Watsco: The HVAC Empire Built on Distribution Dominance

I. Introduction & Cold Open

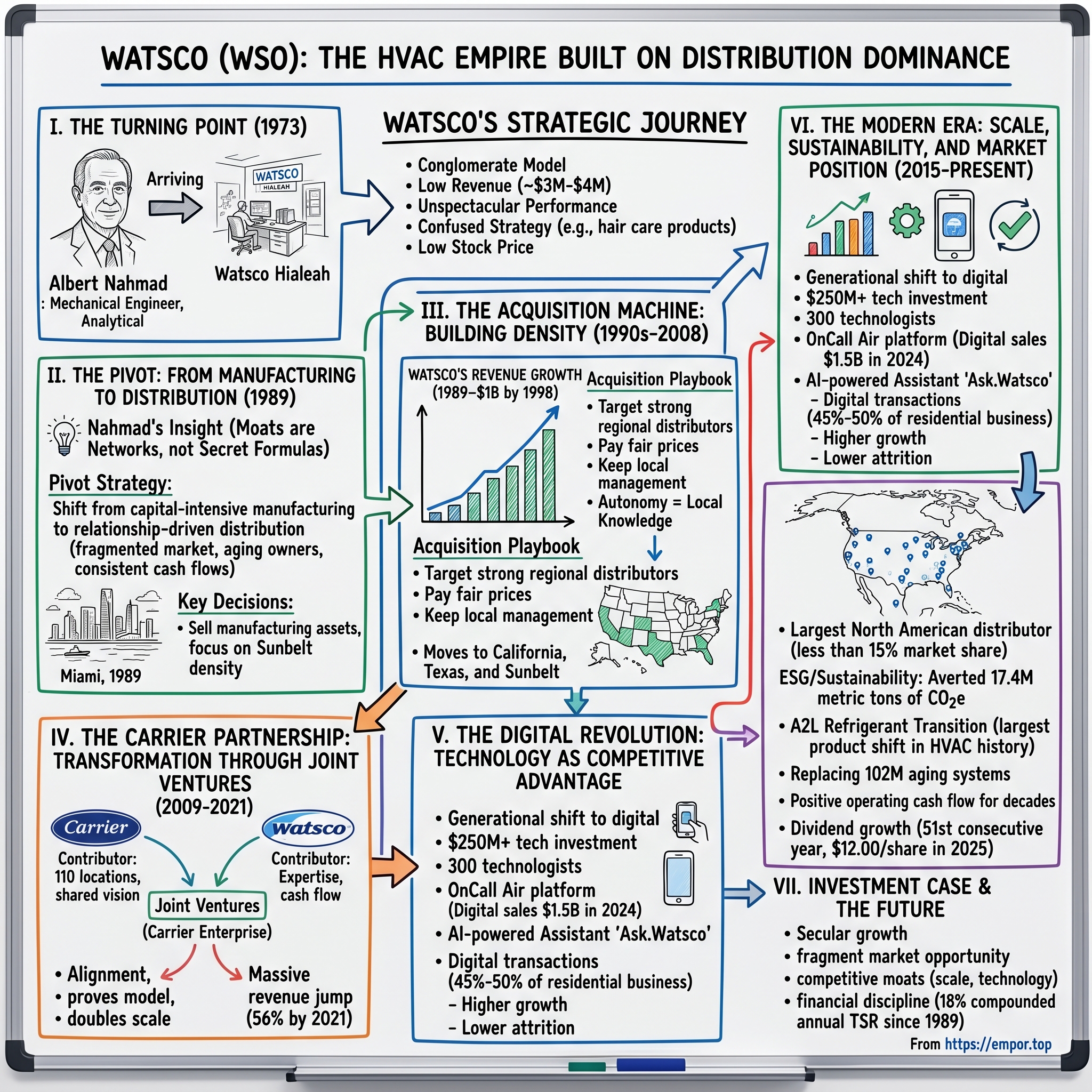

Picture this: It's a sweltering July afternoon in Miami, 1989. The air hangs thick with humidity, the kind that makes your shirt stick to your back the moment you step outside. Inside a nondescript office building, Albert Nahmad is about to make a decision that will transform a sleepy Florida manufacturer into the most dominant force in American HVAC distribution. He's looking at spreadsheets for Gemaire Distributors, a regional Rheem distributor. The numbers are decent, nothing spectacular. But Nahmad sees something else—he sees the future of how America stays cool.

Today, Watsco Inc. stands as the largest distributor of air conditioning, heating, and refrigeration equipment in the HVAC/R distribution industry, with $8.54 billion in revenue and a market capitalization exceeding $20 billion. It's the unsexy business that keeps America comfortable—distributing the equipment that cools your office in August and heats your home in January. Yet few outside the industry know its name, and fewer still understand how a company that once made hair care products became the backbone of American climate control.

This is the story of radical transformation—how Watsco evolved from a small Florida manufacturer bouncing between conglomerates to a focused distribution powerhouse. It's about recognizing that in the digital age, even the most traditional industries can be revolutionized by technology. And it's about the Nahmad family's patient, methodical approach to building what Warren Buffett might call a "wonderful business"—high returns on capital, predictable cash flows, and competitive advantages that compound over decades.

The roadmap ahead takes us from Watsco's humble origins through its conglomerate era, the pivotal shift to distribution, the game-changing Carrier partnerships, and an unlikely digital transformation that has contractors ordering $2.6 billion worth of equipment through their phones. Along the way, we'll uncover why this matters for investors: in a world obsessed with AI and semiconductors, sometimes the best returns come from the companies that simply keep the lights on—and the air conditioning running.

II. Origins: The Pre-Nahmad Era (1947–1972)

The year was 1956. Eisenhower was president, Elvis was scandalizing parents, and in the growing metropolis of Miami, two entrepreneurs saw opportunity in Florida's construction boom. William H. Sutton and Edward L. Blum purchased a small company called Watsco Supply Company, setting up shop in Hialeah, just northwest of Miami. Their timing was impeccable—Florida was experiencing explosive growth as air conditioning made the Sunshine State livable year-round, transforming it from a seasonal tourist destination into a permanent residence for millions.

Initially, Watsco wasn't a distributor at all. The company manufactured heating and cooling equipment, along with door and window parts—basic components for the rapidly expanding Florida housing market. Think of it as a picks-and-shovels play on the great Florida migration. By 1962, just six years after its founding, the company had grown enough to go public, a remarkable achievement for what was essentially a regional manufacturer. The momentum continued, and by 1968, Watsco had graduated to the American Stock Exchange, a sign of growing institutional credibility.

Yet despite these milestones, the numbers tell a more sobering story. Annual revenues through the early 1970s languished between $3 million and $4 million—respectable for a small manufacturer, but hardly the stuff of empire. Florida Trend magazine would later characterize the company's performance throughout the 1970s with a single, damning word: "unspectacular." The company seemed stuck in a no-man's land—too small to compete with major manufacturers, too unfocused to dominate any particular niche.

Like many companies of its era, Watsco fell into the conglomerate trap. The 1960s and early 1970s were the height of conglomerate mania, when ITT owned everything from Sheraton Hotels to Wonder Bread, and Gulf+Western sprawled from oil to Paramount Pictures. Watsco's leadership, following the zeitgeist, began acquiring whatever looked cheap—hair care products, tool and die companies, scattered manufacturing operations. The strategy, if you could call it that, was diversification for its own sake. By 1972, Watsco was less a company than a collection of loosely related businesses, unified only by common ownership and quarterly reporting requirements.

The company's stock price reflected this confusion. Despite being publicly traded for a decade, Watsco remained a penny stock, unknown outside Florida and unloved by Wall Street. Annual reports from this era read like corporate Mad Libs—one year emphasizing HVAC manufacturing, the next highlighting cosmetics, with no coherent narrative threading them together. Revenue growth was anemic, margins were thin, and the company seemed destined for obscurity.

What Watsco needed wasn't another acquisition or a new product line. It needed a complete reimagining of what it could become. That transformation would arrive in December 1973, in the unlikely form of a mechanical engineer with an industrial management degree who had never run a public company before.

III. Enter Albert Nahmad: The Turning Point (1973–1988)

Albert Nahmad didn't look like a corporate revolutionary when he walked into Watsco's Hialeah headquarters in December 1973. At first glance, his resume suggested another MBA-trained executive who would continue the conglomerate playbook. Bachelor's degree in mechanical engineering from the University of New Mexico. Master's in industrial management from Purdue. Stints at W.R. Grace—itself a sprawling conglomerate—and the accounting firm Arthur Young & Co. He was analytical, methodical, almost academic in his approach to business.

But Nahmad brought something different: an engineer's obsession with systems and efficiency. While working at W.R. Grace, he had observed how the best businesses weren't necessarily those with the best products, but those with the best distribution networks. He had seen how Coca-Cola's real moat wasn't its secret formula but its ability to get cold Cokes within arm's reach of desire. This insight would prove transformative, though not immediately.

When Nahmad assumed the chairman, president, and CEO roles in December 1973—an unusual concentration of power that signaled the board's desperation for change—he inherited a company with a market capitalization of roughly $22 million. For context, that's about $150 million in today's dollars, making Watsco a microcap even by 1970s standards. The company was profitable but directionless, a grab bag of manufacturing operations and random acquisitions that generated modest cash flow but no real growth.

Initially, Nahmad didn't revolutionize anything. For his first fifteen years at the helm, he largely continued the conglomerate model, though with more discipline. He pruned some of the more bizarre acquisitions—goodbye, hair care products—while doubling down on manufacturing. The company's financial performance improved modestly; revenues grew, margins expanded slightly, and the stock price crept upward. But this was evolutionary change, not revolutionary transformation.

The 1980s brought a peculiar detour that would later seem almost comical in hindsight. In 1988, just as Nahmad was beginning to formulate his distribution strategy, Watsco acquired Dunhill Staffing Systems, a temporary staffing company. On paper, the logic was sound—staffing was a high-growth, asset-light business with recurring revenues. But it represented the last gasp of the old Watsco, the conglomerate that tried to be everything to everyone.

What outsiders didn't see was the strategic wrestling match happening inside Nahmad's mind. By the mid-1980s, he had begun studying the HVAC industry's structure obsessively. He noticed something others had missed: while HVAC manufacturing was dominated by giants like Carrier and Trane, distribution was incredibly fragmented. Thousands of small, family-owned distributors served local markets, most doing $10-50 million in annual revenue. These businesses had deep customer relationships but lacked scale, technology, and capital. They were ripe for consolidation.

Nahmad also recognized a demographic reality: many of these distributors were owned by aging entrepreneurs with no succession plans. Their children had gone to college and become doctors, lawyers, or tech workers—not interested in running dad's air conditioning warehouse. This created a generational opportunity for someone willing to be the acquirer of choice.

By 1988, Nahmad had made his decision. Watsco would pivot from manufacturing to distribution. But unlike the scattered acquisitions of the past, this would be a focused, methodical strategy. He would start in Florida, where Watsco had relationships and credibility, then expand systematically across the Sunbelt. The Dunhill acquisition would be the last random move; everything afterward would serve the distribution vision.

The market didn't understand it yet, but Nahmad was about to unleash one of the great capital allocation stories in American business—turning that $22 million market cap into today's $20 billion giant.

IV. The Pivot: From Manufacturing to Distribution (1989–1998)

The meeting took place in a conference room overlooking Biscayne Bay in early 1989. Across the table sat the owners of Gemaire Distributors Inc., a South Florida-based distributor of Rheem air conditioning equipment. They had built a solid regional business over decades, with deep relationships among local contractors. But they were tired, ready to retire, and their children had other careers. Nahmad made his pitch: join Watsco, keep running the business, maintain your local identity, but gain access to capital and scale. By year's end, Watsco had acquired a majority interest in Gemaire.

This single acquisition represented more than just adding revenue—it was Nahmad declaring war on the industry's structure. In 1988, he had made the formal decision to pivot Watsco's strategic focus from manufacturing to distribution of HVACR products. The logic was elegant in its simplicity: manufacturing was capital-intensive, cyclical, and dominated by giants with massive R&D budgets. Distribution, by contrast, was fragmented, relationship-driven, and generated predictable cash flows from the enormous installed base of HVAC equipment needing replacement parts and supplies.

Consider the market dynamics Nahmad saw: The North American HVAC distribution market was worth roughly $30 billion in 1989, growing steadily with housing stock and replacement cycles. Yet the largest distributor had less than 5% market share. Most markets were served by one or two local players who had been there for generations. These businesses were profitable—typically generating 5-8% EBITDA margins—but subscale. They couldn't invest in technology, couldn't negotiate better terms with manufacturers, couldn't offer comprehensive training programs to contractors.

Nahmad's playbook emerged quickly and would remain remarkably consistent for decades. First, identify strong regional distributors with good reputations and manufacturer relationships. Second, pay fair prices—not steal them, but not overpay either. Third, and most crucially, keep local management in place. This wasn't slash-and-burn private equity; it was patient capital allocation. The sellers often retained minority stakes, aligning their interests with Watsco's success.

The numbers tell the story of explosive growth. When Nahmad had taken over in 1973, Watsco's market cap was $22 million. By 1989, when the distribution pivot began, it had grown to about $50 million—decent but unspectacular. But once the strategy kicked in, the transformation was remarkable. Revenue grew from under $100 million in 1989 to over $1 billion by 1998. The market cap expanded from $50 million to over $500 million. The compounded annual growth rate of total shareholder return hit 19%—not for a year or two, but sustained over decades.

The acquisition pace was relentless but disciplined. Watsco would typically buy 3-5 distributors per year, each adding $20-100 million in revenue. These weren't transformational deals individually, but collectively they built density. In Florida, Watsco went from one location to fifteen, then thirty. The company could now offer manufacturers complete market coverage, earning better terms and exclusive territories. Contractors could find any part they needed, often delivered the same day.

By the mid-1990s, competitors began to notice. United Refrigeration and Ferguson Enterprises started their own consolidation efforts. But Watsco had first-mover advantage and, more importantly, had earned a reputation as the buyer of choice for family-owned distributors. Word spread through industry conferences and trade associations: if you wanted to sell, Watsco would treat you fairly, keep your people employed, and preserve what you had built.

The 1998 divestiture of Watsco's manufacturing operations marked the final break with its past. The company sold its remaining manufacturing assets to focus entirely on distribution. It was a symbolic moment—Nahmad had completely transformed the company's identity. Revenue had crossed $1 billion, making Watsco the largest independent HVAC distributor in America.

But this was just the foundation. The real scaling would come from density, technology, and an unexpected partnership with one of HVAC's manufacturing giants.

V. The Acquisition Machine: Building Density (1990s–2008)

By 1999, Watsco's headquarters had moved to Coconut Grove, occupying several floors of a gleaming office tower with sweeping views of Biscayne Bay. In the conference room where acquisition targets were evaluated, a map of the United States dominated one wall, covered in colored pins. Red pins showed Watsco locations, blue showed potential acquisitions, yellow indicated competitors. The Sunbelt was turning increasingly red, but Nahmad's ambitions stretched beyond Florida.

The geographic expansion followed climate patterns and demographic trends with scientific precision. After dominating Florida, Watsco moved into California in the mid-1990s, acquiring Baker Distributing and other regional players. California was the second-largest HVAC market after Texas, with year-round cooling needs in the south and heating demands in the north. By 2000, Watsco operated 45 locations across the Golden State, making it the dominant independent distributor from San Diego to Sacramento.

Texas came next, a market so vast that industry veterans called it "three states in one"—the humid Houston-Gulf Coast region, the dry heat of El Paso and West Texas, and the variable climate of Dallas-Fort Worth. Watsco's approach was methodical: acquire the strongest player in each metro area, then fill in with smaller deals to build density. The Three States Supply acquisition in 2001 gave Watsco instant scale in Texas, adding 31 locations and $180 million in revenue.

But the real genius wasn't in the deals themselves—it was in the post-acquisition integration, or rather, the deliberate lack thereof. Watsco's decentralized operating model flew in the face of traditional M&A wisdom. While most acquirers immediately integrated operations, standardized systems, and eliminated redundancies, Watsco did the opposite. Local managers kept their autonomy, made their own inventory decisions, and maintained their customer relationships. The only changes were access to Watsco's balance sheet for inventory purchases and participation in national manufacturer agreements.

This approach solved the fundamental challenge of distribution: it's ultimately a local business. An HVAC contractor in Phoenix has different needs than one in Miami. The products are different—heat pumps versus traditional air conditioners. The seasonal patterns vary. Even the contractor culture differs by region. By maintaining local autonomy, Watsco preserved the intimate market knowledge that made these businesses successful while adding scale advantages.

The numbers validated the strategy. Watsco's acquisition targets typically operated at 5-6% EBITDA margins as independents. Within three years of joining Watsco, those margins usually expanded to 8-10%. The improvement came from better manufacturer terms (volume discounts), reduced financing costs (Watsco's credit was cheaper than local bank loans), and shared best practices (without mandating standardization). A 300-basis-point margin improvement might sound modest, but in distribution, it's transformational.

The 2005 acquisition of East Coast Metal Distributors marked a strategic evolution. This wasn't just another regional player—it was a distributor focused on Goodman products, a value-oriented brand that competed with premium manufacturers like Carrier and Trane. The deal showed Watsco's growing confidence; they could now manage relationships with competing manufacturers, offering contractors choice while maintaining supplier partnerships.

By 2008, Watsco operated over 400 locations across the Sunbelt, with revenues approaching $2 billion. The company had achieved something remarkable: national scale with local execution. But the financial crisis was about to create an unexpected opportunity—one that would transform Watsco from a successful consolidator into a true industry powerhouse through an unlikely partnership with its most important supplier.

VI. The Carrier Partnership: Transformation Through Joint Ventures (2009–2021)

The Carrier Corporation boardroom in Farmington, Connecticut, was tense in early 2009. The financial crisis had devastated new construction, and Carrier's company-owned distribution network—built over decades—was bleeding cash. These weren't independent distributors but Carrier employees, operating from Carrier-owned facilities, selling only Carrier products. The model had worked during the housing boom, but now it was an albatross. Carrier's parent company, United Technologies, was demanding action.

Meanwhile, in Coconut Grove, Albert Nahmad saw opportunity where others saw disaster. Watsco's stock had fallen from $50 to $25, but the company's balance sheet remained pristine—no debt, strong cash flow from replacement demand (air conditioners break regardless of housing starts), and access to capital markets. When Carrier approached about a potential partnership, Nahmad was ready with a proposal that was audacious in its simplicity: create a joint venture, with Watsco contributing its expertise and select locations, Carrier contributing its company-owned distribution network. The deal structure was elegant in its alignment. Watsco issued 3,080,469 shares of common stock to Carrier and contributed 15 locations that presently sell Carrier-manufactured products as consideration for its 60% interest. This wasn't just a financial transaction—it was a strategic marriage. Carrier became a Watsco shareholder, aligning their interests perfectly. If the joint venture succeeded, both parties won. If it failed, both suffered.

The numbers were staggering. Carrier Enterprises LLC, the newly-formed joint venture, with pro-forma revenues of approximately $1.4 billion in 2008, will operate 110 locations in 20 states and Puerto Rico, the Caribbean and Latin America and serve over 19,000 air conditioning and heating contractors. In one stroke, Watsco had nearly doubled its size. Watsco's Chairman and Chief Executive Officer, noted: "This is a blockbuster event for our Company as we are almost doubling our size and scale in the marketplace.

The genius of the structure revealed itself over time. Rather than a one-time acquisition, Watsco negotiated options to increase its ownership progressively. This served two purposes: it reduced initial capital requirements, and more importantly, it allowed Watsco to prove its model worked before Carrier fully committed. Trust was earned, not assumed.

The joint venture performed beyond expectations. Margins improved as Watsco's operational expertise combined with Carrier's brand power. Contractors who had bought only Carrier equipment now had access to complementary products—tools, supplies, refrigerants. The locations that had previously generated 90% of revenue from equipment sales diversified into higher-margin parts and supplies.

Emboldened by success, the partnerships multiplied. In 2011, we formed a second joint venture with Carrier, which we refer to as Carrier Enterprise II, in which Carrier contributed company-owned locations in the Northeast U.S., and we contributed certain locations operating as Homans Associates LLC ("Homans"), a Watsco subsidiary, in the Northeast U.S. Subsequently, Carrier Enterprise II purchased Carrier's distribution operations in Mexico. We have an 80% controlling interest in Carrier Enterprise II, and Carrier has a 20% non-controlling interest.

Then came Canada. In 2012, we formed a third joint venture with Carrier, which we refer to as Carrier Enterprise III. Carrier contributed 35 of its company-owned locations in Canada to Carrier Enterprise III. We have a 60% controlling interest in Carrier Enterprise III, and Carrier has a 40% non-controlling interest.

The pattern was consistent: Watsco would initially take 60% ownership, prove the model worked, then progressively increase its stake as performance improved and trust deepened. By 2021, Watsco had increased its ownership in the original Carrier Enterprise to 80%, in Carrier Enterprise II to 80%, while maintaining 60% of the Canadian operations.

The financial impact was transformational. Combined, the joint ventures with Carrier represented 56% of Watsco's revenues by 2021. The company that had struggled to reach $1 billion in revenue through hundreds of small acquisitions had added multiple billions through three strategic partnerships. More importantly, these weren't just revenue additions—they were margin-accretive, strategically valuable assets that gave Watsco unmatched scale in North American HVAC distribution.

The Carrier partnership also validated Watsco's decentralized model at massive scale. Carrier Enterprise will operate on a decentralized basis and continue to be led by its existing management team, a cornerstone of Watsco's operating strategy. Carrier Enterprise's team will be empowered to make marketing and operational decisions tailored to the particular needs of their local customers. Former Carrier employees, who had operated in a corporate bureaucracy, suddenly found themselves empowered to make local decisions while backed by Watsco's balance sheet and technology platform.

But perhaps the most profound change was yet to come—Watsco's transformation into an unlikely technology company.

VII. The Digital Revolution: Technology as Competitive Advantage (2010s–Present)

In 2014, a Watsco board meeting featured an unusual presentation. Instead of acquisition targets or financial projections, executives were demonstrating a mobile app. On screen, a contractor in a hot Florida attic was using his phone to diagnose an air conditioning unit, check inventory at the nearest Watsco location, and place an order for same-day delivery—all without making a phone call or driving to a branch. Board members, many of whom had been in distribution for decades, watched in amazement. This wasn't how HVAC distribution was supposed to work.

The digital transformation had begun quietly, almost accidentally. Around 2010, Watsco's IT team noticed contractors increasingly asking about online ordering. The initial response was skeptical—HVAC contractors were seen as traditional, relationship-driven customers who valued face-to-face interaction. Why would a 55-year-old contractor who'd been buying from the same counter salesman for twenty years suddenly want to order through a website? But the answer revealed a generational divide. Younger contractors, raised on smartphones and Amazon Prime, expected digital ordering. They wanted to check inventory at 2 AM, compare prices across locations, and track deliveries in real-time. The old model—calling a branch, waiting on hold, driving to pick up parts—was increasingly seen as inefficient. The company estimates that digital transactions now make up 45% to 50% of their residential business.

What started as a defensive move—matching competitors' basic e-commerce offerings—evolved into something far more ambitious. Watsco continues to invest in technologies that enrich the customer experience, drive growth, gain market share and improve operating efficiency. Watsco's digital user-community consists of approximately 64,000 contractors and technicians that engage with Watsco through state-of-the-art platforms capable of influencing every aspect of their day. Since launch, Watsco has generated higher sales growth rates among digital customers, achieved meaningful new customer acquisition and reduced attrition.

The investment numbers were staggering for a distribution company. Watsco pioneered the HVAC/R industry's most comprehensive digital ecosystem, which continues to reshape the industry landscape. The Company has invested more than $250 million in technology over the last five years (an annual current run rate of $60 million) and employs close to 300 technologists. This wasn't just building a website—it was creating an entire digital ecosystem that touched every aspect of the contractor's workflow.

The crown jewel became OnCall Air, Watsco's proprietary digital sales platform that helps contractors sell equipment to homeowners. Picture a contractor in a suburban home, diagnosing a broken air conditioner. Using OnCall Air on their tablet, they can show the homeowner different replacement options, calculate energy savings, apply for financing, and generate a professional proposal—all while sitting at the kitchen table. The gross merchandise value of products sold through OnCallAir®, Watsco's proprietary digital sales platform for contractors, increased 25% to approximately $1.5 billion in 2024 with quotes to homeowners increasing 22% to approximately 313,000 households.

But the real innovation wasn't in consumer-facing tools—it was in the unglamorous backend systems that made distribution more efficient. Pricing optimization tools to provide analytics and insights on more than 200,000 SKUs sold with the goal of modernizing existing processes, enhancing competitiveness and improving margins. Proprietary warehouse management and order fulfillment systems to enable faster, more reliable customer service, accelerate the fulfillment of orders, and enhance warehouse efficiency. Transportation management systems to improve efficiency and productivity of transportation spend. Demand planning and inventory optimization tools to improve fulfillment rates and inventory turns.

The impact on customer behavior was profound. Active users of our technology and e-commerce platforms produce higher growth rates and exhibit approximately 60% less attrition. Contractors who adopted Watsco's digital tools ordered more frequently, bought more products per order, and were far less likely to switch to competitors. The technology created switching costs—once a contractor had their customer database, order history, and workflows integrated with Watsco's systems, moving to another distributor meant starting from scratch.

Ecommerce has become a key driver of Watsco's growth, with its digital sales reaching $2.6 billion in 2024, accounting for 35% of total revenue. In the fourth quarter, Watsco ecommerce sales grew 16%, surpassing the company's overall revenue growth. This wasn't just moving existing sales online—digital customers were buying more, buying more frequently, and buying higher-margin products.

The company also embraced artificial intelligence before it became a buzzword. Watsco is also rolling out artificial intelligence across its business. Internally, over 2,000 employees now use its AI-powered assistant Ask. Watsco to handle customer requests more quickly. Contractors use AL.watsco, another AI tool, to find parts and technical specs in seconds.

Today, more than 70,000 contractors, installers and technicians engage with the Company's platforms, resulting in improved growth and lower attrition. For a company that started as a small Florida manufacturer, Watsco had become one of the most technologically sophisticated distributors in any industry—proof that innovation isn't limited to Silicon Valley startups.

VIII. Modern Era: Scale, Sustainability, and Market Position (2015–Present)

The conference room at Watsco's Coconut Grove headquarters offers a panoramic view of Biscayne Bay, but on this January morning in 2025, all eyes are on the presentation screen. A map of North America glows with over 670 red dots, each representing a Watsco location. From Anchorage to Miami, from Vancouver to Mexico City, the company's reach spans the continent. The presenter, a third-generation HVAC contractor turned Watsco executive, is explaining the A2L refrigerant transition—the most significant regulatory change in the industry's history.2025 operating results reflect the ongoing regulatory transition to next-generation HVAC equipment that incorporates A2L refrigerants, which offer considerably lower global warming potential (GWP), a measurement of environmental impact. The transition encompasses HVAC equipment for residential and commercial applications and will ultimately result in the conversion of nearly $1 billion of inventory (55% of all products sold) across more than 650 locations in the U.S. This isn't just a regulatory compliance exercise—it's the largest product transition in HVAC history, affecting everything from manufacturing to installation to service.

To understand the magnitude, consider that The Environmental Protection Agency (EPA) will require new equipment to use refrigerants with a Global Warming Potential (GWP) of 750 or less, starting January 1, 2025. This means that R-410A, which has a GWP of 2,088, will no longer be used in new equipment. For Watsco, this represents both massive operational complexity and extraordinary opportunity. Every air conditioner and heat pump in their inventory needs to be transitioned. Every contractor needs training on handling mildly flammable refrigerants. Every sales system needs updating with new product specifications.

But step back and consider Watsco's position today. The company was founded more than 60 years ago as a manufacturer of parts, components, and tools used in the HVAC/R industry. From those humble beginnings, Watsco has become the largest distributor in the highly-fragmented $74 billion North American market for HVAC products. Since entering distribution in 1989, Watsco has achieved an 18% compounded annual total-shareholder return through a combination of strong organic growth and the acquisition of more than 70 market-leading businesses.

The scale achieved is staggering. With over 670 locations, Watsco's subsidiaries bring a diverse product base of top-quality HVAC/R equipment and supplies to customers across the US, Canada, Mexico, and the Caribbean. As an industry leader, Watsco now serves more than 125,000 active contractor customers through a network of 690 locations. This isn't just size for size's sake—it's density that creates competitive advantages.

The replacement market thesis has never been stronger. According to data published in March 2023 by the Energy Information Administration, there are approximately 102 million HVAC systems installed in the United States that have been in service for more than 10 years, most of which operate below current efficiency standards. These aging systems represent a massive replacement opportunity, especially as energy costs rise and environmental consciousness grows.

The environmental impact of Watsco's business model deserves attention—not as greenwashing, but as genuine value creation. Based on estimates validated by independent sources, Watsco averted an estimated 17.4 million metric tons of CO2e emissions from January 1, 2020 to June 30, 2023 through the sale of replacement HVAC systems at higher-efficiency standards, an equivalent of removing 3.9 million gas powered vehicles annually off the road. In an era of ESG investing, Watsco offers something rare: a traditional industrial company whose core business directly reduces carbon emissions.

Financial performance reflects the strength of the model. Full-year sales for 2024 were $7.62 billion, up 5% from 2023. Profit was $635 million. eCommerce sales outpaced overall sales growth at $2.6 billion, up 16% during the fourth quarter and 8% for the year. But the real story is consistency—Watsco has generated positive operating cash flow every year for decades, even during the 2008 financial crisis and COVID-19 pandemic.

The dividend track record speaks to this consistency. In April 2025, the Company raised its annual dividend by 11% to $12.00 per share, marking its 51st consecutive year of dividends. This isn't a tech company promising future profits—it's a cash-generating machine that has shared wealth with shareholders for half a century.

Looking forward, the A2L transition represents a multi-year catalyst. The sales mix of new A2L equipment sold in the U.S. in Q2 was approximately 25% during the first quarter and 60% during the second quarter. Other important results: A2L units made up more than 80% of sales by the end of June; R-410A equipment now accounts for less than 5% of inventory. This transition will drive replacement demand as contractors and consumers upgrade to compliant systems, potentially accelerating the replacement cycle for those 102 million aging units.

IX. Playbook: The Watsco Way

Every successful company has a playbook—a set of principles and practices that guide decision-making and create competitive advantages. For Watsco, this playbook has been remarkably consistent over three decades, yet flexible enough to adapt to changing markets. Understanding it is key to understanding why Watsco has generated 19% annual shareholder returns since 1989 while operating in what many consider a boring, commoditized industry.

The acquisition strategy forms the foundation. Since entering distribution in 1989, Watsco has completed 68 acquisitions, including many multi-generation, family-owned businesses. Watsco's "buy and build" strategy can be summarized as follows: Identify and partner with great businesses in the HVAC/R industry · Support their leadership. But the genius isn't in buying companies—anyone with capital can do that. It's in how Watsco buys them and what happens afterward.

Consider the typical acquisition scenario: A family has owned a regional HVAC distributor for three generations. The founder's grandchildren are now running it, but their kids have different careers. The owners face three options: sell to private equity (who will slash costs and flip it), sell to a competitor (who will eliminate the brand and fire half the staff), or sell to Watsco. Watsco's pitch is unique: keep your name on the building, keep your people employed, keep serving your customers the way you always have—just do it with our balance sheet backing you.

The decentralized model is counterintuitive in an era of standardization and synergies. Watsco believes in a decentralized operating model where business units and local leaders are empowered. There's no Watsco way of running a branch—there's the Miami way, the Dallas way, the Phoenix way. Local managers decide inventory levels, pricing strategies, which contractors to extend credit to. Corporate provides capital, technology platforms, and manufacturer relationships, but operational decisions stay local.

This approach solves the fundamental tension in distribution: scale versus service. Customers want the pricing and product availability that comes with scale, but they also want the relationship and responsiveness of a local supplier. Watsco delivers both. A contractor in Houston gets better pricing because Watsco buys millions of units from Carrier, but still deals with the same branch manager he's known for twenty years.

Technology serves as the unifying platform across this decentralized network. While operations stay local, every location uses Watsco's technology stack—the same e-commerce platform, the same inventory management system, the same customer relationship tools. This creates network effects: a contractor working in multiple markets can access his account anywhere, see inventory across locations, have a consistent ordering experience. The technology doesn't replace local relationships; it enhances them.

Capital allocation discipline underpins everything. Watsco operates with no debt, strong cash generation, and consistent dividends. This isn't financial engineering—it's strategic advantage. During downturns, while competitors retrench, Watsco can keep investing, keep acquiring, keep gaining share. Suppliers know Watsco will pay on time. Acquisition targets know Watsco won't need to flip them to pay down debt. The conservative balance sheet enables aggressive growth.

The acquisition criteria have remained remarkably consistent: strong local market position, good manufacturer relationships, cultural fit with Watsco's decentralized model, and reasonable valuation. Watsco walks away from auction processes where private equity drives prices to unsustainable levels. They prefer negotiated deals with families who care about legacy as much as price. Since entering distribution in 1989, Watsco has completed 68 acquisitions at an average multiple that would make private equity firms weep.

Building competitive advantages in a fragmented industry requires patience. Watsco's advantages compound slowly but surely. Scale leads to better manufacturer terms. Better terms lead to better margins. Better margins fund technology investments. Technology creates switching costs. Switching costs reduce customer churn. Lower churn means higher lifetime values. Higher lifetime values justify more investment. It's a flywheel that took decades to build and would take decades to replicate.

The importance of scale in distribution cannot be overstated. In distribution, scale affects everything: purchasing power, delivery efficiency, technology investment capacity, ability to carry inventory. A small distributor might stock 5,000 SKUs; Watsco stocks 200,000. A small distributor might have one location per city; Watsco might have ten, reducing delivery times and costs. A small distributor can't invest $60 million annually in technology; Watsco can and does.

The family control dynamic adds another dimension. Albert Nahmad and Director David Fleeman own approximately 50 percent of the company. This isn't typical for a $20 billion market cap company. The controlling stake means Nahmad can think in decades, not quarters. He can invest in technology that won't pay off for years. He can maintain the decentralized model even when Wall Street analysts question it. He can pass up earnings-accretive acquisitions that would damage culture.

X. Analysis & Investment Case

The investment case for Watsco rests on understanding what kind of business it really is. On the surface, it's a distributor—a middleman between manufacturers and contractors. Dig deeper, and it's a technology platform, a consolidator, a service provider, and increasingly, an essential infrastructure player in the transition to sustainable climate control. The question for investors isn't whether Watsco is a good business—the 19% annual returns since 1989 answer that. The question is whether the next decade can match the last three.

Start with market dynamics. The North American HVAC distribution market remains highly fragmented despite decades of consolidation. Watsco, as the largest player, still has less than 15% market share. Thousands of small distributors remain, many owned by aging entrepreneurs without succession plans. The consolidation runway extends for decades. But fragmentation alone doesn't make a good investment—the key is whether consolidation creates value.

In Watsco's case, it clearly does. The company consistently improves margins at acquired businesses through better manufacturer terms, lower financing costs, and shared best practices. A typical acquisition might have 6% EBITDA margins independently but achieve 9-10% within Watsco's network. This isn't financial engineering—it's operational improvement through scale. Every acquisition makes the next one more valuable through increased density and purchasing power.

The replacement cycle provides a powerful secular tailwind. Those 102 million HVAC systems over 10 years old aren't a theoretical opportunity—they're mechanical equipment that will inevitably fail. Unlike discretionary purchases, air conditioning in Florida or heating in Minnesota isn't optional. When systems break, they get replaced, regardless of economic conditions. This creates remarkably stable demand, even during recessions.

Regulatory tailwinds have never been stronger. The A2L transition forces equipment replacement on a timeline, not just when systems fail. Energy efficiency standards continue tightening. Building codes increasingly mandate higher-efficiency equipment. Each regulation creates replacement demand and typically involves higher-priced, higher-margin equipment. Watsco doesn't lobby for these regulations, but benefits enormously from them.

Competitive positioning reveals substantial moats. Scale advantages in distribution compound—the bigger you get, the harder you are to displace. Technology investments create switching costs—contractors with years of order history, customer data, and workflow integration won't easily switch suppliers. OEM relationships, particularly the Carrier partnership, provide exclusive territories and products competitors can't match. The decentralized model, counterintuitively, makes Watsco harder to compete with—you're not fighting one company but hundreds of entrenched local operations.

The financial profile validates the business quality. Watsco generates returns on invested capital consistently above 15%, remarkable for a distribution business. Operating margins have expanded from 5% to over 10% over the past decade, showing the model's operating leverage. Cash conversion exceeds 100% of net income in most years, funding growth without external capital. The balance sheet remains pristine—no debt, substantial cash, and untapped credit facilities provide financial flexibility.

The bear case deserves serious consideration. Economic sensitivity is real—while replacement demand is stable, new construction is highly cyclical. A housing recession would hurt growth, though likely not as severely as the 2008 experience given the larger replacement market today. Execution risk exists as the company scales—maintaining culture and operational excellence across 690 locations challenges any management team. The A2L transition, while an opportunity, creates operational complexity and inventory risk if mismanaged.

Competition could intensify. Amazon has entered adjacent markets and could theoretically disrupt distribution. However, HVAC's complexity—local relationships, technical expertise, immediate availability needs—creates barriers online players struggle to overcome. Manufacturers could theoretically go direct, but they've shown little appetite for the capital requirements and operational complexity of distribution. Other consolidators exist, but none match Watsco's scale and technology platform.

The bull case rests on multiple expansion drivers. Secular growth from aging equipment, energy efficiency upgrades, and electrification of heating creates sustained demand. The consolidation opportunity remains vast with thousands of acquisition targets. Technology leverage is still early—digital sales at 35% of revenue could reach 50-60% with expanding margins. International expansion beyond North America remains untapped. Climate change, ironically, drives demand for cooling in historically temperate regions.

Valuation requires context. Watsco trades at premium multiples to traditional distributors but discounts to technology-enabled platforms. The market struggles to categorize it—is it an industrial distributor deserving 12x earnings or a technology platform deserving 25x? The answer lies somewhere between, but likely closer to the higher end as digital transformation continues.

The family control dynamic cuts both ways. Positively, it enables long-term thinking, cultural consistency, and strategic patience. Negatively, it concentrates decision-making and creates succession risk. Albert Nahmad is 75; while his son A.J. Nahmad serves as President, the transition timeline remains unclear. However, the institutional knowledge and decentralized model suggest the company could thrive beyond any single leader.

XI. Future Outlook & Key Questions

Looking ahead, several critical questions will determine whether Watsco can maintain its remarkable trajectory or whether the law of large numbers finally catches up to this distribution giant.

The A2L transition presents both the biggest near-term opportunity and risk. Albert H. Nahmad, Chairman and CEO, remarked: "Our second quarter results reflect softer market conditions and the complexities associated with the industry-wide transition to new A2L products. Despite the challenging environment, I am proud that we improved gross margins and generated a measure of earnings growth, which highlights our entrepreneurial culture and the resilience of our business model. Will this transition accelerate replacement cycles as expected, or will complexity and higher costs delay adoption? Early indicators are mixed—adoption is happening but slower than the most optimistic projections.

International expansion potential remains largely untapped. Watsco dominates North American distribution but has minimal presence in Europe, Asia, or other developed markets. These markets have different structures, regulations, and competitive dynamics. Should Watsco export its model internationally, or does its success depend on uniquely American factors—suburban sprawl, extreme weather, fragmented distribution? The company has shown little appetite for international expansion beyond Mexico and the Caribbean, suggesting management sees better returns continuing North American consolidation.

The technology roadmap raises fascinating questions about Watsco's ultimate identity. Is it becoming a software company that happens to distribute HVAC equipment? With 35% of sales digital and growing, AI integration expanding, and contractors increasingly dependent on Watsco's platforms, the company looks more like a technology platform every year. Could Watsco eventually monetize its software separately, selling to other distributors? Could it become the operating system for HVAC contractors, expanding into job scheduling, customer management, and financial services?

Succession planning looms as Albert Nahmad approaches 80. While son A.J. Nahmad serves as President and has been groomed for leadership, the transition from founder to second generation tests any family business. Will the company maintain its entrepreneurial culture, acquisition discipline, and long-term focus? The decentralized model provides some insurance—even corporate upheaval wouldn't immediately affect hundreds of local operations—but leadership matters in capital allocation and strategic direction.

The M&A pipeline and consolidation endgame deserve scrutiny. With over 68 acquisitions completed, has Watsco already bought the best assets? Are remaining targets too small, too expensive, or too difficult to integrate? Or does the fragmented market still offer decades of consolidation opportunity? Barry Logan noted that there are still many family-owned businesses in the industry, and Watsco maintains strong relationships with them. The stability of recent years has clarified valuations, and while private equity remains interested, Watsco is well-positioned to invest when opportunities arise.

Climate change paradoxically benefits Watsco's business model. Rising temperatures increase cooling demand. Extreme weather events damage HVAC equipment, driving replacement. Energy costs make efficiency upgrades economically compelling. Regulations tighten as governments address emissions. While climate change poses existential risks to society, it creates sustained demand for Watsco's products and services. The company doesn't celebrate this dynamic but must navigate its implications.

Digital disruption remains a wildcard. Could new business models—equipment-as-a-service, direct-to-consumer manufacturers, AI-powered procurement platforms—fundamentally reshape distribution? Watsco's technology investments provide some protection, but disruption often comes from unexpected angles. The company's response has been to disrupt itself, investing in technologies that cannibalize traditional counter sales but capture the digital shift.

The bigger picture question: Has Watsco discovered a replicable formula for modernizing traditional distribution, or is HVAC uniquely suited to this model? Could the same playbook work in plumbing, electrical, or industrial supplies? Watsco has shown no interest in adjacent markets, suggesting management believes their advantages are HVAC-specific. But the principles—local operations with centralized technology, patient consolidation, manufacturer partnerships—could theoretically apply elsewhere.

The ultimate test will be whether Watsco can maintain its entrepreneurial edge at massive scale. Many companies lose their hunger after reaching market leadership. Bureaucracy creeps in. Innovation slows. The founder's drive dissipates. Watsco's decentralized model provides some protection—690 locations competing with local rivals maintain urgency—but sustaining culture across decades and generations challenges any organization.

For investors, the key question distills to this: Is Watsco a mature cash cow throwing off dividends while slowly consolidating a fragmented market, or is it still early in a transformation story where technology and sustainability create new growth vectors? The answer likely lies between these extremes—a rare combination of stability and growth, tradition and innovation, that has made Watsco one of the market's most consistent performers.

The next decade will test whether the Watsco way—patient consolidation, technological innovation, operational excellence—can continue generating exceptional returns in a rapidly changing world. The track record suggests betting against them would be unwise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube