Verizon Communications: The Evolution of America's Network Giant

I. Introduction & Episode Roadmap

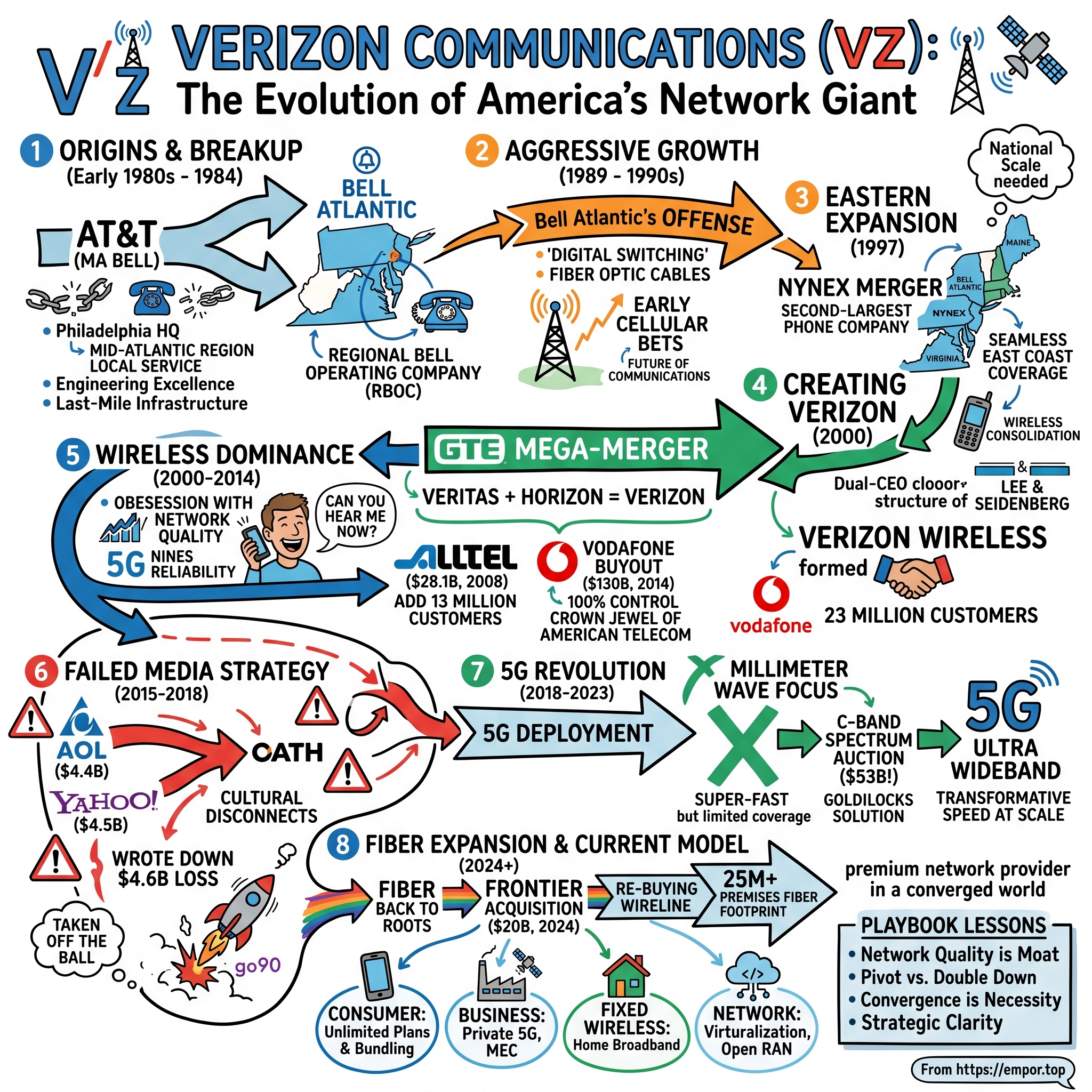

Picture this: It's 2000, the height of the dot-com bubble. Two telecom titans—Bell Atlantic and GTE—are about to merge in what would become one of the largest corporate marriages in American history. The executives gather in a boardroom, knowing they're creating something unprecedented: a telecommunications company that would combine the regional dominance of a Baby Bell with the national reach of an independent carrier. They needed a name that captured this ambition. After cycling through dozens of options, they landed on "Verizon"—a portmanteau of veritas (Latin for truth) and horizon (the limitless future ahead). Little did they know they were naming what would become America's most dominant wireless network.

Today, Verizon Communications stands as a colossus in American telecommunications. Headquartered in New York City, it's the world's second-largest telecommunications company by revenue and operates the largest wireless carrier in the United States, serving 146.1 million subscribers as of June 30, 2025. But how did a regional Baby Bell, born from the ashes of AT&T's court-ordered breakup, transform into the network giant that would pioneer 4G LTE, lead the 5G revolution, and now bet $20 billion on fiber's future?

This is a story of relentless consolidation, spectrum wars that cost tens of billions, network engineering excellence that became a cultural obsession, and strategic pivots—some brilliant, others disastrous. It's about how a company built on copper wires and telephone poles reinvented itself for the wireless age, stumbled trying to become a media company, then doubled down on what it does best: building networks.

We'll trace Verizon's journey from the 1984 Bell System breakup through its formation as Bell Atlantic, the transformative mergers with NYNEX and GTE, the creation of America's most reliable wireless network, the ill-fated media adventures with AOL and Yahoo, the $50 billion bet on C-band spectrum, and the recent $20 billion Frontier acquisition that brings the story full circle—back to fiber, the technology that started it all.

Along the way, we'll explore the strategic decisions that defined each era: Why did Bell Atlantic choose expansion over diversification in the 1990s? How did Verizon Wireless achieve network superiority when everyone had access to the same technology? Why did a company with engineering in its DNA think it could become a content powerhouse? And what does the Frontier acquisition tell us about the future of telecommunications?

The themes that emerge are striking: the power of network effects, the value of spectrum as a scarce resource, the importance of cultural fit in mega-mergers, and the eternal tension between being a utility and being a growth company. It's a playbook for building and maintaining competitive moats in capital-intensive industries, but also a cautionary tale about the limits of corporate transformation.

As we'll see, Verizon's story isn't just about technology or finance—it's about how American business and society communicate, connect, and evolve. From rotary phones to 5G smartphones, from copper lines to fiber optics, from regional monopolies to nationwide competition, Verizon has been at the center of every major shift in how Americans stay connected. The question now: Can it maintain that position as new technologies and competitors emerge?

II. Origins: The Bell System Breakup & Regional Bell Operating Companies

January 1, 1984. At the stroke of midnight, the most powerful monopoly in American history ceased to exist. AT&T—Ma Bell—was officially broken into eight pieces after a decade-long antitrust battle. For executives at the newly independent Bell Atlantic, gathered at their Philadelphia headquarters, it felt less like a corporate restructuring and more like a family torn apart. One engineer who was there that night later recalled: "We'd worked our entire careers for The Phone Company. Suddenly, we were on our own."

Bell Atlantic emerged from this breakup as one of seven Regional Bell Operating Companies (RBOCs), inheriting the local telephone operations across Pennsylvania, New Jersey, Delaware, Maryland, Virginia, and West Virginia. While AT&T kept long-distance services and Western Electric (equipment manufacturing), Bell Atlantic got what seemed like the consolation prize: local phone service in the mid-Atlantic region. But hidden in that inheritance was something invaluable—direct relationships with millions of customers and the last-mile infrastructure that connected them.

The antitrust case that created Bell Atlantic had been brewing since 1974, when the Justice Department filed suit against AT&T for using its monopoly power to stifle competition. Judge Harold Greene, presiding over the case, faced an unprecedented challenge: how do you break up a company that employed over one million people and operated the world's most sophisticated telecommunications network? His solution was surgical—separate the competitive businesses (long-distance, equipment) from the natural monopolies (local service). The theory was elegant; the execution would prove messy.

Raymond Smith, who would become Bell Atlantic's CEO in 1989, understood something crucial from day one: the company's regulated monopoly wouldn't last forever. While other Baby Bells focused on protecting their local franchises, Smith pushed Bell Atlantic to think bigger. "We can't just be the dial tone company," he told his leadership team. The company began investing heavily in new technologies—digital switching, fiber optic cables, and crucially, cellular telephony.

The cultural DNA of Bell Atlantic was pure Bell System: engineering excellence above all else. The company inherited AT&T's obsession with network reliability—the famous goal of "five nines" (99.999% uptime), which meant no more than 5.26 minutes of downtime per year. This wasn't just a technical specification; it was a religion. Engineers would drive through hurricanes to fix downed lines. Technicians carried business cards that said simply "I work for The Phone Company"—no further explanation needed.

But beneath this engineering culture, something else was stirring. In 1984, Bell Atlantic formed Bell Atlantic Mobile Systems, recognizing early that wireless technology could be more than just a niche product for wealthy executives. The company had inherited cellular licenses for major markets including Philadelphia, Pittsburgh, and Washington D.C.—spectrum that would later prove to be worth tens of billions. While Wall Street saw cellular as an expensive toy with limited market potential (McKinsey famously predicted only 900,000 cellular subscribers in the U.S. by 2000), Bell Atlantic's engineers saw something different: the future of communications.

The regulatory environment of the mid-1980s was schizophrenic. On one hand, the Baby Bells were heavily regulated monopolies, with state utility commissions controlling everything from pricing to service territories. On the other, they were suddenly expected to compete in emerging markets like cellular and data services. Bell Atlantic navigated this by becoming a master of regulatory arbitrage—using profits from regulated services to fund investments in competitive markets, all while maintaining the political relationships necessary to gradually loosen restrictions.

By the early 1990s, Bell Atlantic had established itself as the most aggressive of the Baby Bells. While others played defense, Smith played offense. The company was first to deploy digital switching across its entire network, first to test video-on-demand services, and among the most aggressive in building out cellular coverage. But Smith knew that regional scale wouldn't be enough. The future belonged to companies with national reach. Bell Atlantic needed to get bigger, and fast. The stage was set for the merger mania that would define the next decade.

III. The NYNEX Merger & Eastern Expansion (1997)

Ray Smith sat across from Ivan Seidenberg in a Manhattan conference room in late 1995, both men understanding the stakes. NYNEX controlled New York—the financial capital of the world—plus the lucrative Boston-to-Washington corridor. Bell Atlantic had the mid-Atlantic locked down. Apart, they were regional powers. Together, they could dominate the entire Eastern seaboard. "This isn't just about scale," Seidenberg argued, spreading a map across the table. "Look at the cellular footprint we'd create—continuous coverage from Maine to Virginia. "The merger was announced in April 1996 after two years of negotiations, creating what would become the nation's second-largest phone company controlling 39 million phone lines, more than one quarter of the nation's total. But the path to completion was anything but smooth. The deal faced scrutiny from regulators, resistance from competitors, and skepticism from Wall Street about whether two bureaucratic Baby Bells could successfully integrate.

The strategic rationale was compelling on paper. The combined company's assets serviced 25 percent of the overall U.S. market in 13 states and accounted for about 140-billion minutes of long distance traffic. More importantly, the region not only held one-third of the Fortune 500's headquarters, but the U.S. government's nerve center as well. This wasn't just about telephone lines—it was about controlling the communications infrastructure for America's economic and political power centers.

But integration proved challenging. NYNEX and Bell Atlantic had developed distinct cultures over their thirteen years of independence. NYNEX, shaped by the intensity of New York City and the intellectual hubs of Boston, had a more aggressive, urban sensibility. Bell Atlantic, rooted in Philadelphia and the mid-Atlantic, maintained more of the old Bell System's methodical, engineering-driven culture. One former NYNEX executive described the culture clash: "We were Wall Street; they were Main Street. We thought in quarters; they thought in decades."

The regulatory battles were fierce. Critics, including consumer groups, AT&T and MCI Communications Corp., argued that the merger essentially reduced future competition in the two companies' zones and would lead to higher rates. Consumer advocates painted a dystopian picture of re-monopolization. Gene Kimmelman of Consumers Union declared: "It is now clear that this administration's antitrust enforcers will not constrain the avalanche of telecommunications mergers".

Yet the companies pressed forward, making strategic concessions to win approval. The FCC approved the merger on August 14, 1997, subject to market-opening conditions designed to facilitate competition from Maine to West Virginia. The regulatory approval came with strings attached—commitments to open local markets to competitors, invest in advanced services, and maintain employment levels.

The wireless consolidation imperative loomed large in the merger calculus. Both companies had been building out cellular networks independently, creating a patchwork of coverage that frustrated customers who roamed between regions. The merger created continuous cellular coverage from Maine to Virginia—a powerful selling point in an era when "roaming charges" could double or triple a customer's monthly bill. This seamless East Coast coverage would prove crucial in competing with national players like AT&T Wireless and Sprint PCS.

Under the terms of the deal, Raymond W. Smith would remain chairman and CEO while Seidenberg would serve as vice chairman, president, and COO. After one year, Seidenberg would become CEO, and chairman upon Smith's retirement. This carefully choreographed leadership transition reflected the delicate balance needed to merge two proud organizations. But everyone knew the real prize wasn't NYNEX—it was what NYNEX made possible. The merger positioned Bell Atlantic to go after even bigger game.

IV. The GTE Mega-Merger: Creating Verizon (2000)

Chuck Lee, GTE's CEO, looked across the conference table at Ivan Seidenberg in July 1998. Outside the windows of GTE's Stamford, Connecticut headquarters, the telecommunications world was consolidating at breakneck pace. SBC had swallowed Pacific Telesis and was eyeing Ameritech. WorldCom had just announced its audacious $37 billion bid for MCI. "If we don't do this," Lee said, "we'll both be roadkill within five years." The deal they were about to announce would create a $150 billion telecommunications colossus—the largest merger in U.S. history at that time. The Bell Atlantic-GTE transaction was valued at more than $52 billion at the time of the announcement in July 1998, combining Bell Atlantic's sophisticated network with GTE's national footprint. But this wasn't just about size—it was about creating something entirely new in telecommunications: a company that could offer everything from local to long-distance to wireless to internet services across the entire United States.

GTE brought assets that Bell Atlantic desperately needed. Prior to the merger, GTE had been the largest independent telephone company in the U.S., providing local and wireless service in 29 states, as well as nationwide long distance and internet services. Unlike the Baby Bells, which were restricted by the Modified Final Judgment from offering long-distance services, GTE had no such limitations. It could bundle services in ways the RBOCs could only dream about.

The negotiations were complex, involving not just price but power. The new entity was headed by co-CEOs Charles Lee, former CEO of GTE, and Bell Atlantic CEO Ivan Seidenberg. This unusual dual-CEO structure reflected the delicate balance required to merge two proud organizations with distinct cultures. Lee brought GTE's entrepreneurial spirit and national perspective; Seidenberg brought Bell Atlantic's operational excellence and regulatory expertise.

In April 2000, two months before the FCC gave final approval, Bell Atlantic formed Verizon Wireless in a joint venture with Vodafone, which owned AirTouch. Bell Atlantic owned 55% of the venture while Vodafone retained 45%. The deal created a mobile carrier with 23 million customers. This wireless joint venture was crucial—it combined Bell Atlantic's East Coast wireless operations with GTE's national footprint and Vodafone's AirTouch properties, creating instant national scale.

The regulatory gauntlet was grueling. Bell Atlantic and GTE shareowners had to approve the deal, as did 27 state regulatory commissions, the Federal Communications Commission and the Justice Department. Each regulator extracted concessions: commitments to maintain rural service, promises to open networks to competitors, guarantees on employment levels. The approval came with 25 stipulations to preserve competition between local phone carriers, including investing in new markets and broadband technologies.

The name "Verizon" itself was a statement of intent. Marketing consultants had presented dozens of options, but Seidenberg and Lee kept coming back to this portmanteau of veritas and horizon. It signaled both reliability (truth) and forward-thinking (horizon)—a company rooted in Bell System values but looking toward a digital future. The name also had no geographic limitations, unlike "Bell Atlantic" or "GTE," reflecting the company's national ambitions.

On June 30, 2000, the merger officially closed. Verizon became the largest local telephone company in the United States, operating 63 million telephone lines in 40 states. The company also inherited 25 million mobile phone customers. But almost immediately, the new company faced challenges. Approximately 85,000 Verizon workers went on an 18-day labor strike in August 2000 after their union contracts expired. The strike was a reminder that creating a unified company culture would be harder than creating a unified network.

The early 2000s strategy was clear: leverage the combined network to dominate wireless while maintaining the cash cow wireline business. Verizon Wireless, under the leadership of Dennis Strigl, became the crown jewel. The company invested billions in network quality, understanding that in wireless, coverage and reliability were the only sustainable competitive advantages. This obsession with network superiority would define Verizon for the next two decades.

V. Building the Wireless Juggernaut: Verizon Wireless Era (2000-2014)

Paul Marcarelli adjusted his thick-rimmed glasses and walked through Times Square, cell phone pressed to his ear. "Can you hear me now?" he asked. "Good." It was 2002, and this simple phrase would become one of the most recognizable taglines in advertising history. The campaign, originally conceived by agency Bozell, featured Marcarelli as "Test Man" and ran from 2001 to 2010. In the early years, net customers grew 10% to 32.5 million in 2002 and 15% more to 37.5 million in 2003. Customer turnover dropped to 1.8% in 2001, down from 2.5% in 2000.

The campaign wasn't just clever marketing—it reflected a genuine obsession with network quality that permeated Verizon Wireless from top to bottom. Dennis Strigl, CEO of Verizon Wireless, had instituted a culture where network engineers were treated like rock stars. Every Monday morning, Strigl would review detailed network performance metrics, market by market, sometimes down to individual cell sites. Dropped call rates above 1% triggered emergency response teams. This wasn't just corporate theater; it was religious devotion to the idea that network quality was the only sustainable moat in wireless.

The Vodafone joint venture created an interesting dynamic. The British partner brought international expertise and capital but largely let Verizon management run the U.S. operations. This arrangement worked well when the business was growing rapidly, but as the wireless market matured, the ownership structure became increasingly awkward. Vodafone wanted dividends; Verizon wanted to reinvest in network expansion. Every major decision required negotiation between New York and London. In 2008, Verizon made its biggest wireless play yet: acquiring Rural Cellular Corp. for $2.7 billion in cash and assumed debt, followed by the blockbuster announcement that summer to purchase Alltel for $28.1 billion, including $22.2 billion in debt. The Alltel acquisition was audacious even by Verizon standards. The deal came only seven months after Alltel was bought by TPG Capital and Goldman Sachs Group's GS Capital Partners for $27.5 billion—the largest ever private equity investment in the U.S. wireless industry.

The acquisition included 13 million customers, which allowed Verizon Wireless to surpass AT&T in number of customers and reach new markets in rural areas. But the timing seemed insane. This was 2008—Lehman Brothers had just collapsed, credit markets were frozen, and the global financial system was teetering on the brink. Yet Verizon saw opportunity where others saw catastrophe. Goldman Sachs needed liquidity; Verizon had it. The private equity firms had loaded Alltel with debt at peak-market interest rates; Verizon could refinance at crisis-era lows.

The strategic logic was compelling. Alltel had been a roaming partner with Verizon for years, and both used CDMA technology and Qualcomm's BREW platform for content delivery. It also included 57 primarily rural markets that Verizon Wireless does not serve. The combined company would have more than 80 million customers, creating unassailable scale advantages in device procurement, network investment, and marketing.

The "Can You Hear Me Now?" campaign had done its job—Verizon's network was synonymous with reliability. But the company wasn't resting on its laurels. While AT&T was distracted integrating Cingular and dealing with the iPhone exclusivity (which began in 2007), Verizon was quietly preparing for the next technological leap: 4G LTE.

The decision to go all-in on LTE was controversial internally. CDMA had served Verizon well, and the company had billions invested in EV-DO technology. But Seidenberg and Strigl recognized that LTE represented a clean break—a chance to build a network from scratch, optimized for data rather than voice. In December 2010, Verizon launched the nation's first large-scale LTE network, covering 38 cities and 60 airports. AT&T wouldn't launch LTE until nearly a year later.

This first-mover advantage in 4G was devastating to competitors. By the time AT&T and Sprint were rolling out LTE, Verizon had already covered most of the country. App developers optimized for Verizon's network first. Enterprise customers standardized on Verizon's LTE for mission-critical applications. The network effect became self-reinforcing: the best network attracted the most customers, which generated the most revenue, which funded the best network. But the biggest move came on February 21, 2014, when Verizon Communications finalized the acquisition of Vodafone's 45% stake in Verizon Wireless for $130 billion. This deal marked one of the largest acquisitions in telecommunications history and the third-largest M&A deal ever. The transaction consisted of $58.9 billion in cash, $60.2 billion in Verizon stock, and additional considerations including $5 billion in senior notes.

The deal was transformative. Since January 2012, Verizon had paid $25.5 billion in dividends, 45% of which went to Vodafone. Now, all that cash flow would stay in-house. Lowell McAdam, who had succeeded Seidenberg as CEO in 2011, framed it perfectly: "Where can you buy a business that has 100 million loyal customers, 50% margins, that has no integration risk and a great feel in front of it to grow the business even further?"

The acquisition gave Verizon complete control over strategic decisions that had previously required negotiation with London. It could now move faster on network investments, pricing decisions, and technology choices. The timing was crucial—the wireless market was entering a new phase of competition with T-Mobile's "Un-carrier" disruption and Sprint's acquisition by SoftBank. Verizon needed the flexibility to respond quickly.

By 2014, Verizon Wireless had become the crown jewel of American telecommunications. Its network superiority was unquestioned, its customer base was the largest and most profitable, and its cash generation was staggering. The wireless business was generating over $80 billion in annual revenue with EBITDA margins approaching 50%. But success in wireless had masked problems elsewhere in the company. The wireline business was declining, enterprise growth was slowing, and younger consumers were increasingly looking to Silicon Valley, not telecom companies, for innovation. Verizon's next move would surprise everyone.

VI. The Failed Media Strategy: AOL, Yahoo, and go90 (2015-2018)

Tim Armstrong stood before a packed auditorium at AOL's New York headquarters on May 12, 2015, struggling to contain his emotions. "Today isn't just about joining Verizon," he told employees. "It's about building the first global mobile media company." Behind him, Lowell McAdam nodded approvingly. Verizon had just announced it would acquire AOL for $4.4 billion, and both men genuinely believed they were creating the future of digital media. Three years later, that vision would lie in ruins, with Verizon writing off $4.6 billion and essentially admitting defeat. The strategic rationale seemed compelling at the time. Verizon had 1.5 billion connected devices in the United States and touched 70 percent of U.S. Internet traffic. "If you look at what they're able to do from a value-add services standpoint, I think they're going to put more high-quality premium video, more high-quality advertising and commerce", Armstrong explained. The theory was that Verizon could leverage its vast trove of customer data—location, browsing habits, app usage—to create hyper-targeted advertising that would command premium prices.

But the cultural disconnect was evident from day one. Verizon was an engineering company that measured success in network uptime and customer satisfaction scores. AOL was a media company that lived on page views and ad impressions. When Verizon engineers visited AOL's offices, they were bewildered by the ping-pong tables and free kombucha. When AOL executives presented to Verizon's board, they were shocked by requests for five-year ROI projections on content investments. On June 13, 2017, Verizon completed its acquisition of Yahoo for $4.48 billion—$350 million less than the original offer after Yahoo disclosed two massive data breaches affecting more than 1 billion user accounts. The assets were combined with AOL brands under a new subsidiary called Oath, headed by Tim Armstrong. The name itself was telling—an "oath" suggested commitment and trust, but it sounded more like a curse word, which is what many Verizon executives would mutter when discussing the division's performance.

The cultural misalignment became even more pronounced with Yahoo. While AOL at least had Armstrong as a bridge between worlds, Yahoo brought its own dysfunctional culture—a company that had been in perpetual turnaround mode for a decade. Engineers from three different companies (Verizon, AOL, Yahoo) were supposed to work together on integrated platforms, but they couldn't even agree on basic technical standards.

Meanwhile, Verizon launched go90, its own mobile video streaming service aimed at millennials. The service, which debuted in October 2015, was supposed to be Verizon's answer to YouTube and Netflix. It featured content from Vice, Comedy Central, and the NFL. But go90 was a disaster from the start. The app was clunky, the content library was limited, and most importantly, it offered nothing that consumers couldn't get better elsewhere. By 2018, Verizon shut down go90 after burning through an estimated $1.2 billion.

The problems ran deeper than execution. Verizon fundamentally misunderstood the media business. In telecommunications, you build infrastructure once and monetize it for decades. In media, you need fresh content daily. In telecom, customer relationships last years; in media, attention spans are measured in seconds. Verizon executives talked about "synergies" and "convergence," but customers didn't care that their wireless carrier also owned HuffPost.

By December 2018, reality set in. Verizon announced it would write down the combined value of its AOL and Yahoo purchases by $4.6 billion—essentially admitting it had wasted half the money. Tim Armstrong departed, Oath was renamed the generic "Verizon Media," and the company began looking for an exit. In May 2021, Verizon sold the media assets to Apollo Global Management for $5 billion, less than half what it had paid. The media adventure was over.

The failure wasn't just financial—it was strategic. While Verizon was distracted playing media mogul, T-Mobile was revolutionizing wireless pricing, AT&T was building a legitimate media empire with Time Warner, and new competitors like Dish were acquiring spectrum. Verizon had taken its eye off the ball, and competitors were closing the gap. Hans Vestberg, who became CEO in 2018, had a clear mission: get back to basics. For Verizon, that meant one thing above all—the network.

VII. The 5G Revolution & C-Band Spectrum Wars (2018-2023)

Hans Vestberg stood in a Verizon lab in New Jersey in early 2018, holding what looked like a pizza box with antennas. This was a 5G millimeter wave radio, and Vestberg believed it would transform not just Verizon, but entire industries. "This isn't about faster phones," he told his engineering team. "This is about autonomous vehicles, remote surgery, smart cities. This is about the fourth industrial revolution." Three years and $50 billion later, that vision would collide with the harsh realities of physics, competition, and economics. Verizon's 5G strategy began with a fundamental bet: millimeter wave spectrum was the future. In October 2018, the company launched 5G Home, a fixed wireless service, in select neighborhoods of four cities. This was followed by mobile 5G services in spring 2019. The company's first live 5G network trial occurred in 2018, setting precedents for network deployment. Partnering with Qualcomm and Ericsson, Verizon executed the first 5G New Radio (NR) data transmission on a smartphone in December 2018.

The technical advantages of millimeter wave were undeniable. The 28 GHz and 39 GHz frequencies could carry massive amounts of data at speeds exceeding 4 Gbps in ideal conditions. Latency dropped to single-digit milliseconds. But the physics were brutal: millimeter wave signals could only travel a few thousand feet and couldn't penetrate buildings. Rain, leaves, even human bodies could block the signal.

While competitors AT&T and T-Mobile focused on lower-frequency 5G that could cover vast areas using existing towers, Verizon doubled down on millimeter wave. Vestberg's vision was that quality would trump coverage—that customers would pay premium prices for blazing-fast speeds in urban cores, stadiums, and airports. By the end of 2019, Verizon had deployed millimeter wave 5G in 31 cities, but coverage was limited to small pockets around downtown areas.

The limitations became embarrassingly public. Tech reviewers posted videos showing 5G signals disappearing when they walked around a corner or entered a building. Competitors mocked Verizon's "5G on a street corner" approach. T-Mobile's CEO John Legere gleefully pointed out that his company's 5G covered millions while Verizon's covered "parts of stadiums. "The turning point came in February 2021 when the FCC announced the results of Auction 107—the C-band auction. Verizon had spent an astounding $45.5 billion, plus an additional $7.4 billion in clearing costs, for a total of $52.9 billion on C-band spectrum. The company secured between 140 and 200 MHz of spectrum in every available market, more than doubling its mid-band holdings. AT&T spent $23.4 billion, T-Mobile $9.3 billion. The auction raised a record $81.2 billion total.

The C-band spectrum (3.7-3.98 GHz) was the goldilocks solution—not as fast as millimeter wave but with far better coverage, not as broad as low-band but with far more capacity. It could deliver multi-gigabit speeds while covering entire neighborhoods from a single tower. This was the spectrum that would finally allow Verizon to compete with T-Mobile's mid-band 2.5 GHz network.

But the price was staggering. Verizon had to borrow $25 billion just to fund the purchase. Wall Street was stunned. Some analysts praised the bold move; others worried about the debt burden. The company also committed an additional $10 billion in capital expenditures over three years specifically for C-band deployment, on top of its regular $17-18 billion annual capex.

The first phase of C-band spectrum became available in January 2022, but the launch was nearly derailed by a dispute with the aviation industry over potential interference with aircraft altimeters. After tense negotiations involving the White House, Verizon and AT&T agreed to delay and modify their C-band deployments near airports. It was another reminder that spectrum, no matter how expensive, was useless without the ability to deploy it.

By the end of 2023, Verizon had deployed C-band to cover over 230 million people. Download speeds in C-band coverage areas averaged 300-400 Mbps, with peaks exceeding 1 Gbps. The company branded this enhanced 5G as "5G Ultra Wideband," finally delivering on the promise of transformative mobile speeds at scale.

The C-band investment fundamentally changed Verizon's competitive position. T-Mobile could no longer claim network superiority as definitively. AT&T was playing catch-up. But the cost had been enormous—not just the $53 billion for spectrum, but billions more in equipment, installation, and marketing. The question now was whether Verizon could monetize this investment before the next technology disruption arrived.

VIII. The Fiber Expansion: Frontier Acquisition (2024)

The irony was not lost on anyone in the room. As Verizon executives gathered in September 2024 to finalize the $20 billion acquisition of Frontier Communications, someone pulled up the press release from 2016. Back then, Verizon had sold its California, Texas, and Florida wireline operations to Frontier for $10.54 billion. Eight years later, they were buying back essentially the same assets—plus more—for nearly double the price. "Sometimes you have to leave home to appreciate what you had," Hans Vestberg reportedly quipped. Verizon announced the $20 billion acquisition of Frontier Communications on September 5, 2024. The strategic acquisition of the largest pure-play fiber internet provider in the U.S. significantly expanded Verizon's fiber footprint across the nation. Under the terms, Verizon would acquire Frontier for $38.50 per share in cash, representing a premium of 43.7% to Frontier's 90-day volume-weighted average share price.

The deal brought together Frontier's 2.2 million fiber subscribers across 25 states with Verizon's approximately 7.4 million Fios connections in 9 states and Washington, D.C. In addition to Frontier's 7.2 million fiber locations, the company committed to its plan to build out an additional 2.8 million fiber locations by the end of 2026. Together, the combined company would operate fiber networks passing more than 25 million premises in 31 states.

The strategic rationale reflected a fundamental shift in telecommunications: convergence was no longer optional. Cable companies like Comcast and Charter were bundling wireless with broadband. T-Mobile was aggressively pushing fixed wireless access as a broadband alternative. AT&T had fiber passing 27 million locations. Verizon, despite its wireless dominance, was subscale in broadband. The Frontier acquisition was about catching up.

But the irony of buying back assets it had sold was inescapable. In 2016, facing pressure to focus on wireless and reduce debt, Verizon sold its California, Texas, and Florida wireline operations to Frontier for $10.54 billion. At the time, these assets were seen as legacy burdens—copper-heavy networks in competitive markets with declining margins. Frontier had promised to upgrade them to fiber but filed for bankruptcy in 2020, emerging in 2021 with new management and a fiber-first strategy.

Under CEO Nick Jeffery, Frontier had invested $4.1 billion over four years upgrading its network, with fiber now generating more than 50% of revenue. The company Verizon was buying back was fundamentally different from what it had sold—transformed from a rural copper operator into a fiber-forward growth story.

The convergence thesis was compelling. Verizon could bundle fiber broadband with wireless, creating sticky customer relationships and reducing churn. The company projected at least $500 million in annual run-rate cost synergies. More importantly, fiber backhaul for 5G small cells would become increasingly critical as network densification continued. Owning the fiber meant controlling costs and deployment timelines.

Wall Street was divided. Some analysts praised the strategic logic; others worried about the price and integration risks. Craig Moffett of MoffettNathanson was particularly scathing: "For Verizon, this would be a bold step in the direction of convergence… which is, in our view, an absolutely atrocious idea." He noted that even with Frontier, Verizon's fiber footprint would cover a small fraction of the U.S.

The deal faced an unusual hurdle in 2025 when FCC Chair Brendan Carr, appointed by President Trump, opened a probe into Verizon's diversity, equity, and inclusion programs. The FCC ultimately approved the deal in May 2025 after Verizon agreed to end its DEI programs—a controversial condition that highlighted the increasingly politicized nature of telecom regulation.

The Frontier acquisition represented a full-circle moment for Verizon. After years of trying to transform into a media company, experimenting with content, and betting everything on wireless, the company was returning to its roots: building and operating networks. The difference was that these networks—fiber and 5G—were converged, intelligent, and capable of supporting applications that didn't exist when Verizon sold those assets in 2016. Sometimes, the best strategy is to go back to what you know best.

IX. The Current Network & Business Model

Kyle Malady, Verizon's Chief Technology Officer, stands in the company's network operations center in Bedminster, New Jersey, watching thousands of data points stream across massive displays. It's 2024, and the network he oversees is almost unrecognizable from even five years ago. "We're managing 295 MHz of spectrum across low-, mid-, and high-band frequencies," he explains. "We're processing 10 times the data we handled in 2019, but with lower latency and higher reliability. This isn't just evolution—it's a complete transformation."

Verizon's spectrum portfolio represents decades of acquisitions, auctions, and strategic bets. The company holds an average of 161 MHz in low- and mid-band spectrum nationwide, anchored by the massive C-band holdings. In millimeter wave, Verizon owns 1,741 MHz—more than all other carriers combined. This three-layer spectrum strategy—low-band for coverage, mid-band for capacity, high-band for speed—enables the company to optimize network performance based on location and use case.

The business model has evolved into three distinct but interconnected segments. Consumer wireless remains the largest, generating over $90 billion annually from 143 million connections. But growth increasingly comes from premium unlimited plans that now represent over 75% of the customer base. These plans bundle not just data but entertainment subscriptions, cloud storage, and device protection—driving average revenue per user (ARPU) above $50 monthly for postpaid customers.

Verizon Business, the enterprise segment, has transformed from selling circuits to selling solutions. The division generates $30 billion annually, but the mix has shifted dramatically. Traditional wireline services continue their secular decline, but they're being replaced by higher-margin offerings: private 5G networks, mobile edge computing, and managed security services. The company has deployed private 5G networks for manufacturers, ports, and warehouses, enabling use cases like autonomous vehicles and real-time quality control.

The third growth vector is Fixed Wireless Access (FWA), Verizon's answer to cable broadband. Using excess 5G network capacity, the service delivers home internet without physical cables. By 2024, Verizon had 3.5 million FWA subscribers, adding nearly 400,000 quarterly. With speeds exceeding 300 Mbps and pricing at $50 monthly, FWA targets cable's monopoly in suburban and rural markets. The Frontier acquisition will complement FWA with fiber, giving Verizon multiple tools to attack the $130 billion broadband market.

The Internet of Things (IoT) represents a smaller but strategic bet on the future. Verizon connects 35 million IoT devices—from connected cars to smart meters to industrial sensors. The 2016 acquisitions of Fleetmatics ($2.4 billion) and Sensity have positioned Verizon as a leader in fleet management and smart city solutions. These businesses generate relatively modest revenue today but create sticky enterprise relationships and showcase 5G capabilities.

Network virtualization has fundamentally changed how Verizon operates its infrastructure. Over 75% of the core network now runs on cloud-native software, enabling rapid service deployment and dynamic resource allocation. Open RAN initiatives promise to further reduce costs by enabling equipment from multiple vendors to interoperate. The company has committed to covering 20% of its network with Open RAN by 2025.

Mobile Edge Compute (MEC) represents Verizon's bet on distributed computing. By placing servers at cell sites, Verizon can offer single-digit millisecond latency for applications like augmented reality, autonomous vehicles, and real-time analytics. The company has deployed MEC in 19 cities, partnering with Amazon Web Services and Microsoft Azure to bring cloud computing to the network edge.

But challenges abound. Competition from T-Mobile remains fierce, with the "Un-carrier" continuing to take market share with aggressive pricing and marketing. AT&T's fiber footprint dwarfs Verizon's even after the Frontier acquisition. Cable companies are entering wireless through MVNOs, threatening Verizon's convergence strategy. And new technologies—from low-earth orbit satellites to Wi-Fi 6E—could disrupt traditional network models.

The investment burden is staggering. Between spectrum purchases, network deployment, and acquisitions, Verizon has committed over $200 billion to its network over the past decade. Annual capital expenditures run $17-18 billion, and the Frontier acquisition adds another $20 billion to the tab. The company carries $150 billion in debt, though it generates enough cash flow to comfortably service this debt while maintaining its dividend, which has been paid continuously since 1984.

The current strategy under CEO Hans Vestberg is clear: be the premium network provider in a converged world. No more media adventures, no more transformational pivots. Just relentless focus on network quality, coverage, and capabilities. It's a strategy that plays to Verizon's historical strengths but requires perfect execution in an increasingly competitive market. The network is more capable than ever, but so are the competitors. The next chapter of Verizon's story will be written in gigabits, latency measurements, and customer satisfaction scores—the fundamental metrics that have always defined success in telecommunications.

X. Playbook: Business & Strategic Lessons

There's a conference room at Verizon headquarters where executives keep a simple chart: every major strategic decision the company has made since 2000, color-coded by outcome. Green for successful (Vodafone buyout, C-band acquisition), red for failures (go90, media acquisitions), yellow for mixed results (millimeter wave 5G, FWA). The chart serves as a reminder that even the best companies make mistakes—but the great ones learn from them.

Network quality as competitive moat remains Verizon's most enduring lesson. From the "Can You Hear Me Now?" era through 5G leadership, network superiority has commanded price premiums and reduced churn. Verizon's postpaid phone churn consistently runs below 0.9%, industry-leading performance that translates to billions in value. Every 0.1% improvement in churn is worth approximately $500 million in annual revenue. This obsession with quality permeates the culture—engineers matter more than marketers, network metrics trump financial metrics in daily operations, and capital allocation always prioritizes coverage and capacity.

The value and cost of spectrum assets represents telecommunications' ultimate paradox. Spectrum is invaluable—you literally cannot operate without it—yet its value is entirely dependent on execution. Verizon's $53 billion C-band investment looks brilliant today, delivering transformative network improvements. But the same company spent billions on millimeter wave spectrum that covers less than 1% of the population. The lesson: spectrum without a deployment strategy is just expensive air. Successful spectrum strategy requires balancing coverage (low-band), capacity (mid-band), and capability (high-band), with clear use cases for each layer.

When to pivot vs. double down emerges as perhaps the most crucial strategic lesson. Verizon's media adventure from 2015-2018 cost shareholders $10 billion in destroyed value and immeasurable opportunity cost. While Verizon was playing with AOL and Yahoo, T-Mobile merged with Sprint, AT&T bought Time Warner, and new competitors emerged. The failure wasn't in trying something new—it was in pursuing a strategy that didn't leverage core capabilities. Contrast this with the decision to double down on network investment through C-band: expensive, risky, but directly aligned with Verizon's DNA.

M&A integration capabilities separate successful acquirers from serial destroyers of value. Verizon's track record is mixed but instructive. The successful integrations (NYNEX, GTE, Alltel) shared common characteristics: operational synergies, cultural alignment, and clear integration plans. The failures (AOL, Yahoo) lacked all three. The Vodafone buyout worked because it was essentially buying out a financial partner, requiring no operational integration. The Frontier acquisition tests whether Verizon has learned these lessons—early signs suggest yes, with clear synergy targets and complementary footprints.

Managing regulatory relationships in telecommunications isn't optional—it's existential. Verizon has generally excelled here, maintaining relationships across administrations and party lines. The company's approach is pragmatic rather than ideological: comply with regulations, engage constructively with regulators, and pick battles carefully. The recent DEI controversy with the FCC highlights how regulatory dynamics can shift suddenly, requiring flexibility and pragmatism over principle.

The convergence thesis—combining wireless and wireline, mobile and fixed—has evolved from nice-to-have to necessity. Cable companies offering mobile service, T-Mobile pushing fixed wireless, AT&T bundling fiber with wireless—convergence is the new battleground. Verizon was late to recognize this, selling wireline assets just as convergence was becoming critical. The Frontier acquisition represents an expensive acknowledgment of this strategic error.

Capital allocation discipline in capital-intensive industries determines long-term success. Verizon generates $35-40 billion in annual operating cash flow but must invest $17-18 billion in capital expenditures just to maintain competitiveness. This leaves limited flexibility for acquisitions, debt reduction, or shareholder returns. The company has generally maintained discipline, avoiding bidding wars (like T-Mobile/Sprint) and walking away from bad deals. But the media adventure shows what happens when discipline lapses.

The meta-lesson from Verizon's playbook is that strategic clarity matters more than strategic brilliance. Verizon's best decisions—buying out Vodafone, acquiring C-band spectrum, expanding fiber—weren't particularly creative or innovative. They were obvious moves executed well. The worst decisions—media acquisitions, go90, excessive millimeter wave focus—were attempts to be clever that ignored fundamental capabilities.

For investors and operators, Verizon's journey offers a framework for evaluating telecommunications strategies: Does it leverage network assets? Can it be integrated operationally? Will it generate returns above the cost of capital? Does it strengthen competitive position? If the answer to any is no, it's probably a mistake. In an industry where capital is scarce and competition is fierce, there's no room for strategic tourism. Stick to what you know, execute relentlessly, and let the network do the talking.

XI. Analysis & Bear vs. Bull Case

The investment community remains deeply divided on Verizon. At a recent telecommunications conference, one analyst called it "the best-positioned network operator for the next decade," while another, sitting two seats away, labeled it "a value trap in secular decline." Both had compelling data to support their views. The truth, as often happens, lies somewhere in between.

Bull Case:

The optimists point to Verizon's unmatched spectrum portfolio as the foundation for long-term dominance. With 161 MHz of mid-band spectrum and 1,741 MHz of millimeter wave, Verizon has more network capacity than any competitor. The C-band deployment has already transformed network performance, with median 5G download speeds increasing from 60 Mbps to over 300 Mbps in covered areas. This isn't just about speed—it's about capability. Verizon can handle more users, more devices, and more data-intensive applications than any competitor.

The Frontier acquisition creates a fiber-mobile convergence leader with unique competitive advantages. The combined company will pass 25 million premises with fiber, creating bundling opportunities that reduce churn and increase ARPU. Internal data shows that customers with both wireless and home internet services have 50% lower churn rates. With cable companies struggling to compete in wireless and T-Mobile's fixed wireless facing capacity constraints, Verizon's converged offering could capture significant share in the $130 billion broadband market.

5G monetization remains in early innings, with the most lucrative use cases still emerging. Private 5G networks for enterprises are growing 40% annually. Mobile Edge Compute enables new applications in AR/VR, autonomous systems, and real-time analytics. Fixed Wireless Access has already captured 3.5 million subscribers with minimal marketing. As 5G coverage expands and devices proliferate, new revenue streams will emerge. Historical precedent suggests we're only 20% through the 5G monetization curve.

Strong cash flow generation and dividend sustainability provide downside protection. Verizon generates $35-40 billion in operating cash flow annually, covering capital expenditures and leaving $18-20 billion for debt service and shareholder returns. The dividend, yielding approximately 6.5%, has been paid continuously for 40 years. With investment-grade credit ratings and well-laddered debt maturities, financial stress is unlikely absent a severe recession.

Bear Case:

The skeptics counter with Verizon's massive debt load—over $150 billion including the Frontier acquisition. While manageable today, rising interest rates increase refinancing risk. More concerning is the ongoing capital intensity: $17-18 billion annual capex plus spectrum purchases plus acquisitions. The company is trapped on a treadmill, needing constant investment just to maintain competitive position. Free cash flow after dividends barely covers debt reduction, leaving no room for error.

T-Mobile's momentum and pricing pressure show no signs of abating. T-Mobile has gained postpaid phone subscribers for 40 consecutive quarters while Verizon has struggled to grow. T-Mobile's network quality has reached parity in most markets while maintaining a 15-20% price discount. With $80 billion less debt and lower capital intensity due to Sprint synergies, T-Mobile can sustain this pressure indefinitely. Verizon's premium pricing strategy looks increasingly vulnerable.

Cord-cutting and wireless saturation limit growth potential. The U.S. wireless market is 110% penetrated—growth now comes only from market share shifts or ARPU expansion. Both face headwinds. Younger consumers show little brand loyalty, switching carriers for $10 monthly savings. Unlimited plans have commoditized the service, making differentiation difficult. Meanwhile, traditional business services face secular decline as enterprises shift to cloud-based solutions.

Technology disruption from satellite providers poses an existential threat. Starlink has demonstrated that low-earth orbit satellites can deliver broadband comparable to terrestrial networks. Amazon's Project Kuiper and other competitors are coming. If satellite internet reaches performance parity with 5G at lower cost, Verizon's network advantage evaporates. The company would face the innovator's dilemma: cannibalize its own network or watch others do it.

Valuation analysis suggests limited upside. Verizon trades at 8x forward earnings and 5x EBITDA—discounts to historical averages but perhaps justified given growth challenges. The dividend yield of 6.5% implies market skepticism about growth prospects. Sum-of-the-parts analysis values the wireless business at $200 billion, wireline at $20 billion, and other assets at $10 billion. Against $150 billion in net debt, equity value of $80-90 billion implies 15-20% upside to current market capitalization—hardly compelling given execution risks.

Competitive positioning remains strong but not unassailable. Verizon leads in network quality and enterprise relationships but lags in consumer perception and pricing. The brand commands respect but not enthusiasm. Customer satisfaction scores trail T-Mobile. The company wins on reliability but loses on value. This positioning works in enterprise markets but struggles with price-conscious consumers.

The bear-bull debate ultimately centers on whether Verizon can monetize its network investments before technology or competition erodes its advantages. Bulls see a company with unmatched assets trading at distressed valuations. Bears see a former monopolist struggling to grow in a commoditizing industry. Both are partially right. Verizon remains a formidable competitor with significant advantages, but the easy growth of the wireless boom is over. Future returns will depend on execution, capital allocation, and whether management can find new growth vectors beyond traditional connectivity.

XII. Epilogue & "What Would We Do?"

If we were running Verizon tomorrow, the strategic priorities would be clear but the execution would be anything but simple. The company stands at an inflection point where traditional competitive advantages are eroding while new opportunities are emerging. The path forward requires both defending the core business and building new growth platforms—a delicate balance that has eluded many former monopolists.

The AI and edge computing opportunity represents Verizon's most compelling growth vector. The company should position itself as the "computing utility" for the AI age. This means aggressive deployment of edge computing infrastructure, partnering deeply with hyperscalers rather than competing with them. Verizon should offer "Network-as-a-Service" for AI workloads, providing not just connectivity but compute, storage, and inference at the edge. The goal: become indispensable infrastructure for real-time AI applications in autonomous vehicles, smart cities, and industrial IoT. This leverages Verizon's core strength—ubiquitous, reliable infrastructure—while avoiding content and application layers where the company has repeatedly failed.

Private 5G networks for enterprise should be scaled aggressively. Verizon should create a dedicated division with P&L responsibility, specialized sales force, and separate branding. Target the Fortune 500 with turnkey private network solutions that include devices, applications, and managed services. Price aggressively to gain share, accepting lower margins initially to establish market leadership. The enterprise market values reliability over cost—Verizon's sweet spot. Within five years, private networks should generate $5 billion in annual revenue.

International expansion possibilities should be explored cautiously through partnerships rather than acquisitions. Verizon should license its network expertise and operational capabilities to carriers in developed markets facing similar challenges. Create a "Verizon Inside" model where the company provides network design, optimization, and management services without capital investment. Target markets where American technology leadership provides advantage: Japan, Australia, Western Europe. Avoid emerging markets where low-cost operators dominate.

Fixed wireless vs. fiber strategy requires nuanced market segmentation. In dense urban areas where Verizon has fiber, push fiber aggressively—it's superior technology with better economics at scale. In suburban and rural markets, FWA makes more sense, leveraging excess 5G capacity with minimal incremental investment. The key is avoiding channel conflict: position FWA as the premium wireless solution and fiber as the ultimate connectivity experience. Bundle aggressively but price rationally. The goal isn't to win the broadband war but to capture the most valuable customers.

Most importantly, we would radically simplify the business. Verizon has accumulated complexity through decades of acquisitions and strategic pivots. Eliminate marginal businesses, consolidate overlapping operations, and focus relentlessly on three core products: wireless connectivity, broadband internet, and enterprise solutions. Everything else is a distraction. This means divesting non-core assets, sunsetting legacy products, and saying no to seductive but strategically incoherent opportunities.

We would also reset the cultural narrative internally. Verizon employees are engineers and operators who built America's best network. That's the identity to embrace, not trying to be a tech company or media company. Celebrate network uptime, coverage expansions, and customer satisfaction scores. Make heroes of field technicians and network engineers, not dealmakers or strategists. Culture eats strategy, and Verizon's culture is about operational excellence.

On capital allocation, we would implement strict return hurdles. No acquisition or major investment without clear path to 15% IRR. This would likely mean fewer deals but better outcomes. The dividend is sacred—it attracts a specific investor base and cutting it would destroy credibility. But share buybacks should be opportunistic, only when trading below intrinsic value. Debt reduction takes priority until leverage drops below 2.5x EBITDA.

The hardest decision would be whether to attempt a transformational merger. The industrial logic for consolidation is compelling—three national carriers is probably one too many. A combination with Dish or a cable company could create transformational synergies. But regulatory approval would be uncertain, integration risk enormous, and distraction costly. Unless a clear opportunity emerges, organic growth and operational excellence are the better path.

Final thoughts on Verizon's place in telecom history: Verizon represents both the best and worst of American corporate evolution. It successfully navigated the transition from monopoly to competition, from wireline to wireless, from voice to data. It built the nation's best network and created enormous shareholder value. But it also wasted billions on failed diversification, moved too slowly to recognize industry shifts, and sometimes confused engineering excellence with strategic wisdom.

The next decade will determine whether Verizon joins the ranks of former giants that couldn't adapt—think IBM in PCs, GE in conglomerates—or whether it successfully transforms into the essential infrastructure provider for the digital age. The assets are there, the market opportunity is massive, but execution will determine everything. In telecommunications, as in life, the best network doesn't always win—but it usually doesn't lose either. Verizon's challenge is making sure that axiom remains true in an age of technological disruption and fierce competition.

The story of Verizon is far from over. What started as a regional telephone company has evolved into a national technology infrastructure provider. The next chapters will be written in 6G standards, quantum networks, and technologies we can't yet imagine. But the fundamental mission remains unchanged: connecting people, businesses, and things reliably, securely, and at the speed of life. Everything else is just tactics.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube