Warby Parker: The Story of Eyewear's Disruptive Darling

I. Introduction and Episode Roadmap

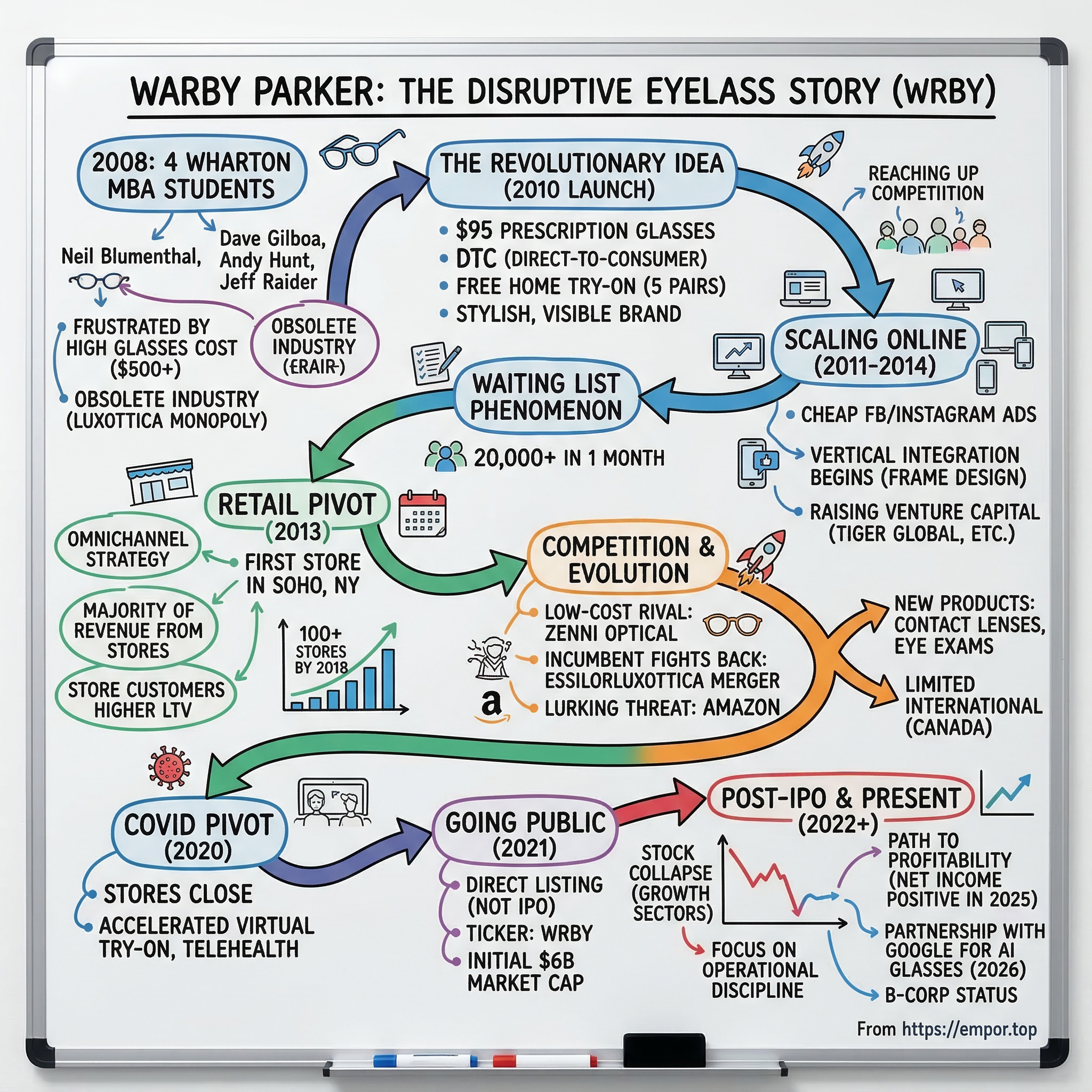

Picture this: it is 2008, and four MBA students at the Wharton School of Business are sitting around a table, griping about a problem that almost every person who wears glasses has experienced but few have questioned. Why do a pair of prescription frames, which cost roughly thirty dollars to manufacture, retail for five hundred dollars or more? Why does buying glasses feel like getting fleeced at a dealership? And why, in an age when consumers could buy almost anything online, did the eyewear industry still operate like it was 1985?

Those four students, Neil Blumenthal, Dave Gilboa, Andy Hunt, and Jeff Raider, would go on to build Warby Parker, a company that took a sledgehammer to one of the most quietly monopolistic industries in the consumer economy. What started as a dorm room thesis project became a cultural phenomenon, a direct-to-consumer pioneer, and eventually a publicly traded company with a market capitalization approaching three billion dollars. Their central innovation was deceptively simple: sell stylish prescription glasses online for ninety-five dollars, a fraction of what traditional optical shops charged, and ship five pairs to your home for free so you could try them on before committing.

But the Warby Parker story is far richer than just a price disruption play. It is a story about vertical integration as competitive strategy. It is about the tension between pure-play e-commerce and physical retail, a debate that Warby settled in a counterintuitive way that separated it from the graveyard of failed DTC brands. It is about building one of the most beloved consumer brands of the 2010s while navigating a pandemic, a brutal public market debut, and the relentless pressure of copycats and incumbents fighting back. And at the heart of it all sits a question that matters deeply to investors: is Warby Parker a growth story with decades of runway, or a maturing brand approaching the ceiling of its addressable market?

To answer that, we need to start with the empire that Warby Parker set out to topple, a company most consumers have never heard of but whose products sit on their faces every single day.

II. The Eyewear Industry Before Warby: Luxottica's Monopoly

Before there was Warby Parker, there was Luxottica. And to understand why four business school students saw an opening in the eyewear market, you have to understand the staggering degree to which one Italian company had wrapped its tentacles around every facet of the industry.

Leonardo Del Vecchio founded Luxottica in 1961 in the small Italian town of Agordo, nestled in the Dolomite mountains. What started as a tiny workshop making eyeglass components grew, through decades of relentless acquisition and vertical integration, into a colossus that controlled roughly eighty percent of the global branded eyewear market by the 2000s. Luxottica did not just make glasses. It owned the brands, it owned the factories, it owned the retail stores, and it even owned the insurance plan that consumers used to pay for the product. The term "monopoly" barely does it justice. It was a vertically integrated empire that would have made John D. Rockefeller nod in approval.

Here is how the playbook worked. On the brand side, Luxottica owned Ray-Ban, Oakley, Persol, and Oliver Peoples outright, while also holding exclusive licensing agreements to manufacture eyewear for fashion houses including Chanel, Prada, Dolce and Gabbana, Burberry, and dozens more. On the retail side, the company owned LensCrafters, Sunglass Hut, Pearle Vision, and Target Optical. And in what was perhaps the most vertically aggressive move of all, Luxottica acquired EyeMed, one of the largest vision insurance providers in the United States, meaning it controlled the insurance plan that paid for the glasses sold in the stores it owned under the brands it manufactured. The consumer was swimming in Luxottica's pool at every point of the transaction without even knowing it.

The result was a pricing structure that bore almost no relationship to the cost of production. A pair of prescription glasses that cost perhaps fifteen to thirty dollars in materials and manufacturing regularly sold for three hundred, four hundred, even five hundred dollars or more at retail. The markups were astonishing, often exceeding ten to fifteen times cost, numbers that would be scandalous in almost any other consumer category. But consumers did not rebel, because they never knew. There was no price transparency, no visible alternative, and the complexity of prescriptions and lens types created an information asymmetry that kept buyers in the dark.

The industry structure also created enormous barriers to entry. A new entrant would need to navigate prescription regulations, optical laboratory requirements, and distribution channel relationships that were all controlled or heavily influenced by the same dominant player. Vision insurance plans created another layer of friction, as consumers assumed they needed to buy from in-network providers, which overwhelmingly meant Luxottica-owned retail chains. And the fashion component of eyewear created a perceived quality gap that made consumers skeptical of lower-priced alternatives, much the same way consumers once associated expensive wine with superior quality regardless of what was actually in the bottle.

But here is the thing about monopoly pricing: it is inherently unstable. Every dollar of excess margin is a gravitational pull attracting disruptors. The only question was when someone with the right combination of insight, timing, and audacity would step through the door. What made the eyewear monopoly particularly vulnerable was the rise of e-commerce and the direct-to-consumer revolution that was beginning to reshape retail in the late 2000s. The same forces that would soon produce Dollar Shave Club in razors, Casper in mattresses, and Allbirds in footwear were about to hit the eyewear industry, and the impact would be seismic.

III. Founding Story: Four MBAs and a Simple Idea (2008-2010)

The origin story of Warby Parker has the feel of a Silicon Valley founding myth, except it happened in Philadelphia and involved people who could actually see the problem sitting on their own noses.

Dave Gilboa, born in 1981 in Sweden and raised in San Diego, arrived at Wharton in 2008 after a stint at the merchant banking division of Allen and Company and a backpacking trip that would become the stuff of startup legend. During that trip, Gilboa lost his glasses. When he looked into replacing them, he was quoted seven hundred dollars, a number so absurd for what was essentially two pieces of plastic connected by a hinge that it sparked genuine outrage. He spent the first semester of business school squinting at whiteboards rather than pay it.

Neil Blumenthal, also born in 1981, came from a very different angle but arrived at the same conclusion. Before Wharton, Blumenthal had spent five years as the director of VisionSpring, a nonprofit organization that trained women in developing countries to give eye exams and sell affordable glasses to their communities. At VisionSpring, Blumenthal saw firsthand what glasses actually cost to make when you stripped away the brand markups and retail overhead. He knew the raw economics of the product, and he knew the industry's pricing was, to put it diplomatically, disconnected from reality.

The two connected at Wharton and quickly pulled in two classmates, Andy Hunt and Jeff Raider, who shared their fascination with the gap between production cost and retail price. Hunt had a background in business strategy, while Raider had worked at a private equity firm and had the finance chops to model out unit economics. Together, the four of them began asking a question so simple that it felt almost impolite: why are glasses so expensive, and what would happen if someone sold them directly to consumers at a fair price?

The answer they arrived at was ninety-five dollars. That number was not chosen randomly. It was high enough to signal quality, far above the rock-bottom prices of discount online retailers, but low enough to feel revolutionary compared to the three-hundred-dollar-plus prices at traditional optical chains. The price had to say "this is a real product from a real brand" while simultaneously communicating that the old way of buying glasses was a ripoff. It was positioning genius, the kind of pricing decision that looks obvious in retrospect but requires genuine insight in the moment.

The bigger challenge was solving the fundamental chicken-and-egg problem of selling glasses online. Consumers had never bought prescription eyewear without trying frames on in person. The fit, the look, the feel on your face, these were tactile decisions that seemed impossible to replicate through a screen. The founders' solution was the Home Try-On program, an idea so simple and so effective that it became Warby Parker's signature. Customers could select five frames from the website, receive them in a box shipped free of charge, try them on at home for five days, and return the ones they did not want, also free. It eliminated the risk of buying sight unseen while creating a social, shareable experience. People would try on frames in front of their friends or post photos on social media asking for opinions, turning a private shopping decision into a viral marketing moment.

The founding team raised a small friends-and-family round, enough to build a website, produce initial inventory, and prepare for launch. They chose the name Warby Parker from two characters in Jack Kerouac's journals, a nod to the literary, slightly intellectual brand identity they wanted to project. The original company was incorporated as JAND Inc. in 2009, with the Warby Parker name reserved for the consumer-facing brand. They spent months building the website, sourcing manufacturers, and testing the concept with fellow students, validating that real demand existed before they put a single dollar into advertising.

What they did not anticipate was just how much demand was waiting.

IV. Launch and The Waiting List Phenomenon (2010-2011)

Warby Parker launched its website in February 2010, timed to coincide with features in GQ and Vogue.com that the founders had been cultivating for months. They had prepared for what they thought would be a healthy initial wave of interest, maybe a few hundred orders, enough to validate the concept and begin the slow climb of a new consumer brand.

Instead, they sold out their entire inventory in the first forty-eight hours. Within the first month, twenty thousand people had joined a waiting list to buy glasses from a company that barely existed.

The numbers were staggering for a bootstrapped startup with no physical presence, no advertising budget, and a product that most people assumed could only be purchased in person. The GQ feature, in particular, proved to be a lightning rod. The magazine framed Warby Parker as the "Netflix of eyewear," a comparison that resonated perfectly with a generation of consumers who were already accustomed to getting their entertainment, their music, and increasingly their household goods delivered directly to their doors. The idea that glasses could follow the same path felt both novel and inevitable.

But behind the euphoric press coverage was operational chaos. The founders were fulfilling orders out of their apartments. Supply chains that were designed for small batch production were suddenly being asked to scale by orders of magnitude. Customer service inquiries were flooding in faster than the team could respond. The Home Try-On boxes were shipping late. The carefully curated brand experience that the founders had envisioned was threatening to collapse under the weight of its own success.

This is a critical moment in any startup's life, the "good problem to have" that can quickly become an existential crisis if mismanaged. What separated Warby Parker from the many startups that have crumbled under similar pressure was the founders' decision to be radically transparent with customers rather than overpromise and underdeliver. They sent personal emails explaining the delays, apologized genuinely, and treated the waiting list as a community to be nurtured rather than a queue to be processed. It was an early signal of the customer-first culture that would become central to the brand's identity.

The early unit economics were compelling. At the ninety-five-dollar price point, with a cost of goods sold in the range of roughly thirty dollars per pair, gross margins hovered around sixty percent or better, strong enough to fund both growth and the company's signature social mission: Buy a Pair, Give a Pair. For every pair of glasses sold, Warby Parker distributed a pair to someone in need through its partnership with VisionSpring, the same nonprofit where Blumenthal had worked before business school. The program was not charity for charity's sake. It was deeply integrated into the brand's identity and served as a powerful marketing tool, giving socially conscious millennial consumers a reason to feel good about their purchase beyond just the price savings.

By the end of 2010, Warby Parker had demonstrated something rare in the startup world: real product-market fit from day one. The waiting list, the press coverage, the word-of-mouth buzz, all of it pointed to a consumer pain point so acute and so widespread that simply offering a credible alternative at a fair price was enough to generate explosive demand. The question now was whether the founding team could build the operational infrastructure to match the brand promise, and whether the magic of the early days could survive the messy reality of scaling a physical goods business.

V. The DTC Golden Era and Scaling Online (2011-2014)

Warby Parker's explosive launch landed it squarely at the forefront of what would become the defining consumer trend of the decade: the direct-to-consumer revolution. Alongside Dollar Shave Club, which launched its viral video campaign in 2012, Casper mattresses, Allbirds shoes, and a wave of other digitally native brands, Warby represented a new way of thinking about retail. Cut out the middlemen. Own the customer relationship. Build a brand online, use social media as your megaphone, and let the incumbents' own bloated cost structures work against them.

The timing was almost unreasonably perfect. Facebook advertising was still cheap and hyper-targetable. Instagram had launched in 2010 and was becoming the dominant visual platform for millennial consumers, precisely the demographic most likely to share photos of themselves trying on Warby Parker frames. The financial crisis had created a consumer mindset that valued smart spending over conspicuous consumption, making the idea of paying less for quality glasses feel aspirational rather than cheap.

Warby leaned heavily into brand building rather than performance marketing. While other DTC startups would later be criticized for spending unsustainable amounts on Facebook and Google ads, Warby invested in storytelling, content creation, and cultural cachet. The brand launched an annual report designed to look like a fashion magazine. It published a literary journal. It hosted events at bookstores and cultural institutions. Every touchpoint was designed to reinforce the idea that Warby Parker was not just a cheaper alternative to LensCrafters but a lifestyle brand that happened to sell glasses, the kind of brand that a certain type of educated, urban, design-conscious consumer would be proud to associate with.

Behind the scenes, the company was making critical strategic bets on vertical integration. Rather than outsourcing manufacturing and design to third parties, Warby began building proprietary capabilities in frame design, lens cutting, and prescription processing. This was expensive and operationally complex, but it gave the company control over quality, speed, and unit economics that competitors relying on contract manufacturers could not match. Over time, Warby would bring a significant portion of its lens production in-house, operating its own optical laboratories in locations including Sloatsburg, New York and Las Vegas, Nevada.

The capital markets responded enthusiastically to the company's early traction. Warby raised a twelve-million-dollar Series A from Tiger Global Management in 2011, followed by additional rounds that would eventually total more than two hundred million dollars in pre-IPO funding. Each round came at a higher valuation, reflecting investors' growing confidence that Warby Parker was not a flash-in-the-pan startup but a durable brand with genuine competitive advantages. The investors who backed Warby during this period read like a who's who of growth-stage venture capital: General Catalyst, Spark Capital, Menlo Ventures, and T. Rowe Price, among others.

The product line expanded steadily during this period. Warby added sunglasses, introduced new frame styles and materials, and experimented with premium offerings at higher price points. The company also invested heavily in technology, developing proprietary tools for virtual try-on, prescription verification, and inventory management. These were not glamorous innovations, but they were the kind of operational infrastructure that would prove essential as the business scaled.

Customer acquisition during this era was remarkably efficient. The Home Try-On program continued to drive organic word-of-mouth, as customers shared their experiences with friends and on social media. Warby's referral program further amplified this growth. But the founders were also watching something else in their data, something that would fundamentally reshape the company's strategy.

VI. The Retail Pivot: From Pure-Play Online to Omnichannel (2013-2018)

In 2013, Warby Parker did something that, on its face, seemed like a betrayal of everything the company stood for. The brand that had built its identity on disrupting traditional retail opened a physical store.

The first location was on Greene Street in SoHo, Manhattan, in a neighborhood known for its gallery spaces and fashion boutiques. It was beautiful, airy, and intentionally designed to feel nothing like the clinical fluorescent-lit optical shops that consumers associated with buying glasses. But for a company whose founding narrative was "we sell glasses online so you do not have to go to a store," the move raised eyebrows. Inside the company, the debate was intense. Were they becoming the very thing they had set out to disrupt? Was this a concession that the pure online model had limits?

The data told an unambiguous story. Despite all the innovation around Home Try-On and virtual try-on technology, the majority of potential customers still wanted to put glasses on their face in a physical space before spending money. Glasses are a deeply personal product. They sit on your face all day, every day. They are one of the first things other people notice about your appearance. The tactile, in-person experience of trying on frames, feeling the weight, checking the fit, seeing yourself in a mirror, was something that even the most sophisticated technology could not fully replicate.

More importantly, the economics of retail were surprisingly compelling. Customers who first interacted with the brand in a physical store showed lifetime values two to three times higher than those who discovered Warby purely online. Store customers bought more pairs, came back more frequently, and were more likely to purchase accessories, sunglasses, and eventually contact lenses. The stores functioned not just as sales channels but as customer acquisition engines, brand billboards that generated foot traffic, awareness, and trust in ways that digital advertising alone could not match.

Warby Parker approached physical retail with the same design-forward, data-driven methodology that had characterized its online business. Stores were deliberately placed in affordable rent locations rather than high-traffic malls, keeping occupancy costs manageable. Layouts were compact and efficient, typically between one thousand and two thousand square feet, a fraction of the size of a traditional optical retailer. The stores used iPad-based point-of-sale systems, integrated seamlessly with the online experience, and offered the same products at the same prices as the website, eliminating any channel conflict.

The company hired "retail advisors" rather than salespeople, a semantic distinction that reflected a genuine cultural difference. Advisors were trained not to push the most expensive frame but to help customers find the right pair, reinforcing the brand promise of accessibility and trust. The stores also housed optometrists who could conduct eye exams, adding a service layer that increased visit frequency and deepened the customer relationship.

The expansion was aggressive. From that single SoHo location in 2013, Warby Parker grew its retail footprint to over one hundred stores by 2018, all company-owned rather than franchised. This gave the company complete control over the customer experience but required significant capital expenditure and operational complexity. Opening a new store meant navigating local regulations, hiring and training staff, securing optometrist partnerships, and integrating the location into the company's inventory management and logistics systems.

By 2018, it was clear that the retail pivot was not a detour from Warby Parker's strategy but its central growth engine. The stores were responsible for a growing majority of the company's revenue. They were profitable at the unit level, with payback periods that justified the investment. And they created a competitive moat that purely online players could not easily replicate. While other DTC brands were struggling with rising customer acquisition costs on Facebook and Google, Warby Parker was building a physical presence that drove awareness, trust, and repeat purchasing in a virtuous cycle.

The lesson here is worth dwelling on for investors. The DTC revolution of the 2010s produced a common narrative that physical retail was dead and digital was the future. Warby Parker's experience suggested a more nuanced truth: for certain product categories, particularly those where fit, feel, and personal style matter, the optimal model was not online-only or offline-only but a carefully integrated combination of both. The companies that figured this out early, Warby chief among them, would prove far more durable than those that clung to the pure digital gospel.

VII. Competition and Market Evolution (2015-2019)

Success in business, like blood in the water, attracts attention from all directions. By the middle of the decade, Warby Parker's disruption of the eyewear industry had spawned a wave of imitators, drawn the attention of traditional incumbents, and raised the competitive intensity of the entire category.

The most visible threat came from the bottom of the market. Zenni Optical, a company that had been quietly selling glasses online at ultra-low prices since 2003, saw its brand awareness surge as consumers became more comfortable purchasing eyewear on the internet. Zenni's prices started as low as six dollars and ninety-five cents per pair, making even Warby's ninety-five-dollar frames look expensive by comparison. EyeBuyDirect, owned by French optical giant Essilor (which would later merge with Luxottica to form EssilorLuxottica), competed in a similar budget tier. These players were not trying to build lifestyle brands. They were competing on price, plain and simple, and they were growing fast.

From the other direction, the traditional industry was fighting back. In 2018, Luxottica and Essilor completed their mega-merger, creating EssilorLuxottica, a behemoth with a combined market capitalization exceeding forty-six billion euros. The merged entity had even more scale, more brands, more retail outlets, and more negotiating leverage than either company had possessed individually. While the merger was partly a defensive move against the direct-to-consumer threat, it also gave the combined company resources to launch lower-priced options and invest in online capabilities that could blunt the insurgents' advantage.

And then there was Amazon. The e-commerce giant had begun selling prescription eyewear in 2019, a development that sent a chill through every player in the online eyewear space. Amazon's advantages were formidable: unmatched logistics infrastructure, a massive existing customer base, extraordinary data capabilities, and the willingness to compete on price in ways that would destroy margins for smaller players. The specter of Amazon's entry loomed over the entire industry like a storm cloud that might or might not materialize into a full-blown hurricane.

Against this intensifying competitive landscape, Warby Parker's strategy crystallized around defending and deepening its moat. The brand invested in experiences and services that pure price competitors could not easily replicate: the physical retail network, the in-store eye exams, the curated design aesthetic, the social mission, and the integrated online-to-offline experience. Warby's competitive position was not based on being the cheapest. It was based on being the best overall value proposition, a combination of price, quality, design, convenience, and brand identity that occupied a sweet spot in the market.

The company also made strategic moves to expand its addressable market. In 2019, Warby Parker launched its contact lens business, Scout by Warby Parker, offering daily disposable lenses on a subscription model. Contact lenses represented an enormous adjacent market with attractive recurring revenue characteristics, the kind of high-frequency, high-retention product that could dramatically increase customer lifetime value. The company also began offering eye exams directly in more of its retail locations, leveraging partnerships with independent optometrists and exploring telehealth capabilities.

International expansion, by contrast, remained limited. Warby Parker opened a small number of stores in Canada but largely avoided the complexity of entering European or Asian markets, where regulatory frameworks, consumer preferences, and competitive dynamics differed significantly from North America. This restraint, while potentially limiting the total addressable market, allowed the company to stay focused and execute in its core geography rather than spreading itself thin.

VIII. The COVID Pivot and Virtual Care (2020-2021)

On March 15, 2020, Warby Parker closed all of its retail stores overnight. In a matter of days, the physical retail network that had become the company's primary growth engine went dark, and the business that had spent seven years building an omnichannel model was suddenly forced back to being an online-only operation.

The speed with which the pandemic struck the retail sector was brutal. For Warby Parker, which had roughly one hundred and twenty-five stores at the time, the closures meant not just lost revenue but also the immediate challenge of managing a workforce that was overwhelmingly employed in retail roles. The company made the difficult decision to furlough a portion of its retail staff while continuing to pay full benefits, a move that aligned with its stated values but came at significant financial cost.

But COVID also created unexpected opportunities. The abrupt shift to remote work sent demand for computer glasses and blue-light-filtering lenses surging. Millions of people suddenly spending eight, ten, twelve hours a day staring at screens discovered they needed vision correction, or that their existing glasses were no longer adequate for all-day screen use. Warby Parker's digital infrastructure, which had been built up over a decade of online operations, was well-positioned to capture this demand even with stores closed.

The company accelerated its investment in virtual try-on technology, leveraging augmented reality capabilities built into modern smartphones to let customers see how frames would look on their faces without leaving home. It also pushed forward with telehealth-enabled eye exams, allowing customers to renew their prescriptions remotely in states where regulations permitted it. These capabilities had been in development before the pandemic, but COVID compressed the adoption timeline dramatically.

When stores began reopening in mid-2020, the experience validated the omnichannel thesis more powerfully than any pre-pandemic strategic planning document could have. Customers wanted both options. Some preferred the convenience of ordering online and doing virtual try-on. Others were eager to return to stores for the in-person experience. The most valuable customers used both channels, browsing online, trying frames in-store, and reordering their favorite styles through the app. The pandemic had not killed physical retail for Warby Parker. It had proven that a robust digital backbone was essential for resilience, while reinforcing that stores remained the highest-converting and highest-LTV customer acquisition channel.

The financial impact of 2020 was significant but not catastrophic. Revenue dipped to approximately three hundred and ninety-four million dollars, down just six percent from 2019 despite months of store closures, a testament to the strength of the online channel. The company posted a net loss of fifty-six million dollars, driven by the costs of managing through the crisis and continued investment in growth. But as the world adapted to living with COVID, Warby Parker emerged with a stronger technology platform, proven omnichannel capabilities, and a management team that had demonstrated its ability to navigate genuine adversity.

Behind the scenes, the co-CEOs were also preparing for the next major chapter in the company's story.

IX. Going Public: The Direct Listing (September 2021)

When Warby Parker decided to go public, it chose the road less traveled. Rather than a traditional initial public offering with underwriters, roadshows, and an allocated pricing process, the company opted for a direct listing on the New York Stock Exchange, following the path blazed by Spotify in 2018 and Slack in 2019.

The direct listing appealed to Warby Parker's founders for several reasons. It avoided the dilutive effect of issuing new shares, meaning existing shareholders, including employees with equity, could sell directly into the market at a price determined by supply and demand rather than by investment bankers' allocations. It also aligned with the brand's ethos of transparency and fairness, the same principles that had driven the ninety-five-dollar price point and the Buy a Pair, Give a Pair program.

The S-1 registration statement, filed in August 2021, pulled back the curtain on the company's financials for the first time. Revenue had grown from three hundred and seventy million dollars in 2019 to five hundred and forty-one million in 2021. The company had served more than two million active customers and operated approximately one hundred and forty-five retail stores across the United States and Canada. Gross margins were healthy at roughly fifty-nine percent, and the company was generating positive revenue growth even as it invested heavily in store expansion, technology, and its vertical supply chain.

But the S-1 also revealed the challenges. Warby Parker had never been profitable on a GAAP basis. Net losses had ballooned from essentially breakeven in 2019 to one hundred and forty-four million dollars in 2021, driven by stock-based compensation expenses related to the direct listing, aggressive store expansion costs, and investments in new product categories. The path to profitability was visible in the unit economics but obscured by the company's growth investments.

WRBY shares began trading on September 29, 2021, opening at fifty-four dollars and five cents and closing the first day at fifty-four dollars and forty-nine cents, implying a market capitalization of roughly six billion dollars. The debut was solid if unspectacular, lacking the dramatic first-day pop of a traditional IPO but achieving stable price discovery that direct listing proponents viewed as a feature, not a bug.

The stock briefly climbed into the high fifties during November 2021, touching levels near sixty dollars in intraday trading. But the honeymoon was short-lived. As the Federal Reserve began signaling interest rate hikes to combat surging inflation, the entire growth stock universe came under severe pressure. High-multiple, unprofitable companies, exactly the category that Warby Parker inhabited, were hit hardest. The rotation out of growth and into value that defined 2022 would test not just Warby Parker's stock price but the market's patience with the entire DTC business model.

X. Post-IPO Challenges and Evolution (2021-Present)

The 2022 growth stock collapse was merciless. From its post-listing highs near sixty dollars, Warby Parker's stock price plummeted, eventually touching single digits as the broader market reassessed the value of unprofitable growth companies in a rising interest rate environment. At its nadir, shares traded below ten dollars, representing a decline of more than eighty percent from the highs. For a brand built on optimism and accessibility, the chart looked grim.

The macro environment made matters worse. Inflation squeezed consumer discretionary spending, and eyewear, while a necessity for many, was also a purchase that consumers could delay in tough times. Customer acquisition costs across digital channels were rising industry-wide, driven by Apple's iOS privacy changes that degraded Facebook ad targeting and by intensifying competition for consumer attention. Meanwhile, competitors at every level of the market were improving: Zenni continued to grow at the low end, traditional optical chains enhanced their online capabilities, and EssilorLuxottica's dominance at the premium tier remained largely unshaken.

Inside the company, the response to these headwinds was steady execution rather than panic. Warby Parker continued to open new stores, expanding from approximately one hundred and sixty locations at the time of the IPO to more than two hundred and thirty by the end of 2025. Management has publicly discussed a long-term target of approximately nine hundred stores, suggesting the company views its physical retail footprint as still in the early innings of build-out. Each new store goes through a disciplined site selection process, with management targeting locations that can achieve profitability within their first or second year of operation.

The financial trajectory told a story of gradual improvement even as the stock languished. Revenue grew from five hundred and ninety-eight million dollars in 2022 to six hundred and seventy million in 2023, then accelerated to seven hundred and seventy-one million in 2024 and eight hundred and seventy-two million in 2025. That last figure represented thirteen percent year-over-year growth, demonstrating that the company could still expand at a meaningful rate even as it scaled.

More importantly, the losses narrowed dramatically. The net loss shrank from one hundred and ten million dollars in 2022 to sixty-three million in 2023 to just twenty million in 2024. And then, in fiscal year 2025, Warby Parker reported its first full year of positive net income: a modest but symbolically significant one point six million dollars. The company had crossed the profitability threshold, not with a dramatic leap but with the persistent narrowing of losses that comes from improving unit economics, operating leverage, and disciplined cost management.

The path to profitability was driven by several factors. Stock-based compensation expense, which had been a massive drag on reported earnings in the years surrounding the direct listing, declined from over one hundred million dollars in 2021 to roughly thirty-five million in 2025. Gross margins stabilized in the mid-fifty-percent range. Operating cash flow grew from just ten million dollars in 2022 to nearly one hundred and eleven million dollars in 2025, and free cash flow turned positive, reaching approximately forty-four million dollars.

In the most recent quarter, Q4 2025 reported in late February 2026, the company showed continued momentum on the top line with revenue of two hundred and twelve million dollars, up about eleven percent year over year. Active customers grew seven percent, and average revenue per customer reached three hundred and twenty-four dollars, a gain of nearly six percent. However, the quarter also showed softness that spooked some investors: earnings per share came in at roughly breakeven, missing the consensus estimate of five cents, and the company's 2026 guidance reflected caution around macroeconomic pressures, calling for ten to twelve percent revenue growth.

Two recent developments deserve attention. In February 2026, Warby Parker appointed Adrian Mitchell as Chief Financial Officer, a hire that strengthens the finance function as the company enters a phase where consistent profitability and capital allocation will matter more than raw growth. And perhaps most intriguing, the company announced a partnership with Google to launch AI-enabled smart glasses in 2026, a move that could open an entirely new product category and potentially redefine Warby Parker's positioning from an eyewear retailer to a wearable technology company.

The stock currently trades around twenty-four dollars, roughly fifty-five percent below its IPO debut price but significantly above its all-time lows. The market capitalization of approximately 2.9 billion dollars values the company at roughly three times trailing revenue, a valuation that reflects both the progress the company has made and the uncertainty that remains.

XI. The Business Model Deep Dive

To truly understand Warby Parker, you need to walk the value chain from start to finish, because the company's most important strategic decision has been its choice to own as much of that chain as possible.

It starts with design. Warby Parker employs its own in-house design team that creates original frame styles rather than licensing designs from external fashion houses. This is a meaningful differentiator in an industry where most brands, even well-known ones, are actually manufactured and designed by Luxottica or EssilorLuxottica under license. By owning the design process, Warby controls the aesthetic identity of its product, the pace at which new styles are introduced, and the intellectual property associated with its frames.

From design, the chain moves to manufacturing. Warby sources frames from a combination of contract manufacturers, primarily in China and Italy, and its own in-house production capabilities. The company operates optical laboratories where it cuts, finishes, and coats lenses, a technically demanding process that requires precision equipment and trained technicians. By bringing lens manufacturing in-house, Warby captures margin that would otherwise go to third-party labs and maintains quality control over the most functionally critical component of the product.

Distribution and fulfillment connect the manufacturing layer to the customer. Warby operates its own fulfillment centers, manages its own logistics, and handles the entire Home Try-On process internally. This is operationally complex, particularly the Home Try-On program, which involves shipping five frames to a customer, receiving them back, inspecting and refurbishing them, and returning them to inventory. The logistical cost is not trivial, but it is a customer experience that competitors have found difficult to replicate at scale.

Finally, there is retail, where Warby now operates over two hundred and thirty company-owned stores. Unlike many consumer brands that franchise their retail operations, Warby's direct ownership gives it complete control over the customer experience, pricing, staffing, and data collection. Every transaction, whether it happens online or in-store, feeds into a unified customer database that informs marketing, product development, and inventory management decisions.

The ninety-five-dollar starting price point, which has gradually crept higher over the years with premium options available at one hundred and forty-five dollars and above, sits in a carefully calibrated position. It is premium enough to signal quality and distinguish Warby from the ultra-cheap online players. But it is accessible enough to feel like a fundamentally better deal than the three-hundred-dollar-plus alternatives at traditional optical retailers. This is what brand strategists call "accessible premium" positioning, a sweet spot that is easy to describe but extremely difficult to maintain. Drop the price too low, and you erode the brand's perceived quality. Raise it too high, and you lose the value proposition that defines the brand.

The unit economics tell a compelling story when you work through them. With cost of goods sold running at roughly forty-six percent of revenue in 2025, gross profit per pair is substantial. But the real question is what happens below the gross profit line: the cost of operating stores, the expense of customer acquisition, the investment in technology and corporate overhead. As the company has scaled, these costs have shown improving leverage. Selling, general, and administrative expenses, which consumed over seventy-five percent of revenue in 2022, declined to approximately fifty-five percent in 2025, driven by a combination of revenue growth, stock-based compensation normalization, and operational discipline.

The revenue mix tells its own story. In 2025, eyewear products generated seven hundred and nineteen million dollars, while services and other revenue, which includes eye exams and related services, contributed fifty-six million, nearly tripling from eighteen million in 2021. This services growth is strategically important because it deepens the customer relationship, increases visit frequency, and creates a moat around the retail experience that purely online competitors cannot match.

The Buy a Pair, Give a Pair program, which has distributed millions of glasses through VisionSpring and other partners, occupies an interesting dual role. It is genuinely philanthropic, providing vision correction to people in developing countries who would otherwise go without. But it is also a powerful marketing asset, giving Warby Parker a story that resonates with consumers who want to feel good about their purchasing decisions. Whether you view it as mission-driven capitalism or strategic philanthropy probably depends on your level of cynicism, but the practical effect is undeniable: it strengthens brand affinity and gives customers an emotional reason to choose Warby over alternatives.

XII. Leadership and Culture

The most unusual thing about Warby Parker's leadership structure is not that it has co-CEOs. Plenty of companies have tried that model. The unusual thing is that it has worked.

Neil Blumenthal and Dave Gilboa have served as co-CEOs since the company's founding, a shared leadership arrangement that defies the conventional wisdom about the need for a single, decisive leader at the top. The arrangement works, according to people who have worked with them, because the two founders bring genuinely complementary skills and temperaments while maintaining deep trust and a shared vision. Blumenthal, who serves as President in addition to co-CEO, tends to focus on brand, culture, and external relationships. Gilboa, who has also served as Principal Financial Officer and Principal Accounting Officer at various points, leans into technology, operations, and finance. Both were born in 1981 and share an earnest, mission-driven orientation that sets the tone for the entire organization.

The other two co-founders, Andy Hunt and Jeff Raider, stepped back from day-to-day operations and now serve as independent directors on the board. Raider went on to co-found Harry's, the DTC razor company, applying many of the same principles that had worked at Warby Parker. The fact that all four founders remain involved in some capacity, more than fifteen years after founding the company, is unusual in consumer startups, where founder departures and internal conflicts are common.

Warby Parker became a certified B Corporation in 2015, a designation that requires companies to meet rigorous standards of social and environmental performance, accountability, and transparency. The B-Corp certification is more than a marketing badge. It is embedded in the company's charter and governance structure, creating a legal framework that obligates the board to consider the interests of all stakeholders, not just shareholders. This stakeholder capitalism model has attracted a certain type of employee and investor while occasionally creating tension with public market shareholders focused primarily on financial returns.

The company's workforce grew from roughly 1,800 employees at the time of the IPO in 2021 to over 4,000 by the end of 2025, with the growth driven primarily by retail store expansion. Managing culture across a distributed workforce that spans corporate headquarters in New York City, optical laboratories, fulfillment centers, and more than two hundred and thirty retail locations is a challenge that the company addresses through intensive hiring practices, ongoing training programs, and a compensation structure that includes equity for all full-time employees, not just executives. Blumenthal and Gilboa each received total compensation of roughly $569,000 in base salary in recent years, modest by public company CEO standards and reflective of the co-founders' emphasis on equitable pay practices.

XIII. Strategic Frameworks: Competitive Position Analysis

To understand where Warby Parker sits in its competitive landscape, it helps to step back and analyze the structural forces shaping the industry through established strategic lenses.

The eyewear industry presents a paradox for potential new entrants. On one hand, the technical barriers to selling glasses online have largely been dissolved. Any entrepreneur with a contract manufacturer and a Shopify store can begin selling frames tomorrow. But replicating what Warby Parker has built, an integrated brand with proprietary manufacturing, over two hundred retail stores, in-house optical labs, and a decade of brand equity, requires hundreds of millions of dollars and years of execution. The capital intensity of vertical integration creates a meaningful barrier, even as the surface-level barriers to entry in online eyewear remain low.

On the supplier side, Warby Parker has largely neutralized supplier leverage through vertical integration. By owning its design process, operating its own optical labs, and sourcing from multiple frame manufacturers, the company is not dependent on any single supplier. This is in stark contrast to the many eyewear brands that rely on EssilorLuxottica for both manufacturing and distribution, creating a dependency that limits their strategic flexibility.

The power of buyers, meaning consumers, is moderate and growing. The proliferation of options, from ultra-budget online retailers like Zenni to traditional chains to Amazon, means consumers have more alternatives than ever before. Switching costs in eyewear are low from a technical standpoint. Your prescription is portable, and there is nothing stopping you from trying a different brand next time. But Warby Parker has created what might be called "soft" switching costs through brand affinity, stored prescription data, the comfort of knowing which frames fit your face, and the positive associations of the shopping experience. These are not lock-in mechanisms in the traditional sense, but they create a degree of customer loyalty that shows up in the company's repeat purchase rates and net promoter scores, which management has cited in the seventy-to-eighty range.

The threat of substitutes is real but manageable. Contact lenses, which Warby Parker now sells, represent the largest substitute product. LASIK and other vision correction surgeries eliminate the need for glasses entirely for some consumers. But the long-term trend is actually favorable for glasses: screen time is increasing, myopia rates are rising globally, and glasses have become a fashion accessory and a form of personal expression in ways that contact lenses and surgery cannot replicate.

Competitive rivalry is the most intense force acting on the business. EssilorLuxottica remains the dominant player in the broader market, with global revenues exceeding twenty-five billion euros. At the budget end, Zenni and EyeBuyDirect continue to grow. Amazon remains a lurking threat, though its prescription eyewear business has not yet achieved the scale that many feared. And every year, new DTC entrants attempt to replicate Warby's model, though few have achieved meaningful scale.

When analyzed through Hamilton Helmer's Seven Powers framework, Warby Parker's competitive position becomes clearer. The company's strongest power is branding. Warby Parker has built one of the most recognizable and respected consumer brands of the past fifteen years. The name connotes stylish, affordable, socially conscious eyewear in a way that no competitor has managed to replicate. This brand equity allows Warby to command higher prices than budget competitors while maintaining the perception of exceptional value relative to traditional optical retailers.

The company's second most significant power, historically, was counter-positioning. When Warby launched, Luxottica and the traditional optical industry simply could not respond without cannibalizing their own high-margin businesses. Dropping prices to ninety-five dollars would have devastated the economics of LensCrafters, Sunglass Hut, and every licensed brand in the portfolio. This asymmetry gave Warby years of relatively uncontested growth. But counter-positioning is a wasting asset. Over time, incumbents adapt. EssilorLuxottica has launched lower-priced online options. Traditional chains have improved their digital capabilities. The counter-positioning advantage, while historically important, is diminishing.

Scale economies are building but remain moderate. Each new store adds to the company's local density, creating efficiencies in marketing, logistics, and brand awareness. Manufacturing scale is improving unit economics in the optical labs. But eyewear is not a winner-take-all market like software, and the scale advantages are incremental rather than transformational.

Network effects are essentially absent. One customer's decision to buy Warby Parker glasses does not make the product more valuable for other customers, which means the company cannot benefit from the powerful demand-side scale economies that drive companies like marketplaces and social networks.

Process power, the accumulated organizational knowledge embedded in systems and workflows, is moderate. Warby's proprietary prescription processing technology, its Home Try-On logistics, and its omnichannel integration represent genuine operational know-how that competitors would find time-consuming to replicate. But it is not impossible, and the processes are not protected by patents or trade secrets in the way that, say, semiconductor manufacturing know-how is protected.

The overall competitive picture suggests that Warby Parker's primary moat is brand, supported by an integrated operating model that creates a customer experience competitors find difficult to match at the same price point. The challenge is that brand is a moat that requires continuous investment to maintain. It can erode if the company fails to innovate, if quality slips, or if a new competitor captures the cultural zeitgeist in a way that makes Warby feel dated. This is the fundamental tension in Warby Parker's competitive position: its strongest power is also its most fragile.

XIV. Bull vs. Bear Case

The bull case for Warby Parker starts with market share arithmetic. The global eyewear market exceeds one hundred and forty billion dollars in annual sales. Warby Parker's eight hundred and seventy-two million dollars in 2025 revenue represents well under one percent of that total. Even in the United States, where the company is best known, its market share is in the low single digits. The bulls argue that Warby is still in the early innings of a long growth story, with enormous runway to capture share from both traditional optical retailers and budget competitors.

The store expansion thesis is central to this argument. With just over two hundred and thirty locations today against a long-term target approaching nine hundred, management believes it has identified roughly four times as many viable store sites as it currently operates. If the company can maintain its historical pattern of new stores achieving profitability within one to two years, each opening creates incremental value. The stores also serve as the primary customer acquisition channel, meaning the company's growth is not dependent on the increasingly expensive and unpredictable digital advertising market.

Contact lenses and services add another dimension to the bull case. Contact lenses are a recurring-revenue product with high retention rates, meaning each new contact lens customer represents a stream of future purchases that bolster lifetime value. Services revenue, including eye exams, nearly tripled from 2021 to 2025, creating a deeper customer relationship and additional reasons to visit stores. The 2026 AI glasses launch in partnership with Google, while speculative, represents genuine optionality. If smart glasses become a meaningful consumer category, Warby Parker's combination of optical expertise, brand trust, and retail distribution could position it as a leading player.

The profitability narrative has also turned a corner. After years of losses, the company posted its first full year of positive net income in 2025 and generated forty-four million dollars in free cash flow. The balance sheet is clean, with roughly two hundred and eighty-six million dollars in cash and no debt. If the operating model continues to show improving leverage, the transition from growth investment to cash generation could accelerate.

The bear case, however, is not without teeth. Competition is coming from every direction. At the low end, Zenni sells functional glasses for a fraction of Warby's price, appealing to cost-conscious consumers who prioritize value over brand. At the high end, EssilorLuxottica's vast portfolio of fashion brands maintains a firm grip on consumers who view eyewear as a luxury accessory. And Amazon's presence in prescription eyewear, while still modest, represents a potentially existential competitive threat from a company with unmatched distribution and data advantages.

Customer acquisition cost inflation is a structural concern. While Warby's shift toward physical retail as an acquisition channel insulates it somewhat from digital advertising cost increases, stores are capital-intensive and geographically limited. There are only so many metro areas in the United States that can support a Warby Parker location, and as the company expands beyond its core coastal markets into smaller cities and suburbs, the productivity of new stores may decline.

The limited international presence is another vulnerability. Warby Parker has a handful of stores in Canada but has made no meaningful push into Europe, Asia, or other major markets. This constrains the total addressable market and creates a growth ceiling that purely domestic execution cannot overcome.

Gross margin trends bear watching. The company's gross margin has declined from roughly sixty percent in the early years to fifty-four percent in 2025. Some of this decline reflects the growing mix of contact lenses, which carry lower margins than frames, and the increasing share of services revenue. But if gross margins continue to compress, it would put pressure on the company's ability to invest in growth while maintaining profitability.

Perhaps the most fundamental question is whether Warby Parker can grow beyond its core demographic. The brand built its identity appealing to urban, educated, socially conscious millennials and Gen Z consumers. As the company expands its store network into less affluent areas and tries to attract a broader customer base, it must do so without diluting the brand cachet that attracted its core customers in the first place. This is the classic brand scaling dilemma, and companies from J.Crew to Starbucks can testify that it is not easy to resolve.

For investors tracking the company's trajectory, three key performance indicators matter most. First, active customer growth rate, which measures the company's ability to expand its customer base beyond early adopters. In 2025, this metric grew seven percent year over year, a solid but decelerating pace that bears monitoring. Second, average revenue per customer, currently at three hundred and twenty-four dollars, which captures the company's success at cross-selling contact lenses, services, and premium products. Third, the company's adjusted EBITDA margin, which reflects operating leverage and the underlying profitability of the business model after stripping out stock-based compensation noise. These three metrics, tracked together over time, will reveal whether Warby Parker is successfully transitioning from growth investment to profitable compounding or plateauing as a mid-size consumer brand.

XV. Lessons for Founders and Investors

The Warby Parker story offers a rich set of lessons, some intuitive and some deeply counterintuitive, for anyone building or investing in consumer businesses.

The first and most fundamental is the importance of timing. Warby Parker launched in 2010, at the exact moment when several trends converged to create ideal conditions for a DTC eyewear brand. Facebook advertising was cheap and effective. Instagram was emerging as the dominant visual platform for millennials. The financial crisis had made consumers receptive to value propositions. And the e-commerce infrastructure, from payments to shipping to website tools, had matured enough to support a complex product like prescription eyewear. A decade earlier, the technology was not ready. A decade later, the window of cheap digital customer acquisition had closed. Warby caught the wave at its peak.

The second lesson is that solving a real, visceral consumer problem creates its own momentum. Every person who had ever paid four hundred dollars for a pair of glasses and felt vaguely ripped off was a potential Warby Parker customer. The company did not need to create demand. It needed to redirect existing frustration into a new channel. This is a fundamentally different and more efficient growth dynamic than companies that must educate consumers about a problem they did not know they had.

The retail pivot offers perhaps the most important lesson for DTC founders and investors. The conventional wisdom of the 2010s held that physical retail was a legacy model destined for obsolescence, and that the future belonged to digitally native brands that could reach consumers directly through their phones. Warby Parker's experience showed that for physical products where fit, feel, and personal style matter, the most durable model integrates both online and offline channels. Many DTC brands that rejected this insight, from mattress companies to shoe brands, struggled to build sustainable businesses because they were dependent on increasingly expensive digital acquisition channels and lacked the brand reinforcement and customer conversion advantages that physical stores provide.

Vertical integration, the decision to control as much of the value chain as possible, is another strategic lesson worth internalizing. By owning its design, manufacturing, distribution, and retail operations, Warby Parker built a level of quality control, margin capture, and competitive defensibility that brands dependent on third-party infrastructure cannot match. It also created operational complexity and capital requirements that serve as barriers to would-be imitators. The lesson is not that vertical integration is always the right choice, but that in categories where customer experience and product quality are key differentiators, owning the full stack can be a powerful competitive weapon.

The co-CEO model, often dismissed as inherently dysfunctional, has worked at Warby Parker in a way that challenges conventional governance wisdom. The key appears to be genuine complementarity of skills and temperament, deep personal trust, and a shared vision that preceded the professional relationship. Few founding teams possess all three of these attributes, which is why the model fails more often than it succeeds. But when it works, it can provide resilience and balance that a single-leader structure cannot.

Finally, the Warby Parker story is a reminder that public market patience is essential for consumer brand building. The company's stock dropped more than eighty percent from its post-listing highs, testing the resolve of early public investors. The path to profitability took five years from the direct listing. Consumer brands compound slowly compared to software companies, and their growth trajectories are lumpy, affected by fashion cycles, macroeconomic conditions, and competitive dynamics that are difficult to predict. Investors who lack the patience to ride through these cycles are unlikely to capture the full value of a brand-building story.

XVI. Epilogue and Future Outlook

As of early 2026, Warby Parker stands at an inflection point. The company has proven that it can achieve profitability, with its first full year of positive net income in 2025. It has demonstrated that its omnichannel model works, with a growing store network, strengthening digital capabilities, and improving unit economics. Revenue has grown at a thirteen percent clip, active customers continue to expand, and the balance sheet is strong with nearly three hundred million dollars in cash.

But the challenges ahead are real. The macroeconomic environment remains uncertain, with consumer discretionary spending under pressure and the company's own 2026 guidance reflecting caution about industry-wide headwinds. Gross margins have trended downward, and the pace of active customer growth, while still positive, has moderated from the hypergrowth days.

The AI glasses partnership with Google represents the most intriguing wildcard in Warby Parker's future. Smart glasses have been a "next big thing" since Google Glass famously flopped in 2013, but the category has gained renewed credibility with Meta's successful Ray-Ban Smart Glasses collaboration with EssilorLuxottica. If Warby Parker and Google can deliver a compelling consumer product that combines Warby's design sensibility and optical expertise with Google's AI and hardware capabilities, it could open an entirely new revenue stream and redefine the company's positioning. However, consumer hardware is notoriously unpredictable, and the partnership's success is far from guaranteed.

The broader scope of practice expansion, deeper into eye exams, medical eyewear, vision health, and potentially hearing aids, represents a more predictable growth vector. By becoming a more comprehensive vision care provider rather than just an eyewear retailer, Warby Parker can deepen customer relationships, increase visit frequency, and capture a larger share of each customer's total spending on vision-related products and services.

The consolidation question occasionally surfaces. Could Warby Parker be an acquisition target? The company's brand equity, retail footprint, and vertically integrated capabilities would be valuable to a larger player seeking to bolster its presence in direct-to-consumer eyewear. But the dual-class share structure gives the co-founders and early insiders effective control over the company, making a hostile acquisition virtually impossible and a friendly one contingent on the founders' willingness to sell, something they have shown no indication of considering.

International expansion remains the great untapped opportunity and the great unanswered question. The company's limited presence outside North America leaves enormous potential markets on the table but also reflects a disciplined approach to capital allocation. The regulatory complexity of prescription eyewear, the diversity of consumer preferences, and the strength of local competitors in markets like Europe and Asia make international expansion genuinely difficult. Whether Warby Parker will eventually crack these markets or remain a predominantly North American brand is one of the key strategic questions that will shape the company's next decade.

What is clear is that Warby Parker has already accomplished something remarkable. It took one of the most concentrated, opaque, and consumer-unfriendly industries in the world and forced it to change. Glasses are cheaper, more accessible, and more stylish than they were before Warby Parker existed. The company gave consumers a choice they did not have before and built a brand that millions of people genuinely love. The question now is not whether Warby Parker changed the eyewear industry. It did. The question is whether it can keep growing, keep innovating, and keep delivering value to both customers and shareholders in a competitive landscape that has fundamentally shifted in response to its own success.

That, in the end, is the innovator's dilemma in reverse. Having disrupted the incumbents, Warby Parker must now defend its position against the next wave of disruptors while continuing to build the brand, expand the store network, and prove that a mission-driven consumer company can deliver long-term shareholder returns. The story is far from over.

XVII. Further Reading

For those looking to go deeper on Warby Parker and the broader themes covered in this episode, the following resources are worth exploring: the Warby Parker S-1 filing from 2021 and subsequent annual reports available on SEC.gov; the 60 Minutes segment on Luxottica from 2012, which remains the definitive mainstream exposé of the eyewear monopoly; Neil Blumenthal and Dave Gilboa's interviews on Guy Raz's "How I Built This" podcast and Reid Hoffman's "Masters of Scale," both of which provide rich founder perspective; the Harvard Business Review article "Direct-to-Consumer is Dead. Long Live Direct-to-Consumer" from 2022, which contextualizes Warby's evolution within the broader DTC reckoning; and The Generalist's deep dive on the DTC landscape from the same period. For competitive and industry context, Grand View Research's eyewear market analysis reports provide useful sizing data, and the EssilorLuxottica annual reports offer a window into how the incumbent views its competitive landscape. For broader strategic thinking, John Mackey's "Conscious Capitalism" and Ben Horowitz's "The Hard Thing About Hard Things" provide frameworks relevant to Warby Parker's stakeholder-driven approach and scaling challenges, respectively.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube