Waters Corporation: From Laboratory Innovation to Global Science Leader

I. Introduction & Cold Open

Picture this: It's March 2004, and pharmaceutical laboratories around the world are about to witness their biggest productivity leap in decades. In a packed conference room at Waters Corporation's headquarters in Milford, Massachusetts, engineers and scientists are preparing to unveil something that will make every existing liquid chromatography system look like a Model T Ford. The ACQUITY Ultra Performance Liquid Chromatography system—UPLC for short—is about to turn a mature, slow-moving industry on its head.

The pharmaceutical chemist who once waited 30 minutes for a single chromatographic run would soon complete the same analysis in 3 minutes. Drug discovery timelines would compress. Operating costs would plummet. And Waters, a company that started in a police station basement, would cement its position as the innovation leader in a $10 billion global market for analytical instruments.

Today, Waters Corporation stands as a $3 billion revenue powerhouse, employing 7,600 people across the globe. Their instruments and software touch nearly every pill you swallow, every food safety test that protects your dinner table, and countless environmental samples that monitor our planet's health. Walk into any major pharmaceutical company's analytical lab—Pfizer, Novartis, Merck—and you'll find Waters equipment humming away, separating complex mixtures into their component parts with nanogram precision.

But here's what makes this story truly fascinating: Waters didn't just build better mousetraps. They created entirely new categories of scientific instruments, turned capital equipment sales into recurring revenue streams, and somehow managed to maintain pricing power in an industry where customers include some of the world's most sophisticated buyers. They've beaten giants like Agilent Technologies and Thermo Fisher Scientific at their own game, not through size, but through relentless focus on a single domain: separation science.

This is the story of how a MIT-trained mathematician named Jim Waters, working with just five employees, built the foundation for what would become one of the most important companies you've never heard of. It's a tale of scientific breakthroughs, savvy acquisitions, near-death experiences, and the kind of operational excellence that would make even the most hardened manufacturing executive weep with joy. It's about building moats in unexpected places—not through network effects or platform dynamics, but through the unglamorous yet essential work of helping scientists separate molecules.

Most importantly, it's a masterclass in how to build an enduring business in the physical world, where atoms matter more than bits, where customer relationships span decades, and where innovation cycles play out over years, not quarters. In an era obsessed with software eating the world, Waters reminds us that somebody still needs to build the tools that actually understand what's in the world.

II. The Basement Beginning: Jim Waters & The Founding Story (1958–1972)

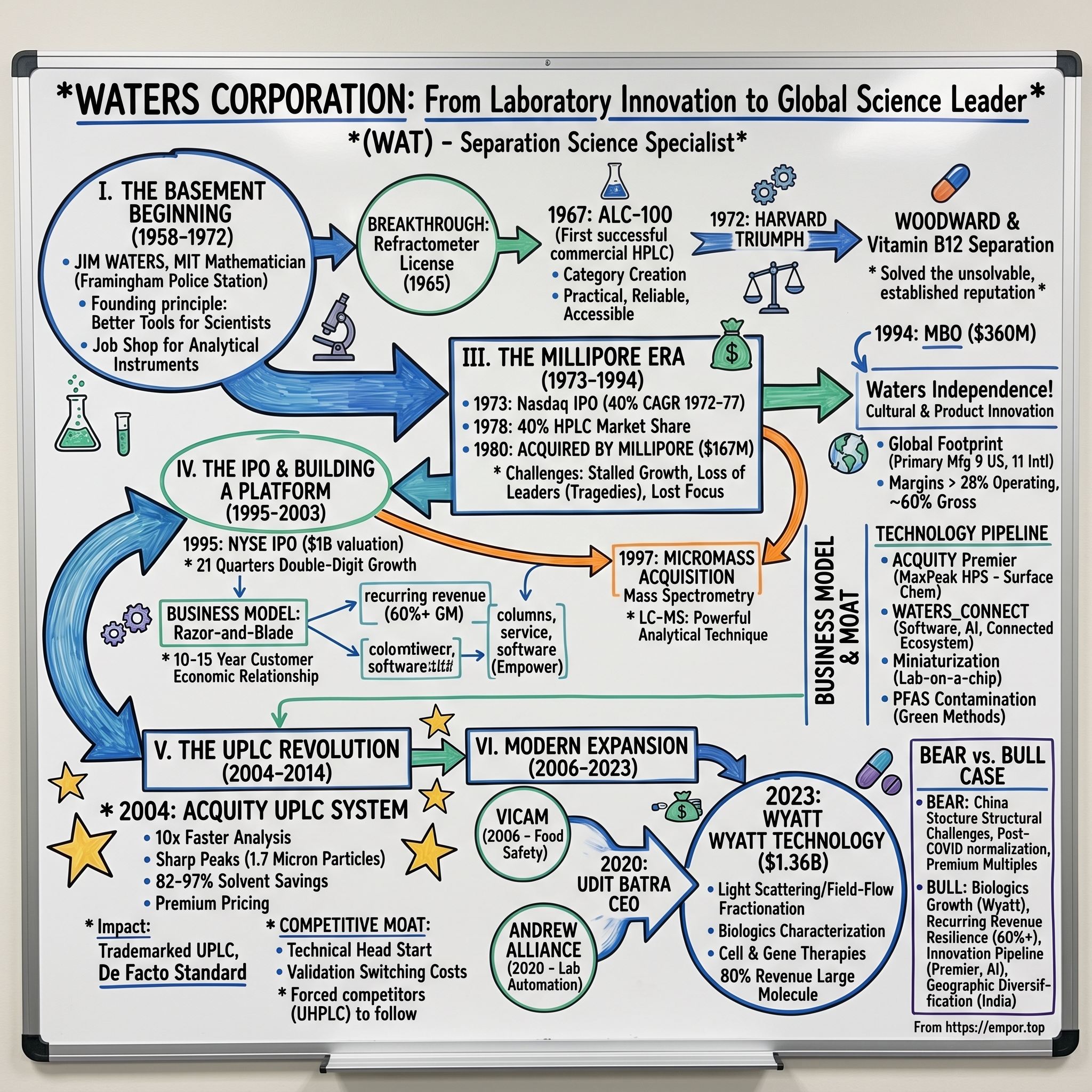

The basement of the Framingham, Massachusetts police station wasn't exactly Silicon Valley garage mythology material. No venture capitalists dropping by with term sheets. No Stanford computer science graduates coding through the night. Just Jim Waters, an MIT-trained mathematician with an entrepreneurial itch, setting up shop in 1958 with a simple belief: scientists needed better tools.

Waters Associates, as the company was first known, began life as a job shop for analytical instruments. Jim Waters had spent years working at various technical companies, but he saw an opportunity in the fragmented, cottage industry of laboratory equipment. Scientists were cobbling together their own analytical systems from various components, often spending more time maintaining equipment than conducting research. Waters believed he could do better.

The early product lineup reads like a random assortment from a scientific garage sale. A boiler feedwater flame photometer—essentially a device that measured sodium levels in steam power plants. A balloon hydrometer for measuring specific gravity. Even a nerve gas detector, developed during the Cold War paranoia of the early 1960s. None of these products would define Waters' future, but they kept the lights on and, more importantly, taught Jim Waters what scientists actually needed versus what they said they wanted.

The breakthrough came in 1965, and it arrived through pure serendipity. Dow Chemical had developed a refractometer for analyzing plastics—a device that measured how light bent as it passed through materials. They needed someone to manufacture and market it. Waters licensed the technology, and suddenly sales took off "like a rocket," as Jim would later recall. For the first time, Waters Associates had a product with real market demand and healthy margins.

But Jim Waters was already thinking bigger. He'd been watching developments in liquid chromatography (LC), a technique for separating complex chemical mixtures that was gaining traction in pharmaceutical research. The problem was that existing LC systems were massive, temperamental beasts—think room-sized mainframe computers before the PC revolution. Scientists needed something that could sit on a laboratory bench, work reliably, and not require a PhD in mechanical engineering to operate. In 1967, Waters introduced the ALC-100 (Analytical Liquid Chromatograph), a breakthrough instrument that would lay the foundation for the modern pharmaceutical industry's analytical capabilities. The ALC-100, which was introduced in 1967, is widely considered to be the first successful commercial HPLC. It was a benchtop system equipped with a Milton Roy pump, syringe injection, and two detectors: a Waters differential refractometer and a UV detector from Laboratory Data Control.

This wasn't just incremental improvement—it was category creation. While competitors were still building room-sized instruments that required dedicated facilities, Waters had put liquid chromatography on a laboratory bench. The system represented Jim Waters' philosophy perfectly: make it practical, make it reliable, and make it accessible to working scientists.

But the real breakthrough—the moment that transformed Waters from equipment vendor to pharmaceutical industry partner—came in 1972. Picture this scene: Harvard University, the laboratory of Professor Robert Woodward, already a Nobel laureate for his 1965 Chemistry prize. Woodward was attempting one of the most complex chemical syntheses ever undertaken: vitamin B12. His team had hit a wall trying to separate two positional isomers of a critical intermediate compound.

One Friday in 1972, Woodward's postdoc Helmut Hamberger came to Waters with a problem. He was trying to separate isomers of an intermediate in the synthesis of vitamin B-12. Woodward had left for Europe, entrusting Hamberger with solving this seemingly impossible separation problem.

Jim Waters' response revealed both his confidence and his humility. "I didn't know who Woodward was. He was just some chemist at Harvard," James Waters says. But his colleague James Little understood the opportunity immediately: "If we can solve a problem for him, we can sell a lot of instruments".

Waters personally took an ALC-100 to Harvard. Within a week—a week!—they had accomplished the separation that had stumped one of the world's greatest chemists. When Woodward returned from Europe, Hamberger and Waters presented him with 200 milligrams of the pure compound. The Harvard triumph didn't just solve a scientific problem; it established Waters' reputation as the company that could solve the unsolvable.

The impact rippled through the pharmaceutical industry immediately. If Waters' instruments could enable Woodward's vitamin B12 synthesis, what else could they accomplish? Orders poured in from pharmaceutical companies worldwide. The message was clear: this wasn't just laboratory equipment; this was the key to drug discovery.

By the time Jim Waters was building this reputation, he was operating with just five employees. Five! Yet they were establishing the innovation culture that would define Waters for the next half-century. Every customer problem was a potential product. Every limitation in existing technology was an opportunity. Every frustrated scientist was a future advocate.

The numbers tell the story of explosive growth that followed. By 1972, Waters had introduced the M6000 pump, providing pulseless flow at 6,000 psi—a major innovation that eliminated the pulsation problems plaguing competitor systems. The company was no longer just assembling components; they were designing the future of analytical chemistry from the ground up.

What Jim Waters understood, perhaps intuitively, was that scientific instruments aren't just tools—they're enablers of discovery. Every improvement in separation capability, every reduction in analysis time, every increase in sensitivity translated directly into faster drug development, safer food, and better understanding of our world. He wasn't selling equipment; he was selling capability.

III. The Millipore Era: From Acquisition to Independence (1973–1994)

The transformation from scrappy startup to industry leader began with an unlikely partnership. In 1969, Dimitri D'Arbeloff, president of Millipore Corporation, joined Waters' board of directors. Millipore, already established in filtration and purification, saw the potential in Waters' liquid chromatography technology. Their $600,000 investment provided more than capital—it brought marketing expertise and distribution channels that Waters desperately needed.

The timing was perfect. The pharmaceutical industry was exploding with new drug discovery programs, environmental regulations were creating demand for analytical testing, and Waters had the technology everyone needed. In 1972, Dow Chemical joined the party, investing $700,000 for a 20% stake. Waters now had the backing of two industry giants, but Jim Waters maintained control and, crucially, the company's innovative culture.

1973 marked a pivotal moment: Waters Associates went public on what would become the Nasdaq, raising capital for expansion while maintaining its entrepreneurial spirit. What followed was a period of growth that would make even today's tech unicorns envious. Between 1972 and 1977, Waters achieved a staggering 40% compound annual growth rate. This wasn't the frothy growth of dot-com speculation—this was real revenue from real products solving real problems.

By 1978, Waters had a 40% market share in liquid chromatography and was five times bigger than any competitor. Think about that dominance for a moment. In a highly technical market with sophisticated buyers, Waters had achieved the kind of market share that platform companies dream about. They did it not through network effects or switching costs (those would come later), but through pure technical superiority and customer focus.

The success attracted inevitable attention. In May 1980, Millipore acquired the company for $167 million and the company was referred to as the Waters Chromatography Division of Millipore. For Jim Waters and early investors, it was a spectacular outcome. For Waters as an organization, it marked the beginning of a complex chapter.

Life inside Millipore started promisingly. Waters maintained its product development momentum, launching new column technologies and expanding internationally. The corporate parent provided resources for growth—new manufacturing facilities, expanded R&D budgets, global distribution networks. Waters opened facilities in Ireland and expanded throughout Europe and Asia. On paper, it was the perfect marriage of innovation and scale.

But corporate life brought unexpected challenges. Due to competition, the early 1980s recession, the early 1990s recession, and lost focus, the company's growth stalled in the 1980s and early 1990s. D'Arbeloff, the chairman of the company, died of cancer and the COO and CTO died in a helicopter crash while commuting between facilities. The human tragedy was devastating, but the business impact was equally severe. Waters lost not just leaders but institutional knowledge and strategic direction.

The anticipated synergies between Waters and Millipore never fully materialized. The anticipated synergies never materialized. Millipore's filtration business and Waters' chromatography business served similar customers but required different technologies, sales approaches, and support structures. The corporate overhead designed for Millipore's mature business stifled Waters' entrepreneurial culture.

By the early 1990s, it was clear that Waters needed independence to thrive. The chromatography market was evolving rapidly, with new competitors emerging from Europe and Japan. Waters' technology advantage was eroding, and the company needed to move fast to maintain its leadership position. Inside the Millipore bureaucracy, "fast" wasn't in the vocabulary.

In 1994, an investor group led by management purchased the company for $360 million. The management buyout, led by CEO Douglas Berthiaume, was a bet that Waters could recapture its innovative spirit as an independent company. The price—more than double what Millipore had paid fourteen years earlier—reflected both Waters' solid business fundamentals and the conviction that unleashed potential existed.

The buyout team faced immediate challenges. They inherited a business that had been optimized for corporate reporting rather than market responsiveness. Product development cycles had stretched. Customer relationships had become transactional rather than collaborative. The competitive landscape had shifted dramatically, with Hewlett-Packard (later Agilent) and Perkin-Elmer making serious investments in liquid chromatography.

But they also inherited tremendous assets: an installed base of thousands of instruments, deep customer relationships in pharmaceutical companies, and a brand that still commanded respect. Most importantly, many of the original Waters innovators remained, waiting for the chance to build again.

The first priority was cultural transformation. The new management team stripped away corporate layers, pushing decision-making back to the people closest to customers and technology. They reinvested in R&D, focusing on the next generation of separation technologies. They rebuilt the sales organization, emphasizing technical expertise over relationship management.

The second priority was product innovation. That year, the company introduced Symmetry HPLC columns. These columns, using new packing materials and manufacturing techniques, offered better reproducibility and longer life than competitive products. It was a signal to the market: Waters was back in the innovation game.

IV. The IPO & Building a Platform (1995–2003)

The boardroom at Waters Corporation in early 1995 buzzed with the kind of nervous energy that only comes before a major public offering. CEO Douglas Berthiaume and his team were about to take Waters public for the second time in its history, but this IPO would be different. This wasn't a small Nasdaq listing like 1973—this was a New York Stock Exchange debut that would value the company at nearly $1 billion.

The public markets loved the Waters story. Here was a company with 60% gross margins, recurring revenue from consumables and service, and dominant positions in growing markets. The IPO priced at the top of its range, and the stock promptly soared. Waters was suddenly flush with capital and currency for acquisitions, but more importantly, it had a scorecard that would drive extraordinary operational discipline.

What followed was a run that would make Waters the darling of Wall Street. The company delivered 21 consecutive quarters of double-digit earnings growth, along with two stock splits. This wasn't financial engineering—Waters was genuinely growing both top line and bottom line through a combination of market expansion, new product introduction, and operational excellence.

The secret sauce was a business model transformation that Jim Waters could never have imagined. While instruments remained the visible face of Waters, the real profit engine was becoming the recurring revenue streams. Every Waters system installed created an annuity of column sales, service contracts, and spare parts. A pharmaceutical company might spend $100,000 on an instrument but would spend multiples of that over the instrument's lifetime on consumables.

Think of it as the razor-and-blade model, but with $100,000 razors and $5,000 blades. The beauty was that once a Waters system was validated in a pharmaceutical company's processes, switching to a competitor became almost impossible due to regulatory requirements. The FDA required extensive revalidation for any change in analytical methods. Waters wasn't just selling instruments; they were embedding themselves in their customers' regulatory documentation.

But Berthiaume knew that organic growth alone wouldn't maintain Waters' leadership position. The analytical instrument industry was consolidating, and Waters needed to expand its technology portfolio. The opportunity came in 1997 with a British company called Micromass.

In 1997, Waters acquired Micromass for $176 million, entering the mass spectrometry market. This wasn't just an acquisition—it was a strategic transformation. Mass spectrometry (MS) was becoming the perfect complement to liquid chromatography. While LC separated complex mixtures, MS identified exactly what those separated components were. Together, LC-MS created the most powerful analytical technique in pharmaceutical discovery.

Micromass brought more than technology. Based in Manchester, England, it gave Waters a European R&D center and deep expertise in a complementary field. The cultures meshed surprisingly well—both companies were founded by scientists, both focused on practical solutions, and both had that particular combination of technical rigor and commercial pragmatism that defines successful instrument companies.

The integration playbook Waters developed with Micromass would become a template for future acquisitions. Rather than forcing immediate integration, Waters maintained Micromass as a separate brand and operation initially, focusing first on commercial synergies. Waters' sales force could now offer complete LC-MS solutions. Micromass gained access to Waters' installed base and pharmaceutical relationships. Revenue synergies came first; cost synergies could wait.

By 1998, the strategy was paying spectacular dividends. Net sales peaked at $618.81 million, and Waters entered the ranks of New England's top 50 public companies. The company that had started in a police station basement was now mentioned in the same breath as Gillette, Raytheon, and State Street.

But beneath the financial success, Waters was quietly building something more important: a platform for the next phase of analytical science. The combination of LC and MS wasn't just additive—it was transformative. Scientists could now identify proteins, characterize metabolites, and understand biological systems at a molecular level. Waters was no longer just supporting pharmaceutical quality control; they were enabling drug discovery itself.

The R&D investment during this period was staggering. Waters was spending over 7% of revenue on R&D, high for an instrument company but necessary to maintain technical leadership. The focus was on three areas: improving separation technology (smaller particles, better column chemistry), enhancing mass spectrometry (better sensitivity, higher resolution), and critically, developing software to handle the massive amounts of data these systems generated.

The software piece often gets overlooked in the Waters story, but it was becoming crucial. A single LC-MS run could generate gigabytes of data. Pharmaceutical companies needed not just to collect this data but to analyze it, archive it, and ensure it met regulatory requirements. Waters' Empower software, launched in 2002 as a rebrand of their Millennium platform, became the industry standard for chromatography data management.

By 2003, Waters had built all the pieces for a major breakthrough. They had the separation science expertise from four decades of LC development. They had mass spectrometry capability from Micromass. They had the software infrastructure to handle complex data. They had relationships with every major pharmaceutical company. And they had a business model that turned capital equipment sales into recurring revenue streams.

The stage was set for what would become the most important product launch in Waters' history. In the company's R&D labs, engineers were putting the finishing touches on a system that would redefine what was possible in liquid chromatography. They called it UPLC—Ultra Performance Liquid Chromatography—and it would change everything.

V. The UPLC Revolution: Redefining an Industry (2004–2014)

The auditorium at the 2004 Pittsburgh Conference—the analytical chemistry world's premier event—was standing room only. Word had leaked that Waters was about to announce something big. Really big. As the lights dimmed and the presentation began, even the most jaded industry veterans leaned forward. What they witnessed over the next hour would fundamentally reshape the analytical instruments industry.

In 2004, the company introduced the Acquity UPLC system, which brought greater speed, resolution, and sensitivity to chromatographic separations and was considered a breakthrough technology. But calling UPLC a breakthrough understates its impact. This was Waters creating an entirely new category of analytical instrumentation, one that would obsolete billions of dollars of installed equipment and force every competitor to scramble for a response.

The technical achievement was staggering. Waters had developed particles just 1.7 microns in diameter—less than half the size of standard HPLC particles. These tiny particles, packed into specially designed columns, could withstand pressures up to 15,000 psi—more than double what existing systems could handle. The physics was elegant: smaller particles meant shorter diffusion paths, which meant sharper peaks and better resolution. Higher pressure meant faster flow rates without sacrificing separation quality.

But here's what made it brilliant from a business perspective: UPLC wasn't just incrementally better than HPLC. It was transformationally better. Analysis times dropped by up to 10x. A separation that took 30 minutes on HPLC could be completed in 3 minutes on UPLC. For a pharmaceutical company running hundreds of samples per day, this wasn't just a nice-to-have improvement—it was a complete reimagining of laboratory productivity. The environmental impact was equally dramatic. A solvent savings of 82% can be achieved by moving to the UPLC method at the 2.1-mm scale; the solvent savings increases to 97% by moving to the UPLC method at the 1.0-mm scale. For large pharmaceutical companies running thousands of analyses per day, this translated to millions of dollars in solvent cost savings and massive reductions in hazardous waste disposal.

To date, Waters has installed thousands of UPLC systems, replacing the workload of tens of thousands of HPLC systems, supported more than 500 peer-reviewed papers, demonstrated reduced solvent consumption up to 95 percent for greener laboratories. Think about the mathematics of that statement: one UPLC system replacing the workload of multiple HPLC systems. This wasn't just an upgrade; it was a complete reimagining of laboratory capacity.

The competitive response was swift and, from Waters' perspective, perfect. Every major competitor—Agilent, Thermo Fisher, Shimadzu—rushed to develop their own "UHPLC" (Ultra High Performance Liquid Chromatography) systems. But here's the genius of Waters' strategy: they had created and trademarked the term "UPLC." Competitors couldn't use it. They were forced to adopt the generic "UHPLC" terminology, which implicitly positioned them as followers.

Moreover, Waters had a multi-year head start on the technology. The 1.7-micron particles weren't just smaller versions of existing technology—they required entirely new chemistry, new manufacturing processes, and new quality control methods. Waters had been working on this for years before launch. Competitors trying to catch up discovered that matching Waters' performance wasn't just about building higher-pressure pumps; it required reimagining the entire system architecture.

The installed base dynamics were particularly favorable to Waters. A pharmaceutical company that had validated methods on UPLC couldn't easily switch to a competitor's UHPLC system without extensive revalidation. In the regulated pharmaceutical industry, this created enormous switching costs. Once Waters got UPLC into a customer's validated processes, that customer was essentially locked in for years.

Waters didn't rest on the initial UPLC success. They rapidly expanded the platform with variants targeted at specific applications. The H-Class for customers wanting UPLC performance with HPLC-like operation. The I-Class for ultimate performance. The M-Class for nano- and micro-scale separations. Each variant addressed a specific market segment while maintaining the core UPLC advantage.

The software integration was equally important. Waters' Empower software was updated to handle the massive data streams that UPLC generated. A single UPLC run might produce 10 times more data points than an HPLC run due to the sharper peaks and faster acquisition rates. Waters ensured that customers could not only generate this data but manage it, analyze it, and maintain regulatory compliance.

By 2010, UPLC had become the de facto standard for high-end pharmaceutical analysis. Regulatory agencies worldwide had accepted UPLC methods. Scientific journals were publishing hundreds of papers using UPLC. Waters had successfully created a new category and positioned themselves as its permanent leader.

The financial impact was staggering. UPLC systems commanded premium prices—often 50% more than comparable HPLC systems. The columns and consumables for UPLC were also premium-priced. Yet customers gladly paid because the productivity gains far exceeded the additional costs. A pharmaceutical company might pay $200,000 for a UPLC system versus $130,000 for an HPLC system, but if that UPLC system replaced three HPLC systems and reduced analysis time by 80%, the ROI was obvious.

The UPLC story also demonstrated Waters' ability to cannibalize its own products when necessary. UPLC directly competed with Waters' own HPLC systems, which still generated significant revenue. Many companies would have slow-rolled such a disruptive technology to protect existing revenue streams. Waters did the opposite—they pushed UPLC aggressively, knowing that if they didn't disrupt themselves, someone else eventually would.

By 2014, a decade after launch, UPLC had transformed from revolutionary technology to industry standard. Waters had installed thousands of systems worldwide, generated billions in revenue, and most importantly, established a competitive moat that persists to this day. Competitors had caught up somewhat on the technology, but Waters maintained advantages in particle chemistry, system design, and crucially, the installed base of validated methods.

The UPLC revolution wasn't just about building a better instrument. It was about understanding customer workflows, regulatory requirements, and the economics of laboratory operations. It was about having the courage to obsolete your own products and the execution capability to deliver transformational rather than incremental improvement. Most of all, it was about proving that even in mature industries, true innovation can create entirely new categories and sustainable competitive advantages.

VI. Modern Expansion & Strategic Acquisitions (2006–2023)

The conference room at Waters headquarters in September 2020 had an unusual energy. After months of virtual meetings during the pandemic, the executive team had gathered to finalize a CEO transition that would mark only the fourth leadership change in the company's 62-year history. In September 2020, Udit Batra was named President and Chief Executive Officer of the company. Batra, coming from Merck KGaA's life science business, represented a new generation of leadership—one that understood both the traditional pharmaceutical market and the emerging frontiers of cell therapy, gene therapy, and precision medicine.

But before diving into the Batra era, we need to understand the strategic foundation built through nearly two decades of careful acquisitions. Waters' M&A strategy from 2006 to 2023 reveals a masterclass in capability building rather than empire building.

In 2006, Waters acquired Vicam, provider of bio-separation and rapid detection products for improving food safety and quality. On the surface, food safety might seem like a distraction from Waters' core pharmaceutical business. But Waters understood something crucial: the same separation technologies used to ensure drug purity could ensure food safety. More importantly, food safety regulations were tightening globally, creating a secular growth driver independent of pharmaceutical spending cycles.

Vicam brought Waters into conversations they'd never been part of before—with food manufacturers, agricultural companies, and government regulators focused on contamination detection. The technology was complementary, the customers were different, and the growth dynamics were uncorrelated with pharma spending. It was diversification done right.

The TA Instruments division, originally acquired in 1996, was continuously expanded through the 2000s and 2010s. Thermal analysis might seem distant from chromatography, but Waters recognized the synergy: the same pharmaceutical companies using LC-MS to characterize drug molecules needed thermal analysis to understand their physical properties. By offering both, Waters became a more strategic partner to drug development teams.

Then came 2020, a year that would test every company's strategy and execution. While the world grappled with COVID-19, Waters made a bold move. In January 2020, Waters acquired Andrew Alliance, a producer of software and robotics for laboratory automation, for $77.4 million. The timing seemed odd—why focus on lab automation during a pandemic?

But Waters saw what others missed: COVID had accelerated laboratory digitization by years. Scientists working remotely needed automated systems that could run without constant supervision. The Andrew Alliance acquisition gave Waters a foothold in laboratory robotics just as the market was exploding. The $77.4 million price tag would look like a bargain within months as demand for lab automation skyrocketed.

Udit Batra's arrival as CEO in September 2020 marked an inflection point. Unlike his predecessors who had grown up in the analytical instruments industry, Batra brought a different perspective. At Merck, he'd run a $7 billion life sciences business. He understood not just what instruments customers bought, but why they bought them and how they created value in drug development.

Batra's strategic vision centered on three pillars: commercial execution, innovation, and digital transformation. But his first major move would dwarf all previous Waters acquisitions. In May 2023, Waters acquired Wyatt Technology for $1.36 billion in cash. This wasn't just Waters' largest acquisition ever—it was a strategic masterstroke that positioned the company at the forefront of the biologics revolution. Waters Corporation (NYSE:WAT) today announced it has entered into an agreement to acquire Wyatt Technology, a pioneer in innovative light scattering and field-flow fractionation instruments, software, accessories, and services, for $1.36 billion in cash, subject to certain adjustments.

Wyatt Technology brought something unique: light scattering technology that could characterize large molecules, proteins, and even entire cells. With more than 80% of its rapidly growing revenues tied to large molecule applications, Wyatt accelerates Waters ability to build a high-growth business in bioanalytical characterization for new modalities. This includes cell and gene therapies, which represents a significant opportunity with a $1.8 billion total addressable market and 10-12% projected annual growth.

The strategic logic was compelling. Traditional small molecule drugs—the kind Waters' LC-MS systems had been analyzing for decades—were giving way to biologics: antibodies, proteins, cell therapies, gene therapies. These new modalities required different analytical techniques. Light scattering could determine the size and aggregation state of proteins. Field-flow fractionation could separate nanoparticles and viral vectors used in gene therapy. Waters' traditional technologies and Wyatt's capabilities were perfectly complementary.

Wyatt is a privately held family company with 2022 revenues of approximately $110 million, and a global workforce of more than 200. The price—over 12 times revenue—raised eyebrows. But Batra and his team saw what others missed. Wyatt has a three-year compound annual growth rate of 20%, which is expected to grow low-teens over the near- to mid-term and has an existing adjusted operating margin of approximately 40%.

Moreover, Waters is expected to generate over $70 million in annual revenue synergies by the fifth year following transaction close. These weren't just theoretical synergies. Waters could immediately start selling Wyatt's technology to its vast pharmaceutical customer base. Every Waters LC-MS customer working on biologics was a potential Wyatt customer.

The acquisition also revealed Batra's strategic philosophy: Waters needed to be wherever the pharmaceutical industry was going, not just where it had been. Cell and gene therapies represented the future of medicine. By 2023, the FDA was approving multiple cell and gene therapies annually. Each approval created demand for analytical tools throughout the development and manufacturing process.

The integration approach was telling. Unlike many acquirers who immediately rebrand and absorb acquisitions, Waters maintained Wyatt as a distinct brand and operation. The Wyatt family members who had built the business stayed on. The Santa Barbara facility remained operational. This wasn't about cost synergies through consolidation; it was about capability expansion and market access.

Batra's broader transformation of Waters went beyond acquisitions. He restructured the commercial organization, investing in digital tools for the sales force and improving customer service. He accelerated R&D investment, focusing on software and data management capabilities. He pushed for operational excellence, implementing lean manufacturing principles and supply chain optimization.

The geographic expansion strategy also evolved under Batra. While China had been a growth driver for years, geopolitical tensions and local competition were creating headwinds. Waters diversified its geographic focus, investing in India, Southeast Asia, and Latin America. Manufacturing facilities were strategically located not just for cost but for market access and supply chain resilience.

By 2023, Waters had primary manufacturing facilities in 9 U.S. locations as well as 11 international locations including Wexford, Wilmslow, Birmingham, Hüllhorst, Singapore, Bangalore, Beijing, and Shanghai. This global footprint provided both operational flexibility and customer proximity.

The software and informatics capabilities that Waters built during this period often get overlooked but were crucial for competitive differentiation. The waters_connect platform unified data from various instruments, enabling customers to manage complex workflows across their laboratories. In an era of increasing data complexity and regulatory scrutiny, this software layer became as important as the instruments themselves.

Looking at the acquisition pattern from 2006 to 2023, a clear strategy emerges. Waters wasn't trying to become a conglomerate like Danaher or Thermo Fisher. Each acquisition—Vicam for food safety, Andrew Alliance for automation, Wyatt for biologics characterization—extended Waters' core separation science capabilities into adjacent markets or complementary technologies. This focused diversification reduced dependence on any single market while maintaining technical coherence.

The cultural transformation under Batra was equally important. Waters had always been an engineering-driven company, focused on technical excellence. Batra brought customer-centricity to the forefront. Product development now started with customer workflows, not technical capabilities. Sales conversations shifted from features to outcomes. Marketing evolved from product specifications to customer success stories.

By the end of 2023, Waters had positioned itself for the next phase of pharmaceutical innovation. The traditional small molecule drugs that had driven growth for decades were becoming generic. The future belonged to biologics, cell therapies, gene therapies, and personalized medicine. Through strategic acquisitions, focused R&D, and cultural transformation, Waters had evolved from a chromatography company to a comprehensive analytical solutions provider for the life sciences.

VII. Business Model & Competitive Dynamics

If you want to understand Waters' business model, forget everything you know about selling scientific equipment and think instead about selling enterprise software. Not because Waters sells software (though they do), but because their economic model mirrors the most successful software companies: land and expand, high switching costs, recurring revenue, and customer lock-in that would make any SaaS executive jealous.

The genius begins with the initial instrument sale. A pharmaceutical company evaluating a Waters UPLC system sees a $150,000-$300,000 capital expenditure. What they don't fully appreciate is that they're not buying equipment—they're entering a 10-15 year economic relationship. That initial system will generate 2-3 times its purchase price in recurring revenue through consumables, service contracts, and software licenses over its lifetime.

Let's break down the razor/blade model that Waters has perfected. The "razor"—the instrument—is actually sold at healthy margins, often 40-50% gross margins. But the real profit engine is the "blades"—the columns, solvents, spare parts, and service contracts that keep the instrument running. These recurring revenues carry gross margins often exceeding 60% and in some cases approaching 70%.Fiscal 2023 revealed the model's resilience: Instrument sales down 7% but recurring revenues up 6%. During economic uncertainty, customers might defer new instrument purchases, but they can't stop running samples. Those columns need replacing every few months. Service contracts auto-renew. Software licenses require annual payments. For fiscal year 2023, instrument system sales decreased 7% as reported and 10% in organic constant currency, while recurring revenues increased 6% as reported.

The switching costs in Waters' business create a moat that Warren Buffett would admire. When a pharmaceutical company validates an analytical method using Waters equipment for FDA submission, that method becomes part of the drug's regulatory filing. Changing to a different vendor's equipment would require complete revalidation—a process that could take months, cost millions, and risk regulatory delays. No procurement manager wants to explain why they disrupted a drug manufacturing process to save 10% on instrument costs.

Consider the lifecycle of a typical Waters customer relationship. A biotech startup might begin with a single UPLC system for $200,000. As they progress through drug development, they add mass spectrometry capability—another $500,000. They need software to manage the data—$50,000 annually. Service contracts—$40,000 per year per instrument. Columns and consumables—$60,000 annually per instrument. By the time that biotech has a drug approved, they might have 20 Waters systems generating $2 million in annual recurring revenue.

The competitive landscape reveals why this model is so powerful. Primary competitors: Agilent Technologies, Thermo Fisher Scientific, Revvity, and Danaher. Each is formidable, but Waters' focused approach gives it advantages. Agilent, spun out of Hewlett-Packard, has broader reach but less depth in chromatography. Thermo Fisher is a $40 billion giant offering everything from pipettes to electron microscopes, but Waters often wins on specialization and support. Danaher's life sciences platforms are impressive, but they're built through serial acquisition rather than organic innovation.

Waters' competitive strategy isn't to be everything to everyone. They consciously chose not to compete in certain markets—clinical diagnostics, for example, despite the massive opportunity. Instead, they dominate specific niches where their technical expertise creates insurmountable advantages. In UPLC, they maintain roughly 70% market share at the high end. In certain pharmaceutical applications, their share approaches 80%.

The geographic dynamics add complexity to the model. China represented a particular challenge in 2023, with sales declining more than 20%. The combination of economic slowdown, geopolitical tensions, and local competition created headwinds. But Waters' response was instructive—rather than panicking, they focused on the applications where they had the strongest differentiation and deepest customer relationships.

The margin structure tells the story of operational excellence. Gross margins consistently above 58%, operating margins approaching 30% in good quarters. These aren't software margins, but for a company manufacturing complex physical products, they're exceptional. The key is the mix shift toward recurring revenue and the operational leverage from the installed base.

Service is a particularly attractive component of recurring revenue. A service contract might cost $40,000 annually for a $200,000 instrument—a 20% attachment rate that's nearly pure margin after the initial year. Waters employs an army of field service engineers who become embedded in customer operations. They're not just fixing instruments; they're consulting on methods, optimizing performance, and identifying opportunities for upgrades.

The consumables business operates on a different cadence than instruments but with equally attractive economics. A single UPLC column might cost $1,000-$2,000 and last for 500-1,000 injections. For a high-throughput pharmaceutical QC lab running hundreds of samples daily, that means replacing columns monthly. The beauty is that these aren't commodity products—each column is precisely manufactured to deliver specific separation characteristics. Customers can't simply switch to generic alternatives without risking method performance.

Software has become an increasingly important part of the recurring revenue story. Waters' Empower software doesn't just control instruments and collect data—it ensures regulatory compliance, manages audit trails, and integrates with laboratory information management systems. Once embedded in a customer's workflow, it becomes part of their quality system, making replacement almost unthinkable.

The business model also benefits from regulatory tailwinds. As regulations tighten globally—whether FDA requirements for pharmaceutical testing, environmental monitoring standards, or food safety protocols—demand for analytical instrumentation increases. Every new regulation potentially creates demand for more testing, more instruments, more consumables. Waters doesn't just sell into these regulations; they help shape them through participation in standards organizations and regulatory committees.

The capital allocation priorities reflect the strength of the model. Waters generates significant free cash flow—typically 20-25% of revenue. This funds R&D (7-8% of revenue), strategic acquisitions, and substantial returns to shareholders through dividends and buybacks. The company doesn't need massive capital expenditures to grow; the marginal cost of producing additional instruments or consumables is relatively low once the infrastructure is in place.

What makes Waters' business model particularly resilient is its diversification within focus. While pharmaceutical and biotech represent the largest market, industrial applications provide countercyclical balance. When pharma spending slows, chemical and materials companies might be expanding. Academic and government markets provide steady, if unspectacular, demand. Food safety and environmental testing offer secular growth independent of economic cycles.

The model's sustainability comes from continuous innovation within established categories. Waters doesn't need to invent entirely new markets; they need to make existing markets more efficient. Every improvement in separation speed, resolution, or sensitivity creates upgrade opportunities within the installed base. It's not disruption; it's evolution—and that's exactly what regulated industries want.

VIII. Financial Performance & Market Position

The numbers tell a story of resilience in the face of headwinds, but you need to read between the lines to understand what's really happening at Waters. Fiscal 2023: $2,956 million in revenue, essentially flat from 2022's $2,972 million. On the surface, stagnation. Dig deeper, and you see a company navigating through a perfect storm while positioning for the next growth cycle.

The headline numbers mask dramatic geographic disparities. Geographically, sales in Asia for fiscal year 2023 decreased 11% as reported and 7% in organic constant currency (with China sales declining more than 20%). China, once Waters' growth engine contributing nearly 20% of revenue, became an anchor. The decline wasn't just cyclical—it reflected structural changes in the Chinese market, from government procurement restrictions to local competition gaining ground.

But here's what the bears missed: Sales in the Americas increased 5% as reported. Sales in Europe increased 7% as reported. Waters was successfully diversifying away from China dependency while maintaining growth in mature markets—not an easy feat for a 65-year-old company.

Fiscal 2024 brought modest improvement: $2,958 million in revenue, flat year-over-year but with improving momentum through the year. The fourth quarter 2024 showed acceleration, with sales of $873 million growing 6% year-over-year. Instruments returned to growth, and recurring revenue maintained its steady climb. The patient was healing. The earnings story deserves careful attention. Non-GAAP EPS growth: $11.86 in 2024 vs $11.75 in 2023. Just 1% growth, but that includes a 5% headwind from foreign exchange. The underlying operational performance was actually quite strong, with 6% earnings growth before currency impacts. GAAP operating income margin of 27.9%; operational excellence drove adjusted operating income margin expansion to 31.0%, effectively neutralizing the challenges posed by foreign exchange headwinds.

These margins in a manufacturing business are exceptional. For context, Apple's operating margins hover around 30%, and they're selling products with massive scale advantages. Waters achieves similar margins while manufacturing complex scientific instruments in relatively small volumes. The secret? Pricing power from technical differentiation and the high-margin recurring revenue streams.

Cash flow generation remains robust. Generated $762 million in operating cash flow; $744 million in free cash flow, representing 25% of full-year sales, and a free cash flow to adjusted net income ratio of 105%. This isn't a capital-intensive business despite manufacturing complexity. Waters converts nearly all its earnings into cash, funding growth while returning capital to shareholders.

The capital allocation framework under Batra has been disciplined. First priority: organic investment in R&D and commercial capabilities. Second: strategic M&A like Wyatt that extends capabilities into adjacent markets. Third: return of capital through dividends and opportunistic buybacks. The company suspended buybacks during the Wyatt acquisition to delever but has maintained its dividend throughout.

Stock performance tells a story of volatility and recovery. From peaks above $400 in 2021, the stock traded down to the $270 range in late 2022 as China concerns and pharma spending normalization weighed on sentiment. By late 2024, it had recovered to the $350-370 range as the business stabilized and growth resumed. The valuation—roughly 30x forward earnings—seems rich until you consider the quality of the business model and the secular growth drivers.

The geographic mix evolution is crucial for understanding future growth potential. While China declined dramatically, other emerging markets picked up slack. India, growing at double-digit rates, is becoming a major pharmaceutical manufacturing hub. Southeast Asia benefits from supply chain diversification away from China. Latin America offers untapped potential in food safety and environmental monitoring.

Even mature markets show surprising resilience. The U.S. pharmaceutical market, despite patent cliffs and pricing pressure, continues to invest in analytical capabilities for biologics and personalized medicine. Europe, with its stringent environmental regulations, drives demand for advanced analytical techniques. These aren't high-growth markets, but they're stable and profitable.

The end-market dynamics reveal portfolio strength. Pharmaceutical at roughly 55% of revenue provides the core, but industrial applications (25%) and academic/government (20%) offer diversification. Within pharma, the mix is shifting from small molecule quality control to large molecule characterization—a higher-value application. The Wyatt acquisition accelerates this transition.

Operational excellence initiatives have quietly transformed the cost structure. Lean manufacturing reduced production costs. Supply chain optimization improved working capital efficiency. Digital tools enhanced sales productivity. These aren't headline-grabbing initiatives, but they've expanded margins by 200-300 basis points over the past three years, creating room for R&D investment and earnings growth even during revenue challenges.

The R&D investment strategy has evolved from pure product development to platform innovation. Rather than developing isolated instruments, Waters creates integrated workflows. The ACQUITY Premier Solution with MaxPeak HPS Technology, launched in 2024, exemplifies this approach—it's not just an instrument but a complete solution including hardware, software, columns, and methods.

Looking at relative performance, Waters has outperformed the broader analytical instruments sector despite its challenges. While competitors struggled with similar China headwinds and pharma normalization, Waters' margins remained more resilient and its innovation pipeline stayed robust. The focused strategy—being the best at separation science rather than the biggest in analytical instruments—continues to pay dividends.

The balance sheet remains conservative, even after the Wyatt acquisition. Net debt to EBITDA below 3x, interest coverage comfortable, and significant untapped credit capacity. This financial flexibility allows Waters to weather downturns while investing for growth—a luxury not all competitors enjoy.

What the numbers ultimately reveal is a company successfully navigating a transition. From dependence on China to geographic diversification. From small molecule focus to biologics leadership. From product sales to solution delivery. From cyclical growth to resilient recurring revenues. The financial performance might look modest on the surface, but the underlying transformation positions Waters for the next decade of growth.

IX. Technology & Innovation Pipeline

Standing in Waters' development laboratories in Milford, you'd see something that would surprise most investors: engineers obsessing over surface chemistry at the molecular level. Not the sexiest topic for a cocktail party, but this attention to infinitesimal details—how proteins interact with stainless steel surfaces, how to prevent ionic compounds from binding to metal—represents the next frontier in analytical science.

The ACQUITY Premier Solution with MaxPeak HPS Technology launched in 2024 represents the most significant innovation since UPLC in 2004. But unlike UPLC's dramatic performance leap, Premier solves a subtler problem that only analytical chemists truly appreciate: analyte/surface interactions that cause sample loss, peak tailing, and poor reproducibility.

Here's the brilliance: Waters developed High Performance Surfaces (HPS) Technology that creates a barrier between the sample and the metal surfaces inside the chromatography system. Think of it as Teflon for molecules—nothing sticks. For pharmaceutical companies analyzing increasingly complex biologics and oligonucleotides, this eliminates a major source of variability and sample loss. One customer reported recovering 40% more of their precious biologic sample using Premier technology.

The innovation required rethinking every surface that contacts the sample—from injection needle to detector flow cell. Waters couldn't just coat existing components; they had to develop new materials, new manufacturing processes, and new quality control methods. It took five years and millions in R&D investment for what seems like an incremental improvement. But that's exactly the kind of innovation that creates competitive moats in analytical instrumentation.

Software has become equally critical to Waters' innovation strategy. The waters_connect platform isn't just instrument control software—it's becoming an intelligent laboratory assistant. Using machine learning algorithms trained on millions of chromatograms, the software can now predict optimal separation conditions, identify potential problems before they occur, and even suggest method improvements.

Consider the method development challenge in pharmaceutical QC. Developing and validating an analytical method traditionally takes weeks or months of trial and error. Waters' Automated Method Development (AMD) system can screen hundreds of conditions overnight, using AI to identify optimal parameters. What once required a PhD chemist working for months can now be accomplished by a technician in days.

The integration of artificial intelligence goes deeper than automation. Waters is developing predictive maintenance algorithms that analyze instrument performance data to predict component failures before they occur. For a pharmaceutical production line where a single hour of downtime can cost hundreds of thousands of dollars, this predictive capability is invaluable.

But perhaps the most ambitious innovation is Waters' push into connected laboratory ecosystems. Every Waters instrument can now upload performance data to the cloud, creating a global database of analytical knowledge. Imagine a pharmaceutical company in Basel encountering an unusual peak in their chromatogram. The waters_connect platform can search similar patterns across millions of analyses worldwide, suggesting potential causes and solutions.

Privacy and security concerns are paramount—pharmaceutical companies won't share proprietary data. Waters solved this through federated learning approaches where the AI models learn from patterns without accessing raw data. It's technically complex but essential for building trust in regulated industries.

The sustainability angle has become a major innovation driver. Analytical laboratories consume enormous amounts of organic solvents—acetonitrile, methanol, hexane—most derived from petroleum and requiring hazardous waste disposal. Waters' new systems reduce solvent consumption by up to 95% compared to traditional HPLC. But they're going further, developing methods using green solvents like ethanol and even supercritical CO2.

The ACQUITY QDa mass detector represents innovation through simplification rather than sophistication. Traditional mass spectrometers require specialized expertise to operate and maintain. The QDa is designed for chemists who aren't mass spec experts—it's essentially plug-and-play mass detection. By democratizing mass spectrometry, Waters expanded their addressable market beyond specialized analytical laboratories.

Looking at emerging applications, Waters is positioning for the cell and gene therapy revolution. These new therapeutic modalities require entirely different analytical approaches. You can't analyze a CAR-T cell the same way you analyze an aspirin tablet. Waters is developing specialized technologies for characterizing viral vectors, analyzing cell surface proteins, and ensuring the quality of gene therapy products.

The convergence of LC, MS, and advanced data analytics is creating new possibilities. Waters' SYNAPT system combines ion mobility spectrometry with mass spectrometry, adding another dimension of separation. It's like going from 2D to 3D vision—suddenly you can see molecular structures that were previously hidden. For characterizing complex biologics with multiple post-translational modifications, this additional dimension is game-changing.

Biosimilar development represents a massive opportunity. As biological drugs lose patent protection, biosimilar manufacturers need to prove their versions are analytically similar to the originator. This requires incredibly detailed characterization—not just molecular weight but glycosylation patterns, higher-order structure, and aggregation state. Waters' comprehensive analytical platforms are perfectly positioned for this market.

The innovation pipeline extends into adjacent areas. Imaging mass spectrometry allows researchers to see where specific molecules are located within tissue samples—crucial for drug development and precision medicine. Waters' DESI technology can analyze tissue samples directly without complex preparation, potentially enabling real-time analysis during surgery.

Waters is also pushing the boundaries of miniaturization. Their microfluidic devices integrate sample preparation, separation, and detection on a chip the size of a microscope slide. While still in development, these "lab-on-a-chip" technologies could eventually enable point-of-care diagnostics and personalized medicine applications.

The competitive response to Waters' innovations reveals their impact. When Waters launched Premier, competitors scrambled to develop their own bio-inert technologies. When Waters introduced the QDa, everyone rushed to create simplified mass detectors. Being the innovation leader means competitors are always playing catch-up, buying Waters time to develop the next breakthrough.

R&D productivity has improved dramatically under Batra's leadership. Rather than pursuing moonshot projects, Waters focuses on solving specific customer problems with measurable value. Every innovation must have a clear business case: How much time will it save? How much will it improve data quality? What's the ROI for customers? This disciplined approach ensures R&D investments translate into commercial success.

The patent portfolio tells its own story. Waters holds over 2,000 patents worldwide, with particular strength in particle technology, surface chemistry, and mass spectrometry. But patents are just the beginning—the real protection comes from know-how. Manufacturing 1.7-micron particles with consistent properties requires expertise that can't be reverse-engineered from a patent filing.

Looking ahead, Waters is investing in several breakthrough technologies. Cyclic ion mobility adds yet another dimension to molecular separation. Next-generation particle technologies promise even better resolution and speed. Advanced AI algorithms could eventually automate method development entirely. While not all these bets will pay off, Waters only needs a few successes to maintain its innovation leadership.

The innovation culture at Waters combines academic rigor with commercial pragmatism. Many employees have PhDs and publish in peer-reviewed journals, but they're equally focused on customer value. This balance—deep science with practical application—defines Waters' approach to innovation and ensures their R&D investments generate returns.

X. Playbook: Key Business Lessons

Lesson 1: Creating New Categories Beats Competing in Existing Ones

The UPLC story from 2004 remains the gold standard for category creation in B2B markets. Waters didn't just build a faster liquid chromatograph—they invented Ultra Performance Liquid Chromatography and owned the terminology. Competitors were forced to use the generic "UHPLC," forever positioning themselves as followers. The lesson? If you're going to innovate, innovate so dramatically that you define a new category. Then own the language around that category.

The genius was in the execution. Waters filed for the UPLC trademark before launch. They published extensively in scientific journals using UPLC terminology. They trained customers to ask for "UPLC" not "fast LC" or "high-pressure LC." By the time competitors caught up technologically, the market vocabulary was set. Every non-Waters ultra-high-performance system was implicitly positioned as "not quite UPLC."

Lesson 2: Switching Costs in B2B Can Be More Powerful Than Network Effects

In consumer technology, network effects rule. In scientific instruments, switching costs dominate. When a pharmaceutical company validates a Waters method with the FDA, switching vendors means revalidation—months of work, regulatory risk, and potential production delays. Waters doesn't need billions of users; they need thousands of deeply embedded customers who can't afford to switch.

The switching costs compound over time. First, there's the validated method. Then trained operators who know Waters' software. Then a library of historical data in Waters' format. Then integration with laboratory information systems. Then service relationships and spare parts inventory. After five years, switching vendors isn't just expensive—it's organizational surgery.

Lesson 3: Operational Excellence Is a Competitive Advantage, Not Just Cost Reduction

Waters' ability to manufacture 1.7-micron particles consistently isn't just about quality—it's a competitive moat. Competitors can match the specifications on paper, but can they deliver the same batch-to-batch reproducibility? Can they scale production while maintaining quality? Operations excellence in complex manufacturing is incredibly difficult to replicate.

This extends beyond manufacturing. Waters' service organization, with response times measured in hours not days, becomes part of the value proposition. Their ability to maintain instruments in validated state through remote diagnostics prevents costly downtime. Operational excellence in every customer touchpoint creates stickiness that transcends product features.

Lesson 4: Managing Through Cycles Requires Portfolio Balance

Waters survived the 2023 China collapse because they had geographic and end-market diversification. While pharma spending is cyclical, food safety regulations steadily tighten. While China declined, India grew. While instruments sales dropped, recurring revenues held steady. The lesson: build a portfolio that has natural hedges.

But balance doesn't mean lack of focus. Waters stayed within separation science, avoiding the temptation to become a laboratory conglomerate. They diversified within their circle of competence, maintaining technical synergies while reducing market concentration risk.

Lesson 5: M&A Success Comes from Capability Building, Not Empire Building

The Wyatt acquisition for $1.36 billion looked expensive at 12x revenue. But Waters wasn't buying revenue—they were buying capability in light scattering technology essential for biologics characterization. Every major Waters acquisition—Micromass for mass spec, Vicam for food safety, Andrew Alliance for automation—added specific capabilities that enhanced the core business.

Compare this to roll-up strategies where companies buy for scale. Waters buys for technology and market access, maintaining the acquired company's innovation culture while leveraging Waters' commercial infrastructure. It's harder to execute but creates more value long-term.

Lesson 6: Recurring Revenue in Capital Equipment Requires Ecosystem Thinking

Waters generates 60%+ recurring revenue not by accident but by design. Every instrument sale creates multiple recurring revenue streams: columns that wear out, service contracts for compliance, software licenses for data management. But this only works if you think ecosystem from day one.

The key insight: make the recurring revenue elements essential, not optional. Columns aren't just consumables—they're part of the validated method. Service isn't just repair—it's compliance assurance. Software isn't just data collection—it's audit trail management. When recurring revenue solves critical problems, it becomes non-discretionary spending.

Lesson 7: Geographic Expansion Requires Localization Beyond Language

Waters' global success comes from understanding that analytical science has local flavors. Chinese customers care about traditional medicine analysis. Indian customers need methods for generic drug manufacturing. European customers prioritize environmental applications. Waters doesn't just translate manuals—they develop region-specific applications and support them locally.

This localization extends to business models. In emerging markets, Waters offers leasing and pay-per-use models recognizing capital constraints. In regulated markets, they emphasize compliance support. In academic markets, they provide educational resources and grants. One size doesn't fit all in global expansion.

Lesson 8: Innovation in Mature Markets Requires Solving Invisible Problems

The ACQUITY Premier with MaxPeak HPS Technology doesn't deliver dramatic performance improvements like UPLC did. It solves the subtle problem of analyte/surface interactions that only expert users notice. But for those experts analyzing precious biologics, eliminating sample loss is worth premium pricing.

The lesson: in mature markets, innovation isn't always about breakthrough performance. Sometimes it's about removing friction that customers have accepted as inevitable. Waters identified a problem customers didn't even articulate—they just assumed sample loss was unavoidable. By solving the "unsolvable," Waters created differentiation in a commoditizing market.

Lesson 9: Build for Regulation, Not Despite It

Waters doesn't view FDA regulations as constraints—they view them as competitive advantages. Every regulatory requirement creates an opportunity to embed Waters deeper into customer workflows. Data integrity regulations? Waters provides compliant software. Method validation requirements? Waters offers validation packages. Audit trails? Built into every system.

Competitors who view regulation as a burden to minimize will always be playing catch-up. Waters designs for regulation from the ground up, making compliance easier for customers while creating switching costs. In regulated industries, making compliance seamless is often more valuable than technical performance.

Lesson 10: Focus Beats Diversification in Technical Markets

Waters could have become another scientific conglomerate through acquisition. They had the cash flow and credibility to buy into adjacent markets—clinical diagnostics, life science tools, or industrial testing. Instead, they stayed focused on separation science, going deeper rather than broader.

This focus enables technical leadership that diversified competitors can't match. When you're competing against divisions of larger companies, focus becomes your advantage. Waters' engineers spend entire careers perfecting chromatography. Competitors' engineers get rotated through different divisions. Depth of expertise wins in technical markets.

The Meta-Lesson: Building Moats in Atoms, Not Bits

In an era obsessed with software and platforms, Waters reminds us that physical world moats can be just as powerful. Manufacturing expertise, application knowledge, and service capabilities can't be replicated with code. Customers can't download a competitor's product. There's no zero marginal cost distribution.

Building a moat in the physical world requires different muscles—patient capital investment, deep technical expertise, and operational excellence. It's harder than building software moats, but once established, these physical moats can last decades. Waters has been the leader in liquid chromatography for 50 years. Try finding a software company with that kind of staying power.

XI. Bear Case vs. Bull Case

Bear Case: The Structural Challenges

Let's start with the elephant in the room: China. The 20%+ decline in 2023 wasn't just a cyclical downturn—it reflects structural challenges that won't easily reverse. The Chinese government's anti-corruption campaigns have permanently changed purchasing patterns. Local competitors like Shimadzu and local Chinese manufacturers are gaining ground with "good enough" technology at 50% of Waters' price. Most concerning, the geopolitical tensions between the U.S. and China create regulatory uncertainty that could limit Waters' ability to sell advanced technologies.

The math is sobering. If China was 15-20% of revenues at peak and that permanently resets to 10%, Waters has lost a major growth driver. Replacing that growth from India and Southeast Asia will take years, and these markets don't offer the same pricing power as China did during its boom years.

Pharmaceutical spending normalization post-COVID presents another structural headwind. The pandemic pulled forward years of analytical instrument purchases as pharma companies rushed to develop vaccines and therapeutics. Now we're seeing the hangover. Big pharma capital budgets are under pressure as patent cliffs loom and R&D productivity remains challenging. When Pfizer and Merck cut capital spending, Waters feels it immediately.

Competition is intensifying in ways that threaten Waters' premium pricing. Agilent has made massive investments in LC-MS, essentially matching Waters' technical capabilities in many applications. Thermo Fisher's acquisition spree has created a formidable competitor with deeper pockets and broader reach. Danaher's operational excellence through the Danaher Business System rivals Waters' own lean initiatives. Even Chinese competitors are moving upmarket, offering 80% of Waters' performance at 50% of the price.

The valuation creates its own risk. At 30x forward earnings, Waters trades at a premium to both the broader market and most analytical instrument peers. This valuation assumes successful execution, margin expansion, and return to growth. Any disappointment could trigger multiple compression. If Waters trades down to 25x earnings—still a premium multiple—that's a 17% decline from valuation alone.

Technological disruption lurks as a long-term threat. While Waters has successfully navigated technology transitions before, the next disruption might come from an unexpected direction. What if AI-driven analysis makes high-resolution separation less critical? What if new modalities like organ-on-a-chip reduce the need for traditional analytical testing? What if synthetic biology enables real-time quality control without offline analysis?

The recurring revenue model, while resilient, faces its own pressures. As customers optimize spending, they're extending service intervals, finding third-party service providers, and using generic consumables where possible. The installed base provides stability, but pricing power on recurring revenues isn't unlimited.

Geographic concentration in developed markets limits growth potential. The U.S. and Europe represent over 70% of revenues, and these are mature markets with single-digit growth at best. Emerging markets offer higher growth but come with currency risk, political instability, and lower margins. Waters' premium positioning doesn't translate easily to cost-conscious emerging markets.

Bull Case: The Underappreciated Strengths

But here's what the bears miss: Waters' installed base isn't just equipment in laboratories—it's embedded in the entire pharmaceutical development and manufacturing infrastructure. Those thousands of validated methods aren't getting replaced because China's economy slows or pharma cuts discretionary spending. The switching costs aren't just financial; they're regulatory, operational, and organizational.

The biologics revolution is just beginning, and Waters is perfectly positioned to benefit. By 2030, biologics are expected to represent 35% of pharmaceutical sales versus 25% today. Every biologic requires 10-100x more analytical testing than small molecules. The Wyatt acquisition gives Waters unique capabilities in light scattering for biologics characterization. As biosimilars proliferate, the need for detailed analytical comparison explodes.

Waters' recurring revenue resilience deserves a premium multiple. In 2023, despite instrument sales declining 7%, recurring revenues grew 6%. This isn't just resilience—it's a fundamental transformation of the business model. At 60%+ recurring revenue, Waters looks more like a life science tools company than a capital equipment manufacturer. Those businesses—like Thermo Fisher's life sciences solutions—trade at premium multiples.

The innovation pipeline under Batra is the strongest in years. The ACQUITY Premier launch shows Waters can still drive meaningful innovation in mature markets. The waters_connect platform positions Waters for the digital transformation of laboratories. The focus on sustainability aligns with customer ESG priorities and regulatory trends. This isn't innovation for innovation's sake—it's targeted at specific customer pain points with clear ROI.

Wyatt synergies are likely underestimated. Waters guided to $70 million in revenue synergies by year five, but this seems conservative. Every Waters pharma customer working on biologics is a potential Wyatt customer. The cross-selling opportunity is enormous. Moreover, Waters can leverage its operational excellence to improve Wyatt's margins over time.

Environmental and food safety regulations provide secular tailwinds independent of economic cycles. PFAS contamination is becoming a global concern, requiring sophisticated analytical techniques. Food fraud detection demands advanced methods. Climate change monitoring needs precise measurement. These aren't discretionary spending items—they're regulatory requirements that will drive demand regardless of economic conditions.

Management execution under Batra has been exceptional given the challenging environment. Margins expanded despite volume headwinds. The organization navigated the Wyatt integration while maintaining operational performance. Commercial execution improved with better sales force effectiveness. This management team has earned credibility.

Geographic diversification is working, just slowly. India grew double-digits in 2024. Southeast Asia is benefiting from supply chain shifts. Latin America remains underpenetrated. While China disappointed, Waters is successfully building presence in other high-growth markets. This diversification will pay off over time.

The balance sheet provides flexibility for opportunistic capital allocation. With modest leverage and strong cash generation, Waters can fund organic growth, pursue strategic acquisitions, and return capital to shareholders. In a downturn, this flexibility becomes even more valuable.

The Verdict

The bear case is real and shouldn't be dismissed. China won't return to boom times. Competition is intensifying. Valuation leaves little room for error. But the bull case rests on more than hope—it's grounded in the fundamental strength of Waters' business model, the secular growth in biologics, and the proven execution of current management.

The key question isn't whether Waters faces challenges—clearly it does. The question is whether the company's competitive advantages—switching costs, innovation capability, recurring revenues—are sufficient to navigate these challenges while generating acceptable returns. History suggests they are.

For long-term investors, the risk/reward depends on time horizon. Over the next year, multiple compression and continued China weakness could pressure the stock. Over the next five years, biologics growth, Wyatt synergies, and geographic diversification should drive solid returns. Over the next decade, Waters' position at the center of analytical science for life sciences seems secure.

The bear case makes Waters a "show me" story requiring proof of return to growth. The bull case sees a high-quality compounder temporarily depressed by transient factors. Both views have merit, which is why the stock will likely remain volatile until the growth trajectory becomes clearer.

XII. Epilogue: The Next Chapter

Standing in the same Milford headquarters where Jim Waters once sketched his first liquid chromatograph designs, you can feel the weight of history and the pull of the future in equal measure. The company that started in a police station basement now employs 8,200 people worldwide, generates nearly $3 billion in revenue, and enables scientific discoveries that touch billions of lives. But what would Jim Waters think of his company today?

He'd probably be amazed by the technology. The ACQUITY UPLC systems achieving separations in minutes that once took hours. Mass spectrometers detecting molecules at attogram levels—that's 10^-18 grams, a million times more sensitive than anything imaginable in 1958. Software using artificial intelligence to optimize methods. It's Arthur C. Clarke's famous maxim in action: sufficiently advanced technology indistinguishable from magic.

But he'd likely recognize the underlying mission hasn't changed. Waters still exists to give scientists better tools. Whether it's a pharmaceutical company developing a life-saving drug, a food manufacturer ensuring product safety, or an environmental agency monitoring water quality, Waters enables science that matters. The tools are infinitely more sophisticated, but the purpose remains constant.