West Pharmaceutical Services: The Hidden Infrastructure of Global Medicine

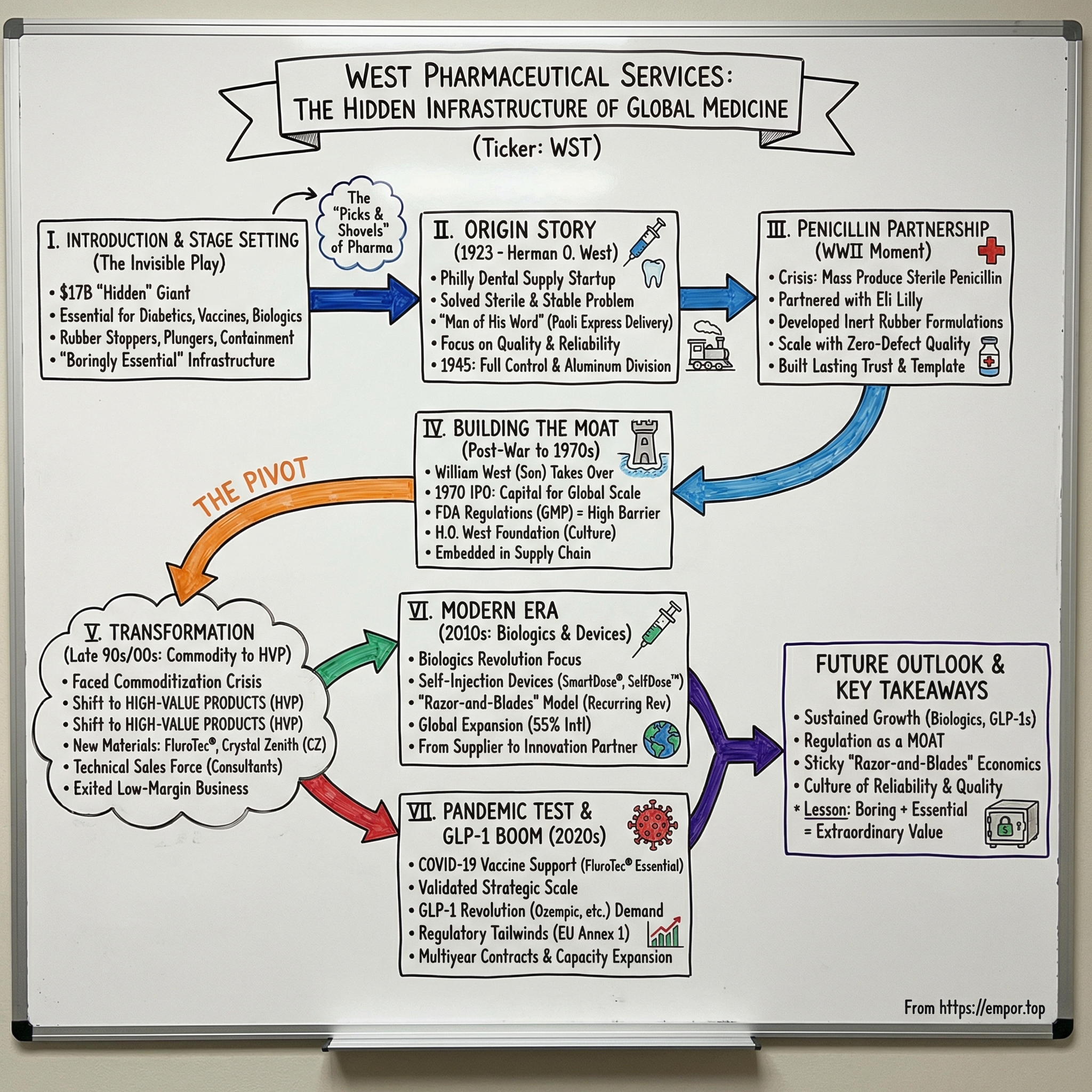

I. Introduction & Stage Setting

Picture this: Every morning, millions of diabetics reach for their insulin pens. Every few weeks, cancer patients receive life-saving biologics through IV drips. In 2021, billions lined up for COVID-19 vaccines delivered through tiny vials. What connects all these moments? A $17 billion company that most people have never heard of—West Pharmaceutical Services.

Walk into any hospital, clinic, or pharmacy in the world, and you're surrounded by West's products, though you'd never know it. Those rubber stoppers sealing vaccine vials? West. The plungers in pre-filled syringes? West. The complex containment systems protecting cutting-edge gene therapies? Also West. They're the ultimate invisible infrastructure play—boring to describe at a cocktail party, but absolutely critical to modern medicine.

Founded in 1923 by a determined entrepreneur named Herman O. West, the company started as a dental supply business in Philadelphia. Herman was manufacturing rubber plungers for dental cartridges when he spotted an opportunity that would define the next century: the emerging pharmaceutical industry needed someone to solve the unglamorous but essential problem of keeping injectable drugs sterile and stable. While everyone else was racing to discover new drugs, Herman decided to own the picks and shovels—becoming the trusted partner for packaging and delivery.

The timing couldn't be more relevant. We're in the midst of a biologics revolution where complex proteins and antibodies are replacing traditional small-molecule drugs. The GLP-1 weight-loss drug boom has created unprecedented demand for self-injection devices. Gene therapies require containment systems that can maintain stability for months. And after COVID-19, the world finally understands that vaccine distribution infrastructure is just as important as vaccine development. West sits at the center of all these trends, yet remains largely unknown outside pharmaceutical circles.

This is the story of how a dental supply startup became the critical infrastructure for the entire injectable drug industry—a century-long journey of strategic positioning, technical excellence, and the power of being boringly essential. It's about recognizing that in healthcare, the companies that enable the miracles often create more value than the miracle-makers themselves.

II. The Herman O. West Origin Story

The man who would revolutionize pharmaceutical packaging learned his most important business lessons from abandonment. When Herman O. West was twelve years old, his father walked out on the family, leaving young Herman to help support his mother and siblings in rural Pennsylvania. That early trauma forged an ironclad principle that would define both the man and his company: always keep your word, always deliver on your promises.

By 1923, Herman had scraped together enough capital to start his own business in Philadelphia. The original West Company was decidedly unglamorous—manufacturing rubber plungers for dental anesthetic cartridges. But Herman possessed a rare combination of technical curiosity and market intuition. While his competitors focused on making cheaper rubber parts, Herman obsessed over quality and reliability. Dentists, he reasoned, would pay a premium for components that never failed during procedures.

The entrepreneurial pivot that would define West's trajectory came through observation. Herman noticed pharmaceutical companies struggling with the same problem that plagued dentists: how to keep injectable medicines sterile and stable. The existing rubber stoppers were inconsistent, often reacting with the drugs they were meant to protect. Herman saw opportunity where others saw a commodity business. These hardships gave Herman a determination and drive that would shape both his character and his company's culture. The phrase "H.O. West was a man of his word" became legendary in pharmaceutical circles. When trucks wouldn't deliver in time, he was known to board the Paoli Express—the fastest way to travel then—carrying boxes of product himself to meet promises.

By 1945, Herman had built enough credibility to make a bold move. He spotted a growth opportunity in aluminum seals and established West's Aluminum Division. This wasn't just product diversification—it was strategic positioning. Herman understood that pharmaceutical packaging would require multiple materials and technologies. While competitors remained focused on rubber, West was already building a multi-material platform.

In 1945, with assistance from Eli Lilly, Herman purchased all shares held by outside stockholders to gain full control. With this control, he obtained financing from Fidelity Bank and began construction of a new manufacturing facility in Phoenixville, Pennsylvania, completed in 1948. The move from the original Philadelphia location represented more than physical expansion—it was Herman's declaration that West would be a major force in pharmaceutical infrastructure.

The numbers tell the story of explosive growth: By 1947, the company produced more than 200 million individual rubber items, including penicillin stoppers, dental plungers, insulin stoppers, and syringes. But Herman's genius wasn't in volume—it was in understanding that each of these products represented a promise. Every stopper that failed meant a contaminated drug. Every plunger that stuck meant a missed dose. In an industry where reliability could mean life or death, Herman positioned West as the company that never failed.

III. The Penicillin Partnership: West's World War II Moment

The telegram arrived at West's Philadelphia headquarters in early 1942: the U.S. government needed help with an urgent wartime crisis. Penicillin, the miracle drug discovered by Alexander Fleming in 1928, could save thousands of soldiers' lives on the battlefield. But there was a massive problem—nobody knew how to package it safely for mass distribution. The drug was incredibly fragile, easily contaminated, and required absolute sterility from production to injection.

During World War II, Herman O. West partnered with Eli Lilly to solve the problem of supplying penicillin in mass quantities for the US Government. This innovation saved many soldiers' lives and has gone on to impact billions of other patients' lives since then. The partnership wasn't just about rubber stoppers—it was about reimagining pharmaceutical logistics at wartime scale.

The technical challenges were staggering. Traditional rubber formulations reacted with penicillin, degrading the antibiotic's potency. Stoppers needed to maintain a perfect seal through temperature extremes—from Arctic supply chains to Pacific island heat. They had to withstand rough handling during transport while maintaining absolute sterility. And they needed to be manufactured by the millions, immediately.

Herman threw West's entire R&D capacity at the problem. His team developed new rubber formulations that were chemically inert to penicillin. They created multi-layer stopper designs that could maintain integrity under extreme conditions. Most importantly, they figured out how to manufacture these complex components at unprecedented scale while maintaining zero-defect quality.

West's relationship with Eli Lilly became crucial. Having just one rubber supplier was a concern for Lilly, as their policy was to have multiple sources for important items. But they didn't need to worry about West. While other suppliers struggled with consistency and delivery, West never missed a shipment. Herman's personal commitment—including those legendary train rides with boxes of stoppers—built trust that would last decades.

The penicillin project transformed West from a specialty supplier into critical wartime infrastructure. By 1944, West was producing millions of stoppers monthly, enabling the mass distribution of penicillin that historians credit with saving over 100,000 Allied lives. But more importantly for West's future, the project established a template: when pharmaceutical companies faced their most complex packaging challenges, they turned to West.

The lessons from the penicillin partnership became West's competitive playbook. First, be there when it matters most—reliability in crisis builds relationships that last decades. Second, solve the hardest problems first—the technical capabilities developed for penicillin created barriers competitors couldn't match. Third, own the infrastructure layer—while others chased blockbuster drugs, West owned the essential components every drug needed.

IV. Building the Moat: Post-War Expansion & Going Public

The post-war pharmaceutical boom of the 1950s and 1960s resembled a gold rush, but Herman West's son William understood a fundamental truth: in a gold rush, the real money isn't in finding gold—it's in selling picks and shovels. As antibiotics, vaccines, and insulin transformed from laboratory curiosities into mass-market medicines, West positioned itself as the essential infrastructure provider for this new industry.

In 1965, William S. West was elected president of The West Company after working for the company for 15 years. That year, sales reached $14 million. One of William's first acts was to create a Corporate Management Committee to lead future development decisions. The transition came at a crucial moment—founder Herman West died after an illness in July 1965.

William inherited more than a company; he inherited a philosophy. Where Herman built through personal relationships and technical excellence, William would add financial sophistication and strategic planning. His vision: transform West from a private family business into a public company capable of global scale.

In 1970, The West Company became publicly held through an initial public offering of $15 per share. The investment money fueled growth, with development of new products including pour-spouts for alcoholic beverages, intravenous packaging solutions, and dispensers for birth control pills. The IPO wasn't just about capital—it was about credibility. Pharmaceutical companies needed suppliers that could match their own growth trajectories and governance standards.

The numbers validated the strategy: Sales grew from $26 million in 1970 to $43 million in 1973, with much of the growth in international and pharmaceutical areas. By 1975, revenue had reached $49.3 million. But the real moat wasn't in the financials—it was in the emerging regulatory environment.

The 1970s brought a wave of FDA regulations that fundamentally changed pharmaceutical manufacturing. Good Manufacturing Practices (GMP) requirements meant that every component touching a drug needed extensive validation, documentation, and quality control. For existing West customers, switching suppliers meant revalidating entire production lines—a process that could take years and millions of dollars. For new entrants, the regulatory burden created an almost insurmountable barrier.

The H.O. West Foundation was formed in 1971 to provide college scholarships for employees' children. This wasn't just corporate charity—it was strategic culture-building. West needed to retain specialized expertise in rubber chemistry, precision manufacturing, and regulatory compliance. The foundation helped build multi-generational loyalty in a business where institutional knowledge mattered.

William West understood that the company's true competitive advantage wasn't in any single product or patent—it was in being embedded so deeply in the pharmaceutical supply chain that extraction became practically impossible. Every new FDA regulation, every additional quality requirement, every validation protocol added another layer to West's moat. By going public, West gained the capital to build global manufacturing redundancy that pharma companies required. By the late 1970s, West wasn't just a supplier—it was infrastructure.

V. The Transformation Years: From Commodity to High-Value

The millennium approached with an existential crisis for West. By the late 1990s, the company faced a stark reality: commoditization was eating their margins alive. Generic rubber stoppers had become a race to the bottom, with competitors from Asia offering similar products at fractions of West's prices. The board even considered the unthinkable—selling the company entirely.

In 1999, the company completed its shift in emphasis when The West Company became West Pharmaceutical Services, Inc. CEO William Little explained the transformation: "West has transformed itself from a designer and manufacturer of products that support the packaging and delivery of injectable pharmaceutical and consumer healthcare products, to a broad-based supplier of products and services that support our customers' entire product development cycle."

But 2000 brought harsh reality. Changes in healthcare, including drug companies conducting in-house packaging and consolidating with other companies, adversely affected the company. West Pharmaceutical Services even considered selling its assets and retained an investment bank, UBS Warburg, to review alternatives for the company. In late 2000, the company announced a 4 percent workforce reduction as well as the closing of its Cleveland office and two plants in Puerto Rico. William Little said of the year's results that it had been "the Company's most difficult year in recent history."

Despite the difficulties, the company decided in 2001 not to offer itself for sale and, instead, to focus on the company's long-term possibilities. This decision marked the beginning of West's most important strategic pivot: moving from commodity rubber stoppers to high-value products (HVP).

The transformation required a complete reimagining of West's business model. Instead of competing on price for generic stoppers, West would focus on technically complex, highly regulated components that commanded premium pricing. This meant developing new materials like FluroTec® barrier film technology, which prevented drug-rubber interactions, and Westar® RS and RU formulations that met the most stringent regulatory requirements. The crown jewel of this transformation was Crystal Zenith (CZ) polymer—a clear, biocompatible material that overcomes problems inherent in glass vials, syringes and cartridges, ideal for high-value molecules, biologicals and biopharmaceuticals, where glass may be a less desirable option because of issues such as chemical interactions and breakage. Developed through West's partnership with Daikyo Seiko, Crystal Zenith represented a paradigm shift. Manufactured from a cyclic olefin polymer, CZ vials offer a break-resistant, high-performance alternative to glass for complex drugs.

The shift to high-value products required more than new materials—it demanded a complete reimagining of West's go-to-market strategy. Instead of selling commodities through distributors, West built a technical sales force that could engage directly with pharmaceutical R&D teams. Sales engineers became consultants, helping customers solve complex containment challenges from drug development through commercialization.

This transformation also meant saying no to low-margin business—a painful but necessary decision. West systematically exited commodity product lines, even when it meant short-term revenue declines. The company focused resources on products where technical differentiation mattered: components for biologics, specialized elastomers for cell and gene therapies, and integrated drug delivery systems.

By the mid-2000s, the strategy was working. Margins expanded as customers paid premiums for West's technical expertise and regulatory support. More importantly, West had repositioned itself from a supplier of rubber parts to a strategic partner in drug development and delivery. The company that almost sold itself in 2000 had found a new identity—and a path to sustainable growth.

VI. The Modern Era: Biologics, Self-Injection & the Device Revolution

The 2010s marked West's transformation from a components supplier to a comprehensive drug delivery partner. The biologics revolution created unprecedented opportunities—complex proteins and antibodies required sophisticated containment and delivery systems that traditional glass and rubber couldn't provide. West positioned itself at the center of this shift.

The numbers tell a compelling story: West commands substantial market share for stopper caps for IV-administered drugs, biologics and gene therapies, with FDA mandates creating strong competitive dynamics. The company's proprietary products now represent approximately 80% of revenue, with contract-manufactured products making up the remaining 20%.

The self-injection revolution became West's most important growth driver. As biologics moved from hospital infusion centers to patient homes, West developed platforms like the SmartDose® on-body injector and SelfDose™ patient-controlled injector. These weren't just devices—they were complete drug delivery ecosystems that pharmaceutical companies could customize for their specific molecules.

West's SelfDose system exemplifies this strategy. Designed for ease of use with features to hide the needle before and after use, it allows patients to control injection rate, improving comfort levels. Human factors studies reported high scores for "ease of administration," "confidence of a complete injection without pain" and "satisfied with the injector system." One healthcare practitioner noted: "The design is less intimidating. I want these in my hospital."

The business model evolved into something resembling razor-and-blades for pharmaceuticals. Every patient using a biologic drug with West components generates recurring revenue with each dose. A single successful drug using West's delivery system can generate revenue for decades. This creates incredibly sticky relationships—once a drug is approved with West components, switching suppliers requires extensive regulatory revalidation.

Geographic expansion accelerated, with approximately 55% of revenue now coming from international markets and 45% from the United States. West established manufacturing facilities across North and South America, Europe, Asia, and Australia, providing the global redundancy that pharmaceutical companies required for supply chain security.

The company's fiscal year 2022 generated $2.89 billion in net sales, reflecting the daily use of over 45 billion components and devices. But more importantly, West had evolved from a supplier to an innovation partner. Pharmaceutical companies now engage West early in drug development, recognizing that delivery system design can be as important as the molecule itself for commercial success.

The rise of cell and gene therapies presented new challenges that played to West's strengths. These ultra-high-value therapies require containment systems that can maintain stability at cryogenic temperatures while preventing any contamination. West's Crystal Zenith vials demonstrated superior viral vector recovery compared to glass or polypropylene, making them the ideal solution for these advanced therapies.

By 2020, West had completed its transformation. No longer just the "rubber stopper company," it had become essential infrastructure for the most advanced medicines in development. The company that started making dental plungers was now enabling breakthrough therapies that could cure genetic diseases and reprogram immune systems.

VII. The Pandemic Test & GLP-1 Opportunity

When the World Health Organization declared COVID-19 a pandemic on March 11, 2020, West's century-old legacy of responding to global health crises kicked into gear. The company that had enabled mass penicillin distribution in World War II now faced an even greater challenge: supporting the fastest vaccine rollout in human history.

Eric Green, West's CEO, made the stakes clear to his team: "We're involved with basically all the vaccines that are in the market." This wasn't hyperbole. West was already the critical supplier of coated stoppers and seals for many pharmaceutical companies working on COVID-19 vaccines. The company's reputation for certainty of supply, derived from global scale and operational flexibility, made them the go-to partner for vaccine developers racing against time.

The technical challenges echoed those of the penicillin crisis 78 years earlier, but at unprecedented scale. Vaccine formulations were challenging, and compatibility of the vaccine with the vial—including containment features and injection devices—was integral to ensuring accurate and efficacious doses. West's FluroTec® film technology, which prevents migration of leachables and reduces interaction with drug products, became essential for maintaining vaccine stability.

West analyses showed their components were FDA/EMA approved for over 125 drugs, including three vaccines and 30 novel drugs. Available in multiple formats and sizes (serum/lyophilization, 13/20mm), they could accommodate a variety of vaccine formats. Taken altogether, stoppers with FluroTec film were clearly the best choice for SARS-CoV-2 vaccine package systems.

The financial impact was immediate and substantial. Wall Street rewarded West handsomely—the company was worth about $10 billion more than at the beginning of the pandemic. Its shares rose from about $130 in March 2020 to $310.95 by April 2021. West expected to generate $260 million in revenue in 2021 just from COVID-19-related products, against 2020's overall revenue of $2.1 billion.

But the pandemic test revealed something more important than financial gains—it validated West's strategic transformation. The company that had pivoted from commodity stoppers to high-value products now proved it could scale innovation under extreme pressure. West's global manufacturing network—25 sites operating across continents—delivered without interruption while competitors struggled with supply chain disruptions. Even as West was managing the COVID vaccine surge, another opportunity emerged that would define the company's next decade: the GLP-1 revolution. Drugs like Ozempic, Wegovy, Mounjaro, and Zepbound weren't just treating diabetes—they were transforming obesity medicine and creating unprecedented demand for self-injection devices.

The numbers were staggering: Semaglutide fills increased by 442% between January 2021 and December 2023. GLP-1s are slated to become the best-selling drug class in 2024, with close to $50 billion in annual sales. For West, this represented a generational opportunity.

West secured a multiyear contract with a major manufacturer for GLP-1 primary packaging elastomer needs. The technical requirements were demanding—these drugs required specialized containment to maintain stability during long-term storage and transport. West's FluroTec barrier film technology and advanced elastomers proved essential for preventing drug-rubber interactions that could compromise efficacy.

The GLP-1 boom also accelerated demand for West's self-injection platforms. These weren't simple pre-filled syringes—they were sophisticated delivery systems that enabled weekly or monthly dosing regimens. West's expertise in human factors engineering, developed over decades of working with biologics, positioned them perfectly for this market.

The regulatory environment provided additional tailwinds. The U.S. Food and Drug Administration determined the shortage of tirzepatide injection has been resolved after being in shortage since 2022 due to increased demand. As shortages eased and production scaled, pharmaceutical companies needed reliable partners who could meet massive volume requirements while maintaining zero-defect quality. Meanwhile, in Europe, the regulatory landscape shifted dramatically with the implementation of EU GMP Annex 1. The revised guidelines, which became effective on August 25, 2023, tripled in length and contained over 30 references to primary packaging material alone. For West, this represented a massive opportunity.

The Annex 1 revision emphasized contamination control strategy (CCS) for the end-to-end manufacturing process, with enhanced requirements for container closure integrity. West offerings included Westar™ Select quality level components, NovaPure® components and Daikyo Seiko's D-Sigma™ components in ready-to-sterilize or ready-to-use formats to cater to customers with different needs based on quality levels.

The regulatory changes created surge in demand for containment solutions navigating regulatory shifts like EU's Annex 1 guidelines. West's DeltaCube™ Modeling Platform utilized big data and statistical analysis to guide vial, stopper and seal combination choices, helping customers better understand factors influencing container closure integrity and mitigate risks.

Looking at 2025 momentum, West was perfectly positioned at the intersection of multiple growth drivers: expected HVP trends in Biologics and Generics, growth from Annex 1 compliance requirements, and continued GLP-1 expansion. The company that had supported COVID-19 vaccine rollout in 2020, continuing the legacy from WWII penicillin partnership, now stood ready to enable the next generation of breakthrough therapies.

VIII. Business Model & Financial Architecture

West's business model represents the pharmaceutical industry's version of Gillette's famous razor-and-blades strategy, but with a crucial difference: once a drug is approved with West's components, switching costs become virtually prohibitive. This creates what Warren Buffett might call a "moat with crocodiles in it."

The company operates through two segments that work in concert. Proprietary products, representing approximately 80% of revenue, include the high-margin containment and delivery systems that pharmaceutical companies specify during drug development. Contract-manufactured products, making up the remaining 20%, provide complementary services that deepen customer relationships and create additional switching barriers.

The genius of this model becomes clear when examining the economics. Every successful drug using West components generates recurring revenue for potentially decades—the patent life of the drug plus years of generic production afterward. A single blockbuster biologic can generate hundreds of millions in cumulative revenue for West over its lifecycle. With over 45 billion components delivered annually, West essentially taxes every injection worldwide. The financial architecture reflects this powerful model. In 2024, West generated $2.893 billion in net sales with operating cash flow of $653.4 million. Capital expenditures of $377 million demonstrate ongoing investment in capacity expansion, particularly for high-value products. The company returned $560.9 million to shareholders through share repurchases, reflecting confidence in long-term prospects.

Geographic diversification provides stability: approximately 55% international markets, 45% United States. This balance insulates West from regional disruptions while capturing global pharmaceutical growth. The long-term strategy involves phasing out lower-margin Standard Products and doubling down on HVP solutions—a deliberate margin expansion strategy that's already showing results.

The margin story reveals the strategy's effectiveness. HVP products now represent approximately 74% of proprietary segment net sales. While destocking pressures temporarily impacted 2024 results, with full-year adjusted-diluted EPS of $6.75 declining 16.5%, the underlying business momentum remains strong. Management guided 2025 adjusted-diluted EPS to $6.00-$6.20, with organic sales growth expected at 2-3%.

What makes West's financial model particularly compelling is its resilience. During the COVID pandemic, the company demonstrated its ability to rapidly scale production while maintaining margins. The current GLP-1 boom shows similar dynamics—West secured multiyear contracts with major manufacturers for primary packaging elastomer needs, creating visibility years into the future.

The cash generation capability enables strategic flexibility. Free cash flow of $276.4 million in 2024, even during a challenging year, funds both growth investments and shareholder returns. The company maintains a fortress balance sheet with $484.6 million in cash and minimal debt, providing ammunition for acquisitions or accelerated organic investment.

Looking ahead, West's financial architecture positions it to capture multiple growth vectors simultaneously. R&D investment continues at healthy levels, ensuring technical leadership. Capital allocation balances growth investment with shareholder returns—a sign of management confidence in the business model's durability.

IX. Competitive Dynamics & Market Position

West operates in what economists call an oligopoly—a market structure where a handful of players control the vast majority of supply. This isn't by accident. The barriers to entry in pharmaceutical packaging are so formidable that no significant new competitor has emerged in decades.

Consider what it takes to compete: FDA validation for every product, which can take years and millions of dollars. Clean room manufacturing facilities requiring hundreds of millions in capital investment. Technical expertise in materials science, sterilization, and drug-rubber interactions that takes decades to develop. Most importantly, the trust of pharmaceutical companies who literally bet billions on your ability to deliver zero-defect quality.

West commands substantial market share for stopper caps for IV-administered drugs, biologics and gene therapies. The competitive landscape includes Aptar (primarily in nasal and pulmonary delivery), Gerresheimer (focused on glass primary packaging), Schott (glass vials and syringes), and Datwyler (elastomeric closures). Each has their stronghold, but West's breadth across elastomers, delivery devices, and integrated systems creates unique competitive advantages.

The real competition isn't for market share—it's for innovation partnerships. When a pharmaceutical company develops a new biologic, they engage packaging partners years before clinical trials begin. By the time a drug reaches market, the packaging components are locked in through regulatory filings. This creates winner-take-all dynamics for each drug program.

West's differentiation comes from three sources. First, technical excellence—the company holds over 450 patents and continues investing heavily in R&D. Second, global manufacturing redundancy—pharmaceutical companies require multiple production sites for supply security. Third, regulatory expertise—West's teams help navigate FDA, EMA, and other regulatory requirements, de-risking the approval process.

The switching costs are astronomical. A pharmaceutical company using West components would need to revalidate their entire manufacturing process, conduct new stability studies, and potentially redo clinical trials to switch suppliers. For a blockbuster drug, this could cost hundreds of millions and delay production by years. No CFO would approve such a switch to save a few percentage points on component costs.

Recent competitive dynamics favor incumbents. The EU's Annex 1 regulations raised quality requirements, making it even harder for new entrants. The shift to biologics and cell therapies requires specialized expertise that takes years to develop. The GLP-1 boom rewards companies that can scale rapidly—something only established players can achieve.

West's response to competition has been strategic focus rather than price competition. The company actively exits commodity products where differentiation is minimal. Instead, it invests in areas where technical complexity creates sustainable advantages. This strategy sacrifices short-term revenue for long-term margin expansion and competitive positioning.

X. Playbook: Lessons for Founders & Investors

West's century-long journey offers a masterclass in building mission-critical infrastructure businesses. The lessons apply far beyond pharmaceutical packaging to any company seeking to become essential infrastructure.

Lesson 1: Own the Unglamorous but Essential Herman West didn't try to discover new drugs—he solved the boring problem of keeping them sterile. This positioning as critical infrastructure rather than innovation leader paradoxically creates more value. While drug companies face patent cliffs and competitive threats, West's business compounds steadily. The lesson: look for problems everyone has but nobody wants to solve.

Lesson 2: Turn Regulation into a Moat Most companies view regulation as a burden. West weaponized it. Every new FDA requirement, every additional validation protocol, every quality standard raises barriers for competitors while strengthening West's position. The company doesn't just comply with regulations—it helps shape them through industry participation. Smart infrastructure businesses make regulation their friend, not their enemy.

Lesson 3: Patience Beats Pivoting In West's 101-year history, the company has essentially done one thing: package injectable drugs safely. While tech companies pivot quarterly, West's consistency created compound advantages. Customer relationships span decades. Technical knowledge accumulates over generations. Manufacturing expertise deepens with every production run. The lesson: picking the right market and staying focused beats constant reinvention.

Lesson 4: Sell Shovels in Gold Rushes During the penicillin boom, COVID vaccine rollout, and current GLP-1 explosion, West provided critical infrastructure while others chased blockbusters. This positioning captures value from every winner without betting on specific outcomes. The company benefits whether Novo Nordisk or Eli Lilly wins the GLP-1 war. Infrastructure players can capture upside with limited downside.

Lesson 5: Make Switching Impossible, Not Illegal West doesn't lock in customers with contracts—it locks them in with physics, chemistry, and regulation. Once a drug is approved with West components, switching becomes practically impossible. This creates customer lifetime values measured in decades, not years. The lesson: build switching costs through technical integration, not legal restrictions.

Lesson 6: Capital Allocation as Competitive Advantage West's capital allocation reflects strategic clarity. Growth capex goes to high-value products. R&D focuses on customer problems, not blue-sky research. M&A targets capability gaps, not revenue growth. Shareholder returns come from excess cash, not leverage. This disciplined approach compounds value over time.

Lesson 7: Culture as Strategy From Herman West's personal guarantee of delivery to today's zero-defect manufacturing, culture drives competitive advantage. West's culture prizes reliability over innovation, consistency over creativity, and long-term relationships over short-term gains. This cultural DNA can't be replicated by competitors, creating sustainable differentiation.

For founders, West demonstrates that boring businesses can create extraordinary value. For investors, it shows that competitive advantages compound in unexpected ways. The company that started making dental plungers became indispensable to global healthcare—not through disruption, but through decades of reliable execution.

XI. Bear vs. Bull Case & Future Outlook

Bull Case: The Secular Growth Story

The bull case for West rests on multiple expanding markets with regulatory tailwinds. The biologics market is projected to grow at 10-12% annually through 2030, nearly double the rate of traditional pharmaceuticals. Every one of these complex molecules requires sophisticated containment and delivery—West's sweet spot.

The GLP-1 opportunity alone could drive growth for a decade. With GLP-1s expected to become the best-selling drug class in 2024 at nearly $50 billion in annual sales, and penetration still in early innings, West's positioning as a key supplier creates massive runway. The company's multiyear contracts for elastomer components provide visibility and volume guarantees.

Self-injection continues shifting from exception to norm. The convenience, cost savings, and patient preference for home administration drive adoption across therapeutic areas. West's device platforms become more valuable as each new biologic launches with self-injection options. The recurring revenue from consumables creates compounding returns.

Regulatory dynamics increasingly favor West. EU's Annex 1 implementation drives European customers to upgrade containment systems. FDA's focus on supply chain security pushes pharmaceutical companies toward proven suppliers. Each new requirement expands West's moat while creating revenue opportunities. The company expects 150 basis points of growth from Annex 1 compliance alone.

Geographic expansion provides additional vectors. Emerging markets' healthcare infrastructure development requires modern packaging standards. China's biologics boom needs Western-quality components. India's growing pharmaceutical manufacturing seeks reliable suppliers. West's global footprint positions it to capture this growth.

The innovation pipeline suggests sustained differentiation. Advanced materials for cell and gene therapies, connected devices for digital health, and sustainable packaging solutions for ESG mandates all play to West's strengths. R&D investment continues generating proprietary technologies that command premium pricing.

Financially, the bull case projects margin expansion as mix shifts toward high-value products. Management's 2025 guidance of $2.875-2.905 billion in revenue and $6.00-6.20 in adjusted EPS implies modest growth, but longer-term dynamics suggest acceleration as destocking ends and new products ramp.

Bear Case: The Maturation Risk

The bear case acknowledges real challenges facing West. Customer concentration remains significant, with top pharmaceutical companies representing outsized revenue portions. If a major customer faced setbacks or switched suppliers, the impact would be material. The negotiating power of large pharma could pressure margins over time.

Technology disruption lurks as a long-term threat. Oral biologics, though technically challenging, could eventually reduce injection dependence. Alternative delivery methods like patches, implants, or inhalation could bypass traditional packaging. While these technologies remain nascent, they represent strategic risks.

The capital intensity of growth creates financial pressure. West spent $377 million on capex in 2024, representing 13% of revenue. Maintaining competitive position requires continuous investment in new facilities, automation, and technology. This capital intensity limits flexibility and pressures returns during downturns.

Competition from low-cost manufacturers increases over time. While regulatory barriers protect developed markets, emerging market customers might accept lower quality for lower prices. Chinese manufacturers are investing heavily in capabilities. Eventually, some could meet Western standards at lower costs.

Market maturation in core products poses growth challenges. Traditional pharmaceutical packaging faces pricing pressure and commoditization. Even high-value products eventually mature. West must continuously innovate to maintain differentiation, but innovation becomes harder as low-hanging fruit gets picked.

Macroeconomic sensitivity could impact near-term results. Healthcare spending faces pressure from government budgets. Drug pricing reforms could cascade to suppliers. Economic downturns delay elective procedures and non-critical treatments, reducing drug demand.

Execution risk increases with complexity. Managing global operations, multiple product lines, and diverse customer requirements creates operational challenges. Quality failures, even minor ones, could damage reputation and customer relationships built over decades.

The Balanced Outlook

The realistic outlook acknowledges both opportunities and challenges. West's 2025 guidance suggests management expects steady but unspectacular growth: 2-3% organic revenue growth and modest margin expansion. This reflects continued destocking headwinds offsetting underlying strength.

Medium-term prospects appear stronger. As destocking normalizes, GLP-1 production scales, and Annex 1 compliance drives upgrades, growth should accelerate. The 2026-2028 period could see high-single-digit organic growth as multiple drivers converge.

Long-term positioning remains favorable despite challenges. West's infrastructure role in healthcare provides resilience. The company survived wars, pandemics, and economic crashes while strengthening its position. Current challenges seem manageable compared to historical tests.

The investment case depends on time horizon and risk tolerance. Short-term investors might find limited upside given current valuation and near-term headwinds. Long-term investors could view current conditions as an entry opportunity for a business with enduring competitive advantages.

XII. Reflection & Key Takeaways

West Pharmaceutical Services represents something increasingly rare in modern markets: a company that creates extraordinary value by being extraordinarily boring. In an era obsessed with disruption, West demonstrates that enabling others' innovations can be more valuable than innovating yourself.

The company's journey from dental plungers to global healthcare infrastructure offers profound lessons about business strategy. West didn't chase trends or pivot to hot markets. It identified a critical need—safe drug packaging—and spent a century becoming indispensable at solving it. This focus created compound advantages that no amount of venture capital or technological disruption can easily replicate.

The infrastructure positioning proves remarkably powerful. West benefits from every major pharmaceutical advance without bearing development risk. Insulin, penicillin, biologics, vaccines, GLP-1s—each wave lifted West regardless of which companies won or lost. This asymmetric upside with limited downside represents the holy grail of business models.

What makes West special isn't any single competitive advantage but how multiple advantages reinforce each other. Regulatory expertise enables customer partnerships. Customer partnerships drive innovation. Innovation strengthens regulatory barriers. Manufacturing scale reduces costs while improving quality. Quality reputation attracts new customers. It's a virtuous cycle built over decades.

The financial performance validates the strategy. A company making rubber stoppers and plastic plungers shouldn't trade at premium multiples or generate superior returns. Yet West does both because markets eventually recognize and reward essential infrastructure. The boring businesses that keep civilization running often create more value than the flashy disruptors that grab headlines.

For investors, West offers lessons about identifying quality. Look for businesses where switching costs exceed switching benefits by orders of magnitude. Find companies whose success depends on execution, not invention. Seek situations where regulation protects incumbents rather than threatens them. Value consistency and reliability over growth and glamour.

The current moment presents interesting dynamics. Short-term headwinds from destocking obscure long-term tailwinds from biologics, GLP-1s, and regulatory changes. Markets often misprice such transitions, creating opportunities for patient capital. West at $17 billion market cap might seem expensive, but infrastructure essential to a trillion-dollar pharmaceutical industry might be cheap.

Perhaps most importantly, West demonstrates that competitive advantages compound in unexpected ways. A delivery guarantee during World War II builds trust that enables COVID vaccine partnerships 75 years later. Technical expertise in rubber chemistry creates capabilities in polymer science decades hence. Customer relationships spanning generations generate knowledge that no competitor can replicate.

In our final analysis, West Pharmaceutical Services isn't just a successful company—it's a template for building enduring value. It shows that in a world obsessed with disruption, there's enormous opportunity in being the stable foundation upon which others build. The company that started by solving dentists' problems with rubber plungers became essential to delivering humanity's most advanced medicines.

The next time you see someone receive an injection—whether insulin for diabetes, a biologic for cancer, or a GLP-1 for weight loss—remember that behind that moment stands a century of innovation in the unglamorous but essential business of pharmaceutical packaging. West's story reminds us that sometimes the most valuable companies are hiding in plain sight, quietly enabling the miracles we take for granted.

For West, the next century promises new challenges—oral biologics, digital health, personalized medicine—but also new opportunities to prove that being boring and essential beats being exciting and optional. As long as humans need medicines delivered safely into their bodies, West will be there, invisible but indispensable, turning rubber and plastic into the infrastructure of modern healthcare.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube