and decided the drain of capital expenditure wasn't worth it.

Roger Enrico, who became PepsiCo CEO in 1996, saw the writing on the wall. The restaurant division's operating margins of 8-10% looked anemic next to Pepsi-Cola's 15% and Frito-Lay's 20%. Wall Street valued PepsiCo as a CPG company, not a restaurant operator. The synergies that seemed so obvious in 1977—captive beverage distribution, shared marketing, operational leverage—had become millstones. Franchisees resented corporate interference, competitors switched from Pepsi to Coke in protest, and the complexity of managing restaurants distracted from PepsiCo's core business.

The decision to exit came down to focus. PepsiCo could be a good CPG company with a mediocre restaurant division, or it could be a great CPG company, period. The choice, painful as it was after twenty years and billions in investment, was clear.

III. The Spin-Off: Birth of Tricon Global Restaurants (1997)

The boardroom at PepsiCo's Purchase headquarters was silent as Roger Enrico laid out his vision. It was January 23, 1997, and he was proposing the unthinkable: spinning off the entire restaurant division. Twenty years, billions of dollars, over 30,000 locations worldwide—all to be cut loose in what would be one of the largest corporate spin-offs in history.

"We're freeing two companies to achieve their full potential," Enrico told analysts on the conference call. Behind the corporate speak was a stark reality: the restaurants were dragging down PepsiCo's valuation, and something had to give.

Created in 1997 as Tricon Global Restaurants, Inc. from PepsiCo's fast food division as the parent corporation of the KFC, Pizza Hut and Taco Bell restaurant companies. The decision was announced in January and the spin off was effected on October 6. Tricon selected Louisville, also the site of KFC's headquarters, as its corporate headquarters. Taco Bell and Pizza Hut continued to be headquartered in Irvine, California and Dallas, Texas, respectively.

The new company faced immediate existential threats. Within weeks of the spin-off, Ameriserve, Tricon's primary food distributor serving 11,000 restaurants, began showing signs of financial distress. The company had taken on massive debt to win the PepsiCo restaurant supply contract, betting everything on volume over margins. By 1999, Ameriserve would declare bankruptcy, leaving Tricon scrambling to keep restaurants supplied with everything from chicken to taco shells.

David Novak, who had turned around KFC as brand president, was tapped to lead the new entity. A marketing executive who'd spent years at PepsiCo learning the restaurant business from the ground up, Novak faced a herculean task. He inherited three iconic brands that barely spoke to each other, 250,000 employees who didn't know if they still had jobs, and franchisees who'd spent years fighting with PepsiCo corporate.

The strategic rationale for independence was compelling on paper. Without PepsiCo's corporate overhead, the restaurants could move faster, make decisions closer to the customer, and most importantly, repair the toxic franchisee relationships that had festered under PepsiCo's ownership. Novak had already proven at KFC that working with franchisees could drive innovation—Crispy Strips were invented by an Arkansas franchisee, and the pot pie was similarly developed alongside franchisees.

But the challenges were monumental. Tricon was born with $4.7 billion in debt, a legacy of PepsiCo's aggressive expansion. The company had to build entire corporate functions from scratch—IT systems, supply chain management, human resources—all while keeping 30,000 restaurants running. And looming over everything was the lifetime Pepsi contract, which guaranteed PepsiCo exclusive beverage rights in perpetuity but also locked Tricon out of negotiating with Coca-Cola, even in markets where Coke dominated.

The early wins came from what Novak called "multi-branding"—putting two or three brands under one roof. A KFC and Taco Bell sharing a kitchen and dining room could serve different dayparts, maximize real estate efficiency, and reduce operating costs. By March 2002, the Tricon-Yorkshire multibranding test consisted of 83 KFC/A&Ws, six KFC/Long John Silver's and three Taco Bell/Long John Silver's and was considered successful.

Novak's masterstroke was cultural. He created what became known as the "recognition culture," where every employee, from fry cooks to executives, was celebrated for achievements. He personally handed out rubber chickens, cheese heads, and "floppy chickens" to high performers. It sounds hokey, but it worked. Employee turnover dropped, same-store sales started growing, and franchisees began viewing corporate as a partner rather than an adversary.

The multi-branding experiments revealed something profound: customers didn't care about corporate structure—they cared about convenience. A family could satisfy everyone's craving in one stop. Dad wanted Original Recipe, mom preferred a chalupa, the kids demanded pizza. Tricon could deliver all three, often from the same kitchen.

By 2001, the transformation was gaining momentum. Same-store sales were growing across all three brands for the first time in years. The Ameriserve crisis, which could have destroyed the company, had forced Tricon to build a more resilient, diversified supply chain. Franchisees were opening new units at the fastest pace in a decade. The company that PepsiCo couldn't wait to jettison was finding its footing.

IV. Transformation to Yum! Brands (2002-2011)

The name "Tricon" had always been a placeholder—corporate, forgettable, meaningless to consumers. David Novak knew the company needed an identity that matched its ambitions. In a brainstorming session in late 2001, someone suggested "Yum!"—simple, universal, emotional. Critics called it silly. Novak called it perfect.

In March 2002, Tricon announced the acquisition of Lexington, Kentucky-based Yorkshire Global Restaurants, owner of the Long John Silver's and A&W Restaurants chains and its intention to change the company's name to Yum! The $320 million deal brought two more brands into the fold, pushing total system sales past $20 billion and making Yum! the world's largest restaurant company by unit count.

The rebranding was about more than just a name. Novak was building something unprecedented: a restaurant company that thought like a consumer packaged goods company. Each brand would maintain its identity while sharing back-office functions, supply chains, and real estate. The corporate center would be lean—just 1,000 employees supporting 33,000 restaurants—focusing on what Novak called "the power of one": one company, multiple brands, infinite possibilities.

The portfolio approach created unexpected synergies. Long John Silver's, struggling as a standalone concept, thrived when paired with A&W in multi-brand locations. The seafood-and-root beer combination sounded odd but worked brilliantly in small towns across America where real estate was scarce and customers wanted variety. By 2005, Yum! was opening a new restaurant every five hours somewhere in the world.

But the real story of this era was China. KFC had entered China in 1987, but under Yum!'s leadership, it exploded. Sam Su, who ran Yum! China, localized the menu beyond recognition—congee for breakfast, rice dishes, egg tarts, tree fungus salad. Traditionalists were horrified. Su didn't care. By 2005, KFC was opening a new restaurant in China every other day. Pizza Hut, repositioned as a casual dining concept with wine and escargot, became the place Chinese families went to celebrate special occasions.

The financial engineering was equally impressive. Yum! pioneered the asset-light model in restaurants, aggressively refranchising company-owned stores. The math was compelling: a company store might generate $1 million in revenue but tie up $500,000 in capital. That same store, franchised, would generate $50,000 in pure-margin royalty fees with zero capital investment. By 2007, 75% of Yum! restaurants were franchised, up from 50% at the spin-off.

David Novak's leadership philosophy permeated everything. He wrote personal notes to thousands of employees. He created Yum! University to train future leaders. He established the "Dynasty Growth Model"—same-store sales growth plus new unit development—that became the industry standard for measuring restaurant performance. Wall Street loved the predictability: steady 5% same-store sales growth, 5-7% unit growth, EPS growth in the low teens, every year like clockwork.

The 2008 financial crisis tested the model but proved its resilience. While casual dining chains collapsed, Yum!'s value positioning thrived. Taco Bell's "Why Pay More" campaign, featuring 89-cent items, drove traffic while competitors raised prices. KFC introduced the "Fill Up" box meals. Pizza Hut launched the $10 Any Pizza deal. The company emerged from the recession stronger, with record margins and accelerating international growth.

In January 2011, Yum! announced its intentions to dispose of its Long John Silver's and A&W brands to focus on its core brands of KFC, Pizza Hut and Taco Bell. For the decade leading up to the company's announcement, major growth had relied on international expansion. With little presence outside North America, the two chains no longer fit in the company's long-term growth plans.

The divestiture of Long John Silver's and A&W marked a strategic inflection point. After a decade of portfolio expansion, Yum! was refocusing on its three core brands—the ones with true global potential. The company had learned that in restaurants, like in investing, concentration often beats diversification.

V. The China Phenomenon & Spin-Off (2000s-2016)

The meeting in Shanghai should have been a celebration. It was 2012, and Yum! China had just opened its 5,000th restaurant. Sam Su, president of Yum! China, had built something unprecedented: a Western fast-food company that was more popular in China than in America. But instead of champagne, the leadership team was in crisis mode. Chinese state media had just broadcast an exposé claiming KFC suppliers were using growth hormones and antibiotics in violation of Chinese law.

The scandal would wipe out two years of same-store sales growth in two months. But it also revealed a deeper truth: Yum! China had become too big, too complex, and too important to remain tethered to Louisville.

The China story began modestly. KFC was the first American fast-food chain to open in China in 1987, with a single location near Tiananmen Square. The conventional wisdom was that Chinese consumers wouldn't eat American fast food. The conventional wisdom was spectacularly wrong. By 2000, KFC had 400 locations. By 2010, it had 3,000. At its peak, Yum! China was opening three new restaurants every day.

The secret was localization beyond what any Western company had attempted. KFC China's menu was 50% different from the U.S. version. Breakfast included congee and youtiao (fried dough sticks). The "Dragon Twister" wrap became a bestseller. During Chinese New Year, KFC offered family buckets with dishes designed for sharing. The Colonel's image was tweaked to look more grandfatherly, less military. In consumer surveys, many Chinese didn't even know KFC was American.

Pizza Hut's transformation was even more radical. Su repositioned it as "Pizza Hut Casual Dining"—a sit-down restaurant where middle-class Chinese families celebrated birthdays and anniversaries. The menu included steaks, pasta, wine, and afternoon tea service. A Pizza Hut in Shanghai looked nothing like one in Chicago, and that was precisely the point. Average check sizes were three times higher than in the U.S.

The numbers were staggering. By 2015, Yum! China generated $6.9 billion in revenue—more than a third of Yum!'s global total. Operating margins exceeded 15%, far higher than the U.S. business. China had 7,000 restaurants versus 15,000 in the U.S., but contributed nearly as much operating profit. Every multinational CEO wanted to know Su's secret.

But success bred complexity. Yum! China needed different supply chains, different marketing, different restaurant formats. Food safety scandals in 2012 and 2014—tainted chicken, expired meat—required crisis management expertise specific to Chinese media and regulators. The subsidiary was negotiating with Chinese provincial governments, navigating Byzantine real estate markets, competing with local chains that copied KFC's model down to the red-and-white color scheme.

Meanwhile, activist investors were circling. Keith Meister of Corvex Management argued that Yum! was undervalued because investors couldn't properly value the China business buried inside a global restaurant company. The China operation deserved a technology multiple—it was digitizing faster than any restaurant company in the world—while the rest of Yum! traded at traditional restaurant valuations.

The board faced an agonizing decision. China represented Yum!'s future—the market where it could add 10,000 more restaurants. But keeping it meant accepting a conglomerate discount, complexity that distracted management, and regulatory risks that could tank the entire company's stock price with one food safety incident. In October 2016, Yum! Brands spun off their Chinese operations into Yum China. This privately held company not only operates all KFC, Pizza Hut, and Taco Bell restaurants in mainland China but also has full rights to several other quick service restaurant chains. The separation was completed on November 1, 2016, with approximately 364 million shares of Yum China stock distributed in the spin-off.

The decision crystallized when Primavera Capital Group and Ant Financial Services agreed to invest $460 million in the new entity—Primavera Capital Group invested $410 million and Ant Financial Services contributed $50 million. The strategic investors brought more than capital; they provided local expertise and government relationships critical for navigating China's complex regulatory environment.

The spin-off transformed two companies overnight. Yum China became a licensee paying 3% royalties on system sales, while Yum! Brands became a pure-play franchisor focused on asset-light growth. Wall Street loved it. Morgan Stanley initiated coverage noting Yum China's penetration in China was about 20 restaurants per million people versus the 600 per million in the U.S.—implying massive growth potential.

For Greg Creed, who had taken over as CEO from David Novak in 2015, the spin-off was validation of a broader strategy: simplify, focus, accelerate. The China business, as successful as it was, had become a distraction. Food safety scares tanked the stock. Currency fluctuations created earnings volatility. The operational complexity of running 7,000 company-owned restaurants in China while franchising everywhere else confused investors.

The numbers post-spin told the story. Yum! Brands' valuation multiple expanded from 18x to 25x earnings as investors embraced the predictable, capital-light model. Yum China, trading independently, commanded a premium valuation reflecting its growth potential and digital leadership. Combined, the two companies were worth 40% more than the pre-spin entity.

VI. The Modern Yum!: Digital Transformation & Asset-Light Model (2016-Present)

The PowerPoint slide that David Gibbs showed the board in 2017 was stark: a graph showing third-party delivery sales exploding from nothing to $50 billion globally in just three years. The CFO's message was clear: Yum! either owned the digital relationship with customers or became a commodity supplier to Uber Eats and DoorDash.

Gibbs had been the architect of Yum!'s transformation even before becoming CEO. David Gibbs gained experience at all three of Yum! Brands' major chains – Taco Bell, KFC, and Pizza Hut – before becoming its CEO in 2020. As CFO, he was the chief architect of Yum! Brands' financial, refranchising and restaurant development strategy to transform the company into a capital-light, pure-play franchisor.

The refranchising strategy was audacious in its scope. In 2016, Yum! still operated nearly 10% of its restaurants—capital-intensive assets that generated revenue but compressed margins. Gibbs' plan: refranchise down to 2% ownership, essentially becoming a brand management and technology platform company. Critics warned that giving up operational control would weaken the brands. Gibbs saw it differently—franchisees, with skin in the game, would operate better than corporate ever could.

The transformation happened with stunning speed. Between 2016 and 2019, Yum! refranchised over 3,000 restaurants, generating $2.3 billion in proceeds. The impact on financials was dramatic: operating margins expanded from 28% to 48%, return on invested capital soared above 100%, and free cash flow conversion exceeded 100% of net income. Yum! had become one of the most capital-efficient companies in the S&P 500.

Then came COVID-19. On March 11, 2020, the WHO declared a pandemic. Within weeks, dining rooms worldwide were shut. For a company that had just transformed into an asset-light franchisor, the timing seemed catastrophic. Franchisees, already leveraged from buying restaurants, faced potential bankruptcy. Analysts predicted a bloodbath. Instead, COVID became Yum!'s finest hour. The company established a Global Franchise Health and COVID-19 Support Team, providing grace periods for royalty payments and deferring capital obligations. Gibbs himself gave up his salary for a year, redirecting it to $1,000 bonuses for restaurant general managers. At the peak, 11,000 Yum! restaurants were closed worldwide, yet the company emerged stronger.

The crisis accelerated digital transformation by five years in five months. Contactless delivery, mobile ordering, curbside pickup—features that had been nice-to-have became essential overnight. Pizza Hut, which had been struggling with delivery competition, suddenly found its infrastructure perfectly suited for lockdown dining. Taco Bell's drive-thru dominance—75% of sales pre-COVID—became a competitive moat. KFC's international markets, particularly Asia which recovered first, provided a playbook for the rest of the world.

The company's acquisition of Southern California-based fast-casual brand Habit Burger Grill closed in March 2020—terrible timing that became a defining moment. His first major move as CEO was a significant milestone for Yum Brands, as it brought a fourth brand into the family. Rather than retreat, Gibbs doubled down, using Yum!'s scale to support Habit through the crisis without laying off a single employee.

But the real transformation was technological. In 2020 and 2021, Yum! Brands made a series of strategic acquisitions focused on technology, targeting companies specializing in order management, delivery logistics, and AI-powered consumer insights. The company acquired Dragontail Systems for $69.1 million, Tictuk Technologies, and Kvantum Inc., an AI-based consumer insights company. These technologies are now being unified and integrated across Yum!'s restaurant brands under a single platform called Byte.

The Byte platform represents Yum!'s answer to the aggregator threat. Rather than ceding the customer relationship to DoorDash or Uber Eats, Yum! built its own technology stack—order management, delivery dispatch, customer data analytics, kitchen automation. By 2023, digital sales exceeded $27 billion, representing over 40% of system sales. The company that once relied entirely on third-party platforms now owned the entire customer journey.

The financial impact has been profound. Despite the pandemic, Yum! returned to growth faster than any major restaurant company. Same-store sales recovered to positive territory by Q3 2020. The stock, which bottomed at $54 in March 2020, soared past $130 by 2021. The company resumed share buybacks, increased its dividend, and accelerated unit growth—all while maintaining investment-grade credit ratings.

VII. Brand Deep Dives: The Three Pillars

KFC: The International Powerhouse

Walk into a KFC in Shanghai at lunch hour and you'll struggle to recognize the brand Colonel Sanders founded. Over half operate under the KFC banner, making it the largest brand in the portfolio by footprint—more than 30,000 locations globally. But the menu tells the real story: congee with preserved egg, egg tarts that rival Hong Kong's best, mushroom rice bowls, and yes, somewhere on the menu, Original Recipe chicken.

KFC's transformation from American southern comfort food to global phenomenon represents perhaps the greatest localization success in fast-food history. In China, where KFC operates more locations than in the United States, the brand isn't seen as foreign—it's woven into the cultural fabric. Chinese families celebrate birthdays at KFC. Business deals close over Family Buckets. During Chinese New Year, KFC sells more meals than any other restaurant chain in the country.

The numbers are staggering. KFC generates over $30 billion in system sales annually, with international markets contributing 70% of profits. In markets like South Africa, KFC commands over 40% market share in quick-service restaurants. In the UK, it's the largest restaurant chain by sales after McDonald's. The brand opens three new restaurants every day, mostly in emerging markets where fried chicken represents aspiration, not indulgence.

The secret has been radical localization within a consistent framework. Every KFC globally serves Original Recipe, but that might represent just 30% of the menu. In Japan, KFC's Christmas campaign has made fried chicken a holiday tradition for millions—customers order weeks in advance. In India, where much of the population is vegetarian, KFC developed an entire plant-based menu. In Indonesia, KFC serves rice with every meal because customers won't consider it a proper meal otherwise.

Digital innovation at KFC outpaces its sister brands. In China, facial recognition technology allows payment without pulling out a phone. AI-powered woks ensure consistent cooking across thousands of locations. Voice-activated ordering in drive-thrus reduces wait times by 30%. The brand that started with pressure fryers in the 1950s now runs some of the most technologically advanced kitchens in the world.

Pizza Hut: The Reinvention Challenge

Pizza Hut accounts for approximately 20,000 locations, but the brand's story over the past decade has been one of constant reinvention in the face of existential competition. Domino's technology revolution, third-party delivery disruption, and fast-casual pizza's rise all threatened Pizza Hut's traditional model. The brand that invented pan pizza found itself playing catch-up in its own category.

The challenges are particularly acute in the United States, where Pizza Hut's dine-in heritage became a liability. Those distinctive red roofs that once symbolized family dinners became albatrosses—expensive real estate in an increasingly delivery-focused world. Between 2015 and 2020, Pizza Hut closed over 1,000 traditional locations while opening smaller delivery/carryout units. The transformation was painful but necessary.

Internationally, Pizza Hut tells a completely different story. In China, upscale casual dining Pizza Huts serve wine, steak, and afternoon tea. In India, Pizza Hut competes not with Domino's but with casual dining chains, offering a date-night experience at QSR prices. The dichotomy is striking: while U.S. Pizza Hut fights for delivery share, international Pizza Hut creates dining destinations.

The brand's response has been to embrace its split personality. In the U.S., Pizza Hut is going all-in on value and convenience—the $10 Tastemaker, partnerships with every major delivery platform, and ghost kitchens in urban markets. Internationally, it's doubling down on experience—table service, premium ingredients, localized flavors that would shock American customers.

Technology investment is finally paying dividends. Pizza Hut's Hut Rewards program has 20 million members. The brand's delivery times have improved by 15% through AI-powered routing. Digital sales represent 75% of transactions in developed markets. But the question remains whether Pizza Hut can reclaim innovation leadership in a category it once defined.

Taco Bell: The Innovation Machine

Taco Bell runs just under 9,000 restaurants, the smallest footprint of the three core brands, but generates outsized influence on culture and innovation. This is the brand that turned a simple hard-shell taco into Doritos Locos Tacos, selling a billion units in the first year. That launches menu items designed specifically to go viral on social media. That convinced Americans to eat a fourth meal at 2 AM.

Taco Bell's innovation extends beyond food. The brand pioneered the value menu with the 59-79-99 cent menu in the 1990s. It created the concept of limited-time offers as marketing events—the return of the Mexican Pizza generated more media coverage than most Super Bowl ads. The Cantina concept brought alcohol to fast food. The Taco Bell Hotel was a three-day brand experience that sold out in two minutes.

The numbers validate the strategy. Taco Bell consistently delivers the highest same-store sales growth in the Yum! portfolio. Average unit volumes exceed $1.8 million, among the highest in fast food. The brand's customer base skews younger than any major QSR chain—Gen Z considers Taco Bell not just food but a lifestyle brand.

International expansion represents Taco Bell's next frontier. After decades of false starts, the brand is finally gaining traction overseas. The key was abandoning the assumption that international customers wanted authentic Mexican food. Instead, Taco Bell positioned itself as rebellious American fast food—a brand that happens to use Mexican-inspired ingredients. Stores in Spain stay open until 4 AM. Locations in Japan feature exclusive menu items that become Instagram phenomena.

The cultural relevance can't be measured in traditional metrics. Taco Bell wedding chapels in Las Vegas book months in advance. The brand's Twitter account, with its surreal humor and engagement with fans, has become a marketing case study. When Taco Bell announced it was removing the Mexican Pizza, the outcry was so intense—including a Change.org petition with 200,000 signatures—that the company brought it back.

Portfolio Synergies

The genius of the three-brand portfolio becomes clear when you examine daypart coverage. KFC dominates lunch and dinner. Pizza Hut owns family occasions and delivery. Taco Bell rules late night and value. Together, they capture nearly every eating occasion except breakfast—a gap the brands are aggressively targeting with varying success.

Operational synergies run deeper than most realize. All three brands can share kitchen equipment for many items. Supply chain overlap—cheese, vegetables, proteins—creates purchasing power that independent chains can't match. Digital infrastructure built for one brand deploys across all three. When Yum! negotiates with DoorDash, it represents 50,000 restaurants, not individual brands.

The portfolio approach also enables risk diversification. When Pizza Hut struggled with U.S. delivery competition, KFC international growth compensated. When COVID shuttered dine-in restaurants, Taco Bell's drive-thru dominance balanced the portfolio. When chicken prices spike, Pizza Hut and Taco Bell absorb the impact. No single commodity, geography, or consumer trend can cripple the company.

VIII. Playbook: The Yum! System

The Franchise Model Mastery

At 98% franchised, Yum! has achieved something remarkable: it generates $7 billion in revenue while operating just 1,000 restaurants directly. The math is beautiful in its simplicity. A company-operated restaurant might generate $2 million in sales but require $1 million in operating costs and $500,000 in capital investment. That same restaurant, franchised, generates $100,000 in pure-margin royalties (5% of sales) with zero capital investment and minimal operating cost.

But the real mastery lies in franchise relations. While competitors battle with operators over everything from menu prices to remodel requirements, Yum! franchisees compete to build new units. The secret: aligned incentives. Franchisees participate in menu development. They vote on marketing campaigns. They share in digital platform economics. When delivery orders come through Yum!'s platform rather than third-party aggregators, franchisees save 10-15% in fees—savings that flow directly to operator profits.

The franchise agreement structure itself demonstrates sophistication. Development agreements require operators to build multiple units over specified timeframes, ensuring growth. Master franchise agreements for international markets transfer operational responsibility while maintaining brand standards. The company provides just enough support—brand marketing, product innovation, technology platforms—while letting local operators handle real estate, labor, and customer service.

The results speak for themselves. Yum! franchisees generate average returns on investment exceeding 20%. Unit-level economics remain strong even in mature markets. The company hasn't faced a major franchisee revolt in over a decade. When private equity firms evaluate restaurant investments, Yum! franchises consistently command the highest multiples.

Portfolio Management Philosophy

The decision to acquire Long John Silver's and A&W in 2002, then divest them in 2011, offers a masterclass in portfolio discipline. In January 2011, Yum! announced its intentions to dispose of its Long John Silver's and A&W brands to focus on its core brands of KFC, Pizza Hut and Taco Bell. For the decade leading up to the company's announcement, major growth had relied on international expansion. With little presence outside North America, the two chains no longer fit in the company's long-term growth plans.

The acquisition made sense in 2002—multi-branding was new, and pairing seafood with chicken or root beer with pizza created unique value propositions in small markets. But as international expansion accelerated, the limitations became clear. Long John Silver's had no international presence. A&W competed with company-owned beverage brands. Management attention divided across five brands diluted focus on the core three.

The 2020 Habit Burger acquisition demonstrates evolved thinking. Unlike Long John Silver's, Habit offers international potential. Its fast-casual positioning provides a platform for premiumization experiments. The timing—closing during COVID—was unfortunate, but strategic logic remains sound: own multiple price points and dining occasions while maintaining operational focus.

Capital Allocation Excellence

Crossed the $60 billion system sales threshold and exceeded all aspects of our long-term growth algorithm—but system sales tell only part of the story. Yum!'s capital allocation framework balances growth investment, dividends, and buybacks with remarkable consistency.

Since 2016, the company has returned over $20 billion to shareholders through dividends and buybacks while maintaining investment-grade credit ratings. The dividend, raised annually for 15 consecutive years, provides steady income. Share buybacks, opportunistic but disciplined, have reduced share count by 30% since the China spin-off.

Growth investment focuses on technology and franchisee success. The $200 million annual technology spend might seem modest for a $7 billion revenue company, but remember: franchisees fund their own capital expenditures. Yum! invests in platforms that benefit the entire system—digital ordering, data analytics, supply chain technology—rather than individual restaurant assets.

The company maintains optimal leverage around 5x EBITDA, below the 6x threshold that would trigger credit downgrades but high enough to maximize equity returns. This capital structure discipline allowed Yum! to weather COVID without cutting the dividend or diluting shareholders, unlike many restaurant peers.

Technology as Competitive Advantage

The Byte platform represents a fundamental shift in how Yum! views technology. Rather than outsourcing to third parties or buying point solutions, the company is building an integrated technology stack that it can monetize across the system—and potentially beyond.

Consider the complexity Byte solves: A customer orders through the KFC app. Byte processes the payment, routes the order to the kitchen display system, dispatches a delivery driver (either Yum!'s or third-party), tracks the order in real-time, collects customer feedback, and feeds data into the recommendation engine for the next order. All of this happens in milliseconds, across dozens of countries, in multiple languages and currencies.

The platform economics are compelling. Yum! charges franchisees a technology fee—typically 1-2% of sales—for platform access. With $65 billion in system sales, that's potentially $1 billion in high-margin technology revenue. More importantly, owning the platform means owning the customer data, enabling personalized marketing that drives frequency and ticket size.

Culture and Talent Development

David Novak's "recognition culture" legacy persists throughout Yum!. The company's leadership development programs—particularly the "Taking People With You" curriculum—have produced dozens of restaurant industry CEOs. When competitors need leadership, they often poach from Yum!'s bench.

The approach to human capital mirrors the franchise model: push responsibility down, reward performance lavishly, and create ownership mentality even among hourly workers. Restaurant general managers receive stock options. High-performing franchisees get first rights to new markets. The annual franchisee convention feels more like a revival meeting than a corporate gathering.

This culture drives innovation from the bottom up. The greatest menu successes—KFC's Nashville Hot Chicken, Taco Bell's Chalupa, Pizza Hut's Stuffed Crust—often originated with franchisees or restaurant managers, not corporate R&D. By creating systems to capture and scale these innovations, Yum! harnesses the creativity of 450,000 global employees.

IX. Analysis & Investment Case

Bull Case: The Platform Story

The optimistic view sees Yum! as fundamentally misunderstood by markets that still view it as a traditional restaurant company. More than 61,000 restaurants across over 155 countries and territories. This scale places it among the largest fast-food chains in the world by number of locations, surpassing giants like McDonald's, Domino's, and Starbucks. This isn't just about restaurant count—it's about building the AWS of food service.

The digital transformation trajectory suggests massive value creation ahead. With digital sales already exceeding $27 billion and growing 20% annually, Yum! could reach $50 billion in digital sales by 2027. At platform economics—20-30% margins versus 5-10% for traditional operations—the incremental profit potential is enormous. If Byte becomes an industry platform that other restaurants adopt, the company transforms from restaurant operator to technology provider.

Emerging market growth remains in early innings. Morgan Stanley says Yum China's penetration in China is about 20 restaurants per million people versus the 600 per million in the U.S. of its former parent. Apply similar math to India, Africa, and Southeast Asia, and the runway extends decades. These markets are digitalizing faster than developed countries, playing to Yum!'s platform strengths.

The asset-light model provides downside protection that investors underappreciate. With 98% franchised, Yum! faces minimal direct exposure to labor inflation, commodity volatility, or real estate risks. Royalty streams are remarkably stable—even during COVID, systemwide sales only declined 4% at the trough. The variable cost structure means margins expand automatically as sales grow.

Generated revenue amounting to 7.08 billion U.S. dollars from its global operations in 2023, but bulls argue the revenue quality deserves premium valuation. Franchise royalties are essentially software-like recurring revenue. Technology fees are growing faster than traditional royalties. International revenues provide currency diversification. The combination deserves SaaS-like multiples, not restaurant multiples.

Bear Case: Structural Headwinds

Skeptics point to fundamental challenges that no amount of financial engineering can solve. QSR market saturation in developed markets is real—the U.S. has one restaurant per 300 people. Growth requires taking share, not expanding the pie. With every major competitor investing billions in digital and delivery, Yum!'s first-mover advantage is evaporating.

Rising labor costs present an existential challenge the asset-light model doesn't solve. Franchisees absorb the direct impact, but struggling unit economics eventually flow through to the franchisor. California's $20 minimum wage for fast-food workers provides a preview—some franchisees are already closing units rather than absorbing the losses. If unit economics break, the entire franchise model breaks with them.

Competition from delivery aggregators remains underappreciated. DoorDash and Uber Eats are becoming the primary customer interface, reducing restaurants to commodity suppliers. Yes, Yum! is building its own platform, but aggregators have scale advantages—they offer consumers choice across hundreds of restaurants, not just three brands. The 30% of sales through third-party platforms represent profits Yum! will never fully recapture.

Geopolitical risks loom larger than bulls acknowledge. Middle East tensions threaten 5,000 restaurants across the region. China relations could deteriorate, impacting royalty flows from Yum China. Emerging markets that drive growth projections face currency crises, political instability, and economic volatility that could derail expansion plans.

The consumer shift to healthier options represents a secular headwind none of Yum!'s brands are positioned to address. KFC is fried chicken. Pizza Hut is cheese and carbs. Taco Bell, despite menu innovations, is perceived as processed food. Younger consumers increasingly favor fresh, local, sustainable options—attributes antithetical to global fast-food chains.

Competitive Reality Check

Versus McDonald's, Yum! appears structurally disadvantaged despite more locations. McDonald's generates $23 billion in revenue from 40,000 restaurants; Yum! generates $7 billion from 61,000. McDonald's commands a $210 billion market cap versus Yum!'s $40 billion. The difference: brand power. McDonald's can charge premium prices and generate higher unit volumes that more than offset Yum!'s location advantage.

Restaurant Brands International provides another sobering comparison. With just four brands and 30,000 locations, RBI generates similar EBITDA to Yum!. The implication: Yum!'s portfolio complexity might destroy value rather than create it. Tim Hortons, Burger King, Popeyes, and Firehouse Subs arguably offer better growth profiles than Pizza Hut and KFC in developed markets.

Domino's technological leadership in pizza delivery remains unmatched despite Pizza Hut's improvements. Domino's generates $4.5 million average unit volume versus Pizza Hut's $1.1 million. The technology gap manifests in every metric: delivery times, order accuracy, customer satisfaction. Pizza Hut is perpetually playing catch-up in its core category.

Yet Yum!'s diversification provides resilience none of these competitors match. When chicken prices spike, McDonald's margins compress while Yum! shifts marketing to pizza and tacos. When China locked down, RBI had minimal exposure while Yum China managed through the crisis. The portfolio approach trades efficiency for stability—a reasonable exchange in uncertain times.

X. Looking Forward: The Next Chapter

The boardroom in Louisville was buzzing with anticipation. After a global search, Board of Directors has unanimously elected Chris Turner, 50, as Chief Executive Officer, effective October 1, 2025. Turner, who currently serves as Chief Financial & Franchise Officer, represents continuity and change—an insider who understands the culture but brings fresh perspective on technology and automation.

Turner inherits a company at an inflection point. The asset-light transformation is complete. The technology platform is built. International expansion continues. But the next phase demands different capabilities: AI integration, automation implementation, and navigating a world where traditional employment models might not exist. The AI revolution at Yum! is already underway. Yum! Brands announced today that it is partnering with NVIDIA to accelerate the development of innovative AI technologies for Yum! restaurants around the globe. Yum! Brands, the world's largest restaurant company with over 61,000 locations, is NVIDIA's first AI restaurant partner. This collaboration brings the two powerhouses together to integrate AI into the restaurant and retail industry at an unprecedented scale.

Through a direct collaboration at the developer level, Yum! was able to deploy NVIDIA AI-powered voice AI agents within three months. This partnership will harness easy-to-use NVIDIA NIM microservices, part of NVIDIA AI Enterprise and available on Amazon Web Services (AWS), to optimize and create efficiencies in restaurant operations, enhancing team member and customer experiences. The AI solutions will be instrumental in three key areas across Yum! Brands: Voice Automated Order-Taking AI Agents: Advancing drive-thru and call center operations with conversational AI, powered by NVIDIA Riva and NVIDIA NIM microservices, that adapts to human speech patterns, understands complex menus and customer preferences and enables a more natural, seamless ordering experience.

The voice AI deployment represents just the beginning. Yum!'s voice AI agents are already being deployed across its brands, including in call centers to handle phone orders when demand surges during events like game days. An expanded rollout of AI solutions at up to 500 restaurants is expected this year. The technology understands natural speech, processes complex orders, suggests add-ons, and operates in multiple languages—essentially replacing human order-takers with 100% accuracy and infinite patience.

But automation extends beyond ordering. Kitchen operations are being revolutionized through AI-powered systems that predict demand, optimize cooking schedules, and ensure consistency across thousands of locations. Using NIM microservices, Yum! can deploy applications analyzing performance metrics across thousands of locations to generate customized recommendations for managers, identifying what top-performing stores do differently and applying those insights system-wide.

The financial impact is already visible. "This quarter, we successfully launched personalized AI-driven marketing campaigns that, relative to traditional digital marketing campaigns, generated significant increases in consumer engagement, leading to increased purchases and a reduction in consumer churn," said Yum CFO Chris Turner on the call with investors.

Ghost kitchens and virtual brands represent another growth vector. Yum! is testing delivery-only locations that require 80% less capital than traditional restaurants. These ghost kitchens can operate multiple brands from a single location, testing new concepts without brand risk. A Pizza Hut ghost kitchen might also operate a wings-only virtual brand, a pasta concept, and experimental menu items that would never appear in traditional locations. In 2024, Yum plans to pass several major milestones for its global footprint. Yum will surpass 60,000 locations, including a KFC footprint of more than 30,000 restaurants and a Pizza Hut tally of beyond 20,000. The company opens a new restaurant every three hours, with particularly aggressive expansion in emerging markets where penetration remains low relative to developed markets.

The next acquisition targets are telling. Rather than traditional restaurant chains, Yum! is eyeing technology companies, ghost kitchen operators, and potentially plant-based brands that could retrofit into existing kitchens. The Habit Burger acquisition proved the company can successfully integrate during crisis; the next deal will likely push into adjacent categories or pure technology plays.

Emerging market expansion remains the primary growth driver. India, with 1.4 billion people and fewer than 1,000 Yum! restaurants, represents decades of growth. Africa, largely untapped except for South Africa, could support 10,000 locations. Southeast Asia continues to urbanize rapidly, creating middle-class consumers who view Western QSR as aspirational dining.

The technology platform monetization potential extends beyond restaurants. If Byte becomes an industry standard—think Shopify for restaurants—Yum! could license the platform to independent operators, creating a SaaS business with 80% gross margins. The company's data on consumer preferences, accumulated from billions of transactions, has value to CPG companies, real estate developers, and financial services firms.

XI. Recent News

The leadership transition announcement came earlier than expected. Board of Directors has unanimously elected Chris Turner, 50, as Chief Executive Officer, effective October 1, 2025. Turner, who currently serves as Chief Financial & Franchise Officer for Yum! Brands, will succeed current Chief Executive Officer David Gibbs, who, in March 2025, informed the Board of Directors of his intention to retire in the next year after 37 years with the Company and a successful tenure as CEO.

Turner's background signals the company's technology-first future. In recent years, he has been instrumental in driving bold actions that leverage Yum!'s scale, such as accelerating the Company's digital and technology transformation through initiatives like the establishment of Byte by Yum!, an AI-driven restaurant technology platform; launching a centralized, global Supply Chain Center of Excellence; and the creation of Saucy by KFC, a bold new restaurant concept.

The Q4 2024 earnings results demonstrated continued momentum. Yum opened 1,804 new restaurants during the quarter, growing its unit count by 5%. The company is also rolling out Byte, its proprietary artificial intelligence-driven software for Pizza Hut, Taco Bell and KFC. For example, the tech makes it easier for consumers to place digital orders and reduces complexity in the kitchen for employees.

The NVIDIA AI partnership represents the most ambitious technology initiative yet. Yum! Brands (NYSE: YUM), the parent company of KFC, Taco Bell, Pizza Hut, and Habit Burger & Grill, announced today that it is partnering with NVIDIA to accelerate the development of innovative AI technologies for Yum! restaurants around the globe. Yum! Brands, the world's largest restaurant company with over 61,000 locations, is NVIDIA's first AI restaurant partner. This collaboration brings the two powerhouses together to integrate AI into the restaurant and retail industry at an unprecedented scale.

Yum!'s voice AI agents are already being deployed across its brands, including in call centers to handle phone orders when demand surges during events like game days. An expanded rollout of AI solutions at up to 500 restaurants is expected this year. The technology goes beyond just ordering—Using NIM microservices, Yum! can deploy applications analyzing performance metrics across thousands of locations to generate customized recommendations for managers, identifying what top-performing stores do differently and applying those insights system-wide.

The Byte platform rollout continues to accelerate. Yum's proprietary point-of-sale system, Poseidon, has been successfully rolled out to 1,700 Taco Bell locations, demonstrating the company's dedication to modernizing its transactional infrastructure. Additionally, the expansion of Dragontail, an AI-driven kitchen management system, to over 4,000 locations with plans for nearly 6,000 more, reflects Yum's ambition to optimize order sequencing for improved freshness and accuracy. The deployment of an AI inventory management system across the majority of KFC U.S. and Taco Bell restaurants marks a significant advancement in streamlining inventory processes. This system, set to expand to over 3,000 additional restaurants in 2024, exemplifies Yum's pursuit of operational excellence and accuracy in inventory management.

New market entries continue despite geopolitical challenges. The company faces headwinds in the Middle East, where boycotts related to the Israel-Hamas conflict have impacted sales. During the quarter, topline sales were impacted by the conflict in the Middle East region with varying degrees of impact across markets in the Middle East and Malaysia and Indonesia, CEO David Gibbs told analysts. Yet expansion continues: In 2024, Yum plans to pass several major milestones for its global footprint. Yum will surpass 60,000 locations, Gibbs said in a statement, including a KFC footprint of more than 30,000 restaurants and a Pizza Hut tally of beyond 20,000.

Franchise economics remain strong despite inflation pressures. The company's approach to supporting operators through economic challenges—grace periods during COVID, technology investments that improve unit economics, marketing support—has maintained franchisee loyalty even as California's $20 minimum wage and rising commodity costs pressure margins.

Competitive responses from McDonald's and others intensify. McDonald's partnership with Google Cloud for AI, Domino's continued technology leadership, and Chipotle's digital success demonstrate that Yum!'s technology advantages are temporary without continuous innovation. The quick-service restaurant wars are increasingly fought on digital battlefields rather than with menu items.

XII. Links & Resources

Official Investor Relations Materials: - Yum! Brands Investor Relations: investors.yum.com - 2023 Annual Report: s2.q4cdn.com/890585342/files/doc_financials/2023/ar/annual-report-2023/index.html - SEC Filings: sec.gov/edgar/browse/?CIK=1041061

Key Leadership Interviews & Presentations: - David Gibbs CNBC Interview on COVID Response (March 2020) - Chris Turner Technology Strategy Presentation (2024) - NVIDIA Partnership Announcement (March 2025)

Industry Analysis & Research: - Morgan Stanley: "Yum China Spin-Off Analysis" (November 2016) - Morningstar: "Wide Moat Rating Justification" (2024) - QSR Magazine Industry Reports

Historical Documentation: - PepsiCo Spin-Off Announcement (January 1997) - Tricon to Yum! Rebrand Documentation (2002) - China Spin-Off SEC Filings (2016)

Books on Franchise Business Models: - "The Education of an Accidental CEO" by David Novak - "Franchise Your Business" by Mark Siebert - "The Franchise MBA" by Nick Neonakis

QSR Industry Publications: - Nation's Restaurant News (nrn.com) - Restaurant Business Magazine (restaurantbusinessonline.com) - QSR Magazine (qsrmagazine.com)

Technology Platform Case Studies: - Byte by Yum! Platform Overview - Dragontail Systems Acquisition Analysis - NVIDIA AI Partnership Technical Documentation

China Market Analysis: - Yum China Investor Relations: ir.yumchina.com - China Restaurant Association Reports - McKinsey China Consumer Reports

Franchise Economics Deep Dives: - Franchise Disclosure Documents (FDD) for KFC, Pizza Hut, Taco Bell - Franchise Times Top 500 Rankings - FRANdata Industry Reports

The Yum! Brands story continues to evolve, shaped by technology disruption, changing consumer preferences, and global economic forces. From its origins as PepsiCo's unwanted restaurant division to becoming the world's largest restaurant company by unit count, Yum! has demonstrated remarkable resilience and adaptability. The next chapter, under Chris Turner's leadership, will determine whether the company can transform from restaurant operator to technology platform—a transition that could redefine not just Yum!, but the entire quick-service restaurant industry.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube