Varex Imaging Corporation: From X-Ray Pioneer to Medical and Security Imaging Leader

I. Introduction and Episode Roadmap

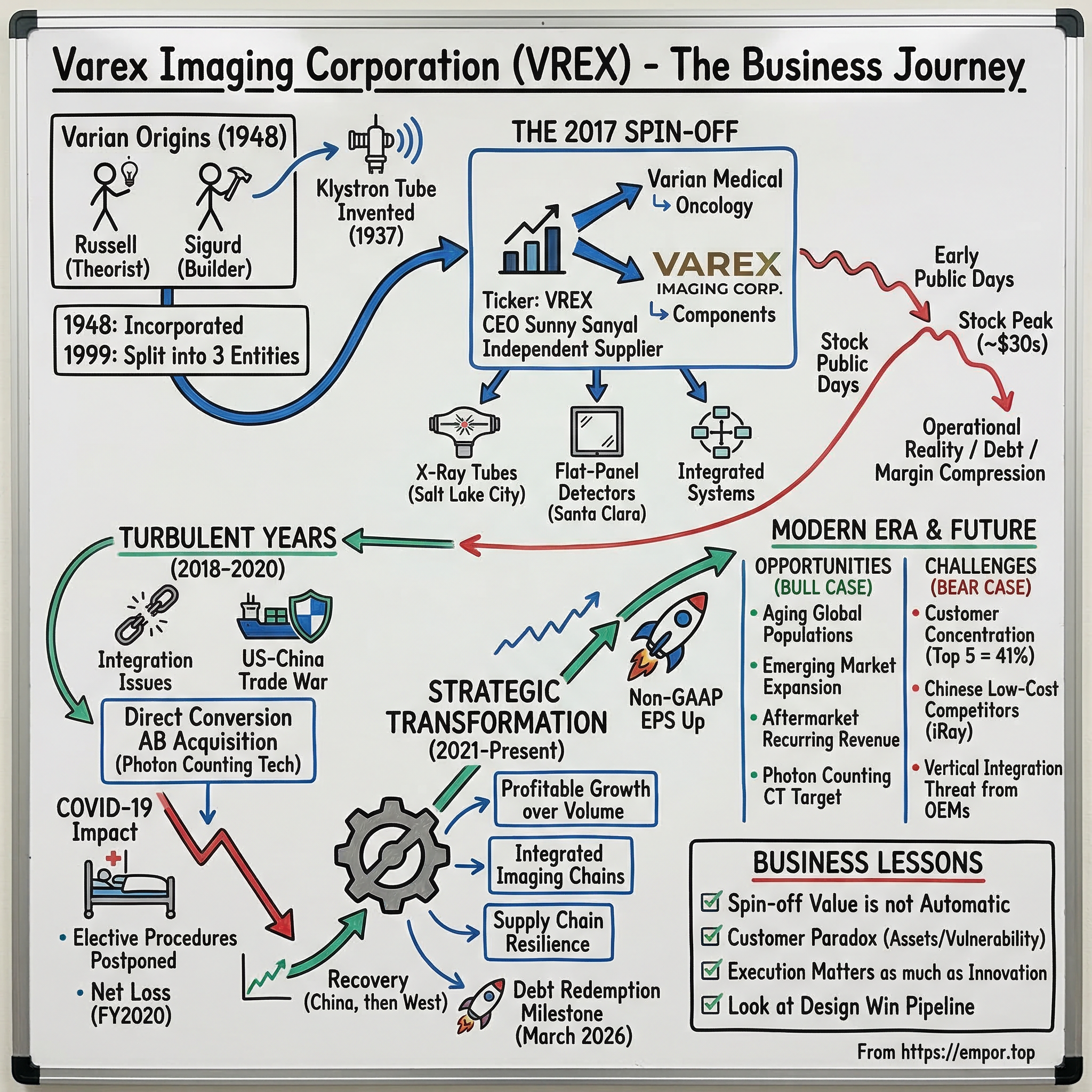

Somewhere inside every CT scanner humming in a hospital basement, every mammography unit in a women's health clinic, and every hulking cargo scanner at a port of entry, there is a component that almost nobody outside the industry has heard of, made by a company that almost nobody on Wall Street pays attention to. That company is Varex Imaging. If Qualcomm is the brains inside your smartphone and Intel was once the processor inside your PC, then Varex is the invisible engine inside the machines that peer through human bodies and shipping containers. It makes the X-ray tubes that generate the radiation and the flat-panel detectors that capture the image on the other side. Without these two components, modern medical imaging simply does not work.

What makes the Varex story worth telling is not just the technology. It is the unusual corporate journey: a business unit that spent more than seven decades nested inside one of Silicon Valley's original companies, Varian Associates, before being spun off in January 2017 into a standalone public company trading under the ticker VREX on the NASDAQ. The spin-off was supposed to unlock value, sharpen focus, and let the imaging components business run at its own pace. What actually happened was more complicated, more painful, and ultimately more instructive than anyone expected.

Today Varex generates roughly $845 million in annual revenue, employs about 2,300 people, and holds the distinction of being the world's largest independent supplier of X-ray imaging components. Its customers read like a who's who of global healthcare: Siemens Healthineers, GE HealthCare, Philips, Canon Medical. Yet the stock trades at roughly $10.81 per share as of mid-March 2026, with a market capitalization of about $453 million, less than half of what it was worth on day one as a public company. That gap between what this business is and what the market says it is worth frames the central tension of this episode.

The story moves through several distinct chapters. First, the deep history inside Varian, one of the most consequential but underappreciated technology companies in American history. Then the logic and mechanics of the 2017 spin-off. Next, the brutal reality check of operating as an independent company through trade wars, pandemics, and shifting technology. And finally, the question that matters most for long-term investors: is Varex a business with durable competitive advantages that is simply misunderstood and mispriced, or is it a component supplier trapped between powerful customers, rising Chinese competition, and technological disruption?

II. The Varian Origins and X-Ray Innovation Legacy (1948-2000s)

The Varex story begins not in a corporate boardroom but in a Stanford University physics lab in the late 1930s, with two brothers who were as different in temperament as they were united in ambition. Russell Varian was the theorist, a quiet, intense physicist who thought in equations. Sigurd Varian was the builder, a pilot and tinkerer who could turn his brother's abstractions into working hardware. Together, in 1937, they invented the klystron tube, the first vacuum tube capable of amplifying electromagnetic waves at microwave frequencies. It was one of those inventions that sounds obscure until you realize it made modern radar possible, which helped win World War II, which changed the trajectory of the twentieth century.

In 1948, the Varian brothers formalized their partnership by incorporating Varian Associates with physicist William Webster Hansen and Edward Ginzton. The initial capital was just $22,000. The company had six employees. Five years later, Varian Associates became the first tenant of Stanford Industrial Park in Palo Alto, a location now widely regarded as the spawning ground of Silicon Valley. Before Hewlett-Packard became the iconic Valley company, before Fairchild Semiconductor launched the transistor revolution, Varian Associates was already there, building the instruments and vacuum technology that would underpin an entire ecosystem.

Over the following decades, Varian grew into a sprawling conglomerate. The klystron tube led to defense radar contracts. Vacuum pump technology opened doors to semiconductor manufacturing. The company developed nuclear magnetic resonance spectroscopy instruments, which would eventually evolve into MRI. And critically for our story, Varian entered the medical technology space through X-ray tube manufacturing. By the 1970s and 1980s, Varian had become a dominant player in radiation oncology equipment, capturing more than half the global market for linear accelerators used to treat cancer. The X-ray tube manufacturing operation, based in Salt Lake City, was the quieter sibling. It did not have the drama of cancer treatment. It did not generate headlines. But it was a deeply profitable, technically demanding business that supplied the foundational components for medical imaging worldwide.

By the 1990s, Varian Associates had become unwieldy. It was a defense contractor, a semiconductor equipment maker, a scientific instrument company, and a medical technology leader all rolled into one. In 1999, the board made a bold decision: split the company into three independent entities. Varian Medical Systems kept the radiation oncology business and the X-ray tube operation. Varian Semiconductor Equipment Associates took the ion implantation business (later acquired by Applied Materials in 2011 for $4.9 billion). Varian, Inc. got the scientific instruments (later acquired by Agilent Technologies in 2010). The 1999 split was a preview of what would happen again in 2017, and it established a pattern: Varian's businesses were individually more valuable than the conglomerate whole.

Within Varian Medical Systems, the X-ray imaging components division continued to evolve through the digital revolution. The transition from analog film-based X-ray to digital flat-panel detectors was as significant for medical imaging as the transition from film cameras to digital cameras was for photography. Varian invested heavily in detector technology, building out capabilities in both X-ray tubes (the components that generate radiation) and digital detectors (the components that capture the resulting image). By the mid-2010s, two distinct businesses coexisted inside Varian Medical: a radiation oncology franchise that sold complete cancer treatment systems directly to hospitals, and an imaging components business that sold tubes, detectors, and related hardware to other equipment manufacturers. These businesses had different customers, different competitive dynamics, different capital requirements, and different growth profiles. The stage was set for another separation.

III. The Great Varian Split: Setting the Stage (2012-2016)

To understand why Varian Medical Systems decided to spin off its imaging components business, you have to understand the fundamental tension that had been building for years. Imagine running two businesses under one roof where one is a premium, direct-to-hospital franchise selling multi-million-dollar cancer treatment machines, and the other is a component supplier selling tubes and detectors to other equipment manufacturers who then compete with each other. The radiation oncology business had marquee customer relationships, strong pricing power, and a clear brand identity. The imaging components business had a completely different set of customers, most of whom were themselves massive corporations like GE, Siemens, and Philips, and a completely different competitive landscape.

By the early 2010s, Wall Street was openly questioning why these two businesses sat inside the same corporate structure. Radiation oncology was a pure-play story with clear comps in the medical device universe. Imaging components was a B2B industrial technology story that confused analysts trying to model Varian. The conglomerate discount was real: investors who wanted exposure to cancer treatment did not necessarily want exposure to the cyclicality of industrial X-ray components, and vice versa.

The strategic review accelerated through 2014 and 2015. Management evaluated several options: a full sale of the imaging components division, a joint venture, or a tax-free spin-off to shareholders. The spin-off won because it preserved optionality. Varian shareholders would own shares in both entities and could decide for themselves which business they wanted to hold. On January 28, 2016, Varian Medical Systems formally announced the planned separation. Every Varian shareholder would receive 0.4 shares of the new company, to be called Varex Imaging Corporation, for every share of Varian they held.

The next twelve months were consumed by the unglamorous but critical work of building a standalone company from scratch. Varex needed its own finance team, its own legal department, its own IT infrastructure, its own board of directors. It needed to establish transfer pricing agreements with its former parent. It needed its own credit facility and capital structure. The company took on approximately $484 million in debt at the time of separation, partly to fund a $200 million cash payment back to Varian Medical as part of the separation terms. This debt load would prove to be one of the most consequential decisions of the entire process, shaping Varex's strategic flexibility for years to come.

The management team that would lead the newly independent company was anchored by Sunny Sanyal as CEO. Sanyal's background was unusual for a medtech leader. Born in India, he earned his electrical engineering degree from the University of Mumbai, a master's in industrial engineering from Louisiana State University, and an MBA from Harvard Business School. His career path ran through management consulting at Arthur Andersen, leadership roles at Accenture and GE Healthcare, a stint as COO at McKesson Provider Technologies, and then CEO of T-System, a healthcare IT company. He came to Varian Medical as president of the imaging components division. Sanyal was not a lifelong imaging engineer. He was an operational executive who understood how to run complex businesses, and Varian's board believed that operational discipline, not just technical innovation, was what the imaging components business needed to thrive on its own.

The pitch to investors was straightforward: Varex would be the world's largest independent supplier of X-ray imaging components, with a dominant position in tubes and detectors, sticky OEM customer relationships, and a long runway for growth driven by aging populations, emerging market healthcare expansion, and the ongoing analog-to-digital conversion in medical imaging. The question nobody could answer definitively was whether independence would be liberating or exposing. Inside Varian, the imaging components business had the backing of a larger balance sheet, shared R&D resources, and the prestige of a well-known corporate parent. As Varex, it would need to prove it could stand on its own.

IV. The Spin-Off Moment and Day One as Varex (2017)

On January 30, 2017, Varex Imaging Corporation began trading on the NASDAQ Global Select Market under the ticker VREX. The first trade crossed at $27.27. The initial market capitalization was approximately $1.06 billion. For a company that most individual investors had never heard of, it was a respectable start.

Sunny Sanyal rang the opening bell at NASDAQ's MarketSite in Times Square and delivered his stump speech to a room of analysts and institutional investors. The message was carefully crafted: Varex was not a startup. It was a seventy-year-old business with deep technical moats, the broadest product portfolio in the industry, and relationships with virtually every major medical imaging OEM on the planet. The company manufactured X-ray tubes in Salt Lake City, digital detectors in Santa Clara, and had operations spanning the globe. Annual revenue at the time was approaching $700 million. The initial investor thesis rested on three pillars: stable growth from the medical imaging installed base, upside from industrial and security applications, and margin expansion as a focused, independent company streamlined its cost structure.

The first big strategic move came just three months later. In May 2017, Varex completed the acquisition of PerkinElmer's medical imaging business for $276 million in cash. This was a transformative deal. PerkinElmer's operation, which generated about $140 million in annual revenue and employed roughly 280 people, gave Varex significantly expanded capabilities in digital flat-panel detectors. The acquisition added manufacturing facilities in Santa Clara, Germany, the Netherlands, and the United Kingdom. It was a bold bet for a company that had barely unpacked its boxes as an independent entity, and it added substantially to the debt load. But the strategic logic was sound: Varex needed to be a full-line imaging components supplier, not just a tube company, and the PerkinElmer business filled critical gaps in the detector portfolio.

The early quarters as a public company went reasonably well. Revenue grew. The analyst community warmed to the story. The stock climbed into the low-to-mid $30s. For a brief honeymoon period, the spin-off narrative was working exactly as planned. But beneath the surface, challenges were accumulating. The debt from the spin-off and the PerkinElmer acquisition meant that Varex was running with leverage that left little room for error. And as any B2B component supplier knows, errors in execution, quality, or customer management can compound quickly when your customers are among the most demanding corporations in the world.

V. The Business Model Deep Dive: How Varex Actually Works

To understand why Varex matters and why its competitive position is more nuanced than it appears, you need to understand what X-ray imaging components actually are and why making them is so difficult.

Start with the X-ray tube. In simple terms, an X-ray tube is a vacuum-sealed device that generates X-ray radiation by accelerating electrons from a cathode to a high-speed collision with a metal target, typically tungsten. The collision produces X-rays that pass through the patient's body and hit a detector on the other side, creating an image. That sounds straightforward, but the engineering challenge is immense. The tungsten target rotates at thousands of revolutions per minute to distribute the enormous heat generated by the electron bombardment. The vacuum inside the tube must be maintained at extremely low pressures. The bearings that support the rotating anode must withstand temperatures exceeding 1,000 degrees Celsius while maintaining micron-level precision. A single manufacturing defect can cause the tube to fail during a medical procedure, which means quality standards are absolute. Varex's Salt Lake City manufacturing facility produces these tubes at scale, and the accumulated know-how from decades of production is a genuine competitive advantage that is very difficult to replicate.

On the other side of the imaging chain sits the flat-panel detector. Think of it as the digital camera sensor of the X-ray world. When X-rays pass through a patient's body, they hit the detector panel, which converts the radiation into an electrical signal that a computer then processes into a diagnostic image. Modern flat-panel detectors use either amorphous silicon or CMOS sensor technology, layered with scintillator materials that convert X-rays into visible light. The manufacturing process requires semiconductor-grade clean rooms and precision that rivals chip fabrication. Varex operates its detector manufacturing primarily out of its Santa Clara facility and holds a 40% ownership stake in dpiX LLC, which produces the amorphous silicon thin-film transistor arrays that form the backbone of many flat-panel detectors.

Beyond tubes and detectors, Varex also produces X-ray generators (the power supplies that drive the tubes), image processing software (through its MeVis acquisition), and various connectors and subsystems that link the imaging chain together. The company has increasingly positioned itself as a provider of complete imaging chain assemblies rather than individual components, bundling tubes, detectors, generators, and software into integrated solutions that reduce the engineering burden on OEM customers.

The customer base architecture is critical to understanding the economics. Varex does not sell to hospitals. It sells to the companies that build the equipment that goes into hospitals. Canon Medical is the single largest customer at approximately 18% of revenue. United Imaging, a rapidly growing Chinese OEM, is the second largest. GE HealthCare, Rapiscan Systems (a security screening company owned by OSI Systems), and Siemens Healthineers round out the top five, which together account for about 41% of total revenue. These are not casual commercial relationships. An OEM that designs a new CT scanner around a specific Varex tube and detector combination goes through a qualification and regulatory approval process that takes two to five years. Once that design is locked in, the OEM is effectively committed to buying from Varex for the life of that product platform, which can be a decade or more. This creates powerful switching costs, but it also means that losing a design win to a competitor can lock Varex out of that revenue stream for years.

The business breaks down into two reportable segments. The Medical segment generates roughly 75% of revenue and supplies components for CT scanners, mammography units, fluoroscopy systems, and general radiography equipment. The Industrial segment contributes about 25% and serves security screening (airport baggage scanners, cargo inspection systems), non-destructive testing for manufacturing quality control, and other industrial applications. The Industrial segment is more cyclical and lumpy, driven by government contracts and capital spending cycles, but it also tends to carry higher margins when business is strong.

Research and development spending runs at about 10-11% of revenue, or roughly $90 million per year, which is high for a company of Varex's size and reflects the technical intensity of the business. Every new generation of CT scanner demands better tube performance, higher-resolution detectors, and faster image processing. Standing still in this market means falling behind. The R&D investment is not optional; it is the price of admission to remain a relevant supplier to OEMs that are themselves spending billions on next-generation imaging platforms.

VI. The Turbulent Years: Challenges and Missteps (2018-2020)

The honeymoon ended quickly. By mid-2018, Varex's stock had dropped from the low $30s to below $20, and the optimistic narrative of the spin-off had collided with operational reality. The problems were multifaceted, and they exposed the difference between being a well-run division inside a larger corporation and being an independent company that had to excel at everything simultaneously.

The first crack appeared in margins. Gross margins, which had been above 36% in FY2017, compressed to 32.8% in FY2018 and essentially stayed there. The PerkinElmer integration was more complex than anticipated. Merging manufacturing operations, harmonizing quality systems, and rationalizing product lines across two organizations consumed management attention and generated unexpected costs. At the same time, some customers experienced quality issues with deliveries. In a business where a single faulty X-ray tube can shut down a hospital scanner, quality problems do not just cost money; they erode trust that takes years to rebuild.

The trade war between the United States and China introduced a new dimension of uncertainty. Varex's industrial and security business had meaningful exposure to Chinese customers, and tariffs on Chinese goods created pricing pressure while retaliatory measures threatened access to a growing market. The industrial segment, which was supposed to be the diversification engine, instead became a source of volatility as government security contracts proved lumpy and unpredictable.

In April 2019, Varex completed the acquisition of Direct Conversion AB, a Stockholm-based company known for its XCounter brand, for approximately 65 million euros. This was a strategically important deal. Direct Conversion was a pioneer in photon counting detector technology, which represents the next generation of X-ray imaging. Unlike conventional detectors that measure the total energy deposited by X-rays, photon counting detectors measure individual X-ray photons and their energy levels, enabling dramatically higher image resolution, spectral imaging capabilities, and lower radiation doses. The acquisition gave Varex a foothold in a technology that could eventually reshape the entire detector market. But in the near term, it was another integration challenge layered on top of the PerkinElmer absorption.

FY2019 marked a low point in operating performance. Revenue was essentially flat at $781 million. Operating income collapsed to just $8 million, down from $84 million two years earlier. The company that was supposed to thrive through independence was instead struggling to maintain basic profitability. The stock drifted into the mid-$20s, and investor patience wore thin. The narrative shifted from "exciting pure-play" to "show me the execution."

The medical imaging market itself was not helping. Hospital capital expenditure is inherently cyclical, driven by reimbursement changes, election-year uncertainty, and the financial health of healthcare systems. When hospitals tighten their budgets, they delay purchases of new imaging equipment, and that delay cascades down to component suppliers like Varex with a lag. Reimbursement pressure on diagnostic imaging procedures, particularly in the United States, had been building for years and was dampening the appetite for expensive new equipment upgrades.

By the time the world entered 2020, Varex was a company that had been through three years of post-spin-off turbulence and was still searching for the operational footing that would justify its independence. The balance sheet carried roughly $395 million in debt. Margins were compressed. The stock was well below its spin-off price. And then a pandemic arrived.

VII. COVID-19 Impact: Crisis and Unexpected Opportunity (2020-2021)

When COVID-19 shut down elective medical procedures worldwide in March 2020, Varex found itself in the crosshairs of two simultaneous demand shocks. Hospitals cancelled or postponed imaging equipment purchases as they scrambled to reallocate resources toward pandemic response. At the same time, the collapse of air travel decimated the airport security screening market, which depended on passenger volumes that had fallen to near zero in many regions. FY2020 revenue dropped to $738 million, gross margins cratered to 25.8%, and the company posted a net loss of nearly $58 million, its worst year since the spin-off.

The response was swift and painful. Varex eliminated 94 positions, furloughed additional staff, withdrew its financial guidance, and took a $15.8 million pre-tax charge for inventory write-downs and restructuring. To shore up liquidity, the company issued $200 million in convertible senior notes due 2025 at a 4% coupon. It was survival mode, and the convertible note issuance, while necessary, added complexity to the capital structure and dilution risk for existing shareholders.

But the pandemic also contained a paradox that would shape Varex's trajectory. COVID-19 demonstrated the irreplaceable role of medical imaging in healthcare. CT scans became a frontline diagnostic tool for assessing lung damage in COVID patients. Chest X-rays were used at unprecedented scale in emergency departments and field hospitals. The pandemic reminded healthcare systems worldwide that imaging infrastructure was not optional, it was essential. And as the acute crisis passed, the pent-up demand from delayed procedures and equipment purchases began building like water behind a dam.

The recovery, when it came, was uneven but real. China's healthcare system recovered first, with Chinese OEM customers resuming orders by mid-2020. Western markets followed through 2021. Revenue rebounded to $818 million in FY2021, and gross margins recovered to 33.2%. The net income of $17 million was modest, but it represented a return to profitability after the devastating prior year. The security screening business remained weak, as air travel recovered more slowly than medical imaging, but cargo and logistics screening provided a partial offset as global supply chains adapted to pandemic-era shipping patterns.

The supply chain disruptions that plagued virtually every manufacturer in 2020-2021 hit Varex hard. The global semiconductor shortage constrained the availability of electronic components used in detector systems and control electronics. Logistics bottlenecks delayed shipments and drove up freight costs. Raw material prices, including the tungsten and rare earth elements used in X-ray tubes, spiked as mining operations were disrupted. Varex's response to these supply chain nightmares would prove to be one of the more constructive outcomes of the pandemic era. The company began diversifying its supply base, qualifying alternative component sources, and investing in supply chain resilience measures that would serve it well in subsequent years.

For investors, COVID represented an inflection point not because of the financial damage, which was severe, but because it clarified the essential nature of Varex's end markets and forced operational improvements that might not have happened otherwise. The company that emerged from the pandemic was leaner, more disciplined, and more focused than the one that entered it.

VIII. The Strategic Transformation: Sunny Sanyal's Turnaround (2021-2023)

The post-pandemic period marked a genuine strategic shift at Varex, driven by Sunny Sanyal's increasingly clear vision of what the company needed to become. The earlier years of independence had been consumed by integration challenges, market headwinds, and operational firefighting. Now, with the pandemic receding and demand recovering, Sanyal had the bandwidth to pursue a more deliberate transformation.

The core philosophy was deceptively simple: prioritize profitable growth over revenue growth for its own sake. This meant exiting low-margin product lines and customer relationships that consumed resources without generating adequate returns. It meant investing selectively in high-value segments where Varex had genuine differentiation. And it meant raising operational standards across manufacturing, quality, and supply chain management to levels befitting a company that aspired to be the unquestioned technology leader in its space.

The detector strategy became a centerpiece of the transformation. Flat-panel detectors were evolving rapidly, with customers demanding higher resolution, faster readout speeds, and lower power consumption. Varex shifted its detector portfolio toward higher-performance, higher-margin products that served the most demanding applications: premium CT, interventional radiology, and advanced mammography. This was not just a product decision; it was a competitive positioning decision. By moving up the performance ladder, Varex was deliberately creating distance between itself and the rising Chinese competitors who were gaining share in the commodity end of the detector market through aggressive pricing.

The China question itself was a strategic puzzle with no easy answer. Chinese OEMs like United Imaging were growing rapidly and becoming important Varex customers. At the same time, Chinese component manufacturers like iRay Technology and Hangzhou Wandong were building competitive alternatives to Varex's products. The geopolitical tension between the US and China added a layer of regulatory and tariff risk that made long-term planning exceptionally difficult. Sanyal's approach was pragmatic: continue serving Chinese OEM customers while investing in manufacturing capabilities outside China (including a new facility in India) to reduce geographic concentration risk.

The industrial and security business received renewed strategic attention. While airport security screening volumes remained depressed relative to pre-COVID levels, the cargo and logistics screening market was growing robustly. Global supply chain security concerns, driven by everything from counterterrorism to customs enforcement, were driving investment in high-energy inspection systems. Varex's Linatron X-ray accelerators, originally developed for non-destructive testing of thick metal structures, found growing demand in cargo scanning applications. A $25 million order for high-energy cargo and vehicle inspection systems from an international customer demonstrated the potential of this market.

FY2022 and FY2023 showed the fruits of the transformation. Revenue grew to $859 million and then $893 million, setting a new post-spin-off record. Gross margins stabilized in the 32-33% range. EBITDA reached $115 million in FY2022. Net income of $30 million in FY2022 and $48 million in FY2023 represented the best profitability since the spin-off. The operational improvements were real: manufacturing yields improved, quality metrics strengthened, and customer satisfaction scores rose.

But the progress was not linear. FY2024 brought a revenue pullback to $811 million as the medical imaging market entered another cyclical downturn, and a peculiar tax situation resulted in $52 million of income tax expense on just $5 million of pretax income, producing a GAAP net loss of $48 million despite improved operations. FY2025 saw revenue recover to $845 million and gross margins improve to 34.4%, the best since FY2016, but a $93.9 million non-cash goodwill impairment charge in the Medical segment drove a GAAP net loss of $70 million. The impairment was triggered by the declining stock price and was compounded by tariff headwinds and a Chinese Ministry of Commerce (MOFCOM) anti-dumping investigation into US and India-made CT X-ray tubes. On a non-GAAP basis, however, FY2025 told a different story: adjusted EPS of $0.90 was up 73% year-over-year, and adjusted EBITDA of $122 million was up 37%.

The management team underwent changes during this period as well. Shubham Maheshwari took over as CFO, and the broader leadership team was refreshed with executives who brought operational rigor and a fresh perspective. The communication with investors became more transparent and realistic, with management providing clearer guidance frameworks and acknowledging challenges more directly rather than spinning narratives.

IX. Modern Era: AI, Digital Transformation, and New Frontiers (2023-Present)

The conversation about artificial intelligence in medical imaging has reached fever pitch, and for Varex, the implications are more nuanced than the headlines suggest. AI in imaging is primarily a software-layer phenomenon. Algorithms that can detect tumors in mammograms, identify stroke signatures in brain scans, or triage emergency cases based on chest X-rays are transforming diagnostic workflows. But these algorithms need data, and that data comes from imaging hardware. Higher-resolution detectors produce better training data for AI models. More sensitive tubes enable lower-dose scans that expand the population eligible for screening. In this sense, AI does not replace the hardware; it makes better hardware more valuable.

The most significant technology on Varex's horizon is photon counting CT, a generational leap in detector technology that promises to be as transformative for CT imaging as the transition from film to digital was for radiography. Conventional CT detectors work like a bucket collecting rain: they capture all the X-ray photons that arrive during a measurement interval and report the total energy. Photon counting detectors work like an eye distinguishing individual raindrops and measuring the size of each one. This enables spectral imaging, where different materials in the body can be distinguished based on how they absorb X-rays at different energy levels. The clinical implications are profound: better tissue characterization, improved detection of subtle lesions, dramatically higher spatial resolution, and lower radiation doses.

Siemens Healthineers broke ground in this space with the FDA clearance of its NAEOTOM Alpha system in September 2021, the world's first photon counting CT scanner. GE HealthCare has been developing competing technology through its 2020 acquisition of Sweden's Prismatic Sensors. Canon Medical and Philips are also pursuing photon counting programs. For Varex, the opportunity is significant. The company's 2019 acquisition of Direct Conversion AB gave it proprietary photon counting detector technology that it has been developing and scaling over the past several years. Management has set a revenue target of $150 million annually from photon counting technology by fiscal 2029, which would represent roughly 15-17% of total revenue.

The global market for photon counting X-ray detectors was valued at approximately $200 million in 2024 and is projected to grow at roughly 10.5% annually to reach $500 million by 2033. Varex's positioning in this market is strong but not guaranteed. The company is collaborating closely with OEM customers on photon counting CT platforms and has made significant R&D progress, including work with the Technical University of Munich. But Siemens has a head start with its own internally developed detector technology, and GE's Prismatic acquisition gives it a proprietary path as well.

Meanwhile, the digital detector penetration story continues to play out globally. More than 60% of healthcare facilities worldwide have shifted from analog to digital imaging platforms, but significant conversion opportunity remains in emerging markets across Africa, Southeast Asia, and Latin America. Varex has opened a new manufacturing facility in India to produce radiographic detectors, positioning itself closer to some of the fastest-growing markets. The emerging market opportunity is real, but it comes with a catch: price sensitivity in developing markets favors lower-cost solutions, which is precisely where Chinese competitors like iRay Technology are strongest.

The competitive dynamics deserve special attention. iRay Technology, based in Shanghai, has emerged as the most formidable Chinese challenger in the flat-panel detector market, with approximately $330 million in revenue and a $3.3 billion market cap on China's STAR Market. iRay's pricing typically runs 15-20% below Western incumbents, and the company has been investing heavily in AI-assisted manufacturing processes that reduce defect rates and improve yields. The broader Chinese component manufacturing ecosystem, supported by government subsidies and local-manufacturing mandates in countries like China, India, and Indonesia, is creating a structural competitive challenge for Western suppliers like Varex.

Varex's go-to-market strategy has evolved in response. Rather than competing on price for individual components, the company has shifted toward presenting fully integrated imaging chain assemblies: tubes, detectors, generators, connectors, and software bundled together as complete subsystems. This approach increases the value Varex delivers to OEM customers, raises the technical bar for competitors who can only offer individual components, and positions Varex as more of a technology partner than a commodity supplier. The software and image processing capabilities acquired through MeVis and developed internally are increasingly important to this strategy, creating recurring revenue streams and deepening customer integration.

In Q1 FY2026, ended January 2, 2026, Varex reported revenue of $210 million, up 5% year-over-year, with the Industrial segment showing particular strength at $65 million, up 17% driven by cargo screening systems. Non-GAAP EPS of $0.19 beat consensus estimates of $0.14. Perhaps most significantly, the company announced on March 6, 2026, the conditional full redemption of all $368 million in outstanding 7.875% Senior Secured Notes due 2027, a major deleveraging milestone that would dramatically reduce the company's interest expense burden, which has been running at $35-44 million per year and consuming a significant portion of operating income.

X. The Playbook: Business and Strategic Lessons

The Varex experience offers a rich set of lessons for anyone thinking about corporate separations, B2B technology businesses, or medtech investing.

The spin-off playbook is the most obvious place to start. The conventional wisdom holds that spin-offs create value because they eliminate the conglomerate discount, sharpen management focus, and align incentives. The Varex evidence is more mixed. The spin-off did sharpen focus, and the management team has been able to pursue strategies specific to the imaging components business that would have been difficult inside Varian Medical. But it also exposed the business to challenges that were muted inside the larger organization: a heavy debt load from the separation, loss of shared R&D and back-office resources, and the need to build investor relations and corporate credibility from scratch. The stock has lost roughly 60% of its value since the spin-off. That is not necessarily an indictment of the separation decision, since some of that decline reflects market conditions, COVID, and cyclical factors rather than structural value destruction. But it is a reminder that spin-off value creation is not automatic and can take much longer to materialize than proponents expect.

The customer concentration paradox is equally instructive. Varex's deep relationships with major OEMs are simultaneously its greatest asset and its greatest vulnerability. Those relationships create switching costs that protect revenue streams for years. But they also create dependency: when Canon or United Imaging or GE decides to change strategy, reduce spending, or bring a component in-house, Varex feels the impact acutely. The top five customers accounting for 41% of revenue is actually an improvement from earlier years, but it still means that the loss of a single major customer would be devastating. The strategic response, diversifying toward aftermarket sales, expanding the customer base to include smaller and emerging-market OEMs, and deepening integration through value-added services, is correct in principle but takes years to execute.

The tension between technology leadership and operational excellence is a theme that runs through the entire Varex story. Being the most innovative supplier in the market is necessary but not sufficient. OEM customers demand not just the best technology but also flawless quality, on-time delivery, and competitive pricing. The post-spin-off quality issues that damaged customer relationships in 2018 and 2019 demonstrated that technical excellence without operational discipline is a recipe for eroding competitive position. The subsequent operational improvements under Sanyal's leadership showed that operational discipline can be learned, but it requires sustained investment and management focus.

The long design-in cycle is a characteristic of the imaging components business that investors frequently underestimate. When Varex wins a design slot in a new imaging platform, it may take two to five years before that win translates into meaningful revenue. This creates a paradox: the most important leading indicator of future performance, the design win pipeline, is largely invisible to outside investors. By the time revenue shows up in quarterly results, the competitive battle that determined it was won or lost years earlier. For long-term investors, understanding the health of the design pipeline matters more than any single quarter's revenue figure.

The private equity question has loomed over Varex for years. At its current valuation of roughly $453 million in market capitalization and about $750 million in enterprise value on $845 million in revenue, the company is trading at less than 1x EV/Sales, which is extraordinarily cheap by medtech standards. A private equity buyer could acquire the business, apply financial engineering to optimize the capital structure, and benefit from the long-term secular tailwinds in medical imaging without the quarterly earnings pressure of public markets. The fact that no PE bid has materialized yet is itself informative: the debt load, the customer concentration risk, and the competitive threats from China may give potential acquirers pause. But the possibility remains a live strategic option that provides a potential floor under the stock.

XI. Porter's Five Forces and Hamilton's Seven Powers Analysis

Understanding Varex's competitive position requires a structured framework. The barrier-to-entry picture tells the first important story. Building a credible X-ray tube or flat-panel detector business from scratch requires hundreds of millions in capital, years of R&D, regulatory clearances from the FDA and European notified bodies, and the patience to endure qualification cycles with OEM customers that can stretch half a decade. Pure startups essentially cannot enter this market. The more relevant competitive threat comes from existing industrial players in China like iRay Technology and Hangzhou Wandong, which benefit from government support, lower cost structures, and access to a domestic market that increasingly favors local suppliers. The entry barriers are high but not impregnable, particularly at the lower end of the market.

Supplier bargaining power presents a moderate constraint. Varex depends on specialized materials including tungsten for X-ray tube anodes, rare earth elements, glass substrates, and semiconductor components for detector systems. China's dominance in rare earth processing and its willingness to restrict exports for geopolitical reasons creates a genuine supply vulnerability. The COVID-era semiconductor shortage demonstrated how disruptions in upstream component availability can cascade through Varex's production schedule. The company has responded by diversifying suppliers and building inventory buffers, but complete insulation from supply chain risk is impossible in a business this technically complex.

Buyer bargaining power is the force that most directly shapes Varex's economics. The OEM customers are among the most sophisticated procurement organizations in the world. GE HealthCare, Siemens Healthineers, Philips, and Canon Medical have deep technical knowledge of the components they purchase, the engineering capability to evaluate alternatives, and in some cases the capacity to manufacture competing products in-house. These buyers constantly pressure Varex on pricing, delivery terms, and technology roadmap alignment. The saving grace for Varex is the switching cost structure: once an OEM has designed its system around Varex components and secured regulatory approval, changing suppliers is prohibitively expensive and time-consuming. The aftermarket business, where hospitals and service organizations purchase replacement tubes and detectors for existing installed equipment, provides better pricing power because the components must be compatible with the installed base and alternative options are limited.

Substitution threat is relatively contained. For the foreseeable future, there is no viable alternative to X-ray-based imaging for the applications Varex serves. MRI and ultrasound are complements, not substitutes. CT scanning, mammography, fluoroscopy, and radiography all fundamentally require X-ray generation and detection. The technology evolution from conventional to photon counting detectors is a transition within the X-ray paradigm, not a departure from it. AI does reduce the number of unnecessary scans in some clinical scenarios, but it also enables more accessible screening programs that expand the total imaging market. The net effect on component demand is likely neutral to positive.

Competitive rivalry within the imaging components space is intense and multi-dimensional. The direct competitors include Trixell (the Thales, Siemens, and Philips joint venture that leads the flat-panel market with roughly 18% share), Canon's electron tubes and detector operations, and the growing Chinese ecosystem led by iRay Technology. Perhaps more concerning than horizontal competitors is the vertical integration threat: each of Varex's major OEM customers has some degree of in-house component manufacturing capability. Siemens makes its own X-ray tubes and participates in the Trixell detector JV. GE HealthCare manufactures proprietary liquid metal bearing tubes. Philips participates in Trixell and sells tubes through its Dunlee subsidiary. Canon makes tubes through Canon Electron Tubes and Devices. The fact that these OEMs continue to buy from Varex despite having internal capabilities speaks to the quality, performance, and cost-effectiveness of Varex's products, but it also means that the threat of further insourcing is always present.

Turning to Hamilton Helmer's Seven Powers framework, the most important source of durable competitive advantage for Varex is switching costs. This is where the real moat lies. An OEM design-in cycle of two to five years, followed by regulatory qualification that can take additional years, followed by a product lifecycle of a decade or more, creates a lock-in effect that is difficult to overcome. The cost to an OEM of switching from a Varex tube to a competitor's tube in an existing product platform includes not just the engineering work to redesign the system, but the regulatory re-approval process with the FDA, CE marking bodies, and other global regulators. This is genuinely expensive and risky, and it means that once Varex is designed in, it is very difficult to design out.

Process power is the second significant source of advantage, and it may be the most underrated. Manufacturing X-ray tubes at scale with consistent quality is genuinely hard. The combination of extreme temperatures, high vacuum, precision bearings, and radiation physics creates a manufacturing challenge that is more akin to semiconductor fabrication than typical industrial manufacturing. Varex has accumulated decades of process knowledge in its Salt Lake City facility that would be extremely difficult and time-consuming for a new entrant to replicate. The quality systems, regulatory compliance infrastructure, and OEM relationship management processes that Varex has built represent institutional capabilities that are embedded in the organization rather than in any individual patent or product design.

Scale economies provide moderate advantage. Varex's position as the largest independent supplier gives it R&D scale that smaller competitors cannot match, spreading development costs over a larger revenue base. Manufacturing scale allows better utilization of expensive capital equipment and more efficient procurement of raw materials. But scale advantages in this business are not overwhelming. Regional competitors, particularly Chinese manufacturers, can achieve sufficient scale in their local markets to be competitive.

Network effects are weak in this B2B component business. There is no meaningful dynamic where more Varex installations make the next installation more valuable. Branding matters less than in consumer markets, though reputation for quality and reliability does influence OEM purchasing decisions. Counter-positioning, the ability to adopt a new business model that incumbents cannot match without damaging their existing business, was relevant during the analog-to-digital transition but is largely played out. Cornered resources, including proprietary tube designs, detector IP, and engineering talent, provide moderate advantage but are not sufficient on their own as technology evolves.

The synthesis of these frameworks points to a company whose competitive position rests primarily on switching costs and process power, buttressed by moderate scale advantages and intellectual property. The key vulnerability is customer concentration combined with the dual threat of Chinese low-cost competition from below and OEM vertical integration from above. The strategic imperative is clear: Varex must continue moving up the value chain through software, AI-enabled capabilities, and next-generation technologies like photon counting faster than commoditization erodes the value of its existing product portfolio. This is a race, and the outcome is not predetermined.

XII. Bull vs. Bear Case and Investment Perspective

The bull case for Varex begins with secular demand. Global populations are aging, and older patients require disproportionately more diagnostic imaging. Emerging markets in Asia, Africa, and Latin America are building out healthcare infrastructure that requires millions of new imaging systems. The World Health Organization estimates that two-thirds of the world's population lacks access to basic diagnostic imaging, representing a massive unmet need that will be addressed over the coming decades. Every new CT scanner, every new X-ray room, and every new mammography unit needs tubes and detectors, and Varex is positioned to supply them.

The digital conversion runway extends the growth story. With roughly 60% of global healthcare facilities having transitioned to digital platforms, there is still significant analog-to-digital conversion opportunity, particularly in developing markets. Beyond first-generation digital, the upgrade cycle from computed radiography to direct flat-panel detection provides another wave of replacement demand in facilities that have already moved past film.

The aftermarket opportunity is perhaps the most compelling element of the bull case. Replacement tubes and detectors for the installed base of imaging equipment represent a growing, higher-margin, more recurring revenue stream than original equipment sales. As the global installed base expands, so does the aftermarket opportunity. This business is less cyclical than OEM sales and provides better pricing power because replacement components must be compatible with existing systems.

The recent deleveraging is a significant positive catalyst. The March 2026 announcement of the conditional redemption of all $368 million in 7.875% Senior Secured Notes would eliminate the company's most expensive debt tranche and could save $25-30 million annually in interest expense, which would flow directly to earnings and free cash flow. On non-GAAP metrics, which strip out the goodwill impairment and other one-time items, FY2025 showed meaningful improvement: adjusted EBITDA of $122 million was up 37% and adjusted EPS of $0.90 was up 73%.

The valuation itself is the bull's strongest argument. At roughly 0.86x EV/Sales and a market cap of $453 million, Varex trades at a fraction of the valuation of medtech peers. If the company can sustain the gross margin improvement seen in FY2025 (34.4%, the best since FY2016) and benefit from the interest expense reduction following the debt redemption, the path to meaningful earnings growth is visible without requiring heroic revenue assumptions.

The bear case starts with customer concentration and the power dynamics it creates. Five customers generating 41% of revenue means that Varex's fortunes are heavily tied to the strategic decisions of a handful of OEMs, each of whom has the technical capability to reduce their dependence on outside suppliers. Canon, the largest customer at 18% of revenue, makes its own tubes and detectors through Canon Electron Tubes and Devices. If Canon decided to accelerate in-house production at the expense of Varex purchases, the impact would be severe.

The China risk is multi-layered. Chinese competitors like iRay Technology are gaining market share through aggressive pricing and increasingly capable products. The Chinese government's anti-dumping investigation into US and India-made CT X-ray tubes, launched in April 2025, could result in tariffs that make Varex products uncompetitive in one of the world's fastest-growing imaging markets. China's restrictions on rare earth exports create supply chain vulnerability for Varex's manufacturing operations. And the broader US-China technology decoupling creates uncertainty for companies like United Imaging, which is simultaneously a major Varex customer and a potential strategic rival.

Technology disruption is a legitimate concern. Photon counting CT, while an opportunity for Varex, is also a threat if major OEMs choose to develop detector technology in-house rather than sourcing from Varex. Siemens has already done this with its NAEOTOM platform. GE's acquisition of Prismatic Sensors suggests a similar path. If the most valuable next-generation technology is developed and manufactured by OEMs rather than purchased from independent suppliers, Varex's strategic relevance diminishes.

The capital structure, while improving, remains a constraint. Even after the note redemption, Varex will carry meaningful debt on a revenue base of about $850 million. The business requires continuous investment in R&D (roughly $90 million per year) and capital expenditure to maintain manufacturing competitiveness. Free cash flow generation has been inconsistent, and the long cash conversion cycle of roughly 224 days means that significant capital is tied up in inventory and receivables at any given time.

For investors tracking Varex's ongoing performance, two KPIs matter most. First, gross margin trajectory. Gross margin is the single best proxy for product mix quality, pricing power, and operational efficiency. The improvement to 34.4% in FY2025 from 31.7% in FY2024 is encouraging, and sustained expansion toward the mid-to-high 30s would validate the strategic transformation. Declines back toward the low 30s would signal competitive pressure or mix deterioration. Second, the design win pipeline and revenue contribution from new product platforms, particularly photon counting technology. Because of the multi-year lag between design wins and revenue, the health of the pipeline is the most important leading indicator of where the business will be in three to five years, even though it is difficult for outside investors to observe directly.

XIII. Epilogue and Future Outlook

Nearly a decade after the spin-off, Varex Imaging sits at a crossroads that is both more challenging and more interesting than anyone anticipated in 2017. The company that began life as a pure-play imaging components supplier with a clear narrative of focus and growth has instead navigated trade wars, a pandemic, margin compression, goodwill impairments, and intensifying competition. Yet the core business endures. The world still needs X-ray tubes and detectors. The OEM customers still need Varex. And the technology roadmap, particularly around photon counting, creates genuine pathways to premium positioning.

The most recent Q1 FY2026 results offered a glimpse of what the business looks like when multiple factors align in its favor. Revenue grew 5%, the Industrial segment surged 17% on cargo screening strength, and earnings beat expectations. The note redemption announced in March 2026 addresses what has been the company's most persistent financial drag, its debt service burden, and could meaningfully improve the earnings profile going forward.

The existential questions that hang over Varex are the same ones that haunt every B2B component supplier in a consolidating industry. Can a component supplier maintain premium positioning when the software and AI layers increasingly capture value? This is the "Intel Inside" question. Intel's experience, where decades of processor dominance eventually gave way to commoditization and architectural disruption, is a cautionary tale. Varex's answer has been to move toward integrated imaging chain solutions and software-enabled products, but the transition is still early.

Will consolidation in OEM customers force consolidation in suppliers? Siemens' acquisition of Varian Medical Systems in 2021 for $16.4 billion removed one major player from the landscape and created a more concentrated buyer universe. If further OEM consolidation occurs, the bargaining power balance could shift further against independent suppliers.

Does vertical integration ultimately win, or do specialists prevail? This is the question that has animated industrial strategy debates for a century, and there is no universal answer. In some industries, the specialists prevail because the technical depth required to excel at a narrow function exceeds what a diversified company can sustain. In others, the integrators win because controlling the full stack creates quality, cost, or speed advantages. The imaging components industry sits somewhere in between, and Varex's long-term fate depends in part on where the balance settles.

For Varex to become dramatically more valuable from here, several things would need to go right simultaneously. Photon counting technology would need to become a major revenue contributor with Varex as a primary supplier. Gross margins would need to continue expanding toward the high 30s or low 40s. The deleveraging would need to continue, freeing up cash for R&D investment and shareholder returns. And Chinese competition would need to plateau or be contained through technology differentiation and trade policy.

For the bear case to play out fully, customer concentration would need to increase, not decrease. Chinese competitors would need to move from the commodity tier into premium applications. OEMs would need to accelerate vertical integration. And the debt burden, even after the note redemption, would need to constrain the company's ability to invest in next-generation technology at the pace required to maintain relevance.

The Varex story is not a glamorous one. There are no consumer brand evangelists, no viral products, no celebrity CEO doing podcast tours. It is the story of a company that makes the components inside the machines that save lives and secure borders, a company whose products are invisible to the billions of people who benefit from them. That invisibility is both its greatest challenge, because investors struggle to get excited about something they cannot see, and its greatest testament, because the best infrastructure is the kind that works so reliably that nobody thinks about it. Understanding companies like Varex matters because they represent the unglamorous foundation upon which healthcare innovation is built. Every breakthrough AI diagnostic algorithm, every new clinical imaging protocol, every screening program that catches cancer early depends on hardware that generates and detects X-rays with precision, reliability, and consistency. That hardware does not make itself.

XIV. Outro and Further Learning

For those who want to go deeper on the Varex story and the broader medical imaging components ecosystem, the following resources provide excellent starting points.

Varex Imaging's own investor relations page offers annual reports (10-K filings), quarterly earnings transcripts, and investor presentations that provide granular detail on product strategy, financial performance, and competitive positioning. The March 2025 investor presentation is particularly useful for understanding management's current strategic framework.

The Varian Medical Systems historical annual reports from the pre-2017 period provide essential context for understanding the legacy and the rationale behind the separation. These filings document the internal debate about the spin-off and the strategic logic that drove it.

The SEC filings surrounding the 2017 spin-off transaction itself, including the Form 10 registration statement, lay out the separation terms, capital structure, and risk factors in exhaustive detail. For investors who want to understand how the debt load was established and the transfer pricing agreements with the former parent were structured, these filings are essential reading.

The FDA and CE Mark regulatory guidance documents for medical imaging devices illuminate the regulatory moat that protects incumbent suppliers. Understanding the qualification and approval process helps explain why switching costs are so high and why new entrants face multi-year timelines to gain market access.

The Radiological Society of North America (RSNA) conference proceedings offer a window into the technology trends shaping the imaging market. RSNA is the industry's largest annual gathering, and the technical presentations and vendor demonstrations reveal the direction of innovation well before it shows up in financial results.

Industry trade publications including DOTmed News, AuntMinnie.com, and Health Imaging News provide ongoing coverage of market developments, product launches, and competitive dynamics that are difficult to track through mainstream financial media.

Market research from firms like Signify Research, IMV Medical, and Frost and Sullivan provides structured analysis of market size, share, and growth trends in medical imaging equipment and components. These reports are expensive but offer the most comprehensive data available on segment-level dynamics.

Clayton Christensen's "The Innovator's Prescription" offers a valuable framework for thinking about healthcare technology disruption, including how component suppliers can be affected by shifts in the value chain.

Finally, academic and industry papers on X-ray detector technology evolution, photon counting CT clinical validation, and medical device supply chain management provide technical depth for investors who want to understand the engineering foundations of Varex's business at a deeper level. IEEE publications on detector technology and Harvard Business School and Wharton research on spin-off value creation are particularly relevant.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube