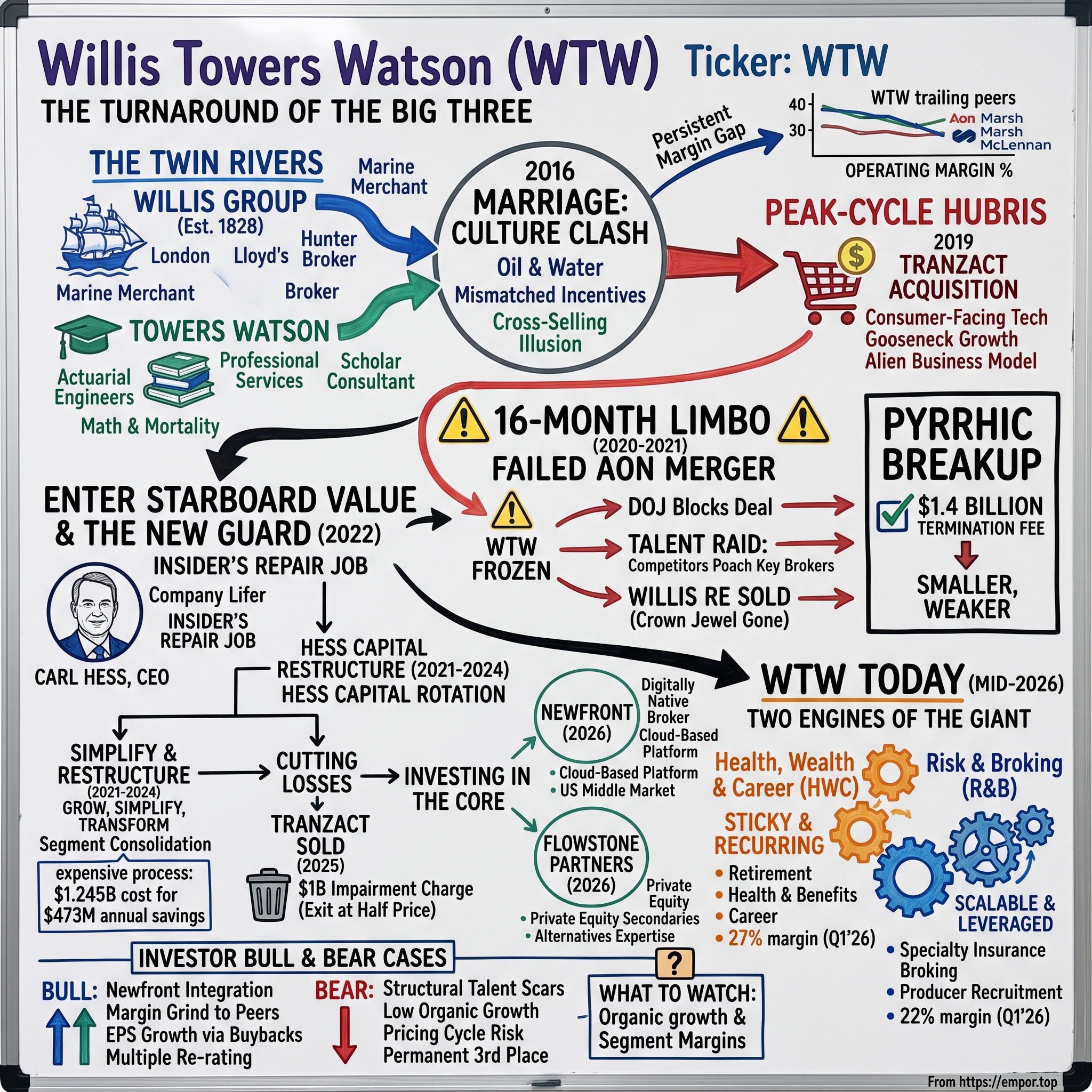

Willis Towers Watson (WTW): The Turnaround of the Big Three

I. Introduction: The Billion-Dollar Breakup & The Underdog of the "Big Three"

Picture the boardroom energy in March 2020. The world is locking down against a pandemic, equity markets are in free-fall, and yet two of the largest insurance brokers on the planet decide this is the moment to attempt the biggest deal their industry has ever seen. Aon and Willis Towers Watson announce a roughly $30 billion all-stock combination that would vault the merged company past Marsh McLennan to become the single largest insurance and advisory broker on Earth. For sixteen months, the deal hangs in the air like a held breath. Then, in July 2021, it collapses. The U.S. Department of Justice sues to block it, the companies walk away, and Aon writes WTW a check for a $1.4 billion termination fee.1[^2]

Here is the uncomfortable truth that the check could not paper over: for WTW, the breakup fee was a bandage on a business that had been quietly bleeding out. During those sixteen months of regulatory limbo, WTW was effectively frozen. It could not deploy capital aggressively, could not reassure its people that they had a future, and could not fight back when rivals came hunting. And they came hunting. Competitors treated WTW's producer roster like an open buffet, walking off with hundreds of the revenue-generating brokers who are, quite literally, the business. A broker's book of clients follows the broker. When the broker leaves, the commissions leave too.

WTW today, in mid-2026. What remains is still a giant. WTW carries a market capitalization of roughly $27 billion and generates about $9.7 billion in annual revenue.7 It runs on two engines. The first is Health, Wealth & Career (HWC) — the actuaries, benefits designers, and retirement consultants who tell the world's largest corporations how to fund pensions and structure employee benefits. The second is Risk & Broking (R&B) — the commercial insurance brokers who place property, casualty, cyber, aviation, and marine coverage for corporate clients. One engine is sticky, recurring, and slow. The other is scalable, high-margin, and hyper-sensitive to talent. Understanding WTW means understanding why those two engines have never quite fired in sync.

The core paradox. For years, WTW has traded at what can only be called an underperformance discount. Its operating margins have chronically trailed those of its larger "Big Three" peers, Marsh McLennan and Aon. Investors have long argued about which WTW they own: a permanent value trap, structurally condemned to third place — or a genuine operational turnaround, mid-repair, under a CEO who spent his entire career inside the company. That is the question this story is built to test, not to answer for you.

The roadmap. To get there, we trace two very different rivers that met in 2016 — a swashbuckling London insurance broker founded in the age of sailing ships, and a buttoned-down actuarial consultancy. We examine the controversial merger that fused them, the peak-cycle acquisition of a Medicare marketing machine that would later be written down by the billions, the failed Aon merger and the talent raid it triggered, the arrival of activist Starboard Value, and the high-stakes capital rotation engineered by CEO Carl Hess — selling the Medicare business at a fire-sale price while buying a Silicon Valley-born broker and a private-equity secondaries specialist. Then we dig into the segment economics, stress-test the management narrative against its own earnings calls, and lay out the bull and bear cases through the lens of competitive strategy. It begins, as so many financial stories do, on the water.

II. The Twin Rivers: Willis Group & Towers Watson

The marine merchant. In 1828, a 28-year-old named Henry Willis hung out his shingle in London.12 He was not, at first, an insurance man at all — he was a merchant, selling imported goods on commission. But London in the early nineteenth century was the beating heart of global maritime trade, and where cargo moved, risk followed. Ships sank. Cargoes rotted. Pirates and storms and simple bad luck could erase a fortune between ports. Merchants needed someone to stand between them and ruin, and the mechanism for that was Lloyd's of London, the coffee-house-turned-marketplace where underwriters wrote coverage on ships and their cargo. Willis moved naturally into brokering marine hull insurance for the very goods he was already trading.12

Over the following decades, the firm grew by merger, the way great London houses did. It combined with the Faber family operation in 1898 to become Willis Faber, and then absorbed Dumas & Wylie in 1928 to become Willis Faber & Dumas.12 This was no longer a one-man commission shop; it was becoming a global brokerage with genuine specialty muscle. Willis helped pioneer the aviation insurance market as flight went from novelty to industry, and its name is stitched into one of the most famous casualties in maritime history — the firm brokered the hull coverage on the RMS Titanic, whose loss in 1912 produced a million-dollar claim that Lloyd's paid out. The cultural DNA laid down in those years is worth naming, because it never left: high-energy, transaction-driven, relationship-heavy, and built around individual producers who live and die by the deals they close. A Willis broker was a hunter.

The actuarial engineers. Now cross the river to an entirely different temperament. The other half of the story descends from a lineage of actuaries — the mathematicians of mortality and money. Its threads run back to a nineteenth-century London actuarial practice and wind through the twentieth century in the United States. The Wyatt Company was founded in 1943; Towers, Perrin, Forster & Crosby traced to a 1934 reinsurance and pension practice. Watson Wyatt, itself the product of a transatlantic actuarial pairing, merged with Towers Perrin in 2010 to form Towers Watson — a professional-services behemoth that became one of the world's definitive authorities on pension actuarial work, corporate benefits design, executive compensation, and human-capital advisory.

If the Willis broker was a hunter, the Towers Watson consultant was a scholar. This was a world of billable hours, multi-year advisory relationships, deep technical credentials, and high-headcount professional stability. You did not close a Towers Watson engagement over a handshake and a lunch; you won it over months of analysis, and then you kept it for a decade because unwinding a Fortune 500 company's pension model is nobody's idea of a fun afternoon.

The DNA mismatch. Hold these two cultures side by side, because the tension between them explains almost everything that follows. Broking rewards individual swagger, tolerates volatility, and pays for the relationships a producer carries in their head. Consulting rewards institutional rigor, punishes volatility, and monetizes expertise that lives in systems and teams. One is a sales culture; the other is a professional-services culture. Merging them would promise the best of both — and risk the immiscibility of oil and water. In January 2016, that experiment began.

III. The 2016 Marriage: Culture Clash & The Cross-Selling Illusion

The deal that almost didn't happen. The architect of the merger was John Haley, the CEO of Towers Watson — an actuary by training and a dealmaker by inclination. In mid-2015, Haley engineered what was billed as a "merger of equals" between Willis Group and Towers Watson, an all-stock transaction valued at roughly $18 billion that would create a firm of some 39,000 employees across 120 countries with more than $8 billion in revenue.11 On paper, it was elegant symmetry: Willis shareholders would own approximately 50.1% of the combined company and Towers Watson shareholders 49.9%.11 Haley would run it.

There was just one problem. Towers Watson's own shareholders looked at the terms and revolted. They felt they were handing over their premier actuarial franchise too cheaply, and in November 2015 the deal wobbled as investors signaled they would vote it down. To rescue it, the companies sweetened the offer with a special cash dividend to Towers Watson shareholders — raised, under pressure, to $10.00 per share — that tilted the overall economics back toward the Towers Watson side and got the vote across the line. The merger completed on January 5, 2016.11 That a "merger of equals" required a special dividend and a near-death vote to survive was the first hint that the two sides valued the union very differently.

The financial realpolitik. Two features of the structure deserve attention because they reveal the real logic of the deal. First, the tax inversion. Willis had already relocated its incorporation to Ireland in 2010, and the combined company kept its tax base there — a meaningful advantage when Ireland's corporate tax rate sat far below the roughly 34% Towers Watson had been paying in the United States.11 A large slice of the deal's promised value was not operational at all; it was fiscal. Second, the synergy story. Management sold investors on cross-selling: pitch Willis's corporate insurance broking to Towers Watson's blue-chip pension and HR clients, and pitch Towers Watson's benefits consulting into Willis's broking relationships. The named cost synergies were relatively modest, on the order of $100-125 million from duplicate-cost reductions.11 The revenue synergies — the exciting part — were the part that depended on culture.

The silos that wouldn't merge. And culture is exactly where the theory broke down. The aggressive, commission-driven brokers of legacy Willis and the conservative, billable-hour consultants of legacy Towers Watson did not naturally trade leads or share clients. A broker who spent years cultivating a risk manager had little incentive to hand that relationship to a pension actuary, and vice versa. Cross-selling, the crown jewel of the merger thesis, turned out to be far easier to draw on a slide than to execute across two incompatible incentive systems. Meanwhile, the newly combined firm inherited legacy headaches, including litigation tied to Willis's historical role in the Stanford Financial Ponzi scheme, which Willis agreed to help settle for $120 million in 2016.10

The scoreboard told the story. Through the back half of the 2010s, WTW's operating margins hovered roughly in the 15-19% range, while Marsh McLennan ran near the mid-20s and Aon pushed toward the high-20s. In a business where the three giants sell broadly similar services to broadly the same clients, a persistent margin gap of eight to ten points is not noise — it is a verdict on execution. WTW had become the structural laggard of the Big Three, and management's answer to a growth problem would soon make matters worse.

IV. Peak-Cycle Hubris: The $1.3 Billion Tranzact Acquisition

The pivot to the consumer. By 2019, John Haley faced a familiar corporate predicament: a mature, slow-growing professional-services firm hunting for a faster top line. His answer was a sharp turn away from everything WTW knew how to do. In July 2019, WTW acquired TRANZACT, a direct-to-consumer digital brokerage that generated Medicare and health-insurance leads and sold policies to individual American retirees, for roughly $1.3175 billion.4 Overnight, a firm built to advise Fortune 500 benefits departments now owned a performance-marketing machine that bought Google and television ads to reel in 65-year-olds shopping for Medicare Advantage plans.

The strategic mismatch. It is hard to overstate how alien this business was to WTW's core. Institutional B2B advisory runs on long sales cycles, deep expertise, and sticky multi-year relationships. Direct-to-consumer Medicare marketing runs on the opposite physics: high velocity, high customer-acquisition cost, high attrition, and brutal sensitivity to advertising efficiency and regulatory rule changes. The value of a Medicare lead-generation business rises and falls with things WTW had no experience managing — the cost of digital ad inventory, call-center conversion rates, and the annual enrollment window that concentrates the whole year into a few frantic weeks. Bolting that onto an actuarial consultancy was less a synergy than a category error.

The valuation trap. Timing compounded the problem. WTW paid a tech-enabled, growth-multiple price for a consumer-acquisition business near the top of a cycle, on the implicit assumption that Medicare lead generation would keep compounding at a rich rate. Instead, the business proved more capital-intensive and more competitive than the deal model assumed. Sustaining lead flow required ever-rising marketing spend, and the economics of insurers paying brokers for Medicare enrollments came under pressure as carriers tightened commissions and regulators scrutinized the sector. What had looked like a growth engine started to look like a treadmill that required more and more spending just to stand still.

The lesson. Tranzact became a textbook illustration of a specific kind of value destruction: buying a non-core, consumer-facing asset primarily to goose a company's reported growth rate, and paying a premium for the privilege. The revenue it added was real, but it was low-quality — cyclical, capital-hungry, and disconnected from any durable advantage WTW possessed. Investors would ultimately pay for the mistake twice: once in the purchase price, and again, years later, in the impairment charges required to admit the error. But that reckoning would fall to Haley's successor. First, WTW would spend sixteen months betting the entire company on a merger that never happened.

V. The 16-Month Limbo: The Failed Aon Merger & The Great Talent Raid

The announcement. In March 2020, as COVID-19 shuttered the global economy, Aon and WTW stunned the industry by announcing a roughly $30 billion all-stock combination. The logic, from Aon's side, was audacious and clear: swallowing WTW would leapfrog Marsh McLennan and make Aon the largest broker in the world, with unmatched scale in commercial risk, reinsurance, and health and benefits. For WTW's John Haley, it was an elegant exit — sell the structural laggard into a premium franchise and let Aon's operators harvest the synergies. It was the kind of deal that looks unbeatable in a pitch and becomes a slow-motion trap in practice.

The paralysis. Because here is what a sixteen-month regulatory review does to a company: it freezes it in amber. Under merger agreements and antitrust protocols, WTW could not run its business as if it were free. Aggressive hiring, bold capital deployment, and strategic pivots were all constrained by the need to preserve the deal and avoid antitrust complications. Every WTW employee spent a year and a half not knowing who would sign their paychecks, whether their division would be sold to satisfy regulators, or whether their internal rival at Aon would end up as their boss. Uncertainty of that duration is corrosive in any company. In a business whose primary assets walk out the door every evening, it is nearly fatal.

The great talent raid. Rivals understood this perfectly, and they pounced. Arthur J. Gallagher, Lockton, Marsh, and a swarm of aggressive middle-market and regional brokers descended on WTW's roster, dangling guaranteed pay packages at star producers and senior consulting partners who had every reason to jump. Why stay at a firm about to be dismembered when a competitor would pay top dollar for your book of business and your certainty? Hundreds of revenue-generating brokers left, and each departure was a double blow — WTW lost the producer and, in many cases, the clients and commission streams that producer controlled. This is the hidden cost that never appeared in the merger math: the deal's mere pendency was hollowing out the asset being sold.

The DOJ steps in. In June 2021, the U.S. Department of Justice filed a civil antitrust lawsuit to block the combination, arguing it would eliminate competition in commercial property and casualty broking for large corporations, in reinsurance broking, and in health-benefits consulting — markets already concentrated among a handful of global players.[^2] Rather than fight a protracted courtroom battle with an uncertain outcome, the companies capitulated. In July 2021, Aon and WTW terminated the merger, and Aon paid WTW a $1.4 billion termination fee.1

The Pyrrhic breakup. Now for the cruelest twist. To grease the deal through regulators, WTW had already agreed to sell its crown jewel — Willis Re, its treaty reinsurance brokerage — to Arthur J. Gallagher for $3.25 billion, a divestiture that completed in December 2021.2 Reinsurance broking is the business of arranging insurance for insurers, and it is one of the most prestigious, high-margin, relationship-dense corners of the entire industry, dominated globally by just three franchises: Aon's Reinsurance Solutions, Marsh's Guy Carpenter, and Willis Re. When the Aon deal died but the Willis Re sale did not, WTW was left with the worst of all worlds. It had shed its scaled reinsurance division to clear a merger that never closed, structurally hollowing out its Risk & Broking segment and surrendering a seat at one of the industry's most valuable tables. The $1.4 billion fee was real money, but it did not buy back Willis Re, and it did not un-poach the producers. WTW emerged from limbo smaller, weaker, and demoralized — and it emerged straight into the sights of an activist investor.

VI. Enter Starboard: Carl Hess's Capital Cleanup & Restructuring Realpolitik

The activist arrives. In late October 2021, with WTW reeling, Starboard Value — the activist fund run by Jeff Smith, a man with a long record of forcing complacent boards into action — disclosed a material stake in the company.3 Starboard did not arrive quietly. It circulated a pointed critique of WTW's long history of poor execution, unmet promises, and margin underperformance relative to Marsh McLennan and Aon, and it argued that the gap was not destiny but the product of a bloated, poorly run organization. The activist thesis was blunt: WTW was a good set of franchises trapped inside a badly managed company, and the fix was operational discipline, margin expansion, and aggressive capital return. For a management team that had just presided over a failed merger and a talent exodus, the arrival of Jeff Smith was the corporate equivalent of a fire alarm.

The new guard. John Haley retired, and on January 1, 2022, Carl Hess became CEO. Hess was, in every sense, a company lifer — an actuary who had joined the Watson Wyatt lineage in 1989 and spent more than three decades inside the firm, most recently running the Investment, Risk, and Reinsurance segment. This cut both ways. On one hand, he knew where every operational body was buried and needed no learning curve. On the other, an insider promoted after a period of underperformance is precisely the kind of "more of the same" choice activists tend to distrust. Hess's job was to prove that a lifer could act like an outsider — to cut, simplify, and reallocate capital with a discipline the company had never shown.

Grow, Simplify, Transform. The centerpiece was a multi-year restructuring program branded "Grow, Simplify, Transform," running from 2021 through 2024. Its explicit goal was to expand WTW's margins toward peer levels by stripping out cost and consolidating a sprawl of legacy silos. The headline outcome, disclosed across the program's life, is worth sitting with: WTW spent roughly $1.245 billion in cumulative program costs and capital expenditure to achieve about $473 million in run-rate annual cost savings.[^15] That is a cost-to-benefit ratio of roughly 2.6 times — you had to spend $2.60 to remove $1.00 of recurring cost. On one reading, that is a program delivering real, durable savings. On another, and the more revealing one, the sheer expense of extracting those savings is itself a confession: it measures just how much operational fat and structural complexity had accumulated inside WTW over the years. Efficient companies do not have $473 million of easy cost lying around; the price of removing it is the receipt for how inefficient the starting point was. The program also delivered the "Simplify" promise, collapsing WTW's legacy business units into two clean reporting segments — HWC and R&B — the structure the company runs on today.

The Hess capital rotation. Cost-cutting was only half the playbook. The more consequential — and more debatable — part was a wholesale rotation of WTW's capital, in which Hess reversed his predecessor's biggest bet and placed new ones of his own.

The first move was to admit the Tranzact mistake in full. In October 2024, WTW agreed to sell TRANZACT to private-equity firm GTCR and technology investor Recognize for roughly $632.4 million, with the deal completing in January 2025.4 Set that against the roughly $1.3175 billion WTW had paid in 2019, and the arithmetic is stark: the company exited at less than half its purchase price, and in connection with the divestiture it recorded more than $1 billion in impairment charges to write the asset down to reality.47 Roughly $700 million of shareholder capital, plus years of management attention, was destroyed in the round trip. Hess deserves credit for cutting a losing position rather than defending it indefinitely — but the loss itself is a permanent mark on the company's capital-allocation record, and no amount of decisive exiting changes that the money is gone.

The second move rotated that freed-up capital back toward technology — but this time in WTW's core B2B world rather than the consumer wilderness. In late 2025, WTW agreed to acquire Newfront, a San Francisco-based, venture-backed, digitally native commercial insurance broker focused on the U.S. middle market and high-growth sectors like technology, fintech, and life sciences. The deal, which completed on January 27, 2026, was structured for up to roughly $1.3 billion: about $1.05 billion upfront (roughly $900 million in cash and $150 million in equity paid to Newfront's employee-shareholders) plus up to $250 million in contingent, largely equity-based earn-outs tied to performance, with additional upside for outperformance.5 Newfront's co-founder and CEO, Spike Lipkin, joined WTW to drive integration.5 The strategic bet is that a modern, cloud-native broking platform can win the tech-forward middle-market clients that legacy brokers struggle to serve efficiently.

The third move, in April 2026, was quieter but telling. WTW completed the acquisition of FlowStone Partners, a specialist in private-equity secondaries — the business of buying and selling existing stakes in private-equity funds — folding it into the Investments business inside HWC.6 The deal price was not disclosed.6 The logic is to inject high-margin alternative-asset capabilities into WTW's wealth and investment advisory, giving both institutional clients and individual wealth investors access to private markets. Three deals, one pattern: sell the low-quality growth, buy higher-quality capabilities, and dare investors to believe that this management team has finally learned to allocate capital well. Whether it has depends on how the two engines actually perform.

VII. Segment Deep Dive: The B2B Engine vs. The Consulting Machine

The architecture. Strip WTW down to its chassis and you find two businesses of nearly equal size but opposite temperament, together producing about $9.7 billion of revenue in fiscal 2025.7[^13] Understanding how each makes money — and where each is fragile — is the key to the whole investment question.

Health, Wealth & Career: the consulting machine. HWC is the larger engine, at roughly 54% of revenue, or about $5.25 billion in fiscal 2025.7 Think of it as three related advisory practices. Retirement is the classic actuarial work — telling corporations how to fund and manage pension obligations, a service governed by regulation and mathematics that clients cannot simply switch off. Health & Benefits designs and administers the medical and insurance benefits that large employers offer their workforces. Career handles compensation benchmarking, workforce design, and human-capital advisory. The economics here are the good kind of boring: highly recurring, multi-year, sticky, with extremely low client churn, because once a company's benefits administration and pension actuarial systems are woven into its HR infrastructure, ripping them out is a nightmare few executives volunteer for. The trade-off is that this is human-capital-intensive work — you grow it by adding consultants, which limits operating leverage and caps organic growth at a modest pace.

In the first quarter of 2026, HWC delivered about 3% organic revenue growth and an operating margin of 27.3%, up roughly 60 basis points year over year.[^8]8 That margin is genuinely strong, and management attributes part of the improvement to the "clean" simplicity of the post-Tranzact portfolio. But the growth number hides real cross-currents. On the Q1 2026 call, management noted that Health grew on international new business and renewals, and Wealth grew on higher retirement work and the Investments business — while Career actually declined, as clients deferred discretionary consulting projects amid geopolitical uncertainty and softening advisory demand in North America.8 That is the tell of a consulting business: the sticky, mandated work keeps compounding, but the discretionary advisory revenue is cyclical and gets cut the moment corporate clients grow cautious.

Risk & Broking: the B2B engine. R&B is the smaller engine at roughly 45% of revenue, or about $4.33 billion in fiscal 2025, but it is arguably the more valuable one to the equity story.7 This is corporate insurance broking — placing property and casualty coverage and specialty lines like aviation, marine, cyber, and financial lines for commercial clients — and its economics are structurally superior to consulting in one crucial respect: operating leverage. Broker compensation is tied to commissions and fees that rise with the insurance premiums placed, and because the cost of placing one more policy is low, incremental revenue drops toward the bottom line at a high rate. It is a more scalable, more capital-light business than consulting, which is exactly why commercial brokerage commands a premium valuation across the industry.

In the first quarter of 2026, R&B posted about 2% organic growth with an operating margin of 22.6%, up roughly 60 basis points year over year — though management acknowledged that a meaningful chunk of the reported improvement came from foreign-exchange tailwinds rather than pure operating gains.[^8]8 Reported R&B revenue rose about 9%, but strip out currency and the organic figure was the soft 2%.[^8] That gap between a flattering reported number and a modest organic one is where a skeptical investor should focus.

The battleground: producers. Here is the mechanism that makes or breaks R&B, and it is intensely human. A commercial broker's value lives in personal relationships with corporate risk managers built over years of renewals, claims, and trust. When a star producer leaves, the millions in premium commissions they control tend to follow them out the door — which is precisely the wound WTW suffered during the Aon limbo. Rebuilding that pipeline is not a matter of a memo; it is years of recruiting experienced producers, onboarding them, and waiting for their books to migrate and season. Hess has invested heavily in exactly this specialized recruitment since 2022, hiring middle-market producers to refill the ranks. But there is an unavoidable lag between paying to hire a producer and seeing that producer's clients show up as revenue — and as we will see, the length of that lag is precisely the thing Wall Street can no longer get management to pin down.

VIII. Investor Q&A & Narrative Stress Test

The elephant in the room. Every earnings call has a question management would prefer not to answer, and for WTW in 2026 it is disarmingly simple: why is the growth so slow? In the first quarter of 2026, WTW reported roughly 3% organic growth overall — about 3% in HWC and 2% in R&B — while Marsh McLennan, Aon, and Arthur J. Gallagher have been posting mid-to-high single-digit organic growth quarter after quarter.[^8]8 In an industry riding the same favorable currents — a multi-year hardening of commercial insurance pricing that lifts commissions for everyone — WTW is consistently rowing slower than the peers sitting in the same river. Some of that is the lingering scar tissue from the talent raid; some of it is the loss of Willis Re; and some of it, critics argue, is chronic underinvestment in the sales engine. Distinguishing among those explanations is the analytical crux.

Where management leaned, where analysts pushed. Reading the Q4 2025 and Q1 2026 calls side by side is instructive, because the choreography is consistent.89 CEO Carl Hess and CFO Andrew Krasner steer toward the topics that flatter the story: the Tranzact divestiture as "clearing the decks," the margin expansion in both segments, the strong capital returns, and the high-margin promise of integrating Newfront's technology. Analysts from firms including Wells Fargo, Goldman Sachs, and Evercore steer the other way — pressing on the deceleration in North American Risk & Broking, probing whether the commercial pricing cycle is finally peaking (which would remove a tailwind WTW has leaned on), and questioning whether the company has under-resourced its pipeline relative to Gallagher's relentless hiring machine.

The revealing moments are where the answers turn vague. Management has been notably imprecise about the single question that most determines the thesis: exactly when the wave of middle-market producer hiring in 2023 and 2024 will convert into measurable domestic market-share gains. "It takes time" is true, but it is not a schedule, and the repeated absence of a concrete timeline — call after call — is itself a data point. When a management team can quantify its cost savings to the last basis point but cannot quantify when its most important growth investment will pay off, an investor is entitled to weigh that asymmetry.

Credibility and skin in the game. The case for trusting this turnaround rests substantially on incentives, and here the record is mixed rather than damning. Hess's compensation ran to roughly $12.5 million in 2024, with a long-term incentive plan tied to adjusted operating-margin hurdles and cumulative free-cash-flow generation — metrics that are at least aligned with what the turnaround is supposed to deliver.[^12] He holds roughly 115,000 shares, worth on the order of $33 million in mid-2026, which is real alignment.[^12] But it is worth naming the limitation: Hess is a career executive defending and repairing a franchise he helped build, not a founder with his net worth and identity fused to the outcome. That does not make him wrong, but it shapes the psychology of the decisions.

The capital-allocation ledger. On behavior over time, the scorecard has genuine entries on both sides. In the credit column: enormous capital returns, including roughly $1.65 billion of share repurchases in 2025, with a target of more than $1.0 billion for 2026 and about $300 million completed in the first quarter.[^8]7 Buybacks at that scale meaningfully shrink the share count and can drive adjusted EPS growth even when revenue growth is pedestrian — which is, candidly, a large part of how WTW is generating double-digit EPS gains off low-single-digit organic growth. In the debit column: the restructuring program's expensive 2.6-times cost-to-benefit ratio, and the roughly $700 million of value vaporized in the Tranzact round trip. A fair reading is that this management team has become a disciplined returner of capital and a decisive cutter of past mistakes, but its record as an acquirer — the very skill on which the Newfront and FlowStone bets now depend — remains unproven at best and negative at worst. That tension carries directly into how the business is defended.

IX. Playbook: Porter's 5 Forces, Hamilton Helmer's 7 Powers & Risk Radar

Porter's Five Forces. Start with the industry structure, because it is unusually favorable and explains why all three giants earn good returns despite mediocre growth. Barriers to entry are high — a global broker needs licensing across scores of jurisdictions, deep compliance infrastructure, worldwide distribution, and proprietary actuarial and risk data accumulated over decades. No venture-backed startup is going to place the global property program for a multinational conglomerate next year. Buyer power is moderate to high — the world's largest corporations can and do squeeze fees, but switching brokers mid-relationship is operationally painful and risky, which blunts that leverage. Competitive rivalry, however, is ferocious. The battle among Marsh McLennan, Aon, WTW, and Gallagher for star producers and marquee corporate accounts is relentless and expensive, and it is precisely this rivalry — the bidding war for talent — that transferred so much value away from WTW during its period of weakness. The threat of substitutes and supplier power (the insurance carriers themselves) round out a structure that protects incumbents collectively while pitting them viciously against one another.

Helmer's 7 Powers. Now the harder question: within that structure, what durable advantages does WTW specifically hold? The most credible is switching costs, concentrated in HWC. Once a large employer embeds WTW's benefits administration or pension actuarial systems into its core HR machinery, migrating to a competitor means re-plumbing critical infrastructure that touches every employee — expensive, disruptive, and rarely worth it. This is the strongest and most defensible power in WTW's portfolio, and it is why HWC's revenue is so sticky and its margins so resilient. Weaker is scale economies in R&B: WTW's global footprint lets it negotiate specialized underwriting capacity with carriers, but this power was structurally diminished the day Willis Re walked out the door, leaving WTW sub-scale against Aon and Marsh in reinsurance. Most speculative is counter-positioning — the Newfront bet. The hope is that Newfront's cloud-native platform lets WTW serve tech-forward middle-market clients in a way legacy, spreadsheet-bound competitors structurally cannot without cannibalizing their existing model. That is a genuine counter-positioning theory, but as of mid-2026 it is a thesis to be proven, not a power WTW demonstrably wields. Notably, WTW does not enjoy meaningful network effects or a branded consumer power; its moat is switching costs and scale, not magic.

The risk radar. Three risks are material rather than decorative. First, a softening insurance pricing cycle: R&B commissions ride on commercial P&C premium rates, so if the multi-year hardening that has flattered the whole industry stalls or reverses, WTW's most valuable engine faces natural revenue pressure — and it would be facing it from a position of slower organic growth than peers. Second, talent-cost inflation: the same competitive rivalry that raided WTW's producers also bids up the price of hiring and keeping them, and rising compensation can quietly erode the very margin gains the $473 million cost program was meant to bank. Third, integration and execution risk: routing over a billion dollars into Newfront reintroduces exactly the hazard that Tranzact embodied. If Newfront's technology does not scale across WTW's legacy systems, or if its entrepreneurial talent chafes inside a large corporation, the deal could become a smaller-scale rerun of the last technology acquisition — and this management's acquisition record gives that fear teeth.

Bull versus bear. The bull case is coherent: Hess integrates Newfront successfully, establishes WTW as the tech-forward middle-market broking leader, and grinds R&B and HWC margins toward the peer range while the buyback machine retires 4-5% of the share count a year. Low-single-digit organic growth plus steady margin expansion plus aggressive repurchases compounds into double-digit adjusted EPS growth, the market re-rates the multiple toward Aon's, and the underperformance discount closes. The bear case is equally coherent and rests on the same facts read differently: the talent scars in R&B prove structural rather than temporary, organic growth stays capped below peers no matter the pricing cycle, Newfront's synergies disappoint, margin expansion stalls once the easy restructuring gains are banked, and WTW remains the permanent third-place giant — a decent business that is a chronically discounted stock, its EPS growth increasingly dependent on buybacks rather than the operating engine.

What to actually watch. Cut through everything and the entire debate collapses onto a small number of observable metrics. The first and most important is Risk & Broking organic revenue growth — the clean, constant-currency figure, stripped of the FX flattery — because it is the single truest gauge of whether the producer-rebuilding investment is converting into share gains and whether the R&B engine is closing the gap with peers. The second is adjusted operating margin in each segment, the direct measure of whether the turnaround's core promise is being delivered and sustained. If those two numbers inflect upward together over the coming quarters, the bull thesis is earning its keep; if organic growth stays stuck in the low single digits while margins plateau, the bear thesis is being confirmed in real time. WTW is a company that has spent a decade explaining why it trails its peers. The next few years will reveal whether Carl Hess's capital rotation finally rewrote that story — or simply added another expensive chapter to it.

References

-

Aon and Willis Towers Watson Terminate $30 Billion Merger — Reuters, 2021-07-26 ↩↩

-

Arthur J. Gallagher to Buy Willis Reinsurance Assets for $3.25 Billion — Reuters, 2021-08-27 ↩

-

Activist Investor Starboard Takes Stake in Willis Towers Watson — WSJ, 2021-10-27 ↩

-

Willis Towers Watson to Sell Tranzact to GTCR and Recognize for $632 Million — Reuters, 2024-10-10 ↩↩↩

-

WTW Completes Acquisition of Newfront — Insurance Journal, 2026-01-27 ↩↩

-

WTW Completes Acquisition of FlowStone Partners — WTW / GlobeNewswire, 2026-04-01 ↩↩

-

WTW Reports Fourth Quarter and Full Year 2025 Earnings — WTW, 2026-02-03 ↩↩↩↩↩↩

-

WTW Q1 2026 Earnings Call Transcript — Seeking Alpha, 2026-04-30 ↩↩↩↩↩

-

WTW Q4 2025 Earnings Call Transcript — Seeking Alpha, 2026-02-03 ↩

-

Willis to Pay $120 Million to Settle Stanford Ponzi Lawsuits — Reuters, 2016-03-23 ↩

-

Willis Group & Towers Watson Agree $18 Billion Merger — Consultancy.uk, 2015-06-30 ↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube