Advanced Drainage Systems: America's Hidden Infrastructure Giant

The Most Important Company You've Never Heard Of

Picture a construction site in the American heartland—maybe a new subdivision outside Columbus, Ohio, or a highway interchange in Texas. Beneath the surface of nearly every project like this lies an invisible network of corrugated plastic pipes, quietly performing one of civilization's most fundamental tasks: managing water. These pipes, more often than not, were made by a company whose name rarely appears in headlines but whose products underpin the infrastructure of modern America.

Advanced Drainage Systems, Inc. (ADS) is an American company that designs, manufactures, and markets polypropylene and polyethylene pipes, plastic leach field chambers and systems, septic tanks and accessories, storm retention/detention chambers, and other water management products. It is the largest maker of high-density polyethylene pipe in the United States.

The puzzle that makes ADS fascinating to students of business strategy is deceptively simple: How did a company making plastic drainage pipes—a product most people never think about—become one of the most important ESG stories in industrial America? With a fiscal year 2024 revenue of $2.874 billion, ADS stands as a key player in this vital industry. The company's market capitalization hovers around $11.5 billion, placing it firmly in mid-cap territory but punching far above its weight in terms of strategic importance.

This is a story about material conversion—the relentless, decades-long displacement of concrete, steel, and clay by lighter, more durable thermoplastic alternatives. It's about vertical integration in recycling that has transformed the company into one of North America's largest plastic recyclers. And it's about the tailwinds of water infrastructure spending that may be just beginning to accelerate.

From Ohio farm drainage to NYSE darling, ADS represents the "boring is beautiful" investment thesis in its purest form. The company has achieved something remarkable: building durable competitive advantages in an industry that most people don't even know exists.

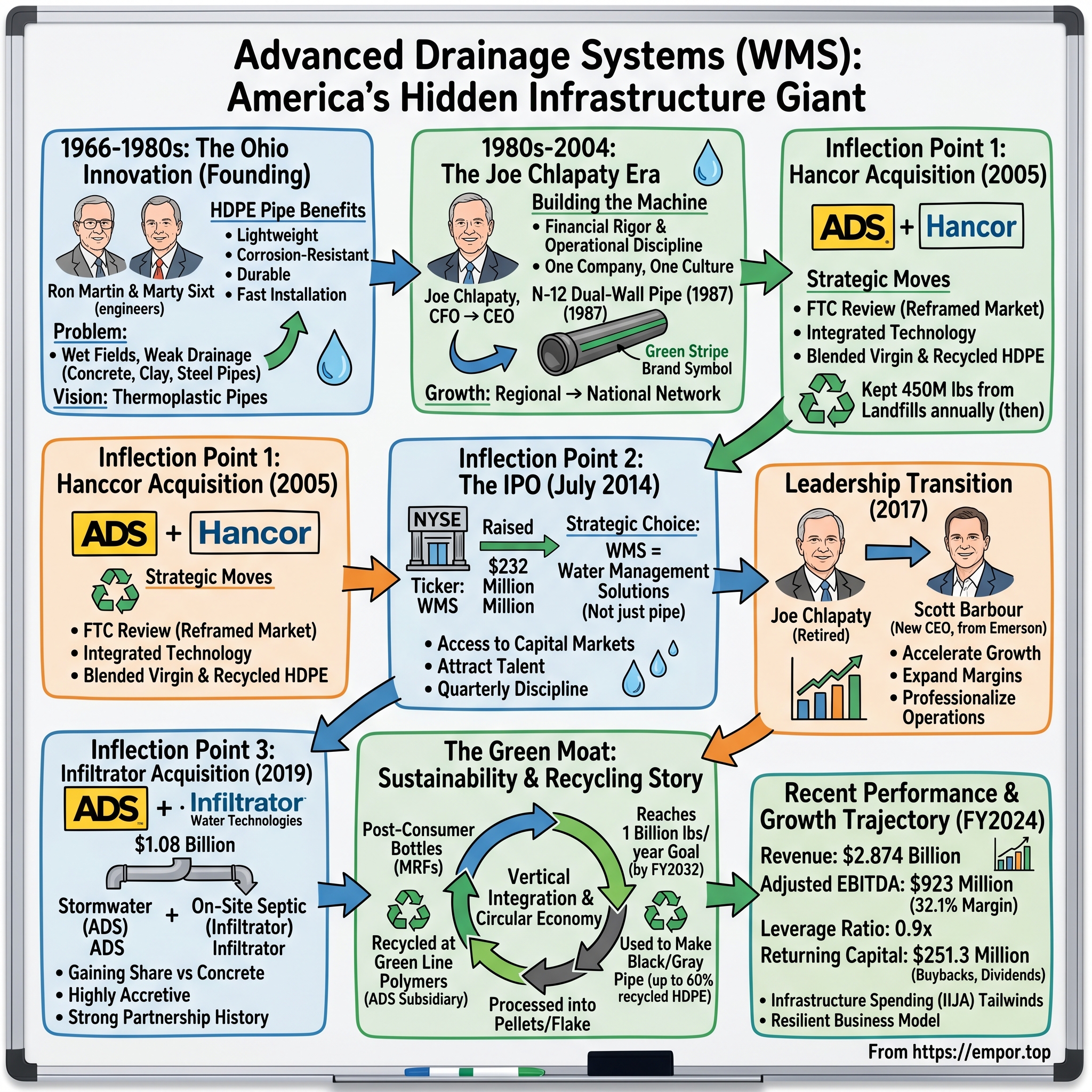

Founding & Early Context: The Ohio Innovation (1966–1980s)

The story begins in 1966, during America's post-war agricultural boom. The company was founded in 1966 by Ron Martin and Marty Sixt, two engineers. The two founders recognized a fundamental problem plaguing American farms: drainage. The corn belt's rich soil was productive, but it was also wet. Farmers needed efficient ways to move water off their fields, and the existing solutions—concrete pipes, clay tiles, and corrugated steel—were heavy, expensive, and prone to degradation.

Martin and Sixt had a different vision. What if you could make drainage pipe from plastic? The material science was there. High-density polyethylene (HDPE) offered a compelling combination of properties: it was light, corrosion-resistant, flexible enough to handle soil movement, and could be manufactured in long lengths that dramatically reduced installation time.

In the early 1970s, the company moved to central Ohio—a strategic location that would prove prescient. Ohio sat at the intersection of America's agricultural heartland and its construction industry supply chains. The Midwest's flat terrain and heavy rainfall made drainage infrastructure essential, while the region's manufacturing base provided access to skilled labor and logistics networks.

The fundamental innovation was corrugated plastic pipe versus traditional concrete and clay tile. Traditional materials had served well for decades, but they came with significant drawbacks. Concrete pipe was heavy—a single section might weigh hundreds of pounds—requiring heavy equipment and large crews for installation. It was also rigid, meaning it could crack under soil movement, and the cement matrix was susceptible to chemical attack from acidic soils.

ADS's thermoplastic corrugated pipe is generally lighter, more durable, more cost-effective and easier to install than comparable products made from traditional materials. A section of corrugated HDPE pipe might weigh a fraction of its concrete equivalent, allowing two workers to maneuver what would otherwise require a crane. The corrugated design provided structural strength while maintaining flexibility—the pipe could bend with soil movement rather than cracking.

The value proposition resonated immediately in agricultural markets. Farmers could drain their fields faster, with less labor, at lower cost. And the plastic pipes didn't corrode or deteriorate like their traditional counterparts. The company built its initial footprint serving the corn belt, establishing a regional manufacturing and distribution network that could deliver product to farms across the Midwest.

What the founders couldn't have known was that they were building infrastructure for something far larger. Agricultural drainage was just the beginning. The same properties that made plastic pipe ideal for farm fields would eventually make it essential for highway drainage, stormwater management, and residential construction. The building blocks of a national infrastructure company were being laid in Ohio's farm country.

The Joe Chlapaty Era Begins: Building the Machine (1980–2004)

In 1980, a young accountant named Joe Chlapaty joined ADS as Chief Financial Officer. At ADS, he served in numerous roles, including as Vice President and Chief Financial Officer (1980), President and Chief Operating Officer (1994), Chief Executive Officer (2004), Chairman of the Board (2008-2017), and Emeritus Chairman (2017-present). When Chlapaty arrived, the company's annual sales were about $50 million—respectable for a regional plastics manufacturer, but a fraction of what it would become.

Chlapaty's background was unusual for someone who would spend nearly four decades transforming an industrial company. Before joining Advanced Drainage Systems, Joseph Chlapaty served as Corporate Accounting Manager, Assistant Treasurer, and Treasurer for Lindberg Corporation and prior to that was with Arthur Andersen LLP. He holds a B.S.B.A. (Cum Laude) from the University of Dubuque, where he was a recipient of both the Wall Street Journal Award and Student Athletic Award, and an M.B.A. from DePaul University. He was also a Certified Public Accountant.

This combination of financial rigor and operational discipline would define Chlapaty's leadership style. He wasn't a visionary technologist or a charismatic salesman. He was a builder—methodical, patient, and relentlessly focused on execution.

The "conversion thesis" that would drive ADS's growth for decades emerged during this period. Chlapaty recognized that ADS wasn't just selling pipe—it was selling a materials revolution. The real opportunity wasn't in taking market share from other plastic pipe makers; it was in converting the massive installed base of concrete, steel, and PVC infrastructure to thermoplastic alternatives.

Thirty years ago, ADS used almost all virgin resin in its pipes. Now products like Mega Green, a dual-wall corrugated HDPE pipe with a smooth interior for hydraulic efficiency, are up to 60 percent recycled HDPE. But the recycling story would come later. In the 1980s, the focus was on geographic expansion—building a national manufacturing and distribution network.

One of the game-changing products came in 1987, when we introduced the N-12 corrugated dual-wall HDPE pipe with a smooth inside wall to improve water flow. We extrude a green stripe on our corrugated pipes, and that has become an iconic symbol and a representation of our brand that lets the customer know they are working with an ADS pipe.

The N-12 pipe was a turning point. The dual-wall design—corrugated on the outside for structural strength, smooth on the inside for hydraulic efficiency—allowed ADS to compete directly with concrete and PVC in larger-diameter applications. Highway departments and municipalities began specifying ADS products for stormwater systems. The market opportunity expanded from farm drainage to the entire construction industry.

Through the 1980s and 1990s, ADS built plant after plant, distribution center after distribution center. The company's culture crystallized around a simple philosophy that would define its approach to acquisitions: "One company, one culture." When ADS opened a new facility or acquired a competitor, the integration playbook was the same—bring people into the ADS system, train them on ADS methods, make them part of the ADS family.

During his leadership role, he guided ADS from $55,000,000 in sales revenue in 1980 to the world's largest producer of thermoplastic corrugated pipe and related products with current sales revenue of approximately $1,500,000,000; 60 manufacturing plants and 19 customer service centers worldwide with approximately 4,000 employees.

By the time Chlapaty became CEO in 2004, the transformation was well underway. But the deal that would truly define his legacy was still ahead.

Inflection Point #1: The Hancor Acquisition (2005)

In the spring of 2005, Joe Chlapaty faced the defining decision of his career. Hilliard, Ohio-based Advanced Drainage Systems Inc. is acquiring competitor Hancor Inc. of Findlay, Ohio, in a transaction that creates the largest plastic pipe company in North America.

The strategic rationale was compelling but legally fraught. According to industry sources, the total North American market for corrugated HDPE pipe is roughly 1.25 billion pounds annually. ADS and Hancor combined will represent about 70 percent of that market.

This was exactly the kind of concentration that attracts Federal Trade Commission scrutiny. ADS and Hancor are the only two national players in the market for HDPE corrugated pipe, a market dominated by regional firms. Regional competitors voiced their concerns: "The little guy, we just get beat up and move on," said one regional player. "We're not in favor of [this deal]. These are the only two national players. The rest of us are mom-and-pop, single-plant operations."

The FTC review that followed was, in Chlapaty's own words, "a major undertaking" and "a nail-biter." The key to clearing the regulatory hurdle was reframing the competitive landscape. According to ADS President and Chief Executive Officer Joe Chlapaty, combining the two biggest players in large-diameter high density polyethylene corrugated drainage pipe will help ADS compete with manufacturers of pipe made of other materials. ADS and Hancor face formidable competition from concrete, steel, PVC and solid-wall PE pipe, he said. "Our collective abilities to compete against alternative materials for storm and sanitary applications will be greatly enhanced."

The argument worked. The FTC approved the merger, accepting that the relevant market wasn't just corrugated HDPE pipe but the broader stormwater management industry, which exceeded $4 billion annually. In July 2005, the FTC closed its investigation, and ADS could proceed with the acquisition.

But clearing regulatory approval was only the first challenge. The integration had to work. Chlapaty's approach was characteristically direct. After the acquisition closed, he traveled to Hancor's headquarters in Findlay, Ohio, and told employees no one needed to worry about layoffs. "It's one company, one culture," he said. "That's the way we presented it, and that's the way we've been."

Combined, the companies will have nearly 40 plants and estimated sales of more than $700 million.

The Hancor deal brought more than manufacturing capacity. It brought technology—specifically, Hancor's advanced capabilities in blending recycled and virgin HDPE. The transaction united ADS's production capabilities, equipment and marketing network with Hancor's material advancements, including a means to blend post-consumer and virgin HDPE and make good pipe. Chlapaty said the process is sophisticated and involves controlling a range of properties so the material can be reprocessed and manufactured into pipe without diminishing quality or performance.

This technological transfer would prove transformative. ADS has gone from using 70 percent virgin material and 24 percent recycled material in 2005 to 37 percent virgin and 57 percent recycled today. "We're keeping 450 million pounds of material out of the landfill each year," Chlapaty said.

The Hancor acquisition established the template that ADS would follow for future deals: acquire strategic capability, integrate quickly, invest in the best practices from both organizations, and maintain the cultural emphasis on "one company, one culture." The company had discovered that being the dominant player in thermoplastic pipe wasn't a regulatory liability—it was a platform for converting the much larger market of traditional materials.

Inflection Point #2: The IPO (July 2014)

For nearly fifty years, Advanced Drainage Systems had operated as a private company. The decision to go public represented a fundamental shift in the company's trajectory.

In July 2014, the company became a public company via an initial public offering on the New York Stock Exchange, raising $232 million.

The timing was strategic. After decades of organic growth and the transformative Hancor acquisition, ADS had built a company with national scale, strong profitability, and a compelling growth thesis. But continuing to grow—especially through acquisition—required access to capital markets. Private ownership had served the company well, but the next phase of expansion would require public market resources.

With over five decades of experience in corporate leadership and community service, Chlapaty's career spans 37 years at Advanced Drainage Systems Inc., where he served as chief financial officer, president, chief executive officer and chairman of the board. During his tenure, he transformed the company from a $55 million business into the world's largest producer of thermoplastic corrugated pipe and related products, with sales revenue reaching approximately $1.5 billion.

The ticker symbol choice was deliberate. Advanced Drainage Systems, Inc. designs, manufactures, and markets thermoplastic corrugated pipes and related water management products in the United States, Canada, and internationally. It operates through Pipe, Infiltrator, International, and Allied Products & Other segments. The company trades under "WMS"—Water Management Solutions—not "ADS" or "PIPE." The symbolism was intentional: ADS wanted investors to understand that this wasn't just a pipe company. It was a water management company, participating in one of the most essential infrastructure markets of the 21st century.

ADS went public in July 2014, a move that King believes put ADS on a fast track for growth and in a better position to attract top-level talent. "Being a publicly traded company has given us the ability to easily access capital," he remarks.

The IPO opened new possibilities. Public market access would enable the acquisition currency needed for the company's next major move. It would help attract executive talent who expected equity compensation. And it would impose the discipline of quarterly reporting, forcing the company to articulate its strategy and demonstrate consistent execution.

One of his crowning achievements was successfully leading the company's initial public offering and listing on the New York Stock Exchange in 2014.

For Chlapaty, who had joined the company when it had $55 million in sales, the IPO represented both culmination and transition. He was approaching his 70th birthday, and the company needed to plan for succession. Going public was part of that planning—establishing the institutional frameworks that would allow ADS to thrive beyond any individual leader.

Leadership Transition: Scott Barbour Takes the Helm (2017)

In 2004, Joe Chlapaty became CEO of the company; he retired in 2017 and was succeeded by Scott Barbour.

The board's succession planning was deliberate. As part of the Company's succession plan, the Board has created a search committee and has hired recruiting firm Korn Ferry (NYSE: KFY) to identify and evaluate both internal and external candidates to succeed Mr. Chlapaty.

The choice of Scott Barbour signaled the board's ambition for ADS's next chapter. Mr. Barbour has over 25 years of experience in the industrials sector. Most recently, he worked for Emerson Electric, a global technology and engineering company that provides solutions for customers in industrial, residential and commercial markets as President and CEO of its $4.5 billion Network Power business.

Barbour's background at Emerson had prepared him for exactly the kind of operational challenges ADS faced. Mr. Barbour was responsible for managing major multi-million dollar contract negotiations, leading and implementing a global profitability optimization program. During his tenure at Emerson, Mr. Barbour also held several leadership positions including Group Vice President of Emerson Client Technologies Group. In these roles, Mr. Barbour drove significant technology initiatives, increased profitability and led new product development.

The board's perspective was clear. Mr. Kidder said, "This announcement comes at the right time as we enter the next chapter of the Company's evolution."

Mr. Kidder continued, "On behalf of the Board and management, we thank Joe for his countless contributions and dedication to the Company. Under his leadership, ADS has grown from a private organization with $50 million in sales to an industry leader, with an exceptionally strong brand and more than $1.2 billion in sales across multiple end markets and geographies."

Barbour's mandate was clear: accelerate growth, expand margins, and professionalize operations for a public company environment. The foundation Chlapaty had built was solid. Now ADS needed to scale it.

Inflection Point #3: The Infiltrator Acquisition (2019)

Less than two years into his tenure, Barbour executed the deal that would define his leadership.

Advanced Drainage Systems announced the acquisition of Infiltrator Water Technologies, a leader in on-site septic wastewater treatment for a purchase price of approximately $1.08 billion, from an affiliate of the Ontario Teachers' Pension Plan and other stockholders.

The strategic rationale extended ADS's addressable market into an entirely new segment. This acquisition builds on ADS' core strengths in water management by combining Infiltrator's leading position in on-site septic wastewater management with ADS' core stormwater-focused platform. This extends ADS' addressable opportunity into the attractive and related on-site septic business. The on-site septic business shares similar conversion dynamics to ADS' core stormwater business, with plastic septic chambers and tanks gaining share faster than traditional products.

The financial profile was compelling. The company posted sales of $275 million in 2018 — up 9 percent from 2016 — for its plastic leach field chambers and septic tanks for mostly residential use. Both businesses are gaining market share as more customers turn to plastic systems for storm water and septic solutions over traditional materials like concrete. Plastic chambers and tanks made of high density polyethylene and polypropylene now account for about 50 percent of the $1.2 billion septic leach field and tank business.

On a pro forma basis for the Company's fiscal year ended March 31, 2019, the combined companies would have had revenues of approximately $1.6 billion, Adjusted EBITDA margins of approximately 20.4% and free cash flow conversion of nearly 50%. ADS' management anticipates that this acquisition will be accretive to Adjusted EBITDA in year one, accretive to EPS in the first full year and yield approximately $20-$25 million in run-rate synergies by year three.

The deal's cultural alignment was exceptional—a rarity in acquisitions of this scale. "This acquisition is a welcomed extension of our more than 15-year partnership built on mutual admiration and respect. We have always shared a similar vision and core values, executed comparable conversion strategies to displace traditional materials, and remained committed to developing innovative, best-in-class products while maintaining a dedication to safety, operational excellence and sustainability through our recycling activities," said Roy Moore, President and CEO of Infiltrator Water Technologies.

The partnership history between the two companies was extensive. In addition to similar visions, conversion strategies and commitments to recycling, ADS and Infiltrator have a long history of strategic partnership. They formed a joint venture called StormTech LLC in 2003 where Infiltrator manufactured chambers for water retention and detention while ADS managed sales, marketing and engineering support. ADS acquired Infiltrator's interest in 2010. Then, in 2012, Infiltrator acquired ADS's septic chamber business.

The recycling synergies were substantial. Infiltrator also brings significant recycled raw material sourcing capabilities, in both polypropylene and polyethylene, with 75% of their collective products sourced from recycled resin, which equates to approximately 150 million pounds of recycled plastic annually.

He specifically refers to ADS' 2019 acquisition of Infiltrator Water Technologies as something that likely "would not have been possible had we not gone public." Infiltrator makes PP-based leach-field chambers and systems, septic tanks and accessories, primarily for use in residential applications.

The Infiltrator acquisition demonstrated the value of going public. The access to capital markets enabled ADS to fund a transformative deal that diversified its end markets, expanded its geographic footprint, and brought complementary recycling capabilities under one roof.

The Business Model Deep Dive: Understanding the Machine

ADS operates through Pipe, Infiltrator, International, and Allied Products & Other segments.

The company offers single, double, and triple wall corrugated polypropylene and polyethylene pipes; plastic leachfield chambers and systems; EZflow synthetic aggregate bundles; wastewater purification through mechanical aeration wastewater for residential and commercial systems; septic tanks and accessories.

The end markets span the construction spectrum. It offers its products for non-residential, residential, agriculture, and infrastructure applications through a network of distribution centers. In 2020, 93% of the company's sales were in the United States and 6% were in Canada.

The "conversion" business model is the company's strategic engine. The opportunity isn't to take share from other plastic pipe makers—it's to convert the massive installed base of traditional materials. Plastic pipes' inherent advantages, such as resistance to corrosion, moisture, and chemicals, lightweight structure, and ease of installation, make them a preferred alternative to traditional construction materials like wood, steel, or concrete in many applications.

The global Corrugated Plastic Pipe Market has been experiencing substantial growth in recent years, driven by various factors that influence the construction, infrastructure, and utility industries. Corrugated plastic pipes, known for their durability, cost-effectiveness, and resistance to corrosion, are becoming increasingly popular as an alternative to traditional piping materials such as concrete and metal.

Plastic pipe demand in the U.S. is forecast to total $26.8 billion in 2028, representing annual increases of 4.8 percent from $21.1 billion in 2023, according to the international market research firm Freedonia Group Inc.

The scale of the infrastructure investment opportunity is substantial. The Environmental Protection Agency estimates $630 billion is needed over the next 20 years to achieve the goals of the Clean Water Act, highlighting the continued opportunity for ADS and Infiltrator to support the development of more resilient water infrastructure.

The recycling advantage is both a cost lever and a competitive moat. "As one of the largest plastic recyclers in North America, we remove over half a billion pounds of recycled plastic from the waste stream each year, incorporating it into products designed to last decades."

The economic logic is compelling: "Further, we are continually working to increase our usage of recycled material, with the goal of reaching one billion pounds purchased annually by Fiscal 2032, nearly doubling the amount of recycled plastic we purchase today. Not only is using recycled plastic an economically viable solution, but it also lowers our carbon footprint."

The Sustainability & Recycling Story: The Green Moat

The recycling story at ADS isn't corporate greenwashing—it's a core business advantage that has been decades in the making.

ADS started using recycled material about 20 years ago and then found itself ramping up purchases from outside processors in the 2000s. "We knew we'd be consuming a lot of this," Barbour said. "That's how the vision for Green Line Polymers started." ADS opened Green Line in 2012 in Pandora, Ohio, to recycle post-industrial HDPE and then added facilities for post-consumer HDPE.

An ADS subsidiary, Green Line Polymers, recycles high density polyethylene plastic and formulates it into recycled resin for the No. 3 extruder of pipe, profiles and tubing in North America, according to Plastics News' newly released ranking.

The vertical integration is substantial. The company, which has a global workforce of 4,400, does not break out the number of Green Line employees. Their contribution, though, is measurable: Ninety-one percent of ADS's nonvirgin HDPE raw material is internally processed through Green Line operations. "That shows the scale of what we're doing. It's a pretty big operation," Barbour said. "Many of our plastic competitors use recycled material to a degree, but none of them are doing this kind of vertical integration."

ADS has utilized recycled plastics in its products for more than 30 years, and its 2024 fiscal year sustainability report highlights that commitment. In fiscal year 2024, the company processed 540 million pounds of postconsumer and postindustrial plastics—about 50 percent of the 1.1 billion pounds of plastic it purchased during that period. In particular, ADS consumed approximately 33 percent of the recycled pigmented HDPE bottles in the U.S., an increase from about 25 percent during the 2023 fiscal year.

ADS sources post-consumer material from more than 500 MRFs across North America.

The ambitious 1 billion pound goal drives continued investment. ADS's goal is to utilize 1 billion pounds of recycled materials annually by 2032, extending the lifecycle of plastic and protecting our most precious resource: water.

Advanced Drainage Systems announced the groundbreaking of a significant expansion to its recycling facility in Cordele, Georgia. This investment will enhance ADS' ability to provide high quality recycled material to our factories in the Southeast. The expansion will increase the facility's total size to 117,000 square feet.

The durability of the products creates a genuine circular economy story. The company's black pipe, which is made from mixed-color HDPE, and its gray pipe, made with PP and designed to compete with concrete, can last up to 100 years after installation. "When we recycle a postconsumer bottle, for example, that bottle will not end up in a landfill for 100 years, because it's going into a product that's going in the ground."

Through the company's vertically integrated in-house recycling operation, ADS Recycling, it reprocesses baled material into flake and pellets. In fiscal year 2024, it invested $36 million to upgrade its existing infrastructure.

Recent Performance & Growth Trajectory

Fiscal 2024 demonstrated the resilience of the ADS business model. Scott Barbour, President and Chief Executive Officer of ADS commented, "Fiscal 2024 was ADS' ninth consecutive year of record profitability. Adjusted EBITDA increased 2% to $923 million due to the effective management of price/cost and strong operational execution. In addition, Adjusted EBITDA margin increased 270 basis points to 32.1%, the highest annual profit margin in the Company's history. The profitability results for the year are especially impressive given the weaker demand environment in the first half of the year, which drove a 6% overall decrease in net sales to $2.9 billion."

The most recent quarterly results show continued momentum. Advanced Drainage Systems (WMS) came out with quarterly earnings of $1.97 per share, beating the Zacks Consensus Estimate of $1.7 per share. This compares to earnings of $1.7 per share a year ago. The construction company reported $1.97 earnings per share for the quarter, topping analysts' consensus estimates of $1.70 by $0.27. The firm had revenue of $850.38 million during the quarter, compared to the consensus estimate of $802.49 million.

Advanced Drainage Systems Inc (NYSE:WMS) reported a 9% increase in revenue and a 17% growth in adjusted EBITDA for the second quarter. The company achieved a 33.8% adjusted EBITDA margin, reflecting strong operational execution.

Infrastructure spending provides ongoing tailwinds. We've been a part of over 600 airport projects in just 4 years. It's clear that the pros turn to us when it comes to stormwater management for airports.

The balance sheet remains strong. Net debt (total debt and finance lease obligations net of cash) was $860.9 million as of March 31, 2024, a decrease of $246.9 million from March 31, 2023. ADS had total liquidity of $1,079 million, comprised of cash of $490.2 million as of March 31, 2024 and $588.9 million of availability under committed credit facilities. As of March 31, 2024, the Company's leverage ratio was 0.9 times.

Capital returns to shareholders have been substantial. In the twelve months ended March 31, 2024, the Company repurchased 1.8 million shares of its common stock for a total cost of $207.3 million. Between common stock repurchased and dividends paid, the Company returned $251.3 million to shareholders in the year ended March 31, 2024.

Competitive Analysis: Porter's Five Forces

Threat of New Entrants: LOW

The barriers to entry in thermoplastic pipe manufacturing are formidable. ADS manages the industry's largest company-owned fleet, an expansive sales team, and a vast manufacturing network of approximately 70 manufacturing plants and 40 distribution centers. Replicating this infrastructure would require hundreds of millions in capital investment and years of operational development.

Beyond physical assets, the company has built relationships with over 500 MRFs for recycled material supply—relationships that took decades to develop and would be nearly impossible for a new entrant to replicate quickly.

Regulatory approvals and certifications create additional barriers. Highway departments, municipalities, and construction codes specify approved materials, and gaining these approvals requires extensive testing and regulatory engagement.

Bargaining Power of Suppliers: MODERATE-LOW

ADS buys both post-consumer and post-industrial plastics and aims to purchase 1 billion pounds of recycled material annually by fiscal 2032. Although the mix varies by year, it typically is about 60% post-industrial and 40% PCR.

The vertical integration through ADS Recycling reduces dependence on external suppliers. The dual sourcing capability—virgin and recycled resins—provides flexibility to shift procurement based on market conditions.

Bargaining Power of Buyers: MODERATE

The customer base is fragmented across thousands of contractors, developers, and municipalities. Products are sold through distribution networks, and engineering support creates switching costs. The technical specifications required for many applications create lock-in effects.

Threat of Substitutes: MODERATE (but trending favorable)

Plastic Pipes: Plastic pipes, such as PVC and HDPE, offer advantages over concrete pipes in terms of corrosion resistance, flexibility, and ease of installation.

One significant threat is the competition from alternative materials such as plastic and metal pipes. These materials offer certain advantages, such as lighter weight and easier installation, which can make them more attractive for specific applications.

The substitution dynamic actually favors ADS. The company benefits from ongoing "conversion" from concrete and steel to plastic—not the other way around.

Industry Rivalry: MODERATE

In the U.S., corrugated HDPE pipe sector, ADS competes mostly against Los Angeles-based JM Eagle; Willmar, Minn.-based Prinsco Inc.; and Camp Hill, Pa.-based Lane Enterprises Corp.

We believe we are the only corrugated HDPE pipe producer with a national footprint, and our competitors operate primarily on a regional and local level. In the corrugated HDPE pipe sector in the United States, our primary competitors on a regional basis are JM Eagle, Lane Enterprises and Prinsco.

ADS's dominant market share in HDPE corrugated pipe means competition is based more on service, technical support, and product breadth than pure price.

Hamilton's 7 Powers Framework Analysis

Scale Economies: STRONG ✓

ADS manages the industry's largest company-owned fleet, an expansive sales team, and a vast manufacturing network of approximately 70 manufacturing plants and 40 distribution centers. The Company is one of the largest plastic recycling companies in North America, ensuring over half a billion pounds of plastic is kept out of landfills every year.

The recycling operations benefit enormously from scale. Processing 500+ million pounds of recycled material annually creates cost advantages that smaller competitors cannot match.

Network Effects: MODERATE

The distribution network creates soft network effects. As ADS expands its manufacturing and distribution footprint, contractors increasingly rely on ADS products because they know they can get consistent supply wherever they're working.

Counter-Positioning: STRONG ✓

Traditional concrete and steel pipe manufacturers face a classic counter-positioning dilemma. To match ADS's plastic offering, they would have to cannibalize their existing businesses and invest in entirely new manufacturing capabilities.

Switching Costs: MODERATE

Engineering specifications, contractor familiarity, and product certifications create moderate switching costs. Once an engineer specifies ADS products, changing mid-project is costly and risky.

Branding: MODERATE

We extrude a green stripe on our corrugated pipes, and that has become an iconic symbol and a representation of our brand that lets the customer know they are working with an ADS pipe.

The green stripe has become recognizable in the construction industry, though brand strength is more relevant in professional/B2B contexts than consumer markets.

Cornered Resource: STRONG ✓

The recycling infrastructure represents a cornered resource. ADS consumed approximately 33 percent of the recycled pigmented HDPE bottles in the U.S. This scale in recycled feedstock procurement is difficult to replicate.

Process Power: STRONG ✓

Chlapaty said the process is sophisticated and involves controlling a range of properties so the material can be reprocessed and manufactured into pipe without diminishing quality or performance.

The ability to blend recycled and virgin materials while maintaining quality standards represents accumulated process knowledge that took decades to develop.

The Bull Case

The bull case for ADS rests on three pillars: infrastructure tailwinds, material conversion, and recycling economics.

Infrastructure Spending Acceleration

The Infrastructure Investment and Jobs Act will significantly boost demand in the infrastructure construction sector over the next five years. Water infrastructure is uniquely positioned to benefit from federal spending programs, and ADS products are specified in highway, airport, and municipal projects across the country.

Material Conversion Runway

The conversion from concrete and steel to plastic is far from complete. The global concrete pipe market is projected to witness a moderate decline with a CAGR of -0.4% during the forecast period of 2023-2032. This decline is primarily attributed to the increasing adoption of alternative materials for pipe manufacturing. As plastic gains share in a $10+ billion addressable market, ADS is positioned to capture disproportionate gains.

Recycling as Competitive Moat

The recycling infrastructure creates a sustainable cost advantage while aligning with ESG mandates. ADS increased overall capital spending by 10% to $184 million in fiscal 2024, investing to increase automation, manufacturing growth and recycling capacity. Continued investment strengthens the moat.

The Bear Case

Cyclical Exposure

ADS remains exposed to construction cycles. The company adjusted its fiscal 2025 revenue guidance downward due to continued choppiness in the non-residential market and weather impacts. Interest rate sensitivity in residential construction creates volatility.

Commodity Input Risk

The primary challenge facing the corrugated plastic pipe market is the volatility of raw material prices. The price of petroleum, which is a key component in the production of plastic materials, can fluctuate significantly due to global supply chain disruptions or changes in oil prices.

Execution Risk in Recycling Expansion

"Today, we have what got us to the first 550 million pounds. But what got us here today is not what gets us to a billion. We're going to have to think outside the box. We're going to start looking at utilizing different types of materials because, frankly, there's no visibility to getting to an 80 percent recovery rate of HDPE out of residential streets, unfortunately."

Reaching the billion-pound goal requires expanding into new material streams with uncertain economics.

Key Performance Indicators for Investors

For investors tracking ADS's ongoing performance, three KPIs deserve particular attention:

1. Recycled Material Utilization Rate

The percentage of recycled content in ADS products—currently around 50%—is a leading indicator of both cost structure evolution and competitive moat strength. Progress toward the billion-pound goal will be visible in this metric.

2. Adjusted EBITDA Margin

The company achieved a record 32.1% Adjusted EBITDA margin in fiscal 2024. Maintaining margins above 30% through cycles demonstrates pricing power and operational efficiency.

3. Conversion Revenue Growth

Growth in revenue from infrastructure and highway applications—areas where plastic is actively displacing concrete—indicates the health of the core conversion thesis.

Conclusion: The Water Management Play

Advanced Drainage Systems represents a rare combination in public markets: a dominant position in an essential but overlooked industry, powered by secular tailwinds and protected by formidable competitive moats.

The company's journey from Ohio farm drainage to billion-dollar water management platform illustrates the value of patient capital allocation, disciplined execution, and strategic clarity. The "boring is beautiful" thesis has delivered exceptional returns for long-term shareholders.

"Water is the world's most precious resource," said Scott Barbour, President and Chief Executive Officer. As climate change intensifies storm events, as aging infrastructure demands replacement, and as plastic recycling becomes increasingly valued, ADS sits at the intersection of multiple powerful trends.

The risks are real—cyclical exposure, commodity input volatility, and execution challenges in recycling expansion. But the fundamental business model—converting traditional materials to thermoplastic alternatives while vertically integrating recycling operations—has proven resilient through multiple cycles.

For investors seeking exposure to essential infrastructure with sustainability characteristics, ADS offers a compelling combination of market leadership, competitive moats, and growth potential. The question isn't whether water management is important—it's whether any other company is better positioned to capture the opportunity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube