Yext: The Search for Search – Location, Knowledge, and the AI Pivot

I. Introduction & Episode Roadmap

It is a strange fate for a technology company to become a household utility in the business world yet remain virtually unknown to the general public. If you have ever looked up a store’s hours on Google Maps, checked a restaurant’s menu on Facebook, or asked Siri where the nearest FedEx drop box is, you have likely interacted with Yext. But for over a decade, Yext (YEXT) existed in the shadows of the digital economy, a silent plumber fixing the leaking pipes of local business data across the internet.

Today, we are looking at one of the most fascinating corporate sagas of the SaaS era. This is the story of a company that started as a local listings management tool, rode the wave of the mobile search explosion, went public with a valuation over $1 billion, faced near-extinction at the hands of Google, and eventually pivoted entirely to become an AI-powered answers platform. It is a journey that takes us from the chaotic streets of pre-smartphone New York to the cutting-edge battlefields of generative AI.

The central question of this episode is simple yet profound: How does a startup survive and thrive when the world’s largest company, Google, decides that your core product feature should be free? Yext’s answer was a painful, high-stakes transformation that saw them abandon their public market independence to go private again, betting the entire farm on the future of enterprise search.

In this deep dive, we will explore the mechanics of "Digital Knowledge Management," a sleepy category that suddenly became the frontline of the AI wars. We will dissect the strategic inflection points that defined CEO Howard Lerman’s tenure, analyze the unit economics of going private, and evaluate whether Yext can actually become the "Snowflake of Knowledge" or if they are merely a middleware feature waiting to be commoditized. We are talking about enterprise pivots, the shadow of the tech giants, and the long, arduous road of trying to build a moat in someone else’s ecosystem.

So, buckle up. We are about to decode the hidden layer of the internet that makes the digital world actually work.

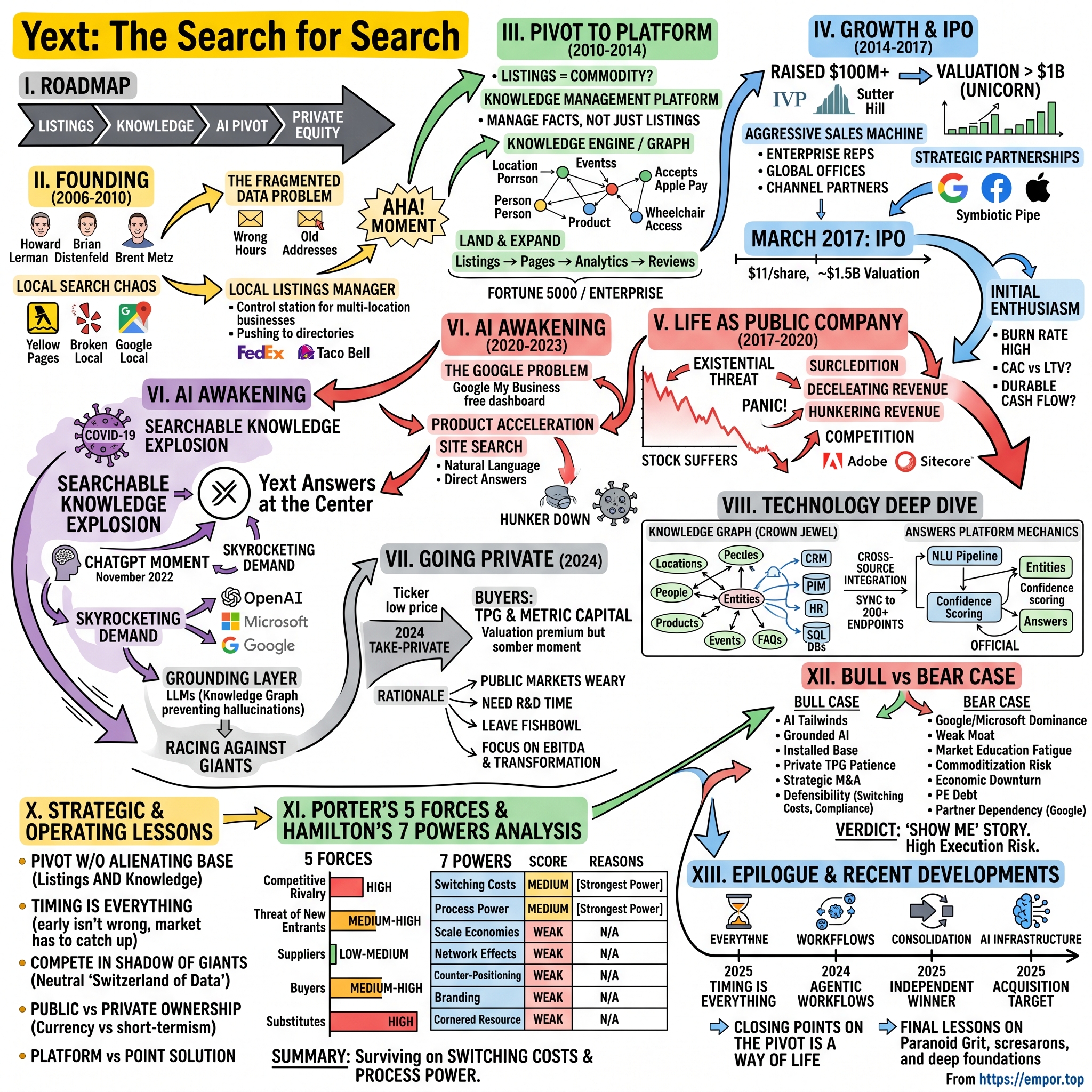

II. Founding Story & The Local Search Problem (2006–2010)

The year was 2006, and the internet was undergoing a tectonic shift that few fully understood. The iPhone was not yet on the market, but the mobile web was looming. In a small office in New York City, a serial entrepreneur named Howard Lerman was wrestling with a problem that was as mundane as it was massive. Lerman had previously worked at a company called KGB—you might remember them as the "542-542" text-message answer service. It was a human-powered search engine, and it was there that Lerman met co-founders Brian Distenfeld and Brent Metz. They saw the future, but they also saw the cracks forming in its foundation.

The "aha" moment did not come from a boardroom strategy session; it came from the sheer chaos of local data. At the time, the Yellow Pages were dying a slow, painful death, and Google Local was just emerging as a chaotic, user-generated mess. For a multi-location business like a FedEx or a Taco Bell, maintaining accurate information online was a nightmare. A store might change its hours, but that update might live on Yelp, be wrong on CitySearch, and missing entirely on MapQuest. The data was fragmented, inconsistent, and often flat-out wrong.

Lerman realized that businesses did not just want to advertise; they wanted control. They wanted to be the "source of truth" for their own facts. This was the genesis of Yext’s first product, a platform that acted as a master control station for local listings. If you updated your phone number in the Yext dashboard, it would push that update to dozens of directories instantly. It was digital plumbing, but it was plumbing that leaking badly.

In the early days, the problem was acute. Consumers were starting to use their phones to find coffee, tires, and doctors, and nothing was more frustrating than driving to a location that was closed or had moved. Yext positioned itself as the savior of the local merchant. They built direct API integrations into the ecosystems of the emerging map and directory players. While Google was the elephant in the room, there was still a long tail of publishers—Yahoo, Bing, Yelp, Foursquare—where businesses needed to be present. The network effects here were subtle but real; the more publishers Yext connected to, the more valuable the Yext dashboard became to a business owner. They were building the pipes, and in the early days of the local web, owning the pipes meant you owned the leverage.

III. The Pivot to Platform: Knowledge Management as a Category (2010–2014)

By 2010, Yext had established a solid business managing listings, but Lerman was restless. He realized that while listings were a great wedge into the market, they were ultimately a commodity. If you just managed a phone number and an address, you were easily replaceable. The strategic inflection point came when Lerman started viewing the business through the lens of structured data. He began to ask: What if we didn't just manage the listing, but we managed the "facts" about the business? What if we became "PowerPoint for facts"?

This was the birth of the Knowledge Engine concept. Yext began a massive rebranding effort, pivoting from a local listings vendor to a "Knowledge Management" platform. The vision was audacious: create a database of entities—locations, people, products, events—and the relationships between them. This was a Knowledge Graph before "Knowledge Graph" became a buzzword synonymous with Google. The goal was to allow a Fortune 500 company to manage thousands of locations with the granularity of a database, pushing structured data like "accepts Apple Pay" or "has wheelchair access" across the web.

This pivot required a fundamental shift in go-to-market strategy. The self-serve SMB (Small and Medium Business) model was chaotic and low-revenue. The real money was in the Enterprise. Yext set its sights on the "Fortune 5000"—companies with hundreds or thousands of locations that were suffering from internal CMS chaos. Landing Marriott, Taco Bell, and FedEx became the priority. These companies didn't just have wrong addresses on Yelp; they had inconsistent data in their own internal systems.

The "land-and-expand" playbook was executed with precision. Yext would land a contract to fix the listings, a clear pain point that was easy to quantify. Once they were in the door, they would expand into "Pages"—Yext hosted landing pages for every location to boost SEO—and then into Analytics and Reviews. They were becoming the operating system for the physical footprint of the digital world. Crucially, this pivot moved Yext out of direct competition with the directory aggregators and turned them into a platform play. They were no longer just a vendor; they were the infrastructure layer for the enterprise's public identity.

IV. Growth, Funding, and the Road to IPO (2014–2017)

The years between 2014 and 2017 were the "golden age" of Yext’s growth. Having successfully pivoted to the enterprise, the company kicked off a massive funding blitz. They raised over $100 million from marquee investors like Sutter Hill Ventures and Institutional Venture Partners (IVP). The valuation climbed steadily into unicorn territory, breaching the $1 billion mark and validating the "Knowledge Engine" thesis in the eyes of Silicon Valley.

With fresh capital, Yext built a formidable sales machine. They hired aggressive enterprise reps, opened offices around the globe, and cultivated a channel partner strategy that saw digital marketing agencies reselling Yext as a critical part of their service stacks. It was a land grab mentality. The strategy was to sign every multi-location brand before a competitor could emerge. They expanded the product suite aggressively, adding modules for social media management, reputation management, and deep analytics that showed businesses how customers were interacting with their data across the web.

Strategic partnerships were the fuel for this growth. Yext inked landmark deals with Google, Facebook, and Apple. In a clever move, they turned their potential enemies into partners by becoming the fastest, most reliable pipe for data into these ecosystems. Google didn't want to build a sales team to call every pizza shop in America; they preferred Yext to do it for them. This symbiotic relationship allowed Yext to scale rapidly.

In March 2017, Yext filed for an IPO. They priced at $11 per share, giving the company a valuation of roughly $1.5 billion. The public markets initially greeted them with enthusiasm. Here was a high-growth SaaS company solving a tangible problem in the burgeoning mobile economy. However, the scrutiny began almost immediately. Investors started digging into the unit economics. The growth was impressive, but the burn rate was high. The cost of acquiring enterprise customers was significant, and while the "land" was easy, the "expand" was not guaranteed. The classic SaaS debate was on: Was Yext building a durable cash-flow machine, or just burning cash to buy revenue?

V. Life as a Public Company: The Search Wars & Existential Threats (2017–2020)

Once the confetti from the IPO settled, the reality of being a public company in the shadow of Google set in. The period from 2017 to 2020 was defined by an existential threat that Yext had always known was coming but had hoped to outrun: The Google Problem. In 2017, Google launched "Google My Business," a free dashboard that allowed businesses to manage their listings directly on Google. Suddenly, the core value proposition of Yext—managing your data on Google—was available for free.

Investors panicked. If Google controls the search results page, and Google gives away the management tools for free, why would a enterprise pay Yext millions of dollars? The stock began to suffer, trading well below its IPO price within a year. The narrative shifted from "high-growth winner" to "potential victim of platform risk."

Under this immense pressure, Yext’s product evolution accelerated. They realized they could not compete on "listings" alone. They had to go where Google could not easily go: deep inside the enterprise’s own ecosystem. They expanded beyond listings into "Site Search" and "Knowledge-driven content." The big bet was the launch of "Yext Answers," a natural language search product for enterprise websites. The positioning shifted from "Manage your listings" to "Be the source of truth for all your knowledge."

The competitive landscape intensified. Legacy CMS players like Adobe and Sitecore started adding "digital asset management" features that encroached on Yext’s turf. Point solutions like Brandify and Rio SEO attacked the listings market from below. The market began to ask a tough question: Is Yext a vitamin or a painkiller? For a retailer with 1,000 locations, listings management was a painkiller. But for a large bank, was "Answers" a necessity?

Financially, the pressure mounted. Revenue growth slowed, decelerating from the 50% range down to the 30s. The path to profitability seemed distant. Then came the COVID-19 pandemic in early 2020. It was a body blow to Yext’s core customer base. Restaurants, retail stores, and hospitality brands—the very multi-location businesses that relied on Yext to tell the world they were open—were shutting their doors. Yext had to hunker down, doubling down on product innovation and enterprise stickiness, betting that when the world reopened, the need for digital accuracy would be greater than ever.

VI. The AI Awakening: Answers Platform & the ChatGPT Moment (2020–2023)

The pandemic years were dark, but they also set the stage for a technological renaissance at Yext. With the world shifting to remote work almost overnight, the need for searchable knowledge exploded. Employees working from home couldn't just walk over to a colleague’s desk to ask a question; they needed a digital brain for the company. Simultaneously, the e-commerce boom forced businesses to rethink their digital storefronts. Site search became mission-critical.

Yext responded by placing the "Answers" product at the very center of their strategy. They stopped being a listings company that also did search; they became an AI search company that also happened to do listings. The technology was impressive. They utilized Natural Language Processing (NLP), semantic search, and deep entity understanding to provide direct answers to user queries rather than a list of blue links. The pitch was simple: "Your company’s ChatGPT for customer questions."

Then came November 2022. The release of ChatGPT by OpenAI was a thunderclap that changed the technology industry overnight. Suddenly, everyone understood what "AI-powered answers" meant. The market that Yext had been painstakingly educating for years was validated in an instant. However, it was a double-edged sword. While the demand for AI answers skyrocketed, so did the threat profile. If OpenAI, Microsoft, and Google were offering generative AI, where did a mid-sized SaaS company like Yext fit in?

The narrative was tense. Yext argued that while foundation models like GPT-4 were brilliant at generating text, they were prone to "hallucinations"—making things up. For an enterprise like a bank or a hospital, a hallucinated answer about a loan rate or a drug dosage is unacceptable. Yext positioned itself as the "grounding" layer. Their pitch became: "Use our Knowledge Graph to ground the LLMs in your facts, ensuring enterprise-grade, hallucination-free answers."

The race was on. Could Yext become the Snowflake of enterprise knowledge, the critical data layer that every company needed? Or would Microsoft and Google simply build these capabilities into their existing enterprise suites and crush Yext like a bug? This period was defined by a frantic product update cycle, integrating with GPT models and rushing out AI features to stay relevant in a world that was moving faster than ever.

VII. Going Private: The 2024 Take-Private & What It Means

By late 2023, the public markets had grown weary of the uncertainty. Despite the AI tailwinds, Yext’s stock was languishing, trading in the single digits—a far cry from its IPO heyday. The market had no patience for a multi-year transformation story, especially one competing with the likes of Microsoft and Google. In early 2024, the news broke: Yext was being taken private.

The buyers were TPG and Metric Capital, two heavy hitters in the private equity world. The deal valued the company at a significant premium to its trading price, but it was a somber moment for early public market investors who had ridden the stock down. The rationale for the deal was clear. The public markets demanded quarterly profits and predictable growth, but Yext needed to invest heavily in R&D to complete its AI pivot. Private equity ownership offered the luxury of time—time to rebuild the platform, time to integrate M&A targets, and time to let the unit economics heal without the harsh glare of the NASDAQ ticker.

This move signaled a broader shift in the SaaS landscape. The "grow at all costs" era that defined the 2010s was officially over. Profitability, capital efficiency, and sustainable unit economics were back in vogue. For Yext, going private was an admission that the transformation was too painful to perform in a fishbowl.

Strategically, this raised new questions. Would TPG slash costs to juice EBITDA, potentially crippling the innovation engine? Or would they double down on the AI thesis, perhaps even rolling Yext up into a larger platform of enterprise software? The departure from public markets allowed for aggressive strategic bets that would have been punished by public shareholders. It allowed Yext to stop worrying about "beating the quarter" and start worrying about "beating Google."

VIII. The Product & Technology Deep Dive

To understand whether Yext can survive the AI wars, we have to look under the hood at their technology. The crown jewel of the Yext architecture is the Knowledge Graph. Unlike a traditional database which stores rows and columns, a Knowledge Graph stores entities and the relationships between them. Yext structures data into entities—Locations, People, Products, FAQs, and Events.

The power of this architecture lies in its multi-source integration capabilities. The Yext platform sits on top of a company’s existing mess of systems: CRMs like Salesforce, PIMs (Product Information Management systems), HR databases, and custom legacy SQL databases. It pulls data from these sources, normalizes it, and syncs it in real-time across 200+ endpoints. When a FedEx store changes its hours in the HR system, Yext detects the change, updates the Knowledge Graph, and pushes the new hours to Google, Apple Maps, Alexa, and the FedEx website simultaneously.

The "Answers" platform mechanics are equally sophisticated. When a user types a question into a Yext-powered search bar, the system runs a Natural Language Understanding (NLU) pipeline. It extracts entities from the query ("Do I need a passport for [Entity: Mexico]?"), checks the Knowledge Graph for the relevant facts, and ranks the potential answers based on confidence and semantic relevance. It then delivers a direct answer, not just a link.

Yext differentiates itself through its claim of "Official" answers. In a world of AI hallucinations and scraped internet data, Yext offers a verified, audit trail. For a regulated industry like finance or healthcare, this is critical. They also emphasize multi-channel consistency—the answer you get on the website should be the same answer you get on the chatbot or the Google Business Profile.

However, the defensibility of this tech stack is the subject of intense debate. Is this a proprietary moat, or just a complex implementation of standard APIs? Yext relies on data network effects—the more you use it, the better your graph becomes—but these effects are siloed per customer. They don't have a "Facebook-style" network effect where one customer’s data helps another. The true moat, if it exists, is in the integration depth. Once Yext is wired into 50 internal systems of a Fortune 500 company, ripping it out is painful. But as we will see in our analysis, that switching cost is significant but perhaps not insurmountable.

IX. Business Model, Customers, & GTM Strategy

Yext operates on a classic SaaS subscription model. Customers sign annual contracts, typically billed in advance. The pricing is tiered, based on the number of entities (locations, products, etc.) being managed and the mix of features required. A small contract might just be Listings, while a massive enterprise contract includes Answers, Pages, Reviews, and Analytics.

The customer segmentation has evolved significantly over the years. In the beginning, Yext chased the "Long Tail" of SMBs—dentists, plumbers, and dry cleaners. They eventually realized that serving these customers profitably at scale was nearly impossible. The support costs were too high, and churn was too frequent. Today, Yext is almost exclusively focused on the Enterprise. Their sweet spot is the "Multi-location Business" (MLB). Think QSR giants like Taco Bell and Wendy’s, retailers like Lululemon, and massive healthcare systems like hospital networks.

They also serve large global enterprises in sectors like Financial Services (e.g., Wells Fargo), Pharmaceuticals, and CPG. These companies may not have thousands of retail locations, but they have thousands of products, complex compliance requirements, and decentralized workforces that need access to knowledge.

The sales motion reflects this enterprise focus. They utilize a high-touch field sales model, with sales cycles that can stretch anywhere from 6 to 18 months. This is not a "credit card and you're done" product; it involves legal reviews, security compliance, and deep technical integration. Once the contract is signed, the Customer Success team takes over to ensure onboarding and drive expansion. The "Land and Expand" strategy is vital here. The initial deal might be for Listings, but the upsell into Answers and Site Search is where the real revenue growth happens.

For investors tracking the company, there are a few key metrics that matter most. Net Revenue Retention (NRR) is the primary indicator of product-market fit within the existing customer base—are they growing their spend year-over-year? Customer Acquisition Cost (CAC) versus Lifetime Value (LTV) tells us if the expensive sales model is worth it. And the "Magic Number" measures sales efficiency. In the private equity era, the focus has shifted heavily toward Free Cash Flow margins, proving that this business can print money if the growth dials are tweaked right.

X. Playbook: Strategic & Operating Lessons

Yext’s journey offers a masterclass in strategic agility. The first major lesson is the art of the pivot without alienating your base. Yext went from listings to knowledge to answers, a journey that spanned nearly a decade. They managed this by using the word "and," not "or." They continued to support the listings business—the cash cow—even as they poured R&D into the AI future. They didn't tell their enterprise customers to stop managing their local data; they told them that managing that data was now the foundation for a much bigger play: AI.

The second lesson is about timing and market narratives. Yext was undeniably early to "Knowledge Management" and "AI Answers." They were talking about structured data and entities back in 2012. But being early is the same as being wrong until the market catches up. For years, the market didn't care about "Knowledge Engines." They only cared when Google and ChatGPT made search cool again. This highlights the brutal reality of innovation: sometimes you have to survive the "winter of indifference" before you get to the "summer of adoption."

The third lesson is competing in the shadow of giants. Yext has had to navigate the waters with Google, Microsoft, and Amazon circling them. Their bet was that enterprises want control and compliance, features that the giants are often too big or too consumer-focused to provide perfectly. Yext positioned themselves as the "Switzerland of Data"—neutral, secure, and dedicated solely to the client's interests.

The fourth lesson concerns the tradeoffs of public vs. private ownership. Going public gave Yext the currency and the brand credibility to land massive enterprise contracts. But it also subjected them to short-termism and the volatility of investor sentiment. Going private in 2024 was a strategic retreat to a defensible position where they could rebuild the castle walls without the stock price acting as a daily scorecard.

Finally, the challenge of Platform vs. Point Solution. Yext has always aspired to be a Platform—the Knowledge Graph for everything. In reality, most customers buy them for specific use cases, like "Fix my Google Maps" or "Make my site search work." The ongoing struggle for Yext is elevating the conversation from the tactical solution to the strategic platform, ensuring they are viewed as infrastructure rather than just a utility.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

To truly understand Yext’s position, we need to apply some rigorous frameworks. Starting with Porter’s 5 Forces, the picture is one of intense pressure.

Competitive Rivalry is undeniably HIGH. The market is fragmented, with CMS vendors, pure-play search platforms, and point solutions all vying for budget. Most dangerously, the tech giants—Google, Microsoft, and Amazon—offer overlapping features for free or as part of larger bundles. While Yext differentiates through multi-platform integration, the price pressure is constant.

The Threat of New Entrants is MEDIUM to HIGH. Barriers to entry for basic listings management are low; anyone can build an API connector. However, the barriers are high for a full-scale enterprise Knowledge Graph with hundreds of integrations. The AI/LLM era lowers the barrier to "answers" features—any startup can plug into OpenAI’s APIs—but the enterprise trust, compliance, and integration depth required to displace Yext take years to build.

Bargaining Power of Suppliers is LOW to MEDIUM. In Yext’s case, the "suppliers" are the publishers like Google, Apple, and Yelp. This is a fragile dynamic. Yext needs these publishers more than they need Yext. If Google decides to cut off API access or change its terms of service, Yext’s business is in trouble. However, cloud infrastructure (AWS, GCP) is commoditized, keeping those costs stable.

Bargaining Power of Buyers is MEDIUM to HIGH. Large enterprise customers have significant leverage. They can squeeze Yext on price, demand long implementation times, or threaten to build solutions in-house. While switching costs exist, they are not infinite, and enterprises are increasingly savvy about using RFPs to pit vendors against each other.

The Threat of Substitutes is HIGH. This is the biggest risk. Customers can choose to DIY with internal teams, use free tools like Google My Business, or turn to Microsoft Search, Algolia, or Elastic for site search. And of course, the rise of ChatGPT offers a substitute for knowledge discovery that bypasses traditional search engines entirely.

Turning to Hamilton Helmer’s 7 Powers, we see a company with strengths, but few permanent advantages.

Scale Economies are WEAK. While SaaS has great unit economics at scale, Yext does not have a winner-take-all dynamic. Customer acquisition remains human-intensive, and their cost structure doesn't allow them to price out competitors simply by virtue of size.

Network Effects are WEAK to MEDIUM. There are modest data network effects—the more a client uses Yext, the better their graph becomes. There are also integration network effects—more publishers make the platform more valuable. But these are not viral or compounding in the way a social network is. Each customer’s data is siloed for privacy and compliance, preventing cross-customer learning.

Counter-Positioning was once MEDIUM but is DECLINING. Yext initially positioned itself as the modern, flexible alternative to rigid legacy CMSs and the consumer-focused Google. However, incumbents like Adobe and Google have aggressively adapted, eroding Yext’s unique positioning. The window of "we are the only ones doing this" has closed.

Switching Costs are MEDIUM, and this is arguably their strongest power. Replacing Yext is a headache. It means re-building connections to 200 publishers, re-pipelining data from CRMs, and re-training staff. As Yext deepens its workflow embedding, these costs rise. But it is still middleware; it is not as sticky as an ERP or a core database.

Branding is WEAK. Yext is not a household name in the C-suite. They lack the aspirational brand power of a Salesforce or a Snowflake. Buyers choose them for functionality and ROI, not for brand affinity. The category of "Knowledge Management" itself is nebulous and poorly defined, further weakening their brand standing.

Cornered Resource is WEAK. Yext owns no proprietary data—customers own their data. They have no unique technology that cannot be replicated by Google or Microsoft given enough time. Their publisher partnerships are valuable but can be replicated or rendered obsolete.

Process Power is MEDIUM. This is where Yext shines. They have developed a refined enterprise sales process and a deep, institutional understanding of multi-location pain points. The know-how required to maintain and update 200+ integrations is a complex operational asset that competitors would struggle to replicate quickly. But process advantages can eventually be copied by well-resourced rivals.

Power Score Summary: Yext is a company surviving on Switching Costs and Process Power. They lack the heavy artillery of Scale, Network Effects, or Cornered Resources. This implies that to survive, they must constantly run faster than the giants, deepening their integration into the customer's workflow faster than the incumbents can close the gap.

XII. Bull vs. Bear Case

So, where does all this leave us as we look toward the future? Let’s break down the Bull and Bear cases.

The Bull Case is compelling. The AI tailwinds are real and accelerating. The ChatGPT moment validated the "Answers" category; enterprises now realize they need a conversational interface for their data. They understand that generic AI is not enough; they need "grounded" AI. Yext’s installed base of thousands of enterprise customers is a massive asset. These companies are already locked in, providing a fertile ground for expansion into the new AI products. Under private ownership, TPG can be patient. They can invest in the product stack and pursue strategic M&A without the quarterly whipping from public markets. There is an argument that Yext’s defensibility is underestimated by Wall Street. The sheer breadth of integration and the depth of workflow embedding create a moat that is wider than it appears. As regulations around AI tighten, the argument for "enterprise-grade, compliant, non-hallucinating answers" becomes a fortress that Microsoft or Google might not be able to breach easily due to their own data privacy issues.

The Bear Case, however, is equally potent. It suggests that Google and Microsoft will inevitably win this war. They have infinite resources, the distribution (every company already uses Office 365 or Google Workspace), and they are the leaders in AI research. If Microsoft Copilot can answer questions from your SharePoint files, why do you need Yext? The Bear case argues that Yext lacks a strong moat. There are no network effects, the brand is weak, and the technology is replicable. The market education fatigue is real; Yext has been evangelizing this category for 15 years. If enterprises haven't fully bought in by now, maybe they never will. There is a significant risk of commoditization. As LLM APIs become cheaper and easier to use, the "Answers" feature becomes trivial to build. In an economic downturn, "Knowledge Management" looks like a discretionary spend compared to core CRM or sales tools. Furthermore, the decision to go private could be interpreted as a distress signal, suggesting that the growth engine has stalled and innovation is slowing under the weight of PE debt service. Finally, Yext’s value is tied to partnerships with Google and Apple. If those partners decide to cut Yext out of the loop, the business model collapses.

The Verdict: Yext is a classic "show me" story. The AI pivot and the protective shield of private ownership offer a legitimate path to a second act. The technology is sound, and the customer base is real. But the execution risk is off the charts. They are trying to hold a line against the tide. The next 2 to 3 years will determine whether Yext becomes the Snowflake of enterprise knowledge—a critical data infrastructure—or a cautionary tale of a SaaS company that successfully pivoted only to get squashed by the platform they depended on.

XIII. Epilogue & Recent Developments

As we close this episode in late 2025, looking back at the trajectory of Yext, we are reminded that timing is everything in technology. Yext’s story is not just about code and sales; it is about narrative and persistence. They were right about the importance of structured data long before it was cool. They were right about the limitations of keyword search long before generative AI arrived. But being right early is often the same as being wrong in the world of venture capital.

In the private markets, the company has continued to integrate Large Language Models (LLMs) deeper into the platform. Recent updates have focused on "Generative AI Agents" that can not just answer questions but perform actions, like booking a reservation or updating a status, using the Knowledge Graph as the source of truth. This move into "agentic workflows" is the new frontier, and Yext is betting that their graph is the only safe foundation for these agents to operate on.

Signals from the private company trajectory suggest a focus on consolidation. TPG has been aggressive in acquiring smaller AI startups to bolt into the Yext engine, particularly in the areas of vector databases and semantic search. This suggests a strategy to bulk up the technological moat before an eventual re-IPO or a sale to a larger strategic player like Oracle or Salesforce.

The broader industry trends point toward a shakeout. The era of vertical SaaS is ending; we are entering the era of "AI Infrastructure." Companies that provide the data layer for AI are the new prize. Yext is right in the crosshairs of this trend. The question is whether they can differentiate enough to be an independent winner, or if they will become an acquisition target for a larger platform trying to plug a hole in their own suite.

Reflecting on the journey from a listings manager in New York to an AI platform, Yext teaches us that the pivot is not a one-time event; it is a way of life. They survived the death of the Yellow Pages, the dominance of Google, and the pandemic. Now, in the AI era, they face their biggest challenge yet.

For founders listening, the lesson is stark: building in competitive markets requires a combination of paranoia and grit. You have to build your house on someone else’s land, but you have to make the foundation so deep they can’t dig you up without ruining the garden. Yext dug deep. Whether the house remains standing in the next decade is a story that is still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube