Xylem: The Operating System of Global Water

I. Introduction and Episode Roadmap

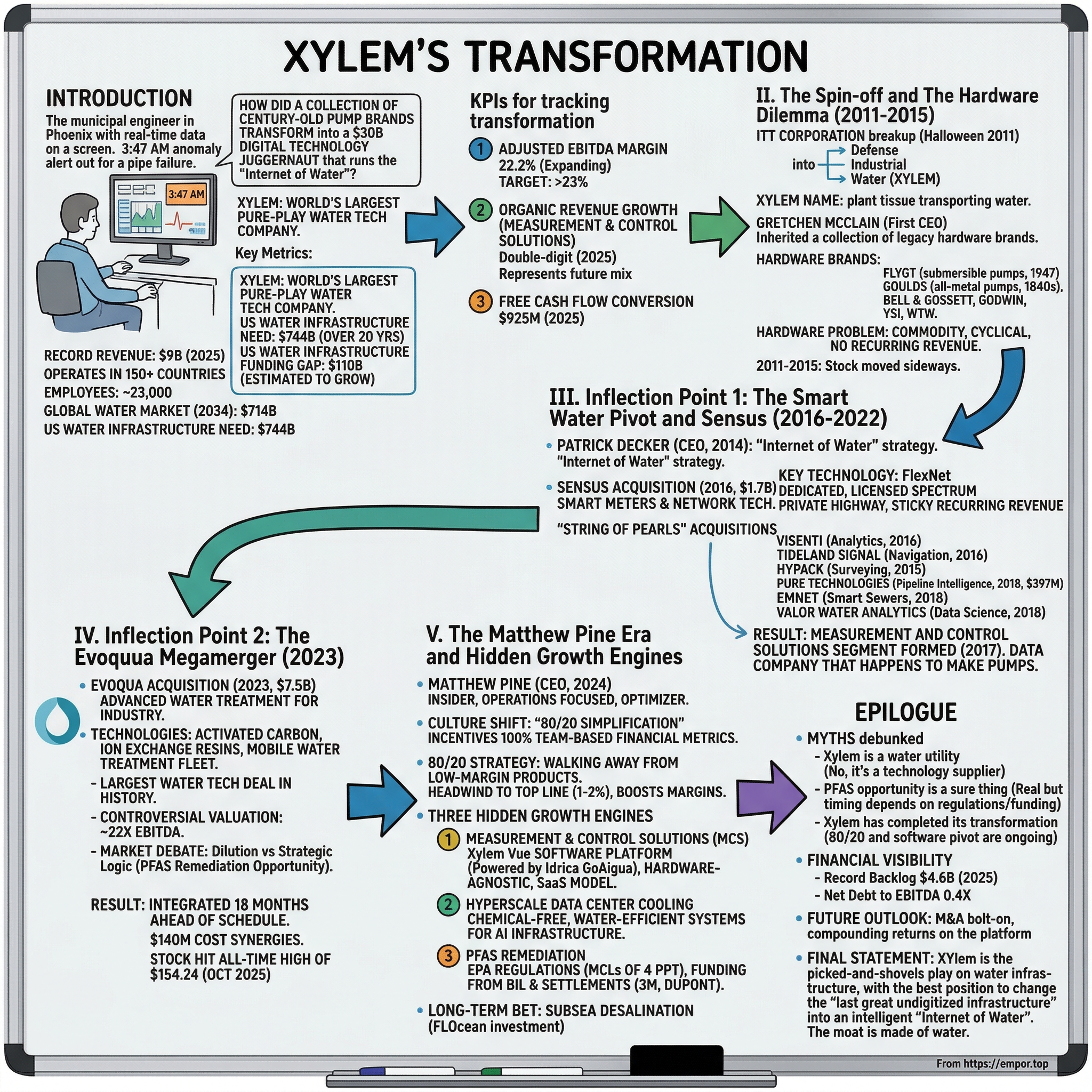

Picture a municipal water engineer in Phoenix, Arizona, staring at a screen full of real-time data. Pressure anomalies detected at 3:47 AM. A buried pipe, installed when Eisenhower was president, is about to fail. The system flags it, reroutes flow, and schedules a crew -- all before a single drop is wasted. The software running that operation? Built by a company most people have never heard of. A company that, fifteen years ago, was a collection of century-old pump brands orphaned from a defense conglomerate.

That company is Xylem.

Here is the question at the center of this story: How does a spun-out hardware division selling century-old pump brands transform into a thirty-billion-dollar digital technology juggernaut that essentially runs the "Internet of Water"? The answer involves one of the most aggressive corporate transformations in modern industrial history -- a pivot so complete that the company's own founding CEO could barely recognize the business a decade later.

The scale of what Xylem has become is staggering. It is the world's largest pure-play water technology company. Its equipment pumps cooling water through AWS hyperscale data centers running AI workloads. Its sensors track PFAS -- the so-called "forever chemicals" -- in your municipal water supply, down to four parts per trillion. Its software platform, Xylem Vue, allows utilities to manage data from any connected device, even competitors' hardware.

The company posted record revenue of nine billion dollars in 2025, operates in over 150 countries, and employs roughly 23,000 people.

To put that in perspective: the global water and wastewater treatment market was valued at approximately $372 billion in 2025 and is projected to reach $714 billion by 2034. The broader water technology market, including infrastructure, piping, and consulting, stretches to $600 billion or more. The EPA estimates the United States alone needs over $744 billion in water infrastructure investment over the next twenty years.

And here is the critical fact: the country faces a $110 billion funding gap in water infrastructure that is expected to grow to $194 billion by 2030. Most American water systems were built more than fifty years ago and are reaching the end of their design lifespan. This is not a growth story built on hype. It is built on physics, chemistry, and the relentless decay of iron and concrete buried underground.

But this story is not about ancient history. The nineteenth-century water wheels, the earliest cast-iron pumps -- that is fascinating backstory, but it is not the narrative that matters to investors.

This is a story of modern corporate transformation: a 2011 spin-off that left the company naked and exposed, aggressive and highly debated mega-acquisitions that the market initially despised, a painful pivot from selling metal to selling software, and a new management team led by CEO Matthew Pine that is relentlessly pruning the business to drive massive margin expansion. Along the way, there is a debate about whether Xylem paid way too much for its biggest deal, a regulatory tsunami that may be the greatest forced-spending event in American water history, and the strange convergence of artificial intelligence and water that nobody saw coming.

Before diving in, a note on the three KPIs that matter most for tracking this business going forward.

First: adjusted EBITDA margin, currently at 22.2% and expanding rapidly under the 80/20 simplification strategy, with a long-term target above 23%. This number tells you whether the shift from low-margin hardware to high-margin digital solutions is working.

Second: organic revenue growth in the Measurement and Control Solutions segment, the digital heart of the company, which grew at double-digit rates in 2025 and represents the future earnings mix.

Third: free cash flow conversion, which in 2025 came in at $925 million.

These three numbers, taken together, tell you whether the transformation from pump company to infrastructure intelligence platform is real or aspirational.

Let us start at the beginning -- or rather, at the moment of separation.

II. The Spin-off and The Hardware Dilemma (2011-2015)

On October 31, 2011 -- Halloween, fittingly -- ITT Corporation carved itself into three pieces. It was corporate surgery that had been years in the making, and to understand why it happened, you have to understand what ITT had become.

ITT Corporation was one of the great American industrial conglomerates, with roots stretching back to 1920 when Sosthenes Behn founded the International Telephone and Telegraph Corporation to build telephone systems in Cuba and Puerto Rico. Over the following decades, ITT became a sprawling empire under the legendary (and controversial) CEO Harold Geneen, who in the 1960s and 1970s acquired hundreds of companies across industries from hotels (Sheraton) to baking (Continental Baking, maker of Wonder Bread) to insurance (Hartford Financial Services).

By the time the conglomerate era ended and the breakup wave of the 1990s hit, ITT had been slimmed down dramatically. The version of ITT that existed in 2011 was a much more focused industrial company, but it still straddled three distinct businesses that the market could not cleanly value: defense electronics, industrial motion technology, and water infrastructure.

The logic for the breakup was the same logic that drove every great conglomerate divorce of the era: each business would be better off independent, with its own balance sheet, its own management team, its own investor base, and its own strategic focus.

The defense business became ITT Exelis (later acquired by Harris Corporation). The industrial pumps, valves, and connectors stayed with the legacy ITT Inc. And the water division -- the business that moved, treated, and tested water -- was spun out under a peculiar new name.

Xylem. Named after the tissue in plants that transports water from roots to leaves. It was the kind of name that a branding consultant would love and a sell-side analyst would struggle to spell. The company's logo featured a stylized water droplet. Wall Street was not quite sure what to make of any of it.

Gretchen McClain, a chemical engineer by training who had risen through ITT's ranks, became Xylem's first president and CEO. On November 1, 2011, she stood on the floor of the New York Stock Exchange as XYL began trading. Two weeks later, on November 16, she rang the opening bell. The company she inherited was no startup. It had $3.2 billion in 2010 revenue, 12,000 employees, and operations spanning more than 150 countries. It was immediately added to the S&P 500. By any measure, this was a fully formed industrial enterprise.

But what exactly was Xylem? At its core, the company was a collection of legendary hardware brands, each with its own storied history.

The crown jewel was Flygt, born in the small Swedish town of Emmaboda, where Per Alfred Stenberg established a foundry in 1901. The real breakthrough came in 1947, when Sixten Englesson, the company's chief engineer, stood in a dark suit holding the frame of what colleagues nicknamed the "Parrot Cage" -- the prototype of the world's first submersible drainage pump.

Englesson's genius was elegantly simple: protect the motor with two mechanical flat seals and cool it using the very water being pumped. The Flygt B-pump hit the market in 1948 and changed the industry forever. By 1956, Flygt had unveiled the first submersible sewage pump, and the brand became synonymous with moving water underground.

Then there was Goulds, whose roots ran even deeper into American industrial history. In 1840, Abel Downs began manufacturing wooden pumps in a former cotton factory in Seneca Falls, New York -- the same town that would host the first women's rights convention eight years later. Seabury S. Gould, a local metalworker, oversaw the casting and assembling of the world's first all-metal pump in the mid-1840s. The company that bore his name survived the Civil War, two World Wars, and multiple corporate owners before landing inside Xylem's portfolio.

Other brands in the stable included Bell and Gossett (commercial HVAC pumps), Lowara (European high-efficiency pumps), Godwin (portable dewatering), and YSI and WTW (water quality analytics).

The problem was simple and existential: these were all hardware businesses. Metal, motors, and machining. If you just sell pumps -- no matter how storied the brand -- you are a commodity. When times are good, utilities buy pumps. When budgets get tight, they defer purchases. There is no recurring revenue in selling a piece of iron that lasts thirty years. The stock market understood this immediately. Xylem was classified as an industrial cyclical, valued accordingly, and largely ignored by growth investors.

In its first full year as an independent company, Xylem generated $3.8 billion in revenue. The market cap hovered around $5 billion. The company was profitable, paying a dividend, and deeply boring. The stock moved sideways for years, trading in the $25 to $35 range from 2012 through 2015, essentially going nowhere while the broader market rallied. For context, the S&P 500 returned roughly 70% over that same period. Xylem shareholders were left standing on the platform watching the train pull away.

The challenge was structural. Water utilities are among the most conservative institutions in the American economy. They operate critical infrastructure that cannot fail. They are governed by public commissions that scrutinize every dollar of capital expenditure. Their procurement cycles can stretch to years. And their technical staff often prefer equipment they know and trust over anything novel.

Selling into this market requires patience, relationships, and a willingness to invest in long sales cycles with uncertain outcomes. It also means that once you win a customer, you tend to keep them -- but only if your product is differentiated enough that switching is painful.

Inside the company, the strategic conversation was evolving. The early insight -- one that would define the next decade -- was that moving water was not enough. Utilities did not just need pumps. They needed to understand what was happening in their networks. Where was the water leaking? How much energy were the pumps consuming? When would a buried pipe fail? The answers to those questions were worth far more than the hardware that moved the water. The trajectory had to change.

Consider the magnitude of the problem Xylem was staring at. American water systems lose an estimated six billion gallons per day to leaks. Six billion. That is enough to supply the daily water needs of roughly forty million people, vanishing underground through cracks in aging pipes because nobody can see it. The industry calls this "non-revenue water" -- water that is treated, pumped, and distributed at enormous expense, then lost before it ever reaches a paying customer. Globally, the non-revenue water problem represents a trillion-dollar opportunity. And the only way to solve it is data: knowing in real time where every drop of water is, how fast it is moving, and where it is being lost.

In 2014, Patrick Decker arrived as CEO, replacing McClain. Decker came from Hanes Brands and had deep experience in brand management and corporate transformation. He was not a water industry lifer. He was a change agent, brought in specifically because the board recognized that Xylem's future could not look like its past. Decker looked at Xylem's portfolio of century-old hardware brands and saw not a museum -- but a platform onto which an entirely new digital business could be built. He described Xylem's strategy as "making a number of acquisitions to build out a portfolio of truly smart water solutions." He began talking about the "Internet of Water" in investor presentations, drawing explicit parallels to the Industrial Internet of Things transformation happening at companies like GE and Honeywell.

The question was how. And the answer, it turned out, would come from Raleigh, North Carolina.

III. Inflection Point 1: The Smart Water Pivot and Sensus (2016-2022)

Walk into the control room of a typical American water utility in 2015, and what you would have found was surprisingly primitive. Paper maps of pipe networks. Manual meter readings taken once a month by a person walking from house to house. Maintenance schedules based on calendar time rather than actual equipment condition. If a pipe burst, the first sign was often a customer calling to report a flooded street.

The digital revolution that had transformed banking, logistics, telecommunications, and manufacturing had barely touched the water sector.

The reasons were understandable. Water utilities are public entities funded by rate-paying customers and bond markets. They operate on thin margins. Their capital budgets are scrutinized by elected officials. And their workforce tends to be experienced, practical, and skeptical of technology promises from outsiders.

But the consequences of this technology gap were becoming impossible to ignore. Water main breaks were increasing. Energy costs for pumping were rising. Aging infrastructure was failing at accelerating rates. And new regulations around water quality were demanding levels of monitoring and reporting that manual processes simply could not deliver.

Patrick Decker understood that the company that could make water infrastructure visible -- that could turn dumb pipes into smart networks -- would command entirely different economics than a pump manufacturer. Software margins, recurring revenue, customer lock-in. The playbook was not new. It was the same playbook that transformed industrial companies from John Deere to Honeywell. But in water, nobody had executed it at scale. The industry was fragmented, conservative, and deeply resistant to change. Which also meant that whoever moved first would have the field largely to themselves.

On August 15, 2016, Xylem announced its first transformational acquisition: Sensus, purchased for $1.7 billion in cash. The deal closed on October 31, 2016 -- exactly five years after the ITT spin-off, a symmetry that felt almost poetic.

What did Sensus bring? At the surface level, it was a provider of smart meters and network technologies serving water, electric, and gas utilities, with more than 80 million metering devices installed globally and approximately 3,300 employees across the United States, United Kingdom, Germany, Slovakia, and China. The revenue was solid -- $837 million in adjusted revenue for the fiscal year ending March 2016, with $159 million in adjusted EBITDA.

But the real prize was FlexNet. And to understand why FlexNet matters so much, you need a brief primer on how utility communication networks work.

When a water utility wants to read a meter remotely -- to know how much water a household or business is using without sending someone to physically look at the dial -- it needs a way for that meter to communicate its data back to a central system. There are broadly two approaches. The first is to piggyback on existing cellular networks, using the same airwaves that carry your smartphone calls and data. This is cheap but unreliable: cellular networks get congested, signal quality varies, and the utility is at the mercy of a third-party carrier's infrastructure decisions. The second approach is to build a dedicated, purpose-built communication network on licensed spectrum -- radio frequencies that the FCC has allocated specifically for this use, where nobody else's traffic can interfere.

FlexNet is Sensus's proprietary point-to-multipoint radio frequency communication network, and it takes the second approach to an extreme degree. It operates on licensed, dedicated spectrum in the United States -- the only FCC-licensed proprietary bandwidth serving water, gas, and electric utilities. Think of it as a private highway while everyone else is stuck in traffic on the public interstate. No interference. No congestion. No dependence on a cellular carrier's business decisions.

The network enables near real-time, two-way communication between utilities and their smart meter endpoints. Smart meters transmit usage data to local base stations, which relay data to management systems for analysis and billing.

Crucially, Sensus had deployed a unique business model: it took on the upfront capital costs of designing and building the network, and the utility then leased it as it connected devices. This meant the utility did not need to make a massive capital outlay to get started -- they could roll out the network incrementally, connecting meters over time.

For Xylem, this created sticky, recurring revenue streams that looked far more like a software-as-a-service business than a traditional industrial equipment sale. Once a utility was on FlexNet, the ongoing lease payments created a predictable revenue base that would persist for years, even decades.

Did Xylem overpay? At 10.7 times Sensus's fiscal year adjusted EBITDA, the market actually loved the deal. Xylem shares rose approximately 3% on the announcement -- an unusual response for an acquirer in a major deal. The multiple was reasonable by industrial acquisition standards, and the deal was immediately expected to be accretive to adjusted earnings in 2017, with at least $50 million in annual cost synergies within three years.

But Sensus was just the beginning. Decker described the company's acquisition strategy as building a "string of pearls" -- each deal adding a specific capability to what was becoming a comprehensive digital water platform.

In November 2016, Xylem acquired Visenti, a Singapore-based smart water analytics company spun out of MIT's SMART research program. Visenti brought real-time leak detection, pipe failure prediction, and water quality monitoring -- the analytical brain to complement FlexNet's communication backbone. In February 2016, Tideland Signal Corporation was acquired for $69 million, adding marine navigation and signaling technologies. In November 2015, Hypack brought hydrographic survey and mapping software.

Then came two deals in early 2018 that completed the foundation. In December 2017, Xylem announced the acquisition of Pure Technologies for approximately $397 million (CAD $509 million), closing in the first quarter of 2018. Pure was a Calgary-based leader in intelligent leak detection and condition assessment for buried pipelines. The premium was massive -- 102.7% above Pure's closing price -- reflecting the strategic value of predictive pipeline intelligence. At roughly 17 times estimated EBITDA (or 11 times including synergies), the price was justifiable because Pure solved a trillion-dollar problem: non-revenue water loss from aging infrastructure that utilities could not see.

Almost simultaneously, in February 2018, Xylem acquired EmNet, whose technology could be described as the brains of a smart sewer system. EmNet installed sensors and actuators across sewer networks that communicated with each other in real time. If a rainwater line was reaching capacity during a storm, the system could identify other pipes to which runoff could be diverted -- turning a dumb gravity-fed sewer into an intelligent, actively managed network. The proof of concept was in South Bend, Indiana, where the technology saved more than one billion gallons of overflow from entering the St. Joseph River annually and generated nearly $450 million in savings for the city. The technology had been originally developed at the University of Notre Dame.

Decker also acquired Valor Water Analytics in February 2018, a Silicon Valley startup previously backed by Y Combinator and 500 Startups, to spearhead advanced data science initiatives from a new West Coast innovation hub.

In 2017, Xylem combined its analytics business with the Sensus and Visenti acquisitions into a newly formed "Measurement and Control Solutions" segment -- giving organizational structure and investor visibility to the digital strategy. This was not just accounting reclassification. It was a declaration: Xylem was no longer just a pump company. It was a data company that happened to make pumps.

The financial results validated the thesis. By the end of the string-of-pearls era, Xylem's Measurement and Control Solutions segment was growing at double-digit rates organically, outpacing the legacy hardware businesses and commanding premium margins.

The installed base of FlexNet networks, once deployed, created switching costs that would prove essentially insurmountable. Consider what it would take for a city like Fort Worth -- which built its entire water management operation around Xylem's AMI system and reduced field investigations by 90% -- to switch to a competitor. They would need to replace every smart meter, every base station, every communication node. Retrain every operator. Re-integrate every back-office system.

The cost would be staggering, the operational risk enormous, and the political consequences for any utility manager who proposed it would be career-ending. This is the beauty of infrastructure-grade switching costs: they are not just financial, they are institutional.

The string-of-pearls strategy also revealed Decker's intellectual framework. He was not randomly acquiring technology companies. Each acquisition filled a specific gap in what was becoming a full-stack digital water platform.

FlexNet provided the communication layer. Smart meters provided the sensing layer. Pure Technologies provided the diagnostic layer. EmNet provided the decision-making layer. Valor Water Analytics provided the customer intelligence layer. Visenti provided the network optimization layer.

Stack them together, and you had something no competitor could match: an end-to-end system for making water infrastructure intelligent. The whole was worth far more than the sum of the parts.

But even this was not enough for Decker. There was still a massive gap in Xylem's capabilities -- one that would require the biggest, most controversial bet of his career to fill.

IV. Inflection Point 2: The Evoqua Megamerger (2023)

To understand why the Evoqua deal was so audacious, you first need to understand what Evoqua was. Before it became a publicly traded company in 2017, Evoqua's water treatment business had been part of Siemens, which sold it to the private equity firm AEA Investors in 2014. AEA took the business public three years later under the ticker AQUA. Evoqua specialized in something very different from Xylem's heritage: advanced water treatment for industrial customers. Where Xylem moved water through pipes and monitored it with sensors, Evoqua purified it, decontaminated it, and made it safe. Its customers ranged from semiconductor manufacturers requiring ultrapure water to food and beverage companies to pharmaceutical plants -- industries where water quality is not just a regulatory box to check but a critical input to the manufacturing process itself.

Evoqua's crown jewels were its treatment technologies: granular activated carbon systems that could strip organic contaminants from water, ion exchange resins that could selectively remove specific chemicals like PFAS and perchlorate, and electrochlorination systems that could disinfect water without hauling chlorine trucks. The company served more than 38,000 customers across 200,000 installations worldwide. But perhaps its most strategic asset was its North American service fleet -- one of the nation's largest mobile water treatment operations, with regeneration facilities strategically located to serve emergency and ongoing treatment needs. This was "water treatment on wheels."

On January 23, 2023, Xylem announced it would acquire Evoqua in an all-stock transaction valued at approximately $7.5 billion. Evoqua shareholders would receive 0.48 shares of Xylem for each Evoqua share, representing roughly $52.89 per share -- a 29% premium over Evoqua's closing price. When the dust settled, Xylem shareholders would own approximately 75% of the combined entity, Evoqua shareholders 25%. The combined company would generate over $7 billion in annual revenue and $1.2 billion in adjusted EBITDA.

This was the largest water technology deal in history. And the market hated it.

Xylem shares plunged as much as 11.7% on the announcement. Evoqua shares soared 13.9%. This is the classic pattern of a deal where the market believes the acquirer overpaid -- value transferring from buyer to seller in real time. CEO Patrick Decker's stated rationale was grand: "Solving the world's water challenges has never been more urgent. Our acquisition of Evoqua creates a transformative global platform to address water scarcity, affordability, and resilience at even greater scale." Wall Street analysts were less moved by the poetry.

The valuation multiples were eye-watering. Xylem was paying approximately 22 times Evoqua's estimated fiscal year 2023 EBITDA -- nearly double the S&P 500's trading multiple at the time. On a forward earnings basis, the multiple stretched to roughly 47 times. Evoqua had generated only $75.5 million in GAAP net income and $50.8 million in free cash flow in 2022.

For context, conservative water peers like Badger Meter had achieved extraordinary returns through disciplined organic growth and targeted bolt-on acquisitions, never paying anything close to 22 times EBITDA. Pentair focused on niche dominance in residential and commercial markets with smaller, tightly scoped deals. The Evoqua price tag was in a different universe.

To frame the debate in capital allocation terms: Badger Meter, with a market cap of roughly $4.6 billion, had compounded shareholder returns at extraordinary rates by staying in its lane -- smart water metering -- and returning capital through buybacks when acquisitions did not meet its hurdle rate.

Pentair, at roughly $16 billion, had actually simplified its portfolio by spinning off its water treatment business (which became Evoqua's competitor Nuveen Water Solutions) and focusing on high-growth residential filtration. Both companies represented the "disciplined compounder" model.

Xylem's Evoqua bet was the opposite: swing big, pay a platform premium, and bet that scale in water technology would prove more valuable than niche dominance.

The analyst reaction was swift and divided.

Citi's Andrew Kaplowitz acknowledged "compelling strategic logic" -- the two companies' product and service offerings were genuinely complementary -- but said he was "not surprised to see Xylem shares trading off on the news because the deal will dilute the company's 2024 earnings."

Raymond James' Pavel Molchanov was blunter. He said that while he had wanted Xylem to make an acquisition, he "doesn't expect this combination -- the largest water technology deal ever -- is the right one." Molchanov pointed to high integration risk given the lack of business overlap, and the fact that the deal would not add to earnings in 2024.

Based on interviews, former Xylem executives called the valuation "crazy expensive" and "surprising," with one arguing that $200 million in cost synergies -- not the $140 million forecasted -- would be necessary to make the deal work.

So what was Decker thinking? Why pay a platform premium that made Wall Street's industrial analysts physically uncomfortable?

The answer is that Decker was not buying earnings. He was buying the missing piece of the puzzle -- and the timing window in which to buy it.

After the string-of-pearls acquisitions, Xylem could move water (pumps), monitor water (sensors and metering), and manage water networks (software). But it could not treat water at an advanced level. If a utility detected PFAS contamination through Xylem's monitoring equipment, it had to call someone else to fix the problem. That someone else was often Evoqua. Decker's logic was that the company controlling the complete water cycle -- from detection to treatment to ongoing management -- would own the customer relationship entirely and capture the full economic value of every drop.

There was also a timing dimension that is often overlooked. The EPA's PFAS regulations, while still being finalized in early 2023, were clearly coming. Decker could see that PFAS remediation would become a multi-billion-dollar mandatory spending event, and Evoqua's advanced carbon and ion-exchange technologies were precisely what utilities would need. If Xylem waited, another acquirer -- perhaps Veolia, perhaps a private equity consortium -- would grab Evoqua first. The "platform premium" was also a "now or never" premium.

Evoqua's service-based model was also strategically complementary in ways that are not obvious at first glance. Where Xylem sold capital equipment -- pumps, meters, sensors -- and collected revenue primarily at the point of sale, Evoqua generated substantial recurring revenue through service contracts, media replacement, and equipment rentals. Mobile demineralizer trailers, emergency response capability, ongoing carbon and resin regeneration. This blended the combined company's revenue mix toward more recurring, less cyclical streams -- exactly the earnings quality shift that investors pay premium multiples for.

The deal closed on May 24, 2023, and what happened next surprised almost everyone.

Xylem integrated Evoqua 18 months ahead of its original three-year plan. In the world of $7 billion-plus industrial mergers, completing integration early is vanishingly rare. The graveyard of industrial mega-mergers is vast: DuPont-Dow took years to untangle, GE's serial acquisitions under Jeff Immelt became case studies in integration failure, and Kraft-Heinz's famous "zero-based budgeting" destroyed brand value even as it cut costs. Most large acquisitions spend years wrestling with incompatible IT systems, clashing cultures, and organizational paralysis. Xylem defied this pattern.

The company delivered $140 million in run-rate cost synergies through procurement scale, network optimization, and elimination of redundant corporate functions. Restructuring and Evoqua synergies alone contributed 125 basis points to margin expansion in 2024. The speed of integration was driven in part by a deliberate organizational choice: rather than slowly merging business units over multiple years, Xylem created a clean new structure on day one.

Effective January 1, 2024, the company reorganized into four segments. Water Infrastructure housed the legacy transport and treatment businesses -- the Flygt and Godwin pumps that moved water through municipal and industrial systems. Applied Water contained the commercial building services and industrial pumping businesses -- Bell and Gossett, Lowara, Goulds. Measurement and Control Solutions held the digital crown jewels -- FlexNet, smart metering, Xylem Vue, and the analytics platforms. And the new fourth segment, Water Solutions and Services, unified Evoqua's treatment technologies with Xylem's dewatering and assessment services. Each addressed a distinct part of the water value chain, and together they constituted the most comprehensive water technology portfolio on the planet.

The financial proof came quickly. By the time Xylem reported its full-year 2025 results -- record revenue of $9.0 billion, adjusted EBITDA margins of 22.2% (up 330 basis points from two years prior), adjusted EPS of $5.08 (up 19%), net income of $957 million, and free cash flow of $925 million -- the narrative had decisively shifted. The Spruce Point Capital short report from August 2023, which had raised concerns about integration risk and accounting quality, had been largely refuted by operational execution. The "overpayment" was increasingly viewed as a masterstroke. Xylem had locked up a dominant position in a global market, and the integration execution had been cited as one of the best examples of a large-scale industrial merger in recent memory.

The stock market ultimately agreed. XYL shares hit an all-time high of $154.24 in October 2025 -- a remarkable recovery from the 11.7% plunge on the deal announcement less than three years earlier. Shareholders who bought Xylem on the day the Evoqua deal was announced and held through the all-time high captured roughly 50% total return, handsomely outperforming the S&P 500 over the same period.

But the strategic transformation was not yet complete. A new leader was about to take the helm with an entirely different mandate.

V. The Matthew Pine Era and the Hidden Growth Engines

Every great corporate transformation has two acts. The first act is visionary: the bold acquisitions, the strategic pivots, the grand declarations of a new future. The second act is operational: the grinding, unglamorous work of making everything actually function as an integrated whole. Patrick Decker was the architect of act one. Matthew Pine is the executor of act two. And in many ways, act two is where the real value creation happens.

On January 1, 2024, Pine became Xylem's third CEO. At 53, he was a company insider who had joined Xylem in 2020 and risen rapidly through the organization, serving as Chief Operating Officer and running both the Applied Water and Measurement and Control Solutions segments, as well as the entire Americas region. His pre-Xylem background was instructive: over 25 years of general management experience at United Technologies, Vestas Wind Systems, Lennox International, and Trane Residential. These are companies known for operational rigor, lean manufacturing, and systematic cost discipline. Pine's MBA from Northeastern University had a finance concentration -- he thinks in margins, returns on invested capital, and free cash flow conversion. In January 2025, he was appointed to the Board of Directors of Trane Technologies, and he sits on both the U.S. Business Roundtable and the World Economic Forum's Alliance of CEO Climate Leaders.

Where Decker was the dealmaker, Pine is the optimizer. Digest the Evoqua merger. Cut the fat. Drive margins. Simplify the portfolio. The era of transformational M&A was over. The era of execution had begun. And Pine's approach to execution is unusually systematic -- almost clinical in its precision.

Pine's incentive structure tells you everything about the culture shift. His 2024 total compensation was $10.58 million, of which 88% was performance-based. His $1.09 million base salary represented just over 10% of total comp -- the rest was tied directly to outcomes.

And those outcomes are unusually rigid. In 2025, Xylem moved its annual incentive plan to 100% team-based metrics. No individual qualitative goals. Zero. Every executive is paid based on three company-wide metrics: adjusted EBITDA margin, organic revenue, and adjusted free cash flow margin. Long-term incentive PSUs are tied to relative total shareholder return and adjusted cumulative EPS.

This is worth emphasizing because it is rare. Most industrial companies retain some element of individual qualitative assessment -- a way for the board to reward executives for "leadership" or "strategic vision" independent of financial results. Xylem has eliminated that entirely. If the company does not hit its financial targets, nobody gets paid. It is a radical commitment to accountability.

Pine holds approximately $32 million in Xylem stock -- over 247,000 shares -- and is mandated to hold at least 6 times his base salary in company equity. When the CEO's personal net worth is this exposed to the stock price, alignment with shareholders is not a talking point. It is a mathematical reality.

The most consequential -- and controversial -- initiative under Pine is the "80/20 simplification," and understanding it is essential to understanding where Xylem is going.

The 80/20 principle in manufacturing holds that roughly 20% of a company's products and customers generate 80% of its profits, while the remaining 80% generate disproportionately little value -- or even destroy it. Many industrial companies pay lip service to this concept. Pine is actually executing it, aggressively, and accepting the top-line pain.

What does this look like in practice? Xylem is deliberately walking away from low-margin, low-value product lines and customer segments.

The highest-profile move came in October 2025, when Xylem announced the sale of its metering assets outside North America -- a roughly $250 million revenue business generating less than 10% EBITDA margin. The deal was expected to close by the end of the first quarter of 2026, and the EPS impact was trivial: roughly two to three cents. But the margin impact was significant: the divestiture alone was projected to improve the Measurement and Control Solutions segment's margins by approximately 100 basis points.

This is the hidden driver of Xylem's recent massive margin expansion. In 2025, the walkaway headwind to the top line was approximately 1% of revenue. In 2026, management has guided the headwind to roughly 2% -- double the impact -- with 2026 described as the "peak year" for purposeful walkaways.

The math is counterintuitive: you are giving up revenue to make the business more profitable. It hurts the top line slightly but makes the remaining business incredibly lucrative. Full-year 2025 adjusted EBITDA margin hit 22.2%, and 2026 guidance calls for 22.9% to 23.3%, with a long-term target of 23% or higher.

The tension this creates was on full display on February 10, 2026, when Xylem reported its fourth-quarter and full-year 2025 results. The numbers were record-breaking by every measure: revenue, EBITDA, EPS, and free cash flow all hit new highs. But 2026 revenue guidance of $9.1 to $9.2 billion -- implying just 1% to 3% reported growth -- came in well below the $9.33 billion Wall Street had expected. The guidance embedded roughly 2% of deliberate revenue walkaways, the 80/20 headwind of purposefully shedding low-margin product lines, plus approximately 1% of foreign exchange headwinds.

The stock dropped 12% in pre-market trading and closed down more than 6% on the day, wiping out roughly $4 billion in market capitalization. It was a stark illustration of the communication challenge that accompanies any 80/20 transformation: the benefits show up in margins and free cash flow, but the costs show up immediately on the top line. Investors who understood the strategy saw it as a deliberate, temporary tradeoff -- the kind of short-term pain that creates long-term compounding. Those who did not saw a nine-billion-dollar company guiding to anemic revenue growth and sold first, asked questions later.

Pine's response on the earnings call was characteristically direct. He described 2026 as a year of "building the foundation" for sustainable, high-quality growth, noting that organic revenue growth, adjusted for walkaways and currency, would be in the 3% to 5% range. The adjusted EBITDA margin guidance of 22.9% to 23.3% implied another 70 to 110 basis points of expansion -- a massive improvement that would bring the company within striking distance of its long-term 23%-plus target. For investors willing to look through the top-line noise, the underlying economics of the business were improving at an accelerating rate.

Beneath the 80/20 transformation, Pine is driving massive growth in several highly lucrative businesses that do not get enough attention.

The fastest-growing engine is Measurement and Control Solutions. In the fourth quarter of 2025, MCS orders surged 22% organically, driven by smart metering demand across water and energy utilities. Revenue grew 10%, and adjusted EBITDA margin expanded 310 basis points to 20.2%. The segment exited 2025 with approximately $1.4 billion in backlog. But the real story within MCS is the Xylem Vue software platform.

Xylem Vue is powered by technology from Idrica, the Spanish water analytics company that developed the GoAigua platform. The origins are worth understanding. GoAigua was built by Global Omnium, a Spanish water utility that had been managing water systems for over 130 years in Valencia. Global Omnium developed the platform to manage its own operations, then spun out the technology into Idrica as a standalone software company. This is significant because GoAigua was not built by Silicon Valley engineers imagining what a water utility might need. It was built by water utility operators solving their own real-world problems. The software carries the DNA of actual operational experience.

Xylem first partnered with Idrica in early 2023, taking a minority stake and distributing GoAigua globally under the Xylem Vue brand. Then, in December 2024, Xylem acquired a controlling 61% stake, integrating Idrica's digital backbone fully into the platform.

What makes Xylem Vue strategically distinctive is that it is hardware-agnostic. To understand why this matters, consider the typical utility's technology situation. A mid-sized water system might have Sensus smart meters on some routes, Badger Meter devices on others, and aging mechanical meters from Neptune or Elster on the rest. Their SCADA system might be from one vendor, their GIS from another, their billing system from a third. Data exists in silos, in incompatible formats, across systems that were never designed to talk to each other.

Xylem Vue sits on top of all of this. It ingests data from any connected device -- even competitors' equipment -- and creates a unified operational picture. A utility does not need to rip out its existing infrastructure to get value from the platform. Xylem Vue layers AI-powered analytics on top of whatever data sources exist: predicting pipe bursts based on pressure patterns and historical failure data, optimizing energy consumption in pumping stations, identifying and prioritizing non-revenue water loss with real-time insights, and generating compliance reports automatically.

The business model is software-as-a-service: recurring subscription revenue with high gross margins and minimal incremental cost per additional customer. Xylem Vue revenues doubled in 2025, and management is guiding for over 30% growth in 2026. This is the recurring revenue, high-margin software business that transforms Xylem's earnings quality and justifies premium valuation multiples. It is also the business that makes the hardware-agnostic strategy so clever: even when a utility buys a competitor's meters, they may still run Xylem's software. In the language of technology strategy, Xylem is trying to own the platform layer -- the layer that is hardest to displace and captures the most value.

The second hidden engine is one that would have been inconceivable when Xylem was spun off in 2011: hyperscale data center cooling. To understand why a water company suddenly matters to the AI industry, consider what happens inside a modern data center. Thousands of GPU chips running AI training workloads generate enormous heat. That heat must be removed continuously, or the chips throttle performance and eventually fail. The dominant cooling method is still evaporative cooling towers, which use water to absorb and dissipate heat. Cooling accounts for 10% to 40% of a data center's total energy costs. And the AI boom is making the problem exponentially worse.

U.S. data centers alone consumed over 75 billion gallons of water in 2023, and water demand for data centers is forecast to increase 130% by 2050. Every major hyperscaler -- Amazon, Microsoft, Google, Meta -- is racing to build new facilities, and every facility needs cooling infrastructure. This is not a technology trend that might happen. It is happening right now, at massive scale.

Xylem, primarily through its Lowara brand (those Italian high-efficiency pumps from the original portfolio), is positioning itself as a one-stop shop for data center water systems: hydronic cooling, water treatment, screening, filtration, heat exchanging, digital monitoring, firefighting, and wastewater management. The differentiated offering is chemical-free cooling. Traditional cooling towers require continuous chemical dosing -- biocides to prevent biological growth, corrosion inhibitors, scale suppressants. These chemicals are expensive, environmentally problematic, and operationally complex. Using Vortisand microsand media filtration and UV disinfection, Xylem eliminates the need for continuous chemical dosing entirely.

The results from customer deployments are compelling: 75% reduction in biocide usage, 40% reduction in water consumption compared to traditional sand filtration. One customer has deployed over 80 UV systems across more than 30 data center locations in the United States. Xylem has collaborated with AWS on large-scale water recovery projects at hyperscale facilities, and in late 2025 launched a dedicated suite of solutions for data center thermal management. The company does not disclose data center revenue separately, but management commentary suggests it is scaling rapidly and becoming a meaningful contributor to the Water Infrastructure and Water Solutions segments. In a world where every major tech company is racing to build AI infrastructure and facing increasing public scrutiny over water consumption, the company providing chemical-free, water-efficient cooling systems sits in an extraordinarily valuable position.

The third hidden engine is the PFAS gold rush. To understand why this matters, a brief chemistry lesson is helpful. PFAS -- per- and polyfluoroalkyl substances -- are a family of roughly 15,000 synthetic chemicals that have been manufactured since the 1940s. They are used in everything from non-stick cookware (Teflon) to firefighting foam to food packaging to waterproof clothing. The reason they are called "forever chemicals" is that the carbon-fluorine bond in PFAS is one of the strongest in organic chemistry. These molecules do not break down in the environment. They do not biodegrade. They persist in soil, water, and biological tissue essentially indefinitely. And decades of industrial use have contaminated drinking water supplies across the United States and around the world.

The health effects of PFAS exposure are still being studied, but the evidence is concerning enough that regulators have acted. In April 2024, the EPA established the first-ever national primary drinking water regulation for PFAS, setting maximum contaminant levels of four parts per trillion for PFOA and PFOS -- the two most common and well-studied compounds. Four parts per trillion is an extraordinarily low threshold. To put it in perspective, that is roughly equivalent to four drops of water in an Olympic-sized swimming pool. Detecting contaminants at that level requires sophisticated analytical chemistry. Removing them requires advanced treatment technology that most water systems do not currently possess.

The compliance deadline has been extended to 2031, and while some regulatory uncertainty exists around other PFAS compounds, the core PFOA and PFOS limits have been upheld by the courts. The American Water Works Association estimates compliance costs of $50 billion or more over twenty years. The 2021 Bipartisan Infrastructure Law allocated $9 billion specifically for drinking water utilities to address emerging contaminants including PFAS. And in a development that is sometimes overlooked, settlement proceeds from 3M and DuPont -- the companies that manufactured many of these chemicals -- began flowing to water utilities in the summer of 2025. These legal settlements create an additional funding source beyond federal appropriations, enabling capital deployment for treatment infrastructure even if government budgets are constrained.

This is where the Evoqua acquisition pays off most directly. The two primary technologies for removing PFAS from drinking water are granular activated carbon filtration and ion exchange resins. Granular activated carbon works by adsorbing PFAS molecules onto the surface of carbon particles -- essentially trapping the chemicals as water flows through a bed of activated carbon. Ion exchange resins work differently: they use specially engineered resin beads that swap harmless ions for PFAS molecules, selectively pulling the contaminants out of the water stream. Evoqua was a leader in both technologies, and its selective single-use ion exchange resin systems -- originally pioneered for perchlorate removal in the 1990s and now adapted for PFAS -- represent some of the most effective solutions available.

Xylem can now offer a single-source PFAS remediation solution from emergency response through media selection, pilot testing, installation, commissioning, and ongoing maintenance. For a small water utility facing a PFAS compliance mandate -- one of the 50,000-plus systems in the United States -- the ability to call a single company and have them handle the entire process from detection to treatment is enormously valuable. The total addressable market for PFAS remediation is estimated at $6 billion to $10 billion-plus -- a market that barely existed five years ago and is now funded by a combination of federal infrastructure dollars, legal settlements, and regulatory mandates.

One more initiative worth noting, because it signals where management sees the long-term frontier: subsea desalination. In November 2025, Xylem joined as a strategic investor in Flocean, a Norwegian startup named a TIME Best Invention of 2025. Flocean participated in a $22.5 million Series A round and joined the Xylem Innovation Labs Accelerator.

The technology is elegant in concept. Traditional desalination plants are massive onshore facilities that use high-pressure pumps to force seawater through reverse osmosis membranes. They are expensive to build, energy-intensive to operate, and produce concentrated brine that must be disposed of -- often by dumping it back into the ocean, where it damages marine ecosystems. Flocean's approach eliminates the pump entirely. Its patented systems operate at 400 to 600 meters ocean depth, where the natural hydrostatic pressure of the water column -- the sheer weight of the ocean above -- provides the force needed to drive reverse osmosis. No onshore plant. No energy-intensive pumps. No toxic brine discharge. No coastal infrastructure footprint.

The company claims seven to eight times lower capital cost per unit of capacity versus conventional onshore desalination. If those economics prove out at scale, it would fundamentally change the calculus of water supply for coastal regions facing drought stress -- from the Middle East to California to Australia. Xylem's investment gives it first-mover access to this technology and the ability to integrate it into its global distribution and engineering ecosystem. This is a long-term bet on water scarcity, not a near-term revenue driver. But it signals a management team that is thinking about where the water industry is heading over the next decade, not just the next quarter.

VI. Playbook: Strategy and Framework Analysis

To understand Xylem's competitive position rigorously, it helps to apply the two most powerful analytical frameworks available: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces.

Start with switching costs, which is Xylem's most potent competitive power. Once a municipality deploys FlexNet infrastructure -- base stations, repeaters, thousands of smart meter endpoints -- migrating to a competitor's system is functionally impossible.

It requires ripping out and replacing all physical meters and network equipment, retraining operations staff, re-integrating with billing, SCADA, and back-office systems, and navigating multi-year municipal procurement cycles. This is not theoretical. Fort Worth Water's Advanced Metering Infrastructure deployment, built on Xylem technology, reduced field investigations by 90% and generated over $1 million in annual cost savings. Those operational improvements create deep institutional dependence. Every year that a utility operates on FlexNet, the switching cost grows.

The Xylem Vue software platform amplifies this effect to a different degree. As utilities build their workflows, dashboards, historical data repositories, and decision-making processes around the platform, the accumulated institutional knowledge and operational dependency makes switching not just expensive but organizationally traumatic.

And because Xylem Vue is hardware-agnostic -- it works with competitors' devices -- utilities that adopt it are locked into Xylem's software layer regardless of whose physical meters they use. This is a subtle but powerful competitive dynamic: the more hardware-agnostic the platform becomes, the stickier it gets, because the utility is no longer tied to Xylem's hardware but is deeply embedded in Xylem's software.

Scale economies represent the second major power. At nine billion dollars in revenue, Xylem is the largest company in the world focused exclusively on water technology. This confers three specific advantages.

First, R&D leverage: Xylem spends approximately $230 million annually on research and development, spread across the broadest product portfolio in the industry. Badger Meter, at roughly one-eleventh the revenue, simply cannot match this investment across as many technology domains.

Second, procurement: the $140 million in Evoqua synergies were driven primarily by scale efficiencies in procurement and network optimization.

Third, global distribution: 23,000 employees across 150-plus countries provide go-to-market infrastructure that smaller competitors cannot replicate.

There is also an element of counter-positioning at work. Xylem's aggressive pivot into digital software and AI analytics creates a dilemma for traditional hardware-focused competitors. Investing heavily in software capabilities would cannibalize their existing business models and require fundamentally different organizational skills. Xylem, having committed to this transformation with billions of dollars in acquisitions and a dedicated software platform, has a head start that traditional pump and valve manufacturers would find extremely costly and organizationally painful to replicate.

A more emerging power is what might be called a cornered resource: FlexNet operates on licensed spectrum, which is a finite, regulated resource. No competitor can simply acquire identical spectrum without regulatory approval.

Additionally, the historical operational data accumulated across thousands of municipal deployments -- flow patterns, leak detection data, consumption analytics -- becomes increasingly valuable as AI and machine learning models are trained on it. This is a potential data moat still in its early stages, but its value compounds with every new deployment.

Now turn to Porter's Five Forces, which reveal an industry structure that is remarkably favorable for incumbents.

Bargaining power of buyers is low. The United States alone has over 50,000 community water systems and more than 23,000 wastewater treatment facilities. Small systems serving fewer than 3,300 people make up 78% of all water systems. This is an extraordinarily fragmented buyer base with no individual customer possessing meaningful leverage over equipment suppliers.

Municipal procurement is governed by public bidding processes with long cycles, further reducing buyer power. Many utilities lack in-house engineering expertise, making them dependent on supplier solutions. And critically, water is non-discretionary -- utilities cannot defer purchases indefinitely, and regulatory mandates like PFAS compliance force spending regardless of budget constraints.

The threat of substitutes is, quite literally, non-existent. There is no substitute for water. Unlike energy, where solar can replace coal or electric vehicles can replace gasoline, water has no alternative input. Drinking water must be treated and distributed. Wastewater must be collected and processed.

The only form of "substitution" is water reuse and recycling, which actually increases demand for treatment technology. Conservation reduces volume but increases the technology intensity per gallon. This is an industry where demand destruction is structurally impossible.

Competitive rivalry is moderate. The industry is fragmented, with no single dominant player. Xylem at $9 billion is the largest pure-play, but in a total addressable market estimated at over $220 billion (Veolia's own estimate), even the biggest players hold low single-digit market shares.

Competition is segmented: Badger Meter dominates in smart metering, Veolia leads in water concessions and operations, Veralto's Hach brand is the gold standard in water quality analytics, and Pentair owns the residential and commercial niche. Growth comes primarily from market expansion -- aging infrastructure replacement, new regulations, climate-driven demand -- rather than share warfare. Pricing is relatively stable due to regulated procurement processes and long product lifecycles.

Barriers to entry are high. Technical barriers include deep domain expertise, regulatory certifications, and years of R&D. Water treatment products must meet stringent health and safety standards from the NSF, EPA, and state-level regulators. Capital barriers are immense: building a global manufacturing and service footprint requires billions.

Relationship barriers matter enormously in a conservative industry where utilities cannot risk deploying untested technology on critical water infrastructure. And FlexNet's licensed spectrum represents a regulatory barrier that money alone cannot overcome.

The net assessment is clear: this is an industry where incumbents with scale, technology, and relationships enjoy structural advantages that are difficult to erode. The competitive moat is not any single factor -- it is the combination of switching costs, scale, counter-positioning, fragmented buyers, zero substitution risk, and high barriers to entry operating simultaneously.

How does Xylem compare to its key competitors? The competitive landscape in water technology is surprisingly fragmented, and each major player has chosen a distinct strategic position.

Veolia, the Paris-listed water giant, is the only company in the world that rivals Xylem in water technology breadth. The French company generated approximately five billion euros in its water technologies division, comparable to Xylem's pre-Evoqua revenue. But Veolia is fundamentally a different animal: it is a diversified environmental services conglomerate that also operates water and wastewater utilities under long-term concession contracts, manages solid waste, and provides energy services. This means Veolia is both a supplier and a customer of water technology. Its conglomerate structure makes it harder for investors to isolate the pure water technology economics.

Veralto, spun off from Danaher in September 2023, is an interesting parallel to Xylem's own spin-off story. At $5.5 billion in revenue and a $24.4 billion market cap, Veralto combines Danaher's former water quality analytics brands (most notably Hach, the gold standard in water quality testing instruments) with its product quality and innovation businesses. But roughly 40% of Veralto's revenue comes from non-water product identification -- marking, coding, and quality assurance for packaging and consumer goods. Veralto is a partial water play, not a pure one.

Pentair, at roughly $4.2 billion in revenue and a $16 billion market cap, has deliberately positioned itself as a residential and commercial water treatment specialist. It dominates in pool equipment, water filtration for homes and restaurants, and flow control for commercial buildings. Pentair explicitly avoids the massive municipal infrastructure market where Xylem dominates, preferring higher-margin, shorter-cycle consumer and commercial products. It is a superb business in its niche but does not compete with Xylem across most of its portfolio.

Badger Meter, at roughly $820 million in revenue and a $4.6 billion market cap, is the most direct competitor in smart water metering. Badger has been one of the best-performing industrial stocks of the past decade, compounding shareholder returns at extraordinary rates through disciplined organic growth, incremental bolt-on acquisitions, and aggressive share buybacks. It represents the "stay focused, compound slowly" model that stands in philosophical contrast to Xylem's "acquire aggressively, transform fast" approach. Badger's E-Series Ultrasonic meters compete directly with Xylem's Sensus products, and the rivalry in municipal metering is fierce. But Badger lacks Xylem's breadth in treatment, infrastructure, and enterprise software.

Roper Technologies' Neptune division is another direct competitor in water metering, but Neptune is a small division within a $59 billion diversified technology conglomerate. Roper's M&A-driven model prioritizes asset-light, software-intensive businesses, and water metering fits that profile well, but it does not receive the strategic focus or investment that a pure-play competitor like Xylem can provide.

The competitive dynamic that matters most is the shift from hardware to software. In a world where pump hardware is increasingly commoditized -- where a well-engineered pump from Grundfos, Sulzer, or KSB can substitute for a Xylem pump in many applications -- the company that owns the data layer captures the premium economics. The software that turns raw sensor readings into actionable intelligence, that predicts failures before they happen, that optimizes energy consumption across an entire water network -- this is where the margin expansion and customer lock-in live.

Xylem, through FlexNet, Xylem Vue, and the Idrica acquisition, has the most advanced position in this transition among pure-play water companies. Whether this translates into sustained premium valuation depends on whether the software business can grow fast enough and achieve high enough margins to shift the company's overall earnings mix. The early evidence -- Xylem Vue revenues doubling in 2025 with 30%-plus growth guided for 2026 -- is encouraging. But the software business remains a relatively small portion of total revenue. The transformation is underway, but it is not yet complete. The next two to three years will determine whether Xylem's premium valuation is justified by durable earnings quality -- or whether it remains, at heart, an industrial company with a software wrapper.

VII. Epilogue: The Future

Before looking forward, it is worth separating myth from reality on a few consensus narratives that surround Xylem.

Myth number one: "Xylem is a water utility." This is perhaps the most common misconception. Xylem does not own, operate, or manage water systems. It sells the technology -- hardware, software, and services -- that utilities use to operate their systems. This is an important distinction because it means Xylem is not subject to rate regulation, does not carry the balance sheet risk of infrastructure ownership, and is not exposed to the political dynamics of water pricing. It is the picks-and-shovels play on water infrastructure, not the mine itself.

Myth number two: "The PFAS opportunity is a sure thing." The PFAS remediation market is real and enormous, but its timing depends on regulatory enforcement, funding flows, and political priorities. The compliance deadline has already been extended to 2031. The proposed federal budget includes significant EPA funding cuts. And while the core PFOA and PFOS drinking water limits have been upheld by the courts, the broader PFAS regulatory framework -- including regulations covering additional compounds -- remains in flux. The opportunity is structurally sound but the timeline is uncertain.

Myth number three: "Xylem has completed its transformation." The 80/20 simplification is still in its early innings. Management has described 2026 as the "peak year" for purposeful revenue walkaways, meaning the deliberate shedding of low-margin businesses is intensifying, not winding down. The Xylem Vue software platform, while growing rapidly, still represents a relatively small portion of total revenue. The company's EBITDA margins, while expanding impressively, remain below the 23%-plus long-term target. The transformation story is real, but it is an ongoing process, not a completed one.

Now, the financial picture. In 2011, Xylem was a $3.8 billion pump company valued as an industrial cyclical. In early 2026, it is a $31.5 billion infrastructure intelligence platform trading at roughly 33 times trailing earnings and 18.7 times enterprise value to EBITDA. Those multiples reflect market recognition of the software optionality and secular tailwinds, even as the stock trades 14% below its October 2025 all-time high of $154.24 following the post-earnings selloff in February 2026. The stock sits at approximately $130 as of early March 2026.

The balance sheet tells a story of financial strength unusual for a company that completed a $7.5 billion acquisition less than three years ago. Net debt to adjusted EBITDA stands at just 0.4 times, with $2.2 billion in available liquidity. The rapid deleveraging is a testament to both the free cash flow generation of the combined business and management's disciplined capital allocation. In February 2026, the board authorized a $1.5 billion share repurchase program with no expiration date, alongside an 8% quarterly dividend increase to $0.40 per share quarterly. The company also exited 2025 with a record backlog of $4.6 billion, providing visibility into future revenue.

Management has guided toward approximately $1 billion in annual M&A spending, generating $60 to $75 million in incremental EBITDA -- a signal that future acquisitions will be bolt-on rather than transformational. The Decker era of mega-deals is over. The Pine era is about compounding returns on the platform that has been built.

What comes next? Three frontiers are worth watching.

First, AI-powered predictive maintenance. Xylem Vue is still in its early innings of leveraging artificial intelligence across water networks. The platform already uses machine learning to predict pipe bursts and optimize energy consumption. As more utilities adopt the platform and generate more data, the AI models improve -- creating a flywheel effect where Xylem's predictive accuracy grows with its installed base. Solutions deployed through the platform have cut visible leaks by 57% and reduced leakage in high-priority areas by 32% in documented cases. The potential here is enormous: if Xylem can demonstrate that its AI reliably prevents infrastructure failures and saves utilities money, the willingness-to-pay for the software will increase materially. This is where the data moat becomes most valuable -- the utility with the most deployment data trains the best predictive models, which attracts more deployments, which generates more data. A classic network effect, applied to water infrastructure.

Second, the convergence of water and AI infrastructure. The explosive growth of data centers driven by AI workloads has created an entirely unexpected source of demand for water technology. The irony is rich: artificial intelligence -- the most digital, most abstract technology trend in the world -- turns out to require enormous quantities of the most physical resource on the planet. Xylem's chemical-free cooling solutions and water management platforms are positioned at the intersection of two of the most powerful secular trends in the global economy. The Flocean subsea desalination investment, while early-stage, suggests management is thinking about where water scarcity will be most acute as these trends accelerate. If desalination costs can be reduced by the seven to eight times that Flocean claims, entirely new water supply options become economically viable for coastal regions facing drought stress.

Third, the PFAS regulatory wave. Regardless of the precise compliance timeline -- currently 2031 -- the fundamental reality is that tens of thousands of water systems will need to install advanced treatment technology to meet enforceable federal standards. The $9 billion allocated by the Bipartisan Infrastructure Law for emerging contaminants, combined with settlement proceeds from chemical manufacturers now flowing to utilities, creates a multi-year spending cycle that plays directly to Xylem's treatment capabilities. And PFAS is likely just the beginning. As water quality monitoring becomes more sophisticated and public awareness of contaminants grows, the number of regulated substances in drinking water is likely to increase over time -- each new regulation creating another wave of mandatory treatment spending.

The risks are real and should be stated plainly.

The 80/20 simplification strategy creates visible near-term revenue headwinds that may persist through 2026 and into 2027. Tariff exposure of approximately $180 million annualized, while management says it will be "substantially offset" by pricing and supply chain actions, adds uncertainty in an era of escalating trade tensions.

China exposure is a meaningful concern: fourth-quarter 2025 orders from China declined nearly 70%, and the geopolitical trajectory suggests this headwind may worsen before it improves.

Federal infrastructure funding represents both an opportunity and a risk. The 2021 Bipartisan Infrastructure Law allocated $55 billion for water, including $43.5 billion through State Revolving Fund loans and grants. But disbursement has been slower than expected: $20.4 billion had been obligated as of July 2025, and award volumes declined 53% in the first half of 2025 compared to the prior year period.

The proposed fiscal year 2026 federal budget includes a 23% reduction in total EPA funding and a 31.5% cut to State Revolving Fund appropriations. If federal infrastructure spending is materially curtailed, the multi-year tailwind that underpins much of the bull case for water technology companies would weaken.

There is also a material legal and regulatory overhang to monitor. PFAS regulations beyond PFOA and PFOS are being reconsidered by the current EPA administration, and while the core drinking water standards have been upheld by the courts, the broader regulatory framework remains in flux.

The say-on-pay vote at Xylem's 2024 annual meeting received 82.7% support -- solid but not overwhelming -- suggesting some investor discomfort with the executive compensation structure.

And the premium valuation -- 33 times trailing earnings, 36 times free cash flow -- leaves limited room for execution stumbles. A company priced for continued transformation must continue to transform.

Finally, a word on what this story means in a broader context. Water is often called the "last great undigitized infrastructure." Energy has been transformed by smart grids, renewable generation, and battery storage. Transportation has been transformed by GPS, ride-sharing, and autonomous vehicles. Telecommunications was transformed decades ago. But water -- the most essential resource on the planet, the one without which life itself ceases -- has remained stubbornly analog, managed by aging infrastructure, paper-based processes, and institutions resistant to change.

What began on Halloween 2011 as a corporate orphan -- a collection of century-old pump brands that Wall Street did not know how to categorize -- has become the company best positioned to change that. Through a decade of deliberate, sometimes controversial acquisitions, a painful but necessary pivot from hardware to software, and a new operational discipline that sacrifices easy revenue for profitable revenue, Xylem has built what may be the most comprehensive competitive position in the global water technology industry.

A company that makes water infrastructure visible, intelligent, and manageable in an era of aging pipes, tightening regulations, climate stress, and explosive AI-driven water demand. The moat is made of water -- and it turns out that might be the most durable moat of all.

VIII. Further Reading

-

Xylem 2025 Annual Report and 10-K Filing -- SEC EDGAR, comprehensive financial and operational detail on all four business segments, risk factors, and management discussion.

-

Xylem 2025 Proxy Statement -- Available at xylem.com/investors. Detailed executive compensation analysis, board composition, and governance structure including the 80/20 transformation metrics.

-

Xylem Q4 2025 Earnings Call Transcript -- Investing.com, February 10, 2026. CEO Matthew Pine's discussion of the 80/20 simplification strategy, 2026 guidance, and long-term margin targets.

-

"In a Water-Scarce World, the Xylem-Evoqua Deal Makes Sense. Why Some Think It's Too Expensive" -- CNBC, January 23, 2023. Essential reading for understanding the initial market debate around the Evoqua acquisition.

-

EPA National Primary Drinking Water Regulation for PFAS -- EPA.gov, April 2024 with May 2025 updates. The regulatory framework driving billions in water treatment spending.

-

Infrastructure Investment and Jobs Act: Water Provisions -- Congressional Research Service Report R46892. Detailed breakdown of the $55 billion in federal water infrastructure funding.

-

"Durable Value Creators: Badger Meter" -- Substack analysis of Xylem's closest pure-play competitor, providing a useful contrast in M&A philosophy and capital allocation strategy.

-

Xylem Investor Day Presentation (2024) -- Available on Xylem investor relations site. The most detailed public presentation of the Xylem Vue platform strategy and segment growth targets.

-

Hamilton Helmer, "7 Powers: The Foundations of Business Strategy" (2016) -- The theoretical framework for understanding Xylem's switching costs, scale economies, and counter-positioning advantages.

-

Global Water Intelligence Market Reports -- GWI's annual data on water market sizing, data center water consumption trends, and desalination technology forecasts providing the macro backdrop for Xylem's addressable market.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube