Virtu Financial: The High-Frequency Trading Machine

Introduction and Episode Roadmap

What if there was a company that made money 1,238 out of 1,238 trading days in a single year? Not a hedge fund with a brilliant macro call. Not a tech giant riding a secular trend. A trading firm, making money every single day, in every kind of market, through flash crashes and financial crises, through meme stock manias and pandemic panics. That company is Virtu Financial.

Virtu sits at the intersection of technology and finance in a way that few companies do. With a market capitalization hovering around six billion dollars, it operates as a market maker across more than 235 trading venues in 36 countries, touching equities, options, fixed income, currencies, commodities, and digital assets.

On any given day, Virtu might handle a quarter of all U.S. retail equity order flow. It quotes prices on 25,000 securities simultaneously. And it does all of this with fewer than a thousand employees.

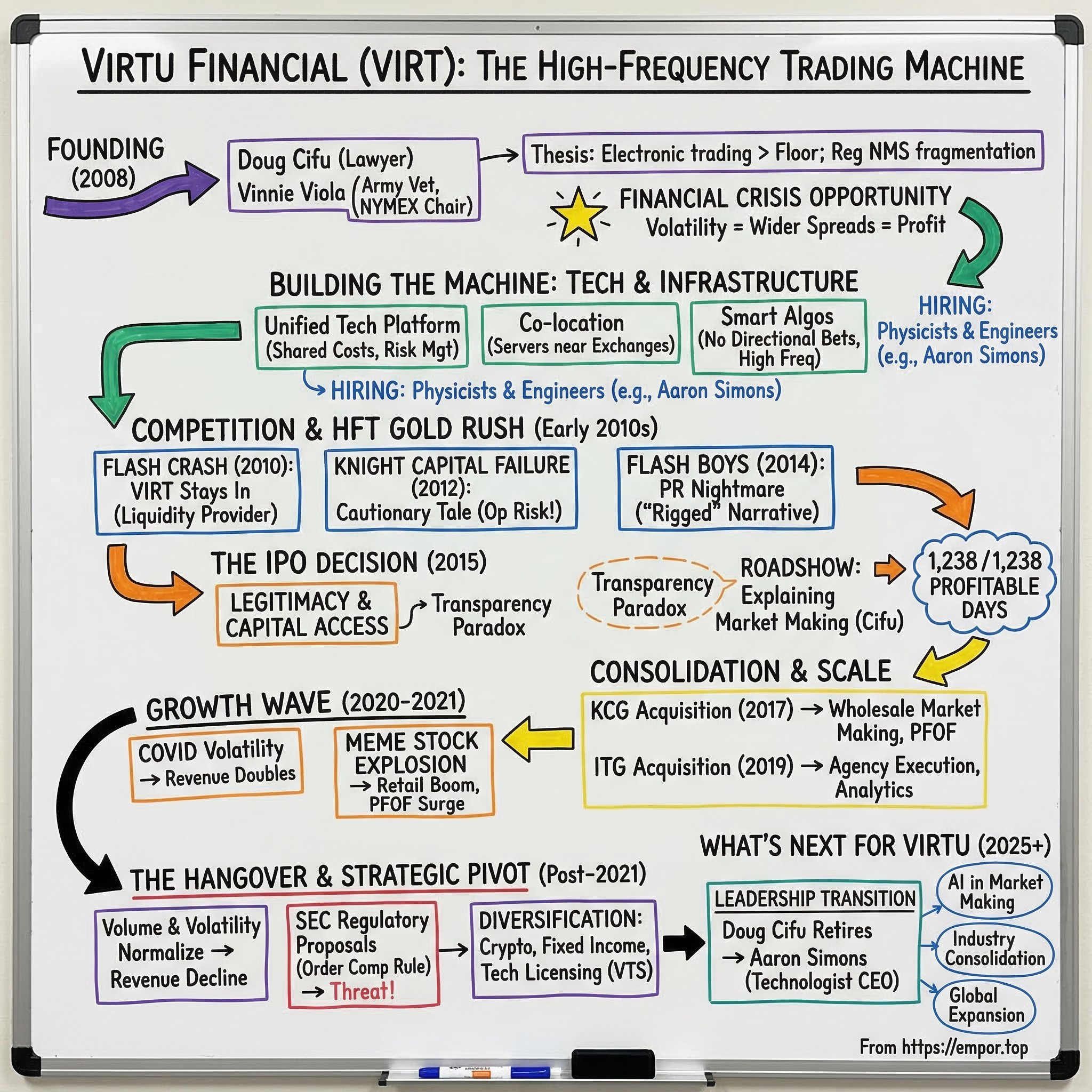

The central question of this story is deceptively simple: How did a secretive trading shop, founded in the depths of the 2008 financial crisis by an Army veteran and a corporate lawyer, survive the Flash Crash, beat Volmageddon, outlast nearly every competitor, and emerge as one of the most consistently profitable financial firms in history? The answer involves a fascinating blend of technology as competitive moat, regulatory arbitrage that most investors never think about, and the relentless evolution from pit trading to microsecond execution.

This is a story about modern market structure, the invisible infrastructure that makes stock markets work, and the people who figured out how to build a machine that prints money, almost literally, every single trading day. It is also a story about what happens when that machine gets dragged into the spotlight, vilified by bestselling authors, scrutinized by Congress, and forced to justify its existence to a skeptical public. Along the way, there are billion-dollar acquisitions, catastrophic competitor failures, meme stock explosions, and the constant tension between secrecy and transparency that defines the high-frequency trading industry.

The themes that run through Virtu's story are universal ones in business: the power of technology to create seemingly insurmountable advantages, the role of regulation in both creating and destroying opportunity, and the challenge of building a durable business in an industry where your competitors are literally trying to be faster than you by nanoseconds.

To set the stage with some key numbers: Virtu generated $3.63 billion in revenue in fiscal year 2025, employed fewer than a thousand people, and achieved an Adjusted EBITDA margin that hit 65 percent in its best quarter. The company's stock, listed on the NYSE under the ticker VIRT, trades around $39, giving it a market capitalization of roughly $5.8 billion. It pays a quarterly dividend of $0.24 per share and has been a consistent repurchaser of its own stock. In July 2025, the company completed its most significant leadership transition when co-founder and CEO Doug Cifu retired and was succeeded by Aaron Simons, a theoretical physicist who had been with the firm since its founding year.

Before diving in, it is worth understanding what market making actually is at its most basic level. When you place an order to buy a stock through your brokerage app, someone has to be on the other side of that trade. That someone is increasingly likely to be Virtu Financial. The company stands ready to buy and sell securities all day, every day, earning a tiny profit on each transaction, the spread between what it pays and what it sells for, but doing it millions of times per day across thousands of securities. It is, in essence, the middleman of the modern stock market, and understanding whether that middleman is a parasite or a vital organ is the central debate that has followed Virtu throughout its existence.

The Origin Story: Doug Cifu Meets Vinnie Viola

Picture the New York Mercantile Exchange in the early 1980s. The trading floor is a cathedral of controlled chaos, men in colored jackets shouting and gesturing, paper tickets flying, the air thick with adrenaline and body heat. Standing in the middle of this pandemonium is a young West Point graduate named Vincent Viola, fresh from the 101st Airborne Division, applying the discipline of military training to the primal arena of commodity trading.

Viola had graduated from West Point in 1977, completed Army Airborne, Infantry, and Ranger Schools, and could have pursued a career in the military. Instead, he arrived at the NYMEX in 1982, where he began trading energy futures. The skills transferred more naturally than one might expect. Reading a chaotic battlefield, making split-second decisions with incomplete information, managing risk when the stakes are existential: these are as relevant in a trading pit as they are in combat. Viola thrived. By 1987, he had founded Pioneer Futures, which became one of the top futures trading firms in the country. He made millions trading oil around the Gulf War, served as Vice Chairman of the NYMEX from 1993 to 1996, and became its Chairman from 2001 to 2004. The man understood markets, not as abstract concepts but as physical, visceral things.

On the other side of Manhattan, Douglas Cifu was building a very different kind of career. A magna cum laude graduate of Columbia University who earned his law degree from the same institution, Cifu joined the white-shoe law firm Paul, Weiss, Rifkind, Wharton and Garrison in 1990. He was the archetypal corporate attorney: meticulous, analytical, comfortable with complexity. He made partner in 1999, served on the Management Committee, became Deputy Chairman of the Corporate Department, and co-headed the Private Equity Group. Private Equity International named him one of the 30 most influential lawyers in global private equity in 2006. By any measure, Cifu had already won the professional game.

But something was pulling him toward a different kind of challenge. Through professional and personal networks, Cifu and Viola found each other, and they recognized something in each other's skill sets that was deeply complementary. Viola understood markets, risk, and the physical infrastructure of trading. Cifu understood corporate structure, capital formation, regulation, and the legal architecture that would be necessary to build a financial technology company in an increasingly complex regulatory environment.

Their founding thesis, crystallized in 2008, was both simple and prescient: electronic trading was eating floor trading alive, and the fragmentation of markets created by recent regulation had opened an enormous opportunity for technology-driven market making.

The Regulation National Market System, known as Reg NMS, had been fully implemented in 2007, and it fundamentally reshaped how stocks traded in America. Before Reg NMS, the New York Stock Exchange handled the vast majority of trading in its listed stocks. After Reg NMS, orders could be routed to any venue offering the best price, which meant that dozens of exchanges and alternative trading systems suddenly competed for order flow.

Think of it like this: before Reg NMS, buying a stock was like going to a single department store where prices were set by the store. After Reg NMS, it was like shopping on the internet, where dozens of retailers compete for your order and the best price wins. This fragmentation was a headache for traditional investors who had to navigate a suddenly complex landscape, but for a firm with the right technology to monitor and trade across all these venues simultaneously, it was a goldmine.

The complementarity of the founding team cannot be overstated. In the world of high-frequency trading, most firms were started by technologists or traders. Virtu was started by someone who understood market structure from the inside, Viola, and someone who understood corporate governance, regulation, and capital formation, Cifu. This combination meant that from day one, Virtu was not just a trading firm; it was a company built to be a company, with the legal architecture, compliance framework, and corporate structure that would eventually enable it to go public and acquire billion-dollar competitors. Most HFT firms are partnerships or LLCs run like academic labs or hedge funds. Virtu was built to be an institution.

On March 19, 2008, Virtu Financial Operating LLC was formally established. The timing seemed terrible. Lehman Brothers would collapse six months later, Bear Stearns had just been rescued, and the financial world was coming apart. But for Viola and Cifu, the crisis was actually the opportunity. Volatility creates wider bid-ask spreads, which creates more profit for market makers. Fear creates trading volume. And the collapse of established financial institutions meant that talented technologists and traders were suddenly available for hire.

The funding decision was telling. Rather than taking private equity money, which would have come with strings, board seats, and a clock ticking toward an exit, Viola and Cifu bootstrapped the company. Viola provided $8.9 million and Cifu contributed $300,000 in founder loans in October 2008. Viola made additional loans of $2 million and $3 million in 2009. These modest amounts, by Wall Street standards, were repaid by 2011, just three years after founding. The company was profitable almost immediately, a fact that would later become both its greatest selling point and its biggest PR problem.

The bootstrapping decision deserves emphasis because it was unusual for the era and consequential for the company's culture. Private equity investors in 2008 were circling the wreckage of the financial system, looking for exactly the kind of technology-driven financial services opportunity that Virtu represented. Taking PE money would have provided a larger war chest, but it would have also imposed external timelines, governance structures, and exit expectations. By keeping control, Viola and Cifu could build patiently, reinvesting profits into technology rather than paying dividends to outside investors. This patient capital approach would prove to be a meaningful competitive advantage, as many PE-backed HFT firms were pushed to optimize for short-term returns rather than long-term infrastructure building.

There is another dimension to the founding story that often gets overlooked. Viola was not just any floor trader; he was the former Chairman of the NYMEX, meaning he had a deep, insider's understanding of how exchanges operated, how they set their fee structures, and how the shift from physical to electronic trading would reshape the industry. He had watched the NYMEX itself go through this transition, seeing open-outcry pits gradually emptied by electronic platforms. He knew, with the certainty of someone who had lived through it, that this transformation was coming to equity markets too, and that the firms best positioned to benefit would be those that treated technology not as a tool but as the business itself.

Building the Machine: Technology and Infrastructure

The server room of a high-frequency trading firm does not look like a hedge fund office. There are no Bloomberg terminals, no traders shouting into phones, no whiteboards covered in macro forecasts. Instead, there are rows of precisely positioned servers, each one co-located within feet of an exchange's matching engine, connected by dedicated fiber optic channels. Temperature is controlled to the fraction of a degree. Latency is measured in microseconds, millionths of a second. In this world, the speed of light is not fast enough.

Virtu's core insight from its earliest days was that market making at scale is fundamentally a technology problem, not a trading problem. The human brain, no matter how brilliant, cannot process the information flowing across 235 trading venues simultaneously and make optimal pricing decisions in microseconds. Only a machine can do that.

So Virtu built a machine.

The co-location strategy was foundational. By placing servers physically adjacent to exchange matching engines in data centers across the world, Virtu shaved microseconds off its execution times. In a business where the difference between profit and loss on any individual trade might be a fraction of a penny, those microseconds compound into enormous advantages across billions of trades. Think of it this way: if a grocery store could restock its shelves one second faster than every competitor, it would not matter much. But if it could restock a billion shelves a day, each one second faster, the cumulative advantage would be staggering.

What truly differentiated Virtu from the dozens of HFT firms that launched in the same era was its unified technology platform. Most competitors built separate systems for different asset classes, one for equities, another for options, another for currencies, and so on. Virtu built a single platform that could handle all of them. This was not merely an elegant architectural choice; it was an economic weapon. A unified platform means shared infrastructure costs, faster deployment of new strategies across asset classes, and simpler risk management. When your competitors need five teams to do what you do with one, your cost structure is fundamentally different.

The proprietary algorithms at the heart of Virtu's system analyze hundreds of parameters simultaneously: order flow dynamics across multiple venues, real-time volatility estimates, correlation matrices between related instruments, inventory positions, and dozens of other variables. These algorithms complete pricing decisions in nanoseconds and can adjust quotes across thousands of securities simultaneously in response to changing market conditions. The "secret sauce" is not any single algorithm but the integrated system: the hardware, the software, the data feeds, the risk models, all working together in a continuous feedback loop.

Risk management was not an afterthought; it was the entire philosophy. Virtu's approach to market making was built on a simple principle: never take directional bets. A traditional hedge fund might decide that Apple stock is going up and buy it. Virtu does not care whether Apple goes up or down. It cares about buying at one price and selling at a slightly higher price, thousands of times per second, while maintaining a roughly neutral position. The system is designed to hold inventory for the shortest possible time, ideally seconds or minutes, almost never overnight. This is why the firm could make money nearly every day: it was not betting on markets, it was taxing the friction of markets.

To grasp the inventory management challenge, imagine running a used car dealership where prices change every second. You buy a car for $20,000, and by the time you have finished the paperwork, it might be worth $19,500 or $20,500. If you hold too many cars in inventory and prices drop, you lose money. If you do not hold enough, you miss sales. Virtu's algorithms solve this problem across 25,000 securities simultaneously, constantly adjusting how many shares of each security they are willing to hold, how wide to set their spreads based on current volatility and inventory levels, and when to aggressively trade out of positions that are becoming too large. The fact that the system manages to do this profitably on virtually every trading day is a testament not to any single breakthrough but to the cumulative refinement of thousands of small optimizations over nearly two decades.

The hiring strategy reflected this technology-first philosophy. Virtu did not recruit from Goldman Sachs trading desks or hedge fund analyst programs. It recruited physicists, mathematicians, and software engineers. Aaron Simons, who joined Virtu in 2008 after completing postdoctoral research in theoretical physics and would eventually become CEO in 2025, epitomized the type. These were people who thought in terms of systems, optimization, and probability distributions, not in terms of "this stock looks cheap."

This hiring philosophy was not unique to Virtu, nearly every HFT firm recruited from the same talent pool, but Virtu's approach to talent was distinctive in one important way. Because the firm was building a unified platform rather than separate systems for each asset class, it could offer engineers and quantitative researchers the opportunity to work on problems that spanned the full breadth of financial markets. A physicist at Virtu might work on equity market-making algorithms one month and currency pricing models the next, a breadth of experience that was harder to find at more siloed competitors. This mattered for retention in an industry where top talent was constantly being poached.

The competitive landscape was brutal. Citadel Securities, backed by Ken Griffin's billions, was building a similar but even larger operation. Jump Trading in Chicago, Two Sigma in New York, Optiver and IMC in Amsterdam, all were pouring resources into the same arms race. The firms that failed, and there were many, typically stumbled on one of three things: inadequate risk management that led to catastrophic losses, technology that could not keep up with the pace of change, or insufficient scale to amortize the enormous fixed costs of the infrastructure. Virtu avoided all three, and by 2012, it had established itself as one of the top-tier HFT market makers globally, consistently profitable and growing.

The arms race dynamic deserves its own explanation, because it illustrates something fundamental about the HFT industry. In most businesses, being ten percent better than your competitor might earn you ten percent more market share. In high-frequency trading, being one microsecond faster can mean the difference between capturing a trade and losing it entirely. This creates an escalating investment dynamic: every improvement by one firm forces all competitors to match or exceed it, which triggers the next round of investment. The result is an industry that spends enormous sums on technology, from custom-designed silicon chips to microwave transmission towers that shave microseconds off data transmission times between Chicago and New Jersey. For Virtu, the key was not necessarily being the absolute fastest, though speed mattered, but having the most efficient overall system. Speed without intelligence is just expensive latency. Virtu's edge was in combining fast execution with smart algorithms and iron-clad risk management into a single, unified platform.

The early profitability also highlighted a counterintuitive truth about the HFT business: during its golden age in the late 2000s and early 2010s, the economics were extraordinary. Spreads were still wide enough, competition was still diffuse enough, and technology advantages were still durable enough that a well-run firm could generate outsized returns on relatively modest capital. The question was always whether these economics would last. As more firms entered the space and the arms race intensified, margins would inevitably compress. The firms that survived would be the ones that had built enough scale and enough operational excellence to remain profitable even as per-trade margins shrank toward zero. Virtu was building for that future even while enjoying the present.

The Competitive Landscape and the HFT Gold Rush

The high-frequency trading industry in its early 2010s heyday resembled nothing so much as the California Gold Rush. The opportunity was real, the early returns were spectacular, and firms poured into the space with the conviction that speed and technology would yield limitless profits. At its peak, there were hundreds of proprietary trading firms globally pursuing some variant of the HFT strategy. The names that would eventually matter, Citadel Securities, Virtu, Jane Street, Optiver, IMC, Jump Trading, were already emerging as leaders, but they were surrounded by scores of smaller shops that would eventually be squeezed out by margin compression and rising technology costs. The competitive dynamics of this period would shape everything that followed.

At 2:32 p.m. on May 6, 2010, the Dow Jones Industrial Average began falling. Within minutes, it had dropped over a thousand points, roughly nine percent, in what became the single largest intraday point decline in history at that time. Procter and Gamble, one of the most stable blue-chip stocks in the world, briefly traded at a penny. Accenture dropped to a cent. Then, almost as quickly as it had fallen, the market bounced back, recovering most of the losses within twenty minutes. The event became known as the Flash Crash, and it brought the world of high-frequency trading into the public consciousness for the first time.

The Flash Crash was a watershed moment for the industry. The subsequent SEC investigation revealed that a mutual fund in Kansas, Waddell and Reed Financial, had triggered the cascade by placing a large sell order for E-mini S&P 500 futures using an algorithm that paid no attention to price or time, only volume. The algorithm sold 75,000 contracts worth roughly $4.1 billion in just 20 minutes, flooding the futures market with sell pressure. As the selling cascaded from futures to equities, HFT firms began withdrawing from the market, draining liquidity at precisely the moment it was needed most. The episode raised a fundamental question about modern market structure: had the shift from human market makers to algorithmic ones made markets more fragile?

The critics argued that old-fashioned NYSE specialists had affirmative obligations to maintain orderly markets, obligations that HFT firms did not share. When the going got tough, the algorithms simply turned off, leaving a vacuum. Defenders countered that even NYSE specialists had no obligation to stand in front of a freight train, and that the Flash Crash exposed flawed exchange rules, particularly the lack of circuit breakers, more than it exposed flawed market makers. The SEC subsequently implemented single-stock circuit breakers, now known as the Limit Up-Limit Down mechanism, which pauses trading in any stock that moves beyond a specified band. This was perhaps the most consequential regulatory response to the Flash Crash, and it directly benefited firms like Virtu by reducing the probability of the kind of cascading price dislocations that make market making genuinely dangerous.

For Virtu, the Flash Crash was a test that it passed. While some HFT firms pulled back their quotes, Virtu's risk management systems kept it in the market, continuing to provide liquidity and capturing the widened spreads that extreme volatility produces. The firm emerged from the event with its reputation among institutional counterparties enhanced: here was a market maker that did not run at the first sign of trouble. This resilience was not accidental; it reflected the foundational design of Virtu's system, which was built to widen spreads and reduce position sizes in volatile markets rather than to withdraw entirely. The difference between Virtu's approach and the approach of firms that withdrew was, at its core, a difference in risk management philosophy.

Two years later, the industry received a far more dramatic cautionary tale. On August 1, 2012, Knight Capital Group, one of the largest market makers in U.S. equities, deployed a software update to its servers. A technician failed to copy the new code for the Retail Liquidity Program to one of eight servers, which triggered dormant legacy code called "Power Peg," a program that had been decommissioned but never removed from the system. In forty-five minutes, the defective code executed four million trades across 154 stocks, accumulating a position of over 397 million shares. By the time Knight could shut the system down, it had lost $440 million, roughly three times its annual earnings.

Knight's stock lost 75 percent of its value in two days. The firm raised a $400 million emergency lifeline from a consortium led by Jefferies, but the rescue came at a devastating cost: the new investors received preferred equity that massively diluted existing shareholders. The damage was fatal to Knight's independence. The firm was ultimately merged with GETCO, a Chicago-based electronic trading firm, to form KCG Holdings, a company that would itself eventually be acquired by Virtu.

The Knight Capital disaster became the defining cautionary tale of the HFT industry, and its lessons deserve examination. The root cause was not exotic or sophisticated; it was a deployment failure, the kind of mundane operational error that happens at technology companies every day. What made it catastrophic was the speed at which electronic trading operates. In a human-driven business, an error might be caught in hours or days. In an HFT firm, an error executing at machine speed can cause hundreds of millions of dollars in losses in minutes. The lesson for the industry was clear: operational risk management, the boring work of code review, deployment procedures, kill switches, and disaster recovery, was as important as the flashy work of algorithm design. For Virtu, Knight's failure reinforced its own emphasis on rigorous risk management and became a permanent reminder of what happens when that emphasis lapses.

Then came Michael Lewis. In March 2014, the bestselling author of "The Big Short" and "Liar's Poker" published "Flash Boys," a narrative built around Brad Katsuyama, a former Royal Bank of Canada trader who had discovered that his orders were being systematically front-run by HFT firms. Lewis's central argument was explosive: the U.S. stock market was "rigged" in favor of high-frequency traders who used their speed advantage to exploit ordinary investors. Katsuyama's solution was IEX, a new exchange with a signature innovation, a 38-mile coil of fiber-optic cable that created a 350-microsecond "speed bump" designed to neutralize HFT latency advantages.

"Flash Boys" landed like a bomb in the HFT industry. The "front-running" accusation, while technically inaccurate from a legal perspective since what HFT firms were doing was not illegal front-running as defined by securities law, resonated powerfully with a public still angry about the financial crisis. The narrative was compelling: Wall Street insiders with faster computers were stealing from ordinary people. It did not matter that the reality was far more nuanced, that market makers like Virtu were actually providing tighter spreads and better execution for retail investors than the old specialist system ever had. The story was too good, too clean, too satisfying in its villainy.

For the firms that had planned to stay in the shadows, "Flash Boys" was merely annoying. For Virtu, which was in the middle of preparing for an initial public offering, it was a potential catastrophe. The front-running narrative threatened to turn the IPO into a referendum on the entire HFT industry. And the timing could not have been worse.

The IEX story is worth dwelling on for a moment because it illustrates the deeper tension in market structure. Katsuyama's exchange, which began trading in October 2013 and received SEC approval as an official exchange in June 2016, was designed to create a level playing field by introducing a deliberate delay. The 38-mile coil of fiber-optic cable in IEX's data center added 350 microseconds of latency to every order, enough to prevent HFT firms from exploiting their speed advantage to pick off stale quotes. It was an elegant solution to a real problem, but it also raised questions about whether speed bumps were treating the symptom rather than the disease. IEX captured roughly three percent of U.S. trading volumes, meaningful but far from dominant, suggesting that the market ultimately valued speed and tight spreads more than the philosophical appeal of a "fair" exchange. For Virtu, IEX was both a competitive nuisance and a validation of its narrative: if the market was truly rigged, why did most order flow continue to go to the venues where HFT firms operated?

The margin compression problem was also becoming visible by 2014. As dozens of firms piled into the HFT space, attracted by the extraordinary returns of the early years, competition drove spreads tighter and tighter. The easy money was disappearing. Some firms responded by taking more risk, seeking wider spreads in less liquid securities or holding positions longer. Others invested in even faster technology, hoping to maintain their edge through sheer speed. Virtu's response was different: it focused on breadth rather than depth, expanding across more asset classes, more venues, and more geographies, using its unified platform to amortize technology costs over the largest possible base of trading activity. This strategy would prove prescient, but in 2014, with the industry under siege from regulators, authors, and public opinion, the immediate challenge was simply surviving the backlash.

The IPO Decision: Going Public in a PR Nightmare

Picture this scene: a group of investment bankers sitting around a conference table, reviewing the draft S-1 filing for Virtu Financial's initial public offering. Someone flags a statistic buried in the risk factors section. Over approximately five years of trading, Virtu had experienced only one losing day out of 1,238 trading days.

One losing day. Out of 1,238.

The bankers debated whether to include the number. On one hand, it was the most compelling proof of concept imaginable. On the other, it was almost too good to be true, the kind of number that invites scrutiny rather than confidence. They included it. The decision would define Virtu's public narrative for years to come.

The reaction was bifurcated along predictable lines. For Virtu's defenders, the statistic demonstrated extraordinary risk management. Here was a firm so disciplined, so precisely calibrated in its approach to market making, that it could generate positive returns in virtually every market environment. For Virtu's critics, the number was proof that something was deeply wrong with the market. How could any company make money every single day unless the game was rigged? The fact that this number appeared in Virtu's IPO filing just weeks before "Flash Boys" hit bookstores created a perfect storm of controversy.

To understand why Virtu decided to go public when every other major HFT firm stayed private, you have to understand the strategic calculus. Going public provided access to public capital markets for future acquisitions. It provided a stronger balance sheet for the collateral requirements of market making. And perhaps most importantly, it provided legitimacy. In an industry defined by secrecy, being a public company with quarterly earnings calls, SEC filings, and independent auditors was a form of counter-narrative: "We have nothing to hide."

But the timing was brutal. "Flash Boys" dominated financial media for weeks. Congressional hearings were held. The FBI and SEC launched investigations into HFT practices. Cable news anchors who had never heard of co-location or latency arbitrage were suddenly experts on market structure.

In April 2014, Virtu made the painful but pragmatic decision to delay its IPO indefinitely. Going public in this environment would have meant pricing the stock at a steep discount, essentially paying a penalty for the industry's reputational crisis. It was the right call, but it required patience and conviction that the facts would eventually overcome the narrative.

The delay lasted nearly a year, a period during which Virtu continued to operate profitably while watching the public narrative around HFT slowly evolve. By early 2015, the "Flash Boys" furor had subsided somewhat. The FBI investigation, launched with great fanfare, had not produced any indictments of major HFT firms. The SEC's investigation was similarly inconclusive. And critically, the data was starting to support what Virtu had always argued: electronic market making had made markets cheaper, faster, and more efficient for ordinary investors. Academic studies showed that bid-ask spreads had narrowed dramatically since the advent of HFT, transaction costs for retail investors had fallen to historical lows, and execution quality for retail orders had improved measurably. The "rigged" narrative was being challenged by evidence, even if it remained alive in the popular imagination.

Virtu used the delay period wisely. Rather than sitting idle, the company continued to refine its technology, expand into new asset classes and geographies, and build the track record that would eventually convince institutional investors to buy in.

In February 2015, Virtu revived its IPO plans. The roadshow was unlike any other in recent memory. Doug Cifu and his team had to do something that most IPO roadshows do not require: explain their entire industry from scratch to institutional investors who had been told by a bestselling book that the industry was a fraud. Cifu, the former corporate lawyer, proved uniquely suited to this challenge. His presentations were detailed, data-driven, and patient, walking investors through the mechanics of market making, the economics of bid-ask spreads, and the risk management systems that produced that famous 1,238-day track record.

On April 16, 2015, Virtu Financial went public on the NASDAQ, priced at $19 per share, the upper end of the expected range, raising over $314 million at a valuation of approximately $2.6 billion. It was the first high-frequency trading firm to complete an IPO, a distinction that carried both pride and burden. The stock performance in its early days as a public company was solid, validating the thesis that investors would look past the "Flash Boys" stigma to focus on the fundamentals of an extraordinarily profitable business.

What the IPO revealed was illuminating. Virtu's financials showed a company with remarkably low headcount for its revenue, enormous operating leverage, and a business model that was far more dependent on technology infrastructure than on individual trading talent. It also showed the volatility sensitivity that would define investor perception for years to come: in high-volatility environments, Virtu's revenue surged, and in low-volatility periods, it compressed. The company was, in a very real sense, a bet on market turbulence. The question for investors was whether turbulence was the exception or the rule. History, it would turn out, favored the latter interpretation.

The IPO also established what would become the central tension for Virtu as a public company: the transparency paradox. By going public, Virtu gave itself access to capital markets and legitimacy, but it also gave its competitors, all of whom remained private, a window into its economics. Every quarter, Citadel Securities, Jane Street, Jump Trading, and every other major HFT firm could read Virtu's earnings report and see exactly how much revenue it was generating, which segments were growing, and where margins were expanding or contracting. Meanwhile, Virtu could not see any of their financials. This information asymmetry was a real competitive disadvantage, one that Cifu acknowledged but argued was worth the tradeoff. The capital and credibility benefits of being public, he believed, outweighed the cost of transparency.

The KCG Acquisition: Consolidation and Scale

The year 2016 marked a turning point. The economics of high-frequency trading had shifted in a way that made consolidation inevitable. The proliferation of HFT firms had tightened bid-ask spreads to the point where margins on individual trades were razor-thin. The fixed costs of technology infrastructure, co-location, data feeds, compliance, remained enormous and were growing. The math was simple: in a business with high fixed costs and compressing per-unit margins, scale was not just an advantage, it was survival.

KCG Holdings, the company born from the merger of Knight Capital and GETCO after the 2012 trading disaster, was an obvious acquisition target. KCG had inherited Knight's extensive wholesale market-making business and institutional client relationships, but it also carried the baggage of Knight's culture, technology debt from integrating two very different systems, and the lingering reputational stain of the $440 million glitch. KCG was profitable but struggling to grow, trapped in a cycle of declining margins and underinvestment in technology.

What Virtu saw in KCG was not just a struggling competitor but a treasure chest of client relationships wrapped in a dysfunctional technology package. KCG's wholesale market-making business served as the execution partner for a huge swath of America's retail brokerage industry, meaning that when a Schwab or Fidelity customer placed a stock order, there was a good chance KCG was on the other side of that trade. This was the gateway to payment for order flow, the practice by which market makers pay brokers for the right to execute their customers' orders, a revenue stream that would become enormously important to Virtu's economics in the years ahead.

These broker relationships were sticky and valuable, built on years of performance data, compliance infrastructure, and technology integration. Replacing a wholesale market maker is not like switching a supplier; it requires months of testing, regulatory review, and systems work. If Virtu could acquire these relationships and migrate them onto its superior technology platform, it would achieve a step-function increase in scale.

On April 20, 2017, Virtu announced the acquisition of KCG for $20 per share, approximately $1.4 billion in cash. The deal was ambitious for a company of Virtu's size, requiring significant leverage and flawless integration. Doug Cifu's vision was clear: become the number-one wholesale market maker in U.S. equities, capable of competing with Citadel Securities on equal terms.

The integration was a high-wire act unlike almost any other in corporate M&A. In most technology integrations, things can go wrong and you fix them over weeks or months. In a market-making technology integration, things can go wrong at the speed of light. The ghost of Knight Capital haunted the entire process: a single botched software deployment had cost that firm $440 million in 45 minutes. Virtu had to migrate KCG's trading systems onto its own unified platform while maintaining uninterrupted service to hundreds of broker clients, any one of whom could route their order flow elsewhere if service quality dipped even briefly. The company projected approximately $208 million in net pre-tax expense savings plus $440 million in capital synergies within two years.

Remarkably, Virtu executed this integration without a major incident, an operational achievement that received little attention precisely because nothing went wrong. In the world of HFT infrastructure, the absence of disaster is the highest form of competence.

The financial impact was dramatic. Revenue jumped from $702 million in 2016 to over a billion in 2017, and then to $1.88 billion in 2018 as the full benefits of the acquisition were realized. Virtu added a new operating segment, Execution Services, alongside its existing Market Making business, creating a more diversified revenue base. On peak days, the combined entity handled roughly a quarter of U.S. equity trading volume. The synergies materialized largely as projected, achieved by eliminating redundant technology, consolidating office space, and optimizing the combined capital base.

Virtu followed the KCG deal with another major acquisition in 2019, purchasing Investment Technology Group for approximately one billion dollars. ITG brought agency execution capabilities, pre-trade and post-trade analytics, workflow technology, and MATCHNow, Canada's largest dark pool. This was a strategically different kind of acquisition. While KCG was about scale in market making, ITG was about building an execution services platform that could serve institutional clients who wanted agency, not principal, execution. The two acquisitions together transformed Virtu from a pure HFT market maker into a diversified financial technology company.

Competitively, the KCG acquisition positioned Virtu as the clear number-two wholesale market maker behind Citadel Securities, the eight-hundred-pound gorilla of the industry. Ken Griffin's firm had more capital, more scale, and arguably better technology in certain areas. But Virtu had something Citadel did not: public transparency. And it had something else that would prove equally important: a client base of smaller regional broker-dealers and asset managers who preferred Virtu's approach of providing aggregation tools and analytics alongside execution. As Cifu would later characterize it, Virtu offered "more of an agency aggregation tool for smaller regional broker dealers and asset managers," differentiating itself from Citadel's dominant but more vertically integrated approach.

The back-to-back acquisitions of KCG and ITG represented a strategic vision that went beyond simple scale. Cifu was building something that no other HFT firm had attempted: a full-service financial technology platform that combined principal market making with agency execution, analytics, and workflow tools. The logic was compelling. Market making is a volatile, cyclical business tied to volatility and volumes. Execution services and analytics are steadier, fee-based businesses that provide revenue even when markets are quiet. By combining both under one roof, Virtu could smooth its earnings profile, cross-sell services to a broader client base, and position itself as more than just a high-frequency trading shop. Whether the market would ever value Virtu as a financial technology company rather than a trading firm remained an open question, but the strategic architecture was being laid.

The Meme Stock Explosion and Retail Trading Boom

If there is one chapter of the Virtu story that reads like a thriller, it is the period from March 2020 through early 2021.

The first week of March 2020 began with a sense of unease and ended with something closer to panic. COVID-19, still being called the "novel coronavirus" by most outlets, was spreading beyond China. Italy locked down. The oil price war between Saudi Arabia and Russia erupted. And the stock market, which had been drifting higher for a decade on the wings of cheap money and corporate buybacks, began to fall. Then it did not stop falling. The VIX, Wall Street's fear gauge, spiked above 80, a level not seen since the depths of the 2008 financial crisis. Trading volumes exploded.

For Virtu Financial, this was the environment the machine was built for. Market making is most profitable when volatility is high and trading volumes are elevated. Both conditions were met to an extreme degree. Wider bid-ask spreads meant more profit per trade. Higher volumes meant more trades. And Virtu's risk management systems, battle-tested through the Flash Crash and every other market dislocation of the previous decade, kept the firm profitable throughout. It is worth pausing on why volatility is so good for market makers. In calm markets, the bid-ask spread on a liquid stock might be a single penny, a razor-thin margin. But when the VIX spikes above 80, as it did in March 2020, spreads can widen to five or ten cents on the same stocks, because the uncertainty about the "true" price is so much greater. Market makers are compensated for taking the risk of quoting prices when no one is sure what anything is worth. The greater the uncertainty, the greater the compensation.

The numbers were staggering. Virtu's revenue more than doubled in 2020, reaching $3.24 billion, up 113 percent from $1.52 billion in 2019. Net income hit $649 million, and diluted earnings per share reached $5.16. These were the kind of numbers that even the most optimistic bull case had not contemplated. To put it in perspective, 2019 had actually been a difficult year for Virtu, with the company posting a net loss of $59 million as low volatility compressed spreads and trading income. The swing from negative $59 million to positive $649 million in a single year illustrated both the extraordinary operating leverage of the business and the fundamental challenge of valuing a company whose fortunes are so tightly tethered to market conditions.

The pandemic also accelerated a trend that had been building for years: the democratization of retail trading. Millions of Americans, stuck at home with stimulus checks and no sports to bet on, discovered the stock market through apps like Robinhood, Webull, and others. Daily average retail trading volumes roughly doubled from pre-pandemic levels. For Virtu, which had invested heavily in wholesale market-making infrastructure through the KCG acquisition, this surge in retail order flow was like turning on a firehose of profitable trades.

But COVID was just the opening act. The real show began in January 2021, when a group of retail traders on the Reddit forum WallStreetBets decided to take on the hedge funds that had shorted GameStop, a struggling video game retailer. What followed was the most chaotic week in trading history. GameStop's stock went from roughly $20 to nearly $500 in a matter of days. AMC Entertainment, BlackBerry, Nokia, and other heavily shorted stocks followed. Robinhood, the commission-free brokerage that had become the weapon of choice for a new generation of retail traders, was at the center of the storm.

Where was Virtu in all of this chaos? On the other side of many of these trades, and not in the way the conspiracy theories suggested. As a wholesale market maker, Virtu executed orders for retail brokerages including Robinhood, Schwab, Fidelity, E-Trade, and more than 200 others. When a Robinhood user bought GameStop, there was a meaningful probability that Virtu was the entity providing the other side of that trade. This was not because Virtu was betting against the retail trader. It was because Virtu's job as a market maker was to provide liquidity, to always be willing to buy or sell at a quoted price. During the meme stock frenzy, Virtu handled approximately 25 percent of total U.S. retail investor order flow.

Payment for order flow became Virtu's golden goose during this period. PFOF is the practice by which market makers like Virtu pay brokerages like Robinhood for the right to execute their customers' orders. The economics work because retail order flow is disproportionately uninformed, meaning retail traders are statistically less likely to be trading on inside information or superior analysis than institutional investors. This makes retail flow more profitable for market makers, who can offer price improvement over the exchange-posted price while still earning a spread. In the first quarter of 2021, Virtu's PFOF payments topped $250 million, up 49 percent year-over-year, reflecting the explosion in retail trading activity.

First quarter 2021 revenue hit a record $1.1 billion. For the full year, revenue was $2.81 billion with net income of $477 million and diluted earnings per share of $3.91.

The company was printing money in the most literal sense that a legal enterprise can.

The profits were real and substantial. But the meme stock era also brought intense regulatory scrutiny that threatened the very business model that produced them. Congressional hearings featured the CEOs of Robinhood, Citadel Securities, and other market participants testifying about payment for order flow. The core question was whether PFOF created a conflict of interest: were market makers providing genuinely better execution for retail investors, or were they paying for the privilege of extracting value from less sophisticated traders? Doug Cifu took to the airwaves to defend the practice, arguing forcefully that PFOF enabled zero-commission trading and delivered measurable price improvement. The data supported his case: retail investors consistently received execution prices better than the best publicly quoted prices. But "data" rarely wins against a compelling narrative, and the narrative, that Wall Street was once again profiting at the expense of the little guy, was powerful.

The irony was rich. The same retail traders who were using Robinhood's commission-free platform to buy GameStop owed the existence of that commission-free model, at least in part, to payment for order flow. The system they were raging against was the system that had made their trading possible. This nuance was largely lost in the public discourse.

There is a myth versus reality dimension here that deserves unpacking. The popular narrative painted market makers as villains profiting from the meme stock chaos. The reality was more complex. Virtu and Citadel Securities were the firms providing liquidity during the most volatile moments, standing ready to buy when panic selling hit and to sell when retail mania was pushing prices to absurd levels. Without market makers, the bid-ask spreads on GameStop during peak frenzy would have been far wider, meaning retail traders would have gotten far worse prices. The market makers were not causing the volatility; they were absorbing it. Whether they were adequately compensated for that service, or excessively compensated, is a legitimate debate. But the simplistic narrative of market makers as predators missed the fundamental service they provided.

The meme stock era also revealed something about Virtu's business model that many investors had not fully appreciated: the sheer concentration of retail order flow. Virtu handled approximately 25 percent of all U.S. retail equity orders through relationships with more than 200 brokerages. This concentration, built largely through the KCG acquisition and expanded through organic growth, meant that Virtu's fortunes were tightly linked to the behavior of retail investors. When retail traders were engaged and active, as they were during COVID lockdowns and meme stock mania, Virtu's revenue surged. When retail enthusiasm waned, revenue declined. This created a business model that was, in essence, a leveraged bet on retail trading activity layered on top of a leveraged bet on market volatility.

The Hangover: Post-Meme Stock Reality and Strategic Pivot

Every cyclical business faces a moment of reckoning: "What do you do when the music stops?" For Virtu, the music did not stop so much as gradually fade. After the champagne years of 2020 and 2021, the hangover arrived on schedule. Retail trading activity normalized. Volatility, as measured by the VIX, declined from the extraordinary levels of the pandemic era. And the revenue trajectory that had seemed limitless began to bend downward.

Revenue declined to $2.36 billion in 2022, with net income falling to $265 million and earnings per share coming in at $2.44, less than half the 2020 peak. Still a strong number by any historical standard, but a meaningful step down from the champagne years. In 2023, the compression continued: revenue dipped to $2.29 billion, and net income dropped 44 percent to $142 million, with earnings per share at just $1.42. Trading income declined more than 20 percent as volumes eased across essentially every asset class. This was the trough, the point at which investors had to decide whether Virtu's peak-era performance was the norm or the aberration.

While Virtu managed the revenue decline, a larger threat was gathering on the regulatory front. In December 2022, the SEC under Chair Gary Gensler proposed four sweeping market structure reforms, including the Order Competition Rule, which would have required certain retail orders to face order-by-order competition in auctions rather than being routed directly to wholesale market makers. The SEC acknowledged explicitly that this proposal would "likely lead to a reduction of PFOF." For Virtu, which derived a significant portion of its Market Making segment revenue from wholesale execution of retail order flow, this was an existential threat, or at least it appeared to be one.

Virtu's strategic response was multifaceted. The first and most obvious move was diversification beyond equities. The company expanded its crypto market-making capabilities through partnerships, including a notable arrangement with Talos to stream spot digital asset liquidity to institutional clients. It appointed a Head of Business Development for Digital Assets, signaling that crypto was not a side project but a strategic priority.

Fixed income was another frontier, and potentially the most significant one. The bond market is enormous, roughly $50 trillion in the United States alone, but it remains surprisingly antiquated in how it trades. While equities have been fully electronic for years, a large portion of bond trading still happens over the phone or through manual request-for-quote processes. Virtu launched an agency fixed income RFQ platform with a dealer network of nearly 20 brokers, betting that the electronification of bond trading, which was still far behind equities in terms of automation, represented a growth opportunity analogous to what equities had offered a decade earlier. If bonds follow the same trajectory that equities did after Reg NMS, the firms that build the best electronic market-making infrastructure will capture enormous value. Options market making expanded globally. International operations, already spanning 50 countries, received additional investment.

Perhaps the most intriguing strategic initiative was technology licensing, which emerged as a potential new revenue stream. The question was whether Virtu could sell its infrastructure, the same technology platform that powered its own trading, as a service to other financial institutions. This would represent a fundamental shift from being a technology-enabled trading firm to being a financial technology company, a transition that could unlock higher valuation multiples and more predictable revenue.

Through all of this, there was one metric that the market watched obsessively: could Virtu maintain its "profitable every day" track record? The answer, inevitably, was more nuanced than the headline stat suggested. In periods of very low volatility, daily profitability in the market-making business was harder to sustain, and the diversification into execution services and analytics meant that the firm's P&L was no longer driven solely by the market-making machine. The identity that had defined Virtu since its IPO filing was evolving.

By 2024, the recovery had begun. Revenue rose 25.4 percent to $2.88 billion, net income recovered to $276 million, and normalized adjusted earnings per share came in at $3.55. The strategic bets were starting to pay off, and the regulatory landscape had shifted meaningfully. The SEC's most aggressive market structure proposals, including the Order Competition Rule and Regulation Best Execution, had not been adopted. The regulatory sword of Damocles had not fallen, at least not yet. Meanwhile, the SEC did move forward on more incremental changes, unanimously adopting amendments in September 2024 that moved approximately 74 percent of stocks to half-penny tick increments and reduced access fee caps from 30 mils to 10 mils, with a compliance deadline pushed to November 2026.

The post-meme stock period also forced a reckoning with a question that every cyclical business must answer: what is the normalized earning power of this company? The peaks of 2020 and 2021 were clearly unsustainable, driven by once-in-a-generation volatility and retail trading enthusiasm. The trough of 2023, with earnings per share of just $1.42, felt overly pessimistic given the company's scale advantages and diversification progress. The truth, as with most cyclical businesses, lay somewhere in between. For investors, the challenge was determining the appropriate multiple for a company whose earnings could swing from $1.42 to $5.16 in the space of two years, depending largely on market conditions that no one can predict. This volatility of earnings, paradoxically driven by the same market volatility that fuels the business, has kept Virtu's valuation compressed relative to what a technology company with similar margins and growth rates would command.

The Business Model Deep Dive: How Virtu Actually Makes Money

To understand Virtu's business, one must first understand what a market maker actually does, and why the service is far more valuable than most people realize.

Imagine a farmers' market with only one stall selling apples. When a buyer arrives, the stall owner gets to set the price. When a seller arrives with a bushel of apples, the stall owner also sets the price, and the difference between what the stall owner pays for apples and what they sell them for is the spread. This is, at the most basic level, what a market maker does. Virtu continuously quotes prices at which it will buy a security, the bid, and prices at which it will sell it, the ask, across 25,000 securities on 235 venues. The difference between the bid and ask, the spread, is where the profit comes from.

The complication is that the apple analogy breaks down in important ways. In financial markets, prices change constantly, new information arrives every microsecond, and inventory can become toxic if the market moves against you before you can sell what you have bought.

This is why technology matters so much. Virtu's algorithms must continuously reprice thousands of securities in response to a firehose of market data, manage inventory to minimize directional risk, and route orders to the venues that offer the best execution, all in microseconds. The margin of error is essentially zero: a system that is even slightly slow in updating its prices will be systematically picked off by faster competitors, a phenomenon known in the industry as "adverse selection."

The company operates through two primary segments.

The Market Making segment is the core business, the machine that quotes prices and captures spreads. This segment is highly sensitive to volatility and trading volumes. When markets are turbulent, spreads widen and volumes increase, which is why Virtu's revenue spikes during crises. When markets are calm, spreads compress and volumes decline. In the first quarter of 2025, this segment generated $691 million in revenue.

The Execution Services segment, built through the KCG and ITG acquisitions, serves institutional clients who need to execute large orders without moving the market. This is an agency business, meaning Virtu acts as an intermediary rather than a principal, earning commissions and fees rather than trading profits. It also includes analytics products that help clients measure and improve their execution quality, and workflow technology that integrates with clients' existing systems. This segment contributed $141 million in revenue in the first quarter of 2025, a smaller but steadier stream that provides ballast when market-making revenue fluctuates.

Payment for order flow, or PFOF, sits at the intersection of these two businesses and is worth understanding in detail because it is the single most controversial aspect of Virtu's business model. When Robinhood or Schwab routes a retail customer's order to Virtu for execution, Virtu pays the broker a small fee per share for the privilege. Virtu then executes the order at a price that provides "price improvement" over the national best bid or offer, meaning the retail customer gets a slightly better price than they would have gotten on a public exchange. Virtu profits from the difference between the price improvement it provides and the spread it captures. The economics work because retail order flow is less informed and less toxic than institutional flow, making it more predictable and more profitable to trade against.

Understanding the operating leverage in this business is critical for investors, and it is extraordinary. Virtu's technology platform, the servers, the algorithms, the co-location infrastructure, costs roughly the same whether it processes one million trades or ten million trades in a day. This means that when trading volumes surge, as they did during COVID and the meme stock era, revenue scales up dramatically while costs barely move. This is why Virtu's margins are so sensitive to market conditions and why the company can swing from strong profitability in volatile markets to more modest returns in calm ones.

Perhaps the most counterintuitive aspect of Virtu's business model is how few people it takes to run it. The company had 969 employees at last count. Compare that to a traditional investment bank with tens of thousands of employees, or even a mid-size asset manager with hundreds. The ratio of revenue per employee is astronomical, reflecting the fact that the core business is run by machines, not people. The people design the machines, maintain the machines, and manage the regulatory and client relationships around the machines, but the actual trading is almost entirely automated.

To put the economics in context, compare Virtu to a traditional stock exchange like the New York Stock Exchange. Both are essential infrastructure providers in the capital markets ecosystem. Both earn revenue from the flow of orders through their systems. But while the NYSE earns fixed fees per transaction regardless of market conditions, Virtu's revenue is tied to the spread it captures, which widens in volatile markets and compresses in calm ones. This is why Virtu's revenue can more than double in a year like 2020 and then fall back by a third when markets calm down. The operating leverage works in both directions.

The comparison to traditional market makers is equally instructive. Under the old NYSE specialist system, human market makers stood at designated posts on the trading floor, maintaining order books and providing liquidity for assigned stocks. They had formal obligations to maintain fair and orderly markets but also enjoyed privileged access to order flow information. The specialists made money, but they were constrained by the speed of human cognition and the costs of maintaining a physical presence on the trading floor. Virtu replaced this model entirely: faster, cheaper, and operating across thousands of securities simultaneously rather than a handful. The human specialist has been replaced by an algorithm, and the cost of providing liquidity has plummeted as a result. Average bid-ask spreads in U.S. equities have fallen by more than half since the rise of electronic market making, saving investors billions of dollars annually. This is the fact that Virtu's defenders always cite, and it is a genuine and significant benefit.

Regulatory Environment and Industry Evolution

The regulatory landscape that shapes Virtu's business is a layered system built over decades, and understanding it is essential to understanding both the opportunity and the risk.

Think of the regulatory environment as the playing field on which Virtu operates. Change the field, and you change the game entirely. This is not a metaphor; it is the literal reality of market structure. Every major regulatory change in the past two decades has created winners and losers among trading firms, and Virtu's ability to navigate these shifts has been central to its survival.

The foundation is Regulation NMS, the 2005 SEC rule fully implemented in 2007 that shattered the old model of centralized exchange trading. The Order Protection Rule, the heart of Reg NMS, requires that orders be executed at the best available price across all exchanges. This simple mandate created the fragmented market structure that makes electronic market making viable. Before Reg NMS, the New York Stock Exchange's specialists handled the bulk of trading in listed stocks. After Reg NMS, orders could be routed to any of dozens of venues, from traditional exchanges to electronic communication networks to dark pools. This fragmentation was the oxygen that HFT firms breathed.

In Europe, the equivalent regulatory framework is MiFID II, which took effect in January 2018. MiFID II brought its own set of opportunities and constraints for firms like Virtu, including requirements around pre-trade transparency, position limits, and systematic internaliser rules. Virtu operates in Europe through Virtu Europe Trading Limited, registered in Ireland and regulated by the Central Bank of Ireland, with a MiFID branch in Paris. The European regulatory environment is different enough from the U.S. to create both complexity and opportunity, as firms with the expertise to navigate both regimes enjoy a competitive advantage over those that operate in only one.

For Virtu specifically, the most significant recent regulatory development was the SEC's December 2022 package of market structure proposals. The Order Competition Rule, the most aggressive of the four proposals, would have required retail orders above a certain threshold to be exposed to competition in periodic auctions before a wholesaler could execute them. This was a direct attack on the PFOF model that generated significant revenue for Virtu. The proposal generated fierce debate. Proponents argued it would improve execution quality for retail investors. Opponents, including Virtu, argued it would destroy the zero-commission trading model and actually harm the retail investors it purported to help.

So where do things stand today? As of early 2026, the Order Competition Rule and the related Regulation Best Execution proposal have not been adopted. The political winds shifted, enforcement priorities evolved, and the proposals appear to have stalled. The tick size and access fee reforms were adopted, but these are more incremental changes that Virtu can adapt to. The regulatory sword of Damocles still hangs, however: a future SEC chair could revive the proposals, and the debate over PFOF is far from settled.

The crypto regulatory environment represents a wild card. Virtu has expanded into digital asset market making, but the rules governing crypto trading are fragmented across jurisdictions and evolving rapidly. The lack of a clear regulatory framework creates both opportunity, as less regulated markets often have wider spreads and more profitable market-making opportunities, and risk, as regulatory crackdowns can disrupt business models overnight.

How does Virtu navigate this complex and constantly shifting regulatory landscape? Through a combination of lobbying, compliance investment, and diversification. Being a public company gives Virtu a seat at the table in regulatory discussions that private firms often lack. Its quarterly earnings calls and SEC filings provide a platform for advocating its positions on market structure. And its diversification across asset classes, geographies, and business lines provides some insulation against any single regulatory change.

The transparency paradox is real: being public in a secretive industry means that competitors can study Virtu's financials, while Virtu cannot see theirs. Citadel Securities, Jane Street, Jump Trading, all are private and disclose only what they choose to. Virtu's quarterly earnings are public record, meaning competitors know exactly how profitable each business line is, which products are growing, and where the vulnerabilities might lie. This asymmetry is the price of the legitimacy and capital access that public markets provide.

One regulatory development worth watching is the maker-taker fee structure that governs exchange economics. Under the current system, exchanges pay rebates to firms that "make" liquidity by posting limit orders and charge fees to firms that "take" liquidity by executing against posted orders. This system incentivizes market makers to post aggressive quotes but also creates complex incentive structures that critics argue distort order routing decisions. Any changes to the maker-taker model could have significant implications for Virtu's economics, as the rebates earned from exchanges represent a meaningful component of the firm's market-making revenue.

The crypto regulatory landscape adds another layer of complexity. Unlike equities, which are governed by a well-established SEC framework, digital assets exist in a regulatory gray zone where the SEC, CFTC, and state regulators all claim jurisdiction over different aspects of the market. Virtu has expanded into crypto market making cautiously, leveraging its existing technology platform and risk management expertise, but the lack of regulatory clarity means that the rules could change dramatically and quickly. This is both an opportunity, because less regulated markets tend to have wider spreads, and a risk, because regulatory crackdowns can shut down profitable activities overnight.

Porter's Five Forces and Hamilton's Seven Powers Analysis

Understanding Virtu's competitive position requires moving beyond the company's own narrative and examining the structural forces that shape the industry. It is not enough to know that Virtu is profitable; investors need to understand whether that profitability is durable, defensible, and growing. Two frameworks are particularly useful here: Michael Porter's Five Forces, which maps the external competitive environment, and Hamilton Helmer's Seven Powers, which identifies the internal sources of competitive advantage that create pricing power and sustainable returns.

Starting with the threat of new entrants, a force that many investors underestimate in this industry. The barriers to entering electronic market making are genuinely high. A new entrant needs to invest hundreds of millions of dollars in technology infrastructure, obtain regulatory approvals across multiple jurisdictions, establish co-location arrangements with dozens of exchanges, build relationships with brokers and institutional clients, and recruit scarce quantitative and engineering talent. The capital requirements alone are daunting, but the knowledge requirements are equally formidable. Building a market-making algorithm that works consistently without blowing up is extraordinarily difficult, as Knight Capital's experience demonstrated. That said, the barriers are not insurmountable, and well-funded firms with deep technical talent continue to enter the space.

The bargaining power of suppliers is moderate. Exchanges set the fees for trading, market data, and co-location, and these fees represent significant costs for market makers. However, the proliferation of competing venues, a direct consequence of Reg NMS, gives market makers some leverage. If one exchange raises fees too aggressively, order flow can be routed elsewhere. Data feed costs are less negotiable, as certain exchange data is effectively mandatory for competitive market making.

Buyer power is relatively low. Retail investors access Virtu's services indirectly through their brokers and have no say in which market maker executes their orders. Institutional clients have more choice, but they need liquidity regardless of who provides it, and switching costs, while not prohibitive, involve integration, testing, and relationship management that create friction.

The threat of substitutes is moderate and evolving. Exchanges themselves have developed their own market-making programs. Dark pools offer alternative execution venues. And some brokers are exploring internalization, executing customer orders against their own inventory rather than sending them to external market makers. None of these substitutes have fundamentally displaced wholesale market making, but they exert pricing pressure.

Competitive rivalry is very high, and this is arguably the single most important force shaping Virtu's economics. Citadel Securities is the dominant player, generating $4.9 billion in revenue in the first half of 2024 alone and continuing to grow. Jane Street has emerged as a powerhouse, handling more than 10 percent of North American equity volume and nearly a quarter of U.S. ETF primary market activity. Hudson River Trading has grown rapidly, more than doubling its net trading revenue year-over-year in recent quarters. Optiver, IMC, and Flow Traders in Amsterdam round out a competitive field where the firms are secretive, well-capitalized, and technically sophisticated.

Through the lens of Hamilton Helmer's Seven Powers framework, Virtu's competitive position comes into sharper focus.

Scale Economics: This is where Virtu's case is strongest. The enormous fixed costs of technology infrastructure, co-location, regulatory compliance, and talent are spread over massive trading volumes. Each incremental trade adds revenue with minimal incremental cost, creating a virtuous cycle where larger firms have structurally lower cost-per-trade than smaller competitors.

Network Effects: These are limited in market making, and this is an important distinction from true platform businesses. There is a weak form of network effect in that more liquidity attracts more order flow, which enables tighter spreads, which attracts more order flow. But this is more of a scale effect than a true network effect, and it does not create the kind of lock-in that network effects produce in platform businesses.

Counter-Positioning: Virtu does not possess this power. It is not upending an incumbent business model in a way that incumbents cannot replicate without damaging their existing businesses. All of Virtu's major competitors are pursuing essentially the same strategy.

Switching Costs: These are moderate. Broker relationships take time to build and involve technology integration, compliance agreements, and performance monitoring. But brokers can and do switch market makers, and the PFOF model actually encourages competition among wholesalers because brokers route flow to whichever market maker offers the best combination of payment and execution quality.

Branding: In a business-to-business market-making context, branding power is essentially nonexistent. Nobody chooses a market maker based on brand affinity.

Cornered Resource: Virtu has meaningful advantages here. Its proprietary technology platform, built and refined over 18 years, is not something a competitor can replicate overnight. Its co-location infrastructure, its quantitative talent, including a CEO with a background in theoretical physics, and its institutional knowledge of market microstructure across dozens of countries and asset classes represent cornered resources that are genuinely difficult to replicate.

Process Power: This is Virtu's strongest power. The years of algorithmic refinement, the risk management systems that have been stress-tested through every major market dislocation of the past two decades, the execution excellence that produces consistent daily profitability, these are the products of organizational processes that cannot be easily copied. Process power is, by its nature, the hardest form of competitive advantage to observe from the outside and the hardest to replicate, because it is embedded not in any single person or piece of technology but in the way the entire organization operates.

Taking the Seven Powers assessment together, Virtu possesses three of the seven powers, with scale economics, cornered resource, and process power forming the core of its competitive advantage. The absence of strong network effects, counter-positioning, and branding means that the moat, while real, requires constant investment to maintain. The overall moat assessment is nuanced. Technology and process power are real and substantive, but they are constantly under attack. Scale helps but does not guarantee victory, as Citadel's superior scale demonstrates. The key vulnerabilities are regulatory changes that could upend the PFOF model, technology disruption from well-funded competitors, and the inherent margin compression that comes from intense competition among sophisticated firms all pursuing the same basic strategy.

Bear versus Bull Case

The bull case for Virtu starts with its track record, and it is a genuinely impressive one. This is a company that has been profitable through the 2008 financial crisis, the Flash Crash, the post-Flash Boys PR nightmare, the low-volatility desert of 2017 to 2019, the COVID crash, the meme stock mania, and the subsequent normalization. Few financial firms of any kind can claim that kind of consistency across such varied market environments. The bears who predicted PFOF bans have been wrong so far. The bears who predicted technology disruption have been wrong so far. The bears who predicted that meme stock volumes would never return have been partially vindicated but partially wrong, as 2025 volumes have recovered strongly.

Virtu is an essential infrastructure provider in modern markets. As long as people trade stocks, options, currencies, and commodities, someone needs to provide liquidity. The question is not whether market makers will exist, but which ones will survive and thrive. Virtu's scale advantages continue to compound: its unified technology platform allows it to add new asset classes and geographies at relatively low incremental cost, and its Execution Services segment provides a recurring revenue stream that is less volatile than pure market making.

The diversification strategy is showing results. The expansion into crypto, fixed income, and options reduces the firm's historical dependence on equity market making and PFOF. International growth provides exposure to markets where electronic trading is less mature and spreads are wider, offering margin expansion opportunities. The launch of Virtu Technology Solutions in March 2025 represents a potentially transformative shift toward technology licensing revenue.

The 2025 financial performance has been strong: revenue of $3.63 billion, up 26 percent year-over-year, with net income of $912 million and diluted earnings per share of $5.13. The second quarter's Adjusted EBITDA margin of 65.1 percent was the highest on record, suggesting that the diversification and technology investments of recent years are bearing fruit. The stock yields a quarterly dividend of $0.24 per share, and management repurchased $48.1 million in shares during the first quarter alone. The return on equity of 23.7 percent in 2025 compares favorably to most financial services firms and many technology companies.

The balance sheet is solid but carries meaningful leverage: $1.13 billion in cash and equivalents against $2.07 billion in long-term debt, a legacy of the acquisition-driven growth strategy.

The debt level is manageable given the company's cash generation, but it does mean that a severe downturn in trading volumes or a regulatory shock could create financial stress. Management has been steadily deleveraging, and the debt-to-EBITDA ratio has improved significantly since the KCG and ITG acquisition era.