Warner Bros. Discovery: The Streaming Wars' Most Controversial Merger

I. Introduction & Episode Roadmap

Picture this: It's April 2022, and David Zaslav stands before a packed auditorium at Warner Bros.' iconic Burbank lot. The former Discovery CEO, now helming a $130 billion media colossus, promises to unite "the best of both worlds"—Discovery's unscripted reality empire with Warner's century of Hollywood storytelling. Fast forward to late 2024: that same company announces it's splitting in two, its stock down over 70% from merger highs, carrying $34.6 billion in net debt against $39.3 billion in revenue.

How did we get here? How did a company that owns Batman, Harry Potter, HBO's prestige dramas, CNN's news empire, and Discovery's reality TV juggernaut become Wall Street's favorite punching bag? The answer lies in a century-long saga of ambition, miscalculation, and the brutal economics of entertainment's digital transformation.

This is not just another failed merger story. It's the story of how Hollywood's golden age studio system collided with cable TV's glory days, then crashed headfirst into the streaming revolution. It's about legendary moguls from Jack Warner to Steve Ross to David Zaslav, each believing they'd cracked the code on media's future. It's about debt—mountains of it—used to finance dreams that reality couldn't support.

The fundamental question we're exploring: Was the Warner Bros. Discovery merger doomed from the start, a desperate attempt by two cable-era companies to stay relevant? Or was it the right strategy executed at the worst possible time, when interest rates soared, streaming losses mounted, and the entire entertainment industry discovered that maybe, just maybe, Netflix's model wasn't replicable?

Our journey spans a full century—from four immigrant brothers screening silent films in Pennsylvania coal towns to a Nasdaq-listed behemoth announcing its own breakup. We'll dissect every major merger, from the defensive Time Warner combination that fought off raiders, to the AOL disaster that vaporized $200 billion in value, to AT&T's bungled attempt at convergence, culminating in Discovery's audacious bet to swallow a company three times its size.

Along the way, we'll uncover patterns that repeat like a broken reel: the allure of vertical integration, the clash between creative cultures and financial discipline, the siren song of new technology that promises to change everything. We'll meet the dealmakers and the dreamers, the accountants and the auteurs, all convinced they held the winning hand in media's high-stakes poker game.

Three key themes will guide our analysis. First, the transformation of legacy media—how companies built for theaters and cable boxes struggle to reinvent themselves for smartphones and smart TVs. Second, the role of debt-fueled M&A in media consolidation, where borrowed billions become both weapon and burden. Third, the unforgiving economics of streaming, where the old rules of windowing and syndication collapse into an all-you-can-eat buffet that's surprisingly hard to monetize.

By the end, you'll understand not just what happened to Warner Bros. Discovery, but what it means for the future of entertainment itself. Because this isn't just a business story—it's about who controls the stories we tell ourselves, how we consume them, and whether the old guardians of culture can survive in an age where tech giants write billion-dollar checks for content without blinking.

The clock is ticking toward 2026, when Warner Bros. Discovery will cease to exist as we know it, splitting into two companies that might finally deliver what one couldn't: sustainable profits and a clear strategic vision. Whether that's vindication or admission of failure depends on your perspective. But one thing's certain—this is a story worthy of Hollywood itself, complete with ambition, hubris, and a ending that nobody saw coming.

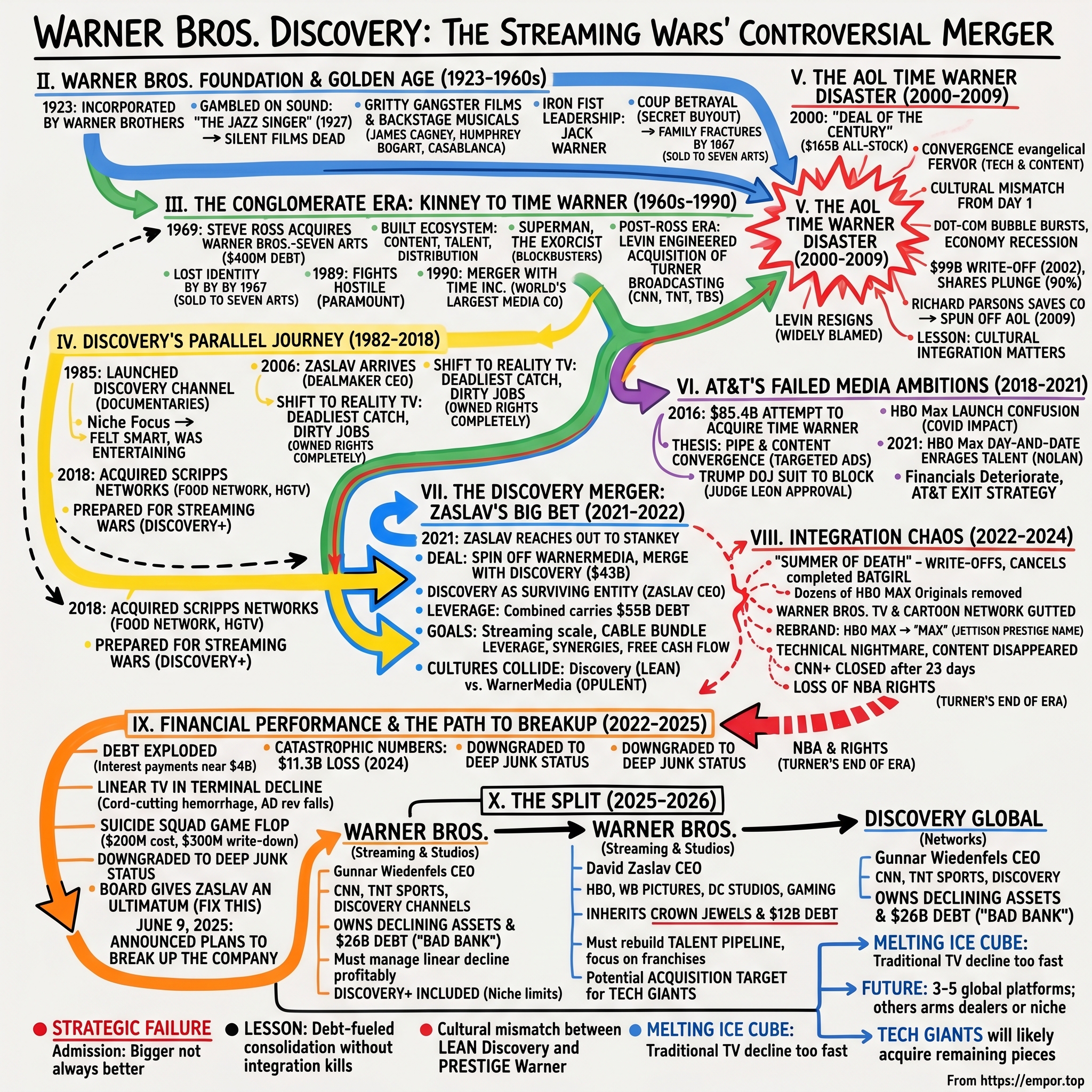

II. Warner Bros. Foundation & Hollywood's Golden Age (1923–1960s)

The story begins not in Hollywood's sun-drenched boulevards but in the gritty industrial towns of Pennsylvania and Ohio, where four Polish-Jewish immigrant brothers—Harry, Albert, Sam, and Jack Warner—scraped together $20,000 to purchase their first movie projector in 1903. They traveled from town to town, screening films in rented halls and carnival tents, learning the entertainment business from the ground up. Harry, the eldest, handled the money. Albert managed distribution. Sam, the technical wizard, ran the projectors. And Jack, the youngest and most aggressive, had dreams that stretched far beyond those makeshift theaters.

By April 4, 1923, when Warner Bros. Pictures officially incorporated, the brothers had already survived multiple near-bankruptcies and learned a crucial lesson: in entertainment, you either innovate or die. They'd watched competitors with deeper pockets dominate the industry's best talent and theater chains. But the Warners had something their rivals lacked—a gambler's instinct for technology and a working-class sensibility that would define their studio's identity for decades.

The company's first major gamble nearly destroyed them. In 1925, while established studios like MGM and Paramount were printing money with silent films, the Warners bet everything on a curiosity called Vitaphone—a sound synchronization system that nobody wanted. They mortgaged their studio, their homes, even borrowed against life insurance policies. Harry Warner famously dismissed the innovation even as he funded it: "Who the hell wants to hear actors talk?"

Then came October 6, 1927, and everything changed. "The Jazz Singer," starring Al Jolson, premiered at the Warner Theatre in New York. When Jolson looked directly at the camera and declared, "You ain't heard nothin' yet!"—his voice booming through the theater—the audience erupted. It wasn't just the novelty of synchronized sound; it was the emotional power of hearing a performer's voice matched to their image. The film grossed $3.9 million (roughly $65 million today) against a $422,000 budget. Within two years, silent films were dead, and Warner Bros. had leaped from industry afterthought to major studio.

But tragedy struck at the moment of triumph. Sam Warner, the brother who'd championed sound technology, died of a brain infection one day before "The Jazz Singer's" premiere. His death marked the beginning of fractures that would define the studio's internal dynamics. Harry, devastated by Sam's loss, became increasingly conservative. Jack, emboldened by success, grew more ruthless and ambitious. The tension between art and commerce, between family and business, would simmer for decades.

The 1930s established Warner Bros. as Hollywood's social conscience—and its most reliable profit machine. While MGM produced glossy musicals and Paramount crafted sophisticated comedies, Warner Bros. gave Depression-era audiences what they craved: gritty gangster films, backstage musicals about struggling performers, and social dramas that acknowledged economic hardship. James Cagney shoving a grapefruit in Mae Clarke's face in "The Public Enemy." Edward G. Robinson's psychotic Rico in "Little Caesar." These weren't just movies; they were reflections of American anxiety, packaged as entertainment.

The studio system Warner Bros. perfected was a marvel of vertical integration. They owned the entire pipeline: production facilities in Burbank, distribution networks across the country, and by 1928, a chain of 250 theaters. They signed actors, directors, and writers to long-term contracts, essentially owning their creative output. Stars like Bette Davis, Humphrey Bogart, and Joan Crawford weren't just employees—they were assets, carefully managed and ruthlessly exploited.

Jack Warner ran the studio with an iron fist wrapped in a glad hand. He was notorious for his terrible jokes, his right-wing politics, and his willingness to betray anyone for a buck. During the 1947 House Un-American Activities Committee hearings, he eagerly named names of suspected communists, destroying careers to protect his studio. Yet he also green-lit "Casablanca" when other studios passed, recognizing that a wartime romance could capture the zeitgeist. The film, rushed into production to capitalize on the Allied invasion of North Africa, became the studio's defining achievement—a perfect blend of commerce and art that still generates revenue eight decades later.

The post-war era brought existential challenges. In 1948, the Supreme Court's Paramount Decree forced studios to divest their theater chains, breaking the vertical integration that guaranteed profits. Television emerged as an existential threat, keeping audiences home. But the deepest wound was self-inflicted. In 1956, Jack Warner orchestrated a boardroom coup that would haunt the studio's culture for generations.

Harry Warner had always insisted the studio remain a family business. But Jack, seeing an opportunity when Harry was hospitalized, secretly bought out his brothers' shares for $22 million, gaining complete control. When Harry discovered the betrayal, he reportedly never spoke to Jack again, dying two years later. Albert, disgusted, retreated from Hollywood. Jack Warner now ruled alone, but he'd destroyed the family bonds that built the empire.

Under Jack's sole leadership through the 1960s, Warner Bros. produced both triumphs and disasters. "My Fair Lady" won Best Picture in 1964, but cost so much it barely broke even. "Who's Afraid of Virginia Woolf?" pushed creative boundaries but alienated conservative audiences. The studio that once understood exactly what Americans wanted to see had lost touch with a changing culture. By 1967, when Jack finally sold his stake to Seven Arts Productions for $32 million, Warner Bros. wasn't just losing money—it had lost its identity.

The Warner brothers built more than a studio; they created a template for how outsiders could conquer Hollywood through technology, chutzpah, and an understanding of what ordinary people wanted to watch. Their legacy—hundreds of films, thousands of jobs, innovations that transformed entertainment—would outlive family feuds and financial struggles. But as Jack Warner cleared out his office in 1967, one question lingered: could Warner Bros. survive without a Warner?

III. The Conglomerate Era: Kinney to Time Warner (1960s–1990)

Steve Ross didn't know anything about making movies when his father-in-law handed him control of a funeral parlor business in 1954. But the Brooklyn-born entrepreneur understood something more important: how seemingly unrelated businesses could feed each other. By 1969, Ross had transformed that funeral parlor into Kinney National Service, a conglomerate spanning parking lots, cleaning services, and rental cars. His next acquisition would be his most audacious—Warner Bros.-Seven Arts, the struggling movie studio, purchased for $400 million in borrowed money.

Hollywood's old guard was horrified. Here was this parking lot magnate, this son of Jewish immigrants who grew up in Brooklyn's rough neighborhoods, taking over Jack Warner's throne. At the first meeting with Warner Bros. executives, Ross showed up in a pink shirt and no tie—scandalous in buttoned-down Burbank. But Ross had a vision that the Hollywood establishment couldn't see: entertainment wasn't about individual movies or shows, it was about building an ecosystem where content, talent, and distribution reinforced each other.

Ross immediately did something unthinkable in cost-conscious Hollywood—he started spending lavishly on relationships. Private jets for talent. Million-dollar bonuses for executives. Legendary parties at his East Hampton estate where Barbra Streisand mingled with investment bankers. "I don't care about budgets," Ross told his studio chief. "I care about great movies and happy talent." This philosophy was the opposite of Jack Warner's penny-pinching tyranny, and it worked. Within three years, Warner Communications (reincorporated from Kinney National in 1972) was producing "The Exorcist," "All the President's Men," and "Superman"—blockbusters that redefined commercial filmmaking.

But Ross's real genius lay in recognizing that content was becoming software. In 1976, he bought Atari for $28 million, seeing video games as another form of entertainment that Warner could dominate. By 1982, Atari was generating more profit than the entire movie studio. When MTV launched in 1981, Warner's record labels suddenly had a 24-hour commercial for their artists. Ross didn't just build a media company; he built a machine that turned culture into cash.

The 1980s brought a new kind of threat: corporate raiders who saw Warner's collection of assets as worth more in pieces than whole. By 1989, Ross faced his greatest challenge when Paramount Communications (formerly Gulf+Western) launched a hostile takeover bid. The attack came from Martin Davis, a vulgar, combative executive who'd transformed a manufacturing conglomerate into a media powerhouse. Davis offered $175 per share for Time Inc., the publishing giant Ross had been courting as a defensive merger partner.

The Time Inc. merger was Ross's masterpiece of financial engineering and cultural destruction. Time's button-down magazine editors—who saw themselves as guardians of American journalism—were horrified at merging with Hollywood's flashiest studio. But Ross sold them on a vision: combining Time's prestigious brands (Time magazine, Sports Illustrated, Fortune) with Warner's entertainment assets would create an unassailable media fortress. The merger, completed in 1990 as a $14 billion stock swap, created the world's largest media company.

Ross promised Time executives equal representation, but everyone knew who really ran things. He controlled the board through loyalty and largesse, keeping Time's journalists at arm's length from Warner's entertainment operations. The cultures never meshed—Time's church-and-state separation between editorial and business crashed against Warner's everything-is-negotiable ethos. One Time executive described board meetings as "watching Presbyterians try to dance with Jews."

The promised synergies proved elusive. Time's magazines didn't suddenly start selling Warner movies, and Warner's studios didn't create content specifically for Time's publications. But Ross had achieved his real goal: building a company too big to raid, too diversified to fail. When he died of prostate cancer in December 1992, Warner Communications had grown from a $400 million acquisition to a company worth $25 billion.

The post-Ross era exposed the empire's shaky foundations. Gerald Levin, the Time Inc. executive who succeeded Ross, lacked his predecessor's charisma and deal-making instincts. Yet Levin harbored even grander ambitions. In 1996, he engineered the $7.5 billion acquisition of Turner Broadcasting System, bringing Ted Turner's cable networks—CNN, TNT, TBS—into the fold. Turner, the "Mouth of the South" who'd built a cable empire from his father's billboard company, became Time Warner's largest individual shareholder and vice chairman.

Turner's assets were everything broadcast networks weren't: always on, advertisement-heavy, and perfectly suited for cable's emerging dominance. CNN had redefined news as 24-hour entertainment. TNT and TBS grabbed old movies and TV shows—much of it from Warner's own library—and repackaged them for cable audiences. The deal made strategic sense, combining content creation with cable distribution.

But Turner himself was a wild card. Bipolar, brilliant, and utterly uncontrollable, he'd show up to board meetings in jeans, rail against corporate bureaucracy, then disappear to his Montana ranch for weeks. He clashed constantly with Levin, seeing him as a bloodless technocrat who didn't understand entertainment. "We're in the emotion business," Turner would shout during meetings. "You can't run it like a fucking insurance company!"

By 1999, Time Warner looked unstoppable. It owned Warner Bros. studios, HBO's premium cable network, Time Inc.'s magazines, Turner's cable channels, Warner Music Group, and chunks of cable systems. Revenue exceeded $27 billion. The stock had tripled since Ross's death. Levin, the unlikely emperor of this media kingdom, started looking for the next big thing that would cement his legacy.

He found it in a Dulles, Virginia office park, where a company called America Online had figured out how to charge millions of Americans $23.90 a month to access the internet. What happened next would become the most catastrophic merger in corporate history, but in late 1999, it looked like destiny. The internet was the future, Time Warner had the content, and AOL had the pipeline. What could possibly go wrong?

IV. Discovery's Parallel Journey: From Cable Educational Network to Reality TV Empire (1982–2018)

John Hendricks sat in his cramped Bethesda apartment in 1982, surrounded by stacks of VHS tapes containing nature documentaries nobody wanted to broadcast. Hendricks founded the Cable Educational Network, Inc., in Bethesda, Maryland, in 1982 to provide documentary programming to cable broadcasters. The University of Alabama history graduate had spent years consulting for educational institutions, watching the explosive growth of cable television from the sidelines, waiting for someone—anyone—to create what seemed obvious: a channel dedicated to documentaries. "It seemed to me very obvious that after the creation of movie channels, after the creation of sports channels, news channels, that cable television would emerge with a documentary service. But it never came. So, in 1982, I decided if no one's going to create it, I would."

The economics were brutal. To be a cable network, you have to have a satellite transponder, and the lease was $336,000 a month. [That was] the biggest fixed expense and then programming [and] staff costs. Hendricks mortgaged his house, maxed out credit cards, and spent three years knocking on doors from Wall Street to Hollywood. Most investors laughed. Educational television? On cable? The broadcasters had tried that with PBS—it barely survived on donations. But Hendricks had noticed something the suits missed: cable viewers weren't looking for another CBS or NBC. They wanted specificity, depth, obsession. They wanted to dive deep into subjects the networks only skimmed.

On June 17, 1985, Hendricks launched the Discovery Channel with $5 million in start-up capital led by the American investment firm Allen & Company. Several investors (including the BBC, Allen & Company, and Venture America) raised $5 million in start-up capital to launch the network. The Discovery Channel began broadcasting on June 17, 1985. At the time, the channel was available in just 156,000 households and broadcast for twelve hours a day, from 3PM to 3AM, a humble start for what would become a global media giant. The programming was eclectic, even radical for American television—About seventy-five percent of its early content had never been broadcast on American television before. The schedule was packed with cultural and wildlife documentaries, science and history specials, and it even broadcast programming from the Soviet Union, offering viewers a rare glimpse behind the Iron Curtain during the Cold War.

But Hendricks understood something fundamental about American viewers that would transform Discovery from educational curiosity to reality TV empire: people didn't actually want to be educated. They wanted to feel smart while being entertained. This subtle distinction would define Discovery's evolution over the next three decades. By 1986, the channel had seven million subscribers. The 1990s marked a period of rapid expansion. Discovery Channel Europe launched in 1989, followed by a wave of international growth into Asia, Africa, Latin America, and the Middle East. The company also diversified, acquiring The Learning Channel (TLC) in 1991 and launching new networks such as Animal Planet, Discovery Kids, and Discovery Health Channel through the late 1990s.

The real transformation began in 2006 with the arrival of David Zaslav, a cable industry veteran who'd spent nearly two decades at NBCUniversal. Prior to Discovery, Zaslav worked at NBCUniversal where he helped develop and launch the cable channels CNBC and MSNBC. Zaslav became CEO and president of Discovery, Inc. in 2006, and oversaw the company as it went public in 2008 and then merged with WarnerMedia in April 2022. Zaslav became CEO of Discovery Communications in November 16, 2006, succeeding Judith McHale. Where Hendricks was an idealist who happened to succeed in business, Zaslav was a dealmaker who happened to work in content. David Zaslav was born into a Jewish family in New York City's Brooklyn borough on January 15, 1960. His family was part of the diaspora from Poland and Ukraine. At the age of eight, he moved with his family to Ramapo, New York, where he graduated from Ramapo High School.

Zaslav immediately recognized Discovery's fundamental problem: prestige documentaries about Arctic foxes didn't pay the bills. What did? Shows about regular people doing dangerous or unusual jobs. In the early 2000s, the channel began to attract a broader audience by incorporating more reality-based series focusing on automotive, occupations, and speculative investigation series; though the refocused programming strategy proved popular, Discovery Channel's ratings began to decline by the middle of the decade. Some critics said such shows strayed from Discovery's intention of providing more educationally based shows aimed at helping viewers learn about the world around them. In 2005, Discovery changed its programming focus to include more popular science and historical themes. The network's ratings eventually recovered in 2006.

Under Zaslav, Discovery became a content machine built on a simple formula: find real people doing interesting things, film them cheaply, own the rights completely. "Deadliest Catch." "Dirty Jobs." "MythBusters." These weren't documentaries in any traditional sense—they were soap operas disguised as educational content, dramatic narratives wrapped in the veneer of learning. The margins were extraordinary. Unlike scripted dramas that cost millions per episode, Discovery could produce an hour of reality programming for a fraction of the cost while charging similar advertising rates.

Zaslav instigated a shift in strategy by the company, aiming to see itself as a "content company" rather than a "cable company" by bolstering its main networks (such as its namesake Discovery Channel) as multi-platform brands. This wasn't just semantic positioning—it was preparation for the streaming wars to come. Zaslav launched new networks aggressively: Planet Green (later rebranded as Destination America), The Hub, Oprah Winfrey Network (OWN), Velocity (later rebranded as MotorTrend), and Investigation Discovery, as well as the company's 2018 acquisition of Scripps Networks Interactive, expansion of its digital education operations, and launch of streaming service discovery+.

The Scripps acquisition in 2018 was Zaslav's masterpiece of cable consolidation. On July 31, 2017, Discovery announced it would acquire Scripps Networks Interactive, owner of networks such as Food Network, HGTV, and DIY Network, for $14.6 billion, pending regulatory approval. On March 6, 2018, the acquisition was completed, with the company renamed as Discovery, Inc. afterwards. Following the purchase, SNI shareholders owned 20% of Discovery's stock. The deal made strategic sense on multiple levels. "Together, we're about 20% of the viewership on cable, and we're at the very top of the list in quality," Discovery CEO David Zaslav told CNNMoney in a phone interview Monday morning.

But the Scripps deal revealed something darker about cable's future. In the years since, the cable business has come under increased pressure from online players like Netflix and YouTube. Channel owners have been challenged to prove that they have must-see, must-carry programming, lest they risk losing distribution. Discovery wasn't buying Scripps because cable was thriving—it was consolidating because cable was dying. The strategy was defensive: combine to gain leverage against distributors, pool resources for the inevitable streaming battle, hope that scale could offset secular decline.

Zaslav understood what many legacy media executives refused to acknowledge: the bundle that made cable television the most profitable entertainment model in history was unraveling. Younger viewers weren't just cord-cutting; they'd never plugged in to begin with. Discovery's response was to double down on what it did best—own content completely, produce it cheaply, and distribute it everywhere. During its 2018 upfronts, Zaslav stated that the company was now strongly focused on serving "passionate fans and passionate audiences", and was preparing to increase its focus on direct-to-consumer offerings targeting such audiences. The SNI purchase, Eurosport's Olympics rights, and the aforementioned Motor Trend-branded network were described as being examples of this strategy.

By 2020, Discovery had transformed from John Hendricks' educational dream into something unrecognizable: a reality TV conglomerate that happened to own nature documentaries. Revenue exceeded $11 billion. The company operated dozens of networks globally. Discovery+ launched with 55,000 episodes of content—the vast majority unscripted reality shows about home renovation, cooking competitions, and true crime. It was profitable, scalable, and completely defensible against Netflix's prestige drama onslaught.

But Zaslav wanted more. He'd built Discovery into a content powerhouse, but in the streaming era, content alone wasn't enough. You needed franchises, theatrical releases, prestige that attracted subscribers rather than just filling time. Discovery had "Shark Week" and "90 Day Fiancé," but it didn't have Batman or Harry Potter. As 2020 turned to 2021, with Discovery's market cap hovering around $20 billion, Zaslav started making phone calls. One of them was to John Stankey, CEO of AT&T, who was desperate to unload a media empire that had become an albatross around his telecom company's neck.

V. The AOL Time Warner Disaster: Tech Bubble's Biggest Casualty (2000–2009)

On January 10, 2000, at the Equitable Center in midtown Manhattan, two CEOs stood before a packed auditorium to announce what they called "the deal of the century." Under the terms of the merger, which was cleared by the Federal Trade Commission in December 2000 and formally completed in January 2001, AOL shareholders owned 55 percent of the new company while Time Warner shareholders owned 45 percent. The idea was to combine Time Warner's impressive book, magazine, television and movie production capabilities with AOL's 30 million Internet subscribers to form the ultimate media empire. AOL's co-founder, chairman and chief executive officer, Steve Case, became chairman of the new company, while Time Warner chairman and CEO Gerald Levin was named its CEO.

The optics were carefully orchestrated. Steve Case, the 41-year-old CEO of America Online, wore his signature khakis and open collar—Silicon Valley casual invading Manhattan's corporate corridors. Gerald Levin, Time Warner's 60-year-old chief executive, had shed his usual suit for a casual sweater, trying desperately to look like he belonged in the digital future. They embraced for the cameras, a gesture that would later grace countless business school case studies as the visual embodiment of corporate hubris.

On January 11, 2000, AOL and Time Warner announced their intention to merge, creating what AOL CEO Stephen Case and Time Warner CEO Gerald Levin called the 21st century's first fully integrated communications, media, and entertainment company. The numbers were staggering: AOL, a company that had existed for barely 15 years and owned no content, was buying Time Warner—with its century of entertainment assets, from Warner Bros. studios to HBO to Time magazine—in an all-stock deal valued at $165 billion. It remains, adjusted for inflation, the largest merger in American corporate history.

Levin was best known for orchestrating with Steve Case the disastrous merger between AOL and Time Warner in 2000, at the height of the dot-com bubble, which destroyed $200 billion in shareholder value as the bubble collapsed. But on that January morning, both men spoke with evangelical fervor about convergence, synergy, and the new economy. Case promised that Time Warner's content would flow seamlessly through AOL's digital pipes to eager consumers. Levin, who had a habit of quoting Hegel in board meetings, spoke of a "transformational event" that would "fundamentally change the way people get information, communicate, and are entertained."

The cultural mismatch was evident from day one. A lot of people thought that the merger was a brilliant move and worried that their own companies would be left behind. At the time, the dot-coms could do no wrong, and AOL was at the head of the pack as the 'dominant' player. Its sky-high stock market valuation, bid up by investors looking for a windfall, made the young company more valuable in market cap terms than many blue chips. Then CEO Steve Case was already shopping around before the Time Warner opportunity came up. On the other side, Time Warner anxiously tried, and failed, to establish an online presence before the merger. And here, in one fell swoop, was a solution. The strategy sounded compelling. Time Warner, via AOL, would now have a footprint of tens of millions of new subscribers. AOL, in turn, would benefit from access to Time Warner's cable network as well as to the content, adding its layer of so-called 'user friendly' interfaces on top of the pipes.

But beneath the public optimism, the deal was born of desperation on both sides. Case joined AOL's predecessor company, Quantum Computer Services, as a marketing vice-president in 1985, became CEO of the company (renamed AOL) in 1991, and, at the height of the dot-com bubble in 2000, orchestrated with Gerald M. Levin the merger that created AOL Time Warner, described as "the biggest train wreck in the history of corporate America." Case knew AOL's dial-up model was dying—broadband was coming, and AOL didn't own any pipes. Levin, haunted by Time Warner's failed attempts to establish an internet presence and still smarting from nearly losing the company to hostile raiders a decade earlier, saw the merger as his legacy play.

The integration began immediately and disastrously. AOL executives, flush with paper wealth from their inflated stock, descended on Time Warner's divisions like conquering heroes. They demanded that CNN create more "clickable" content. They told Warner Bros. to prioritize straight-to-web movies. They insisted that Time Inc.'s prestigious magazines become "digital first." The Time Warner veterans, many of whom had spent decades building their brands, responded with barely concealed contempt. One Warner Bros. executive recalled AOL counterparts showing up to meetings in matching fleece vests, like "a cult that had discovered PowerPoint."

The potential windfall promised by the plan to sell Time Warner content through the AOL network never materialized, and when the Internet bubble burst in 2001, the company's losses reached record proportions. The timing could not have been worse. A few scant months after the deal closed, the dot com bubble burst and the economy went into recession. Advertising dollars evaporated, and AOL was forced to take a goodwill write-off of nearly $99 billion in 2002, an astonishing sum that shook even the business-hardened writers of the Wall Street Journal.

The numbers told a story of unprecedented corporate destruction. In 2002, as investors pulled out en masse of many Internet-related stocks, AOL Time Warner reported a quarterly loss of $54 billion, the largest ever for a U.S. company. The loss comes on the heels of a $54 billion charge taken in the first quarter, bringing to total an annual loss of $98.7 billion, the largest ever recorded by a U.S. company. So did AOL Time Warner's shares, which plunged from a high of $104 to a low of $10 within two years, wiping out billions of dollars (and costing Turner alone an estimated $2 billion). AOL was also losing subscribers and subscription revenue. The total value of AOL stock subsequently went from $226 billion to about $20 billion.

Levin, widely blamed by shareholders for allowing Time Warner and its stable old-media assets to be effectively taken over and dragged down by the ailing new-media division, resigned in December 2001. He was replaced by Richard Parsons, a decision that later contributed to increasing internal tensions and the departure of chief operating officer Bob Pittman, who had been passed over in favor of Parsons. Levin's departure was both overdue and tragic. In 1997, Levin's son Jonathan, a 31-year-old high school English teacher in the Bronx, was murdered by a former student who tortured him with a knife until he surrendered the password to his bank ATM card. The personal tragedy had clearly affected his judgment during the merger negotiations.

He was thrust into the media limelight in May 2002 when he took over the chairmanship of AOL Time Warner when the company was in free-fall after one of the most infamous mistakes in corporate history: the merger of internet goliath AOL with old-school media company Time Warner. "At that moment," he said, "they were not looking for a visionary or necessarily Mr. Charismatic or someone to replicate the dimension of a mogul." Almost nobody recalls that I was the CEO who had the largest recorded loss in the history of American corporations. For the year 2002, my first annual report, we took a write-down of $99 billion.

Richard Parsons, the 6-foot-4 former Rockefeller aide nicknamed "Huggy Bear," became the unlikely savior. Parsons became CEO of AOL Time Warner in 2002, replacing Gerald Levin, who stepped aside two years after the media giant's disastrous $165 billion merger with the upstart internet company. As CEO and later chairman, he led Time Warner's turnaround, dropping "AOL" from the corporation's name and shrinking the company's $30 billion in debt to $16.8 billion by selling Warner Music and other properties. "The merger did not work out quite the way many of us expected. The internet bubble burst and we had to fix the leaks," Parsons told The Independent in 2004. "It was not as monumental a task as many people thought, as the fundamental businesses of the old Time Warner — like publishing, the cable networks and movies — was running well." He said that after the merger, AOL's business had collapsed and Warner Music Group was declining, along with the entire music industry.

In 2003, the company announced that it was removing "AOL" from its name, and in 2009, Time Warner spun off AOL. The symbolism was unmistakable—Time Warner was exorcising the digital demon that had nearly destroyed it. By the time AOL was finally spun off as an independent company in 2009, it was valued at $3.4 billion, roughly 2% of what it had been worth at the merger's announcement.

The lessons from the AOL Time Warner disaster would echo through every subsequent media merger. Following the deal, CNBC named him as one of the "Worst American CEOs of All Time." According to The New York Times, the merger is used by business schools as a case study of "the worst [deal] in history." It proved that content and distribution, despite what investment bankers preached, didn't automatically create value when combined. It showed that cultural integration mattered more than financial engineering. Most importantly, it demonstrated that in times of technological disruption, the old guard's desperation and the new guard's arrogance could create a catastrophically expensive cocktail.

VI. AT&T's Failed Media Ambitions: The WarnerMedia Era (2018–2021)

Randall Stephenson stood at the investor podium in October 2016, radiating the confidence of a man who'd just solved corporate America's convergence puzzle. AT&T has clinched an $85.4 billion agreement to acquire Time Warner in a stock and cash deal that values the media giant at $107.50 per share, capping a whirlwind few days of negotiations that promise to turn AT&T into one of the entertainment industry's largest players. This purchase price implies a total equity value of $85.4 billion and a total transaction value of $108.7 billion, including Time Warner's net debt. The AT&T CEO, a veteran telecom executive who'd spent his entire career climbing the Ma Bell ladder, believed he'd cracked the code that had eluded his predecessors: combining distribution with content to create an unassailable competitive moat.

This is a perfect match of two companies with complementary strengths who can bring a fresh approach to how the media and communications industry works for customers, content creators, distributors and advertisers," said Randall Stephenson, AT&T chairman and CEO. His thesis was seductively simple. AT&T owned the pipes—wireless networks, satellite TV through DirecTV, broadband infrastructure. Time Warner owned the content—HBO's prestige dramas, Warner Bros.' blockbusters, CNN's news operation, Turner's cable networks. Together, they'd create targeted advertising nirvana, using AT&T's customer data to deliver personalized ads across Time Warner's content, all while launching a streaming service to compete with Netflix.

But Stephenson's vision faced an unexpected obstacle: Donald Trump. On the campaign trail in October 2016, then-candidate Donald Trump spoke in Gettysburg, Pa. He noted that Time Warner owned CNN, and then declared his opposition to the $85 billion proposed sale. It is, he said then, "a deal we will not approve in my administration because it's too much concentration of power in hands of too few." The president's animosity toward CNN was legendary, and many suspected political motivations when the Justice Department sued to block the merger.

The six-week trial in spring 2018 became a referendum on vertical integration in the digital age. Leon, based in Washington, D.C., said the evidence and testimony provided by the government were faulty and that it never proved the merged entity would have increased leverage over its competitors. "Ultimately, I conclude that the Government has failed to meet its burden to establish that the proposed transaction is likely to lessen competition substantially," the judge wrote. On June 12, 2018, Judge Richard Leon delivered a stunning rebuke to the government, approving the deal without conditions. The $85.4 billion acquisition closed late Thursday, shortly after the Justice Department said it would not apply for a stay of federal judge Richard Leon's ruling that let the deal go forward.

"The content and creative talent at Warner Bros., HBO and Turner are first-rate. Combine all that with AT&T's strengths in direct-to-consumer distribution, and we offer customers a differentiated, high-quality, mobile-first entertainment experience," AT&T Chairman and CEO Randall Stephenson said in a statement. "We're going to bring a fresh approach to how the media and entertainment industry works for consumers, content creators, distributors and advertisers." Jeff Bewkes, the chairman and CEO of Time Warner which includes Warner Bros, Turner and HBO, has agreed to remain with the company as a senior advisor during a transition period, AT&T said. But the victory celebrations were short-lived. John Stankey, the AT&T executive tapped to run the newly christened WarnerMedia, immediately alienated the creative community with his Silicon Valley jargon and data-obsessed approach.

At a town hall with HBO employees in summer 2018, Stankey delivered what became an infamous speech about needing more "engagement" and "hours of viewing." He told the premium network that had built its reputation on "It's not TV, it's HBO" that it needed to become more like Netflix—more content, more frequently, for more audiences. Richard Plepler, HBO's CEO and guardian of its prestige brand, sat stone-faced. Within six months, he'd resigned, followed by a parade of other Time Warner executives who couldn't stomach AT&T's corporate culture.

The strategic confusion was embodied in HBO Max's troubled development and launch. On April 20, 2020, WarnerMedia announced HBO Max's launch date as May 27. The service launched into a pandemic-altered world with a confused brand identity—was it HBO? Was it something else? Why was it the same price as HBO but with more content? All of these entrants, as well as incumbents led by Netflix, are operating in a marketplace defined by COVID-19, which has boosted overall streaming viewing but also complicated the supply chain. The title initially intended as the flagship attraction for HBO Max, a reunion special with the original cast of Friends, was delayed by the pandemic. Anna Kendrick's romantic comedy Love Life has stepped in as the service's marquee show at launch.

The strong affiliation with legacy HBO network, however, proved an early stumbling block in terms of subscriber growth as the effort to communicate to linear viewers how to "activate" a streaming account proved unwieldy. The official launch of HBO Max in May 2020, which marked the last of four major new competitors to Netflix launched over a seven-month span, was also completely waylaid by Covid. While WBD CEO David Zaslav is as enamored of HBO as the AT&T regime overall, his management team concluded that the "HBO" in the name positioned the general entertainment service as slightly too rarified to match rivals like Disney+ or Netflix.

The pandemic accelerated every problem with AT&T's media strategy. AT&T's WarnerMedia announced Thursday that its entire slate of 2021 theatrical releases will debut free for U.S. subscribers of HBO Max at the same time they hit theaters. It's the boldest move from a major movie studio grappling with theater shutdowns due to the Covid-19 pandemic. The decision to release Warner Bros.' entire 2021 slate simultaneously on HBO Max—including tentpoles like "Dune" and "The Matrix 4"—enraged theater owners, talent, and agents. Christopher Nolan, Warner's most bankable director, called HBO Max "the worst streaming service" and accused AT&T of using the pandemic to sabotage the theatrical experience.

Meanwhile, the financials were deteriorating. Market reaction to the deal was never especially positive, partly because a lot of analysts deemed AT&T's $85.4 billion acquisition an overpay and partly because of a heavy assumption of debt in the combined company. As WarnerMedia entered the streaming fray with the launch of the once-and-future HBO Max, losses on that side of the business piled up. AT&T had added roughly $50 billion in debt to acquire Time Warner, bringing total obligations to over $180 billion. The company's stock price stagnated as investors questioned whether a telecom company could successfully run a creative enterprise.

The integration never improved. AT&T executives, accustomed to predictable infrastructure investments and regulated returns, couldn't understand Hollywood's hit-driven economics. They imposed corporate processes on creative decisions, demanded synergies that didn't exist, and fundamentally misunderstood that content creation wasn't like building cell towers. By early 2021, barely three years after closing the Time Warner acquisition, Stephenson's successor John Stankey was quietly shopping for an exit.

In 2021, AT&T threw in the towel. The solution came from an unexpected source: David Zaslav, whose Discovery had transformed from educational documentaries to reality TV empire, saw an opportunity to fulfill his Hollywood ambitions. Discovery Inc. CEO David Zaslav reached out to his counterpart at AT&T, John Stankey, about a possible deal. After several months of behind-the-scenes negotiations, the two companies made it official in May 2021, announcing plans to merge. The deal structure was elegant in its face-saving creativity: AT&T would spin off WarnerMedia and merge it with Discovery, receiving $43 billion in cash and debt relief while AT&T shareholders would own 71% of the new company.

The AT&T era would be remembered as a $50 billion tuition payment in why telecom companies shouldn't buy Hollywood studios. The convergence thesis—that owning pipes and content together created unique value—had failed spectacularly. AT&T's attempt to compete in streaming had burned billions in losses while alienating the creative community that made the content valuable in the first place. As WarnerMedia employees prepared for their third corporate parent in five years, one veteran Warner Bros. executive summed up the sentiment: "AT&T understood everything about our business except what made it special."

VII. The Discovery Merger: Zaslav's Big Bet (2021–2022)

The phone call that would reshape Hollywood came on a February morning in 2021. Discovery Inc. CEO David Zaslav reached out to his counterpart at AT&T, John Stankey, about a possible deal. After several months of behind-the-scenes negotiations, the two companies made it official in May 2021, announcing plans to merge. Zaslav, sitting in his home office overlooking the Long Island Sound, had prepared for this moment for years. The Discovery CEO had spent the pandemic studying every aspect of WarnerMedia's business, convinced that AT&T's bungled ownership created a once-in-a-lifetime opportunity.

"John, you've got an incredible asset that you're not equipped to run," Zaslav said, according to people familiar with the conversation. "We know content. You know connectivity. Let's solve both our problems." Stankey, exhausted from defending the Time Warner acquisition to increasingly hostile investors, was ready to listen. AT&T's stock had gone nowhere since the merger closed. Activist investor Elliott Management was circling. The streaming losses were mounting. Something had to give.

The deal structure they negotiated was a masterpiece of financial engineering that allowed both sides to claim victory. The two companies officially merged after WarnerMedia was spun off by AT&T, joining forces with Discovery in a deal valued at $43 billion. AT&T would spin off WarnerMedia to its shareholders, who would own 71% of the new company, while Discovery shareholders would own 29%. But here was the key: Discovery would be the surviving entity, with Zaslav as CEO. AT&T would receive $43 billion in cash and debt assumption, essentially recouping half its purchase price while getting out of the content business entirely.

The numbers seemed impossible. Discovery, with a market cap of roughly $20 billion, was effectively taking over WarnerMedia, valued at $130 billion just three years earlier. How? Leverage. Massive, eye-watering amounts of leverage. The combined company would carry $55 billion in debt, a load that would define every strategic decision going forward. disagreements over the ownership of the new company between AT&T and Discovery shareholders, and the amount of debt transferred to Discovery when they merged with WarnerMedia.

Zaslav sold the merger as a streaming play, but insiders knew the real strategy: create enough scale in traditional TV to milk the dying cable bundle for every last dollar while building a streaming service that could eventually achieve profitability. Discovery brought cheap, unscripted content that generated reliable cash flow. WarnerMedia brought prestige and franchises. Together, they'd have leverage against distributors, advertisers, and talent.

The cultural challenges were apparent from day one. Discovery operated like a private equity shop—lean, scrappy, obsessed with margins. WarnerMedia, despite AT&T's cost-cutting, still operated like a Hollywood studio—expensive, prestigious, believing content was king. When Discovery executives first toured the Warner Bros. lot in Burbank, they were stunned by the opulence. "They had a coffee bar that served nothing but coffee—different types of coffee," one Discovery executive marveled. "At Discovery, we had a Keurig machine and considered ourselves lucky."

The merger was officially completed on April 8, 2022, with trading beginning on the Nasdaq on April 11. But even before the deal closed, Zaslav was making his intentions clear. In investor calls, he hammered three themes: synergies, streaming discipline, and free cash flow. Gone was AT&T's "HBO Max at any cost" strategy. In its place, Zaslav promised a path to streaming profitability by 2024, $3 billion in cost synergies, and a focus on "quality over quantity."

The integration team, led by Discovery CFO Gunnar Wiedenfels, approached WarnerMedia like a corporate raider from the 1980s. Every contract was scrutinized. Every production deal was renegotiated. Every executive's compensation was benchmarked against Discovery's austere standards. The message was clear: the country club days were over.

Zaslav stated that the combined company would need to have "one culture" that "starts with people feeling safe, people feeling valued for who they are", as opposed what he described as a culture of internal competition between WarnerMedia's businesses. But his actions suggested a different priority: cutting costs at any price. Within weeks of the merger closing, the layoffs began. First, redundant corporate positions. Then, entire divisions deemed "non-strategic." CNN+, the streaming news service that had launched just two weeks before the merger closed, was shuttered after 23 days, becoming a $300 million punchline.

The talent community watched in horror as Zaslav dismantled decades of relationships. Development deals were cancelled. Production commitments were rescinded. The HBO Max content pipeline, built at enormous expense under AT&T, was dramatically reduced. "We're not trying to win the direct-to-streaming movie business," Zaslav declared, effectively abandoning the strategy that AT&T had bet billions on.

Wall Street initially loved it. Discovery's stock, which had traded at $24 when the merger was announced, jumped above $30 in the first weeks after closing. Analysts praised Zaslav's "financial discipline" and "rational approach" to streaming. The free cash flow story was compelling: combine Discovery's profitable cable networks with WarnerMedia's premium content, cut costs aggressively, and generate enough cash to pay down debt while building a sustainable streaming business.

But the honeymoon was brief. As Zaslav's cost-cutting grew more aggressive, the creative community revolted. The decision to kill "Batgirl," a nearly completed $90 million film, for a tax write-off became a symbol of everything wrong with the new regime. Directors, writers, and actors who'd worked with Warner Bros. for decades suddenly found their projects cancelled, their deals terminated, their calls unreturned.

The streaming strategy was equally chaotic. The plan to combine HBO Max and Discovery+ into a single service made logical sense but proved technically and culturally complex. HBO executives watched in horror as their prestige brand was diluted with "90 Day Fiancé" and "Dr. Pimple Popper." Discovery executives couldn't understand why HBO needed to spend $200 million on a single season of television. The two cultures weren't merging; they were colliding.

By the end of 2022, less than nine months after the merger closed, the stock had fallen below $10, erasing tens of billions in market value. The debt load that had seemed manageable when interest rates were near zero now looked crushing as the Federal Reserve hiked rates aggressively. The synergies Zaslav promised were being achieved, but at the cost of gutting the creative engine that made the content valuable. The streaming subscriber growth had stalled, and the linear TV business was declining faster than expected.

Zaslav's grand bet—that he could succeed where telecommunications giants and tech companies had failed—was looking increasingly questionable. He'd acquired the assets he'd coveted for decades, but at a price and debt load that left no margin for error. As 2023 dawned, with a writers' strike looming and streaming losses still mounting, the architect of the deal was already contemplating his next move: perhaps breaking up the company he'd just spent $130 billion assembling.

VIII. Integration Chaos: The Batgirl Debacle & Max Rebrand (2022–2024)

The email arrived at 2:47 PM on a Tuesday in August 2022. Adil El Arbi and Bilall Fallah, the directors of "Batgirl," were in Morocco attending Adil's wedding when they learned their $90 million movie—fully shot, deep in post-production—had been cancelled. Not delayed. Not sent to streaming. Cancelled. Deleted. It would never see the light of day. The film would instead become a tax write-off, a line item on Warner Bros. Discovery's balance sheet worth more dead than alive.

that clash led to things like the scrapping of a completed Batgirl movie as a tax writeoff, the un-branding of HBO Max as Max (and then re-branding as HBO Max later this year). Leslie Grace, the film's star, found out through social media. Michael Keaton, returning as Batman, learned from his agent. The crew members who'd spent months in Glasgow creating Gotham City discovered their work had been vaporized when the trades broke the story. In Hollywood, where even the worst films usually see some form of release, the complete erasure of "Batgirl" was unprecedented, savage, and symbolic of everything David Zaslav represented to the creative community.

The decision came from Zaslav himself, after a test screening in Burbank that spring. According to executives present, Zaslav watched the film stone-faced, occasionally checking his phone. When the lights came up, he turned to his lieutenants and delivered his verdict: "This is not a theatrical film, and it's not good enough for streaming. We're better off taking the write-off." The tax benefit: roughly $40 million. The reputational cost: incalculable.

But "Batgirl" was just the beginning of what insiders called the "Summer of Death." "Scoob!: Holiday Haunt," a $40 million animated film, was also sacrificed to the tax gods. Dozens of HBO Max originals were removed from the platform entirely—not because they were unsuccessful, but because removing them allowed the company to write down their value and avoid paying residuals. Shows that creators had spent years developing simply vanished, their existence erased from the platform they were made for.

The carnage extended beyond content. Warner Bros. Television, once the most prolific supplier of scripted programming in Hollywood, saw its development slate cut by 70%. The storied Warner Bros. Animation, home to Looney Tunes and DC animated projects, was gutted. Cartoon Network, which had launched the careers of countless animators, essentially ceased original production. Each cut was justified by the same refrain: synergies, efficiency, and the path to profitability.

Meanwhile, the rebrand of HBO Max into simply "Max" became a case study in corporate dysfunction. Warner Bros Discovery has confirmed its long-expected plan to jettison the "HBO" from HBO Max, announcing that its rebranded streaming service will be called Max. The new offering, which combines programming from HBO Max and Discovery, will go live May 23. The decision to drop "HBO" from the name—the most prestigious brand in television—baffled industry observers. The internal logic was that "HBO" was too niche, too coastal, too premium to attract the mass audience needed to compete with Netflix. But the execution was catastrophic.

The technical migration from HBO Max to Max turned into a customer service nightmare. Millions of subscribers found themselves locked out of accounts. Passwords didn't work. Content disappeared and reappeared randomly. The app, rebuilt from scratch to accommodate Discovery+ content, was buggy and user-hostile. The algorithm, designed to surface both prestige HBO content and reality TV from Discovery, created jarring recommendations: "Because you watched Succession, you might enjoy Dr. Pimple Popper."

The cultural integration was even worse. The joint company's first major project – the streaming launch of Max – offered content from Warner Bros., Discovery Channel, HBO, CNN, Cartoon Network, Animal Planet, and more. HBO executives, who'd spent decades cultivating a brand synonymous with quality, watched in horror as their carefully curated platform became a dumping ground for all of Warner Bros. Discovery's content. The homepage that once featured prestige dramas now promoted "90 Day Fiancé" spin-offs and Property Brothers marathons.

Casey Bloys, HBO's programming chief and one of the few senior executives to survive the merger, fought a rearguard action to protect the brand. In meetings, he argued passionately that HBO's value wasn't just its content but its curation, its taste level, its promise to subscribers that everything bearing its name met a certain standard. Zaslav's response was brutally pragmatic: "Casey, taste doesn't scale."

The talent relations disaster deepened with every decision. When James Gunn and Peter Safran were brought in to run DC Studios, their first act was to cancel nearly every project in development, including sequels to successful films and nearly completed projects. Henry Cavill was unceremoniously dismissed as Superman via a Instagram post. The entire DC television universe on The CW was cancelled with barely a farewell. Directors who'd been developing projects for years were ghosted. Writers learned their deals were dead from the trades.

The contrast with the competition was stark. While Disney+ celebrated its Marvel series, while Netflix lavished hundreds of millions on creators like Ryan Murphy and Shonda Rhimes, while Apple TV+ built prestige with Ted Lasso and Severance, Warner Bros. Discovery was known for what it destroyed, not what it created. The company that owned many of Hollywood's most valuable franchises—Harry Potter, DC Comics, Game of Thrones—seemed determined to strip them for parts rather than build on them.

CNN's transformation under Chris Licht, Zaslav's handpicked choice to replace Jeff Zucker, became another public relations disaster. CNN+, the streaming service that had attracted top talent like Chris Wallace and Kasie Hunt, was shut down after just 23 days, before many subscribers had even activated their accounts. The message to the industry was clear: Warner Bros. Discovery would rather write off investments than admit mistakes or give projects time to find an audience.

The human cost was staggering. By the end of 2023, Warner Bros. Discovery had laid off over 10,000 employees—roughly 15% of its workforce. Entire departments were eliminated. The Warner Bros. lot in Burbank, once bustling with development executives, writers, and producers, felt like a ghost town. The few executives who remained operated in constant fear, knowing that Zaslav's next earnings call might eliminate their division entirely.

NBA rights loss and sports strategy failures. The loss of NBA rights to NBC and Amazon in 2024—after Turner had broadcast basketball since 1984—symbolized the company's retreat from premium content. The decision to let the rights go after decades was purely financial, but it sent a message that Warner Bros. Discovery was no longer playing to win but merely to survive.

Even successful properties were mishandled. "The Last of Us," HBO's video game adaptation that became a cultural phenomenon, succeeded despite the chaos, not because of it. "House of the Dragon," the "Game of Thrones" prequel, drew huge audiences but operated on slashed budgets compared to its predecessor. The few wins were overshadowed by the constant drumbeat of cancellations, write-offs, and layoffs.

By mid-2024, the Max rebrand was being quietly reversed in some markets, with "HBO" returning to the name in an admission that removing it had been a mistake. But the damage was done. The service that had launched as HBO Max with 64 million subscribers was struggling to grow, with churn rates increasing as confused customers couldn't find content or simply gave up on the degraded experience.

The irony was cruel. Zaslav had achieved his lifelong dream of running a Hollywood studio, of controlling Batman and Harry Potter and HBO. But in his relentless pursuit of efficiency, synergies, and cash flow, he'd destroyed much of what made those properties valuable. The creative community that had once viewed Warner Bros. as the gold standard now saw it as a cautionary tale. As one veteran producer put it: "David wanted to own Hollywood so badly that he killed it to afford it."

IX. Financial Performance & The Path to Breakup (2022–2025)

The numbers told a story of slow-motion corporate destruction. Total revenues were $39.3 billion, a 4% ex-FX decrease compared to the prior year. Net income available to Warner Bros. Discovery, Inc. was $(11.3) billion, which includes $7.5 billion of pre-tax acquisition-related amortization of intangibles, content fair value step-up, and restructuring expenses and a $9.1 billion non-cash goodwill impairment charge in the Networks segment. In the last 12 months, WBD had revenue of $38.34 billion and -$10.80 billion in losses. Loss per share was -$4.40. The company has $3.90 billion in cash and $37.43 billion in debt, giving a net cash position of -$33.52 billion.

These weren't just bad numbers—they were catastrophic. The $11.3 billion annual loss for 2024 represented one of the largest corporate losses in American history, surpassed only by the AOL Time Warner disaster two decades earlier. The irony was lost on no one. Warner Bros. Discovery had managed to recreate the financial destruction of the AOL merger without even needing a tech company to blame.

The debt burden had become existential. Ended the year with $34.6 billion of net debt. When interest rates were near zero, carrying $55 billion in gross debt seemed manageable, even strategic. But as the Federal Reserve hiked rates to combat inflation, debt service costs exploded. What had been a $2 billion annual interest expense ballooned to nearly $4 billion. Every dollar spent on interest was a dollar not invested in content, not used to compete with Netflix or Disney.

The streaming business, supposedly the company's future, remained stubbornly unprofitable despite constant promises of imminent profitability. Max had achieved positive EBITDA contribution in certain quarters, but only through aggressive cost-cutting that gutted its content pipeline. Subscriber growth had stalled at around 110 million globally—impressive in isolation, but far short of Netflix's 280 million or Disney+'s 165 million. The churn rate, which the company stopped disclosing in detail, was rumored to exceed 7% monthly, among the highest in the industry.

Meanwhile, the linear television business—still generating the majority of cash flow—was in terminal decline. Cord-cutting accelerated from a steady drain to a hemorrhage. Warner Bros. Discovery lost 2 million traditional pay-TV subscribers per quarter. Advertising revenue, once reliable as death and taxes, fell double digits year-over-year as marketers fled to digital platforms. The TV networks that Discovery had spent billions acquiring were now worth a fraction of their purchase price, as evidenced by the $9.1 billion goodwill impairment charge.

The Studios segment provided the only bright spots, but even these were dimming. While films like "Barbie" and "The Nun II" had performed well theatrically, the overall slate was thin, a direct result of Zaslav's cost-cutting. The decision to dramatically reduce theatrical releases in favor of "quality over quantity" meant fewer shots on goal in a hit-driven business. When "The Flash" and "Shazam! Fury of the Gods" flopped despite massive marketing spends, there wasn't enough pipeline to compensate.

Gaming, once a reliable profit center, had become a disaster zone. "Suicide Squad: Kill the Justice League," which cost over $200 million to develop, generated less than $50 million in revenue—one of the biggest flops in video game history. The gaming division took a $300 million write-down, and Zaslav openly mused about exiting the business entirely, despite owning some of gaming's most valuable IP.

The strategic failures compounded the financial ones. The loss of NBA rights—which Turner had broadcast since 1984—wasn't just about losing basketball games. It was about losing one of the few pieces of content that could still aggregate large, simultaneous audiences and command premium advertising rates. Without the NBA, TNT's value to distributors plummeted, accelerating the decline of carriage fees that still represented billions in high-margin revenue.

By early 2025, the stock market had rendered its verdict. Warner Bros. Discovery shares, which had briefly touched $30 in the merger's early days, traded below $8. The company's market capitalization had fallen to less than $20 billion—meaning the equity was worth less than the debt. Bond prices suggested distress, trading at 70 cents on the dollar. Credit rating agencies had downgraded the company to deep junk status, making refinancing prohibitively expensive.

The board, which had rubber-stamped Zaslav's every decision, finally began asking uncomfortable questions. John Malone, the cable pioneer who'd orchestrated Discovery's rise and effectively controlled the company through super-voting shares, was reportedly furious. The man who'd spent decades building cable empires watched his last great deal destroy billions in value. According to sources close to the board, Malone gave Zaslav an ultimatum in a private call: "Fix this, or I will."

The fix, when it came, was both radical and inevitable. June 9, 2025 – New York – Warner Bros. Discovery (NASDAQ: WBD) (the "Company," "WBD," "we," "us," "our") today announced plans to separate the company, in a tax-free transaction, into two publicly traded companies, enabling each to maximize its potential. Warner Bros. Discovery (NASDAQ: WBD) today announced plans to separate the company, in a tax-free transaction, into two publicly traded companies.

The announcement was dressed up as strategic brilliance, but everyone understood it for what it was: an admission of failure. The merger that was supposed to create a streaming giant capable of competing with Netflix and Disney had instead created an unmanageable conglomerate drowning in debt. The synergies never materialized. The cultures never merged. The strategic vision never cohered.

The Streaming & Studios company will consist of Warner Bros. Television, Warner Bros. Motion Picture Group, DC Studios, HBO, and HBO Max, as well as their legendary film and television libraries. This was the crown jewel, the business investors actually wanted to own—IP-rich, streaming-focused, with a clear path to profitability if properly managed.

Global Networks will include premier entertainment, sports and news television brands around the world including CNN, TNT Sports in the U.S., and Discovery, top free-to-air channels across Europe, and digital products such as the profitable Discovery+ streaming service and Bleacher Report (B/R). This was the "bad bank"—the declining linear assets that would carry most of the debt and gradually wind down as cable television died its inevitable death.

The financial engineering of the split was complex but revealing. The majority of the $38 billion in debt would stay with Global Networks, which would use its still-substantial but declining cash flows to service and pay down obligations. Streaming & Studios would emerge with a cleaner balance sheet, though still carrying enough debt to constrain its strategic flexibility. Global Networks would retain a 20% stake in Streaming & Studios, providing some upside exposure while allowing for future monetization to pay down debt.

David Zaslav, President and CEO of Warner Bros. Discovery, will serve as President and CEO of Streaming & Studios. Gunnar Wiedenfels, currently CFO of Warner Bros. Discovery, who will serve as President and CEO of Global Networks. The leadership structure told its own story: Zaslav got the glamorous Hollywood assets he'd always coveted, while Wiedenfels inherited the thankless task of managing decline.

As 2025 progressed, the unraveling accelerated. Major talent agencies advised clients to avoid Warner Bros. projects given the uncertainty. Streaming competitors circled like vultures, poaching executives and making plays for valuable IP. The stock price continued its relentless decline, with some analysts questioning whether the company would survive long enough to complete the split.

The path to breakup had been paved with broken promises, destroyed value, and abandoned strategies. From AT&T's convergence dreams to Zaslav's synergy fantasies, every corporate combination had made the problems worse, not better. The company that would soon cease to exist as Warner Bros. Discovery had become a cautionary tale of corporate ambition, a reminder that in media, bigger is not always better, and sometimes the best deal is the one you don't make.

X. The Split: Warner Bros. vs. Discovery Global (2025–2026)

The separation announcement came with corporate fanfare but landed with a thud. Warner Bros. Discovery (NASDAQ: WBD) today announced corporate names and senior leadership appointments for when the company separates in mid-2026. "Streaming & Studios," which will be home to Warner Bros. Television, Warner Bros. Motion Picture Group, DC Studios, HBO, HBO Max and Warner Bros. Gaming Studios, as well as their legendary film and television libraries, will be called Warner Bros., honoring the legacy of more than a century of industry-defining storytelling.

For David Zaslav, the split represented both vindication and defeat. He would finally run a pure-play Hollywood studio, achieving the dream that had driven him since his Discovery days. But he'd achieved it by destroying $100 billion in market value, alienating the creative community, and saddling both successor companies with challenges that might prove insurmountable. "We will proudly continue the more than century-long legacy of Warner Bros. through our commitment to bringing culture-defining stories, characters and entertainment to audiences around the world," said Zaslav.

The Warner Bros. entity—as the streaming and studios company would be known—inherited the assets everyone recognized: Harry Potter, DC Comics, HBO's prestige programming, the Warner Bros. movie and TV production apparatus. On paper, it looked formidable. The studio had a library valued at over $30 billion, franchises that had generated tens of billions in revenue, and HBO Max's improving streaming platform. But scratch beneath the surface, and the problems were evident.

The talent pipeline Zaslav had systematically destroyed would take years to rebuild. Major franchises were in disarray—DC's cinematic universe had been rebooted so many times that audiences had lost track, Harry Potter was mired in J.K. Rowling controversies, and HBO's post-"Succession" development slate looked thin. The streaming service, while approaching profitability, faced an uncertain future competing against tech giants with unlimited resources and Netflix's first-mover advantage.

More problematic was the debt allocation. While Global Networks would carry the majority of the obligations, Warner Bros. would still inherit roughly $12 billion in debt—manageable for a growing company, potentially crushing for one facing the uncertainties of Hollywood production and streaming competition. The company would need to generate consistent hits and streaming growth just to service its obligations, leaving little room for error or strategic investment.

The leadership team at Discovery Global includes Gunnar Wiedenfels, currently CFO of Warner Bros. Discovery, who will serve as President and CEO of what everyone understood was the "bad bank" of the split. Discovery Global would own assets that, just a decade earlier, would have been considered premium: CNN, despite its struggles, remained one of the world's most recognized news brands. TNT Sports, even without the NBA, still had MLB, NHL, and NCAA tournament rights. Discovery's international channels reached hundreds of millions of homes across Europe and Asia.

But these were melting ice cubes, and everyone knew it. Linear television's decline wasn't slowing—it was accelerating. Younger demographics had completely abandoned traditional TV. Advertisers were following them to digital platforms. The business model that had generated tens of billions in profits over decades was entering its terminal phase. Wiedenfels's job wasn't to grow Discovery Global but to manage its decline profitably enough to service the roughly $26 billion in debt it would carry.

The inclusion of Discovery+ in the Global Networks portfolio was particularly revealing. The streaming service, profitable but stagnant at around 25 million subscribers, represented the limits of niche streaming. It proved you could make money in streaming with the right content and cost structure, but also that not every service could be Netflix. Discovery+ would likely never grow beyond its core audience of reality TV enthusiasts, a metaphor for the entire Global Networks business—profitable but limited, sustainable but shrinking.

The operational separation would be extraordinarily complex. The two companies had spent three years integrating systems, combining operations, and creating "synergies." Now they had to be unwound. Shared services had to be duplicated. Contracts had to be renegotiated. Employees had to choose sides. The cost of separation was estimated at $2 billion—money neither company could really afford but both had to spend.

The human toll was significant. Employees who'd survived multiple mergers, reorganizations, and layoffs now faced another upheaval. Many simply gave up. Voluntary attrition exceeded 20% in some divisions as people fled for the stability of Netflix, Amazon, or tech companies. Those who remained operated in a state of perpetual uncertainty, unsure which company they'd end up in or whether their jobs would survive the split.

For CNN, the split represented yet another ownership change in a tumultuous period. CNN has been through multiple corporate reconfigurations in recent years. The network's founder Ted Turner said in a statement Monday that he wishes "all the best" for CNN ahead of the next transition. "While I haven't been involved with CNN and its operations for more than two decades, I continue to hold deep affection for the company, its leadership, and the dedicated employees and staff," Turner said. "I have the utmost respect for the important work CNN does, and I wish them all the best as they navigate this new chapter following the recent announcement of the planned split." Turner's statement, while diplomatic, carried an undertone of sadness—his creation had become a corporate orphan, passed between owners who saw it as an asset to be optimized rather than a journalistic institution to be nurtured.

The market reaction to the split was mixed. Some analysts praised the strategic clarity—finally, investors could choose between a growth-oriented content company and a cash-generative declining asset. Others questioned whether either company was viable standalone. Warner Bros. faced enormous competition with a weakened position. Discovery Global was a melting ice cube with a massive debt load. Combined, they were problematic; separated, they might be doomed.

The separation is expected to be completed by mid-2026, subject to closing and other conditions, including final approval by the Warner Bros. Discovery board and regulatory approvals. But even as lawyers drafted separation agreements and bankers structured the debt allocation, larger questions loomed. Would Warner Bros. become an acquisition target for a tech giant looking for content? Would Discovery Global simply liquidate its assets as they declined, eventually disappearing entirely?

The employees who'd lived through the Warner Bros. Discovery era had a gallows humor about it all. They'd survived the AOL disaster, the AT&T debacle, and the Discovery merger. Now they were preparing for whatever came next. As one longtime Warner Bros. executive put it: "We've been sold, merged, integrated, synergized, and split so many times, I've lost count. The only constant is that someone in a suit will show up every few years promising to fix everything, then leave with a golden parachute when it doesn't work."

"By operating as two distinct and optimized companies in the future, we are empowering these iconic brands with the sharper focus and strategic flexibility they need to compete most effectively in today's evolving media landscape," Zaslav said in a statement. The corporate speak couldn't hide the reality: this was an admission that the grand experiment had failed. The company that was supposed to challenge Netflix and Disney was instead breaking apart, its pieces worth less than the whole, its future uncertain.

As preparations for the split continued through late 2025, both companies faced immediate challenges. Warner Bros. needed to rebuild its creative pipeline while managing debt service. Discovery Global needed to squeeze every last dollar from declining assets while maintaining enough relevance to avoid complete irrelevance. Neither task was enviable. Both were necessary.

The split wouldn't officially complete until mid-2026, but Warner Bros. Discovery as a unified entity was already dead. It had become two companies sharing a corporate structure, each planning for a future without the other. The promised synergies had become dis-synergies. The unified culture Zaslav had promised had never materialized. What remained were two wounded companies, each hoping that separation would somehow heal what combination had broken.

XI. Playbook: M&A and Media Lessons

The Warner Bros. Discovery saga offers a masterclass in how not to execute media M&A. Each merger in the company's tortured history—AOL-Time Warner, AT&T-Time Warner, Discovery-WarnerMedia—failed for predictable reasons that executives ignored in their pursuit of scale, synergy, and stock options. The patterns repeat with such consistency that they constitute a playbook of destruction.

The Perils of Debt-Fueled Media Consolidation

Every major transaction in Warner's history was funded primarily with debt, based on projections that never materialized. The AOL merger assumed internet advertising would grow exponentially. AT&T assumed content and distribution synergies would justify the premium. Discovery assumed streaming losses would quickly reverse. In each case, leverage that looked manageable at signing became crushing when reality hit.