Venture Global: The Disruptors Who Built America's LNG Giant

I. Introduction & Episode Thesis

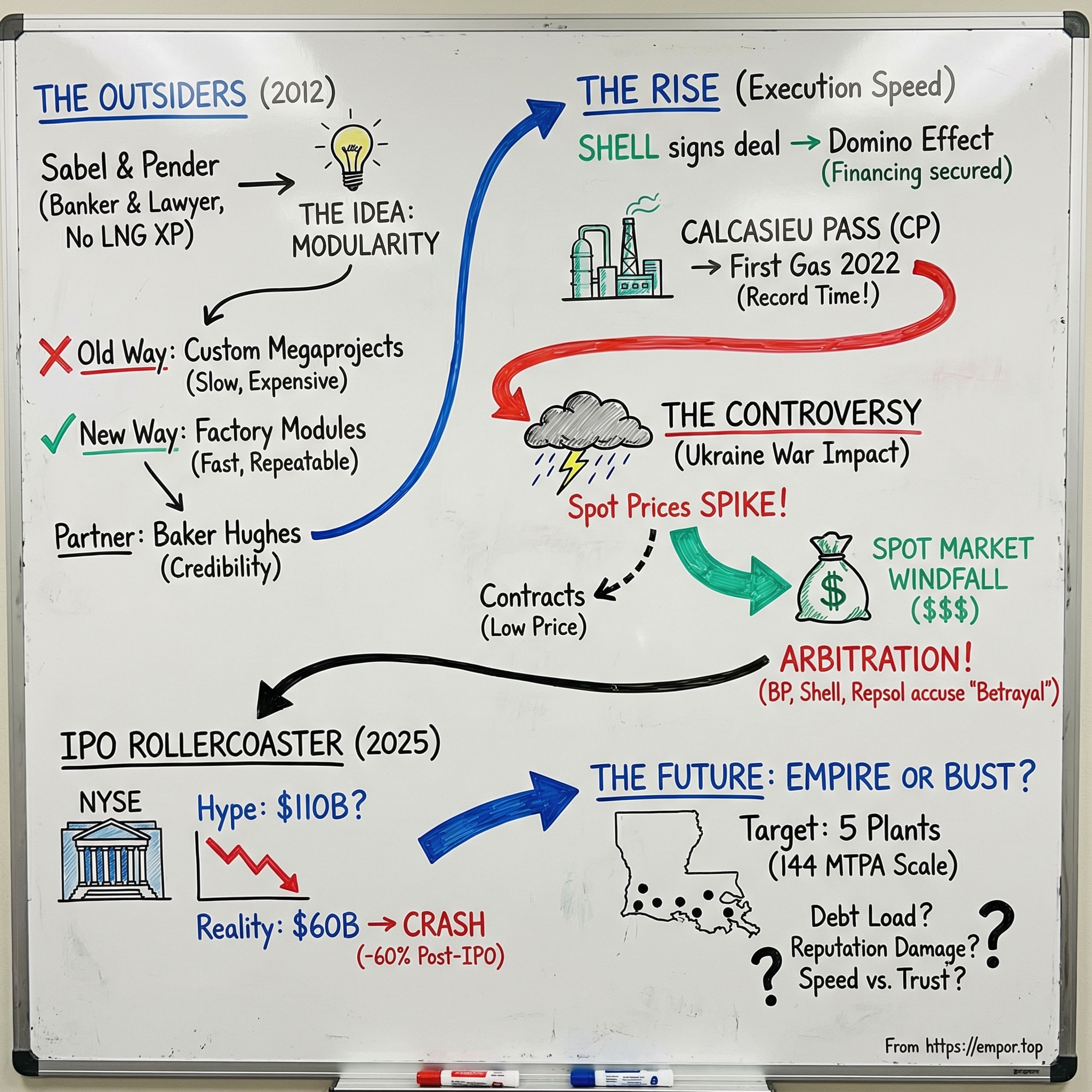

Picture this: Two middle-aged professionals—one a Washington lawyer, the other an investment banker—driving a rented Chevy across the dusty backroads of Texas in 2013. No energy experience. No LNG background. Just a PowerPoint deck and an audacious dream to revolutionize how America exports natural gas. They're pitching anyone who will listen, often getting laughed out of rooms by industry veterans who've spent decades building massive LNG terminals.

Fast forward to January 2025: those same two outsiders just took their company public at a $60 billion valuation, making it the largest oil and gas IPO in over a decade. Venture Global, the pure-play liquified natural gas company they founded, has become the second-largest LNG exporter in the United States, trailing only industry pioneer Cheniere. The founders—Mike Sabel and Bob Pender—saw their paper fortunes soar to $24 billion each at the IPO, only to watch the stock crater 60% in the following weeks, erasing $39 billion in market value.

This is a story about disruption in one of the world's most capital-intensive industries. It's about how two complete outsiders looked at the traditional LNG playbook—dominated by oil supermajors building $20 billion mega-projects over decades—and asked: What if we built these facilities like we manufacture cars? What if we could snap together LNG plants like Legos?

The central question driving this episode: How did Sabel and Pender build one of America's most valuable—and controversial—energy companies while breaking every rule in the industry playbook? And perhaps more importantly, why are some of their biggest customers now suing them for billions while the stock market questions whether their revolutionary approach actually works?

We'll journey from their failed coal plant in Sri Lanka to the Louisiana bayous where they're betting $100 billion on transforming global energy markets. Along the way, we'll unpack the modular revolution that promised to democratize LNG production, the customer battles threatening to derail their empire, and the geopolitical forces that could make Venture Global either the most prescient bet in energy or a cautionary tale about moving too fast in an industry that rewards patience.

This isn't just a business story—it's a referendum on whether outsiders can truly disrupt industries built on hundred-year relationships and engineering excellence. It's about the tension between innovation and execution, between growth and reputation, between serving shareholders and serving customers who've signed 20-year contracts worth billions.

The journey from that rented Chevy to Wall Street begins with understanding who these unlikely founders really were...

II. The Unlikely Founders: Sabel & Pender's Origin Story

The conference room at Sullivan & Cromwell's Washington office had seen its share of high-stakes negotiations, but in 2012, Bob Pender wasn't there to close another deal. The Big Law partner was having what he'd later describe as his "Jerry Maguire moment"—that crystallizing realization that he'd spent decades climbing the wrong mountain. At 58, after three decades navigating the corridors of power from his stint as a White House law clerk during the Carter administration to advising Fortune 500 companies, Pender was ready to build something rather than just advise others who did.

Meanwhile, in Virginia, Mike Sabel was experiencing his own professional restlessness. The investment banker had dropped out of the University of Michigan decades earlier, choosing the trading floor over the classroom. He'd built a respectable career in commercial finance and investment banking, but at 54, he felt the pull of entrepreneurship. Unlike the typical energy executive path through petroleum engineering at Texas A&M followed by decades at ExxonMobil, Sabel's resume read more like a Wall Street generalist—which is precisely why nobody took him seriously when he started talking about LNG.

Their partnership began, improbably, with a failed coal plant in Sri Lanka in 2009. Sabel and Pender had teamed up to develop what they thought would be a straightforward infrastructure project. But Sri Lankan politics, environmental concerns, and the global financial crisis conspired against them. Most people would have retreated to their comfortable careers. Instead, the failure sparked an unlikely epiphany.

"We were sitting in this hotel in Colombo, basically licking our wounds," Sabel would later recount to investors. "And we started talking about Haiti—how could a country like that ever get reliable energy? They couldn't build a massive import terminal. They needed something smaller, more flexible." That conversation led them to liquified natural gas, specifically the challenge of making it accessible to smaller markets that couldn't justify billion-dollar infrastructure.

The "outsider advantage" would become their calling card, though at the time it felt more like a liability. When they started making rounds to Houston energy companies in 2012, the reception was brutal. Here were two guys with zero LNG experience, no engineering backgrounds, and no relationships with the Japanese utilities and European buyers who dominated the market. Industry veterans would listen politely, then show them the door with barely concealed smirks. The data point that crystallized their outsider status: Venture Global was founded by two entrepreneurs who had no LNG experience. In an industry where CEOs typically have 30-year careers at Chevron or Shell, this was heresy. Pender was a Washington DC attorney who served as a White House law clerk during the Carter administration, while Sabel spent decades in investment banking and commercial finance after dropping out of University of Michigan.

Their 2013 fundraising tour became the stuff of legend within Venture Global. They drove door-to-door across Texas in a rented Chevy, pitching investors on a plan to build natural gas export plants faster, cheaper and better than anyone else. One potential investor in Houston reportedly asked them if they knew what LNG stood for. Another suggested they might want to start with something simpler, like a car wash.

But buried in their inexperience was a profound insight. The LNG industry had ossified around a model created in the 1960s: massive, custom-built facilities that took a decade to construct and required the balance sheets of oil supermajors. Everyone accepted this as immutable fact. Sabel and Pender, unburdened by decades of "how things are done," asked a different question: What if we're building these plants the same way we built automobiles in 1920—one at a time, by hand?

Sabel, 57, and Pender, 71, have redrawn nearly everything, from the design of their facilities to the way they handle customers. Their backgrounds—Sabel in structured finance, Pender in complex transactions—gave them a different lens. They saw LNG not as an engineering problem but as a financial and manufacturing puzzle.

The failed Sri Lankan coal plant, rather than being a setback, became their business school. They tried to build a coal power plant in Sri Lanka in 2009, but failed. They then got the LNG bug. When they considered how Haiti could import smaller amounts of gas to meet its needs, they seized upon LNG. The Haiti conversation was pivotal—it forced them to think about energy infrastructure for the developing world, not just massive projects for Japan or Europe.

By late 2012, they had incorporated Venture Global from a shared workspace in Arlington, Virginia—about as far from Houston's energy corridor as you could get while still being in America. They had no employees, no permits, no customers. Just an idea that the entire industry was doing it wrong.

Susan Sakmar, a University of Houston visiting law professor who's written a book on LNG, said "They came out of nowhere, total dark horses. It remains to be seen that they are the disruptors they claim to be until they give buyers their cargoes".

Their radical solution would come from an unlikely source: a conversation with an equipment manufacturer about building LNG plants the way you'd build cars...

III. The Modular Revolution: Reimagining LNG Infrastructure

The conference room at Baker Hughes' Houston facility in 2014 was designed to impress—polished mahogany table, oil paintings of offshore rigs, the subtle message that serious engineering happened here. Lorenzo Simonelli, CEO of the industrial giant, was skeptical when Sabel and Pender walked in with their PowerPoint. Baker Hughes had been building LNG equipment for decades. What could these outsiders possibly teach them?

Then Sabel pulled out a napkin—literally—and started sketching. "Look at how we build everything else in America," he said, drawing boxes and arrows. "Cars, planes, even houses now. We build them in factories with quality control, standardization, economies of scale. Then we assemble them on site. Why are we still building LNG plants like medieval cathedrals?"

The traditional LNG model was indeed cathedral-like: massive, bespoke facilities with production trains capable of processing 5 million tonnes per annum (MTPA) each, requiring armies of specialized welders, pipefitters, and engineers camping in man-camps for years. A typical project like Chevron's Gorgon in Australia had blown through $54 billion and taken over a decade. The complexity was staggering—imagine building a refinery, a power plant, and a cryogenic facility all at once, in remote locations, with everything custom-fabricated on site.

Sabel stated in an interview that "our Eureka moment" was to reduce the scale so it could be built in factories. The insight was deceptively simple: instead of building massive 5 MTPA trains on site, why not build smaller 0.626 MTPA modular units in factories, then ship them to location and snap them together?

Baker Hughes was working on modular trains or chillers, which turn gas into liquid. These are manufactured in factories, then snapped together as Legos, to start exports more quickly. The technology existed—Baker Hughes had been experimenting with mid-scale liquefaction for smaller markets. But nobody had tried to use it for a world-scale export facility.

The math was compelling. Traditional projects needed 3,000-5,000 workers on site for years. Modular construction could reduce that to 500-800, with most work done in controlled factory environments. Construction time could drop from 5-6 years to 3-4 years. Most importantly, you could start generating cash flow from the first modules while still building the rest.

They modified designs to run using a larger number of smaller units, or trains. They chose a modular design, allowing factories to fabricate difficult pieces and later combine them like massive Legos on site, promising a faster ramp-up and less downtime for maintenance.

But the industry's reaction was brutal. BloombergNEF deemed Venture Global's first facility "highly unlikely" in a 2015 report. The skepticism wasn't unfounded. Modular had been tried before in other industries with mixed results. The nuclear industry's modular reactor dreams had largely failed. Modular refineries had proven more expensive than traditional builds.

The technical challenges were immense. How do you transport modules the size of apartment buildings? How do you ensure quality control when pieces are built in different locations? How do you manage the interfaces between modules—the thousands of connection points where pipes, wires, and control systems must align perfectly? Baker Hughes, as a strategic LNG technology supplier to Venture Global for more than 100 million tons per annum (MTPA) of production capacity, has already provided comprehensive LNG solutions to the Calcasieu Pass and Plaquemines LNG facilities. The relationship that started with skepticism had evolved into one of the industry's most important partnerships.

The highly-efficient liquefaction train system (LTS) supplied by Baker Hughes is modularized, helping to lower construction and operational costs with a "plug and play" approach that enables faster installation. These modules will be manufactured, assembled, tested and transported from BHGE's state-of-the-art plants in Italy.

The real innovation wasn't just making things smaller—it was rethinking the entire value chain. Traditional LNG plants required specialized construction crews who traveled the world building these facilities. Venture Global's approach meant that welders in Italy could build modules during regular shifts, with their families nearby, producing consistent quality in climate-controlled facilities.

Calcasieu Pass holds the global record for the fastest construction of a large scale greenfield LNG project, moving from FID to first LNG in 29 months. This wasn't just incrementally faster—it was revolutionary. The industry standard was 48-60 months.

Lorenzo Simonelli, CEO of Baker Hughes, later reflected: He said that Sabel and Pender were "very motivated professionals" who had achieved their LNG dreams. But achieving those dreams required more than motivation—it required reimagining an entire industry's approach to construction.

The modular revolution promised to democratize LNG production. If you could build these facilities faster and cheaper, suddenly countries and companies that couldn't afford traditional mega-projects could enter the market. It was the difference between needing ExxonMobil's balance sheet and being able to finance a project with private equity and debt.

But promises are cheap in the energy industry. The real test would come when they tried to build their first facility, secure customers, and prove that modular could work at scale.

The path from PowerPoint to production would require navigating Louisiana politics, Wall Street skepticism, and the chicken-and-egg problem of needing customers to get financing while needing financing to attract customers...

IV. Building the Business: From Zero to First Gas (2013–2022)

The Calcasieu Parish Police Jury meeting in Lake Charles, Louisiana, on a humid Tuesday evening in August 2014 wasn't supposed to be dramatic. The agenda item—a tax abatement for something called "Venture Global LNG"—barely merited attention from the dozen residents in attendance. But Mike Sabel had flown down from Virginia specifically for this meeting, knowing that everything hinged on these local politicians understanding his vision.

"We're not asking you to trust us," Sabel told the jury members, his investment banker polish slightly wilted in the Louisiana heat. "We're asking you to trust Shell, BP, and the other companies who are betting billions on us delivering what we promise."

He was bluffing, of course. At that moment, Venture Global had exactly zero customers signed up.

Sabel and Bob Pender, formerly a partner at Washington, DC-based law firm Hogan Lovells, founded Venture Global in 2013. Starting with just themselves and a handful of advisors, they faced the classic energy infrastructure challenge: you need permits to get customers, customers to get financing, and financing to build anything. It was a three-dimensional chess game where every move depended on moves they hadn't made yet.

The Louisiana bet was calculated. The state offered generous tax incentives for LNG projects, had existing pipeline infrastructure from decades of petrochemical development, and—critically—had a political establishment eager for economic development post-Hurricane Katrina. While Texas had more established LNG players, Louisiana offered a hungrier, more flexible environment for newcomers.

Their first breakthrough came from an unexpected source: the Federal Energy Regulatory Commission (FERC). In 2015, while industry analysts were calling their project "highly unlikely," FERC quietly began processing Venture Global's permit applications with unusual speed. The reason? The Obama administration, despite its climate rhetoric, saw LNG exports as a geopolitical tool against Russia. A new player promising faster, cheaper facilities aligned perfectly with this agenda.

But permits don't pay bills. By late 2015, Sabel and Pender had burned through their initial seed capital and were facing the prospect of shuttering the company. They needed a customer—a real, blue-chip buyer willing to sign a 20-year contract with a company that existed mostly on paper.

Enter Shell. The oil major was in a bind. It needed additional LNG supply for its global trading operation but didn't want to wait 5-6 years for a traditional project. In early 2016, Shell's trading team in London took a massive gamble: Shell signed a 20-year purchase agreement that then helped attract other buyers.

Venture Global received authorization to export LNG from the Energy Department in 2016 and signed long-term deals with major oil companies including Shell, BP, Edison, and Sinopec. The Shell deal was the catalyst. Within months, BP, Edison, and Sinopec followed, each signing long-term purchase agreements. Suddenly, Venture Global had over $100 billion in contracted revenue—on paper.

The financing puzzle came together in 2017-2018. With blue-chip customers locked in, Wall Street banks that had previously laughed them out of the room were now eager to lend. The company raised $4.3 billion in project financing for Calcasieu Pass, a remarkable achievement for a startup in such a capital-intensive industry.

Construction began in earnest in 2019. True to their modular promise, the site looked different from traditional LNG projects. Instead of thousands of workers welding pipes in the Louisiana heat, trucks arrived carrying pre-built modules from Baker Hughes' Italian factories. The modules—some as large as four-story buildings—were connected like giant Lego blocks. Then COVID hit.

The pandemic should have killed Venture Global. Construction sites shut down. Supply chains collapsed. Workers couldn't travel. But the modular approach proved its worth. While competitors' sites sat idle, Baker Hughes continued manufacturing modules in Italy, stockpiling them for when construction could resume.

Venture Global's first facility, Calcasieu Pass, commenced producing LNG in January 2022. This was remarkable timing. Russia had just invaded Ukraine, sending European gas prices soaring. Suddenly, American LNG wasn't just competitive—it was desperately needed.

Calcasieu Pass has reached this milestone in just 68 months from the final investment decision on the project, making it among the fastest greenfield LNG projects completed. But the path wasn't smooth. Due to its innovative, first-of-its kind configuration consisting of many mid-scale, modular liquefaction trains and process facilities that are delivered and installed sequentially, as well as Venture Global's owner-led approach to construction, the project was able to overcome significant unforeseen challenges, including a global pandemic, two hurricanes, and a force majeure event that arose due to major manufacturing issues with the facility's power island.

The hurricanes—Laura and Delta in 2020—tested the modular design in ways nobody anticipated. Traditional LNG plants, built as monolithic structures, either survived intact or suffered catastrophic damage. Calcasieu Pass's modular design allowed damaged sections to be replaced while others continued operating—a flexibility that would later become central to customer disputes.

By early 2022, as that first molecule of gas was supercooled to -260°F and loaded onto a waiting tanker, Sabel and Pender had proven the skeptics wrong. They'd built a major LNG export facility faster than anyone thought possible, using a method the industry said wouldn't work, during a pandemic that should have stopped them cold.

But success in the energy industry isn't measured in technical achievements—it's measured in contracts fulfilled and profits delivered. And on that score, controversy was already brewing.

The same flexibility that enabled their rapid construction would soon put them at odds with the very customers who'd taken a chance on them...

V. The Customer Controversy: Arbitration Drama

The email arrived at Shell's London trading floor at 3:47 AM on a Tuesday morning in March 2023. It was from Venture Global's commercial team, and its contents would spark one of the nastiest disputes in LNG history. "Due to ongoing commissioning activities," the message read, "we regret to inform you that contracted cargoes from Calcasieu Pass will be further delayed."

Shell's traders were incredulous. They could see the ship tracking data—dozens of LNG tankers had been loading at Calcasieu Pass for over a year. The facility was clearly producing LNG. So where was it going?

The answer lay in a single word that would come to define the controversy: "commissioning."

In the LNG industry, commissioning cargoes—the initial production used to test and optimize a facility—can be sold on the spot market rather than delivered to long-term contract holders. It's a standard practice that typically lasts a few months. Venture Global had been in "commissioning" for over a year, and would ultimately remain there for over three years.

In 2023, Venture Global earned $7.8 billion from spot sales, according to an analysis by Bloomberg based on data from the Energy Department. These spot sales came during a period of sky-high prices following Russia's invasion of Ukraine, when LNG was selling for 5-10 times the price locked into long-term contracts.

It also became the most controversial supplier of the industry after six customers filed contract claims. Co-chairs Michael Sabel & Robert Pender founded the company and have since turned it upside down with strong contracts, great timing, and a plan to build three giant factories quickly. Sabel, a former banker and investment adviser, and Pender, a financial lawyer, have successfully rebutted accusations of self-dealing from BP, Shell and Repsol SA.

The customers' accusations were explosive. They alleged that Venture Global was deliberately keeping the facility in "commissioning" status to avoid delivering cheap contracted gas while profiting from astronomical spot prices. Internal documents obtained during arbitration proceedings showed that certain production units at Calcasieu Pass were operating at over 95% capacity—well above typical thresholds for declaring commercial operations.

BP's legal filing was particularly scathing, alleging a pattern of "systematic breach of contract" and "bad faith dealing." The British oil major claimed it had been forced to buy replacement cargoes on the spot market at enormous premiums, costing hundreds of millions in losses.

Shell went further, suggesting that Venture Global's entire modular design—touted as revolutionary—was being weaponized against customers. Because the facility consisted of 18 separate modules, Venture Global could claim that as long as any module was undergoing work, the entire facility remained in commissioning.

The plant has been producing commissioning cargoes since 2022, but Venture has cited problems with equipment, chiefly its heat steam recovery generators (HSRG), as preventing it from shipping cargoes to contract holders.

Venture Global's defense was technical but not implausible. The company pointed to genuine equipment failures, particularly with the heat recovery steam generators that provided power to the facility. These weren't minor issues—several units had suffered catastrophic failures requiring complete rebuilds.

Venture Global CEO Sabel acknowledged that its contract prices were lower than other companies, but said it would have been "a lot more helpful" if it had been able sign deals at higher price points. He rejected Shell's claim that Calcasieu pass was built at the expense of long-term customers and believes "the issue relating to CP1" (Calcasieu) will be resolved when Shell delivers gas to these buyers by early in next year.

The arbitration proceedings, held behind closed doors in London and New York, became a battleground over the definition of "substantial completion." Venture Global argued that their contracts allowed for extended commissioning periods given the novel technology. Customers countered that three years of "commissioning" while generating billions in revenue was unprecedented and abusive.

Industry veterans watched with fascination and horror. "This is what happens when outsiders don't understand the unwritten rules," one senior executive at a competing LNG company told reporters off the record. "In this industry, your word is your bond. You might optimize around the edges, but you don't stiff your foundational customers."

The controversy had practical implications beyond the courtroom. Other potential customers began demanding stronger contractual protections. Some walked away from negotiations entirely. European utilities, already skeptical of American suppliers after previous disputes with Cheniere, viewed Venture Global as confirming their worst fears about U.S. reliability.

Those delays have drawn public criticism and arbitration cases from nine long-term contract holders. By early 2024, the number had grown as additional customers joined the arbitration proceedings.

In April 2025, after immense pressure from regulators and customers, Venture Global announced the commercial operation date for its inaugural LNG export project – Calcasieu Pass – and the commencement of the sale of low-cost, U.S. LNG to the project's long-term customers. The facility had finally, officially, exited commissioning.

But the damage to relationships was done. During Shell plc's markets day in March, CEO Wael Sawan said the company, which is a contract holder, was still pursuing legal compensation and planned to share more information about a resolution later this year.

The arbitration drama revealed a fundamental tension in Venture Global's model. The same agility and innovation that allowed them to build faster also created opportunities for contractual gamesmanship. The modular design that reduced construction risk introduced operational complexity that could be exploited—or at least appeared to be exploitable—during the commissioning phase.

For investors considering the company's IPO, the customer controversy raised existential questions: Was this a one-time issue born of unique market conditions and equipment failures? Or did it reveal something fundamental about management's approach to stakeholder relationships?

These questions would loom large as Venture Global prepared for its public market debut, with investment bankers now forced to price in not just the company's revolutionary technology, but also its damaged reputation...

VI. The IPO Saga: From $110B Dreams to Reality Check

The 44th-floor conference room at Goldman Sachs hummed with nervous energy on that January morning in 2025. Mike Sabel stood before a room of the world's most powerful investment bankers, each representing a different bracket of what was supposed to be the triumphant return of energy IPOs. The PowerPoint deck promised a $110 billion valuation—which would make Venture Global more valuable than ConocoPhillips and approaching the market cap of Chevron.

"Gentlemen, and ladies," Sabel began, his banker instincts kicking in despite being on the other side of the table now, "we're not just selling an LNG company. We're selling America's energy independence."

The timing seemed perfect. Trump had just returned to the White House, immediately declaring a "national energy emergency" and promising to "drill, baby, drill." The new administration had reversed Biden's pause on LNG export permits. European buyers were desperate for non-Russian gas. Asian demand was soaring.

The initial plans were ambitious: 50 million shares at $40-46, targeting that $110 billion valuation. The roadshow schedule was packed—New York, Boston, London, Singapore, Tokyo. Sabel and his CFO would tell the story of disruption, of David beating Goliath, of modular technology revolutionizing global energy markets.

But behind the scenes, the book-building process was revealing uncomfortable truths.

"The arbitration issue keeps coming up," reported one syndicate desk head to the lead underwriters. Institutional investors—the pension funds, sovereign wealth funds, and mutual funds that anchor large IPOs—were spooked by the customer disputes. The question wasn't whether Venture Global would win or lose the arbitrations, but what it said about management's character.

Then came the meetings with long-only fundamental investors, the sophisticated buyers who would form the stable shareholder base. Their models showed troubling trends. Yes, revenue had grown dramatically, but free cash flow generation was concerning given the massive capital requirements. The company needed to spend over $100 billion to complete its five announced projects. Where would that money come from if capital markets soured? By mid-January, reality hit. Venture Global Inc. slashed the marketed range for its initial public offering, bringing the potential valuation well below its $110 billion target. The company now aimed to sell 70 million shares at a price range of $23 to $27, compared with its prior target of selling 50 million shares for $40 to $46 each.

The revised pricing represented a stunning climb-down. At the midpoint, the company would be valued at around $65 billion—still massive, but a far cry from the $110 billion ambition. More shares at a lower price suggested desperation to raise a specific amount of capital, likely to fund the ongoing construction projects that were burning through cash.

On January 23, 2025, the final pricing was announced: Venture Global, Inc. announced the pricing of its initial public offering of 70,000,000 shares of its Class A common stock at a public offering price of $25.00 per share. The $1.75 billion raise at a $60.5 billion valuation was respectable but underwhelming.

Venture is the first major IPO under the Trump administration. The symbolism should have been powerful—American energy independence, fossil fuel renaissance, economic nationalism. But when trading began on January 24, 2025, the market rendered its verdict.

Shares closed 4% lower at $24, putting the company's market capitalization around $58 billion. For a normal IPO, a 4% first-day decline would be disappointing. For a company that had cut its target valuation by 45% before pricing, it was devastating.

The aftermath was brutal. Within weeks, the stock had cratered more than 60%, erasing $39 billion in paper value. The founders' fortunes, which had briefly touched $24 billion each, shrank accordingly. The investment banks that had underwritten the deal faced angry calls from clients who'd been allocated shares.

Still, Venture's IPO is the largest by an oil and gas company in a decade. At a valuation of around $60 billion, it would be the tenth-largest publicly traded energy company. By any objective measure, taking a 12-year-old startup public at that valuation was a remarkable achievement.

But the market's message was clear: revolutionary technology and rapid growth weren't enough to overcome concerns about customer relationships, capital intensity, and management credibility. The IPO that was supposed to herald a new era of American energy dominance instead became a cautionary tale about the limits of disruption in capital-intensive industries.

For Sabel, the former investment banker who'd spent his career taking companies public, the irony was palpable. He'd built a company worth tens of billions, but the market—his old domain—remained skeptical of the very innovation that made it possible.

With public market scrutiny now a daily reality, Venture Global would need to prove that its business model could generate not just revenue, but sustainable free cash flow...

VII. The Business Model: Infrastructure as Competitive Advantage

Standing on the observation deck overlooking Plaquemines Parish in December 2024, Mike Sabel watched as the first drops of supercooled LNG trickled through the test lines of his second facility. Below him, a small city of steel and concrete stretched to the horizon—18 modular trains for this facility alone, each a self-contained factory for turning American shale gas into liquid gold. This wasn't just infrastructure; it was a $20 billion bet that the world would need American energy for decades to come.

Venture Global's business model is deceptively simple: buy cheap American natural gas, cool it to -260°F to shrink its volume 600-fold, load it onto specialized tankers, and sell it to energy-hungry customers worldwide. But the execution of this simple idea required reimagining how LNG infrastructure gets built, financed, and operated.

Venture is in various stages of commissioning, building and developing five natural gas liquefaction and export facilities near the Gulf of Mexico in Louisiana. Those projects are expected to have peak production capacity of 143.8 million tonnes per year. To put that in perspective, that's enough gas to power Germany for two years or Japan for three.

The five facilities—Calcasieu Pass, Plaquemines, CP2, CP3, and Delta LNG—represent different stages of Venture Global's evolution. Calcasieu Pass, now finally in commercial operation, serves as proof of concept. Plaquemines, which achieved first production in December 2024, demonstrates the ability to replicate and scale. CP2, having just achieved financial close on $15.1 billion in project financing, shows the market's continued appetite for Venture Global's model despite the controversies.

The capital intensity is staggering. The company plans to spend more than $100 billion in capex to complete these five projects. For context, that's more than the market cap of Phillips 66 or Valero, established energy giants with decades of operations. The financial performance tells a remarkable growth story, albeit one with complexity beneath the surface. In Q2 2025: Revenue nearly tripled to $3.1 billion with operating income up 186%. The company exported 89 cargoes totaling 331 TBtu of liquefied natural gas, a new record for Venture Global, and an increase of 53 cargoes from Q2 2024.

For the full year 2024, the company generated revenue of approximately $5.0 billion and net income of $1.5 billion. These are extraordinary numbers for a company that only started production in 2022.

But the revenue model reveals both the genius and the controversy of Venture Global's approach. The company operates on two parallel tracks: long-term contracts signed at fixed prices years in advance, and spot sales at market prices. During the commissioning phase—which lasted over three years at Calcasieu Pass—the company could sell at spot prices that were often 5-10x higher than contracted rates.

The company maintained its full-year 2025 Consolidated Adjusted EBITDA guidance at $6.4-6.8 billion. But EBITDA isn't cash flow. The capital intensity of the business means that even with billions in EBITDA, the company continues to consume cash for construction.

The infrastructure itself is becoming the moat. Each facility represents not just production capacity but a node in an integrated network. The company's vertically integrated business includes assets across the LNG supply chain including LNG production, natural gas transport, shipping and regasification. They own pipelines, control shipping capacity, and are developing import terminals in Europe and Asia.

The modular approach delivers unexpected financial benefits. These factors enable Venture Global to earn 40-50% of the cost of each project before other Gulf Coast greenfield projects generate revenue. Traditional competitors spend 5-6 years in pure construction before seeing a dollar of revenue. Venture Global can start generating cash after 2.5 years.

On July 28, 2025, the company announced the final investment decision for Phase 1 of the CP2 Project with the successful closing of a $15.1 billion project financing. This milestone represents the largest standalone project financing ever, demonstrating continued capital market support despite the stock price collapse.

The financing structure is sophisticated. Rather than relying entirely on corporate debt or equity, each project is financed individually with non-recourse project debt. This limits risk—if one project fails, it doesn't take down the entire company—while allowing aggressive expansion.

Standard & Poor's upgraded Calcasieu Pass Bonds to investment grade (BBB-), reflecting improved financial stability. This is crucial for attracting institutional capital and reducing borrowing costs.

But questions remain about sustainability. The company expects to export 144-149 cargoes from Calcasieu Pass and 227-240 cargoes from Plaquemines in 2025. At what point does growth capital spending moderate? When does the company transition from cash consumer to cash generator?

The business model, in essence, is a bet on three things: that global LNG demand will continue growing for decades, that modular construction will maintain its cost and speed advantages, and that capital markets will continue funding expansion. So far, all three bets are paying off—but the margin for error is thin.

This infrastructure-as-advantage strategy would be tested against a shifting global energy landscape...

VIII. The Macro Thesis: Energy Transition & Geopolitics

The war room at Venture Global's Arlington headquarters on February 24, 2022, looked more like a geopolitical command center than a corporate office. Multiple screens showed Russian tanks rolling into Ukraine, European gas prices spiking to record levels, and tanker tracking data as LNG vessels reversed course mid-Atlantic to head for Europe instead of Asia. Mike Sabel stood watching, knowing that everything had just changed for American LNG.

"This is our Churchill moment," he told his team, perhaps overdramatically. But the sentiment wasn't entirely wrong. In a single day, Europe's energy strategy for the next decade had been rewritten, and Venture Global was positioned to help fill the void left by Russian gas.

The macro thesis underpinning Venture Global's $100 billion bet is elegant in its simplicity: the world needs cleaner energy than coal and oil, renewables alone can't provide reliable baseload power, and natural gas—particularly LNG—is the bridge fuel for the next 30-50 years. Every data point supports this narrative, yet every assumption could be wrong.

Trump's national energy emergency declaration in January 2025 removed one of the biggest regulatory obstacles facing the industry. His decision to resume processing export permit applications for new LNG projects could pave the way for almost 100 million metric tons per annum of additional LNG by 2031. For Venture Global, with multiple projects awaiting permits, this was like Christmas morning.

But the real driver isn't American policy—it's global energy mathematics. Countries moving from oil and coal struggle to go all-in on renewables. Germany's energiewende has cost over €500 billion and still left them dependent on natural gas for grid stability. Japan, post-Fukushima, needs LNG to keep the lights on. China, despite massive renewable investments, is building LNG import terminals at breakneck pace.

Shell forecasts LNG demand to swell by more than 50% through 2040. The International Energy Agency, hardly a fossil fuel cheerleader, projects natural gas demand growing through 2050 in most scenarios. Even in net-zero pathways, gas with carbon capture remains essential.

The European pivot post-Ukraine has been extraordinary. In 2021, Europe imported about 155 billion cubic meters of Russian pipeline gas. By 2024, that had fallen to under 30 bcm. The gap has been filled primarily by LNG, with American exports to Europe surging from 22 bcm in 2021 to over 70 bcm in 2024. Venture Global's Calcasieu Pass alone has accounted for approximately 10% of the LNG exported from the U.S. to Europe.

Asia tells a different story but with the same ending. China's LNG imports grew from essentially zero in 2006 to becoming the world's largest importer by 2021. India, Pakistan, Bangladesh, Vietnam—all are building import terminals and signing long-term contracts. The region is expected to account for 75% of global LNG demand growth through 2040.But not everyone agrees with this rosy outlook. IEEFA expects Europe's LNG demand to peak by 2025 and decline through 2030. Europe imported a record amount of LNG in 2022 to replace lost Russian pipeline gas supplies, but in the last two years overall gas demand has fallen 20% to its lowest level in a decade and is expected to fall by 11% between 2023 and 2030.

The competition is fierce and getting fiercer. Qatar, the longtime LNG king, is expanding capacity from 77 MTPA to 142 MTPA by 2030. Australia, despite higher costs, continues to dominate Asian markets with geographic advantage. New players—Mozambique, Tanzania, Canada—are entering the fray.

Within the U.S., Cheniere remains the dominant player with first-mover advantages and established customer relationships. But Venture Global's bet is that the market is big enough for multiple winners, and that their modular approach gives them a structural cost advantage that will matter more over time.

The climate debate adds another layer of complexity. LNG produces about 50% less CO2 than coal when burned, making it a cleaner transition fuel. But methane leakage during production and transport can offset these benefits. The Inflation Reduction Act and European carbon border adjustments are creating new economic realities that could favor or punish LNG depending on implementation.

Global natural gas demand growth is forecast to slow from 2.8% in 2024 to around 1.3% in 2025. The increase this year is expected to be almost entirely driven by North America and Europe, with the growth in consumption in the Asia-Pacific region – where many markets tend to be sensitive to higher prices – falling to its weakest annual rate since the energy crisis in 2022.

Yet the longer-term trajectory remains intact. The report sees global demand growth picking up again in 2026 and accelerating to around 2% as a considerable increase in LNG supply eases market fundamentals and fosters stronger demand growth. LNG demand is set to see fast growth over the next two years thanks to decarbonization efforts across the world prompting a shift away from coal, and infrastructure expansion in Asia.

Venture Global's timing couldn't be better—or worse, depending on your perspective. They're bringing massive new supply online just as the market is transitioning from shortage to potential oversupply. IEEFA expects global LNG supply capacity to rise to 666.5 MTPA by the end of 2028, which could be sufficient to meet all global demand requirements through 2040, even under optimistic industry forecasts.

This oversupply risk is real. If all announced projects come online as planned, the 2027-2030 period could see a glut that crashes prices and strands assets. Venture Global's response is speed—get facilities built and contracts signed before the music stops.

The geopolitical tailwinds are undeniable. Energy security has trumped climate concerns in most Western capitals. The U.S.-China competition is creating parallel energy systems. Europe's desperate diversification away from Russia has created a generational opportunity for American LNG.

But tailwinds can become headwinds. A Russia-Ukraine peace deal could see Russian gas return to Europe. A global recession could crush demand. Technological breakthroughs in batteries or nuclear could accelerate the renewable transition beyond current projections.

These macro forces would ultimately be filtered through the complex dynamics of corporate governance and founder control...

IX. Power Dynamics & Governance Evolution

The boardroom on the 12th floor of Venture Global's Arlington headquarters has an unusual seating arrangement. At most public companies, the CEO sits at the head of the table, flanked by independent directors. Here, Mike Sabel and Bob Pender sit side by side at the center, a physical manifestation of the unique power structure they've maintained even after going public.

Together, Sabel, Pender and other employees own just over 90% of the company. This isn't just majority control—it's near-absolute dominion over a $60 billion public company. The ownership is structured through a dual-class share system that would make even Silicon Valley founders jealous.

Sabel and Pender together own all of Venture Global's Class B shares through holding company Venture Global Partners II, LLC. Sabel is credited with half of those shares based on an overview of the company's ownership structure filed as an exhibit in a 2024 lawsuit and a Dec. 18, 2023 Federal Register filing explaining the ownership of the LLC.

The 2020 governance change was pivotal but subtle. Pender stated, "It has been an exhilarating decade working with Mike to create Venture Global LNG and to help reshape the global LNG industry. In particular, through Venture Global, we are so proud that we have materially reduced the cost of LNG at a critical moment of transition for the world's energy needs. We have succeeded in large part because of the singular focus we have both personally fully invested, now I need to step back a bit. There is no person I trust more than Mike to lead this company we created together into the future. I remain fully committed to Mike, the company and its success, but in a different role where I can add the highest value and at a more balanced pace".

This transition—Sabel becoming sole CEO while Pender moved to Executive Co-Chairman—was orchestrated to clarify leadership for public market investors while maintaining the partnership structure. But make no mistake: major decisions still require both founders' agreement.

The IPO created paper fortunes worth approximately $24 billion each at listing, though the subsequent stock decline has reduced these significantly. Still, even at current depressed prices, each founder controls wealth exceeding $10 billion—enough to place them among America's richest individuals.

The board composition post-IPO reflects a careful balance. Independent directors with energy industry credentials were added to satisfy governance requirements. But with 90% voting control, these directors serve more as advisors than checks on management power.

This concentration of power has implications beyond corporate governance. When customers complain about contract fulfillment, they're not dealing with professional managers worried about their next job—they're dealing with owner-operators who view the company as their life's work. When investors push for strategic changes, they face founders who can simply ignore them.

The employee ownership component—that remaining portion of the 90%—creates interesting dynamics. Early employees who joined when Venture Global was just two guys with a PowerPoint now hold stakes worth tens or hundreds of millions. This has created a culture of ownership but also golden handcuffs that make it hard to leave despite the intense work environment.

Pacific Investment Management Co. (PIMCO) holds the only significant minority stake, a position they've maintained since the early financing rounds. Their presence provides some institutional credibility, but their influence is limited by the founders' super-majority control.

The governance structure enables fast decision-making—critical in the volatile LNG market. When the Ukraine crisis created opportunities, Venture Global could pivot immediately without board debates or shareholder votes. When equipment failures required expensive fixes, management could commit resources without lengthy approvals.

But this structure also enables the behaviors that led to customer arbitrations. With no meaningful board oversight or shareholder accountability, management could pursue aggressive commissioning strategies that maximized short-term profits at the expense of long-term relationships.

The public market has rendered its verdict on this governance model through the stock price. The 60% decline from IPO suggests investors want either more influence or lower valuations to compensate for their powerlessness.

The question for potential investors: Is founder control a feature or a bug? In industries requiring long-term thinking and massive capital commitments, owner-operators often outperform professional managers. Jeff Bezos didn't step down from Amazon until it was worth $1.7 trillion. Elon Musk's control of Tesla and SpaceX enables bold bets professional managers wouldn't make.

But energy is different from tech. It's an industry built on relationships, reputation, and reliability. The cowboy capitalism that works in Silicon Valley might be incompatible with the gentleman's agreements that govern global energy markets.

As Venture Global matures, pressure will build for governance evolution. Large institutional investors who sat out the IPO might require board representation or enhanced minority rights before investing. Customer relationships might improve with more independent oversight. Capital markets might provide cheaper funding with stronger governance.

But for now, Sabel and Pender remain firmly in control of their creation, for better or worse.

The lessons from Venture Global's journey offer a playbook for disruption in capital-intensive industries...

X. Playbook: Lessons in Disruption

The Outsider Advantage

The pattern repeats across industries: outsiders see opportunities that insiders miss. Sabel and Pender's lack of LNG experience wasn't a bug—it was the feature that enabled them to question fundamental assumptions. They didn't know that LNG plants "had" to be massive, custom-built projects. They didn't accept that commissioning "should" last three months. Their ignorance of industry norms became their competitive advantage.

The lesson isn't that expertise doesn't matter—Venture Global hired hundreds of industry veterans to execute their vision. Rather, it's that industry expertise can create blind spots. The most profound innovations often come from applying insights from one domain to problems in another. Sabel's structured finance background led him to see LNG facilities as financial instruments. Pender's legal expertise helped navigate the complex web of permits and contracts that would have paralyzed others.

Modular Thinking

The modular revolution extends beyond physical construction. Venture Global modularized everything: financing (project-by-project rather than corporate), operations (independent trains that can run separately), even commercial strategy (different pricing for different phases). This approach reduced risk, increased flexibility, and accelerated learning curves.

The highly-efficient liquefaction train system (LTS) supplied by Baker Hughes is modularized, helping to lower construction and operational costs with a "plug and play" approach that enables faster installation. But the real innovation was recognizing that modularization changes the entire value chain. When you build in factories, you access different labor pools, achieve different quality standards, and enable different financing structures.

Speed as Strategy

In commodity markets, being first matters more than being best. Venture Global's Calcasieu Pass holds the global record for the fastest construction of a large scale greenfield LNG project, moving from FID to first LNG in 29 months. This speed created multiple advantages: capturing high prices during the Ukraine crisis, learning faster than competitors, and achieving scale before the market saturates.

Speed also became a defensive moat. By the time competitors understood the modular model, Venture Global had already locked up the best sites, signed the key customers, and achieved scale economies. The first-mover advantages in LNG—where customers sign 20-year contracts—are particularly durable.

Capital Access

Venture Global mastered the art of sequential capital raising. Start with venture funding to prove the concept. Graduate to project finance once you have customer contracts. Layer in different types of debt as projects mature. Finally, access public markets for permanent capital. Each funding round de-risked the next, creating a virtuous cycle.

The $15.1 billion project financing for CP2—the largest standalone project financing ever—demonstrates the model's maturity. When banks compete to lend you $15 billion for a single project, you've transcended startup status.

Regulatory Navigation

Energy is among the most regulated industries in America. Venture Global needed permits from FERC, DOE, EPA, Army Corps of Engineers, and countless state and local authorities. Their approach was counterintuitive: rather than fighting regulations, they embraced them as competitive barriers.

By becoming experts at regulatory navigation—hiring former regulators, engaging early with agencies, over-investing in compliance—they turned bureaucracy into a moat. Competitors might copy their technology, but could they navigate the regulatory maze as effectively?

Customer Lock-in

The 20-year take-or-pay contracts that are standard in LNG create extraordinary customer lock-in. Once signed, customers are essentially partners for two decades. This transforms the business model from commodity trading to infrastructure ownership.

But lock-in works both ways. The customer arbitrations revealed the dark side of long-term contracts: when relationships sour, you're stuck with unhappy partners for decades. The art is structuring contracts that align interests while maintaining flexibility for unforeseen circumstances.

Risk Management

Venture Global's risk framework is sophisticated. Construction risk is mitigated through modular building and fixed-price contracts. Commodity risk is hedged through long-term contracts with price floors. Operational risk is reduced through redundancy—multiple small trains instead of few large ones. Financial risk is contained through project-level non-recourse debt.

But they missed reputational risk. The customer disputes revealed a blind spot in their risk matrix. In industries built on trust, reputational damage can be more costly than financial losses.

The Platform Play

Venture Global isn't just building LNG plants—they're building a platform. The pipeline networks, shipping capacity, and import terminals create an integrated system that's worth more than the sum of its parts. Each new facility strengthens the network effects.

This platform thinking extends to capabilities. The expertise developed building Calcasieu Pass made Plaquemines faster and cheaper. The relationships formed with contractors, suppliers, and regulators compound over time. The data generated from operations enables continuous improvement.

Vertical Integration

Unlike pure-play operators who focus on one part of the value chain, Venture Global integrated vertically from gas procurement through shipping to regasification. This integration captures more margin, reduces transaction costs, and provides operational flexibility.

But vertical integration also increases complexity and capital requirements. The question is whether the benefits of integration outweigh the costs of complexity.

The Disruption Paradox

Venture Global's story illustrates the disruption paradox: the very qualities that enable disruption can prevent sustainable success. The aggressiveness that allowed them to build faster than anyone thought possible also led to customer disputes. The founder control that enabled bold bets also reduced accountability. The outsider mentality that questioned everything also alienated industry incumbents.

The challenge for disruptors is knowing when to shift from insurgent to incumbent mentality. When do you stop breaking rules and start following them? When do you prioritize stability over growth? When do you trade speed for sustainability?

These strategic choices would ultimately determine whether Venture Global represents a transformative investment opportunity or a cautionary tale...

XI. Analysis & Investment Case

Bull Case: The Energy Transformation Play

The optimistic scenario for Venture Global rests on three pillars, each supported by powerful secular trends that could drive decades of growth.

First, the global energy transition paradoxically strengthens natural gas demand. As countries shut coal plants and nuclear reactors while struggling with renewable intermittency, gas becomes the essential bridge. Decarbonization initiatives will play a key role in China's gas demand growth over 2025-2030. China will lead the LNG imports growth over this period followed by the markets in South and Southeast Asia. Even aggressive net-zero scenarios require gas through 2050, especially when paired with carbon capture.

Second, Venture Global's modular technology provides sustainable competitive advantages. The company emphasized its competitive advantages, including faster project completion times (2.5 years versus the industry average of 5+ years), the ability to sell commissioning cargoes during construction, and targeting 140% of nameplate capacity. These factors enable Venture Global to earn 40-50% of the cost of each project before other Gulf Coast greenfield projects generate revenue. This isn't just incrementally better—it's categorically different, like comparing Tesla's manufacturing to traditional automakers.

Third, the geopolitical realignment toward energy security over climate concerns creates generational tailwinds. Europe's permanent divorce from Russian gas, China's energy insecurity, and America's energy dominance agenda align perfectly with Venture Global's expansion plans. The company is essentially a leveraged bet on American energy nationalism—a bet that's paying off under both Republican and Democratic administrations.

The financial metrics in the bull case are compelling. If the company achieves its 143.8 MTPA capacity target and maintains $3-4/MMBtu margins, annual EBITDA could exceed $20 billion by 2030. At a 10x EBITDA multiple—reasonable for infrastructure assets—that implies a $200 billion valuation, a 3x+ return from current levels.

The first-mover advantages in securing prime Louisiana sites, establishing customer relationships, and achieving scale create barriers to entry that strengthen over time. Even if competitors copy the modular approach, they can't replicate the learning curve advantages or the locked-in customer base.

Bear Case: The Execution and Trust Deficit

The pessimistic scenario sees multiple threats converging to pressure the business model.

The customer arbitration issue isn't just about money—it's about trust. In an industry where your word is your bond, Venture Global has been branded as unreliable. Major customers including Shell, BP, and Repsol pursuing arbitration sends a signal to every potential customer: buyer beware. Future contracts will likely include stronger protections, reducing profitability and flexibility.

The capital intensity is staggering and risky. Spending $100+ billion on infrastructure assumes decades of stable demand—a bold bet when renewable costs are plummeting and battery technology is advancing rapidly. If the energy transition accelerates faster than expected, these could become stranded assets by 2040.

The market structure is deteriorating. Operational and under-construction LNG projects will be able to push total available supply above demand estimates over 2027-28, suggesting oversupply and margin compression ahead. With Qatar, Australia, and new entrants flooding the market with supply, the golden age of LNG pricing may be ending just as Venture Global scales up.

Operational complexity increases exponentially with scale. Managing 18 modular trains is different from managing 180. Each facility adds technical, commercial, and regulatory complexity. The company's track record—three years of commissioning at Calcasieu Pass—raises questions about operational excellence.

The governance structure is problematic for public market investors. With founders controlling 90% voting rights, minority shareholders have no meaningful influence. This structure might work for a startup but seems inappropriate for a $60 billion public company. The stock's 60% decline suggests the market agrees.

Competition is intensifying from both traditional players and new entrants. Cheniere is expanding aggressively. Qatar is adding massive capacity. Even oil majors like ExxonMobil and Chevron are entering the LNG export business. Venture Global's first-mover advantage is eroding.

Valuation Framework

The challenge in valuing Venture Global is determining whether it's an infrastructure company, a commodity producer, or a hybrid. Each lens yields different valuations:

As Infrastructure: Pipeline companies and utilities trade at 10-12x EBITDA, implying a $60-75 billion valuation based on 2025 guided EBITDA of $6.4-6.8 billion. This assumes stable, regulated-like returns—questionable given the commodity exposure and customer disputes.

As Commodity Producer: Oil and gas E&P companies trade at 4-6x EBITDA, implying a $25-40 billion valuation. This seems too punitive given the long-term contracts and infrastructure ownership, but reflects the market's current view.

As Hybrid: A blended multiple of 7-8x EBITDA might be appropriate, implying a $45-55 billion valuation—roughly where the stock trades today. This suggests the market is fairly valued unless you believe either the bull or bear case strongly.

The key variables for valuation are: 1. Utilization rates: Can they achieve the promised 140% of nameplate capacity? 2. Margin sustainability: Will the spread between U.S. gas and global LNG prices persist? 3. Capital efficiency: Can they complete projects at promised costs and timelines? 4. Contract renewal: Will customers renew after current contracts expire? 5. Terminal value: What's the business worth in 2040 when contracts roll off?

Risk-Reward Analysis

The asymmetry is striking. In the bull case, the stock could triple as projects come online and cash flow accelerates. In the bear case, it could halve if arbitrations go badly or markets oversupply.

The critical insight is timing. The next 2-3 years will determine whether Venture Global is a transformational investment or a value trap. Key milestones to watch: - Resolution of customer arbitrations - Plaquemines ramp-up to full production - CP2 construction progress and first LNG - 2026-2027 LNG market balance - Governance evolution and institutional adoption

For risk-tolerant investors with 5+ year horizons, the current valuation might offer attractive risk-reward. The company is trading at a significant discount to replacement cost, has locked-in revenue for decades, and operates in a structurally growing market.

For conservative investors, the red flags are too numerous to ignore. Customer disputes, governance concerns, execution risks, and market structure deterioration suggest waiting for more clarity—even if it means paying higher prices later.

The Fundamental Question

Ultimately, investing in Venture Global comes down to a simple question: Do you believe the world needs massive amounts of American LNG for the next 20 years?

If yes, then Venture Global—despite its flaws—offers one of the most leveraged ways to play this theme. Their infrastructure is real, their contracts are signed, and their technology works.

If no—if you believe renewables will advance faster, batteries will solve intermittency, or geopolitical tensions will ease—then Venture Global is building monuments to a dying industry.

The market, in its wisdom or folly, is currently splitting the difference. At $60 billion, it's pricing in success but not dominance, growth but not transformation. Whether that's too optimistic or too pessimistic will only be known in hindsight.

As we look toward the future, the scenarios for Venture Global range from becoming the ExxonMobil of the 21st century to becoming a cautionary tale about the perils of growing too fast in a capital-intensive industry...

XII. Epilogue & Future Scenarios

Standing at the edge of Plaquemines Parish in late 2025, watching another LNG tanker disappear into the Gulf horizon, Mike Sabel might reflect on how far he's come from that rented Chevy traversing Texas twelve years ago. But the harder question isn't about the past—it's about what comes next. The decisions made in the next 24 months will determine whether Venture Global becomes an enduring energy giant or a brilliant flame that burned too bright.

Scenario 1: The Arbitration Apocalypse

In the darkest timeline, the customer arbitrations go catastrophically wrong. International tribunals rule that Venture Global deliberately breached contracts, awarding billions in damages to Shell, BP, and others. More damaging than the financial penalties would be the reputational destruction. New customers refuse to sign contracts without onerous protections. Existing customers exercise early termination clauses where possible. Banks hesitate to provide project financing.

The stock craters to $5-10, valuing the company at barely more than invested capital. Sabel and Pender, their paper fortunes evaporated, face shareholder lawsuits alleging self-dealing. The company survives but as a wounded animal—forced to sell assets to raise cash, unable to complete its ambitious expansion plans. Competitors cherry-pick their best employees and contractors.

In this scenario, Venture Global becomes a case study at Harvard Business School—not for innovation, but for how hubris and short-term thinking can destroy long-term value. The modular revolution continues, but led by others who learned from Venture Global's mistakes.

Scenario 2: The Goldilocks Resolution

The more likely scenario sees a negotiated resolution to the arbitrations—painful but not fatal. Venture Global pays $2-3 billion in settlements, agrees to governance improvements, and commits to clearer commercial terms going forward. Customers grumble but recognize they need the LNG supply. The stock recovers to $30-40 as uncertainty clears.

The company successfully completes its five announced projects by 2030, achieving 100+ MTPA of production capacity. Cash flow generation accelerates as construction spending moderates. By 2027, they're generating $5+ billion in annual free cash flow, enabling dividends and share buybacks.

The governance structure gradually evolves. Sabel and Pender maintain control but add truly independent directors and enhance minority shareholder rights. Institutional investors slowly warm to the story. The stock re-rates to $50-60 as the company transitions from growth to harvest mode.

In this future, Venture Global becomes the Occidental Petroleum of LNG—not the biggest player, but a respectable, profitable, shareholder-friendly company that found its niche and executed well.

Scenario 3: The Energy Transformation Champion

In the optimistic scenario, everything clicks. The arbitrations are resolved quickly and cheaply. Plaquemines and CP2 ramp up ahead of schedule. The modular model's advantages compound—each new facility is built faster and cheaper than the last. Operating margins expand as the company leverages its infrastructure platform.

More importantly, the macro environment cooperates. The energy transition proceeds exactly as Venture Global predicted—renewable growth but with massive gas backup requirements. Carbon capture technology makes gas truly clean. Geopolitical tensions keep energy security paramount. LNG demand grows even faster than forecasted.

The company announces projects 6 through 10, targeting 200 MTPA by 2035. They expand internationally, building import terminals in Europe and Asia. They integrate further upstream, acquiring gas production assets when prices are low. They become a full energy company, not just an LNG exporter.

The stock soars to $100+, valuing the company at $200+ billion. Sabel and Pender become American energy titans, mentioned alongside Rockefeller and Pickens. The company joins the S&P 500, becomes a dividend aristocrat, and anchors pension fund portfolios globally.

The Next Decade: Key Decisions

Several critical decisions will determine which scenario unfolds:

Capital Allocation: Does the company continue its breakneck expansion, or does it moderate growth to return cash to shareholders? The tension between empire-building and shareholder returns will define the investment case.

International Expansion: Should Venture Global remain U.S.-focused or expand globally? Building facilities in Africa, Southeast Asia, or the Middle East could provide growth but adds complexity and risk.

Vertical Integration: How far upstream and downstream should they go? Acquiring gas production makes them more integrated but more capital-intensive. Building power plants in importing countries captures more value but requires new capabilities.

Technology Evolution: Will they continue innovating or rest on their laurels? The next S-curve might be floating LNG, hydrogen compatibility, or carbon capture integration. Missing the next wave could be fatal.

Governance Evolution: Can the founders evolve from entrepreneurs to institution-builders? The transition from founder-led to professionally-managed is treacherous but necessary for long-term survival.

Succession Planning: Sabel is 57, Pender 71. Who takes over when they step down? Is there a deep bench of talent, or does the company depend entirely on its founders? The answer will significantly impact long-term value.

The Historical Parallel

Venture Global's story echoes previous energy transformations. In the 1860s, John D. Rockefeller saw that oil's future wasn't in production but in refining and distribution infrastructure. In the 1950s, George Mitchell spent decades perfecting fracking despite industry skepticism. In the 1990s, Enron tried to transform energy markets through financial innovation—until fraud brought it down.

Which parallel proves most relevant? Are Sabel and Pender the Rockefellers of LNG, building an enduring empire? The George Mitchells, pioneering technology that transforms the industry? Or the Ken Lays, whose aggression and corner-cutting ultimately destroy their creation?

Final Thoughts

The entrepreneurial audacity that created Venture Global—two complete outsiders revolutionizing a century-old industry—deserves respect regardless of the ultimate outcome. They've already succeeded in ways nobody predicted: building functional LNG export facilities using radical new methods, creating tens of billions in value, and forcing an entire industry to reconsider its assumptions.

But the transition from insurgent to incumbent, from disruptor to operator, from entrepreneur to institution remains incomplete. The next chapter will determine whether Venture Global enters the pantheon of great American energy companies or becomes a footnote in the industry's history.

For investors, employees, customers, and competitors, the Venture Global story offers lessons that transcend the specific context of LNG: - Innovation can come from anywhere, especially from outsiders unencumbered by conventional wisdom - Speed and execution matter more than perfect planning in rapidly evolving markets - Capital intensity requires patient capital and aligned incentives - Trust, once broken, is nearly impossible to rebuild in relationship-based industries - Governance matters eventually, even if founders can ignore it initially

As the sun sets over the Louisiana bayous, with the mechanical hum of compressors turning methane into liquid gold, the Venture Global story continues to unfold. Whether it ends in triumph or tragedy, transformation or disappointment, remains unwritten. But one thing is certain: the energy industry will never be quite the same after two outsiders in a rented Chevy dared to dream differently.

The next decade will reveal whether that difference creates enduring value or expensive lessons. Either way, the attempt itself—the sheer audacity of building America's LNG giant from nothing—has already earned its place in business history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube