YETI Holdings Inc.: From Texas Coolers to Premium Lifestyle Empire

I. Introduction & Episode Roadmap

Here is a question that sounds absurd on its face: How do you build a billion-dollar company selling coolers? Not software. Not pharmaceuticals. Not fintech. Coolers. The insulated boxes people throw in the back of a truck to keep beer cold.

And yet YETI Holdings, a company founded in 2006 by two brothers from Driftwood, Texas, has done exactly that — and then some. With a market capitalization hovering around $2.8 billion as of early 2026, annual revenues approaching $1.9 billion, and gross margins north of 57%, YETI has built one of the most remarkable consumer brand stories of the twenty-first century. The company turned a commodity product into a status symbol, made drinkware aspirational, and created a lifestyle brand that sits comfortably alongside names like Patagonia, Lululemon, and even Apple in the premium consumer pantheon.

The YETI story touches on almost every theme that matters in modern business. Premium positioning in a commoditized market. Community-driven brand building before "influencer marketing" had a name. Private equity professionalization and the tension between authenticity and scale. Category expansion that doubled the addressable market overnight. A bruising intellectual property war with copycats. A public listing that Wall Street initially greeted with a shrug — before the stock quintupled. A pandemic that supercharged demand. And a competitive landscape that has only intensified, with Stanley's viral tumbler moment proving that even dominant brands can be challenged by cultural shifts on TikTok.

This is a story about how two outdoorsmen with no MBA between them saw a gap in the market — coolers that could actually survive serious use — and built a brand so powerful that millions of people now proudly display its logo on their trucks, their desks, and their Instagram feeds. It is also a story about what happens when a brand becomes so successful that everyone wants a piece of it, and what it takes to stay premium when the world is trying to commoditize you.

The core puzzle at the heart of YETI's story is deceptively simple: the company sells products that are functionally similar to alternatives costing one-fifth the price, and customers keep coming back for more. Understanding why — and whether that dynamic can endure — is the key to understanding everything about this business.

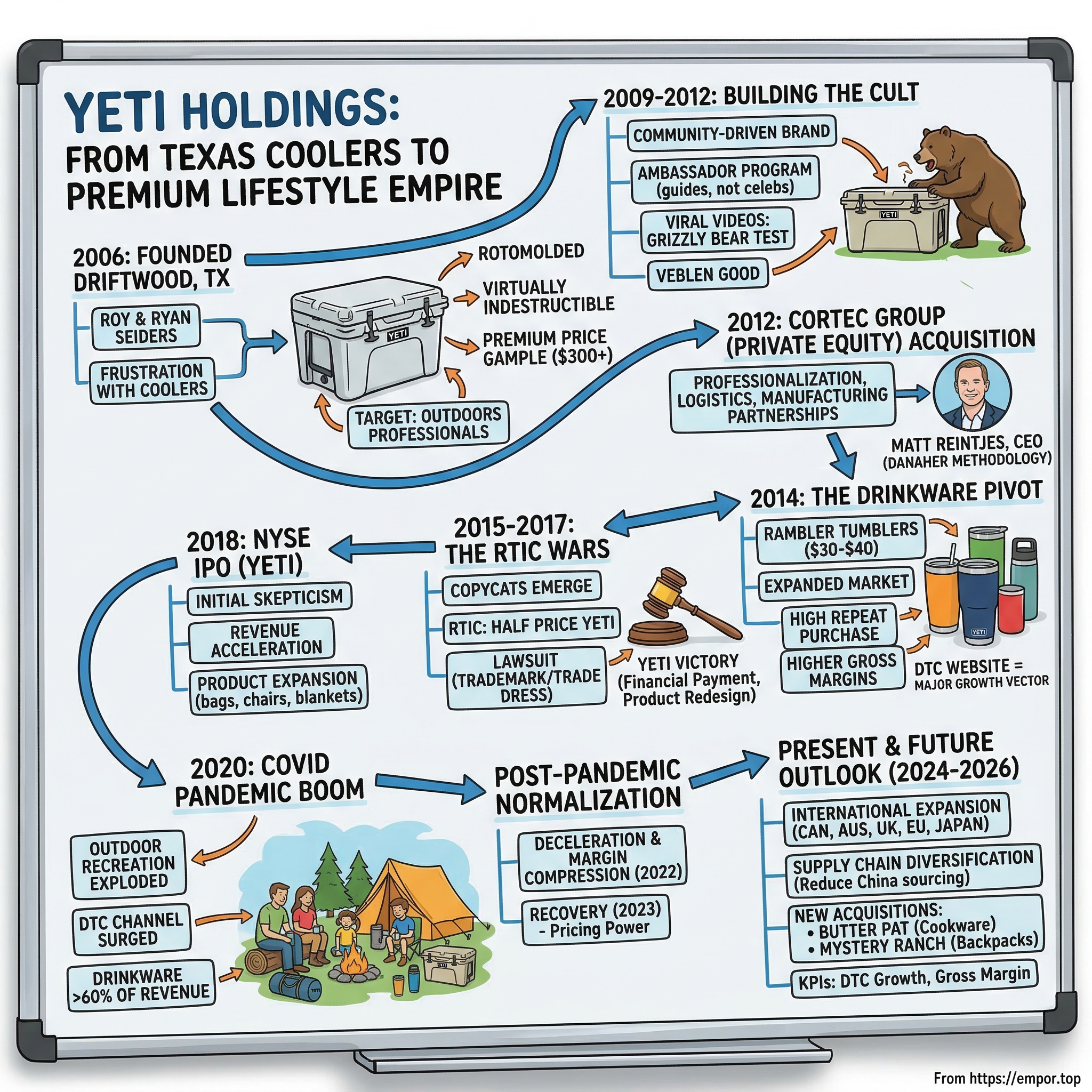

II. The Seiders Brothers & Genesis Story (2006-2009)

The story begins not in a Silicon Valley garage but in the Texas Hill Country, where Roger Seiders — a Houston-area high school shop teacher and avid fisherman — raised his two sons, Roy and Ryan, on a steady diet of outdoor adventure and entrepreneurial tinkering. Roger had designed his own fishing rods and eventually launched a fishing rod epoxy brand called Flex Coat. The apple, as they say, did not fall far from the tree.

Ryan Seiders graduated from Texas A&M in 1996 and almost immediately started a fishing rod company called Waterloo Rods, making specialty rods designed for grass fishermen along the Texas Gulf Coast. Roy, meanwhile, carved out his own niche making custom boats designed for shallow-depth fishing. Both brothers were deeply embedded in the outdoor community — not as weekend warriors, but as people whose livelihoods depended on gear that worked.

The origin insight came from Roy's frustration with the coolers available on the market. As someone who spent long days on the water guiding fishing trips, he needed a cooler that could actually hold ice for days, survive being thrown around in a boat, and withstand the kind of abuse that commercial use demands. Every cooler he bought broke — hinges snapped, latches failed, lids warped, and ice melted in hours rather than days. The products available from legacy brands like Igloo and Coleman were designed for backyard barbecues, not for serious professionals who needed their catch to stay cold on multi-day trips.

Roy began importing and distributing coolers but remained unsatisfied with the available options. He wanted a product built to his exact specifications. Ryan, who had recently sold his fishing rod company, offered to help. In 2006, working out of their father's garage in Dripping Springs, Texas, the brothers founded YETI Coolers.

The technological breakthrough was rotational molding — or rotomolding — a manufacturing process that creates a seamless, one-piece shell with uniform wall thickness. Think of it like a hollow chocolate Easter egg, but made from heavy-duty polyethylene. The mold rotates on two axes while the plastic melts and coats every surface evenly, eliminating the seams, joints, and weak spots that cause traditional coolers to crack and fail. The Seiders brothers partnered with a factory in the Philippines that had experience with this technique and spent two years iterating before arriving at their flagship product: the YETI Tundra, which launched in 2008.

The Tundra was a revelation for anyone who had ever cursed a broken cooler on a fishing trip. It featured rotomolded construction, freezer-quality gasket seals, heavy-duty rubber T-latches, and pressure-injected polyurethane foam insulation. It could hold ice for days, not hours. It was virtually indestructible. And it cost upward of $300.

That price point was the gamble that defined the company. In a market where the average cooler sold for $30 to $50, the Seiders brothers were asking ten times more. The conventional wisdom said this was insane. But the brothers understood something that market research could not quantify: their target customer — hunting guides, commercial fishermen, serious outdoors professionals — cared about performance above all else. These were people who would spend $50,000 on a boat and $1,000 on a fishing rod without blinking. A $300 cooler that actually worked was not a luxury; it was a tool.

Initial distribution was hyper-local and hyper-targeted. Roy and Ryan sold through Texas tackle shops, feed stores, and the word-of-mouth networks of fishing and hunting guides who were already part of their social circles. There was no national advertising, no retail strategy, no marketing plan. Just a great product placed in front of the people most likely to appreciate it, sold by two guys who spoke the same language as their customers.

The early years were a grind. Revenue was modest, and the brothers were essentially running a niche business for a niche audience. But something important was happening beneath the surface: every guide who bought a Tundra became an unpaid evangelist. When clients saw the cooler that kept their catch perfectly cold for three days straight, they asked about it. When fellow guides saw it survive being dropped off a tailgate, they wanted one. The product was doing the marketing, and the network effect — while small — was real and growing.

III. Building the Cult: Community Before Marketing (2009-2012)

By 2009, YETI had something that most consumer brands spend millions trying to manufacture: genuine grassroots credibility. The company had not spent a dime on traditional advertising, yet its name was spreading through the outdoor community like wildfire. The reason was beautifully simple — the product was so obviously superior to everything else on the market that it marketed itself.

But Roy and Ryan Seiders were savvy enough to recognize that organic word-of-mouth, while powerful, needed to be nurtured and directed. What they built next was an ambassador program that predated the modern influencer economy by years and, in many ways, remains more effective than anything Instagram has produced since.

The YETI ambassador program was built on a radical premise: find the most respected, most authentic voices in outdoor culture — not the most famous — and give them the product. The brothers recruited hunting guides, fishing captains, rodeo cowboys, snowboarders, and professional skiers who were leaders within their communities. High-profile outdoorsmen like Jim Shockey and Flip Pallot received YETI coolers and provided video testimonials, even when the company could not afford formal sponsorship deals. The key was authenticity: these were real users who genuinely loved the product, not paid celebrities reading scripts.

The vetting process was deliberately rigorous. YETI took up to two years to evaluate potential ambassadors, ensuring they were genuine community leaders rather than social media opportunists. By the time the program matured, it included more than 150 ambassadors across a range of outdoor disciplines. As YETI's CMO later stated, the company would "never cede control to the whims of influencers and celebs." This was anti-influencer influencer marketing.

The go-to-market strategy targeted the places where serious outdoors people gathered: fishing tournaments, hunting expos, tailgating events, and outdoor trade shows. YETI did not try to reach everyone. It tried to reach the right people — the opinion leaders whose endorsement carried weight with everyone below them in the outdoor hierarchy. If the most respected fishing guide in South Texas was using a YETI, every recreational angler who aspired to that lifestyle wanted one too.

Then came the viral moments that changed everything. YETI produced a series of videos showing its coolers being subjected to extreme punishment tests, but the one that captured the internet's imagination showed a grizzly bear attempting — and failing — to break into a YETI Tundra. The video was cleverly produced, genuinely entertaining, and served as both marketing and product validation in a single package. YETI's Tundra Hard Coolers eventually earned certification as bear-resistant by the Interagency Grizzly Bear Committee, meaning they had withstood grizzly bear attacks for an hour or more without being breached. For a cooler company, this was the equivalent of a crash-test five-star rating — objective, dramatic proof that the premium price was justified.

Ice retention challenges followed, with users posting videos and photos showing how many days their YETI coolers could keep ice frozen in brutal summer heat. The results were staggering — five days, seven days, sometimes longer — and they spread across hunting forums, fishing blogs, and early social media channels with the enthusiasm of genuine discovery.

What emerged from all of this was something far more powerful than a product preference: a brand identity. YETI became synonymous with a certain kind of American outdoor culture — tough, authentic, unapologetic about quality, and willing to pay for the best. The cooler became, as one observer put it, "the tactical vest for your beer." It was not just a container; it was a statement about who you were and what you valued.

Distribution expanded carefully into retailers that reinforced this identity: Bass Pro Shops, outdoor specialty stores, hardware chains, and sporting goods retailers. YETI was deliberate about where its products appeared, understanding that shelf placement shapes brand perception. You would not find a Tundra at Walmart — not yet, and not ever. That restraint was itself a form of marketing.

The premium positioning created something counterintuitive: the price became a feature, not a bug. In outdoor culture, where gear choices signal competence and commitment, carrying a YETI cooler communicated that you were serious. It was a Veblen good — a product whose desirability increases with its price because the price itself conveys status. The rancher who put a YETI in his truck bed was making a statement to every other rancher at the feed store. The tailgater who brought a Tundra to the college football parking lot was declaring allegiance to a tribe.

By 2012, YETI had built something that most consumer brands can only dream of: a passionate, loyal community that identified with the brand on a personal level. Revenue was growing rapidly, and the brothers had proven that a premium-priced product in a commoditized category could not only survive but thrive. The question was no longer whether the model worked — it was how big it could get.

IV. Category Expansion: The Drinkware Pivot (2012-2014)

If the Tundra cooler was YETI's proof of concept, the Rambler tumbler was the move that transformed a niche outdoor equipment company into a mainstream lifestyle brand. On April 9, 2014, YETI introduced the Rambler 20 and Rambler 30 — double-wall, vacuum-insulated stainless steel tumblers that applied the same "wildly overbuilt for the mission" philosophy to a product people could carry every day.

The technology was not new — vacuum insulation had been around since the thermos was invented in the early 1900s. But YETI's execution was superior. The Ramblers used 18/8 kitchen-grade stainless steel, a construction technique that eliminated condensation on the outside while keeping drinks cold (or hot) for hours, and a design aesthetic that was distinctly YETI — rugged, clean, substantial in the hand. They came in at $30 to $40, a steep premium over generic travel mugs but an accessible price point compared to a $300 cooler.

The strategic brilliance of the drinkware pivot cannot be overstated. It solved three problems simultaneously. First, it expanded the addressable market from "people who buy coolers" to "everyone who drinks beverages" — a category roughly a thousand times larger. Second, it created a repeat purchase dynamic that coolers lacked: a person might buy one cooler every decade, but they would buy multiple tumblers, in different sizes and colors, as gifts and impulse purchases. Third, drinkware carried even higher gross margins than coolers, improving the overall profitability of the business.

The suburban breakthrough happened almost immediately. The Rambler tumbler became the product that took YETI from fishing guides to soccer moms, from duck blinds to desk drawers, from the marina to the minivan. It was the bridge product that made the brand accessible to consumers who might never set foot in a Bass Pro Shop but who wanted to signal an affinity for the outdoor lifestyle. You did not need to hunt elk to appreciate a tumbler that kept your coffee hot for six hours.

What made the tumbler phenomenon particularly interesting was the logo culture it spawned. The YETI logo — a simple, clean silhouette of a sasquatch — became a badge. People did not just use YETI tumblers; they displayed them. Companies ordered custom-branded Ramblers as corporate gifts. Colleges, sports teams, and nonprofits sold co-branded versions as fundraisers. The tumbler became a canvas for identity expression, and every custom logo reinforced YETI's position as the default premium option.

The Rambler line expanded rapidly: the Colster can holder and 10-ounce Lowball arrived in 2015, followed by 18-, 36-, and 64-ounce bottles in 2016. Each new form factor addressed a different use case and price point, creating an ecosystem of products that encouraged collectors to accumulate the full set.

The revenue impact was seismic. Net sales surged from roughly $90 million in 2013 to nearly $450 million by 2015, with drinkware driving much of the acceleration. The product mix began its dramatic and permanent shift: by fiscal year 2025, drinkware accounted for approximately $1.09 billion of YETI's $1.87 billion in revenue — roughly 58% of total sales. The cooler company had become a drinkware company that also sold coolers.

Distribution expanded accordingly. YETI products appeared in REI, Dick's Sporting Goods, Ace Hardware, and lifestyle retailers that would never have stocked a rotomolded cooler. Each new channel brought new customers, and each new customer reinforced the brand's cultural cachet. The flywheel was spinning faster.

V. The Private Equity Chapter: Cortec Group (2012-2018)

On June 15, 2012, a New York-based private equity firm called Cortec Group Fund V acquired approximately two-thirds of YETI Coolers for a reported $67 million. The deal was the first platform investment for Cortec's Fund V, which had closed in 2011 with $620 million in committed capital. Fifth Street Finance Corp. provided a $47.5 million one-stop financing facility to support the acquisition.

For the Seiders brothers, the Cortec investment represented a partial exit and a recognition that the business they had built in their father's garage had outgrown their ability to manage it alone. Roy and Ryan were product visionaries and community builders, but scaling a consumer brand from tens of millions to hundreds of millions in revenue required operational infrastructure, supply chain expertise, and professional management. Private equity brought all three.

Cortec's playbook was textbook PE professionalization. The firm brought in experienced operators to build out logistics, manufacturing partnerships, and retail distribution. In September 2015, Cortec hired Matt Reintjes as President and CEO — a move that would prove transformational. Reintjes was not an outdoor industry lifer; he was a disciplined operator with a degree in economics from Notre Dame, an MBA from the University of Virginia's Darden School, and nine years at Danaher Corporation, the conglomerate famous for its Danaher Business System — a relentless methodology for improving operational efficiency. He had also served as COO of Bushnell Outdoor Products and led Vista Outdoor's Outdoor Products division. In other words, he knew both premium consumer brands and the mechanics of scaling them.

Under Reintjes, YETI accelerated its transformation from a regional outdoor brand to a national lifestyle company. The product line expanded beyond hard coolers and drinkware into soft coolers, bags, chairs, blankets, dog bowls, and a growing array of accessories. Manufacturing partnerships were formalized and diversified across Asia and the Americas. The direct-to-consumer channel — YETI's website — was invested in as a strategic priority rather than an afterthought.

But the PE chapter also brought tensions. Manufacturing shifted overseas — primarily to China for drinkware and the Philippines for hard coolers — sparking grumbling among the outdoor community that valued "American-made" authenticity. The reality was more nuanced: YETI had partnered with overseas manufacturers from the very beginning, and the company never owned any manufacturing facilities. All production was through third-party partners including Plastics Professionals, Centro Incorporated, Solar Plastics, and others. But perception matters in brand building, and the scaling of overseas production became a talking point for competitors.

The copycat explosion also accelerated during this period. YETI's success had proven that consumers would pay a premium for better-built outdoor products, and the market responded with a flood of imitators. Ozark Trail, Walmart's house brand, offered look-alike coolers at a fraction of the price. But the most threatening competitor emerged from much closer to home.

The PE investment proved to be one of the great private equity returns of its era. When Cortec finally exited — through the October 2018 IPO and subsequent secondary offerings stretching into February 2021 — the firm had generated more than 25 times its invested capital on a gross basis and more than 20 times on a net basis. PitchBook called it one of the "best PE funds of the millennium." On a $67 million investment, Cortec ultimately realized returns in the billions.

VI. The RTIC Wars & Competition Onslaught (2015-2017)

In 2015, twin brothers John and Jim Jacobsen of Cypress, Texas, launched RTIC — a company whose products looked almost identical to YETI's but were sold at roughly 40% lower prices. The Jacobsens had deep familiarity with the cooler market, and RTIC's marketing was deliberately provocative, positioning its products as "half the price of a YETI and holds more ice." The internet commonly repeated the claim that RTIC's founders were related to the Seiders brothers, but this was incorrect — they were simply two different pairs of Texas brothers who happened to end up in the same industry.

What was not in dispute was that RTIC's products bore a striking resemblance to YETI's. The design language, the construction approach, even the marketing tone were clearly derivative. For YETI, this represented an existential question: if someone could sell a functionally similar product at half the price, was the brand premium real or was it an illusion that would evaporate under competitive pressure?

In July 2015, YETI filed a lawsuit against RTIC alleging trademark and trade dress infringement. The litigation was aggressive and expensive, but the company's leadership believed that protecting intellectual property was essential to defending the brand. Trade dress — the overall visual impression of a product — is notoriously difficult to enforce, but YETI had a strong case given the near-identical appearance of RTIC's early products.

The settlement came on February 2, 2017, in United States District Court. RTIC and the Jacobsen brothers were required to make a financial payment to YETI (the amount was not disclosed), cease sales of all infringing products — hard-sided coolers, soft-sided coolers, and drinkware — and redesign their entire product line. It was a comprehensive victory that sent a clear message to the market: YETI would spend whatever it took to defend its intellectual property.

The RTIC episode was the most dramatic, but it was far from the only competitive challenge. Walmart's Ozark Trail brand offered coolers that mimicked YETI's design at mass-market prices. Hydro Flask carved out a strong position in drinkware, particularly on the West Coast and among younger consumers. Klean Kanteen, Pelican, Grizzly, and dozens of other entrants fragmented the market that YETI had essentially created from nothing.

The strategic lesson was profound. YETI maintained its premium positioning not by matching competitors on price — which would have been suicidal for a brand built on exclusivity — but by doubling down on what made it different. Better content. More authentic community engagement. Continued product innovation. Distribution discipline. And relentless litigation when competitors crossed the line from inspiration to imitation.

The competitive onslaught also forced a reckoning with the fundamental question of YETI's moat. Was it a product company with a marketing advantage, or a marketing company that happened to make products? The answer, increasingly, was the latter. The functional gap between a YETI tumbler and a $10 Ozark Trail tumbler was real but relatively modest — both kept drinks cold, both were made of stainless steel. The enormous price gap was justified by brand, not by physics. YETI was selling identity, belonging, and aspiration. That is a very different kind of moat than a patent or a network effect, and whether it was durable enough to justify a premium valuation would become the central debate among investors for years to come.

VII. Going Public: The 2018 IPO & Beyond (2018-2020)

On October 24, 2018, YETI Holdings priced its initial public offering at $18 per share — below the original range of $19 to $21 and with a reduced share count of 16 million shares, down from the initially proposed 20 million. Of those shares, just 2.5 million were offered by the company itself, with the remaining 13.5 million sold by existing shareholders, primarily Cortec. Trading began the following day on the New York Stock Exchange under the ticker "YETI."

The reception was, by any measure, chilly. The below-range pricing and downsized offering reflected genuine skepticism from institutional investors. Their concerns were reasonable: the cooler market appeared mature, competition was intensifying from both high-end and low-end players, the company had significant exposure to Chinese manufacturing at a time of rising trade tensions, and the growth narrative was not immediately obvious. Could a cooler company really sustain the kind of revenue growth that justified a premium multiple?

The skeptics were wrong. YETI's revenue had been $779 million in fiscal year 2018. By 2019, it climbed to $914 million. By 2020, it crossed a billion dollars for the first time, reaching $1.09 billion. This was not the trajectory of a mature product company running out of runway — it was acceleration.

The engine behind this growth was the direct-to-consumer channel. While legacy wholesale partnerships with Dick's, REI, and ACE Hardware remained important, YETI's website was becoming the company's most powerful growth vector. DTC sales offered higher margins, richer customer data, and the ability to control the brand experience from first click to unboxing. The company invested heavily in e-commerce infrastructure, digital marketing, and a content strategy designed to drive traffic and conversion.

Product innovation continued to expand the addressable market. Bags, chairs, blankets, dog bowls, and a growing range of accessories transformed YETI from a cooler company into a lifestyle platform. Each new category leveraged the existing brand equity and distribution infrastructure, and each new product created another touchpoint with consumers.

Then came the pandemic. When COVID-19 shut down indoor entertainment, forced families outdoors, and supercharged e-commerce adoption, YETI found itself at the intersection of every tailwind in the consumer economy. Outdoor recreation exploded. People who had never gone camping suddenly needed coolers, tumblers, and outdoor gear. And they were buying online, where YETI's DTC channel was already best-in-class.

The stock reflected this transformation. From its IPO price of $18, YETI shares climbed past $90 by late 2020, representing a five-fold increase in just over two years. The market capitalization exceeded $7 billion at its peak in 2021. The narrative had completely flipped: YETI was no longer a cooler company that might be a fad — it was a premium lifestyle brand with a long runway for growth.

The realization that crystallized during this period was strategic: YETI had built a platform, not just a product. The brand was the asset, and it could be extended into virtually any category where "premium outdoor lifestyle" carried meaning. The cooler was the origin story, but the story was no longer about coolers.

VIII. The Brand Playbook: How YETI Actually Works

Understanding YETI requires understanding how the brand functions as a business system — not just what the company sells, but why people buy it, how the brand stays relevant, and what operational machinery makes it all work. This is where YETI separates from the pack of consumer goods companies.

The content marketing operation is the crown jewel. In 2015, YETI launched "YETI Presents," a documentary film series that has since produced more than 75 short films. What makes these films remarkable is what they do not do: they do not sell products. YETI's founders explicitly directed the content team not to worry about showing the product or even mentioning it. Instead, the films chronicle the lives of people who work and play in the outdoors — surfers, hunters, fishermen, cowboys, chefs — with the kind of production quality and storytelling craft that would be at home at Sundance. The series has won awards at film festivals, and notable entries include a film about Jimmy Buffett and the laidback culture of 1970s Key West.

In 2023, YETI elevated this approach by launching the Pretty Wild Fellowship — a $200,000 documentary grant created in partnership with Academy Award-winning filmmakers Elizabeth Chai Vasarhelyi and Jimmy Chin and the Points North Institute. Four filmmakers each received $50,000 to produce outdoor documentaries. This was not traditional advertising; it was patronage of the arts, designed to associate the YETI brand with the highest level of storytelling about the natural world.

The retail experience reinforces the brand identity. YETI expanded to 24 owned retail stores by the end of fiscal year 2024, including its first Canadian location in Calgary. These stores function as "brand temples" — immersive environments designed to communicate the YETI lifestyle rather than simply move inventory. The company plans to add four to six new stores annually, though leadership has been clear that physical retail will remain a small piece of the overall business. The primary DTC focus is e-commerce.

The customization economy has become another powerful brand amplifier. Corporate logos, team colors, university crests — YETI products have become the default canvas for branded merchandise in the premium tier. Every custom tumbler bearing a company logo is both a sale and an advertisement, extending the brand's reach into boardrooms, trade shows, and gift bags without a dollar of traditional marketing spend.

Why do people pay five times more for a YETI than a functionally adequate alternative? The answer operates on three levels. At the functional level, YETI products are genuinely superior — better ice retention, more durable construction, more thoughtful design. At the emotional level, YETI purchases feel like an investment in quality rather than an expense on consumption. And at the identity level, owning YETI products signals membership in a tribe that values the outdoors, authenticity, and a willingness to pay for the best. The logo on a tumbler or the sticker on a truck bumper communicates something about the owner, and that communication has value.

The gender and demographic expansion has been a quiet but strategically important evolution. YETI's early customer base was overwhelmingly male — hunters, fishermen, and tailgaters in the South and Southwest. Under Reintjes, the company has deliberately broadened its appeal to women, families, and urban consumers without alienating the core audience. Product design has become more color-diverse and lifestyle-oriented, and marketing content features a wider range of outdoor activities beyond traditional hunting and fishing. The Rambler tumbler was the initial bridge product for this expansion, but it has continued across categories.

Sponsorship strategy targets communities rather than celebrities. YETI partners with the World Surf League, rodeo circuits, fishing leagues, and outdoor festivals — events that bring together the company's target consumers in authentic settings. The company has resisted the temptation to pursue mass-market celebrity endorsements, understanding that credibility in outdoor culture comes from participation, not association.

On the manufacturing and supply chain front, YETI has evolved significantly. Hard coolers are produced in the United States — primarily in Iowa, Wisconsin, and South Carolina — and in the Philippines. Drinkware has historically been manufactured in China, with soft coolers and accessories sourced from China, Vietnam, and the Philippines. In response to tariffs reaching as high as 145% on Chinese imports, the company accelerated diversification in 2025, targeting more than 90% of drinkware production outside China by year-end, with key suppliers ramping operations in Thailand and Malaysia. The estimated tariff impact was approximately $100 million, with 90% related to China.

Sustainability messaging has centered on durability — the argument that a product built to last a lifetime generates less waste than cheap alternatives that are replaced every few years. This "buy it for life" positioning has resonated with environmentally conscious consumers and provides a defense against criticism of the premium price point.

IX. Inflection Point: COVID and the Outdoor Boom (2020-2021)

When the world shut down in March 2020, something unexpected happened to outdoor recreation: it exploded. Families who had never gone camping bought tents. People who had never hiked bought boots. And millions of consumers who had never considered spending $300 on a cooler suddenly found themselves planning outdoor adventures because there was literally nothing else to do. YETI was perfectly positioned to capture this surge.

Revenue jumped from $914 million in 2019 to $1.09 billion in 2020 — a 19% increase that looks even more impressive given that the first quarter of the pandemic created significant supply chain disruptions and retail shutdowns. The DTC channel absorbed much of the demand that could not flow through temporarily closed wholesale partners, with website sales surging as consumers shifted to e-commerce out of necessity and then out of preference.

The following year was even bigger. Fiscal 2021 revenue hit $1.41 billion, a 29% increase that represented the company's fastest growth rate as a public company. Gross margins expanded to 57.8%, up from 57.6% the prior year, demonstrating that YETI could grow rapidly without sacrificing pricing power. Net income reached $213 million, and the market rewarded this performance with a valuation that peaked above $7 billion.

But the pandemic boom also raised uncomfortable questions about sustainability. How much of the demand spike was permanent behavioral change, and how much was a temporary bubble driven by stimulus checks, remote work, and limited entertainment alternatives? Management was emphatic that the shift was structural: Americans had rediscovered the outdoors, and the habits formed during the pandemic — camping trips, backyard entertaining, outdoor cooking — would persist. The new customers acquired during the boom were not one-time buyers; they were joining the YETI ecosystem.

The product mix evolution told its own story. Drinkware had grown to represent approximately 60% of revenue by 2021, confirming that the category was not just a supplement to the cooler business but its primary growth engine. The everyday use case — coffee in the morning, water at the gym, cocktails on the patio — provided a purchase frequency that coolers could never match.

Supply chain management during this period became a competitive differentiator. While many consumer brands struggled with shortages, delays, and stockouts, YETI managed its inventory and manufacturing relationships well enough to keep products on shelves and deliveries flowing. The company's decision to maintain multiple manufacturing partners across multiple geographies provided resilience that single-sourced competitors lacked.

The 2020 pandemic year also produced a remarkable cash flow result: $366 million in operating cash flow and $343 million in free cash flow, driven partly by favorable working capital dynamics. The company used this liquidity to pay down $165 million in debt, strengthening the balance sheet at precisely the moment when financial flexibility mattered most.

X. The Maturation Phase: Growth, Margins, and International (2021-Present)

The post-pandemic normalization was inevitable but still jarring. After two years of exceptional growth, fiscal 2022 revenue increased only 13% to $1.60 billion — respectable by any normal standard but a deceleration that spooked investors accustomed to faster expansion. More concerning, gross margins compressed sharply to 47.8% as freight costs surged, input costs rose, and the company faced the residual impact of pandemic-era supply chain disruptions. Net income fell to $90 million, less than half the prior year's level. The stock, which had peaked above $100 in late 2021, cratered to the low $30s.

Recovery came in 2023, as supply chain pressures eased and YETI's pricing power reasserted itself. Revenue rose to $1.66 billion, gross margins recovered to 56.9%, and net income rebounded to $170 million. The fiscal year 2024 saw continued improvement: $1.83 billion in revenue, 58.1% gross margins, and $176 million in net income. The company was back on a trajectory, albeit at a more moderate growth rate than the pandemic-era peaks.

International expansion became the most compelling growth narrative. In fiscal 2018, the year of the IPO, international revenue was just $17 million — barely 2% of total sales. By fiscal 2024, international revenue had reached $339 million, accounting for 18.5% of the total. The growth rate was striking: international sales increased 25% in the fourth quarter of fiscal 2025 and 16% for the full year. Canada, Australia, and the United Kingdom were the most developed markets, with YETI opening its first Canadian retail store in Calgary during 2024. The company was also unlocking the DACH region — Germany, Austria, and Switzerland — and building early traction in Japan. Management targeted lifting the international mix to 20-25% of total sales over the medium term, with high-teen to 20% annual growth.

The competitive landscape shifted dramatically with the Stanley Cup tumbler phenomenon. Stanley, a brand founded in 1913 that had been largely forgotten, experienced a viral renaissance when its 40-ounce Quencher tumbler became a TikTok sensation. The hashtag #StanleyTumbler accumulated approximately 700 million views, almost entirely from user-generated content. Stanley's revenue surged past $750 million, and on Amazon, Stanley outsold YETI in unit volume — roughly 596,000 units per month versus YETI's 357,000.

The Stanley phenomenon was instructive for what it revealed about the drinkware market and YETI's position within it. Stanley captured a younger, more trend-driven demographic — the same consumers who cycle through viral products at TikTok speed. YETI, by contrast, appealed to consumers who valued longevity and performance over momentary cultural relevance. Both brands benefited from the "Stanley versus YETI" comparison that dominated social media, keeping YETI in the cultural conversation even as Stanley captured the viral moment. Whether Stanley's momentum would prove durable or ephemeral remained an open question.

The dupe economy presented a related challenge. TikTok culture had normalized the idea that "good enough" alternatives to premium products were not just acceptable but savvy. Gen Z consumers, in particular, showed greater willingness to choose functional equivalents at lower price points. Whether this represented a generational shift in consumer behavior or a phase that would pass as incomes grew remained a key debate.

Recent management changes reflected the company's evolution. In February 2026, Scott Bomar joined as CFO, replacing the retiring Mike McMullen. Bomar brought more than 20 years of retail finance experience from Home Depot, signaling YETI's increasing focus on retail operations and omnichannel execution. CEO Matt Reintjes, now in his eleventh year leading the company, joined the Harley-Davidson board as an independent director in September 2025, further cementing his reputation as a premium brand operator.

On the product innovation front, YETI made two notable acquisitions in early 2024: Butter Pat Industries, a premium cast iron cookware maker, and Mystery Ranch, a technical backpack brand, for a combined purchase price of approximately $48.5 million. These acquisitions signaled an intent to extend the YETI brand into adjacent outdoor categories — cooking and load-carrying — where the "premium, built for life" positioning resonated.

In March 2023, the company had faced a recall of 1.9 million soft coolers and gear cases — Hopper M20, M30, and SideKick Dry models — due to magnet-lined closures that could degrade and release small magnets, posing an ingestion hazard. No injuries were reported, and the company handled the recall proactively, but it served as a reminder that product quality — the foundation of the brand — requires constant vigilance.

The fiscal year 2025 results, reported in February 2026, showed a company that was growing steadily if not spectacularly. Revenue reached $1.87 billion, up 2% year-over-year. The company repurchased 8.2 million shares for $297.6 million, demonstrating confidence in its own valuation and returning capital to shareholders in the absence of a dividend. For fiscal 2026, management guided for 6-8% sales growth, a target that would put YETI on track to reach the $2 billion revenue milestone.

The stock, which had experienced enormous volatility — from $18 at the IPO to above $100 in late 2021 to the low $30s in 2022 and back to $36 as of early March 2026 — reflected the market's ongoing debate about whether YETI was a growth company or a mature brand trading at a premium it could no longer justify.

XI. Porter's Five Forces Analysis

Threat of New Entrants: Medium-High. The barriers to entering the insulated products market are deceptively low. Contract manufacturers in China, Southeast Asia, and the Philippines will produce coolers and tumblers to spec for virtually anyone with a purchase order. The raw materials — stainless steel, polyethylene, polyurethane foam — are commodity inputs. And social media has lowered the cost of customer acquisition to the point where a clever TikTok video can launch a brand overnight. Stanley's resurgence from near-obscurity to $750 million in revenue proves that even a century-old dormant brand can capture market share with the right product-market-moment fit. The barrier that remains genuinely high is brand building — creating the kind of emotional connection and cultural cachet that justifies a three-to-five-times price premium. That takes years, capital, and authenticity that cannot be faked. But the functional product itself can be replicated by anyone with a catalog.

Bargaining Power of Suppliers: Low to Medium. YETI does not own manufacturing facilities. All production is outsourced to third-party partners, which in theory creates supplier dependence. In practice, however, rotomolding and vacuum insulation technology are widely available, and YETI's scale — approaching $2 billion in revenue — gives it significant negotiating leverage. The company maintains relationships with multiple manufacturers across geographies, reducing the risk of any single supplier holding disproportionate power. The primary supply chain risk is not supplier leverage but commodity input costs — steel and plastic prices fluctuate with global markets — and trade policy, as the tariff environment around Chinese manufacturing has demonstrated.

Bargaining Power of Buyers: Medium. Individual consumers have minimal bargaining power — YETI sets prices and customers either pay or they do not. Brand loyalty is high among core customers, and the emotional switching costs (giving up a brand you identify with) exceed the functional switching costs (both products keep drinks cold). However, wholesale partners like Dick's Sporting Goods, REI, and ACE Hardware have moderate leverage in negotiating margins and shelf placement. YETI's decision to exit Lowe's to focus on DTC and key wholesale accounts illustrates the tension between distribution breadth and margin protection. As DTC sales crossed $1 billion in fiscal 2024, representing roughly 60% of total revenue, the company has reduced its dependence on any single wholesale partner.

Threat of Substitutes: High. This is the force that keeps YETI investors up at night. Functional substitutes are everywhere: Ozark Trail tumblers perform 90% of the insulation function at 20% of the price. RTIC, Hydro Flask, Klean Kanteen, and dozens of others offer credible alternatives at various price points. The reason YETI survives — and thrives — despite this substitution pressure is that the company is not selling insulation. It is selling identity, status, and belonging. That emotional premium is real and measurable in revenue, but it is also inherently fragile. In an economic downturn, when consumers trade down from premium to value, substitution risk increases significantly.

Competitive Rivalry: High. The insulated products market is intensely competitive across every price point. Stanley's viral success demonstrated that market positions can shift rapidly. Private label threats from major retailers add another dimension of pressure. Innovation in product design, materials, and marketing is continuous, with competitors racing to match YETI's content strategy, community building, and product extensions. What keeps rivalry from becoming commoditizing is YETI's pricing discipline — the company has never engaged in promotional discounting to defend share, understanding that the moment a premium brand competes on price, it ceases to be premium.

XII. Hamilton's 7 Powers Framework Analysis

Scale Economies: Moderate. YETI benefits from manufacturing scale — larger production runs reduce per-unit costs — and marketing efficiency improves as the brand's fixed content investments are amortized over a larger revenue base. But this is not a business where scale creates the kind of structural cost advantages that characterize true scale economies. A competitor with half YETI's revenue could achieve similar unit economics. The 57% gross margin is driven primarily by pricing power, not cost advantages.

Network Effects: Low. YETI products do not become more valuable as more people use them — there is no functional network effect comparable to a payments platform or social network. However, there is a subtle social dynamic at work: as YETI ownership becomes more widespread within a social group, it creates pressure for others to join. The "everyone at the tailgate has one" phenomenon drives demand through social conformity rather than functional interdependence. This is closer to a bandwagon effect than a true network effect, and it can work in reverse if the brand becomes too ubiquitous and loses its aspirational edge.

Counter-Positioning: Strong historically, diminishing. When YETI launched, incumbent cooler companies like Igloo and Coleman could not respond without cannibalizing their existing businesses. They were built around $30 coolers sold through mass retailers; matching YETI's premium positioning would have meant admitting their core products were inferior and alienating their existing customers. This counter-positioning gave YETI a multi-year window to establish the premium cooler category without serious competition from the companies best equipped to challenge it. That window has largely closed — the market now accepts premium coolers as a legitimate category, and competitors of all sizes have entered.

Switching Costs: Moderate. The functional switching costs are low — a Stanley tumbler keeps coffee hot just as well as a YETI Rambler. But the emotional and identity-based switching costs are surprisingly high. Consumers who have invested in multiple YETI products — coolers, tumblers, bags, accessories — have built an ecosystem that creates soft lock-in. More importantly, the "YETI person" identity is the real switching cost. Abandoning the brand means abandoning a piece of self-image, which most consumers are reluctant to do. This is similar to how Apple users stay in the ecosystem not because of technical switching costs but because of identity and familiarity.

Branding: Very Strong. This is YETI's primary power and the foundation of the entire business. The brand commands a three-to-five-times price premium over functionally comparable alternatives, and customers pay it willingly. The affective valence — the emotional response customers have to the brand — is overwhelmingly positive among core users. The brand reduces uncertainty (customers trust that any YETI product will be high quality), signals status (the logo communicates values and identity), and creates belonging (owning YETI products connects you to a community). The brand has strengthened over nearly twenty years, surviving competition, copycats, and market cycles. This is the kind of durable competitive advantage that is extremely difficult to replicate.

Cornered Resource: Low to Moderate. YETI has no unique technology, proprietary manufacturing process, or irreplaceable patent portfolio. Rotomolding and vacuum insulation are widely accessible. The cornered resource, to the extent one exists, is the brand itself — which by definition cannot be quickly replicated by competitors. The Seiders brothers' original vision and authenticity were initially unique, but the brand has now transcended its founders and exists as an independent asset.

Process Power: Moderate. YETI has developed superior processes in product development, content creation, community building, and DTC operations. The ambassador program, the YETI Presents film series, the retail store experience — these are operational capabilities that took years to build and are difficult to replicate. But they are ultimately replicable by well-funded competitors with enough time and talent. Process power provides an ongoing advantage but not an insurmountable one.

Primary Moat Assessment: YETI is fundamentally a brand business. Its competitive advantage rests not on technology, scale, or network effects but on the emotional connection between the brand and its customers. The durability of this moat depends on YETI's ability to maintain brand relevance, cultural cachet, and the perception of authenticity — a task that requires constant investment and creative renewal.

XIII. Bull vs. Bear Case

The Bull Case

The optimistic thesis for YETI rests on several interlocking arguments. First, the brand moat has proven remarkably durable through nearly two decades of competition, copycats, and market cycles. Despite the flood of alternatives — from budget Ozark Trail tumblers to viral Stanley Quenchers — YETI has maintained its premium pricing and grown revenue from $779 million at the IPO to $1.87 billion without a single year of revenue decline. The brand has survived the ultimate test: it works even when consumers have abundant cheaper alternatives.

Second, international expansion represents genuine early innings. With more than 80% of revenue still coming from the United States, the opportunity to replicate the domestic playbook in Canada, Australia, Europe, and Japan is substantial. International sales are already growing at 16-25% annually, and the company has barely begun to invest in localized marketing, retail presence, and distribution partnerships outside North America. The outdoor lifestyle is global, and YETI's brand attributes — quality, durability, authenticity — translate across cultures.

Third, product category expansion continues to extend the addressable market. The 2024 acquisitions of Butter Pat Industries and Mystery Ranch signal ambition beyond coolers and drinkware. Cast iron cookware, technical backpacks, and potentially apparel represent categories where the YETI brand could command premium pricing. Each new category leverages existing brand equity, distribution infrastructure, and customer relationships.

Fourth, the DTC channel provides both margin expansion and strategic control. With DTC sales exceeding $1 billion and representing roughly 60% of revenue, YETI has reduced its dependence on wholesale partners and captured the higher margins that come with direct customer relationships. The e-commerce infrastructure is mature and scalable.

Fifth, durability as a product philosophy aligns with secular sustainability trends. The "buy it for life" positioning resonates with consumers who are increasingly conscious of waste and environmental impact, providing a values-based justification for the premium price.

Finally, strong cash generation — $212 million in free cash flow in fiscal 2025 — supports both reinvestment and shareholder returns. The company repurchased nearly $300 million in stock during fiscal 2025, demonstrating financial discipline and confidence in intrinsic value.

The Bear Case

The skeptical thesis raises equally valid concerns. Market saturation in core categories is real: how many coolers and tumblers can one household own? The U.S. market may be approaching a ceiling where growth depends on taking share rather than expanding the category, and taking share gets harder as competitors improve.

Competition has intensified, not abated. Stanley's viral success demonstrated that brand loyalty in drinkware is more fragile than YETI investors assumed. A single TikTok moment can shift consumer attention and purchasing patterns faster than traditional brand-building can respond. If a new competitor captures the next viral moment, YETI's premium positioning provides no defense.

Economic sensitivity is a structural vulnerability. YETI products are discretionary luxury goods for most buyers. In a recession, the $40 tumbler is one of the first things a squeezed consumer can easily trade down to a $10 alternative. The company's 1.77 beta — meaning the stock moves nearly twice as much as the market — reflects this cyclicality.

The commoditization question looms large: functional parity between YETI and alternatives at one-fifth the price puts enormous pressure on the brand premium. If that premium erodes — through generational shifts in consumer values, economic pressure, or brand fatigue — the impact on margins would be severe. The 57% gross margin is a signal of pricing power, but it also paints a target on the company's back.

International growth, while promising, remains unproven at scale. Outdoor culture varies significantly across markets, and the American outdoor identity that underpins YETI's brand may not translate as naturally to European or Asian consumers. The company will need to invest heavily in localized marketing and distribution, and returns on that investment are uncertain.

Wholesale dependence, while declining, still represents roughly 40% of revenue. These partnerships involve margin pressure and limited control over the brand experience. And with YETI exiting channels like Lowe's, the company is betting that DTC growth will more than offset any lost wholesale volume.

The KPIs That Matter

For investors tracking YETI's ongoing performance, two metrics stand above all others:

-

DTC revenue growth rate — This is the single most important indicator of brand health and margin trajectory. DTC sales carry higher margins than wholesale, provide direct customer data, and reflect genuine consumer demand unmediated by retail partner decisions. Sustained double-digit DTC growth signals that the brand remains vibrant; deceleration would be an early warning of brand fatigue or competitive displacement.

-

Gross margin percentage — YETI's 57%+ gross margins are the financial expression of its brand premium. Any sustained compression in gross margins would signal that the company is losing pricing power — whether through competitive pressure, input cost inflation, or the need to discount. Conversely, margin stability or expansion in the face of competition validates the brand moat thesis.

XIV. Key Lessons & Playbook

For Founders: What YETI Teaches About Building a Premium Brand

The first and most important lesson is that product quality can be the marketing strategy. The Seiders brothers did not build YETI through advertising; they built it through a product so demonstrably superior that customers became evangelists. In a world saturated with marketing noise, a product that genuinely delivers on its promise cuts through more effectively than any campaign. The bear-proof videos, the ice retention challenges, the testimonials from professional guides — none of this would have worked if the cooler had been mediocre. Premium positioning starts with premium performance.

The second lesson is about community architecture. YETI built its ambassador program around authenticity rather than reach. The company selected community leaders — the fishing guide everyone respects, the rodeo cowboy who actually rides — and gave them products rather than paychecks. This created a marketing ecosystem that was credible because it was real, and it proved durable because it was built on genuine relationships rather than transactional influencer deals. The two-year vetting process for ambassadors is the kind of discipline that separates enduring brands from flash-in-the-pan trends.

The third lesson concerns pricing as positioning. By launching at $300+ in a market where $30 was standard, YETI did not just set a high price — it created a new category. Premium pricing signaled premium quality, attracted customers who valued quality over price, and created an aspirational dynamic that cheaper alternatives could not replicate. The conventional wisdom says you compete on price or differentiation; YETI proved that price can be the differentiation.

The fourth lesson is about knowing when to bring in professional management. Roy and Ryan Seiders were brilliant at creating the brand, but they recognized that scaling it required capabilities they did not have. The Cortec partnership and the hiring of Matt Reintjes brought operational discipline, supply chain expertise, and strategic vision that transformed a regional success story into a national platform. The brothers' willingness to step back from day-to-day management — while maintaining their influence on brand and product — was a mark of maturity that many founders struggle to achieve.

The fifth lesson is about content as brand equity. YETI Presents — the documentary film series that deliberately avoids showing or mentioning the product — represents a radical approach to brand building. By investing in high-quality storytelling about the outdoor lifestyle, YETI created an emotional connection with consumers that goes far deeper than product features. The Pretty Wild Fellowship, with its $200,000 in documentary grants, elevates this approach to patronage. Not every company can or should invest this way, but for brands built on identity and lifestyle, content is not a marketing expense — it is the product.

For Investors: What YETI Reveals About Consumer Brand Investing

Brand moats are real but they require constant maintenance. YETI's brand has proven durable through competition, copycats, and market cycles, but it has required continuous investment in content, community, product innovation, and distribution management. A brand is not a patent that sits on a shelf; it is a living asset that depreciates if neglected.

Consumer behavior change creates investment opportunities, but distinguishing permanent shifts from temporary spikes is the critical challenge. The pandemic-era boom inflated expectations that the company spent two years normalizing. The lesson is not that outdoor spending was a bubble — it was not — but that the rate of change during the pandemic was unsustainable, and investors who extrapolated those growth rates were bound to be disappointed.

Beware the paradox of premium ubiquity. When a brand designed to signal exclusivity becomes universally popular, it risks losing the very quality that made it premium. YETI has managed this tension better than most, but the Stanley phenomenon — and the broader "dupe" culture on TikTok — suggests that younger consumers may not value brand loyalty the way their predecessors did. Investors should watch for signs that YETI's customer base is aging without being replenished.

Margin sustainability is never guaranteed. YETI's 57%+ gross margins are extraordinary for a consumer products company and invite both admiration and concern. Competitors see those margins and view them as an opportunity to undercut on price while still earning attractive returns. The margin is justified only as long as the brand premium holds, and the brand premium holds only as long as consumers perceive YETI as meaningfully different from alternatives. It is a circular logic that works beautifully when the brand is strong and collapses rapidly when it weakens.

Strategic Principles

Create categories, do not just enter them. YETI did not compete in the existing cooler market; it created the premium cooler market. This is a fundamentally different strategic act that allows the creator to set the rules, define the price points, and establish the brand associations.

Distribution strategy shapes brand perception. Where a product is sold communicates as much as any advertisement. YETI's deliberate exclusion from mass-market retailers like Walmart — even as competitors flooded those channels — preserved the premium positioning that justified the premium price.

Protect intellectual property aggressively. The RTIC lawsuit was expensive and distracting, but the settlement — which forced a competitor to redesign its entire product line — sent a clear message to the market and preserved YETI's competitive position. Companies that fail to defend their IP invite unlimited imitation.

XV. Recent Developments & Future Outlook (2024-2026)

The current chapter of the YETI story is defined by a tension between proven brand strength and uncertain growth trajectory. Fiscal 2025 delivered $1.87 billion in revenue — a modest 2% increase over the prior year that fell short of the double-digit growth rates investors enjoyed during the pandemic era. The company guided for 6-8% sales growth in fiscal 2026, a target that would put revenue near the $2 billion milestone but represents a pace that many growth investors find insufficient for the premium valuation.

International momentum provides the most compelling growth vector. The Q4 2025 results showed international sales growing 25%, with strength across Canada, Australia, and the United Kingdom. Australia delivered its strongest quarter ever. The company is unlocking the DACH region in Continental Europe and building early-stage traction in Japan. Management's medium-term target of lifting international mix to 20-25% of sales, up from roughly 21% in fiscal 2025, implies continued above-average growth outside North America.

The supply chain transformation is both a challenge and an opportunity. With tariffs on Chinese imports reaching as high as 145%, YETI has accelerated its manufacturing diversification. The company targets producing more than 90% of drinkware outside China by the end of 2025, with key suppliers ramping capacity in Thailand and Malaysia. The goal is to reduce China-sourced U.S. product costs to below 5% of total. If achieved, this would substantially insulate the business from further tariff escalation, but the transition itself involves execution risk and potential short-term cost inflation.

Product innovation continues to expand the brand's reach. The Mystery Ranch and Butter Pat acquisitions position YETI in technical backpacks and premium cast iron cookware — categories that align with the "built for the wild" brand identity and address the overlanding and high-end camping markets. Whether these acquisitions prove to be strategic accelerants or expensive distractions will depend on YETI's ability to integrate the brands and leverage its distribution and marketing capabilities.

The competitive landscape demands ongoing vigilance. Stanley's viral moment may or may not prove durable, but it demonstrated that consumer attention in drinkware can shift rapidly. The proliferation of "dupes" — affordable alternatives promoted through social media — continues to pressure the premium price point, particularly among younger consumers. YETI's response has been consistent: stay true to the brand, invest in quality and content, and refuse to compete on price. Whether that discipline will prove sufficient against evolving consumer preferences remains the central open question.

The share repurchase activity — $297.6 million in fiscal 2025 following $200 million in fiscal 2024 — reflects management's conviction that the stock is undervalued relative to intrinsic value. With the share count declining from 87 million to 81 million over the past few years, these buybacks provide meaningful per-share earnings growth even in a period of modest revenue expansion.

As YETI approaches its twentieth anniversary in 2026, the company finds itself at an inflection point. The brand is stronger than ever — gross margins above 57%, a growing international footprint, a DTC business exceeding $1 billion, and a product portfolio that extends well beyond the original cooler. But the growth challenges are equally real: domestic market saturation, intensifying competition, tariff uncertainty, and the eternal question of whether a premium brand can maintain its magic at scale.

XVI. Epilogue & Reflections

What makes YETI remarkable is not the cooler. It is the brand — and the systematic, disciplined, patient process by which it was built. Roy and Ryan Seiders started with a simple insight: existing coolers were not good enough for serious outdoor professionals. They built a product that solved that problem with overwhelming force — a cooler so overbuilt it could survive a grizzly bear. And then they spent nearly two decades extending that reputation for uncompromising quality into adjacent categories, new geographies, and new customer segments without ever sacrificing the premium positioning that made the brand valuable in the first place.

The Seiders brothers' legacy is that of two outdoorsmen — not MBAs, not marketers, not technologists — who understood their customer so deeply that they could build a product the customer did not know they needed and charge ten times what anyone thought reasonable. They then had the wisdom to partner with Cortec and hire Matt Reintjes to professionalize the business, preserving the brand's soul while scaling its operations. That combination of founder authenticity and professional execution is rare and accounts for much of YETI's success.

What is most surprising about the YETI story is how sustainable the premium positioning has proven to be. In theory, a product with no patented technology, no network effects, and no meaningful functional differentiation from competitors priced at 80% less should not be able to maintain a 57% gross margin for nearly a decade as a public company. And yet YETI has done exactly that. The brand premium has not merely survived competition — it has strengthened through it, because each competitor that enters the market validates the category that YETI created and serves as a foil against which YETI's quality and identity stand out.

The open question is whether the brand magic can persist for another twenty years. History suggests that premium consumer brands can endure for generations — Patagonia, founded in 1973, remains the gold standard for outdoor apparel. Lululemon, founded in 1998, has grown from yoga pants to a global athletic lifestyle brand. Apple, of course, has demonstrated that brand premium and functional parity can coexist indefinitely. But history also offers cautionary tales: brands that became too ubiquitous, too diluted, or too associated with a generation that aged out of cultural relevance.

YETI's future depends on its ability to remain relevant to new generations of consumers while staying true to the outdoor authenticity that built the brand. It must expand internationally without losing the American identity that resonates in domestic markets. It must innovate in new categories without overextending the brand. And it must navigate a competitive landscape where social media can create — and destroy — brand momentum faster than any time in history.

The bigger story that YETI tells is about the power of brand as a competitive advantage in a world where products are increasingly commoditized. When anyone can manufacture a vacuum-insulated tumbler, the company that wins is not the one with the best insulation — it is the one that makes customers feel something when they pick up the product. YETI makes people feel like they belong to a tribe of people who value quality, authenticity, and the outdoors. That feeling, more than any rotomolded construction or double-wall vacuum insulation, is what justifies the premium price and powers the business.

Whether that feeling proves to be a durable competitive advantage or a fading cultural moment is the question that will determine YETI's next chapter. The evidence so far — nearly two decades of consistent brand building, expanding margins, and growing revenue — suggests the former. But in consumer markets, nothing is guaranteed except that the market will keep testing you.

XVII. Further Reading & Resources

Top 10 Long-Form References:

- "Built for the Wild" by YETI — the company's own brand book and founding story, available through YETI's corporate storytelling archives

- YETI IPO S-1 Filing (October 2018) — SEC filings providing a comprehensive deep dive into the business model, risk factors, and financial history at the time of the public listing

- Harvard Business Review: "How YETI Made a Cooler a Status Symbol" — a brand strategy case study examining the premium positioning playbook

- Outside Magazine: "The YETI Effect" — cultural impact analysis of how YETI transformed the outdoor industry and aspirational outdoor culture

- Forbes: "The Seiders Brothers Built YETI" — detailed founder profiles covering Roy and Ryan's backgrounds, origin story, and early strategic decisions

- Wall Street Journal: "YETI vs. RTIC: The Cooler Wars" — investigative reporting on the intellectual property litigation and competitive dynamics

- Modern Retail: "YETI's DTC Strategy" — analysis of the digital transformation and e-commerce channel that now drives more than half of total revenue

- YETI investor presentations and quarterly earnings calls (2018-2026) — the evolving strategic narrative as told by management to Wall Street

- "The Luxury Strategy" by Kapferer and Bastien — academic framework for understanding premium brand theory, directly applicable to YETI's pricing and positioning strategy

- Equity research from Baird, Piper Sandler, and other sell-side analysts — institutional perspectives on competitive positioning, valuation, and growth outlook

Additional Resources:

- YETI Presents documentary film series (75+ films available at yeti.com/films) — the company's content marketing in action

- Podcast interviews with Roy and Ryan Seiders — firsthand accounts of the founding story and brand philosophy

- Consumer sentiment analysis and NPS surveys tracking brand perception over time

- Cortec Group case study materials on the YETI investment — one of the most successful PE returns of its era

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube