Warner Music Group: From Hollywood Sideshow to Streaming Powerhouse

I. Introduction & Episode Roadmap

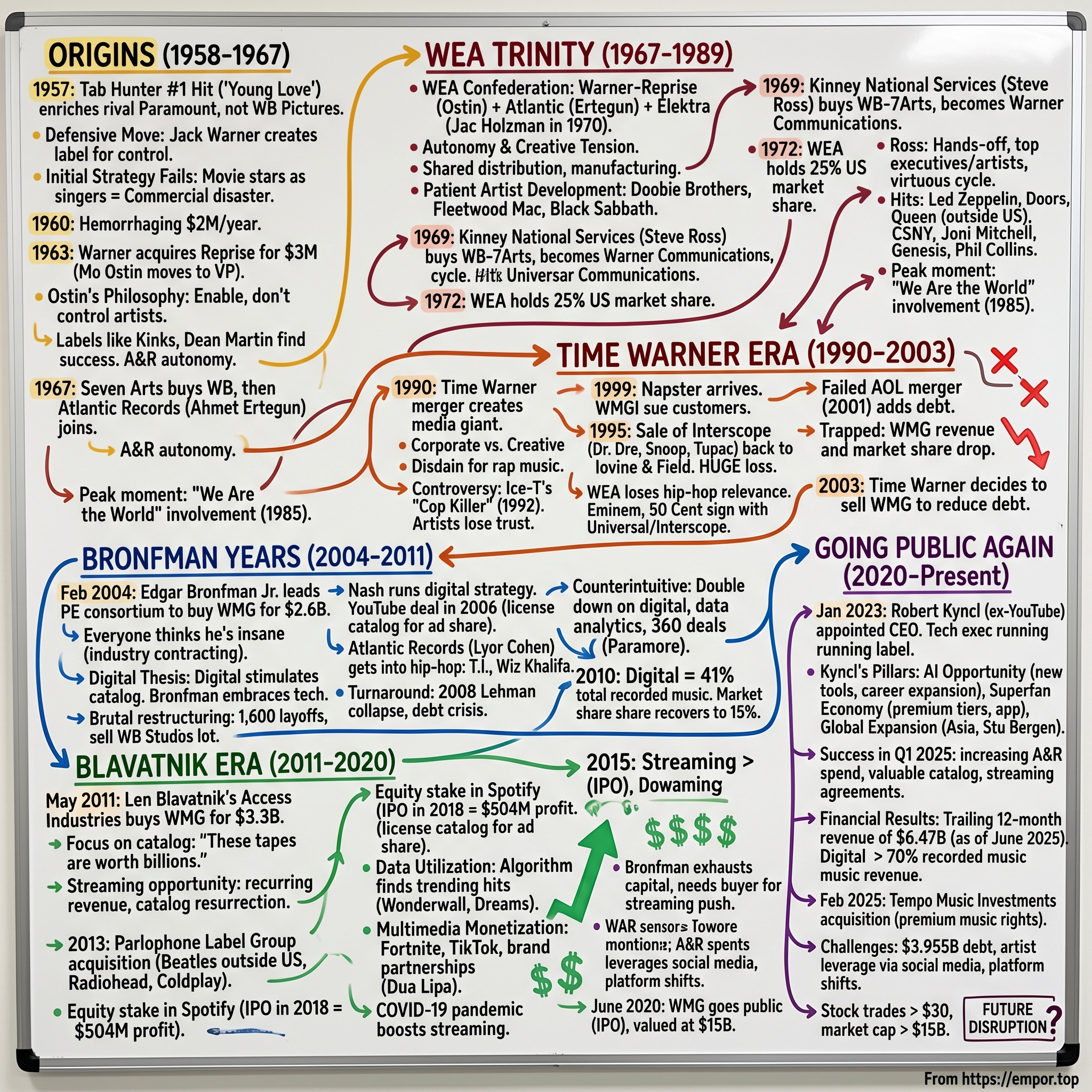

Picture this: It's 1957, and Tab Hunter—a blonde, blue-eyed heartthrob under contract with Warner Bros. Pictures—scores a #1 hit with "Young Love." There's just one problem. The song enriches rival Paramount Pictures through their Dot Records label, while Warner Bros., despite owning Hunter's acting rights, sees nothing from his musical success. Jack Warner, the legendary studio mogul known for his iron grip on talent, is furious. Not at Hunter, but at himself—for missing an entire revenue stream.

This corporate embarrassment would spawn Warner Music Group, today a $15 billion music empire that controls roughly 16% of the global recorded music market. From a defensive maneuver by a paranoid movie studio to one of the "Big Three" record companies alongside Universal and Sony, WMG's journey reads like a rock opera—complete with corporate villains, creative heroes, spectacular crashes, and triumphant comebacks.

The central paradox of Warner Music Group is this: How did a company that began as Hollywood's reluctant, tone-deaf stepchild become the industry's most prescient predictor of format shifts? How did the label that championed counterculture in the 1970s, then catastrophically misread hip-hop in the 1990s, ultimately nail the streaming transition better than rivals with deeper pockets?

Today's WMG, headquartered in a sleek Manhattan tower far from its humble origins above a Burbank machine shop, represents artists from Ed Sheeran to Cardi B, from Bruno Mars to Dua Lipa. In 2024, Warner Music Group reported revenues of $6.43 billion, with the Warner Music Group's overall current share slipping to 15.98% of the U.S. market. But these numbers only hint at the drama beneath.

This episode explores three key themes that define Warner's trajectory. First, the eternal tension between creative risk-taking and corporate control—a battle that has raged since day one. Second, the company's uncanny ability to completely botch one technological transition (digital downloads) while absolutely nailing the next (streaming). And third, the underappreciated power of catalog—those dusty old recordings that turned out to be digital gold mines.

What you'll learn goes beyond Warner's specific journey. This is a masterclass in how industries transform, how corporate culture shapes strategic decisions, and why sometimes the smartest move is selling to private equity exactly when everyone thinks you're doomed. Let's dive into how a movie studio's paranoid side project became one of the most important companies in entertainment.

II. Origins: The Hollywood Studio's Reluctant Entry (1958-1967)

The machine shop at 3701 Warner Boulevard in Burbank, California, wasn't exactly Abbey Road. In 1958, as mechanics below fixed studio equipment and the smell of motor oil wafted through vents, Warner Bros. Records opened its first office on the floor above. The setting was perfect metaphor for what Jack Warner thought of his new record label: a mechanical necessity, not an artistic endeavor.

Warner Bros. Pictures had been forced into the music business by pure defensive paranoia. When Tab Hunter's "Young Love" hit #1 in 1957, enriching rival Paramount's Dot Records while Warner Bros. collected nothing despite owning Hunter's acting contract, Jack Warner experienced what colleagues described as "volcanic fury." Not at the money left on the table—though that stung—but at the loss of control. In the studio system, Warner Bros. owned every aspect of their stars' careers. This music loophole was intolerable.

The initial strategy was laughably naive: Warner Bros. Records would simply record the studio's contract actors singing. After all, if Tab Hunter could have a hit, why not the rest of the Warner stable? The label's first releases included albums by TV cowboys, B-movie actresses, and anyone else on the lot who could carry a tune (and many who couldn't). The results were predictable: commercial disaster and industry ridicule.

By 1960, Warner Bros. Records was hemorrhaging $2 million annually—serious money for what Jack Warner considered a vanity project. The label had signed the Everly Brothers for a then-staggering $1 million, but even legitimate artists couldn't overcome the fundamental problem: nobody at Warner Bros. understood the record business. They were applying movie studio logic to an entirely different industry.

Enter Frank Sinatra—not as savior, but as unlikely catalyst. In 1960, Sinatra had launched Reprise Records with the tagline "a label where artists are in charge." He'd grown tired of Capitol Records' control over his material and wanted creative freedom. By 1963, despite artistic success, Reprise was struggling financially. Sinatra needed corporate backing; Warner needed credibility and expertise.

The 1963 acquisition of Reprise for $3 million brought Warner something more valuable than Sinatra's star power: Mo Ostin. A former accountant at Verve Records who'd become Reprise's administrative vice president, Ostin was the antithesis of a Hollywood executive. Quiet, bespectacled, and obsessed with jazz, he understood something revolutionary: the record business wasn't about controlling artists—it was about enabling them.

Under Ostin's influence, Warner-Reprise began its transformation. Instead of forcing contract actors to sing, they started signing real musicians. Instead of chasing existing hits, they began developing artists. The Kinks, Petula Clark, and Dean Martin gave the label its first taste of consistent success. But the real revolution was cultural. Ostin created an environment where A&R executives had autonomy, where artistic vision mattered more than quarterly earnings, where being "too weird" was often a selling point.

By 1967, Warner Bros. Records had gone from industry joke to legitimate player, generating profits and critical acclaim. But Jack Warner, now 75 and tired of fighting with his board, was ready to sell. Seven Arts Productions, a Canadian company run by Elliot Hyman, bought Warner Bros.—including its now-promising record division—for $32 million.

The Seven Arts deal would prove transformative, not because of Seven Arts itself (which would flame out within two years) but because of what came with it: Atlantic Records. The label that Ahmet Ertegun and Herb Abramson had built from a one-room office in 1947 into R&B's most important company was now Warner's sibling. The stage was set for something unprecedented in the music business: a record company that could match corporate muscle with creative credibility. The machine shop was about to become a hit factory.

III. The WEA Trinity: Building a Music Empire (1967-1989)

Ahmet Ertegun didn't want to sell Atlantic Records. In late 1967, sitting in his Manhattan office surrounded by gold records from Ray Charles, Aretha Franklin, and Wilson Pickett, the Turkish-born son of a diplomat had built something singular: a label that Black artists trusted and white audiences bought. But his partner Jerry Wexler was exhausted, and more importantly, the music business was changing. Distribution was becoming everything, and independents were getting crushed.

When Seven Arts bought Warner Bros. and immediately acquired Atlantic for $17.5 million, Ertegun negotiated something unprecedented: complete autonomy. Atlantic would use Warner's distribution muscle but maintain total creative control. He'd seen what happened to other independents absorbed by majors—they became soulless profit centers. Ertegun would rather shut down than let that happen to Atlantic.

The arrangement created an fascinating dynamic. You had Mo Ostin at Warner-Reprise in Burbank, signed acts like Van Morrison and James Taylor. Ahmet Ertegun at Atlantic in New York, working with Led Zeppelin and Crosby, Stills & Nash. And then, in 1970, came the third piece: Elektra Records, bought for $10 million, run by Jac Holzman who'd discovered The Doors and Love.

What emerged wasn't a record company but a confederation—WEA (Warner-Elektra-Atlantic). Each label maintained its identity, its roster, even its own promotion teams. They only shared distribution and manufacturing. It was corporate structure as jazz improvisation: structured chaos that somehow worked.

The magic was in the creative tension. When Atlantic's Jerry Wexler thought Led Zeppelin was "uncategorizable noise," Ertegun signed them anyway. When Warner's staff thought Neil Young was uncommercial, Ostin gave him a generous deal with complete creative control. When Elektra's Holzman wanted to sign Queen, the other labels thought they were too theatrical—Holzman signed them to worldwide rights everywhere except the U.S. and Canada.

This was the era when WEA perfected what became known as "artist development"—a patient, expensive process of building careers rather than chasing hits. The Doobie Brothers released three albums before breaking through. Fleetwood Mac was on their tenth album before "Rumours" made them superstars. Black Sabbath's first album sold modestly; WEA kept investing until they became metal gods.

The financial results were staggering. By 1972, WEA had captured 25% of the U.S. music market. The combined revenue of the three labels exceeded $400 million. But the real asset was cultural capital. WEA had somehow fused countercultural credibility with mainstream success. They had the Grateful Dead and Alice Cooper, Joni Mitchell and Deep Purple, James Taylor and Parliament-Funkadelic.

Behind this creative explosion was a corporate evolution equally dramatic. In 1969, Kinney National Services—a company that started with funeral homes and parking lots—bought Warner Bros.-Seven Arts for $400 million. Run by Steve Ross, a former funeral director with Hollywood dreams, Kinney spun off its non-entertainment assets in 1971 to become Warner Communications.

Ross was the anti-Jack Warner: charismatic where Warner was tyrannical, generous where Warner was stingy, hands-off where Warner was controlling. He paid his executives lavishly, flew artists on the corporate jet, and most importantly, never interfered with creative decisions. His philosophy was simple: hire the best people and get out of their way.

The approach created a virtuous cycle. Top executives wanted to work for WEA because of the autonomy. Top artists wanted to sign because of the executive talent. The money followed the music. By 1978, Warner Communications' music division was generating over $1 billion in revenue, with operating margins approaching 20%.

But the peak moment—the one that captured WEA's peculiar genius—came in 1985 with "We Are the World." Quincy Jones produced it for Columbia Records, but when he needed studio time at A&M Records, and engineering from multiple labels, it was Warner's Mo Ostin who made the calls that brought everyone together. The biggest charity single in history happened because WEA understood something fundamental: sometimes cooperation creates more value than competition.

Yet even as WEA dominated the 1970s and early 1980s, cracks were forming. The label executives who'd built the empire were aging. New genres were emerging that WEA didn't understand. And Steve Ross, the benevolent corporate parent who'd protected the music division's independence, was looking at bigger deals—specifically, a merger with Time Inc. that would fundamentally alter WEA's DNA. The confederation that had conquered rock was about to face its first existential crisis: what happens when artists stop running the asylum?

IV. Time Warner Era: Corporate Consolidation & Creative Tensions (1990-2003)

The Time Warner merger announcement on January 10, 1990—a $14.9 billion combination creating the world's largest media company—should have been Steve Ross's triumph. Instead, standing at the podium of the Time-Life Building, he looked uncomfortable. When a reporter asked about "synergy," that era's favorite buzzword, Ross gave an uncharacteristically vague answer. He knew what the Time Inc. executives didn't: you can't synergize creativity.

Time Inc. brought prestige (Time Magazine, Sports Illustrated, HBO) and a buttoned-up corporate culture that viewed Warner's music division with barely concealed disdain. Time executives referred to the record company as "the music people" in a tone typically reserved for discussing exotic diseases. They were particularly horrified by rap music, which WEA had been slow to embrace but was now pursuing aggressively.

The collision came in 1992 with Ice-T's "Cop Killer" on Warner's Sire Records. The song, performed with Ice-T's metal band Body Count, contained lyrics about retaliating against police brutality. Police organizations launched boycotts. Politicians denounced Time Warner. Shareholders, including Beverly Hills police pension funds, demanded the song's removal. Charlton Heston read the lyrics at a shareholders meeting, censoring the profanity while claiming moral outrage.

Gerald Levin, who'd become CEO after Ross's death from prostate cancer in December 1992, faced a decision that would define Time Warner's relationship with its music division. Unlike Ross, who would have backed his artists, Levin wavered. After months of pressure, Ice-T voluntarily removed the song from future pressings, but the damage was done. Artists saw that Time Warner would fold under political pressure.

The aftermath was catastrophic for WEA's hip-hop credibility. In 1995, facing continued controversy over Death Row Records releases distributed through Interscope (which Atlantic backed), Time Warner sold its 50% stake in Interscope back to founders Jimmy Iovine and Ted Field. With that sale went Dr. Dre, Snoop Dogg, Tupac—the architects of West Coast hip-hop's commercial explosion.

The numbers told the story: In 1995, hip-hop generated $825 million in revenue. By 2000, it was $1.8 billion. WEA, which had dominated rock in the 1970s, captured almost none of this growth. While Interscope—now distributed by Universal—had Eminem, 50 Cent, and Dr. Dre, Warner had... silence. They'd literally sold away the future to appease corporate overlords.

Meanwhile, a different storm was gathering. In June 1999, an 18-year-old college dropout named Shawn Fanning released Napster. Within months, millions were downloading music for free. The industry's response was to sue its own customers—Time Warner joined the RIAA's lawsuit campaign that would eventually target over 35,000 individuals, including 12-year-olds and grandmothers.

Edgar Bronfman Jr., who ran Universal Music, later admitted: "We used to fool ourselves into thinking our content was scarce. Napster taught us it was infinite." Time Warner's response was even worse—they had no response. While Apple's Steve Jobs was developing iTunes, Time Warner was developing more aggressive legal strategies.

The January 2001 merger with AOL—valued at $165 billion, the largest in history—was supposed to solve everything. AOL would bring Time Warner into the digital age. Instead, it became the worst merger in corporate history. AOL's dial-up business was collapsing just as broadband emerged. The promised "synergies" never materialized. By 2002, the company posted a $98.7 billion loss, the largest in corporate history.

For Warner Music Group, trapped inside this corporate disaster, the situation was desperate. Revenue fell from $4.1 billion in 2000 to $3.3 billion in 2003. Market share dropped below 13%. The artist roster was aging—Madonna, though still profitable, wasn't the future. Younger acts were signing elsewhere.

In late 2003, Time Warner CEO Dick Parsons made a decision: Warner Music Group had to go. The company needed to reduce debt from the AOL catastrophe, and the music division—once Steve Ross's crown jewel—was expendable. The only question was who would be crazy enough to buy a record company while Napster's successors were destroying the industry.

The answer came from an unexpected source: Edgar Bronfman Jr., heir to the Seagram fortune, who'd already bought and sold Universal Music, now wanted Warner. His plan wasn't to fight digital distribution but to embrace it. The corporate suits who'd neutered WEA's creative culture were about to be replaced by private equity sharks. Whether that was better or worse remained to be seen. But one thing was certain: the Time Warner era—13 years of corporate interference, missed opportunities, and cultural tone-deafness—was finally ending.

V. The Bronfman Years: Private Equity & Digital Awakening (2004-2011)

Edgar Bronfman Jr. had already destroyed one family fortune in the music business. In 2000, he'd sold Seagram—his family's 80-year-old liquor empire—to Vivendi in exchange for stock, then watched $3 billion in family wealth evaporate when Vivendi nearly collapsed. Yet here he was in February 2004, leading a private equity consortium to buy Warner Music Group for $2.6 billion.

"Everyone thought Edgar was insane," recalled one banker involved in the deal. The music industry had contracted 25% since 1999. Tower Records was heading toward bankruptcy. iTunes, launched a year earlier, was cannibalizing CD sales at an accelerating rate. Buying a record company in 2004 was like buying a typewriter factory in 1985.

But Bronfman saw something others missed. In WMG's 2005 annual report—the first after going public at $17 per share in May—he laid out a contrarian thesis: "We believe digital distribution will stimulate incremental catalog sales." While competitors fought digital, Bronfman would monetize it.

The strategy required brutal restructuring. Within 18 months, Bronfman cut $250 million in costs, laying off 1,600 employees—20% of the workforce. The Warner Brothers Studios lot in Burbank, where the company began above that machine shop, was sold. Sacred cows were slaughtered: the legendary Atlantic Records New York headquarters was shuttered, operations consolidated.

But the real revolution was philosophical. Bronfman hired a young executive named Michael Nash from EMI to run digital strategy. Nash's mandate was simple but radical: make friends with Silicon Valley. While Universal and Sony sued YouTube for copyright infringement, Nash was in Mountain View, negotiating.

The September 2006 deal with YouTube was transformative. Warner would license its entire catalog for streaming in exchange for a share of advertising revenue. The other majors thought Bronfman had lost his mind—why give away music for free? But the numbers told a different story. YouTube became WMG's laboratory for understanding digital consumption. Which songs went viral? What drove repeat listens? How did visual content affect audio sales?

By 2008, the strategy was paying off. The New York Times reported that Atlantic Records—the same label that Time Warner had nearly destroyed over hip-hop—became the first major label to generate more than half its U.S. revenue from digital sales. This wasn't just iTunes downloads; it was ringtones, streaming, gaming licenses—anywhere music could be monetized digitally.

Lyor Cohen, who Bronfman brought in to run recorded music in 2004, embodied this new approach. A former hip-hop manager who'd run Def Jam, Cohen understood what Time Warner never did: you don't fight cultural change, you monetize it. Under Cohen, Warner finally embraced hip-hop, signing T.I., B.o.B, and Wiz Khalifa. The label that had sold Interscope was suddenly relevant in rap again.

But September 2008 brought catastrophe. Lehman Brothers collapsed, credit markets froze, and WMG's debt—$2.3 billion worth—suddenly looked crushing. The stock price, which had reached $30 in 2007, crashed to $2.50. Bondholders were demanding restructuring. One analyst called WMG "a melting ice cube."

Bronfman's response was counterintuitive: he doubled down on digital. While cutting another $100 million in costs, he increased investment in data analytics and digital marketing. WMG became the first major to hire data scientists, building algorithms to predict hit potential and optimize release strategies.

The 360 deals that became industry standard started here. Instead of just recording rights, Warner would take percentages of touring, merchandising, and endorsements. Artists initially resented sharing more revenue, but Warner could now afford bigger advances and more marketing support. Paramore, signed to a 360 deal in 2005, saw their income triple despite selling fewer albums than projected.

By 2010, the turnaround was undeniable. Digital revenue had grown to 41% of total recorded music sales. Warner's market share had recovered to 15%. The company that many predicted would die had become the industry's most digitally advanced major label.

But Bronfman was exhausted. Seven years of fighting bondholders, restructuring operations, and evangelizing digital had taken its toll. More importantly, he saw what was coming: streaming would require massive capital investment, and WMG's debt load made that impossible. The company needed a buyer with deep pockets and patience.

In May 2011, Len Blavatnik's Access Industries bought Warner Music Group for $3.3 billion—a 30% premium to its trading price. Blavatnik, who'd invested $25 million in the 2004 buyout, had watched Bronfman transform a dying business into a digital pioneer. Now, with his billions from selling Russian oil assets, Blavatnik could fund the next transformation.

The Bronfman era ended with a paradox: he'd saved Warner Music by accepting the industry's decline. Instead of pretending CDs would recover, he'd built for a digital future. The company he handed to Blavatnik was smaller but smarter, leaner but more agile. Most importantly, it had learned the lesson that eluded Time Warner: in technology transitions, the first casualty should be ego, not opportunity.

VI. The Blavatnik Era: From Crisis to Streaming Gold Rush (2011-2020)

Len Blavatnik's first all-hands meeting at Warner Music Group in July 2011 was deliberately held not in a conference room but in the company's archive vault. Surrounded by master recordings from Frank Sinatra to Madonna, the Ukrainian-born billionaire made his point without words: these dusty tapes were worth billions if monetized correctly.

Blavatnik was an unlikely music mogul. His fortune came from Russian aluminum and oil, sold perfectly before the 2008 crash for $7 billion. He'd named his holding company Access Industries because, he once explained, "access to opportunity is everything." Now he had access to one of music's three major catalogs at exactly the right moment.

The 2012 annual report contained a single sentence that would define the Blavatnik era: "Music streaming represents significant promise and opportunity for the music industry." While competitors worried streaming would cannibalize downloads, Blavatnik saw a different model: recurring revenue, predictable growth, and most importantly, catalog resurrection.

Consider the math: Warner's catalog contained roughly 50,000 albums. On physical media, maybe 5,000 were economically viable to keep in print. On streaming services, all 50,000 could generate revenue. A forgotten 1973 progressive rock album that sold twelve copies in 2010 could suddenly earn thousands in micro-payments from playlist inclusions.

The July 2013 acquisition of Parlophone Label Group from Universal for £487 million demonstrated Blavatnik's strategy. Universal was forced to sell Parlophone by EU regulators after buying EMI. The crown jewel was obvious: The Beatles' catalog outside America. But Blavatnik saw deeper value: Radiohead, Coldplay, Pink Floyd—artists whose deep catalogs would thrive in streaming's infinite shelf space.

Stephen Cooper, the restructuring specialist Blavatnik installed as CEO, approached streaming deals with private equity discipline. Instead of fighting Spotify for higher per-stream rates like other labels, Cooper negotiated for equity stakes and minimum revenue guarantees. When Spotify went public in 2018, Warner's stake was worth $504 million—pure profit from embracing what others resisted.

The real innovation was in data utilization. Blavatnik hired tech executives from Amazon and Netflix to build Warner's analytics infrastructure. They discovered patterns invisible to traditional A&R: songs that underperformed on radio but exploded on streaming, markets where catalog outperformed new releases, optimal release times down to the hour.

This data-driven approach produced unexpected hits. "Wonderwall" by Oasis, released in 1995, suddenly generated millions in streaming revenue after Warner's algorithm identified it trending on social media and placed it strategically in Spotify playlists. Fleetwood Mac's "Dreams," from 1977, hit #1 on streaming charts in 2020 after a TikTok video went viral—Warner had been positioning catalog tracks for exactly such moments.

By 2015, the transformation was complete. Streaming revenue surpassed download revenue for the first time. Warner's revenues, which had bottomed at $2.87 billion in 2010, climbed steadily. Market share recovered to 17%. The company that had nearly died five years earlier was now valued at over $6 billion in private market transactions.

But Blavatnik wanted more than recovery—he wanted dominance in the streaming age. In 2017, he poached Stu Bergen from International Creative Management to run international operations, specifically to break Western artists in China and India where streaming was exploding. Bergen's first win: making Dua Lipa a superstar in Asia before she broke in America, reversing traditional geographic development.

The company also pioneered what internally was called "multimedia monetization." When Warner signed Dua Lipa in 2015, they didn't just get recording rights—they got synchronization rights for films, gaming rights for Fortnite, and brand partnership rights. Her song "Levitating" earned more from TikTok licensing and Fortnite events than traditional sales.

By 2019, Blavatnik faced a pleasant problem: Warner Music was worth too much to keep private. The catalog value alone—boosted by streaming's recurring revenue model—exceeded $8 billion by some estimates. Meanwhile, competitors were going public at massive valuations. Universal was preparing an IPO that would value it at €30 billion.

The COVID-19 pandemic should have derailed everything. Live music stopped. Retail stores closed. New releases were postponed. Instead, streaming exploded as locked-down consumers binged music. Warner's streaming revenue grew 20% in the first quarter of 2020 alone. The pandemic had accidentally proven Blavatnik's thesis: streaming was recession-proof.

On June 3, 2020, Warner Music Group went public again at $25 per share, raising $1.9 billion and valuing the company at $15 billion. Despite a global pandemic, despite economic uncertainty, despite everything—the market believed in streaming's future. The stock closed its first day up 8%.

Blavatnik retained 72% economic ownership and 98% voting control. He'd invested roughly $3.3 billion in 2011 and now held stock worth nearly $11 billion. But the real victory wasn't financial. He'd taken a company left for dead and rebuilt it for the streaming age. The next challenge would be maintaining that momentum as the industry faced new disruptions: TikTok, artificial intelligence, and direct-to-fan platforms that threatened the entire label model.

VII. Going Public Again: The Streaming Renaissance (2020-Present)

Robert Kyncl's appointment as Warner Music Group CEO in January 2023 was announced via YouTube video—a deliberate symbol. The former YouTube Chief Business Officer, who'd built the platform into music's largest streaming service by volume, represented something unprecedented: a tech executive running a major label.

"The music industry always hired from within," Kyncl explained in his first investor call. "That's why it kept missing technological shifts. I'm here to ensure Warner never misses another one."

The timing was critical. As of June 2025, Warner Music Group has a trailing 12-month revenue of $6.47 billion, but the streaming boom that lifted all boats was moderating. Spotify's subscriber growth was slowing. Apple Music had plateaued. The industry needed its next act. Kyncl's vision centers on three strategic pillars. First, artificial intelligence—not as threat but opportunity. Warner Music is developing AI tools to expand the music output and careers of the label's artists and songwriters, with Kyncl emphasizing that "When it comes to generating AI, it needs to be put in proper context. Framing it only as a threat is inaccurate". Warner is hiring for a Director of AI Automation & Growth role, focused on "identifying, developing, and implementing innovative AI solutions that enhance operational efficiency and drive strategic growth".

The approach reflects Kyncl's YouTube experience. As YouTube's chief business officer, he helped develop Content ID fingerprinting software that tracked copyrighted material and built commercial relationships with copyright holders, creating "a multibillion-dollar business per year". Now he's applying that playbook to AI-generated music.

Second, the "superfan" economy. While streaming democratized access, it commoditized engagement. A casual listener pays the same $10.99 monthly as someone who plays their favorite artist 500 times. Kyncl sees opportunity in premium tiers, exclusive content, virtual concerts—anything that lets superfans pay more for deeper connection. Warner is developing a superfan app with "a team of incredible technology talent from Google and Stripe and Instacart," designed to help "artists connect directly with their superfans," who "are generally the people that consume the most and spend the most". The app has progressed from its earlier beta version first tested by employees in spring 2024, with Ed Sheeran now "actively posting" on an in-development version.

The opportunity is massive. Goldman Sachs estimated the superfan monetization opportunity in recorded music at $4.5 billion in 2024. UMG's Boyd Muir noted that "Superfans, the most avid 20% to 30% of all music listeners, once drove more than 70% of recorded music spending"—a dynamic streaming's flat-rate model destroyed.

Third, global expansion beyond Western markets. Kyncl's hiring of Stu Bergen from International Creative Management in 2017 specifically targeted Asia, where streaming adoption is still early. The strategy already shows results: Dua Lipa broke in Asia before America, reversing traditional development patterns.

But the most striking aspect of Kyncl's tenure is what he hasn't done: panic. While Universal and Sony scramble to respond to TikTok's influence, Warner quietly builds proprietary technology. While competitors sue AI companies, Warner negotiates licenses. It's a confidence born from surviving near-death—once you've traded at $2.50 per share, every day above zero feels like victory. The latest financial results tell a story of measured success. In Q1 2025, CEO Robert Kyncl noted "success with new stars, global superstars, longtime legends, and irreplaceable catalog," emphasizing the company's strategy to "increase our A&R spend, acquiring valuable catalogs, and striking important agreements with streaming services". For fiscal year 2024, which ended September 30, 2024, Kyncl described WMG's performance as demonstrating "strength and adaptability in a thriving, fast-moving market," noting the company "continues to evolve WMG, based on the principle that simplicity and focus drive higher intensity and global impact," which is "enhancing our ability to attract original artists and songwriters at all stages of their careers".

The stock market has responded favorably. From its June 2020 IPO price of $25, Warner now trades above $30, giving it a market capitalization exceeding $15 billion. Access Industries' patience has been rewarded: Blavatnik's $3.3 billion investment in 2011 is now worth over $11 billion, not counting dividends.

Yet challenges remain. The company's debt load—$3.955 billion as of December 2024—constrains flexibility. Competition for talent intensifies as artists gain leverage through social media. And the next technological disruption—whether AI, blockchain, or something unforeseen—looms. But for a company that began as a movie studio's grudging side project, survival itself is triumph. Prosperity is just the encore.

VIII. The Modern WMG Business Model

The numbers that define Warner Music Group's modern business model would have seemed like science fiction to Jack Warner. In calendar Q3 2023, recorded music streaming revenues reached $848 million, up 8.9% year-over-year, representing nearly 66% of recorded music revenue. This isn't just a format shift—it's a fundamental reimagining of what a record company does.

Consider the economics: In the CD era, Warner manufactured plastic discs for $1, sold them to retailers for $10, who sold them to consumers for $15. Warner kept its $9 profit regardless of whether the consumer played the CD once or a thousand times. Today, Warner gets fractions of pennies per stream, but those fractions arrive forever. A hit song from 1975 generates revenue every single day in 2024.

The business now splits into two distinct but synergistic divisions. Recorded Music, generating roughly 80% of revenue, encompasses everything from artist development to playlist placement. Music Publishing, the remaining 20%, manages songwriting copyrights—a business that's proven remarkably resilient as songs get licensed for films, commercials, video games, and yes, TikTok videos.

Warner Chappell Music, the publishing arm, increased its turnover by 15.1% year-over-year in calendar Q3 2023 to $298 million, with growth coming from "the continued growth in streaming" as well as the impact of digital deal renewals, including the company's TikTok licensing deal renewal.

The real transformation is in catalog monetization. Warner's catalog—containing everyone from Led Zeppelin to Madonna—was once a depreciating asset. Physical albums went out of print; radio played only the hits. Streaming changed everything. Algorithms don't discriminate by release date. A 1968 Doors deep cut can suddenly explode on TikTok, generating millions in unexpected revenue.

The 360-degree deals that Bronfman pioneered have become standard. When Warner signs an artist today, they're not just getting recording rights. They're getting merchandise, touring, endorsements—every revenue stream an artist generates. Artists initially resented sharing more, but Warner can now afford bigger advances and more marketing support. It's portfolio theory applied to pop music.

But the most significant shift is from product company to service company. Warner doesn't sell music anymore; it sells access, discovery, and experience. The company employs more data scientists than A&R scouts, more programmers than producers. They're not in the music business—they're in the attention business, competing not with other labels but with Netflix, TikTok, and Fortnite for consumer engagement.

The margin structure tells the story. In the CD era, Warner's gross margins approached 50%—they were essentially a manufacturing business with high fixed costs. Today's streaming margins are lower but more predictable. No inventory, no returns, no retail markdowns. Every song in the catalog is always in stock, always available, always generating revenue.

The company's February 2025 acquisition of a controlling stake in Tempo Music Investments, an investment platform for premium music rights, demonstrates this catalog-first strategy. The deal will "provide the Company with additional revenue at a high margin" and "become more accretive over time, as rights revert to Tempo".

Digital now represents over 70% of total recorded music revenue, but that understates the transformation. Even "physical" sales are increasingly digital—vinyl purchased online, CDs ordered through Amazon. The entire value chain has been digitized, from artist discovery on TikTok to royalty payments via blockchain.

The paradox of the modern music business is that as music became free to consumers, it became more valuable to platforms. Spotify needs Warner's catalog to keep subscribers. YouTube needs it to keep viewers. TikTok needs it to keep creators creating. Warner's leverage isn't in controlling distribution—it's in controlling content that platforms can't survive without.

This model scales beautifully. Adding a million new listeners costs Warner nothing. Entering a new market requires no physical infrastructure. A hit in Nigeria spreads to London overnight. The same song can generate revenue simultaneously from a Spotify stream in Stockholm, a TikTok video in Tokyo, and a film placement in Hollywood.

Yet vulnerabilities persist. Warner doesn't control its distribution destiny—if Spotify changes its payment model, Warner's economics change overnight. The company depends on platforms it doesn't own, algorithms it doesn't control, and consumer behaviors it can only influence, not dictate. It's a fundamentally different business than the one Mo Ostin built, requiring different skills, different strategies, and most importantly, different definitions of success.

IX. Playbook: Key Business Lessons

The Warner Music Group story offers a masterclass in corporate evolution, but not the kind taught at business schools. This is evolution through catastrophe, transformation through near-death, success through spectacular failure. The lessons are counterintuitive, often contradictory, and absolutely essential for understanding how industries transform.

Lesson 1: Creative Risk vs. Corporate Control Is a False Choice

The conventional narrative says you must choose: either you're an artist-friendly creative haven or a profit-maximizing corporation. Warner's history suggests otherwise. The company thrived when it found leaders who understood both languages—Mo Ostin spoke to artists but delivered for shareholders, Steve Ross lavished money on talent but demanded returns. The disasters came when Warner chose one side: Time Warner's corporate suffocation killed creativity; Bronfman's initial artist-first approach nearly killed the company. The magic happens in the tension between these forces, not in resolving it.

Lesson 2: Timing Beats Strategy

Warner had the same strategic insight about hip-hop that it had about streaming: this is the future. But timing was everything. They entered hip-hop late, during peak controversy, and retreated just as it exploded commercially. They entered streaming early, when others were suing Napster, and rode the wave perfectly. The lesson isn't about being first or fast—it's about reading the cultural moment. Hip-hop in 1992 was rebellion; streaming in 2008 was inevitability. Warner confused the two.

Lesson 3: Catalog Value Compounds in Unexpected Ways

Every Warner executive since 1970 knew the catalog had value. What they didn't understand was how that value would compound with technological change. Physical media limited catalog exploitation—shelf space was finite, manufacturing had minimums. Digital removed these constraints. A song recorded in 1965 could suddenly generate millions in 2020 because someone used it in a TikTok video. The lesson: assets that seem fully valued in one technological paradigm can become exponentially more valuable in the next.

Lesson 4: The Best Time to Sell Is When Everyone Thinks You're Doomed

Time Warner sold WMG in 2004 when the music industry was "dying." Bronfman sold in 2011 when streaming hadn't proven profitable. Both sellers thought they were escaping disaster; both buyers made fortunes. The pattern holds across industries: maximum pessimism often coincides with maximum opportunity. The key is distinguishing between existential threats (the music industry disappearing) and transitional challenges (formats changing).

Lesson 5: Organizational Culture Survives Ownership Changes

Despite five different owners since 1967, certain Warner traits persist: artist autonomy, label independence, creative risk-taking. These survived corporate mergers, private equity, and public markets. Culture, it turns out, is more durable than capital structure. But it requires conscious preservation—leaders who understand what makes the company special and protect it through transitions.

Lesson 6: Data and Intuition Are Complements, Not Substitutes

The modern Warner runs on data—streaming analytics, social media metrics, algorithmic predictions. But the biggest successes still come from intuition. Signing Dua Lipa wasn't data-driven; keeping faith in catalog value wasn't algorithmic. Data tells you what is; intuition tells you what could be. The companies that win combine both.

Lesson 7: Industry Structure Matters More Than Company Strategy

Warner's strategic choices mattered less than industry structure evolution. When there were six major labels, Warner thrived despite mistakes. When there are three, even perfect execution yields modest returns. The consolidation that "saved" the industry also capped its upside. Sometimes the most important strategic decision is recognizing when industry structure limits what strategy can achieve.

Lesson 8: Building for Multiple Owners Is Its Own Skill

Most companies build for permanence. Warner has built for transactions—structured for easy sale, clear value proposition, separable assets. This isn't cynical; it's realistic. In industries facing technological disruption, ownership changes are inevitable. Building a company that can survive and thrive through these transitions is perhaps the ultimate corporate skill.

The meta-lesson is that Warner's survival required abandoning almost everything that made it successful initially. The company that championed physical albums now celebrates their obsolescence. The label that fought MTV now partners with TikTok. The business that sued Napster now depends on streaming. This isn't hypocrisy—it's evolution. And in industries facing technological disruption, evolution is the only strategy that matters.

X. Bull vs. Bear Case Analysis

The Bull Case: Streaming's Second Act

The bulls see Warner Music Group at an inflection point. Streaming penetration in developed markets sits around 60%, leaving substantial room for growth. But the real opportunity lies in emerging markets—India, Africa, Latin America—where streaming adoption is just beginning. With smartphones becoming ubiquitous and data costs plummeting, three billion new consumers are entering the addressable market.

Price increases represent another untapped lever. Netflix charges $15-20 monthly; Spotify charges $10.99. Music, arguably more essential to daily life than video content, remains underpriced. Every $1 increase in monthly subscription prices flows almost directly to label bottom lines. Warner's CFO Bryan Castellani points to "healthy global subscriber trends" as evidence the market will bear higher prices.

The catalog thesis grows stronger with time. As Warner's vault expands—through both acquisition and reversion of rights—it becomes a perpetual annuity. Streaming platforms need deep catalogs to reduce churn; Warner owns music that defines generations. This isn't a melting ice cube; it's a compound interest machine.

Artificial intelligence, rather than threat, becomes opportunity. AI needs training data; Warner owns it. AI enables new creative tools; Warner can license them. AI creates new use cases for music; Warner monetizes them. The company's proactive approach—hiring AI specialists, negotiating licenses rather than suing—positions it to benefit from, rather than be disrupted by, the technology.

The superfan economy could double the revenue per user. If 20% of listeners pay 3x more for premium experiences, the math is compelling. Warner's early moves here—building proprietary apps, testing with Ed Sheeran—could establish first-mover advantage in a multi-billion dollar market.

Consolidation economics favor the incumbents. The barriers to creating a competing major label are insurmountable—you'd need decades of catalog, global infrastructure, and platform relationships. As the industry consolidates from six to three majors, pricing power increases. It's an oligopoly with a product consumers can't live without.

The Bear Case: Peak Music's Structural Challenges

The bears see fundamental structural problems. Warner is eternally third place among majors, with roughly half Universal's market share. In winner-take-all markets, third place is precarious. One bad year of A&R decisions, one lost bidding war for a superstar, and market share evaporates.

Access Industries' 72% economic ownership and 98% voting control creates governance concerns. Public shareholders own equity but not influence. Blavatnik could take the company private at any time, potentially at an unfavorable price. This ownership overhang limits institutional investment and multiple expansion.

The streaming economics are troubling. Platforms capture most of the value—Spotify's market cap exceeds all three majors combined. As platforms consolidate and labels remain fragmented, negotiating leverage shifts. Warner depends on companies it doesn't control for distribution it can't replace.

Artist leverage is increasing exponentially. Social media enables direct-to-fan relationships. Distribution is democratized. Recording costs approach zero. Why does an artist need a label? Warner's 360 deals extract more revenue but offer less unique value. The next Taylor Swift might not sign with a major at all.

Competition from independent distribution platforms intensifies. Companies like DistroKid, CD Baby, and TuneCore let artists keep 85-100% of revenues versus 15-20% with majors. As these platforms add services—marketing, playlist pitching, data analytics—the major label value proposition erodes.

The TikTok threat is existential. The platform has become the dominant music discovery engine, yet labels have minimal influence over its algorithm. Songs explode randomly, back catalog surges unpredictably, and Warner can only react, not control. Building artist careers in this environment is like gambling, not investing.

Technological disruption accelerates. Web3 promises artist-owned platforms. Blockchain enables direct monetization. AI might make human artists optional. Warner survived one technological transition; assuming it survives the next is hubris.

The Verdict: A Complicated Investment

The truth lies between these extremes. Warner Music Group is neither doomed nor dominant. It's a mature business in a growing industry, with structural advantages and structural challenges. The bull case requires everything going right—streaming growth, price increases, superfan monetization. The bear case requires only one thing going wrong—a platform shift, a technological disruption, a loss of artist relevance.

The investment case ultimately depends on time horizon and risk tolerance. For patient investors who believe in music's cultural durability and streaming's continued growth, Warner offers exposure to a essential consumer behavior at a reasonable valuation. For those worried about technological disruption and platform dependency, it's a value trap waiting to spring.

What's certain is that Warner Music Group will look very different in five years. Whether that's better or worse for shareholders remains the multi-billion dollar question.

XI. Epilogue: "If We Were CEOs"

If we inherited Robert Kyncl's office tomorrow, looking out from Warner's Manhattan headquarters at an industry transforming in real-time, what would we do? The answer isn't in fighting the last war—streaming is won—but preparing for the next one.

Priority One: Own the Relationship

The existential risk to Warner isn't AI or TikTok—it's disintermediation. Every layer between artist and fan that gets removed diminishes Warner's value. So we'd build what platforms can't: genuine, direct, monetizable relationships. Not another app competing with thousands, but infrastructure that artists actually need.

Imagine "Warner Studios"—physical and virtual spaces where artists create, fans engage, and content flows seamlessly to every platform. Think Apple Stores meets Abbey Road meets Twitch. Artists get world-class facilities and technical support. Fans get exclusive access and experiences. Warner gets content, data, and relationships that platforms can't replicate.

Priority Two: The Emerging Markets Leapfrog

The next billion music consumers won't follow Western patterns. They'll skip ownership entirely, experience music through short-form video, and value curation over collection. Warner needs infrastructure built for these behaviors, not adapted from existing models.

We'd establish Warner Lagos, Warner Mumbai, Warner São Paulo—not satellite offices but autonomous entities with local leadership, local capital, and local decision-making. Let them sign artists Western A&R would never understand, develop models that don't make sense in Manhattan, and build for consumers who experience music completely differently.

The opportunity is massive: India alone could surpass the U.S. as the world's largest music market by 2030. But winning requires more than translation—it requires reimagination.

Priority Three: The AI Collaboration Engine

Rather than defensive licensing, we'd make Warner the premier AI music laboratory. Partner with every major AI company not to restrict but to explore. What happens when AI can create infinite variations of classic songs? When dead artists can "collaborate" with living ones? When every listener gets personalized versions of their favorite tracks?

We'd establish ethical frameworks, authentication systems, and revenue models before regulators impose them. Create "AI-certified" tracks that guarantee human involvement. Build tools that augment rather than replace human creativity. The goal: make Warner synonymous with responsible AI innovation, attracting both artists who embrace technology and those who fear it.

Priority Four: The Superfan Treasury

The superfan opportunity is real but misunderstood. It's not about charging more for the same product—it's about creating entirely new value. We'd build "Warner Treasury," a blockchain-based platform where superfans can own authentic pieces of music history.

Limited edition remasters with artist commentary. Original demo recordings. Virtual concert tickets that appreciate in value. Fractional ownership of song royalties. NFTs that actually have utility—backstage access, studio sessions, artist interactions. Make fandom an investment, not just an expense.

Priority Five: The Format Shift Preparation

Streaming won't last forever. Something will replace it—we don't know what, but we can prepare for the transition. We'd create Warner Labs, tasked with one mission: imagine and prototype the next format.

Spatial audio experiences? Music in the metaverse? Neural interfaces that trigger emotional responses? Most experiments will fail, but Warner needs to be experimenting. The company that missed hip-hop can't afford to miss the next cultural shift.

Priority Six: The Talent Sustainability Model

The current model—massive advances to stars, minimal investment in development—is unsustainable. We'd create Warner Academy, identifying talent at age 15, not 25. Provide education, mentorship, and gradual development. Build careers, not just hits.

Think sports academies but for music. Scout globally, develop locally, deploy strategically. Create a pipeline of talent that doesn't depend on viral TikTok moments or bidding wars. Make artist development a competitive advantage again.

The Uncomfortable Truth

Here's what we wouldn't do: try to recreate the past. The era of labels as gatekeepers is over. The period of controlling distribution has ended. The time when A&R intuition trumped data has passed.

Warner Music Group's next chapter isn't about reclaiming lost power—it's about finding new forms of value creation. In a world where music is infinite and free, the scarcity isn't in recordings but in attention, community, and meaning. The label that figures out how to create and capture those scarce resources wins the next era.

The irony is perfect: Warner began as a defensive move by a movie studio, survived by abandoning everything that made it successful, and now thrives by embracing what once threatened to destroy it. The next transformation will require similar courage—letting go of streaming while it's still growing, embracing technologies that seem threatening, and building for customers who don't yet exist.

If Jack Warner could see his reluctant creation today—a technology company that happens to deal in music—he'd be appalled. Mo Ostin might be confused. Even Edgar Bronfman would be surprised. But Len Blavatnik and Robert Kyncl understand: in industries facing perpetual disruption, the only sustainable strategy is permanent revolution.

The question isn't whether Warner Music Group will exist in 20 years—music is too essential to human experience for its major distributors to disappear. The question is whether it will be recognizable. If history is any guide, the answer is no. And that's exactly why it will survive.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube