WEC Energy Group: Building the Midwest's Energy Future

I. Introduction & Episode Setup

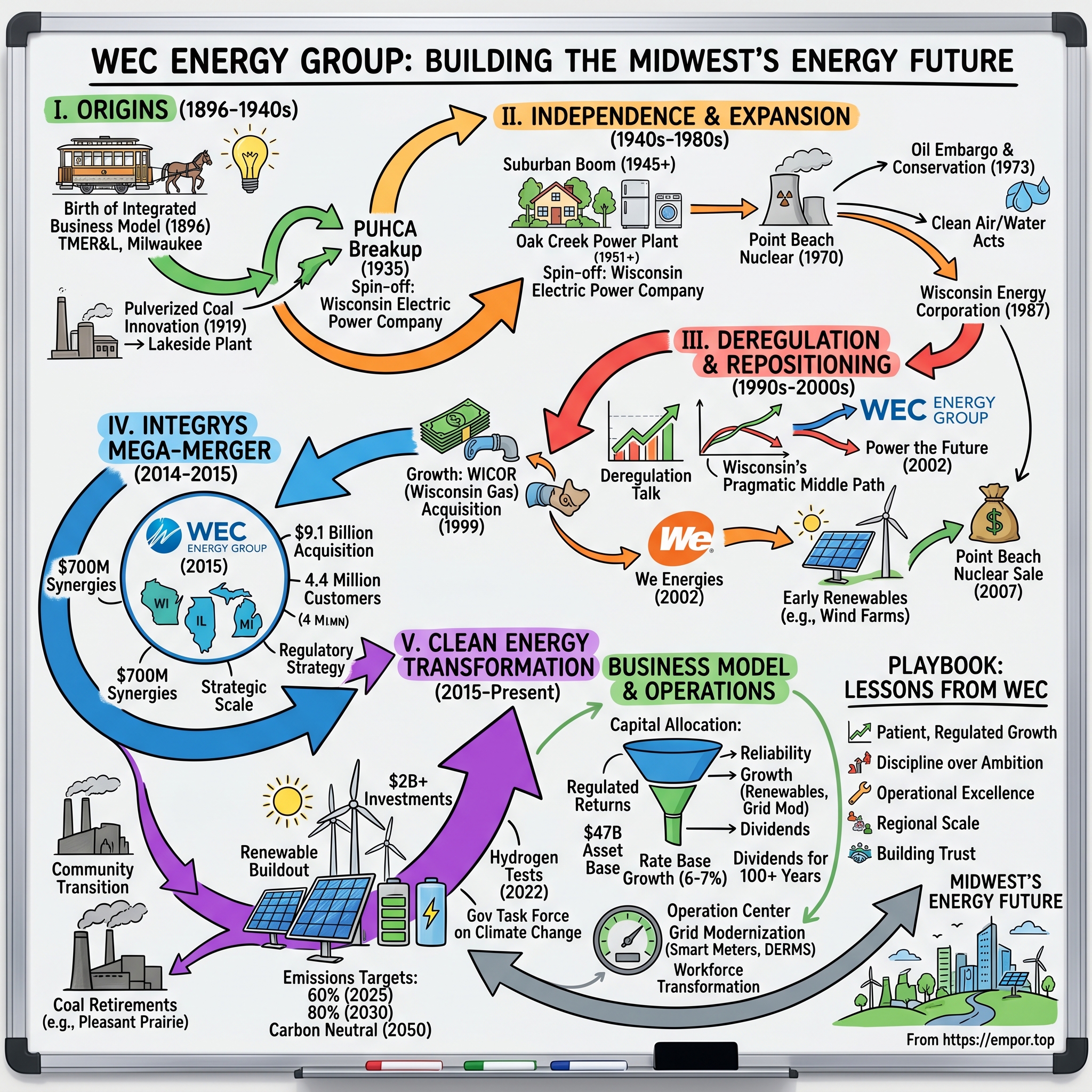

Picture this: It's 1896 in Milwaukee, and the clatter of horse-drawn carriages fills the streets. A group of businessmen gather in a wood-paneled boardroom, not to discuss railroads or steel—the industrial darlings of the Gilded Age—but something far more audacious. They're planning to electrify the city's streetcars and, in a stroke of genius that would define American utilities for the next century, sell the excess power to light homes and power factories. This wasn't just infrastructure; it was the birth of an integrated business model that would evolve into today's WEC Energy Group.

Fast forward to 2024, and that Milwaukee streetcar company has morphed into one of America's premier regulated utilities, serving 4.4 million customers across Wisconsin, Illinois, Michigan, and Minnesota. The numbers tell a story of quiet dominance: $1.5 billion in net income, $4.83 per share, and an asset base spanning 72,400 miles of electric distribution lines and 47,000 miles of gas pipelines. But numbers alone don't capture the remarkable transformation—from streetcars to nuclear power, from coal to renewables, from local monopoly to multi-state powerhouse. The WEC story matters because it's the archetypal American utility evolution—one that mirrors the nation's own energy journey. From the Progressive Era's municipal ownership battles to the nuclear age's promise and peril, from deregulation's false starts to today's clean energy transition, WEC has been both participant and bellwether. In 2024, the company posted net income of $1.5 billion ($4.83 per share) with consolidated revenues of $8.6 billion, numbers that reflect not just financial success but the culmination of 128 years of strategic pivots and patient capital deployment.

What makes WEC particularly fascinating for investors isn't just its steady dividends or regulated returns—it's how the company has repeatedly reinvented itself while maintaining the stability that utility investors crave. Revenue is forecast to grow 6.5% annually over the next three years, compared to 5.8% for the industry, suggesting WEC has found a formula for outperformance even within the constraints of regulation.

This is a story of three major transformations: first, from streetcar operator to integrated utility; second, from local monopoly to multi-state powerhouse through the $9.1 billion Integrys merger; and third, the ongoing pivot from fossil fuels to clean energy. Each transformation required different skills—entrepreneurial vision in the early days, financial engineering during consolidation, and now technological adaptation and stakeholder management in the energy transition.

The roadmap ahead explores how a company born in the age of Edison navigates the era of Musk—how regulatory frameworks designed for coal plants adapt to solar farms and battery storage, how a business model predicated on selling more kilowatt-hours evolves when efficiency becomes a virtue, and how a Midwest utility positions itself for the AI-driven electricity boom while maintaining its social license to operate.

As we'll see, the answer lies not in disruption but in evolution—a distinctly Midwestern approach that values reliability over revolution, steady returns over moonshots, and serving communities over conquering markets. It's a playbook that has worked for over a century, but as the energy transition accelerates and new technologies emerge, the question becomes: Can WEC's deliberate pace keep up with a rapidly changing world?

II. Origins: The Milwaukee Streetcar Era (1896-1940s)

The rain was coming down in sheets that September morning in 1896 when John I. Beggs stepped off the train in Milwaukee. The former Edison executive had been dispatched by the North American Company, one of the era's great utility holding companies, with a mission that seemed almost quixotic: consolidate Milwaukee's chaotic patchwork of competing streetcar lines and power companies into a single, integrated utility. As he surveyed the city's muddy streets, where electric trolleys competed with horse-drawn carriages and gas lamps flickered alongside primitive arc lights, Beggs saw not chaos but opportunity.

The Milwaukee Electric Railway and Light Company (TMER&L) that emerged from Beggs' consolidation efforts wasn't just another streetcar company—it was America's first truly integrated power utility. The genius of the model was elegant: build an electric railway system that would require massive generating capacity for peak morning and evening commutes, then sell that excess power during off-peak hours to light homes and power factories. It was infrastructure as a platform business, decades before Silicon Valley would claim to invent the concept.

By 1900, TMER&L operated 12,000 square miles of interurban rail across southeastern Wisconsin, connecting Milwaukee to Racine, Kenosha, and the surrounding farmlands. But the real innovation was happening behind the scenes. The company's engineers realized that the same generators powering streetcars could illuminate the city's streets, run factory motors, and bring electric light into middle-class homes. Every mile of track laid created not just transportation infrastructure but a potential customer base for electric power.

The technical challenges were immense. Direct current, favored by Edison, couldn't be transmitted over long distances. Alternating current, championed by Westinghouse and Tesla, was still viewed with suspicion. TMER&L's engineers had to build different systems for different purposes—600-volt DC for the streetcars, 2,300-volt AC for transmission, stepped down to 110 volts for residential customers. The East Wells Power Plant became a cathedral of copper and steel, its massive dynamos humming with the promise of the electric age.

Then came 1919, a year that would transform not just TMER&L but the entire electric utility industry. At the East Wells plant, engineers conducted experiments with a radical new technology: pulverized coal. Instead of shoveling chunks of coal into furnaces, they ground it into powder as fine as talcum and blew it into the combustion chamber. The results were staggering—efficiency jumped by 30%, emissions dropped, and suddenly the economics of electric power generation shifted dramatically. Milwaukee had become the proving ground for a technology that would power America's industrial expansion for the next century.

Recognizing the implications, TMER&L's leadership moved quickly. In 1921, they formed Wisconsin Electric Power Company as a subsidiary specifically to build the Lakeside Power Plant on Milwaukee's lakefront. When it opened in 1925, Lakeside was the world's first power plant designed from the ground up to burn pulverized coal exclusively. The four towering smokestacks became landmarks visible from ships far out on Lake Michigan, monuments to Milwaukee's emergence as an industrial powerhouse.

But TMER&L was more than an engineering success—it was a financial innovation. As a subsidiary of the North American Company, itself part of the vast utility empire controlled by the Electric Bond and Share Company, TMER&L had access to capital markets that local utilities couldn't tap. The holding company structure allowed for financial engineering that would make modern private equity firms envious: leveraging local monopolies, cross-subsidizing between territories, and using complex pyramiding structures to maintain control with minimal equity investment.

The social impact was profound. Milwaukee's working-class neighborhoods, many populated by German and Polish immigrants, were among the first in America to have universal electric service. The interurban rail system allowed workers to live in suburban Wauwatosa or West Allis while working in Milwaukee's factories. Department stores stayed open after dark, illuminated by electric lights. Movie theaters proliferated, their marquees blazing with incandescent bulbs. The Milwaukee Journal installed electric-powered printing presses that could produce 50,000 copies an hour.

Yet this golden age contained the seeds of its own transformation. The very success of the holding company model attracted scrutiny from Progressive reformers who saw these utility empires as threats to democracy. Robert La Follette, Wisconsin's firebrand senator, railed against the "power trust" from the Senate floor. State utility commissions, including Wisconsin's pioneering Public Service Commission established in 1907, began asserting greater control over rates and service territories.

The streetcar business itself was becoming problematic. Henry Ford's Model T, which rolled off assembly lines by the millions in the 1920s, offered individual mobility that fixed-rail transit couldn't match. Maintaining tracks and overhead wires became increasingly expensive as automobile traffic tore up street surfaces. Labor disputes with motormen and conductors periodically paralyzed the city. By the late 1920s, TMER&L's managers could see that the streetcar era was ending, but the power business was just beginning.

The 1929 stock market crash and subsequent Depression accelerated these trends. The North American Company's complex financial structure, built on leverage and cross-holdings, began to unravel. President Franklin Roosevelt's administration, viewing utility holding companies as symbols of Wall Street excess, pushed through the Public Utility Holding Company Act of 1935 (PUHCA), which would ultimately force the breakup of the great utility empires.

Between 1938 and 1941, TMER&L underwent a series of complex mergers and reorganizations, absorbing Wisconsin Electric Power Company, Wisconsin Gas and Electric Company, and Milwaukee Gas Light Company. The streetcar operations were spun off (they would limp along until 1958, when the last trolley made its final run). What emerged was a new entity: Wisconsin Electric Power Company, an independent, regulated utility focused solely on providing electricity and natural gas to southeastern Wisconsin.

The transformation was complete. What had begun as a streetcar company had evolved into a modern utility, shaped by technological innovation, financial engineering, regulatory pressure, and changing consumer preferences. The integrated model that John I. Beggs had pioneered—using infrastructure investment to create multiple revenue streams—would remain the foundation of the business. But the swashbuckling era of utility empire-building was over, replaced by a new model of regulated monopoly that would define the industry for the next half-century.

III. Independence & Post-War Expansion (1940s-1980s)

The papers were signed on a humid August morning in 1943, in a boardroom overlooking Lake Michigan. After years of legal wrangling, Wisconsin Electric Power Company was finally free—spun off from the North American Company's crumbling empire as an independent, Wisconsin-focused utility. CEO George Kneeland, a taciturn engineer who'd risen through the ranks, looked out at the lake and saw not freedom but responsibility. The war was raging, Milwaukee's factories were running three shifts producing everything from submarine engines to mess kits, and electricity demand was straining the system to its breaking point.

"Gentlemen," Kneeland told his management team, "we're no longer beholden to New York bankers or Washington bureaucrats. We sink or swim on our own." It was both liberating and terrifying. For the first time in nearly fifty years, the company's fate rested entirely in Wisconsin hands.

The timing couldn't have been more fortuitous. As GIs returned home in 1945 and 1946, they brought with them dreams of suburban homes filled with electric appliances. The Levittown model was spreading across America, and Milwaukee's periphery exploded with new subdivisions. Each split-level ranch house represented a new customer who would need not just lights but electric ranges, water heaters, television sets, and—increasingly—air conditioning.

Wisconsin Electric's engineers had anticipated this boom. Even during the war years, they'd been planning what would become the Oak Creek Power Plant, a massive complex on Lake Michigan designed to dwarf anything previously built in Wisconsin. When the first 120-megawatt unit came online in 1951, it was a marvel of engineering efficiency. But that was just the beginning. Over the next seventeen years, seven more units would be added, ultimately creating a 1,800-megawatt complex that could power all of Milwaukee with capacity to spare.

The scale was staggering. Oak Creek consumed 15,000 tons of coal daily, delivered by unit trains from Wyoming's Powder River Basin. Its intake pipes sucked in 600 million gallons of Lake Michigan water daily for cooling. The plant's four distinctive striped smokestacks, painted in alternating bands of red and white to warn aircraft, became landmarks visible from downtown Milwaukee. Local kids called them "the candy canes."

But Wisconsin Electric wasn't operating in isolation. In 1957, the company joined with utilities across the Midwest to form the Mid-America Interpool Network (MAIN), creating what was then the largest power pooling network in the United States. The concept was revolutionary for its time: instead of each utility maintaining enough capacity for its own peak demand, they would share reserves across a vast transmission network stretching from the Dakotas to Michigan.

The MAIN agreement represented a fundamental shift in utility thinking. Competition gave way to cooperation, at least in operations. Wisconsin Electric could now buy power from Commonwealth Edison during summer peaks and sell excess capacity to Northern States Power during winter cold snaps. The grid became a living organism, with electricity flowing to where it was needed most, regulated by engineers in control rooms that looked like something from a science fiction movie.

Then came the nuclear age. In 1962, Wisconsin Electric announced plans for the Point Beach Nuclear Plant, to be built on a pristine stretch of Lake Michigan shoreline near Two Rivers. The local reaction was mixed—some saw it as progress, others as potential catastrophe. The company launched a massive public relations campaign, bringing in experts from the Atomic Energy Commission, hosting community meetings, even building a visitor center with a model reactor that schoolchildren could tour.

When Point Beach Unit 1 achieved criticality in November 1970, followed by Unit 2 in 1972, Wisconsin Electric had pulled off something remarkable. The plant immediately established a worldwide reputation for efficiency, consistently ranking among the top performers in capacity factor and safety metrics. The two Westinghouse pressurized water reactors could generate 1,000 megawatts with a pellet of uranium the size of a fingertip producing as much energy as a ton of coal.

The economics were intoxicating. Nuclear fuel costs were minimal compared to coal, and the plants could run continuously for 18 months between refueling. Wisconsin Electric's rates, already among the lowest in the Midwest, dropped further. Industrial customers like Allis-Chalmers, Briggs & Stratton, and the breweries that made Milwaukee famous expanded operations, drawn by cheap, reliable power.

But the 1970s brought a rude awakening. The 1973 Arab oil embargo sent energy prices soaring. While Wisconsin Electric wasn't directly dependent on oil, the psychological impact was profound. Americans suddenly realized their vulnerability to energy disruptions. Conservation became a virtue overnight. Wisconsin Electric, which had spent decades encouraging customers to use more electricity, now had to promote efficiency.

The company's response was characteristically methodical. They launched one of the nation's first utility-sponsored home insulation programs, offering low-interest loans for weatherization. They redesigned rate structures to discourage waste while protecting low-income customers. They even experimented with "time-of-use" pricing, installing special meters in volunteer homes that charged different rates for peak and off-peak usage—a concept that wouldn't become mainstream for another thirty years.

Environmental regulations added another layer of complexity. The Clean Air Act of 1970 required expensive scrubbers on coal plants. The Clean Water Act of 1972 restricted thermal pollution from cooling water. Wisconsin Electric spent hundreds of millions retrofitting Oak Creek and other plants with pollution control equipment. The towering hyperbolic cooling towers at the Pleasant Prairie Plant, opened in 1980, became monuments to this new environmental consciousness.

Pleasant Prairie itself represented both the apex and the end of an era. The two 617-megawatt coal-fired units were engineering marvels, with computerized controls, sophisticated emissions monitoring, and efficiency rates approaching 40%. But they would be the last major coal plants Wisconsin Electric would build. Three Mile Island's partial meltdown in 1979 had effectively killed new nuclear construction, natural gas was still too expensive, and renewable energy remained a fantasy.

In 1987, recognizing that the utility business was becoming more complex and capital-intensive, Wisconsin Electric restructured itself as Wisconsin Energy Corporation, a holding company with Wisconsin Electric as its primary subsidiary. New non-utility subsidiaries—Wispark (real estate development), Wisvest (investments), and Witech (emerging technologies)—were created to explore opportunities beyond the traditional utility model.

CEO Richard Abdoo, who took the helm in 1987, was a different breed from the engineers who'd run the company for decades. Harvard Business School-trained and politically savvy, Abdoo understood that the utility's future depended as much on regulatory relationships and financial engineering as on power plant operations. He began positioning Wisconsin Energy for a world where competition, not monopoly, might define the electricity business.

The transformation from the post-war expansion era to this new uncertain future was jarring. Wisconsin Electric had spent forty years in a predictable rhythm: build plants, add customers, raise rates to cover costs, repeat. The regulatory compact was simple—provide reliable service, and regulators would ensure a fair return on investment. But as the 1980s ended, that compact was fraying. Deregulation talk filled industry conferences. Independent power producers were challenging utility monopolies. Industrial customers demanded choice.

The company that entered the 1990s bore little resemblance to the independent utility that had emerged from the holding company breakup in 1943. It was larger, more sophisticated, more environmentally conscious, but also more vulnerable to forces beyond its control. The age of the comfortable monopoly was ending, though few could predict just how tumultuous the transition would be.

IV. The Deregulation Era & Strategic Repositioning (1990s-2000s)

Richard Abdoo was nursing his third cup of coffee in Wisconsin Energy's executive conference room on a frigid January morning in 1992 when the call came from California. Pacific Gas & Electric's CEO was on the line, breathless with evangelistic fervor about electricity deregulation. "Dick, this is going to revolutionize our industry. Customers choosing their power supplier like they choose long-distance carriers. Market forces, not regulators, setting prices. You need to get Wisconsin ready."

Abdoo hung up the phone and turned to his leadership team. "Gentlemen, California's about to blow up their entire utility model. The question is: do we follow them off the cliff, or chart our own course?"

It was the question every utility CEO in America was grappling with. The deregulation fever that had transformed airlines, telecommunications, and natural gas was coming for electricity. Enron's Jeffrey Skilling was barnstorming the country, preaching the gospel of competitive markets. Investment banks were salivating over trading opportunities. Industrial customers were demanding choice. The century-old model of regulated monopoly seemed as antiquated as the streetcars Wisconsin Electric once operated.

But Abdoo, despite his Harvard MBA and comfort with financial innovation, was skeptical. Electricity wasn't a commodity like natural gas or oil that could be stored and traded. It had to be generated and consumed instantaneously, with supply and demand balanced to the microsecond or the entire grid would collapse. The physics of electrons didn't care about economic theory.

Wisconsin's approach would prove prescient. While California rushed toward full deregulation and states like Texas and Pennsylvania followed suit, Wisconsin chose a middle path. The state would allow some competitive generation and give large industrial customers limited choice, but maintain the fundamental structure of regulated utilities. It was a characteristically Midwestern solution—pragmatic, incremental, avoiding both the status quo and radical disruption.

This strategic positioning allowed Wisconsin Energy to play offense while others played defense. In 1994, the company acquired Wisconsin Southern Gas Company for $245 million, adding 200,000 natural gas customers in southern Wisconsin. It was a modest deal, but it demonstrated Wisconsin Energy's intent to grow through acquisition rather than just organic expansion.

The real opportunity came in 1998 with the purchase of Edison Sault Electric Company (ESELCO) in Michigan's Upper Peninsula for $75 million. ESELCO was a tiny utility serving just 22,000 customers, but it came with something invaluable: a foothold in Michigan's regulatory environment and access to the state's industrial customers, particularly the paper mills that dotted the UP.

Then came the deal that would transform Wisconsin Energy from a large regional utility into a multi-state powerhouse. In 1999, Abdoo announced the acquisition of WICOR, Inc., parent company of Wisconsin Gas, for $1.4 billion. WICOR wasn't just a gas utility—it was a diversified energy company with operations in multiple states and a significant presence in liquefied natural gas. The merger would create the largest combined electric and natural gas provider in Wisconsin, serving over 2 million customers.

The WICOR integration was a masterclass in utility consolidation. Wisconsin Energy eliminated duplicate functions, consolidated control rooms, and leveraged purchasing power for everything from transformers to office supplies. The synergies exceeded $50 million annually, far above initial projections. More importantly, the combined company now had the scale to compete in a consolidating industry.

A symbolic moment came in 2000 when Wisconsin Electric added its one-millionth electric customer, a young family in Waukesha whose suburban home bristled with the latest technology—high-speed internet, home theater system, central air conditioning. The utility that had started by lighting downtown Milwaukee now powered a sprawling metropolitan area stretching from the Illinois border to Sheboygan.

In 2002, recognizing the need for a unified brand, Wisconsin Electric and Wisconsin Gas were rebranded as We Energies. The new name and logo—a stylized "e" that could represent both energy and the environment—signaled a break from the past. This wasn't your grandfather's utility company.

The "Power the Future" strategy launched that same year was audacious in scope. Wisconsin Energy would spend $7 billion over a decade to modernize and expand its generation fleet. The centerpiece was the expansion of the Oak Creek Power Plant, adding two 615-megawatt supercritical coal units with the latest pollution control technology. These weren't your grandfather's coal plants either—they featured computerized controls, selective catalytic reduction systems for nitrogen oxides, scrubbers for sulfur dioxide, and baghouses for particulate matter.

Simultaneously, the company built two 545-megawatt combined-cycle natural gas units at Port Washington, taking advantage of newly abundant shale gas that was transforming America's energy landscape. These plants could ramp up or down quickly, providing the flexibility needed to balance an increasingly complex grid.

The nuclear question loomed large. Point Beach Nuclear Plant had been a cash cow for decades, but post-9/11 security requirements, aging equipment, and the lack of a permanent waste repository were driving costs higher. In 2007, Wisconsin Energy made a shocking announcement: it would sell Point Beach to FPL Energy (later NextEra) for $924 million while signing a long-term agreement to purchase the plant's output.

The deal was brilliant financial engineering. Wisconsin Energy monetized an aging asset at peak value, transferred operational and regulatory risk to FPL, but maintained access to carbon-free baseload power. The $924 million could be redeployed into new generation and transmission infrastructure with higher returns and lower risk.

Early renewable investments began during this period, though they seemed almost quaint compared to the massive coal and gas projects. A 20-megawatt wind farm here, a 1-megawatt solar demonstration project there. Few could imagine that within two decades, renewable energy would dominate new capacity additions.

The 2008 financial crisis tested Wisconsin Energy's strategy. Electricity demand plummeted as factories closed and commercial buildings went dark. The company's stock price fell from $50 to $30. Credit markets froze, threatening the massive capital program. But Wisconsin Energy's conservative balance sheet and regulated revenue stream provided stability that pure-play generation companies lacked.

As the decade ended, the limitations of deregulation were becoming apparent. California's electricity crisis of 2000-2001 had exposed the vulnerability of market-based systems to manipulation. Enron's spectacular collapse revealed the dangers of treating electricity as a financial commodity. Texas customers faced price spikes during heat waves. Pennsylvania saw reliability degradation as competitive pressures discouraged infrastructure investment.

Wisconsin's cautious approach had been vindicated. We Energies' customers enjoyed rates 20% below the national average, reliability exceeded 99.9%, and the company maintained its investment-grade credit rating throughout the financial crisis. The integrated utility model, declared obsolete by deregulation advocates, had proven remarkably resilient.

But Abdoo and his team knew bigger changes were coming. Climate change was moving from environmental concern to business imperative. The Obama administration's election in 2008 signaled likely carbon regulations. Natural gas from hydraulic fracturing was revolutionizing power generation economics. And renewable energy costs were beginning their dramatic decline.

The company needed scale to navigate these challenges. In 2010, Wisconsin Energy began exploring what would become its most transformative deal: the acquisition of Integrys Energy Group. It would take five years to complete, but when it did, it would create one of America's premier regulated utilities, with the size and scope to thrive in an increasingly complex energy landscape.

V. The Integrys Mega-Merger & Birth of Modern WEC (2014-2015)

Gale Klappa was standing in the nineteenth-floor boardroom of Wisconsin Energy's downtown Milwaukee headquarters on a gray morning in June 2014, looking out at Lake Michigan's choppy waters. In two hours, he would announce the largest acquisition in Wisconsin corporate history—a $9.1 billion deal to acquire Integrys Energy Group. The presentations were ready, the financing lined up, the regulatory strategy mapped out. But Klappa, who'd succeeded Abdoo as CEO in 2004, knew that deals of this magnitude were won or lost in execution, not announcement.

"This isn't just about getting bigger," Klappa told his assembled team of executives, bankers, and lawyers. "It's about creating a utility with the scale and capabilities to lead the energy transformation that's coming whether we're ready or not."

The path to this moment had been anything but straightforward. Integrys itself was the product of a 2007 merger between Wisconsin Public Service Corporation and Peoples Energy Corporation, creating a multi-state utility serving customers from Wisconsin's Fox Valley to Chicago's North Shore. But integration challenges, regulatory setbacks, and the 2008 financial crisis had left Integrys struggling. Its stock had underperformed, its non-utility energy marketing business was bleeding cash, and activist investors were circling.

For Wisconsin Energy, Integrys represented a once-in-a-generation opportunity. The combined company would serve 4.4 million customers across four states, own and operate $30 billion in assets, and generate revenues approaching $12 billion annually. It would vault Wisconsin Energy from the ranks of mid-sized regional utilities into the big leagues, competing with the Exelons and Dominions of the world.

The deal structure was elegant in its simplicity: Wisconsin Energy would pay $71.47 per Integrys share, a 17% premium to the pre-announcement price. The total transaction value of $9.1 billion included $5.8 billion in equity and the assumption of $3.3 billion in Integrys debt. Financing would come from a combination of cash, new debt, and $1.2 billion in common stock issued to Integrys shareholders.

But the real complexity lay in execution. The merger required approval from four state utility commissions—Wisconsin, Illinois, Michigan, and Minnesota—each with different priorities, processes, and political dynamics. The Federal Energy Regulatory Commission would scrutinize market power implications. The Department of Justice would examine antitrust concerns. Environmental groups would demand clean energy commitments. Consumer advocates would fight for rate protections.

The regulatory campaign was orchestrated with military precision. Wisconsin Energy deployed teams to each state capital, hired local counsel who knew the commissioners and staff, engaged with community groups and elected officials. The message was carefully calibrated for each audience: operational efficiencies would benefit ratepayers, increased scale would support infrastructure investment, local management would be maintained, no mass layoffs were planned.

In Wisconsin, the pitch emphasized home-state pride—creating a Fortune 500 company headquartered in Milwaukee at a time when corporate headquarters were fleeing the Midwest. In Illinois, where Peoples Gas had been struggling with a controversial pipeline replacement program, Wisconsin Energy promised fresh capital and better project management. In Michigan and Minnesota, the focus was on maintaining local autonomy while accessing greater resources.

The numbers were compelling. Wisconsin Energy projected $700 million in synergies over five years, primarily from corporate overhead reduction, supply chain optimization, and financing savings. The combined company would have the balance sheet strength to fund $12 billion in infrastructure investment over five years without diluting shareholders. Credit rating agencies indicated the merged entity would maintain investment-grade ratings.

But numbers alone don't close deals of this magnitude. The human element was crucial. Klappa personally met with every Integrys board member, addressing concerns about Milwaukee versus Chicago control, management structure, and cultural fit. Key Integrys executives were offered retention packages and meaningful roles in the combined company. Union contracts were honored, pension obligations maintained.

The integration planning was exhaustive. Fifteen working teams covering everything from IT systems to fleet management spent months mapping out Day One readiness and long-term consolidation. The companies discovered unexpected synergies: Integrys's expertise in gas distribution complementing Wisconsin Energy's electric generation strength, Wisconsin Energy's renewable development capabilities matching Integrys's transmission assets.

The regulatory approval process was a marathon. Wisconsin's Public Service Commission held twelve days of hearings, reviewing 15,000 pages of testimony and exhibits. Illinois focused on Peoples Gas's troubled pipeline program, extracting commitments for enhanced oversight and cost controls. Michigan and Minnesota, with smaller customer bases, were primarily concerned about maintaining local service quality and employment.

Environmental groups initially opposed the deal, concerned it would entrench fossil fuel infrastructure. Wisconsin Energy responded with unprecedented clean energy commitments: retiring older coal plants, investing in renewable generation, and supporting energy efficiency programs. The Sierra Club, while not endorsing the merger, withdrew its opposition after securing specific carbon reduction targets.

The financing was equally complex. In volatile markets still recovering from the financial crisis, Wisconsin Energy had to maintain financial flexibility while avoiding excessive dilution. The solution was a multi-tranche offering: $800 million in long-term bonds at historically low rates, a $1.5 billion bridge facility for short-term needs, and a measured equity issuance program to maintain balance sheet strength.

On June 29, 2015, after eighteen months of negotiations, regulatory proceedings, and integration planning, the deal closed. Wisconsin Energy Corporation became WEC Energy Group, a name change that signaled the company's evolution from a Wisconsin-centric utility to a regional energy leader. The Milwaukee headquarters was maintained, but operations centers in Green Bay, Chicago, and Minneapolis ensured local presence.

The first-year results exceeded expectations. Synergy capture ran ahead of schedule, hitting $180 million versus a $140 million target. Customer satisfaction scores improved across all service territories. The stock price rose 15%, outperforming the utility index. Credit ratings were affirmed at A- by Standard & Poor's and A3 by Moody's.

But the real victory was strategic positioning. WEC Energy Group now had the scale to invest in grid modernization, the geographic diversity to spread regulatory risk, the financial strength to navigate the energy transition, and the operational expertise to integrate renewable resources while maintaining reliability.

The Integrys merger also brought unexpected assets. Wisconsin Public Service's century-old history—founded in 1883 to provide electricity to the booming paper mills of the Fox River Valley—added gravitas. Peoples Energy's origins dated to 1855, making it older than the City of Chicago itself. These weren't just utilities; they were institutions woven into the fabric of their communities.

The cultural integration proved surprisingly smooth. Both companies shared Midwestern values: operational excellence, customer focus, community engagement, and financial conservatism. The jokes about "Wisconsin nice" meeting "Chicago tough" quickly gave way to mutual respect and collaboration.

As 2015 ended, WEC Energy Group stood transformed. It was now the eighth-largest electric and gas distribution company in the United States by market capitalization. It served major metropolitan areas (Milwaukee, Chicago) and rural communities alike. It operated everything from nuclear plants to wind farms, from interstate gas pipelines to neighborhood distribution lines.

More importantly, it had the scale and capabilities to lead rather than follow the energy transformation. The age of the small, state-focused utility was ending. The future belonged to companies with the resources to invest billions in infrastructure, the expertise to integrate complex technologies, and the financial strength to weather regulatory and market volatility. WEC Energy Group had positioned itself to be one of those winners.

VI. The Clean Energy Transformation (2015-Present)

The email arrived at 3:47 AM on a Tuesday morning in March 2021. Chuck Matthews, WEC Energy Group's VP of Generation, was already awake, monitoring the MISO grid as an arctic blast sent temperatures plummeting to -30°F across Wisconsin. The message was from the plant manager at Pleasant Prairie: "Unit 2 just tripped offline. Frozen coal. We're done."

Matthews wasn't surprised. Pleasant Prairie, once the crown jewel of Wisconsin's coal fleet, had become a liability. The economics that once made coal king had reversed completely. Natural gas was cheaper, renewable energy was now cost-competitive even without subsidies, and the social license to operate coal plants was evaporating. Within six months, Pleasant Prairie would close permanently, marking the end of an era and the acceleration of WEC's clean energy transformation.

The transformation had actually begun years earlier, though few recognized it at the time. In 2015, shortly after the Integrys merger closed, Gale Klappa made a bold announcement: WEC Energy Group would reduce carbon emissions 40% below 2005 levels by 2030. Environmental groups scoffed—it wasn't aggressive enough. Investors worried—it was too aggressive. But Klappa and his team had run the numbers. The economics of energy were shifting faster than either activists or analysts realized. By 2020, WEC had not just met but exceeded that original 40% reduction goal—a decade early. After exceeding the firm's original goal of cutting carbon emissions 40% by 2030 from 2005 levels, WEC Energy Group established a new 2030 target of reducing emissions 70% and becoming carbon neutral by 2050. Early retirement of more than 1,800 megawatts of coal power aided in early emissions accomplishment. The company immediately set more aggressive targets: 60 percent reduction in carbon emissions by 2025 from its electric generation fleet and an 80 percent reduction by the end of 2030.

The speed of change was breathtaking. Between 2018 and 2021, WEC retired nearly 2,500 megawatts of coal-fired generation. Pleasant Prairie's 1,190 megawatts went offline. The Pulliam Plant in Green Bay shut down after 65 years of operation. Edgewater Unit 4, once the pride of Sheboygan, fell silent. Each closure was a community trauma—hundreds of jobs lost, tax bases eroded, identities challenged. WEC worked to soften the blow with retraining programs, economic development initiatives, and gradual transitions, but the pain was real. The renewable buildout was equally dramatic. As the largest renewable energy investor in the state, WEC knew the importance of clean energy. Projects like the Paris Solar-Battery Park maintained reliability, delivered significant savings to customers and supported the goals of the Governor's Task Force on Climate Change. The Paris Solar-Battery Park was part of the company's plans to invest $2 billion in new solar, wind and battery storage projects by 2025.

The Badger Hollow Solar Park, which went online in November 2020, became Wisconsin's first large-scale solar energy park. The 150-megawatt facility sprawled across 1,000 acres of former farmland in Iowa County, its 300,000 panels tracking the sun from dawn to dusk. Local farmers who leased their land for the project earned more from solar than they ever had from corn or soybeans.

But the real innovation was happening at the intersection of renewable energy and grid stability. WEC's $28 billion five-year capital plan, the largest in the company's history, included more than $9.1 billion in new renewable investments in solar, wind and battery storage across its utilities and WEC Infrastructure business between 2025 and 2029. These weren't just generation assets; they were grid resources that could provide frequency regulation, voltage support, and black-start capability.

The hydrogen experiments were particularly intriguing. In the fall of 2022, WEC successfully led a first-of-its-kind hydrogen power test. During two weeks of testing, hydrogen and natural gas were tested in blends up to 25%/75% by volume to power one of the generating units that serves customers of Upper Michigan Energy Resources, a WEC Energy Group subsidiary. The testing was performed on an 18-megawatt unit that uses a technology known as RICE—reciprocating internal combustion engines. The RICE unit was continually monitored during the test to measure performance, output and emissions data.

The results were promising. The hydrogen blend burned cleaner than pure natural gas, with lower nitrogen oxide emissions. The equipment handled the fuel mix without modification. Most importantly, it proved that existing natural gas infrastructure could potentially be repurposed for hydrogen as the technology matured and costs declined.

Natural gas itself became a bridge fuel, though environmental groups bristled at the term. WEC built new combined-cycle plants that could ramp up quickly to complement intermittent renewables. These weren't your father's gas turbines—they achieved efficiency rates approaching 60%, used advanced emissions controls, and were designed for eventual conversion to hydrogen or carbon capture.

The regulatory landscape evolved to support the transition. Wisconsin's Public Service Commission approved performance-based ratemaking that rewarded utilities for achieving environmental goals, not just building assets. Illinois implemented a zero-emission credit program that valued carbon-free generation. Michigan and Minnesota adopted renewable portfolio standards requiring increasing percentages of clean energy.

Customer expectations shifted dramatically. Large industrial customers—from paper mills to data centers—demanded renewable energy to meet their own sustainability commitments. Residential customers installed rooftop solar, battery storage, and electric vehicle chargers, transforming from passive consumers to active participants in the grid. WEC had to evolve from a one-way power delivery company to a platform managing multidirectional energy flows.

The financial implications were profound. Traditional utility economics assumed 30-40 year depreciation schedules for power plants. Now, coal plants were being retired after 20 years, creating stranded assets. But renewable energy, with minimal fuel costs and declining capital costs, offered a different value proposition. Once built, a wind farm or solar array could generate electricity at near-zero marginal cost for decades.

In December 2024, the transformation received a massive boost. The Biden administration offered WEC Energy Group Inc.'s Wisconsin subsidiary as much as $2.5 billion in financing for the construction of renewable power and battery storage projects. The Energy Department's conditional loan guarantee to Wisconsin Electric Power Co. would be used to fund the addition of more than 1,650 megawatts of utility-scale projects that are expected to include wind, solar, energy storage and hydropower.

This federal support validated WEC's strategy and provided low-cost capital for the energy transition. But it also raised questions about the durability of clean energy policies across changing administrations, the role of government in energy markets, and whether ratepayers or taxpayers should bear transition costs.

As 2024 ended, WEC stood at an inflection point. In support of its goal to reduce carbon emissions from electric generation 60% by 2025 and 80% by 2030, WEC was planning to eliminate coal as an energy source by the end of 2032 and have a carbon-neutral electric generation fleet by 2050. The company that had pioneered pulverized coal technology a century earlier was now leading the transition away from it.

The transformation wasn't complete—far from it. Coal still provided baseload power on the coldest winter nights. Natural gas remained essential for grid stability. The intermittency of renewables created operational challenges. Battery storage was promising but expensive. Hydrogen was years from commercial viability.

But the direction was clear and the momentum unstoppable. WEC Energy Group had committed to a clean energy future, not from ideological zeal but from economic pragmatism. The numbers no longer supported fossil fuels. The technology had reached inflection points. Customers, regulators, and investors all pointed the same direction. The only question was how fast the transition would occur and whether WEC could maintain reliability and affordability along the way.

VII. Business Model & Financial Architecture

Scott Lauber was presenting to a room full of portfolio managers at a Barclays utility conference in New York in September 2024. The question from the Fidelity analyst was predictable but still made him pause: "How do you explain to a software engineer in Silicon Valley why a regulated utility deserves a 10% return on equity when Treasury bonds yield 4% and the S&P 500 has returned 15% annually?"

Lauber smiled. "Because when that engineer's data center needs 100 megawatts of reliable power, 24/7/365, with five-nines reliability, we're the only game in town. And when the polar vortex hits and it's minus-30 in Wisconsin, our customers don't care about our allowed return—they care that the lights stay on and the heat keeps flowing. "The question captured the fundamental tension in regulated utility investing. Unlike competitive businesses where returns fluctuate with market forces, utilities operate under a regulatory compact that provides predictable, though capped, returns in exchange for an obligation to serve all customers reliably. Understanding this model is crucial to understanding WEC's financial architecture.

The foundation is the rate base—the net book value of assets on which the utility earns a return. WEC Energy Group has approximately 34,000 stockholders of record, 7,000 employees and more than $47 billion of assets. This $47 billion asset base isn't just power plants and transmission lines; it's the ticket to earning regulated returns. Every dollar invested in approved infrastructure becomes part of the rate base, earning the allowed return on equity (ROE) set by regulators.

The allowed ROE varies by jurisdiction and reflects the regulatory environment's view of appropriate utility returns. In 2024, the industry average was approximately 9.7%, though WEC's blended rate across its four-state footprint was slightly lower due to the mix of regulatory environments. Wisconsin tends to be constructive, Illinois more challenging, Michigan moderate, and Minnesota traditionally supportive of utility investment.

The capital structure matters as much as the allowed return. Regulators typically assume a hypothetical capital structure of roughly 50% debt and 50% equity, though actual structures may vary. WEC maintains investment-grade credit ratings—critical for accessing low-cost debt markets. The spread between the cost of debt (around 4-5%) and allowed ROE (9-10%) creates the equity return that attracts investors.

WEC Energy Group (NYSE: WEC) today reported net income based on generally accepted accounting principles (GAAP) of $1.5 billion, or $4.83 per share, for 2024. This compares to earnings of $1.3 billion, or $4.22 per share, for 2023. The 14.5% earnings growth reflected not just operational excellence but the power of the regulatory model—as WEC deployed capital into its system, earnings grew predictably.

Consolidated revenues for the full year were $8.6 billion, down $293.1 million from revenues in 2023. The revenue decline might seem concerning, but it actually reflected the pass-through nature of utility economics. Lower natural gas prices meant lower customer bills but had minimal impact on WEC's earnings, which are driven by the return on rate base, not commodity prices.

The revenue requirement formula is deceptively simple: Revenue Requirement = Operating Expenses + Depreciation + Taxes + (Rate Base × Weighted Average Cost of Capital). Every component is scrutinized in rate cases, with armies of lawyers, engineers, and economists debating everything from the useful life of a transformer to the appropriate equity risk premium.

Rate cases are the crucible where financial theory meets political reality. WEC files detailed testimony supporting its requested rates, consumer advocates argue for lower returns, industrial customers negotiate special rates, and commissioners balance competing interests. The process can take 6-12 months, with outcomes rarely matching initial requests but generally landing within a predictable range.

The timing of rate cases is itself a strategic decision. File too frequently, and you're seen as greedy. Wait too long, and regulatory lag erodes returns. WEC has mastered the art of sequencing rate cases across its jurisdictions, maintaining a steady flow of rate relief while avoiding regulatory fatigue.

Capital allocation follows a clear hierarchy. First priority: maintaining and modernizing the existing system to ensure reliability. Second: growth investments in renewable generation and grid modernization that expand the rate base. Third: returning cash to shareholders through dividends. WEC's dividend yield of approximately 3.5% might seem modest, but the consistency is what matters—the company has paid dividends for over 100 years and raised them annually for the past two decades.

The dividend payout ratio of roughly 65-70% of earnings strikes a balance between returning cash to shareholders and retaining capital for growth. This self-funding model reduces reliance on external capital markets, important during periods of volatility. It also signals management's confidence in future earnings stability.

Regulatory mechanisms smooth earnings volatility. Fuel adjustment clauses pass commodity price changes directly to customers. Weather normalization adjustments protect against unseasonably mild or severe weather. Infrastructure trackers allow recovery of certain investments between rate cases. Bad debt riders recover uncollectible accounts. These mechanisms transform what could be a volatile commodity business into a predictable earnings stream.

The infrastructure investment cycle drives long-term value creation. WEC's $28 billion five-year capital plan translates directly into rate base growth of 6-7% annually. Apply a 10% allowed ROE to that growing rate base, layer in modest operating leverage, and you get earnings growth of 5-7% annually—not spectacular, but remarkably consistent.

This consistency attracts a specific investor base. Pension funds love the predictable cash flows that match long-term liabilities. Income-focused retail investors appreciate the dividend stability. ESG funds increasingly recognize utilities as essential to the energy transition. Even growth investors are discovering that steady 5-7% earnings growth compounded over decades creates substantial value.

The comparison to other utilities reveals WEC's strengths. Its pure-play regulated model avoids the volatility of merchant generation. The four-state footprint provides regulatory diversification without unwieldy complexity. The focus on electric and gas distribution, the most stable utility segments, reduces technology risk. The strong balance sheet provides flexibility for opportunistic investments.

But the model has limitations. Returns are capped by regulation, regardless of operational excellence. Growth depends on regulatory approval, not market dynamics. Capital intensity means constant funding needs. Technological disruption—from distributed generation to hydrogen—threatens traditional utility economics.

The energy transition adds complexity. Retiring coal plants before they're fully depreciated creates stranded costs. Building renewable generation requires massive upfront capital with uncertain cost recovery. Grid modernization investments may not earn traditional returns. Electrification could boost demand, but also brings new competitors.

The financial architecture must evolve while maintaining its fundamental stability. Performance-based ratemaking ties returns to outcomes, not just investments. Green bonds fund renewable projects at attractive rates. Tax equity partnerships monetize renewable tax credits. Power purchase agreements transfer development risk while maintaining cash flows.

The ultimate measure of the model's success is total shareholder return. Over the past decade, WEC has delivered annual returns of approximately 10-12%, matching or exceeding the S&P 500 with far lower volatility. The combination of dividend yield (3-4%) and earnings growth (5-7%) creates a compelling value proposition for risk-adjusted returns.

As Lauber concluded his presentation to the portfolio managers, he returned to the fundamental value proposition: "We're not a high-growth tech stock, and we're not trying to be. We're an essential service provider with a regulatory mandate, a protected market position, and predictable cash flows. In an uncertain world, that certainty has value. And as the energy transition accelerates, our role becomes more critical, not less."

The analysts nodded, understanding that in the casino of modern markets, utilities offer something increasingly rare: a predictable bet with favorable odds, backed by essential assets and regulatory protection. It might not be exciting, but for those who understand the model, it's beautifully boring.

VIII. Current Operations & Strategic Position

The control room at the Milwaukee headquarters looks like something from a NASA mission control—dozens of screens displaying real-time data from across WEC's four-state territory. It's 2:47 PM on a sweltering August afternoon in 2024, and the operators are orchestrating a complex ballet. A thunderstorm is rolling through Chicago, knocking out distribution lines. A wind farm in Iowa is producing at maximum capacity. The Point Beach nuclear plant is ramping down for scheduled maintenance. And a massive data center in Madison just requested an additional 50 megawatts of power—immediately.

This is the reality of running a modern multi-state utility: thousands of decisions per hour, millions of customers depending on flawless execution, and billions of dollars of infrastructure operating in perfect synchronization. WEC Energy Group (NYSE: WEC), based in Milwaukee, is one of the nation's premier energy companies, serving 4.7 million customers in Wisconsin, Illinois, Michigan and Minnesota.

The portfolio of operating companies reads like a history of Midwest utilities. We Energies, the flagship, serves southeastern Wisconsin including Milwaukee and its suburbs. Wisconsin Public Service covers the northeastern part of the state, including Green Bay and the Fox Valley. Peoples Gas provides natural gas to Chicago. North Shore Gas serves Chicago's affluent northern suburbs. Michigan Gas Utilities operates across Michigan's Lower Peninsula. Minnesota Energy Resources serves communities along the Minnesota-Wisconsin border. Upper Michigan Energy Resources powers the rugged Upper Peninsula.

Each utility maintains its local identity and relationships while benefiting from centralized functions. Procurement is consolidated—when WEC buys transformers, it buys for all utilities, leveraging scale for better prices. IT systems are standardized, reducing costs and improving cybersecurity. Best practices are shared across operations, with Wisconsin Public Service's tree-trimming innovations adopted by We Energies, and Peoples Gas's pipeline replacement techniques used in Minnesota.

The 60% ownership stake in American Transmission Company (ATC) provides a unique strategic advantage. ATC owns and operates high-voltage transmission lines across Wisconsin and Michigan's Upper Peninsula, earning regulated returns on critical infrastructure. As renewable generation proliferates in rural areas while demand concentrates in cities, transmission becomes increasingly valuable. ATC's $5 billion capital plan through 2029 will strengthen the grid while growing WEC's earnings.

The generation portfolio reflects the ongoing transition. Natural gas comprises the largest share at approximately 45% of capacity, providing flexible, dispatchable power. Coal, once dominant, has shrunk to less than 20% and continues declining. Nuclear, through the Point Beach purchase agreement, provides carbon-free baseload. Renewables—wind, solar, and hydro—are growing rapidly and will represent over 30% of capacity by 2030.

For the full year, retail deliveries of electricity — excluding the iron ore mine in Michigan's Upper Peninsula — were up by 0.5 percent. Electricity consumption by small commercial and industrial customers was 0.7 percent higher during 2024. These modest growth rates mask significant underlying shifts. Residential usage per customer continues declining due to efficiency improvements, but customer counts grow steadily. Industrial demand is rebounding as manufacturing returns to America. And new categories—data centers, electric vehicle charging, marijuana cultivation—are emerging as significant loads.

The distribution infrastructure is the unglamorous workhorse of the operation. Those 72,400 miles of electric distribution lines and 47,000 miles of gas pipelines require constant maintenance, upgrading, and expansion. Every year, WEC replaces hundreds of miles of aging pipe, thousands of poles, and countless transformers. It's invisible work—until it isn't. When a winter storm knocks out power or a gas leak forces evacuations, distribution operations leap from obscurity to headlines.

Grid modernization is transforming this traditional infrastructure into an intelligent network. Smart meters provide real-time usage data, enabling dynamic pricing and rapid outage detection. Distribution automation allows remote switching to reroute power around problems. Advanced sensors detect potential failures before they occur. It's the marriage of century-old copper wires with cutting-edge software.

The technology initiatives extend beyond traditional utility operations. WEC's investment in distributed energy resource management systems (DERMS) allows integration of customer-owned solar panels, batteries, and electric vehicles into grid operations. Virtual power plant pilots aggregate thousands of smart thermostats and water heaters into controllable demand response resources. Blockchain experiments explore peer-to-peer energy trading between neighbors with solar panels.

Customer expectations have evolved dramatically. The days of accepting multi-day outages are over. Customers expect the same digital experience from their utility as from Amazon or Netflix—mobile apps, real-time information, predictive alerts, one-click service requests. WEC has invested heavily in customer-facing technology, with mixed results. The mobile app has strong adoption, but billing system upgrades have faced challenges.

Regulatory relationships across four states require delicate balancing. Wisconsin's Public Service Commission tends toward traditional regulation with a focus on reliability and affordability. Illinois demands aggressive environmental commitments and scrutinizes every dollar of capital spending. Michigan emphasizes economic development and industrial competitiveness. Minnesota prioritizes renewable energy and energy justice for disadvantaged communities.

The stakeholder ecosystem extends far beyond regulators. Environmental groups push for faster decarbonization. Industrial customers negotiate special rates and reliability guarantees. Unions protect jobs and wages. Communities hosting power plants worry about tax base erosion as facilities close. Investors demand consistent returns. Politicians seek credit for low rates and clean energy. Managing these competing interests requires diplomatic skills rivaling the State Department.

Infrastructure investment priorities reflect this complex balancing act. The $28 billion five-year capital plan allocates roughly 40% to renewable generation, 30% to distribution infrastructure, 20% to transmission, and 10% to other investments. Every dollar is scrutinized for its impact on rates, reliability, and environmental goals.

The renewable buildout is accelerating. Two large solar farms are under construction in Wisconsin. A 200-megawatt wind farm in Illinois will come online in 2025. Battery storage projects are being deployed at substations to manage renewable intermittency. The Paris Solar-Battery Park, combining 310 megawatts of solar with 165 megawatts of battery storage, represents the future—renewable generation paired with storage to provide dispatchable clean energy.

Natural gas infrastructure remains contentious. Environmental groups oppose any gas investment as incompatible with climate goals. But gas provides essential reliability, especially during polar vortexes when renewable output drops and demand spikes. WEC's strategy threads the needle—maintaining gas infrastructure for reliability while planning for eventual transition to hydrogen or other clean fuels.

The workforce transformation is profound. Coal plant operators are retraining as wind technicians. Meter readers have become data analysts. Line workers are learning to integrate distributed solar. The company has launched apprenticeship programs with technical colleges, creating pipelines for next-generation utility workers who are as comfortable with Python code as with power lines.

Competition is emerging from unexpected quarters. Tech giants like Google and Microsoft are exploring direct renewable energy development for their data centers. Oil majors like BP and Shell are entering the electricity business. Startups are offering "utility in a box" solutions for microgrids. Tesla's solar roof and Powerwall battery threaten traditional utility economics. WEC must compete while constrained by regulation—like boxing with one hand tied.

The strategic position is strong but not unassailable. WEC controls essential infrastructure in growing markets with supportive regulation. The multi-state footprint provides diversification. The pure-play regulated model avoids merchant generation volatility. The strong balance sheet enables sustained investment. The experienced management team has navigated multiple industry cycles.

But challenges loom. Distributed generation could strand transmission and distribution assets. Electrification might not materialize as quickly as expected. Extreme weather events are increasing in frequency and severity. Cybersecurity threats grow more sophisticated. Political polarization makes long-term planning difficult.

The path forward requires strategic clarity. WEC must continue the renewable transition while maintaining reliability. It must modernize infrastructure while controlling costs. It must embrace new technologies while protecting core operations. It must serve existing customers while preparing for new demands. It must deliver consistent financial returns while investing for transformation.

As the control room operators manage another summer peak, they embody WEC's current position—one foot in the past, managing legacy infrastructure, and one foot in the future, integrating new technologies. It's a challenging balance, but one WEC has maintained for over a century. The question isn't whether they can manage today's complexity—they clearly can. The question is whether they can evolve fast enough for tomorrow's challenges.

IX. Playbook: Lessons from WEC's Evolution

The story was legendary within WEC's executive ranks. In 1999, during the height of deregulation mania, CEO Richard Abdoo was offered the chance to acquire a portfolio of merchant power plants across the country. Investment bankers promised spectacular returns. "Dick," they said, "you're leaving money on the table staying fully regulated." Abdoo's response became company lore: "I'd rather leave money on the table than leave shareholders holding the bag."

Two years later, Enron collapsed. Merchant generators went bankrupt. Companies that chased deregulation destroyed billions in shareholder value. WEC, boring and regulated, kept paying dividends and growing steadily. The lesson was clear: in utilities, patient discipline beats aggressive ambition every time.

This philosophy—patient, regulated growth—forms the foundation of WEC's playbook. Unlike tech companies that can pivot business models quarterly, utilities operate on generational timescales. A power plant built today will operate for 30-40 years. A transmission line will carry electricity for half a century. Customer relationships span lifetimes. This temporal reality shapes every strategic decision.

The power of compound growth in a regulated utility is often underestimated. WEC's 6-7% annual rate base growth might seem pedestrian compared to software companies doubling revenue yearly. But that steady growth, compounded over decades, creates enormous value. A dollar invested in WEC's rate base in 2000 has grown to over $4 today, all while generating regulated returns. It's the tortoise and hare, utility edition.

Navigating utility consolidation requires a specific expertise. WEC has completed over a dozen acquisitions, from small gas utilities to the transformative Integrys merger. The playbook is consistent: identify utilities with overlapping service territories or complementary operations, pay a fair premium that regulators will accept, capture synergies through operational integration, maintain local relationships and identities, and reinvest savings into infrastructure. It's not flashy, but it works.

The Integrys integration exemplified this approach. Rather than slash costs and centralize operations, WEC maintained local management and gradually integrated back-office functions. Customers barely noticed the change, regulators appreciated the stability, and shareholders benefited from $700 million in synergies. Compare this to botched utility mergers where aggressive cost-cutting triggered service degradation and regulatory backlash.

Managing the energy transition while maintaining reliability is perhaps the greatest challenge facing modern utilities. WEC's approach balances ambition with pragmatism. Yes, they've committed to net-zero emissions by 2050. But they're not shutting down dispatchable generation until replacements are proven. They're building renewables aggressively but maintaining gas plants for reliability. They're investing in emerging technologies but not betting the company on unproven solutions.

The key insight is that reliability trumps everything in utility operations. Customers might support clean energy in surveys, but they revolt when the lights go out. Regulators might mandate renewable targets, but they punish utilities for blackouts. WEC has learned to frame the energy transition as a reliability enhancement, not a trade-off. Modern renewables paired with storage and backed by flexible gas generation can be more reliable than aging coal plants.

Stakeholder management in utilities resembles three-dimensional chess. Every decision affects multiple constituencies with conflicting interests. Raising rates to fund infrastructure angers customers but pleases investors. Closing coal plants satisfies environmentalists but devastates host communities. Building renewables excites politicians but worries grid operators.

WEC has developed sophisticated stakeholder engagement strategies. They bring union leaders into planning discussions before announcing plant closures. They work with communities on economic transition plans years before facilities retire. They engage environmental groups on clean energy commitments while explaining reliability constraints. They educate investors on long-term value creation beyond quarterly earnings. It's exhausting but essential.

The regulatory relationship is particularly crucial. WEC treats regulators as partners, not adversaries. They share data transparently, even when it doesn't support their position. They propose reasonable rate increases rather than aggressive asks that get cut. They deliver on commitments, building trust over time. When Wisconsin regulators approved WEC's latest rate case with minimal modifications, it reflected decades of credibility-building.

Capital discipline in a capital-intensive business seems obvious but proves difficult in practice. The temptation to overbuild is strong—more assets mean more rate base mean more earnings. But WEC has learned that disciplined capital allocation creates more value than aggressive expansion. They've walked away from projects with inadequate returns. They've sold assets at peak valuations. They've returned capital to shareholders rather than chase marginal investments.

The Point Beach nuclear sale exemplified this discipline. Rather than spend billions on life extensions with uncertain regulatory recovery, they monetized the asset and secured long-term power purchase agreements. The $924 million proceeds were redeployed into higher-return renewable projects. Short-term earnings took a hit, but long-term value increased.

Scale matters enormously in modern utilities. The fixed costs of regulation, technology, and environmental compliance can crush small utilities. But spread across WEC's 4.7 million customers, these costs become manageable. Scale provides negotiating leverage with suppliers, funding capacity for major projects, expertise depth for complex challenges, and geographic diversification against local economic downturns.

This recognition drives WEC's consolidation strategy. They're not trying to become a national utility—the regulatory complexity would be overwhelming. But regional scale within the Midwest provides optimal balance between size and manageability. They can standardize operations across similar markets while maintaining local relationships.

ESG leadership has evolved from corporate responsibility to competitive advantage. WEC's early commitment to carbon reduction seemed costly when announced. But it positioned them perfectly for ESG-focused investment flows, government infrastructure funding, technology partnerships with clean energy leaders, and talent recruitment among environmentally conscious workers.

The $2.5 billion Department of Energy loan guarantee for renewable projects validates this strategy. Government support flows to companies demonstrating environmental leadership. WEC's track record of exceeding carbon reduction targets made them an obvious recipient. Companies that fought environmental regulations are now scrambling to catch up.

Building trust through consistent execution might be WEC's greatest strength. They've met or exceeded earnings guidance for 20 consecutive years. They've raised dividends annually since 2004. They've achieved top-quartile reliability metrics across all service territories. They've delivered on every major environmental commitment. This consistency creates a virtuous cycle—trust enables regulatory flexibility, which supports strategic investments, which generate returns, which build more trust.

The human element often gets overlooked in utility strategy. WEC has cultivated a distinct culture combining engineering precision with Midwestern pragmatism. They promote from within, developing deep institutional knowledge. They celebrate operational excellence, not financial engineering. They measure success in decades, not quarters. This culture provides stability through industry turbulence.

The technology adoption strategy balances innovation with reliability. WEC isn't trying to be the first adopter of every new technology. They let others debug innovations, then deploy proven solutions at scale. They participated in early smart meter pilots, learned from others' mistakes, then rolled out successfully. They're following the same playbook with battery storage, hydrogen, and grid modernization technologies.

Risk management in utilities requires particular sophistication. Commodity price risk, weather variability, regulatory uncertainty, technology disruption, and cybersecurity threats all require different mitigation strategies. WEC has built a comprehensive risk management framework that identifies threats early, quantifies potential impacts, develops mitigation strategies, and monitors continuously.

The portfolio approach to generation resources exemplifies this risk management. Rather than bet everything on one technology, they maintain a diverse mix that provides optionality. If natural gas prices spike, they have renewables and nuclear. If renewable output drops, they have dispatchable gas. If carbon prices emerge, they have clean resources. It's more expensive than going all-in on one technology, but far less risky.

Looking across WEC's century-plus history, the consistent theme is evolution, not revolution. They didn't abandon streetcars overnight for electric distribution. They didn't shut all coal plants the day they committed to clean energy. They don't chase every new technology or business model. Instead, they evolve deliberately, maintaining stability while adapting to change.

This evolutionary approach frustrates both aggressive investors seeking higher returns and environmental activists demanding immediate transformation. But it has created enormous value for patient shareholders while maintaining reliable service for millions of customers. In an industry where the stakes—keeping the lights on and heat flowing—couldn't be higher, WEC's playbook of patient, disciplined, incremental progress has proven remarkably effective.

The lesson for investors is clear: in utilities, boring is beautiful. The companies that survive and thrive are those that resist the temptation of aggressive expansion, maintain operational excellence through all cycles, build trust with all stakeholders over decades, and evolve steadily rather than disrupt radically. WEC has mastered this playbook, creating a template for successful utility management in an era of unprecedented change.

X. Bear & Bull Cases

Bear Case: The Risks That Keep Management Awake

Tom Richardson, WEC's Chief Risk Officer, was presenting to the board's audit committee on a cold February morning in 2024. His slide deck was titled "Black Swans and Gray Rhinos: Existential Threats to the Utility Model." The directors, seasoned executives from various industries, leaned forward. Richardson wasn't known for hyperbole.

"Ladies and gentlemen," he began, "our business model has survived for over a century. But the convergence of technological, regulatory, and societal changes could fundamentally challenge our existence within the next decade."

The regulatory risk across multiple jurisdictions tops the concern list. WEC operates in four states, each with different political climates, regulatory philosophies, and stakeholder dynamics. A single adverse regulatory decision—say, Illinois disallowing recovery of gas infrastructure investments—could destroy billions in shareholder value overnight. The Illinois Commerce Commission's recent disallowance of certain capital expenditures under the QIP rider, resulting in charges against earnings, exemplifies this risk.

Political polarization amplifies regulatory uncertainty. Wisconsin might have a Republican legislature and Democratic governor, creating gridlock on energy policy. Illinois swings between pro-business and populist sentiment. Michigan's industrial base demands cheap power while environmental groups push for aggressive clean energy mandates. Minnesota's progressive politics favor renewables but rural communities depend on reliable, affordable energy. Threading this political needle becomes harder as positions become more entrenched.

Stranded asset risk from the accelerated clean energy transition represents potentially the largest financial threat. WEC still has billions of dollars of coal and natural gas infrastructure on its books. If decarbonization accelerates faster than planned—driven by technology breakthroughs, policy changes, or social pressure—these assets could become worthless before they're fully depreciated. The Pleasant Prairie closure left hundreds of millions in unrecovered investments. Multiply that across the entire fossil fleet, and the numbers become staggering.

The natural gas business faces existential questions. Environmental groups increasingly oppose not just new gas infrastructure but the entire concept of gas utilities. Cities are banning gas hookups in new construction. Electrification mandates could strand WEC's 47,000 miles of gas distribution pipes. Yet WEC continues investing billions in gas infrastructure, betting that hydrogen or renewable natural gas will extend its useful life. If that bet proves wrong, the write-offs could be catastrophic.

Rising interest rates impact capital-intensive businesses disproportionately. Utilities are essentially leveraged bets on interest rate spreads—borrow at X%, earn regulated returns of X+5%. When rates rise, borrowing costs increase immediately, but regulated returns adjust slowly through rate cases. The math is brutal: a 200 basis point increase in interest rates could reduce earnings by 10-15% until new rates are approved. With $47 billion in assets requiring continuous refinancing, interest rate sensitivity is extreme.

The Federal Reserve's recent hiking cycle demonstrated this vulnerability. WEC's borrowing costs increased by $200 million annually, but rate relief lagged by 12-18 months. In a sustained high-rate environment, utilities could face a vicious cycle: higher costs require rate increases, which face political resistance, leading to compressed margins and reduced infrastructure investment, triggering reliability issues and regulatory penalties.

Electrification uncertainty clouds growth projections. Bulls assume massive electricity demand growth from electric vehicles, heat pumps, and industrial electrification. But adoption could disappoint. EVs remain expensive despite subsidies. Heat pumps struggle in extreme cold. Industrial customers might choose efficiency over electrification. If electricity demand grows at 0.5% annually instead of the projected 2-3%, WEC's growth investments would generate inadequate returns.

Competition from distributed generation poses a fundamental threat to the utility model. As solar-plus-storage costs decline, customers can increasingly self-generate. Every rooftop solar installation reduces utility revenue while the fixed costs of maintaining the grid remain. It's the utility death spiral: fewer kilowatt-hour sales across the same infrastructure base require higher rates, encouraging more customers to self-generate, necessitating even higher rates.