Vertiv Holdings: The Infrastructure Behind the AI Revolution

I. Introduction & Episode Setup

Picture this: December 31st, 2023. As Wall Street traders pack up for New Year's Eve, one stock sits atop the S&P 500 leaderboard with a jaw-dropping 252% annual return. Not Nvidia. Not Meta. Not even Tesla during one of its legendary runs. The winner? A company most investors had never heard of—Vertiv Holdings, symbol VRT.

Here's the kicker: while everyone was obsessing over AI chips and large language models, this 78-year-old company from Columbus, Ohio was quietly selling the picks and shovels for the entire AI gold rush. Every time ChatGPT processes a query, every time a Tesla trains its Full Self-Driving neural net, every time a hyperscaler builds another data center—Vertiv's equipment is there, keeping the servers cool and the power flowing. Vertiv Holdings is an American multinational provider of critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments. The company designs, manufactures, and services the critical infrastructure that keeps the digital economy running—primarily under the Vertiv, Liebert, NetSure, Geist, Energy Labs, ERS, Albér, and Avocent brands.

Think of Vertiv as the company that builds the foundation upon which the entire AI revolution stands. While Nvidia makes the GPUs and OpenAI trains the models, Vertiv ensures those billions of transistors don't melt into silicon soup. It's the ultimate infrastructure play—boring, essential, and suddenly very, very profitable.

What makes this story particularly fascinating is how a company founded in a Columbus garage in 1946 to cool mainframe computers positioned itself at the center of the AI infrastructure boom nearly 80 years later. This isn't just a story about cooling systems and power management. It's about how patient capital, strategic positioning, and perfect timing can transform an industrial workhorse into a tech darling.

Over the next several hours, the story unpacks how Ralph Liebert's insight about computer heat became a multibillion-dollar business, why Emerson Electric spent 16 years building then divesting this asset, how a Goldman Sachs SPAC deal created unexpected value, and most importantly, why the AI revolution has made Vertiv's products not just useful, but absolutely mission-critical.

The story explores the physics of why AI changes everything for data center infrastructure, dives deep into the liquid cooling revolution that's reshaping the industry, and examines whether Vertiv's explosive growth is sustainable or if this is another infrastructure bubble. Along the way, it extracts lessons about infrastructure investing, the power of being technology-agnostic, and why sometimes the best tech investments have nothing to do with software.

II. Origins: From a Garage in Columbus to Computer Cooling Pioneer

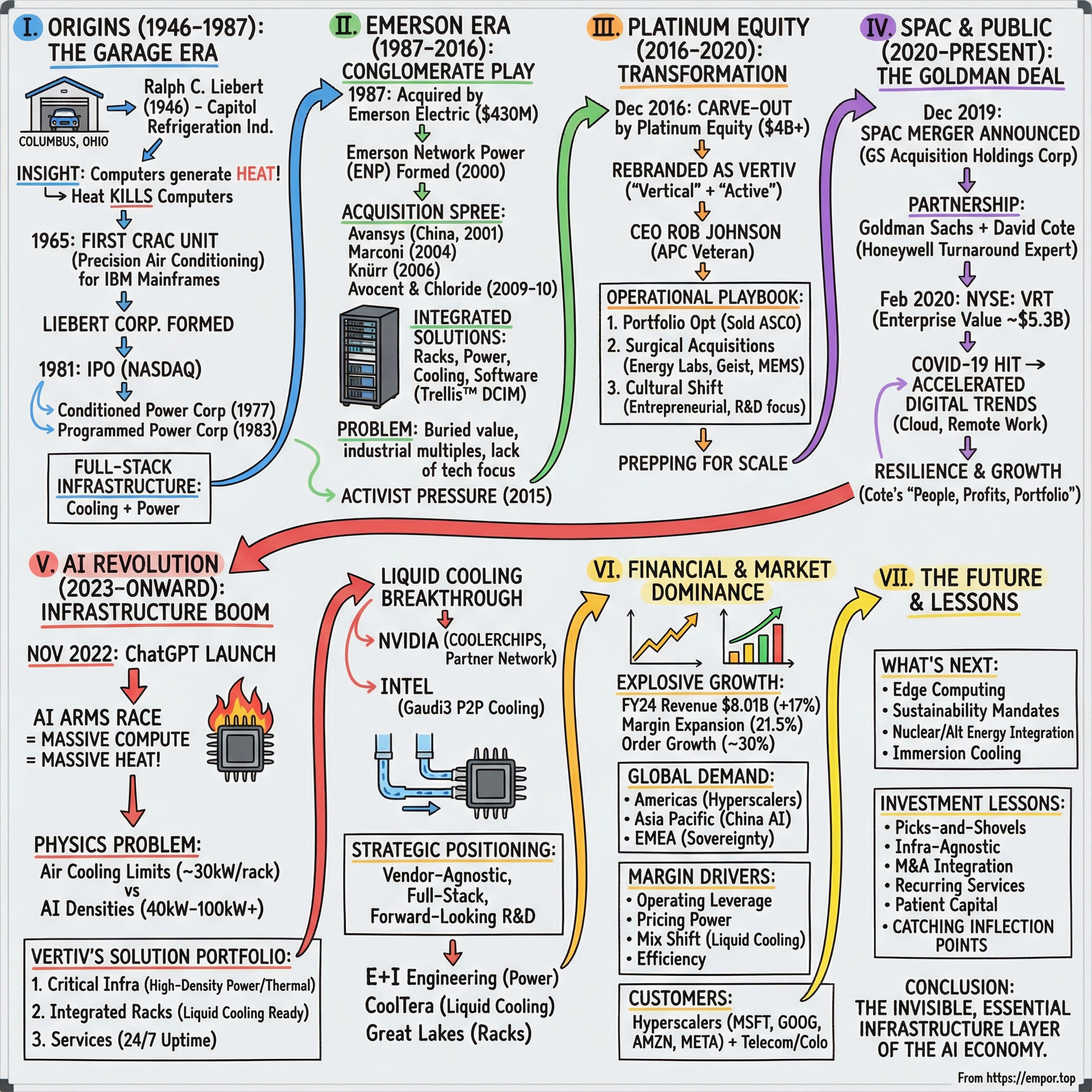

The story begins in 1946, in a modest garage in Columbus, Ohio. World War II had just ended, and America was transitioning from military production to civilian innovation. Ralph C. Liebert (1918-1984), a young engineer with a refrigeration background, founded Capitol Refrigeration Industries and began developing the first prototype precision air conditioner in his garage.

But Liebert wasn't building just another air conditioner. He was obsessed with a problem that most people didn't even know existed yet: the delicate thermal requirements of the emerging computer age. While others saw computers as calculating machines, Liebert saw them as heat generators—expensive, temperamental heat generators that would fail catastrophically if their environment wasn't precisely controlled.

For nearly two decades, Liebert refined his invention, waiting for the market to catch up to his vision. The breakthrough came in early 1965—a moment that would transform both his company and the entire computing industry. The prototype was introduced to IBM in Chicago, and recognizing the machine's potential, IBM arranged for Liebert to debut his invention at the World Computer Conference in Philadelphia.

This wasn't just a product demonstration; it was a revelation. In 1965, Liebert Corporation was formed as the industry's first manufacturer of computer room air conditioning (CRAC) units. These weren't your typical window units or industrial coolers. Liebert CRAC systems were the first totally redundant, self-contained units capable of maintaining air temperature, humidity and air quality within the precision tolerances necessary for media and equipment used in computer rooms, taking advantage of the raised floor plenums typically found in such rooms.

The fundamental insight was elegant in its simplicity but revolutionary in its implications: computers generate heat, and heat kills computers. As mainframes grew more powerful, they generated more heat. As they generated more heat, they became more vulnerable to failure. And as businesses became more dependent on these machines, any failure became catastrophically expensive.

Liebert's solution addressed not just temperature but the entire environmental equation. Humidity control was equally critical—too dry and you'd get static discharge that could fry circuits; too humid and you'd get condensation that could short systems. The precision required was extraordinary: temperature variations of just a few degrees or humidity swings of 5-10% could mean the difference between reliable operation and system failure.

The market response was explosive. The company enjoyed double-digit growth in this market niche during the next several decades. Every bank installing a mainframe, every insurance company building a data center, every government agency computerizing its operations—they all needed Liebert's precision cooling systems.

By the late 1970s, Liebert had expanded beyond just cooling. In 1977, Liebert launched sister company Conditioned Power Corporation to design and manufacture power distribution, conditioning and monitoring systems for the data processing industry. This wasn't mission creep—it was strategic integration. The same customers who needed precision cooling also needed clean, uninterrupted power.

In 1981, the company became a public company via an initial public offering on the NASDAQ. In 1983, the company acquired Programmed Power Corporation from Franklin Electric, expanding the capabilities of the company's power division to include the design and manufacture of uninterruptible power supplies.

The company was now a full-stack infrastructure provider, offering everything needed to keep computer rooms operational. But Ralph Liebert wouldn't live to see the full fruition of his vision. He passed away in 1984, leaving behind a company that had fundamentally shaped how the world thought about computer infrastructure.

In 1980, Larry L. Liebert (1945-2023), Ralph's son, took over management of the company. Under the younger Liebert's leadership, the company continued its expansion, opening international facilities and broadening its product line. In 1985, the company organized its Liebert Global Services division and introduced SiteScan, its site management system.

But the biggest change was yet to come. The personal computer revolution was beginning to transform computing from centralized mainframes to distributed networks. The internet was emerging from academic laboratories. And a much larger player had taken notice of Liebert's strategic position in this evolving ecosystem.

III. The Emerson Era: Building a Conglomerate Play

In 1987, Liebert Corporation was acquired by Emerson Electric for $430 million in stock. For a company that had started in a garage just 41 years earlier, this represented a spectacular outcome. But for Emerson Electric, the St. Louis-based industrial conglomerate, Liebert was more than just another acquisition—it was a cornerstone for an ambitious vision of the digital future.

Emerson saw what others missed: as computing moved from specialty applications to the heart of every business, the infrastructure supporting those computers would become mission-critical. They weren't buying a cooling company; they were buying a position in the emerging digital infrastructure market. Under Emerson's ownership, Liebert retained its brand identity but became part of something much larger. For the first 13 years under Emerson, Liebert operated as a wholly owned subsidiary, maintaining its entrepreneurial culture while benefiting from the resources of a Fortune 500 company.

In 2001, Emerson made two key moves in the fast-growing Asian markets, purchasing Avansys, China's leading network power provider, and forming Emerson Network Power India Private Ltd. This acquisition was particularly strategic—Avansys gave Emerson direct access to China's booming telecommunications and internet infrastructure market, a market that would soon become the world's largest.

The real transformation came in 2000, when Emerson consolidated its network and computer protection businesses to form its Emerson Network Power (ENP) platform group. This wasn't just a reorganization—it was a fundamental reimagining of how infrastructure products should be delivered to market. Instead of selling cooling, power, and monitoring as separate products, ENP would offer integrated solutions for the entire data center stack.

The acquisition spree accelerated. ENP expanded its telecom industry solutions with the 2004 acquisition of Marconi outside plant and power system. In 2006, ENP acquired Germany-based Knürr, a provider of enclosure systems. Each acquisition added another piece to the puzzle—racks, enclosures, monitoring software, power distribution units.

The crown jewels came in 2009 and 2010. Emerson strengthened with two major acquisitions: Avocent Corporation, a leader in delivering solutions that enhance companies' integrated data center management capabilities and Chloride, which provides commercial and industrial uninterruptible power supply systems and services. Avocent brought KVM switches and IT management systems. Chloride, a British company with a 100-year history, brought industrial-grade UPS systems and a strong European presence.

By 2011, Emerson Network Power had become a juggernaut. Emerson introduced the Trellis™ platform, the first data center infrastructure management (DCIM) hardware and software package that could control a complete array of data center equipment and IT resources from a single console. This was the holy grail of data center management—a single pane of glass to monitor and control everything from cooling to power to server utilization.

The portfolio now included industry-leading flagship brands: ASCO® (automatic transfer switches), Chloride® (UPS systems), Liebert® (cooling and power), NetSure™ (DC power systems), and Trellis™ (infrastructure management software). The company could outfit an entire data center from the ground up, providing everything except the servers themselves.

But here's where the story takes an unexpected turn. Despite this impressive portfolio, despite the strategic positioning, despite the growing importance of data centers—Emerson Network Power was struggling to get the respect it deserved from investors. Buried within Emerson Electric's sprawling conglomerate structure, ENP's growth story was obscured by slower-growing industrial businesses. The market valued Emerson as an industrial company trading at industrial multiples, not as a technology infrastructure play.

By 2015, activist investors were circling. They saw what Emerson's management was slowly coming to realize: Network Power was worth more outside of Emerson than within it. The business needed focus, investment, and most importantly, a story that Wall Street could understand and value appropriately.

The stage was set for one of the most significant carve-outs in technology infrastructure history.

IV. The Platinum Equity Deal: Liberation and Transformation

On December 1, 2016, the deal closed. Platinum Equity acquired the business from Emerson in a transaction valued in excess of $4 billion, with Emerson retaining a subordinated interest. The company was immediately rebranded as Vertiv—a name meant to evoke both "vertical" (as in vertical markets) and "active" (suggesting dynamism and energy).

But the real story wasn't the name change. It was the CEO.

Rob Johnson, most recently an operating partner at Kleiner Perkins Caufield & Byers, spent 10 years at American Power Conversion (APC), a leader in data center infrastructure. In 1989, Rob founded and led Systems Enhancement Corporation, a company that created innovative software and hardware solutions for the data center industry. He sold the company to American Power Conversion (APC) in 1997 at which point he became general manager of APC. After his promotion to CEO, Rob eventually managed the company's sale to Schneider Electric for $6.1 billion in 2007.

Johnson brought something crucial to Vertiv: credibility. Here was someone who had built a data center infrastructure company from scratch, sold it to a major player, then successfully integrated it into a larger organization before orchestrating one of the industry's biggest exits. He understood the technology, the customers, and most importantly, how to create value in this market.

As Johnson put it, "It's a fresh start for a business that already has so much going for it." As an independent company, Vertiv would operate with great freedom to make business strategy and investment decisions, move more quickly like a startup, and focus on innovative solutions for customers, including those in the growing cloud computing, mobile, and IoT networks.

Platinum Equity's playbook was classic private equity, but with a twist. Unlike financial engineers who simply cut costs and lever up, Platinum specialized in operational transformation. Tom Gores, Platinum's Chairman and CEO, made their intentions clear: "I'm very proud of the relationship and mutual trust that the Emerson and Platinum Equity teams have built with one another. Emerson is a world class company that we know shares our commitment to creating value, and this is an important investment in a business that will be a cornerstone in our portfolio. It plays to our core strengths. In addition to our capital resources, we will deploy our global operations skills to build on the foundation Emerson created and take this business to another level."

The transformation began immediately. First came portfolio optimization. In 2017, Vertiv sold its ASCO power switch business to Schneider Electric for $1.25 billion—a strategic divestiture that both raised capital and eliminated a non-core asset. This was Johnson's APC playbook in reverse: instead of being acquired by Schneider, he was selling to them.

Then came the acquisitions. The company made three acquisitions in 2018: Energy Labs, Geist and MEMS. Energy Labs brought advanced battery monitoring technology. Geist added intelligent rack PDUs and environmental monitoring. MEMS (Motion Energy Management Systems) provided kinetic energy recovery systems. Each acquisition was surgical, adding specific capabilities that Vertiv's hyperscaler customers were demanding.

But the real genius of the Platinum era was the cultural transformation. For 16 years under Emerson, Network Power had operated like a division of a conglomerate—slow, bureaucratic, focused on quarterly earnings. Under Platinum, Vertiv operated like a growth company—fast, entrepreneurial, focused on winning customers and building products.

The company invested heavily in R&D, particularly in liquid cooling technologies that would become critical for AI workloads. They streamlined the supply chain, improved manufacturing efficiency, and most importantly, got closer to customers. Johnson personally visited major hyperscalers, understanding their roadmaps and aligning Vertiv's development to stay ahead of their needs.

The results were impressive. Revenue grew from $4.4 billion in 2016 to nearly $5 billion by 2019. Margins expanded. Customer satisfaction improved. The company was ready for its next transformation.

But Johnson and Platinum had an even bigger vision. The infrastructure market was consolidating. The hyperscalers were concentrating spending. The edge computing revolution was beginning. To capture these opportunities, Vertiv needed scale, capital, and most importantly, a currency for acquisitions.

It was time to go public. But this wouldn't be a traditional IPO. The market conditions weren't right, and the timeline was too long. Instead, they would take a different path—one that would bring in not just capital, but operational expertise from one of the most successful industrial executives of the modern era.

V. Going Public via SPAC: The Goldman Sachs Deal

The announcement came on December 10, 2019: Vertiv would go public through a merger with GS Acquisition Holdings Corp (NYSE: GSAH), a special purpose acquisition company co-sponsored by an affiliate of The Goldman Sachs Group, Inc. and David M. Cote.

David Cote wasn't just any SPAC sponsor. This was the legendary CEO who had transformed Honeywell from a troubled conglomerate into an industrial powerhouse during his 16-year tenure from 2002 to 2017. Under his leadership, Honeywell's market cap had grown from $20 billion to over $120 billion. He understood operational excellence, he understood industrial technology, and perhaps most importantly, he understood how to create shareholder value.

As Cote put it: "Platinum Equity, Rob Johnson and his team have done a tremendous job over the last several years positioning Vertiv for long-term success. The Company is exactly the asset we were looking for, with a great position in a good industry, products differentiated by technology, strong organic and inorganic growth potential, and opportunities for sustained improvements over time."

The deal structure was complex but elegant. The transaction valued Vertiv at approximately $5.3 billion enterprise value, or 8.9x the company's estimated 2020 pro forma Adjusted EBITDA of approximately $595 million. Goldman's SPAC had raised $690 million in its IPO, but the real firepower came from a massive $1.239 billion PIPE (private investment in public equity) that brought in institutional investors at $10 per share.

The ownership structure post-transaction would see Platinum Equity retain approximately 38% of the company—a significant stake that aligned their interests with public shareholders. The deal's sponsors, including Cote and affiliates of The Goldman Sachs Group, would own approximately 5%. The remaining ownership would be distributed among PIPE investors and public shareholders.

Rob Johnson continued as CEO, while Cote served as Executive Chairman, bringing his operational expertise and public market credibility to the board. This wasn't a financial engineering play—it was a strategic combination of operational excellence and growth capital.

The timing seemed perfect. The deal was announced in December 2019 and was expected to close in Q1 2020. Data center demand was accelerating. 5G deployments were beginning. Edge computing was emerging. The hyperscalers were ramping capital spending.

Then COVID-19 hit.

The combination was approved by GS Acquisition Holdings Corp shareholders on February 6, 2020. On February 10, 2020, Vertiv began trading on the NYSE under the ticker VRT. The timing couldn't have been worse—or so it seemed. Within weeks, the world would shut down, markets would crash, and every assumption about the future would be questioned.

But here's where the story takes an unexpected turn. While the pandemic created short-term chaos, it accelerated the exact trends that Vertiv was positioned to capture. Remote work drove cloud adoption. Digital transformation accelerated by years. Data center construction, far from slowing, actually accelerated as hyperscalers scrambled to add capacity.

As Rob Johnson noted: "Today marks an important milestone in Vertiv's history, as we enter the public markets well positioned to create shareholder value and capture the growth opportunities we see on the horizon. This is possible thanks to the hard work of everyone at Vertiv, the fantastic customers we have the good fortune to work with, the partnership of Dave Cote and Goldman Sachs, and Platinum Equity's support over the past few years."

The stock initially struggled, falling below $10 as the market panicked. But Cote's steady hand and Johnson's operational execution began to show results. By focusing on what Cote called "people, profits and portfolio," Vertiv navigated the pandemic while positioning for the recovery.

The company didn't just survive—it thrived. Orders began accelerating in the second half of 2020. Margins expanded despite supply chain challenges. Most importantly, Vertiv began winning major hyperscaler contracts that would drive growth for years to come.

By early 2021, the stock had doubled from its SPAC price. But this was just the beginning. The real catalyst was still to come: the AI revolution that would transform data centers from storage facilities into computational powerhouses, and make Vertiv's cooling and power solutions not just important, but absolutely critical.

VI. The Modern Portfolio: Riding the AI Wave

By 2023, the data center landscape had fundamentally changed. ChatGPT had launched in November 2022, setting off an AI arms race that would transform every aspect of computing infrastructure. Suddenly, the challenge wasn't just keeping servers cool—it was managing heat densities that would have been unimaginable just years earlier.

In May 2023, Vertiv was selected by Nvidia after securing a $5m grant from ARPA-E's COOLERCHIPS program. Their joint objective over the next three years is to address the challenge of cooling high-density compute by integrating direct liquid cooling and immersion cooling into a single system. This wasn't just another partnership—it was a recognition that the future of AI computing would require completely reimagining data center infrastructure.

The physics problem was stark. Traditional air cooling works up to about 30 kilowatts per rack. Beyond that, air simply can't move heat fast enough. But AI workloads were pushing rack densities to 40kW, 60kW, even 100kW and beyond. Nvidia's latest H100 GPUs consumed 700 watts each. Stack eight of them in a DGX system, add networking and other components, and you're looking at heat densities that would literally melt traditional infrastructure.

Vertiv's solution portfolio had evolved to meet this challenge across three critical dimensions:

Critical Infrastructure & Solutions: The company's AC and DC power management systems now handled power densities that would have blown circuits just years earlier. Their thermal management products evolved from simple CRAC units to sophisticated liquid cooling systems. And their integrated modular solutions allowed hyperscalers to deploy entire AI clusters as pre-configured units.

Integrated Rack Solutions: These weren't just metal frames to hold servers. Vertiv's racks incorporated single-phase UPS systems, intelligent power distribution, and most critically, liquid cooling manifolds and cold plates. A single rack could now handle what would have required an entire room of equipment just a decade earlier.

Services & Spares: With AI workloads, downtime wasn't just expensive—it could mean falling behind in the AI race. Vertiv's services division provided preventative maintenance, acceptance testing, engineering and consulting, and 24/7 remote monitoring. With over 300 service centers and more than 4,000 service field engineers globally, they could respond to issues anywhere, anytime.

But the real breakthrough was liquid cooling. In December 2023, Vertiv announced its collaboration with Intel to provide pumped two-phase (P2P) liquid cooling infrastructure for the Gaudi3 AI accelerator. The liquid cooled solution has been tested up to 160kW accelerator power using facility water from 17°C up to 45°C (62.6°F to 113°F).

Think about that for a moment: 160 kilowatts from a single accelerator. That's enough power to run about 100 homes. All concentrated in a chip the size of a dinner plate. And Vertiv's cooling system could handle it using relatively warm water—no need for expensive chillers or exotic cooling fluids.

The technology behind this was sophisticated. Pumped two-phase cooling uses the phase change from liquid to vapor to absorb massive amounts of heat. It's the same principle as sweating, but engineered to nanometer precision. The coolant flows directly over the chip, absorbs heat, partially vaporizes, then gets pumped to a condenser where it releases the heat and returns to liquid form.

In March 2024, Vertiv joined the Nvidia Partner Network (NPN) as a Solution Advisor: Consultant partner. This formalized a relationship that had become critical for both companies. Nvidia CEO Jensen Huang directly cited the partnership: "New data centers are built for accelerated computing and generative AI with architectures that are significantly more complex than those for general-purpose computing. With Vertiv's world-class cooling and power technologies, Nvidia can realize our vision to reinvent computing and build a new industry of AI factories".

The concept of "AI factories" was revolutionary. These weren't traditional data centers that happened to run some AI workloads. These were purpose-built facilities designed from the ground up to support massive parallel processing for AI training and inference. And every aspect—from power distribution to cooling to rack design—had to be reimagined.

Vertiv's strategic positioning was brilliant. While competitors focused on either power or cooling, Vertiv offered the complete stack. Their recent acquisitions now made perfect sense. In 2021, Vertiv acquired E+I Engineering, a global provider of switchgear, busway and modular power solutions, for $1.8 billion—giving them the power distribution capabilities needed for AI-scale deployments.

In December 2023, Vertiv acquired CoolTera Ltd, a provider of coolant distribution infrastructure for data center liquid cooling technology, strengthening its thermal management portfolio for high-density compute cooling requirements. In July 2025, Vertiv announced a $200 million agreement to acquire Great Lakes Data Racks & Cabinets, a manufacturer of customized data rack enclosures, seismic cabinets, and cable management systems.

Each acquisition added a piece to the puzzle. Together, they created an integrated solution that could take power from the grid, distribute it to AI accelerators, cool those accelerators, and manage the entire system through sophisticated software—all from a single vendor.

The customer list read like a who's who of the digital economy: Vertiv's major customers include Alibaba, America Movil, AT&T, China Mobile, Equinix, Ericsson, Siemens, Telefonica, Tencent, Verizon and Vodafone. But increasingly, the big hyperscalers—Microsoft, Google, Amazon, Meta—were driving the most demanding requirements.

Vertiv's approach was to stay one GPU generation ahead of Nvidia. While Nvidia was shipping H100s, Vertiv was already designing cooling for the next generation. While others were figuring out 40kW racks, Vertiv was testing 100kW+ configurations. This forward-looking approach created a powerful moat—by the time competitors caught up to current requirements, Vertiv was already solving next year's problems.

The AI boom had transformed Vertiv from an industrial infrastructure company into a critical enabler of the AI revolution. Every large language model trained, every image generated, every autonomous vehicle simulation—they all ran on infrastructure that Vertiv helped design, build, and maintain.

VII. Financial Performance & Market Position

The numbers tell a story of explosive growth meeting operational excellence. Fourth quarter 2024 net sales of $2,346 million, 26% higher than fourth quarter 2023. Fourth quarter diluted EPS of $0.38 and adjusted diluted EPS of $0.99, up 77% from fourth quarter 2023. Full Year 2024 Revenue reached $8.01 billion, up 17% from FY 2023.

But the headline numbers only tell part of the story. The real revelation is in the margin expansion. Adjusted operating margin expanded to 21.5% in the fourth quarter 2024 compared to fourth quarter 2023, driven by strong volume growth, favorable commercial execution and manufacturing and procurement productivity benefits. For a company that was generating mid-teen margins just a few years ago, this represented a fundamental transformation in profitability.

The order book tells the forward-looking story. Organic orders (excluding foreign exchange) for the TTM period ended December 2024 were up ~30% compared to the December 2023 TTM period, driven by strength in the hyperscale and colocation data center market. Pipeline increased sequentially from third quarter 2024 reflecting strength in data center project activity.

Think about what 30% organic order growth means in context. This isn't a small software startup doubling revenue from a tiny base. This is an $8 billion revenue company growing orders at 30% annually. That's adding roughly $2.4 billion in new orders each year—equivalent to adding a Fortune 1000 company worth of business annually.

The geographic and segment breakdown reveals the global nature of the AI infrastructure boom:

Americas Region: The largest and fastest-growing segment, driven by hyperscaler investments in AI infrastructure. The U.S. alone accounts for the majority of global AI compute capacity, and Vertiv is capturing a significant share of this investment.

Asia Pacific: Particularly strong in China, where domestic AI development is driving massive infrastructure investment. Despite geopolitical tensions, the fundamental need for cooling and power transcends borders.

EMEA (Europe, Middle East, Africa): Growing rapidly as European regulations around data sovereignty drive local data center construction, and Middle Eastern countries invest oil revenues in becoming AI hubs.

The customer concentration story is both a risk and an opportunity. On one hand, having major customers like the hyperscalers creates concentration risk. On the other hand, these are some of the most financially strong, fastest-growing companies in the world. When Microsoft announces $50 billion in annual capex for AI infrastructure, a significant portion flows to companies like Vertiv.

But what's really driving the margin expansion? Several factors:

Operating Leverage: As volumes increase, fixed costs get spread over a larger revenue base. Every additional cooling unit or power system sold drops incrementally more profit to the bottom line.

Pricing Power: In a supply-constrained environment where delivery times for critical infrastructure stretch months, Vertiv can command premium prices. When a hyperscaler needs cooling for a new AI cluster, waiting isn't an option.

Mix Shift: The move toward higher-value liquid cooling solutions and integrated systems drives higher margins than traditional air cooling and standalone products. A liquid cooling system for an AI cluster can cost millions versus hundreds of thousands for traditional cooling.

Manufacturing Efficiency: Investments in automation and lean manufacturing are paying off. Vertiv has approximately 5% of sales into research and development—in 2024, that meant $352.1 million in R&D spending.

Service Attachment: High-margin service contracts that come with equipment sales. When you're cooling $100 million worth of GPUs, the service contract becomes non-negotiable.

The balance sheet had also transformed. From the leveraged structure coming out of the Platinum acquisition, Vertiv had dramatically improved its financial position. Cash generation was strong, debt levels were manageable, and the company had the financial flexibility to continue investing in growth.

The working capital dynamics were particularly interesting. In a normal business, rapid growth consumes cash as you build inventory and extend credit to customers. But Vertiv's position was so strong that customers were actually pre-paying for equipment to secure allocation. This created negative working capital dynamics—growth was actually generating cash rather than consuming it.

Looking at competitive positioning, Vertiv competed primarily with Schneider Electric, Eaton, Legrand and Huawei. But the competitive dynamics had shifted. While these were formidable competitors with strong positions in traditional data center infrastructure, Vertiv had established a clear leadership position in high-density liquid cooling for AI workloads.

The moat was widening. Each successful deployment with a hyperscaler created reference-ability that helped win the next deal. Each generation of GPU that Vertiv successfully cooled added to their knowledge base. The R&D investments were creating proprietary technologies that would take competitors years to replicate.

"Data centers are crucial for meeting the world's digital demands," said Giordano Albertazzi, Vertiv's Chief Executive Officer. "Vertiv's commitment to customer collaboration and innovation is setting the pace for what's possible. But there's still more to be done. Efficiency of compute has always been core to the industry. As technology advances to unlock the full potential of AI applications, it becomes more broadly accessible to everyone. With that accessibility comes a broader, more pervasive use of AI technology which we believe would generate more data and therefore require more data centers. As a result, I am confident in the growth trajectory of Vertiv, and we are reaffirming the five-year financial framework we presented at our investor event last November."

The five-year framework suggested continued robust growth, margin expansion, and cash generation. But even these optimistic projections might prove conservative if AI adoption continues to accelerate at current rates.

VIII. The AI Infrastructure Boom: Timing, Technology & TAM

The AI revolution isn't just changing software—it's fundamentally rewiring the physical infrastructure of the digital economy. Every ChatGPT query, every Midjourney image, every autonomous driving simulation requires massive computational power. And with great computational power comes great heat.

The physics are unforgiving. Modern AI workloads are driving rack densities into three- and four-digit kilowatts. A single rack consuming 100kW generates as much heat as 70 residential space heaters running simultaneously. Stack hundreds of these racks in a data center, and you're dealing with heat output measured in megawatts.

Traditional cooling simply can't handle this. Air has low heat capacity—it takes enormous volumes moving at high speeds to remove significant heat. At densities above 30kW per rack, air cooling becomes impractical. The fans required would consume more power than the servers themselves, and the noise would be deafening. The total addressable market is staggering. Capital spending on procurement and installation of mechanical and electrical systems for data centers is likely to exceed $250 billion by 2030, according to McKinsey estimates. But even this might be conservative. Data centers equipped to handle AI processing loads are projected to require $5.2 trillion in capital expenditures, while those powering traditional IT applications are projected to require $1.5 trillion in capital expenditures. Overall, that's nearly $7 trillion in capital outlays needed by 2030.

McKinsey's analysis of current trends suggests that global demand for data center capacity could rise at an annual rate of between 19 and 22 percent from 2023 to 2030 to reach an annual demand of 171 to 219 gigawatts (GW). To put that in perspective, 219 gigawatts is roughly equivalent to the entire power generation capacity of Germany.

The hyperscalers are leading this charge. Cloud service providers (CSPs) such as Amazon Web Services, Google Cloud, Microsoft Azure, and Baidu are the companies fueling most of today's incremental demand for AI-ready data centers. That's because of the capacity these hyperscalers require to run large foundational models developed in-house, such as Google's Gemini, or to host models developed by AI companies, such as OpenAI's ChatGPT.

Worldwide data center capex was forecast to grow at a CAGR of 21 percent by 2029. Accelerated servers for AI training and domain-specific workloads could represent nearly half of data center infrastructure spending by 2029. The top four U.S.-based cloud service providers—Amazon, Google, Meta, and Microsoft—were expected to account for nearly half of global data center capex in 2025.

The concentration of spending was remarkable. Just four companies—Amazon, Google, Meta, and Microsoft—were expected to drive nearly half of global data center investment. These aren't just customers; they're partners in innovation. When Microsoft needs cooling for a new AI training cluster, they don't just place an order—they collaborate with Vertiv on next-generation solutions that will define the industry standard.

The shift from air to liquid cooling isn't optional—it's physics-driven necessity. The AI-dedicated data center is an emerging class of infrastructure. Although very few exist so far, they're designed for the unique properties of AI workloads — high absolute power requirements, higher power density racks, and the additional hardware (such as liquid cooling) that comes with it.

New data and forecasts from Synergy Research Group show that the average capacity of hyperscale data centers to be opened over the next four years will be almost double that of current operational hyperscale data centers. The trend has always been for the critical IT load of hyperscale data centers to grow in size over time, but generative AI technology and services are power hungry and have supercharged that trend. Meanwhile, as the average IT load of individual data centers ramps up, the number of operational hyperscale data centers will continue to steadily grow. There will also be some degree of retrofitting existing data centers to boost their capacity. The overall result is that the total capacity of all operational hyperscale data centers will grow almost threefold by 2030.

This isn't just growth—it's a complete reimagining of data center infrastructure. The average new data center being built today has double the capacity of existing facilities. And these aren't just bigger boxes with more servers. They're fundamentally different architectures designed from the ground up for AI workloads.

The competitive dynamics are fascinating. While the market is growing rapidly, it's also consolidating around a few key players who can handle the complexity and scale required. Colocation providers that are able to offer build-to-suit development services—that is, those able to build and operate data centers customized to the specific needs and designs of each hyperscaler—might prove to be particularly attractive partners.

Vertiv is perfectly positioned here. They're not just selling products; they're co-designing entire data centers with hyperscalers. When a company like Meta wants to build a new AI training facility, Vertiv is involved from day one, helping design the power distribution, cooling systems, and rack configurations that will optimize performance.

The technology evolution is accelerating. Nvidia's H100 GPUs consume 700 watts each. The next generation H200s push that higher. The B100s and B200s coming next will push power consumption even further. Each generation requires not just more cooling capacity but smarter cooling—precision delivery of cooling exactly where it's needed, when it's needed.

This is where Vertiv's partnerships become critical. Being selected for the COOLERCHIPS program with Nvidia wasn't just about the $5 million grant—it was about being at the forefront of defining next-generation cooling technology. The collaboration with Intel on Gaudi3 cooling ensures Vertiv remains vendor-agnostic while staying ahead of the technology curve.

The sustainability angle adds another dimension. At present, Goldman Sachs Research estimates the power usage by the global data center market to be around 55 gigawatts (GW). This is comprised of cloud computing workloads (54%), traditional workloads for typical business functions such as email or storage (32%), and AI (14%). But AI's share is growing rapidly, and with it comes pressure to improve efficiency.

Liquid cooling isn't just about handling higher heat loads—it's also more efficient. Water has 4,000 times the heat capacity of air by volume. This means liquid cooling systems can operate with higher temperature differentials, reducing or eliminating the need for mechanical chillers. Some of Vertiv's latest systems can operate with facility water temperatures up to 45°C (113°F), enabling free cooling in most climates.

The edge computing revolution adds another layer of opportunity. AI inference—actually running AI models rather than training them—is moving to the edge. This means smaller, distributed data centers closer to users. Each of these edge facilities needs cooling and power infrastructure, creating thousands of additional deployment opportunities.

Electric and gas utility capex is expected to surpass US$1 trillion cumulatively within the next five years (2025–2029) for the 47 biggest investor-owned utilities. For the hyperscalers, reaching the trillion-dollar threshold is expected in only three years, with spending projections reaching half a trillion dollars annually by the early 2030s. And for data centers more broadly, spending could reach a trillion dollars within three years.

These aren't just big numbers—they represent a fundamental restructuring of global infrastructure. The investment required rivals major national infrastructure programs. And unlike roads or bridges that last decades with minimal maintenance, data center infrastructure needs constant refreshing as technology evolves.

The timing couldn't be better for Vertiv. They've spent years building the technology, partnerships, and manufacturing capacity needed for this moment. While competitors scramble to develop liquid cooling solutions, Vertiv is already shipping at scale. While others try to understand AI workload requirements, Vertiv is already designing systems for GPUs that won't ship for two years.

IX. Playbook: Lessons in Infrastructure Investing

The Vertiv story offers a masterclass in infrastructure investing—not the boring, dividend-yielding, utility-like infrastructure of old, but the dynamic, high-growth infrastructure that powers technological revolutions. The key lessons from the Vertiv story are:

The Picks-and-Shovels Approach Works—If You Pick the Right Tools

During the California Gold Rush, the saying goes, the real winners weren't the miners but the merchants selling picks and shovels. Levi Strauss didn't pan for gold; he sold denim jeans to those who did. Similarly, Vertiv isn't training AI models or building chatbots—they're selling the critical infrastructure everyone needs to participate in the AI revolution.

But here's the nuance: not all picks and shovels are created equal. Selling commodity servers in the AI age is like selling bronze picks when everyone needs diamond-tipped drills. Vertiv's focus on the hardest problems—ultra-high-density cooling, massive power distribution, integrated systems—ensures they're selling the specialized tools that command premium prices and create switching costs.

Infrastructure-Agnostic Positioning Creates Optionality

Vertiv works with Nvidia, AMD, Intel, and every other chip maker. They cool Google's TPUs, Amazon's Inferentia chips, and Tesla's Dojo supercomputers. This vendor-agnostic position is crucial. They don't need to bet on which chip architecture wins—they win regardless.

Compare this to companies that bet everything on one technology or vendor. When Intel dominated, companies built entirely around x86 architecture thrived. When ARM emerged, many struggled to adapt. Vertiv's model is different: whoever makes the chips, those chips need cooling and power.

M&A as a Growth Accelerator in Fragmented Markets

The infrastructure market was historically fragmented—hundreds of companies making specialized products. Vertiv's acquisition strategy under both Emerson and Platinum consolidated this fragmentation, creating a one-stop shop for data center infrastructure.

Each acquisition wasn't just about adding revenue; it was about completing the portfolio. E+I Engineering brought power distribution. CoolTera added liquid cooling components. Great Lakes provided specialized racks. Together, these create a solution that's worth more than the sum of its parts.

The key is integration. Many companies acquire for the sake of growth but fail to integrate. Vertiv integrated aggressively, creating unified solutions that leverage components from multiple acquisitions. A single rack might incorporate power distribution from E+I, cooling from the core Liebert technology, monitoring from Avocent, and cabinet design from Great Lakes.

The Recurring Revenue Model Through Services

Equipment sales are lumpy and cyclical. Services provide predictable, high-margin revenue streams. Vertiv's service business—preventative maintenance, remote monitoring, emergency response—creates recurring revenue that smooths out the volatility of equipment cycles.

More importantly, services create stickiness. When you're maintaining cooling for $100 million worth of GPUs, switching service providers isn't just inconvenient—it's risky. This creates powerful retention dynamics and provides deep customer insights that inform product development.

Capital Intensity and the Importance of Scale

Infrastructure is capital-intensive. Factories, inventory, R&D—all require massive upfront investment. This creates a natural moat. A startup might design innovative cooling technology, but can they manufacture at scale? Can they provide global service? Can they guarantee supply when lead times stretch to months?

Vertiv's scale becomes self-reinforcing. Higher volumes drive lower unit costs. Lower costs enable competitive pricing. Competitive pricing drives more volume. It's a virtuous cycle that's extremely difficult for new entrants to break.

Timing Matters: Catching the Inflection Point

Vertiv had been in the data center cooling business for decades, but the AI revolution changed everything. Suddenly, their specialized expertise in high-density cooling went from nice-to-have to mission-critical. The company was perfectly positioned when the market inflected.

But this wasn't luck. Vertiv had been investing in liquid cooling for years before AI made it essential. They were already working on 40kW rack solutions when the market was still at 10kW. This forward investment meant they were ready when demand exploded.

Building Switching Costs Through Critical Infrastructure

When your product failure means millions in lost compute time, customers don't switch vendors lightly. When your equipment is literally built into the structure of a data center, replacement isn't just expensive—it requires shutting down operations.

Vertiv has systematically increased switching costs by moving from discrete products to integrated systems. It's one thing to swap out a CRAC unit. It's entirely another to replace an integrated liquid cooling system that's plumbed into every rack, connected to building management systems, and monitored by proprietary software.

The Power of Ecosystems and Partnerships

Vertiv doesn't just sell to customers; they partner with them. The NVIDIA collaboration, the Intel partnership, the hyperscaler relationships—these aren't vendor-customer relationships but strategic partnerships where Vertiv helps define the future of data center infrastructure.

These partnerships create competitive advantages beyond just sales. They provide early visibility into technology trends, influence over standards, and credibility with other customers. When Nvidia says Vertiv is their cooling partner, every AI startup takes notice.

Operational Excellence as a Differentiator

In commodity markets, operational excellence just keeps you competitive. In specialized markets with high growth, operational excellence becomes a massive differentiator. Vertiv's ability to scale manufacturing, maintain quality, and meet delivery schedules when competitors struggle creates value far beyond cost savings.

David Cote's Honeywell playbook—focus on people, portfolio, and performance—transformed Vertiv's operations. Margins expanded not through price increases alone but through systematic operational improvements that competitors couldn't match.

The Value of Patient Capital

Vertiv's journey from Emerson subsidiary to Platinum portfolio company to public company shows the value of patient capital. Each owner brought something different—Emerson brought scale and resources, Platinum brought operational focus and growth capital, and public markets brought currency for acquisitions and long-term stability.

The SPAC transaction, despite its complexity, was brilliantly timed. It provided liquidity for Platinum while bringing in David Cote's operational expertise and public market credibility. The structure allowed Vertiv to go public quickly, capturing the AI boom rather than waiting for traditional IPO windows.

The Infrastructure Paradox

Here's the paradox: infrastructure is supposed to be boring, stable, and commoditized. But technological disruptions create windows where infrastructure becomes exciting, dynamic, and differentiated. The companies that recognize and capture these windows can generate venture-like returns from industrial businesses.

Vertiv captured such a window. The AI revolution created unprecedented demand for specialized cooling. The shift from air to liquid cooling reset the competitive landscape. The explosion in rack densities made their expertise invaluable. What was once boring industrial equipment became cutting-edge technology.

X. Bear vs. Bull Case & Valuation

Every investment thesis has two sides. Let's examine both with the rigor they deserve.

The Bull Case: Infrastructure for the Next Industrial Revolution

AI Infrastructure Buildout in Early Innings

We're perhaps in the second inning of AI infrastructure deployment. Current estimates suggest $7 trillion in data center investment by 2030, but history shows that transformational technologies consistently exceed initial projections. The internet, mobile computing, cloud—all grew far beyond early estimates. If AI truly becomes as transformational as electricity, current projections may prove conservative.

Vertiv is capturing an outsized share of this growth. Their liquid cooling leadership, hyperscaler relationships, and integrated solutions position them as the infrastructure provider of choice for AI deployments. As rack densities push beyond 100kW, Vertiv's technology becomes not just preferable but essential.

Liquid Cooling Transition Creates Replacement Cycle

The shift from air to liquid cooling isn't optional—it's physics-mandated. This creates a massive replacement cycle as existing data centers upgrade infrastructure. Even facilities built five years ago need retrofitting for AI workloads. This isn't just growth from new construction but replacement of existing infrastructure—a double tailwind.

The replacement cycle extends beyond just cooling. Higher densities require new power distribution, new racks, new monitoring systems. Vertiv's integrated portfolio captures value across this entire upgrade cycle.

Strong Partnerships and First-Mover Advantage

The partnerships with Nvidia, Intel, and major hyperscalers create a formidable moat. These relationships took years to build and provide advantages that money alone can't buy: early access to roadmaps, influence over standards, and credibility with customers.

First-mover advantage in liquid cooling is particularly valuable. Every successful deployment adds to Vertiv's knowledge base. Every problem solved becomes intellectual property. Every customer becomes a reference. Competitors starting now are years behind on the learning curve.

Operating Leverage and Margin Expansion

Current margins of 21.5% could expand further. Fixed cost absorption, pricing power, and mix shift toward higher-value products all support continued margin expansion. If margins reach 25%—not unreasonable for a market leader in a high-growth, specialized market—earnings could surprise significantly to the upside.

The services business provides additional leverage. As the installed base grows, service revenue grows with it. Service margins typically exceed product margins, and revenue is recurring. This creates a compounding effect on profitability.

International Expansion and Edge Computing

While the U.S. leads in AI infrastructure, international markets are accelerating. China's domestic AI development, Europe's digital sovereignty initiatives, Middle Eastern diversification efforts—all drive infrastructure investment. Vertiv's global presence positions them to capture this growth.

Edge computing adds another growth vector. AI inference at the edge requires thousands of smaller deployments, each needing infrastructure. This distributed model plays to Vertiv's strengths in standardized, modular solutions.

The Bear Case: Peak Cycle and Structural Risks

High Valuation Multiples

At current valuations, Vertiv trades at premium multiples that embed significant growth expectations. Any disappointment—whether in growth rates, margins, or market conditions—could trigger multiple compression. The stock's spectacular run has pulled forward years of returns.

History shows that infrastructure investments are cyclical. The telecom boom of the late 1990s, the server boom of the 2000s, the cloud buildout of the 2010s—all experienced periods of overinvestment followed by painful corrections.

Cyclical Exposure to Data Center Capex

Data center investment is inherently cyclical. Hyperscalers don't build linearly—they invest in bursts, then digest capacity. If AI adoption slows or efficiency improvements reduce infrastructure needs, Vertiv could face a sharp deceleration in growth.

Recent developments like DeepSeek's efficient models raise questions about future infrastructure needs. If AI models become dramatically more efficient, the massive infrastructure buildout might prove excessive. This would hit Vertiv directly.

Competition from Larger Players

Schneider Electric, Eaton, and others aren't standing still. These companies have massive resources and are investing aggressively in liquid cooling. As the market matures and standards emerge, Vertiv's first-mover advantage could erode.

Chinese competitors pose a particular threat. Companies like Huawei have strong positions in their domestic market and ambitions to expand globally. They could compete aggressively on price, compressing margins across the industry.

Technology Risk and Rapid Innovation Cycles

Cooling technology could evolve in unexpected ways. Immersion cooling, phase-change materials, or entirely new approaches could obsolete current solutions. Vertiv's heavy investment in current-generation liquid cooling could become a liability if technology shifts.

Chip-level innovations could also reduce cooling requirements. More efficient processors, novel architectures, or quantum computing could change infrastructure needs dramatically. Vertiv must constantly innovate to stay relevant.

Customer Concentration Risk

Heavy reliance on a few large hyperscalers creates vulnerability. If one major customer shifts strategy, brings capabilities in-house, or faces its own challenges, Vertiv's results could suffer materially. The negotiating power of these massive customers could also pressure margins over time.

Valuation Framework

Current metrics suggest the market is pricing in continued exceptional growth:

- Forward P/E multiples well above historical averages

- EV/Sales ratios that assume margin expansion continues

- DCF models requiring 20%+ growth rates for extended periods

The key question: Is this the beginning of a multi-decade infrastructure super-cycle, or are we near the peak of an investment bubble?

Bull case valuation scenarios suggest significant upside if: - AI infrastructure spending exceeds current projections - Vertiv maintains or expands market share - Margins reach 25%+ through operational excellence - International and edge markets develop faster than expected

Bear case scenarios point to potential downside if: - Infrastructure spending normalizes after the initial AI buildout - Competition intensifies and margins compress - Technology shifts obsolete current solutions - Macro conditions deteriorate and reduce IT spending

The truth likely lies somewhere between these extremes. Vertiv has transformed from a sleepy industrial company to a high-growth technology enabler. The question for investors is whether current valuations already reflect this transformation or if there's still room to run.

XI. The Future: What's Next for Vertiv

The chess pieces are moving on multiple boards simultaneously. Let's examine where Vertiv might be heading over the next decade.

Edge Computing and Distributed Infrastructure

The future of computing isn't just massive centralized data centers—it's also thousands of edge locations processing data near its source. Autonomous vehicles, smart cities, industrial IoT, augmented reality—all require local processing to minimize latency.

Each edge location needs infrastructure, but the requirements differ from traditional data centers. Edge sites must be self-contained, remotely managed, and resilient to harsh environments. Vertiv's modular solutions and remote monitoring capabilities position them well for this distributed future.

The edge opportunity could dwarf the centralized data center market. If every cell tower, every factory, every hospital becomes a mini data center, the infrastructure opportunity multiplies exponentially.

Sustainability and Energy Efficiency Mandates

Regulatory pressure on data center energy consumption is intensifying globally. The EU's Energy Efficiency Directive, Singapore's data center moratorium, California's water usage restrictions—all force the industry toward more efficient solutions.

Liquid cooling isn't just about handling heat; it's about efficiency. By enabling higher operating temperatures and reducing or eliminating mechanical cooling, liquid systems can dramatically reduce energy consumption. Vertiv's solutions that operate with 45°C water enable free cooling in most climates, slashing energy costs.

The sustainability angle creates both opportunity and risk. Companies that lead in efficiency will win mandates and contracts. Those that lag could face regulatory restrictions or customer defection.

Nuclear Power and Alternative Energy Integration

The power demands of AI are forcing a renaissance in nuclear power. Microsoft's Three Mile Island deal, Amazon's nuclear investments, Google's SMR partnerships—hyperscalers are securing dedicated nuclear capacity for data centers.

This creates new infrastructure challenges. Nuclear plants need cooling systems. Data centers at nuclear sites need specialized infrastructure. The integration of renewable energy sources—solar, wind, hydro—requires sophisticated power management systems.

Vertiv's power management expertise becomes crucial here. As data centers move from grid-connected to self-powered, infrastructure requirements change dramatically. Companies that can manage complex power sources, storage systems, and distribution networks will thrive.

Geographic Expansion Opportunities

While the U.S. leads in AI infrastructure, other regions are accelerating:

Asia-Pacific: China's domestic AI industry, Japan's Society 5.0 initiative, India's digital transformation—all drive infrastructure investment. Despite geopolitical tensions, the fundamental need for data center infrastructure transcends borders.

Middle East: Oil-rich nations are investing petroleum revenues in becoming AI hubs. Saudi Arabia's NEOM project, UAE's AI ambitions, Qatar's smart city initiatives—all require massive infrastructure investment.

Europe: Data sovereignty regulations force local data processing. Combined with aggressive sustainability targets, this creates demand for efficient, compliant infrastructure solutions.

Africa and Latin America: These emerging markets are leapfrogging traditional infrastructure, going straight to modern data centers. The opportunity is enormous but requires localized solutions and partnerships.

The Next Generation of Cooling Technology

Current liquid cooling is just the beginning. Next-generation technologies under development include:

Immersion Cooling: Submerging entire servers in dielectric fluid. This enables even higher densities and eliminates the need for fans entirely. Vertiv's acquisitions and R&D investments position them to lead here.

Two-Phase Cooling: Using the phase change from liquid to vapor for maximum heat absorption. This technology, already in Vertiv's portfolio, could become standard for ultra-high-density deployments.

Direct-to-Chip Cooling: Bringing coolant directly to processors through cold plates and microchannels. As chips integrate more functions, this precision cooling becomes essential.

Waste Heat Recovery: Turning data center heat into useful energy. District heating, industrial processes, even agriculture could use data center waste heat, creating new revenue streams.

Potential M&A Targets and Market Consolidation

The infrastructure market remains fragmented despite recent consolidation. Potential acquisition targets for Vertiv might include:

- Specialized liquid cooling component manufacturers

- Software companies focused on data center management

- Power electronics specialists for next-generation distribution

- Service companies with strong regional presence

- Edge infrastructure specialists

Alternatively, Vertiv itself could become an acquisition target. Strategic buyers like Schneider Electric or financial buyers attracted to the growth profile might see value in Vertiv's market position.

Market consolidation seems inevitable. The complexity and scale required for next-generation infrastructure favor larger players. Smaller companies will struggle to match R&D investments and global reach.

The AI Evolution and Infrastructure Implications

AI's evolution will drive infrastructure requirements in unexpected ways:

Model Size: If models continue growing exponentially, infrastructure needs could exceed current projections. Trillion-parameter models might require dedicated data centers just for training.

Efficiency Improvements: Conversely, breakthroughs in model efficiency could reduce infrastructure needs. Sparse models, quantization, novel architectures—all could change the equation.

Specialized Hardware: As AI matures, specialized processors for specific tasks will emerge. Each might have unique cooling and power requirements, creating complexity but also opportunity.

Quantum Computing: The eventual arrival of practical quantum computers will create entirely new infrastructure challenges. Cooling requirements for quantum systems are extreme, requiring near absolute-zero temperatures.

The Platform Play

Vertiv's future might not just be selling products but becoming a platform—the operating system for data center infrastructure. By combining hardware, software, and services into integrated solutions, they could lock in customers and capture more value.

Imagine Vertiv offering Infrastructure-as-a-Service: customers specify compute requirements, and Vertiv handles everything else—power, cooling, monitoring, maintenance. This would transform the business model from transactional sales to recurring revenue streams.

The data generated by monitoring thousands of data centers could itself become valuable. Predictive maintenance, efficiency optimization, capacity planning—all could be offered as value-added services powered by AI analysis of operational data.

Conclusion: The Infrastructure Layer of the AI Economy

Vertiv's story is far more than a successful corporate transformation or a well-timed SPAC transaction. It's a case study in how patient capital, strategic positioning, and operational excellence can capture value during technological disruptions.

From Ralph Liebert's garage in Columbus to partnerships with the world's leading technology companies, Vertiv has evolved from cooling mainframes to enabling the AI revolution. The company that once sold air conditioners to computer rooms now provides the critical infrastructure for humanity's attempt to create artificial general intelligence.

The investment thesis remains compelling but complex. The bull case sees Vertiv as essential infrastructure for a multi-decade AI buildout, with expanding margins, strong competitive positions, and multiple growth vectors. The bear case warns of cyclical exposure, valuation risks, and technological disruption.

What's certain is that Vertiv sits at the intersection of several powerful trends: the AI revolution, the energy transition, the edge computing explosion, and the global digitalization of everything. Few companies are as leveraged to these themes while maintaining the operational excellence to capitalize on them.

For investors, Vertiv offers a way to bet on AI infrastructure without picking winners in the model or chip wars. It's the ultimate picks-and-shovels play for the AI gold rush—selling the essential equipment that everyone needs regardless of who strikes gold.

The next decade will test whether Vertiv can maintain its leadership position as competition intensifies and technology evolves. Can they continue innovating fast enough? Can they maintain margins as the market matures? Can they navigate the cyclicality inherent in infrastructure investments?

These questions don't have easy answers. But what's clear is that Vertiv has transformed from a sleepy industrial company into a critical enabler of the AI age. Whether you're bullish or bearish on the stock, you can't ignore the company's central role in building the infrastructure of our AI-powered future.

In the end, Vertiv's story reminds us that the most important technologies are often the most invisible. While everyone focuses on chatbots and image generators, companies like Vertiv are building the physical foundation that makes it all possible. They're the infrastructure layer of the AI economy—invisible but essential, boring but beautiful, and potentially, very profitable.

The machines are learning. The data centers are growing. The infrastructure is evolving. And at the center of it all, keeping the servers cool and the power flowing, is a company that started in a garage with a simple insight: computers generate heat, and heat kills computers.

Seventy-eight years later, that insight is worth tens of billions of dollars and growing.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube