Yatsen Holding: The "Data-First" Beauty Empire

I. Introduction: The L'Oréal of the Digital Age?

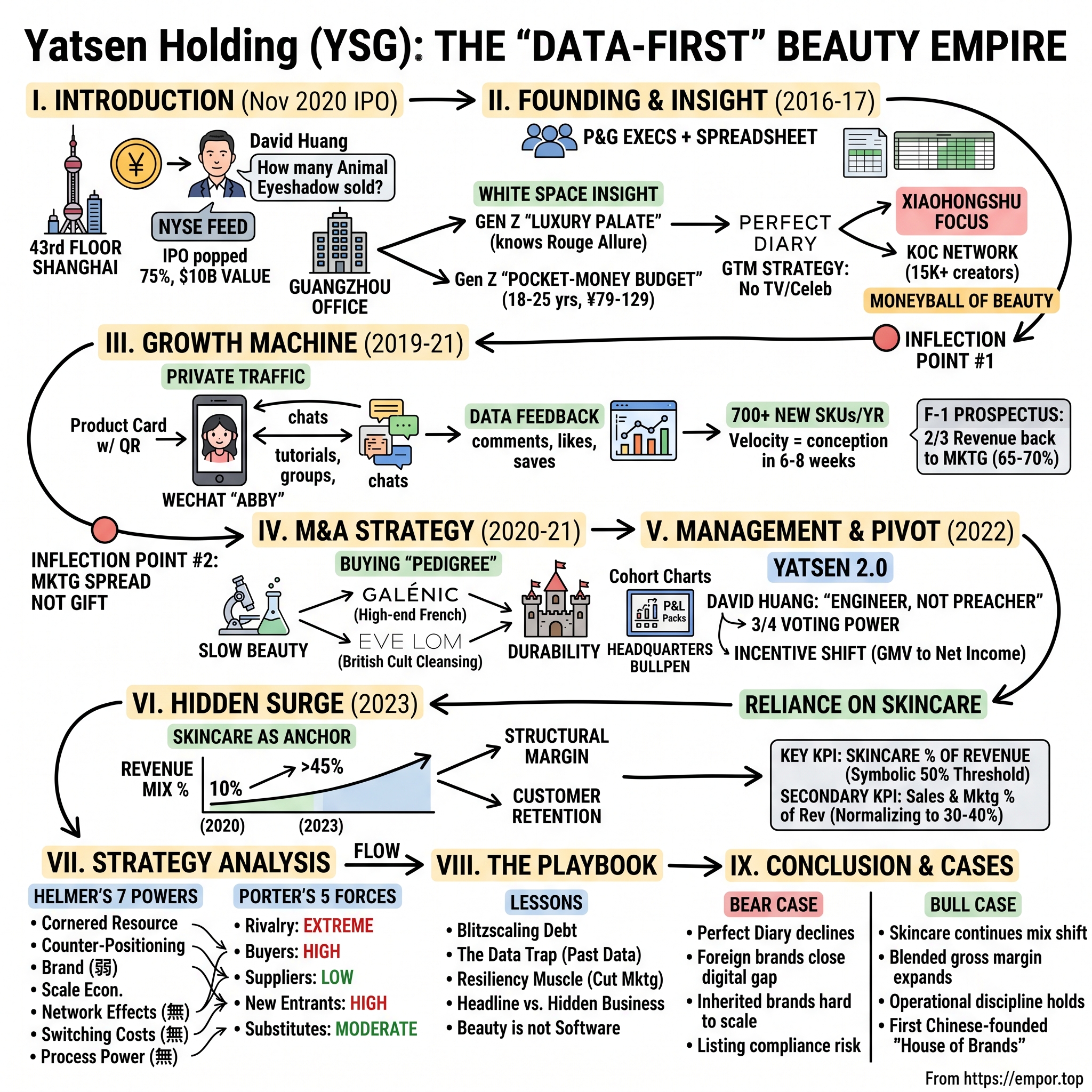

It was a Wednesday evening in Shanghai, November 19, 2020. On the 43rd floor of a glass tower in Jing'an, a 37-year-old man with the unremarkable demeanor of a mid-level accountant stared at a live feed from the New York Stock Exchange. The feed was blurry, the Wi-Fi jittery, but the number in the corner was clear enough. His company—a four-year-old Chinese cosmetics startup called Yatsen—had just priced its IPO at $10.50 a share. Within hours, the stock would pop 75%, valuing the company at more than $10 billion.

Jinfeng Huang—who goes by David inside the company—did not crack a smile. According to colleagues present that night, he asked a single question: "How many bottles of Perfect Diary Animal Eyeshadow did we sell during the livestream?" The answer came back in seconds. This was a company where every decision, every celebration, every sigh of relief was mediated by a dashboard.

Here's the hook, and it's a strange one. Three former Procter & Gamble executives, armed with a spreadsheet and a WeChat account, had just built a multi-billion-dollar beauty conglomerate in under four years. They had gone toe-to-toe with L'Oréal and Estée Lauder on Chinese soil and, for a fleeting moment, appeared to be winning. And then, over the next 36 months, they would watch that same $10 billion market cap evaporate to under $500 million. They would fire roughly a third of their staff, cut marketing spend by more than half, and dismantle the very growth playbook that had made them famous.

This is the story of Yatsen Holding Limited, ticker YSG on the New York Stock Exchange. But more broadly, it is the story of a generational experiment in Chinese consumer capitalism. Could a "Designed in China" beauty brand, born on a livestream and raised on algorithms, actually grow up into something durable? Could you build a L'Oréal in four years if you had enough data? Or is beauty, in the end, too human—too tied to emotion, heritage, and the inexplicable chemistry between a face and a lipstick tube—to be "hacked" by engineers?

The thesis we want to pressure-test tonight is this: Is Yatsen a fast-fashion beauty company running on Instagram economics, or is it a technology company that happens to sell lipstick? Because the answer shapes everything—how you value it, who competes with it, and whether the next ten years look like a comeback or a slow fade.

The backdrop matters. China's beauty market was worth roughly $80 billion by the mid-2020s, the second largest in the world, and the fastest-growing among major economies for over a decade. Foreign conglomerates—L'Oréal, Estée Lauder, Shiseido, LVMH's beauty division—had treated the country as a gold rush since the 1990s, opening flagship counters in Shanghai's Plaza 66 and Beijing's SKP. They were the aspirational choice. Local brands, by contrast, were often cheap, chalky, and sold in second-tier city supermarkets under shrink-wrap.

Then something shifted. Call it the Guochao movement—"national tide"—a rising confidence among Chinese Gen Z consumers that their own country's brands could be cool, premium, and globally competitive. Huawei did it in phones. Li Ning did it in sneakers. Yatsen's bet, made in 2016, was that it could do the same in lipstick. The question was whether a data-first philosophy, honed on the unique rails of Chinese digital commerce, could be exported into a category where "heritage" and "mystique" had always been the moat. That tension—between the algorithm and the aesthetic—is what the next three hours are about.

II. The Founding & The "Perfect" Insight

Picture a cramped office in Guangzhou in late 2016. The paint is still fresh. There are no proper desks—just fold-out tables from a wholesale market. Three men in their early thirties are sitting around a plastic chair with a Mac laptop open to Tmall's seller dashboard. One of them is Jinfeng Huang, and he has just spent an hour arguing with a supplier about whether a particular shade of matte pink should be called "Sunset Whisper" or "Velvet Rogue." The supplier doesn't care. David cares enormously, because he has already run the search volume on both phrases in Baidu.

To understand David Huang, you have to understand P&G in China in the 2000s. That was the Harvard Business School of Chinese consumer marketing—brutal rotational programs, airtight brand management rigor, data obsession before data was cool. David came out of that machine, did a stint at China International Capital Corporation, and then took a formative detour into a company called Yunifang. Yunifang was one of China's earliest D2C skincare successes, riding the first wave of Taobao commerce with mask sheets priced for teenagers. It failed to fully capitalize on its early lead, but David saw something there that would haunt him for years: the realization that traditional retail gatekeepers—department store counters, beauty editors, TV ads—were no longer required to build a brand in China.

In 2016, David and his two co-founders, Chen Yuwen and Lv Jianhua, sat down to map what they called the "white space." At the top of the market, foreign luxury brands held the prestige position—a MAC lipstick cost around 170 yuan, a Dior lipstick over 300. At the bottom, legacy Chinese brands competed on price and distribution muscle. But in between, they saw a yawning gap: a generation of 18-to-25-year-olds who wanted the aesthetic of luxury—the photogenic packaging, the Instagram-ready texture, the complex undertones—but at a price point they could afford on a pocket-money budget. Call it 79 to 129 yuan, roughly $12 to $20.

This was the real founding insight of Perfect Diary. Not "cheap makeup." Not "copying Western trends." It was this: Gen Z consumers in China had developed a luxury palate before they had a luxury income. They had grown up watching K-drama tutorials and scrolling through Sephora hauls on Xiaohongshu. They knew what "Rouge Allure Velvet" felt like without ever having touched one. Yatsen's bet was that it could bottle that aspiration at a price that turned beauty into an impulse purchase.

Perfect Diary launched on Taobao in early 2017. The name itself was deliberate—English-sounding, aspirational, unburdened by any "Chinese-ness" that might dampen the luxe aura. The first hero product was a 16-color eyeshadow palette, and the go-to-market strategy broke every rule of the Western beauty playbook. There was no department store counter. No celebrity endorsement deal. No TV campaign. Instead, there was Xiaohongshu.

This is inflection point number one, and it is the most important thing to understand about Yatsen's early rise. Xiaohongshu—literally "Little Red Book"—is a Chinese lifestyle and commerce app that functions like Instagram and Pinterest had a baby with Amazon Reviews. By 2017, it had become the de facto beauty discovery engine for Chinese Gen Z. And Yatsen did something counterintuitive: rather than hiring a handful of big celebrities or macro-influencers, it built what became one of the largest Key Opinion Consumer networks in China. KOCs are not stars; they are ordinary users with a few thousand followers, often university students, who post earnest, unpolished reviews. Yatsen at its peak was working with more than 15,000 of them.

The logic was straight out of Michael Lewis. Call it the Moneyball of beauty. Traditional cosmetics companies believed brand was built through aspiration—a Charlize Theron staring mysteriously into a camera. Yatsen believed brand was built through distributed, authentic-feeling advocacy at massive scale, seeded across thousands of small creators whose combined reach dwarfed any single Vogue cover. The KOC model was also, critically, dramatically cheaper per impression—and it came with a feedback loop. Every comment, every like, every save on a Xiaohongshu post became training data. By early 2019, Yatsen's product development team was using that data to predict, weeks in advance, which shade of "crushed velvet" orange would trend next. They'd manufacture a pre-sale, iterate on packaging based on saves and comments, and have the finished SKU in consumers' hands within six to eight weeks of concept.

That velocity, layered on top of the aspirational-affordable positioning, is what turned Perfect Diary from a Tmall challenger brand into China's number one domestic color cosmetics brand by 2019. And it set the table for the next chapter—where the real moat was not the product line at all, but the relationship with the customer after the sale.

III. The Growth Machine: Private Traffic & The "WeChat" Moat

Let's talk about Abby. Not a person, exactly. More of a ghost in the machine.

If you bought a Perfect Diary lipstick on Tmall in 2019 and unboxed it at home in your bedroom in Chengdu, tucked inside the slick pink packaging was a little card. On the card was a QR code and a cheerful handwritten-looking note from a young woman named Xiao Wanzi—or sometimes Abby, or sometimes one of several other friendly personas. Scan the code, and you were invited to add her as a contact on WeChat. Do that, and within hours she'd start chatting with you—sending you tutorials, asking what you thought of the lipstick, inviting you into a small WeChat group of "fellow Perfect Diary lovers."

Abby was not a chatbot. Abby was a person—or rather, hundreds of people, working in shifts inside Yatsen's customer operations centers, each managing thousands of WeChat relationships and dozens of WeChat groups. This was the private traffic engine, and in the 2019-to-2021 period, it was arguably the single most defensible asset Yatsen built.

To understand why this mattered, you need to understand a peculiarity of the Chinese internet. In the West, the beauty customer relationship is mediated by Instagram, Meta ads, Shopify email lists, and Sephora's loyalty program. All of these are rented channels. In China, the equivalent channels—Tmall, Douyin, Xiaohongshu—are even more rented, and the platforms extract even heavier tolls in the form of ad spend and commission. WeChat is the one place where, once you have a consumer's private account, you can message them for free, forever. It is the closest thing in Chinese commerce to an owned channel.

Yatsen built an industrial-scale operation to harvest that channel. By late 2020, the company disclosed in its prospectus that it had accumulated relationships with tens of millions of consumers across its private traffic network. The Abby personas were the front line—warm, chatty, slightly older-sister-coded, trained to drop product tips and flash-sale links into group chats with the pacing of a well-rehearsed variety show. Western beauty executives visiting Shanghai would ask, incredulously, whether this was legal. Chinese beauty executives would ask, less incredulously, how they could copy it.

And yet, what made the private traffic moat powerful in 2020 also exposed Yatsen's deeper vulnerability. A relationship where the company has to constantly entertain its customers to keep them engaged is a relationship that requires endless novelty. So the product machine ran hot. The company pushed out more than 700 new SKUs a year at its peak, across Perfect Diary and its early sister brands. Collaborations with the Metropolitan Museum of Art, with Discovery Channel, with the Chinese National Geographic magazine produced eyeshadow palettes themed around endangered animals, Egyptian tombs, and Yunnan mountain ranges. Each launch generated a fresh content cycle; each content cycle fed the Abby groups; each Abby group generated more purchases; each purchase funded more launches. It was a flywheel that looked magnificent from the outside and felt, from the inside, like running a factory on caffeine.

By the time Yatsen filed its F-1 with the SEC in October 2020, the company had more than doubled revenue in each of the prior three years. Perfect Diary had become the number one domestic color cosmetics brand in China by market share, dethroning legacy players that had been on the shelves since the 1990s. The S-1 also showed the downside: selling and marketing expenses were running at roughly 65 to 70 percent of revenue. For every dollar that came in, two-thirds went straight back out to KOLs, KOCs, platform ads, Abby wages, and influencer seeding.

That brings us to inflection point number two. The November 2020 IPO priced Yatsen at $10.50 a share, above the indicated range, raising just over $600 million in gross proceeds. The stock opened at $18.40 and closed the first day above $18. The market was buying the flywheel. Inside Yatsen, the mood was not triumphant. In an internal memo that David Huang sent the morning after the listing—later quoted in Chinese business press—he reminded staff that "growth without margin is a loan from the future, not a gift." With that loan now on the balance sheet in the form of public shareholders and quarterly expectations, the question became: what would they buy with the proceeds? The answer, it turned out, was already sitting on their M&A shortlist, half a world away in a quiet laboratory in the French Alps.

IV. M&A Strategy: Buying "Pedigree"

In the summer of 2020, months before the IPO priced, a delegation from Yatsen flew into Lavaur, a small town northeast of Toulouse in the south of France. Lavaur is the kind of place where the pharmacy closes for lunch. It is also the historical home of Pierre Fabre, one of France's iconic family-held pharmaceutical and dermocosmetic groups. Yatsen was there to negotiate the acquisition of a brand called Galénic—a high-end French skincare line that had been sold in European pharmacies for roughly half a century.

If you were at that meeting, you would have noticed the cultural gap immediately. The Pierre Fabre team spoke in the cadence of a hundred-year-old family company—long decision cycles, reverence for the lab, skepticism of digital-native upstarts. The Yatsen team spoke in the cadence of a Chinese growth startup—conversion rates, livestream CPMs, Tmall flagship forecasts. The deal closed in September 2020 and was announced in October. Terms were not publicly disclosed in dollar amounts, but the strategic meaning was clear: Yatsen was buying its way into Europe's pharmacy-grade skincare pedigree, a segment it could not build from scratch, particularly not quickly.

The Galénic acquisition was the opening move in what became Yatsen's most important strategic pivot: the transition from a single-brand color cosmetics flywheel to a multi-brand house, with skincare as the anchor. Color cosmetics—lipstick, eyeshadow, blush—is a brutal category. It is driven by novelty, social feeds, and seasonality. Margins look great on paper, but lifetime value is shallow; a 19-year-old may buy three lipsticks in a year and then switch brands entirely. Skincare is the opposite. It is driven by routine, efficacy claims, and trust. A consumer who finds a serum that works stays for years. Gross margins are higher, inventory turns are more predictable, and the category is dramatically less correlated to short-form video trend cycles.

In March 2021, Yatsen doubled down. It announced the acquisition of Eve Lom, the British cult-classic cleansing balm brand, from Manzanita Capital for an amount widely reported in the cosmetics trade press to be in the $200 million range. Eve Lom was nearly forty years old at that point—founded by Eve Lom herself in 1985, beloved by British Vogue editors, stocked at Liberty of London, revered for its one-jar cleansing balm ritual. It was "slow beauty" in its purest form: one product, zero launches per year, a customer base that would pay full price again and again.

Let's benchmark the spend, because this is where the analysis gets interesting. Beauty industry trade press at the time estimated the Eve Lom deal at roughly four to five times trailing sales. By prevailing multiples in the sector, that was—given Eve Lom's heritage and brand equity—a fair but not bargain-bin price. Compare it to L'Oréal's acquisition of Aesop, which closed in 2023 for $2.5 billion, a reported multiple closer to twenty times EBITDA on a far larger, faster-growing brand. Or Estée Lauder's acquisition of DECIEM, parent of The Ordinary, completed in 2024 at a $2.2 billion valuation implying a double-digit multiple of sales. On those comps, Yatsen's purchases of Galénic and Eve Lom looked like disciplined value-hunting. They were buying "heritage" at multiples that, had they been paid by a Western strategic, would have been considered restrained.

But here is the trap Yatsen walked into. Buying a slow-beauty brand at a reasonable multiple only works if you can grow it. And the operational challenge was enormous. European prestige brands are architected around a completely different cadence than Chinese fast beauty. Eve Lom's entire product range at acquisition was tiny. Galénic had complex regulatory and ingredient dossiers designed for French pharmacy channels, not Tmall livestreams. You cannot simply plug these brands into the Perfect Diary flywheel—dump them on Xiaohongshu, flood Abby's WeChat groups with flash sales—without actively destroying the thing that made them valuable to acquire in the first place.

Over 2022 and 2023, Yatsen wrestled publicly and privately with how to scale these European brands in China without cheapening them. Galénic was re-launched with a hero product called Le Sérum in China, backed by significant marketing investment in higher-end channels. Eve Lom was carefully introduced to the Tmall Luxury Pavilion rather than to mass-market Taobao. Both brands grew, but slowly—and they did so while the legacy Perfect Diary business was contracting, creating a squeeze in the middle. The company also added DR.WU, a Taiwanese clinical skincare brand with a loyal following around mandelic acid formulations, via commercial arrangements in Mainland China. Combined with domestic skincare brands including Little Ondine and Pink Bear, the Yatsen portfolio by 2023 looked nothing like the single-brand juggernaut that had gone public in late 2020.

The M&A chapter, in short, was not the expansion story it first appeared to be. It was a defensive pivot disguised as offense—a recognition that the original "data-first" thesis, applied to color cosmetics alone, could not build a durable company on its own. Whether Yatsen had bought the right brands at the right price, and whether it could actually operate them, would be tested over the two years that followed, as the company's share price fell and its founder's grip on the organization came under the sharpest scrutiny of his career.

V. Management, Incentives & The "Yatsen 2.0" Pivot

To walk into Yatsen's Guangzhou headquarters in 2022 was to walk into a company in the middle of a quiet revolution. The open-plan floors that had once hummed with the adrenaline of daily livestream production now felt more like a consulting firm bullpen—analysts clustered around cohort charts, product managers presenting P&L packs, and whiteboards covered in customer retention curves rather than launch calendars. The change had a name inside the company: "Yatsen 2.0." And it was being driven, with some personal pain, from the office of the founder.

David Huang sits at the center of this story, and it is worth understanding what kind of leader he actually is. Those who have worked with him describe him as relentlessly analytical, slightly shy in front of cameras, and deeply uncomfortable with the persona of the Chinese "founder-celebrity"—the Jack Ma-style visionary with the keynote stage and the quotable one-liners. David gives few interviews. The ones he does give are careful, technical, more likely to discuss customer acquisition cost by channel than to offer a sweeping vision for Chinese consumerism. His own description of his management philosophy, offered in a rare 2021 Chinese business magazine interview, was "engineer, not preacher." He prefers dashboards to speeches.

The shareholding structure reflects this founder-centric grip. David Huang holds approximately a quarter of Yatsen's economic equity, but through a dual-class share structure common to U.S.-listed Chinese companies, he controls roughly three-quarters of the voting power. That means when Yatsen 2.0 was designed—when the company was told to stop chasing GMV and start protecting margin—there was no meaningful public-market resistance that could have stopped him. This is a company where the founder can run a multi-year marathon at the expense of quarterly sprints, because no institutional shareholder has the votes to make him sprint.

The incentive restructuring, begun in late 2021 and accelerated through 2022, was the hinge of Yatsen 2.0. Historically, internal bonuses and team KPIs had been tied overwhelmingly to Gross Merchandise Value—the dollar volume of product sold through a channel. This was the standard metric in Chinese D2C, because it aligned with platform rankings on Tmall and Douyin and made for clean comparisons to competitors. But GMV KPIs have an ugly side effect: they reward growth regardless of profitability. A product manager could hit their number by buying traffic, discounting aggressively, and gifting product to influencers—and walk away with a bonus check even if the unit economics were underwater.

Under Yatsen 2.0, the company rewrote those incentive contracts. Product manager bonuses shifted toward net income contribution, channel gross margin, and skincare segment growth. Marketing teams were measured on payback period rather than raw reach. Brand managers were forced to present quarterly P&Ls that looked more like a traditional conglomerate's divisional statements than a growth startup's cohort dashboard. Several senior executives, particularly on the Perfect Diary side, departed. Others adapted. The cultural shift was wrenching. One mid-level manager, quoted anonymously in a Chinese industry publication in 2022, described the mood as "going from running a music festival to running a hospital."

The culture David preserved through this transition is what he privately called "data-driven ownership." Yatsen has historically structured its organization so that every product line—every hero SKU, every sub-brand—has an internal owner who functions almost like a mini-CEO. They own the P&L. They own the launch calendar. They own the customer acquisition cost math. They are held accountable in a way that would be genuinely unusual at a legacy cosmetics company, where product decisions are typically spread across brand marketing, R&D, and regional commercial teams. The tradeoff is real: this structure breeds entrepreneurial energy, but it can also lead to brand-level cannibalization and, in a downturn, to internal score-settling. Yatsen 2.0 attempted to preserve the entrepreneurial ownership model while layering in grown-up margin discipline—a balancing act that is still being tested.

What this pivot really revealed about David Huang is that he was willing to burn down his own legend to save the company. The blistering growth playbook that had made Perfect Diary a case study was, in Yatsen 2.0, treated explicitly as a problem to be unwound. Marketing spend as a percentage of revenue began a multi-year descent. Product launches were cut dramatically. Private traffic operations, the fabled Abby network, were consolidated and automated. These were not moves a growth-mode founder makes easily. They are the moves a founder makes when he believes the company has enough years left in it to earn back credibility, provided it survives the next eight quarters.

And survival, by 2023, was the explicit goal. The once-mighty $10 billion market cap had fallen to under $1 billion. Delisting rumors floated. Analyst coverage thinned. Against that backdrop, the one part of the business that was quietly working—skincare—was becoming disproportionately important to the entire thesis.

VI. The Hidden Business: The Skincare Surge

If you had looked only at Yatsen's share price chart during 2022 and 2023, you would have assumed the company was dying. If you had looked only at the financial statements, you would have noticed something much stranger: a company in the middle of a quiet internal transformation, with one half shrinking and the other half compounding. The public narrative was about Perfect Diary's decline. The actual financial story was about skincare's rise.

Set the scene. In the financial year ending December 2020, color cosmetics—led by Perfect Diary—represented the overwhelming majority of Yatsen's revenue. Skincare, in its infancy as a segment, accounted for roughly a tenth of the top line. Fast forward to the financial year ending December 2023, and the ratio had shifted dramatically. Skincare had grown to account for more than forty-five percent of total net revenues, approaching parity with color cosmetics. By certain quarterly slices, skincare had already crossed the fifty percent threshold. This was not a rounding-error shift. This was the re-engineering of a company from the inside.

What drove it? Part of it was portfolio expansion—the Galénic and Eve Lom acquisitions, combined with the DR.WU partnership, supplied a ready-made skincare roster. But the more interesting driver was what happened when Yatsen applied its data-and-content engine to those acquired brands. Take DR.WU as the cleanest case study. DR.WU was a clinical-positioning Taiwanese brand known for its mandelic acid serums—a chemical exfoliant popular in Asia for managing acne and pigmentation. Outside its home market, DR.WU had been a mid-size, steady-state business. Yatsen brought it into Mainland China through commercial arrangements, repositioned the hero mandelic acid SKUs on Xiaohongshu through long-form efficacy-driven content (rather than fast-fashion lookbooks), ran targeted campaigns in Abby's private traffic groups, and layered in livestream commerce with dermatology-adjacent creators.

The result: DR.WU's mandelic acid serum became a top-selling product in its segment on Tmall. This was, in microcosm, Yatsen's bet. Take a foreign brand with genuine clinical credibility, plug it into China's unique commerce rails, and let the data-operations muscle do the rest. It worked not because Yatsen was better at chemistry than Pierre Fabre, but because Yatsen was better at translating clinical credibility into Chinese-language content at commercial scale.

Now, the margin story. This is where the "hidden" transition gets financially interesting. Color cosmetics—lipstick, eyeshadow, blush—typically carries gross margins in the high fifties to low sixties percent range. That sounds healthy, but in Yatsen's case it is offset by brutal marketing costs. Skincare, particularly prestige or clinical-positioning skincare, carries gross margins in the seventy percent-plus range. Even after marketing costs, the contribution margin on a Galénic serum or an Eve Lom cleansing balm is structurally superior to that of a Perfect Diary eyeshadow. Said simply: as skincare's share of revenue climbs, the blended gross margin of the entire company climbs with it. Yatsen's reported gross margin has expanded materially from its 2020-era levels, and the driver is the mix shift, not pricing power on the legacy business.

There is also a durability argument. Skincare customers are retained. They finish a bottle of serum and they reorder. They stack products into routines. They forgive a missed trend because they trust the formulation. This is the exact opposite of the Perfect Diary customer dynamic, where a shade that trends one quarter becomes cringe the next. If you believe Yatsen's long-run value depends on customer retention—and for a consumer company, you almost always should—then the skincare shift is the story. The Perfect Diary business is the past. The skincare business is the future. And the mathematics of the transition are doing more to determine Yatsen's fate than any single product launch could.

The risk, of course, is that this math is still in motion, and that the middle of the transition is the ugliest part. Yatsen is, in 2026, a company where the loudest, most visible brand is shrinking, where the growing brands are less familiar to the average Chinese consumer, and where the corporate overhead is still calibrated to the scale of its IPO-era self. Whether skincare grows fast enough to cover that overhead, without needing another equity raise, is the operational question that separates the bull case from the bear case. And it is the question that the Strategy Analysis section of this episode will attempt to answer.

VII. Strategy Analysis: The 7 Powers & 5 Forces

Let's put Yatsen under Hamilton Helmer's 7 Powers framework, because it is genuinely the sharpest tool for assessing whether a company's advantages will survive contact with competitive reality. Helmer defines a "power" as a condition that creates the potential for persistent differential returns. Most companies don't have one. A few have two. Great companies stack them.

Start with Cornered Resource. This is the one where Yatsen has a legitimate, underappreciated asset: its proprietary database of tens of millions of private-traffic WeChat consumers. No Chinese beauty brand of comparable size has replicated the depth of Yatsen's one-to-one messaging relationships. No Western brand can come close—they are structurally locked out of WeChat at that intimacy of access. In theory, this is a cornered resource. In practice, it has a half-life. WeChat has tightened its policies on commercial messaging repeatedly. Consumer fatigue with Abby-style engagement has set in; open rates and conversion rates in private traffic groups have declined across the industry since 2021. The database is an asset, but it is a depreciating one unless continuously refreshed—which itself costs money.

Counter-Positioning. This is where Yatsen earned its initial lift. In 2017 through 2019, Perfect Diary counter-positioned against L'Oréal and Estée Lauder in a way those incumbents literally could not respond to without damaging their own economics. L'Oréal could not suddenly go "digital-only" because its counter-staff network in department stores was both a revenue engine and a fixed-cost anchor. It could not cut prices to Perfect Diary levels without cheapening its own brand. It could not flood Xiaohongshu with 15,000 KOCs without burning its own Vogue-driven brand equity. Counter-positioning is a temporary power, though. Once the incumbent figures out how to respond without cannibalizing itself—by launching masstige sub-brands, buying into KOC networks, opening Tmall flagship stores—the advantage compresses. By 2023, L'Oréal's and Estée Lauder's Chinese digital operations had substantially closed that gap.

Brand. This is Yatsen's weakness, and it is worth dwelling on. Perfect Diary has high awareness. Almost every Chinese Gen Z consumer could name the brand by 2020. But awareness is not power. What matters is whether the consumer pays a premium for the brand, or would be distressed if it disappeared. Perfect Diary, at its core, competes on product-for-product value at a specific price tier. That is a fashion brand position, not a beauty brand position. The entire M&A strategy around Galénic and Eve Lom was, in Helmer's framework, an attempt to purchase Brand Power that could not be organically built at speed.

Scale Economies and Network Effects. Yatsen has modest scale economies in manufacturing—it can source from top-tier Korean, Japanese, and Chinese OEMs like Cosmax and Kolmar at volumes that give it cost parity with larger players. It does not have true network effects in the classic sense; each consumer's value does not increase with the addition of more consumers. The Abby network is closer to a scale advantage in operations than a network effect.

Switching Costs and Process Power. Largely absent. A Perfect Diary consumer can switch to Florasis, Colorkey, or a resurgent legacy brand with essentially zero friction. And Process Power—the kind of deeply embedded operational excellence Toyota has—is hard to claim for a company that has publicly rewired its own KPIs twice in four years.

So Yatsen's realistic power stack is this: a weakening Cornered Resource in private traffic, a compressing Counter-Positioning against incumbents, and a purchased Brand Power that is still being integrated. That is not nothing. But it is also not the durable moat of a true L'Oréal-in-the-making.

Now Porter's 5 Forces. Rivalry in Chinese beauty is extreme. The "lipstick wars" of Tmall—where dozens of domestic and foreign brands competed on shade drops, livestream pricing, and Singles' Day discounts—are structurally brutal. New entrants appear weekly. Li Jiaqi, the livestream phenomenon once nicknamed the "lipstick brother," can sell out a small brand's annual inventory in a single 90-second segment—and turn on a different brand the next week.

Bargaining power of buyers is high. Gen Z is a fickle master. Discovery happens on platforms (Xiaohongshu, Douyin) that the buyer owns, not the brand. Switching costs are zero. Price transparency is total.

Bargaining power of suppliers is low. China has built the world's most competitive cosmetics OEM ecosystem, with Korea's Cosmax and Kolmar running Chinese facilities alongside dozens of domestic contract manufacturers. A brand can commission a formulation and have it in-market in weeks. This is good for Yatsen on cost; it is bad for Yatsen on differentiation, because every competitor has access to the same supply chain.

Threat of substitutes is moderate. Consumers can substitute with other cosmetics, with skincare that doubles as "no makeup makeup," or with spending those yuan on travel and experiences.

Threat of new entrants is high—possibly the highest of any major consumer category in China. A well-capitalized founder with a Xiaohongshu strategy can stand up a color cosmetics brand in six months.

Put the Helmer and Porter lenses together, and the strategic picture is clear: Yatsen operates in the single most hostile consumer environment in global beauty, with meaningful but eroding advantages, and is deploying capital to buy its way into structurally defensible categories before the old moat runs dry. Whether that race finishes in time is the question every long-term investor needs to sit with.

VIII. The Playbook: Lessons for Investors & Founders

Step back from the company for a moment and consider what Yatsen's arc teaches. Because whatever happens to the share price over the next few years, this is already one of the more instructive case studies in modern consumer capitalism, and the lessons generalize far beyond beauty.

Lesson one: the blitzscaling debt. Venture capital and public markets can, for a while, fund any level of customer acquisition cost. If you are willing to spend two dollars to acquire a dollar of revenue, and investors are willing to underwrite that spend in exchange for growth, you can manufacture a flywheel that looks indistinguishable from genuine product-market love. Yatsen, in its 2018 to 2021 run, was a pure example of this. Marketing at roughly seventy percent of revenue was not a bug in the early business; it was the feature. The bet was that scale and category leadership would eventually create pricing power, customer stickiness, and margin expansion. That bet did not pay off on the original timeline. The lesson is not that blitzscaling never works—it worked for Meituan, for Pinduoduo, for Shein—but that it only works if the category has native retention dynamics. Color cosmetics does not. Social commerce does. The match between growth playbook and category economics is everything.

Lesson two: the data trap. This one is subtle, and it applies to any company that prides itself on being "data-driven." Data tells you what people bought yesterday. It tells you which shade of orange trended last week. What data cannot tell you is what people will feel about a brand in five years. It cannot tell you whether they will still want to be seen with your product when they are older, wealthier, and less interested in signaling youth. It cannot predict generational shifts in taste. Yatsen's entire 2018-to-2020 rise was driven by a cohort that was, at the time, 18 to 25 years old. By 2026, that cohort is 24 to 31 years old, with different budgets, different aesthetics, and different shopping platforms. Data alone does not handle that transition. Brand does. And brand is the thing that was under-invested in during the growth years.

Lesson three: the resiliency muscle. Here is where Yatsen has quietly earned a real badge. The ability to cut marketing spend from the seventy-percent-of-revenue range down toward the thirty-percent-of-revenue range over a handful of years, while maintaining operational continuity and brand investment in skincare, is genuinely difficult. Most growth-mode companies do not have this muscle. They have a team architected around scaling channels, a product organization architected around constant launches, and an incentive structure that rewards top-line momentum. Rewiring all three, simultaneously, while the public markets are punishing the stock, is a test many CEOs fail. David Huang has not failed it yet. Whether the company has enough runway to let the newly disciplined operating model compound is a different question, but the operating transformation itself is the playbook other Chinese consumer companies should study closely when the next growth-to-profitability crunch arrives.

Lesson four, which is the investor-specific corollary of the three above: distinguish between the headline business and the hidden business. For at least two years, Yatsen's public narrative was entirely about Perfect Diary's decline, which was real. Meanwhile, skincare was quietly going from less than ten percent of revenue to nearly half. Investors who read only the headlines missed the transition. Investors who read the segment disclosures saw it clearly. In any company going through a strategic pivot, the segment line items are almost always more informative than the topline, and the mix shift is almost always more consequential than the absolute growth rate. This is not a unique lesson, but Yatsen is an unusually clean example of it playing out in public.

Lesson five, and the one that connects back to the opening thesis: beauty is not software. Software companies can be built on data alone, because the product is the data. Beauty products are not. A serum is a chemical, packaged in glass, sold against an emotional promise. You can use data to optimize every step of that chain—formulation, packaging, targeting, pricing—but you cannot replace the chain's center with data. At the center, there is still the question of whether a young woman in Hangzhou feels that a particular eyeshadow, applied one evening before a dinner with friends, makes her feel the way she wants to feel. No dashboard tells you that. Any company, in any category, that operates in the space between data and emotion has to eventually decide which one is the master. Yatsen's first five years treated data as the master. The next five will test whether emotion can be re-centered without losing the operational edge that data discipline brought.

IX. Conclusion & Bull/Bear Case

The bear case, if you are inclined toward it, goes roughly like this. Perfect Diary is a declining asset. Its core 18-to-25-year-old cohort has aged up, and the brand has not re-earned its relevance with the next cohort. Domestic competitors, particularly Florasis and Colorkey, have matched Yatsen on digital-native execution and may have done so while building deeper brand equity. Foreign incumbents—L'Oréal, Estée Lauder, Shiseido—have closed the digital-operations gap. The acquired European brands, Galénic and Eve Lom, are high-quality assets but are structurally difficult to scale in China without violating the slow-beauty aesthetics that made them valuable in the first place. Corporate overhead associated with being a NYSE-listed multi-brand group is not small, and the company has had to operate with reduced analyst coverage and depressed equity currency for three years. A delisting-and-privatization outcome, either voluntary by the founder or driven by listing-compliance pressure, cannot be ruled out. On the Helmer framework, the durable power stack is thin. On the Porter framework, the industry conditions are nearly as hostile as they get. That is the bear case in one paragraph.

The bull case runs through the skincare mix shift. If skincare continues the trajectory it has been on—climbing from roughly ten percent of revenue in 2020 toward and past fifty percent in the years ahead—the company's economics begin to look qualitatively different. Blended gross margin expands. Customer retention lengthens. Marketing intensity falls naturally, because skincare consumers don't need to be re-seduced every season. At the same time, Yatsen retains what a traditional conglomerate envies: a deep operational bench in Chinese digital commerce, a cornered resource in private-traffic relationships even as it depreciates, and a founder with three-quarters of the voting rights who is willing to make multi-year decisions against short-term pressure. If Galénic and Eve Lom scale another two to three times from their current Chinese revenue base, and if DR.WU-style partnerships continue to produce category leaders, Yatsen arrives in the late 2020s as a genuinely unusual entity: the first Chinese-founded "house of brands" in beauty operating at global scale, with the data muscle to keep running the playbook L'Oréal cannot. That is not a mass-market lottery ticket; it is a plausible, well-defined scenario that requires specific operational execution over several years.

Sitting between the two cases is the practical question of which single metric best tracks which scenario is unfolding. For Yatsen, the signal-to-noise-rich KPI is skincare revenue as a percentage of total net revenues. There is a fair argument that the moment this ratio durably crosses fifty percent—and stays there, not flickering across it due to seasonal color-cosmetics swings—Yatsen has effectively completed its transformation from a D2C color cosmetics company into a diversified Chinese beauty conglomerate with skincare as its anchor. Below that threshold, the legacy business still dominates the financial complexion of the company. Above it, skincare sets the margin profile and the retention profile of the whole enterprise.

A secondary KPI worth watching is sales and marketing expense as a percentage of revenue. The company's public commentary has repeatedly emphasized operational discipline, and this ratio is the cleanest single indicator of whether that discipline is holding. In the growth era, this ratio sat at roughly the two-thirds-of-revenue level. By 2024 and into 2025, it had compressed meaningfully. If it continues to normalize toward the industry average for multi-brand beauty companies—roughly the thirty-to-forty-percent range—Yatsen's ability to generate durable net income becomes a real question rather than an aspirational one.

A few second-layer diligence items deserve acknowledgment. Like all U.S.-listed Chinese companies, Yatsen operates under the persistent overhang of audit-inspection and listing-compliance regimes governed by the Public Company Accounting Oversight Board and the Holding Foreign Companies Accountable Act framework. The two governments reached a broad agreement in 2022 that substantially reduced the delisting tail risk for compliant Chinese issuers, but the regulatory regime remains sensitive to geopolitical winds. Separately, cross-border data-handling requirements associated with Yatsen's private-traffic database and cosmetic-use information fall under China's Personal Information Protection Law and evolving generative AI and cross-border data regulations—material compliance work that does not show up in topline commentary but is real operational burden. These are not presented as bear-case clinchers; they are the ambient regulatory gravity that any investor in a U.S.-listed Chinese consumer name should carry on the second page of their mental model.

Is Yatsen the next L'Oréal? That framing, which Chinese business press loved in 2020, always flattered both parties too much. L'Oréal is a 120-year-old balance sheet of patents, counters, and brand equity built across multiple continents and multiple depressions. Yatsen is a ten-year-old company that, over its first five years, demonstrated an unusual ability to build a brand from zero on Chinese digital rails, and over its next five years has had to demonstrate a much less glamorous set of skills—margin discipline, portfolio integration, leadership continuity through a downturn. Whether it is a spark that burned too bright or a more durable enterprise that happens to be in its awkward teenage years is exactly the kind of question the 2026-to-2028 window will answer. The tools to watch that question unfold are the two KPIs above and the segment-level disclosures; the story to watch is whether a company founded as a data experiment can rediscover the human center of its category without losing the engineering edge that got it here.

X. Epilogue & Reading List

For listeners who want to go deeper, a handful of references are worth pulling up alongside this episode. A valuable frame is the broader report literature on "the third wave of Chinese consumer brands," covering the shift from copy-cat beginnings to Guochao-era domestic pride and into today's more operationally rigorous house-of-brands attempts; these reports by leading Chinese management consultancies map how Yatsen's playbook fits into a larger generational pattern. For a narrower lens, various business school case studies on D2C beauty in China, developed in the 2020-to-2023 window, capture the KOC and private-traffic mechanics in granular detail and are useful for understanding why the Abby architecture was as hard to replicate as it was. Yatsen's own annual reports and investor presentations—available through the company's investor relations site and through the SEC EDGAR system under the ticker YSG—remain the most authoritative source for segment-level revenue and margin data.

The key metric to watch, as discussed, is skincare revenue as a percentage of total net revenues, with the working hypothesis that fifty percent is the symbolic and operational threshold. The secondary lens is marketing intensity. And the narrative lens, which no KPI can fully capture, is whether Yatsen's acquired European brands begin to generate their own cultural gravity in China—whether a Chinese consumer in 2028 reaches for a Galénic serum because of what it is, not because of who owns it. That is the kind of quiet transformation that beauty analysts will only notice in hindsight, and it is the kind of transformation on which the house-of-brands thesis ultimately rests.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube