Waste Management: From Garbage Hauler to Environmental Solutions Giant

I. Introduction & Episode Roadmap

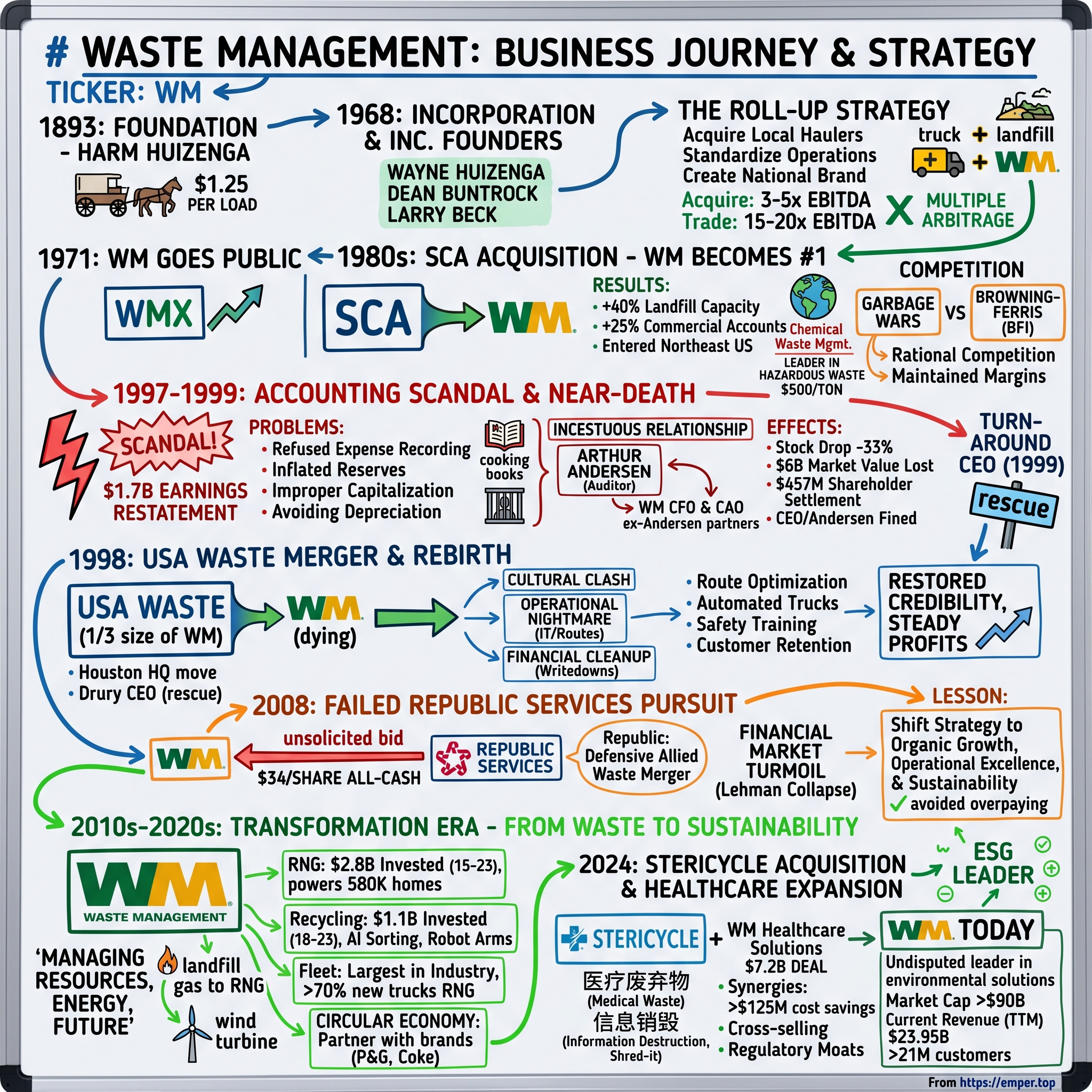

Picture this: It's 1893, and a Dutch immigrant named Harm Huizenga is hauling garbage through Chicago's muddy streets with a single horse-drawn wagon, charging $1.25 per load. Fast forward 131 years, and his grandson's company controls the waste streams of half of America, generates $24 billion in annual revenue, and operates the largest fleet of natural gas vehicles in North America. This is the story of Waste Management—a tale of entrepreneurial vision, spectacular scandal, and ultimate redemption that transformed society's literal trash into Wall Street treasure.

Today's Waste Management stands as North America's undisputed environmental solutions leader, with a market capitalization exceeding $90 billion and trailing twelve-month revenues of $23.95 billion. But calling WM just a "garbage company" is like calling Amazon a bookstore. The company has evolved from a fragmented collection of local haulers into a sophisticated environmental services platform that turns methane from landfills into renewable energy, processes millions of tons of recyclables, and now, with its recent Stericycle acquisition, safely handles the nation's medical waste.

The journey from Harm's wagon to today's sustainability powerhouse wasn't linear. It's a story punctuated by audacious roll-up strategies, accounting fraud that nearly destroyed the company, hostile takeover attempts, and a complete reimagining of what a waste company could be in the 21st century. Three entrepreneurs—Wayne Huizenga, Dean Buntrock, and Larry Beck—took a centuries-old business and applied Wall Street sophistication to Main Street garbage routes, forever changing how America handles its waste.

What makes this story particularly compelling for students of business history is how WM navigated multiple existential crises while building what Warren Buffett might call a "moat"—infrastructure so extensive and permits so difficult to replicate that new competitors face nearly insurmountable barriers. The company owns 254 active landfills, operates 337 transfer stations, runs 97 recycling facilities, and commands a fleet of 26,000 collection vehicles. These aren't just assets on a balance sheet; they're the physical manifestation of decades of strategic positioning.

Over the next several hours, we'll explore how three entrepreneurs recognized opportunity in America's most fragmented industry, how they nearly lost everything to accounting fraud, and how the company reinvented itself as an ESG leader before ESG was even a term. We'll dissect failed hostile takeovers, analyze the economics of route density, and understand why two companies—WM and Republic Services—now dominate an industry that once comprised thousands of mom-and-pop operators.

This episode will take you from Chicago's immigrant neighborhoods to Houston's corporate boardrooms, from the accounting scandals that predated Enron to the renewable energy facilities that now power thousands of homes. We'll examine the playbook for industry consolidation, the challenges of operational integration at massive scale, and the strategic pivot from waste disposal to environmental solutions. Along the way, we'll extract lessons for operators building in fragmented markets and investors seeking to understand the dynamics of essential services.

Buckle up. This isn't just a story about trash—it's about American capitalism, entrepreneurial vision, and the unglamorous businesses that keep modern society functioning. Let's begin where all great business stories start: with an immigrant, a dream, and a single horse-drawn wagon.

II. The Pre-History: Harm Huizenga & The Early Days (1893–1968)

The year was 1893, the same year Chicago hosted the World's Columbian Exposition, showcasing America's emergence as an industrial power. While millions marveled at electric lights and the world's first Ferris wheel, a Dutch immigrant named Harm Huizenga saw opportunity in something far less glamorous: the growing piles of garbage accumulating in Chicago's rapidly expanding neighborhoods. Armed with little more than a wooden wagon, a tired horse, and an immigrant's determination, Harm began what would become one of America's great business dynasties.

Harm had arrived from the Netherlands with the wave of Dutch Reformed immigrants settling in the Midwest. Like many of his countrymen, he possessed what neighbors called "Dutch stubbornness"—a refusal to be outworked and an almost religious devotion to reliability. His business model was devastatingly simple: for $1.25 per wagon load, he would haul away whatever Chicago's residents and businesses didn't want. No contracts, no corporate structure, just a handshake and a promise to show up when he said he would.

The Chicago that Harm navigated was a city exploding with growth and garbage. The population had tripled between 1880 and 1890, reaching over one million residents. The Great Fire of 1871 had necessitated massive reconstruction, and with industrialization came waste—factory refuse, construction debris, household garbage, and the detritus of urban life. The city's approach to waste management was chaotic at best. Some neighborhoods had municipal collection, others relied on private haulers, and many simply dumped garbage in alleys or burned it in backyard incinerators.

Harm's genius wasn't in innovation—he was doing what hundreds of other immigrants were doing across American cities. His edge came from consistency and an almost obsessive focus on customer relationships. While other haulers might skip a pickup after a heavy night at the tavern, Harm's wagon appeared like clockwork. Dutch Reformed principles meant no work on Sundays, but Monday through Saturday, Chicago's North Side residents knew they could count on the Huizenga wagon.

By 1900, Harm had expanded to three wagons and brought his sons into the business. The family operation grew methodically, adding routes in Chicago's booming immigrant neighborhoods—Polish, Italian, Irish enclaves where small businesses needed reliable waste removal. The Huizengas developed an informal but sophisticated understanding of route density economics decades before any MBA would put a name to it. They learned that profit wasn't in the hauling; it was in the efficiency of the route. Ten stops on one block paid better than ten stops across ten blocks, even at the same price.

The business faced its first existential challenge in 1910 when Chicago implemented new sanitation ordinances requiring licensed haulers to meet specific standards. Many informal operators couldn't afford compliance. The Huizengas, who had been meticulously saving profits, purchased proper trucks, secured necessary permits, and watched as dozens of competitors disappeared overnight. It was an early lesson in the value of regulatory compliance as competitive advantage—a theme that would echo through the industry's entire history.

Through the 1920s, as Chicago became the hub of American commerce, the Huizenga operation evolved with it. They were among the first to recognize that commercial accounts—stores, restaurants, small factories—provided steadier revenue than residential pickups. A handwritten ledger from 1923, discovered decades later in a family attic, showed the company serving over 200 commercial accounts, each paying monthly fees ranging from $5 to $50. The math was compelling: one restaurant paying $30 monthly equaled twenty-four residential pickups.

The Depression tested every small business in America, and garbage hauling was no exception. Families couldn't afford pickup services; businesses closed by the dozens. But the Huizengas adapted with characteristic pragmatism. They began accepting payment in trade—hauling garbage for restaurants in exchange for meals, servicing grocery stores for produce. They survived while better-capitalized competitors folded, acquiring routes from failed haulers for pennies on the dollar.

World War II brought unexpected prosperity. With men heading overseas, labor was scarce, and those who remained could charge premium prices. The Huizengas also discovered a lucrative niche: military contracts. The rapid construction of training facilities around Chicago created mountains of construction waste, and the military paid promptly and in full—a rarity in the garbage business where collections could be as challenging as the physical work itself.

By 1950, the company had transitioned fully from horse-drawn wagons to a fleet of trucks. Harm's grandson Wayne, born in 1937, spent summers riding routes, learning the business from the ground up. Workers recalled Wayne as a teenager, wrestling garbage cans and charming customers with equal enthusiasm. He possessed something his grandfather recognized immediately: the rare combination of operational understanding and entrepreneurial vision.

The 1950s and early 1960s represented the golden age of independent garbage hauling. America's post-war suburban explosion created endless demand for waste services. Every new subdivision needed garbage collection, every new shopping center required dumpster service. The Huizenga company, now operating as "Southern Sanitation," had expanded beyond Chicago into surrounding suburbs. By 1965, they operated 20 trucks and served thousands of customers across Cook County.

But Wayne Huizenga saw what his family's ledgers couldn't capture: inefficiency at a massive scale. Across America, thousands of small operators duplicated efforts, drove overlapping routes, and lacked the capital for modern equipment or disposal facilities. In Chicago alone, over 200 independent haulers competed for business, often with multiple trucks serving the same street. Wayne would later describe driving through Cicero, Illinois, and counting seven different garbage trucks on a single block—"absolute insanity from an economic perspective."

The American waste landscape of the 1960s was indeed a study in fragmentation. No company controlled more than 1% of the national market. Disposal was haphazard—open dumps, burning, illegal dumping in wetlands. Environmental regulation was virtually nonexistent. Customer service meant showing up most of the time. Pricing was random, often based on personal relationships rather than economic logic. It was, in short, an industry begging for consolidation.

Wayne's vision extended beyond operational efficiency. He understood that Wall Street money could transform a fragmented industry, that professional management could replace handshake deals, that scale could create competitive advantages no family operation could match. But vision alone wouldn't suffice. He needed partners who understood both the operational complexities of garbage hauling and the financial engineering required for rapid scaling.

Enter Dean Buntrock, who ran a successful hauling operation in Oak Brook, Illinois, and Larry Beck, whose family operated routes on Chicago's South Side. The three men met in 1967 at an industry conference in Milwaukee. Over beers at a German restaurant, they discovered shared frustration with the industry's inefficiencies and mutual ambition to build something larger. Buntrock brought operational excellence, Beck contributed established commercial relationships, and Wayne provided the audacious vision.

By early 1968, the three had sketched out a plan on a restaurant napkin that would transform American waste management. They would use public market capital to rapidly acquire local haulers, integrate operations for efficiency, and create the industry's first national brand. The economics were compelling: most mom-and-pop operators would sell for 3-5 times earnings, while public markets would value an integrated company at 15-20 times. The arbitrage opportunity was massive.

The waste industry of 1968 looked nothing like today's consolidated market. It was characterized by thousands of small, family-owned businesses, minimal environmental oversight, and a complete absence of national players. Technology meant having trucks with hydraulic lifts. Environmental consciousness meant not dumping directly into Lake Michigan. This was the landscape Wayne Huizenga, Dean Buntrock, and Larry Beck surveyed as they prepared to launch Waste Management, Inc.

What happened next would transform not just their fortunes, but the entire structure of American waste services. The age of the independent hauler was ending; the era of corporate waste management was about to begin.

III. The Founding & Early Roll-Up Strategy (1968–1972)

Dean Buntrock's office in Oak Brook, Illinois, wasn't much to look at in March 1968—a converted farmhouse with drafty windows and floors that creaked with every step. But on March 11, around a table covered with coffee stains and acquisition targets mapped on index cards, three men formally incorporated what would become Waste Management, Inc. Wayne Huizenga signed with characteristic flourish, Dean Buntrock with the careful precision of an engineer, and Larry Beck with the casual confidence of someone who'd been making deals since childhood. The initial capitalization: $37,000 cobbled together from family savings and a second mortgage on Buntrock's house.

Their first acquisition closed within weeks—Acme Disposal of Milwaukee, purchased for $185,000 with $10,000 down and seller financing for the rest. The owner, nearing seventy and tired of fighting with the Teamsters, practically begged them to take over. It was a pattern they'd see repeated hundreds of times: aging owners, no succession plans, and an industry where a bad back meant the end of your career. Acme brought 3,000 residential customers and four trucks held together, as Wayne later joked, "by rust and prayer."

The integration playbook they developed with Acme became their template for the next 133 acquisitions. Step one: retain the previous owner for six months to ensure customer continuity. Step two: immediately upgrade equipment—nothing built confidence like new trucks with the bold yellow and black Waste Management logo. Step three: raise prices 10-15%, losing the unprofitable customers while improving margins on those who stayed. Step four: optimize routes using what Buntrock called "common sense geometry"—no more zigzagging across town because that's how old Joe had always done it.

By summer 1968, they'd completed six acquisitions and faced their first crisis. A seller in Pompano Beach, Florida, had allegedly misrepresented his customer count by 40%. Wayne flew down in a rage, ready to unwind the deal, but discovered something interesting: the Florida operation, though smaller than advertised, had exclusive municipal contracts worth three times what they'd paid. It was a lesson in hidden value that would guide future acquisitions—sometimes the asset wasn't what it seemed, but better.

The pace was relentless. Larry Beck spent 200 nights on the road in 1969, visiting targets, negotiating deals, and drinking bourbon with sellers who needed to trust you before they'd sell you their life's work. He developed a reputation as the closer—the guy who could convince a stubborn owner that selling to Waste Management meant preserving their legacy, not destroying it. His standard pitch: "You built something remarkable. We want to make it part of something bigger, not tear it down."

The numbers tell only part of the story. By December 1969, they'd completed 43 acquisitions across nine states, but behind each deal was drama. There was the Memphis operator who demanded payment in gold coins, convinced paper money would soon be worthless. The Dallas company that came with a fleet of trucks and, unexpectedly, a lawsuit from the EPA for illegal dumping. The Phoenix acquisition where they discovered the seller's son had been skimming cash for years, making the actual profits 50% higher than reported.

Going public changed everything. The IPO on May 10, 1971, raised $6 million at $16 per share, valuing the company at $22 million. Wayne remembered standing on the floor of the New York Stock Exchange, watching as "WMX" appeared on the ticker for the first time. A garbage company was now trading alongside General Motors and IBM. The symbolism wasn't lost on him—waste management was becoming a real industry, not just a collection of local services.

Public capital accelerated their acquisition machine. They developed what employees called the "Waste Management Formula": identify the leading hauler in a mid-sized market, offer 4-5 times trailing earnings (when the seller expected 2-3 times), pay 20% cash and 80% in WM stock, and promise to keep the seller's employees. The stock component was genius—sellers became shareholders, invested in the company's continued success.

The integration challenges were immense. Each acquired company had different trucks, different accounting systems, different relationships with unions. In Akron, they inherited a handshake agreement with the Teamsters that no one had documented. In Birmingham, the previous owner's wife had been keeping books in a system only she understood—and she refused to explain it after the sale. In Portland, they discovered their new acquisition had been illegally dumping in the Columbia River Gorge, requiring expensive cleanup.

But for every problem, they found opportunities. Route density became their obsession. Buntrock developed a metric he called "revenue per route mile"—simply put, how much money did each mile of driving generate? By combining overlapping routes from acquired companies, they often doubled this metric within six months. A Chicago neighborhood that required three trucks from three different companies could be served by one WM truck, dramatically reducing costs. The operational playbook became their competitive moat. By 1972, the company had made 133 acquisitions with $82 million in revenue, but the real achievement was standardizing chaos. Each market had different regulations, different unions, different disposal methods. Buntrock created what he called the "integration matrix"—a 90-day plan that transformed acquired companies into Waste Management operations. Day 1-30: financial integration and route analysis. Day 31-60: equipment standardization and employee training. Day 61-90: customer communication and price adjustments.

The company had 60,000 commercial and industrial accounts and 600,000 residential customers in 19 states and the provinces of Ontario and Quebec. This geographic spread created unexpected challenges. In Quebec, they had to navigate French-language requirements and different union structures. In Texas, they discovered that what worked in Chicago's dense neighborhoods failed in Houston's sprawling subdivisions. Each market required subtle adaptations while maintaining overall standardization.

The human element proved crucial. Wayne instituted what he called "millionaire makers"—promising key employees in acquired companies that if they stayed and hit targets, their WM stock would make them wealthy. It worked. By late 1972, over 100 former owners and managers of acquired companies had become millionaires through stock appreciation. This created a powerful network effect: sellers would call other owners, evangelizing the benefits of joining Waste Management.

Technology, primitive by today's standards, gave them an edge. They were among the first to use computer systems for route optimization, installing an IBM System/360 in their Oak Brook headquarters. The computer, which cost more than most of their acquisitions, could calculate optimal routes for hundreds of trucks across multiple markets. Competitors still relied on drivers who'd memorized routes over decades.

The company's culture balanced entrepreneurial aggression with operational discipline. Monday morning meetings in Oak Brook became legendary for their intensity. Wayne would grill managers about every metric—tons collected per truck, gallons of fuel per mile, customer complaints per thousand accounts. But Friday afternoons were for celebrating wins, with champagne toasts for successful acquisitions and bonuses distributed in cash-filled envelopes.

Labor relations required delicate handling. The Teamsters controlled garbage collection in most major cities, and they didn't initially trust these corporate types from Oak Brook. Larry Beck spent countless hours in union halls, drinking beer with shop stewards, convincing them that Waste Management's growth meant more jobs, better equipment, and steadier employment. His promise: "We're not here to break unions; we're here to build a company where union workers want to work."

By the end of 1972, patterns had emerged that would define the industry for decades. First, scale created insurmountable advantages—larger companies could afford better equipment, offer lower prices through efficiency, and spread regulatory compliance costs across more revenue. Second, disposal assets (landfills and transfer stations) were more valuable than collection routes. Third, the combination of collection and disposal created a vertically integrated model competitors couldn't match.

The speed of transformation was breathtaking. In just four years, three entrepreneurs had aggregated what took individual families generations to build. They'd proven that professional management could transform a fragmented, unsophisticated industry into a modern corporation. Wall Street took notice—WM stock had tripled since the IPO, and analysts were beginning to understand the predictable, recession-resistant nature of waste management.

But success bred challenges. Competitors began copying their playbook. Browning-Ferris Industries (BFI), based in Houston, went public in 1970 and started its own aggressive acquisition campaign. Smaller operators formed alliances to resist takeover attempts. Environmental regulations, virtually nonexistent when they started, began tightening. The easy acquisitions—willing sellers at reasonable prices—were becoming scarce.

As 1972 ended, Wayne, Dean, and Larry faced a strategic inflection point. They'd proven the roll-up strategy worked, but maintaining growth would require bigger deals, more capital, and navigation of increasingly complex regulatory environments. The scrappy startup phase was over; the challenge now was building a sustainable corporation while maintaining entrepreneurial energy. The foundation was solid, but the real test of their vision lay ahead.

IV. The SCA Acquisition & Becoming #1 (1980s)

The morning of August 13, 1984, found Dean Buntrock pacing his Oak Brook office, staring at a simple equation scrawled on his whiteboard: "WM + SCA = ?" For seven years, Service Corporation of America had been their white whale—the acquisition that would definitively crown Waste Management as the undisputed king of garbage. Now, after multiple rejected offers and heated boardroom battles, they were hours away from announcing a deal that would reshape the industry forever.

SCA had grown to become the third largest waste hauler amidst all this internal turmoil. Its territory stretched from Boston, Massachusetts, all the way to California. By 1976, the company's sales were $660,000,000, including all of its subsidiaries. SCA's fleet of garbage trucks had swelled to 1,800 in 90 cities. It had 39 landfills, 100 municipal contracts, 110,000 commercial accounts and 100,000 dumpsters. The prize was massive, but it came with baggage—literally and figuratively.

The dance between WM and SCA had begun in 1977 when Buntrock first approached SCA's controversial president, Tom Viola, with an all-stock merger proposal. SCA had rejected an offer by Waste Management in 1977, and this was no different. What would have amounted to an $210 million deal, was rejected by the company. Viola, whose connections to organized crime in New Jersey were an open secret in the industry, dismissed the offer with characteristic bravado: "We don't need Wayne Huizenga's charity."

But by 1984, SCA was hemorrhaging cash and credibility. The company's criminal connections would become known after the murder of several independent contractors who had challenged SCA in New Jersey. Immediately afterwards, the towns reverted to SCA's services. In response to these accusations, SCA tried to dispose of all of its New Jersey operations, but couldn't find a buyer. Environmental disasters piled up like the waste in their landfills. One of these dumps in Niagara Falls, New York, near the infamous Love Canal site, became a local terror. Lagoons of industrial waste would emerge during rainstorms, and highway officials reported of numerous explosions and fires.

The breakthrough came through an unlikely partnership. Waste Management joined forces with Genstar Corporation, a San Francisco-based conglomerate, to structure a deal that would satisfy antitrust regulators while giving WM control of SCA's crown jewels. The transaction, based on shares outstanding as of June 30, is $423.2 million. Under a separate agreement, Waste Management agreed to initially shoulder 60 percent of the cost of acquiring SCA, with Genstar picking up the remaining 40 percent. WMAC will begin a tender offer for all outstanding shares of SCA common stock for $28.50 per share in cash. Final allocation of cost will be determined on the basis of the value of the businesses distributed.

The structure was financial engineering at its finest. Waste Management will take over SCA properties that do not face antitrust problems. Genstar will take over the remaining facilities. This allowed WM to cherry-pick the best assets while avoiding regulatory scrutiny in markets where the combined company would have monopolistic control.

Most significant among its many acquisitions was the 1984 purchase of 60% of SCA Services, Inc., a Boston-based company ranking third in the waste-treatment industry. The purchase added about $200 million to WMI's $1 billion revenue, opening up 43 markets for the parent company and increasing its total number of landfills to 89. The math was staggering—overnight, Waste Management's landfill capacity increased by 40%, its commercial accounts grew by 25%, and its geographic footprint expanded into lucrative Northeast markets they'd struggled to penetrate.

But the SCA acquisition was merely the capstone of a decade of strategic brilliance. By 1982, the company had become the world's largest waste disposal company, surpassing $1 billion in sales. This milestone—crossing the billion-dollar threshold—had symbolic importance that transcended finance. It meant Wall Street finally took the garbage business seriously.

The path to dominance hadn't been smooth. Throughout the early 1980s, Waste Management battled its Houston-based rival, Browning-Ferris Industries (BFI), in what industry insiders called "the garbage wars." Both companies pursued the same strategy: acquire local haulers, integrate operations, raise prices. The competition was fierce but rational—neither company engaged in predatory pricing that would destroy industry economics.

Wayne Huizenga, who'd stepped back from day-to-day operations but remained on the board, described the dynamic: "BFI kept us honest. Every acquisition we didn't make, they did. Every market we entered, they followed. It was like playing three-dimensional chess against an opponent who knew all your moves."

The companies developed an unspoken détente in certain markets. In Houston, BFI's backyard, Waste Management competed but didn't aggressively undercut pricing. In Chicago, WM's territory, BFI maintained a presence but focused on commercial rather than residential accounts. This rational competition allowed both companies to maintain healthy margins while consolidating the industry.

International expansion added another dimension to WM's growth. By 1985, the company operated in Saudi Arabia (handling waste from oil installations), Argentina (Buenos Aires municipal contracts), and Australia (industrial waste management). Each international venture taught valuable lessons. In Saudi Arabia, they learned to operate in extreme heat that could melt truck tires. In Argentina, they navigated hyperinflation that made monthly contracts worthless. In Australia, they discovered that environmental regulations could be even stricter than in the U.S.

The company's Chemical Waste Management subsidiary, established in 1975, had quietly become the nation's largest handler of hazardous waste. Under a three-quarter-owned subsidiary, Chemical Waste Management, Inc., WMI rapidly enlarged its presence in the toxic field, acquiring a number of the largest toxic landfills and by 1980 emerging as the industry leader. As they had demonstrated in founding WMI in 1968, Buntrock and Huizenga displayed remarkable foresight in thus plunging into the hazardous-waste business. Rapidly increasing public fears about all forms of toxic waste soon made it extremely difficult to gain approval for new landfills, which in turn drove up the market value of existing sites, many of them in the hands of Chemical Waste Management by the early 1980s.

The hazardous waste business operated on different economics than traditional garbage. Disposal fees could reach $500 per ton versus $20 for regular waste. Regulatory compliance costs were astronomical, but so were the barriers to entry. By 1985, Chemical Waste Management controlled 40% of the U.S. hazardous waste disposal capacity, generating margins that exceeded 40%.

Technology investments, often overlooked in narratives about the company's growth, provided crucial competitive advantages. WM pioneered the use of satellite tracking for truck fleets, allowing real-time route optimization. They developed proprietary landfill engineering techniques that increased capacity by 30% without expanding acreage. Their laboratories could analyze waste composition in hours rather than days, crucial for hazardous materials handling.

The corporate culture evolved dramatically during this period. The scrappy entrepreneurialism of the 1970s gave way to professional management. Harvard MBAs joined former garbage truck drivers in Oak Brook headquarters. The company recruited executives from oil companies, chemical manufacturers, and management consulting firms. This cultural transformation created tension—old-timers complained about "corporate types who'd never picked up a garbage can"—but it was necessary for managing a billion-dollar enterprise.

Environmental opposition intensified as WM grew larger. While such moves had not satisfied critics such as Greenpeace International, it appeared that WMI learned a lesson from its legal battles and took some pains to adopt more safety measures. As proof of its progress in these areas, WMI can point to the long-term contracts it won in the late 1980s to handle much of the waste from Portland, Oregon; and Seattle, Washington; two cities known for their strong environmental commitment. The Portland and Seattle contracts were particularly significant—if environmentally conscious Pacific Northwest cities trusted WM, it validated their claims of responsible operations.

By 1985, Waste Management's transformation was complete. From three entrepreneurs with a handful of trucks, they'd built North America's first national waste management company. They controlled the entire waste stream—from collection to disposal to treatment. They'd proven that professional management could transform a fragmented, unsophisticated industry into a modern, profitable enterprise.

'Together, Waste Management and SCA will be stronger both financially and operationally,' said Dean Buntrock, chairman of Waste Management. His words at the SCA acquisition announcement proved prophetic, but not in the way he intended. The company was indeed stronger, but the rapid growth and aggressive accounting that fueled their rise would soon threaten to destroy everything they'd built.

V. The Accounting Scandal & Near-Death Experience (1997–1999)

The call came at 3 AM on a February morning in 1998. Phillip Rooney, Waste Management's president, was jolted awake by his general counsel: "Phil, the Wall Street Journal has the story. They're running it tomorrow. Everything." Within hours, one of corporate America's most spectacular accounting frauds would be exposed, threatening to destroy the empire Wayne Huizenga, Dean Buntrock, and Larry Beck had spent three decades building.

When a new CEO took charge of the company in 1997, he ordered a review of the company's accounting practices in 1997. In 1998 Waste Management restated its 1992–1997 earnings by $1.7 billion, making it the largest restatement in history. The numbers were staggering, but the human drama behind them was even more compelling—a story of gradual moral compromise, willful blindness, and the corruption of corporate culture.

The roots of the scandal traced back to the early 1990s when Waste Management's spectacular growth began to slow. The easy acquisitions were gone. Environmental regulations had tightened. Competition from BFI and emerging players had intensified. For the first time in the company's history, meeting Wall Street's quarterly expectations became a struggle.

Dean Buntrock, who'd risen from running his father-in-law's small hauling company to CEO of a Fortune 500 corporation, couldn't accept slowing growth. In management meetings, he'd pound the table: "We've never missed a quarter. We're not starting now." The pressure cascaded down through the organization like toxic waste seeping through soil.

The fraud began small, almost innocently. began "cooking" the accounting books by refusing to record expenses necessary to write off the costs of unsuccessful and abandoned landfill development projects; establishing inflated environmental reserves (liabilities) in connection with acquisitions so that the excess reserves could be used to avoid recording unrelated operating expenses, improperly capitalizing a variety of expenses; failing to establish sufficient reserves (liabilities) to pay for income taxes and other expenses; avoiding depreciation expenses on their garbage trucks by both assigning unsupported and inflating salvage values and extending their useful lives; assigned arbitrary salvage values to other assets that previously had no salvage value; failed to record expenses for decreases in the value of landfills as they were filled with waste.

Thomas Hau, the Chief Accounting Officer, was the architect of many schemes. A former Arthur Andersen partner who'd audited Waste Management before joining the company, Hau knew exactly how to manipulate the numbers to fool auditors—or so he thought. He'd extend depreciation schedules on garbage trucks from 5 years to 8 years, instantly reducing expenses by millions. When trucks were obviously worthless, he'd assign them "salvage values" that kept them on the books as assets.

The landfill accounting was particularly creative. As landfills filled with garbage, their value should decrease—simple logic. But Hau's team would argue that each ton of waste actually increased the landfill's value because it brought them closer to closure and redevelopment. It was accounting alchemy, turning liabilities into assets with the stroke of a pen.

The company went public in 1971 and by 1972, the company was generating about $82 million in revenue and had made 133 acquisitions. The company offered environmental services to almost 20 million customers in America, Canada, and Puerto Rico. But by the 1990s, that rapid growth had created a byzantine corporate structure that made fraud easier to hide. Hundreds of subsidiaries, thousands of properties, millions of transactions—the complexity overwhelmed even sophisticated auditors.

The relationship with Arthur Andersen was thoroughly corrupted. James Koeing, who was the CFO of Waste Management, Inc., was trained at Arthur Andersen as an auditor. Thomas Hau, who was the CAO of Waste Management, Inc., was trained at Arthur Andersen as an auditor, was a partner there for 30 years, was the engagement partner for the Waste Management, Inc. audit, and was the head of the Arthur Andersen audit division for the Waste Management, Inc. account. Bruce D. Tobecksen, who was the Vice President of Finance at Waste Management, Inc., was the audit manager of the Waste Management, Inc. audit and others at Arthur Andersen. These important chief officers at Waste Management, Inc. all came from Arthur Andersen.

This incestuous relationship created a fatal conflict of interest. Arthur Andersen found errors in Waste Management, Inc.'s accounting books and would come up with adjustments and methods in which they could be fixed; however, the Waste Management Inc. officers refused to make those adjustments that Arthur Andersen proposed. In order for the fraudsters to cover their tracks, the stakeholders bribed Arthur Andersen by telling them that they would receive additional fees outside of the agreement that they originally had made. Arthur Andersen, in turn, issued unqualified opinions in the audit report for Waste Management, Inc. and wrote off the accounting errors over time in order to conceal the fraud.

The "special fees" to Arthur Andersen were staggering. Beyond their $7.5 million annual audit fee, Andersen received $11.8 million in consulting fees, $6 million for "special projects," and millions more in undocumented payments. It was legalized bribery, buying clean audit opinions with shareholder money.

The reason why the Waste Management, Inc. 1998 scandal occurred was in an attempt to meet predetermined earnings targets by expanding profits and pushing down or foregoing expenses. Revenues were not increasing as fast as they should have been. The chief officers recognized this and began to commit fraudulent activities as aforementioned in order for their financial statements to state what they wanted them to state. In a company such as Waste Management, Inc., officer compensation is tied to the earnings that the company produces. If Waste Management, Inc. were to struggle in falling short of their earnings target, it would endanger the officers of the company. The stakeholders, in turn, looked to committing fraud in order to protect their own lives. Compensation tied to earnings brings about a major culture of fraud in any occupational environment.

Dean Buntrock personally benefited enormously from the fraud. The individual who reaped the benefits from the waste management fraud is Dean Buntrock. The Securities and Exchange Commission (SEC) estimates that Buntrock amassed over $17 million through various means, including performance-based bonuses, retirement benefits, charitable contributions, and the sale of company stock, all while the fraud was unfolding. One particularly egregious instance of Buntrock's self-serving behavior was his manipulation of tax benefits by donating inflated company stock to his former college, ultimately funding a building named in his honor. This scheme not only allowed Buntrock to evade taxes but also perpetuated a facade of philanthropy, masking his true motives of personal enrichment.

The fraud began unraveling in 1997 when the board, under pressure from institutional investors, brought in a new CEO from outside the company. The new chief executive, suspicious of the too-good-to-be-true numbers, ordered an independent review of the company's accounting practices. What they found shocked even the forensic accountants.

On November 14, 1997, the company reclassified or adjusted certain items in its financial statements for 1996 and the first nine months of 1997. On August 3, 1999, the company would have to restate first-quarter results downward, partly because of changes in the value of landfills and other assets in connection with its acquisition last year of Wheelabrator Technologies Inc.

The public revelation was devastating. Revelations of irregular accounting led to a major drop in stock price and to the replacement of top executives after a new CEO ordered a review of the company's accounting practices in 1998. Waste Management's shareholders lost more than $6 billion in the market value of their investments when the stock price plummeted by more than 33%. In a single day, the company lost more market value than most garbage companies were worth in total.

The legal aftermath was swift and severe. On July 8, 1999, a class action lawsuit was filed against WMI and certain officers for issuing false statements. Waste Management paid US$457 million to settle a shareholder class-action suit in 2003. The SEC fined Waste Management's independent auditor, Arthur Andersen, US$7 million for its role. Dean Buntrock was personally fined $20 million and banned from ever serving as an officer or director of a public company. Other executives faced similar sanctions.

The human toll extended beyond financial penalties. Longtime employees watched their retirement savings evaporate as WM stock collapsed. Customers questioned whether a company that couldn't manage its own books could be trusted with hazardous waste. Competitors circled like vultures, poaching clients and employees from the wounded giant.

Inside the Oak Brook headquarters, the atmosphere was funereal. Employees described walking through "halls of shame," passing empty offices of fired executives. The cafeteria, once buzzing with acquisition celebrations, fell silent. Security guards were posted to prevent document destruction. FBI agents interviewed hundreds of employees.

The company teetered on the edge of bankruptcy. Banks threatened to call loans. Bondholders demanded immediate repayment. Major customers canceled contracts. Several municipalities threatened to ban Waste Management from bidding on future work. The company that had once seemed invincible was days away from collapse.

In November 1999, turn-around CE was brought in to help Waste Management recover. The turnaround specialist faced an almost impossible task: restore credibility, restructure operations, and somehow convince stakeholders that a company built on fraud could be trusted again.

But perhaps the most tragic aspect was how unnecessary it all was. Waste Management's core business remained strong. Their trucks still collected garbage. Their landfills still operated. Their recycling facilities still processed materials. The fraud hadn't been needed to run a profitable business—it had been perpetrated solely to maintain an unsustainable growth narrative.

The scandal would forever change corporate America's approach to accounting oversight. It predated Enron but presaged many of the same issues: aggressive accounting, complicit auditors, executives enriching themselves at shareholders' expense. The Waste Management fraud became a Harvard Business School case study in how good companies go bad.

For the waste management industry, the scandal had a silver lining. It forced professionalization of financial reporting across the sector. Competitors who might have been tempted by similar schemes saw the devastating consequences. Environmental regulations tightened, but so did financial oversight.

As 1999 ended, Waste Management faced an existential question: Could a company so thoroughly corrupted by fraud be salvaged? The answer would come from an unexpected source—their fiercest competitor would become their salvation.

VI. The USA Waste Merger & Rebirth (1998–2000s)

John Drury sat in his Houston office on a sweltering July day in 1998, staring at a proposal that would have seemed like fantasy just months earlier. The CEO of USA Waste Services, a company one-third the size of Waste Management, was about to swallow the industry giant whole. It was a minnow eating a whale, made possible only because the whale was dying from self-inflicted wounds.

In 1998 Waste Management merged with USA Waste Services, Inc. USA Waste Services CEO John E. Drury retained the chairmanship and CEO position of the combined company. Waste Management then relocated its headquarters from Chicago to Houston. The merged company retained the Waste Management brand. But calling it a "merger" was corporate euphemism—this was a rescue mission disguised as a combination of equals.

USA Waste had been founded in 1987 by Don Moorehead and others who saw opportunity in the chaos following the 1980s leveraged buyout boom. They'd quietly assembled a collection of distressed assets, turned around failing operations, and built a reputation for operational excellence without the financial engineering that had corrupted Waste Management. By 1997, USA Waste generated $3.2 billion in revenue with margins that made Wall Street salivate.

The initial merger discussions were surreal. Drury recalled the first meeting: "Here I was, sitting across from executives of the company we'd all grown up idolizing, and they were begging us to save them. It was like watching Michael Jordan ask a high school coach for playing time."

The deal structure was complex but clever. Technically, USA Waste would acquire Waste Management for $13.3 billion in stock, but the combined company would keep the Waste Management name—the brand still had value despite the scandal. USA Waste shareholders would own 60% of the combined entity, despite contributing only 35% of the revenue. It was a tacit acknowledgment of which company was truly healthy.

Integration planning began immediately, but the cultural clash was severe. Waste Management employees, even those untainted by scandal, carried the stench of corporate failure. USA Waste employees, proud of their scrappy underdog status, viewed their new colleagues with barely concealed contempt. In the Houston headquarters, former USA Waste and legacy Waste Management employees literally sat on opposite sides of the cafeteria.

Drury's first all-hands meeting set the tone for integration. Standing before 500 employees in Houston, he was blunt: "The old Waste Management is dead. The fraud, the old boys' network, the Chicago way of doing business—all dead. We're building something new, and if you're not on board, there's the door." Seventeen executives resigned that day.

The operational integration was a nightmare of complexity. Two companies with incompatible IT systems, different truck specifications, overlapping routes, and conflicting union contracts had to become one. In markets where both companies operated, they had to eliminate redundancy without triggering antitrust concerns. Some cities had USA Waste collecting on Monday, Wednesday, Friday and Waste Management on Tuesday, Thursday, Saturday—the same street served by different companies that were now one.

Route optimization alone took eighteen months. Engineers worked around the clock, mapping every stop, measuring every mile, timing every pickup. In Denver, they discovered that combining routes could eliminate 40 trucks and save $3 million annually. Multiplied across hundreds of markets, the synergies were massive—but so was the human cost. Thousand of drivers lost their jobs.

The financial cleanup was equally daunting. Forensic accountants discovered fraudulent accounting tentacles reaching into every corner of the business. Landfills valued at $100 million were worth $40 million. Trucks supposedly worth $10 million were scrap metal. Contracts reported as profitable were actually losing money. Each revelation required painful writedowns and explanations to increasingly skeptical investors.

In late 1999, John Drury stepped down as chairman due to brain surgery. Rodney R. Proto then took the position of chairman and CEO. That year also brought trouble for the newly expanded company in the form of an accounting scandal. Drury's sudden departure due to health issues created a leadership vacuum at the worst possible moment. The company needed steady leadership, but instead got musical chairs in the C-suite.

Rodney Proto, Drury's successor, lacked his predecessor's commanding presence. A career waste executive who'd risen through USA Waste, Proto was competent but uninspiring. His town halls felt like funeral services. His strategy presentations put board members to sleep. At a time when Waste Management needed a visionary leader, they got a caretaker.

The company has since implemented new technologies, safety standards, and operational practices. The operational improvements were real but unglamorous. New GPS systems tracked every truck in real-time. Automated arm trucks replaced manual collection, reducing injury rates by 60%. Maintenance schedules were standardized across the fleet. Safety training became mandatory, not optional. These weren't innovations that made headlines, but they slowly rebuilt the company's operational credibility.

Customer retention became an obsession. Every lost account was scrutinized. Sales teams were deployed to visit every major customer, essentially apologizing for the scandal while promising better service. In many cases, they had to accept lower prices just to keep the business. The company that once raised prices at will now begged customers not to leave.

The municipal market was particularly challenging. City councils debated in public sessions whether to trust Waste Management with their contracts. In Seattle, activists showed up with signs reading "Criminals Out of Our Garbage." In Philadelphia, the city council held three hearings before reluctantly renewing WM's contract—with a 20% price reduction and quarterly audits.

Wall Street remained skeptical. Despite operational improvements, WM stock languished below $20, less than half its pre-scandal peak. Analysts questioned whether the company could ever restore margins to historical levels. Short sellers circled, betting on continued decline. Credit rating agencies maintained junk status on WM bonds, making capital expensive.

But gradually, quarter by quarter, the fundamentals improved. On-time pickup rates increased from 94% to 98%. Customer complaints fell by 40%. Safety incidents declined by half. Employee turnover, which had spiked to 30% during the scandal, normalized to industry averages. The blocking and tackling of garbage collection slowly restored confidence.

Technology investments, delayed during the crisis, resumed with vengeance. The company spent $500 million on new fleet management systems, customer service platforms, and landfill monitoring technology. They hired CTOs from tech companies, not just waste industry veterans. Digital transformation became a strategic priority, not an afterthought.

The cultural transformation was perhaps most significant. The old Waste Management culture—aggressive, growth-at-any-cost, ethically flexible—was systematically dismantled. New values were institutionalized: "Integrity First," "Customers Always," "Safety Above All." Ethics training became mandatory. Whistleblower hotlines were established. Financial controls were strengthened to the point of paranoia.

By 2003, the transformation was largely complete. The company that had nearly collapsed was now generating steady profits, winning back customers, and slowly rebuilding its reputation. Revenue reached $11.6 billion with legitimate earnings. The stock recovered to $30. Credit ratings returned to investment grade.

The Waste Management that emerged from this crucible was fundamentally different from the one Wayne Huizenga and Dean Buntrock had built. It was more professional but less entrepreneurial, more compliant but less aggressive, more stable but less exciting. The cowboys who'd consolidated the industry had been replaced by professional managers who colored inside the lines.

Yet the company had survived what should have been a fatal blow. The merger with USA Waste, painful as it was, had provided the leadership, capital, and credibility needed for resurrection. The headquarters move to Houston symbolically severed ties with the corrupt Chicago past. The company that had defined corporate fraud in the 1990s would become a model of operational excellence in the 2000s.

As one longtime employee reflected: "We went from being the company everyone wanted to be, to the company everyone pitied, to the company everyone respected for surviving. It wasn't the journey we planned, but we made it." The scars remained, but Waste Management was ready to write its next chapter.

VII. The Failed Republic Services Pursuit (2008)

David Steiner's knuckles were white as he gripped the podium on the morning of July 14, 2008. The Waste Management CEO was about to announce the boldest move in the industry's history: an unsolicited, all-cash bid to acquire arch-rival Republic Services for $34 per share—a transaction valued at $14.8 billion. As he looked out at the assembled press, Steiner knew he was either about to create an unstoppable industry juggernaut or trigger a corporate war that would consume both companies.

On July 14, 2008, Waste Management offered a $34 per share all-cash bid to acquire arch-competitor Republic Services, Inc. On August 11, 2008, the bid was raised to $37 per share. The timing seemed perfect. The financial crisis was just beginning to bite, credit markets were tightening, and Republic's stock had fallen 20% from its peak. Steiner believed Republic's board would have no choice but to consider an offer representing a 22% premium to the closing price.

The strategic rationale was compelling. Combined, Waste Management and Republic would control 65% of the U.S. waste disposal market. The synergies were mouthwatering—$500 million in annual cost savings from eliminating duplicate routes, combining disposal networks, and leveraging procurement scale. Investment bankers at Goldman Sachs had run the numbers dozens of times; the math always worked.

But Steiner had underestimated James O'Connor, Republic's CEO. O'Connor, a former accountant who'd risen through the ranks of Republic's predecessor companies, viewed the offer as opportunistic and insulting. In a hastily convened board meeting in Phoenix, he rallied his directors: "They think we're weak. They think the crisis gives them leverage. We'll show them what Republic Services is made of."

Republic's response was swift and devastating. Within 48 hours, they announced their own blockbuster deal: a merger with Allied Waste Industries, the industry's third-largest player. The $11.8 billion transaction would create a company nearly equal in size to Waste Management, effectively blocking WM's takeover attempt while creating a formidable competitor.

The Allied deal was a masterpiece of defensive strategy. Republic and Allied had been in quiet merger discussions for months, but WM's hostile bid accelerated everything. O'Connor and Allied CEO John Zillmer worked through the night, their lawyers drafting merger agreements in a Phoenix conference room while Waste Management's bankers waited for a response that would never come.

Steiner was furious. At a emergency board meeting in Houston, he pounded the table: "They'd rather destroy value with Allied than create value with us. It's corporate ego over shareholder interests." The board authorized a raised bid—$37 per share, taking the total value to $15.4 billion. It was an extraordinary price, 50% above where Republic had traded just six months earlier.

The public relations battle was fierce. Waste Management took out full-page ads in the Wall Street Journal and USA Today, appealing directly to Republic shareholders. The headline was blunt: "Your Board is Denying You a 50% Premium." Republic countered with their own campaign, emphasizing the strategic benefits of the Allied merger and questioning whether WM could even finance their bid given the deteriorating credit markets.

Behind the scenes, the financial engineering was complex. Waste Management had arranged $17 billion in committed financing from a consortium of banks led by JPMorgan and Bank of America. But as Lehman Brothers collapsed in September and credit markets froze, those commitments looked increasingly shaky. Banks that had eagerly offered billions in July were now questioning whether they could fund anything.

The regulatory battle added another dimension. Waste Management hired an army of antitrust lawyers to argue that a WM-Republic combination would face minimal regulatory issues. Republic's lawyers countered that the combined company would face years of scrutiny and forced divestitures. They produced maps showing markets where the combined company would have 80% or even 90% market share.

On August 15, 2008, Republic Services, Inc. denied Waste Management's bid for a second time. On October 13, 2008, Waste Management withdrew its bid for Republic Services, citing financial market turmoil. The October withdrawal was particularly painful. Lehman had collapsed, AIG had been bailed out, and credit markets had essentially ceased functioning. Even if Republic had accepted the offer, financing $15 billion was now impossible.

The internal post-mortem at Waste Management was brutal. Some board members questioned whether pursuing a hostile takeover during a financial crisis showed poor judgment. Others argued they should have moved faster, before Republic could arrange the Allied defense. The investment banking fees alone—$45 million to Goldman Sachs and other advisors—were a bitter pill for a failed transaction.

But the failed pursuit had unintended consequences that would prove valuable. First, it forced Waste Management to articulate a clear strategic vision beyond simple consolidation. The presentation materials prepared for Republic shareholders became the blueprint for WM's next decade of growth. Second, it identified operational weaknesses that needed addressing—Republic's superior technology and customer service metrics were eye-opening.

The Republic-Allied merger, completed in December 2008, created exactly the competitor Waste Management had feared. The new Republic Services, with $9 billion in revenue and 35,000 employees, was a formidable rival. O'Connor's integration of Allied was masterful, achieving $200 million in synergies within 18 months. The company Waste Management had tried to buy was now its most dangerous competitor.

The industry dynamics shifted dramatically. The cozy duopoly of the early 2000s, where Waste Management and Republic Services rationally competed, evolved into genuine rivalry. Pricing became more aggressive. Competition for municipal contracts intensified. Both companies accelerated technology investments to gain competitive advantage.

For David Steiner, the failed acquisition became a defining moment. Rather than dwelling on the loss, he pivoted Waste Management's strategy toward organic growth and operational excellence. "If we can't buy growth, we'll build it," he told employees. Capital that would have funded the Republic acquisition was redirected toward recycling infrastructure, renewable energy projects, and fleet modernization.

The financial crisis that killed the Republic deal created other opportunities. Dozens of smaller waste companies, starved of credit, became acquisition targets at distressed prices. Waste Management spent $1.8 billion on tuck-in acquisitions from 2009-2011, buying assets that Republic, distracted by Allied integration, couldn't pursue. The collection of smaller deals ultimately created more value than one mega-merger might have.

The failed Republic pursuit also catalyzed a cultural shift at Waste Management. The company had always been acquisitive, dating back to Wayne Huizenga's roll-up strategy. But the Republic rejection forced introspection about organic growth, innovation, and operational excellence. Engineers and operators, not just dealmakers, became corporate heroes.

Technology became a particular focus. Stung by Republic's superior customer service platforms, Waste Management invested $500 million in digital transformation. They built customer portals, mobile apps, and automated billing systems. Route optimization software, using machine learning algorithms, reduced miles driven by 15% while improving on-time performance.

The environmental services pivot accelerated. Unable to grow through mega-mergers, Waste Management doubled down on sustainability. They positioned themselves not as garbage haulers but as environmental solution providers. Renewable energy from landfill gas, advanced recycling technologies, and organic waste processing became strategic priorities rather than side businesses.

By 2010, the wisdom of the failed pursuit was debatable. Waste Management had avoided overpaying for an acquisition at the market peak. They'd been forced to improve operations rather than rely on financial engineering. The company that emerged from the failed Republic bid was leaner, more innovative, and more focused than the one that had launched it.

Yet questions lingered. Had Waste Management missed its last chance for transformative consolidation? Would the industry now remain split between two giants forever locked in combat? Could organic growth and operational improvement really replace the acquisition machine that had built the company?

As one board member reflected years later: "Not getting Republic was either the best thing that ever happened to us, or the worst. Maybe both." The failed pursuit had closed one chapter of Waste Management's history—the era of industry consolidation through mega-mergers—and opened another focused on transformation and sustainability.

VIII. The Transformation Era: From Waste to Sustainability (2010s–2020s)

Jim Fish stood before a crowd of investors at the 2022 Investor Day in Houston, holding up a simple black rectangle—the company's new logo. Gone was "Waste Management" spelled out in full. In its place: simply "WM" in bold, modern typeface. "We're not just managing waste anymore," Fish declared. "We're managing resources, energy, and the future of sustainability."

In February 2022, Waste Management CEO Jim Fish announced that the company would officially shorten its trade name to "WM" as part of a rebranding to emphasize its growing focus on sustainability and environmental services, including compressed natural gas and landfill gas utilization. The rebrand was more than cosmetic—it represented a fundamental reimagining of what a waste company could be in the 21st century.

The transformation had been building for years. In 2010, when David Steiner remained CEO, Waste Management's landfills were still seen primarily as holes in the ground where garbage went to die. By 2020, those same landfills had become renewable energy generators, producing enough electricity to power 580,000 homes annually through methane capture. The shift from liability to asset was revolutionary.

The economics of renewable natural gas (RNG) were compelling. Landfills naturally produce methane as organic waste decomposes—traditionally seen as a problem requiring expensive mitigation. But with natural gas prices rising and renewable energy credits available, that methane became liquid gold. WM invested $2.8 billion between 2015 and 2023 in RNG infrastructure, building processing plants that turned landfill gas into pipeline-quality fuel.

The company's network includes 337 transfer stations, 254 active landfill disposal sites, 97 recycling plants, 135 beneficial-use landfill gas projects and six independent power production plants. With 26,000 collection and transfer vehicles, WM has the largest trucking fleet in the waste industry. This massive infrastructure network became the backbone of their sustainability transformation.

The recycling business underwent its own revolution. For decades, recycling had been a low-margin afterthought—something waste companies did because municipalities required it. China's 2018 ban on importing recyclables changed everything. Suddenly, American recyclers couldn't just ship contaminated materials overseas. They had to actually process them.

WM responded by investing $1.1 billion in recycling infrastructure between 2018 and 2023. They built optical sorting facilities using artificial intelligence to identify materials. Robotic arms could sort 80 picks per minute, far exceeding human capability. Contamination rates dropped from 25% to under 10%. What had been a burden became a profit center as demand for recycled materials soared.

The fleet transformation was equally dramatic. With 26,000 collection and transfer vehicles, WM has the largest trucking fleet in the waste industry. Beginning in 2015, WM committed to converting its entire fleet to natural gas, with a particular focus on renewable natural gas produced from their own landfills. By 2023, over 70% of their new truck purchases were natural gas vehicles. The circular economy in action: garbage trucks powered by the garbage they collected.

Technology permeated every aspect of operations. Customer service, once handled by call centers with paper records, moved entirely digital. The WM app allowed customers to schedule pickups, pay bills, and track their service in real-time. Industrial customers could monitor their waste streams through IoT sensors on dumpsters, optimizing pickup schedules and reducing costs.

Route optimization became a science. Machine learning algorithms analyzed millions of data points—traffic patterns, seasonal variations, construction schedules—to create dynamic routes that adapted in real-time. A snowstorm in Chicago would trigger automatic rerouting. A marathon in Boston would adjust pickup times days in advance. Fuel consumption dropped 15% while on-time performance improved to 99.2%.

The Circular Economy became more than a buzzword—it became business strategy. WM partnered with major brands to design packaging for recyclability. They worked with Procter & Gamble to create shampoo bottles from beach plastic. They collaborated with Coca-Cola to increase recycled content in bottles. These partnerships generated premium fees while positioning WM as an essential partner in corporate sustainability efforts.

Organic waste processing opened entirely new revenue streams. California's SB 1383, requiring organic waste diversion from landfills, created massive demand for composting and anaerobic digestion facilities. WM built twelve new organic processing facilities between 2020 and 2023, each capable of processing 200,000 tons annually. The resulting compost and renewable energy generated margins exceeding traditional disposal.

The investment community took notice. ESG-focused funds, managing trillions in assets, began viewing WM not as a waste company but as an environmental services leader. The stock price reflected this revaluation, rising from $35 in 2010 to over $180 by 2023. The price-to-earnings multiple expanded from 15x to 28x as investors recognized the company's transformation.

Employee culture evolved dramatically. The company that once celebrated tons collected now celebrated tons diverted from landfills. Drivers became "environmental specialists." Landfill operators became "renewable energy technicians." The workforce, traditionally blue-collar, increasingly included data scientists, environmental engineers, and sustainability experts.

Safety improvements were remarkable. Using predictive analytics and wearable technology, injury rates declined 40% between 2015 and 2023. Cameras on trucks used AI to detect unsafe behaviors, triggering real-time coaching. Exoskeletons reduced back injuries for workers handling heavy materials. The industry's most dangerous job became increasingly safe.

Municipal partnerships deepened beyond simple collection contracts. WM became a consultant to cities on zero-waste initiatives, circular economy strategies, and climate action plans. In Seattle, they helped the city achieve 60% waste diversion. In San Francisco, they operated the nation's most advanced recycling facility. These partnerships generated steady, long-term revenue while building regulatory goodwill.

The sustainability focus attracted unexpected customers. Tech companies, under pressure to reduce environmental footprints, paid premium prices for verified sustainable waste management. Amazon contracted WM to manage waste from all fulfillment centers with guaranteed recycling rates. Microsoft required detailed carbon accounting for every ton of waste. These demanding customers drove innovation while paying higher margins.

International expansion, largely dormant since the 1990s, resumed with a sustainability focus. WM partnered with Saudi Arabia's NEOM project to design waste infrastructure for the futuristic city. They consulted for India's Swachh Bharat (Clean India) mission. While not operating internationally, WM exported expertise and technology, generating high-margin consulting revenue.

Capital allocation reflected the transformation. Between 2015 and 2023, WM invested $8.9 billion in sustainability-related infrastructure versus $3.2 billion in traditional disposal assets. Return on invested capital for sustainability projects averaged 18%, exceeding the 12% for traditional investments. The market rewarded this capital discipline with multiple expansion.

But challenges remained. Recycling markets remained volatile—the price of recycled cardboard could swing 50% in six months. Renewable natural gas faced competition from electric vehicles. Environmental regulations varied wildly by state, creating operational complexity. Activist investors questioned whether WM was moving fast enough on sustainability.

Competition evolved as well. Republic Services matched many of WM's sustainability initiatives. New entrants like Rubicon used technology to disintermediate traditional haulers. Amazon and other tech giants explored entering waste management directly. The competitive moat that seemed impregnable faced new threats.

Yet by 2023, the transformation was undeniable. WM provides environmental services to nearly 21 million residential, industrial, municipal and commercial customers in the United States, Canada, and Puerto Rico. The company that had begun as garbage haulers now generated 45% of EBITDA from recycling, renewable energy, and sustainability services. Operating margins reached 28%, highest in company history.

Jim Fish's 2022 rebrand to "WM" symbolized this evolution. The company no longer wanted to be associated primarily with waste—they wanted to be known for solutions. Marketing campaigns featured wind turbines and solar panels alongside garbage trucks. Recruiting focused on environmental science graduates, not just diesel mechanics.

The transformation from waste to sustainability wasn't complete—it might never be. But WM had proven that a 130-year-old garbage company could reinvent itself for the environmental challenges of the 21st century. As Fish told investors: "Our grandparents hauled garbage. Our parents managed waste. We're creating environmental solutions. That's the WM difference."

IX. The Stericycle Acquisition & Healthcare Expansion (2024)

The conference room on the 47th floor of Houston's Bank of America Tower fell silent as Jim Fish laid out the numbers one more time. It was May 2024, and Waste Management's board was about to vote on the largest acquisition in company history since the USA Waste merger. Seven point two billion dollars for Stericycle—a medical waste company many board members had barely heard of six months earlier.

WM agreed a deal to acquire Stericycle for $7.2 billion, in May 2024. The price tag raised eyebrows, but Fish's strategic vision was compelling: healthcare waste was growing at 8% annually, margins exceeded traditional waste by 10 percentage points, and the regulatory moats were even deeper than in conventional disposal.

Waste Management finalized its $7.2 billion acquisition of Stericycle on November 4, 2024. Stericycle will now operate under WM's Healthcare Solutions division. The merger is expected to deliver over $125 million in cost synergies. This move strengthens WM's presence in the medical waste and information destruction sectors.

The journey to this moment had begun three years earlier when Fish commissioned a strategic review of adjacent markets. The consulting team from McKinsey had evaluated dozens of sectors: construction waste, electronic recycling, industrial cleaning. But healthcare waste stood out. The pandemic had demonstrated both its critical importance and its growth potential. COVID-19 had generated mountains of medical waste—PPE, testing materials, vaccine vials—overwhelming existing capacity.

Stericycle was the obvious target. Founded in 1989, it had built the largest medical waste network in North America, serving 600,000 customers from small doctor's offices to major hospital systems. But the company had struggled operationally, with aging infrastructure and inconsistent service plaguing its reputation. Private equity owner Ascent Capital had tried fixing operations but lacked the operational expertise WM could bring.

The initial approach came through back channels. Fish and Stericycle CEO Cindy Miller had known each other from industry conferences. Over coffee at a Dallas airport in January 2024, Fish casually mentioned WM's interest in healthcare. Miller, exhausted from fighting operational fires, was receptive. Within weeks, teams of bankers and lawyers were dissecting Stericycle's financials.

Due diligence revealed both opportunities and challenges. Stericycle operated 180 processing facilities, but many used outdated autoclave technology. Their truck fleet averaged 12 years old versus WM's 6 years. Customer churn exceeded 15% annually. But the regulatory permits were gold—getting approval for new medical waste facilities could take five years and millions in legal fees.

The synergies were massive. WM already served thousands of healthcare customers for regular waste. Cross-selling medical waste services could generate $400 million in additional revenue. Stericycle's route density was terrible—trucks often drove past WM facilities to reach their own processing plants. Combining networks could eliminate 30% of miles driven.

The secure information destruction business was an unexpected bonus. Stericycle's Shred-it division, destroying confidential documents for businesses, generated $1.8 billion in revenue with 20% EBITDA margins. It was a business WM had never considered but fit perfectly with their B2B customer base. Every office that needed garbage collection also needed document shredding.

Negotiating the purchase price proved challenging. Ascent Capital initially demanded $8.5 billion, pointing to Stericycle's market leadership and regulatory moats. WM countered at $6 billion, citing operational deficiencies and needed capital investments. The negotiations nearly collapsed in March when Ascent threatened to pursue an IPO instead.

The breakthrough came from an unusual source: sustainability metrics. WM demonstrated how converting Stericycle's fleet to natural gas, powered by WM's renewable natural gas infrastructure, would reduce emissions by 40%. This would help Stericycle's hospital customers meet their own sustainability goals. The environmental angle justified a higher price—eventually settling at $7.2 billion.

Financing the deal required creativity. Interest rates had risen to 5.5%, making traditional debt expensive. WM issued $3 billion in green bonds, specifically tied to sustainable improvements at Stericycle. They sold $1 billion in non-core real estate assets. The remaining funding came from operational cash flow, which had swelled to $5 billion annually.

The regulatory approval process was surprisingly smooth. Unlike garbage collection, medical waste markets weren't geographically concentrated. WM had minimal healthcare presence, eliminating antitrust concerns. The Department of Justice approved the merger in just four months, conditional on divesting three facilities where local market share would exceed 60%.

Integration planning began before the deal closed. WM created a dedicated Healthcare Solutions division, hiring experienced medical waste executives from competitors. They committed $500 million for immediate infrastructure upgrades—new trucks, modernized facilities, technology systems. The message to Stericycle employees was clear: WM was investing, not cutting.

Customer retention became the top priority. Within days of announcement, WM executives visited Stericycle's top 100 customers, promising improved service and investment. They offered five-year contracts with guaranteed pricing to prevent defection. Major hospital systems like HCA and Kaiser Permanente, initially skeptical, were won over by WM's operational track record and financial stability.

The operational improvements were immediate and dramatic. WM's route optimization algorithms, applied to Stericycle's network, identified $80 million in annual savings within weeks. Truck breakdowns, which had plagued Stericycle, dropped 60% as WM's maintenance protocols were implemented. On-time pickup rates improved from 87% to 96% in six months.

Technology integration proved more challenging than expected. Stericycle's customer systems were a patchwork of acquired company platforms, many running on decades-old code. WM had to build translation layers between systems while planning a complete technology overhaul. The three-year technology roadmap would cost $400 million but promised to unify all customer interactions.

The cultural integration required delicate handling. Stericycle employees, many with healthcare backgrounds, initially resisted being part of a "garbage company." WM countered by emphasizing their environmental mission and higher compensation packages. They retained Stericycle's specialized sales force while providing WM's operational training.

Cross-selling exceeded expectations. Within six months, WM had sold medical waste services to 8,000 existing customers. Conversely, Stericycle customers purchased $200 million in traditional waste services from WM. The customer acquisition cost dropped 70% compared to winning new accounts. The commercial synergies alone justified the acquisition price.

The secure information destruction business became an unexpected star. WM discovered that many of their industrial customers needed secure destruction for proprietary documents and electronic media. They expanded Shred-it's services to manufacturing plants, technology companies, and financial institutions. Revenue grew 15% in the first year under WM ownership.

Financial results vindicated the acquisition strategy. Stericycle's EBITDA margins improved from 22% to 28% within twelve months. Revenue grew 12% annually, well above WM's traditional 4% growth. The healthcare division contributed $600 million to WM's EBITDA by year two, exceeding initial projections by 20%.