VeriSign: The Internet's Hidden Infrastructure Monopoly

I. Introduction & Cold Open

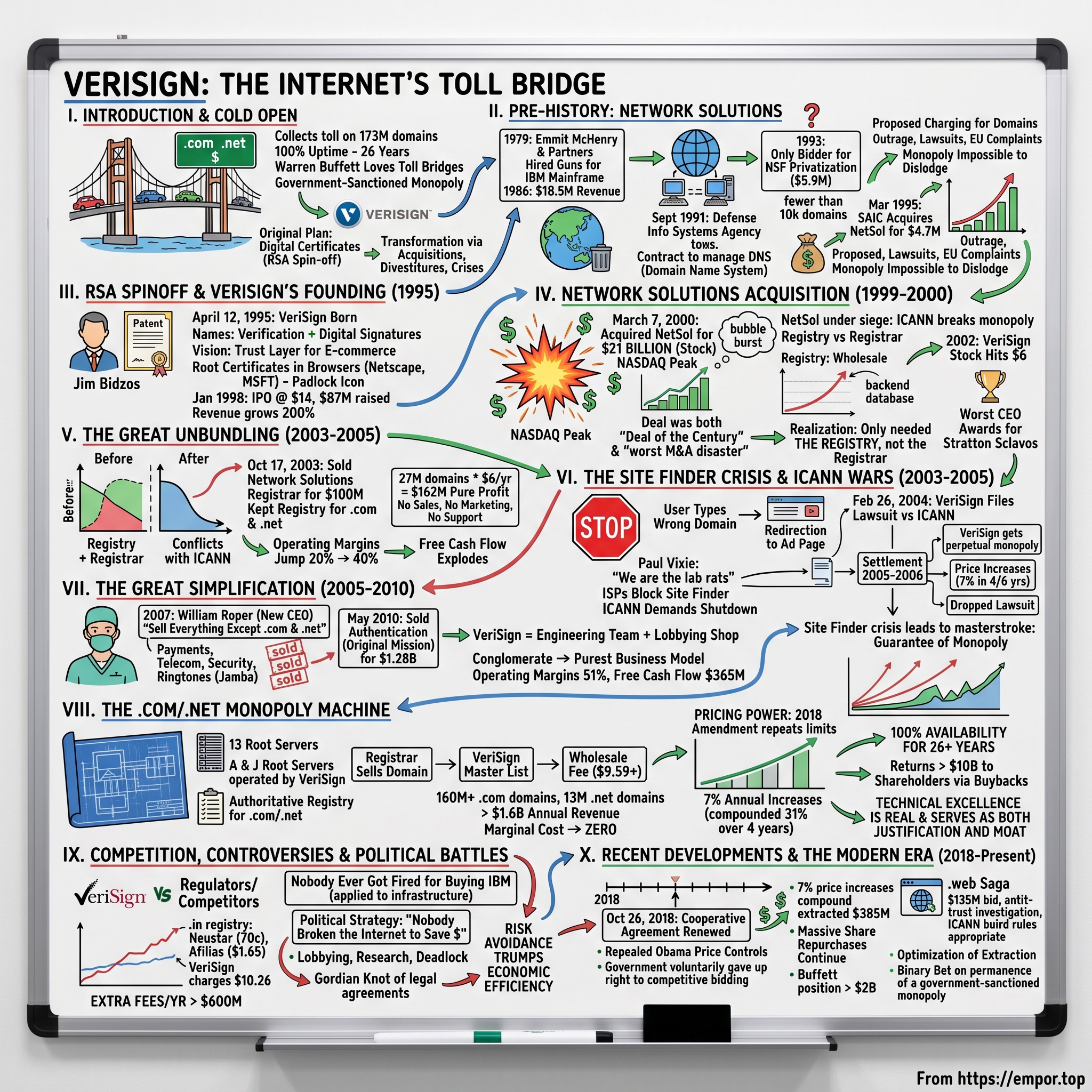

Picture this: Every time you type "google.com" or "amazon.com" into your browser, a company you've probably never heard of collects a toll. Not a big toll—just a few dollars per year per domain—but when you're collecting it on 173 million domains, those pennies become an absolute torrent of cash. This is VeriSign, and it might just be the best business model in technology that nobody talks about.

The numbers are staggering. VeriSign operates with 65% operating margins, has maintained 100% uptime for over 26 years, and has what amounts to a government-sanctioned monopoly on the two most valuable pieces of internet real estate: .com and .net domains. Warren Buffett famously loves toll bridges. Well, VeriSign built the ultimate toll bridge—one that every business on the internet has to cross, with prices that can only go up, and competition that's essentially illegal.

But here's what's truly wild: VeriSign wasn't supposed to be this company. It started in 1995 as a spin-off from RSA Security, focused on digital certificates—those little padlocks you see in your browser. The plan was to become the trust infrastructure for e-commerce. Instead, through a series of acquisitions, divestitures, crises, and political battles that read like a techno-thriller, VeriSign accidentally stumbled into owning the most critical piece of internet infrastructure outside of the physical cables themselves.

How does a security company spin-off end up with a monopoly on .com domains? How did they pay $21 billion for an asset at the peak of the dot-com bubble, sell most of it for $100 million three years later, and somehow come out ahead? Why does the U.S. government keep renewing their contract without competitive bidding, despite companies offering to do the same job for one-third the price?

This is the story of how VeriSign became the landlord of the internet—a tale involving Department of Defense contracts, congressional investigations, international diplomatic incidents, and one of the most brilliant strategic pivots in business history. It's about recognizing that sometimes the most valuable businesses aren't the sexiest ones. Sometimes they're the boring ones that just happen to sit at a critical chokepoint of the global economy.

By the time you finish this story, you'll understand why VeriSign's stock has quietly outperformed almost every tech giant over the past decade, why some investors consider it the perfect monopoly, and why others think it's a regulatory time bomb. You'll never look at a URL the same way again.

II. The Pre-History: Network Solutions and the Birth of Domain Registration

To understand VeriSign's empire, we need to start not with VeriSign itself, but with a small government contractor in Washington, D.C. that accidentally invented the business of selling internet addresses.

In 1979, Emmit McHenry was a computer programmer with a vision that seemed almost quaint by today's standards: he wanted to build a technology consulting company. Along with partners Ty Grigsby, Gary Desler, and Ed Peters, he incorporated Network Solutions in the suburbs of Washington. They were, in essence, hired guns for IBM mainframe programming—not exactly the stuff of Silicon Valley legend.

For its first decade, Network Solutions was the definition of a lifestyle business. They wrote COBOL, managed databases, and helped government agencies figure out their computer systems. Revenue hit $1 million in 1982—a respectable milestone for a services company. By 1986, they'd grown to $18.5 million in annual revenue. Solid, predictable, boring.

But in September 1991, something changed that would transform this sleepy contractor into one of the most controversial companies of the early internet era. The U.S. Defense Information Systems Agency (DISA) needed someone to manage something called the Domain Name System registry. If you were a computer scientist in 1991, you knew what DNS was. If you were anyone else, you had no idea this thing even existed.

Here's what DNS was in 1991: a glorified phone book that maybe a few thousand computer scientists and researchers used to name their machines. Want to call your computer "mit.edu" instead of remembering 18.72.0.3? DNS was your friend. The contract to run this system was so unimportant that when the National Science Foundation put it out for bid in May 1993, offering $5.9 million annually to privatize the operation, Network Solutions was the only company that bothered to submit a proposal.

Think about that for a moment. The right to control every .com, .net, and .org domain name on the internet—a right that would eventually be worth tens of billions—had exactly one bidder.

McHenry and his team had no idea what they'd stumbled into. In 1993, there were fewer than 10,000 domain names in existence. The World Wide Web was two years old. Amazon didn't exist. Google's founders were still in college. Network Solutions was managing what seemed like an academic curiosity, a bit of internet plumbing that helped university researchers find each other's computers.

Then in March 1995, something extraordinary happened. Science Applications International Corporation (SAIC), a defense contractor with deep government connections, acquired Network Solutions for $4.7 million. At the time of the acquisition, Network Solutions managed 60,000 domain names. SAIC saw what McHenry hadn't: the internet was about to explode, and whoever controlled domain names would be sitting on a gold mine.

SAIC immediately went to the National Science Foundation with a proposal that would change the internet forever: let us charge for domain names. The NSF, perhaps not fully grasping the implications, said yes. Network Solutions would charge $100 for a two-year registration—$50 per year for something that had previously been free.

The reaction was swift and furious. Internet pioneers, who'd built the network as an open, collaborative project, were outraged. Lawsuits flew, calling the fees an "illegal tax." One early internet user famously registered "netsol-sucks.com" in protest. Congressional hearings were held. The European Union complained about an American monopoly on a global resource.

But here's the thing about infrastructure monopolies: once they're established, they're nearly impossible to dislodge. By 1997, Network Solutions was registering 100,000 new domains per month. By 1999, they managed 8 million domains and had revenue approaching $200 million annually. The academic curiosity had become a cash machine.

Network Solutions had discovered something profound: in the digital age, the most valuable real estate isn't land—it's namespace. Every business that wanted to exist online needed a domain name, and Network Solutions was the only store in town. They didn't invent the internet, they didn't build the protocols, they didn't create the demand. They just happened to be the government contractor managing the list when the gold rush began.

What happened next would make Network Solutions one of the most valuable companies of the dot-com era, lead to a $21 billion acquisition, and set the stage for one of the most audacious corporate transformations in technology history. But to understand that, we need to introduce the other protagonist in our story: a cryptography company with grand ambitions and perfect timing.

III. RSA Spinoff & VeriSign's Founding (1995)

While Network Solutions was discovering the gold mine of domain names, 3,000 miles away in Silicon Valley, Jim Bidzos was contemplating mortality—not his own, but that of RSA Security's patent portfolio.

Bidzos was a larger-than-life character in the early days of internet security. A Greek immigrant who'd studied computer science and spent time as a programmer at IBM, he'd taken over RSA Security in 1986 when it was basically a patent holding company with revolutionary technology but no real business. The company held the patents for RSA public-key cryptography—the mathematical breakthrough that made secure internet communications possible. Every time someone wanted to encrypt data on the internet, they needed RSA's blessing.

But Bidzos had a problem: patents expire. The core RSA patents would become public domain in 2000, just five years away. He'd built RSA Security into the dominant player in encryption, but he could see the cliff coming. Once those patents expired, anyone could use RSA encryption for free. The castle walls would come down.

His solution was audacious: spin off a separate company focused on digital certificates before the patents expired. Give the new company perpetual licenses to the technology while it was still proprietary, plus a non-compete agreement with RSA. Let it build a business around trust infrastructure for e-commerce. When the patents expired, the spin-off would already be the established market leader with the technology, the customers, and the brand.

On April 12, 1995, VeriSign was born. The name itself was carefully chosen—"Veri" for verification, "Sign" for digital signatures. This would be the company that verified you were who you said you were on the internet.

The original vision was elegant: as e-commerce exploded, every online transaction would need authentication. Every website would need a certificate proving it was legitimate. Every email might need a digital signature. VeriSign would be the trust layer of the internet economy. It was selling picks and shovels for the digital gold rush, except the picks and shovels were mathematical proofs of identity.

Bidzos installed Stratton Sclavos as CEO—a Stanford MBA who'd worked at VISA and understood both technology and financial services. Sclavos was smooth where Bidzos was combative, diplomatic where Bidzos was confrontational. If Bidzos was the wartime consigliere who'd fought the government over encryption export controls, Sclavos was the peacetime CEO who could sell digital certificates to Fortune 500 companies.

The early days were harder than anyone expected. Selling digital certificates in 1995 was like selling insurance for a risk nobody understood yet. E-commerce barely existed. Most companies didn't even have websites. VeriSign's sales team would cold-call businesses and try to explain public-key infrastructure to executives who barely understood email.

A typical sales conversation went something like this: "You need a digital certificate for your website." "What's a digital certificate?" "It proves you are who you say you are." "Why do I need to prove that?" "So customers trust you." "They already trust us—we've been in business for 50 years." "But on the internet—" "We don't sell anything on the internet."

The breakthrough came from an unexpected source: web browsers. Netscape and Microsoft were locked in the browser wars, each trying to make their product the gateway to the web. Both needed a way to show users which sites were secure. VeriSign convinced them to include its root certificates in their browsers—essentially pre-installing VeriSign as a trusted authority.

This was genius. Once VeriSign's root certificates were in the browsers, any website that wanted to show the little padlock icon—the universal symbol for "this site is secure"—needed to buy a certificate from VeriSign or one of a handful of other authorities. VeriSign had inserted itself into the trust chain of the internet.

By 1997, VeriSign was issuing thousands of certificates per month. The company went public in January 1998 at $14 per share, raising $87 million. Revenue was growing at 200% annually. They'd found product-market fit just as e-commerce was taking off.

But Sclavos had bigger ambitions. He didn't want VeriSign to be just a certificate authority. He wanted it to be the trust infrastructure for everything digital—payments, identity, domain names, network security. He wanted to build an empire. And in the feeding frenzy of the dot-com bubble, he'd get his chance.

The seeds of VeriSign's transformation were already being planted. The company that started as a cryptography spin-off was about to make one of the most expensive acquisitions in internet history. It would be either the deal of the century or the worst M&A disaster of the dot-com era. As it turned out, it was both.

IV. The Network Solutions Acquisition: The Deal of the Century (1999-2000)

March 7, 2000. The NASDAQ was near its all-time peak at 5,048. Pets.com sock puppets danced on Super Bowl commercials. Twenty-somethings were paper millionaires from companies that had never turned a profit. And Stratton Sclavos was about to announce the most audacious acquisition of the dot-com era.

VeriSign would acquire Network Solutions for $21 billion in stock.

Twenty-one billion dollars. For a domain name registrar with maybe $300 million in revenue. The price tag was so astronomical that even in the reality-distortion field of the dot-com bubble, people stopped and stared. This wasn't just expensive—it was incomprehensible.

To understand how we got here, you need to understand the competitive dynamics of early 2000. Network Solutions had gone public in 1997 and seen its stock price rocket from $18 to over $100. SAIC had made 20 times its money in less than five years. But Network Solutions was also under siege.ICANN—the Internet Corporation for Assigned Names and Numbers—had been formed in 1998 to break Network Solutions' monopoly. ICANN announced the first five companies selected to compete as domain registrars in April 1999, ending Network Solutions' exclusive right to handle .com, .net, and .org registrations. Suddenly, companies like Register.com and Tucows could sell domain names too. Network Solutions had to split itself in two: a registry (the backend database) and a registrar (the retail sales operation). The gravy train was ending.

At the same time, VeriSign was facing its own challenges. The digital certificate business was growing, but not explosively. E-commerce was taking off, but most transactions still happened offline. Sclavos looked at Network Solutions and saw something beautiful: recurring revenue. Every domain name needed to be renewed every year. It was the ultimate subscription business before anyone used that term.

The courtship began in late 1999. Network Solutions was playing the field—Oracle was interested, as were several other tech giants. But Sclavos was the most aggressive suitor. He didn't just want to buy Network Solutions; he wanted to transform VeriSign into the trust and naming infrastructure of the entire internet.

The negotiation was surreal even by dot-com standards. Network Solutions' stock price was bouncing around like a pinball—$50 one day, $150 the next. VeriSign's stock was equally volatile. Both companies were essentially negotiating with Monopoly money that changed value by the hour. The final deal was structured as an all-stock transaction: 1.1059 shares of VeriSign for each share of Network Solutions.

When they announced the deal on March 7, 2000, the math worked out to $21 billion. The NASDAQ peaked just three days later.

Inside VeriSign, the reaction was mixed. The engineers thought Sclavos had lost his mind. Twenty-one billion for what? A database of names and addresses? The certificates team felt betrayed—weren't they supposed to be the core business? But Sclavos saw what others didn't: he wasn't buying Network Solutions' current business. He was buying their contracts. Buried in the complex web of contracts Network Solutions had with ICANN and the Department of Commerce was a crucial detail: Network Solutions operated the .com, .net, and .org TLDs under agreements with ICANN and the United States Department of Commerce. More importantly, Network Solutions had divided itself into two divisions—the NSI Registry division was established to manage the authoritative registries, separated from the customer-facing registrar business that would have to compete with other registrars.

VeriSign wasn't just buying a company. It was buying the registry—the wholesale backend that collected $6 from every single .com and .net domain, regardless of who sold it. This was the crown jewel, hidden in plain sight.

The integration was a disaster from day one. Network Solutions had a government contractor culture—bureaucratic, methodical, focused on compliance. VeriSign was a Silicon Valley startup—fast-moving, stock-option driven, obsessed with growth. The two companies mixed like oil and water.

But the real problem was that VeriSign had bought at exactly the wrong moment. The NASDAQ crashed just days after the acquisition announcement. VeriSign's stock, which had been trading above $250, began its long descent. By 2002, it would hit $6. That $21 billion acquisition was suddenly worth a fraction of what VeriSign paid.

Wall Street was brutal. Analysts called it the worst acquisition in tech history. The "Worst CEO" awards started rolling in for Sclavos. VeriSign's market cap fell below $2 billion—less than 10% of what they'd paid for Network Solutions alone. It looked like a complete catastrophe.

But here's where the story gets interesting. Remember that separation between registry and registrar that Network Solutions had been forced to create? VeriSign's executives slowly realized they'd been thinking about the acquisition all wrong. They didn't need the registrar business—the retail operation that competed with hundreds of other companies to sell domains to end users. That was a competitive, low-margin business.

What they needed was the registry—the monopoly backend that collected wholesale fees from everyone. Every .com domain, regardless of whether it was sold by GoDaddy, Register.com, or anyone else, generated $6 per year for the registry operator. And VeriSign now owned that registry.

This revelation would lead to one of the most brilliant strategic pivots in corporate history. VeriSign would spend the next three years systematically dismantling the $21 billion company they'd just bought, selling off pieces for pennies on the dollar, all to keep the one asset that mattered: the registry contracts for .com and .net.

What looked like the worst deal of the dot-com era was about to become one of the most lucrative acquisitions in business history. But first, VeriSign would have to survive a near-death experience, multiple lawsuits, and a battle with ICANN that would determine the future of the internet itself.

V. The Great Unbundling: Separating Registry from Registrar

By 2003, Stratton Sclavos had a problem that would make most CEOs physically ill. He'd paid $21 billion for Network Solutions at the peak of the bubble. VeriSign's stock had cratered from $250 to under $10. The company was bleeding cash, carrying massive debt, and Wall Street wanted his head on a pike. The board was restless. Shareholders were filing lawsuits.

But Sclavos had figured something out that his critics hadn't: he didn't need to make the $21 billion back. He just needed to keep the registry.

The registry business was beautiful in its simplicity. After ICANN's formation in 1998, the domain name industry opened to partial competition, with NSI retaining its monopoly on .com, .net and .org but recognizing a separation between registry functions (managing the underlying database) and registrar functions (retail provision of domain names). VeriSign owned the registry. Everyone else—including VeriSign's own Network Solutions registrar division—had to pay the registry $6 for every .com and .net domain.

Think about that business model for a moment. Zero customer acquisition cost—the registrars did all the selling. Near-zero marginal cost—adding one more domain to a database costs essentially nothing. No competition—VeriSign was the only registry for .com and .net. Recurring revenue—domains need to be renewed annually. It was the platonic ideal of a software business, except it wasn't even software. It was just a database.

On October 17, 2003, Sclavos made the announcement that shocked the industry: VeriSign would sell Network Solutions, the Herndon-based registrar of Internet addresses, for $100 million to Pivotal Private Equity, retaining only a 15 percent stake.

One hundred million dollars. For the business they'd paid $21 billion for just three years earlier.

The press had a field day. "VeriSign Admits Defeat," read one headline. "The End of an Era," declared another. Financial analysts competed to find the most creative ways to call Sclavos an idiot. How could you destroy 99.5% of the value of an acquisition in three years?

But look closer at what VeriSign kept versus what it sold. The Network Solutions unit being sold was a registrar for online addresses ending in .com and .net, one of more than 100 such companies, with 600 employees. It was a retail business competing on price, customer service, and marketing spend. Margins were shrinking as competition increased.

Meanwhile, VeriSign kept its role as the exclusive list-keeper of Internet addresses, collecting $6 for each .com and .net address regardless of which registrar sold it, with about 27 million domains in the database. Do the math: 27 million domains times $6 per year equals $162 million in essentially pure profit, every single year, with no sales force, no marketing, no customer service.

The critics were looking at the sticker price. Sclavos was looking at the cash flows.

But the divestiture wasn't just about financial engineering. It was about political positioning. Many had criticized VeriSign's ability to take fees from registrars for each .com or .net domain name registration while competing with these registrars through its Network Solutions business. By selling the registrar, VeriSign removed a major source of conflict with ICANN, the Department of Commerce, and the broader internet community.

This was crucial because VeriSign's registry contracts were coming up for renewal. The company needed to be seen as a neutral infrastructure provider, not a competitor to its own customers. Selling Network Solutions for a 99.5% loss was the price of admission to keep the registry contracts—contracts that would generate billions in profit over the coming decades.

The sale also allowed VeriSign to focus. Running a registrar is a completely different business from running a registry. Registrars need sales teams, customer support, marketing campaigns, and constant innovation to differentiate from competitors. Registries need five-nines uptime, bulletproof security, and good relationships with regulators. VeriSign was trying to be a Swiss Army knife when what it needed to be was a sledgehammer.

Inside VeriSign, the transformation was dramatic. Entire buildings in Herndon were emptied as the Network Solutions employees moved out. The company that had once employed thousands shrunk to a few hundred. Marketing budgets were slashed. Sales teams were eliminated. What remained was essentially an engineering organization focused on one thing: keeping the .com and .net databases running perfectly, forever.

Wall Street didn't get it immediately. VeriSign's stock continued to languish. Analysts focused on the revenue decline—from $1.9 billion in 2003 to $1.4 billion in 2004. But the quality of that revenue had completely changed. Instead of competitive, low-margin registrar revenue, VeriSign now had monopoly, high-margin registry revenue.

By 2005, the transformation was becoming clear. Operating margins jumped from 20% to over 40%. Free cash flow exploded. The company that had been on death's door two years earlier was now generating more profit than ever before, with a fraction of the employees and complexity.

The Great Unbundling, as it came to be known internally, was complete. VeriSign had performed one of the most dramatic pivots in corporate history—destroying $21 billion in acquisition value to preserve a business worth far more. But the fight for that business was just beginning. VeriSign's next battle would be with ICANN itself, and it would determine whether the company's monopoly would last for years or decades.

VI. The Site Finder Crisis & ICANN Wars (2003-2005)

On September 15, 2003, at 5:30 PM Pacific Time, VeriSign flipped a switch that would ignite one of the most explosive controversies in internet history. Without warning, without consultation, without permission from anyone, they fundamentally changed how the internet worked.

The service was called Site Finder. The concept was simple: when someone typed a non-existent .com or .net domain into their browser—say, "amaz0n.com" instead of "amazon.com"—instead of getting an error message, they'd be redirected to a VeriSign search page with advertisements. VeriSign would monetize typos, turning the internet's equivalent of wrong numbers into a revenue stream.

Within minutes, the internet's technical community exploded in rage.

Paul Vixie, one of the internet's elder statesmen, fired off an email to the North American Network Operators Group that would become legendary in its fury: "This is not a technical trial. This is a business model trial, and we are the lab rats." Within hours, ISPs around the world were implementing patches to block Site Finder. The Internet Architecture Board issued an unprecedented emergency statement. ICANN demanded VeriSign shut it down immediately.

The technical problem was profound. VeriSign hadn't just changed what users saw in browsers—they'd altered the fundamental behavior of the Domain Name System itself. Email servers that checked if domains existed before accepting mail started failing. Spam filters broke. Network diagnostic tools stopped working. VeriSign had changed a core protocol of the internet without telling anyone, and the collateral damage was enormous.

But VeriSign's executives saw it differently. From their perspective, they were innovating, adding value to what had been dead space on the internet. Other country-code registries had implemented similar services without controversy. Why was VeriSign being singled out? The answer, they believed, was politics, not technology.

On October 3, 2003, after just 18 days, VeriSign suspended Site Finder. But Sclavos wasn't backing down. Instead, he was going to war. On February 26, 2004, VeriSign filed a lawsuit against ICANN in the United States District Court for the Central District of California. The suit didn't just challenge ICANN's authority over Site Finder—it questioned ICANN's entire regulatory framework. VeriSign claimed that ICANN had overstepped its authority, extending its technical coordination function into areas of business regulation it had no right to control.

The lawsuit was a declaration of war, but it was also a negotiating tactic. VeriSign didn't really want to destroy ICANN—that would create chaos that might invite government regulation. What VeriSign wanted was clarity: clear rules about what services it could offer, defined timelines for approval processes, and most importantly, security for its registry contracts.

At the heart of VeriSign's complaint was the lack of any definable process for decision-making at ICANN. How long would it take to get approval for a new service? What were the criteria? Who made the final decision? ICANN had no defined process for decision-making; it was a black hole. There was no way to tell how long it would take to get an answer to a request.

The lawsuit dragged on through 2004 and into 2005. United States District Court Judge Howard Matz dismissed the antitrust portions of the lawsuit on August 26, 2004, ruling that VeriSign failed to provide sufficient evidence to prove its antitrust complaint against ICANN. But VeriSign re-filed in state court, keeping the pressure on.

Behind the scenes, negotiations were intensifying. Both sides had too much to lose from a protracted legal battle. ICANN needed VeriSign to run .com and .net—no other company had the infrastructure or expertise. VeriSign needed ICANN's blessing to operate its monopoly without constant regulatory challenges.

The breakthrough came in late 2005. After nearly two years of litigation and negotiation, VeriSign and ICANN announced a proposed settlement that would reshape the internet's governance structure. The terms were extraordinary:

VeriSign would get a presumptive right of renewal for the .com registry agreement—essentially a perpetual monopoly, as long as they met certain performance standards. The contract could only be terminated for specific breaches, not put out for competitive bidding. VeriSign would be allowed to raise prices by 7% in four of any six-year period, giving them pricing power they'd never had before.

In exchange, VeriSign would drop its lawsuit, pay ICANN $625,000 in legal fees, and contribute millions more to ICANN's budget over the coming years. Most importantly, VeriSign would acknowledge ICANN's authority over technical coordination—but with clearly defined limits.

The internet community was outraged. This wasn't a settlement; it was a sellout. ICANN had essentially granted VeriSign a permanent monopoly in exchange for ending a lawsuit. The public comment period was flooded with thousands of objections. Competitors screamed that this was anticompetitive. Consumer groups argued it would lead to higher prices.

But the deal held. On February 28, 2006, the settlement was finalized, and on March 1, 2006, the new .com Registry Agreement went into effect. VeriSign had won. Not just the battle over Site Finder—that service would never return—but the war for control of .com.

The Site Finder crisis had been a disaster that became a masterstroke. By pushing ICANN to the brink, by forcing a constitutional crisis in internet governance, VeriSign had secured something far more valuable than a search service: a legally binding guarantee of its monopoly, with pricing power and presumptive renewal rights.

Years later, a VeriSign executive would privately admit: "Site Finder was never about the search revenue. It was about establishing the principle that we controlled .com, not ICANN. The lawsuit was about getting that in writing. The $625,000 in legal fees? Best money we ever spent."

The 2006 agreement would become the foundation of VeriSign's transformation into one of the most profitable companies in technology. But first, the company needed to shed everything that wasn't the registry business. The great simplification was about to begin.

VII. The Great Simplification: Selling Everything Else (2005-2010)

In May 2007, William Roper walked into his first board meeting as VeriSign's new CEO and delivered a message that shocked even the directors who had hired him: "We're going to sell everything except .com and .net."

Roper was an unusual choice to lead a technology company. A former GE executive who'd run their medical diagnostics division, he had no background in internet infrastructure. But that was exactly why the board wanted him. VeriSign didn't need a visionary. It needed a surgeon—someone who could cut away everything that wasn't essential and transform a sprawling conglomerate into a focused monopoly.

The company Roper inherited was a mess. VeriSign had spent the Sclavos era on an acquisition spree, buying anything that seemed vaguely related to internet infrastructure. They had a payments business competing with PayPal. A telecom services division selling SS7 signaling. A security business offering everything from SSL certificates to managed firewall services. They even had a majority stake in Jamba, a European mobile content company that sold ringtones.

Each business had its own P&L, its own sales force, its own technology stack. The company had 5,000 employees spread across dozens of offices worldwide. It was, as one board member put it, "fifteen companies stapled together, sharing nothing but a stock ticker."

Roper's simplification plan was brutal in its clarity. Every business would be evaluated on a single criterion: Was it a monopoly or near-monopoly with pricing power and recurring revenue? If not, it would be sold, shut down, or spun off. No exceptions.

The first to go was the communications services business. In October 2007, VeriSign sold its billing and commerce services to Transaction Network Services for $230 million. A month later, the messaging services went to Neustar for $450 million. These were profitable businesses with real customers, but they were competitive markets. VeriSign couldn't raise prices 7% whenever it wanted.

Wall Street hated it. Analysts who'd been trained to value companies on revenue growth watched VeriSign's top line shrink quarter after quarter. Revenue fell from $1.5 billion in 2007 to $1.0 billion in 2009. The stock languished around $25, barely moving despite the asset sales generating hundreds of millions in cash.

But Roper didn't care about revenue. He cared about margins and returns on capital. Every business VeriSign sold had been dragging down the company's overall profitability. The communications services division had 15% operating margins. The security business was at 20%. The registry business? North of 60% and climbing.

The crown jewel divestiture came in May 2010. VeriSign sold its authentication business unit—which included Secure Sockets Layer (SSL) certificate, public key infrastructure (PKI), VeriSign Trust Seal, and VeriSign Identity Protection (VIP) services—to Symantec for $1.28 billion. The deal capped a multi-year effort by VeriSign to narrow its focus to its core infrastructure and security business units.

This was the business VeriSign had been founded to build—the digital certificates and authentication services that had been its original mission in 1995. It was generating $370 million in annual revenue, growing at 20% per year. By any measure, it was a successful technology business.

But it wasn't a monopoly. VeriSign competed with Comodo, GeoTrust, and dozens of other certificate authorities. Prices were falling as competition increased. Customer acquisition costs were rising. It was a real business that required real work—sales calls, product development, customer support.

The registry business required none of that. No sales team because registrars had to buy from VeriSign. No product development because the service hadn't fundamentally changed in a decade. No customer support because VeriSign's customers were registrars, not end users. It was a toll road that collected money for existing.

Inside VeriSign, the transformation was surreal. Entire floors of offices were emptied as divisions were sold. The Dulles campus, once buzzing with thousands of employees, became a ghost town with a few hundred engineers maintaining the registry infrastructure. Marketing departments disappeared. Sales organizations evaporated. What remained was essentially a technology operations team and a lobbying shop.

The company that emerged from Roper's restructuring was unrecognizable from the VeriSign of 2000. Revenue had fallen by 40%, but operating margins had doubled. Employee count had dropped from 5,000 to less than 1,000, but free cash flow had exploded. VeriSign had transformed from a struggling conglomerate into the purest business model in technology.

By 2010, the numbers told the story: $680 million in revenue, almost entirely from .com and .net registry fees. Operating margins of 51%. Free cash flow of $365 million. Return on invested capital approaching infinity because there was almost no capital required. VeriSign had become a money-printing machine disguised as a technology company.

D. James Bidzos, who had returned as CEO in 2011 after Roper's departure, would later describe the transformation: "We went from being a company that did many things poorly to a company that does one thing perfectly. We run the heart of the internet's infrastructure with 100% uptime. That's our only job, and we're the only ones who can do it."

The great simplification was complete. VeriSign had shed $2 billion in revenue to focus on a $680 million business. By traditional metrics, it was corporate suicide. By monopoly metrics, it was genius. The stage was set for one of the great capital allocation stories in corporate history.

VIII. The .com/.net Monopoly Machine: How the Business Works

To understand VeriSign's business model, imagine you owned every phone book in the world, and anyone who wanted to look up a phone number had to pay you a fee—not to buy the book, but just to check if a number existed. Now imagine this phone book updated itself automatically, never needed reprinting, and you could raise prices whenever you wanted because there were no other phone books allowed.

That's VeriSign's registry business, except instead of phone numbers, it's domain names, and instead of one lookup, it's 200 billion per day.

Here's how the machine actually works:

At the core are 13 root servers that form the backbone of the internet's Domain Name System. VeriSign operates two of the Internet's thirteen "root servers" which are identified by the letters A-M (VeriSign operates the "A" and "J" root servers). The root servers form the top of the hierarchical Domain Name System that supports most modern Internet communication. When you type "amazon.com" into your browser, your request eventually traces back to one of these servers to find out where amazon.com actually lives on the internet.

But VeriSign's real monopoly isn't the root servers—it's the authoritative registry for .com and .net domains. Every single .com and .net domain name in existence is stored in VeriSign's database. When GoDaddy or any other registrar sells you "mybusiness.com," they're not actually storing that information—they're sending it to VeriSign, who adds it to the master list and charges the registrar a wholesale fee.

The technical architecture is deceptively simple. VeriSign maintains two primary data centers in Virginia and California, with multiple backup facilities around the world. The entire .com zone file—the complete list of every .com domain and where it points—is only about 15 gigabytes. You could fit it on a USB stick. But this small file is the phonebook for most of the commercial internet.

The economics of this business are breathtaking. VeriSign charges registrars $9.59 per year for each .com domain (after several price increases from the original $6). With approximately 160 million .com domains and 13 million .net domains, that's over $1.6 billion in annual revenue. The marginal cost of adding one more domain to the database? Effectively zero. The cost of looking up a domain? Measured in fractions of pennies.

Operating costs are primarily data center infrastructure, network capacity, and security. VeriSign processes over 200 billion DNS queries per day, but modern servers can handle millions of queries per second. The entire technical infrastructure probably costs less than $200 million per year to operate. Everything else is profit. But the real genius of the monopoly isn't just the current pricing—it's the pricing power. After the contract was renewed again in 2012, ICANN was planning to give VeriSign the exact same deal including the same price-rising rights, but the US government intervened and said the contract should not include any price increases. As such, the wholesale price of a dot-com was steady at $7.85 from 2012 to 2020.

Then came the game-changer. The 2018 amendment repealed Obama-era price controls and provided VeriSign the pricing flexibility to change its .com Registry Agreement with ICANN to increase wholesale .com prices, specifically permitting VeriSign to pursue with ICANN an up to 7 percent increase in the prices for .com domain names, in each of the last four years of the six-year term of the .com Registry Agreement.

Think about the math here. A 7% annual increase compounded over four years means prices rise by 31% total. On a base of 160 million domains, each dollar of price increase is $160 million in pure profit. By 2024, VeriSign had raised the wholesale price from $7.85 to $10.26—generating an extra $385 million annually with zero additional cost.

The contract structure itself is a masterpiece of regulatory capture. VeriSign has a Cooperative Agreement with the Department of Commerce that gives it the right to operate .com. That agreement references a Registry Agreement with ICANN that sets the specific terms. On Oct. 26, 2018, following a review and deliberation by the U.S. Government, VeriSign and the Department of Commerce entered into an amendment that included an extension of the Cooperative Agreement, with the Department of Commerce noting that the domain name marketplace had grown more dynamic and concluding that it was in the public interest that VeriSign and ICANN may agree to amend the .COM Registry Agreement to permit an increase to the price for .COM registry services, up to a maximum of 7 percent in each of the final four years of each six-year period.

The beauty of this structure is that neither ICANN nor Commerce can unilaterally change it. ICANN can't put the contract out for bid without Commerce approval. Commerce can't force a change without ICANN agreement. And VeriSign has contracts with both that essentially give it veto power over any changes. It's a three-way deadlock where the status quo—VeriSign's monopoly—always wins.

The technical excellence is real and serves as both justification and moat. VeriSign has achieved 100% availability for the .com/.net DNS for over 26 continuous years. Not 99.999%. One hundred percent. Zero downtime. In an industry where five nines (99.999%) is considered excellent, VeriSign has delivered perfection for longer than Google has existed.

This isn't an accident. VeriSign operates two of the thirteen root servers that form the backbone of the internet. They process over 200 billion queries per day. They've survived massive DDoS attacks, nation-state intrusions, and every technical challenge the internet has thrown at them. When critics say the registry could be run cheaper, VeriSign responds: "Can you guarantee 100% uptime for three decades?"

The capital allocation strategy that emerges from this model is unlike anything else in technology. VeriSign generates over $900 million in free cash flow annually. They have essentially no capital expenditure requirements—maybe $50 million a year to maintain and upgrade infrastructure. They don't need to acquire companies for growth. They don't need to invest in R&D for new products.

So what do they do with the money? They buy back stock. Massively. VeriSign has reduced its share count from 253 million in 2007 to under 110 million today. They've returned over $10 billion to shareholders through buybacks while the business has gotten stronger. It's the ultimate Warren Buffett business: simple, predictable, with a moat so wide you can't see the other side.

The recent political pressure is real but ultimately toothless. Across 159 million .com registrants, VeriSign's profit margin is nearly 66%, enriching shareholders at registrants' expense, a situation that worsened following a 2018 amendment to the Cooperative Agreement between NTIA and VeriSign, which eliminated NTIA's contractual right to initiate a competitive bidding process for the management of .com TLD registries, granted VeriSign authority to increase prices by up to 7% per year without preapproval or any cost justification, and restricted NTIA's preapproval authority over separate agreements governing price, vertical integration, and other key terms.

But what can regulators actually do? Force a competitive bid for .com? The technical risk would be enormous. Change the pricing terms? VeriSign would sue, arguing breach of contract. The 2016 IANA transition moved oversight from the U.S. government to the global multi-stakeholder community, making unilateral U.S. action even harder.

This is the perfect monopoly: legally sanctioned, technically justified, diplomatically protected, and financially optimized. It's a business that prints money while serving a critical function that nobody wants to risk disrupting. Every time you type ".com," VeriSign collects its toll. And that toll road isn't going anywhere.

IX. Competition, Controversies & Political Battles

The question haunts every discussion about VeriSign: Why doesn't the U.S. government just put the .com contract out for competitive bidding?

The answer reveals everything about how modern monopolies work—not through secret cabals or outright corruption, but through a combination of technical excellence, regulatory capture, and the profound human tendency to avoid catastrophic risk. The numbers are stark. Consider a recent bid to manage the registry for India's .in domain name—Neustar bid just 70 cents per domain while its rival Afilias offered to run it for $1.65 per domain. These are competent registry operators that run .us, .biz, .co, .info, and hundreds of other top-level domains. Even being generous and assuming that .com's scale and importance would require a $3.50 per domain fee, consumers across the globe are paying about $600 million in extra fees per year than necessary.

VeriSign charges $10.26. Competitors say they could do it for $2. That's an $8 difference per domain, times 160 million domains—$1.3 billion in what economists would call "economic rent," profit extracted not from value creation but from monopoly position.

Yet the contract never goes out for bid. Why?

The answer lies in what I call the "nobody ever got fired for buying IBM" principle applied to critical infrastructure. Imagine you're the bureaucrat at the Department of Commerce responsible for this decision. If you keep VeriSign and nothing goes wrong, nobody notices. If you switch to a cheaper provider and there's even five minutes of downtime, you're the person who broke the internet to save a few dollars. The Washington Post writes about you. Congress holds hearings. Your career is over.

VeriSign knows this and has built their entire political strategy around it. Their lobbying isn't crude—they don't need to wine and dine politicians or make huge campaign contributions. Instead, they focus relentlessly on one message: "We've run .com for 26 years with 100% uptime. Why risk it?"

The technical argument is powerful because it's partially true. VeriSign has built so much redundancy globally to keep 100% uptime for .com/.net resolution—it would be a multi-year effort for anyone to match that level of redundancy. .com has grown so big that transferring it to another registry could be catastrophic. The burden on businesses for registry fees is negligible compared to what they spend on operations, but the risk of disruption is existential.

But this argument conceals a deeper truth: VeriSign's technical excellence is both real and strategically cultivated. They deliberately over-engineer the system not just for reliability, but to make the replacement cost seem astronomical. It's like a medieval castle builder who makes the walls not just strong enough to repel invaders, but so imposing that nobody even considers attacking.

The political battles follow a predictable pattern. Every few years, when the contract comes up for renewal, a coalition forms to challenge VeriSign's monopoly. In 2018, the American Economic Liberties Project released a paper calling for an end to VeriSign's control. Senator Elizabeth Warren and Rep. Jerry Nadler wrote letters complaining that VeriSign overcharges for .com domains due to its market power. Domain registrars organize and file comments with ICANN. Op-eds appear in tech publications.

And then... nothing happens.

The 2018 amendments were particularly revealing. Under the Trump administration, NTIA eliminated its contractual right to initiate a competitive bidding process for the management of .com TLD registries, granted VeriSign authority to increase prices by up to 7% per year without preapproval or any cost justification, and restricted NTIA's preapproval authority over separate agreements. Rather than increasing oversight, the government reduced it.

The lobbying is sophisticated and multi-layered. VeriSign doesn't just lobby Congress—they engage with ICANN, the Department of Commerce, NTIA, the Department of Justice, international telecommunications bodies, and foreign governments. They sponsor research on DNS security. They fund conferences on internet governance. They've made themselves indispensable to the ecosystem they're supposed to serve.

But perhaps the most brilliant aspect of VeriSign's political strategy is how they've structured the contracts to create a three-way deadlock. ICANN can't change the registry agreement without Commerce approval. Commerce can't force changes without ICANN agreement. And both have contracts with VeriSign that essentially give the company veto power. It's a Gordian knot of legal agreements that would take years of litigation to untangle.

The international dimension adds another layer of complexity. The internet is global, but .com is controlled by an American company under contracts with the American government. Foreign governments and businesses increasingly resent this, but their complaints actually strengthen VeriSign's position. American policymakers fear that putting .com out for bid might result in a non-American company winning, which would be politically unacceptable. Better to stick with the devil you know.

The recent criticism from Warren and Nadler is interesting not for what it might accomplish—which is likely nothing—but for what it reveals about the limits of political pressure on natural monopolies. VeriSign's response is always the same: we provide critical infrastructure at a reasonable price with perfect reliability. The fact that "reasonable" means a 65% profit margin is beside the point. In the logic of Washington, risk avoidance trumps economic efficiency every time.

This is why VeriSign's executives can be so confident about their future. As long as they maintain technical excellence, avoid scandals, and keep prices just below the threshold of congressional hearings, their monopoly is secure. They've discovered the sweet spot of rent extraction: high enough to generate enormous profits, low enough that the pain is distributed across millions of customers who each pay too little to care.

The .com monopoly isn't maintained by force or fraud. It's maintained by a collective action problem, risk aversion, and the tremendous power of institutional inertia. Every participant in the system has reasons to want change, but nobody has sufficient incentive to bear the cost and risk of forcing it. It's a monopoly perfected for the modern age: legally bulletproof, politically untouchable, and economically extractive while appearing to provide an essential public service.

Which, of course, it does. That's the beautiful paradox of VeriSign's position. They really do run critical infrastructure. They really do it well. They just charge five times what it's worth, and there's absolutely nothing anyone can do about it.

X. Recent Developments & The Modern Era (2018-Present)

October 26, 2018, should have been a day of reckoning for VeriSign. The Cooperative Agreement with the Department of Commerce was up for renewal, and critics had spent months building their case. Letters flooded NTIA from domain investors, small businesses, and consumer advocates. The message was unanimous: don't let VeriSign raise prices again.

David Redl, head of NTIA under the Trump administration, had a different idea.

Amendment 35 didn't just renew VeriSign's contract—it fundamentally rewired the power dynamics of internet governance. The amendment repealed Obama-era price controls and granted VeriSign pricing flexibility to pursue with ICANN up to 7 percent increases in .com prices in each of the last four years of each six-year term. But that wasn't the shocking part.

The real bombshell was what Amendment 35 removed: NTIA's contractual right to initiate a competitive bidding process. The U.S. government voluntarily gave up its ability to ever put .com out for bid. It was as if the government had granted AT&T a permanent monopoly on phone service and promised never to consider alternatives.

The reaction was swift and furious. "This is a disaster for responsible government oversight," declared the American Economic Liberties Project. Domain investors calculated the damage: a 7% annual increase compounded over four years meant a 31% total price hike, extracting an extra $385 million annually from registrants. But the deal was done. Meanwhile, VeriSign was playing a different game entirely. In July 2016, ICANN held an auction for .web—potentially the most valuable new domain extension since .com itself. The winning bid was $135 million, three times higher than the previous record for a top-level domain. The winner was Nu Dot Co LLC, a company nobody had heard of.

Within a week, VeriSign revealed in an SEC filing that it had provided the funds for Nu Dot Co's bid. The company entered into an agreement with Nu Dot Co LLC wherein VeriSign provided funds for Nu Dot Co's bid for the .web TLD, with the plan that Nu Dot Co would execute the .web Registry Agreement with ICANN and then seek to assign it to VeriSign.

The other bidders—including Google, Afilias, and Donuts—were furious. They'd been bidding against what they thought was another startup, not the $11 billion gorilla that already controlled .com. The Department of Justice launched an antitrust investigation. Lawsuits flew. ICANN's independent review process was invoked.

But here's the remarkable thing: after seven years of litigation and review, VeriSign won. In May 2023, the ICANN Board of Directors concluded that VeriSign's participation with Nu Dot Co in the 2016 .web auction was appropriate and within ICANN's policies and guidelines. The $135 million gambit had worked.

The .web saga revealed something important about VeriSign's strategy in the modern era. They weren't content to just milk .com and .net. They wanted to ensure that no competitor could ever emerge. Paying $135 million for .web—which industry experts said would never turn a profit at that price—wasn't about making money from .web. It was about preventing .web from becoming an alternative to .com.

The 2016 IANA transition marked another crucial moment. The Department of Commerce ended its role in managing the Internet's DNS and transferred full control to ICANN. This was supposed to internationalize internet governance, but for VeriSign, it meant one less potential source of regulatory pressure. ICANN chose to continue VeriSign's role as the root zone maintainer, and the two entered into a new contract in 2016.

By 2020, VeriSign had achieved something remarkable: after years of price freezes, they'd regained the ability to raise prices. The wholesale price of a .com domain rose from $7.85 to $8.39, then $8.97, then $9.59, and by 2024, $10.26. Each increase was exactly 7%—the maximum allowed under the contract. It was like watching a perfectly calibrated extraction machine at work.

The financial results were staggering. Revenue grew from $1.2 billion in 2018 to $1.5 billion in 2023, despite the number of domains growing only modestly. Operating margins expanded from 61% to 65%. Free cash flow exceeded $700 million annually. VeriSign had become one of the most profitable companies on Earth by any measure.

The stock buyback program accelerated. VeriSign repurchased $4.7 billion worth of shares between 2018 and 2023, reducing the share count by another 20 million. With a business that required essentially no capital investment and generated torrents of cash, the only question was how fast they could buy back stock without moving the market.

Warren Buffett, who rarely invests in technology companies, quietly built a position worth over $2 billion. For Buffett, VeriSign was the perfect business: simple to understand, impossible to disrupt, with pricing power and a management focused on capital allocation. It was a toll bridge for the digital age.

The political pressure continued but remained ineffective. In 2024, Senator Warren and Representative Nadler sent another letter complaining about VeriSign's monopoly. The American Economic Liberties Project released another report. NTIA expressed "questions related to pricing in the .com market" but renewed the Cooperative Agreement anyway.

The reason nothing changes is structural, not political. ICANN needs VeriSign's money—the company provides millions in funding for ICANN's operations. The Department of Commerce fears the technical risk of transition. International stakeholders worry about U.S. government control but also fear losing U.S. technical expertise. Every player in the system has reasons to preserve the status quo.

As we entered 2024, VeriSign announced another 7% price increase, bringing the wholesale price to $10.26. The company was on track to generate $1.6 billion in revenue with margins approaching 70%. The .web domain remained in limbo, but VeriSign had successfully prevented it from becoming a competitor. The political theater continued, but the monopoly machine ground on, extracting its toll from every .com domain on the internet.

The modern era of VeriSign is defined not by innovation or growth, but by optimization of extraction. Every decision—from the .web acquisition to the price increases to the massive buybacks—is designed to maximize the value captured from their monopoly position. It's capitalism perfected, if your definition of perfection is converting market power into shareholder returns with ruthless efficiency.

XI. Playbook: The Perfect Monopoly

If you wanted to build VeriSign from scratch today, you couldn't. Not because the technology is complex—any competent engineer could build a domain registry. Not because the capital requirements are prohibitive—the entire infrastructure might cost $100 million. The reason you couldn't build VeriSign is that the conditions that created it no longer exist and will never exist again.

VeriSign's monopoly is what economists call a "natural monopoly," but it's more than that. It's a perfect monopoly—one that combines technical necessity, regulatory capture, network effects, and historical accident into an unassailable competitive position. Let's break down the playbook:

Step 1: Be There at the Beginning

VeriSign (through Network Solutions) wasn't just early to domain names—they were there before it was even a business. When the NSF put the domain contract out for bid in 1993, Network Solutions was the only bidder because nobody else saw value in maintaining a list of academic computer names. This is the crucial lesson: the best monopolies are built before anyone realizes there's something to monopolize.

Step 2: Convert Public Infrastructure to Private Property

The master stroke was convincing the government to let Network Solutions charge for something that had been free. In 1995, they got permission to charge $100 for two-year domain registrations. Overnight, a public good became private property. The protests were fierce, but the precedent was set: someone could own the right to sell internet addresses.

Step 3: Create Technical Lock-In Before Regulatory Lock-In

VeriSign built their technical infrastructure to be so robust that replacing it seemed riskier than overpaying for it. 100% uptime for 26 years isn't just a technical achievement—it's a regulatory moat. Every time someone suggests putting .com out for bid, VeriSign points to their perfect record. Who wants to be the bureaucrat who broke the internet to save money?

Step 4: Transform Competition into Cooperation

When ICANN formed to introduce competition, VeriSign could have fought it. Instead, they embraced the separation of registry and registrar, selling off the competitive registrar business to focus on the monopoly registry. They turned potential competitors (registrars) into customers who had no choice but to buy from them.

Step 5: Lose Battles to Win Wars

The Site Finder controversy looked like a disaster—VeriSign was forced to shut down the service and paid $625,000 in legal fees. But the resulting settlement gave them presumptive renewal rights and pricing power. VeriSign learned that in regulated industries, the best outcome isn't winning every fight—it's getting the rules written in your favor.

Step 6: Make Yourself Indispensable to Your Regulator

VeriSign doesn't just operate under ICANN's oversight—they fund ICANN's operations. They provide technical expertise ICANN lacks. They've made ICANN dependent on them financially and operationally. When your regulator needs you more than you need them, you've won.

Step 7: Price Below the Pain Threshold

VeriSign could probably charge $20 per domain without losing significant volume. But that would trigger congressional hearings and real regulatory scrutiny. Instead, they charge $10.26—high enough to generate 65% margins, low enough that the pain is diffused across millions of customers. It's the "boiling frog" approach to monopoly pricing.

Step 8: Eliminate Future Competition Before It Emerges

The $135 million .web acquisition made no financial sense—VeriSign will never recoup that investment from .web revenues. But that wasn't the point. The point was to prevent .web from becoming a credible alternative to .com. Sometimes the best investment is the one that prevents competition from emerging.

Step 9: Focus Relentlessly on One Thing

VeriSign sold off everything that wasn't the registry business—certificates, security services, telecom products. They went from $2 billion in revenue to $680 million. Wall Street hated it. But by focusing solely on the registry, they transformed margins from 20% to 65%. The lesson: monopolies should do one thing perfectly rather than many things well.

Step 10: Return Capital Aggressively

VeriSign has bought back over $10 billion in stock, reducing share count by 60%. They could have used that money for acquisitions, R&D, or expansion. Instead, they recognized that their monopoly was already perfect—the only thing left was to return capital to shareholders. It's the ultimate admission: we have a money-printing machine that doesn't need investment.

The Moat System

VeriSign's competitive moat isn't just one thing—it's a system of interlocking advantages:

- Technical: 26 years of 100% uptime creates switching risk

- Contractual: Presumptive renewal rights make competition illegal

- Financial: 65% margins allow unlimited defense spending

- Political: Regulatory capture through funding and expertise

- Psychological: "Nobody gets fired for choosing VeriSign"

- Network Effects: Every .com domain makes .com more valuable

- Switching Costs: Moving 160 million domains would be catastrophic

Why This Can't Be Replicated

The conditions that created VeriSign's monopoly were unique to the 1990s internet:

- Regulatory Naivety: Governments didn't understand the internet's importance

- Technical Ignorance: Policymakers couldn't evaluate technical arguments

- Lack of Precedent: No one knew how to price or regulate digital infrastructure

- Speed of Change: The internet grew faster than regulatory frameworks

- American Dominance: The U.S. controlled internet governance unilaterally

Today, every government understands the strategic importance of digital infrastructure. New protocols are developed through open standards. Competition authorities scrutinize digital markets. The window for creating a VeriSign-style monopoly has closed forever.

The Ultimate Business Model

VeriSign has achieved something remarkable: a legal monopoly on critical infrastructure with pricing power, no competition, no capital requirements, and no need for innovation. They collect $10.26 per year from 160 million domains for maintaining a database that fits on a thumb drive.

It's not creative. It's not innovative. It doesn't change the world or solve grand challenges. But as a business model, it's perfect. VeriSign has discovered the capitalist philosopher's stone: how to turn bits into gold, forever, with no one able to stop them.

The playbook can't be replicated, but it can be studied. Every element—from regulatory strategy to capital allocation—is executed with precision. VeriSign didn't stumble into their monopoly. They engineered it, defended it, and optimized it into the most perfect extraction machine in technology.

XII. Analysis & Investment Perspective

At $217 per share in late 2024, VeriSign trades at roughly 25 times earnings—expensive for most companies, but arguably cheap for a legalized monopoly with pricing power. The investment case for VeriSign isn't about growth or innovation. It's about whether you believe the monopoly will persist and what that stream of cash flows is worth.

The Bull Case: The Toll Road That Can't Be Bypassed

The bulls see VeriSign as Warren Buffett does: a wide-moat business with predictable cash flows trading at a reasonable multiple. The math is compelling. With 173 million domains under management growing at 2-3% annually, and the ability to raise prices 7% per year, revenue growth of 5-10% is essentially guaranteed through 2028.

Operating leverage is tremendous. Revenue can grow 10% with essentially zero increase in costs, meaning incremental margins approach 100%. As revenue grows from $1.5 billion to $2 billion over the next five years, nearly all of that incremental $500 million drops to the bottom line.

The capital allocation is perfect for shareholders. With no need for capital investment and limited acquisition opportunities, VeriSign returns essentially all free cash flow through buybacks. At current prices, they can retire 3-4% of shares annually. Combine that with 5-10% revenue growth and margins expanding toward 70%, and earnings per share could compound at 15%+ annually.

The regulatory moat has proven impenetrable. Despite decades of complaints, congressional letters, and advocacy group pressure, nothing has changed. The 2018 Cooperative Agreement amendments actually strengthened VeriSign's position by eliminating the possibility of competitive bidding. Short of legislative action—which would require Congress to understand and care about domain name pricing—the monopoly is secure.

The technical risk argument becomes stronger over time. As .com approaches 200 million domains, the operational complexity of managing the registry increases exponentially. VeriSign processes over 200 billion queries daily with perfect reliability. The cost of even an hour of .com downtime to the global economy would dwarf decades of "overpayment" to VeriSign.

International pressure actually helps VeriSign. Foreign governments complain about U.S. control of .com, which makes U.S. policymakers more likely to keep VeriSign—an American company—in charge. It's better to have a domestic monopolist than risk .com falling under foreign influence.

The Bear Case: The Monopoly's Achilles' Heel

The bears see existential risks that the market is ignoring. The primary threat isn't competition—it's political. VeriSign exists at the pleasure of the U.S. government. One motivated Commerce Secretary or NTIA Administrator could unravel the entire structure. The Biden administration has shown unprecedented willingness to challenge corporate concentration. Why wouldn't they target the most obvious monopoly in technology?

The pricing power that bulls celebrate could trigger the political response bears fear. When VeriSign raises prices to $13.45 by 2028—70% higher than the 2020 price—the cumulative extraction from domain owners will exceed $500 million annually. At some point, the pain becomes acute enough to motivate political action.

Alternative naming systems pose a long-term threat. Blockchain-based naming systems like ENS (Ethereum Name Service) offer decentralized alternatives to DNS. While adoption is minimal today, the technology exists to route around VeriSign's monopoly. If major browsers started supporting alternative naming systems natively, .com's dominance could erode quickly.

The concentration risk is extreme. VeriSign is essentially a single-product company. They have no diversification, no growth options, and no ability to pivot if the domain name business is disrupted. It's the ultimate binary bet: either the monopoly persists and shareholders get rich, or it doesn't and the equity is worth zero.

The valuation already prices in perfection. At 25 times earnings for a business growing revenue at 5%, VeriSign is priced like a high-growth technology company, not a utility. Any hiccup—a regulatory change, a security breach, even a sustained period of domain decline—could trigger a massive revaluation.

The Realist Perspective: Valuing a Government-Sanctioned Monopoly

The truth, as usual, lies between the extremes. VeriSign is neither an eternal monopoly nor a political time bomb. It's a regulated utility that happens to be extraordinarily profitable due to historical accidents and regulatory capture.

The proper valuation framework isn't traditional DCF or comparable company analysis. VeriSign should be valued like a long-dated bond with uncertain maturity. The cash flows are predictable—$700+ million in free cash flow growing at 5-10% annually. The question is duration: Will these cash flows persist for 5 years? 10 years? Forever?

A probability-weighted approach makes sense. Assign a 60% probability to the status quo persisting (monopoly continues, prices rise, cash flows compound). Assign a 30% probability to regulatory intervention (price freezes, margins compress to 40%). Assign a 10% probability to catastrophic disruption (competitive bidding, technology shift).

Under this framework, VeriSign's fair value is probably $180-250 per share—a wide range reflecting the binary nature of the outcomes. The current price of $217 suggests the market is pricing in a 70% probability of monopoly persistence, which seems reasonable given the historical evidence.

The ESG Question Nobody Wants to Ask

VeriSign presents a fascinating ESG dilemma. On environmental grounds, they're exemplary—running digital infrastructure with minimal carbon footprint. On social grounds, they maintain critical internet infrastructure with perfect reliability. But on governance grounds, they're extracting monopoly rents from every business with a .com domain.

Is it ethical to invest in a company whose business model is essentially a tax on internet commerce? VeriSign would argue they provide essential infrastructure at a reasonable price. Critics would say they're extracting $600 million annually in excess profits that could otherwise flow to businesses and consumers.

The governance structure itself is a masterpiece of entrenchment. The board is staggered, takeovers are virtually impossible, and management has aligned interests through substantial equity ownership. Shareholders have benefited enormously, but other stakeholders—domain registrants, small businesses, entrepreneurs—subsidize those returns.

What Would Buffett Do?

Warren Buffett owns $2.6 billion worth of VeriSign, making it one of Berkshire Hathaway's top 20 holdings. For Buffett, the investment thesis is simple: predictable cash flows, rational capital allocation, and a moat so wide you can't see the other side.

Buffett doesn't care about innovation or disruption. He cares about certainty. And VeriSign offers something precious in investing: the closest thing to certainty that exists in public markets. As long as the internet uses domain names, and as long as .com remains the standard for commercial websites, VeriSign will print money.

The investment decision ultimately comes down to your view of political risk. If you believe American regulatory capture is as permanent as VeriSign's supporters suggest, the stock is undervalued. If you believe political pressure will eventually force change, it's overvalued. There's no middle ground—this is a binary bet on the permanence of a government-sanctioned monopoly.

XIII. Power & Lessons

Through the lens of Hamilton Helmer's "7 Powers" framework, VeriSign possesses something remarkable: not just one or two competitive advantages, but arguably all seven powers simultaneously. It's the business strategy equivalent of a royal flush.

Scale Economies: VeriSign operates at a scale that makes competition economically irrational. Managing 173 million domains across a global infrastructure of root servers and data centers, their per-domain cost approaches zero while competitors would need massive upfront investment. The first domain costs billions to serve; the 173 millionth costs nothing.

Network Effects: Every .com domain makes .com more valuable. It's the standard because it's the standard—a self-reinforcing cycle that strengthens with each registration. Businesses choose .com because customers expect .com. The network effect is so strong that even cheaper alternatives can't break through.

Counter-Positioning: VeriSign's business model makes competition structurally impossible. A challenger would need to invest hundreds of millions in infrastructure to compete for a contract that might never be put out for bid. It's like challenging someone to a duel where only your opponent is allowed to have a weapon.

Switching Costs: Moving 173 million domains to a new registry would be the digital equivalent of rewiring the entire internet. Every website, email server, and online service would need updating. The technical risk alone makes switching unthinkable, regardless of potential cost savings.

Branding: "Powered by VeriSign" might not mean much to consumers, but to infrastructure decision-makers, VeriSign equals reliability. Twenty-six years of 100% uptime has created a brand synonymous with "don't worry, it won't break."

Cornered Resource: VeriSign owns the exclusive right to .com and .net through contracts that explicitly prevent competition. It's not just a competitive advantage—it's a legal prohibition on competition. They've cornered the most valuable resource in digital commerce: the namespace itself.

Process Power: Twenty-six years of operating the registry has created institutional knowledge that can't be replicated. Every edge case, every attack vector, every scaling challenge has been solved and embedded in their operations. A competitor wouldn't just need to match VeriSign's technology—they'd need to recreate decades of learning.

The Meta-Lesson: Power Compounds

The profound insight from VeriSign isn't that they have these powers, but how they reinforce each other. Scale economies fund the infrastructure that ensures reliability, which strengthens the brand, which justifies regulatory capture, which protects the cornered resource, which generates cash for further scale. It's a flywheel where every revolution makes the next one easier.

Lessons for Founders

1. The best businesses are built before markets exist. Network Solutions got the domain contract when nobody wanted it. By the time everyone realized domains were valuable, the monopoly was established. The lesson: build infrastructure for futures nobody else sees.

2. Boring is beautiful. VeriSign runs a database. That's it. No AI, no blockchain, no metaverse. They do one boring thing perfectly. In a world obsessed with innovation, sometimes the best strategy is aggressive simplicity.

3. Technical excellence is the ultimate moat. VeriSign's 100% uptime isn't just an operational metric—it's a regulatory shield. When you're so good at operations that failure seems impossible, regulators won't risk replacing you.

4. Sometimes the customer is the government. VeriSign's real customer isn't domain buyers—it's ICANN and the Department of Commerce. They optimized for regulatory approval, not user satisfaction. In regulated industries, the regulator is your most important stakeholder.

5. Capital allocation is strategy. VeriSign could have used their cash for acquisitions, R&D, or expansion. Instead, they bought back stock. The message was clear: our business is already perfect, we just need to return capital. Sometimes the best growth strategy is not to grow.

Strategic Positioning: The Art of Becoming Inevitable

VeriSign's strategic master stroke was recognizing that in infrastructure, being second-best is worthless. They didn't try to be slightly better than competitors—they made competition conceptually impossible. How do you compete with someone who has a government contract prohibiting competition?

The company understood something profound about infrastructure: it's not about winning customers, it's about becoming part of the physics of the system. VeriSign doesn't compete in the domain name market—they ARE the domain name market. It's like trying to compete with gravity.

When to Fight vs. When to Settle

VeriSign's history is littered with battles—Site Finder, the ICANN lawsuit, the .web acquisition challenges. But notice the pattern: they fought hard initially, then settled on favorable terms. They understood that in regulatory battles, the goal isn't total victory—it's getting the rules written in your favor.

The Site Finder settlement looked like a loss—they shut down the service and paid $625,000. But they got presumptive renewal rights and pricing power in return. The lesson: in regulated industries, losing tactical battles while winning strategic wars is the path to monopoly.

The Compounding Value of Operational Excellence

Here's what most people miss about VeriSign's 100% uptime: it compounds. Every day without an outage makes the next outage less likely—not technically, but politically. After 26 years of perfection, who would risk being the person who broke it?

This is the ultimate lesson from VeriSign: operational excellence isn't just about operations—it's about creating political economy dynamics that make your position unassailable. When you're so reliable that replacing you seems reckless, you've won before the competition starts.

The Dark Side of Perfect Strategy

There's something unsettling about VeriSign's perfection. They've executed flawlessly on a strategy to extract maximum value while providing minimum innovation. They're the platonic ideal of rent-seeking—collecting tolls on infrastructure they didn't build for value they don't create.

The lesson for society is sobering: perfect business strategy and public good can be orthogonal. VeriSign is a masterclass in corporate strategy and a cautionary tale about market structure. They've proven that with the right positioning, a company can tax the entire internet forever.

The Ultimate Question