Vulcan Materials: Building America's Infrastructure

I. Introduction & Episode Setup

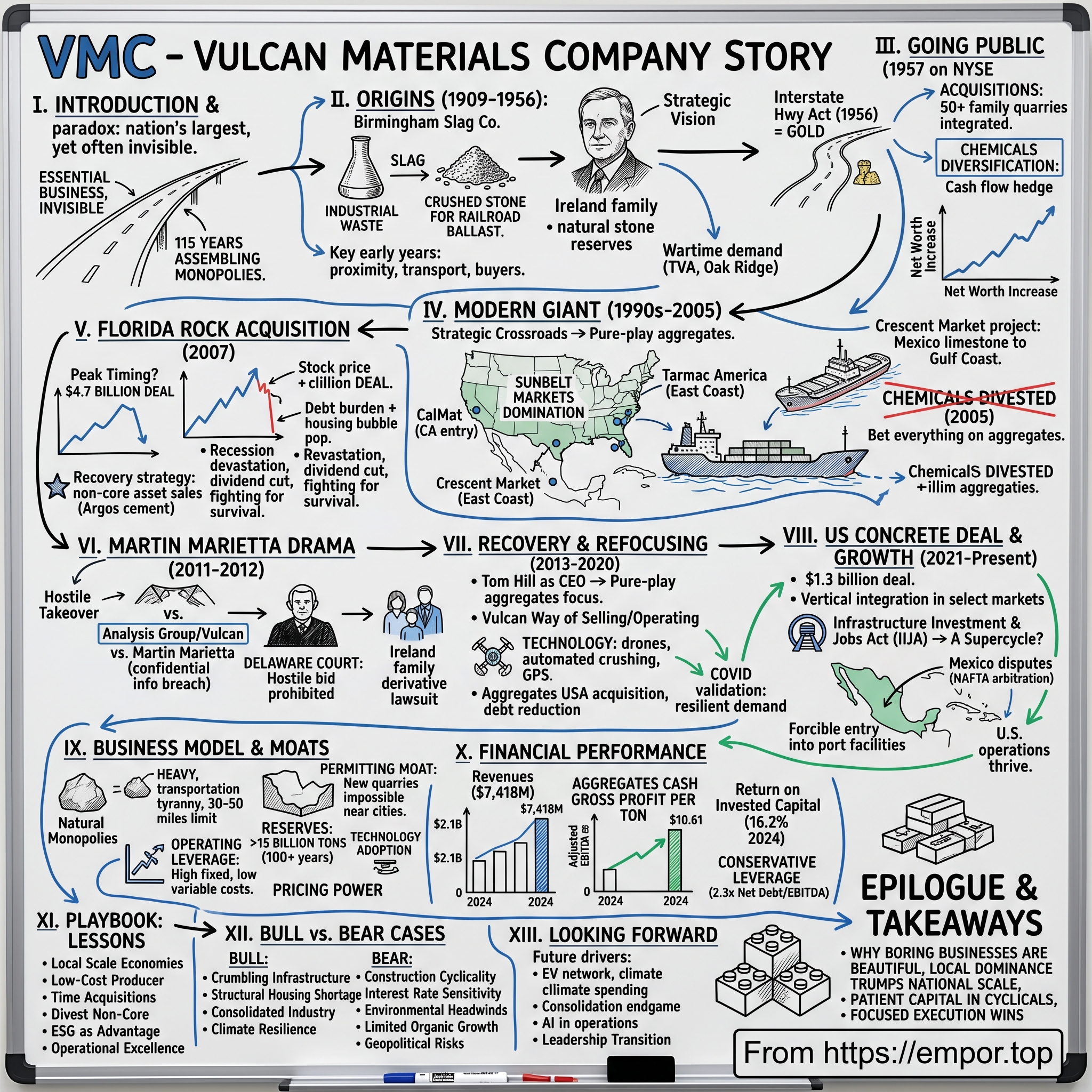

Picture this: You're driving down an interstate highway, passing construction sites where new office towers rise from the ground, crossing bridges that span mighty rivers. Every single one of these structures—the road beneath your tires, the concrete in those buildings, the aggregate in that bridge—likely contains materials that passed through the hands of one company. Yet most Americans have never heard of Vulcan Materials Company, despite it being the nation's largest producer of construction aggregates.

Here's the paradox that defines modern infrastructure: The most essential businesses are often the most invisible. Vulcan Materials controls roughly 700 active aggregates facilities across the United States, processes over 350 million tons of crushed stone, sand, and gravel annually, and commands a market capitalization north of $35 billion. How did a company that started in 1909 as Birmingham Slag Company—literally selling industrial waste from steel production—transform into the backbone of American construction?

The answer lies in one of capitalism's most underappreciated truths: Sometimes the best businesses are built not on cutting-edge technology or network effects, but on the immutable laws of physics and geography. You see, aggregates—crushed rock, sand, and gravel—have a unique economic characteristic that creates natural monopolies. These materials are so heavy relative to their value that transportation costs typically exceed production costs beyond 30-50 miles from the quarry. This simple fact of physics means that whoever controls the rock deposits near growing cities essentially owns a toll booth on all construction activity in that market.

Think about it this way: You can ship an iPhone from China to Cincinnati for a few dollars. But trucking a ton of crushed stone just 50 miles might cost more than the rock itself. This transportation tyranny transforms what should be a commodity business into a collection of local monopolies. And Vulcan has spent 115 years assembling the best collection of these monopolies in America.

The story we're about to tell spans three distinct eras of American capitalism. First, the industrial age when Birmingham Slag rode the coattails of Southern steel production. Second, the interstate highway boom when Vulcan Materials went public and surfed the greatest infrastructure build-out in human history. And third, the modern era of financial engineering and industry consolidation, where Vulcan transformed from a diversified industrial conglomerate into a pure-play aggregates powerhouse.

Along the way, we'll encounter visionary leaders who saw opportunity where others saw worthless rock piles, hostile takeover battles fought in Delaware courtrooms, and multi-billion dollar acquisitions timed at exactly the wrong moment. We'll explore how a business that sells rocks—literally the most basic commodity imaginable—maintains EBITDA margins above 25% and returns on invested capital that would make a software company jealous.

Most importantly, we'll unpack the strategic playbook that allowed Vulcan to compound shareholder value through booms, busts, and everything in between. Because while technology companies capture headlines, it's companies like Vulcan that literally build the physical world around us. And in an era of renewed infrastructure investment, understanding the aggregates industry isn't just academic—it's essential to grasping how America will rebuild itself over the next generation.

II. Origins: From Steel Slag to Strategic Vision (1909-1956)

The story begins not with grand ambition but with industrial waste. In 1909, Birmingham, Alabama was earning its nickname as the "Pittsburgh of the South," its skyline punctuated by blast furnaces that ran day and night, transforming Appalachian iron ore into the steel that would build America's railroads and skyscrapers. But for every ton of steel produced, these furnaces generated mountains of slag—a glassy, porous byproduct that steel companies paid to haul away.

Two entrepreneurs, Solon Jacobs and Henry Badham, saw opportunity in these waste piles. They recognized that blast furnace slag, when crushed and graded, made excellent railroad ballast—the crushed stone that forms the trackbed supporting railroad ties. Their timing was impeccable: America's rail network was expanding at breakneck pace, and every mile of new track required thousands of tons of ballast. On a handshake and $10,000 in capital, they founded Birmingham Slag Company in the industrial suburb of Ensley, quite literally in the shadow of the steel mills.

The early years were lean but instructive. Jacobs and Badham learned that success in the aggregates business required three things: proximity to raw materials, access to transportation, and relationships with large-scale buyers. They had all three. The slag piles were free for the taking (steel companies were happy to be rid of them), the Louisville & Nashville Railroad ran directly through their property, and the railroad companies themselves became their primary customers. It was a beautiful circular economy—the waste from making steel rails became the foundation for laying those same rails across the South.

By the 1930s, Birmingham Slag had established itself as a regional player, but the real transformation came with the New Deal and World War II. When the Tennessee Valley Authority began its massive dam-building program in 1933, Birmingham Slag became a critical supplier. The company provided aggregates for Wilson Dam, Wheeler Dam, and ultimately for the secretive Oak Ridge facility where America developed the atomic bomb. During the war years, the company supplied materials for Redstone Arsenal in Huntsville (later to become NASA's rocket development center), Fort McClellan, and dozens of military installations across the Southeast. The pivotal moment came in 1916 when Charles Lincoln Ireland, an Ohio banker whose family operated stone quarries in Ohio, Kentucky, and West Virginia, purchased Birmingham Slag and placed his three sons—Glenn, Eugene, and Barney—in charge of the company. The Ireland family brought not just capital but a strategic vision that would transform a regional slag processor into a national powerhouse. Charles Ireland had secured heavy equipment left over from the construction of the Panama Canal—massive steam shovels and rail equipment that gave Birmingham Slag processing capabilities its competitors couldn't match.

The 1920s brought Alabama's Good Roads Movement, and Birmingham Slag was perfectly positioned. When the state passed the 1922 Alabama Bond Issue for Good Roads, setting off a construction boom across the South, the company's production soared. The Irelands opened new processing plants in Fairfield and Wylam, expanding beyond slag into natural aggregates—crushed limestone, sand, and gravel. They were learning a crucial lesson: while slag was useful, natural stone reserves were the real prize. Unlike slag piles that depended on steel production, quarries offered century-long reserve lives and predictable extraction economics.

World War II marked Birmingham Slag's transformation from regional supplier to strategic national asset. Birmingham Slag was a major supplier to the Tennessee Valley Authority beginning in 1939 and also provided materials for construction of the Oak Ridge National Laboratory, Redstone Arsenal, Fort McClellan and other military facilities during World War II. The company's materials literally built the infrastructure of America's atomic age and space program. This wartime experience taught the Ireland family another crucial lesson: government contracts provided steady demand through economic cycles, and proximity to major projects trumped almost every other competitive factor.

By 1951, leadership had passed to the third generation. Charles W. Ireland, grandson of the Ohio banker, had become president and developed a plan to expand the company. He faced two challenges: the coming interstate highway boom would require capital far beyond what a family business could muster, and the Ireland family needed to address mounting estate tax concerns that threatened to force a sale upon the death of senior family members.

When President Dwight Eisenhower announced his commitment to build a $50 billion interstate highway system across the country in 1954, Charles W. Ireland knew Birmingham Slag stood at an inflection point. The company could remain a successful regional player, or it could leverage this once-in-a-generation infrastructure program to become something much larger. He chose transformation.

The solution was elegant: merge with a publicly traded company to access capital markets while maintaining family control. Ireland found the perfect target in Vulcan Detinning Company of Sewaren, New Jersey, which had been trading on the New York Stock Exchange since the 1920s. With significant negotiating help from the company's outside legal counsel, Bernard "Barney" Monaghan, Ireland directed the company's transition to a public corporation through the purchase of Vulcan Detinning Company.

Bernard Monaghan deserves special attention here. A Rhodes Scholar and Harvard Law School graduate who served as the Ireland family's corporate attorney, Monaghan negotiated the merger with Vulcan Detinning and later orchestrated the acquisition of a dozen construction aggregate companies through the 1950s and into the early 1960s. His combination of legal acumen and strategic vision would prove instrumental in Vulcan's next chapter. The Irelands convinced him to leave his law practice and join the company full-time—a decision that would reshape the American aggregates industry.

III. Going Public & Early Expansion (1957-1980s)

Vulcan Materials Company became a publicly traded company with trading beginning on January 2, 1957, under the symbol VMC, with shares selling for $12.69 and 13,800 shares changing hands in the first five days. The timing could not have been more fortuitous. Eisenhower's Federal Highway Act had passed just months earlier, authorizing the construction of 41,000 miles of interstate highways. For a company in the aggregates business, it was like striking gold.

But Monaghan and the Irelands understood something deeper about the opportunity before them. The interstate system wasn't just about the highways themselves—it would fundamentally reorganize American life around the automobile, spurring suburban development, shopping centers, office parks, and industrial facilities, all requiring massive quantities of aggregates. They weren't just selling rocks; they were selling the raw material of American expansion.

The newly public Vulcan moved with stunning speed. In 1957, Vulcan acquired nine companies, including Lambert Brothers of Knoxville, Tennessee, and W.E. Graham & Sons General Contractors of North Carolina, mostly family-owned businesses that provided Vulcan with plants, stone reserves, and experienced employees. This established the template for Vulcan's growth strategy: acquire family-owned quarry operations with proven reserves, retain the local management who understood the market dynamics, and provide them with capital and best practices to improve operations.

Vulcan's merger with Union Chemicals and Materials in 1957 made it a diversified company better able to adapt to changes in the crushed stone market. This diversification into chemicals wasn't random—it was strategic genius. The chemicals business, particularly chloralkali production, provided steady cash flows that were countercyclical to construction. When building slowed, chemical demand often increased as industrial production picked up. This natural hedge would prove invaluable through multiple economic cycles.

Monaghan was named president and chief executive officer in 1959, and by 1961, Vulcan had acquired some 50 family-owned companies and employed approximately 5,250 workers. The pace was breathtaking, but Monaghan had developed a unique approach to integration. Rather than imposing corporate uniformity, he allowed acquired companies to maintain their local identities and relationships while providing them with Vulcan's financial strength and operational expertise. Much of the credit for successful mergers is due to Monaghan, who worked closely with owners of merging companies, explaining the protocols of going public.

The aggregates business in the 1960s was still highly fragmented, with thousands of small, family-owned quarries operating across America. Most were single-location operations, vulnerable to local economic downturns and lacking the capital for modern equipment. Vulcan offered these families a graceful exit—liquidity for the older generation, continued employment for those who wanted to stay, and the satisfaction of seeing their life's work become part of something larger.

From 1956 to 1960, Vulcan's net worth increased almost sevenfold to $72 million from $11 million, and it became the largest producer of construction aggregates material in the country. But size alone wasn't the goal. Vulcan was systematically building what would become an insurmountable competitive advantage: a network of strategically located quarries near high-growth markets, connected by an increasingly sophisticated logistics operation.

The 1970s brought new challenges—the oil crisis, stagflation, and a slowdown in highway construction as the interstate system neared completion. But Vulcan's diversified model proved its worth. The chemicals division, which had grown through acquisitions of chlorine and caustic soda producers, generated steady profits even as construction materials faced headwinds. The company also began exploring international opportunities, establishing operations in Mexico to serve Gulf Coast markets via ship—a prescient move that would pay dividends decades later.

By 1981, Vulcan had transformed from a regional slag processor into a Fortune 500 company. With sales of $793 million, it entered the prestigious list at number 367. But more importantly, it had assembled the foundation of what would become an aggregates empire: over 200 quarry locations, a thriving chemicals business providing financial stability, and a management culture that balanced entrepreneurial local operations with corporate scale advantages.

The company's success attracted attention from Wall Street, but also from competitors. Regional aggregates companies began consolidating, trying to replicate Vulcan's model. Martin Marietta Materials, founded in 1961 as a spin-off from the aerospace company, emerged as a particularly aggressive competitor, focusing exclusively on aggregates while Vulcan maintained its diversified approach. This rivalry would simmer for decades before exploding into one of the most dramatic hostile takeover battles in American corporate history.

IV. The Modern Aggregates Giant Emerges (1990s-2005)

The Berlin Wall had just fallen, and with it, the old certainties of American business were crumbling too. In Birmingham, Vulcan Materials faced a strategic crossroads that would define its next quarter-century. The company's chemicals division, long a source of steady profits and strategic comfort, was becoming an anachronism. Wall Street had fallen in love with "pure plays"—companies focused on a single industry where investors could make clean bets on specific sectors. Vulcan's hybrid model was increasingly viewed as a "conglomerate discount" that depressed its stock price. The 1990s began with a recession that tested every aggregates company, but Vulcan emerged with a clear strategic vision. Under the leadership of CEO Houston Blount, who had risen through the ranks since joining in 1970, the company embarked on its most aggressive expansion phase yet. The strategy was straightforward but bold: dominate the fastest-growing Sunbelt markets through strategic acquisitions while competitors remained cautious.

On November 16, 1998, Vulcan announced it was purchasing CalMat Company, a producer of asphalt and ready-mixed concrete based in Los Angeles, for $760 million in cash. This wasn't just another acquisition—it was Vulcan's entry into California, the nation's largest construction materials market. CalMat controlled prime quarry locations throughout Southern California, including irreplaceable reserves near Los Angeles where new permits were virtually impossible to obtain due to environmental restrictions. This growth was due in part to several acquisitions and joint ventures, including the 1998 purchase of CalMat Company, California's leading aggregates producer.

The CalMat deal demonstrated Vulcan's evolved acquisition philosophy. Rather than buying distressed assets cheaply, they were willing to pay premium prices for strategic positions that couldn't be replicated. In densely populated California, where a single quarry might serve millions of people and new mining permits faced decades of environmental review, existing operations were worth far more than their book value. It was a lesson in scarcity economics that would inform Vulcan's strategy for the next decade. Shortly after CalMat, Vulcan made another transformative move. Tarmac America (aggregates production and distribution assets) was acquired on 04-Oct-2000 by Vulcan Materials Company, adding significant East Coast operations and deepening Vulcan's presence in high-growth Southeast markets. While Greece's Titan Cement acquired Tarmac's cement operations for $636 million, Vulcan focused on the aggregates assets—the true prize in their strategic calculus.

By 1999, these acquisitions had transformed Vulcan's scale. Sales for 1997 and 1998 posted respectable single-digit gains of 6 and 7 percent, respectively, while earnings from 1997 to 1998 doubled to 22 percent. Yet 1999 took Vulcan into a vastly different arena, with net sales soaring by 33 percent from 1998's $1.8 billion to 1999's $2.4 billion. The company had crossed a critical threshold—it was now large enough to influence pricing in multiple major markets simultaneously.

Meanwhile, Vulcan's innovative Crescent Market project demonstrated the company's willingness to think beyond traditional boundaries. Vulcan's innovative Crescent Market project led to construction of a large quarry and deep water seaport on the Yucatán Peninsula of Mexico, just south of Cancun. This quarry supplies Tampa, New Orleans, Houston, and Brownsville, Texas, as well as other Gulf coast seaports, with crushed limestone via large 62,000-ton self-discharging ships. The project solved a fundamental problem: Gulf Coast markets needed aggregates, but local geology provided limited rock resources. By shipping limestone from Mexico via specially designed 62,000-ton self-discharging vessels, Vulcan could serve markets that would otherwise be supply-constrained.

The most profound strategic shift came with the decision to exit the chemicals business entirely. For decades, the chemicals division had provided stable cash flows and diversification benefits. But by the early 2000s, it had become clear that the aggregates and chemicals businesses required fundamentally different capabilities, capital allocation strategies, and management focus. The chemicals business faced increasing environmental regulations, required continuous capital investment to remain competitive, and operated in global markets with volatile pricing.

On June 7, 2005, Vulcan completed the sale of its chemicals business, known as Vulcan Chemicals, to Occidental Chemical Corporation. The sale price wasn't disclosed publicly, but the strategic implications were clear: Vulcan was betting everything on aggregates. This wasn't diversification—it was the opposite. The company was concentrating all its resources, management attention, and strategic focus on becoming the dominant player in construction materials.

The timing of this transition proved prescient. The early 2000s saw a construction boom driven by low interest rates, expanding suburbs, and a housing bubble that seemed to have no ceiling. Vulcan's newly focused strategy allowed it to capitalize fully on this growth. Without the distraction of managing a chemicals business, management could focus on optimizing quarry operations, improving logistics, and identifying the next strategic acquisition targets.

By 2005, Vulcan had assembled an enviable portfolio of assets: dominant positions in California through CalMat, expanded Southeast operations through Tarmac, innovative logistics capabilities through the Mexico operations, and a pure-play focus that Wall Street increasingly valued. The company controlled over 350 active aggregates facilities and had proven reserves measured in billions of tons. More importantly, it had developed a deep bench of operational expertise—managers who understood the nuances of local markets, the complexities of permitting, and the art of maximizing value from every ton of rock.

V. The Florida Rock Acquisition: Peak Timing (2007)

The boardroom at Vulcan's Birmingham headquarters hummed with tension on a February morning in 2007. CEO Don James, who had led the company since 1997, stood before a presentation that would define his legacy: the acquisition of Florida Rock Industries for $4.7 billion—by far the largest deal in Vulcan's history. Outside, the construction industry was experiencing unprecedented growth. Housing starts had hit records, commercial development was booming, and infrastructure spending was robust. It seemed like the perfect time for a transformative acquisition.

On February 19, 2007, Vulcan announced that it would buy stone and cement producer Florida Rock Industries for $4.7 billion. The merger consideration was structured as a combination of cash and stock, with seventy percent of Florida Rock shares to be settled in cash at $67.00 per share—a generous premium to the trading price. For Florida Rock shareholders, it was an offer too good to refuse. For Vulcan, it was a bet that the construction boom had years left to run.

Florida Rock brought assets that Vulcan coveted: dominant positions in Florida's high-growth markets, a cement business that provided vertical integration opportunities, and most importantly, irreplaceable quarry locations in a state where environmental regulations made new permits nearly impossible. The company controlled critical infrastructure for serving Florida's booming population growth—from Miami's skyline to Orlando's sprawl to Jacksonville's port expansion.

Don James articulated the strategic rationale with conviction. The combined company would have unmatched scale in the Southeast, the nation's fastest-growing region. Synergies would exceed $100 million annually through optimized logistics, eliminated redundancies, and enhanced pricing power. The cement assets, while not core to Vulcan's pure-play aggregates strategy, could be divested later at attractive multiples. Most compellingly, Florida Rock's quarry locations could never be replicated—in the flat, environmentally sensitive Florida landscape, existing permits were worth their weight in gold.

Wall Street initially cheered the deal. Analysts praised the strategic fit and projected that the combined company would generate record cash flows as America's building boom continued. Vulcan's stock price reflected this optimism, reaching above $122 per share as the acquisition positioned the company to benefit from that decade's building boom.

But there were warning signs for those willing to see them. Housing starts had begun declining in late 2006. Subprime mortgages were defaulting at increasing rates. The credit markets were showing signs of stress. Inside Vulcan, some board members questioned the timing—why pay peak multiples at what might be the top of the cycle? James and his team, however, believed any downturn would be mild and brief, similar to previous cycles the company had successfully navigated.

Vulcan completed the acquisition of Florida Rock on November 16, 2007—almost precisely as the financial world began to unravel. Bear Stearns had collapsed months earlier. The credit crisis was spreading. By the time Vulcan closed the deal, the housing market wasn't just cooling—it was in free fall.

The numbers tell a story of breathtaking destruction. From its peak above $122, Vulcan's stock price collapsed below $40 as the Great Recession devastated construction markets. Housing starts fell by 70%. Commercial construction virtually stopped. State and local governments, facing budget crises, slashed infrastructure spending. Vulcan, which had leveraged its balance sheet to fund the Florida Rock acquisition, found itself with $3.7 billion in debt just as its cash flows evaporated.

The Florida Rock acquisition became a case study in cyclical timing. The assets themselves were excellent—prime quarry locations, strong market positions, good operations. But buying at the absolute peak of the cycle with borrowed money transformed what should have been a strategic triumph into a near-death experience. Vulcan was forced to slash its dividend, lay off thousands of employees, and idle numerous facilities. The company that had spent a century building itself into an aggregates powerhouse was suddenly fighting for survival.

Yet the crisis also revealed Vulcan's underlying strength. Even in the depths of the recession, the company maintained positive cash flow. The irreplaceable nature of its quarry network meant that when construction eventually recovered, Vulcan would still control the essential raw materials. The same transportation economics that created local monopolies in good times provided pricing power even in bad times—customers had no alternative sources for aggregates.

James and his team executed a painful but necessary restructuring. Non-core assets were sold to reduce debt. The cement operations acquired from Florida Rock were eventually divested to Cementos Argos for $720 million in cash, providing crucial liquidity. Operating costs were slashed through facility consolidations and workforce reductions. Most importantly, Vulcan maintained its best quarry locations and customer relationships, preserving the foundation for eventual recovery.

The Florida Rock acquisition offers profound lessons about capital allocation in cyclical industries. The strategic logic was sound—Florida's long-term growth trajectory remained intact, the assets were irreplaceable, and the synergies were real. But timing matters enormously in capital-intensive businesses. The difference between buying at the cycle's peak versus its trough can determine whether a deal creates or destroys shareholder value. Vulcan learned this lesson the hard way, but it would emerge from the crisis as a leaner, more focused company—and with a deep appreciation for the importance of balance sheet strength through cycles.

VI. The Martin Marietta Hostile Takeover Drama (2011-2012)

The December night was bitter cold in Raleigh, North Carolina, as Martin Marietta Materials CEO Ward Nye reviewed the confidential documents one more time. For eighteen months, he had been engaged in secret merger negotiations with Vulcan Materials. Now, with talks collapsed and patience exhausted, he was about to launch one of the most audacious hostile takeover attempts in the construction materials industry's history. The prey would become the predator. The backstory reads like a corporate thriller. Martin Marietta and Vulcan had been exploring a friendly merger since 2010, entering into confidentiality agreements to share sensitive financial data and strategic plans. But as negotiations dragged on, the relative positions of the companies shifted. Martin Marietta, which had initially feared being acquired, watched as Vulcan struggled with the Florida Rock debt burden while its own balance sheet strengthened. Ward Nye, Martin Marietta's CEO, saw an opportunity to flip the script.

After a year and a half of behind-the-scenes negotiations fell apart, Martin Marietta Materials Corp. announced a $4.8 billion buyout bid for Vulcan Materials Co. in December 2011. But this wasn't just any hostile takeover—it was one launched using confidential information obtained during friendly merger negotiations. Martin Marietta had taken Vulcan's internal projections, synergy analyses, and strategic plans—all shared under non-disclosure agreements—and used them to formulate its hostile bid.

Vulcan's CEO Don James was furious. Not only was Martin Marietta trying to steal his company at a depressed valuation, but they were using Vulcan's own confidential information against them. The battle quickly moved to the Delaware Court of Chancery, where some of American capitalism's most important disputes are resolved.

In a much-anticipated decision, a Delaware judge ruled in favor of Analysis Group client Vulcan Materials Company, the target of a $5.3 billion hostile takeover bid by Martin Marietta Materials. Chancellor Leo Strine's opinion was scathing. Martin Marietta Materials "thoroughly breached" confidentiality agreements with competitor Vulcan Materials during merger negotiations and as a result, its effort at a hostile takeover bid would be prohibited for the next four months.

The court found that Martin Marietta had violated both a Non-Disclosure Agreement (NDA) and a Joint Defense Agreement (JDA) by using and disclosing Vulcan's confidential information without consent. Martin Marietta argued that the agreements didn't explicitly prohibit a hostile takeover, but Strine rejected this narrow reading. The agreements prohibited using confidential information except for evaluating a "Transaction," which the court found meant only a friendly, negotiated deal—not a hostile raid.

The Delaware Supreme Court affirmed the Court of Chancery's decision, with the court enjoining Martin from proceeding with a takeover for four months because both Confidentiality Agreements effectively provided a contractual stipulation to irreparable harm. The four-month injunction effectively killed the hostile bid. By the time Martin Marietta could legally proceed, market conditions had changed, Vulcan's stock price had recovered somewhat, and the element of surprise was lost.

The case had broader implications for the industry. It demonstrated that even in the rough-and-tumble world of construction materials, there were rules of engagement. Companies couldn't use the pretense of friendly negotiations to gather intelligence for a hostile assault. The decision also highlighted Vulcan's vulnerability—despite winning the legal battle, the company had been exposed as a potential takeover target with a weakened balance sheet and operational challenges.

For Don James, the victory was bittersweet. He had saved Vulcan from a hostile takeover, but questions about his leadership persisted. Members of the founding family of Vulcan Materials Co. have sued CEO Don James and directors. Glenn and William Ireland filed a derivative lawsuit, claiming James and the Vulcan board erred in not accepting Martin Marietta's buyout offer. They argued that James was protecting his own position rather than maximizing shareholder value.

The Martin Marietta drama revealed deep fissures within Vulcan. Some shareholders and even founding family members believed the company should have accepted the offer, viewing James's resistance as self-serving. Others saw the hostile bid as opportunistic, taking advantage of Vulcan's temporary weakness following the Florida Rock acquisition. The battle lines drawn during this conflict would influence Vulcan's strategic direction for years to come.

VII. Recovery & Strategic Refocusing (2013-2020)

Tom Hill took the helm as Vulcan's CEO in 2014, inheriting a company that had survived near-death experiences but emerged scarred and cautious. A Vulcan lifer who had joined the company in 1986 and worked his way up through operations, Hill understood that recovery required more than financial engineering—it demanded a fundamental rethinking of what Vulcan should be.

The strategic refocusing began with a clear-eyed assessment of the Florida Rock assets. While the quarries were indeed irreplaceable, the cement and ready-mix concrete operations didn't fit Vulcan's pure-play aggregates strategy. Vulcan announced an agreement to sell its Florida cement and concrete operations to Colombia-based Cementos Argos for $720 million in cash. The divestiture was painful—selling assets acquired at peak prices for a fraction of their cost—but it provided crucial debt reduction and simplified Vulcan's business model.

Hill's strategy was elegantly simple: become the best pure-play aggregates company in America. This meant divesting everything that didn't directly support the core aggregates business. Ready-mix plants in non-strategic markets were sold. Cement operations were eliminated. Even some quarries in marginal markets were divested. Every dollar of proceeds went toward debt reduction and reinvestment in the highest-return aggregates facilities.

The operational transformation was equally dramatic. Hill implemented what he called "Vulcan Way of Selling"—a disciplined approach to pricing that emphasized value over volume. Rather than chasing market share with low prices, Vulcan would focus on selling to customers who valued reliability, quality, and service. This meant walking away from some business, but it also meant improving margins on every ton sold.

Technology became a surprising differentiator. While aggregates might seem like the ultimate old-economy business, Hill recognized that operational excellence required modern tools. Vulcan invested in automated crushing equipment that could produce more consistent gradations with less labor. GPS-equipped trucks optimized delivery routes. Drone surveys mapped quarry reserves with unprecedented precision. These investments didn't transform the product—crushed rock remained crushed rock—but they dramatically improved productivity and safety.

The recovery accelerated as the U.S. economy strengthened through the mid-2010s. Housing starts gradually recovered from their recession lows. State and local governments, having deferred maintenance during the crisis, began rebuilding infrastructure. The Federal Highway Trust Fund, while perpetually underfunded, continued to support steady if unspectacular growth in road construction. Vulcan was perfectly positioned to benefit from this recovery, with its streamlined operations and strategic market positions.

In 2017 Vulcan Materials acquired another Birmingham-based company, Aggregates USA, for $900 million, adding 31 facilities in Georgia, Florida, Tennessee, South Carolina and Virginia. This acquisition demonstrated Vulcan's evolved M&A philosophy. Rather than transformative mega-deals like Florida Rock, the company now pursued targeted bolt-on acquisitions that expanded its presence in existing markets or filled strategic gaps. The Aggregates USA assets were immediately accretive, required minimal integration risk, and strengthened Vulcan's Southeastern fortress.

By 2020, the transformation was complete. Vulcan had reduced its debt-to-EBITDA ratio from crisis peaks to conservative levels. Margins had expanded to industry-leading levels through disciplined pricing and operational improvements. The company had successfully navigated the transition from diversified industrial conglomerate to focused aggregates pure-play. Most importantly, it had rebuilt its credibility with investors who had been burned by the Florida Rock debacle.

The COVID-19 pandemic provided an unexpected validation of Hill's strategy. While many industries collapsed in spring 2020, construction was deemed essential in most states. Aggregates demand proved remarkably resilient—roads still needed repair, infrastructure projects continued, and after a brief pause, residential construction exploded as Americans fled cities for suburbs. Vulcan's lean operating model and strong balance sheet allowed it to maintain operations and even continue selective growth investments while competitors retrenched.

VIII. The U.S. Concrete Deal & Growth Strategy (2021-Present)

The Zoom call in June 2021 had an air of déjà vu. Tom Hill was announcing another major acquisition, and investors who remembered Florida Rock held their breath. But this time was different. In June 2021, Vulcan Materials announced they would be acquiring US Concrete (USCR) for $74 per share, a 30% premium on the date of the announcement. The deal is valued at $1.3 billion.

U.S. Concrete wasn't just another aggregates company—it was a major ready-mix concrete producer with operations in many of Vulcan's key markets. The acquisition will allow for integrated expansion of Vulcan and make the subsidiary debt-free with adequate working capital. Unlike the Florida Rock deal, this was about vertical integration in select high-value markets, not geographic expansion. And critically, Vulcan was buying with a strong balance sheet at reasonable multiples, not stretching for a transformative deal at cycle peaks.

The strategic logic was compelling. In markets like New York City, San Francisco, and Dallas, ready-mix concrete commanded premium prices due to logistics constraints and strict specifications. By controlling both the aggregates supply and the ready-mix production, Vulcan could capture more of the value chain while ensuring its aggregates had a guaranteed outlet. It was selective vertical integration—not trying to be all things to all customers, but strategically integrating where it created the most value. More significantly, the timing aligned with a generational infrastructure opportunity. The Infrastructure Investment and Jobs Act (IIJA), signed into law by President Biden on November 15, 2021, authorized $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward "new" investments and programs. For the construction and engineering sector, the Infrastructure Investment and Jobs Act of 2021 (IIJA) is expected to boost national annual construction spending to 7% in each of the next 5 years.

For Vulcan, this represented the infrastructure spending cycle they had been positioning for since the Great Recession. The IIJA allocated $110 billion for roads, bridges and other major infrastructure projects—all requiring massive quantities of aggregates. Unlike previous infrastructure bills that were backloaded or underfunded, this legislation front-loaded spending with clear appropriations. States began planning projects immediately, knowing federal matching funds were secured.

The company's geographic footprint aligned perfectly with infrastructure priorities. Vulcan's strong positions in high-growth Sunbelt states meant it would benefit disproportionately from highway expansion in Texas, Florida, Georgia, and the Carolinas. Its California operations would capture spending on seismic retrofits and highway maintenance. Even its legacy Southeastern quarries would see increased demand from bridge replacements and road repairs. However, Vulcan's international operations faced unprecedented challenges. The Mexican government has suspended the three-year customs permit granted in March 2022 to the Mexican subsidiary of the Company and has begun a proceeding that could result in the revocation of that permit. Since late 2018, Vulcan Materials has been engaged in a NAFTA arbitration with Mexico over Mexico's repudiation of an agreement to unlock a portion of Vulcan's aggregates reserves in Mexico and the arbitrary shutdown of a portion of the Company's quarrying operations there.

The situation deteriorated dramatically in 2023. On Tuesday, March 14, 2023, CEMEX (NYSE:CX), aided by armed Mexican police and military, forcibly entered Vulcan's port facilities near Playa del Carmen. The company has quarried limestone legally in Mexico—on land that it owns—for over 30 years, but President López Obrador's government had taken an increasingly hostile stance, claiming environmental concerns while apparently seeking to expropriate valuable coastal property for tourism development.

This geopolitical risk highlighted a vulnerability in Vulcan's strategy. While the Mexico operations had provided cost-effective access to Gulf Coast markets for decades, political instability could quickly transform an asset into a liability. Should the Company be unable to fully operate in Mexico for the balance of 2022, the potential EBITDA impact would range from $80 million to $100 million, approximately 5% of guidance. While not catastrophic, it demonstrated that even a pure-play aggregates company faced risks beyond market cycles.

Despite these challenges, Vulcan's core U.S. operations continued to thrive. The combination of infrastructure spending, housing demand, and disciplined pricing drove record performance. The company demonstrated that it had learned from past mistakes—maintaining a conservative balance sheet, focusing on operational excellence, and avoiding transformative acquisitions at cycle peaks. The U.S. Concrete deal proved to be immediately accretive, validating the strategy of selective vertical integration in high-value markets.

IX. Business Model & Competitive Moats

To understand Vulcan's competitive advantages, imagine trying to start a competing quarry near Atlanta. First, you'd need to find a suitable rock formation—not just any rock, but granite or limestone that meets strict specifications for construction use. Then you'd need to acquire the land, which near any major city is expensive and likely already developed. Next comes the permitting process: environmental impact studies, traffic analyses, noise assessments, community hearings. In most jurisdictions, this takes 5-10 years if you're lucky, decades if you're not, and sometimes it's simply impossible.

Even if you somehow secured a permitted quarry site, you'd face the tyranny of transportation economics. Aggregates are so heavy relative to their value that trucking costs typically equal production costs at just 30 miles from the quarry. At 50 miles, transportation might be double the production cost. This means a quarry can only economically serve customers within a tight radius—creating what economists call a "natural monopoly" in that local market. A competitor 60 miles away might as well be on another planet.

This transportation moat is Vulcan's primary competitive advantage. The company owns quarries within economic trucking distance of virtually every major U.S. city. In markets like Los Angeles, Atlanta, or Dallas-Fort Worth, Vulcan often controls multiple quarries positioned to serve different parts of the metropolitan area. Customers—concrete producers, asphalt plants, construction companies—have few alternatives. They can't import aggregates from China like steel or lumber. They can't substitute digital solutions like newspapers did. They need rock, they need it locally, and Vulcan has it.

The permitting moat compounds over time. Environmental regulations have made new quarry permits nearly impossible to obtain near major cities. In California, the last significant new quarry permit in a major market was issued in the 1990s. Vulcan's existing permits, some dating back decades, are essentially irreplaceable. As cities expand and encroach on existing quarries, these permitted reserves become even more valuable. It's like owning the only gas station for 50 miles on a desert highway—except the government has banned anyone from building new gas stations.

Reserve life creates another competitive advantage. Vulcan controls over 15 billion tons of proven and probable reserves, representing nearly 100 years of production at current rates. These aren't just numbers on a balance sheet—they're legally permitted, geologically proven rock deposits that would cost tens of billions of dollars to replicate, if replication were even possible. When a construction company signs a multi-year supply agreement with Vulcan, they know the quarry will still be producing long after the project is complete.

The operating leverage in this business model is extraordinary. A quarry has high fixed costs—equipment, labor, permits, land—but very low variable costs. Once you've invested in crushers, screens, and conveyors, the cost to produce an additional ton of rock is minimal. This means that in strong markets, incremental revenue flows almost directly to the bottom line. When demand increases 10%, profits might increase 30% or more. Of course, this leverage works in reverse during downturns, but the local monopoly dynamics provide pricing power that cushions the impact.

Vulcan has systematically enhanced these natural moats through operational excellence. The company operates at lower costs than smaller competitors through economies of scale in purchasing, maintenance, and logistics. Its large reserve base allows for long-term mine planning that optimizes the extraction sequence, maximizing the value of every acre. Sophisticated blasting techniques developed over decades minimize waste and improve product quality. These operational advantages compound the geographic moats, making it even harder for competitors to challenge Vulcan's market position.

Pricing power represents the ultimate test of a moat, and Vulcan has consistently demonstrated it. Even during the Great Recession, when volumes collapsed by 40%, the company maintained positive gross margins and cash flow. This resilience stems from the essential nature of the product—infrastructure must be maintained even in recessions—and the lack of alternatives. When a pothole needs filling or a bridge needs repair, the work can't wait for better pricing from a distant quarry.

The technology disruption that has upended so many industries simply doesn't apply to aggregates. You can't digitize crushed rock. 3D printing might eventually produce some structures, but it still needs aggregate inputs. Autonomous vehicles might reduce transportation costs, but not enough to overcome the basic physics of moving heavy materials long distances. Even recycling, while important in some markets, can't replace virgin aggregates for many specifications. Vulcan's moat isn't just deep—it's getting deeper as regulations tighten and urban expansion continues.

X. Financial Performance & Unit Economics

The numbers tell a story of remarkable financial performance built on the foundation of local monopolies and disciplined execution. Total revenues $ 7,418 million for full year 2024, with Adjusted EBITDA (Full Year 2024): $2.1 billion. These headline figures, while impressive, only hint at the underlying unit economics that drive Vulcan's success.

The real magic lies in the aggregates cash gross profit per ton—the purest measure of Vulcan's pricing power and operational efficiency. Aggregates Cash Gross Profit per Ton (Q4 2024): Expanded 16% to $11.50, while Aggregates Cash Gross Profit per Ton (Full Year 2024): Grew by 12% to $10.61. To put this in perspective, Vulcan is extracting rock from the ground—the most basic commodity imaginable—and generating over $10 of cash gross profit per ton. That's the power of local monopolies combined with operational excellence.

The pricing dynamics deserve special attention. Aggregates Freight-Adjusted Price (Q4 2024): Improved 11%, demonstrating that even in a moderating inflationary environment, Vulcan maintains exceptional pricing power. This isn't price gouging—it's the natural result of supply-demand imbalances in local markets where new supply is essentially impossible to create. When a highway project needs aggregates, the contractor has no choice but to pay Vulcan's prices or truck materials from distant quarries at prohibitive cost.

Operating leverage shows up dramatically in the margin expansion. Adjusted EBITDA Margin: Improved for the eighth consecutive quarter year-over-year. This consistent improvement reflects the high fixed cost/low variable cost nature of quarry operations. Once you've covered your fixed costs—equipment depreciation, labor, permits—additional tons generate exceptional incremental margins. During strong demand periods, this operating leverage can drive margin expansion that would make software companies envious.

The balance sheet tells a story of financial discipline learned from hard experience. Net Debt to Adjusted EBITDA Leverage (Year End 2024): 2.3 times, a conservative level that provides flexibility for acquisitions while maintaining resilience for downturns. At December 31, 2024, the ratio of total debt to Adjusted EBITDA was 2.6 times, or 2.3 times on a net debt basis, reflecting over $600 million of cash on hand. The Company's weighted-average debt maturity was 13 years, and the effective weighted average interest rate was 5 percent.

Return on invested capital provides the ultimate measure of value creation. Return on Invested Capital (Year End 2024): 16.2%. This exceptional ROIC reflects the combination of high margins, efficient asset utilization, and the irreplaceable nature of Vulcan's quarry network. Few industrial companies can sustain ROIC above 15% through cycles—Vulcan has done it consistently by owning assets that literally cannot be replicated.

The capital allocation framework reflects lessons learned from the Florida Rock experience. Growth capital is directed toward highest-return projects—typically debottlenecking existing quarries or adding downstream capabilities in strategic markets. Maintenance capital requirements are relatively modest, around 5-6% of revenue, reflecting the durability of quarry assets. Acquisitions are pursued opportunistically but with strict return criteria and conservative financing. The dividend provides a stable return to shareholders while preserving flexibility for growth investments.

Looking at segment performance, the aggregates business remains the crown jewel, generating the vast majority of profits with minimal capital intensity. The asphalt and ready-mix segments provide strategic value in select markets but require more working capital and face more competition. The company's focus remains clear: maximize the value of the aggregates franchise while selectively participating in downstream markets where integration creates value.

Cost management has become increasingly sophisticated under the "Vulcan Way of Operating" initiative. SAG Expenses (Full Year 2024): 2% lower than the prior year; 7.2% of revenue. This isn't about cutting to the bone—it's about systematic improvements in productivity, from optimized blast patterns that reduce drilling costs to predictive maintenance that minimizes equipment downtime. Every percentage point improvement in cost flows directly to the bottom line given the company's pricing power.

The forward outlook suggests continued strong performance. Against the demand backdrop, I just described, we expect to deliver between 2,350,000,000 and $2,550,000,000 of adjusted EBITDA in 2025. This guidance implies continued margin expansion and demonstrates management's confidence in both the demand environment and their operational execution capabilities.

XI. Playbook: Lessons for Investors & Operators

After studying Vulcan's 115-year journey, several timeless lessons emerge for both investors evaluating industrial companies and operators building them. These aren't abstract theories but hard-won insights paid for with billions in shareholder capital through booms and busts.

Building Local Scale Economies in Commodity Businesses

The first lesson challenges conventional wisdom about commodities. Traditional thinking suggests commodity businesses are terrible investments—undifferentiated products, no pricing power, returns that barely cover cost of capital. Vulcan proves this wrong by showing that local commodities can be wonderful businesses. The key is recognizing that "local" transforms the economics entirely. When transportation costs exceed product value at modest distances, whoever controls local supply enjoys monopoly-like economics. The playbook: identify commodities with high weight-to-value ratios, secure strategic locations near demand centers, then systematically build scale within those local markets.

The Power of Being the Low-Cost Producer

In commodity businesses, being the low-cost producer isn't just an advantage—it's the only sustainable competitive position. Vulcan achieves this through multiple reinforcing factors: scale economies in purchasing and maintenance, superior quarry locations that minimize transportation, operational excellence that maximizes tons per employee, and long reserve lives that enable optimal extraction sequencing. The lesson: in commodities, you must be the low-cost producer or you're eventually dead. There's no middle ground.

Timing Acquisitions Through Cycles

The Florida Rock acquisition stands as a $4.7 billion monument to the importance of cycle timing. Buying at the peak with leverage nearly killed Vulcan. Contrast that with recent acquisitions made with a strong balance sheet at reasonable multiples. The playbook is clear: build financial strength during upturns, then deploy capital aggressively during downturns when assets are cheap and competitors are retrenching. This requires exceptional discipline—resisting the urge to do big deals when times are good and having courage to invest when the outlook appears bleak.

Managing Through Downturns: 2008 and COVID Lessons

Vulcan survived 2008 by recognizing that survival trumps everything else during existential crises. They slashed costs, sold assets, cut the dividend—whatever it took to preserve the core business. But they also maintained critical customer relationships and kept their best assets, positioning for eventual recovery. COVID taught different lessons: with a strong balance sheet, downturns become opportunities to gain share and improve operations while competitors struggle. The key is entering downturns with financial flexibility.

When to Lever Up vs. When to Hunker Down

Leverage amplifies returns in good times but can destroy companies in bad times. Vulcan's experience suggests clear rules: lever up only for acquisitions that are immediately accretive with clear synergies, maintain conservative metrics even after leveraging transactions (target 2-3x debt/EBITDA), and always model downside scenarios assuming revenue drops 30-40%. If the company can't survive that stress test, don't do the deal. The graveyard of industrial companies is littered with those who thought "this time is different" at cycle peaks.

The Discipline of Divesting Non-Core Assets

Vulcan's transformation from diversified industrial to pure-play aggregates demonstrates the power of focus. They sold the chemicals business despite its stable cash flows. They divested cement operations even though vertical integration had strategic logic. Each divestiture was painful—selling assets for less than purchase price hurts—but essential for strategic clarity. The lesson: complexity is the enemy of returns. Better to do one thing exceptionally well than multiple things adequately.

ESG as Competitive Advantage in Extractive Industries

Modern quarry operations face intense environmental scrutiny. Vulcan has turned this challenge into competitive advantage by exceeding environmental standards, creating barriers for new entrants. Their quarry reclamation programs, water management systems, and community engagement initiatives aren't just good citizenship—they're moats that make new permits nearly impossible for competitors to obtain. In extractive industries, ESG excellence protects your social license to operate and creates barriers to entry.

The Innovation Paradox in "Old Economy" Businesses

While Vulcan will never be confused with a technology company, they've systematically adopted technology that improves operations: GPS-guided trucks, automated crushing systems, drone surveying, predictive maintenance algorithms. The lesson: in old economy businesses, innovation means incremental improvements compounded over time, not revolutionary disruption. A 2% annual productivity improvement compounded over decades creates enormous value.

Capital Allocation as the Ultimate Differentiator

Through multiple management teams and economic cycles, capital allocation has determined Vulcan's shareholder returns more than any other factor. The best operators can be undermined by poor capital allocation (Florida Rock), while average operations can generate strong returns through shrewd capital deployment. The framework is straightforward but requires discipline: maintain flexibility through conservative leverage, invest in highest-return projects regardless of glamour, return excess capital to shareholders rather than chase growth, and time major moves based on cycle position, not calendar years.

Culture and Operational Excellence

The "Vulcan Way of Selling" and "Vulcan Way of Operating" might sound like corporate buzzwords, but they represent systematic approaches to continuous improvement in a business where 1% better annually compounds to transformational change. This isn't about breakthrough innovation but rather thousands of small improvements: a better blast pattern that reduces drilling by 5%, route optimization that saves 10 minutes per delivery, predictive maintenance that reduces downtime by 2%. In a high fixed-cost business, these improvements flow directly to the bottom line.

XII. Bear vs. Bull Case Analysis

Bull Case: The Infrastructure Renaissance Thesis

The optimistic case for Vulcan starts with a simple observation: America's infrastructure is crumbling and must be rebuilt. The American Society of Civil Engineers gives U.S. infrastructure a C- grade, estimating $2.6 trillion in needed investment over the next decade. The Infrastructure Investment and Jobs Act represents just the down payment on this massive rebuilding effort. State and local governments, flush with federal funds and facing urgent needs, will drive aggregates demand for years.

Beyond public spending, demographic trends support sustained demand. The U.S. faces a structural housing shortage estimated at 3-5 million units. Whether single-family homes in expanding Sunbelt suburbs or multifamily projects in urban cores, each unit requires hundreds of tons of aggregates for foundations, driveways, and infrastructure. The reshoring of manufacturing, accelerated by supply chain concerns and geopolitical tensions, means new factories, warehouses, and logistics facilities—all aggregates-intensive projects.

The consolidated industry structure enables rational pricing behavior. After decades of consolidation, the top five aggregates producers control over 50% of U.S. production. Unlike the destructive competition seen in fragmented industries, these large players understand that pricing discipline benefits everyone. Vulcan, as the largest player with the best assets, stands to benefit most from this rational oligopoly structure.

The irreplaceable nature of Vulcan's assets grows more valuable over time. Environmental regulations make new quarry permits in metropolitan areas virtually impossible. Existing quarries near cities become more valuable as urban expansion continues and transportation costs rise with fuel prices and driver shortages. Vulcan's 15 billion tons of reserves represent options on decades of future development that cannot be replicated at any price.

Operating leverage provides explosive earnings growth potential. With high fixed costs already covered, incremental volume generates exceptional margins. If volumes grow just 5% annually with 5% price increases, EBITDA could grow 15%+ annually. This operating leverage, combined with disciplined capital allocation, could drive 20%+ annual returns for patient shareholders.

Climate resilience spending represents a new growth vector. Rising sea levels, stronger storms, and extreme weather events require massive infrastructure investments. Seawalls, elevated highways, hardened buildings—all require aggregates. The energy transition itself demands aggregates for wind turbine foundations, solar panel installations, and electric grid expansion. Vulcan benefits regardless of which green technologies win.

Bear Case: The Cycle Peak Warning

The pessimistic view starts with a sobering historical pattern: construction is among the most cyclical industries, and aggregates demand closely follows construction activity. We're potentially near a cycle peak, with interest rates having risen dramatically and signs of cooling in construction markets. When the next recession hits—and one always does—aggregates volumes could fall 20-40%, just as they did in 2008.

Interest rate sensitivity poses immediate risks. Higher rates don't just slow construction activity; they fundamentally change project economics. A commercial development that penciled out at 3% rates might be unviable at 6%. State and local governments, facing pension pressures and budget constraints, might defer infrastructure projects despite federal funding availability. The housing affordability crisis, exacerbated by high rates, could crater residential construction.

Environmental and permitting headwinds continue intensifying. While existing quarries become more valuable as permits get harder, they also face increasing operational restrictions. Noise ordinances, dust controls, traffic limitations—each new regulation increases costs and potentially reduces capacity. Climate activists increasingly target extractive industries, potentially creating political pressure that constrains operations regardless of actual environmental impact.

Limited organic growth opportunities present a strategic challenge. Vulcan already dominates most attractive markets. Organic growth requires either taking share from competitors (difficult in rational oligopoly) or waiting for market growth (limited by economic cycles). This forces reliance on acquisitions for growth, but attractive targets are scarce and expensive. The company risks overpaying for growth or accepting low returns.

Acquisition integration risks loom large. Vulcan deployed $2.3 billion on acquisitions in 2024. Integrating these operations while maintaining operational excellence presents challenges. History shows that serial acquirers often stumble, either overpaying, losing focus, or destroying culture through rapid integration. The larger Vulcan becomes, the harder it is to move the needle without taking greater risks.

Technology disruption, while seemingly remote, can't be dismissed entirely. 3D printing of structures could reduce aggregates demand for some applications. Recycled concrete aggregates might take share in certain specifications. Carbon taxes or emissions regulations could disadvantage carbon-intensive quarrying operations. While none threaten the core business near-term, dismissing disruption entirely ignores history's lessons.

Mexico operations demonstrate geopolitical vulnerabilities. The ongoing disputes with the Mexican government show that even domestic companies face international risks. If Mexico expropriates Vulcan's operations without fair compensation, it's not just the loss of EBITDA—it's the precedent that property rights can be violated. This could impact valuations across the sector as investors price in political risk previously considered minimal.

Valuation concerns merit consideration. At current levels, Vulcan trades at premium multiples to historical averages. The market prices in successful execution of the growth strategy, continued margin expansion, and sustained infrastructure spending. Any disappointment—a delayed infrastructure bill, integration challenges, unexpected cost inflation—could trigger multiple compression. In a recession, the stock could fall 40-50%, as it has in previous downturns.

Synthesis: The Balanced View

The truth likely lies between extremes. Vulcan possesses genuine competitive advantages—irreplaceable assets, local monopolies, operational excellence—that should generate value through cycles. The infrastructure needs are real and will drive demand over the long term. But cycles remain inevitable, and the next downturn will test the company's resilience and management's skill.

For long-term investors, the key question isn't whether a downturn will come—it will—but whether Vulcan can survive it and emerge stronger. The company's improved balance sheet, refined strategy, and experienced management suggest it can. The bear case risks are real but manageable; the bull case upside is substantial if execution continues.

The optimal approach might be patience: wait for the next downturn to build positions, then hold through the full cycle. Vulcan's business model rewards patient capital but punishes market timers who buy at cycle peaks. Like the aggregates business itself, success comes not from revolutionary breakthroughs but from steady accumulation of advantages over time.

XIII. Looking Forward: The Next Chapter

The infrastructure bill implementation alone could drive a decade of growth. With $550 billion in new federal spending now flowing into projects, the multiplier effects are just beginning. Every federal dollar typically triggers state and local matching funds, union pension fund investments, and private sector participation. We're potentially seeing the beginning of a construction supercycle not seen since the interstate highway build-out of the 1950s and 1960s.

The electric vehicle charging network buildout represents an underappreciated demand driver. Building 500,000 EV charging stations by 2030 requires not just the chargers themselves but massive infrastructure: reinforced concrete pads, highway pull-offs, electrical substations, and grid connections. Each charging plaza might require thousands of tons of aggregates. Vulcan's strategic locations along interstate corridors position it perfectly to supply these projects.

Climate resilience construction could dwarf traditional infrastructure spending. Miami alone is considering $5 billion in seawalls and elevated infrastructure. New York's post-Sandy resilience plans exceed $20 billion. Every coastal city faces similar needs. Inland cities must manage increased flooding, requiring expanded storm water systems, reinforced bridges, and elevated roadways. This isn't optional spending—it's existential for many communities. Vulcan's Southeastern and coastal presence aligns perfectly with the highest-risk, highest-spending regions.

The consolidation endgame offers intriguing possibilities. While Vulcan is already the largest aggregates producer, the industry remains fragmented with thousands of small operators. As environmental regulations tighten and capital requirements increase, smaller operators will struggle. Vulcan could acquire dozens of bolt-on operations annually, each too small to matter individually but collectively adding significant capacity and eliminating potential competitors. The end state might be 3-4 super-regional producers controlling 70%+ of U.S. production—a structure that would enable even more rational pricing.

Technology adoption in operations continues accelerating. Artificial intelligence and machine learning applications in quarry operations are still nascent. Imagine AI-optimized blast patterns that maximize yield while minimizing energy use, predictive algorithms that schedule maintenance before failures occur, or autonomous haul trucks that operate 24/7. Each innovation might improve margins by just 1-2%, but compounded over years, they transform the business. Vulcan's scale provides the resources to invest in these technologies and spread costs across massive production volumes.

Leadership transition looms as a critical inflection point. Tom Hill has successfully navigated the post-Financial Crisis recovery and positioned Vulcan for growth. But he's approaching traditional retirement age, and choosing his successor will be crucial. The next CEO must balance operational excellence with strategic vision, maintain pricing discipline while pursuing growth, and navigate both economic cycles and technological change. The wrong choice could unravel decades of value creation; the right choice could unleash another generation of growth.

International expansion remains a wildcard. While the Mexico experience has been challenging, demographic trends suggest enormous infrastructure needs across Latin America. Brazil's infrastructure deficit exceeds even that of the United States. Colombia, Chile, and Peru all face massive urbanization pressures requiring construction materials. Vulcan's expertise in quarry operations and logistics could translate internationally, but political risks and capital requirements present significant hurdles.

The ESG evolution could fundamentally reshape the industry. Carbon pricing, if implemented, would advantage efficient operators like Vulcan while penalizing subscale competitors. Quarry reclamation requirements might make new permits even scarcer, further entrenching incumbents. Water rights in drought-prone regions could become as valuable as the rock itself. Vulcan's proactive ESG approach positions it to benefit from, rather than be disrupted by, environmental regulations.

The next recession—whenever it arrives—will test everything. Vulcan has the balance sheet strength to survive and potentially thrive through a downturn. But each cycle brings surprises. The 2008 crisis nearly destroyed the company despite decades of successful operation. COVID initially looked catastrophic but proved manageable. The next crisis might come from unexpected sources: a commercial real estate collapse, a state and local government funding crisis, or geopolitical disruption. Management's ability to navigate uncertainty will determine whether Vulcan emerges stronger or struggles to recover.

XIV. Epilogue & Key Takeaways

Standing back from Vulcan's 115-year history, what emerges isn't just a corporate success story but a meditation on the nature of competitive advantage in industrial America. This is a company that sells rocks—literally the most basic commodity imaginable—yet generates returns on capital that technology companies would envy. The paradox resolves when you understand that Vulcan doesn't really sell rocks; it sells proximity, reliability, and the irreplaceable right to extract resources from strategic locations.

Why Boring Businesses Can Be Beautiful

The investment world's obsession with disruption and innovation blinds many to the beauty of boring businesses. Vulcan will never have a viral moment, won't revolutionize how we communicate, and can't digitally scale to billions of users. But it owns quarries that cannot be replicated, serves customers who have no alternatives, and operates in markets where new competition is essentially illegal due to permitting restrictions. Sometimes the best investments are hiding in plain sight, disguised by their mundanity.

The aggregates industry teaches us that competitive advantages don't require proprietary technology or network effects. Physics can be a moat—when your product is too heavy to ship economically, you have a local monopoly. Regulation can be a moat—when new permits are impossible, existing operations become priceless. Time can be a moat—when you've operated quarries for decades, your extraction costs are lower than any new entrant could achieve. These old-economy moats might be less glamorous than software platforms, but they're often more durable.

The Power of Local Market Dominance

Vulcan's success demonstrates that in certain industries, local dominance trumps national scale. It's better to be the only quarry within 50 miles of Atlanta than to have quarries scattered across rural America. This concentration strategy—building dense networks in high-growth markets rather than spreading thin across geography—creates reinforcing advantages. Customers depend on you, competitors can't enter, and you can optimize operations across multiple facilities. The lesson applies beyond aggregates: in any business with high transportation costs relative to value, local density beats geographic breadth.

Patient Capital in Cyclical Industries

Perhaps the most important lesson from Vulcan's journey is the value of patience in cyclical industries. The investors who bought Vulcan in 2009 at $25 per share and held through today earned spectacular returns. Those who bought at the 2007 peak above $120 and sold during the crisis lost fortunes. The business didn't fundamentally change—the same quarries, same customers, same products. Only sentiment and cycle position changed. This argues for a contrarian approach: buy cyclicals when everyone fears them, hold through the recovery, and sell (or at least don't buy) when optimism peaks.

The company's history also teaches us about the importance of balance sheet strength through cycles. Leverage amplifies returns in good times but can destroy companies in downturns. Vulcan nearly died from too much debt in 2008, learned that lesson, and now maintains conservative leverage even when activists might push for more aggressive capital structures. In cyclical industries, survival is the prerequisite for success. You can't compound returns if you don't survive the downturn.

Final Reflections on Building an Aggregates Empire

Vulcan Materials stands as a testament to the power of focused execution in an unglamorous industry. From its origins selling industrial waste from Birmingham steel mills to becoming a $35 billion corporation controlling irreplaceable assets across America, the company has demonstrated that sustainable competitive advantages can be built in the most basic industries. The key is recognizing what actually drives value—not technology or innovation, but control of scarce resources, operational excellence, and disciplined capital allocation.

As America embarks on a generational infrastructure rebuild, Vulcan is positioned to benefit enormously. But the company's history reminds us that linear extrapolation is dangerous in cyclical industries. There will be another downturn, another crisis that tests management's skill and shareholders' resolve. The companies that survive and thrive through multiple cycles are those that respect the cycle, maintain financial flexibility, and never forget that in commodity businesses, the low-cost producer wins and everyone else eventually loses.

For investors, Vulcan offers a fascinating case study in finding value where others see only commoditization. For operators, it provides a playbook for building competitive advantages in seemingly advantageless industries. And for students of business history, it reminds us that sometimes the most profound lessons come not from Silicon Valley disruption but from Birmingham quarries, where patient capital and operational excellence compound over decades into something remarkable.

The story of Vulcan Materials is far from over. The next chapter will bring new challenges—technological, environmental, political—that will test whether the company's competitive advantages remain durable. But if history is any guide, betting against a company that controls irreplaceable assets, operates at the lowest cost, and maintains the financial strength to survive downturns has proven to be a losing proposition. In a world obsessed with the new and novel, there's enduring value in owning the rocks beneath our feet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube