Viasat: The Audacious Bet on Satellite Broadband

I. Introduction and Episode Roadmap

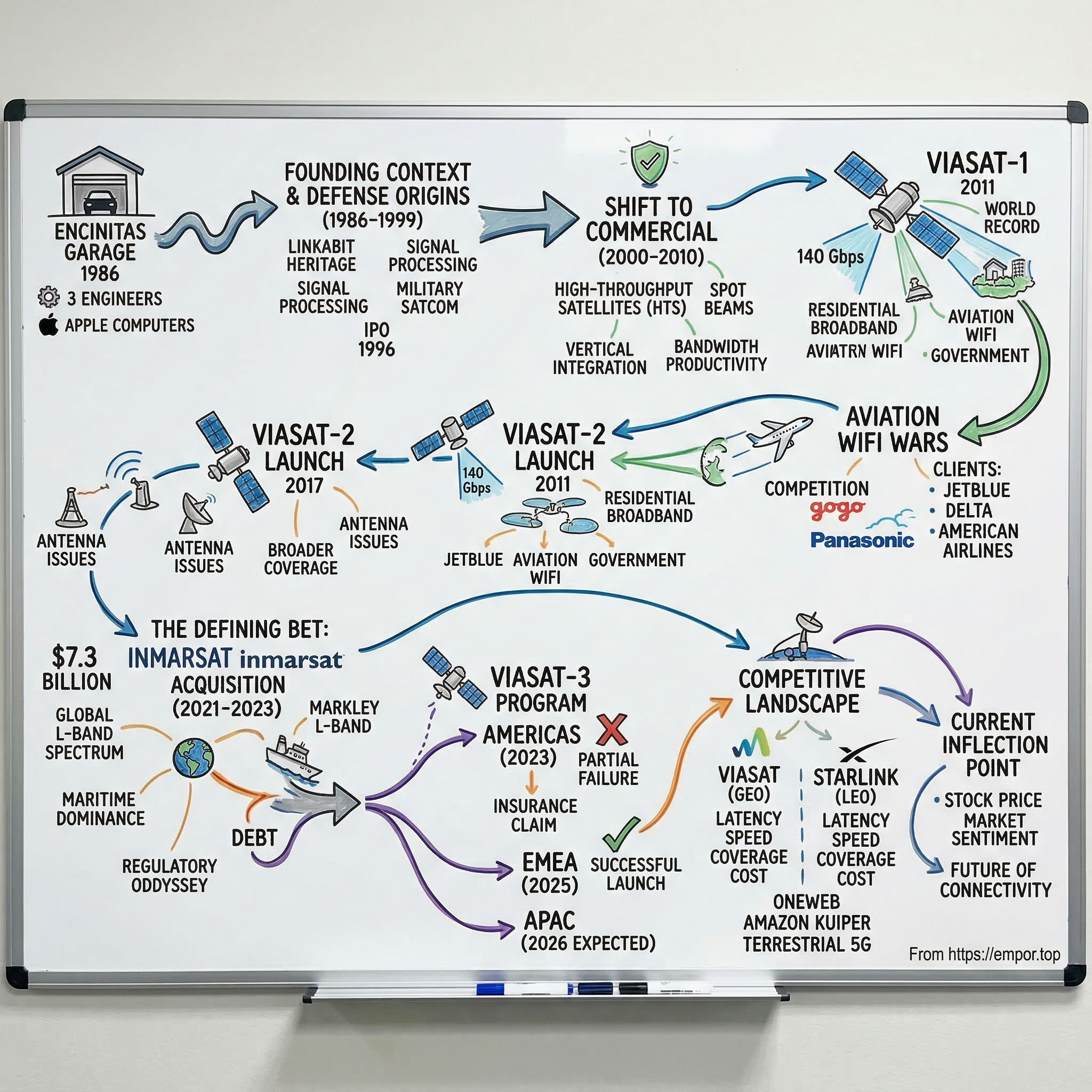

Picture a modest garage in Encinitas, California, 1986. Three engineers huddle over a handful of Apple computers, sketching satellite waveforms on notepads, burning through twenty-five thousand dollars of their own savings. They have no satellite, no commercial product, and no guarantee the Pentagon will return their calls. Four decades later, the company they built from that garage operates a global fleet of the most powerful communications satellites ever launched, connects passengers on thousands of commercial flights mid-ocean, provides encrypted data links to the U.S. military, and just closed one of the largest acquisitions in satellite industry history. The company is Viasat, and its story is one of the most audacious multi-decade bets in telecommunications.

How did a defense contractor satellite company become one of the most ambitious players in global broadband? That is the question at the center of this episode. Viasat today generates over four and a half billion dollars in annual revenue. It is the dominant provider of in-flight WiFi on commercial airlines, a critical supplier of cybersecurity and tactical communications to the Department of Defense, and a satellite internet provider locked in an existential contest with Elon Musk's Starlink. The company acquired Inmarsat, the legendary British maritime satellite operator, for seven point three billion dollars. It launched what was supposed to be the highest-capacity satellite ever built, only to watch that satellite partially fail in orbit. Its stock cratered to seven dollars and then surged nearly six hundred percent in less than a year.

The drama here is real. Viasat represents a forty-year journey from Cold War defense contracts to betting the entire company, repeatedly, on the thesis that bandwidth delivered from space would become as essential as electricity. Its founder, Mark Dankberg, has staked his career on a single conviction: that geostationary satellites, orbiting twenty-two thousand miles above the equator, can deliver more useful bandwidth per dollar than any other technology. The market has whipsawed between believing him and writing his obituary, sometimes within the same fiscal year.

The story touches nearly every theme that matters in modern business: capital intensity as both moat and millstone, the tension between visionary ambition and brutal unit economics, the challenge of competing against a billionaire with his own rocket company, and the question of whether being early is the same as being right.

What makes Viasat's story particularly fascinating for investors is the current inflection point. The stock bottomed at seven dollars and thirty-six cents in April 2025, a price that valued the entire company, including its satellite fleet, global spectrum licenses, aviation business serving thousands of commercial aircraft, and a defense technology portfolio generating hundreds of millions in revenue, at less than a billion dollars. By March 2026, the stock trades around forty-six dollars, a roughly six-fold increase. Was the bottom irrational pessimism, or is the current price irrational optimism? Understanding the answer requires understanding the full history of how this company got here.

The space internet wars are here, and Viasat is fighting on every front.

II. Founding Context and the Defense Contractor Origins (1986-1999)

To understand Viasat, you first have to understand Linkabit, and to understand Linkabit, you have to understand the remarkable concentration of communications talent that emerged in San Diego in the 1970s and 1980s. Linkabit was founded in 1968 by Irwin Jacobs, Andrew Viterbi, and Leonard Kleinrock, three academics whose theoretical work on digital communications would reshape the entire telecommunications industry. The company focused on building satellite communication equipment for the U.S. military, and it became a hothouse of engineering talent that would eventually spawn more than one hundred San Diego technology companies, the most famous being Qualcomm.

Mark Dankberg arrived at Linkabit in 1979, after a stint as a communications engineer at Rockwell International. He held bachelor's and master's degrees in electrical engineering from Rice University, where he had developed a deep understanding of signal processing and information theory, the mathematical foundations that determine how much data you can squeeze through any given communications channel. At Linkabit, he was drawn to the intersection of these disciplines and satellite technology.

Dankberg rose to assistant vice president at M/A-COM Linkabit (M/A-COM had acquired Linkabit in 1980), working on military satellite communications systems and absorbing the engineering culture that Jacobs and Viterbi had built. The Linkabit culture was distinctive: technically rigorous, obsessively focused on performance metrics, and deeply skeptical of conventional wisdom about what was technically possible. Dankberg later called Jacobs "a fabulous role model" as an entrepreneur, and the influence shows. Like Jacobs, Dankberg would build a company that combined deep technical expertise with commercial ambition, and like Jacobs, he would bet on a technology thesis that the establishment considered implausible.

In July 1985, Jacobs, Viterbi, and seven other Linkabit veterans left to found Qualcomm, which would become one of the most valuable technology companies in history through its invention of CDMA cellular technology. Dankberg did not join them. He had a different vision, one rooted not in cellular telephony but in satellite bandwidth. In May 1986, Dankberg cofounded Viasat with two fellow Linkabit alumni, Mark Miller and Steve Hart. They started in Dankberg's garage with those Apple computers and twenty-five thousand dollars of personal capital.

The timing mattered. Ronald Reagan's defense buildup was still in full swing, and the Pentagon was hungry for better tactical satellite communication terminals. The big defense primes, Raytheon, Lockheed, and Hughes, dominated satellite communications procurement, but they were slow-moving bureaucracies optimized for billion-dollar programs, not the nimble, rapid-innovation approach that a small startup could offer.

Within its first year, Viasat secured two U.S. government defense contracts, which validated the company's technical approach and helped the founders raise three hundred thousand dollars in venture capital from Southern California Ventures. The business model was straightforward: build specialized digital satellite communication equipment for the military, focusing on areas where the incumbent contractors were underperforming. Dankberg later said the key insight was that satellite communication systems were fundamentally information technology products that happened to use satellites, not aerospace products that happened to carry data. This distinction mattered because it meant the design optimization should prioritize data throughput and spectral efficiency rather than the traditional aerospace metrics of mass, power, and orbital mechanics.

Throughout the late 1980s and 1990s, Viasat built a reputation for engineering innovation in defense SATCOM. The company designed tactical data links, satellite modems, and network management systems for various military programs. This was not glamorous work, but it was technically demanding and it generated steady, reliable revenue from government contracts. More importantly, it gave Dankberg and his team deep expertise in the physics and engineering of satellite communications, knowledge that would prove invaluable when they eventually turned their attention to the commercial market. There is a pattern in the Linkabit diaspora worth noting: Qualcomm took the cellular path and became a behemoth; Viasat took the satellite path and remained, for decades, a specialist. Both founders were shaped by the same engineering culture, but they read the market differently. Jacobs saw that mobile phones would transform how people communicate on the ground. Dankberg saw that satellites would transform how people communicate everywhere the ground cannot reach.

The post-Cold War defense drawdown of the early 1990s tested Viasat's resilience. Government budgets tightened, contracts became more competitive, and many small defense contractors were acquired or went under. Viasat survived by being lean and technically excellent, winning work on programs where its engineering capabilities gave it an edge over larger but less nimble competitors. This period hardened the company's culture of doing more with less, a trait that would serve it well during the capital-intensive commercial ventures ahead.

Viasat went public on the NASDAQ on December 3, 1996, a decade after its founding. The IPO was modest by the standards of the dot-com era, but it gave the company the public currency and capital market access it would need for the massive bets ahead. At this point, Viasat was still fundamentally a defense contractor. Revenue came almost entirely from government systems. The commercial satellite market was still dominated by traditional operators selling transponder capacity at premium prices. Dankberg, however, was already thinking about something different. He saw that bandwidth demand was growing exponentially, that terrestrial infrastructure would never reach large parts of the world, and that satellites could be engineered to deliver far more capacity than anyone in the industry believed possible. The question was whether he could build a company capable of making that leap.

III. The Shift to Commercial: Laying the Groundwork (2000-2010)

The first decade of the new millennium was when Dankberg's vision began to crystallize into strategy. The dot-com bust had demonstrated that bandwidth demand was real even if many of the companies trying to serve it were not. The digital divide between urban and rural America was widening. Cable and DSL providers had no economic incentive to extend their networks to sparsely populated areas. And the existing satellite internet providers, notably HughesNet, offered speeds that were painfully slow, with tiny data caps and prices that seemed designed to discourage use.

Dankberg saw an opening. The traditional approach to satellite broadband used wide-beam satellites that spread their signal across entire continents. This was like trying to water a garden with a fire hose pointed at the sky: most of the capacity missed the plants. What if you could focus the signal into narrow beams aimed at specific population centers, reusing the same frequencies across different geographic areas the way a cellular network reuses spectrum across different cell towers? The concept was called high-throughput satellite technology, or HTS, and it promised to deliver orders of magnitude more capacity from a single satellite than anything previously launched.

Think of it this way. A traditional satellite might cover all of North America with a single beam, delivering perhaps ten to twenty gigabits per second of total throughput. That sounds like a lot, until you divide it among hundreds of thousands of users across millions of square miles. The result is that each user gets a trickle, maybe a few megabits if they are lucky, often much less during peak usage.

An HTS satellite, by contrast, could use dozens or even hundreds of narrow "spot beams," each illuminating a relatively small area on the ground, perhaps a few hundred kilometers across. Because the beams do not overlap, the same frequencies can be reused across multiple beams, multiplying the total capacity dramatically. If you have seventy beams, each using the same block of frequencies, you effectively get seventy times the capacity of a single-beam satellite using the same amount of spectrum.

It is the same principle that allows your mobile phone to get a strong signal even though millions of other phones use the same frequencies. Your cell tower only serves a small area, and a tower ten miles away can reuse those exact same frequencies without interference. Dankberg was essentially proposing to bring the cellular revolution to space, replacing the satellite equivalent of a single enormous broadcast tower with a grid of focused beams that could reuse spectrum aggressively.

Dankberg did not just want to buy this kind of satellite from a manufacturer and lease capacity like a traditional operator. He wanted Viasat to design the satellite payload itself, build the ground network infrastructure, manufacture the user terminals, and sell directly to consumers. This vertical integration philosophy was unusual in the satellite industry, where the standard model involved separate companies for manufacturing, launching, operating, and retailing. But Dankberg believed that controlling the entire stack was the only way to optimize the economics at every layer.

Meanwhile, Viasat was quietly building commercial capabilities in other domains. The company entered the aviation communications market, recognizing that airline passengers represented a captive audience willing to pay for connectivity during long flights. It also continued to grow its defense business, which provided the cash flows needed to fund commercial research and development. The financial discipline during this period was remarkable: Viasat was essentially using defense contract profits to subsidize one of the most expensive gambles in telecommunications, the decision to build its own high-capacity satellite from scratch.

Dankberg articulated his thesis in characteristically engineering terms. He focused obsessively on what he called "bandwidth productivity," defined as the ratio of useful bandwidth delivered to total lifetime capital cost. Most satellite operators thought about their business in terms of transponder leases, orbital slots, and spectrum rights. Dankberg thought about it in terms of bits per dollar. If he could deliver ten times more bits for twice the capital, he would win. This was not just a business strategy; it was an engineering philosophy that permeated every design decision at Viasat, from the satellite payload architecture to the consumer terminal antenna design to the network management software.

The broader context of this period was the explosive growth of internet traffic and the growing political urgency around the digital divide. The FCC was increasingly focused on extending broadband to underserved communities, and government subsidy programs were being designed to close the gap. Satellite providers that could demonstrate competitive speeds and reasonable pricing would be positioned to capture these subsidies and the market they opened.

The ViaSat-1 decision represented a company-defining bet. Building and launching a geostationary satellite costs hundreds of millions of dollars, takes years from design to orbit, and carries the risk of catastrophic loss if something goes wrong during launch or deployment. For a company of Viasat's size at the time, this was not a side project. It was an all-in wager that Dankberg's "bandwidth productivity" thesis was correct: that maximizing useful bandwidth per total lifetime capital cost would create economics so compelling that they would overwhelm every competitor stuck with the old model. The analogy Dankberg often used was oil drilling: you could either drill many shallow wells or invest heavily in a single deep well that produces far more per dollar invested. He was betting on the deep well.

IV. ViaSat-1 Launch: The Breakthrough Moment (2011-2012)

On October 19, 2011, a Proton rocket lifted off from the Baikonur Cosmodrome in Kazakhstan carrying a satellite that would change the economics of space-based broadband. ViaSat-1 reached its geostationary orbital slot at 115.1 degrees West, unfurled its solar panels and antennas, and began transmitting. It entered the Guinness Book of World Records as the highest-capacity communications satellite ever launched. Its total throughput of one hundred and forty gigabits per second was more than all other communications satellites covering North America combined.

That fact is worth pausing on. A single satellite, designed by a company that most people had never heard of, delivered more bandwidth than the entire fleet of satellites that Intelsat, SES, Telesat, and every other operator had pointed at North America. The traditional satellite industry had spent decades launching expensive spacecraft that each added a few gigabits of capacity. Viasat had just launched one that delivered more than all of them put together.

The technology behind this achievement was the spot beam architecture that Dankberg had been developing for years: seventy-two Ka-band spot beams, sixty-three covering the United States including Alaska and Hawaii, and nine covering Canada. Each beam focused its energy on a relatively small area, allowing aggressive frequency reuse across the footprint. The Ka-band frequency range, roughly twenty-six to forty gigahertz, offered more available bandwidth than the older Ku-band or C-band frequencies that traditional satellites used, but it came with a trade-off: Ka-band signals are more susceptible to absorption by water vapor and rain, a phenomenon known as "rain fade." Heavy thunderstorms could temporarily degrade service, a limitation that competitors were quick to highlight.

The business model crystallized around three markets. The first was residential broadband, launched under the brand name Exede (later simply rebranded as Viasat). This targeted the roughly twenty million American households that lacked access to adequate terrestrial broadband, offering download speeds of twelve megabits per second and later higher tiers, far exceeding what HughesNet or other satellite providers could deliver. The second was aviation, where Viasat's high-capacity satellite could deliver genuine broadband to aircraft in flight. The third was government, where the military's appetite for bandwidth in remote and contested environments was essentially insatiable.

The early aviation wins were particularly significant. JetBlue, the New York-based carrier known for its customer-friendly approach, had announced its partnership with Viasat in 2010 and became the first airline to equip its entire fleet with Ka-band satellite WiFi. The proposition was audacious: free WiFi for every passenger on every flight, including streaming video. At the time, the dominant in-flight connectivity provider was Gogo, whose air-to-ground system offered speeds comparable to dial-up internet and charged passengers handsomely for the privilege. Viasat's JetBlue deployment was a proof of concept that satellite broadband could actually deliver the Netflix-in-the-sky experience that passengers wanted.

The government market, while less visible to the public, was equally important to the business case. Military operations in Afghanistan and Iraq had demonstrated an insatiable demand for bandwidth in theaters where no terrestrial infrastructure existed. Special operations forces, intelligence agencies, and command centers all needed high-speed data links, and traditional military satellites were chronically overloaded. ViaSat-1's commercial capacity could be leveraged for government customers, creating a dual-use model that improved utilization and economics on both sides.

The residential launch, however, revealed the challenges inherent in satellite broadband. Customer acquisition costs were high because every subscriber needed a professionally installed dish antenna, typically costing Viasat several hundred dollars per customer before they generated a single dollar of revenue. Weather could temporarily degrade Ka-band signals during heavy rain, leading to service interruptions that frustrated customers accustomed to always-on terrestrial broadband. And there was the fundamental physics problem that no geostationary satellite can escape: latency.

To understand why latency matters so much, consider what happens when you click a link on a webpage. Your request has to travel up twenty-two thousand miles to the satellite, back down twenty-two thousand miles to a ground station, then across the terrestrial internet to the server, and the response has to make the entire journey in reverse. That round trip adds approximately six hundred milliseconds of delay before anything even begins to load. For browsing or streaming video, where the content is buffered, this is barely noticeable. But for video calls, where every word needs to travel that path in real time, the delay creates an awkward, halting conversation. For online gaming, where milliseconds matter, it is essentially unusable. For financial trading, it is disqualifying.

Dankberg argued that latency was tolerable for most consumer use cases and that raw bandwidth, the total amount of data you could move per second, mattered more than the time it took for each individual packet to arrive. He pointed out, correctly, that the vast majority of internet usage was streaming video, web browsing, and email, all applications where latency is largely imperceptible. The market would eventually test that thesis with brutal efficiency.

V. The Aviation WiFi Wars and Market Positioning (2012-2017)

The in-flight connectivity market of the mid-2010s was a genuine battleground, with multiple companies deploying fundamentally different technologies and competing for contracts worth hundreds of millions of dollars. Understanding the technology landscape is essential to understanding Viasat's competitive position.

Gogo, the incumbent, had built its business on air-to-ground technology. It deployed a network of more than two hundred ground towers across the continental United States, each projecting directional signals upward toward passing aircraft. The system worked reasonably well over land, but it had two fatal limitations: it provided no coverage over oceans, and its bandwidth was severely constrained. Passengers using Gogo's early service experienced speeds that made checking email frustrating and streaming video impossible.

Panasonic Avionics, the Japanese electronics giant's aerospace subsidiary, took a different approach, using Ku-band satellite connectivity. Ku-band operates at a lower frequency than Viasat's Ka-band, which makes it somewhat less susceptible to rain fade but limits the total bandwidth available. Panasonic partnered with satellite operators like Intelsat to provide global coverage, and it won contracts with several international carriers.

Viasat's Ka-band approach occupied a different point on the performance curve. Ka-band satellites could deliver significantly higher speeds than either air-to-ground or Ku-band systems, with Viasat advertising download speeds of thirty megabits per second and peaks approaching ninety megabits on equipped aircraft. The trade-off was higher capital intensity, since Viasat needed to build and launch its own satellites, and somewhat greater weather sensitivity.

The airline contracts reflected these technology choices, and the bidding process for each one was a high-stakes competition that could shape the in-flight connectivity market for a decade.

JetBlue was Viasat's flagship customer and evangelist, offering free WiFi that passengers consistently rated as a key reason for choosing the airline. The JetBlue partnership was more than a contract; it was a living advertisement. Every passenger who streamed Netflix at thirty-five thousand feet and told their friends about it was marketing for Viasat's technology.

Delta Air Lines became another major win, one of the most important in Viasat's history. Delta, the largest airline in the United States by revenue, eventually equipped over a thousand aircraft with Viasat connectivity, including widebody international aircraft (A330s, A350s, 767s) and narrowbody domestic planes (A220s, 737 MAXs). By August 2025, over eight hundred eighty Delta mainline planes had Viasat connectivity installed, making it the largest single-airline deployment in Viasat's fleet.

American Airlines equipped its narrowbody fleet with Viasat connectivity, and by April 2025, American launched free WiFi for all passengers. These contracts represented billions of dollars in lifetime value and years of installation work, as equipping a single aircraft requires taking it out of service for several days while technicians install the antenna, wiring, and onboard systems.

The competitive dynamics were fascinating. Gogo, despite its first-mover advantage, found itself increasingly disadvantaged by its technology choice. Air-to-ground simply could not deliver the bandwidth that modern passengers demanded. The company eventually pivoted, developing a satellite-based product called 2Ku that used Ku-band capacity, effectively acknowledging that its original approach was a dead end. In business aviation, the market dynamics were different. Here, Gogo and Viasat eventually found a way to collaborate, with Gogo distributing Viasat's Ka-band services for private jets alongside its own products.

The business aviation segment deserves separate mention because its economics are fundamentally different from commercial aviation. A private jet owner or fractional share operator is willing to pay far more per aircraft for connectivity because the decision-maker is often the passenger. Business aviation customers demanded genuine broadband for video conferencing, file transfers, and streaming, and they were willing to pay monthly fees that would be unthinkable for a commercial airline distributing costs across hundreds of passengers per flight. Viasat recognized this early and built a dedicated business aviation offering that became a significant revenue contributor with attractive margins.

The network effect in aviation connectivity was real but subtle. Each new satellite Viasat launched increased its total capacity, which allowed better service quality, which made it easier to win new airline contracts, which generated revenue to fund the next satellite. This virtuous cycle depended on one critical assumption: that Viasat could keep launching satellites faster than competitors could deploy alternative technologies. As long as that held, the company's position in aviation would strengthen with each generation. The question was whether the cycle could keep spinning fast enough to outpace an entirely new class of competitor that was about to enter the arena.

VI. ViaSat-2 and Doubling Down (2017-2019)

On June 1, 2017, ViaSat-2 launched aboard an Arianespace Ariane 5 rocket, carrying a design capacity of over three hundred gigabits per second, more than double its predecessor. The satellite's coverage footprint was deliberately broader than ViaSat-1, extending over the Atlantic Ocean, the Caribbean, Mexico, and Central America in addition to North America. This geographic expansion was critical for aviation, since major airline routes cross the Atlantic and Caribbean regularly, and for opening new residential markets in underserved regions.

However, ViaSat-2 brought its own headaches. During orbital testing, engineers discovered that two of the satellite's four Ka-band reflector antennas had not deployed properly, causing some spot beams to perform differently than ground tests predicted. The effective capacity was reduced to approximately two hundred sixty gigabits per second, roughly eighty-seven percent of the design target.

This is a pattern worth noting because it reveals a core risk in the satellite business that terrestrial network operators never face. When you build a cell tower on the ground, you can send a technician to fix it. When a satellite is orbiting twenty-two thousand miles above the earth, there is no repair option. Whatever you launch is what you have for the next fifteen years. A reflector that does not fully deploy, a solar panel that underperforms, a software bug in the onboard processor, any of these can permanently reduce the capacity and value of an asset that cost hundreds of millions of dollars to build and launch. There is no recall, no patch, no second chance for the hardware.

Viasat insisted the issue would not materially impact planned services, but it foreshadowed the antenna problems that would prove far more devastating on the next generation satellite.

The capital intensity question was becoming impossible to ignore, and it is worth understanding why satellite economics are so different from terrestrial network economics. ViaSat-2 cost approximately six hundred million dollars to build and launch. Including ground infrastructure, the total investment in the ViaSat-1 and ViaSat-2 system ran well over a billion dollars.

A cable company building fiber to homes makes incremental investments: each new neighborhood costs a predictable amount, and you can stop building whenever the economics stop working. A satellite operator makes a massive, irrevocable lump-sum investment years before the satellite generates its first dollar of revenue. You spend six hundred million dollars, wait three to four years for manufacturing and testing, launch the satellite, and then hope that the market conditions you predicted half a decade ago still hold true. If technology shifts, if a competitor emerges, if customer preferences change, you cannot redirect that capital. It is literally floating in space.

These satellites had expected lifespans of roughly fifteen years, meaning Viasat needed to generate enough revenue over that period not only to recoup the investment but also to fund the next generation. The satellite business is fundamentally a capex treadmill: you must keep building more expensive satellites to maintain your competitive position, and each generation is a bet that cannot be unwound once the rocket leaves the pad.

On the residential front, Viasat rolled out unlimited data plans and speed improvements to compete more aggressively with HughesNet and the emerging threat of Starlink. SpaceX had announced its Starlink constellation in 2015, and while it would not begin beta service until 2020, the mere announcement cast a shadow over every geostationary satellite operator. If Elon Musk could put thousands of low-earth orbit satellites into space and offer low-latency broadband at competitive prices, what future did high-latency GEO broadband have?

Dankberg's response to the Starlink threat was characteristically contrarian. He argued that GEO satellites delivered more bandwidth per dollar of capital invested, that the physics of frequency reuse favored large geostationary platforms over massive constellations, and that Starlink's economics would prove far more challenging than Musk suggested. In industry presentations, Dankberg would pull up slides showing that a single ViaSat-3 satellite could deliver more total throughput than hundreds of Starlink satellites combined, at a fraction of the launch and replacement cost. The argument was technically valid in a narrow sense: per-bit capital cost was indeed lower for high-capacity GEO satellites when the capacity was fully utilized.

But the argument missed a crucial point. Customers do not buy bits per dollar of satellite capital cost. They buy an experience: speed, latency, reliability, coverage. And on the metrics that consumers actually cared about, particularly latency and peak speed, LEO was structurally superior. Dankberg was right about the economics being harder than advertised, as Starlink would burn billions before approaching profitability. But he may have underestimated the sheer force of Musk's execution capability and willingness to subsidize growth with SpaceX launch revenue. More fundamentally, he may have underestimated how much latency matters to the modern internet user, accustomed to sub-second response times on every device they own.

The government and defense business continued to provide a stable revenue base during this period. Viasat's cybersecurity products, tactical communications terminals, and secure networking solutions were deeply embedded in military programs, generating predictable revenue with relatively high margins. The company's Link 16 tactical data link equipment, which enables real-time information sharing between military aircraft, ships, and ground forces, became a cornerstone product used by NATO allies worldwide. This was the financial anchor that allowed the company to make its commercial bets without facing immediate liquidity crises.

Revenue growth during this period told the story of a company in transition. By fiscal year 2019, Viasat generated over two billion dollars in revenue, roughly split between its three segments: Government Systems contributed about nine hundred fifty-six million, Satellite Services about six hundred eighty-four million, and Commercial Networks about four hundred twenty-eight million. The defense business remained the foundation, but the commercial segments were growing faster and increasingly defined the company's identity and valuation in the public markets.

VII. The Inmarsat Acquisition: The Defining Bet (2021-2023)

In November 2021, Viasat announced the transaction that would define the company's future for better or worse: the acquisition of Inmarsat for seven point three billion dollars. It was, by a wide margin, the largest deal in Viasat's history and one of the largest in the entire satellite industry.

The scale of the bet was staggering. At the time of the announcement, Viasat's own market capitalization was roughly five billion dollars. It was proposing to buy a company valued at more than itself, funded substantially with debt, at a time when interest rates were beginning their sharpest climb in decades. This was not a bolt-on acquisition. It was a transformative merger that would more than double the company's revenue, triple its debt, and fundamentally reshape its competitive position.

To understand why Dankberg made this bet, you have to understand what Inmarsat was and what it represented.

Inmarsat was founded in 1979 as the International Maritime Satellite Organization, an intergovernmental body created to enable distressed ships at sea to communicate with shore-based rescue services. It was privatized in 1999 and had evolved into a global mobile satellite communications provider, operating a fleet of satellites in both geostationary orbit and highly elliptical orbits. Its crown jewels were threefold. First, it held exclusive L-band spectrum licenses covering the entire globe, a resource that no amount of money could easily replicate because the International Telecommunication Union allocates orbital slots and spectrum rights through a process that takes decades. Second, it dominated maritime satellite communications, providing connectivity and safety services to more than half the world's merchant shipping fleet. Third, it had built a significant aviation connectivity business of its own, serving airlines with its Global Xpress Ka-band service.

The strategic rationale was compelling on paper. By combining Viasat's Ka-band capacity and aviation technology with Inmarsat's L-band spectrum, maritime dominance, and global network, Dankberg believed he could create a connectivity powerhouse with unmatched reach across aviation, maritime, government, and enterprise mobility. The combined company would have the broadest spectrum portfolio in the industry, the most extensive ground infrastructure, and the deepest customer relationships in every high-value mobility market.

To appreciate why spectrum matters so much, think of it like beachfront real estate. There is a finite amount of electromagnetic spectrum suitable for satellite communications, and it was allocated decades ago through international treaties. You cannot create more of it. You cannot buy it on the open market. The only way to acquire it is to buy a company that holds it. Inmarsat's L-band spectrum was particularly valuable because L-band signals penetrate weather, foliage, and building materials better than higher-frequency bands, making them ideal for maritime safety services and mobile communications in challenging environments. Combined with Viasat's Ka-band capacity for high-throughput data, the merged company would have a spectrum portfolio unmatched by any competitor.

The deal was structured with approximately five hundred fifty-one million dollars in cash to Inmarsat shareholders (reduced from an original eight hundred fifty million after Inmarsat paid a special dividend), roughly forty-six million shares of Viasat common stock, and the assumption of approximately three point four billion dollars of Inmarsat net debt. Viasat drew about one point three five billion dollars of committed financing at closing, including a secured term loan and an unsecured bridge loan. The leverage was enormous.

What followed was an eighteen-month regulatory odyssey that tested the patience of everyone involved. The deal required approval from three major jurisdictions, each with its own concerns and timelines.

The UK's Competition and Markets Authority launched a Phase 1 investigation, given Inmarsat's London headquarters and the transaction's implications for British defense and maritime interests. Inmarsat was not just any company in the UK; it was a former intergovernmental organization with deep ties to the British government and the maritime industry. Questions about whether a U.S.-controlled Viasat would maintain Inmarsat's UK operations, jobs, and commitment to maritime safety services were politically sensitive.

The European Commission opened an in-depth Phase II investigation, examining whether the combination of Viasat's and Inmarsat's aviation connectivity businesses would harm competition for European airlines. The Commission's concerns centered on the possibility that the merged entity would have excessive market power in certain in-flight connectivity segments.

The U.S. Federal Communications Commission conducted its own review, focusing on spectrum licensing and national security implications. Competitors raised objections at every stage. OneWeb and Eutelsat, which had recently announced their own merger, argued that the Viasat-Inmarsat combination would create an unfair competitive advantage. Geopolitical concerns swirled around foreign ownership of spectrum assets that were used for government and military communications by multiple nations.

Through it all, Viasat management had to keep both companies operating effectively while unable to integrate them. The regulatory limbo created its own costs: key talent at both companies was uncertain about their future, customers questioned the stability of their service providers, and competitors exploited the uncertainty to win business.

The CMA provisionally cleared the deal on March 1, 2023, with final unconditional clearance on May 9. The FCC approved on May 19. The European Commission gave unconditional approval on May 23, after its extended investigation. None of the regulators imposed conditions, a significant outcome that validated the companies' argument that the combination would enhance rather than harm competition.

The deal finally closed on May 30, 2023, eighteen months after announcement. For Dankberg and his team, who had spent a year and a half in regulatory limbo while simultaneously preparing for the ViaSat-3 Americas launch, the closing was both a relief and the starting gun for an enormous integration challenge. The combined company now had over seven thousand employees across dozens of countries, a fleet of more than a dozen satellites in various orbits, ground stations on every continent, and customer relationships spanning every major airline, shipping company, and government agency in the world. But the integration challenges were just beginning.

Merging two complex global organizations, each with its own satellite fleet, ground infrastructure, customer base, technology stack, and corporate culture, is among the most difficult tasks in business. The history of mergers in the satellite industry is littered with integration failures where the combined entity proved less valuable than the sum of its parts.

Inmarsat's London-based team had a maritime and regulatory heritage fundamentally different from Viasat's San Diego engineering culture. Inmarsat employees had spent careers in a company originally created by international treaty, with deep relationships with the International Maritime Organization, the International Civil Aviation Organization, and government regulators worldwide. Viasat's culture was more entrepreneurial, more engineer-driven, and more comfortable with risk.

Overlapping assets had to be rationalized. Both companies operated ground stations, network operations centers, and customer support organizations that served similar but not identical functions. Revenue synergies, including cross-selling Viasat's aviation products to Inmarsat's airline customers and vice versa, required organizational alignment that could not happen overnight. Cost synergies, estimated at over two hundred million dollars annually, demanded painful decisions about redundant operations and headcount.

The financial impact was immediate and visible. Revenue jumped from two point five six billion dollars in fiscal 2022 (the last full year before Inmarsat) to four point two eight billion in fiscal 2023, reflecting roughly eleven months of Inmarsat contribution. But the net loss widened dramatically as integration costs, amortization of acquired intangible assets, and interest expense on the massively expanded debt load weighed on the bottom line. Total debt ballooned to over seven point five billion dollars. The company was now operating at a leverage ratio that left very little room for error.

VIII. ViaSat-3: The Most Ambitious Gamble Yet (2023-Present)

The ViaSat-3 program was supposed to be Dankberg's magnum opus. Three ultra-high-capacity geostationary satellites, each designed to deliver over one terabit per second of total throughput, positioned to provide seamless global coverage across the Americas, Europe-Middle East-Africa, and Asia-Pacific. Each satellite would carry one of the largest Ka-band reflector antennas ever sent to space, mounted on a deployable boom roughly eighty to ninety feet long. The total program cost ran into the billions of dollars. If successful, the ViaSat-3 constellation would make Viasat the undisputed leader in high-throughput geostationary satellite capacity, with economics that Dankberg argued would be competitive with low-earth orbit constellations for many applications.

On April 30, 2023, just days before the Inmarsat deal closed, the first ViaSat-3 satellite, designated Americas, launched aboard a SpaceX Falcon Heavy rocket. The launch itself was flawless. The satellite reached its orbital slot. Solar panels deployed. And then something went wrong.

During the weeks-long process of deploying the massive Ka-band reflector antenna, built by Northrop Grumman, an "unexpected event" occurred. The reflector was one of the largest ever sent to space, attached to a deployable boom roughly eighty to ninety feet long. Deploying a structure that large in the vacuum of space, where temperature swings between sunlight and shadow can exceed five hundred degrees, is one of the most mechanically complex operations in satellite engineering. The boom takes days to fully extend, and the process cannot be rushed or reversed.

The reflector failed to deploy properly. The exact cause was not immediately disclosed, but the practical impact was devastating. Without a fully functioning main antenna, the satellite's Ka-band commercial capacity was crippled. Viasat's most important satellite, the one that was supposed to validate the entire ViaSat-3 architecture, was unable to deliver anything close to its designed capability.

The disclosure hit the stock market with brutal force. On July 12 and 13, 2023, when Viasat revealed the extent of the problem, the stock suffered its worst trading days in company history. The timing could not have been worse. The company had literally just closed the Inmarsat acquisition weeks earlier, loading itself with billions in debt to fund a global expansion strategy predicated on ViaSat-3 capacity. Investors who had been willing to give Dankberg the benefit of the doubt on the Inmarsat acquisition now faced the prospect of a company carrying over seven billion dollars in debt while its crown jewel satellite floated uselessly in orbit. The stock, which had traded above sixty dollars before the Inmarsat announcement, would eventually crater to seven dollars and thirty-six cents by April 2025, a decline of nearly ninety percent from its peaks.

Viasat filed an insurance claim of four hundred twenty-one million dollars, described as potentially the largest satellite insurance claim ever filed. The satellite was insured for four hundred twenty million dollars across multiple policies against a total mission cost of approximately seven hundred million dollars. Viasat announced that it would not replace the Americas satellite, instead focusing on extracting whatever limited value it could from the partially functioning spacecraft. By August 2024, the damaged satellite entered limited commercial service for aviation customers in North America, operating at roughly ten percent of its intended capacity. It was a remarkable engineering salvage effort, but it represented a fraction of the capacity that had been planned.

The ViaSat-3 program did not end there. The second satellite, designated EMEA (Europe, Middle East, Africa), successfully launched on November 13, 2025, aboard a United Launch Alliance Atlas V 551 rocket from Cape Canaveral. As of early 2026, it is undergoing in-orbit testing with commercial service expected to begin in the first half of 2026. The third satellite, covering Asia-Pacific, is anticipated to launch later in 2026. The success of these remaining satellites is critical to Viasat's global strategy and to demonstrating that the Americas failure was an isolated manufacturing defect rather than a systemic design flaw.

The existential question hanging over the entire ViaSat-3 program is whether geostationary satellite economics can work in the Starlink era. Dankberg has argued consistently that a single GEO satellite delivering a terabit of capacity costs far less than the thousands of LEO satellites needed to achieve similar aggregate throughput. The math, he contends, favors GEO for applications where latency is tolerable: aviation, maritime, rural broadband, enterprise mobility. The counterargument, increasingly supported by market evidence, is that latency matters more than Dankberg admits, that LEO costs are falling faster than GEO advocates predicted, and that the consumer market, which represents the largest addressable revenue pool, will never accept six-hundred-millisecond delays when twenty-millisecond alternatives exist.

IX. The Competitive Landscape: Starlink, LEO, and the Space Internet Wars

By early 2026, SpaceX's Starlink has become the most disruptive force in the history of satellite communications. With over six million subscribers across more than one hundred forty countries and nearly eight thousand satellites in low-earth orbit, Starlink has achieved a scale that no satellite operator has ever approached. Its median download speed reached approximately one hundred five megabits per second, nearly double what it delivered just two and a half years earlier. Its latency of roughly forty-five milliseconds, while not matching fiber, is close enough for video calls, online gaming, and virtually every consumer application. By contrast, Viasat's median download speeds have been significantly lower, and its inherent GEO latency of approximately six hundred eighty milliseconds makes real-time applications functionally impossible.

The physics trade-offs between GEO and LEO are worth understanding clearly, because they determine the competitive landscape for the next decade. A geostationary satellite sits at roughly thirty-six thousand kilometers altitude, appearing to hover motionless over a fixed point on the equator. This is fantastically convenient: three satellites can theoretically cover the entire globe, ground antennas do not need to track a moving target, and the satellite remains in service for fifteen-plus years. The cost is latency. Light travels at roughly three hundred thousand kilometers per second, so a round trip to GEO and back takes at minimum about five hundred milliseconds, with network processing adding more.

A low-earth orbit satellite, by contrast, orbits at roughly five hundred fifty kilometers altitude. The round-trip signal delay is only a few milliseconds, comparable to terrestrial networks. But the satellite is moving at twenty-seven thousand kilometers per hour, passing over any given ground station in just a few minutes. Imagine trying to have a conversation by shouting at passing cars on a highway: each car hears a few words before it zooms past, and you have to seamlessly hand off to the next car. That is essentially what LEO satellite networks do, thousands of times per second, across the entire planet.

Continuous coverage requires thousands of satellites in coordinated orbits, with sophisticated handoff protocols as each satellite zooms past. The satellites have shorter lifespans (roughly five years versus fifteen for GEO), meaning the constellation must be continuously replenished. If you stop launching replacement satellites, your network degrades within a few years as existing satellites deorbit. This creates a perpetual launch obligation that GEO operators do not face.

The total system cost is staggering, but SpaceX has a unique structural advantage that no other company on earth possesses: it builds its own rockets, launches its own satellites, and amortizes the cost across its dominant commercial launch business. When SpaceX launches Starlink satellites on its own Falcon 9 rockets, the marginal cost of adding satellites to a launch is a fraction of what any competitor would pay for commercial launch services. This cost advantage is structural and essentially unreplicable.

For Viasat, the competitive picture is nuanced by market segment, and this segmentation is arguably the single most important concept for investors to understand.

In residential broadband, the battle is effectively over. Starlink's combination of lower latency, higher speeds, and competitive pricing has made GEO satellite broadband a product of last resort. According to independent speed test data, Starlink's median download speed of roughly one hundred five megabits per second dwarfs what Viasat delivers to residential customers, and its upload speeds have improved even as Viasat's have declined. Viasat's fixed broadband revenues declined sixteen percent year over year in recent quarters, and the trajectory shows no sign of reversing. The question is not whether Viasat can compete in residential broadband, but how quickly and gracefully it can manage the decline of this legacy business.

In aviation, however, Viasat retains significant advantages. Aircraft move through multiple satellite coverage zones during a single flight, and GEO satellites provide seamless coverage across entire oceanic routes without the complex handoff challenges that LEO faces with fast-moving aircraft. Viasat's Ka-band system has been proven on thousands of commercial aircraft over a decade of operations. Starlink's aviation product, called Starlink Aviation, secured a major win when United Airlines announced in September 2024 that it would equip over one thousand planes with Starlink, transitioning away from Viasat. This was a significant competitive blow, but other major carriers, including Delta and American, continue to operate with Viasat, and the company reported approximately three thousand seven hundred fifty commercial aircraft in service with its system plus an additional fourteen hundred sixty in backlog.

In maritime, the Inmarsat acquisition gave Viasat the dominant position in commercial shipping connectivity and safety services. The company's NexusWave maritime product has secured orders from over two thousand vessels, including contracts with major shipping companies like Stena Bulk, Mitsui O.S.K. Lines, Pacific Basin, and Anglo-Eastern. Starlink's maritime offering is growing rapidly, but the regulatory and safety certification requirements for maritime communications create barriers to rapid displacement of established providers.

Beyond Starlink, the competitive landscape includes the merged OneWeb-Eutelsat entity, which focuses on enterprise and government markets with its LEO constellation, and Amazon's Project Kuiper, which has begun launching test satellites but remains years behind Starlink in deployment. Amazon has committed over ten billion dollars to Kuiper and plans to deploy a constellation of over three thousand satellites, but the project has faced repeated delays and has not yet begun commercial service. If Kuiper eventually reaches scale, it would represent yet another well-funded LEO competitor with the resources to sustain losses indefinitely.

Traditional GEO operators like SES and Intelsat have struggled with declining legacy revenues and the challenge of transitioning to next-generation architectures. Intelsat emerged from bankruptcy in 2022 and has been focused on stabilizing its business. SES completed its acquisition of Intelsat in early 2025, creating the largest traditional satellite operator by revenue, but the combined entity still faces the fundamental challenge of competing against LEO constellations with a GEO-centric fleet. These consolidation moves mirror Viasat's own Inmarsat acquisition in their recognition that scale is necessary for survival.

The 5G wireless expansion and ongoing fiber buildout represent additional competitive pressures in markets where terrestrial alternatives are feasible. The U.S. government's Broadband Equity, Access, and Deployment (BEAD) program is channeling billions of dollars into extending fiber and fixed wireless to rural communities, directly reducing the addressable market for satellite broadband providers. Every household that gains access to terrestrial broadband is a household that will never subscribe to satellite internet.

X. The Business Model and Unit Economics Deep Dive

Viasat's financial structure as of fiscal year 2025 reveals a company in transition, generating substantial revenue but struggling to convert that revenue into returns that justify the capital invested. Total revenue for fiscal year 2024 (ending March 2025) reached four point five two billion dollars, up from four point two eight billion the prior year. The company reports in two segments since its reorganization.

The Communications Services segment, representing roughly seventy-three percent of revenue, encompasses everything from airline WiFi and maritime connectivity to government satellite services and residential broadband. Within this segment, the divergent growth rates tell the story of a company in transition.

Aviation has been the growth engine, expanding at approximately fifteen percent year over year as more airlines equip their fleets and passenger demand for in-flight connectivity continues to grow. This is the segment where Viasat's competitive position is strongest and where the Inmarsat acquisition adds the most value through expanded global coverage.

Government satellite communications grew at about nine percent, driven by military modernization programs and the increasing importance of secure space-based communications in an era of great-power competition.

Maritime was roughly flat, declining about three percent as the competitive landscape shifted, though the NexusWave product launch suggests potential for stabilization.

Fixed broadband, the legacy residential business, continued its steep decline of sixteen percent annually as Starlink captured market share. This segment is the financial equivalent of a melting ice cube, still generating meaningful revenue today but shrinking every quarter with no realistic path to recovery.

The Defense and Advanced Technologies segment, or DAT, accounts for roughly twenty-seven percent of revenue and includes information security and cybersecurity products, space and mission systems, and tactical networking equipment. This segment has been growing in the mid-teens percentage range, supported by a healthy backlog and modernization spending across NATO defense forces. Deutsche Bank's February 2026 upgrade to Buy was partly predicated on the argument that this segment could command a significantly higher standalone valuation if separated from the communications business, an intriguing corporate strategy idea that management has not publicly endorsed.

The capital expenditure cycle is perhaps the most important feature of Viasat's business model. Building a geostationary satellite costs five hundred million to over a billion dollars. The ground infrastructure, including gateway stations that connect the satellite network to the terrestrial internet, user terminals for homes and aircraft, and network operations centers, adds hundreds of millions more. Each satellite has a design life of roughly fifteen years, creating a relentless replacement cycle. In fiscal 2024, Viasat spent over one billion dollars on capital expenditures, and in fiscal 2023 it spent over one point five billion, including costs related to ViaSat-3 satellites and Inmarsat integration.

Free cash flow has been deeply negative for years, which is the fundamental challenge with Viasat's investment thesis. You can grow revenue, you can even grow EBITDA, but if the capital expenditures required to sustain the business consume all the operating cash flow, equity holders are left with nothing.

Fiscal 2024 showed negative one hundred twenty-two million dollars of free cash flow, a significant improvement from negative eight hundred fifty-one million in fiscal 2023, but still firmly in cash-burning territory. The improving trajectory was driven by declining satellite construction spending as the ViaSat-3 program moved past its peak investment phase.

The most encouraging recent development came in the Q3 fiscal year 2026 earnings report (February 2026), where the company posted a net income of twenty-five million dollars, beating consensus estimates of a loss by a wide margin, and generated positive free cash flow. The quarter also showed adjusted EBITDA of three hundred eighty-seven million dollars and a total backlog of nearly four billion dollars. Management reiterated guidance for positive free cash flow in both fiscal 2026 and fiscal 2027, accelerating their previous timeline by a year. This was the quarter that catalyzed the stock's recovery from single digits.

The debt load remains the most significant financial risk. Total debt stood at seven point five billion dollars at the end of fiscal 2024, with net debt of approximately five point nine billion. To put this in context, Viasat's annual interest expense exceeded four hundred million dollars in fiscal 2024, consuming nearly half of its operating cash flow. Every dollar spent servicing debt is a dollar that cannot be invested in new satellites, ground infrastructure, or competitive responses to Starlink.

The Ligado Networks settlement, announced in June 2025, provided a critical financial lifeline. The settlement arose from a long-running dispute involving Inmarsat's L-band spectrum and Ligado's plans to use adjacent spectrum for terrestrial wireless services. Under the agreement, Viasat received five hundred sixty-eight million dollars in fiscal 2026, including a four hundred twenty million dollar lump sum in October 2025 and a one hundred million dollar payment in March 2026, plus ongoing quarterly payments of approximately sixteen million dollars, increasing three percent annually, extending through 2107. Yes, 2107, over eighty years of recurring payments. Management used the initial Ligado proceeds to retire three hundred million dollars of term loan principal, meaningfully reducing the debt burden. The Ligado settlement was the kind of windfall that only comes from owning genuinely scarce spectrum assets, and it illustrated the hidden value embedded in the Inmarsat acquisition that the market had been underappreciating.

But even after these actions, Viasat carries leverage that makes it vulnerable to any sustained downturn in revenue or increase in interest rates. The comparison to SpaceX's economics is instructive but somewhat misleading. SpaceX is privately held, willing to sustain losses, and subsidizes Starlink's growth with its dominant commercial launch business. Viasat is publicly traded, carries seven-plus billion in debt, and must demonstrate profitability to maintain access to capital markets. These are fundamentally different competitive positions, and the capital structure disadvantage weighs on every strategic decision Viasat makes.

XI. Leadership and Culture: The Mark Dankberg Factor

Mark Dankberg is seventy years old and has led Viasat for four decades. In an industry where CEO tenures average five to seven years, this continuity is extraordinary. He is, in every meaningful sense, the company. His engineering background shapes every strategic decision. His personal conviction that bandwidth productivity, the ratio of useful bandwidth delivered to total lifetime capital cost, is the metric that determines winners and losers in satellite communications has driven every major investment the company has made.

Dankberg's leadership style combines deep technical fluency with a willingness to make asymmetric bets that most CEOs would find terrifying. Consider the pattern. Building ViaSat-1 was a bet-the-company moment for a firm generating a few hundred million in defense revenue. Launching ViaSat-2 doubled down on an architecture that was still unproven commercially. The Inmarsat acquisition tripled down, leveraging the company to acquire a global operator three times its pre-deal size. The ViaSat-3 program quadrupled down, committing billions more to the same GEO thesis even as Starlink's LEO constellation was demonstrating an alternative future.

Each of these bets was rational in isolation. Taken together, they reveal a CEO whose risk tolerance far exceeds industry norms, and whose conviction in his thesis borders on the absolute. At every stage, Dankberg has wagered that his thesis about GEO satellite economics would prove correct over a long enough time horizon. The market has alternatively rewarded him spectacularly and punished him brutally for this conviction. San Diego Entrepreneur of the Year in 2000, Satellite Industry Executive of the Year in 2003, and then watched his stock lose ninety percent of its value two decades later as the market questioned whether his thesis had been overtaken by events.

His core philosophy can be summarized in a few key principles. First, vertical integration is essential. Viasat designs its own satellite payloads, builds its own ground terminals, operates its own network, and sells directly to end users. This allows optimization across the entire stack but requires competence at every layer. Second, bandwidth demand will always grow faster than supply. Dankberg has consistently argued that the world's appetite for connectivity is insatiable and that the companies positioned to deliver the most bandwidth at the lowest cost will eventually win. Third, the right comparison for satellite economics is not fiber or 5G but rather the cost of extending those terrestrial technologies to areas they cannot economically reach. In rural America, over oceans, in remote military theaters, and on moving platforms like aircraft and ships, satellites are not competing with fiber. They are the only option.

The succession question is unavoidable for a seventy-year-old founder-CEO. Dankberg briefly attempted a leadership transition in November 2020, moving to Executive Chairman while Rick Baldridge took over as CEO. But Dankberg returned to the CEO role effective July 1, 2022, reportedly because he felt the company needed his direct involvement during the critical Inmarsat acquisition and ViaSat-3 launch period. There is no publicly announced succession plan, and the company's key executives, including CFO Garrett Chase, CTO Girish Chandran, and the heads of the commercial and government businesses, are capable operators but none has been visibly groomed as the next CEO. For a company carrying this much debt and navigating this much competitive disruption, the key-person risk around Dankberg is material.

The broader management team reflects Viasat's dual heritage as both a defense contractor and a commercial technology company. Craig Miller leads the government business. James Dodd runs commercial services. Girish Chandran, who has been CTO since the company's early years, provides engineering continuity. The San Diego engineering culture that Dankberg inherited from Linkabit remains embedded in the organization, emphasizing technical excellence, willingness to tackle hard problems, and a certain stubborn confidence that the physics will eventually vindicate the strategy.

XII. Strategic Analysis: Porter's Five Forces

To assess Viasat's competitive position rigorously, it helps to examine the industry through Michael Porter's framework.

The threat of new entrants is high and rising. Declining launch costs, driven primarily by SpaceX's reusable rockets, have dramatically lowered the capital barrier to deploying satellite capacity. Amazon's Project Kuiper, backed by one of the world's largest companies, represents a credible new LEO entrant. Direct-to-device satellite partnerships between telecom operators and companies like AST SpaceMobile are creating new competitive architectures. The traditional barriers of spectrum rights and regulatory approvals remain significant but are not insurmountable for well-funded players.

Supplier bargaining power is moderate. Viasat relies on satellite manufacturers (Boeing built ViaSat-1 and ViaSat-2, while the ViaSat-3 bus was built by Boeing with the antenna by Northrop Grumman) and launch providers (SpaceX, ULA). However, Viasat's vertical integration, designing its own satellite payloads and much of its ground equipment, significantly reduces its dependence on external suppliers compared to traditional satellite operators who buy turnkey systems.

Buyer bargaining power is medium-high and varies by segment. Airlines negotiating in-flight connectivity contracts have significant leverage because they control terminal access and can credibly threaten to switch providers. United's decision to move to Starlink demonstrated this leverage vividly. Residential consumers are price-sensitive and increasingly have alternatives. Government customers tend to be more loyal due to security clearance requirements and certification costs, but they also drive hard bargains on pricing.

The threat of substitutes is high and represents the most significant strategic challenge. In residential broadband, Starlink is not just a substitute but a superior product for most customers. Terrestrial 5G and fixed wireless access are expanding their reach. Fiber-to-the-home buildouts, accelerated by government subsidies, are reducing the addressable market for satellite broadband. In aviation and maritime, the substitute threat is lower because there are fewer alternatives for over-ocean connectivity, but Starlink's rapid entry into both segments is changing this calculus.

Competitive rivalry is very high across every segment. Starlink's scale, cost advantages from vertical integration with SpaceX, and rapid iteration cycle create constant competitive pressure. Traditional GEO operators are fighting for survival. The pace of technology innovation is accelerating, and price competition is intensifying as more capacity comes online. This is an industry where multiple well-funded players are willing to sustain losses for years to capture market share.

The overall Porter's assessment is unfavorable. Viasat operates in an industry with high entry threat, high substitute threat, high rivalry, moderate-to-high buyer power, and only moderate supplier power partially offset by vertical integration. This is structurally a difficult industry in which to earn attractive returns on capital, which helps explain why Viasat has struggled to generate positive free cash flow despite growing revenues. The competitive forces are simply relentless.

XIII. Strategic Analysis: Hamilton's Seven Powers

Hamilton Helmer's Seven Powers framework offers a complementary lens for evaluating Viasat's competitive durability.

Scale economics are moderate but nuanced. Satellite capacity utilization is critical to economics, since the cost of a satellite is largely fixed regardless of how many customers it serves. Think of it like a hotel: whether you have one guest or a full house, the mortgage payment is the same. Higher utilization means lower cost per bit. Viasat's ground infrastructure, including hundreds of gateway stations and network operations centers around the world, provides some scale benefit that new entrants cannot easily replicate. But the fundamental scale advantages are limited by the fact that competitors can and do launch their own satellites, and each new constellation resets the capacity equation.

Network effects are weak to moderate. In aviation, there is a mild network effect: more equipped aircraft improve the overall coverage and reliability of the service, making it more attractive to airlines. But this is not a viral, consumer-driven network effect like a social platform. Passengers do not choose airlines based on the WiFi provider.

Counter-positioning was historically Viasat's strongest power. The high-throughput satellite model genuinely disrupted traditional GEO operators who were locked into wide-beam architectures and could not match Viasat's bandwidth economics without cannibalizing their existing business. But the irony is palpable: Viasat is now being counter-positioned by Starlink, which built a fundamentally different architecture (LEO) that traditional GEO operators, including Viasat, cannot easily replicate without abandoning their existing capital base. The disruptor became the disrupted.

Switching costs are moderate. Airlines that have installed Viasat equipment on hundreds of aircraft face significant costs to rip out and replace that hardware, including aircraft downtime, installation labor, and new certification. But these costs, while real, are not prohibitive for large carriers as United's Starlink transition demonstrated. Government contracts create stickier switching costs through certification requirements and security clearance dependencies.

Branding is moderate. Viasat has strong brand recognition in aviation, where airline passengers associate its name with quality WiFi. In the consumer market, the Viasat brand has less cachet. In government and defense, credibility and track record matter more than brand per se, and Viasat has decades of that.

Cornered resources are moderate. Viasat's spectrum licenses, particularly the L-band spectrum acquired with Inmarsat, are genuinely valuable and difficult to replicate. Orbital slots for geostationary satellites require ITU coordination and are a finite resource. However, LEO operators do not need geostationary orbital slots, and alternative spectrum bands are becoming available through regulatory reforms.

Process power is moderate to strong. Viasat's decades of experience in satellite payload design, ground network engineering, and complex systems integration represent accumulated know-how that is genuinely difficult to replicate quickly. The ability to design a terabit-class satellite payload in-house is a rare capability. But process power alone is insufficient to overcome a competitor with superior architecture and lower costs.

The overall assessment is sobering but not hopeless. Viasat lacks a dominant, durable competitive power in the Helmer framework. It operates in a highly competitive, capital-intensive industry facing a competitor in Starlink that possesses superior counter-positioning (LEO versus GEO) and significant scale economics (thousands of satellites, millions of subscribers, vertically integrated launch capability). Viasat's best competitive positions are in aviation and maritime, where its installed base, regulatory certifications, and spectrum assets create moderate switching costs and process power advantages. These are defensible niches, but they are niches.

The key insight from combining Porter's and Helmer's frameworks is that Viasat's competitive position is segment-dependent. In consumer broadband, the company has virtually no durable advantage against Starlink. In aviation and maritime, it has a combination of process power, switching costs, and cornered resources (spectrum) that create a defensible if not impregnable position. In government and defense, security certifications and long-standing relationships provide the stickiest competitive protection. The strategic imperative is clear: double down on the segments where durable advantages exist and manage the decline in segments where they do not.

XIV. Bull versus Bear Case

The Bull Case

The most compelling argument for Viasat centers on market segmentation, and it is worth steel-manning this case because it is more nuanced than the bears give it credit for. Not every connectivity application requires low latency, and not every customer can be served by Starlink. The satellite communications market is not a single winner-take-all contest but rather a collection of distinct markets with different competitive dynamics, customer requirements, and barriers to entry. Aviation remains Viasat's strongest franchise. The company connects thousands of commercial aircraft and has a backlog of nearly fifteen hundred more. Airlines value reliability, proven technology, and the seamless coverage that GEO satellites provide over oceanic routes. Delta and American continue to expand their Viasat deployments, and the global aviation market is still in the early stages of equipping fleets with genuine broadband.

Maritime is the next pillar. The Inmarsat acquisition gave Viasat a dominant position in commercial shipping connectivity and maritime safety services that is backed by decades of regulatory certification and customer relationships. The NexusWave product has gained rapid traction, with over two thousand vessels ordered. The maritime market is inherently global, favoring operators with worldwide coverage, and the safety-of-life regulatory requirements create significant barriers to rapid competitive displacement.

The integration of Inmarsat, if successful, could unlock over two hundred million dollars in annual cost synergies while creating revenue cross-selling opportunities that neither company could pursue independently. The combined spectrum portfolio, spanning L-band, Ka-band, and other frequencies, is the broadest in the industry and supports an expanding range of mobility applications including the Equatys direct-to-device joint venture with Space42.

The defense and advanced technologies business provides a stable, growing revenue base with attractive margins and a substantial backlog. Military modernization spending across NATO allies, cybersecurity demand, and the increasing importance of satellite communications in modern warfare all represent structural tailwinds. Deutsche Bank's suggestion that this business could be worth more as a standalone entity highlights the potential for value unlocking through corporate actions.

The ViaSat-3 EMEA satellite's successful November 2025 launch was a critical proof point. If EMEA enters commercial service successfully and the APAC satellite launches on schedule, Viasat will have demonstrated that the Americas failure was an isolated defect rather than a fundamental design flaw. The combined capacity of even two functioning ViaSat-3 satellites would significantly expand Viasat's global coverage and economics.

Finally, the stock's dramatic recovery from its April 2025 low of seven dollars and thirty-six cents to approximately forty-six dollars demonstrates that the market recognizes the company's asset value and turnaround potential. The Ligado settlement, accelerated free cash flow timeline, and Q3 fiscal 2026 earnings beat all suggest operational momentum.

The Bear Case

The bear case is equally worth steel-manning, because the risks are not hypothetical; they are playing out in real time. The most dangerous scenario for Viasat is the one where Starlink's advantages prove universal rather than segment-specific. If Starlink Aviation can match or exceed Viasat's reliability on aircraft while offering lower latency and lower pricing, the airline contract renewals coming in the next few years could go badly. United's defection was the canary in the coal mine.

The ViaSat-3 Americas failure was not just a one-satellite problem. It destroyed hundreds of millions of dollars of value, rattled the satellite insurance market, and raised questions about Viasat's ability to execute on its most critical programs. The remaining ViaSat-3 satellites must perform flawlessly, because another failure would be catastrophic for a company carrying this much debt.

The debt burden itself is the most immediate risk. Over seven billion dollars in total debt, with net debt of roughly five to six billion, creates massive interest expense (over four hundred million dollars annually) and limits financial flexibility. If revenues decline, if integration costs exceed expectations, or if capital markets become less accommodating, the company could face a refinancing crisis. The interest rate environment, while having moderated from 2023-2024 peaks, remains elevated relative to the near-zero rates that prevailed when much of this debt was incurred.

The Inmarsat integration remains ongoing and inherently risky. Merging two global satellite operators with different technologies, cultures, and customer bases is a multi-year process where execution failures can destroy value faster than strategic synergies can create it. Revenue synergies in particular are notoriously difficult to achieve in technology mergers.

In residential broadband, the decline is structural and accelerating. Viasat cannot compete with Starlink on speed, latency, or increasingly on price. Every dollar of residential revenue lost reduces the utilization of Viasat's satellite capacity, worsening the economics for all services. This creates a vicious cycle: lower utilization means higher per-subscriber costs, which makes it harder to compete on price, which drives more subscribers to Starlink, which further reduces utilization.