Worthington Enterprises: Building Value Through Steel, Strategy, and Culture

I. Introduction and Episode Roadmap

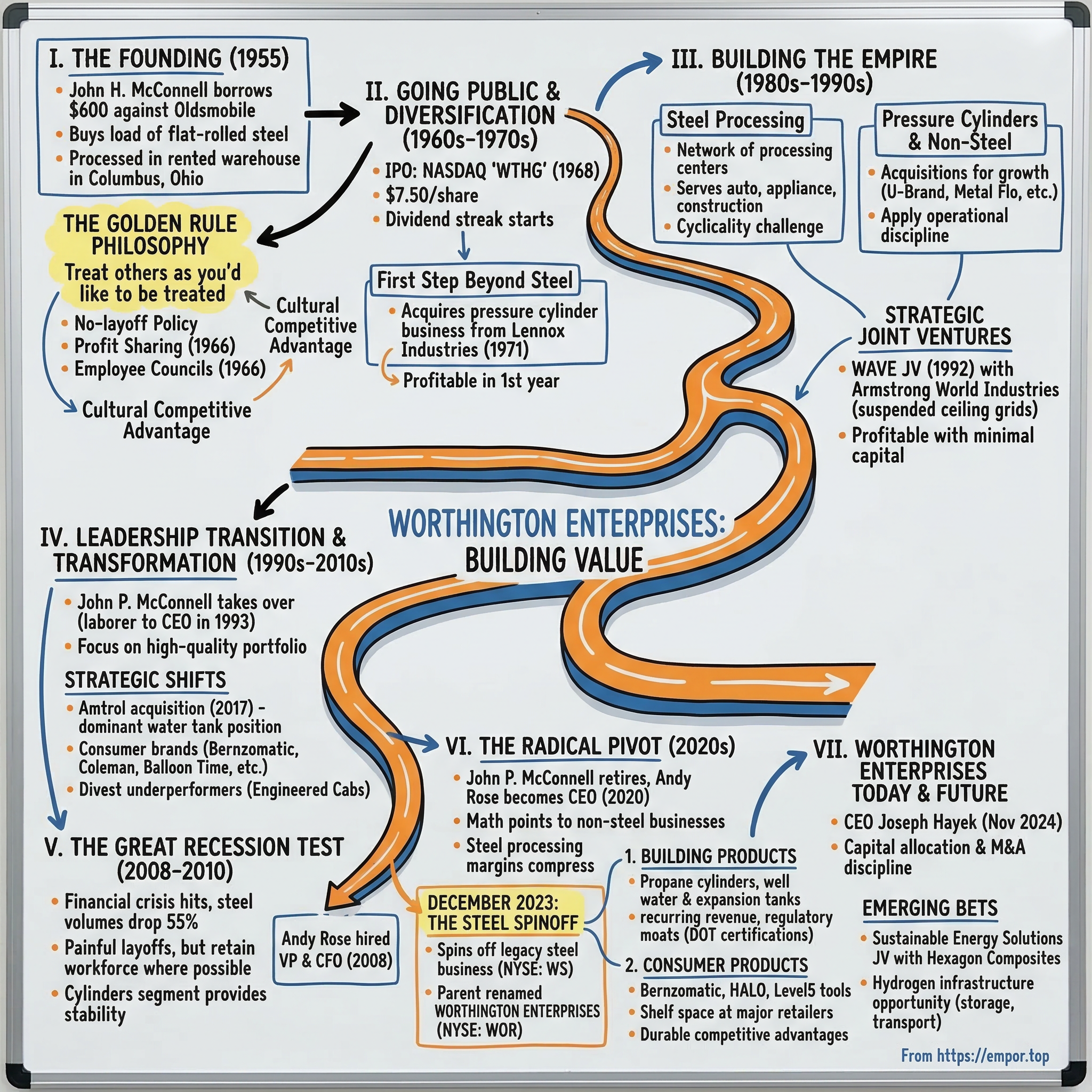

Picture this: a young steel salesman in 1955 Columbus, Ohio, borrows six hundred dollars against his Oldsmobile, buys a single load of flat-rolled steel, and starts processing it in a rented warehouse. Seven decades later, that six-hundred-dollar bet has become Worthington Enterprises, a company with a two-and-a-half-billion-dollar market capitalization, six thousand employees, and one of the most radical corporate transformations in American industrial history. In December 2023, after sixty-eight years of continuous operation, the company spun off its founding steel processing business entirely, essentially firing its own origin story.

That is the question at the heart of this deep dive: How does a company that literally had "Steel" in its original name decide that steel is no longer its future? And more intriguingly, how does a corporate culture built on a single philosophical principle, the Golden Rule, survive such a rupture?

Worthington's story is not a Silicon Valley disruption narrative. There are no hockey-stick growth charts or blitz-scaling playbooks. Instead, it is a masterclass in patient industrial capitalism, in how a family-controlled manufacturer navigated cyclicality, diversified thoughtfully, survived recessions without mass layoffs, and ultimately had the courage to shed its identity in pursuit of better returns. The company's trajectory touches on themes that matter deeply for long-term investors: culture as competitive advantage, the discipline of capital allocation, portfolio management in mature industries, and the emerging bet on hydrogen infrastructure that could define Worthington's next chapter.

Today, Worthington Enterprises trades on the NYSE under the ticker WOR at roughly forty-seven dollars per share. Its CEO is Joseph Hayek, a former investment banker who took the helm in November 2024. The company operates across Building Products, Consumer Products, and a nascent Sustainable Energy Solutions segment. Its products range from propane cylinders and helium tanks to Bernzomatic torches, Balloon Time party kits, and hydrogen storage systems. It generates about $1.15 billion in annual revenue with improving margins and a balance sheet carrying just seventy-six million dollars in net debt.

The company currently employs about six thousand people across its operations, down from the roughly twelve thousand at the combined Worthington Industries before the spinoff. Its beta of 1.2 suggests slightly higher volatility than the broader market, consistent with a mid-cap industrial company exposed to construction and consumer cyclicality. The fifty-two-week trading range of $39 to $71 reflects meaningful investor uncertainty about the post-spinoff growth trajectory.

But to understand where Worthington is going, you have to understand where it came from. And that story begins with a Depression-era kid from West Virginia who believed that treating people right was not just good ethics but the ultimate business strategy.

II. Founding Story and The John McConnell Vision (1955-1970s)

John Henderson McConnell was born on May 10, 1923, in Pughtown, West Virginia, a tiny community where his father worked in the steel mills for sixty cents an hour. The Great Depression shaped everything about McConnell's worldview: the value of hard work, the fragility of economic security, and the belief that loyalty between employer and employee was not just a nicety but a survival mechanism.

After high school, McConnell followed his father into the mills, starting as a laborer at Weirton Steel Corporation. He could have attended college on a football scholarship, but chose the factory floor instead. When World War II broke out, he enlisted in the U.S. Navy, spending three years in the Pacific aboard the aircraft carrier USS Saratoga. After the war, he used the GI Bill to attend Michigan State University, where he majored in business administration, played football, and graduated in 1949.

McConnell's post-college career began as a steel salesman for Weirton Steel, and it was in this role that he spotted the gap. Major steel producers were building ever-larger mills, chasing massive tonnage orders, and growing increasingly uninterested in filling the specialized, custom-cut orders that smaller manufacturers needed. A company making appliance parts, for instance, might need steel cut to specific widths, thicknesses, and shapes. The big mills simply did not want to bother. McConnell saw opportunity in that disdain.

In June 1955, he incorporated the Worthington Steel Company in Columbus, Ohio. His startup capital was famously modest: six hundred dollars borrowed against his 1952 Oldsmobile. He used that money to buy his first load of steel, which he processed and sold to local manufacturers. The business model was what the industry calls "toll conversion," essentially acting as a middleman between the giant steel mills and the smaller manufacturers who needed customized product. Worthington would buy large coils from the mills, then cut, slit, blank, and shape them to customer specifications.

First-year results were promising for a one-man operation: five employees, roughly $350,000 in sales, and about $14,000 in profit. Not bad for a business started with borrowed car money.

But what made McConnell different from the dozens of other small steel processors who emerged during the 1950s was not his processing equipment or his sales technique. It was his philosophy. From the very beginning, McConnell ran his company on what he called the Golden Rule: "We treat our customers, employees, investors, and suppliers as we would like to be treated." This was not a poster on the break room wall. It was the operating system of the entire company.

McConnell implemented three radical policies that defied the norms of mid-century American manufacturing. First, a no-layoff policy: when business slowed, he would shift workers to maintenance tasks, painting, equipment repair, anything to keep them employed. Second, profit sharing: beginning in 1966, all employees were put on salary and given quarterly profit-sharing checks. Third, employee councils: also introduced in 1966, these councils created a two-way communication channel between factory workers and management, decades before such practices became fashionable in management textbooks.

The cynics would say these were soft, feel-good policies that could not survive contact with economic reality. McConnell would argue the opposite. Employee retention was extraordinarily high, which meant lower training costs and deeper institutional knowledge. Workers who shared in the profits had direct incentive to reduce waste, improve quality, and serve customers better. And the no-layoff policy meant that when business recovered from downturns, Worthington could ramp up production faster than competitors who had to rehire and retrain.

By 1967, annual sales had reached $12.5 million. The company was growing fast enough to need external capital, and McConnell made the decision to go public. On October 29, 1968, Worthington made its first public stock offering, selling 150,000 shares at $7.50 per share on NASDAQ under the ticker WTHG. The company has paid a dividend every single quarter since that IPO, a streak that now stretches over fifty-seven years.

The move to public markets gave McConnell the capital to expand, but he was careful not to let Wall Street's short-term pressures compromise his philosophy. The company remained firmly founder-controlled, and the Golden Rule stayed at the center of every decision. In an era when most manufacturing companies treated workers as disposable inputs, paying them hourly wages and laying them off at the first sign of economic softness, McConnell was building something genuinely different. His employees were salaried, shared in the profits, and had a voice through councils. The result was a workforce that thought like owners, because in a very real sense, they were.

It is worth pausing to understand how unusual this was in 1960s American manufacturing. The United Auto Workers were locked in pitched battles with Detroit automakers over wages and benefits. Steel mills were notorious for adversarial labor relations. And here was McConnell in Columbus, Ohio, running a non-union shop where employees had profit sharing and job security, and where they voluntarily worked harder because they believed the system was fair. The company earned a spot in The 100 Best Companies to Work for in America in both the 1985 and 1993 editions, one of the few industrial manufacturers to make the list.

McConnell's personal life was also intertwined with Columbus in ways that matter for understanding the company's DNA. He was deeply philanthropic, contributing to Ohio State University, local charities, and community organizations. Most famously, he committed $120 million of his own money in 1997 to bring an NHL franchise to Columbus, founding the Columbus Blue Jackets. For McConnell, business and community were inseparable, and that ethos permeated every level of Worthington Industries.

By the early 1970s, Worthington was ready to take the first step beyond steel processing, and it would prove to be one of the most consequential decisions in the company's history.

III. Building the Steel Processing Empire (1970s-1990s)

In 1971, McConnell made an acquisition that would eventually reshape the entire company. He purchased a small, unprofitable pressure cylinder business from Lennox Industries in Columbus. The operation was struggling, but McConnell saw potential. Within its first year under Worthington management, the cylinder business turned profitable. That same year, McConnell renamed the company from Worthington Steel to Worthington Industries, a signal that ambitions extended beyond a single commodity.

Throughout the 1970s and 1980s, Worthington expanded aggressively on both fronts. The steel processing business grew through a combination of new facility construction and strategic acquisitions across North America. The company built a network of processing centers that could serve automotive OEMs, appliance manufacturers, construction companies, and agricultural equipment makers. Each facility was positioned to serve regional customers with quick turnaround, turning what the big mills treated as a nuisance into a reliable, high-service business.

The pressure cylinder business expanded too. In 1978, Worthington acquired U-Brand Corporation, adding pipe fittings. In 1988, it bought Metal Flo Corp in Canada, establishing a presence in the Canadian cylinder market. By 1992, it had acquired North American Cylinders in Alabama, moving into acetylene cylinders and high-pressure tanks. Each acquisition followed the same playbook: buy underperforming or undermanaged businesses, apply Worthington's operational discipline and culture, and turn them profitable.

But the steel processing business faced an inherent challenge that would haunt it for decades: cyclicality. Steel is one of the most cyclical commodities in existence. When the economy booms, steel demand surges and processors do well. When recession hits, orders evaporate overnight. Running a no-layoff policy through steel's boom-and-bust cycles required extraordinary financial discipline and a willingness to sacrifice short-term profitability for long-term employee loyalty.

McConnell's solution was twofold. First, he built a buffer through diversification, which is why the cylinder and other non-steel businesses mattered strategically, not just financially. Second, he pioneered a joint venture strategy with steel producers themselves. The most significant of these was the WAVE joint venture, founded in 1992 as a fifty-fifty partnership with Armstrong World Industries. The venture combined Worthington's National Rolling Mills acquisition from 1984, which made steel grids for suspended ceiling systems, with Armstrong's ceiling product expertise. WAVE was, by all accounts, "founded on the strength of a handshake," and it would grow into a highly profitable operation employing over four hundred people across seven manufacturing facilities. For long-term investors, WAVE is notable because it demonstrated that Worthington could create value not just through outright acquisition but through partnership, sharing risk and expertise in ways that generated superior returns.

The leadership transition from founder to second generation happened gradually, which is itself a lesson. John P. McConnell, the founder's son, started at the company in 1975 as a general laborer at a Louisville, Kentucky steel plant, not in the corner office. He worked his way through multiple operating roles over nearly two decades before succeeding his father as CEO in 1993 and becoming Chairman in 1996. The elder McConnell stepped back slowly, confident that the philosophy he had built was embedded deeply enough to survive beyond his direct control. He was right, but the real test was still decades away.

To understand the toll conversion model that drove Worthington's growth, think of it like a tailor for metal. A steel mill produces enormous coils of flat-rolled steel, sometimes weighing twenty tons or more. But a washing machine manufacturer needs steel cut to precise dimensions. An auto parts maker needs it stamped into specific shapes. A construction company needs it bent at exact angles. The mills do not want to handle this customization because it slows their high-volume production lines. Worthington fills that gap, buying the large coils, bringing them to its processing centers, and using specialized equipment, slitters, blankers, levelers, and presses, to transform them into exactly what each customer needs. The processor earns a margin on the conversion service, which is typically modest on a per-ton basis but can be quite profitable at scale.

The challenge is that this is fundamentally a spread business. When steel prices rise, the processor's raw material costs increase, and margins can compress if the company cannot pass through price increases quickly enough. When prices fall, the processor may be sitting on inventory purchased at higher prices. To illustrate: if Worthington bought ten thousand tons of steel at $800 per ton and the market price dropped to $600 before the processed product was sold, the company would face $2 million in potential inventory losses on that single batch. Multiply that across the millions of tons processed annually, and you can see how quickly commodity price swings can wipe out an entire quarter's profit.

This inherent commodity exposure made steel processing a business that could produce excellent returns in good years and devastating losses in bad ones, a dynamic that would eventually push Worthington to seek refuge in more stable product lines. It also explains why the company's earnings were so volatile on a year-to-year basis, making it difficult for long-term investors to value the stock with confidence.

In 2000, Worthington Industries moved from NASDAQ to the New York Stock Exchange, trading under the familiar WOR ticker. By then, the company had grown to twelve thousand employees and $1.9 billion in annual sales. The McConnell family remained firmly in control, and the Golden Rule philosophy was deeply embedded. The question was whether steady and reliable would be enough for the next chapter.

IV. The Diversification Era and Building the Portfolio (1990s-2000s)

Under John P. McConnell's leadership, Worthington's diversification strategy accelerated with clear intent. The younger McConnell understood something that his father's generation did not fully confront: steel processing alone could not deliver the growth and margin profile that public market investors increasingly demanded. The pressure cylinder business and joint ventures like WAVE were already proving that Worthington could generate superior returns outside its core steel operations, and McConnell leaned into that signal.

The pressure cylinders segment became the growth engine of the portfolio. What had started as a small Columbus acquisition in 1971 expanded into a dominant North American platform. The business manufactured and distributed propane tanks, helium cylinders, refrigerant containers, and specialty tanks for medical and industrial applications. Worthington built consumer brands that transformed commodity metal containers into recognizable products: Bernzomatic for handheld torches, Coleman for outdoor products, Balloon Time for helium party kits, and Mag-Torch for professional-grade equipment.

The consumer brand strategy was particularly shrewd. Propane tanks and helium cylinders are, at their core, commodity products. A tank is a tank. But Worthington recognized that in the consumer and retail channels, brand recognition, packaging quality, and distribution relationships created meaningful differentiation. Getting shelf space at Home Depot, Lowe's, and Tractor Supply required more than just manufacturing capability; it required marketing, logistics, and retailer relationships. Once established, those relationships became barriers to entry that commodity competitors struggled to replicate.

The Engineered Cabs business, which manufactured enclosed operator cabs for agricultural and construction equipment, added another diversification leg. Think of these as the protective enclosures that surround the driver's seat on a combine harvester or a construction excavator: custom-engineered metal and glass structures that must meet strict safety and ergonomic standards. It was a niche business, but niches can be profitable when you have the engineering capability and customer relationships to serve them well.

On the acquisition front, the mid-1990s were particularly active. Worthington acquired Dietrich Industries in 1996 for $146 million plus $30 million in assumed debt, adding metal framing products used in commercial construction. The following year, the Gerstenslager Company acquisition for $113 million strengthened automotive body panel capabilities. Each acquisition followed the same logic: industrial businesses with strong customer relationships, modest but defensible margins, and opportunities for operational improvement under Worthington's cultural and operational playbook.

The acquisition strategy revealed something important about McConnell's approach to growth. Unlike many industrial conglomerates of the era that acquired aggressively and then struggled to integrate, Worthington was selective and patient. The company preferred businesses that were underperforming relative to their potential, often due to poor management or cultural dysfunction, because those were the businesses where the "Worthington Way" could make the biggest difference. Buy a mediocre business, install the Golden Rule, share profits with employees, invest in equipment and training, and watch productivity climb. It was a repeatable formula that worked because the cultural foundation was genuine, not a corporate veneer.

Through the 2000s, the portfolio hummed along. Steel processing still contributed the lion's share of revenue, roughly sixty to sixty-five percent, but the diversified segments increasingly drove profitability. The cylinders business in particular showed superior margins because it combined manufacturing with distribution networks and consumer brands, creating layers of value-add that pure steel processing could not match.

The joint venture strategy continued to pay dividends. Beyond WAVE, Worthington maintained partnerships with major steel producers that allowed it to share the capital intensity and cyclical risk of steel processing. These ventures were structured so that each partner contributed complementary capabilities: Worthington brought processing expertise and customer relationships, while mill partners contributed raw material supply and production capacity.

Financially, the company through the 2000s delivered exactly what you would expect from a well-managed industrial conglomerate: consistent but unspectacular returns, reliable dividends, and a balance sheet that reflected disciplined capital allocation. Revenue grew steadily, and the stock performed in line with industrial peers.

The CEO succession from John H. McConnell to John P. McConnell, while smooth operationally, raised the perennial question that haunts family-controlled businesses: was the son chosen because he was the best candidate, or because he was the founder's son? By most accounts, John P. earned the role through nearly two decades of operational experience, starting as a laborer and working through every level of the organization. The company's continued growth and cultural coherence under his leadership suggests the transition was meritocratic, but the question would resurface again when the company eventually transitioned to non-family leadership.

For long-term investors, the real value was accumulating beneath the surface, in the form of brands, distribution networks, customer relationships, and a culture that would prove its worth when adversity struck. That test arrived with devastating force in 2008.

V. The Great Recession and Resilience Test (2008-2010)

The financial crisis of 2008-2009 hit Worthington like a wrecking ball. The company's fiscal year ends in May, so its fiscal 2009 results captured the full horror of the recession. Net sales fell to $2.6 billion from $3.1 billion the prior year, a fourteen percent decline. Volumes in the steel processing business plummeted an astonishing fifty-five percent as the automotive industry collapsed and construction ground to a halt. General Motors and Chrysler, major Worthington customers, were fighting for survival.

The financial damage was severe: a net loss of $108.2 million for fiscal 2009, compared to net earnings of $107.1 million just a year earlier. The loss included $105 million in inventory write-downs as steel prices cratered, a $96.9 million goodwill impairment charge, and $43 million in restructuring costs. John P. McConnell, still serving as Chairman and CEO, described the period bluntly: "The last nine months of our fiscal year were very difficult as the global economy plunged into deep recession."

The recession tested the Golden Rule philosophy in ways that nothing before had. The no-layoff policy, which had been a point of pride for over fifty years, buckled under the strain. Worthington announced facility closures in Louisville, Kentucky and Renton, Washington, and a workforce reduction of nearly three hundred employees. For a company that had built its identity on never letting people go, this was a painful concession to economic reality.

But the company's response, even in its compromised form, stood in stark contrast to competitors who slashed headcounts by the thousands. Where possible, Worthington used the playbook McConnell had established decades earlier: reduced hours, temporary salary cuts, reassignment to maintenance work, and voluntary sabbaticals. The goal was to preserve as much of the workforce as possible so that when demand recovered, the company would be ready to ramp quickly.

That bet paid off. When the economy began recovering in 2010, Worthington's experienced workforce allowed it to resume production faster and with higher quality than competitors who had gutted their organizations. Employee loyalty, built over decades of fair treatment, translated directly into operational advantage during the recovery.

The portfolio benefits of diversification also showed up clearly. While the steel processing and automotive segments were in crisis, the pressure cylinders business remained relatively stable. People still needed propane for their grills, helium for party balloons, and refrigerant for their HVAC systems. Consumer staple products in the cylinder segment provided a floor under the company's performance that pure-play steel processors did not have.

For the company's future strategic direction, the 2008 recession was an inflection point even though it was not recognized as such at the time. The crisis laid bare a fundamental truth: the steel processing business was enormously capital-intensive, deeply cyclical, and increasingly commoditized, while the cylinders and consumer products businesses were more resilient, higher-margin, and growing. It would take another decade for the company to act on that insight, but the seeds of the 2023 spinoff were planted in the wreckage of the Great Recession.

One notable personnel decision during this period would prove enormously consequential. In 2008, Worthington hired Andy Rose as Vice President and CFO. Rose arrived from the outside during the depths of the crisis, and his fresh perspective on the company's portfolio and capital allocation would eventually reshape its entire strategic trajectory.

The recession also revealed something important about the structural economics of Worthington's different businesses. Steel processing, even at its best, operated on thin margins that could evaporate entirely when volumes dropped. The business required enormous amounts of working capital, inventory that could depreciate rapidly, and continuous capital investment in equipment. Cylinders and consumer products, by contrast, maintained margins through the downturn because their end markets were more diversified and their products had more pricing power. A propane tank might be a commodity, but consumers were not shopping around for the cheapest option during a recession; they were simply refilling the tank they already had at their nearest exchange location. This structural difference would become the intellectual foundation for the spinoff decision a decade and a half later.

VI. The Transformation Inflection Point: 2010s Strategic Shifts

The 2010s were when Worthington Industries began its slow transformation from steel processor with diversifications to diversified industrial company with steel heritage. The changes were subtle at first, but in retrospect, the decade was a masterclass in managed decline of a legacy business and patient construction of a higher-quality portfolio.

The broader steel industry was undergoing its own structural shifts during this period. Mini-mills like Nucor and Steel Dynamics had fundamentally disrupted the economics of steelmaking, producing high-quality flat-rolled products at costs that traditional integrated mills struggled to match. For steel processors like Worthington, this meant more competitive sourcing options but also more competition in the processing space itself, as mini-mills began offering their own value-added services to customers. The spread between raw material cost and processing revenue was narrowing, making it harder to earn attractive returns even in good economic times.

Simultaneously, the automotive industry was pursuing lightweighting strategies to meet increasingly stringent fuel economy standards. Aluminum, carbon fiber, and advanced high-strength steels were replacing conventional steel in vehicle bodies, changing the mix of materials that processors needed to handle. Worthington invested in capabilities to process these newer materials, but the trend was unmistakable: the steel processing business was facing headwinds that went beyond cyclicality into structural decline.

In September 2020, a pivotal leadership change formalized what had been building for years. John P. McConnell stepped down as CEO after twenty-seven years, handing the role to Andy Rose. McConnell remained as Executive Chairman but would retire from the board entirely in September 2023. For a company that had been led by a McConnell for sixty-five of its sixty-eight years of existence, this was seismic. The family was stepping back, and professional management was taking full control.

The strategic rationale that Rose and his team pursued was straightforward: steel processing margins were compressing as the industry consolidated and competition from minimills intensified. Automotive lightweighting trends threatened to substitute aluminum for steel in key applications. Meanwhile, the pressure cylinders business was delivering superior returns on invested capital with less cyclicality. The math pointed clearly toward tilting the portfolio.

The divestiture of the Engineered Cabs business in November 2019 was an early and telling signal. Worthington sold the unit to Angeles Equity Partners in a cashless transaction, retaining only a minority ownership position. Angeles merged it with another cab manufacturer, Crenlo Cab Products, to create a larger combined entity. For Worthington, the message was clear: businesses that did not fit the company's evolving margin and growth profile would be exited, even if they had been part of the portfolio for decades.

The real strategic development of the era was the 2017 acquisition of Amtrol for $283 million, which was the company's largest acquisition at the time. Amtrol was the largest U.S. provider of expansion tanks for plumbing and HVAC applications, and the deal dramatically expanded Worthington's Building Products segment. For those unfamiliar with expansion tanks, these are vessels installed in water heater and boiler systems that absorb the pressure changes caused by water expanding as it heats. Building codes in most U.S. jurisdictions require them, which means demand is directly tied to new construction and water heater replacement cycles, both of which are large, predictable, and non-discretionary markets. The Amtrol deal gave Worthington a dominant position in this space, adding a product line with regulatory barriers to entry, code-mandated demand, and long replacement cycles of ten to fifteen years.

In fiscal 2022, Worthington made another transformative acquisition: Tempel Steel Company, a precision motor and transformer laminations manufacturer, for approximately $255 million. Tempel added five facilities, 1,500 employees, and importantly, a strong presence in electrical steel laminations used in motors and transformers. This was significant because it bolstered the steel processing business to a scale where it could credibly stand alone as a public company. In other words, the Tempel acquisition was not just growth for growth's sake; it was preparation for separation.

On the consumer products side, the June 2022 acquisition of Level5 Tools for approximately $55 million plus earn-out brought premium drywall taping and finishing tools into the portfolio. General Tools & Instruments had been acquired in 2021, adding over 1,200 specialized tools. These moves built out a Consumer Products segment with strong brands and distribution relationships that could stand independently of the steel processing operations.

Capital allocation shifted noticeably during this period. The company became more disciplined about return on invested capital, more willing to divest underperformers, and more focused on higher-margin acquisitions. The total picture was a company methodically rebuilding itself, shedding lower-return assets and acquiring higher-return ones, all while maintaining the cultural foundation that McConnell had established.

The revenue segmentation data tells this story with remarkable clarity. In fiscal 2015, Steel Processing generated $2.15 billion, Pressure Cylinders $1.0 billion, and Engineered Cabs $193 million. By fiscal 2019, Steel Processing was $2.44 billion, Pressure Cylinders had grown to $1.21 billion, and Engineered Cabs had shrunk to $116 million before being divested. The cylinders business was growing faster, with better margins, and requiring less incremental capital. Yet the stock traded at a multiple that reflected the consolidated company's blended economics, dominated by steel processing's thin margins and heavy cyclicality.

For investors watching during this era, the challenge was precisely this: the financial results still looked like a cyclical steel company because steel processing dominated the revenue line. The market was not giving Worthington credit for its higher-quality businesses because they were buried inside a conglomerate structure. Wall Street analysts covered the company as a steel stock, it appeared in steel industry indices, and it attracted investors who wanted cyclical commodity exposure. The consumer brands and building products investors who might have been natural holders of Worthington's non-steel businesses were nowhere to be found. That recognition gap would become the primary argument for the spinoff.

VII. The WAVE Joint Venture and Cylinders Dominance (2017-2020)

The late 2010s and early 2020s were the period when Worthington's non-steel businesses truly came into their own. The pressure cylinders operation had grown from that tiny 1971 Lennox acquisition into North America's dominant player, and the WAVE joint venture continued to generate outsized returns with minimal capital requirements from Worthington.

WAVE, the Armstrong Worthington Venture, deserves special attention because it illustrates one of Worthington's most underappreciated strategic capabilities: the ability to create value through partnership. The fifty-fifty joint venture with Armstrong World Industries had been operating for over twenty-five years by this point, manufacturing commercial suspended ceiling and drywall grid systems across seven facilities. WAVE consistently contributed equity income to Worthington's financial statements, essentially free cash flow from a capital-light structure that required no additional investment.

The cylinders business, meanwhile, was undergoing its own transformation. The market dynamics in pressure cylinders were fundamentally different from steel processing. Regulatory barriers were high: every cylinder had to meet Department of Transportation safety certifications. Distribution networks took decades to build. Customer relationships in the propane exchange market created genuine switching costs because end users became accustomed to specific exchange locations and networks. These structural advantages produced more predictable earnings and higher returns on capital than steel processing could ever deliver.

The Amtrol acquisition in 2017 had added water system tanks to the portfolio, expanding the total addressable market while sharing the same manufacturing expertise and distribution infrastructure. By 2020, Worthington was the clear leader in North American pressure cylinders, with a portfolio spanning propane, helium, refrigerant, medical, and industrial applications.

There is an important distinction between the economics of manufacturing cylinders and processing steel that explains why the cylinders business commanded higher valuations. In steel processing, Worthington was essentially a middleman: buying commodity steel at market prices, adding relatively modest value through cutting and shaping, and selling into competitive industrial markets. The processor's margin depended heavily on steel price movements and volume throughput. In cylinders, the economics were fundamentally different. A pressure cylinder is an engineered safety product with DOT certification, brand identity, and distribution infrastructure layered on top. The raw material cost, primarily steel, was a smaller proportion of the final product value. The rest was engineering, testing, certification, logistics, and brand, all of which were higher-margin activities with less commodity exposure. This distinction explains why investors were willing to pay a premium for Worthington's cylinder earnings but discounted its steel processing earnings.

COVID-19's impact on Worthington was a perfect illustration of the portfolio's mixed character. The automotive segment, still part of the steel processing operation, suffered as auto plants shut down. But cylinders surged. Stay-at-home orders drove propane demand as people grilled more, invested in outdoor heating, and upgraded their outdoor living spaces. Balloon Time helium kits flew off shelves as parents threw home birthday parties. The consumer products segment benefited from the same home improvement boom that lifted Home Depot and Lowe's.

By fiscal 2021, Worthington delivered extraordinary results: net income of $724 million on revenue of $3.2 billion, driven by both the COVID-related demand surge and soaring steel prices. These results were somewhat artificial, reflecting a once-in-a-generation commodity cycle, but they served a strategic purpose: they filled the company's war chest with cash and demonstrated the earnings power of the non-steel businesses. The WAVE joint venture, meanwhile, benefited from construction activity in 2024 and expanded into data center solutions, adding another growth vector to the partnership that had begun with a handshake three decades earlier.

The revenue mix told the strategic story clearly. In fiscal 2021, steel processing still contributed about $2.1 billion of the $3.2 billion in revenue. But by fiscal 2023, the segmentation had evolved: Building Products generated $586 million, Consumer Products $686 million, and the new Sustainable Energy Solutions segment contributed $146 million. The non-steel businesses were approaching the scale needed to support a standalone public company, and the board knew it.

One detail that reveals the maturation of the non-steel businesses: by fiscal 2022, the Pressure Cylinders segment, which had been renamed and reorganized into Building Products and Consumer Products, was generating revenue of roughly $1.3 billion on its own, not far from the $1.4 billion total company revenue when Worthington first went public decades earlier. These were no longer side businesses or diversification experiments; they were the core of a legitimate mid-cap industrial enterprise. The question was no longer whether they could stand alone, but when the board would make the call.

VIII. The Radical Pivot: The Steel Spinoff Decision (2022-2024)

On November 9, 2023, Worthington Industries' board approved the separation of its steel processing business into an independent public company. Three weeks later, on December 1, 2023, the split became reality. Shareholders received one share of Worthington Steel (NYSE: WS) for every share of Worthington Industries they held, and the parent company renamed itself Worthington Enterprises, continuing to trade as WOR.

After sixty-eight years, the company spun off the very business that had created it.

The strategic logic was compelling on paper. Steel processing and the diversified products businesses had fundamentally different capital requirements, growth profiles, margin structures, and investor appeal. Steel processing was mature, deeply cyclical, and capital-intensive, requiring continuous investment in equipment and facilities just to maintain market position. The cylinders, consumer products, and sustainable energy businesses had better growth trajectories, higher returns on invested capital, and appeal to a different class of investor.

There was also a valuation argument. Conglomerate discounts are real, and Worthington had been living with one for years. Public market investors increasingly preferred pure-play exposure. An infrastructure fund interested in steel processing had no interest in holding exposure to Balloon Time helium kits, and conversely, a consumer products investor did not want to bear the risk of steel price volatility. By separating, each business could attract its natural shareholder base and be valued on its own merits.

The preparation for the spinoff was itself a multi-year strategic exercise. The Tempel Steel acquisition in fiscal 2022, which had puzzled some investors at the time, now made sense in retrospect: it was designed to give the steel processing business enough scale, diversity, and standalone viability to succeed as an independent company. Without Tempel's electrical steel laminations adding another billion-plus in revenue and providing exposure to growing markets like electric vehicle motors, the steel processing operation might have been too small or too narrowly focused to attract investor interest as a standalone entity. In essence, Worthington spent $255 million on an acquisition that was not intended to strengthen the parent company but to prepare its future child for independence.

The execution was clean. Worthington Steel, led by CEO Geoffrey Gilmore, took the legacy steel processing and electrical steel laminations businesses, including the Tempel operations. It was a roughly $3.4 billion annual revenue company, immediately added to the S&P SmallCap 600 index. Worthington Enterprises retained the Building Products, Consumer Products, and Sustainable Energy Solutions segments, emerging as a $1.2 billion revenue company with a leaner, higher-margin profile.

The leadership split was equally clean. Andy Rose remained CEO of Worthington Enterprises initially, with Joseph Hayek serving as Chief Financial and Operations Officer. Gilmore, who had deep steel processing experience, took the Worthington Steel helm. The McConnell family's direct involvement in governance ended with John P. McConnell's retirement from the board in September 2023, though the family retained significant share ownership in both entities.

Market reaction was initially muted, as spinoffs often are. The shares of newly independent companies typically underperform in the first six months as index funds that held the parent company automatically sell the smaller spinoff, creating artificial selling pressure unrelated to fundamentals. Investors also needed time to understand the new structures and develop independent financial models. But the thesis was clear: Worthington Enterprises would trade at a higher multiple because its businesses merited it, while Worthington Steel would attract value-oriented investors comfortable with cyclical industrial exposure.

The financial logic was reinforced by the numbers. Looking at the historical revenue segmentation, steel processing had generated $3.93 billion in fiscal 2022, dwarfing the combined $1.3 billion from Building Products, Consumer Products, and Sustainable Energy Solutions. But those smaller segments generated disproportionate operating income. The market assigns different multiples to different types of earnings: stable, growing, branded product earnings command premium valuations, while cyclical commodity earnings trade at discounts. By separating, each dollar of earnings could be valued at its appropriate multiple.

The cultural challenge was perhaps the most profound dimension of the separation. The "Worthington Way" had been a unifying force across the entire organization for nearly seven decades. Could it survive partition into two separate companies, each with its own board, management team, and strategic priorities? Both companies committed to maintaining the Golden Rule philosophy, but institutional culture is fragile, and spinoffs have a way of creating identity crises. Worthington Enterprises kept the name, the headquarters at 200 Old Wilson Bridge Road in Columbus, and the cultural heritage. Worthington Steel moved next door to 100 Old Wilson Bridge Road, literally a few steps away but operationally a world apart.

The academic literature on spinoffs suggests that separations tend to create value when the businesses being separated have genuinely different strategic needs, when management attention is diluted by the conglomerate structure, and when the market is applying an inappropriate discount to the combined entity. Worthington's spinoff checked all three boxes. Steel processing needed heavy capital investment in equipment and working capital, a tolerance for cyclical swings, and a management team focused on operational efficiency in a commodity business. Building products and consumer brands needed innovation, brand building, M&A discipline, and a management team focused on growth and margin expansion. Asking one leadership team to excel at both was asking too much.

For investors evaluating the spinoff, the key question was whether Worthington Enterprises could deliver on its promise of superior growth and margins without the steel processing revenue that had been its financial anchor for decades. The early post-spinoff data would begin to answer that question.

IX. Worthington Enterprises Today: The New Company (2024-Present)

The Worthington Enterprises that emerged from the December 2023 spinoff is a fundamentally different company from the one John McConnell founded. With steel processing gone, the company now operates through two primary segments: Building Products and Consumer Products, with a Sustainable Energy Solutions operation structured as a joint venture.

Building Products is the larger segment, generating $654 million in fiscal 2025 revenue. This segment manufactures and sells propane and refrigerant cylinders, well water and expansion tanks, and specialty products sold primarily to gas producers, distributors, and building materials companies. The Amtrol acquisition gave this segment a dominant position in water system tanks, and the ongoing investment in propane cylinder exchange networks creates the kind of recurring revenue stream that investors love in industrial businesses.

Consumer Products contributed $500 million in fiscal 2025 revenue. This segment sells branded tools, outdoor living products, and celebration products under recognizable names like Bernzomatic, Coleman, Balloon Time, Mag-Torch, Garden-Weasel, Level5, and General Tools. Distribution runs primarily through the major home improvement and outdoor retailers. The June 2024 acquisition of HALO, an outdoor cooking company making pizza ovens, griddles, and pellet grills, expanded the segment's presence in the fast-growing outdoor living category.

The Sustainable Energy Solutions business took a strategic turn in June 2024 when Worthington sold 49% of the segment to Hexagon Composites for approximately $10 million, forming a joint venture. In the same transaction, Worthington acquired Hexagon Ragasco, the global market leader in composite LPG cylinders, for approximately $98 million. This was a clever swap: Worthington traded direct ownership of a small, pre-revenue hydrogen business for a partnership with a global composites leader while simultaneously acquiring Ragasco's established, profitable composite cylinder operation.

The hydrogen bet, while derisked through the joint venture structure, remains the most speculative element of Worthington's strategy. The Sustainable Energy Solutions segment offers on-board fueling systems and gas containment solutions for hydrogen, compressed natural gas, and other industrial gases. To understand why this matters, consider the basic physics: hydrogen is the lightest element in the universe and must be stored at extremely high pressures, typically 350 to 700 bar, to achieve useful energy density. Building containers that can safely hold gas at these pressures requires precisely the kind of metallurgical and composite engineering expertise that Worthington has spent decades developing for propane and industrial gas cylinders. The company's Cosmos product line includes both stationary storage bundles for hydrogen fueling stations and transportable systems designed for road transport in compliance with European safety standards.

If hydrogen infrastructure deployment accelerates as many analysts project, Worthington's combination of manufacturing expertise and Hexagon's composite technology could position the joint venture as a significant player. But the timing is uncertain, and the revenue contribution remains minimal. Worthington has committed to a net-zero emissions pathway by 2050 in line with the Science Based Targets initiative, which aligns its corporate sustainability goals with its business strategy in hydrogen and alternative fuels.

On the acquisition front, Worthington has been active. In January 2026, the company completed the acquisition of LSI Group, a Logansport, Indiana-based manufacturer of standing-seam metal roof clips and retrofit components. The deal extends Worthington's Building Products segment into the commercial metal roofing market, adding brands like BPD, Logan Stampings, and Roof Hugger. According to management commentary from the fiscal Q2 2026 earnings call in December 2025, the acquisition contributed to a nineteen percent year-over-year increase in net sales to $327.5 million.

Perhaps most intriguingly, Worthington is developing meaningful exposure to data center construction. As artificial intelligence drives massive investment in data center infrastructure, the company's building products, metal roofing components, and HVAC-related tanks are finding growing demand. Management has highlighted this as a secular growth driver, and analysts have noted that data center-related revenue is becoming a material portion of Building Products sales.

The financial profile of the new company is markedly different from old Worthington Industries. Fiscal 2025 revenue was $1.15 billion with gross profit of $318 million, representing a gross margin of about twenty-eight percent, substantially higher than the low-teens margins typical of steel processing. Operating cash flow of $210 million and free cash flow of $159 million supported a clean balance sheet with just $76 million in net debt. The current ratio stands at 3.5, reflecting significant financial flexibility.

Leadership under CEO Joseph Hayek represents a new chapter. Hayek, who took over from Andy Rose on November 1, 2024, brings a different background than any previous Worthington leader. Born in 1972, he earned his bachelor's degree from Miami University in Ohio and an MBA from Duke University, where he was named a Rollins Scholar. His career began in investment banking, spending a decade at Raymond James and Wachovia advising industrial companies on mergers and capital markets transactions. He then served as president of PCM/Sarcom, an IT solutions provider, before joining Worthington in 2014 as VP of Mergers and Acquisitions.

Hayek's trajectory within Worthington tells you everything about the company's strategic evolution. He started in M&A, moved to VP and General Manager of the Oil and Gas Equipment business unit, then became CFO in 2018, where he led the company through COVID to record earnings and oversaw the development of the "Worthington 2024" strategic initiative that culminated in the steel spinoff. After the separation, he served as Chief Financial and Operations Officer before being named CEO.

His leadership team includes Colin Souza as CFO, born in 1989, representing a notably young executive team for an industrial company. James Bowes leads Building Products, Steven Caravati heads Consumer Products, and Sonya Higginbotham oversees corporate affairs and sustainability. The team's youth and professional management orientation mark a clear departure from the founder-family governance that characterized Worthington's first six decades.

Hayek's elevation to CEO signals that the board views disciplined capital deployment and strategic M&A as the primary levers of value creation going forward. His total compensation of approximately $2.4 million positions him modestly relative to peers, consistent with Worthington's culture of restraint and alignment with employee interests.

X. The Business Model and Competitive Dynamics

To understand why Worthington Enterprises might be more valuable as a standalone company than as part of the old conglomerate, you need to understand the structural advantages of its core businesses.

The Building Products segment, and the pressure cylinder business at its heart, operates with a moat that is unusual for a manufacturing company. Start with regulatory barriers: every pressure cylinder sold in the United States must meet Department of Transportation safety certifications. These certifications require extensive testing, documentation, and ongoing compliance, creating a meaningful barrier for potential new entrants. You cannot simply set up a factory and start making propane tanks.

Then consider the distribution network. Worthington has built a cylinder exchange and refurbishment infrastructure over decades. Propane cylinder exchange works like this: a consumer buys a full propane tank at a retailer, uses the propane, and brings the empty tank back to exchange for a full one. The company that controls the exchange network, the cage displays at the front of hardware stores and gas stations, owns a recurring revenue stream with genuine switching costs. Retailers are reluctant to change exchange providers because the displays, logistics, and customer expectations are all calibrated to a specific system. Building a competing network from scratch would require enormous capital and decades of retailer relationship building.

The water tank and expansion tank business, bolstered by the Amtrol acquisition, benefits from building codes and plumbing regulations that mandate these products in residential and commercial construction. When a building code says you need an expansion tank in your water heater system, that is a regulatory moat that no amount of competitive innovation can erode.

In Consumer Products, the competitive dynamics are different but still favorable. The key brands, Bernzomatic, Coleman cylinders, and Balloon Time, have established shelf space at the major retailers. In consumer packaged goods terminology, shelf space is everything. Losing a planogram position at Home Depot or Lowe's is devastating, and gaining one is extraordinarily difficult. Worthington's decades-long retailer relationships, combined with brand recognition among end consumers, create a defensive position that commodity competitors and private label alternatives struggle to penetrate.

The sustainable energy segment is the most speculative but potentially most valuable piece. Hydrogen infrastructure is a nascent market with enormous potential. The global hydrogen economy is projected by various industry analysts to require trillions of dollars in infrastructure investment over the next two decades, and storage and transport are among the most critical bottlenecks. Every hydrogen fueling station needs high-pressure storage, every hydrogen transport vehicle needs certified containers, and every industrial hydrogen user needs on-site storage solutions. Worthington's joint venture with Hexagon Composites brings together metal fabrication expertise with composite materials technology, positioning the partnership for storage, transport, and distribution applications. The Cosmos product line, which includes both stationary and transportable high-pressure gas storage systems, is designed specifically to address these infrastructure needs.

Capital allocation under the new Worthington Enterprises follows a clear hierarchy: invest in organic growth within existing segments, pursue disciplined acquisitions that expand market position or enter adjacent markets, return cash to shareholders through dividends and buybacks, and maintain balance sheet flexibility for opportunistic moves. The company's $250 million cash position and modest debt load provide ample capacity for this strategy. With net debt to EBITDA of just 0.4 times, the balance sheet has significant room for leverage-funded acquisitions if the right opportunities emerge. Management has indicated a willingness to lever up to two to three times for a compelling deal, suggesting that the current conservative posture is a choice driven by deal-flow quality rather than financial constraint.

The company's days of sales outstanding, a measure of how quickly customers pay, runs at about seventy-two days, which is typical for industrial businesses with significant B2B exposure. Inventory turns are moderate, with days of inventory outstanding around seventy-four days, reflecting the manufacturing and logistics complexity of the cylinder business. These working capital metrics are roughly in line with industrial peers and do not suggest any unusual cash conversion challenges.

One question that matters for investors evaluating the culture: does the no-layoff policy still exist? In its purest form, no. The 2008 recession forced departures from the strict policy, and the spinoff itself inevitably involved workforce restructuring. But the spirit of the Golden Rule continues to inform how the company manages through cycles, with an emphasis on retention, redeployment, and treating employees as long-term partners rather than variable costs. In a labor market where skilled manufacturing workers are increasingly scarce, this cultural orientation has practical advantages that extend well beyond sentiment.

There is an important subtlety in the competitive dynamics of the cylinder exchange business that deserves elaboration. Think of it like the razor-and-blade model, but for propane. The initial sale of a cylinder is just the beginning. The real value is in the ongoing exchange cycle: empty tank returned, full tank purchased, repeat. The company that controls the exchange infrastructure at retail locations controls a recurring revenue stream with high customer retention. Switching to a competitor's exchange network means finding different locations, potentially different cylinder formats, and disrupting an established routine. These switching costs are not enormous individually, but in aggregate, across millions of consumers, they create a highly predictable revenue base that underpins the segment's valuation premium.

XI. Porter's Five Forces Analysis

Understanding Worthington's competitive position requires examining the structural forces that shape its industries. The picture that emerges is one of moderate-to-strong competitive positioning, particularly in the Building Products segment, with more challenging dynamics in Consumer Products.

Threat of New Entrants: Low to Moderate. The pressure cylinder and tank manufacturing businesses benefit from genuine barriers. DOT safety certifications require years of testing and regulatory compliance. To put this in perspective, obtaining a DOT special permit for a new cylinder design can take twelve to eighteen months and cost hundreds of thousands of dollars in testing alone. Manufacturing pressure vessels demands specialized metallurgical expertise, quality control systems, and ongoing regulatory compliance that new entrants must build from scratch. Distribution networks for cylinder exchange programs took Worthington decades to build, one retailer relationship at a time. The capital requirements for entering this space at scale are substantial, both in manufacturing equipment and in the logistics infrastructure needed to collect, refurbish, refill, and redistribute cylinders. However, in consumer products and outdoor living, barriers are lower. Import competition from Asian manufacturers and new direct-to-consumer brands can chip away at market share, though they typically compete on price rather than distribution infrastructure.

Bargaining Power of Suppliers: Moderate. Post-spinoff, Worthington's raw material exposure has shifted meaningfully. Steel is still an input for cylinder manufacturing, but the company is no longer a pure steel processor buying millions of tons annually. Specialty steels, aluminum, and composite materials each have their own supplier dynamics. Interestingly, the company now purchases some of its steel from Worthington Steel, the very business it spun off, an arrangement that presumably comes with favorable terms given the shared heritage and ongoing relationships. The Hexagon Ragasco acquisition added composite materials to the mix, with more specialized and potentially concentrated supplier bases. Scale purchasing provides some leverage, but Worthington is not large enough to dictate terms to global commodity suppliers. The reduced dependence on any single raw material, however, is a meaningful benefit of the post-spinoff structure.

Bargaining Power of Buyers: Moderate to High. The customer base splits into two distinct groups. In Building Products, the buyer base includes gas producers, distributors, and OEMs who have moderate negotiating leverage but face genuine switching costs. In Consumer Products, the picture is more challenging. Home Depot and Lowe's are enormously powerful retailers that can and do squeeze margins from their suppliers. Maintaining shelf space requires constant investment in brand support, promotions, and product innovation. Private label competition provides retailers with an implicit threat that keeps branded manufacturers honest on pricing.

Threat of Substitutes: Moderate and Evolving. The most significant substitution risk is structural: the energy transition. If the world electrifies rapidly and propane demand declines, Worthington's largest product category faces secular headwinds. Electric grills, heat pumps replacing propane furnaces, and battery-powered tools all represent potential substitution threats over the long term. However, the hydrogen opportunity provides a natural hedge: the same pressure vessel technology used for propane can be adapted for hydrogen storage. In the near term, propane remains deeply embedded in American outdoor and residential heating culture, and substitution is gradual rather than abrupt.

Competitive Rivalry: Moderate. In pressure cylinders, the North American market is relatively consolidated, with Worthington holding a top-two position. This concentration reduces destructive price competition, though large customers can still play competitors against each other. The competitive landscape includes Manchester Tank, Amerigas, and various regional players, but none match Worthington's combination of manufacturing scale, brand portfolio, and distribution network density. In consumer products, rivalry is more fragmented and intense, with competition from both established brands and lower-cost imports. Bernzomatic competes with brands like Victor Technologies and various imported alternatives; the outdoor living category has proliferated with dozens of new entrants since COVID. The commercial roofing market entered through the LSI acquisition is competitive but benefits from specification-based selling where brand reputation and contractor relationships matter more than price alone.

XII. Hamilton's Seven Powers Framework Analysis

Hamilton Helmer's framework provides a complementary lens to Porter's forces, focusing specifically on the sources of durable competitive advantage.

Scale Economies: Moderate. Worthington benefits from manufacturing scale in cylinders and tanks, spreading fixed costs over larger production runs. Distribution network density creates regional scale advantages: the more exchange locations and delivery routes within a geography, the lower the per-unit logistics cost. However, these scale advantages are regional rather than global, and the post-spinoff company is smaller than the combined entity, somewhat reducing overall scale benefits. This is not a business where winner-take-all scale dynamics apply.

Network Effects: Weak to Moderate. The cylinder exchange network has mild network characteristics. More exchange locations create more convenience for end users, which drives more participation, which justifies more locations. Think of it like a physical version of a two-sided marketplace: Worthington connects propane consumers (who want convenient exchange locations) with retailers (who want foot traffic from cylinder exchange customers). The more locations, the more consumers participate, which makes the network more attractive to retailers. But unlike digital platforms, these network effects are geographically bounded and linear rather than exponential. A consumer in Phoenix does not benefit from more exchange locations in Boston. The network effects are real but modest, providing incremental advantage rather than winner-take-all dynamics.

Counter-Positioning: Weak. Worthington is not disrupting incumbents with a fundamentally new business model. The company pursues sustaining innovation, improving existing products and expanding into adjacent markets rather than redefining categories. This is not a criticism; most industrial companies create value through operational excellence and incremental improvement rather than disruptive innovation. The hydrogen pivot is forward-looking but represents a natural extension of existing capabilities rather than a counter-position against established energy players. No incumbent is being displaced by Worthington's strategy; rather, the company is positioning itself to serve emerging markets alongside existing competitors.

Switching Costs: Moderate to Strong. This is one of Worthington's most important competitive advantages. Cylinder exchange customers face logistical switching costs because their existing infrastructure, cage displays, and supply chain are calibrated to Worthington's system. OEM customers for engineered products involve custom tooling, integration testing, and safety certifications that create genuine stickiness. Water system tanks specified by plumbing contractors develop a preference stickiness based on familiarity and reliability. Consumer products, however, have low switching costs; a homeowner will buy whatever torch is on the shelf.

Branding: Moderate. Bernzomatic, Coleman cylinders, and Balloon Time have meaningful consumer recognition in their categories, but they are not aspirational or premium brands. In B2B markets, the Worthington name carries significant weight based on decades of reliability and the company's cultural reputation. Trust matters in products where safety is paramount, and Worthington's track record is a genuine brand asset. Still, brand power alone would not prevent a sufficiently determined competitor from entering these markets.

Cornered Resource: Weak to Moderate. Worthington does not control any truly irreplaceable resources. Its DOT certifications, manufacturing expertise, and distribution relationships are valuable but theoretically replicable by a well-capitalized competitor willing to invest years of effort. The company's culture, the Golden Rule philosophy and its associated employee loyalty, is perhaps its most defensible intangible asset, precisely because it cannot be acquired or copied through a single strategic decision. It is the product of decades of consistent behavior.

Process Power: Moderate. Decades of refinement in cylinder production, quality control, and lean manufacturing create operational advantages that are difficult for competitors to replicate quickly. Manufacturing a pressure cylinder involves dozens of steps: forming, welding, heat treating, testing, finishing, and certification, each of which must meet exacting safety standards. Worthington has refined these processes over fifty years, achieving yields and quality levels that newer competitors cannot easily match. The company's ability to consistently integrate acquisitions, applying its cultural and operational playbook to underperforming businesses, is itself a form of process power. The Amtrol, Level5, Hexagon Ragasco, and LSI acquisitions all followed a recognizable pattern that reliably generates value.

Beyond manufacturing, the cultural processes that Worthington has developed, the employee councils, profit sharing, and Golden Rule governance, represent a form of organizational process power that is genuinely difficult to replicate. You cannot install culture through a consulting engagement or a board mandate; it must be built over decades of consistent behavior. This is perhaps Worthington's most underappreciated competitive advantage, and it is one that no competitor can acquire through M&A.

The overall assessment is that Worthington Enterprises possesses moderate durable competitive advantages, concentrated primarily in switching costs, process power, and scale economies within specific product lines. The spinoff was partly a recognition that steel processing had declining competitive power while the retained businesses had stronger and more defensible moats. For investors comparing Worthington to industrial peers like AZZ Inc., Standex International, or UniFirst, the key differentiator is the combination of regulatory barriers, distribution infrastructure, and cultural cohesion, none of which are individually dominant but which together create a multi-layered defensive position.

XIII. The Playbook: Business and Strategic Lessons

Worthington's seven-decade journey offers lessons that extend well beyond the industrial sector. The company's evolution from a one-man steel processing shop to a focused building and consumer products company, with a spinoff of its founding business along the way, provides a rare longitudinal case study in strategic adaptation.

Culture as Strategy, Not Sentiment. The most counterintuitive lesson from Worthington's history is that the Golden Rule was not a soft, feel-good policy. It was hard-edged competitive strategy. The no-layoff philosophy, profit sharing, and employee councils generated measurable advantages: lower turnover, higher productivity, faster recovery from recessions, and deeper institutional knowledge. When competitors laid off experienced workers during downturns and then scrambled to rehire during recoveries, Worthington's retained workforce allowed it to capture market share at exactly the right moment.

Consider the math: if the average cost of hiring and training a manufacturing worker is twenty to thirty thousand dollars, and Worthington retained a thousand workers through a recession that competitors laid off, the company saved twenty to thirty million dollars in rehiring costs alone, before accounting for the productivity advantage of experienced workers versus new hires. Over multiple recession cycles, this advantage compounded significantly. The lesson is not that every company should adopt a no-layoff policy. It is that cultural commitments, consistently maintained, compound over time in ways that are nearly impossible for competitors to replicate.

Myth vs. Reality: The "Boring Industrial" Label. There is a persistent market narrative that companies like Worthington are boring, predictable, slow-moving industrial businesses that cannot generate exciting returns. The reality is more nuanced. Worthington's total return from its 1968 IPO through 2023 significantly outperformed the S&P 500 over certain multi-decade windows, driven by the compounding effects of dividend reinvestment, disciplined acquisitions, and margin expansion. The lesson is that "boring" businesses with durable competitive advantages and disciplined management can generate superior long-term returns precisely because they are underappreciated and under-followed by the investment community.

Portfolio Management: Knowing When to Exit Your Legacy. Perhaps the most courageous strategic decision in Worthington's history was the 2023 spinoff of its founding steel processing business. After sixty-eight years, the family and board had the intellectual honesty to acknowledge that the business that created the company was no longer its best use of capital. This is extraordinarily rare in corporate America, where attachment to founding businesses frequently prevents value-maximizing decisions. The lesson for investors and operators alike is to evaluate businesses on their forward merits, not their historical significance.

Patient Capital Enables Long-Term Thinking. The McConnell family's sustained involvement provided Worthington with something most public companies lack: patient capital. The no-layoff policy, the willingness to sacrifice short-term earnings for long-term employee loyalty, the discipline to avoid growth-at-any-cost acquisitions, all of these required shareholders who could tolerate suboptimal quarterly results in exchange for compounding advantages over decades. This is particularly rare in public markets, where activist investors and quarterly earnings pressure routinely force companies into short-term optimization at the expense of long-term value creation. Worthington's family ownership structure provided an implicit defense against this pressure, allowing management to make decisions with five-to-ten-year time horizons rather than ninety-day ones. The irony is that by eventually stepping back from governance, the McConnell family enabled the most transformative strategic move in the company's history.

Distribution and Service Trump Product in Industrial Markets. Worthington's most defensible competitive positions are not in products themselves but in the infrastructure surrounding them. The cylinder exchange network, the retailer shelf space, the DOT certifications, and the contractor relationships all create value that is independent of any specific product's technical superiority. This is a broadly applicable lesson for industrial investors: in markets where products are relatively commoditized, the companies that build the best distribution and service infrastructure tend to generate the most durable returns.

Recognizing Strategic Inflection Points. Worthington's leadership team deserves credit for recognizing that the 2008 recession and subsequent competitive dynamics represented a structural shift, not a cyclical blip. Steel processing margins were compressing permanently, not temporarily. The response was measured but decisive: diversify, acquire higher-quality businesses, divest underperformers, and ultimately separate. The contrast with companies that clung to declining businesses until forced by crisis into fire-sale restructurings is instructive.

Capital Allocation Evolution: From Growth-Focused to Returns-Focused. In Worthington's early decades, capital allocation was growth-oriented: reinvest in the business, expand capacity, acquire new businesses, and grow the revenue line. Under John P. McConnell and then Andy Rose, the approach evolved toward returns-focused allocation: every dollar of capital needed to earn an attractive return on invested capital, and businesses that could not meet that hurdle would be exited. The elevation of Joseph Hayek, a former investment banker whose entire career has been organized around capital markets and deal-making, to the CEO role is the ultimate expression of this evolution. The company's current approach treats capital as the scarcest resource, deploying it with discipline toward the highest-return opportunities, whether those are organic investments, acquisitions, dividends, or share repurchases. This is a common arc for maturing industrial companies, but Worthington executed it more deliberately and successfully than most.

The Acquisition Playbook. Worthington's acquisition history reveals a consistent pattern worth noting. The company tends to acquire businesses that are number one or number two in their niche, that have strong brand recognition or regulatory moats, and that can benefit from integration into Worthington's distribution and manufacturing infrastructure. Amtrol, Level5, Hexagon Ragasco, and LSI Group all fit this profile. The company avoids transformative mega-deals in favor of tuck-in acquisitions that can be integrated without straining the balance sheet or management bandwidth. This disciplined approach reduces integration risk but also limits the upside from any single deal.

XIV. Bull Case, Bear Case, and Investment Thesis

The Bull Case for Worthington Enterprises rests on several pillars. First, the post-spinoff company is a pure-play on pressure cylinders, building products, and consumer brands with materially better margins than old Worthington. Gross margins of roughly twenty-eight percent compare favorably to the low-teens margins typical of steel processing. Second, the company holds a dominant market position in North American pressure cylinders, with genuine structural advantages in distribution, regulatory compliance, and switching costs. Third, the hydrogen infrastructure opportunity, while speculative, provides optionality that the market may be underpricing. The joint venture with Hexagon Composites derisks the bet while preserving upside. Fourth, the data center construction boom creates a secular demand tailwind for building products that could persist for years. Fifth, disciplined capital allocation under CEO Hayek, a former investment banker, suggests acquisitions will be accretive and balance sheet management prudent. The stock trades at roughly fourteen times next twelve months' earnings, which is not demanding for a company with these structural characteristics.

The Bear Case is equally real and deserves careful consideration. The core propane cylinder business is mature with limited organic growth. Volume gains depend on population growth, new household formation, and outdoor living trends, none of which are high-growth drivers. The energy transition represents a genuine long-term risk: if electric alternatives to propane heating and grilling gain meaningful traction, Worthington's largest market shrinks. Consider that Traeger, Weber, and other grill makers are already investing in electric and pellet alternatives that could reduce propane tank demand over time.

Consumer products face relentless pressure from private label alternatives and import competition, with powerful retailers squeezing margins. The relationship with Home Depot and Lowe's, while valuable, is also a source of vulnerability: these retailers have the scale and incentive to develop their own private label cylinder and tool brands if Worthington's margins become too attractive. The post-spinoff company is smaller and less diversified than old Worthington, meaning any downturn in construction or consumer spending hits harder. Revenue concentration in building and consumer products creates cyclical exposure to housing starts, renovation activity, and discretionary consumer spending.

The hydrogen infrastructure opportunity, while exciting, has uncertain timing and could take a decade or more to generate meaningful revenue. Hydrogen faces fundamental economic challenges: green hydrogen production remains expensive relative to natural gas, fueling infrastructure is nascent, and competing technologies like battery electric vehicles may capture much of the transportation market before hydrogen infrastructure can scale. Finally, maintaining the Worthington culture across a transformed company with new leadership is inherently challenging, and the intangible cultural advantage may erode faster than expected.