W. R. Berkley: The Specialty Insurance Powerhouse

I. Introduction & Episode Teaser

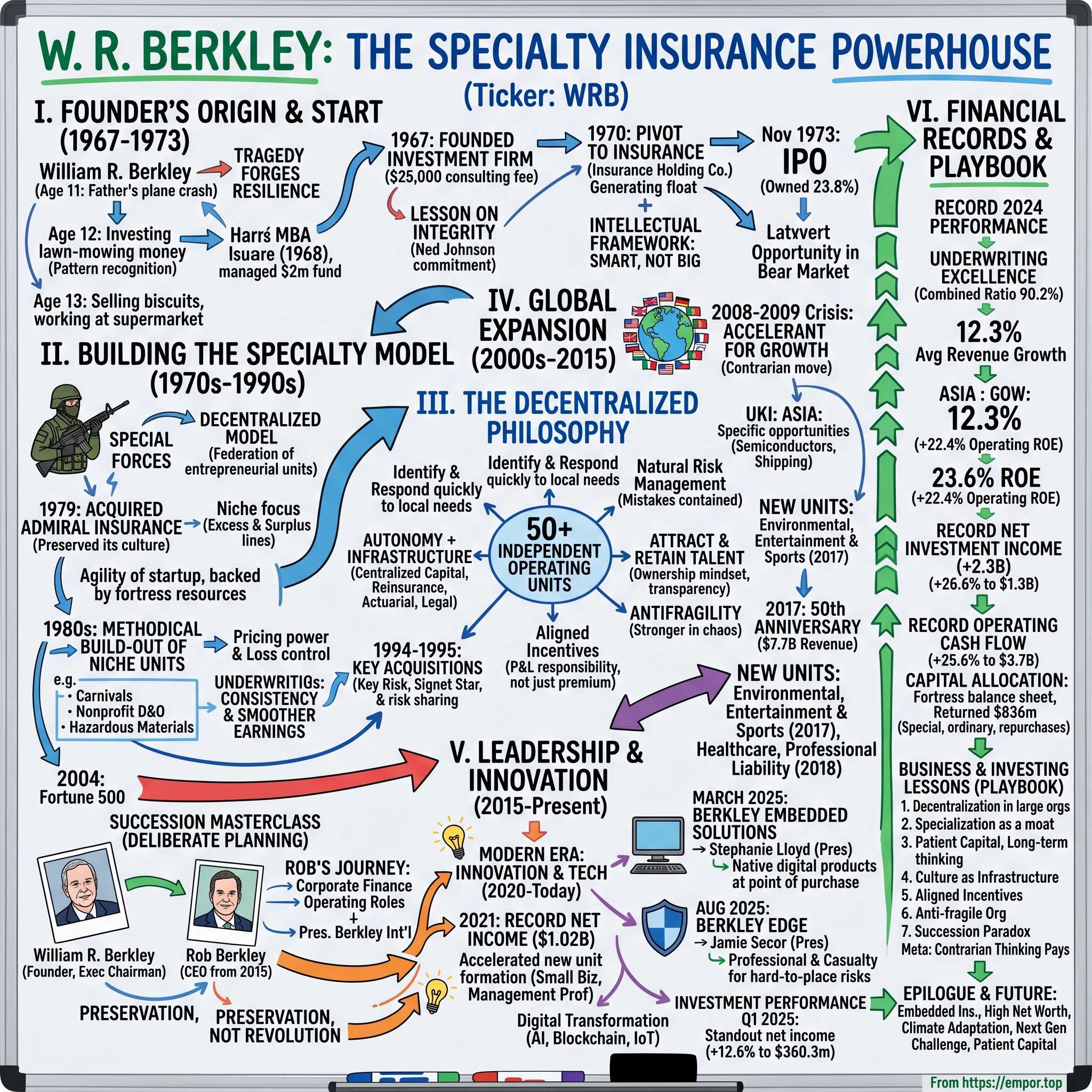

Picture this: It's 1967, and a 21-year-old kid fresh out of Harvard Business School decides to start an investment firm with $25,000 in consulting fees from his former boss. Fast forward to today, and that firm—W. R. Berkley Corporation—commands a $26 billion market capitalization, generates $13.6 billion in annual revenue, and sits comfortably at #397 on the Fortune 500. The question that should fascinate every student of business is deceptively simple: How did William R. Berkley build one of America's most successful specialty insurance companies from scratch, and why has his decentralized model proven so enduringly powerful?

The answer lies not in a single brilliant insight, but in a collection of counterintuitive decisions that flew in the face of insurance industry orthodoxy. While competitors built centralized empires with rigid hierarchies, Berkley created something radically different—a confederation of 50+ entrepreneurial units, each operating with the agility of a startup but backed by the resources of a financial fortress. While others chased market share with commoditized products, Berkley obsessed over niches so specific that competitors couldn't even find them on a map. And while the industry lurched between boom and bust cycles, Berkley maintained an almost Buddhist-like commitment to underwriting discipline that has produced positive underwriting income for 51 consecutive years.

This is a story about three fundamental themes that have shaped modern American capitalism: the power of decentralization in an age of corporate gigantism, the competitive advantages of deep specialization versus broad diversification, and the compounding magic of patient capital in an impatient world. It's also, at its core, a deeply human story about a boy who lost his father in a plane crash at age 11, started investing his lawn-mowing money at 12, and built his grief and grit into one of the insurance industry's most remarkable success stories.

The Berkley model represents something profound about organizational design—proof that you can build a Fortune 500 company that operates like a network of small businesses, that culture can be a more powerful coordinating mechanism than command-and-control, and that in insurance, knowing what risks not to take matters more than any algorithm or actuarial table. As we'll see, this isn't just a business story; it's a masterclass in how to build an anti-fragile organization that gets stronger, not weaker, in times of chaos.

II. The Founder's Origin Story & Early Years (1967–1973)

The summer of 1967 reads like a classic American bootstrapping tale, but with a twist that would define everything that followed. William R. Berkley was 11 years old when his father was killed in an airplane crash, an event that transformed a middle-class family in North Jersey into something far more precarious. His father was the pilot of a company plane which crashed enroute from Alabama to Chicago. "I had a very hard time accepting my father's death and the immediate changes it meant for our family," he says.

The tragedy forged a remarkable resilience. He started investing in the stock market at age 12 with money he made from lawn mowing. Think about that for a moment—while other kids were buying baseball cards, young Bill Berkley was studying price-to-earnings ratios. He bought stock in Decca records, reasoning that if so many of his friends were buying records, then the company must be doing well. When the stock price increased and Berkley realized a profit, he was hooked on the idea of becoming an investor. This wasn't just precociousness; it was pattern recognition at its purest—a skill that would later allow him to see opportunity in the most arcane corners of the insurance market.

Determined to be self-sufficient and not a burden to his mother, Berkley sold Austin biscuits door to door at an apartment complex. Looking to expand, he came up with the idea of selling his product to the local supermarket. At age 13, he became friends with the store's owner, who gave him a job. The entrepreneurial DNA was already expressing itself—not through lemonade stands but through actual P&L responsibility before he could legally drive.

Berkley graduated from the New York University Stern School of Business with an undergraduate degree in 1966, attending on a full scholarship that he would later describe as his "big break." He received an MBA from Harvard Business School in 1968. While at Harvard, he ran a $2 million mutual fund out of an apartment on the Harvard campus with a classmate, Paul Dean. This wasn't your typical student club—they were managing real money, making real investment decisions, experiencing real consequences.

The founding story of W. R. Berkley Corporation contains a lesson about integrity that Berkley would carry through five decades of business. Berkley worked full time for Fidelity until he completed his MBA. He knew he wanted to start his own business, and his mentor at Fidelity, Ned Johnson, offered him a $25,000 investment in Berkley's new company. But here's where it gets interesting: "This was money I was counting on to get my start," Berkley says. "But after many discussions, Fidelity's attorneys counseled Johnson not to go through with the deal." In the end, Johnson decided to keep his commitment and gave Berkley the money as a consulting fee. "This was a huge lesson for me. From then on, I've known the importance of keeping your word and honoring your commitments," Berkley says.

With that $25,000—not an investment but a consulting fee born from honor—In 1967, he founded W. R. Berkley Corporation as a small investment firm. The early years were lean, scrappy, opportunistic. Berkley was essentially running a one-man hedge fund, looking for undervalued situations across the market. But something about insurance caught his eye—perhaps the mathematical elegance of risk pricing, perhaps the inefficiencies in how traditional insurers operated, or perhaps the simple observation that insurance touches everything in the economy yet was run like it was still 1950.

The transformation from investment boutique to insurance powerhouse wasn't immediate. In 1970, Berkley began to focus on the insurance industry with the establishment of W. R. Berkley Corporation as an insurance holding company. The pivot was calculated: insurance companies generate float—premiums paid today for claims that might come tomorrow—creating a perpetual pool of investable capital. For someone who'd been investing since age 12, this was the ultimate leverage.

In November 1973, when the company became a public company via an initial public offering, he owned 23.8% of the company. The timing was brutal—the 1973-74 bear market was one of the worst in American history, with the Dow Jones falling 45%. But Berkley understood something fundamental: insurance is a business that gets more attractive when everyone else is scared. As capital fled the industry, opportunities multiplied for those brave enough to underwrite risk intelligently.

What's remarkable about these early years isn't just the entrepreneurial hustle—it's the intellectual framework Berkley was building. He wasn't trying to build the biggest insurance company; he was trying to build the smartest one. The seed of decentralization was already there: if a 21-year-old with $25,000 could spot opportunities that billion-dollar insurers missed, what would happen if you created an entire organization of entrepreneurial underwriters, each focused on their own niche? That question would drive the next five decades of growth.

III. Building the Specialty Insurance Model (1970s–1990s)

The insurance industry in the 1970s operated like a medieval guild—centralized, hierarchical, and allergic to change. Lloyd's of London still conducted business with quill pens (metaphorically speaking), and American insurers weren't much better. Into this ossified world, Bill Berkley brought a radical idea: what if you ran an insurance company like a venture capital firm?

The concept was deceptively simple but revolutionary in practice. Instead of building one massive insurance company with rigid departments and Byzantine approval processes, Berkley would create dozens of small, autonomous units, each focused on a specific niche where they could develop genuine expertise. Think of it as the insurance equivalent of special forces units versus a traditional army—smaller, faster, deadlier in their specific domains.

The first major validation of this model came through acquisition. Admiral Insurance, founded in 1974, specialized in excess and surplus lines—essentially, the weird stuff that traditional insurers wouldn't touch. When Berkley acquired Admiral in 1979, he didn't absorb it into a corporate blob. Instead, he kept it independent, preserved its entrepreneurial culture, and used it as a template for what would become the Berkley way.

This decentralized structure wasn't just organizational poetry; it solved real business problems. Traditional insurers suffered from what economists call the "agency problem"—the people making underwriting decisions were so far removed from the consequences that they had little incentive to be disciplined. A middle manager at a giant insurer could write bad business for years before anyone noticed. But if you're running a 50-person specialty unit with your name on the door and your compensation tied directly to underwriting profit? Suddenly, every risk decision matters.

The 1980s saw Berkley methodically building out this confederation of specialty units. Each one focused on a niche so specific it seemed almost absurd to outsiders. One unit might specialize in insuring traveling carnivals. Another might focus exclusively on nonprofit directors' and officers' liability. A third might underwrite risks for companies transporting hazardous materials through specific corridors. To a traditional insurer, these markets were too small to matter. To Berkley, they were goldmines of specialized knowledge and pricing power.

The beauty of specialization revealed itself in the numbers. When you're the only insurer who truly understands the risks of, say, high-rise window washing companies, you can price appropriately. Your loss ratios are lower because you know which risks to avoid. Your expenses are lower because you're not trying to be everything to everyone. And your customer retention is higher because where else are they going to go?

By the early 1990s, the model was hitting its stride. The acquisition of Key Risk Management Services Inc. in 1994 added expertise in alternative risk solutions—captives, self-insurance programs, and other structures that helped large corporations manage their own risks more efficiently. This wasn't just adding another specialty unit; it was adding a capability that made the entire network more valuable.

The 1995 acquisitions marked a inflection point. Berkley acquired the remaining 40% interest in Signet Star from Gen Re, giving it full control of a reinsurance platform. In the same year, the company acquired MECC for $138 million, adding medical excess and workers' compensation expertise. These weren't random acquisitions—they were carefully chosen pieces that strengthened the overall network. Each new unit could share risk with others, creating internal diversification while maintaining external specialization.

What made this period remarkable wasn't just the growth—revenue expanded from millions to billions—but the consistency. While other insurers went through violent cycles of hard and soft markets, writing too much business when prices were low and pulling back when prices were high, Berkley's decentralized model provided natural stabilization. When one market went soft, unit managers would pull back. When another market hardened, different managers would lean in. The portfolio effect was powerful: smoother earnings, better returns on equity, and most importantly, avoiding the catastrophic losses that periodically devastated competitors.

The cultural innovation was as important as the structural one. Each unit president was essentially a CEO of their own small company. They had P&L responsibility, hiring authority, and the ability to make quick decisions without layers of corporate approval. This attracted a different type of executive—entrepreneurial, risk-aware, ownership-minded. While competitors fought bureaucratic battles, Berkley units were winning business through speed and expertise.

By 2004, W. R. Berkley had crossed a symbolic threshold, joining the Fortune 500. By 2007, it was generating revenues of $5.5 billion. But these milestones were almost incidental to Berkley. The real achievement was proving that in insurance—an industry that seemed to reward scale above all else—a network of small, specialized units could outperform monolithic giants. It was a lesson in organizational design that would influence not just insurance but business thinking more broadly: sometimes the best way to get big is to stay small.

IV. The Decentralized Operating Philosophy

Picture walking into W. R. Berkley's headquarters and trying to find "the insurance department." You can't, because it doesn't exist. Instead, you'd find something that looks more like a venture capital portfolio than a traditional insurer—more than 50 operating units, each participating in a niche market requiring specialized knowledge about a territory or product. This isn't corporate restructuring for its own sake; it's a fundamental reimagining of how large organizations should operate.

The philosophy is disarmingly simple yet profound: allow each unit to identify and respond quickly and effectively to changing market conditions and local customer needs. But simplicity in concept doesn't mean simplicity in execution. Building a decentralized empire requires solving a paradox—how do you maintain coherence without control, achieve scale without standardization, ensure quality without micromanagement?

Berkley's answer was to treat each operating unit like a franchise with a twist. Unlike McDonald's, where every burger must be identical, Berkley units could be radically different from each other. One might specialize in insuring traveling carnivals, another in cyber liability for financial institutions, a third in workers' compensation for California restaurants. The only commonalities were underwriting discipline, financial accountability, and an entrepreneurial mindset.

The magic happens at the intersection of autonomy and infrastructure. The structure allows them to capitalize on the benefits of economies of scale through centralized capital, investment and reinsurance management and actuarial, financial and legal staff support. Think of it as having the best of both worlds—the agility of a startup with the balance sheet of a Fortune 500 company. Each unit president runs their business like they own it (because, through compensation structures, they partially do), but they can tap into centralized resources when needed.

This decentralized structure provides financial accountability and incentives to local management and enables us to attract and retain the highest caliber professionals. The talent equation is crucial. When you're competing with tech companies and hedge funds for top talent, telling someone they'll be employee #50,000 working in cubicle farm #7 isn't compelling. But telling them they'll run their own $100 million P&L with real autonomy? That attracts a different caliber of person—entrepreneurial, accountable, willing to eat what they kill.

The numbers validate the model spectacularly. Of the company's 51 operating units, 44 were organized and developed internally. This isn't growth through acquisition; it's organic cellular division, like a healthy organism reproducing itself. From 1974 to 2015, management compounded per-share book value (with dividends included) at an annualized rate of 17.3 percent compared to 10.8 percent for the S&P 500 over the same period.

The decentralized approach also solved the information problem that plagues large insurers. In a traditional hierarchy, by the time market intelligence travels from a field underwriter to the C-suite and back down as policy, the opportunity has passed. But when the person seeing the opportunity is also the person who can act on it? Speed becomes a weapon. We hire local insurance executives who have specialized knowledge of their customers, markets and products, and we link their compensation to meeting performance objectives.

Consider how this plays out in practice. When cryptocurrency emerged, traditional insurers formed committees to study it. Berkley? One of their units was already writing crypto custody insurance while competitors were still scheduling their first meeting. When the sharing economy exploded, Berkley units were insuring Airbnb hosts and Uber drivers while traditional insurers were debating whether these were commercial or personal lines.

The structure also creates natural risk management. In a centralized company, one bad decision at the top can sink the ship. At Berkley, mistakes are contained. If one unit writes bad business, it's a $50 million problem, not a $5 billion catastrophe. The portfolio effect works both ways—diversification of risk and diversification of opportunity.

The segment is highly decentralized with a large number of independently operating units none of which provides more than eight percent of gross premiums. This granularity is deliberate. No single unit can bring down the company, but any single unit can discover the next big opportunity. It's antifragility through architecture.

The cultural implications run deep. In most large companies, politics matters more than performance. At Berkley, with transparent P&Ls and direct accountability, there's nowhere to hide. You either make an underwriting profit or you don't. You either grow profitably or you don't. The numbers don't lie, and neither does your compensation.

This model has proven remarkably resilient across market cycles. During hard markets, when pricing is attractive, unit managers lean in. During soft markets, when competition drives prices below acceptable returns, they pull back. The aggregate effect is a natural countercyclical buffer that smooths earnings without top-down commands.

What Berkley built wasn't just a different organizational chart—it was a different organizational physics. While competitors operated like massive cruise ships, slow to turn and vulnerable to icebergs, Berkley operated like a flotilla of speedboats, each nimble enough to navigate its own waters but traveling together toward the same destination. The model would prove its worth not just in good times, but especially when storms hit the industry.

V. Global Expansion & Market Positioning (2000s–2015)

The 2000s represented a fascinating inflection point for W. R. Berkley. While American competitors were consolidating domestically, Berkley looked at a map and saw something different—not countries to conquer but niches to discover. The international expansion that followed wasn't empire building; it was pattern recognition on a global scale.

The acquisition of Garnet Captive Services LLC in August 2006 might seem like a minor footnote—a San Francisco insurance brokerage and alternative risk consulting firm—but it represented something larger. Captive insurance (where companies essentially self-insure through their own insurance subsidiaries) was exploding as corporations sought more control over their risk management. Berkley didn't just buy a company; they bought expertise in helping Fortune 500 companies become their own insurers. This was meta-insurance—insuring the insurers who insured themselves.

The global footprint that emerged was deliberately asymmetric. The company operates commercial insurance businesses in the United Kingdom, Continental Europe, South America, Canada, Mexico, Scandinavia, Asia and Australia and reinsurance businesses in the United States, United Kingdom, Continental Europe, Australia, the Asia-Pacific region and South Africa. Notice the pattern? They weren't trying to plant flags everywhere. They were following opportunity, establishing beachheads where their decentralized model could thrive.

The UK operation, established in the early 2000s, became a template for international expansion. Rather than exporting American products to British markets, they hired British underwriters who understood British risks. The London market wasn't just another geography—it was the spiritual home of specialty insurance, where Lloyd's of London had been writing unusual risks since coffee houses ruled the Thames. Berkley didn't compete with Lloyd's; they learned from it, absorbed its DNA, and applied their own operational excellence.

Continental Europe presented different challenges. Each country had its own regulatory regime, its own insurance culture, its own definition of acceptable risk. A monolithic American insurer would have struggled. But Berkley's decentralized model was built for this complexity. Each European unit could adapt to local conditions while tapping into global capital and expertise. What worked in Germany might fail in Italy, but that was fine—different units, different strategies, same discipline.

The financial crisis of 2008-2009 became an unexpected accelerant for international growth. While competitors retreated to core markets, Berkley saw opportunity in disruption. European insurers, particularly those exposed to banking risks, pulled back from specialty lines. American competitors, scorched by mortgage-related losses, turned inward. Berkley, with its disciplined underwriting and diverse portfolio, had dry powder when others were playing defense.

Asia represented the future, but not in the way most Western insurers imagined. While competitors chased the Chinese dream of 1.4 billion potential customers, Berkley focused on specific opportunities. They weren't trying to sell auto insurance to emerging middle classes; they were insuring semiconductor manufacturers in Taiwan, shipping companies in Singapore, renewable energy projects in India. The same specialization that worked in Peoria worked in Pune—if you understood it deeply enough.

The Latin American expansion followed a similar logic. Rather than competing with local insurers on their home turf, Berkley found niches that locals couldn't or wouldn't serve. Mining companies in Chile needed specialized coverage. Brazilian infrastructure projects required complex risk assessment. Mexican manufacturers serving U.S. supply chains needed seamless cross-border solutions. Each represented a puzzle that Berkley's specialized units were uniquely equipped to solve.

By 2017, as the company celebrated its 50th anniversary, the transformation was complete. The Company marked its 50th anniversary, having ended 2016 with $7.7 billion in total revenue, more than $23 billion in total assets and $5 billion in stockholders' equity. But the real achievement wasn't size—it was reach. Berkley insurance businesses operate around the world, delivering specialized expertise to niche markets through more than 190 office locations in the United States, United Kingdom, Canada, Continental Europe, South America, Scandinavia, Australia, Asia, and Mexico.

The formation of Berkley Environmental and Berkley Entertainment & Sports were established as independent operating units in 2017 showed that even at 50, the company hadn't lost its entrepreneurial edge. Environmental liability was becoming a massive concern as climate change accelerated. Entertainment and sports presented unique risks as events became more complex and expensive. Rather than force-fitting these into existing units, Berkley created new ones. The cellular division continued.

In 2018, the strategic evolution accelerated. The Company formed Berkley Healthcare. Berkley Select and Monitor Liability Managers were combined into one operating unit to provide a single entity for professional liability with superior expertise. Healthcare liability was exploding as medical technology advanced and patient expectations rose. Professional liability was morphing as the gig economy blurred traditional employment lines. Berkley didn't just react to these changes; they anticipated them, creating structures to capitalize on emerging risks.

The international expansion validated a crucial insight: insurance isn't really about geography, it's about expertise. A Berkley unit specializing in cyber liability could serve clients in London, Singapore, and São Paulo because cyber risks don't respect borders. A unit focused on renewable energy could underwrite wind farms in Texas and solar installations in Spain because the physics of sustainable power generation are universal.

What Berkley built during this period wasn't just an international presence—it was a global network of local expertise. Each unit remained entrepreneurial and autonomous, but they could share knowledge, distribute risk, and leverage collective insights. When a new risk emerged in one market, every other market could learn from that experience. When a catastrophe struck one region, the global portfolio provided stability. It was decentralization with benefits of scale—the best of all possible worlds.

VI. Leadership Transition & Second Generation (2015–Present)

The insurance industry has a succession problem. Founder-CEOs cling to power like barnacles, family transitions implode in boardroom coups, and "smooth transitions" usually mean anything but. So when W. R. Berkley Corporation announced in early August that W. Robert Berkley, Jr., President and Chief Operating Officer and a 17-year veteran of the company, will succeed his father as CEO on October 31, 2015, the industry held its breath. Would this be another nepotistic disaster, or could the Berkleys pull off what so few family businesses manage—a genuine transfer of entrepreneurial DNA?

The answer starts with understanding that this wasn't a sudden decision but a masterclass in deliberate succession planning. W. Robert Berkley, Jr. will assume the role of chief executive officer, continuing the transition plan implemented by the Board of Directors when he was appointed president and chief operating officer in 2009. Six years of preparation—not a weekend announcement, not a health scare forcing the issue, but a methodical process of knowledge transfer and authority expansion.

Rob Berkley (as he's known to distinguish him from his father) didn't parachute into the C-suite with an MBA and a birthright. From July 1995 to August 1997, he was employed in the Corporate Finance Department of Merrill Lynch Investment Company. He learned the language of Wall Street before speaking insurance. When he joined W. R. Berkley Corporation in September 1997, he started at the bottom—or at least the middle—working his way through various operating roles.

The progression tells the story: Vice President from 2000 to 2002, Senior Vice President from 2002 to 2003, Senior Vice President of Specialty Operations from 2003 to 2005, Executive Vice President from 2005 to 2009. Each role expanded his understanding of the decentralized model, each promotion earned rather than inherited. Mr. Berkley served as President of Berkley International, LLC since April 2008, giving him crucial experience with the company's global operations before taking on enterprise-wide responsibilities.

What made this transition remarkable wasn't just its smoothness but its philosophy. As executive chairman, William R. Berkley will continue to be fully engaged in the Company's activities, primarily focused on investments and strategy. This wasn't retirement; it was role specialization. The founder would focus on what he did best—capital allocation and strategic vision—while his son handled operations and execution.

"The culture my father has built over the past 48 years at W. R. Berkley Corporation has created remarkable value, and I am deeply committed to the long-term success of our company," Robert Berkley said in a statement. Note the emphasis: not changing the culture but preserving it, not revolution but evolution.

The market's reaction was telling—essentially a shrug. No stock price volatility, no analyst downgrades, no customer defections. This was partly because Rob Berkley had been visibly running large portions of the company for years, partly because the decentralized model meant no single person—not even the CEO—was indispensable. The 50+ operating units would continue running their businesses regardless of whose name was on the corner office door.

The father-son dynamic added complexity but also continuity. "Most importantly, however, I am indebted to my father for his years of guidance and mentorship. Not only have I had the privilege of learning from the best, but I look forward to continuing that close working relationship for many years to come". This wasn't corporate speak—the two would continue working together daily, with Bill Berkley remaining the company's largest shareholder and board chairman.

The transition also validated the decentralized model in an unexpected way. Because each operating unit ran independently, the CEO change didn't cascade through the organization as reorganization. Unit presidents didn't have to reapply for their jobs or adjust to new management styles. The entrepreneurial culture that attracted them remained intact.

Under Rob Berkley's leadership, the company accelerated its pace of new business formation. The younger Berkley brought a digital native's perspective to an analog industry. He understood that millennials didn't buy insurance the way their parents did, that cyber risks were as real as fire risks, that embedded insurance could transform distribution models. But he also understood that these insights meant nothing without underwriting discipline.

The continuity of strategy was perhaps most important. While other new CEOs feel compelled to make their mark with dramatic pivots, Rob Berkley doubled down on what worked. More specialization, not less. More decentralization, not less. More patient capital allocation, not quarterly earnings management. The model his father built wasn't broken; it was just getting started.

What the Berkleys achieved was rare in American business—a successful family succession that strengthened rather than weakened the company. They proved that nepotism and meritocracy aren't always opposites, that sometimes the best person for the job happens to share your DNA, and that great businesses are built not just by founders but by the institutions they create to outlive them.

VII. Modern Era: Innovation & Technology (2020–Today)

The pandemic should have been a disaster for insurers. Travel ground to a halt, businesses shuttered, courts closed, and the global economy froze. Yet 2021 became W. R. Berkley's annus mirabilis. Re/insurance holding company W. R. Berkley Corporation has reported a nearly twofold increase in net income over 2021, which totaled $1.02 billion. In 2021, the Company exceeded our targeted 15% after-tax return on equity and grew our net premiums written by over 22%.

The numbers were staggering: The fourth quarter was highlighted by more than 26% growth in net premiums written and an 18.7% annualized return on equity. This wasn't just beating expectations; it was rewriting them. While competitors struggled with COVID-related losses and business interruption claims, Berkley's specialty focus and disciplined underwriting paid off spectacularly.

What made this performance remarkable wasn't just the magnitude but the mechanism. Robust premium growth was driven by continued strong rate increases in nearly all lines of business combined with higher exposure growth. The hard market that began in 2019 accelerated through the pandemic, and Berkley was perfectly positioned to capitalize. Their decentralized model meant each unit could adjust pricing in real-time, capturing opportunity while avoiding concentration risk.

The formation of Berkley Management Professional and Berkley Small Business Solutions in 2021 showed that even amid record profits, the company wasn't resting. Management professional liability was exploding as boards faced unprecedented scrutiny over ESG issues, cyber breaches, and pandemic responses. Small businesses, devastated by lockdowns, needed specialized coverage that traditional insurers couldn't provide. Berkley didn't just serve these markets; they created bespoke units to dominate them. The announcement of Berkley Embedded Solutions in March 2025 represents something far more significant than another product launch—it's a recognition that insurance distribution is fundamentally changing. W. R. Berkley Corporation (NYSE: WRB) today announced the formation of Berkley Embedded Solutions to deliver tailored insurance products and services to customers at the point of purchase. This new business will bring together the best of modern technology, purpose-built digital-first insurance products, and complementary services with Berkley's strong underwriting culture and reach.

The concept of embedded insurance—where coverage is integrated directly into the purchase of another product or service—isn't new. But Berkley's approach is different. Rather than trying to retrofit traditional products into digital channels, they're building native digital products from scratch. When you buy a rental car, the insurance should appear seamlessly. When you purchase expensive electronics, protection should be one click away. When a small business signs up for a delivery service, liability coverage should be automatic.

Stephanie Lloyd has been named president of the new business. Ms. Lloyd joins Berkley with 20 years of experience in the property and casualty insurance business, with leadership roles that spanned underwriting, product development, and distribution. She most recently led a successful global technology company in the digital health and well-being space, serving as its chief executive officer. The choice of Lloyd signals serious intent—this isn't a side project but a core strategic initiative.

The timing is crucial. Traditional insurance distribution—agents, brokers, lengthy applications—works for complex commercial risks but fails for simple, high-frequency transactions. Millennials and Gen Z consumers expect insurance to be as easy as ordering an Uber. Small businesses want coverage that turns on and off with demand. The gig economy needs insurance that follows workers across platforms. Berkley Embedded isn't chasing these trends; it's building infrastructure for them.

What makes this particularly powerful is the combination with Berkley's existing strengths. Berkley Embedded's value proposition will be offering traditional insurance industry expertise while simultaneously meeting customers where they want to be met. They have the underwriting discipline to price risk accurately, the balance sheet to handle claims, and now the technology to distribute at scale. It's the insurance equivalent of having both a factory and a marketplace.

The launch of Berkley Edge in August 2025 addressed a different but equally important opportunity. W.R. Berkley Corp. announced the formation of Berkley Edge, a new business providing professional liability and casualty insurance for small to mid-sized businesses. Berkley Edge will focus on hard-to-place and distressed risks, offering coverage exclusively through wholesale brokers.

The excess and surplus (E&S) lines market has exploded as traditional insurers retreat from complex risks. Professional liability, in particular, has become a minefield. Directors and officers face personal exposure from shareholder lawsuits. Cyber breaches can bankrupt companies overnight. Employment practices liability claims have skyrocketed. Traditional insurers often won't touch these risks, creating opportunity for specialists.

W. R. Berkley has named Jamie Secor as president of the division. With a career in the insurance sector spanning more than 25 years, Secor has expertise in underwriting for challenging and non-traditional insurance risks. Most recently, she was the chief underwriting officer at a specialty lines property and casualty insurance company. Again, the leadership choice matters—Secor isn't a digital native experimenting with insurance but an insurance veteran who understands the complexity of professional liability.

The E&S strategy reflects a deeper truth about modern insurance: the middle is disappearing. Simple, commoditized risks are moving to digital platforms with algorithmic underwriting. Complex, unique risks require human expertise and bespoke solutions. Berkley is positioning itself at both extremes—embedded for the simple, E&S for the complex—while competitors fight over the shrinking middle.

The broader digital transformation extends beyond new units. Berkley's existing businesses are incorporating artificial intelligence for underwriting, blockchain for claims processing, and IoT sensors for risk monitoring. But unlike insurtechs that lead with technology, Berkley leads with risk understanding and adds technology as a tool. The difference matters when a claim arrives.

The investment performance during this period deserves attention. W.R. Berkley's investment operations delivered standout performance in Q1 2025, with net investment income increasing 12.6% to $360.3 million compared to the prior year period. This growth represents a significant contributor to the company's overall profitability and helped offset the impact of higher catastrophe losses in the quarter. The improvement in investment income came primarily from a dramatic turnaround in investment fund performance, which swung from a $29.3 million loss in Q1 2024 to a $27.0 million gain this quarter. This $56.3 million positive swing demonstrates the portfolio's resilience and the improving performance of alternative investments.

This investment success isn't accidental. With Bill Berkley still involved as Executive Chairman, focusing on investments and strategy, the company benefits from six decades of capital allocation expertise. The combination of underwriting profit and investment income creates a powerful compounding machine—premiums generate float, float generates returns, returns fund growth.

The modern era of W. R. Berkley isn't about abandoning what worked but extending it into new domains. The decentralized model that conquered traditional specialty lines now attacks digital distribution. The underwriting discipline that produced decades of profitability now powers algorithmic risk selection. The entrepreneurial culture that attracted talent to insurance now draws technologists and data scientists.

What we're witnessing is rare in corporate history—a successful transformation that preserves rather than destroys the founding culture. Berkley isn't becoming a tech company that happens to sell insurance; it's remaining an insurance company that happens to use technology brilliantly. The distinction matters enormously for long-term value creation.

VIII. Financial Performance & Market Position

The insurance business is simple at its core: collect premiums, invest the float, pay claims, and hope you priced the risk correctly. But beneath W. R. Berkley's 2024 record performance lies a more complex truth about capital allocation and underwriting excellence. The Company once again set new financial records in 2024. Full year results were highlighted by record net income, with outstanding underwriting performance and net investment income, culminating in a 23.6% return on beginning of year equity. Growth in book value per share was 23.5%, before $836 million of capital returned to shareholders through special and ordinary dividends and share repurchases.

Let's start with the crown jewel: underwriting performance. Our calendar year combined ratio of 90.2% once again demonstrated our focus on managing volatility. For context, a combined ratio below 100% means the company is making an underwriting profit—they're collecting more in premiums than they're paying out in claims and expenses. At 90.2%, Berkley is generating roughly a 10% profit margin on underwriting alone, before any investment income. This is extraordinary in an industry where many competitors are happy to break even on underwriting and make their money on investments.

The growth trajectory tells an equally compelling story. Revenues have been growing at an average rate of 12.3% per year—well ahead of GDP growth and inflation. This isn't just premium growth for growth's sake; it's profitable expansion. For the full year 2024, the company achieved a return on equity of 23.6% and an operating return on equity of 22.4%. To put this in perspective, the average S&P 500 company generates ROE around 15%. Berkley is generating returns 50% higher than the market average.

The investment portfolio has become a significant profit driver as interest rates normalized. Setting further records in 2024, W. R. Berkley saw its net investment income grow 26.6% from 2023 to a high of $1.3 billion, while operating cash flow increased 25.6% to $3.7 billion. On this, the firm commented, "We positioned our investment portfolio well for changes in the environment, which resulted in robust growth in net investment income from our fixed-maturity portfolio and a strong contribution to total return from net unrealized gains on our equity portfolio. Current reinvestment rates continue to exceed our annual book yield, and our invested assets have increased from record operating cash flow, positioning us for further investment income growth in 2025."

The capital allocation philosophy deserves special attention. In 2024, W. R. Berkley Corporation returned a total of $835.6 million to shareholders, consisting of $412.3 million in special dividends, $303.7 million in share repurchases, and $119.6 million in regular dividends. This balanced approach—special dividends when excess capital accumulates, share buybacks when the stock is undervalued, and consistent regular dividends—demonstrates sophisticated capital management.

Today W.R. Berkley Corporation has the market capitalization of 26.85 B, positioning it as a mid-cap insurer with large-cap performance. The valuation metrics suggest the market appreciates but perhaps doesn't fully value the consistency. With a P/E ratio around 16, the stock trades at a modest premium to book value, reasonable for a company generating 20%+ returns on equity.

The balance sheet strength cannot be overstated. With minimal debt relative to equity and a conservative investment portfolio, Berkley has weathered every storm—from the dot-com bust to the financial crisis to COVID—without diluting shareholders or taking government bailouts. This fortress balance sheet allows them to be aggressive when others retreat, capturing market share during hard markets while maintaining underwriting standards.

What makes these numbers particularly impressive is their consistency. This isn't a one-year wonder or a cyclical peak. W. R. Berkley has maintained dividend payments for 51 consecutive years, demonstrating through multiple economic cycles that the model works in all weather. The company has averaged mid-teens ROE over decades, not quarters.

The cash generation is perhaps the most underappreciated aspect. Operating cash flow reached a record $1.2 billion, a 15.2% increase from the prior year. This isn't accounting profit but actual cash that can be reinvested or returned to shareholders. In a capital-intensive business like insurance, generating consistent free cash flow while growing is the holy grail.

The expense discipline shows in the numbers. While revenues have grown dramatically, the expense ratio has remained controlled. This operating leverage means that incremental premium dollars drop more profit to the bottom line. It's the compound effect of fifty years of operational excellence—every basis point of efficiency gained stays gained.

Looking at peer comparisons, Berkley consistently outperforms. While the industry celebrates single-digit ROEs in soft markets, Berkley maintains teens. While competitors write business at combined ratios above 100% hoping to make it up on investments, Berkley maintains underwriting profit through the cycle. While others consolidate to find synergies, Berkley grows organically.

The international diversification adds stability without sacrificing returns. With operations across multiple continents and currencies, Berkley has natural hedges against regional economic downturns or catastrophes. Yet they haven't fallen into the trap of growth for growth's sake—each international operation must meet the same return hurdles as domestic units.

The financial performance validates the strategy completely. You can talk about decentralization and specialization all day, but ultimately the numbers have to work. At W. R. Berkley, they don't just work—they sing. This is a company generating software-like returns with insurance-like stability, venture capital-like growth with blue-chip-like consistency. It's a remarkable achievement that deserves recognition as one of the great American business success stories.

IX. Playbook: Business & Investing Lessons

The W. R. Berkley story offers a masterclass in contrarian organizational design and capital allocation. While business schools teach centralization and standardization, Berkley built an empire on autonomy and specialization. While Wall Street demands quarterly earnings smoothing, Berkley embraces volatility in pursuit of long-term value. The lessons transcend insurance—they're universal principles for building enduring businesses.

Lesson 1: The Power of Decentralization in Large Organizations

The conventional wisdom says that as companies grow, they must centralize to achieve economies of scale. Berkley proves the opposite can be true. By maintaining 50+ autonomous units, they've created what economists call "small company effects at scale"—the entrepreneurial energy and accountability of a startup with the resources and stability of a Fortune 500 company.

The key insight is that information decay increases with organizational layers. In a traditional hierarchy, by the time market intelligence travels from the field to headquarters and back, the opportunity has vanished. Berkley's structure collapses this distance. The person seeing the opportunity is the person who can act on it. Speed becomes a sustainable competitive advantage.

But decentralization without accountability is chaos. Berkley solves this through radical transparency—every unit's P&L is visible, compensation is tied directly to performance, and there's nowhere to hide. This creates a Darwinian meritocracy where good ideas flourish and bad ones die quickly.

Lesson 2: Specialization as a Moat

Peter Thiel talks about competition being for losers. Berkley took this to heart decades before "Zero to One" was written. Instead of competing in commoditized markets, they found niches so specific that they had no real competitors. When you're the only insurer who truly understands the risks of traveling rodeos or high-altitude window washing, you have pricing power.

The lesson extends beyond insurance: Bill Berkley reflected that insurance is embedded in everything that happens in the real world. Whether it's Uber cars or shared ownership of bicycles or mopeds, or Airbnb, each one of those new ideas requires insurance. Every innovation creates new risks that someone must understand and price. By staying specialized and nimble, Berkley can move faster than larger, more bureaucratic competitors.

Lesson 3: Patient Capital and Long-Term Thinking

In an industry obsessed with quarterly combined ratios, Berkley plays a different game. They'll deliberately shrink during soft markets rather than chase unprofitable growth. They'll hold investments for decades rather than trade for quarterly gains. They'll spend years developing expertise in a new area before writing significant business.

Bill Berkley captured this philosophy perfectly: We're always concerned with the outcome that is the unforeseen event, which allows us to avoid the extremes and have more consistent results. We're not willing to take mediocre returns if the risks of zero or negative returns are substantial. This isn't about avoiding risk—insurance is fundamentally about taking risk. It's about taking intelligent risks where the odds are in your favor and the downside is capped.

Lesson 4: Culture as Infrastructure

Most companies treat culture as a nice-to-have, something for HR posters and annual retreats. At Berkley, culture is the operating system. The entrepreneurial mindset, ownership mentality, and long-term orientation aren't just values—they're selection criteria, compensation drivers, and strategic filters.

The culture is self-reinforcing. Entrepreneurial people attract other entrepreneurial people. Success in one unit inspires innovation in others. The decentralized structure means cultural antibodies quickly reject those who don't fit. After 50+ years, the culture has become stronger than any individual, including the founder.

Lesson 5: The Power of Aligned Incentives

Charlie Munger says "Show me the incentive and I'll show you the outcome." Berkley's incentive structure is a thing of beauty. Unit presidents are compensated based on multi-year underwriting profits, not premium growth. Investment managers are rewarded for long-term returns, not quarterly marks. The founding family still owns a significant stake, aligning their interests with outside shareholders.

This alignment cascades through the organization. When everyone from the CEO to the newest underwriter has skin in the game, decision-making improves dramatically. There's no agency problem because agents think like principals.

Lesson 6: Building Anti-Fragile Organizations

Nassim Taleb coined the term "anti-fragile" to describe systems that get stronger under stress. Berkley's decentralized structure is inherently anti-fragile. When one unit struggles, others thrive. When markets dislocate, they have dry powder to capitalize. When catastrophes strike, their diversification provides stability.

The anti-fragility extends to human capital. Because each unit operates independently, Berkley is constantly developing new leaders. If key executives leave, the bench is deep. If entire industries disappear, other units fill the gap. The organization is resilient by design, not luck.

Lesson 7: The Succession Paradox

Most founder-led companies struggle with succession because the founder is irreplaceable. Berkley solved this by making the founder's primary creation—the decentralized model—more important than the founder himself. When Rob Berkley succeeded his father, he was taking over a system, not filling shoes.

The lesson is profound: the greatest founders build organizations that don't need them. By pushing authority down and building cultural infrastructure, Bill Berkley created something that will outlast him by generations.

The Meta-Lesson: Contrarian Thinking Pays

Every major decision in Berkley's history went against conventional wisdom. Start an insurance company at 21? Decentralize instead of centralize? Focus on tiny niches instead of big markets? Shrink during soft markets instead of grabbing share? Each contrarian bet paid off precisely because it was contrarian.

The deeper insight is that competitive advantages come from doing things differently, not better. You can't beat incumbents at their own game. But if you change the game—as Berkley did with decentralization and specialization—you don't have to.

For investors, the Berkley model offers a template for identifying exceptional businesses: Look for companies with aligned incentives, decentralized decision-making, specialized expertise, patient capital, and cultures that attract A-players. These characteristics compound over time, creating widening moats and accelerating returns.

For operators, Berkley demonstrates that you can build a large company that maintains entrepreneurial energy, that culture can scale if designed correctly, and that giving up control can increase power. These aren't just insurance lessons—they're universal principles for building enduring organizations in any industry.

X. Analysis & Bear vs. Bull Case

Every investment thesis has two sides, and W. R. Berkley—despite its impressive track record—faces legitimate challenges alongside compelling opportunities. The debate isn't whether Berkley is a good company (it clearly is) but whether it's a good investment at current valuations given future uncertainties.

The Bull Case: Compounding Excellence

The optimists point to irrefutable evidence: consistent outperformance that spans decades, not quarters. Berkley has generated returns on equity above 15% for most of the past decade, with 2024's 23.6% ROE representing not an outlier but an acceleration. When a company consistently generates returns 50% above market averages, betting against it requires extraordinary conviction.

The decentralized model continues to prove its superiority, especially as markets fragment and niches multiply. Every new technology, regulation, or business model creates insurable risks that Berkley's specialized units can address faster than monolithic competitors. The structure that worked for traveling carnivals in the 1980s now works for cryptocurrency custody and AI liability.

Capital allocation remains best-in-class. Management returns excess capital through special dividends and buybacks while maintaining fortress balance sheet strength. With the founding family still holding significant equity, alignment between management and shareholders is absolute—rare in today's corporate landscape.

The embedded insurance opportunity could be transformational. As commerce increasingly moves online and consumers expect seamless experiences, Berkley's new embedded insurance initiatives position them at the intersection of traditional underwriting excellence and digital distribution. If they can crack the code of profitable digital distribution while maintaining underwriting discipline, the growth runway is enormous.

Perhaps most compelling is valuation. Despite consistent outperformance, Berkley trades at reasonable multiples—a P/E around 16 and modest premium to book value. Quality typically commands premium valuations; Berkley offers quality at fair prices.

The Bear Case: Shadows Lengthening

Skeptics raise uncomfortable questions starting with reserve adequacy. Some analysts have identified WRB as having concerning reserve positions, particularly in liability lines. While Berkley has never had major reserve blowups, the long-tail nature of liability insurance means problems can hide for years before emerging.

The reinsurance segment has been a persistent drag on returns. While the insurance operations consistently generate underwriting profits, reinsurance results have been volatile and occasionally disappointing. In a business where one bad year can erase five good ones, this volatility matters.

Premium growth is decelerating just as the market becomes more competitive. After years of hard market conditions that allowed aggressive price increases, the cycle appears to be turning. Professional liability, cyber, and other specialty lines that drove recent growth face increasing competition and pressure on margins.

Catastrophe exposure in an era of climate change presents existential questions. While Berkley has managed catastrophe risk well historically, the increasing frequency and severity of natural disasters could challenge even the best underwriting models. One hundred-year storms now happen every decade.

The competitive landscape is evolving rapidly. Insurtechs backed by billions in venture capital are attacking profitable niches. Traditional competitors are copying Berkley's decentralized model. Even tech giants like Amazon are entering insurance. The moats that protected Berkley for decades may be narrowing.

The Balanced View: Navigating Uncertainty

The truth, as usual, lies between extremes. Berkley faces real challenges, but their track record suggests unusual capability in addressing them. The reserve concerns are worth monitoring but should be contextualized against fifty years of conservative underwriting. The reinsurance struggles are disappointing but represent a small portion of overall operations.

The cycle dynamics matter but perhaps less than bears suggest. Berkley has prospered through multiple soft markets by maintaining discipline and exploiting hard markets when they arrive. Their ability to shrink profitably during soft markets and grow profitably during hard markets is proven.

Climate change is indeed a wildcard, but it affects all insurers equally. If anything, Berkley's diversification and specialization position them better than peers to navigate a changing risk landscape. They can exit unprofitable lines faster and enter emerging opportunities more nimbly.

The technology disruption narrative is overplayed. Insurance remains fundamentally about risk assessment and capital allocation—areas where experience and judgment matter more than algorithms. Berkley's embedded insurance initiatives show they can adopt new distribution models while maintaining underwriting excellence.

Investment Implications

For long-term investors, Berkley offers a compelling proposition: a proven business model generating superior returns through cycles, run by aligned management, trading at reasonable valuations. The company has navigated every crisis from the 1970s inflation to 2008 financial collapse to COVID, emerging stronger each time.

For traders and short-term investors, the picture is murkier. Insurance stocks are notoriously volatile, subject to catastrophe losses, interest rate movements, and cycle dynamics. Berkley's commitment to long-term value over quarterly smoothing means earnings can be lumpy.

The key question isn't whether Berkley is a good company—it demonstrably is—but whether it can maintain its advantages as the industry evolves. The bull case rests on proven execution and structural advantages. The bear case warns that past performance doesn't guarantee future results, especially as the competitive and environmental landscapes shift.

What tips the scales for many investors is management quality and alignment. With the Berkley family still significantly invested and Rob Berkley proving himself a worthy successor to his father, betting against this team requires courage or foolishness. They've navigated every storm for fifty years. Why would the next fifty be different?

XI. Epilogue & Future Outlook

The insurance industry stands at an inflection point. Climate change is rewriting risk models that worked for centuries. Technology is transforming distribution channels that haven't changed since Benjamin Franklin founded the first American insurance company. Demographics are shifting as wealth transfers between generations and geographies. Into this maelstrom, W. R. Berkley brings fifty years of evolution, adaptation, and profitable growth—suggesting the next chapter could be the most interesting yet.

The Embedded Insurance Revolution

The future of insurance distribution isn't agents and brokers—it's invisible, embedded, automatic. When you buy a product, insurance appears seamlessly. When you start a business, coverage activates instantly. When risks change, protection adjusts dynamically. Berkley's investment in embedded solutions positions them at the forefront of this transformation.

But embedded insurance isn't just about technology—it's about trust and underwriting. Many insurtechs can build slick apps; few can price risk profitably. Berkley brings something unique: five decades of underwriting data and discipline combined with modern distribution capabilities. They're not trying to disrupt insurance; they're trying to perfect it.

The High Net Worth Opportunity

The great wealth transfer has begun. Over $70 trillion will change hands from baby boomers to younger generations over the next two decades—the largest wealth transfer in human history. This wealth needs protection: art collections, wine cellars, yacht fleets, private aircraft, multiple homes across continents.

Berkley's high net worth initiatives target this opportunity precisely. These aren't mass market products but bespoke solutions for complex risks. When you own a Basquiat and a Bugatti, you need insurers who understand both the assets and the lifestyle. Berkley's specialty model was built for exactly this type of complexity.

Climate Adaptation, Not Climate Denial

While politicians debate climate change, insurers must price it. Berkley's approach is pragmatic: accept that weather patterns are changing, adjust models accordingly, price appropriately, and maintain discipline. They're not betting on climate stability; they're building resilience against climate volatility.

The company's geographic and line diversification provides natural hedges. When hurricanes hit Florida, earthquake coverage in California remains profitable. When floods devastate commercial property, professional liability continues generating returns. This portfolio approach to catastrophe risk is more robust than any single prediction about future weather patterns.

Technology as Tool, Not Master

Artificial intelligence and machine learning are transforming insurance, but not in the way most expect. The winners won't be companies with the best algorithms but those who combine artificial intelligence with actual intelligence. Berkley's approach—human judgment augmented by technology rather than replaced by it—positions them perfectly.

Each specialty unit can adopt technology appropriate to their niche. Cyber liability units use different tools than workers' compensation specialists. This bottoms-up innovation is more effective than top-down digital transformation. Technology serves the business, not vice versa.

The Organizational Model as Competitive Advantage

Looking forward, Berkley's decentralized structure becomes even more valuable. As markets fragment and niches multiply, monolithic insurers struggle to keep pace. But Berkley can spawn new units as fast as opportunities emerge. Cryptocurrency insurance? Create a unit. Space tourism liability? Launch a team. Synthetic biology coverage? Build expertise.

This cellular division model is infinitely scalable. Whether Berkley has 50 units or 500, the principles remain: local autonomy, specialized expertise, aligned incentives, cultural cohesion. It's an organizational structure built for a complex, fast-changing world.

The Enduring Power of Patient Capital

In a world of quarterly capitalism and algorithmic trading, Berkley's patient approach becomes increasingly differentiated. They can wait out soft markets while competitors chase unprofitable growth. They can invest in 10-year opportunities while others optimize for next quarter. They can build expertise while others buy momentum.

This patience is enabled by ownership structure—with the founding family still significantly invested, there's no pressure for short-term earnings manipulation. Rob Berkley can make decisions his public company peers cannot, creating strategic options others lack.

The Next Generation's Challenge

The transition from founder to second generation was managed brilliantly, but the third generation transition looms. Will the Berkley family maintain control? Will the culture survive without family leadership? Will the decentralized model work without its architects?

History suggests family businesses struggle beyond the third generation, but Berkley has defied conventional wisdom before. The institutional strength—the 50+ entrepreneurs running their own businesses within Berkley—provides stability beyond any individual or family.

China and the Next Frontier

Berkley has notably minimal exposure to China, the world's second-largest economy. As U.S.-China relations evolve and Chinese businesses expand globally, this could be opportunity or vulnerability. Will Berkley find profitable niches in Chinese risks? Or will Chinese insurers use their home market profits to compete globally?

The answer likely depends on specialization. Chinese insurers can compete on scale and price but struggle with specialized expertise. Berkley's model—deep knowledge of specific risks—translates across cultures better than commoditized products.

The Ultimate Question

Will W. R. Berkley be larger and more profitable in 2035 than 2025? The bear case sees a maturing business facing new competitors, climate challenges, and technology disruption. The bull case sees an adaptive organization with proven resilience entering new markets with wind at its back.

The answer depends less on predicting the future than on organizational capability. Berkley has reinvented itself repeatedly—from investment boutique to insurance holding company, from domestic to international, from traditional to digital distribution. This adaptive capacity, more than any specific strategy, suggests continued success.

Insurance is ultimately about promises—promises to pay when disaster strikes, promises to be there when needed, promises that span decades. W. R. Berkley has kept its promises for fifty years through inflation, recession, catastrophe, and pandemic. In an uncertain world, that reliability has value beyond any financial metric.

The epilogue isn't an ending but a continuation. The next chapter of the Berkley story remains unwritten, but the authors—thousands of entrepreneurs operating with autonomy and accountability—are already at work. If history is any guide, they'll find opportunity where others see only risk, build value where others see only complexity, and continue compounding excellence long after the current generation has passed the torch.

For investors, customers, and competitors alike, one thing seems certain: W. R. Berkley will remain formidable. They've built something rare in American business—an organization that gets stronger with age, more valuable with complexity, more profitable with patience. That's not just a business model; it's a philosophy of capitalism that deserves study, respect, and perhaps, investment.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube