Virtus Investment Partners: The Story of a Multi-Boutique Asset Manager

I. Introduction & Episode Roadmap

Picture this: a company managing over one hundred and fifty billion dollars in assets, with fifteen distinct investment boutiques under its umbrella, run by about eight hundred employees out of Hartford, Connecticut. And yet, if you stopped the average investor on the street and asked them about Virtus Investment Partners, you'd almost certainly get a blank stare. This is not BlackRock. This is not Vanguard. This is not even a household name among financial advisors. But Virtus may be one of the most fascinating transformation stories in modern asset management, a tale of survival, reinvention, and the relentless pursuit of a model that somehow works in an industry where the gravitational pull toward passive indexing has destroyed dozens of active managers.

Here is the question at the heart of this story: How did a Hartford insurance company's investment management arm, spun off at the absolute worst moment in financial history, claw its way from twenty-two billion dollars in assets under management to a peak of one hundred seventy billion? And what does that journey tell us about the future of active management in an era when most experts have declared it dead?

The answer lies in what the industry calls the "multi-boutique model." Rather than building one monolithic investment firm with a single culture and process, Virtus assembled a federation of specialized investment managers, each with their own philosophy, team, and identity, all operating under one corporate umbrella. Think of it as the Berkshire Hathaway approach applied to asset management: buy great teams, leave them alone to do what they do best, and provide the plumbing, distribution, and capital they need to grow.

This is a story about survival through the 2008 financial crisis, strategic transformation through a decade of acquisitions, and the ultimate test facing every active manager today: Can you justify your fees in a world where an index fund costs almost nothing? The answer, as we'll see, is complicated, fascinating, and still very much unresolved.

The key themes we'll explore are threefold. First, the art of the roll-up, how Virtus built its acquisition playbook and what separates a good deal from a bad one in asset management. Second, the multi-boutique model itself, why it works in theory, where it breaks down in practice, and what the economics actually look like under the hood. And third, the existential question facing the entire active management industry: What happens when the tide of passive investing meets the immovable object of human talent and specialized expertise?

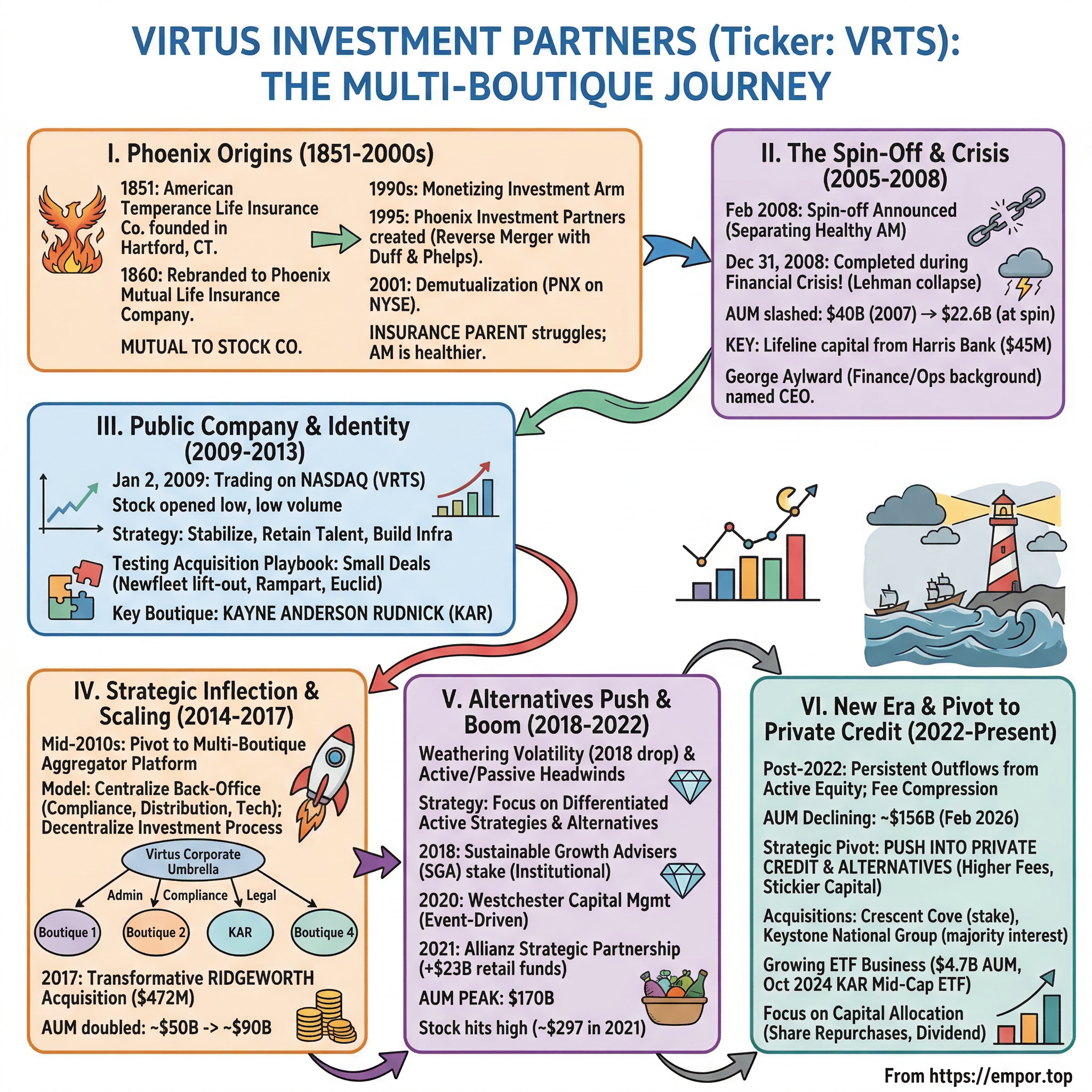

II. The Phoenix Companies Origins & Early History (1851-2000s)

In 1851, a group of prominent Hartford businessmen, religious leaders, and civic figures pooled their resources to found The American Temperance Life Insurance Company. The premise was radical for its time: the company would only insure individuals who abstained from alcohol, a bet that sober policyholders would live longer and cost less in claims. Hartford was already becoming the insurance capital of America, and this new venture fit neatly into the city's growing financial ecosystem.

As the temperance movement faded from cultural prominence, the company recognized it needed a broader mandate. In 1860, it rebranded as Phoenix Mutual Life Insurance Company, dropping the abstinence requirement and opening its doors to all comers. The name change proved prescient in more ways than one. Phoenix Mutual would rise, fall, and rise again repeatedly over the next century and a half, much like its mythological namesake. The company famously insured President Abraham Lincoln, and paid the claim to his survivors after the assassination in 1865, an early demonstration of institutional credibility that would serve the brand well for generations.

Over the next hundred and thirty years, Phoenix Mutual grew steadily through the insurance industry's golden age, merging with Home Life Insurance Company in 1992 to become Phoenix Home Life Mutual Insurance Company. But the really interesting part of the story, the part that gives birth to Virtus, begins in the mid-1990s.

Insurance companies have always needed to manage enormous pools of capital, the premiums they collect, the reserves they maintain, the float that sits between when money comes in and when claims go out. For most of insurance history, this was handled internally. But by the 1990s, the asset management industry had evolved into its own profit center, and insurance companies began to realize their investment arms could be monetized as standalone businesses. This was the era when many of today's asset management giants were born from insurance parentage: Lincoln National spun out Delaware Investments, Cigna's investment arm became separate, and dozens of similar transactions played out across the industry.

On November 1, 1995, Phoenix created its dedicated asset management subsidiary through a reverse merger combining Phoenix Home Life's investment operations with Duff & Phelps Corporation, creating Phoenix Investment Partners with approximately thirty-five billion dollars in combined assets. This was the moment that planted the seed for everything that would follow. The newly formed entity immediately began assembling a portfolio of boutique managers, acquiring stakes in Kayne Anderson Rudnick in 2002, GMG/Seneca Capital Management in 1997, and Zweig Advisers in 1998. The multi-boutique DNA was there from the very beginning.

Then came the demutualization wave. In 2001, Phoenix converted from a mutual company owned by its policyholders to a publicly traded stock company, becoming The Phoenix Companies, Inc., listed on the New York Stock Exchange under the ticker PNX. This was part of a broader industry trend, MetLife, Prudential, and John Hancock all demutualized around the same time, driven by the logic that public markets could provide growth capital that mutual structures could not.

But here is the crucial detail that sets the stage for everything that follows: The Phoenix Companies' insurance business was struggling. The parent company would eventually be acquired by Nassau Financial Group in 2016, but long before that, it became clear that the asset management arm was far healthier than the insurance operation it served. The question became: Could the investment management business stand on its own?

III. The Spin-Off and the Worst Timing in Financial History (2005-2008)

On February 7, 2008, The Phoenix Companies made an announcement that would either prove brilliant or catastrophic, depending on how the next twelve months played out. The company declared its intention to spin off Phoenix Investment Partners as an independent, publicly traded entity. The asset management business would be rebranded as Virtus Investment Partners, a name derived from the Latin word for virtue and strength. The timing seemed reasonable. Markets were choppy but not yet in freefall, and the strategic logic was sound: Separate the healthy asset management business from the struggling insurance parent, give it its own stock, its own board, and the freedom to pursue its own destiny.

Then Lehman Brothers collapsed.

The spin-off was completed after market close on December 31, 2008, quite literally in the final hours of the worst year for financial markets since the Great Depression. Phoenix shareholders received one share of Virtus for every twenty shares of Phoenix they held. The newly independent company was born into chaos. Assets under management, which had stood at forty billion dollars in 2007, had been slashed nearly in half to twenty-two point six billion dollars by the time of the spin-off, as market declines and client redemptions ravaged the portfolio.

There is a detail worth noting here that speaks to George Aylward's foresight as a leader. Before the spin-off, Aylward, who had been named President of Phoenix Investment Partners in 2006, orchestrated a deal with Harris Bankcorp, a subsidiary of Bank of Montreal, to invest forty-five million dollars in convertible preferred stock, giving Harris a twenty-three percent equity position in the new company. This was not just capital; it was a lifeline. In the midst of the worst financial crisis in eighty years, having a strong banking partner willing to put real money into your company was the difference between survival and oblivion.

George Aylward had joined Phoenix Investment Partners' corporate finance team in 1996, after starting his career at PriceWaterhouse in the financial services group. Born in 1964, he held degrees from the University of Connecticut and the University of Massachusetts, along with a CPA designation. He had served as Chief of Staff to the CEO of The Phoenix Companies from 2002 to 2004, then as COO of the investment management subsidiary, before being elevated to President. He was an operations and finance person by training, not a portfolio manager or investment star. This would prove to be exactly the right profile for what the company needed: someone who could build systems, structure deals, and create a platform, rather than someone who wanted to manage money personally.

Virtus began trading on NASDAQ on January 2, 2009. The stock opened in the single digits. Trading volumes were anemic, some days seeing only a few thousand shares change hands. The company was a rounding error in the financial services universe, too small to appear on most institutional investors' radars, too obscure for retail investors to notice. But it was alive, and in the winter of 2009, that counted for something.

IV. Going Public & Finding an Identity (2009-2013)

The first two years of Virtus's independent existence were a study in survival. The stock traded in the low single digits through early 2009, touching as low as four dollars in March of that year, when the broader market hit its crisis nadir. Daily trading volumes regularly dipped below ten thousand shares. This was a company that the market had essentially written off, an orphaned spin-off from a troubled insurance company, dumped into public markets at the worst possible moment, with no natural shareholder base and no analyst coverage to speak of.

But George Aylward and his team, including CFO Michael Angerthal who had joined in 2008 specifically to prepare the company for independence, had a plan. Angerthal brought a distinctive background to the role: he had earned his BBA in Accounting from Pace University and an MBA in Corporate Finance from Columbia Business School, then spent nine years across several GE units including GE Capital and GE Real Estate, absorbing the GE playbook of disciplined financial management and operational efficiency. Before joining Virtus, he had served as CFO of CBRE Realty Finance. Together, Aylward and Angerthal formed a leadership duo that combined strategic vision with financial discipline, a combination that would prove essential in the years ahead.

The post-crisis asset management landscape was brutally Darwinian. The first wave of money flowing into passive index funds was accelerating, driven by the humiliation that most active managers had suffered during the crisis. Fee compression was beginning to bite. And for a firm of Virtus's size, roughly twenty billion dollars in AUM, the competitive position was precarious: too small to compete with the giants on distribution and brand recognition, too large to operate as a nimble boutique with a single concentrated strategy. They were stuck in what strategy consultants call "the valley of death" for mid-sized asset managers.

The company's early strategy was straightforward: stabilize the existing business, retain investment talent, and begin building the infrastructure that would support future growth. Virtus already had a few strong boutiques within its portfolio, most notably Kayne Anderson Rudnick, a Los Angeles-based firm specializing in high-quality growth equities. Kayne Anderson Rudnick had been partially acquired by Phoenix back in 2002, with full ownership following in September 2005. The firm had a distinctive investment philosophy centered on owning high-quality companies with strong competitive positions, and it would eventually become the single most important asset within the Virtus empire.

By 2011, the team began testing the acquisition playbook that would define the next decade. In June of that year, Virtus executed a team lift-out from ING to create Newfleet Asset Management, bringing over approximately five point two billion dollars in multi-sector fixed income assets. This was not a traditional acquisition of a corporate entity; it was a recruitment of a team, which is often the most effective way to build an asset management business because the relationships and investment process travel with the people, not the corporate shell.

The following year, Virtus completed two more deals. In October 2012, it acquired Rampart Investment Management, a Boston-based firm specializing in customized options strategies managing about one point four billion dollars. In December 2012, it added Euclid Advisors, bringing international equity capabilities through a team of industry veterans. These were small deals by any measure, but they were teaching Virtus how to identify, evaluate, integrate, and retain boutique teams. Each deal was a rehearsal for the larger transactions that would follow.

The stock, meanwhile, began its recovery. From that four-dollar nadir in March 2009, shares climbed steadily through 2012 and into 2013, reflecting both the broader market recovery and growing investor recognition that Virtus was building something different. Revenue grew from approximately three hundred twenty-two million dollars in 2016, the earliest full-year figure in the available data, having built up from much smaller figures in the early years. The multi-boutique thesis was taking shape, but the real transformation was still ahead.

V. The Multi-Boutique Transformation: Strategic Inflection (2014-2017)

Every great corporate transformation has an inflection point, a moment when the leadership team stops experimenting and fully commits to a strategic direction. For Virtus, that moment arrived in the mid-2010s, when the company shifted from opportunistically adding boutiques to systematically building a multi-boutique aggregator platform.

To understand why this mattered, it helps to understand the multi-boutique model itself. Imagine you are a talented portfolio manager running a small investment firm. You are brilliant at picking stocks, but you hate dealing with compliance, technology, marketing, fund administration, and the dozens of intermediaries who stand between you and the end investor. You have two choices: stay independent and struggle with all of that overhead, or sell your firm to a large asset manager and risk losing your autonomy, your culture, and eventually your best people. The multi-boutique model offers a third path. You sell a majority stake to a parent company like Virtus, which takes over all the operational and distribution headaches, but you retain control over your investment process, your team, your brand identity, and your day-to-day culture. It is the best of both worlds, at least in theory.

Affiliated Managers Group, or AMG, had pioneered this model starting in the 1990s, typically taking minority equity stakes in independent managers. Virtus took a different approach, generally acquiring majority or full ownership positions, which gave it more control but also more responsibility for integration. Victory Capital, another peer, developed yet another variation, fully integrating acquired firms onto a single operating platform while preserving some degree of investment autonomy.

In January 2015, Virtus acquired ETF Issuer Solutions, later renamed Virtus ETF Solutions, which gave the company a platform for listing and distributing exchange-traded funds. This was a small but strategically important move: ETFs were clearly the growth vehicle in asset management, and having the plumbing in place to launch and distribute ETFs would prove valuable as the company grew.

But the true game-changer of this era was not a small bolt-on. It was the deepening relationship with Kayne Anderson Rudnick. Though KAR had been part of the Virtus family since the Phoenix days, the boutique's investment performance during the post-crisis bull market was exceptional, and its assets under management were growing rapidly. By the mid-2010s, KAR was becoming the crown jewel of the Virtus portfolio, specializing in high-quality small and mid-cap growth equities with a process rooted in fundamental research and a focus on companies with sustainable competitive advantages. The firm was based in Los Angeles, far from Hartford, and operated with almost complete autonomy, exactly the way the multi-boutique model was designed to work.

Then came the deal that truly transformed the company's scale. In June 2017, Virtus acquired RidgeWorth Investments from Lightyear Capital for four hundred seventy-two million dollars. This was a transformative transaction by every measure. RidgeWorth brought approximately forty billion dollars in assets under management across three affiliated boutiques: Ceredex Value Advisors, Seix Investment Advisors, and Silvant Capital Management. In a single stroke, Virtus roughly doubled its AUM from approximately fifty billion to ninety billion dollars.

The RidgeWorth deal illustrated both the opportunities and risks of the multi-boutique roll-up. On the opportunity side, Virtus was acquiring established teams with strong track records at a time when smaller multi-boutique platforms were struggling to compete independently. On the risk side, integrating three new affiliates simultaneously, each with its own culture and investment approach, while maintaining the autonomy that made those teams valuable in the first place, was an enormous operational challenge. The purchase price of nearly half a billion dollars was significant for a company of Virtus's size, and the debt taken on to fund the deal would remain on the balance sheet for years.

Revenue jumped from three hundred twenty-two million dollars in 2016 to four hundred twenty-four million in 2017, a thirty-two percent increase driven largely by the RidgeWorth integration. Earnings per share more than doubled. The market took notice, and Virtus's stock, which had been trading around a hundred eighteen dollars at the end of 2016, climbed to a hundred fifteen by year-end 2017, reflecting both the scale benefits and investor concerns about digesting such a large acquisition.

VI. Scaling Up Through Strategic Partnerships (2017-2019)

With the RidgeWorth integration underway, Virtus entered a period of consolidation and selective growth. The company needed to prove that it could digest a major acquisition while maintaining investment performance across its expanding roster of boutiques. This was the operational test that would determine whether Virtus was a real platform or just a collection of disparate investment firms stapled together under a common corporate name.

The key to Virtus's integration approach was a principle that sounds simple but is extraordinarily difficult to execute: centralize everything that doesn't touch the investment process, and decentralize everything that does. Distribution, compliance, technology, fund administration, accounting, legal, and HR were all handled at the parent company level. Investment decisions, portfolio construction, research, client relationships, and team management remained firmly within each boutique. This created what management described as operational leverage: Each new affiliate added to the platform benefited from existing infrastructure without requiring proportional increases in corporate overhead.

The financial results during this period told a mixed story. Revenue climbed to five hundred fifty-one million dollars in 2018 and five hundred sixty-two million in 2019, reflecting the full contribution of RidgeWorth assets. But net income was more volatile, as the company navigated market gyrations, fee compression across the industry, and the ongoing costs of building out its platform infrastructure. Earnings per share came in at roughly nine dollars in 2018, then jumped to nearly twelve dollars in 2019 as operating efficiencies began to materialize.

In July 2018, Virtus made another significant move, acquiring a seventy percent stake in Sustainable Growth Advisers, or SGA, for one hundred five million dollars. SGA was a Stamford, Connecticut-based growth equity manager with eleven point six billion dollars in assets, primarily from institutional clients. This was a different kind of acquisition for Virtus. SGA brought a predominantly institutional client base, compared to the retail-heavy mix of most Virtus affiliates, and its focus on large-cap growth equities complemented Kayne Anderson Rudnick's small and mid-cap orientation.

The SGA deal also illustrated a key element of how Virtus structured its acquisitions. Rather than buying one hundred percent of each firm outright, Virtus often acquired majority stakes, leaving existing partners with meaningful equity ownership and alignment. This approach served multiple purposes: it reduced the upfront purchase price, it kept the founding team financially motivated, and it ensured that the investment professionals who made the firm valuable in the first place had every incentive to stay and grow the business.

The industry backdrop during this period was increasingly challenging. The relentless flow of capital from active to passive strategies was accelerating, with index funds and ETFs gathering hundreds of billions in net new assets each year while active equity managers hemorrhaged capital. Virtus's response was to lean into what it did best: specialized, differentiated active strategies where boutique managers could demonstrate genuine edge. The company was not trying to compete with Vanguard on fees or BlackRock on scale. It was betting that there would always be a market for genuinely talented active managers, particularly in less efficient corners of the market like small-cap equities, event-driven strategies, and multi-sector fixed income.

By the end of 2019, Virtus had built a platform with approximately one hundred billion dollars in total assets, up from twenty-two billion at the time of the spin-off a decade earlier. The stock had risen from single digits to over a hundred twenty dollars. The multi-boutique thesis was working, at least in the aggregate. But the real tests, both of the model and of the company's ambitions, were about to arrive.

VII. Weathering Volatility & Continuing the Roll-Up (2018-2020)

The year 2018 delivered a sharp reminder that asset management is, at its core, a leveraged bet on market levels. The fourth quarter of that year saw the S&P 500 drop nearly twenty percent from its September highs, and for asset managers whose revenue is calculated as a percentage of assets under management, that kind of decline hits the income statement immediately and mercilessly. There is no inventory to sell through, no backlog to work off. When markets fall, revenue falls with them, often before expenses can be adjusted.

Virtus navigated this volatility with the discipline that characterized Aylward's management approach. The company did not panic-cut teams, did not abandon its acquisition strategy, and did not chase short-term performance by encouraging its boutiques to deviate from their investment processes. This patience would pay off when markets recovered in 2019, but the episode underscored a fundamental vulnerability of the asset management business model: revenues are inherently volatile, tied to the unpredictable movements of global financial markets, while costs, particularly the compensation of highly skilled investment professionals, are relatively fixed.

The industry headwinds during this period were not just cyclical. The structural shift from active to passive management was accelerating, driven by three reinforcing dynamics. First, the academic evidence that most active managers underperform their benchmarks over long periods continued to accumulate. Second, the fee gap between active and passive had widened to the point where active managers needed to outperform by hundreds of basis points just to break even with a cheap index fund. Third, the rise of financial advisors using model portfolios built around passive ETFs was reducing the demand for actively managed mutual funds that had been Virtus's bread and butter.

Virtus's response to these headwinds was both strategic and tactical. Strategically, the company began shifting its acquisition focus toward higher-fee, stickier asset classes, particularly alternatives and event-driven strategies. Tactically, it invested heavily in its distribution platform, building relationships with the wirehouses, registered investment advisors, and institutional consultants who controlled access to the end investor.

In 2020, as the pandemic struck, Virtus completed its acquisition of Westchester Capital Management in October for one hundred thirty-five million dollars. Westchester was a specialist in global event-driven strategies, best known as the home of The Merger Fund, which had been launched in 1989 as the first mutual fund devoted exclusively to merger arbitrage. This was exactly the kind of differentiated, hard-to-replicate strategy that the multi-boutique model was designed to attract: a highly specialized team with decades of experience in a niche that passive funds could not easily replicate.

The pandemic itself created an unexpected operational test for Virtus. The multi-boutique model, with its emphasis on boutique autonomy and distributed decision-making, turned out to be naturally suited to remote work. Each boutique was already accustomed to operating independently, making its own investment decisions, and managing its own team dynamics. The centralized corporate functions, distribution, compliance, technology, could transition to remote work without disrupting the investment process at any of the affiliates. This structural resilience, while not planned, became an unexpected advantage during a period when many monolithic asset managers struggled with the cultural and operational challenges of sudden remote work.

Revenue for 2020 came in at six hundred three million dollars, reflecting both market dislocations and the partial-year contribution of the Westchester acquisition. Earnings per share were approximately ten dollars diluted. But the seeds of the next phase of growth had already been planted.

VIII. Market Boom & The Alternatives Push (2020-2022)

The eighteen months following the pandemic crash represented arguably the most consequential period in Virtus's history. As markets recovered with stunning velocity, propelled by unprecedented fiscal and monetary stimulus, Virtus executed a series of acquisitions that dramatically reshaped the company's profile and ambitions.

The first major move came in February 2021, when Virtus announced a strategic partnership with Allianz Global Investors. Under this agreement, Virtus became the adviser and distributor for approximately twenty-three billion dollars in Allianz-managed retail mutual fund assets, and the NFJ Investment Group, managing roughly seven billion dollars in value-oriented equities, joined Virtus as an affiliated manager. This partnership increased Virtus's mutual fund assets by approximately forty percent overnight, to about fifty-four billion dollars. It was a creative deal structure: rather than a traditional acquisition, it was a partnership that gave Virtus distribution rights and fee income without the full cost of acquiring a corporate entity.

Then, in January 2022, Virtus closed on the acquisition of Stone Harbor Investment Partners, a specialist in emerging markets debt and multi-asset credit managing approximately fourteen point seven billion dollars. Stone Harbor brought institutional credibility in a fixed income niche that was difficult to replicate organically and that commanded premium fees.

The combined impact of these deals was dramatic. Revenue surged from six hundred three million in 2020 to nine hundred seventy-five million in 2021, an increase of more than sixty percent. Net income more than doubled to two hundred eight million dollars, and diluted earnings per share hit twenty-six dollars. The stock price responded accordingly, reaching two hundred ninety-seven dollars by the end of 2021, a return of roughly three thousand percent from the post-spin-off lows. For investors who had bought Virtus at four dollars in March 2009 and held through all the volatility, this was a generational wealth-creation story.

But the alternatives push was about more than just scale. It reflected a fundamental strategic insight: in a world where passive funds were eating the lunch of traditional active equity and fixed income managers, the best defense was to move into asset classes where passive alternatives did not exist or were impractical. Merger arbitrage, event-driven strategies, infrastructure investing, emerging markets debt, liquid alternatives, these were all areas where human judgment, specialized expertise, and relationship networks still mattered, and where fees could be maintained at levels that justified the cost of maintaining autonomous boutique teams.

By the end of 2021, Virtus had quietly built what amounted to a forty-billion-dollar-plus alternatives and multi-asset platform, representing roughly twenty-two percent of total assets under management. This was not the kind of alternatives business that a Blackstone or KKR would recognize, it was not private equity or real estate with locked-up capital. But within the world of liquid and semi-liquid alternatives accessible to retail and institutional investors through mutual funds and separate accounts, it was a significant and growing franchise.

The year 2022, however, brought a harsh reality check. As the Federal Reserve embarked on its most aggressive interest rate hiking cycle in decades, both equity and fixed income markets declined simultaneously, a rare and painful combination for multi-asset managers. Virtus's AUM declined from its 2021 highs, and net outflows resumed as clients redeemed from strategies that had suffered market-related losses. Revenue held relatively steady at eight hundred eighty-two million dollars, but net income declined to one hundred eighteen million as market headwinds and integration costs weighed on profitability. The stock pulled back sharply from its highs.

IX. The New Era: Navigating Headwinds and Pivoting to Private Credit (2022-Present)

The post-2022 environment has tested Virtus's model in ways that the bull market of 2020-2021 never could. The company has faced a triple challenge: persistent outflows from traditional active equity strategies, fee compression across the industry, and a stock price that has declined significantly from its 2021 peaks. As of mid-March 2026, shares trade around one hundred twenty-six dollars, roughly forty percent below their all-time highs, with a market capitalization of approximately eight hundred fifty million dollars.

The financial performance, however, has been more resilient than the stock price suggests. Revenue came in at eight hundred forty-one million dollars in 2023, dipped slightly, then declined to eight hundred thirty-one million in 2025. But net income actually increased from one hundred thirty-one million in 2023 to one hundred thirty-eight million in 2025, and diluted earnings per share climbed from seventeen dollars seventy-one cents to nearly twenty dollars, reflecting the impact of share repurchases and operational efficiencies. The company has been actively buying back stock, reducing diluted shares outstanding from seven point six million in 2022 to six point nine million in 2025, a reduction of nearly ten percent.

Assets under management, after peaking at one hundred seventy point seven billion in mid-2025, have declined to one hundred fifty-five point nine billion as of February 2026, driven by net outflows of eight point one billion in the fourth quarter of 2025 alone. These outflows have been concentrated in quality-oriented equity strategies, precisely the area where passive alternatives are most competitive and where fee sensitivity is highest.

Management's response has been to accelerate the push into private credit and alternative strategies, areas where passive alternatives are essentially non-existent and fee levels remain attractive. In December 2025, Virtus acquired a thirty-five percent minority stake in Crescent Cove Advisors, a San Francisco-based private credit firm specializing in lending to middle-market technology companies, with approximately one billion dollars in assets. In the same month, the company announced an agreement to acquire a majority interest in Keystone National Group, described as a pioneer in wealth channel private credit strategies. The Keystone deal closed on March 1, 2026, just two weeks before this writing.

These moves represent a meaningful strategic evolution for Virtus. Where the company once focused almost exclusively on liquid, daily-valued strategies distributed through mutual funds and separate accounts, it is now building capabilities in private credit, an asset class with higher fees, stickier capital, and structural barriers to passive competition. The wealth channel angle is particularly interesting: as registered investment advisors and wealth managers increasingly seek to offer their clients access to private market strategies that were historically available only to institutional investors, platforms like Virtus that can package and distribute these strategies through familiar fund structures stand to benefit from a major secular trend.

The ETF business has also emerged as a bright spot. Virtus's ETF assets reached approximately four point seven billion dollars by the end of 2025, with a seventy-four percent organic growth rate over the trailing twelve months. The company launched the Virtus KAR Mid-Cap ETF in October 2024 and the Virtus Silvant Growth Opportunities ETF in 2025, leveraging the investment capabilities of its boutiques in the industry's fastest-growing distribution vehicle.

George Aylward remains at the helm as President and CEO, now in his eighteenth year leading the company through its independence. His total compensation of approximately three point seven million dollars, while significant, is modest by the standards of financial services CEOs running comparably complex organizations. The leadership team has been remarkably stable, with CFO Angerthal, COO Richard Smirl, Head of Distribution Barry Mandinach, and Chief Legal Officer Andra Purkalitis all serving in their roles for many years. This continuity has been a quiet advantage: in an industry where leadership turnover can trigger client and talent departures, Virtus's management stability has provided a foundation of trust for both affiliated boutiques and external stakeholders.

X. The Multi-Boutique Business Model Deep Dive

To truly understand Virtus, you need to understand how the money flows through the machine. At its simplest, Virtus earns investment management fees, a percentage of assets under management charged annually but collected monthly or quarterly. The 2025 revenue breakdown tells the story: of the company's eight hundred thirty-one million dollars in total revenue, seven hundred twenty-five million came from investment management fees. Within that, open-end mutual funds contributed two hundred eighty-seven million, retail separate accounts two hundred ten million, institutional accounts one hundred sixty-eight million, and closed-end funds sixty-one million.

The average fee rate across the platform runs at approximately forty-two basis points, or roughly four-tenths of one percent of assets managed annually. This is meaningfully higher than the industry average for traditional active managers and dramatically higher than the single-digit basis point fees charged by passive index funds. The premium reflects Virtus's concentration in specialized strategies, small and mid-cap equities through Kayne Anderson Rudnick, multi-sector fixed income through Newfleet, event-driven strategies through Westchester, and emerging markets debt through Stone Harbor, where the value of active management is more demonstrable and where passive alternatives are less available or less effective.

The affiliate structure is the architectural innovation that makes the whole thing work. Virtus owns majority or full equity stakes in each of its fifteen-plus boutiques. Each affiliate operates under a management agreement that specifies the revenue-sharing arrangement: the boutique retains a portion of the investment management fees it generates, typically reflecting the costs of its investment team and a profit-sharing component, while Virtus retains the remainder to cover corporate overhead, distribution costs, and profit.

Distribution is perhaps the single most important value-add that Virtus provides to its boutiques. The company employs a large wholesaling force, led by Executive VP Barry Mandinach, that maintains relationships with the broker-dealers, wirehouses, and RIA platforms that control access to the end investor. For a boutique managing five billion dollars in assets, building and maintaining this distribution infrastructure independently would be prohibitively expensive. Through Virtus, they get access to a distribution machine that covers the entire intermediary landscape without having to build it themselves.

Why do boutiques partner with Virtus rather than staying independent or joining competitors? The answer boils down to a simple economic calculation. An independent boutique managing ten billion dollars faces a harsh reality: after paying for compliance, technology, fund administration, back-office operations, marketing, and distribution, the margin on the business can be thin, particularly for smaller firms. By joining Virtus, the boutique founders receive a significant upfront payment for their equity, ongoing revenue sharing that typically exceeds what they could earn independently, and the freedom to focus exclusively on investment management rather than running a small business.

The retention game is equally important. In asset management, the assets follow the people. If a key portfolio manager leaves, their clients often follow, sometimes within weeks. Virtus structures its affiliate agreements with long-term incentive arrangements that keep key personnel financially aligned over multi-year periods. The combination of equity participation, attractive revenue sharing, and operational autonomy creates what management describes as "golden handcuffs" that are both generous and genuinely desired, a critical distinction from the coercive retention structures that have failed at other firms.

The capital-light nature of the business deserves emphasis. Unlike banks, which need massive balance sheets to support lending, or insurance companies, which need reserves to back policies, asset managers need relatively little capital to operate. Virtus's primary assets are its people, its relationships, and its contractual agreements with affiliates. The company's balance sheet carries significant goodwill and intangible assets from past acquisitions, but the ongoing capital requirements of the business are modest, which allows for substantial free cash flow generation relative to revenue.

That said, the model has clear limitations. The reliance on Kayne Anderson Rudnick, which accounts for roughly forty percent of total AUM, creates significant concentration risk. If KAR's investment performance deteriorates, or if key personnel depart, the impact on Virtus would be severe. The multi-boutique structure also creates complexity: each affiliate has its own investment process, risk management framework, and operational needs, which makes the parent company's oversight function more challenging than it would be in a monolithic firm.

XI. Industry Context & Competitive Landscape

The asset management industry has undergone a tectonic shift over the past two decades, and Virtus sits at the intersection of nearly every major trend reshaping the business. On one side, the passive investing revolution has created an oligopoly of mega-managers, BlackRock, Vanguard, and State Street, that together control over twenty trillion dollars in assets and continue to gather the lion's share of net new flows. On the other side, specialized boutiques with genuine investment edge continue to thrive in niches that passive strategies cannot easily replicate. The middle ground, where mid-sized active managers historically lived, has become a killing field.

Virtus's most direct peer is Affiliated Managers Group, or AMG, the firm that essentially invented the multi-boutique model in the 1990s. AMG takes a different approach, typically acquiring minority equity stakes in larger, more established independent managers. AMG's assets under management of approximately eight hundred thirteen billion dollars dwarf Virtus's one hundred fifty-six billion, and its focus on alternatives and private markets is more mature, with private markets and liquid alternatives representing a majority of EBITDA. But AMG has faced its own challenges, including the departure of several high-profile affiliates and questions about whether its minority-stake model provides sufficient control to manage risk effectively.

Victory Capital, trading under the ticker VCTR, represents the more aggressive end of the multi-manager spectrum. Victory operates twelve autonomous investment franchises on a fully integrated centralized operating and distribution platform, combining boutique investment autonomy with industrial-scale operational efficiency. In April 2025, Victory completed a transformative strategic partnership with Amundi, acquiring Amundi's U.S. business, which included the Pioneer Investments brand and approximately one hundred nineteen billion dollars in AUM. Victory's CEO has publicly targeted one trillion dollars in AUM, a level of ambition that makes Virtus look conservative by comparison. With a market capitalization of approximately nine billion dollars, Victory trades at a significant premium to Virtus, reflecting the market's belief in its superior growth trajectory.

Federated Hermes, listed as FHI, is often mentioned in the same breath as Virtus but operates a fundamentally different business. Federated manages approximately nine hundred three billion dollars, a record figure achieved in mid-2025, but more than half of its revenue comes from money market and liquidity assets, a business that bears little resemblance to Virtus's focus on active equity, fixed income, and alternatives. The money market business provides stable, fee-driven revenue with limited market sensitivity, but it also operates at razor-thin margins and is vulnerable to disruption from direct money market access through platforms like Treasury Direct.

Then there are the diversified players, Franklin Templeton and Invesco, that have attempted to compete across virtually every asset class and distribution channel. These firms have the scale and brand recognition that Virtus lacks, but they also carry the organizational complexity and cultural challenges that come with trying to be all things to all investors. Franklin Templeton's acquisition of Legg Mason in 2020 was arguably the largest and most ambitious deal in the multi-boutique space, combining two multi-affiliate platforms into a single entity managing over one point five trillion dollars.

The distribution landscape deserves special attention because it is the single most important competitive battleground in asset management outside of investment performance itself. There are essentially three distribution channels that matter: the wirehouses and broker-dealers that serve high-net-worth individuals, the registered investment advisor channel that has been the fastest-growing segment for a decade, and the institutional consultants that advise pension funds, endowments, and foundations. Virtus has historically been strongest in the intermediary channel, selling through broker-dealers and increasingly through RIA platforms. Its institutional presence, while growing through affiliates like SGA and Stone Harbor, remains a relative weakness compared to larger competitors.

The secular trends shaping the industry are largely unfavorable for traditional active managers, but not uniformly so. Passive growth continues to accelerate, but the explosion of alternative investments, particularly in private credit, infrastructure, and real assets, has created new opportunities for firms with the right capabilities. Fee compression is real and ongoing, but it is most acute in large-cap equity and core fixed income, where Virtus has limited exposure. The consolidation thesis, the idea that the industry will continue to consolidate as smaller managers struggle to achieve viable scale, generally benefits platforms like Virtus that can serve as acquirers.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

The threat of new entrants in asset management is paradoxical. On one hand, starting a boutique investment firm has never been easier: two talented portfolio managers with a Bloomberg terminal and a compliance consultant can launch a hedge fund or separate account business from their living room. The barriers to creating a fund are low. On the other hand, the barriers to building a scaled distribution platform are enormous. Getting on the approved lists at major wirehouses, building relationships with institutional consultants, achieving the AUM thresholds required by major platforms, these take years of effort and millions of dollars in distribution spending. Virtus's value proposition to boutiques is precisely this: it provides the scaled distribution infrastructure that would take a new entrant decades to build.

Supplier power in asset management is uniquely high because the "suppliers" are the investment professionals themselves. In manufacturing, if a supplier raises prices, you can find another supplier. In asset management, if your star portfolio manager leaves, the assets walk out the door with them. This is perhaps the single greatest risk in the multi-boutique model: each boutique is, in essence, a small team of individuals whose departure would immediately destroy value. Virtus mitigates this risk through equity participation, revenue sharing, and cultural autonomy, but the risk can never be fully eliminated.

Buyer power has increased dramatically over the past decade. Institutional investors have become far more sophisticated in evaluating fees, and the rise of fee-based advisory models in the retail channel has created intense pressure on fund expense ratios. Platform access matters enormously; being included on or excluded from a major wirehouse's recommended list can mean billions of dollars in flows. Virtus's distribution team exists precisely to navigate these gatekeepers.

The threat of substitutes is the existential challenge facing the entire active management industry. Passive index funds, direct indexing, factor-based ETFs, and increasingly sophisticated do-it-yourself tools all represent alternatives that are cheaper and, in many cases, deliver comparable or superior long-term returns. Virtus's defense against substitution is specialization: its boutiques operate in niches where passive alternatives are less effective, less available, or non-existent.

Competitive rivalry is intense and increasing. As the total addressable market for traditional active management shrinks, the remaining firms are competing more aggressively for a declining pool of assets. Scale advantages are emerging: larger firms can spread distribution and technology costs across a bigger asset base, reducing per-unit costs and allowing for more competitive fee structures. This dynamic favors consolidation and makes it harder for mid-sized firms like Virtus to compete purely on price.

Hamilton's 7 Powers

Scale economics in asset management are moderate. Distribution and operations benefit from scale, as the cost of maintaining a wholesaling force or a technology platform does not increase linearly with AUM. However, the boutique structure inherently limits scale economies at the investment management level: each boutique remains relatively sub-scale compared to monolithic competitors. The corporate parent captures some scale benefits, but these are partially offset by the revenue-sharing arrangements with affiliates.

Network economics are essentially absent in traditional asset management. Unlike a platform business where each additional user makes the service more valuable to existing users, adding a new client to an investment fund does not meaningfully benefit existing clients. There are weak network effects in distribution, where broader platform coverage can attract more boutiques, which in turn attract more clients, but these effects are modest.

Counter-positioning is moderate. The multi-boutique model positions Virtus differently from monolithic firms, offering a combination of investment specialization and operational scale that traditional competitors cannot easily replicate. However, this positioning is not unique to Virtus; AMG, Victory Capital, and others offer similar value propositions, limiting the defensive value of this particular form of counter-positioning.

Switching costs are moderate for institutional clients, who face search costs, transition costs, and governance hurdles when changing managers, but are low for retail investors, who can redeem from a mutual fund with a phone call or a mouse click. The stickiness of alternative and private credit strategies, where capital is often locked up for longer periods, is one reason Virtus's push into these areas is strategically important.

Branding power is weak at the Virtus corporate level but stronger at the boutique level. Kayne Anderson Rudnick, Stone Harbor, and Westchester Capital have meaningful brand recognition within their respective niches. Few investors, however, choose a fund because it carries the Virtus name, and corporate brand awareness remains limited outside the financial advisor community.

Cornered resources are limited. Investment talent is inherently mobile; portfolio managers can and do leave for competitors or to start their own firms. While Virtus's retention structures are well-designed, they cannot permanently lock in talent the way a patent locks in intellectual property.

Process power is moderate. Virtus has developed a repeatable acquisition playbook, from sourcing and evaluating potential affiliates, to structuring deals with appropriate incentive alignment, to integrating new firms onto the corporate platform. This institutional capability is difficult to replicate quickly and represents a genuine, if modest, competitive advantage.

The overall assessment is sobering for long-term investors. Virtus lacks the kind of deep, durable moats that characterize the best compounding businesses. Its success depends primarily on execution quality, talent retention, acquisition discipline, and market conditions, factors that are difficult to predict and impossible to control. Asset management is ultimately a hits-driven, people-dependent business, and the multi-boutique model, for all its elegance, does not change that fundamental reality.

XIII. Bull vs. Bear Case

Bull Case

The case for Virtus begins with the industry consolidation thesis. As the asset management industry continues to bifurcate between passive giants and specialized active managers, mid-sized firms are being forced to either achieve scale or be acquired. Virtus, with its proven acquisition playbook and established platform infrastructure, is well-positioned to be a consolidator rather than a target. Every boutique that struggles with distribution, compliance, or operational costs is a potential acquisition target, and there are hundreds of them.

The alternatives growth story provides a second pillar. The shift toward alternative investments, particularly private credit, is a secular trend that plays directly to the multi-boutique model's strengths. These strategies command higher fees, generate stickier capital with longer lock-up periods, and face essentially no competition from passive alternatives. Virtus's recent acquisitions of stakes in Crescent Cove and Keystone National Group suggest management is positioning aggressively for this opportunity.

The company's investment performance across many of its boutiques has been strong, with Kayne Anderson Rudnick in particular delivering consistent results in quality-oriented growth equities. When performance is good, organic growth follows, and the compounding effect of positive flows on a fee-based revenue model can be powerful.

Valuation offers another argument. At a market capitalization of roughly eight hundred fifty million dollars, Virtus trades at a notable discount to peers like Victory Capital and Federated Hermes on most conventional metrics. With nearly twenty dollars per share in earnings and a quarterly dividend of two dollars forty cents, the stock offers a dividend yield above seven percent, unusually high for an asset manager of this quality. If the discount to peers narrows, or if a private equity buyer recognizes the value of the platform and takes the company private, significant upside exists from current levels.

Finally, the share buyback program has been a meaningful source of value creation. By reducing diluted shares from seven point six million to six point nine million over three years, management has amplified per-share earnings growth even as top-line revenue has been relatively flat. If this capital allocation discipline continues, it should provide a floor for per-share value creation even in a challenging revenue environment.

Bear Case

The bear case starts with the single most powerful force in modern finance: the relentless shift from active to passive management. This trend shows no signs of abating. In fact, it may be accelerating as a new generation of investors, raised on the gospel of index investing, enters their peak earning and investing years. Every dollar that flows from active to passive is a dollar of potential fee income that Virtus will never see.

Fee compression is destroying margins industry-wide, and Virtus is not immune. The company's average fee rate of approximately forty-two basis points is under constant pressure as competitors cut fees to retain assets and platforms demand more favorable economics. Even a few basis points of fee compression across the platform translates to tens of millions of dollars in lost revenue.

Talent risk is the Achilles' heel of the entire multi-boutique model. The departure of a key portfolio manager or team can cripple an affiliate overnight. Kayne Anderson Rudnick, which accounts for forty percent of total AUM, represents a particularly acute concentration risk. If KAR's leadership team were to depart, or if their investment performance were to deteriorate meaningfully, the impact on Virtus would be severe and potentially irreversible.

Scale disadvantages relative to the mega-managers are real and growing. BlackRock, Vanguard, and Fidelity can spread their technology, distribution, and compliance costs across trillions of dollars in assets, achieving per-unit economics that Virtus cannot match. In an industry where scale advantages are becoming more important, being the smallest publicly traded multi-boutique platform is a vulnerable position.

The dependence on M&A for growth raises sustainability questions. Virtus has executed well on acquisitions historically, but the pipeline of attractive targets is not infinite. As the market for quality boutiques becomes more competitive, with private equity firms, sovereign wealth funds, and larger asset managers all bidding for the same properties, acquisition multiples may rise to levels that make deals less accretive.

Finally, the complexity of the multi-boutique structure makes the true economics somewhat opaque. Revenue-sharing arrangements with affiliates, amortization of intangible assets from acquisitions, and the consolidation of entities with minority interests all make it harder for investors to assess the underlying profitability and sustainability of the business. This complexity can weigh on the stock's valuation multiple.

Key KPIs to Track

For investors monitoring Virtus's ongoing performance, three metrics matter above all others.

First, organic net flow rate: the percentage of beginning-of-period AUM represented by net client flows, excluding the impact of market movements and acquisitions. This is the single best measure of whether the company is winning or losing the battle for investor capital. Positive organic flows indicate that the product lineup, investment performance, and distribution efforts are working; persistent negative flows, as the company has experienced recently, signal that the business is shrinking at its core even if acquisitions mask the decline.

Second, investment management fee rate: the blended average fee earned per dollar of AUM across the entire platform. This metric captures the combined effects of fee compression, mix shift between higher-fee and lower-fee strategies, and the success of the company's push into higher-fee alternatives. A declining fee rate, even with stable AUM, translates directly to lower revenue and narrower margins.

Third, operating margin adjusted for affiliate revenue sharing: the percentage of net revenue (after payments to affiliates) that the corporate parent retains as operating profit. This metric strips out the pass-through economics of the affiliate model and reveals the true profitability of the platform itself, the infrastructure, distribution, and corporate overhead that Virtus provides to its boutiques.

XIV. Playbook: Lessons for Founders & Investors

The Virtus story offers a dozen hard-won lessons, but a few stand out as particularly instructive for founders building businesses and investors evaluating them.

Survival is the first strategy. Virtus was born at the worst possible moment, spun off into the teeth of the worst financial crisis in eighty years, with assets hemorrhaging and no natural shareholder base. Many comparable firms did not survive this period. Virtus did, not through brilliance but through prudence, the Harris Bankcorp capital infusion, the disciplined management team, the patience to wait for markets to recover. In investing and in business, the ability to survive bad periods is often more important than the ability to capitalize on good ones. Warren Buffett's first rule of investing, "don't lose money," applies equally to corporate strategy.

Find your differentiation or die. Virtus could not compete head-on with BlackRock on scale, with Vanguard on fees, or with the largest active managers on brand recognition. Rather than trying to be a slightly smaller version of the giants, Aylward built something structurally different: a federation of specialists united by a common platform. This is the classic strategic insight from Michael Porter: when you cannot win the existing game, change the game.

Alignment matters more than control. The genius of the multi-boutique model, when it works, is that it aligns the interests of the corporate parent with the interests of the boutique investment teams. Equity participation, revenue sharing, and operational autonomy keep the people who generate the value, the portfolio managers and analysts, financially and psychologically invested in the outcome. The corollary is that misalignment, through excessive corporate interference, unfair economic terms, or cultural disrespect, can destroy a boutique faster than any market downturn.

Distribution is the moat, not investment performance. This is a counterintuitive lesson, but it is one of the most important in asset management. There are thousands of talented investment managers in the world who cannot gather meaningful assets because they lack distribution. And there are mediocre managers at large firms who manage enormous pools of capital because they benefit from powerful distribution platforms. The multi-boutique model works because it recognizes this asymmetry: it pairs investment talent, which is abundant, with distribution scale, which is scarce.

Roll-ups require discipline. Not every acquisition works. Cultural fit matters enormously; a boutique that thrives on autonomy will wilt under heavy corporate oversight, and a team that needs structure will flounder without it. Virtus has generally been disciplined about the types of firms it acquires, favoring differentiated strategies with strong performance records and stable teams. The failures in the multi-boutique space, and there have been many, typically result from acquiring teams for the wrong reasons, overpaying, or imposing corporate cultures that drive away the talent that made the acquisition valuable.

Pivot toward secular trends. Virtus's shift toward alternatives and private credit may prove to be the most important strategic decision of Aylward's tenure. The company recognized that the traditional active equity and fixed income businesses were facing structural decline and moved aggressively toward asset classes with stronger secular tailwinds. This kind of strategic pivot is easy to describe but extraordinarily difficult to execute, particularly in a multi-boutique model where each affiliate has its own inertia and preferences.

Capital allocation separates the winners. Asset managers generate substantial free cash flow relative to their capital requirements, which means the quality of capital allocation decisions, dividends versus buybacks versus acquisitions versus debt reduction, has an outsized impact on long-term shareholder returns. Virtus's combination of significant share buybacks, a generous dividend, and selective acquisitions has been a reasonable approach, though the elevated debt levels from past acquisitions remain a point of concern.

XV. Epilogue & Future Outlook

As of March 2026, Virtus Investment Partners stands at a crossroads that is both specific to the company and emblematic of the broader active management industry. The questions facing George Aylward and his team are the same ones that confront every mid-sized active manager: In a world increasingly dominated by passive giants and alternative asset mega-firms, is there a sustainable middle ground?

The optimistic scenario envisions Virtus as a consolidation platform that continues to attract high-quality boutiques, expands its alternatives and private credit capabilities, and benefits from the generational wealth transfer that is expected to channel trillions of dollars through the RIA channel over the next decade. The company's established distribution relationships, proven acquisition playbook, and portfolio of differentiated investment strategies provide a solid foundation for this outcome.

The pessimistic scenario sees the inexorable shift toward passive investing continuing to erode the company's traditional active equity and fixed income businesses, with alternatives growth insufficient to offset the decline. In this world, Virtus's AUM continues to shrink through net outflows, fee compression squeezes margins, and the stock price drifts lower until the company itself becomes an acquisition target for a larger platform.

The macro environment adds layers of uncertainty. Interest rates remain elevated relative to the post-2008 era, creating both opportunities and challenges for fixed income managers. Market volatility has increased, which generally benefits active managers who can navigate turbulent markets but also increases the risk of AUM-destroying drawdowns. The retirement crisis, as millions of Americans face the prospect of inadequate savings, could drive demand for the kind of outcome-oriented, risk-managed strategies that some Virtus boutiques specialize in.

Technology disruption looms as both a threat and an opportunity. Artificial intelligence and machine learning are transforming investment research, portfolio construction, and risk management, creating the possibility that some of the human judgment currently provided by boutique teams could be automated. At the same time, AI tools could make smaller teams more productive, potentially strengthening the boutique model by allowing small teams to punch above their weight. The rise of direct indexing, which allows individual investors to own customized baskets of securities rather than mutual funds, represents a structural threat to the mutual fund business that has been Virtus's core distribution vehicle.

Could Virtus itself become an acquisition target? At a market capitalization of roughly eight hundred fifty million dollars, the company is squarely in the range that private equity firms have historically found attractive for asset management take-privates. The high free cash flow generation, predictable revenue streams, and potential for operational improvements make it a classic PE candidate. Whether the current management and board would be receptive to such an approach is an open question, but the financial characteristics of the business argue that it would attract serious interest at the right price.

What would success look like in 2030? Perhaps it means Virtus has grown AUM back above two hundred billion dollars through a combination of organic growth, market appreciation, and selective acquisitions. Perhaps it means the alternatives platform has grown to fifty billion dollars or more, with private credit, infrastructure, and real assets representing a meaningful share of revenue. Perhaps it means the company has been taken private, with a PE sponsor providing the capital and strategic patience to accelerate the transformation. Or perhaps it means Virtus has been acquired by a larger platform, with its boutiques absorbed into a bigger ecosystem that offers even greater distribution reach.

The challenge of building enduring value in asset management has never been greater. The industry's fundamental economics, fee-based revenue tied to volatile markets, dependence on mobile human talent, and relentless competition from passive alternatives, make it one of the most difficult businesses in which to compound value over long periods. Virtus's story, from temperance insurance in 1851 to multi-boutique platform in 2026, is a testament to both the possibilities and the perils of this endeavor. The next chapter has yet to be written, but the authors, a small team in Hartford and fifteen boutiques scattered across the country, have shown they know how to adapt, survive, and build. Whether that is enough in the years ahead remains the central question for anyone evaluating Virtus Investment Partners.

XVI. Further Reading & Resources

Books:

-

The Hedge Fund Mirage by Simon Lack, a bracingly honest look at the economics of asset management and who actually captures the returns generated by investment firms.

-

Invested by Charles Schwab, chronicling the transformation of the brokerage and investment industry from a pioneer who reshaped how Americans invest.

-

More Money Than God by Sebastian Mallaby, a comprehensive history of the hedge fund industry and the alternative investment strategies that Virtus is increasingly pursuing.

-

The Man Who Solved the Market by Gregory Zuckerman, the story of Jim Simons and Renaissance Technologies, illustrating what a truly successful boutique investment firm looks like at the extreme end of the spectrum.

Long-Form Reading:

-

Virtus Investment Partners annual letters and investor presentations (2015-present), available on the company's investor relations website, provide management's own perspective on strategy and performance.

-

Research papers on the multi-boutique model, comparing AMG, Virtus, and Victory Capital, offer academic perspectives on whether this organizational structure creates or destroys value.

-

SEC filings, particularly Virtus's 10-K annual reports, contain detailed information on acquisition structures, affiliate agreements, and revenue-sharing arrangements that are essential for understanding the true economics of the business.

-

Morningstar and Lipper fund performance reports for boutique track records provide the investment performance data that ultimately drives the company's organic growth or decline.

-

Industry reports from Cerulli Associates and McKinsey on asset management trends offer the macro context necessary for evaluating Virtus's competitive position.

-

The ongoing debates about the viability of active management, documented across academic journals, industry publications, and financial media, provide the intellectual backdrop for the most fundamental question facing Virtus and its peers.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube