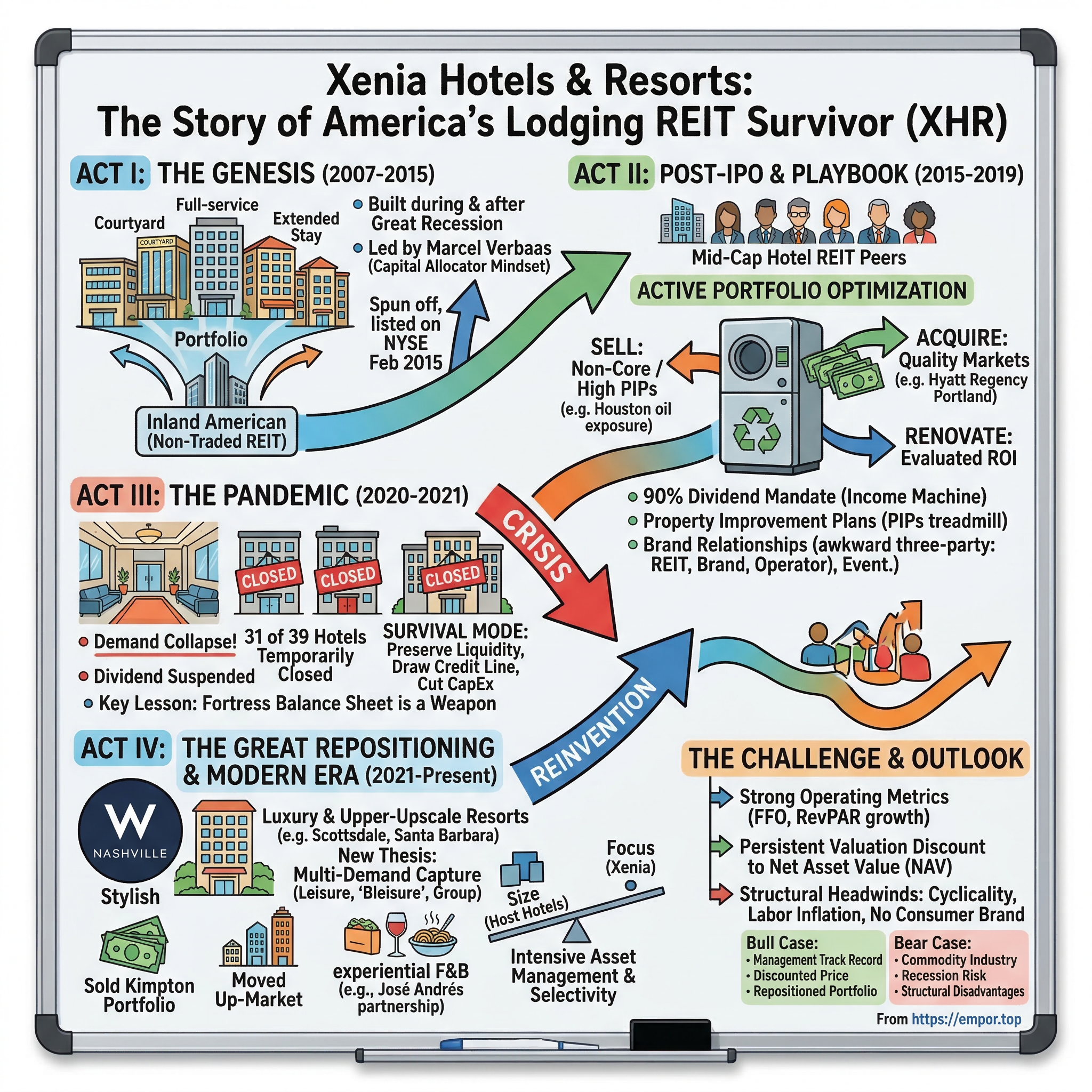

Xenia Hotels & Resorts: The Story of America's Lodging REIT Survivor

I. Introduction & Episode Roadmap

Picture this: a Tuesday morning in March 2020. The lobby of a gleaming Marriott-branded hotel in downtown Denver sits empty. The front desk clerk stares at a reservation screen showing zero check-ins for the day. Upstairs, four hundred freshly made beds will go unslept in. Within seventy-two hours, the hotel will close its doors entirely, its staff furloughed, its revenue reduced to precisely nothing. This scene played out simultaneously at thirty-one of Xenia Hotels & Resorts' thirty-nine properties, an overnight annihilation of a business that had been carefully assembled over nearly a decade.

Xenia Hotels & Resorts is a lodging REIT—a real estate investment trust that owns premium hotels across the United States. As of early 2026, the company trades on the NYSE under the ticker XHR with a market capitalization hovering around $1.3 billion. It owns thirty hotels totaling roughly 8,900 rooms, concentrated in the luxury and upper-upscale segments. The portfolio reads like a greatest-hits list of American hospitality: a W Hotel in Nashville, a Hyatt Regency in Scottsdale, resort properties in Santa Barbara and San Diego, and urban gems scattered from Orlando to Portland.

But the central question of this story isn't about glamorous lobbies or infinity pools. It's this: how did a spinoff from a non-traded REIT—a vehicle most sophisticated investors wouldn't touch—become one of the last pure-play hotel REITs standing? And what does that survival tell us about capital allocation, cyclical resilience, and the brutal economics of owning hotels in America?

Hotel REITs occupy one of the most unforgiving corners of the real estate universe. Unlike apartment buildings with twelve-month leases or office towers with ten-year contracts, hotels reprice their inventory every single night. There is no contractual revenue floor. When demand evaporates—as it did spectacularly in 2020—revenue doesn't decline gradually. It falls off a cliff. This daily repricing creates enormous operating leverage in both directions: spectacular margins when occupancy runs high, and devastating losses when it doesn't. Layer on top of that the complex relationships with global hotel brands like Marriott and Hyatt, the constant capital requirements to renovate and maintain properties, and the REIT structure's mandate to distribute ninety percent of taxable income as dividends, and you have what might be the most operationally challenging form of real estate ownership ever devised.

This story moves through four distinct acts. First, the genesis—how a lodging portfolio was assembled from the wreckage of the Great Recession and then spun off into a publicly traded company. Second, the playbook—how Xenia's management team developed a disciplined approach to buying, selling, and renovating hotels that set the company apart from its peers. Third, the crisis—the existential threat of the pandemic and the desperate measures required to survive. And fourth, the reinvention—how Xenia emerged from COVID-19 with a fundamentally different portfolio and a new thesis about what American travelers actually want. Along the way, we'll encounter themes that resonate far beyond the hotel industry: the power of a fortress balance sheet, the difference between structural moats and execution advantages, and the age-old question of whether a well-run company in a tough industry can ever truly reward its shareholders.

The uncomfortable truth that hangs over this entire narrative is that Xenia's stock, as of this writing, trades below the price where it first opened on the New York Stock Exchange more than eleven years ago. This is a company that has done many things right—and still hasn't been rewarded by the market. Understanding why requires understanding everything that follows.

II. The REIT Revolution & Hotel Industry Context (1990s–2000s)

To understand Xenia's story, you first have to understand the peculiar financial architecture that makes it possible: the Real Estate Investment Trust. Congress created the REIT structure in 1960 with a straightforward idea—give ordinary investors access to large-scale, income-producing real estate the way mutual funds gave them access to stocks. The deal was simple: if a company invested primarily in real estate, distributed at least ninety percent of its taxable income to shareholders, and met certain ownership diversification requirements, it could avoid paying corporate income tax. The catch, of course, was that ninety-percent payout requirement. REITs would be income machines, not growth vehicles. The structure assumed real estate was a stable, cash-flowing asset class that could comfortably return most of its earnings without starving itself of capital.

For decades, that assumption held. Apartment REITs, office REITs, and retail REITs flourished. Their properties generated predictable rental income under long-term leases, and the ninety-percent payout worked beautifully. Then someone had the idea of applying this structure to hotels—and immediately discovered that the REIT framework was never designed for a business where revenue could swing thirty percent in either direction within a single quarter.

The modern lodging REIT era began in earnest during the 1990s. Host Hotels & Resorts, the lodging arm spun off from Marriott International in 1993, became the sector's bellwether. Sunstone Hotel Investors went public in 1995. By the late 1990s, a half-dozen hotel REITs traded on major exchanges, each promising investors a way to own premium hotels and collect fat dividends. The economics looked compelling on paper: hotels generated high revenues per square foot, the hospitality industry was booming, and franchise relationships with brands like Marriott and Hilton provided built-in demand through loyalty programs and reservation systems.

But the lodging REIT model contained fundamental tensions that would take years to fully expose. The first was the franchise relationship itself. Hotel REITs didn't operate their own properties—they couldn't, under REIT tax rules that originally prohibited significant operational involvement. Instead, they owned the physical real estate and signed franchise agreements with brands like Marriott, Hyatt, and Hilton, while hiring third-party management companies to run the day-to-day operations. This created an awkward three-party arrangement: the REIT owned the building, the brand controlled the guest experience and pricing standards, and the management company actually ran the hotel. The REIT paid franchise fees to the brand (typically four to six percent of room revenue) and management fees to the operator (typically two to three percent of total revenue plus incentive fees). By the time you added up these fees, the REIT was giving away a meaningful chunk of its revenue to parties whose interests didn't always align with the property owner's.

The second tension was capital intensity. Hotel brands imposed something called Property Improvement Plans—PIPs—that required owners to renovate their hotels on regular cycles, typically every six to eight years. These weren't suggestions; they were contractual obligations. Fail to complete a PIP, and the brand could terminate your franchise agreement, stripping the hotel of its flag and its connection to the brand's reservation system and loyalty program. A Marriott that loses its Marriott flag isn't worth anywhere near what it was the day before. PIPs could cost tens of millions of dollars per property, and they came due regardless of where the hotel was in the economic cycle. This was capital spending that couldn't be deferred without existential consequences, a treadmill that hotel REITs could never stop running on.

The third tension was the industry's core metric: Revenue Per Available Room, universally known as RevPAR. RevPAR combines occupancy rate and average daily rate into a single number that captures how effectively a hotel monetizes its room inventory. It became the lodging industry's equivalent of same-store sales in retail—the number that analysts watched above all others. But RevPAR was ruthlessly cyclical. During the tech boom of the late 1990s, RevPAR growth was spectacular. During the recession of 2001, it cratered. And the 2008 financial crisis revealed just how violent the swings could be.

The Great Recession devastated the hotel industry with a severity that shocked even veteran operators. National RevPAR fell more than sixteen percent in 2009, the worst annual decline in the modern era. Occupancy rates plunged below sixty percent. Hotels that had been underwritten at peak economics suddenly couldn't cover their debt service. Distressed assets flooded the market as overleveraged owners—many of them private equity firms that had paid premium prices during the 2006-2007 boom—were forced to hand properties back to lenders or sell at fire-sale prices. For hotel REITs, the crisis was a near-death experience. Host Hotels cut its dividend by eighty percent. Sunstone suspended its dividend entirely. Several smaller lodging REITs were acquired at distressed prices or ceased to exist.

But destruction creates opportunity, and the post-crisis landscape set the stage for a new generation of hotel companies to emerge. Among them was a lodging portfolio being quietly assembled within a non-traded REIT based in the suburbs of Chicago—a portfolio that would eventually become Xenia Hotels & Resorts.

III. Genesis: The Private Equity Years & Formation (2007–2015)

The story of Xenia Hotels & Resorts doesn't begin with a dramatic founding moment or a visionary entrepreneur sketching ideas on a napkin. It begins in the offices of Inland American Real Estate Trust, a non-traded REIT headquartered in Oak Brook, Illinois—a sprawling suburb west of Chicago better known for its shopping mall than for financial innovation. Inland American was one of the largest non-traded REITs in the country, a vehicle that raised billions from retail investors through broker-dealer networks, investing in a grab bag of commercial real estate assets: shopping centers, office buildings, student housing, and hotels. It was the kind of entity that sophisticated institutional investors regarded with suspicion—non-traded REITs were illiquid, opaque, and laden with fees that enriched their sponsors at the expense of shareholders.

But within this unlikely corporate parent, something genuinely interesting was happening on the hotel side. Beginning in 2007, a team led by Marcel Verbaas started building a lodging portfolio with a clear thesis: acquire quality hotel assets in strong metropolitan markets at compelling prices, renovate and reposition them, and generate attractive risk-adjusted returns. The timing was simultaneously terrible and perfect. Terrible because 2007 was the absolute peak of the pre-crisis hotel market, when cap rates were compressed and prices were inflated. Perfect because the portfolio assembly continued through 2008, 2009, and beyond—years when distressed sellers were practically giving away premium hotels.

Marcel Verbaas, a Dutch-born executive who had cut his teeth in lodging finance at GE Capital and CNL Hospitality Corp, brought a European rigor to an industry that often operated on instinct and relationships. His background in corporate finance—stints at Ocwen Financial, Stormont Trice Development, and CNL's hospitality platform—gave him a balance-sheet-first mentality that would prove prophetic. Verbaas didn't think about hotels the way a hotelier did, obsessing over thread counts and restaurant concepts. He thought about them the way a capital allocator did, obsessing over cost of capital, renovation ROI, and the spread between acquisition price and replacement cost.

The team focused on what the industry calls upscale select-service and extended-stay hotels—properties that offered quality rooms and modern amenities but without the massive food-and-beverage operations, convention ballrooms, and army of staff that full-service luxury hotels required. The logic was compelling: select-service hotels had lower operating costs, better profit margins, and less cyclical revenue than their full-service counterparts. A Courtyard by Marriott might not generate the headline RevPAR of a Ritz-Carlton, but it also didn't need a brigade of chefs, a sommelier, and a team of banquet servers. The breakeven occupancy for a select-service hotel might be forty percent; for a full-service luxury property, it could be sixty percent or higher. In a downturn, that difference was the gap between survival and distress.

The portfolio grew steadily through the post-recession years. By 2014, the lodging assets within Inland American had become a substantial business in their own right—roughly forty-six hotels with over twelve thousand rooms spread across nineteen states and the District of Columbia. The properties carried flags from the biggest names in hospitality: Marriott, Hyatt, Hilton, Kimpton. They were concentrated in major metropolitan statistical areas—San Francisco, Los Angeles, Denver, Houston, Dallas, Orlando—markets with deep demand pools and high barriers to new supply.

The decision to spin off the hotel portfolio came in August 2014, when Inland American's board—under pressure from investors frustrated by the non-traded REIT's poor returns and governance issues—announced that it would separate its lodging assets into a standalone, publicly traded company. The entity would be called Xenia Hotels & Resorts, named for the ancient Greek concept of hospitality and generosity toward strangers. It was a name that signaled ambition: this wasn't going to be just another hotel REIT. The management team that had built the portfolio would stay on to run it, led by Verbaas as Chairman and CEO.

The separation was executed as a pro rata taxable distribution—each Inland American shareholder received one share of Xenia for every eight shares of Inland American they held, with the distribution of ninety-five percent of Xenia's common stock completed on February 3, 2015. On February 4, Xenia's shares began trading on the New York Stock Exchange. In conjunction with the listing, the company launched a modified Dutch Auction tender offer to repurchase up to $125 million of its own shares at a price range of $19.00 to $21.00 per share—a savvy move that simultaneously established price discovery and signaled management's confidence in the portfolio's value.

The market reception was warm but not euphoric. Shares opened at $21.00 on the first day, touched an intraday high of $23.65, and settled to close at $20.55. The management team was now running a publicly traded company with a clean balance sheet, a focused portfolio, and something to prove. Their pitch to the investment community was straightforward: "We're different from other hotel REITs because we have higher-quality assets, better locations, a fortress balance sheet, and a management team with a track record of disciplined capital allocation."

It was a compelling story. The question was whether the public markets would give them the time and patience to execute it—and the lodging cycle was already showing signs of age.

IV. Going Public: The 2015 IPO & REIT Conversion

The Xenia that emerged into the public markets in February 2015 was a company caught between two identities. On one hand, it was a fresh start—a newly independent entity with no legacy corporate parent dictating strategy, no overhead from an unwieldy non-traded REIT structure, and a management team hungry to prove themselves on the public stage. On the other hand, it inherited the complicated reality of its origin: many of its initial shareholders were the retail investors who had bought into Inland American through broker-dealer networks, people who often had limited understanding of REIT investing and who, frankly, were already disappointed by years of underwhelming returns from the non-traded structure.

The company established its new headquarters in Orlando, Florida—a deliberate break from the Inland American mothership in suburban Chicago and a strategic choice that placed management closer to one of their most important markets and the hospitality industry's center of gravity. The new leadership team crystallized around three key figures. Verbaas remained as Chairman and CEO, bringing continuity and the capital allocator's mindset that had shaped the portfolio from the beginning. Barry Bloom, a veteran hotel operator, took the role of President and COO, providing the operational counterweight to Verbaas's financial orientation. And in April 2016, the team recruited Atish Shah as CFO—a hire that said everything about where Xenia wanted to position itself.

Shah's resume read like a hospitality finance all-star compilation. He held a Master of Management in Hospitality from Cornell's School of Hotel Administration and an MBA from Wharton—credentials that bridged the gap between industry expertise and Wall Street fluency. He had spent nearly a decade at Hilton Hotels in the late 1990s and 2000s, followed by seven years at Hyatt Hotels, where he rose to Senior Vice President and served a stint as Interim CFO. Before joining Xenia, he had worked at Lowe Enterprises, a hospitality-focused private equity fund. In Shah, Xenia got someone who understood hotel operations from the inside out but who also spoke the language of institutional investors. His appointment was a signal that Xenia wasn't content to be a sleepy hotel owner collecting management fees. The company wanted to be taken seriously as a capital allocator in a sector that desperately needed more of them.

At the time of its public listing, Xenia's portfolio comprised roughly forty-six hotels—a mix of select-service, extended-stay, and some full-service properties. The concentration in top metropolitan areas was a selling point: San Francisco, Los Angeles, Denver, Houston, Dallas-Fort Worth, Orlando, and Washington D.C. But this geographic mix also carried hidden risks. Houston, for example, was heavily exposed to the energy sector, and oil prices had already begun their devastating decline from the $100-per-barrel levels of mid-2014. San Francisco, while boasting some of the highest hotel rates in the country, was also one of the most politically hostile environments for hotel owners, with rising labor costs, restrictive regulations, and an aggressive union presence.

The REIT structure imposed its own set of constraints. The ninety-percent distribution requirement meant Xenia had to return the vast majority of its taxable income to shareholders as dividends, leaving limited retained earnings for acquisitions, renovations, or debt reduction. This wasn't a problem in good times, when hotels generated strong cash flows and external capital markets provided cheap financing. But in downturns, the distribution requirement became a straitjacket—the company would have to maintain its dividend even as cash flows declined, or cut the dividend and face the wrath of income-focused shareholders who had bought the stock precisely for that yield.

The competitive landscape that Xenia entered was crowded and stratified. At the top sat Host Hotels & Resorts, the industry giant with a market capitalization exceeding ten billion dollars and a portfolio of iconic luxury properties like the Manchester Grand Hyatt San Diego and the Ritz-Carlton Naples. Host had scale advantages that Xenia could never match—better financing terms, more institutional analyst coverage, and the ability to make headline-grabbing acquisitions. At the other end sat economy-focused REITs like Apple Hospitality, which owned hundreds of Hampton Inns and Residence Inns—lower rates but also lower volatility. In the middle were Xenia's true peers: Sunstone Hotel Investors, RLJ Lodging Trust, DiamondRock Hospitality, Pebblebrook Hotel Trust. These mid-cap hotel REITs competed for the same assets, the same investors, and the same analyst attention, differentiating primarily on portfolio quality, geographic mix, and management credibility.

Xenia's initial performance as a public company was respectable but not spectacular. Revenue in 2015 came in at $976 million, with earnings per share of $0.79. The company established a quarterly dividend of $0.275 per share, translating to an annual payout of $1.10—a yield that was attractive relative to the REIT sector but not extraordinary. The stock traded in a range roughly between $16 and $22 during its first year, never straying far from the IPO price. The message from the market was clear: prove it.

The real question was whether Xenia could differentiate itself from the pack of mid-cap hotel REITs, all of which told variations of the same story—quality assets, good locations, disciplined management. In the commodity business of hotel ownership, storytelling alone wouldn't create value. Execution would, and the next four years would be Xenia's opportunity to demonstrate whether its management team's capital allocation instincts were genuinely superior, or merely average dressed up in better marketing.

V. The Playbook: Capital Allocation & Portfolio Optimization (2015–2019)

The boardroom of Xenia Hotels & Resorts in Orlando, sometime in late 2015: Marcel Verbaas and his team were staring at a spreadsheet that would define the company's strategy for the next half-decade. Each row represented a hotel in their portfolio. Each column captured a metric—RevPAR growth, margin trajectory, market supply pipeline, renovation costs, brand competitiveness, geographic risk factors. The exercise was ruthlessly analytical. Every property was being evaluated not just on its current performance but on a forward-looking assessment of whether it deserved Xenia's capital. Properties that couldn't earn their keep—that sat in weakening markets, that required disproportionate renovation spending, that faced overwhelming new supply—would be sold. The proceeds would be recycled into better assets in better markets.

This "recycling machine," as the strategy came to be known, was Xenia's central differentiating philosophy. Most hotel REITs were passive owners—they acquired properties, maintained them adequately, collected the cash flows, and distributed dividends. Xenia aspired to something more active: continuous portfolio optimization, treating the company's asset base like an investment portfolio that needed regular rebalancing rather than a static collection of real estate.

The results came fast. In 2016, Xenia sold four non-core hotels for $119 million, deploying the proceeds into properties in stronger markets and share repurchases. The sales were strategically motivated: several of the disposed properties sat in markets with unfavorable supply-demand dynamics, and management concluded that no amount of renovation or rebranding would change the fundamental competitive position of those assets. Better to take the capital and invest it where the wind was at your back.

The Houston exposure was a textbook case of proactive portfolio management. When oil prices collapsed in 2014-2015, many hotel REITs with Houston properties simply held on, hoping for a recovery. Verbaas and his team took a more clinical view. They analyzed the city's hotel supply pipeline—which was enormous, with thousands of new rooms under construction even as energy-sector demand was contracting—and concluded that Houston's hotel economics would be challenged for years. They began reducing their Houston exposure, selling properties at prices that, while below replacement cost, were still well above what those same properties would be worth once the new supply came online and crashed local RevPAR.

On the acquisition side, Xenia's most significant move during this period was the purchase of the Hyatt Regency Portland at the Oregon Convention Center for $190 million in 2019—roughly $317,000 per key. It was the kind of deal that showcased the team's analytical approach. Portland was a market with strong demand fundamentals—a growing tech sector, a vibrant food-and-tourism scene, and relatively constrained supply compared to Sun Belt competitors. The Hyatt Regency was a six-hundred-room convention hotel with direct skybridge access to the Oregon Convention Center, giving it a competitive position that would be nearly impossible to replicate. The acquisition price was well below estimated replacement cost, providing a margin of safety.

Throughout this period, Xenia invested over $200 million in capital expenditure programs across the portfolio—renovating lobbies, updating room products, adding technology infrastructure, refreshing food-and-beverage concepts. This wasn't vanity spending. Each renovation dollar was evaluated against its expected return on investment, with management tracking the RevPAR lift generated by completed projects and comparing results against initial underwriting. Properties that renovated successfully—showing measurable increases in rate and occupancy—validated the capital allocation thesis. Those that didn't informed future spending decisions.

Brand relationship management became another dimension of the strategy. Xenia worked across a diverse stable of brands—Marriott, Hyatt, Hilton, Kimpton—and the management team developed a sophisticated understanding of when to rebrand a property and when to maintain its existing flag. Rebranding was expensive and disruptive, typically requiring a full renovation to meet the new brand's standards, plus transition costs as the hotel disconnected from one loyalty program and connected to another. But when the economics justified it—when a property could command significantly higher rates under a different flag, or when a brand change aligned with shifts in the local market's demand composition—Xenia pulled the trigger.

The financial discipline underpinning all of this was conservative leverage. While many hotel REITs operated with debt-to-assets ratios of fifty percent or higher, Xenia targeted a range of thirty-five to forty percent. This meant slower growth—the company couldn't bid as aggressively on acquisitions as more levered competitors—but it also meant resilience. In a cyclical business where downturns could arrive without warning, balance sheet conservatism was a form of insurance. The dividend was maintained at $1.10 per share annually throughout this period, providing a steady return to income-focused investors.

The results were steady if not spectacular. RevPAR grew at a low-to-mid single-digit pace, roughly in line with the industry. Margins expanded modestly as renovations and portfolio upgrades took effect. Total returns were respectable but didn't dramatically outperform the lodging REIT sector.

Between 2016 and 2017, Xenia executed what amounted to a major portfolio repositioning—selling lower-quality assets, acquiring urban select-service hotels in stronger markets, and deliberately reducing exposure to oil-dependent and commodity-driven local economies. This was the first major inflection point in the company's public history, a period where management's willingness to make tough decisions—selling properties that were generating current income but whose long-term prospects were deteriorating—established the credibility that would prove essential when far more difficult decisions lay ahead.

By 2019, the portfolio had been pruned from forty-six hotels to roughly forty, a net reduction that improved average quality metrics across the board. RevPAR per property was higher, margins were wider, and the geographic mix was more defensible. But there was an uncomfortable fact that shadowed all of this execution: Xenia's stock was trading below its IPO opening price. After four years of disciplined portfolio management, operational execution, and shareholder-friendly capital allocation, the market was essentially saying that the company was worth less than when it started. For investors who had hoped that quality execution would translate into stock price appreciation, this was deeply frustrating—and it raised a question that would haunt Xenia for years: in a sector that the market simply didn't want to own, could any amount of operational excellence overcome structural headwinds?

VI. The Storm Clouds Gather: Industry Headwinds (2018–2019)

By 2018, the American lodging industry was exhibiting all the classic symptoms of a cycle running on fumes. RevPAR growth, which had been robust in the years immediately following the Great Recession, had decelerated to low-single-digit territory—enough to keep hotels profitable but not enough to excite investors or justify the capital intensity of the business. The problem wasn't demand, which remained reasonably healthy as the economy continued its post-crisis expansion. The problem was supply.

Between 2015 and 2019, the United States added roughly half a million new hotel rooms to its inventory—an avalanche of new supply that diluted pricing power across virtually every major market. Developers, attracted by the same strong demand fundamentals that hotel REITs cited in their investor presentations, had been breaking ground on new properties at a pace not seen since the mid-2000s. The irony was painful: the very conditions that made existing hotels attractive to own were simultaneously attracting competitors who would undermine those same economics.

Labor cost inflation compounded the supply problem. By 2018, the U.S. unemployment rate had fallen below four percent, and the hospitality industry—which depended on a large workforce of housekeepers, front desk agents, maintenance workers, food servers, and kitchen staff—was competing for workers against every other service sector employer. Wages rose accordingly, and hotels, with their thin margins and high fixed-cost structures, absorbed the impact directly to the bottom line. A hotel generating sixty dollars per occupied room in housekeeping revenue was now paying materially more to clean each room, compressing margins that were already under pressure from sluggish RevPAR growth.

Then there was the Airbnb question. By the late 2010s, the home-sharing platform had gone from a quirky startup to a genuine threat to the traditional hotel industry, with millions of listings worldwide and a particular impact on the leisure and extended-stay segments that were Xenia's bread and butter. Academic research and industry analyses offered conflicting assessments of Airbnb's impact—some studies suggested it had capped hotel pricing power by five to ten percent in major markets, while others argued that it primarily expanded the overall travel market rather than stealing share from hotels. But the psychological impact on hotel REIT valuations was unambiguous: investors applied a permanent discount to the sector, reasoning that the threat of substitution would only grow as Airbnb's network effects strengthened.

The "lower for longer" interest rate environment added another layer of complexity. Low rates were theoretically good for REITs, reducing borrowing costs and making dividend yields more attractive relative to bonds. But in practice, the extended period of low rates created a valuation paradox: hotel REITs traded at persistent discounts to their net asset values, as investors questioned whether the REIT structure was the optimal way to own hotels when private capital—flush with dry powder from pension funds, sovereign wealth funds, and family offices—could buy the same assets without the public market's volatility and the ninety-percent distribution constraint.

Investor fatigue with the lodging REIT sector became palpable. Conference attendance from buy-side investors declined. Analyst coverage thinned. The sector's weighting in major REIT indices shrank as other property types—cell towers, data centers, industrial warehouses—captured investor imagination with their secular growth stories and technology-adjacent narratives. Hotel REITs, by contrast, were seen as old economy, cyclical, and lacking the structural tailwinds that justified premium multiples.

Xenia's response to these gathering headwinds was characteristically disciplined. Rather than chasing growth through aggressive acquisitions—a temptation that had destroyed value at numerous hotel companies over the decades—management doubled down on portfolio quality. Properties in markets with unfavorable supply-demand dynamics were sold. Renovation programs were calibrated to maximize rate premium relative to new competitors. The balance sheet was kept clean, with leverage ratios well below the sector average.

But discipline doesn't always translate into stock performance. By the end of 2019, Xenia's shares were trading in the high teens—below the $21 opening price from nearly five years earlier. The company had done virtually everything right operationally, and the market had yawned. Revenue reached $1.149 billion that year, the highest in the company's public history. Earnings per share, however, had declined to $0.49, reflecting the margin compression from rising costs and moderating RevPAR growth. The business was healthy but not thriving, profitable but not exciting, well-managed but trapped in a sector that the investment community had decided it didn't want to own.

In hindsight, the pre-pandemic years look like a dress rehearsal—a period when Xenia built the institutional muscle and balance sheet resilience that would prove critical when the real crisis arrived. The management team didn't know that a global pandemic was about to devastate their industry. But the conservative leverage, the active portfolio management, and the culture of capital discipline they had cultivated meant that when the storm hit, Xenia was better prepared than most.

VII. The Pandemic: Existential Crisis & Survival Mode (2020–2021)

The first confirmed COVID-19 case in the United States was reported on January 20, 2020. Within sixty days, the American hotel industry experienced a demand collapse that made the Great Recession look like a minor inconvenience. What happened to Xenia Hotels & Resorts between March and June of 2020 represents one of the most extreme episodes of business destruction in modern corporate history—and the management response offers a masterclass in crisis leadership.

The numbers are almost incomprehensible. Full-year 2020 revenue came in at $370 million, down sixty-eight percent from $1.149 billion the prior year. EBITDA turned deeply negative at negative $95 million, compared to positive $266 million in 2019. The company reported a net loss of $163 million. But the full-year figures actually understate the severity of the crisis, because they include the relatively normal first two and a half months before the shutdown. The second quarter of 2020 was apocalyptic: RevPAR cratered, occupancy at the hotels that remained open fell to roughly eleven percent, and even that number was misleading because many of the "guests" were stranded travelers or healthcare workers receiving discounted rates.

Thirty-one of Xenia's thirty-nine hotels temporarily suspended operations between late March and early April. The properties that remained open did so primarily because of contractual obligations or because they served as quasi-essential facilities in their communities. The company furloughed the vast majority of its corporate and property-level staff. Capital spending plans were slashed by roughly $50 million. And on the most painful decision of all—the dividend—management acted swiftly and decisively. The last pre-pandemic quarterly dividend of $0.275 per share was declared on February 21, 2020 and paid on April 15. After that, the dividend was suspended entirely. It would not be reinstated for two and a half years.

The survival playbook that Marcel Verbaas, Barry Bloom, and Atish Shah executed during this period was built on a single overriding principle: preserve liquidity at all costs. Everything else—growth plans, renovation schedules, acquisition pipelines, employee morale—was subordinated to the imperative of ensuring that Xenia could survive an indefinite period of near-zero revenue. The company drew down its revolving credit facility, building a cash fortress. Management renegotiated debt covenants with lenders, securing the breathing room needed to weather an unprecedented downturn without triggering technical defaults. They pursued PPP loans and other government assistance programs, not out of opportunism but out of genuine necessity.

The decisions about which hotels to keep open and which to mothball were agonizing. Each property had its own set of considerations: contractual obligations with brands and management companies, local market conditions, the cost of maintaining a closed building versus the cash burn of operating at single-digit occupancy, the risk of property damage or deterioration during an extended closure. Bloom's operational expertise was critical here—he understood the physical realities of hotel operations in a way that a pure financial executive might not, knowing which systems had to keep running to prevent pipe freezes, mold growth, or equipment failure, and which expenses could be safely eliminated.

What differentiated Xenia during this period was the balance sheet that management had spent the previous five years fortifying. Companies that had entered the pandemic with aggressive leverage—debt-to-EBITDA ratios of six, seven, eight times or higher—found themselves in genuine existential peril. Some hotel REITs were forced to sell assets at fire-sale prices to meet debt obligations. Others entered negotiations with lenders that amounted to soft restructurings. A few ultimately merged with competitors or were taken private by opportunistic buyers who smelled blood in the water. Xenia, with its conservative leverage and substantial liquidity, was never in danger of default. It was in danger of value destruction—the stock price hit an intraday low of $6.28 on March 18, 2020, representing a loss of roughly seventy percent from pre-COVID levels—but not of insolvency.

The recovery, when it came, was uneven and revealing. Leisure travel rebounded first, as vaccinated Americans with cabin fever and pent-up savings rushed to beaches, mountains, and national parks. Business travel lagged badly, with corporate road warriors replaced by Zoom calls and video conferences. Convention and group business, which had been a significant revenue driver for many hotel REITs, essentially evaporated and would take years to recover. Xenia's portfolio, which had historically skewed toward business-travel-dependent urban markets, was partially exposed to these unfavorable trends. But properties in leisure-oriented locations—resort-adjacent hotels, drive-to destinations—rebounded faster and more powerfully than anyone had expected.

Revenue recovered to $616 million in 2021, still forty-six percent below the 2019 peak but trending in the right direction. The recovery was driven almost entirely by rate rather than occupancy—a phenomenon that surprised many industry observers. Hotels were charging more per night than they had before the pandemic, even with significantly fewer guests. Consumers, it turned out, were willing to pay premium prices for travel experiences after months of lockdown. The question was whether this pricing power was permanent or merely a sugar high that would dissipate as the novelty of post-pandemic travel wore off.

For Xenia's management team, the pandemic crystallized a strategic insight that would reshape the company over the next several years. The old thesis—that urban, business-travel-dependent hotels in major metropolitan areas represented the safest and most profitable investments—had been brutally challenged. The new thesis that was forming was more nuanced: the future of hotel ownership lay in properties that could capture multiple demand streams—leisure, business, "bleisure" (the emerging hybrid of business and leisure travel), extended stays, and group events—in markets where people actually wanted to spend time, not just conduct meetings. This insight would drive the most aggressive portfolio transformation in Xenia's history.

VIII. The Great Repositioning: Post-Pandemic Strategy (2021–2023)

In the aftermath of the pandemic, a fierce debate raged within the hotel industry about what had permanently changed and what would eventually revert to pre-COVID norms. Were business travelers really gone for good? Would conventions ever return to their former scale? Had remote work permanently altered the geographic distribution of hotel demand? Most hotel REITs hedged their bets, making incremental adjustments to their portfolios while hoping that the old patterns would reassert themselves. Xenia made a bigger bet.

The strategic transformation that Xenia executed between 2021 and 2023 represents the third major inflection point in the company's history—and arguably the most consequential. Under Verbaas's direction, the company embarked on an aggressive program of asset sales and selective acquisitions designed to fundamentally reposition the portfolio away from its historical dependence on urban business travel and toward the demand patterns that the pandemic had revealed and accelerated.

The most dramatic move came early: the sale of seven Kimpton-branded hotels for $483 million. This was a portfolio-defining transaction that removed a significant chunk of Xenia's urban, lifestyle-hotel exposure in a single stroke. The Kimpton brand—beloved by boutique hotel enthusiasts for its wine hours and eclectic décor—had been particularly hard hit by the pandemic because its properties were concentrated in downtown locations that depended on business travelers and urban tourists. The sale price represented strong execution given the timing, and the proceeds provided substantial capital for reinvestment.

The Residence Inn Boston Cambridge, a 221-room extended-stay property, was sold separately for $107.5 million—roughly $486,000 per key. This was a premium asset in one of America's strongest hotel markets, and selling it was counterintuitive on the surface. But management's analysis concluded that the property's future upside was limited relative to alternatives: Cambridge's hotel supply pipeline was growing, labor costs in Massachusetts were rising relentlessly, and the capital that the sale freed up could generate better returns deployed elsewhere.

On the acquisition side, the headline transaction was the purchase of the W Nashville for $328.7 million in 2022—approximately $950,000 per key. This was a statement acquisition. The 346-room luxury lifestyle hotel, located in Nashville's booming Gulch neighborhood, represented exactly the kind of property that Xenia's evolved thesis favored: a luxury-branded asset in a leisure-friendly market with strong in-migration trends, favorable tax policies, no state income tax, and a rapidly growing music-and-entertainment tourism industry. Nashville's hotel fundamentals had outperformed virtually every major American city through the pandemic recovery, and the W Hotel—with its rooftop bar, multiple dining venues, and association with one of hospitality's most coveted lifestyle brands—was positioned to capture the city's premium demand.

The acquisition illustrated a broader portfolio evolution. Xenia's luxury exposure grew from roughly twenty-six percent of portfolio value in 2018 to approximately thirty-seven percent by 2025. The company was deliberately moving up-market, away from the select-service hotels that had been the foundation of its original portfolio and toward luxury and upper-upscale properties that commanded higher rates, attracted more affluent guests, and demonstrated less sensitivity to economic cycles. This was a meaningful strategic shift—and a risky one, given that luxury hotels also carried higher operating costs, more intensive capital requirements, and greater exposure to the discretionary spending of high-income consumers.

Brand partnerships evolved in parallel. Xenia increasingly favored differentiated, lifestyle-oriented brands over commoditized flags. The Marriott Autograph Collection—a soft brand that allowed individual properties to maintain unique identities while accessing Marriott's reservation system and loyalty program—became a favored franchise structure. Management also invested in food-and-beverage repositioning, including a partnership with celebrity chef José Andrés's restaurant group at the W Nashville—the kind of experiential enhancement that could drive rate premiums and generate ancillary revenue beyond room nights.

The company also invested in creative conversions, transforming existing properties to capture new demand patterns. Hotels that had been positioned primarily for business travelers were reconcepted to attract leisure visitors, with upgraded pool areas, expanded outdoor spaces, and enhanced spa and wellness amenities. These investments reflected the management team's conviction that the boundary between business and leisure travel had permanently blurred—that the guest who flew to Phoenix for a Monday meeting was increasingly staying through Wednesday to play golf, and that the hotel that could serve both needs would outperform the one designed exclusively for either.

Balance sheet optimization accompanied the portfolio transformation. Xenia refinanced its debt at what, in hindsight, were relatively favorable rates compared to the higher interest rate environment that would follow. Maturities were extended, providing runway to execute the strategic plan without pressure from near-term debt towers. The dividend was reinstated in the third quarter of 2022 at a reduced quarterly rate of $0.10 per share—less than half the pre-pandemic level but a meaningful signal of confidence in the company's recovery trajectory.

By the end of 2023, revenue had recovered to $1.025 billion—approaching but not quite reaching the 2019 peak of $1.149 billion, though the portfolio was meaningfully smaller. On a same-property basis, the hotels that Xenia retained were performing at or above their 2019 levels, validating the portfolio transformation thesis. The company had emerged from the pandemic with fewer but better hotels, a more diversified demand base, and a management team whose crisis leadership had earned hard-won credibility.

Whether the transformation was aggressive enough—and whether the market would ever reward it with a higher stock price—remained very much an open question.

IX. The Modern Era: Scale Disadvantage or Focused Advantage? (2023–Present)

Walk through the lobby of Xenia's W Nashville today—past the sculptural art installation, through the buzzing lobby bar where a DJ spins vinyl on Thursday nights, past couples in cowboy boots heading out to Lower Broadway—and you're seeing the physical manifestation of a company that has bet everything on the thesis that quality beats quantity in the hotel business. The property commands average daily rates north of four hundred dollars. Its rooftop pool draws not just hotel guests but Nashville locals willing to pay steep day rates for the privilege. The José Andrés restaurant generates per-square-foot revenues that rival Manhattan fine dining. This single asset produces more economic value than several of the hotels Xenia sold to acquire it.

But the W Nashville also crystallizes the central strategic tension of Xenia's modern era: is this a company that is too small to compete, or one whose focus gives it an edge?

The numbers frame the question starkly. Xenia's current portfolio consists of thirty hotels with roughly 8,900 rooms and a total enterprise value of approximately $2.8 billion. Compare that to Host Hotels & Resorts, which owns roughly seventy-seven properties with over forty thousand rooms and an enterprise value exceeding $17 billion. Host can negotiate brand-wide agreements with Marriott and Hyatt that reduce franchise fees by basis points that translate into millions of dollars annually. Host's cost of capital is lower, its analyst coverage deeper, its liquidity premium larger. In the world of hotel REITs, size confers advantages that are difficult for smaller players to replicate.

And yet Xenia's management team argues—with some justification—that focus provides its own form of advantage. A smaller portfolio allows for more intensive asset management: Verbaas and Bloom can personally visit every property multiple times per year, build relationships with general managers, identify operational improvements that a larger company's regional directors might miss. The company's active portfolio management strategy—continuously evaluating each property's position and making buy-sell-hold decisions with analytical rigor—is easier to execute with thirty hotels than with seventy. And Xenia's concentrated portfolio allows it to be genuinely selective in its acquisitions, pursuing only the specific assets in specific markets that fit its thesis rather than having to deploy capital at scale to move the needle on a massive enterprise.

The operating metrics support the argument that the portfolio transformation has worked. In 2025, same-property RevPAR reached $181.97, up 3.9 percent year over year, with average daily rates of $265.38 and occupancy of 68.6 percent. Same-property hotel EBITDA margins expanded by 129 basis points to 25.8 percent. Adjusted FFO per diluted share came in at $1.76, up nearly eleven percent from the prior year, and adjusted EBITDAre reached $258.3 million. Revenue for 2025 hit $1.079 billion. These are healthy numbers for a company of Xenia's size, suggesting that the properties it retained and acquired are performing well.

Management has also been increasingly aggressive with shareholder returns. In 2025, Xenia repurchased 9.4 million shares at an average price of $12.87 per share, deploying $120.4 million in buybacks. Combined with a quarterly dividend that was raised from $0.12 to $0.14 per share—a seventeen percent increase—the total capital return to shareholders was substantial. The buyback program was particularly significant because it reflected management's view that the stock was trading at a meaningful discount to the intrinsic value of the underlying real estate. Buying back shares at twelve to thirteen dollars when the properties were worth considerably more per share on a private-market basis was, in management's assessment, a better use of capital than acquiring additional hotels at prevailing market prices.

The 2026 outlook, provided in the company's most recent guidance, suggests continued momentum. Group room revenue pace was up approximately fifteen percent as of October 2025, with roughly thirty-five percent of room-night demand coming from group bookings—a significant recovery from the pandemic-era collapse in convention and meeting business. Same-property RevPAR growth was guided at 1.5 to 4.5 percent, with adjusted FFO per share expected between $1.78 and $1.99. Capital expenditure plans of $70 to $80 million reflect ongoing investment in property quality. And a remaining share repurchase authorization of $97.5 million signals continued commitment to returning excess capital.

Recent portfolio moves have continued the pattern of strategic pruning. The sale of the Fairmont Dallas—a 545-room full-service hotel—for $111 million in 2025 was motivated by the property's upcoming need for a costly renovation that management concluded would generate insufficient returns. Simultaneously, the acquisition of fee-simple ownership of the land beneath the Hyatt Regency Santa Clara for $25 million eliminated a ground lease that had been a persistent drag on the property's economics—a classic Xenia move, unglamorous but accretive.

The industry consolidation backdrop adds another dimension. Park Hotels & Resorts and Sunstone Hotel Investors have been the subject of merger speculation. Private equity firms continue to circle the lodging REIT sector, attracted by the persistent discount to net asset value. Xenia itself is frequently mentioned as a potential takeout candidate—its manageable size, clean balance sheet, and high-quality portfolio make it an attractive target for a larger REIT seeking to add scale or a private equity firm looking to take a hotel platform private.

But the valuation disconnect persists. As of mid-March 2026, Xenia trades at approximately $14.16 per share—still below its first-day opening price of $21.00 from February 2015. The current dividend yield of roughly four percent is attractive for income investors, but the total return over the company's eleven-year public life has been disappointing relative to both the broader market and other real estate sectors. This is the fundamental paradox of Xenia's story: a company that has executed well, managed its balance sheet conservatively, and transformed its portfolio intelligently, yet has failed to generate the stock price appreciation that its operational performance would seem to justify. Understanding why requires diving into the structural economics of the hotel REIT business model.

X. The Business Model Deep Dive: Why Hotel REITs Are Hard

There is a reason that Warren Buffett, who has invested in everything from insurance companies to railroad monopolies, has never bought a hotel REIT. The economics of hotel ownership are structurally inhospitable to the value investor's dream of buying great businesses with durable competitive advantages at reasonable prices.

Start with revenue volatility. An apartment REIT signs twelve-month leases. An office REIT signs ten-year leases. A cell tower REIT signs twenty-year agreements with built-in escalators. A hotel REIT signs zero-night leases—every room is repriced every single day, and there is no contractual guarantee that tomorrow's rate will be anything like today's. This daily repricing is the defining characteristic of the hotel business, and it cuts both ways. In strong demand environments, hotels can raise rates rapidly, capturing inflation and demand surges in real time. But when demand falls—whether from recession, pandemic, weather event, or local market disruption—revenue declines are immediate and proportional. There is no lag, no cushion, no contractual floor. The revenue just disappears.

Layer on top of this the operating leverage inherent in the business. Hotels have high fixed costs—mortgage payments, property taxes, insurance, maintenance staff, utilities, brand franchise fees—that must be paid regardless of occupancy. Variable costs like housekeeping and food supplies decline with lower occupancy but don't disappear, and many hotels operate with union contracts that limit management's ability to reduce labor costs quickly. The result is that a hotel's profit margins swing dramatically with small changes in occupancy. A hotel running at seventy-five percent occupancy might generate a thirty percent EBITDA margin. The same hotel at sixty percent occupancy might generate a fifteen percent margin. And at forty-five percent occupancy, it might be losing money. This operating leverage magnifies the revenue volatility, creating earnings swings that make hotel REITs among the most cyclical securities in the equity market.

The capital intensity of hotel ownership is another structural burden. Brand franchise agreements require regular renovation cycles—the dreaded PIPs—and these are not optional. A hotel owner who defers renovation risks losing their franchise agreement, which would strip the property of its brand affiliation, its connection to the brand's reservation system and loyalty program, and a significant portion of its revenue-generating capacity. Think of it like maintaining a franchise restaurant: you can't run a McDonald's with peeling paint and broken equipment, because the franchisor will revoke your license. Hotels face the same dynamic but at enormously larger scale—a single PIP can cost $20 million or more, requiring complete room renovations, lobby redesigns, technology upgrades, and compliance with the brand's latest design standards.

The brand relationship itself is a double-edged sword. On one hand, affiliation with Marriott, Hyatt, or Hilton provides access to massive loyalty programs with hundreds of millions of members, sophisticated revenue management systems, global distribution networks, and brand recognition that drives direct bookings. A Marriott-branded hotel captures guests through Marriott Bonvoy that it would never attract as an independent property. On the other hand, the hotel owner pays dearly for these benefits. Franchise fees typically run four to six percent of room revenue. Marketing fees add another two to three percent. Management fees—paid to the third-party company that actually operates the hotel—add another two to four percent of total revenue. By the time all of these fees are paid, the hotel owner is giving away ten to fifteen percent of total revenue to parties whose interests don't always align with maximizing the owner's returns.

The REIT structure compounds these challenges. The ninety-percent distribution requirement means that hotel REITs can't retain substantial earnings to fund renovations, make acquisitions, or build cash reserves for downturns. When capital is needed—and in the hotel business, it is always needed—the company must access external markets through debt issuance, equity offerings, or asset sales. Each of these has costs: debt increases leverage and interest expense, equity issuance dilutes existing shareholders, and asset sales may require disposing of properties at inopportune times. The REIT structure, designed for stable, cash-flowing real estate, sits uneasily atop the volatile, capital-intensive hotel business.

Third-party management adds another layer of complexity. Because of historical REIT tax rules, hotel REITs outsourced the actual operation of their properties to management companies—firms like Aimbridge Hospitality, Highgate, or Crescent Hotels that employed the staff, managed the day-to-day operations, and reported results back to the owner. This separation of ownership from operations created agency problems: management companies were typically compensated as a percentage of revenue, giving them incentives to maximize revenue (which might mean excessive discounting) rather than profit. The management company's employees staffed the hotel, but the REIT owner paid their wages. The management company made hiring and compensation decisions, but the REIT bore the cost.

This constellation of structural challenges explains why hotel REITs have persistently traded at discounts to their estimated net asset values—and why sophisticated private equity firms and sovereign wealth funds often prefer to own hotels outside the public REIT structure. In a private structure, the owner retains complete flexibility over capital allocation, distributions, and timing of asset sales. There is no quarterly earnings pressure, no public market volatility, and no REIT distribution requirement. The same asset that trades at a discount to NAV in a public REIT might be valued at or above NAV in a private transaction. This valuation arbitrage has been a persistent feature of the hotel industry, and it helps explain why companies like Xenia—despite strong operational execution—have struggled to generate sustained stock price appreciation.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

To truly understand Xenia's competitive position, it helps to apply two rigorous analytical frameworks: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers. Together, they paint a picture that is sobering in its clarity.

Start with competitive rivalry, which is ferocious. The hotel industry is fragmented across thousands of owners—from individual property operators to global REITs to sovereign wealth funds—all competing for the same travelers. Online distribution has made hotel shopping nearly frictionless: a consumer searching for a hotel in Nashville sees dozens of options ranked by price, reviews, and location, and can switch from a Marriott to a Hyatt to an independent boutique with a single click. Brand loyalty programs create some stickiness, but the loyalty belongs to the brand, not the property owner. Xenia might own a spectacular Marriott in Scottsdale, but the Marriott Bonvoy member has no idea—and no reason to care—that Xenia owns it. The competition is for the guest's attention and wallet, and it is relentless.

The threat of new entrants is moderated by the substantial capital requirements of hotel development—building a new full-service hotel costs hundreds of millions of dollars—and by the relationships required to secure brand franchise agreements. But these barriers are far from insurmountable. When hotel economics look attractive in a market, developers build. They always build. The pipeline of new rooms under construction in any given year serves as a constant reminder that whatever pricing power existing hotels enjoy is temporary, subject to the inevitable arrival of new competition. This is particularly true in Sun Belt markets like Nashville, Austin, and Phoenix, where favorable regulatory environments make development easier and faster than in supply-constrained markets like Manhattan or San Francisco.

Supplier power presents an underappreciated challenge. The most powerful "suppliers" in the hotel business aren't the linen vendors or the food distributors—they're the hotel brands themselves. Marriott, Hyatt, and Hilton control franchise agreements that dictate renovation standards, service requirements, marketing fees, and technology mandates. They operate massive loyalty programs that drive significant booking volume, creating a dependency relationship where the hotel owner needs the brand more than the brand needs any individual hotel owner. If Marriott terminates a franchise agreement, the hotel loses access to Marriott Bonvoy's 200 million-plus members and Marriott's reservation system overnight. If a hotel owner terminates its relationship with Marriott, the brand simply re-flags a different property down the street. This asymmetry gives brands significant leverage in negotiations—leverage that manifests as higher fees, more demanding PIPs, and less flexibility for owners.

Buyer power is equally intense. Online travel agencies like Booking.com and Expedia have created unprecedented price transparency, allowing consumers to comparison-shop across hundreds of properties in seconds. Corporate travel managers negotiate aggressively for volume discounts. Group and convention planners play hotels against each other for meeting business. The result is a buyer environment where hotels have limited ability to charge above-market rates without immediately losing bookings to competitors. The brands' own direct booking campaigns—Marriott's "It Pays to Book Direct," Hilton's "Stop Clicking Around"—have helped shift some volume away from OTAs, but the fundamental dynamic of empowered, price-sensitive buyers remains.

The threat of substitutes has intensified significantly over the past decade. Airbnb and its competitors have created a massive alternative lodging supply that competes directly with hotels for leisure and extended-stay demand. Serviced apartments and corporate housing compete for business travelers on longer assignments. The rise of remote work has reduced the need for business travel altogether—a Zoom call is the ultimate substitute for a hotel room. While hotels retain advantages in consistency, service, and loyalty-program benefits, the competitive landscape has permanently expanded.

Turning to Helmer's Seven Powers framework, the analysis becomes even more revealing—and more uncomfortable for hotel REIT bulls. Scale economies, which provide structural advantage to many businesses, offer limited benefit to Xenia. The company's thirty-hotel portfolio provides no meaningful procurement advantages over competitors, and the overhead savings from being larger are modest compared to the fixed costs at the property level. Host Hotels, with ten times the asset base, can spread corporate overhead across a much larger revenue base, but even Host's scale advantages are small relative to the operating costs embedded at individual properties.

Network effects, the most powerful source of competitive advantage in the modern economy, are completely absent from hotel ownership. A hotel is not a marketplace, a social network, or a payment platform. Xenia's thirty hotels don't become more valuable because another guest stays at one of them. The network effects in hospitality belong to the brands—Marriott Bonvoy, Hilton Honors, World of Hyatt—and Xenia doesn't own any of those.

Counter-positioning—where an incumbent's business model prevents it from responding to a challenger's approach—offers Xenia only weak protection. The company's focused portfolio strategy differs from diversified peers like Host, but it's unclear that Host is structurally unable to adopt a similar focus if it chose to. The differentiation is one of management choice, not structural constraint.

Switching costs are negligible for hotel guests, who face zero friction in choosing a different property for their next trip. For brand relationships, there are moderate switching costs—changing a hotel's flag involves expense and disruption—but these costs protect the brand-owner relationship, not Xenia's competitive position against other hotel owners.

Xenia has no consumer brand. No traveler has ever said, "I want to stay at a Xenia hotel." The company is invisible to its ultimate customers, who interact entirely with the Marriott, Hyatt, or Kimpton brands on Xenia's properties. This is a fundamental structural weakness that no amount of operational excellence can overcome.

Cornered resources—unique assets that competitors cannot replicate—provide partial advantage. Some of Xenia's properties occupy genuinely premium locations: beachfront sites, convention-adjacent plots, irreplaceable urban locations where zoning restrictions prevent new competing development. But these advantages, while real, are modest and can be replicated by any well-capitalized buyer willing to pay the market price for similar properties.

Which brings us to Xenia's one genuine source of competitive power: process power. This is the advantage that comes from organizational capabilities that are difficult to replicate—in Xenia's case, the capital allocation discipline, asset management expertise, and operational rigor that the management team has demonstrated over more than a decade. The ability to consistently identify which properties to buy, which to sell, when to renovate, and how to optimize operations at the property level is a genuine skill that not all hotel REITs possess. It is Xenia's single sustainable advantage.

The brutal conclusion of this analysis is that Xenia operates in what might fairly be called commodity hell. The company has one genuine competitive power—process excellence—in an industry characterized by brutal competitive rivalry, empowered buyers, powerful suppliers, real substitute threats, and minimal barriers to entry. Success depends almost entirely on execution rather than structural moats. This is not a death sentence—companies can thrive for decades on execution advantages—but it does explain why the market applies a persistent valuation discount and why investors remain skeptical despite strong operational results.

XII. Bull Case vs. Bear Case

Every investment thesis eventually reduces to a question of what you believe will matter more: the things working in a company's favor, or the things working against it. For Xenia Hotels & Resorts, both lists are substantial.

The bull case begins with management. Marcel Verbaas and his team have built a track record of disciplined capital allocation that spans nearly two decades, from the initial portfolio assembly during the Great Recession through the pandemic survival and the post-COVID portfolio transformation. These are not operators who chase growth at any price. They sold Houston hotels before the oil crash fully materialized. They maintained conservative leverage when competitors were levering up. They navigated the pandemic without the distressed asset sales or dilutive equity offerings that hobbled several peers. And in the recovery, they've been willing to sell strong assets—like the Kimpton portfolio and the Residence Inn Boston Cambridge—when the price was right and the proceeds could be better deployed elsewhere. This is the kind of capital allocation discipline that, in other industries, earns management teams premium valuations.

The portfolio is now positioned squarely for the demand patterns that emerged from the pandemic. Xenia's properties in leisure-oriented markets like Nashville, Scottsdale, San Diego, and Santa Barbara are capturing the "bleisure" trend—business travelers extending trips for leisure, remote workers choosing attractive destinations, and leisure travelers willing to pay premium rates for quality experiences. The growing luxury exposure, now roughly thirty-seven percent of portfolio value, positions the company in the segment with the strongest pricing power and the most resilient demand. Group revenue pace up fifteen percent for 2026 suggests that convention and meeting business, the last piece of the demand recovery, is finally materializing.

The balance sheet provides genuine optionality. With total liquidity around $640 million, net debt to EBITDA of approximately 4.6 times, and no near-term debt maturities that threaten the company's stability, Xenia can play offense when opportunities arise. The share repurchase program—$120 million deployed in 2025 at an average price well below estimated NAV—demonstrates management's willingness to use that flexibility aggressively when they believe the stock is undervalued. The quarterly dividend increase to $0.14 per share signals confidence without overcommitting cash flow.

The valuation itself is perhaps the strongest element of the bull case. Xenia trades at an estimated twenty to thirty percent discount to its net asset value, meaning investors can buy the portfolio for significantly less than the cost of assembling it in the private market. For a patient investor willing to wait for the valuation gap to close—whether through stock price appreciation, private equity takeout, or strategic merger—the current price offers a meaningful margin of safety.

The bear case, however, is equally compelling—and begins with the structural challenges that no management team, however skilled, can fully overcome. Xenia operates in a commodity business without meaningful competitive moats. The company has no consumer brand, no network effects, no switching costs, and no scale advantages. Its single competitive power—process excellence in capital allocation—is the most fragile form of advantage, dependent on the continued tenure and judgment of specific individuals rather than embedded in the business's structure.

The size question is real. At $1.3 billion in market capitalization, Xenia is a small-cap stock that struggles for investor attention. Institutional investors who want hotel REIT exposure gravitate toward Host Hotels, which offers superior liquidity and analyst coverage. Smaller investors seeking yield can find it in larger, more diversified REITs. Xenia occupies an awkward middle ground—too small to be a core holding, too illiquid for many institutional mandates, too operationally complex for yield-focused retail investors.

Recession vulnerability looms as a permanent overhang. If business travel weakens—whether from economic downturn, further adoption of video conferencing, or corporate cost-cutting—RevPAR at Xenia's urban and convention-oriented properties would decline sharply. The leisure segment, while currently robust, is ultimately discretionary: consumers cut travel spending when the economy softens. The operating leverage that magnifies upside in good times would work in reverse, compressing margins and potentially forcing another dividend cut.

Labor cost inflation appears structural rather than cyclical. The hospitality industry's workforce has never fully recovered from the pandemic exodus, when millions of hotel workers found employment in other sectors and never returned. Wages have risen permanently, and Xenia's properties—particularly those in markets with high costs of living—face ongoing pressure on the largest line item in their operating budgets.

The capital intensity treadmill never stops. Brand PIPs, which can cost tens of millions per property, continue to come due. The Fairmont Dallas sale in 2025 was explicitly motivated by the property's need for a costly renovation that management concluded wouldn't generate sufficient returns—a reminder that hotel ownership involves a perpetual cycle of spending to maintain competitive relevance. Free cash flow after maintenance capital expenditures is considerably lower than headline FFO suggests, and this is the money actually available for dividends, buybacks, debt reduction, or growth.

Perhaps most challengingly, hotel REITs as a sector have traded at persistent NAV discounts for years, and there is no obvious catalyst for this to change. The discount isn't a temporary market inefficiency—it reflects a rational investor preference for real estate without operational risk. Data centers, cell towers, industrial warehouses, and even self-storage facilities offer more predictable cash flows, lower capital intensity, and stronger secular tailwinds. Until the investment community's preference structure changes, hotel REITs may continue to trade at discounts regardless of how well individual companies execute.

For investors evaluating Xenia, two key performance indicators matter above all others. The first is same-property RevPAR growth, which captures the organic revenue trajectory of the portfolio and reflects both pricing power and demand trends. This single metric encapsulates everything from market positioning to brand effectiveness to competitive dynamics. The second is adjusted FFO per share, which measures the cash earnings available to shareholders after accounting for the company's capital structure and share count. Together, these two numbers tell you whether Xenia's portfolio is getting better at generating revenue and whether that revenue improvement is translating into actual shareholder value.

XIII. Lessons & Playbook Themes

Xenia's story distills into a handful of lessons that extend well beyond the hotel industry—truths about capital allocation, cyclical businesses, and the tension between operational quality and structural advantage.

The first and most important lesson is that in commodity businesses, capital allocation is everything. When your product is essentially interchangeable with competitors'—when a guest can substitute your Marriott for the Marriott across the street without meaningful friction—the only durable advantage comes from how you deploy capital. Which assets do you buy, at what prices, in which markets? Which do you sell, and when? How much do you invest in renovation, and does that investment generate measurable returns? How do you balance dividends, buybacks, debt reduction, and growth? Xenia's management team has answered these questions consistently well for more than a decade, and that consistency is the foundation of whatever investment case exists for the company.

The second lesson is that a fortress balance sheet is a competitive weapon in cyclical industries. Conservative leverage isn't exciting. It doesn't generate headlines or attract momentum investors. But when the cycle turns—and in the hotel industry, the cycle always turns—the company with liquidity and low leverage survives, while overleveraged competitors are forced into distressed sales, dilutive financing, or outright failure. Xenia's pandemic survival was not a matter of luck or government bailouts. It was the direct result of balance sheet decisions made years earlier, when management chose to forgo the growth that higher leverage could have financed in favor of the resilience that lower leverage provided.

The third lesson is about strategic self-awareness. Xenia's management knew what kind of company they were—and, more importantly, what kind they weren't. They weren't Host Hotels, with the scale to dominate the luxury segment. They weren't Apple Hospitality, with hundreds of economy properties generating steady, low-volatility cash flows. They were a mid-cap hotel REIT that needed to compete on portfolio quality, market selection, and asset management intensity rather than size. The focus on select-service initially, and then the deliberate move up-market into luxury and upper upscale, reflected a realistic assessment of where the company could win rather than an aspirational desire to be something it couldn't be.

The fourth lesson concerns adaptability. The post-pandemic portfolio transformation was not incremental. Xenia sold hundreds of millions of dollars of properties in markets and segments that had been core to its identity, and reinvested in a fundamentally different portfolio mix. Management didn't cling to the pre-COVID thesis out of sunk-cost bias or institutional inertia. They reassessed the landscape, identified the permanent changes, and acted decisively. This willingness to kill your own thesis when the evidence demands it is one of the rarest and most valuable qualities in corporate leadership.

The fifth lesson is structural and perhaps the most uncomfortable: sometimes there is no moat, and that's okay. Not every successful company needs to fit neatly into a competitive advantage framework. Xenia has no network effects, no meaningful scale economies, no consumer brand, and no switching costs. Its success—to the extent it has been successful—comes from doing ordinary things extraordinarily well: buying right, selling right, renovating right, managing right. This is process power in its purest form, and while it is the most fragile and least sustainable of Hamilton Helmer's seven powers, it is real.

The sixth lesson touches on the gap between quality and valuation. Xenia is, by most operational measures, a well-run company. Its RevPAR growth is competitive. Its margins are expanding. Its balance sheet is clean. Its management team is credible and disciplined. And yet the stock has underperformed its IPO price for more than a decade. This is a reminder that business quality and investment returns are not the same thing—that a good company in a structurally challenged sector can remain undervalued for far longer than fundamental analysis would suggest. For investors, the question is whether patience will eventually be rewarded, or whether the sector's structural headwinds will permanently prevent the valuation gap from closing.