The Wendy's Company: The Financial Engineering of a Burger Queen

I. Introduction & The June 2026 Meme Wave

On the afternoon of Wednesday, June 24, 2026, something strange happened to a fifty-seven-year-old hamburger chain. Trading desks watched the ticker for The Wendy's Company — symbol WEN, the same red-pigtailed mascot that has stared out from highway signs since the Nixon administration — light up with a velocity normally reserved for crypto tokens and small-cap biotech. The stock spiked as much as 42% intraday, tripping Nasdaq's volatility circuit breakers and forcing consecutive trading halts.1 Over roughly forty-eight hours, a beaten-down restaurant operator that Wall Street had largely written off became the most-discussed stock on Reddit's r/WallStreetBets.

The rallying cry, as it had been for GameStop and AMC five years earlier, was sentimental rather than financial: "We need to save Wendy's." It is worth pausing on the irony the Wall Street Journal flagged in its coverage — the meme crowd once again "confused a bet against a stock with a deliberate effort to put a beloved company out of business."1 Short sellers do not want Wendy's to vanish; they had simply bet that the latest turnaround plan looked, in the Journal's words, "half-baked." But that distinction is exactly what makes a meme squeeze combustible. Heavy short interest is dry kindling. When a household name with a small float jumps, the shorts must race to buy shares at any price to return what they borrowed, and their losses are, in theory, unlimited.

Wendy's ticked every box. It is small for a household name — on the eve of the spike, McDonald's was roughly 160 times its market value and Burger King's parent, Restaurant Brands International, about 30 times larger.1 Small companies are easy to move. It carried heavy short interest from funds skeptical of the story. And it is beloved, which is why squeezes happen to GameStop and not to Amalgamated Widget Inc.

But here is where the meme tape and the business story collide. The June rally did not come out of nowhere. It landed on top of a genuine corporate drama: a new operations-obsessed CEO poached from the sandwich chain Potbelly, a freshly hired CFO who followed him in the door on June 23,6 an aggressive store-closure program branded "Project Fresh," and — the detail that turned a turnaround into a powder keg — SEC disclosures showing that activist billionaire Nelson Peltz's Trian Fund Management, already Wendy's largest shareholder, was exploring taking the whole company private.7 As the Journal noted, Peltz "reportedly was mulling a buyout. That just got more expensive."1

So the question Empor wants to answer is not "should you have bought the meme." It is the deeper one underneath: how did one of America's iconic burger brands become a leveraged, asset-light royalty machine that an activist might want to swallow whole — and is there a real business worth saving in there, or just a debt-laden cash cow being milked?

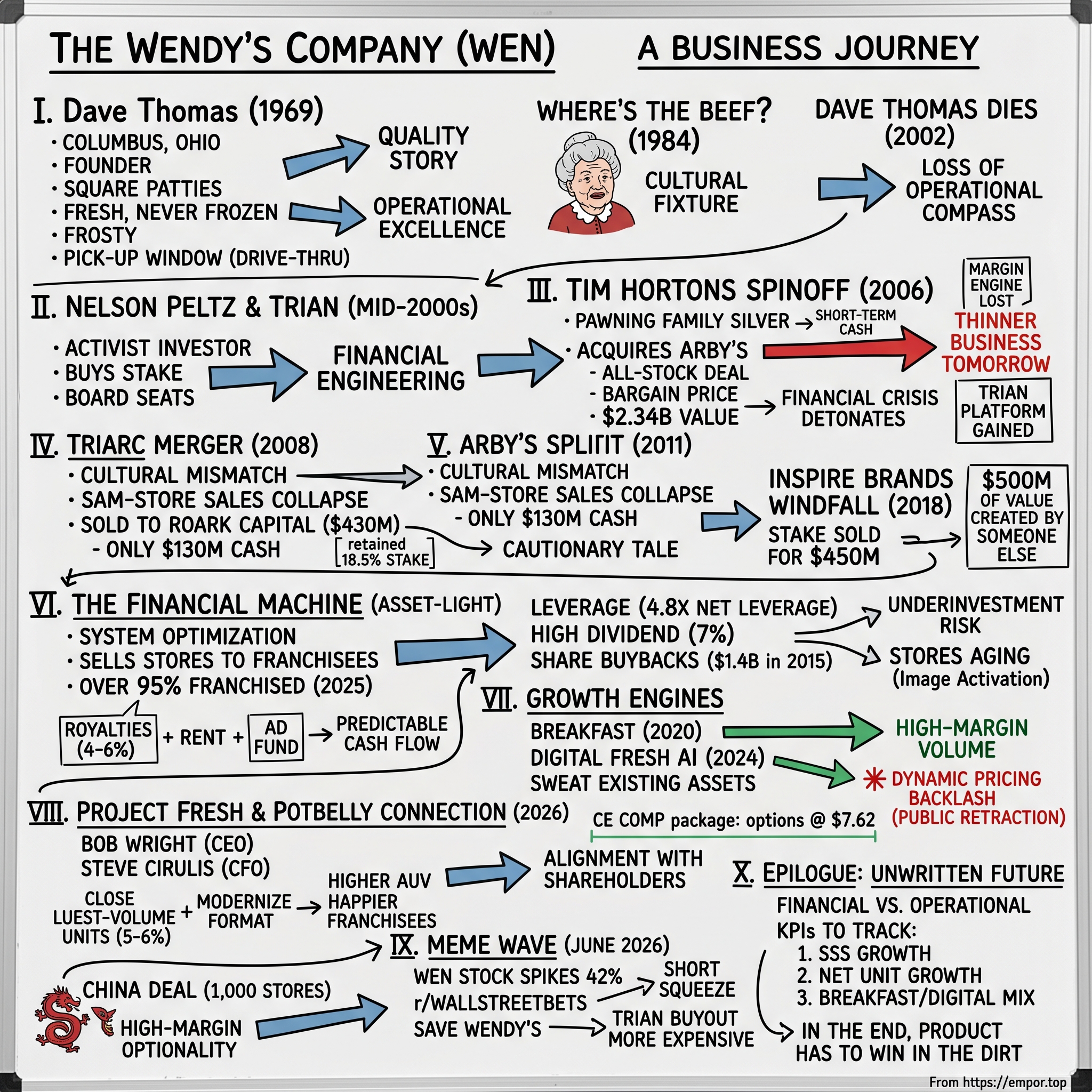

This is, at its heart, a story about financial engineering. Wendy's is square patties and chocolate Frostys on the surface. Underneath, it is a twenty-year activist chess game: a Canadian coffee empire spun off, a disastrous merger with Arby's, a fire-sale divestiture that left half a billion dollars on the table, a balance sheet levered to nearly five times earnings, and now a management reunion betting that operations — not financial structuring — will finally win the day. From Dave Thomas's drive-thru in Columbus, Ohio in 1969 to the trading halts of June 2026, this is how the burger queen got engineered.

II. Dave Thomas and the Art of the Square Patty

Picture Columbus, Ohio, November 1969. A stocky thirty-seven-year-old named Rex David Thomas — everyone called him Dave — opens a restaurant downtown and names it after his eight-year-old daughter Melinda Lou, whose siblings could only manage "Wenda." The pigtailed redhead on the sign was his daughter idealized. Thomas had a peculiar résumé for a man about to build a national chain: he was a high-school dropout, adopted as an infant, who had bounced through restaurant kitchens since he was twelve. His most important apprenticeship came courtesy of a goateed Kentuckian named Harland Sanders — the Colonel of KFC — for whom Thomas had turned around four failing franchises before cashing out his stake for over a million dollars. That money seeded Wendy's.

Thomas absorbed from Sanders a conviction that would define everything: in fast food, the product and the operating system are the strategy. Where McDonald's had won the 1960s by industrializing the hamburger into a frozen, uniform puck, Thomas zigged. His patties were fresh, never frozen, and — crucially — square. The squareness was not a gimmick; it was merchandising made physical. A square patty hangs over the edge of a round bun, so the customer literally sees more beef than the competition served. It was a silent, daily jab at the frozen round patties of McDonald's and Burger King, and it told a quality story without a single word of copy.

Around that core, Thomas built a menu engineered for margin and repeatability. The Frosty — a frozen dairy dessert deliberately made too thick to drink through a straw and too thin to eat comfortably with a spoon — was simple to produce and absurdly high-margin. The fries were salted and sold in volume. Nothing on the early menu required culinary genius to reproduce in the thousandth store as in the first. That replicability is the unglamorous engine of every great quick-service chain.

His most underrated innovation, though, was a window. Thomas was among the first to build the modern pick-up window drive-thru — a dedicated lane with its own grill line, so that car orders did not choke the front counter. In an industry where the entire economics turn on how many cars you can serve per hour at a fixed piece of real estate, this quietly reset Wendy's throughput. Decades later, the drive-thru would still account for the majority of the chain's sales, and the breakfast and digital strategies of the 2020s would lean on the same lanes Thomas first carved out.

Then came the line that made Wendy's a cultural fixture. In 1984, an eighty-one-year-old actress named Clara Peller peered into a competitor's oversized bun and barked, "Where's the beef?" The ad became a national catchphrase, jumped into a presidential primary debate, and burned Wendy's quality positioning into the American memory. Thomas himself eventually became the pitchman, appearing in more than 800 commercials as the rumpled, grandfatherly everyman who seemed to genuinely like his own hamburgers — an authenticity that no marketing department could manufacture.

When Dave Thomas died in January 2002, Wendy's lost more than a founder. It lost its operational compass and its face. The chain that Thomas had run on product obsession would, within three years, find itself in the crosshairs of a very different kind of operator — one who looked at Wendy's not as a hamburger company but as a portfolio of mispriced assets. The square patty was about to meet the spreadsheet.

III. Enter Nelson Peltz: The Activist Conquest & Triarc Merger

Nelson Peltz did not eat his way to control of Wendy's; he financed his way there. By the mid-2000s, Peltz was already a Wall Street archetype — the activist investor who buys a stake, writes a pointed letter, wins board seats, and forces a sleepy company to disgorge value it has been sitting on. His firm, Trian Fund Management, which he ran with partner Peter May and a younger lieutenant named Edward Garden, specialized in consumer and food brands. In 2005, Trian turned its attention to Wendy's International and built a stake of roughly 5.5%, then began the familiar campaign: this company, the argument went, was a collection of underappreciated assets buried inside a bloated corporate structure.

The first asset Peltz pried loose was a Canadian crown jewel. Wendy's had acquired the coffee-and-doughnut icon Tim Hortons back in 1995 for about $400 million, and over the following decade Tim Hortons had quietly become the highest-growth, highest-margin business in the entire portfolio — a beloved national institution in Canada whose economics outshone the American burger parent that owned it. Peltz's logic was textbook sum-of-the-parts: the market was valuing Tim Hortons at a discount because it was trapped inside Wendy's. Spin it off, let it trade on its own, and shareholders capture the difference.

In 2006, the board did exactly that, IPO-ing and then fully spinning off Tim Hortons. The move generated an immediate cash windfall and a pop for shareholders. But strip away the financial choreography and look at what Wendy's was left holding: it had just severed its single best growth-and-cash-flow engine. The spin-off unlocked value the way pawning the family silver unlocks value — real money today, a thinner business tomorrow. Wendy's would spend the next two decades hunting for a margin engine to replace what it had given away.

With Tim Hortons gone and Wendy's operating results still soft, Peltz made his decisive move. By 2008 he controlled Triarc Companies, a holding company whose main asset was the roast-beef chain Arby's. In April 2008, Triarc agreed to acquire Wendy's International in an all-stock deal, and the transaction closed that September.2 The headline value was about $2.34 billion, struck at roughly $30.09 per Wendy's share — a premium of about 26.7% to where the stock had been trading.2

Now, the natural assumption is that an activist who has been agitating a stock would end up overpaying to seize it. The numbers say the opposite. Standalone Wendy's was acquired at roughly 8.9 times its forward 2008 EBITDA. The combined Wendy's/Arby's Group was valued at about 8.5 times EBITDA — and once you factored in the roughly $160 million in cost synergies Peltz projected, the effective multiple dropped to around 6.3 times. For a household-name brand with thousands of locations, that is not a premium price; it is a bargain.

The tell is in who sued. Wendy's own shareholders went to court to block the merger, arguing that Peltz had used the company's operational weakness — weakness he had a hand in spotlighting — to acquire it on the cheap, swapping their Wendy's shares for stock in his own vehicle at an unfavorable ratio. Read in hindsight, the deal looks less like an overpayment and more like a masterstroke of timing. Peltz gained control of Wendy's brand equity and a vast portfolio of real estate at an attractive multiple just as the September 2008 financial crisis detonated and asset prices collapsed everywhere else. Trian now had its platform. The only problem was the roast beef it brought along.

IV. The Arby's Split & The $450 Million Spinoff Blunder

The marriage of Wendy's and Arby's was supposed to be a synergy machine. Two quick-service brands, one corporate overhead, shared purchasing power, combined real-estate muscle — on the pro-forma slide it all penciled out. In the parking lot, it did not. The two chains served different customers, ran different kitchens, and pulled in different directions, and the cultural mismatch showed up fast in the one place it cannot hide: same-store sales.

Arby's was the anchor dragging the boat down. In 2010, the roast-beef chain's same-store sales collapsed by 9.2%, and the segment posted an operating loss of roughly $35 million, bleeding into the profitability of a combined company that was supposed to be the whole point of the merger. For a management team that had sold investors on operational discipline, watching one half of the house lose nearly a tenth of its sales in a single year was an indictment. Trian made the call to amputate.

In June 2011, Wendy's/Arby's Group sold Arby's to the private-equity firm Roark Capital. The structure tells you how eager they were to be rid of it: the aggregate value was about $430 million, but only $130 million of that was cash, with roughly $190 million in assumed debt and an $80 million tax benefit rounding out the figure.3 To preserve a sliver of upside — and to signal that they had not entirely given up on the brand — Wendy's retained an 18.5% minority stake in the divested company.3

That retained stake is where the story turns from a clean refocusing into a cautionary tale about benchmarking. The Wendy's board, desperate to become a pure-play burger company, implicitly valued Arby's as a broken asset worth roughly the price of its debt. Roark saw something else: a turnaround. Roark's operators, steeped in multi-brand restaurant franchising, did to Arby's what the previous owners could not — fixed the menu, sharpened the marketing ("We Have The Meats"), and rebuilt average unit volumes. Arby's became the seed of a multi-brand juggernaut that Roark would later christen Inspire Brands, eventually folding in Buffalo Wild Wings, Sonic, Jimmy John's, and Dunkin'.

The punchline arrived in 2018. Wendy's sold its remaining stake in Inspire Brands — by then diluted to about 12.3% — for $450 million.4 Read that again against the 2011 deal: the leftover minority slice alone fetched more cash than the entire sale of Arby's had brought in seven years earlier. The board had been right that Arby's did not belong inside Wendy's. It had been badly wrong about what Arby's was worth in better hands. The episode is a clean illustration of a recurring pattern in this story — Trian is superb at financial structuring and at identifying mispriced assets to acquire, but the same impatience that drives a clean portfolio can leave enormous operational upside on the table when it comes time to sell. Half a billion dollars of Inspire's value was created by someone else, on the other side of a deal Wendy's was relieved to sign.

With Arby's gone and the Inspire windfall banked, Wendy's was finally what Peltz had wanted all along: a focused, single-brand burger company. The question was what kind of machine Trian would now build on top of it. The answer was a financial one.

V. The Financial Machine: High Leverage, Big Buybacks, and Asset-Light Limits

To understand Wendy's as an investment, you have to stop thinking of it as a company that sells hamburgers. By 2025, it barely did. After years of a strategy management called "System Optimization," Wendy's had sold the vast majority of its company-operated restaurants to franchisees. By 2025, well over 95% of the roughly 7,397 Wendy's locations worldwide were owned and operated by franchisees, not by the corporation itself.9 The corporate parent that emerged from this refranchising is, functionally, a real-estate and royalty holding company that happens to have a hamburger logo.

Here is how it actually makes money, and it is worth slowing down because it is the crux of the whole story. First, royalties: franchisees pay Wendy's a percentage of their gross sales — typically in the 4% to 6% range — for the right to use the brand and system. This is high-margin, predictable cash that requires almost no capital from Wendy's once the store exists. Second, the real-estate spread: Wendy's owns or holds the master lease on thousands of restaurant sites and subleases them to franchisees at a markup, pocketing the difference as rent. Third, the advertising fund: franchisees contribute a mandatory percentage of sales (around 4%) into a national marketing pool that drives brand awareness. The genius of this model is that the corporation captures a slice of every burger sold across the system while bearing almost none of the cost of frying it.

Now, why does a business build itself this way? Because predictable cash flows are the perfect collateral for debt. When your revenue is a near-guaranteed royalty and rent stream, lenders will let you borrow aggressively against it, and that is precisely what Trian did. By late 2025, Wendy's was operating at roughly 4.8 times net leverage — net debt of nearly five times EBITDA.9 In the world of asset-light franchisors, that is an aggressive but not unheard-of structure. The logic is that levering up a stable cash machine and returning the proceeds to shareholders generates higher returns on equity than letting cash sit idle.

And return it they did. In 2015, Wendy's executed a $1.4 billion share buyback — an enormous sum for a company its size — including a controversial $211 million purchase of stock directly from Trian itself, a related-party transaction that critics noted let the largest shareholder cash out at the company's expense. Alongside buybacks, Wendy's maintained an aggressive dividend, and by 2026 the beaten-down share price had pushed the dividend yield to roughly 7% — a level that signals either a bargain or a market betting the payout is unsustainable.8

This is where the elegance of the model meets its limit, and the limit is the whole bear case in miniature. Leverage of 4.8 times is wonderfully efficient when interest rates are near zero — cheap debt, fat equity returns. But rates are not near zero anymore. In a higher-rate world, interest expense eats into the free cash flow that should be funding the business, and that creates a structural problem: Wendy's has been chronically starved of corporate capital to reinvest in physical store remodels — what the company calls "Image Activation." Meanwhile, McDonald's, sitting on a far stronger balance sheet, poured billions of its own cash into modernizing its restaurants. A skeptical investor looks at this and sees the core tension of the entire Trian era: the financial structure that maximized shareholder returns in the 2010s may have quietly underinvested the brand into competitive disadvantage by the 2020s. You cannot out-engineer a tired restaurant. Eventually the product has to win in the dirt — and to win in the dirt, you sometimes have to spend money the balance sheet no longer easily allows.

The company's answer to that squeeze has been to chase growth that costs almost nothing to add. Which brings us to breakfast.

VI. The Incremental Engine: Breakfast Daypart & Digital FreshAI

On the morning of March 2, 2020, Wendy's did something it had tried and failed to do for decades: it launched breakfast nationwide, rolling the menu out to roughly 6,000 U.S. restaurants behind about $20 million of company support.11 The Breakfast Baconator and the Honey Butter Chicken Biscuit hit the menu boards. The timing, in retrospect, was almost comically cruel — within weeks, COVID-19 emptied American highways and shuttered the morning commute that a breakfast daypart depends on. A lesser idea would have died right there.

It did not die, and the reason is the most beautiful economics in the entire Wendy's model. Breakfast is incremental in the purest sense. The real estate is already paid for. The kitchen already exists. The drive-thru lane Dave Thomas built is sitting empty between 6:30 and 10:30 in the morning, generating zero revenue while the rent meter runs. Add a morning daypart and almost every dollar of breakfast sales arrives after the fixed costs — rent, equipment depreciation, the manager's salary — have already been covered by lunch and dinner. The incremental margin on that morning dollar is therefore unusually rich.

Breakfast climbed to roughly 8% to 10% of global systemwide sales — a meaningful new layer of high-margin volume laid on top of an existing cost base.8 For a company structurally short of reinvestment capital, growth that requires no new buildings is exactly the kind of growth it can afford. The analytical read is straightforward: when a franchisor can grow same-store sales by better utilizing assets it already owns rather than by building new ones, it improves both unit economics and franchisee profitability at once — and franchisee profitability is the lifeblood of an asset-light model, because unhappy franchisees stop building stores.

The same "sweat the existing asset" logic drove the digital push. By the mid-2020s, digital sales had grown to over 15% of Wendy's U.S. sales — orders placed through the app or kiosks that lift average checks, capture customer data, and smooth out labor. Digital is to data what breakfast is to real estate: a way to extract more value from infrastructure that is already in the ground.

But the digital story also produced the company's most self-inflicted wound. In early 2024, then-CEO Kirk Tanner floated plans to test digital menu boards with "dynamic pricing." The internet did what the internet does. Within hours, "dynamic pricing" had been recast as Uber-style surge pricing for hamburgers — the specter of a Baconator costing more at noon than at 3 p.m. The backlash was ferocious and the optics catastrophic for a brand whose entire identity is value. Wendy's was forced into a public retraction, clarifying that it had never intended hour-by-hour surge pricing, only daypart-specific promotions and AI-driven upselling through a system it branded FreshAI. The episode is a small but telling case study in management communication: a genuinely sensible operational tool was described in language that handed critics a weapon, and the company spent more brand equity cleaning up the message than it could have gained from the feature. For a chain that lives and dies on the perception of value, that was an own goal — and a reminder that the company's prized sarcastic, online-native voice cuts both ways.

By late 2025, with breakfast maturing, digital growing, and the dynamic-pricing wound still tender, Wendy's faced a harder problem than menu innovation. Its U.S. store base was aging, foot traffic was sliding, and beef and labor inflation were squeezing franchisee margins. The fix would require not a new daypart but a new operator — and Wendy's found one it already knew.

VII. "Project Fresh" and the Potbelly Connection

In May 2026, the Wendy's board ended months of uncertainty and named a permanent chief executive. The choice was a homecoming. Robert D. "Bob" Wright, 58, was appointed President and CEO effective May 21, 2026, taking over from interim chief Ken Cook, who slid back into his role as CFO.5 Wright was not a stranger to the red pigtails. He had been Wendy's Executive Vice President and Chief Operations Officer from 2014 to 2019 — the operational nuts-and-bolts era — with earlier tours of duty at Domino's and Checkers.5 This was the board reaching for an operator, not a financier.

What made Wright credible was where he had just been. From 2020 to 2025 he ran Potbelly Corporation, the toasted-sandwich chain, and engineered one of the more impressive small-cap restaurant turnarounds of the decade — growing average unit volumes sharply and culminating in Potbelly's roughly $566 million sale to convenience-and-fuel operator RaceTrac. He arrived at Wendy's with a turnaround playbook that had just paid off, and a reputation as someone who fixes restaurants rather than refinances them.

He did not arrive alone. On June 23, 2026, Wright poached his former Potbelly partner, Steve Cirulis, to serve as Wendy's Chief Financial Officer and Chief Strategy Officer.6 Reuniting the CFO who helped him turn Potbelly around signaled that Wright intended to run the same plays at ten times the scale — and it was this management reassembly, layered on top of the Trian take-private chatter, that gave the June meme rally its narrative spark.

The strategy they inherited and now own is branded "Project Fresh," launched in late 2025. It marks a philosophical break from the growth-at-all-costs unit expansion of prior years. Instead of opening stores, Project Fresh is about pruning them. Wendy's moved to close roughly 5% to 6% of its oldest, lowest-volume U.S. units — on the order of 300 to 350 restaurants — by mid-2026, with the survivors and new builds shifting to a high-efficiency, digital-first "Global Next Gen" format.8 The thesis is that a smaller, healthier, more modern footprint generates higher average unit volumes and happier franchisees than a sprawling base studded with tired, money-losing locations. It is a quality-over-quantity bet.

The most investor-relevant detail of the new regime is how Wright is paid, because compensation reveals what the board actually wants. His package is built almost entirely around a stock-price recovery. The base salary is a modest $1 million, with a target annual bonus of 175%, or about $1.75 million.10 The real money is in the equity: a grant of 1,772,898 stock options struck at an exercise price of $7.62 per share, vesting over three years and expiring in 2036.10 Those options are worthless unless the stock climbs meaningfully above $7.62. In other words, Wright makes generational money only if common shareholders make money first — a clean alignment that contrasts sharply with the related-party flavor of the 2015 Trian buyback.

The honest analytical caveat is that incentives are not outcomes. A well-structured option grant tells you the board has aligned management with shareholders; it does not tell you the turnaround will work. Wright executed brilliantly at Potbelly, but Potbelly is a sandwich chain a fraction of Wendy's size, and a turnaround that moves the needle on a few hundred stores is a different animal from one that must re-energize a 7,397-unit global system against the deepest-pocketed competitor in the industry. The bet is that operational DNA travels. Whether it scales is the open question — and to frame that question properly, we need to war-game the competitive board.

VIII. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the meme tape and the activist intrigue, and the durable question is whether Wendy's possesses any real competitive advantage — the kind of structural edge that lets a business earn excess returns that rivals cannot compete away. Two frameworks help stress-test that: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces.

Hamilton's 7 Powers Applied to Wendy's

Counter-Positioning (weak, and weakening). For decades, "fresh, never frozen" square beef was a genuine counter-position — a quality stance the frozen-patty incumbents could not easily copy without admitting their own product was inferior. The trouble is that the counter-position has been overrun from above. Fast-casual players like Five Guys and Shake Shack now own the "premium, fresh burger" high ground, while McDonald's and Burger King own value and scale below. Wendy's is squeezed in the middle, stuck fighting the QSR value wars on price rather than defending a differentiated quality position. The power that once defined the brand has largely eroded.

Scale Economies (decisively lagging). This is where the math is brutal. McDonald's operates roughly 45,356 stores worldwide against Wendy's 7,397.89 Scale in fast food is not vanity — it compounds into lower per-unit advertising costs, superior purchasing power on beef and logistics, and the cash to modernize stores. McDonald's can spread a national ad campaign across six times the locations, and it can negotiate input costs Wendy's simply cannot match. This is a structural disadvantage Wendy's cannot close; it can only navigate around it.

Switching Costs (asymmetric). For the burger eater, switching costs are zero — the next drive-thru is across the street, and customers are ruthlessly price-sensitive. But for franchisees, switching costs are enormous. A franchisee is locked in by 20-year franchise agreements and property subleases that make exiting the system painful and slow. This is the power that actually underwrites the financial model: the predictable royalty and rent streams that support 4.8x leverage exist precisely because franchisees cannot easily walk away. The moat protects the holding company, not the brand at the counter.

Brand (moderate). Wendy's punches above its weight culturally, thanks to a sarcastic, viral social-media persona and genuine nostalgia equity dating to "Where's the beef?" But brand power in QSR is only real if it confers pricing power, and Wendy's repeatedly demonstrates the opposite — it must discount aggressively to drive traffic. A brand you love but won't pay a premium for is a marketing asset, not an economic moat.

Porter's Five Forces

Threat of new entrants — low. Building a national drive-thru footprint is staggeringly capital-intensive, and the real estate alone is a moat against newcomers. No one is going to assemble 7,000 locations from scratch.

Bargaining power of buyers — very high. Customers have effectively infinite substitutes and, in an inflationary environment, acute price sensitivity. This is the force that keeps Wendy's discounting.

Bargaining power of suppliers — moderate to high. Beef and broader commodity inflation, plus rising labor costs, pinch franchisee margins directly. Wendy's lacks McDonald's purchasing leverage to absorb input shocks.

Threat of substitutes — high. The competition is not just other burgers. It is fast-casual, convenience-store grab-and-go (Wawa, 7-Eleven, and — fittingly — RaceTrac, the buyer of Wright's old Potbelly), and the cheapest substitute of all, cooking at home.

Competitive rivalry — extreme. The "Big Three" burger war between McDonald's, Burger King, and Wendy's is a brutal, largely zero-sum fight for share, fought with value menus, app promotions, and loyalty programs.

Put the two frameworks together and a sober picture emerges. Wendy's real, defensible power is not at the counter — it is in the franchise contracts and real estate that lock in cash flow. That is a perfectly good business to own at the right price. It is not, however, a business with the competitive armor to dictate terms against McDonald's. Which sets up the central investment debate.

IX. The Bull vs. Bear Case & Activist Take-Private Test

Start with the scoreboard, because scale is the backdrop against which everything else plays out. In 2025, McDonald's ran about 45,356 stores generating roughly $139 billion in system sales and around $26.9 billion in revenue, commanding something close to 40% of the U.S. burger market.8 Burger King's parent, RBI, ran roughly 19,800 Burger King locations as part of a system generating $46.8 billion in sales. Wendy's, by contrast, operated 7,397 stores producing about $14.0 billion in system sales and roughly $2.2 billion in revenue — perhaps 10% to 12% of the U.S. burger market and a low-single-digit slice of global fast food.89 Wendy's is the clear number three, and number three in a scale game is a precarious place to stand.

So why would anyone own Wendy's over McDonald's? The bull case rests on three legs.

First, the Potbelly dream team. If Wright and Cirulis execute Project Fresh — pruning the dead weight, modernizing the footprint into the Global Next Gen format, and driving U.S. average unit volumes higher — the company's margins and franchisee health improve simultaneously, and a stock priced for stagnation re-rates. This is the bet that operational competence, freshly proven at Potbelly, can finally do what financial engineering could not.

Second, the 中国 China option. On May 8, 2026, Wendy's signed what it called the largest development deal in its history — an agreement with an experienced local operator to build up to 1,000 restaurants across China over roughly ten years.12 Unlike KFC, McDonald's, and Starbucks, which have deep, established China footprints, Wendy's has had virtually no presence there.12 A capital-light, royalty-bearing master-franchise expansion into the world's largest consumer market is exactly the kind of high-margin growth vector the model is built to capture — and it costs Wendy's almost nothing to fund, since the local partner builds the stores.

Third, the dividend floor. A roughly 7% yield, if sustainable, pays investors to wait and arguably puts a floor under the share price.8

The bear case answers each leg. The debt burden is the heart of it: 4.8x net leverage in a higher-rate world means interest expense consumes cash flow that should be modernizing restaurants, leaving Wendy's perpetually outgunned on capital by McDonald's.9 A 7% dividend yield, viewed less charitably, is the market's way of pricing in the risk that the payout gets cut. On Project Fresh, closing 300-plus stores is a gamble that those customers migrate to surviving locations; if they don't, Wendy's has simply, permanently shrunk its domestic royalty base — the very asset the whole financial model is built on. And on competition, a revitalized Burger King — fortified by its parent's roughly $300 million "Reclaim the Flame" investment — plus an ever-aggressive McDonald's could simply crush Wendy's on value and digital loyalty, the two battlegrounds where scale matters most. The China deal, for its part, is a ten-year promise with no disclosed timeline for openings and a long history of Western chains stumbling in China; it is optionality, not earnings.12

Which frames the activist stress test hanging over all of it. Is Wendy's a viable long-term public company, or a debt-laden cash cow being milked by Trian? With Trian's early-2026 SEC disclosures revealing it was exploring a take-private bid,7 the skeptical read writes itself: Peltz may want to take Wendy's private precisely to perform radical restructurings — most obviously, selling and leasing back the corporate real estate to extract a one-time cash windfall — away from the scrutiny of public markets and quarterly reporting. A take-private at a modest premium to a depressed stock would let Trian capture the upside of any Wright-led turnaround for itself rather than sharing it with public shareholders. That is the governance question a long/short investor would press hardest: whose interests does a take-private actually serve?

And here the June 2026 meme spike becomes genuinely consequential rather than a sideshow. As the Journal dryly observed, Peltz's contemplated buyout "just got more expensive."1 By pushing the share price up as much as 42% in a session,1 the Reddit crowd may have inadvertently priced the stock above whatever level Trian had penciled in for a clean take-private. The meme, in other words, might have done what no proxy advisor could — temporarily protecting public shareholders by making it too expensive for the largest shareholder to buy them out. Whether that protection holds or fades with the meme is one of the more genuinely uncertain questions in this entire story.

X. Epilogue & Outro

Set down the trading halts, the activist filings, and the framework matrices, and what remains is a deceptively simple business that has spent twenty years being optimized by financiers and is now, finally, being handed back to operators. The arc runs from Dave Thomas obsessing over whether a square patty hung far enough over the bun, to Nelson Peltz treating the same company as a portfolio of assets to spin, merge, divest, and lever — and back, perhaps, to a CEO whose stock options are worthless unless he can make the restaurants themselves better.

For investors trying to track whether the turnaround is real rather than rhetorical, three KPIs cut through the noise. The first is U.S. same-restaurant sales growth — the single cleanest signal of whether Project Fresh is working. If pruning the weak stores and modernizing the rest is genuinely lifting demand, comparable sales at the surviving restaurants must turn and stay positive; anything less means the company shrank its base without improving it. The second is net unit growth, which tells you whether the much-hyped China buildout and Global Next Gen openings are actually outpacing the domestic closures — whether the royalty base is expanding or quietly eroding. The third is the breakfast and digital sales mix, the proxy for whether Wendy's is squeezing more high-margin volume out of real estate it already owns, the one lever it can pull without spending capital it doesn't have.

The deeper lesson of Wendy's is that financial engineering and operational excellence are not substitutes for one another, and the market eventually figures out which one a company has been running on. Trian's structuring extracted enormous value for shareholders in the easy-money 2010s — and may have starved the brand of the reinvestment it needed to compete when money stopped being easy. A great brand can survive decades of being treated as a balance sheet. But the test that Bob Wright and Steve Cirulis now face is the one Dave Thomas never had to think about in financial terms and never stopped thinking about in operational ones: in the end, the product has to win in the dirt. Whether Wendy's becomes a genuine turnaround or remains a pawn in activist finance is, as of June 2026, still unwritten — and that uncertainty, not the meme, is the real story.

References

-

Meme Traders Flock To Wendy's — The Wall Street Journal, 2026-06-26 ↩↩↩↩↩↩

-

Triarc Companies to Acquire Wendy's International in $2.3 Billion Deal — Reuters, 2008-04-24 ↩↩

-

Wendy's/Arby's Sells Arby's to Roark Capital for $430 Million — The Wall Street Journal, 2011-06-13 ↩↩

-

Wendy's Sells Remaining Stake in Inspire Brands for $450 Million — Bloomberg, 2018-08-16 ↩

-

Wendy's Appoints Former Potbelly CEO Robert D. Wright as President and CEO — Nation's Restaurant News, 2026-05-20 ↩↩

-

Wendy's Poaches Potbelly CFO Steven Cirulis to lead 'Project Fresh' — CFO Dive, 2026-06-23 ↩↩

-

Schedule 13D/A Amendment by Trian Fund Management on Wendy's Holdings — SEC Edgar, 2026-02-15 ↩↩

-

The Wendy's Company Q1 2026 Quarterly Results — Wendy's IR, 2026-05-08 ↩↩↩↩↩↩↩

-

The Wendy's Company 2025 Annual Report (Form 10-K) — Wendy's IR, 2026-02-18 ↩↩↩↩↩

-

Wendy's Appoints Robert D. "Bob" Wright as President and CEO; CEO Stock Option Grant (Form 4) — StockTitan, 2026-05-20 ↩↩

-

Wendy's to launch breakfast nationwide in March — CNBC, 2020-02-04 ↩

-

Wendy's Form 8-K Exhibit 99.1 — China development agreement for up to 1,000 restaurants — SEC Edgar, 2026-05-08 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube