Verisk Analytics: The Data Monopoly That Powers Insurance

I. Introduction & Framing

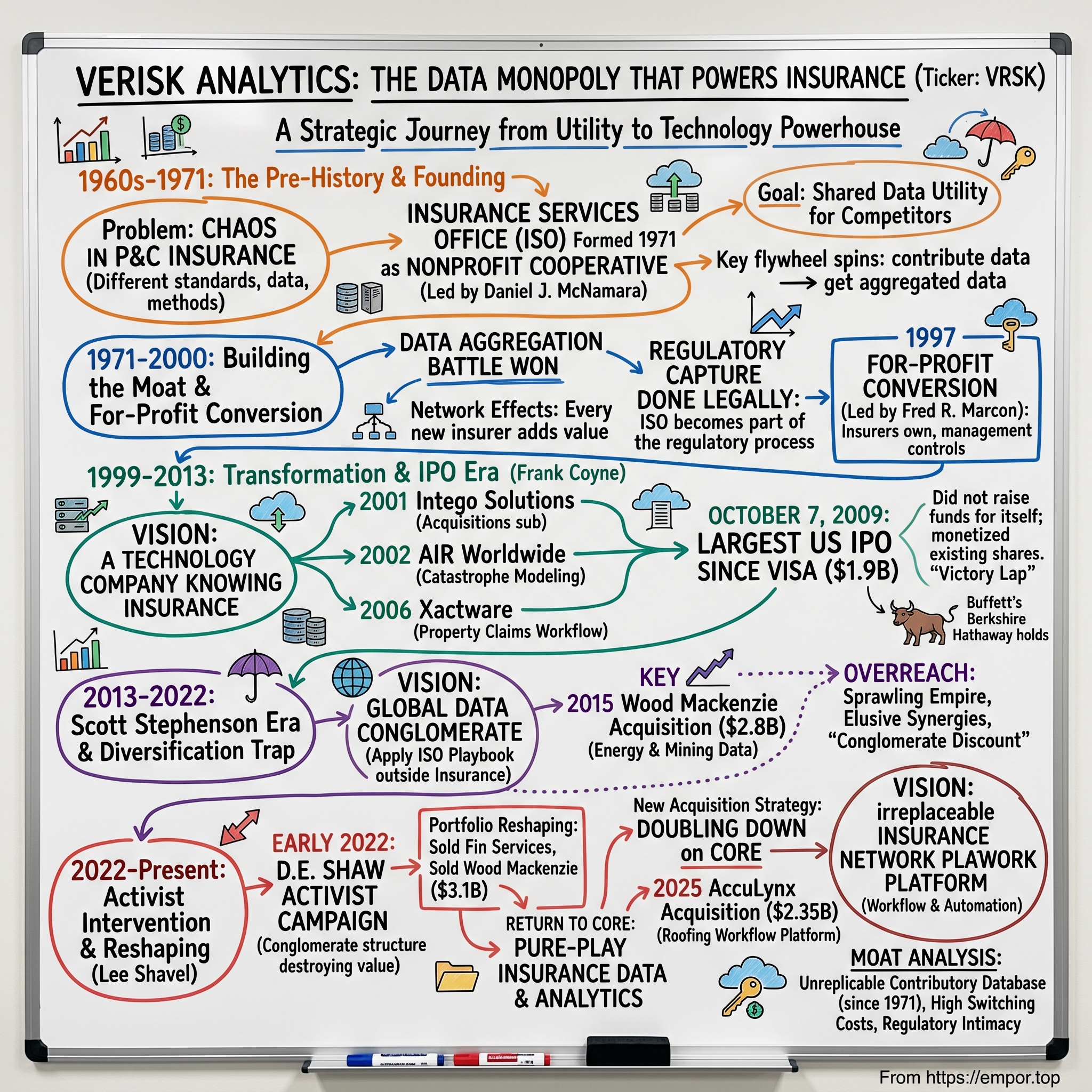

Picture this: It's October 7, 2009, the depths of the financial crisis. Banks are collapsing, credit markets are frozen, and IPOs have become extinct. Yet on this day, a company most Americans have never heard of rings the opening bell at the Nasdaq, raising $1.9 billion in the largest U.S. IPO since Visa went public eighteen months earlier. The stock, priced at $22, immediately jumps 20%. Warren Buffett's Berkshire Hathaway, a major shareholder, doesn't sell a single share.

The company? Verisk Analytics—a data provider so deeply embedded in the insurance industry that virtually every property and casualty policy written in America touches its systems. How did a boring insurance data cooperative, founded in 1971 as a non-profit industry association, transform into a $36 billion technology monopoly that commands pricing power even Warren Buffett respects?

This is the story of how Insurance Services Office (ISO) built one of the most powerful network effects in business history—not through social media or marketplace dynamics, but through something far more mundane: standardized insurance forms and shared actuarial data. It's a tale of strategic patience, regulatory capture done legally, and the counterintuitive insight that sometimes the best monopolies are built by helping your customers compete with each other. The roadmap ahead: We'll trace how a nonprofit industry cooperative systematically built switching costs so high that even trillion-dollar insurance companies can't escape its gravitational pull. We'll examine the brilliant capital allocation decisions, the strategic missteps into unrelated businesses, and the activist intervention that brought the company back to its core. Most importantly, we'll unpack the lessons for building essential infrastructure in regulated industries—a playbook that applies far beyond insurance.

Because here's what makes Verisk truly fascinating: It raised $1.9 billion in its 2009 IPO, making it the largest IPO by a U.S. company since Visa's IPO in early 2008, yet the firm did not raise any funds for itself. Every penny went to selling shareholders. The company didn't need capital—it had already won. The IPO was simply the victory lap, allowing insurance companies to monetize the monopoly they had accidentally created by cooperating with each other.

II. The Pre-History: Why ISO Had to Exist (1960s-1971)

The year is 1969. Neil Armstrong has just walked on the moon, Woodstock defines a generation, and in the decidedly less glamorous world of property and casualty insurance, chaos reigns. Picture an insurance executive in Hartford trying to price homeowners' policies across fifty states. Each state has its own rating bureau with different forms, different data standards, different actuarial methodologies. A single national insurer might need to file rates with dozens of separate organizations, each speaking its own statistical language.

This wasn't just inefficient—it was dangerous. Without standardized data, insurers couldn't accurately price risk. Too high, and they'd lose business to competitors. Too low, and they'd face insolvency when catastrophes struck. The industry needed what computer scientists would later call a "protocol layer"—a common language for describing and pricing risk.

Enter Daniel J. McNamara, a career insurance executive who understood both the technical complexities of actuarial science and the political realities of state regulation. McNamara had spent years watching insurers duplicate each other's efforts, each company maintaining its own loss data, policy forms, and rating algorithms. He saw an opportunity hiding in plain sight: What if competitors could share non-competitive information while still competing fiercely on price and service?

The Insurance Services Office (ISO) was formed in 1971 to provide a "one-stop shop" for statistical information to member insurers, founded on April 1 under the leadership of Daniel J. McNamara, who remained president of the company until his retirement in 1987. The founding wasn't a Silicon Valley garage startup story—it was a careful orchestration involving hundreds of insurance companies, state regulators, and industry associations.

The genius of the ISO model lay in its structure as a nonprofit cooperative. Insurance companies weren't buying from a vendor; they were contributing to a shared utility. This distinction proved crucial for regulatory approval. State insurance commissioners, always suspicious of industry collaboration that might reduce competition, could hardly object to a nonprofit that would make the market more efficient and transparent.

McNamara's masterstroke was recognizing that insurance companies desperately wanted to cooperate on data while competing on everything else. They needed common policy language so customers could compare offerings. They needed aggregated loss data to price rare events. They needed standardized forms that regulators would accept across state lines. But no single insurer could build this infrastructure alone—the network effects only worked if everyone participated.

The initial value proposition was simple but powerful: contribute your loss data, get back the aggregated data of the entire industry. It was like a primitive blockchain for insurance information—distributed, tamper-resistant through regulatory oversight, and valuable only through collective participation. The more insurers that joined, the more valuable the data became. The flywheel began to spin.

By standardizing policy language, ISO solved a problem insurers didn't even realize was costing them billions. Before ISO, every insurer maintained teams of lawyers and actuaries to draft state-specific policy forms. Post-ISO, they could use standardized forms with minor modifications. The savings were immediate and substantial. More importantly, standardization made the insurance market more liquid—customers could actually compare policies, regulators could evaluate rates more easily, and reinsurers could better understand the risks they were assuming.

By the end of its 25th year, ISO was recognized as a leader in using data to help the U.S. insurance industry make smarter decisions. But this understates the transformation. ISO hadn't just improved decision-making; it had become the central nervous system of American property and casualty insurance. Every rate filing, every policy form, every actuarial calculation flowed through its systems. The industry utility had quietly become indispensable infrastructure.

III. Building the Monopoly: The ISO Years (1971-2000)

The conference room at ISO's Pearl River, New York headquarters, circa 1985. Daniel McNamara stands before a wall-sized map of the United States, each state color-coded by the depth of ISO's penetration. The nonprofit that started with a handful of insurers now serves over 1,400 companies. But McNamara isn't celebrating—he's explaining to his board why ISO needs to think bigger.

"Gentlemen," he says, pointing to the map, "we've won the data aggregation battle. But data without analytics is just expensive storage. Our members don't just need information—they need insight."

This moment marked ISO's evolution from data collector to intelligence provider. The contributory database model had created an unassailable moat: insurers contributed claims data because they needed the aggregated industry data to price policies accurately. But McNamara saw that raw data was just the beginning. The real value lay in turning that data into actionable intelligence.

The network effects were beautiful in their simplicity. Every new insurer that joined didn't just add their data—they added unique loss patterns, geographic exposures, and risk correlations that made everyone else's data more valuable. A California earthquake claim helped price Florida hurricane risk through advanced catastrophe modeling. A warehouse fire in Ohio informed coverage decisions for similar structures in Oregon. The database became a living, breathing map of American risk.

But ISO's true genius lay in how it handled the regulatory environment. In an industry where state insurance commissioners wielded enormous power, ISO positioned itself as their ally, not their adversary. When regulators needed data to evaluate rate increases, ISO provided it. When they wanted standardized forms to protect consumers, ISO created them. When they demanded transparency in actuarial methods, ISO opened its models for review.

This regulatory alignment created switching costs that went beyond mere economics. An insurer couldn't just decide to leave ISO—they'd need regulatory approval to use non-ISO forms and rates in dozens of states. Regulators, comfortable with ISO's standards and processes, had little incentive to approve alternatives. The nonprofit had essentially achieved regulatory capture, but in reverse: instead of capturing the regulators, it had been captured by them, becoming so essential to the regulatory process that its position was unassailable. The transition from nonprofit to for-profit in 1997 marked a critical inflection point. Insurance Services Office, Inc.'s (ISO) member insurers voted to convert the company to a for-profit stock corporation, with the conversion becoming effective Jan. 1, intended to retain and enhance ISO's value to customers, and maintain ISO's leadership position in the industry. Fred R. Marcon, ISO's chairman, president and CEO, orchestrated this transformation with surgical precision. At a membership meeting, the proposal received 117,837,329 votes out of a total of 162,394,940 eligible votes, or nearly 73 percent of the eligible votes, when a favorable vote of two-thirds of the members' votes was needed for approval.

The ownership structure post-conversion was ingenious: About 85 percent of ISO's outstanding shares would be owned in the form of class B common stock by property/casualty insurers that were ISO members, with ownership of ISO's class A shares restricted to the company's directors and employees, and to the ESOP, while ownership of class B shares was restricted to insurance and reinsurance companies. The insurers owned their captor—but management controlled the board.

By 1995, ISO's revenues had reached $237 million. By 2000, they would exceed $400 million. The for-profit conversion unleashed entrepreneurial energy that had been dormant in the nonprofit structure. But more importantly, it set the stage for what would come next: the transformation from industry utility to technology powerhouse.

IV. The Transformation Begins: Frank Coyne Era (1999-2013)

Frank Coyne arrived at ISO in February 1999 with the demeanor of a Fortune 500 executive and the instincts of a venture capitalist. Standing before ISO's board in early 2000, newly appointed as CEO, he laid out a vision that seemed almost heretical: "We're not a data company serving insurance. We're a technology company that happens to know insurance better than anyone else. "Coyne had joined ISO in February 1999 as president and chief operating officer, became CEO in July 2000, and chairman in 2002. His first major move was both symbolic and strategic: he created Intego Solutions in 2001, a subsidiary designed explicitly for acquisitions, and appointed Scott Stephenson, a senior partner from Boston Consulting Group, to lead it. Stephenson wasn't an insurance insider—he was a strategy consultant who understood technology platforms and network effects. The message was clear: ISO was going shopping, and not just for insurance assets.

The 2002 acquisition of AIR Worldwide marked the beginning of ISO's transformation into a true analytics company. AIR had pioneered catastrophe modeling—using sophisticated algorithms to predict the probability and severity of natural disasters. In an era before climate change dominated headlines, this seemed like an esoteric capability. But Coyne saw what others missed: as weather patterns became more volatile, the ability to model catastrophic risk would become not just valuable but essential. The 2006 Xactware acquisition for an undisclosed sum proved even more transformative. Founded in 1986, Xactware's customers included 16 of the top 20 property insurers and approximately 80 percent of insurance repair contractors and service providers. During the record-breaking hurricane seasons of 2004 and 2005, Xactware's products were used to settle more claims than all its competitors combined. This wasn't just software—it was the language in which property claims were written.

Here's what made Xactware brilliant: it created a two-sided network where both insurers and contractors had to use the same platform. If you were a roofing contractor and wanted to work with insurance companies, you needed Xactware to generate estimates in the format insurers required. If you were an insurer, you needed Xactware because that's what all your contractors used. The switching costs weren't just financial—they were ecosystem-wide.

In 2004, ISO had entered the healthcare market through acquisitions, but the real strategic masterstroke came in 2008. In 2008, Verisk Analytics was established to serve as the parent holding company of ISO. This wasn't mere corporate restructuring—it was positioning for what Coyne saw coming: the opportunity to take this collection of essential infrastructure public at exactly the right moment.

Under the leadership of Verisk Analytics Chairman, President, and CEO Frank Coyne, the company prepared for its public debut during the worst financial crisis since the Great Depression. While other companies hoarded cash and battened down the hatches, Coyne saw opportunity in chaos. Insurance companies needed liquidity, markets were desperate for quality assets, and Verisk had something rare: predictable, subscription-based revenues in an essential industry.

The preparation for the IPO revealed Coyne's strategic brilliance. He wasn't raising capital for growth—Verisk was already highly profitable. Instead, he was providing liquidity to insurance company shareholders who needed cash during the crisis while simultaneously creating a public currency for future acquisitions. It was financial jujitsu: using the crisis that was crushing others to accelerate Verisk's transformation.

V. The IPO and Going Public (2009)

The morning of October 7, 2009, Frank Coyne stood on the Nasdaq trading floor, surrounded by Verisk executives and representatives from major insurance companies. Outside, the financial world was still reeling—unemployment approaching 10%, banks failing weekly, credit markets frozen. Inside, something remarkable was happening: demand for Verisk shares was overwhelming.

The $1.9 billion raised made it the largest IPO by a U.S. company since Visa's IPO in early 2008, more than 18 months earlier. Pricing its IPO shares at $22, above its target range of $19 to $21, the market's enthusiasm was immediate. Shares of Verisk rose nearly 24 percent in their first day of trading on Nasdaq, after the company completed the largest IPO by a U.S. company in 18 months. Verisk shares gained $5.22 to close at $27.22, after touching $28.97 earlier in the trading session.

What made this IPO unique wasn't just its size or timing—it was its structure. The firm did not raise any funds for itself in the IPO, which was designed to provide an opportunity for the firm's casualty and property insurer owners to sell some or all of their holdings and to provide a market price for those retaining. All 85.25 million shares in the IPO were being sold by Verisk's existing shareholders, which include American International Group Inc., Hartford Financial Services Group and ACE Group Holdings.

The genius lay in the details. Insurance companies desperately needed liquidity during the crisis, but they couldn't afford to lose access to Verisk's services. The IPO solved both problems: insurers could monetize their stakes while Verisk became an independent public company, still serving all of them equally. It was like selling your ownership in the town's only water utility while keeping your water service—and getting top dollar because everyone knew the town couldn't function without it.

Berkshire Hathaway was the only company among the firm's largest shareholders that did not sell any of its stock in the October 2009 IPO. In an action described by investment research company Morningstar as a "vote of confidence" in Verisk, Berkshire Hathaway was the only major shareholder not selling a stake. When Warren Buffett holds while everyone else sells, the market pays attention.

The Buffett signal mattered enormously. Here was the world's most famous value investor, known for his discipline and long-term thinking, essentially saying: "This company is so valuable, I won't sell even at these prices, even in this crisis." For institutional investors trying to evaluate a complex business they'd never heard of, Buffett's implicit endorsement was worth more than any roadshow presentation.

"It immediately gives credibility, because if he (Buffett) owns it you know he has done his work, and it is a positive vote on management," said Paul Lountzis, president of Lountzis Asset Management, which has about $60 million in assets under management and counts Berkshire as its largest holding. Lountzis said that could bode well for another IPO candidate, life insurance firm Symetra Financial, which is also partly owned by Berkshire Hathaway and filed this week to raise up to $575 million with a public stock sale.

The market conditions that seemed disastrous were actually perfect for Verisk. In normal times, investors chase growth stories and speculative ventures. During a crisis, they crave stability, predictability, and essential services. Verisk offered all three. Its subscription model meant recurring revenues. Its position in insurance meant it was essential infrastructure. Its decades of operation meant proven durability.

"The performance of our IPO could give a sense of confidence to other companies, that if they have good story, the market will support it," Coyne said. He was underselling it. Verisk hadn't just completed a successful IPO—it had proven that quality businesses could access public markets even in the worst conditions. The IPO window, slammed shut for eighteen months, creaked open.

The IPO transformed Verisk from an industry cooperative into a growth platform. With public stock as currency, the company could now acquire businesses that insurance companies would never have approved as owners. The governance constraints that had limited ISO's expansion were gone. The transformation Coyne had envisioned—from data utility to technology powerhouse—could now accelerate.

But perhaps most importantly, going public changed Verisk's DNA. The company that had operated for decades as a slow-moving utility suddenly had quarterly earnings calls, growth expectations, and a stock price that moved every second. This pressure would drive both tremendous value creation and, eventually, strategic overreach. The seeds of both triumph and future activist battles were planted on that October morning at the Nasdaq.

VI. The Scott Stephenson Era: Global Expansion (2013-2022)

Scott Stephenson took the CEO reins in April 2013 with the measured confidence of a Boston Consulting Group partner who had spent twelve years learning Verisk from the inside. Where Coyne had been the dealmaker who took Verisk public, Stephenson was the strategist who would transform it into a global data conglomerate. His vision was audacious: Why stop at insurance? Data and analytics were eating every industry. Verisk had the playbook—now it just needed to replicate it everywhere.

Mr. Stephenson joined the company in 2001, focusing on bringing new value and functionality to the company's product offerings. In 2002, he was promoted to Executive Vice President, working with the senior management team to move the business to higher levels of growth and profitability. Mr. Stephenson became Chief Operating Officer in 2008, with responsibility for the company's operating units, and was named President in 2011.

Standing before investors at his first earnings call as CEO in May 2013, Stephenson outlined his thesis: "Insurance was just the beginning. Every industry dealing with complex risks needs better data and analytics. Energy companies modeling commodity prices. Banks assessing credit risk. Governments preparing for climate change. We're going to serve them all. "The 2015 Wood Mackenzie acquisition for £1.850 billion (approximately $2.8 billion) represented Stephenson's boldest move yet. Wood Mackenzie was a global leader in data analytics and commercial intelligence for the energy, chemicals, metals and mining verticals, with revenue and EBITDA of £227 million and £107 million respectively for 2014, representing an EBITDA margin of 47.1%. This wasn't just diversification—it was a declaration that Verisk's model could work anywhere complex data met critical decisions.

The strategic logic seemed impeccable. Energy companies, like insurers, needed sophisticated data and analytics to price risk, allocate capital, and navigate regulatory environments. Wood Mackenzie had spent forty years building the same kind of essential infrastructure in energy that ISO had built in insurance. The EBITDA margins—47.1%—proved the business model's power. Better yet, climate change created natural synergies: insurers needed to understand energy transition risks, while energy companies needed to understand climate impacts.

But Stephenson's ambitions didn't stop there. Between 2013 and 2020, Verisk acquired dozens of companies across financial services, healthcare compliance, and supply chain management. Each acquisition came with a compelling strategic rationale. Financial services needed fraud detection. Healthcare needed claims analytics. Supply chains needed risk assessment. The unifying theme: wherever there was complexity and regulatory oversight, Verisk could build a data moat.

The market initially loved this story. Verisk's stock price rose from around $60 at the beginning of Stephenson's tenure to over $200 by 2021. Revenue grew from $1.5 billion in 2013 to $2.8 billion in 2021. The company seemed to have cracked the code: take the ISO playbook, apply it to new verticals, and watch the network effects compound.

Yet beneath the surface, cracks were forming. Each new vertical required different expertise, different sales processes, different regulatory relationships. The synergies that looked obvious in PowerPoint presentations proved elusive in practice. Insurance clients didn't care about energy data. Energy clients didn't need insurance analytics. The conglomerate was becoming harder to manage, harder to explain, and harder to value.

By 2021, Verisk was operating in so many markets that even seasoned analysts struggled to understand its strategy. The company that had once been laser-focused on insurance data now described itself as a "leading data analytics provider serving customers in insurance, energy and specialized markets, and financial services." The clarity that had made the 2009 IPO so compelling had given way to complexity.

The technology transformation Stephenson championed was real and necessary. Verisk invested billions in cloud infrastructure, artificial intelligence, and machine learning capabilities. The company's data scientists built sophisticated models that could predict everything from hurricane paths to fraudulent claims patterns. But technology alone wasn't enough to justify the sprawling empire Verisk had become.

Most troublingly, the core insurance business, while still growing, was no longer getting the focused attention it deserved. Competitors like Guidewire were attacking specific verticals with modern, cloud-native solutions. Insurtechs were building specialized tools that challenged pieces of Verisk's offering. The moat remained formidable, but for the first time in decades, it wasn't getting wider.

VII. The Activist Intervention & Portfolio Reshaping (2022-2023)

The letter arrived at Verisk's Jersey City headquarters in early 2022 like a declaration of war written in the polite language of Wall Street. D.E. Shaw, the quantitative hedge fund known for its analytical rigor and activist campaigns, had taken a significant position in Verisk. Their message was blunt: the conglomerate structure was destroying shareholder value. The sum of the parts was worth far more than the whole.D.E. Shaw's analysis was devastating in its precision. They had been privately engaging with Verisk since October 2021, but after five months of discussions, they went public with their frustrations. Their letter stated they were "seriously concerned about the long-term underperformance of the Company's share price" and believed that if Verisk transformed into a pure-play insurance business through separation of all non-insurance assets, it could unlock up to $20 billion of shareholder value—a stock price appreciation of more than 70%.

The critique hit every pain point: the acquisition of non-core businesses had been "dilutive to the quality of Verisk's insurance assets," organic revenue growth had disappointed, margins had contracted, and the market had grown skeptical of capital allocation. D.E. Shaw's math was simple but compelling: insurance data businesses traded at premium multiples, energy and financial services businesses didn't. The conglomerate discount was destroying billions in value. What followed was a masterclass in strategic retreat under pressure. In October 2022, Verisk announced the signing of a definitive agreement under which an affiliate of Veritas Capital would acquire Verisk's Energy business, Wood Mackenzie, for $3.1 billion in cash consideration payable at closing plus future additional contingent consideration of up to $200 million. The company that Verisk had bought for $2.8 billion in 2015 was being sold for $3.1 billion seven years later—barely keeping pace with inflation, a clear destruction of shareholder value when considering the opportunity cost.

Earlier in 2022, Verisk had also sold its Financial Services business to TransUnion for $515 million. The message to the market was clear: Verisk was returning to its roots as a pure-play insurance data and analytics company. Lee Shavel, who had been named CEO to execute this transformation, stated: "This transaction best positions Verisk to expand our role as a strategic data, analytics, and technology partner to the global insurance industry, and as a result, drive growth and returns that will create long-term shareholder value."

The activist campaign had worked. D.E. Shaw's public pressure, combined with the board's recognition that the conglomerate structure wasn't working, forced one of the most dramatic strategic reversals in recent corporate history. In less than eighteen months, Verisk went from aggressively acquiring in new verticals to systematically divesting everything outside insurance.

The market's reaction was swift and positive. Verisk's stock, which had been languishing in the low $180s when D.E. Shaw went public with their campaign, surged past $230 as the divestitures were announced. The conglomerate discount that had plagued the company was disappearing as investors could once again understand and value Verisk as a focused insurance technology company.

But the real vindication came from the operational improvements that followed. Without the distraction of managing disparate businesses, Verisk's management could focus on what they did best: deepening the moat in insurance data and analytics. Margins began expanding again. Organic growth accelerated. Customer satisfaction scores improved. The company that had lost its way in pursuit of empire-building had rediscovered its core competency.

The D.E. Shaw intervention would go down as one of the most successful activist campaigns of the decade—not because it broke up a company or forced a sale, but because it helped a great business remember what made it great in the first place. Sometimes the best strategy isn't to expand the castle—it's to fortify the keep.

VIII. The New Era: Insurance Network Platform (2023-Present)

Lee Shavel's first all-hands meeting as CEO in April 2023 felt different from the grand pronouncements of his predecessors. No talk of conquering new industries or building global empires. Instead, Shavel, a Verisk insider who had run the insurance business for years, spoke like someone who had watched a master craftsman nearly destroy their work by overreach: "We're not trying to be everything to everyone anymore. We're going to be irreplaceable to insurance. "The announcement in July 2025 that Verisk would acquire AccuLynx for $2.35 billion in cash marked Shavel's first major move, and it was telling. AccuLynx is the leading SaaS platform providing end-to-end business management workflow for residential property contractors with expertise in roofing. This wasn't diversification into energy or financial services—this was doubling down on the core insurance ecosystem.

The strategic logic was elegant. According to Verisk data, more than a third of property insurance claim value is related to roofing materials. AccuLynx's platform sits at the center of roofing contractors' workflow, addressing each critical stage from lead generation and sales to materials ordering and job management. Most importantly, most of AccuLynx's customers perform insurance-driven repairs and restoration.

Richard Spanton, AccuLynx's founder, captured the synergy perfectly: "I'm incredibly proud of what we've created and excited to see AccuLynx join Verisk. The synergies are undeniable—especially between AccuLynx and Xactimate, a tool I relied on heavily from day one. I always envisioned them working together. Now they will. "The financial results validate the strategy. For the full year 2024, consolidated revenues were $2,882 million, up 7.5% and up 7.1% on an organic constant currency basis. Income from continuing operations was $951 million, up 23.7%, while adjusted EBITDA was $1,576 million, up 9.9% on both a consolidated and OCC basis. The adjusted EBITDA margin for the trailing twelve months reached 54.6%—extraordinary for any business, testament to the moat's depth.

What makes the AccuLynx acquisition so strategic is how it extends Verisk's network effects. Now, when a homeowner files a roofing claim, the entire transaction—from the insurance adjuster's estimate in Xactimate to the contractor's bid in AccuLynx to the final payment—flows through Verisk's systems. Each participant in the ecosystem becomes more locked in because switching would mean losing integration with every other participant.

Shavel's vision for Verisk as an "insurance network platform" represents a fundamental evolution from the data utility model. Where ISO once provided static data and forms, Verisk now orchestrates dynamic workflows. Where insurers once bought data, they now participate in networks. The company isn't just selling information anymore—it's selling connectivity, efficiency, and increasingly, automation powered by artificial intelligence.

The market has responded positively but cautiously. Verisk's stock trades around $260 as of late 2024, well above the crisis lows but still below the peaks reached during the conglomerate years. Investors seem to be waiting for proof that the focused strategy will accelerate organic growth and expand margins further. The AccuLynx acquisition, while strategically sound, adds leverage at a time when interest rates remain elevated.

Yet the long-term opportunity is compelling. Climate change is making weather more volatile, increasing the value of sophisticated risk modeling. Cyber insurance is exploding as a category, requiring entirely new datasets and analytical capabilities. The digitization of insurance workflows is still in early innings, with enormous efficiency gains yet to be captured. And Verisk sits at the center of all these trends, with unmatched data assets and deeply embedded customer relationships.

IX. The Business Model & Moat Analysis

To truly understand Verisk's power, imagine trying to compete with it. You're a well-funded startup with brilliant engineers and deep pockets. You want to build a better insurance data platform. Here's what you face:

First, the data problem. Verisk has been collecting insurance claims data since 1971. Its ClaimSearch database contains 1.5 billion claims. Every major insurer contributes data because they need access to everyone else's data to price risk accurately. You can't replicate fifty years of history, and no insurer will give you their data unless you already have everyone else's. It's a classic chicken-and-egg problem with no solution.

Second, the regulatory moat. In most states, insurance rates must be filed with and approved by regulators. These regulators have been working with ISO/Verisk forms and methodologies for decades. They trust the data, understand the models, and have built their entire oversight apparatus around Verisk's standards. Asking them to approve your alternative isn't just about proving your data is good—it's about overcoming institutional inertia measured in decades.

Third, the workflow integration. Verisk isn't just a data provider anymore—it's woven into the operational fabric of insurance companies. Underwriters use Verisk data feeds in their pricing models. Claims adjusters use Xactimate on every property claim. Fraud investigators query ClaimSearch as standard procedure. Catastrophe modeling teams run AIR Worldwide simulations for reinsurance purchases. Replacing Verisk would mean reengineering dozens of critical business processes simultaneously.

The revenue model reflects this entrenched position. Subscription-based services generate predictable, recurring revenue with minimal marginal costs. Once an insurer integrates Verisk's data feeds, the cost of switching far exceeds any potential savings from a cheaper alternative. Price increases flow directly to the bottom line—when you're essential infrastructure, customers grumble but pay.

The operating margins tell the story: often exceeding 35% on an adjusted EBITDA basis, with some segments reaching above 50%. These aren't software margins built on code that can be replicated—they're network effect margins built on relationships, data, and regulatory positions that took half a century to establish.

The contributory database model creates a virtuous cycle that strengthens with scale. More insurers contribute more data, making the analytics more accurate, making the service more valuable, attracting more insurers. It's the same dynamic that powers Google's search algorithm or Facebook's social graph, but applied to commercial insurance data. The difference? Consumers might switch social networks for novelty. Insurance companies don't make infrastructure decisions based on what's trendy.

Consider the switching costs from an insurer's perspective. Moving away from Verisk would require: - Retraining thousands of employees on new systems - Reconfiguring automated underwriting models - Refiling rates with regulators in fifty states - Renegotiating reinsurance treaties based on different catastrophe models - Losing access to industry-wide claims data for fraud detection - Explaining to contractors why they need to learn new estimating software

The network effects compound across the value chain. Contractors use Xactimate because insurers require it. Insurers use Xactimate because contractors know it. Regulators approve Xactimate estimates because both insurers and contractors use it. Each participant's dependence reinforces every other participant's lock-in.

The data advantage goes beyond mere accumulation. Verisk's analytical models have been refined through millions of claims, tested against actual outcomes, and validated by regulators. A competitor might claim to have better algorithms, but can they prove those algorithms work across every geography, peril, and property type? Can they demonstrate to regulators that their loss costs are actuarially sound? Can they convince reinsurers to accept their catastrophe models for billion-dollar treaties?

This is why private equity firms and strategic buyers circle Verisk constantly but never pounce. The business is too essential to risk disrupting, too complex to improve through financial engineering, and too profitable to justify the premium required for acquisition. It's the rarest of assets: a monopoly that everyone knows about but no one can do anything about.

X. Power Dynamics & Strategic Lessons

The Verisk story offers a masterclass in building and maintaining corporate power in regulated industries. The lessons extend far beyond insurance, applying to any market where data, regulation, and network effects intersect.

Lesson 1: The Trojan Horse of Cooperation ISO began as a nonprofit cooperative, a structure that disarmed potential opposition. Regulators couldn't object to insurers sharing data for consumer benefit. Competitors couldn't complain about joining an industry association. By the time ISO converted to for-profit and went public, the dependencies were so deep that unwinding them would have been catastrophic for the entire industry.

Lesson 2: Regulatory Capture Through Service Verisk didn't capture regulators through lobbying or revolving doors. It captured them through indispensability. By providing standardized forms, actuarial data, and analytical tools that made regulators' jobs easier, Verisk became part of the regulatory infrastructure itself. The company doesn't fight regulation—it enables it, and in doing so, makes regulation a competitive moat.

Lesson 3: The Platform Pivot The evolution from data provider to platform orchestrator shows how traditional businesses can adapt to digital disruption. Verisk didn't just digitize its existing services—it reimagined its role from information vendor to workflow enabler. The AccuLynx acquisition exemplifies this: instead of just providing data about roofing claims, Verisk now powers the entire roofing claims ecosystem.

Lesson 4: The Diversification Trap The Wood Mackenzie saga illustrates a critical strategic tension. The same capabilities that make you dominant in one vertical can seem applicable everywhere. But success in insurance data didn't translate to energy markets because the underlying network effects didn't transfer. Competitors in energy didn't need to share data. Regulators didn't require standardized models. The lesson: network effects are market-specific, not company-specific.

Lesson 5: The Activist Paradox D.E. Shaw's successful campaign demonstrates both the power and limits of activist investing. They correctly identified that Verisk's conglomerate structure destroyed value. But their victory wasn't in breaking up the company or forcing a sale—it was in helping management rediscover focus. Sometimes the best activism is simply holding up a mirror.

Lesson 6: Capital Allocation in Essential Businesses Verisk's capital allocation journey—from aggressive diversification to focused consolidation—shows how essential businesses face unique challenges. When your core business has seemingly unlimited pricing power and margins, the temptation to expand is overwhelming. But the very factors that make the core business exceptional (regulatory requirements, network effects, switching costs) make replication nearly impossible.

Lesson 7: The Time Arbitrage Building a business like Verisk requires extreme patience. It took twenty-six years to go from founding to for-profit conversion, thirty-eight years to IPO. In an era of rapid startup scaling, Verisk's half-century journey seems anachronistic. But that timeline is precisely what makes the moat unassailable. Competitors can't replicate fifty years of data collection with five years of venture funding.

The meta-lesson may be the most important: in certain industries, slow and steady doesn't just win the race—it prevents the race from ever starting. By the time competitors realize what you've built, the game is already over.

XI. Bull vs. Bear Case

Bull Case: The Irreplaceable Infrastructure Thesis

The optimistic view starts with a simple observation: insurance is becoming more complex, not less. Climate change is making weather patterns more volatile and extreme events more frequent. Cyber attacks are evolving faster than defenses. Supply chain disruptions are revealing hidden correlations. Social inflation is driving claim costs higher. Every increase in complexity increases the value of Verisk's data and analytics.

The network effects are still strengthening. Every new data point makes the models more accurate. Every new customer makes the network more valuable. Every new regulation makes switching harder. The AccuLynx acquisition shows Verisk can extend its platform deeper into workflows, capturing more value while making customers more dependent. The company hasn't just built a moat—it's built a moat that widens itself.

Pricing power remains largely untested. When you're typically less than 0.1% of an insurer's premiums but essential to their operations, there's substantial room for price increases. A 10% annual price increase on a $10 million Verisk spend is $1 million—annoying but not worth the switching costs. For Verisk, that's pure margin expansion.

The AI opportunity is enormous and underappreciated. Verisk has the richest insurance dataset in existence, the customer relationships to deploy solutions, and the regulatory trust to get new models approved. As AI transforms insurance from reactive to predictive, Verisk's data becomes even more valuable. They don't need to build the best AI—they have the only complete training set.

International expansion remains nascent. Verisk has focused primarily on the U.S. market, but insurance is globalizing. Climate change affects everyone. Cyber risks cross borders. As international insurers seek sophisticated analytics, Verisk's proven models and reputation position it as the natural partner.

Valuation remains reasonable relative to quality. Trading at roughly 30x forward earnings, Verisk is priced like a good business, not a great one. Compare that to software companies with similar margins but weaker moats trading at 40-50x earnings. As investors better understand the network effects and pricing power, multiple expansion seems likely.

Bear Case: The Disruption and Saturation Thesis

The skeptical view begins with market saturation. Verisk already serves virtually every significant P&C insurer in America. Organic growth in the core business is limited to insurance market growth (mid-single digits) plus price increases. That's a good business but not an exciting one. The AccuLynx acquisition adds growth but also integration risk and leverage.

Technology disruption remains a constant threat. Yes, Verisk has data advantages, but AI is democratizing analytics. Open-source models trained on public data might prove "good enough" for many use cases. Insurtechs are building modern architectures that bypass legacy infrastructure. Young actuaries trained on Python and cloud computing might not accept "because we've always used Verisk" as an answer.

Regulatory risk cuts both ways. The same regulations that protect Verisk could turn against it. Antitrust scrutiny is increasing across the technology sector. Insurance regulators might question whether one company should control so much critical infrastructure. Data privacy laws could restrict the sharing arrangements that power the contributory database. A single adverse regulatory decision could unravel decades of competitive advantages.

Customer concentration creates vulnerability. The insurance industry is consolidating, giving large carriers more negotiating leverage. If the top ten insurers collectively pushed back on pricing or demanded alternatives, Verisk would have limited recourse. The company's profitability depends on customers accepting annual price increases indefinitely—that assumption might not hold during the next insurance market downturn.

Execution risk on the platform strategy is substantial. The AccuLynx acquisition needs to integrate smoothly while maintaining growth. The AI investments need to generate returns. The international expansion needs to overcome entrenched local competitors. Shavel's vision is compelling, but vision and execution are different things.

ESG concerns might seem trivial but could matter increasingly. Verisk enables insurance, and insurance enables development in climate-vulnerable areas. As climate impacts worsen, questions about the industry's role in perpetuating unsustainable development patterns could affect Verisk's social license to operate. Young talent might choose competitors with clearer climate benefits.

The Balanced View

Reality likely lies between these extremes. Verisk's moat is genuinely extraordinary—few businesses enjoy such entrenched competitive positions. But extraordinary doesn't mean permanent. The company will likely continue generating strong cash flows and steady growth for years, justifying a premium valuation.

The key variables to watch: organic growth acceleration (proving the platform strategy works), margin expansion (demonstrating continued pricing power), and successful AI deployment (staying ahead of technological disruption). If Verisk executes on all three, the bull case dominates. If it stumbles on any, the bear concerns gain credence.

For investors, Verisk represents a classic quality vs. growth trade-off. You're unlikely to see explosive returns, but you're also unlikely to see the business fundamentally impaired. In a world of increasing uncertainty, there's value in owning irreplaceable infrastructure—even if it's boring infrastructure that processes insurance forms.

XII. Epilogue: What's Next?

The story of Verisk Analytics is far from over. As we look toward the next decade, several themes will likely define the company's trajectory and, more broadly, the evolution of data monopolies in regulated industries.

Climate change isn't just a risk to model—it's reshaping the entire insurance industry. As weather patterns become more volatile, historical data becomes less predictive. This challenges Verisk's traditional models but also creates opportunity. The company that can best combine historical data with forward-looking climate projections will own the future of property insurance. Verisk's acquisition of atmospheric and environmental research capabilities positions it well, but execution will determine success.

The AI transformation presents both opportunity and threat. Large language models can interpret unstructured claims notes. Computer vision can assess property damage from photos. Machine learning can detect fraud patterns humans miss. Verisk has the data to train these models and the customer relationships to deploy them. But it also has the innovator's dilemma: will it disrupt its own profitable services with AI alternatives before competitors do?

The international expansion question looms large. American insurance markets are sophisticated but saturated. Emerging markets need insurance infrastructure as climate risks increase and middle classes grow. Can Verisk export its model to countries with different regulatory regimes, data protection laws, and competitive dynamics? Or will local champions emerge, using Verisk's playbook against it?

The platform evolution continues with fascinating implications. If Verisk successfully becomes the operating system for insurance workflows, it could capture dramatically more value. Imagine Verisk processing payments, managing documents, coordinating repairs, even selling policies directly. Each expansion would face resistance, but the logic of integration is powerful. The company that already knows the risk, prices the policy, and estimates the claim might naturally handle everything in between.

The generational transition in the insurance industry creates unique dynamics. Younger professionals expect modern tools, API integrations, and real-time data. They're less attached to legacy systems and more willing to experiment with alternatives. Verisk must balance serving its traditional customers while appealing to digital natives. The AccuLynx acquisition suggests it understands this challenge, but cultural transformation is harder than strategic acquisition.

The data sovereignty debate will intensify. As data becomes more valuable and privacy concerns grow, questions about who owns insurance data will become pressing. Does claims data belong to insurers, policyholders, or society? Should one company control information essential to a critical industry? These aren't just regulatory questions—they're philosophical ones about market structure and corporate power in the information age.

Looking back, Verisk's journey from nonprofit insurance cooperative to $36 billion technology company illustrates fundamental truths about building enduring businesses. Patient capital, regulatory alignment, network effects, and disciplined focus created extraordinary value. The activists were right that diversification diluted that value, but the core franchise remained intact.

Looking forward, Verisk faces the challenge every essential business eventually confronts: how to grow when you already serve everyone who needs you. The answer will likely come from serving them more deeply rather than more broadly. The company that started by standardizing insurance forms might end by reimagining insurance itself.

For students of business strategy, Verisk offers rich lessons. For insurance professionals, it provides essential services. For investors, it presents a fascinating study in competitive advantage. For society, it raises important questions about market power and essential infrastructure.

But perhaps the most remarkable aspect of the Verisk story is how unremarkable it seems. A boring business in a boring industry quietly built one of the world's most powerful data monopolies. No charismatic founder, no viral growth, no disruption narrative—just five decades of patient execution and compound advantage.

In an era obsessed with overnight unicorns and revolutionary disruption, Verisk reminds us that some of the most valuable businesses are built slowly, quietly, and inevitably. The company that processes insurance claims might not capture imaginations like social media or artificial intelligence ventures. But when the next hurricane hits, wildfire spreads, or cyber attack succeeds, Verisk's data and analytics will determine who pays what to whom.

That's not just a business model—it's a responsibility. How Verisk exercises its market power, serves its stakeholders, and evolves its platform will shape not just its own future but the future of risk management in an increasingly uncertain world. The next chapter of the Verisk story isn't just about financial returns—it's about whether essential infrastructure companies can balance private profit with public purpose.

The data monopoly that powers insurance has been built. The question now is what it will build next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube