Valero Energy: America's Refining Powerhouse

I. Introduction & Episode Roadmap

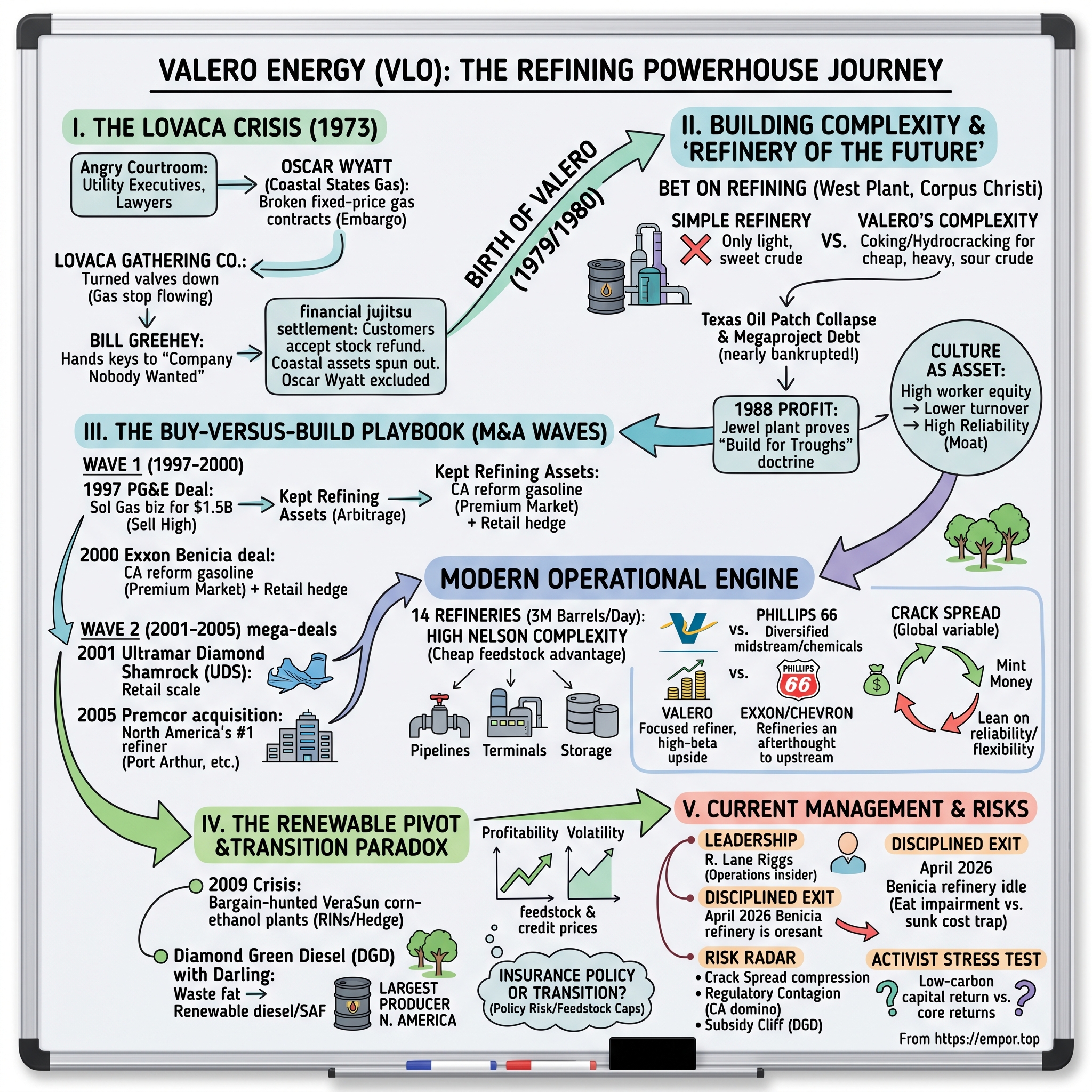

It is a sweltering August afternoon in 1973, and a courtroom in South Texas is packed to the walls with angry men. Utility executives, municipal lawyers, furious purchasing agents from forty-odd Texas towns — they have all come because the gas has stopped flowing. LoVaca Gathering Company, a pipeline subsidiary of Houston's Coastal States Gas, had signed long-term contracts to deliver natural gas at thirty cents per thousand cubic feet. Then the Arab oil embargo hit, spot prices rocketed toward two dollars, and rather than honor a contract that would bankrupt it, LoVaca simply turned the valves down. Homes went cold. Factories went dark. And regulators, when the dust settled, ordered the company to refund its customers $1.6 billion — at the time among the largest such orders in the history of the state.

Into that disaster walked a thirty-seven-year-old finance executive named Bill Greehey, handed the keys to a company nobody wanted. Most observers gave him months. What he built instead, over the next three decades, became the largest independent petroleum refiner in the world: Valero Energy Corporation, named after Mission San Antonio de Valero — the original name of the Alamo.

Fast forward to today. Valero ranks among the largest companies in America by revenue. In a strong year it pushes roughly three million barrels of crude through its plants every single day, and it has somehow also become the largest producer of renewable diesel in North America. In the first quarter of 2026 alone it earned $1.3 billion, or $4.22 per share, as Gulf Coast refining margins surged to $16.06 a barrel.7 This is a company born from a legal cleanup that turned into one of the great counter-cyclical compounding machines of American industry.

How did that happen? That is the story we are going to tell. And we are going to tell it without rooting for the home team. Valero has a genuinely impressive operating record, but it also sits in the most cyclical, most politically exposed, most capital-hungry industry in the country — and it faces an energy transition that could, eventually, shrink its core market to nothing. So as we go, we will keep asking the harder questions: When management says it can win, what is the evidence? And what would prove it wrong?

A few themes will recur. The first is the buy-versus-build playbook — Valero's habit of acquiring multi-billion-dollar refineries at deep discounts to what it would cost to build them, almost always at the bottom of the cycle when sellers are desperate. The second is complexity arbitrage — the unglamorous engineering edge that lets Valero digest the cheapest, ugliest, highest-sulfur crude on earth and turn it into clean fuel. The third is culture as a balance-sheet asset — Greehey's bet that aligning workers with shareholders through equity would lower turnover and raise reliability in a business where a single day of unplanned downtime costs a million dollars or more. And the fourth, the one still unresolved, is the energy-transition paradox: can a refiner credibly become a low-carbon energy company, or is it simply managing a very profitable, very long sunset?

There is also a meta-lesson lurking underneath the whole story, and it is the reason a refiner deserves a careful business history at all. Conventional finance theory says commodity producers should not earn excess returns over a full cycle — when everyone sells an identical product, competition drives prices to the marginal cost of production, and capital gets destroyed in the booms by overbuilding and in the busts by bankruptcy. Refining is the textbook example: capital-intensive, cyclical, undifferentiated. And yet Valero turned a $1.6 billion liability into one of the most valuable downstream energy enterprises on earth. That is an anomaly worth explaining, because the explanation — operate cheaper, buy counter-cyclically, return cash relentlessly, and never fall in love with an asset — is a transferable playbook for any brutal, capital-heavy industry. The neutral investor's job is to figure out how much of that anomaly is durable structure and how much is simply a great operator catching favorable cycles.

Let us start where Valero started — in the wreckage of the worst gas-supply scandal Texas had ever seen.

II. The LoVaca Crisis & The Birth of Valero (1973–1980)

To understand Valero, you have to understand the man who ran Coastal States Gas: Oscar Wyatt, a brilliant, brawling wildcatter who built a sprawling energy empire and made enemies the way other men make small talk. In the late 1960s, Wyatt's LoVaca subsidiary had locked itself into fixed-price gas contracts with cities and utilities across South Texas. It was a reasonable bet in a world of cheap, stable energy. It became a catastrophe the moment the 1973 embargo sent prices vertical. LoVaca was now obligated to sell gas for a fraction of what it cost to acquire — so it curtailed deliveries, raised prices, and triggered a wave of lawsuits and regulatory fury that would drag on for years.2

The man tapped to clean it up had come up inside the company. Greehey had joined Coastal in 1963; by 1968, at thirty-two, he was a senior vice president of finance — the executive who understood the bond indentures nobody else wanted to read. So in 1973 the courts and the company turned to him to negotiate a settlement that most analysts thought impossible.2 He inherited an entity hemorrhaging roughly two million dollars a month, with employee turnover around forty percent, hated by every customer it had.

What Greehey did next set the template for the rest of his career: he ran toward the problem. He stabilized the workforce, laid out concrete goals, and within two months had the operation generating cash rather than burning it. Then came the hard part — convincing some four hundred angry customers to accept a settlement rather than litigate Coastal into oblivion. It took six years. The structure he ultimately negotiated was a piece of financial jujitsu. The disputed assets would be spun out of Coastal into a brand-new, independent company that would fund the $1.6 billion refund. Crucially, the plaintiffs — the very customers who had been wronged — would receive a majority of the new company's stock. And Oscar Wyatt, the architect of the whole mess, would be explicitly excluded from owning any of it. The plaintiffs would not settle on any other terms.2

So on the last day of 1979, Valero Energy Corporation was born — a roughly billion-dollar-revenue company assembled from LoVaca and other Coastal pipeline assets, at the time one of the largest corporate spinoffs the country had seen.2 Greehey chose the name himself, after the Alamo mission, and moved the headquarters to San Antonio. The symbolism was not subtle: a company expected to make a doomed last stand, run by a man who had no intention of losing.

Consider how unusual the cap-table was. The company's largest single block of shareholders was, in effect, its own aggrieved former customers — the cities and utilities that had sued. That is an almost unheard-of way to start a public company, and it imposed an unusual discipline from day one: the owners were the very people the predecessor business had wronged, and they were watching. Whether by design or by temperament, Greehey internalized a stakeholder-first posture early, and it would later flower into the employee-ownership culture that became a genuine competitive asset. The other lesson buried in the founding is about asymmetric opportunity. Most executives, handed a $1.6 billion liability and a forty-percent turnover rate, would have managed for damage control. Greehey treated it as raw material. The same situation that looked like a career-ending booby trap to everyone else looked, to a man who understood balance sheets and human incentives, like a company that could be rebuilt from zero with no entrenched legacy and a clean strategic slate. That reframing — liability as opportunity — is the through-line of the next forty years.

It is worth pausing on what kind of leadership that settlement required, because it foreshadows everything. Greehey did not win by litigating harder than the four hundred plaintiffs or by finding a clever legal escape hatch. He won by sitting across the table from furious counterparties, year after year, and constructing a deal in which they got something real — equity in the new company, the satisfaction of seeing Wyatt cut out — rather than a pyrrhic courtroom victory over a corpse. He restored the operation to profitability while negotiating, so there was a viable business worth fighting over rather than a husk to be carved up. This is the same temperament he would later bring to acquisitions: find the deal where the counterparty is desperate, structure it so both sides can live with it, and make sure the underlying asset is sound enough to be worth owning once the dust clears.

Here is the part worth sitting with as investors. Valero began life owning natural-gas pipelines, a small marine terminal, several hundred million dollars of settlement-related debt — and not a single refinery. Its entire reason for existing was to discharge a liability. Nothing about that origin suggested a future refining champion. What it did provide was something subtler and more durable: a CEO who had spent six years staring down hostile creditors and learned, in his bones, that the best assets often come attached to the worst situations. That instinct — that crisis is where value hides — would become the company's defining edge. But first Greehey had to decide what this orphaned pipeline company was actually going to be.

III. Bill Greehey: The Corporate Architect & The "Refinery of the Future" (1980–1996)

Bill Greehey did not come from energy royalty. He was born in 1936 in Fort Dodge, Iowa, in a working-class neighborhood where nearly everyone, including his father, worked at the gypsum mill for close to minimum wage. There was a roof and there was love, he would later say, but not much money. What shaped him was watching his mother try business after business — a bakery, a fish market, a small restaurant — never striking it rich but never stopping either. He worked odd jobs from the age of twelve. After high school he enlisted in the Air Force, which stationed him at Lackland in San Antonio, and on the GI Bill he enrolled at St. Mary's University, parking cars at a hospital at night and on weekends while attending classes by day with a wife and two children at home. He finished an accounting degree, with honors, in under three years.2

That biography matters because it explains the operating philosophy. Greehey's signature move, again and again, was to take the job nobody else wanted — the unreadable bond indenture, the toxic subsidiary, the half-built refinery — and turn it into a platform. He had no romance about glamour. He had a deep, almost physical understanding of cash, risk, and the value of being the person who does the hard thing.

By 1981, Greehey had made the defining strategic decision of Valero's early life. Natural-gas pipelines were regulated, low-growth, and going nowhere exciting. Refining, by contrast, was where crude got turned into transportation fuel — the actual engine of the economy. So he bet the company on building a grassroots refinery in Corpus Christi, the plant later known as the West Plant. The projected cost was around $100 million. The timing was about as bad as timing gets.

Through the early 1980s, the Texas oil patch collapsed. Crude fell from nearly forty dollars a barrel toward the low teens. The savings-and-loan crisis gutted regional banks; commercial real estate cratered. And Valero's refinery, beset by the cost inflation and scope creep that plague every megaproject, ballooned from that $100 million estimate to something on the order of $750 million. The company piled on debt, fell behind schedule, and bled cash. The Wall Street parlor game became guessing the date of bankruptcy, not whether it would come.

But Greehey had designed something the doubters underestimated. While the rest of the industry built simple refineries that could only process expensive, light, low-sulfur "sweet" crude, Greehey built complexity. The Corpus Christi plant was engineered with heavy coking and hydrocracking capacity — the expensive equipment that lets a refinery digest cheap, heavy, high-sulfur "sour" crude that nobody else wanted. Think of it this way: most refineries are like a kitchen that can only cook prime cuts. Greehey built a kitchen that could take the cheapest, toughest scraps and turn out the same premium dish. When the spread between cheap heavy crude and expensive light crude was wide, that capability minted money. When margins were thin, it was the difference between surviving and dying. The West Plant would become known as the last grassroots refinery built in the United States, and one of the most complex in the world.1

The payoff was not immediate — the early results were genuinely catastrophic. By the mid-1980s, with crude in freefall and construction debt crushing the income statement, the company faced a real prospect of insolvency, and the only way through was triage. In 1987 Greehey made the surgeon's decision: separate the steady, cash-generating gas business from the money-losing refinery, so the former could keep the latter alive while oil markets healed. It was the corporate equivalent of clamping off a bleed to save the patient. The bet was that refining conditions would eventually turn — and in 1988 they did, with Valero posting a genuine profit for the first time in years. The plant that nearly killed the company had become its crown jewel, and the lesson Greehey drew was permanent: build the business to survive catastrophe, because in commodities catastrophe always comes.

That lesson would be tested again, brutally, in 2009, when the financial crisis collapsed refining margins and Valero bled roughly a million dollars a day for a stretch, laid off hundreds of workers, and ultimately shut a refinery in Delaware City. Both times — the 1980s and 2009 — Valero survived where weaker competitors did not, and the reason was not luck but design: feedstock flexibility, geographic diversity, and a balance sheet built for the troughs rather than the peaks.

Alongside the engineering, Greehey built something rarer in heavy industry: a workplace people did not want to leave. Profit-sharing, premium benefits, and a culture of genuine employee ownership — eventually approaching a fifth of the company's stock held by its own workforce — pushed turnover to roughly half the industry average and landed Valero, repeatedly, on Fortune's "100 Best Companies to Work For," reaching number three the year Greehey retired.2 Skeptics dismiss this as feel-good corporate folklore, and it is fair to ask whether it actually drove returns. The mechanism is concrete: in a refinery, an engaged operator who notices a leaking seal or an off-spec reading at 3 a.m. prevents the unplanned shutdown that costs millions; a workforce that owns equity has skin in exactly those small decisions. Low turnover also preserves the hard-won tacit knowledge of how to run a specific, idiosyncratic plant safely. That is not soft HR spending — in this industry it is an operating moat. The question now was whether Greehey could turn one great refinery into an empire. The answer would come from learning to buy instead of build.

IV. The First Wave of M&A: Playing the Cycles (1997–2000)

By the mid-1990s, refining sat at the bottom of a brutal cycle, and refineries were being dumped at fire-sale prices. The integrated oil majors — Exxon, Chevron, Shell — had decided that the real money was upstream, in finding and producing oil, and that downstream refining was a low-return nuisance to be shed. Greehey, who had nearly gone bankrupt building a refinery, looked at the same landscape and saw the opposite conclusion: why build when you can buy world-class assets for, as he liked to put it, ten cents on the dollar?

But before he could go shopping, Greehey pulled off the single most elegant piece of financial engineering in the company's history. In 1997, Pacific Gas & Electric agreed to acquire Valero's natural-gas operations in a deal valued at roughly $1.5 billion. California was deregulating its power market, and electric utilities were desperate for gas assets — Valero was selling into a feeding frenzy of billion-dollar utility-gas combinations. Here is the beautiful part: rather than a simple sale, Valero merged its gas business into PG&E and spun its refining assets into a new publicly traded company that kept the Valero name. In effect, Greehey sold the natural-gas business — the very thing the company had been created around — for $1.5 billion in cash, and got to keep the Corpus Christi refinery essentially for free. He had sold the house and kept the garage, then set about turning the garage into a mansion.

Armed with that cash, Valero moved fast. In 1997 it bought three Gulf Coast refineries from Basis Petroleum — two in Texas, one in Louisiana — instantly becoming the largest independent refiner on the Gulf Coast. Then, in 2000, came the strategically pivotal deal: Valero paid roughly $895 million, plus about $120 million for inventories, to acquire Exxon's Benicia refinery in the San Francisco Bay Area along with some 350 Exxon-branded service stations.

Benicia mattered for two reasons that reveal how Greehey thought. First, it opened the door to California's reformulated-gasoline market — the cleaner-burning fuel the state's regulators require, which trades at a structural premium to ordinary Gulf Coast gasoline precisely because so few refineries can make it. Roughly seventy percent of Benicia's output was that premium California gasoline. Buyers in California, in other words, had nowhere else to go. Second, the retail stations gave Valero a counter-cyclical hedge: retail fuel margins tend to widen exactly when refining margins compress, smoothing the company's earnings through the cycle. As Greehey put it, retail was a natural growth area because its margins moved opposite to refining.

It is worth dwelling on why the PG&E transaction was such a masterstroke, because it shows Greehey thinking like a capital allocator rather than an operator. He recognized two things the market was mispricing simultaneously. California utilities, scrambling for gas assets in a deregulation land-rush, would overpay for exactly the kind of pipeline business Valero no longer wanted — so he sold high into a frenzy. And the refining assets he was keeping were being valued by the market as if refining were a permanently dying business — so he held low. The merger-and-spinoff structure let him capture both mispricings in a single, tax-efficient stroke, and it left the new pure-play Valero with a war chest and no encumbering legacy business. Selling your weakest asset at the top of its market to fund the accumulation of your strongest assets at the bottom of theirs is the entire game, and few executives ever pull it off this cleanly.

In three short years, from 1997 to 2000, Valero transformed from a one-refinery Texas operator into a national player spanning the Gulf Coast, the Midwest, and the West Coast, with revenue climbing from under $2 billion toward $14 billion. The strategic logic underneath the shopping spree was consistent and, in hindsight, formidable: buy complexity others couldn't operate, in markets others couldn't enter, at prices far below replacement cost, using a balance sheet kept deliberately flexible. It worked because Greehey understood that in a commodity business the cheapest assets always come up for sale at the moment of maximum pessimism. And the pessimism was about to get a lot deeper — which, for Valero, meant the opportunities were about to get a lot bigger.

V. Consolidating North America: The Ultramar and Premcor Mega-Deals (2001–2005)

In September 2001, Bill Greehey walked into Valero's San Antonio boardroom and proposed swallowing a company much larger than his own. The target was Ultramar Diamond Shamrock — UDS — a refining-and-marketing colossus with seven refineries across the U.S. and Canada, more than 5,000 retail outlets, and revenues that dwarfed Valero's. The price was about $6 billion: roughly $4 billion in equity and $2 billion of assumed debt.[^4] Wall Street's first reaction was disbelief. How could a company absorb a competitor of comparable or greater size without choking on the integration? And the deal closed in December 2001 — three months after the September 11 attacks had collapsed air travel and refining demand along with it.

Greehey's logic was, once again, counter-cyclical and structural. UDS brought enormous retail scale (those counter-cyclical margins again), a large North American footprint reaching into Canada, and a midstream logistics business that Valero would later spin off. The regulators extracted their pound of flesh — the FTC required Valero to divest the Golden Eagle refinery in Northern California and dozens of retail stations to preserve competition in the California gasoline market.[^4] But when the dust settled, Valero had vaulted into the top tier of American refiners, with a dozen-plus refineries and throughput approaching two million barrels a day. The integration, far from the predicted disaster, delivered synergies well ahead of plan — bulk purchasing, logistics optimization, and the transplant of Valero's operating culture onto a much larger base.

Four years later came the deal that made Valero number one. On April 25, 2005, Greehey announced an $8 billion acquisition of Premcor, adding refineries in Port Arthur, Texas; Memphis, Tennessee; Delaware City, Delaware; and Lima, Ohio.3 The structure let Premcor holders choose stock or cash — roughly 0.99 Valero shares or $72.76 per share — with the cash portion capped at half the total. The deal vaulted Valero past every rival to become the largest refiner in North America.3

The bears had an obvious objection: Valero was buying at the top of the refining cycle, paying a rich multiple for assets whose earnings might be at a peak. Greehey's rebuttal was the heart of the buy-versus-build doctrine, and it is worth understanding because it is the company's central capital-allocation argument to this day. The Port Arthur refinery alone, he pointed out, would cost something like $4.4 billion to replicate from scratch — and that is if you could even get the permits, which in practice you could not, because no major grassroots refinery had been built in the U.S. since the 1970s. So even paying what looked like a full price on near-term earnings, Valero was acquiring sophisticated, sour-crude-capable, effectively irreplaceable assets for a fraction of their replacement value. As Greehey told analysts, the company was buying strategic refineries for far less than what it would cost to build them, and would improve their profitability by capturing synergies and raising reliability.3

Was he right? On the numbers of the moment, yes: 2005 net income roughly doubled to about $3.6 billion, and the Premcor plants delivered hundreds of millions in synergies. But the honest, neutral read is more nuanced. The replacement-cost argument is genuinely powerful — irreproducible assets purchased below reproduction cost are a real edge — yet it is also the argument every acquirer at a cyclical peak reaches for. The test is not the logic but the through-cycle returns, and there the verdict is mixed: Delaware City, one of the Premcor plants, would be shut down within a few years when the financial crisis crushed margins. Buying irreplaceable assets cheaply is a great strategy; it does not make every individual plant a winner.

There was one more move in this era that revealed the financial sophistication underneath the operating story. In 2006, Valero spun off its midstream logistics arm — the pipelines and terminals it had partly inherited through the UDS deal — into a separately traded partnership, Valero LP, soon renamed NuStar Energy. The logic was pure capital-markets arbitrage: stable, fee-based pipeline cash flows command a far higher valuation multiple inside a tax-advantaged partnership structure than they do buried on a volatile refiner's balance sheet. By separating them, Valero crystallized value that the market had been undervaluing. It was the same instinct that would later drive the CST Brands retail spinoff — create value inside the conglomerate, then unlock it through a clean separation when the market will pay a premium for the pure-play pieces. For investors, this is a tell about management's mindset: Valero has consistently treated its corporate structure as something to be optimized, not preserved for its own sake.

Greehey, now sixty-nine, stepped down as CEO in January 2006 and as chairman a year later, handing off the largest independent refining system on the continent. The empire was built. The question for his successors was whether they could keep it disciplined — and whether the assets themselves would age gracefully.

VI. Modern Operational Engine & Segment-Level Realities (2006–Present)

Walk into Valero's operations center in San Antonio today and you are looking at the nerve center of a continent-spanning machine. After idling the Benicia refinery in April 2026 — more on that shortly — Valero runs fourteen petroleum refineries with a combined throughput capacity in the low three-million-barrels-a-day range, with the bulk of that capacity clustered on the Gulf Coast near the crude supply, the export docks, and the cheap natural gas that fuels the plants.1 In the first quarter of 2026 the system ran about 2.9 million barrels a day.7 Refining is, overwhelmingly, the business — generally the source of the large majority of operating earnings in any normal year, with everything else a rounding error by comparison.

The engineering edge that Greehey designed in the 1980s is now embedded across the whole fleet. Valero's portfolio carries a high average Nelson Complexity rating — the industry's standard yardstick for how much upgrading equipment a refinery has — meaningfully above the U.S. average.1 The practical translation: when heavy Mexican Maya or Canadian Western Select crude trades at a wide discount to light benchmark crude, Valero's plants can gorge on the cheap stuff and convert it into premium clean fuel, capturing a feedstock discount that simpler refineries simply cannot. Across three million barrels a day, even a few dollars of discount per barrel compounds into very large numbers. This is the complexity-arbitrage moat, and it is real — but it is worth stressing that it is a relative advantage that lives and dies with the heavy-light crude spread, which itself swings with OPEC policy, Canadian production, and sanctions on heavy-crude producers like Venezuela. The moat widens and narrows; it does not stand still.

The post-Greehey leadership kept running the buy-versus-build playbook, including across the Atlantic. In March 2011, under CEO Bill Klesse, Valero agreed to buy Chevron's Pembroke refinery in Wales — one of the largest and most complex refineries in Western Europe, with roughly 270,000 barrels a day of capacity and a high complexity rating — for about $730 million plus roughly a billion dollars of working capital, bundled together with interests in pipelines, fuel terminals, an aviation-fuel business, and a network of more than a thousand Texaco-branded wholesale sites across the UK and Ireland.4 The deal was vintage Valero on three counts: it was struck cheaply in the wreckage of the European downturn, it acquired complexity (the ability to run cheaper crudes), and it came with logistics and marketing infrastructure that widened the company's optionality. It also dovetailed with a portfolio-pruning move in the opposite direction — Valero had exited the high-cost U.S. East Coast in 2010 by selling refineries in Delaware City and Paulsboro, and could now serve that Atlantic Basin market from Wales whenever the economics favored it. Exit the disadvantaged assets, buy the advantaged ones cheaply, and arbitrage the geographic spread in between: the doctrine did not change just because the founder had left.

The second pillar of the operating story is reliability, and here the evidence is more straightforwardly in Valero's favor. The company consistently runs its plants at high utilization — generally above the industry average — and in refining, utilization is close to destiny. Every day a unit is down for an unplanned reason can cost one to two million dollars in lost margin. Decades of standardized processes, disciplined turnaround planning, and a safety culture that empowers any worker to halt an unsafe operation have made Valero one of the more reliable operators in the business. When you cannot differentiate your product — a gallon of gasoline is a gallon of gasoline — running your assets harder and safer than the next operator is the competitive advantage.

There is a third, quieter pillar that rarely makes headlines but matters enormously: logistics. Valero owns or controls thousands of miles of pipelines, vast crude and product storage, and dozens of marine terminals. This infrastructure is what turns geographic diversity into a money-making advantage rather than a coordination headache. It lets the company source crude from wherever it is cheapest, move product to wherever margins are richest, store output through a margin trough to sell into a recovery, and keep running during disruptions that cripple less-integrated competitors. When Hurricane Harvey shut down much of the Houston refining complex in 2017, Valero's network let it keep supplying customers from plants outside the storm's path while rivals scrambled. In a business of pennies per gallon multiplied across billions of gallons, the ability to physically optimize the flow of molecules is a structural edge that is easy to overlook on the income statement.

How does that stack up against the competition? The U.S. refining industry is now a consolidated oligopoly dominated by a handful of players, and consolidation is itself a structural tailwind — fewer, larger, more disciplined operators are less prone to the ruinous price wars that historically savaged refining margins. Marathon Petroleum is the other titan, operating the country's single largest refinery at Galveston Bay and a comparable company-wide footprint to Valero.10 Phillips 66 sits a notch below on pure refining scale — its wholly-owned and joint-venture refineries totaled roughly 1.9 million barrels a day before it closed its Los Angeles refinery at the end of 2025 — but it trades at a premium to Valero because it has diversified into midstream and chemicals, which the market rewards with steadier, less cyclical multiples.10 The integrated supermajors, ExxonMobil and Chevron, refine too, but their downstream operations are an afterthought to their upstream exploration businesses, and their refineries often underperform a focused independent precisely because capital and management attention flow elsewhere.

That contrast frames the investment debate neatly. Valero is the relatively pure-play, highly efficient refining operator — it does one thing and does it about as well as anyone. That purity is a feature when crack spreads are fat: there is maximum leverage to the upside, as the swing from a Q1 2025 loss to a $1.3 billion Q1 2026 profit demonstrated. It is a liability when margins collapse, because there is little diversification to cushion the blow. An investor choosing between Valero and a diversified peer is, at bottom, choosing how much cyclicality they want to own. The market prices that choice explicitly, awarding the diversified names a valuation premium for their smoother earnings and the pure-play a discount for its volatility. Neither is "better" in the abstract; they are different risk profiles, and the honest framing is that Valero is the higher-beta way to express a bullish refining view.

It helps to make the crack spread concrete, because it is the single concept a reader most needs to internalize. A common shorthand is the "3-2-1 crack" — the margin from taking three barrels of crude and producing two barrels of gasoline and one of distillate (diesel and jet). When that spread on the Gulf Coast runs above roughly $25 a barrel, a low-cost operator like Valero mints money; when it compresses below $15, the company leans on its complexity discount, its reliability, and its renewable and logistics operations just to defend acceptable returns. The brutal truth of the business is that this number is set by the global balance of crude supply and refined-product demand, not by Valero — which is why the same fleet of plants produced a net loss in early 2025 and a $1.3 billion profit a year later.7 Operational excellence determines how much of the available margin Valero captures; it does not determine how much margin exists to capture.

One more structural move shaped the modern company: in 2013, Valero spun off its retail gas stations into a separate public company, CST Brands, which was later acquired by Alimentation Couche-Tard.5 At the time, retail had been Greehey's prized counter-cyclical hedge — so why give it up? Because by 2013 the strategic logic had flipped. Valero wanted to be a focused wholesale manufacturer of fuels, freeing capital and management attention for the low-carbon investments it was beginning to make, and the market was willing to pay a higher multiple for retail as a standalone business than it did buried inside a refiner. It was the same value-unlocking instinct that had separated NuStar's pipelines years earlier. Which brings us to the most debated chapter of the modern Valero story: the bet on renewables.

VII. The Renewable Pivot: Diamond Green Diesel & SAF Optionality

The first move into renewables came, characteristically, in the depths of a crisis. In 2009, with the financial crash crushing refining margins and Valero losing roughly a million dollars a day, the company went bargain-hunting in an unexpected aisle: it bought ten corn-ethanol plants out of bankruptcy, mostly assets of the failed producer VeraSun, scooped up for a fraction of their construction cost. Critics scratched their heads — why was an oil refiner buying corn-ethanol plants? The answer was vintage Valero. Ethanol is blended into virtually every gallon of U.S. gasoline by federal mandate, the plants were available for pennies on the dollar, and they fit the existing logistics and blending operation. Today that ethanol segment produces well over a billion gallons a year and, in 2025, delivered roughly $374 million in operating income on record production — a small but genuinely profitable, counter-cyclical complement to the core.9

It is worth understanding why those ethanol economics work at all, because the same machinery underpins the much larger renewable-diesel bet. The U.S. Renewable Fuel Standard obligates refiners and importers to blend rising volumes of biofuels into the nation's gasoline and diesel, and compliance is tracked through tradable credits called RINs — Renewable Identification Numbers — attached to each gallon of biofuel produced.[^13] A company that produces qualifying biofuel generates valuable RINs; a refiner that does not blend enough must buy them. Owning ethanol and renewable-diesel production therefore does double duty: it earns the product margin and generates the compliance credits Valero would otherwise have to purchase to satisfy its own obligations as a fuel manufacturer. In other words, a chunk of the renewable business is best understood not as a standalone profit center but as a hedge against the regulatory cost of being a refiner in the first place. That framing also flags the central fragility, which we will return to: the value of the whole structure is created by government mandate and can be diminished by government decision.

The bigger and more strategic bet was Diamond Green Diesel, the 50/50 joint venture Valero formed in 2011 with Darling Ingredients, a rendering company that collects waste animal fats and used cooking oil.[^6] The concept is elegant: take low-value waste fats and grease, run them through hydrotreating equipment much like a refinery's, and produce renewable diesel — a fuel chemically near-identical to petroleum diesel, but one that qualifies for lucrative low-carbon incentives. Renewable diesel earns federal credits and, crucially, California Low Carbon Fuel Standard credits, and it can be sold through the same pipelines and trucks as ordinary diesel. Darling sources the waste feedstock; Valero contributes the refining know-how and the offtake. The venture scaled aggressively — a major St. Charles expansion, then a second plant at Port Arthur — to roughly 1.2 billion gallons of annual capacity, making Valero the largest renewable-diesel producer in North America.1 On top of that, the partners added sustainable aviation fuel capability at Port Arthur, capable of upgrading a large slice of the plant's output into clean jet fuel for airlines facing their own decarbonization mandates.1

Here is where neutrality matters, because the renewable story is often told too cleanly. Diamond Green Diesel is real, it is the largest player in its niche, and in good years it has been very profitable — it earned on the order of $507 million of operating income in 2024. But in 2025 it swung to a full-year operating loss of roughly $156 million.9 What happened? Two things collided: the cost of waste-fat feedstock climbed as more renewable-diesel capacity chased the same limited supply of grease, and the price of the environmental credits that underwrite the economics fell. Then, just as quickly, the segment snapped back to $139 million of operating income in the first quarter of 2026 alone.7 That is a business swinging from a nine-figure annual loss to a nine-figure quarterly profit — extraordinary volatility that tells you something important. Renewable-diesel margins are not really a fuel business; they are a policy and feedstock-spread business, and both inputs are outside Valero's control.

The newest layer is sustainable aviation fuel. The partners added SAF capability at the Port Arthur plant, capable of upgrading a large share of its output into clean jet fuel for airlines facing their own decarbonization mandates and corporate ESG commitments.1 On paper this is attractive: jet fuel is one of the hardest fuels to electrify, so it is a corner of the energy system where liquid hydrocarbons — and their low-carbon substitutes — will be needed for decades, and SAF commands a premium over conventional jet fuel. But the same skeptical lens applies. Airline demand for SAF is, today, overwhelmingly a function of regulation and voluntary pledges rather than unsubsidized economics; airlines will buy it as cheaply as compliance allows, not at any price. Whether SAF becomes a durable high-margin business or merely a compliance commodity depends, once again, on policy choices outside Valero's control.

So how should an investor weigh the renewable segment as a whole? It is plausibly material to the long-term case — it is the company's most credible claim to relevance in a decarbonizing world, it leverages existing refining infrastructure and hydrotreating know-how, and Valero has deliberately structured Diamond Green Diesel as a self-funding joint venture rather than a balance-sheet cash sink. But "optionality" is the honest word for it, not "transformation." Its profitability depends on the persistence of subsidies that a future Congress or a future California administration could alter with the stroke of a pen, and on a waste-feedstock pool — used cooking oil, animal fats — that is structurally finite and increasingly contested as competitors build their own renewable-diesel capacity. The bet is rational and cheaply held; the conviction it deserves is moderate, not absolute. The right way to hold it in your head is as an insurance policy with a fluctuating premium, not as the second act of the Valero growth story. And that same disciplined-but-clear-eyed posture — invest, but never fall in love, and never let the option consume capital the core business has better claims on — is exactly what the current management team is being tested on.

VIII. Inside Current Management: Riggs, Alignment, and Incentives

Succession at Valero has been notably orderly, which is itself a governance data point. Greehey handed to Bill Klesse, Klesse to Joe Gorder, and Gorder to the man running the company today — each a long-tenured insider, each promoted from within, with none of the disruptive outsider-CEO drama that so often destroys value in industrial companies. The man in the chair now did not parachute in from Wall Street. R. Lane Riggs joined the company in 1989 as an entry-level process engineer at the McKee refinery in the Texas Panhandle, and spent the next three-plus decades climbing through operations — the refineries, the commercial organization, the chief operating officer's chair — before succeeding Joe Gorder as CEO and president on June 30, 2023, and adding the chairman's title on January 1, 2025.1 In an industry where the work is fundamentally about running dangerous, complex chemical plants safely and reliably, there is something fitting about a lifelong engineer in the corner office. Riggs talks like an operator, not a marketer, and the strategy under him has been continuity rather than reinvention: run the assets hard, return cash to shareholders, and keep the renewable bets disciplined.

The clearest test of his judgment came in California. For years, Valero — like every refiner in the state — had absorbed a tightening vise of regulation, fees, and litigation, even as California's unique fuel specifications nominally offered premium margins. In April 2025, Riggs made the hard call: Valero filed notice with the California Energy Commission of its intent to idle the Benicia refinery, the same plant Greehey had bought in 2000, by the end of April 2026.8 The company took a roughly $1.1 billion pre-tax impairment charge against Benicia and Wilmington combined.68 By the time you read this, Benicia has been idled, and Valero plans to supply Northern California instead through imported blendstock — keeping the profitable marketing position while shedding the money-losing manufacturing.

This is exactly the kind of decision that reveals management quality, and it deserves credit on its own terms. The trap that destroys value in capital-intensive industries is the sunk-cost trap — pouring fresh capital into a structurally disadvantaged asset because closing it means admitting the original purchase was a mistake. Riggs refused the trap, ate the impairment, and reallocated. That is the behavior of a management team optimizing for through-cycle returns rather than for ego or for next quarter's optics. It is also, bluntly, an indictment of California's policy environment, which has now driven multiple major refiners to exit the state.

Assessing management credibility, though, requires looking at behavior over time rather than at a single good decision, and here the record is reassuringly consistent. Across the post-Greehey leadership, the narrative has not lurched: run the assets safely and at high utilization, buy counter-cyclically when assets are cheap, prune the disadvantaged plants without sentiment, and return a large and steady share of cash flow to owners. The capital-return discipline is not just rhetoric — even in a weak refining year like 2025 the company kept paying and buying back, and in the first quarter of 2026 it returned $938 million to shareholders while raising the dividend.79 Management has framed its target as returning a high proportion of operating cash flow through the cycle, and the actuals have broadly tracked the promise. When things have gone wrong — the renewable-diesel loss, the California exit — the explanations on the earnings calls have been specific and mechanical (feedstock spreads, credit prices, regulatory costs) rather than evasive or blame-shifting. That consistency between what is said across filings and calls and what actually happens is, for a long-term investor, worth more than any single quarter's beat.

On alignment, the structure is about as shareholder-friendly as large-cap refining gets, at least on paper. Valero's governance requires the CEO to hold company stock worth a high multiple of base salary, and Riggs personally owns a substantial stake — several hundred thousand shares worth tens of millions of dollars — so his net worth genuinely moves with the stock.11 The pay package is overwhelmingly variable and at-risk, with short-term incentives weighted toward the operational metrics that actually drive a refiner's results — mechanical availability and refining operating cost per barrel — and long-term incentives delivered entirely in equity, half of it tied to relative total shareholder return against a peer group of energy companies, with payouts that can swing from zero to double the target.11 There are strict no-hedging and no-pledging rules and a clawback policy.11 The skeptic's caveat is worth stating: relative-TSR plans reward beating a basket of equally cyclical peers, which can pay out handsomely even in a year when shareholders lost money in absolute terms, simply because the other refiners did worse. Alignment is strong, but it is alignment to relative performance in a sector that can sink together. With management's incentives on the table, the real question becomes whether the business itself has durable advantages — or just a good operator riding a cyclical wave.

IX. Strategic Playbook: 7 Powers, Porter's 5 Forces, & Competitor Benchmarking

Strip away the narrative and ask the cold question: what, exactly, protects Valero's profits from competition? In a commodity business, the default answer is "nothing" — which is why most commodity companies destroy capital over a full cycle. Valero is an exception worth dissecting, and Hamilton Helmer's 7 Powers framework is a useful scalpel.

The first and most important power is scale economies, but in a specific form — call it the complexity advantage. Building a coker unit, the equipment that cracks heavy oil residue into valuable products, costs hundreds of millions of dollars whether it sits at a small regional plant or a giant one. For a 100,000-barrel-a-day refiner, that is a prohibitive bet. For a three-million-barrel-a-day system, it is a rounding error spread across an enormous base. Scale, in other words, is what enables complexity, and complexity is what lets Valero buy the cheapest crude on earth. The same scale lets the company optimize crude purchasing globally and shift production between plants to chase regional margins. This is a genuine, durable edge.

The second power is a cornered resource, though not the usual kind — it is the refineries themselves, plus their permits and logistics. No major grassroots refinery has been built in the United States in roughly half a century, because the environmental permitting is effectively impossible to obtain. That regulatory wall, paradoxically, protects the incumbents: every existing complex refinery is an asset that literally cannot be reproduced. This is the deep logic behind Greehey's replacement-cost doctrine, and it grows stronger, not weaker, as older simple refineries close and the surviving complex capacity becomes more precious. The third power is process power — the accumulated operating excellence, embodied in that industry-leading reliability and low operating cost per barrel, that cannot be bought off the shelf or replicated in a quarter.

Run the same business through Porter's Five Forces and the picture sharpens. The threat of new entrants is essentially zero — you cannot build a new refinery, full stop. Buyer power is low: clean-fuel specifications like California's CARB gasoline and federal Tier 3 standards mean buyers must purchase from compliant complex refiners, and gasoline is a daily necessity for hundreds of millions of drivers. Supplier power is moderate and partly neutralized by Valero's feedstock flexibility — when one crude grade gets expensive, the plants can switch to another, which blunts the pricing power of any single producer or cartel. The two forces that genuinely threaten the business are rivalry, which is intense and undifferentiated — a structural reason refining margins are so violently cyclical, since every operator sells an identical commodity into the same market — and the threat of substitutes, which is the existential long-term question. Electric vehicles are a real, slow-moving substitution threat to gasoline, the largest single product. Diesel and especially jet fuel are far harder to electrify and will persist much longer.

It is worth making the complexity advantage tangible, because it is the least intuitive of the powers. Picture two kitchens. One can only cook with prime, pre-trimmed cuts bought at full price; the other has the equipment and skill to take the cheapest, toughest, fattiest scraps the butcher cannot sell and turn them into the same finished dish. On any given night both restaurants charge the same menu price — the product is identical — but the second kitchen pockets the difference between cheap inputs and expensive ones. A Valero coker and hydrocracker do exactly that with crude oil: they upgrade heavy, high-sulfur residue that simpler refineries cannot process into the same gasoline and diesel everyone else sells. Because that upgrading equipment is enormously expensive to build and only pays off at scale, it is precisely the kind of advantage that compounds for the largest operators and stays out of reach for the small ones. That is scale economics and process power working together, and it is the most durable, least policy-dependent edge Valero has.

The honest synthesis: Valero has a legitimately defensible position against competitors — the entry barriers, cornered assets, and operating edge are real and not mere management rhetoric. What it cannot fully defend against is the market itself shrinking, and against the savage cyclicality that comes from selling a commodity. The moat protects share of a pie whose ultimate size is set by forces — crude spreads, fuel demand, government policy — that no refiner controls. That is precisely where the risks live.

X. Risk Radar & Activist/Skeptical Investor Stress Test

Start with the risk that dwarfs all others on any given quarter: crack-spread compression. The crack spread — the gap between what Valero pays for crude and what it gets for refined products — is the master variable, and it is wildly volatile. Gulf Coast refining margins sank to roughly $8.44 a barrel in late 2024, a level at which higher-cost refiners flirt with negative cash margins, before recovering sharply to $16.06 a barrel by the first quarter of 2026.7 That is the whole business in one statistic: the same assets, the same team, producing a net loss in early 2025 and a $1.3 billion profit a year later, driven almost entirely by a margin Valero does not set.7 No amount of operational excellence fully insulates a pure-play refiner from this. It is the single most important thing for an investor to watch, and it is fundamentally unpredictable quarter to quarter.

The second risk is regulatory and policy contagion — the "California domino." Benicia's closure was driven by a regulatory environment that made refining there uneconomic, and it was not an isolated event: Phillips 66 closed its Los Angeles refinery at the end of 2025, and California now faces a genuine question about in-state fuel supply. The live concern for Valero shareholders is whether other states — Washington, Oregon, New York among them — adopt California-style low-carbon and air-quality regimes that force further closures or load the surviving plants with compliance costs. There is a genuinely perverse silver lining for survivors: each closure removes supply and tightens the market, supporting margins for the refineries that remain standing, and Valero's posture of supplying California through imported blendstock rather than in-state production may prove the smarter side of that trade. But the broader signal is unambiguous and unfavorable — the political direction of travel in the country's most populous and trend-setting states is hostile to the core product, and that hostility raises the cost and lowers the strategic value of refining assets wherever the contagion spreads. A skeptic would note that "everyone else is closing, so our margins improve" is a comforting story right up until the demand those closures were responding to also disappears.

The third risk sits on the renewable side: the subsidy cliff. Diamond Green Diesel's economics rest on a stack of government supports — federal production credits and California's Low Carbon Fuel Standard chief among them. A shift in federal policy or a re-rating of LCFS credit prices can flip the segment from profit to loss, as 2025 demonstrated in real time. This is policy risk dressed up as a clean-energy growth story, and it should be underwritten as such.

Now put on the activist's hat and stress-test the strategy directly. A skeptical long-short investor would press hardest on capital allocation into low-carbon projects. Why, the argument runs, is Valero deploying capital into renewable ventures at lower return hurdles than traditional refining, in a segment that just posted a nine-figure annual loss, when that capital could be returned to shareholders or invested in the higher-returning core? Is sustainable aviation fuel a genuine economic opportunity or a compliance-driven narrative that airlines will buy only as cheaply as regulation forces them to? Management's defense is coherent: the renewable bets are structured to be capital-light and largely self-funding through the joint venture, they leverage existing infrastructure, and they function as a relatively cheap insurance policy on Valero's long-term relevance. The activist's rejoinder is that "insurance policy" is the language companies use to justify projects that would not clear the hurdle on their own merits. Both are partly right. The fair verdict is that the renewable strategy is defensible as modest optionality but would become a real governance problem if management ever let it grow into an empire-building exercise that consumed capital the core business and shareholders had better claims on. So far, the cash-return discipline suggests they understand that line — which sets up the closing question of where the durable value actually comes from.

XI. Epilogue, Lessons & The Bear vs. Bull Cases

Step back from the quarter-to-quarter noise and Valero's record is genuinely remarkable: a company conjured out of a $1.6 billion legal liability that became the largest independent refiner in the world, throwing off billions in cash and returning the bulk of it to shareholders. In the first quarter of 2026 alone it sent $938 million back to investors through dividends and buybacks, having raised its dividend to $1.20 a share in January, even as it absorbed the Benicia wind-down.7 For full-year 2025, a mediocre refining year, it still produced about $2.3 billion of net income — $3.3 billion adjusted — and roughly $6 billion of operating cash flow.9 This is not a company in distress. It is a disciplined cash machine in a violently cyclical industry.

The bull case is straightforward and rests on the moats we have already dissected. Valero is the most efficient, lowest-cost, most reliable large-scale operator of irreplaceable complex assets, and as older simple refineries close — in California and around the world — the survivors' capacity becomes more valuable, supporting structurally firmer margins for the disciplined few. The renewable-diesel and SAF franchise, funded largely off petroleum cash flows rather than dilutive equity or expensive debt, gives the company a credible foothold in whatever low-carbon fuel market ultimately materializes. And management has shown it will return 40 to 50 percent of operating cash flow to shareholders through the cycle and will close losing assets rather than feed them. If you believe liquid transportation fuels — especially diesel and jet — will be needed for decades, Valero is arguably the highest-quality way to own that reality.

The bear case is equally coherent and should not be waved away. The energy transition is a one-way demand threat to gasoline, Valero's single largest product; as EVs approach cost parity, the slope of gasoline's decline could steepen faster than the managed, gradual fade the bulls assume. The whole bull thesis quietly depends on demand declining slowly — a gentle couple of percent a year that allows orderly capacity rationalization and sustained profitability. A sharper drop would trigger industry-wide distress, and the timing of that inflection is genuinely unknowable. California's regulatory squeeze is a live preview of how quickly a hostile policy environment can render even a premium asset uneconomic. Refining margins themselves are unforecastable and can stay compressed for years when new mega-refineries in Asia and the Middle East flood the global market faster than demand grows, and as a relatively pure-play refiner Valero has less diversification to cushion those troughs than a more integrated peer. The renewable pivot, meanwhile, depends on subsidies that a future administration can curtail and on a structurally scarce waste-feedstock pool that intensifying competition is already bidding up — a dynamic that could permanently cap the margins of the very business that is supposed to guarantee long-term relevance. And environmental liabilities, litigation, and compliance costs only ever seem to ratchet in one direction. The deepest bear worry is not any single one of these but the possibility of being caught in the middle of the transition — neither a pure cash-returning sunset play harvesting a declining asset, nor a credible clean-energy growth company — and rewarded for neither.

So what should an investor actually watch? Three things, above all, and resisting the temptation to drown in the dozens of metrics a refiner discloses each quarter. First and foremost, the crack spread — specifically the Gulf Coast refining margin per barrel — because it swamps everything else in any given period and is the truest real-time read on the core business. A reader does not need to model it; they need only watch which direction it is moving and how far it sits from the rough breakeven zone for higher-cost competitors, because that gap is where Valero's profits are made. Second, refinery reliability and throughput utilization, the operational metric where Valero's edge is most durable and most within management's control. When crack spreads are strong, the binding constraint on profit is simply how many barrels you can physically run; sustained high utilization is the proof that the operating moat is intact and that the company is capturing the available margin rather than leaking it to downtime. Third, the renewable-diesel result and the policy backdrop behind it — the segment's swing from a 2024 profit to a 2025 loss to a strong first quarter of 2026 is the cleanest gauge of whether the energy-transition bet is creating value or quietly consuming it, and the trajectory of federal biofuel credits and California's low-carbon credit prices is the leading indicator beneath that swing. Track those three and you understand most of what matters about Valero; everything else is detail.

Where does that leave a long-term investor weighing the two cases? Not at a verdict — that depends on one's own read of the transition's slope and one's tolerance for cyclicality — but at a clear sense of what the debate actually hinges on. The bull and bear cases do not really disagree about Valero's competitive quality; both sides largely concede that it is among the best operators in its industry. They disagree about the industry. The bull is buying a high-quality company in a shrinking but long-lived and consolidating market, betting that disciplined cash returns more than compensate for the eventual fade. The bear is selling the market, not the company, betting that no amount of operating excellence outruns a contracting addressable demand and violent cyclicality. That is a genuinely useful clarification, because it tells the investor exactly what to monitor: this is a bet on the durability and slope of liquid-fuel demand, mediated by an unusually capable operator, not a bet on whether that operator can out-execute its peers. It probably can.

The deepest lesson of the Valero story is the one Bill Greehey learned in a hostile courtroom in 1973 and never unlearned: in cyclical, commoditized industries, the spoils go to the lowest-cost operator with the financial flexibility to buy when everyone else is selling and the discipline to return capital when there is nothing worth buying. Valero mastered that balance across four decades and three near-death cycles. Whether that mastery is enough to navigate a transition that threatens not the company's competitive position but the size of its market itself — that is the question the next decade will answer, and it is one no amount of operating excellence can settle in advance. Crisis, after all, is where this company was born. It may yet be where it is tested again.

References

-

Valero Energy 2024 Annual Report (Form 10-K) — SEC EDGAR, 2025-02-21 ↩↩↩↩↩↩↩

-

William E. Greehey — Horatio Alger Association member biography ↩↩↩↩↩↩

-

Valero to Acquire Premcor for $8 Billion to Become Top Refiner — Oil & Gas Journal, 2005-04-25 ↩↩↩

-

Valero to Buy Chevron's Pembroke Refinery for $730 Million — Reuters, 2011-03-11 ↩

-

CST Brands Retail Spinoff (Form 10-12B/A) — SEC EDGAR, 2013-04-12 ↩

-

Valero to Idle California Refinery Benicia; Takes $1.1B Impairment — Reuters, 2025-01-23 ↩

-

Valero Energy Reports First Quarter 2026 Results — Valero Investor Relations, 2026-04-30 ↩↩↩↩↩↩↩↩

-

Valero Announces Notice to the California Energy Commission Regarding its Benicia, California, Refinery — Valero Investor Relations, 2025-04-16 ↩↩

-

Valero's refining segment drives higher 2025 earnings — Oil & Gas Journal, 2026-01 ↩↩↩↩

-

U.S. refining capacity largely unchanged as of January 2025 — U.S. Energy Information Administration, 2025 ↩↩

-

Valero Energy Corporation SEC filings (proxy statements and Section 16 insider filings) — SEC EDGAR ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube