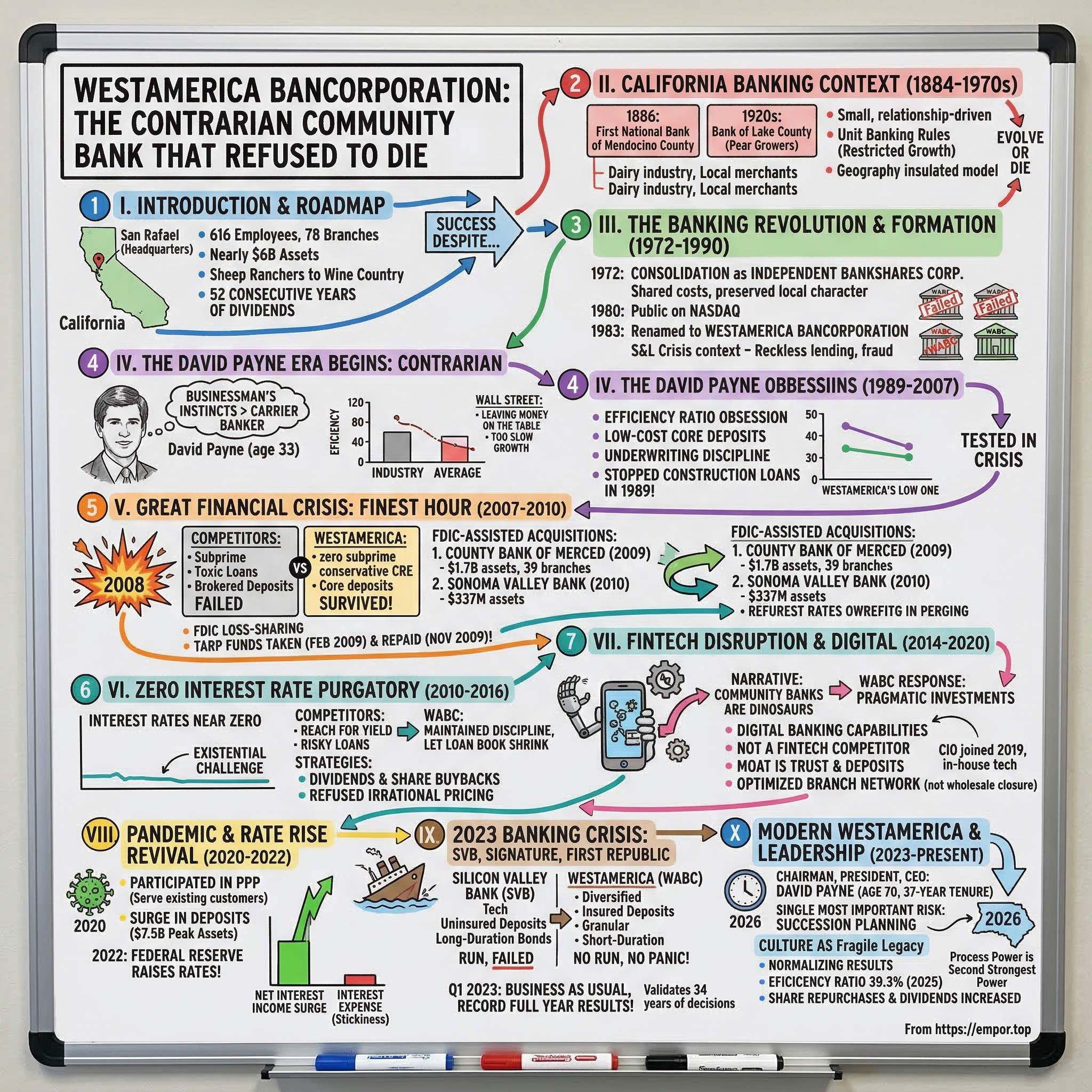

Westamerica Bancorporation: The Contrarian Community Bank That Refused to Die

I. Introduction and Episode Roadmap

Picture this: a bank with just 616 employees, sitting in a quiet office on Fifth Avenue in San Rafael, California, running nearly six billion dollars in assets across 78 branches scattered through the wine country, farmland, and foothills of Northern and Central California. No flashy headquarters in the Financial District. No celebrity CEO doing podcast tours. No mobile-first neobank strategy deck promising to "reimagine money." Just a community bank, doing community banking, the way it has been done since sheep ranchers in Mendocino County needed someone to hold their money in 1886.

And yet, somehow, this bank has survived everything the American financial system has thrown at it over the past four decades. The savings and loan crisis of the late 1980s. The dot-com bust. The Great Financial Crisis, when hundreds of California banks failed around it. A decade of zero interest rates that should have starved it to death. The fintech revolution that was supposed to make it irrelevant. And the regional banking panic of March 2023, when Silicon Valley Bank collapsed and depositors across the country suddenly remembered that banks can, in fact, fail.

Through all of it, Westamerica Bancorporation kept doing what it does: taking deposits, making conservative loans, running an absurdly lean operation, and mailing dividend checks to its shareholders. Fifty-two consecutive years of dividends, to be precise. The stock carries a beta of 0.59, meaning it moves about half as much as the broader market on any given day. In an industry defined by boom-and-bust cycles, leverage, and the occasional catastrophic failure, that kind of consistency borders on the surreal.

The central question of this story is deceptively simple: how? How did a small-town California bank not only survive an era of relentless consolidation, where thousands of community banks were swallowed by larger competitors, but actually thrive? The answer lies almost entirely in one man's contrarian philosophy, a philosophy so stubbornly conservative that Wall Street analysts spent years calling it foolish before grudgingly admitting it might be genius.

This is the story of David Payne, the printing-company heir who took over a scandal-plagued bank at age thirty-three and turned it into one of the most efficiently run financial institutions in America. It is the story of how saying "no" can be a competitive advantage. And it is, at its core, the anti-Silicon Valley Bank story, a case study in what happens when a bank decides that being boring is the whole point.

II. California Banking and the Founding Context (1884-1970s)

To understand why Westamerica exists, you have to understand the world that created it, a world where California's economy ran not on software and semiconductors, but on sheep, dairy cows, Gravenstein apples, and Bartlett pears.

In the decades after the Gold Rush, California's banking system developed in a peculiar fashion. The big San Francisco banks, institutions like Wells Fargo and Bank of America's predecessor, Bank of Italy, were tightly linked to the railroad interests and the urban mercantile class. If you were a sheep rancher in Mendocino County or a dairy farmer in Marin, those big-city banks had little interest in your business. The distances were vast, the roads were terrible, and the economics of small agricultural lending did not pencil out for institutions focused on trade finance and real estate speculation in the cities.

So the farmers and ranchers built their own banks. In 1886, the Foster family of Marin County chartered the First National Bank of Mendocino County, originally called the First National Bank of Cloverdale, to finance sheep ranching operations in the rugged hills north of San Francisco. Around the same time, dairy industry businesspeople and local merchants founded the Bank of Marin. In western Sonoma County, the Bank of Sonoma County opened its doors to serve cattle ranchers, dairy farmers, and the apple growers who supplied the nation's applesauce industry. By the 1920s, the Bucknell family and other prominent pear growers created the Bank of Lake County to serve the agricultural communities around Clear Lake.

These were not glamorous institutions. They were small, conservative, relationship-driven banks where the loan officer knew every borrower by name and probably attended the same church. Their deposits came from local businesses and farming families. Their loans went to fund equipment purchases, crop cycles, and the occasional modest real estate transaction. The concept of "growth at all costs" would have been incomprehensible to the men who ran them.

For decades, this model worked beautifully, insulated by geography and regulation. California's banking laws, like those in many states, restricted geographic expansion. Unit banking rules and geographic limitations meant that a bank in Mendocino County could not simply open branches in Sacramento or Los Angeles. This created a patchwork of small, locally focused institutions, each dominant in its own little fiefdom, each protected from direct competition by the very regulations that constrained its growth.

But the world these banks were built for was changing. By the 1960s and 1970s, the regulatory walls were beginning to crack. Interstate banking deregulation was on the horizon. The big banks were getting bigger. And the small agricultural communities of Northern California were evolving, their economies diversifying beyond farming into tourism, retirement communities, and, eventually, the spillover effects of the technology boom further south. The question for institutions like the Bank of Marin and First National Bank of Mendocino County was existential: adapt or die. Their answer, in 1972, was to band together.

III. The Banking Revolution and Westamerica's Formation (1972-1990)

In 1972, these scattered community banks took a step that would prove prescient: they consolidated under a single holding company called Independent Bankshares Corporation. The logic was straightforward. Individually, each bank was too small to invest in the technology, compliance infrastructure, and management talent needed to compete in an increasingly sophisticated industry. Together, they could share costs while preserving the local character that their customers valued. The holding company commenced operations in 1973, and for the next decade, it operated as a quiet confederation of small-town banks.

The 1980s brought two transformative developments. First, in 1980, the company went public on the NASDAQ, raising capital that would fuel its next phase of growth. Second, in 1983, the holding company renamed itself Westamerica Bancorporation, a signal that its ambitions extended beyond any single county or community. The name change coincided with the beginning of a nationwide wave of banking deregulation that would reshape the industry for decades.

The deregulation story is worth pausing on because it created both the opportunity and the threat that defined Westamerica's subsequent strategy. Throughout the 1980s, states began dismantling the geographic restrictions that had protected community banks. Interstate banking became legal. Branching restrictions loosened. Suddenly, the big banks could expand into territory that had been the exclusive domain of institutions like Westamerica. At the same time, the savings and loan crisis was ravaging California. Hundreds of thrifts and banks failed, casualties of reckless real estate lending, deregulation-fueled speculation, and outright fraud. The California banking landscape was littered with casualties.

For a well-capitalized, conservatively run bank, this chaos was an opportunity. Westamerica began a controlled program of acquisitions, picking up smaller banks and failed institutions at attractive prices. This was not the aggressive, empire-building acquisition strategy of a Bank of America or a Citicorp. It was opportunistic and disciplined, focused on filling in geographic gaps in Northern California and acquiring low-cost deposit bases that could be integrated without significant risk.

By the late 1980s, the company had grown meaningfully, but it was also carrying baggage. Management scandals and some bad loan decisions had tarnished its reputation. The board needed fresh leadership, someone who could clean house and chart a new course. They turned to an unlikely candidate: a thirty-two-year-old from one of the bank's founding families who had never actually been a banker.

IV. The David Payne Era Begins: Contrarian from Day One (1989-2007)

David Payne's path to the corner office of Westamerica Bancorporation was anything but conventional. Born in 1955, Payne grew up in the orbit of the Gibson family's business empire in Northern California, which included printing, publishing, and cable television operations. His grandfather, Luther Gibson, had chaired Vaca Valley Bank, one of Westamerica's predecessor institutions, giving Payne a family connection to banking but no direct experience running one. He joined Westamerica's board of directors in 1985, became Chairman in 1988 at the remarkable age of thirty-two, and assumed the roles of President and CEO in 1989.

Industry observers were skeptical, to put it mildly. Here was a company reeling from management scandals and bad loans, and the board was handing the keys to a kid whose primary qualification was running a family printing business. American Banker later described him as someone many people initially "wrote off as unqualified." What those skeptics missed was that Payne's outsider perspective would become his greatest asset. He did not arrive with the ingrained assumptions of a career banker. He arrived with a businessman's instinct for operational efficiency and a deeply conservative temperament that would prove almost prophetically well-suited to the decades ahead.

Payne's philosophy crystallized early and never wavered. "We aren't everything to everybody, and we don't try to be," he told interviewers. Where other bank CEOs talked about growth targets, market share, and geographic expansion, Payne talked about efficiency ratios, deposit costs, and underwriting discipline. He made a decision in 1989 that perfectly encapsulated his approach: he stopped making construction loans entirely. At the time, with California real estate booming, this seemed almost perverse. Construction lending was one of the most profitable activities a California bank could pursue. But Payne had watched the savings and loan crisis unfold in real time, and he understood that the loans generating the highest returns in good times were the same loans that destroyed banks in bad times.

This was the Payne playbook in its purest form: identify the risks that other banks were taking, and refuse to take them. While competitors gorged on commercial real estate lending, Payne kept Westamerica's loan book conservative and diversified. While other banks chased growth by offering above-market rates on deposits, Payne focused on building a franchise of low-cost core deposits, the checking and savings accounts of local businesses and individuals who banked with Westamerica out of habit and convenience, not because they were shopping for the highest yield. While the industry invested heavily in expansion, opening branches in every strip mall and suburban intersection, Payne ran a lean branch network and invested in in-house technology to reduce operational costs.

The efficiency ratio became his obsession. In banking, the efficiency ratio measures how much a bank spends to generate a dollar of revenue. A ratio of sixty percent means the bank spends sixty cents to make a dollar. The industry average for community banks typically hovers between fifty-five and sixty-five percent. Under Payne's leadership, Westamerica drove its efficiency ratio into the low forties and eventually into the high thirties, a level of operational discipline that few banks of any size have ever achieved. By 2025, the ratio stood at 39.3 percent, meaning Westamerica was spending less than forty cents to generate each dollar of revenue. To put that in perspective, many large banks with all their scale advantages cannot match that number.

Wall Street did not love this approach. Throughout the late 1990s and 2000s, analysts repeatedly criticized Payne for leaving money on the table. The bank was not growing fast enough. It was not leveraging its balance sheet aggressively enough. It was sitting on excess capital that could be deployed for higher returns. The stock traded at modest multiples, reflecting the market's assessment that Westamerica was a well-run but sleepy institution with limited upside.

Payne's response to these criticisms was to keep doing exactly what he was doing. He returned excess capital to shareholders through steady dividends and share buybacks rather than deploying it into risky lending or overpriced acquisitions. He maintained one of the lowest loan-to-deposit ratios in the industry, keeping a massive securities portfolio that provided liquidity and safety at the expense of higher-yielding but riskier loans. And he kept his cost of deposits almost impossibly low, often below ten basis points, by focusing on relationship banking and non-interest-bearing accounts rather than competing on price.

The man was, in essence, running the banking equivalent of a bunker. And for years, the world told him he was wrong, that he was too cautious, too conservative, too boring. Then 2008 happened.

V. The Great Financial Crisis: Westamerica's Finest Hour (2007-2010)

The financial crisis that began in 2007 and peaked in 2008-2009 was, for American banking, a reckoning of biblical proportions. Nationally, more than five hundred banks failed between 2008 and 2013. In California, the carnage was particularly severe. The state's intoxication with real estate had created a banking system riddled with toxic construction loans, overconcentrated commercial real estate portfolios, and aggressive growth strategies funded by volatile brokered deposits. When the music stopped, it stopped hard.

Washington Mutual, the nation's largest savings institution with over three hundred billion dollars in assets, was seized by the FDIC in September 2008, the largest bank failure in American history. IndyMac, another California-based institution, had already collapsed earlier that summer. Dozens of smaller California banks followed, their balance sheets poisoned by the same disease: too many bad loans to too many borrowers who could never have repaid them.

And in San Rafael, David Payne was watching it all unfold from behind a fortress balance sheet he had spent two decades constructing. Westamerica had almost zero subprime mortgage exposure. It had not chased construction lending. Its commercial real estate concentrations were well within regulatory guidelines. Its deposit base was composed overwhelmingly of low-cost core deposits from long-standing customer relationships, not the hot money that fled at the first sign of trouble. When the panic hit and depositors began moving their money out of banks they perceived as risky, some of that money flowed directly into Westamerica's accounts.

But Payne was not content to simply survive. He saw the crisis as an opportunity to execute a strategy he had been contemplating for years: acquiring failed competitors at deep discounts through FDIC-assisted transactions.

The first and most significant acquisition came on February 6, 2009, when the FDIC closed County Bank of Merced, California. County Bank had been a midsized institution with roughly $1.7 billion in assets and $1.3 billion in deposits, spread across thirty-nine offices in California's Central Valley. It had done exactly what Payne had refused to do: loaded up on risky real estate loans in an overheated market. When those loans went bad, County Bank went under. Westamerica stepped in as the acquiring institution, purchasing approximately $1.2 billion in loans and repossessed collateral under a loss-sharing agreement with the FDIC. Under the terms of the deal, the FDIC would absorb eighty percent of losses on the first $269 million of loan losses and ninety-five percent of losses beyond that threshold. For Westamerica, it was a remarkably asymmetric bet: the downside was capped, the upside was significant, and the deal instantly expanded the bank's geographic footprint and deposit base.

Thirty-nine County Bank offices reopened as Westamerica branches. The estimated cost to the FDIC's Deposit Insurance Fund was $135 million, a cost borne by the government, not by Westamerica. The deal was textbook Payne: wait for others to fail, buy their assets at a discount, let the government absorb the losses, and integrate the viable customers into a well-run operation.

The second FDIC-assisted acquisition came on August 20, 2010, when Westamerica acquired the failed Sonoma Valley Bank, a smaller institution with about $337 million in assets and $217 million in loans. Sonoma Valley Bank had collapsed under the weight of risky lending, and the FDIC later pursued its former officers for $12 million in damages. Once again, Westamerica absorbed the viable assets and customers while the FDIC bore the credit losses.

It is worth noting that Westamerica did participate in the government's Troubled Asset Relief Program, receiving $83.7 million in February 2009 under the Capital Purchase Program. But the way it handled TARP told you everything about the institution's character. While many banks that took TARP funds held onto the money for years, using it as cheap capital, Westamerica repaid the entire amount in two installments, in September and November of 2009, less than nine months after receiving it. The government earned $3.63 million in profit on the transaction. Payne had taken the money as a precautionary buffer during the most acute phase of the crisis, and returned it the moment it was clear the bank did not need it.

By the end of 2010, the crisis had transformed Westamerica's competitive position. The bank had expanded its footprint into the Central Valley, absorbed hundreds of millions of dollars in low-cost deposits, and established a reputation as one of the few truly safe community banks in California. The "boring bank" was suddenly looking like the smartest bank in the state.

VI. The Zero Interest Rate Purgatory (2010-2016)

If the financial crisis was Westamerica's finest hour, the decade that followed was its most grueling test. The Federal Reserve's response to the crisis was to drive interest rates to essentially zero and keep them there, year after year, well beyond what anyone initially expected. For a bank whose entire business model was built around earning a spread between what it paid depositors and what it earned on loans and securities, this was an existential challenge.

Consider the basic arithmetic. Westamerica's deposit costs were already extraordinarily low, often below ten basis points, meaning the bank was paying depositors less than a tenth of a percent on their money. In a normal interest rate environment, that gave the bank enormous room to earn a profitable spread on its assets. But when the Fed pushed rates to zero, the yields on the bank's securities portfolio and loan book collapsed too. The spread narrowed painfully. Net interest income, the lifeblood of any community bank, came under intense pressure.

The temptation in this environment was enormous. Banks across the country responded to margin compression by "reaching for yield," making riskier loans at longer maturities, buying longer-duration securities, or entering business lines they had no experience in. The logic was seductive: if you cannot earn a reasonable return on safe assets, you have to take more risk to maintain profitability.

Payne refused. Westamerica maintained its conservative underwriting standards. It did not extend loan maturities to chase higher yields. It did not pile into long-duration bonds that would generate unrealized losses when rates eventually rose. It did not enter commercial real estate lending in a meaningful way, even as competitors were aggressively booking these higher-yielding loans. As Payne himself observed in interviews, "Every time I think loan pricing is going to be a little more rational, it isn't." He acknowledged that competitors were pricing loans at levels that were "either not profitable or not as profitable as we would want it to be." Rather than match those prices, he let the loan book shrink and redeployed assets into shorter-duration securities.

The financial results during this period reflected the pain. Revenue grew modestly, from $182 million in 2016 to $206 million in 2019. Net income was stable but unspectacular, hovering around $59 to $80 million. EPS crept from $2.30 to $2.98 over the same period. The stock, while never collapsing, underperformed growth-oriented bank stocks that were benefiting from aggressive lending and leverage.

Investors grew frustrated. Growth investors fled. Analysts questioned whether the Payne model was obsolete in a zero-rate world. Why own a bank that refused to grow when competitors were posting much higher returns on equity?

Payne's answer was dividends and buybacks. Rather than deploying capital into loans he considered mispriced, he returned it to shareholders. The bank maintained its unbroken streak of quarterly dividends, and periodically repurchased shares at what management considered attractive valuations. The implicit message was clear: we would rather give you your money back than invest it in loans we believe are priced irrationally.

This was the period that truly tested whether the Payne philosophy was a strategy or just stubbornness. The answer would not become clear until the next crisis. And the next crisis, as it turned out, would vindicate everything.

VII. The Fintech Disruption and Digital Transformation (2014-2020)

Layered on top of the interest rate challenge was a more existential question: could a 130-year-old community bank survive the digital revolution in financial services? By the mid-2010s, the narrative in financial media was unambiguous. Community banks were dinosaurs. The future belonged to neobanks like Chime, digital lending platforms like SoFi, and payment companies like Square that were unbundling traditional banking services and delivering them through sleek mobile apps at lower costs. The branch was dead. The relationship banker was a relic. Banking was being "disrupted," and the incumbents, especially the small, technology-challenged ones, were doomed.

Westamerica's response to this narrative was characteristically pragmatic. The bank invested in digital banking capabilities, including online and mobile banking platforms, but it did not panic and overspend on flashy technology partnerships or attempt to reinvent itself as a fintech competitor. The reason was grounded in a clear-eyed understanding of its customer base. Westamerica served small businesses and individuals in Northern and Central California communities, many of them in smaller towns and rural areas. These customers valued personal relationships, local knowledge, and the convenience of having a banker who understood their business. They were not, by and large, the urban millennials who were flocking to Chime and Venmo.

This is not to say that Westamerica ignored technology. Under Chief Information Officer Brian Donohoe, who joined in 2019, the bank continued to build and maintain its technology infrastructure in-house rather than outsourcing to third-party vendors, a Payne-era decision that gave the bank more control over its systems and, critically, kept costs low. The bank's 616 employees operated 78 branches across 21 counties, a number that reflected careful optimization over decades. Branches that were not generating sufficient activity were closed or consolidated, while others were reformatted to handle changing customer behavior. The goal was not to eliminate branches but to right-size the network.

The fundamental insight that guided Westamerica through the fintech era was that its moat was not technology. It was trust and deposits. A neobank could offer a slightly better mobile experience, but it could not replicate decades of relationships with local businesses, the inertia of established deposit accounts, and the comfort of having a physical branch in your town where you could walk in and talk to a real person. The switching costs in community banking are real: changing your business banking relationship means moving payroll, rerouting receivables, reestablishing lines of credit, and building trust with a new team. For Westamerica's core customers, the marginal convenience of a better app was simply not worth the disruption.

The branch closure trend across the industry continued to accelerate during this period, but Westamerica's approach was selective rather than wholesale. The bank recognized that its branches served a dual function: they were not just transaction processing centers, they were deposit-gathering outposts. And those deposits, overwhelmingly low-cost and sticky, were the raw material of the entire business model.

VIII. The Pandemic and Rate Rise Revival (2020-2022)

When COVID-19 shut down the California economy in March 2020, the banking industry faced yet another stress test. For Westamerica, the pandemic was manageable but required careful navigation. The bank participated in the Paycheck Protection Program, processing loans for existing customers to help small businesses survive the lockdowns. By the third quarter of 2021, average PPP loan balances stood at $145 million, declining to $69 million by year-end as the loans were forgiven by the SBA. The bank earned modest fee income from PPP, but Payne's approach was characteristically focused: serve existing customers first, do not chase PPP fee income from borrowers you have never met.

The pandemic also triggered a massive surge in deposits across the banking system. Government stimulus payments, reduced consumer spending, and general uncertainty drove cash into bank accounts at unprecedented rates. Westamerica's total assets swelled from $5.6 billion at the end of 2019 to $6.7 billion by the end of 2020 and peaked at $7.5 billion by the end of 2021. The bank was, quite literally, swimming in deposits it could not profitably deploy in a zero-rate environment. Net interest income crept up modestly, from $157 million in 2019 to $171 million in 2021, but the returns on all that excess liquidity were negligible.

Then came the turning point.

In March 2022, the Federal Reserve began raising interest rates for the first time in years, and the pace of increases accelerated rapidly through the year as inflation surged. For most banks, the rate hikes were a mixed blessing. Higher rates meant higher yields on new loans and securities, but they also created massive unrealized losses on existing bond portfolios purchased during the low-rate era. Banks that had loaded up on long-duration bonds to chase yield found themselves sitting on billions of dollars in paper losses, a problem that would later destroy Silicon Valley Bank.

Westamerica, characteristically, was positioned almost perfectly. Because Payne had refused to extend durations during the zero-rate years, the bank's securities portfolio was relatively short-dated and less vulnerable to the mark-to-market losses that plagued competitors. And because Westamerica's deposit base was overwhelmingly composed of low-cost core deposits and non-interest-bearing accounts, the bank did not have to raise deposit rates as aggressively as competitors who relied on rate-sensitive money.

The result was an earnings explosion. Net interest income surged from $171 million in 2021 to $220 million in 2022, driven by higher yields on the bank's asset portfolio while deposit costs barely budged. Interest expense in 2022 was just $1.9 million on a $7 billion balance sheet, an almost comically low number that reflected the extraordinary stickiness of Westamerica's deposit franchise. Net income jumped from $87 million to $122 million. EPS rocketed from $3.22 to $4.54.

The boring bank was printing money, and this time, the world was paying attention.

IX. The 2023 Banking Crisis: SVB, Signature, First Republic

On Thursday, March 9, 2023, Silicon Valley Bank disclosed that it had sold $21 billion in securities at a $1.8 billion loss and needed to raise capital. By Friday, a bank run was underway. By Sunday, the FDIC had seized the bank. Within weeks, Signature Bank and First Republic Bank had also collapsed, and the entire regional banking sector was in panic.

The parallels between what happened to SVB and what Westamerica had spent decades avoiding were almost too perfect. SVB had concentrated its deposit base in a single industry, technology startups, and funded those deposits with long-duration bonds that plummeted in value when rates rose. When depositors panicked, SVB could not liquidate its underwater securities fast enough to meet withdrawals. The bank failed not because its loans were bad, but because its balance sheet was fundamentally mismatched, exactly the kind of duration and concentration risk that Payne had been preaching against for thirty years.

Consider the contrast. Where SVB's deposits were concentrated in a single industry, Westamerica's were diversified across thousands of small businesses, individuals, and agricultural operations in twenty-one counties. Where SVB relied heavily on large, uninsured deposits that could flee overnight, Westamerica's deposit base was granular and predominantly insured. In the first quarter of 2023, non-interest-bearing deposits accounted for forty-seven percent of Westamerica's average deposits, while higher-cost time deposits represented just two percent. The bank's cost of deposit funding was three basis points, essentially zero.

Did Westamerica experience some deposit outflows during the crisis? Yes, total deposits declined 4.5 percent between December 2022 and March 2023, a moderate decline consistent with industry-wide trends as some depositors moved cash to too-big-to-fail institutions or money market funds offering higher yields. But there was no bank run. No panic. No emergency liquidity measures. Westamerica reported net income of $40.5 million and diluted EPS of $1.51 for the first quarter of 2023, business as usual during what was, for much of the banking industry, a near-death experience.

For the full year 2023, Westamerica posted its best results ever. Net interest income hit $280 million, up from $220 million the prior year, as the full impact of higher interest rates flowed through the asset portfolio. Net income reached $162 million, a record. EPS peaked at $6.06. The efficiency ratio remained in the low forties. The stock held up far better than most regional bank peers, which saw their shares hammered by fifty percent or more during the March panic.

The 2023 banking crisis validated every decision David Payne had made over the previous thirty-four years. The conservative underwriting. The refusal to chase yield. The obsession with low-cost core deposits. The short-duration securities portfolio. The fortress balance sheet. Every strategy that had seemed overly cautious in good times proved to be genius in bad times. And it proved it not just once, but twice, first in 2008 and again in 2023. The "sleepy community bank" had outlasted, outperformed, and out-survived institutions ten, twenty, fifty times its size.

X. Modern Westamerica and the Leadership Question (2023-Present)

As of early 2026, David Payne remains at the helm of Westamerica Bancorporation as Chairman, President, and Chief Executive Officer. He is seventy years old and has led the institution for thirty-seven years, a tenure that places him among the longest-serving bank CEOs in America. There has been no announced succession plan and no public indication that Payne intends to step down imminently.

The question of succession is the single most important qualitative risk facing Westamerica's shareholders. The company's strategy, culture, and competitive advantages are so thoroughly identified with one individual that it is fair to ask whether they can survive his eventual departure. Payne has never been just a CEO in the conventional sense. He has been the architect, the enforcer, and the embodiment of a philosophy that permeates every aspect of the organization. When he eventually steps aside, the new leader will inherit not just a bank but a culture, and cultures, as any organizational psychologist will tell you, are fragile things.

The current senior team reflects long tenures and deep institutional knowledge. Chief Credit Administrator Russell Rizzardi has been in his role since 2008. Banking Division Manager Robert Baker has been with the company since 1995. Chief Financial Officer Anela Jonas joined in a senior capacity in 2024. Chief Information Officer Brian Donohoe has been managing the bank's technology since 2019. This is a team that has been steeped in the Payne philosophy for years, if not decades, which offers some comfort on continuity.

The bank's recent financial performance, while still strong by absolute standards, has reflected the normalization of the interest rate tailwind. Net interest income declined from the 2023 peak of $280 million to $251 million in 2024 and further to $217 million in 2025. Net income fell from $162 million to $139 million to $116 million over the same period. EPS declined from $6.06 to $5.20 to $4.53. Total assets have contracted from the pandemic peak of $7.5 billion to approximately $6 billion, reflecting deposit outflows and the natural runoff of pandemic-era excess liquidity.

These declines, while notable, need context. The 2023 results were extraordinary, driven by the unprecedented speed of rate increases and the unique dynamics of the post-pandemic deposit surge. The 2025 results, while lower, still represent a highly profitable bank operating with exceptional efficiency. An efficiency ratio of 39.3 percent, a return on equity of roughly twelve percent, and a net profit margin above forty percent are numbers that most bank CEOs would celebrate.

In December 2025, the board authorized a new share repurchase program for up to two million shares, approximately eight percent of shares outstanding. The quarterly dividend was raised to $0.46 per share, or $1.84 annualized, representing a yield of approximately 3.6 percent. Since Payne became Chairman in 1988, dividends per share have risen twelvefold and capital levels have increased tenfold.

XI. The Business Model Deep Dive

Strip away the narrative and the history, and what you find at the core of Westamerica is a deceptively simple business model executed with unusual discipline. Understanding its components explains why the model works, and why it is so hard for competitors to replicate.

The deposit franchise is the foundation of everything. As of 2023, nearly half of Westamerica's average deposits were non-interest-bearing, meaning the bank paid nothing for almost half of its raw material. Higher-cost time deposits, the CDs that depositors shop around for, represented just two percent of the total. The bank's overall cost of deposit funding was three basis points, a number so low it barely registers. In a world where many banks pay one hundred or two hundred basis points for deposits, this is an almost unbelievable competitive advantage. These deposits are sticky because they are built on relationships, not rates. When a small business has its checking account, its payroll, and its line of credit at Westamerica, it does not switch banks because a competitor is offering a quarter point more on a savings account.

The loan portfolio reflects Payne's underwriting discipline. Westamerica makes commercial loans, residential and commercial real estate loans, and consumer installment loans, including indirect automobile loans. What it does not do is concentrate in any single sector or chase the highest-yielding, riskiest categories. Payne famously stopped making construction loans in 1989 and never resumed. The bank has consistently maintained one of the lowest levels of commercial real estate concentration among its peers. When loan demand does not meet Payne's pricing and credit standards, the bank simply does not make the loan. It deploys the capital into securities instead, accepting lower returns in exchange for lower risk and higher liquidity.

The efficiency obsession is what ties the model together. With 616 employees running a six-billion-dollar institution, Westamerica runs leaner than almost any comparable bank. The efficiency ratio of 39.3 percent in 2025 is not just good, it is extraordinary. To understand what this means in practice, consider that a typical community bank with a sixty percent efficiency ratio spends fifty percent more per dollar of revenue than Westamerica. Over decades, this compounding cost advantage is enormous. It means Westamerica can remain profitable at interest rate levels that would push less efficient competitors into the red.

The technology strategy supports this efficiency. By building and maintaining its systems in-house, Westamerica avoids the expensive vendor contracts and integration costs that plague many community banks. This approach requires talented internal technologists, which is why the CIO role has been a key position in the company, but it gives the bank greater control and lower long-term costs.

The branch network has been optimized over decades. Seventy-eight branches across twenty-one counties sounds like a lot until you realize that this is the result of careful pruning and acquisition integration over forty years. Each branch exists because it generates enough deposit activity to justify its costs. There are no vanity branches, no flagship locations designed to impress, no branches kept open for political reasons. Every location earns its keep.

Capital allocation follows a simple hierarchy: maintain a fortress balance sheet first, pay dividends second, buy back shares third, and make acquisitions only when exceptional opportunities arise. The dividend has been paid for fifty-two consecutive years. Share repurchases occur when management believes the stock is attractively valued. Acquisitions happen only when banks fail and can be purchased at steep discounts with FDIC loss-sharing protection.

Why is this model hard to replicate? Because it requires decades of patience and discipline in an industry that rewards short-term growth. Any bank CEO could theoretically adopt the Payne playbook: stop making risky loans, focus on low-cost deposits, run a lean operation, return capital to shareholders. But in practice, the pressures from investors, analysts, boards, and competitors to grow faster and earn more make it almost impossible to sustain this approach for thirty-seven years. The Payne model is not just a strategy, it is a culture, and building that culture took a generation.

XII. Porter's Five Forces Analysis

Understanding Westamerica's competitive position requires examining the structural forces that shape its industry and the specific niche the bank has carved out within it.

The threat of new entrants into community banking is moderate. Regulatory barriers are substantial: obtaining a bank charter requires significant capital, extensive regulatory approvals, and ongoing compliance costs that deter casual entrants. However, fintech companies have found ways to offer banking-like services without traditional charters, effectively entering the market through the side door. Companies like Chime, SoFi, and numerous payment platforms compete for the same customers without bearing the full regulatory burden. For Westamerica specifically, the threat is attenuated by the fact that its core market, small businesses and individuals in smaller Northern California communities, is less attractive to fintech disruptors focused on urban millennials and tech workers.

The bargaining power of suppliers, which in banking means primarily the providers of funding, is low to moderate. Westamerica's primary "supplier" is its depositors, and the bank's extraordinarily low cost of deposits reflects the weak bargaining position of individual depositors who value convenience and relationships over yield optimization. In wholesale funding markets, banks are price takers, but Westamerica's minimal reliance on wholesale funding makes this largely irrelevant.

The bargaining power of buyers, meaning borrowers and deposit customers, is moderate. Customers can and do switch banks, and the proliferation of digital alternatives has made comparison shopping easier. However, the switching costs for business banking relationships remain meaningful. Moving a business banking relationship involves significant operational disruption, and many of Westamerica's customers have been with the bank for decades.

The threat of substitutes is the most significant competitive force. Credit unions, which enjoy tax advantages that allow them to offer slightly better rates, compete directly for retail deposits. Large national banks offer breadth of services and technology platforms that community banks cannot match. Fintech platforms offer convenience and speed. Private credit funds compete for commercial lending opportunities. The substitution threat is real and ongoing, but Westamerica's defense, its combination of local presence, relationship depth, and low-cost deposits, has proven durable.

Competitive rivalry within community banking is intense and accelerating. Industry consolidation has been relentless: the number of FDIC-insured banks in the United States has declined from over fourteen thousand in 1985 to fewer than five thousand today. Margin compression, regulatory costs, and technology investment requirements create constant pressure to merge. Within this environment, Westamerica has survived by being more efficient and more conservative than competitors, allowing it to remain profitable at margin levels that would force less disciplined banks to sell.

XIII. Hamilton's Seven Powers Framework Analysis

Hamilton Helmer's Seven Powers framework provides a more granular lens for evaluating Westamerica's competitive moat. Of the seven powers, two stand out as genuinely strong, one is moderate, and the remainder are weak to moderate.

Scale economies provide a moderate advantage. Westamerica is not large enough to achieve the scale economies of a JPMorgan or Bank of America, but within its specific geographic markets, it has sufficient scale to spread fixed costs across a meaningful deposit base. Its 78 branches and in-house technology platform represent fixed investments that smaller competitors cannot easily match. The efficiency ratio advantage, nearly twenty percentage points better than many peers, reflects the compounding benefit of operational scale within a focused geographic footprint.

Network effects are essentially absent in community banking. Unlike payment networks or social media platforms, a bank does not become more valuable to each customer as more customers join. There is no inherent network effect in having your checking account at the same bank as your neighbor.

Counter-positioning is one of Westamerica's strongest powers. The Payne playbook, refusing to chase growth, maintaining ultra-conservative underwriting, and accepting lower returns in exchange for lower risk, is directly counter to the strategies pursued by larger competitors and growth-oriented community banks. Larger banks cannot easily adopt this approach because their shareholders, analysts, and compensation structures all incentivize growth. A large bank CEO who announced "we are going to stop growing and focus on efficiency" would be fired within a quarter. Westamerica's ability to pursue this strategy without facing immediate shareholder revolt reflects the institutional legitimacy that Payne has built over decades. It is a genuinely powerful form of counter-positioning.

Switching costs are moderate to strong, particularly for business banking customers. As noted earlier, moving a business banking relationship is operationally disruptive and psychologically costly. Many of Westamerica's commercial customers have been with the bank for decades, and the personal relationships with local bankers create a form of loyalty that transcends rate competition.

Branding provides a moderate advantage, primarily local in nature. Westamerica is a trusted and recognized brand in Northern and Central California, particularly in the smaller communities where it operates. This brand does not extend nationally and has limited value outside its geographic footprint, but within that footprint, it carries significant weight.

Cornered resources are weak to moderate. The low-cost deposit franchise is valuable, but it is not truly "cornered" in the Helmer sense, as other banks could theoretically build similar franchises over time. The closest thing to a cornered resource is the institutional culture and knowledge embedded in the long-tenured management team, but this is more accurately classified under Process Power.

Process Power is Westamerica's second strongest competitive advantage. The operational efficiency, underwriting discipline, and cultural DNA that Payne has built over thirty-seven years represent a form of organizational capability that is genuinely difficult to replicate. It is not enough to know what Westamerica does; you have to be able to do it consistently, year after year, through boom times and busts, without succumbing to the temptation to deviate. This kind of process excellence is built over decades and cannot be copied overnight.

The primary moats, then, are counter-positioning and process power: Westamerica does banking differently, and it has institutionalized that difference into an organizational culture that compounds over time.

XIV. Bull vs. Bear Case and Investment Thesis

The Bull Case

The case for Westamerica begins with its extraordinary track record of survival and profitability through every conceivable market environment. This is a bank that has navigated the S&L crisis, two recessions, a global financial meltdown, a decade of zero rates, a pandemic, and a regional banking panic, all while maintaining profitability and paying dividends every single quarter for over half a century. In an industry where catastrophic failure is an ever-present risk, that track record is worth a significant premium.

The fortress balance sheet provides a margin of safety that few banks can match. With minimal debt, conservative underwriting, and a deposit base that costs almost nothing, Westamerica can remain profitable in interest rate environments that would crush less disciplined competitors. The bank's negative net debt position, meaning its cash exceeds its borrowings, is a luxury in an industry defined by leverage.

The efficiency advantage compounds over time. At a 39 percent efficiency ratio, Westamerica has roughly twenty percentage points of cushion versus the industry average. This means that in a margin compression environment, Westamerica can remain profitable long after competitors are forced to cut dividends, sell assets, or seek merger partners. It is the operational equivalent of a low-cost producer in a commodity industry.

Rising interest rates benefit the bank disproportionately because of its low-cost deposit franchise. When rates rise, Westamerica's asset yields increase while its deposit costs barely move, creating a natural expansion in net interest margin. This dynamic was dramatically illustrated in 2022-2023, when net interest income surged by more than sixty percent.

Industry consolidation creates a potential pipeline of acquisition opportunities. As weaker banks fail or seek merger partners, Westamerica is positioned to acquire deposits and customers at attractive prices, as it did during the 2008-2010 crisis. The bank's clean balance sheet and regulatory standing make it an ideal acquirer for FDIC-assisted transactions.

Capital allocation is shareholder-friendly and disciplined. The combination of steady dividends, opportunistic share buybacks, and conservative reinvestment ensures that shareholders receive a consistent return on their investment without excessive risk.

The Bear Case

The most significant risk is succession. David Payne is seventy years old and has been CEO for thirty-seven years. There is no publicly announced succession plan, and the company's entire identity is bound up in one man's philosophy. The history of founder-led companies transitioning to professional management is mixed at best. If Payne departs and his successor loosens the conservative disciplines, the franchise could deteriorate rapidly.

California presents demographic headwinds. The state has experienced net population outflows in recent years, driven by high costs of living, tax burdens, and remote work flexibility. Northern California's smaller communities, Westamerica's core market, are particularly vulnerable to population decline. Fewer people means fewer deposits, fewer loans, and less economic activity to support a community bank.

The growth ceiling is real. The Payne model explicitly sacrifices growth for safety. This means the stock is unlikely to ever be a multi-bagger. In an environment where investors can earn seven percent on risk-free Treasury bills, the incremental return from owning a conservatively managed community bank stock may not justify the equity risk. The stock has historically traded at modest multiples, and there is no obvious catalyst for a significant re-rating.

Fintech competition and big bank encroachment continue to erode the community banking model. Every year, more banking activity migrates to digital channels where scale players have inherent advantages. While Westamerica's customers have proven loyal so far, generational turnover, as older, relationship-oriented customers are replaced by younger, digitally native ones, could gradually undermine the deposit franchise.

A return to lower interest rates would compress margins again, as it did during the 2010-2016 period. The bank's 2025 net interest income of $217 million, while solid, is already well below the 2023 peak of $280 million, demonstrating the sensitivity of earnings to the rate environment.

Regulatory burden falls disproportionately on smaller banks. Compliance costs are largely fixed, meaning a bank with six billion in assets bears a much higher per-dollar regulatory cost than a bank with six hundred billion. As regulatory requirements continue to expand in the wake of the 2023 banking crisis, these costs could further squeeze smaller institutions.

Key Metrics to Watch

For investors tracking Westamerica's ongoing performance, two metrics matter above all others.

First, the net interest margin, which measures the spread between what the bank earns on its assets and what it pays for its funding. This is the single most important driver of Westamerica's profitability, and it is highly sensitive to the interest rate environment. When the NIM expands, earnings grow; when it contracts, they shrink. Tracking the quarterly NIM tells you whether the fundamental economics of the business are improving or deteriorating.

Second, the efficiency ratio, which measures operating expenses as a percentage of revenue. This is the metric that captures Westamerica's most distinctive competitive advantage. As long as the efficiency ratio stays in the low forties or below, the bank's cost structure is providing a meaningful buffer against margin compression and competitive pressure. If the efficiency ratio starts drifting toward fifty percent or above, it would signal that the operational discipline that has defined the institution is beginning to erode.

XV. Epilogue and Reflections

There is a particular kind of courage in saying no. In an industry that celebrated growth, leverage, and innovation, David Payne built a career on restraint, discipline, and the willingness to be called boring. He stopped making construction loans when everyone else was getting rich on them. He refused to chase yield when the market punished him for it. He bought failing banks when others were still pretending their own balance sheets were clean. And he ran the tightest ship in community banking, not for a quarter or a year, but for nearly four decades.

The result is an institution that stands as a living rebuke to some of the most deeply held assumptions in American finance. You do not have to grow fast to create value. You do not have to take big risks to earn big returns. You do not have to disrupt anything to remain relevant. Sometimes, the most powerful strategy is simply to do the basics extraordinarily well, year after year, through every cycle, without deviation.

What Westamerica teaches is not just about banking. It is about the power of compounding discipline. Every year that Payne maintained his conservative underwriting standards, the bank's reputation for safety grew. Every cycle that vindicated his caution attracted more stable deposits. Every crisis that destroyed less disciplined competitors cleared the competitive landscape. The advantages accumulated slowly, almost imperceptibly, but over thirty-seven years, they became formidable.

There is a question that hangs over every contrarian success story: was it genius, or was it luck? In Payne's case, the answer seems clear. A strategy that works through one crisis might be luck. A strategy that works through five consecutive crises, each of different origin and character, is something else entirely. It is a system, a philosophy, a culture that has been tested in fire repeatedly and emerged intact each time.

The future of Westamerica is uncertain in the way that all futures are uncertain. Payne will eventually step aside. The interest rate environment will continue to fluctuate. Fintech will continue to evolve. California's demographics will continue to shift. But the institution that Payne built, with its fortress balance sheet, its low-cost deposits, its hyper-efficient operations, and its culture of disciplined conservatism, is better positioned to weather whatever comes next than almost any community bank in America.

In a world obsessed with disruption, scale, and growth at all costs, Westamerica Bancorporation is proof that there is another way. It is the boring bank that outlasted them all.

XVI. Further Reading and Resources

- Westamerica Bancorporation Annual Reports and Shareholder Letters (1990-present), available at westamerica.com

- FDIC Studies: "The Banking Crisis of 2008-2009: How Community Banks Survived"

- "The End of Banking" by Jonathan McMillan, on the evolution of banking business models

- SNL Financial / S&P Global Market Intelligence reports on California banking market dynamics

- American Banker profiles of David Payne and Westamerica Bancorporation

- FDIC Failed Bank List (2008-2010), documenting County Bank and Sonoma Valley Bank acquisitions

- "The Bankers' New Clothes" by Anat Admati and Martin Hellwig, on bank capital and regulation

- Federal Reserve Bank of San Francisco papers on community banking trends

- ProPublica TARP Bailout Tracker: Westamerica Bancorporation entry

- Westamerica investor presentations and quarterly earnings call transcripts, particularly 2008-2009, 2022-2023, and 2025 periods

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube