Universal Insurance Holdings: The Florida Property Insurance Survivor

I. Introduction and Episode Roadmap

Picture a map of Florida's private property insurance market in 2020, dotted with the logos of dozens of carriers. Now fast-forward to 2023. More than half of those logos have vanished—companies swallowed by insolvency, crushed by litigation abuse, or simply unwilling to bet another season against Atlantic hurricanes. And yet, standing amid the wreckage, one mid-cap insurer headquartered in Fort Lauderdale keeps writing policies, paying claims, and compounding book value at rates that would make most specialty finance companies envious. That company is Universal Insurance Holdings, ticker UVE.

Universal is not a household name. It does not advertise during the Super Bowl. Its market capitalization, roughly $950 million as of early 2026, barely registers against the Allstates and Progressives of the world. But in the narrow, high-stakes arena of Florida homeowners insurance, Universal has become one of the last credible private-market players standing—writing more than $1.6 billion in annual premiums, serving nearly 900,000 policyholders across nineteen states, and posting a 2025 return on equity north of thirty percent.

The central question of this story is deceptively simple: how did a small regional insurer, born in the aftermath of Hurricane Andrew, navigate catastrophic storms, a litigation crisis that bankrupted its peers, a global reinsurance squeeze, and relentless regulatory pressure—and come out the other side stronger than ever? The answer touches on insurance economics, climate science, legal reform, and the unglamorous art of operational discipline in a market where a single bad September can wipe out a decade of profits.

This is a story about tail risk, survivor economics, and the strategic value of being the last player standing. Along the way, it reveals why property insurance in hurricane country may be the most consequential—and least understood—corner of American finance.

II. Insurance 101 and Why Property Insurance Is Different

Before diving into Universal's story, it helps to understand why property insurance is fundamentally unlike most other financial businesses—and why Florida, in particular, is the industry's most dangerous playground.

At its core, every insurance company runs the same basic model. Customers pay premiums upfront. The insurer pools that money—the famous "float" that Warren Buffett rhapsodizes about—and invests it until claims come due. If the premiums collected exceed the claims paid plus operating expenses, the insurer earns an underwriting profit. If the investment returns on the float exceed the cost of capital, there is a second layer of profit. The best insurance businesses, like Berkshire Hathaway's GEICO, make money on both sides.

The key metric is the combined ratio: the sum of claims costs (the loss ratio) and operating expenses (the expense ratio), expressed as a percentage of premiums earned. A combined ratio below one hundred percent means the insurer is making money on underwriting alone, before investment income. Above one hundred percent, and the insurer is essentially paying customers to hold their money—a viable strategy only if investment returns compensate for the underwriting loss.

Now, property and casualty insurance—particularly homeowners coverage in hurricane-exposed states—differs from life or health insurance in one critical respect: the distribution of losses is wildly asymmetric. A life insurer can model mortality tables with actuarial precision over millions of policyholders; death rates are stable, predictable, and not subject to a single catastrophic event wiping out a quarter of the portfolio in an afternoon. Health insurers face utilization risk, but costs tend to be mean-reverting.

Property insurance in Florida is different. In a quiet year, loss ratios might run in the fifties—extremely profitable. But a single Category 4 hurricane can generate losses that exceed five or ten years of accumulated premiums in a matter of hours. This is the "fat tail" problem: the probability distribution of losses has a long right tail populated by low-frequency, high-severity events that can destroy an insurer's surplus overnight.

This is where reinsurance enters the picture. Reinsurance is insurance for insurance companies—a mechanism for ceding a portion of catastrophic risk to global reinsurers like Swiss Re, Munich Re, and RenaissanceRe in exchange for a premium. Think of it as a deductible in reverse: the primary insurer keeps the first layer of losses (the "retention"), and the reinsurer picks up everything above that threshold, up to a contractual limit. The stack of reinsurance contracts, layered from the retention up to the maximum covered loss, is called the "reinsurance tower."

For a Florida property insurer, the reinsurance tower is not a nice-to-have. It is existential. Without it, a single major hurricane could consume the entire surplus of the company. With it, the insurer's net exposure to a catastrophic event is limited to its retention—typically tens of millions of dollars rather than hundreds of millions or billions. The trade-off, naturally, is cost: reinsurance premiums consume a substantial share of the primary insurer's revenue, sometimes exceeding thirty percent of direct premiums earned.

Florida adds another layer of complexity. The state sits in the crosshairs of Atlantic hurricanes, with 1,350 miles of coastline, explosive coastal development, and a population that has grown from roughly thirteen million in 1990 to nearly twenty-three million today. Climate science suggests that while the total number of Atlantic hurricanes may not increase dramatically, the proportion of the most intense storms—Category 4 and 5—is rising, and sea-level rise amplifies storm surge damage even from weaker systems.

On top of the physical risk, Florida's regulatory environment has historically squeezed insurers from both sides: the Office of Insurance Regulation must approve rate increases, creating friction when carriers need to reprice risk quickly, while a unique legal framework—until recently—allowed litigation abuse to inflate claims costs far beyond what wind and water actually caused. Understanding these dynamics is essential to appreciating what Universal Insurance Holdings has accomplished, and what challenges still lie ahead.

III. Origins and Early Years (1990s–2008)

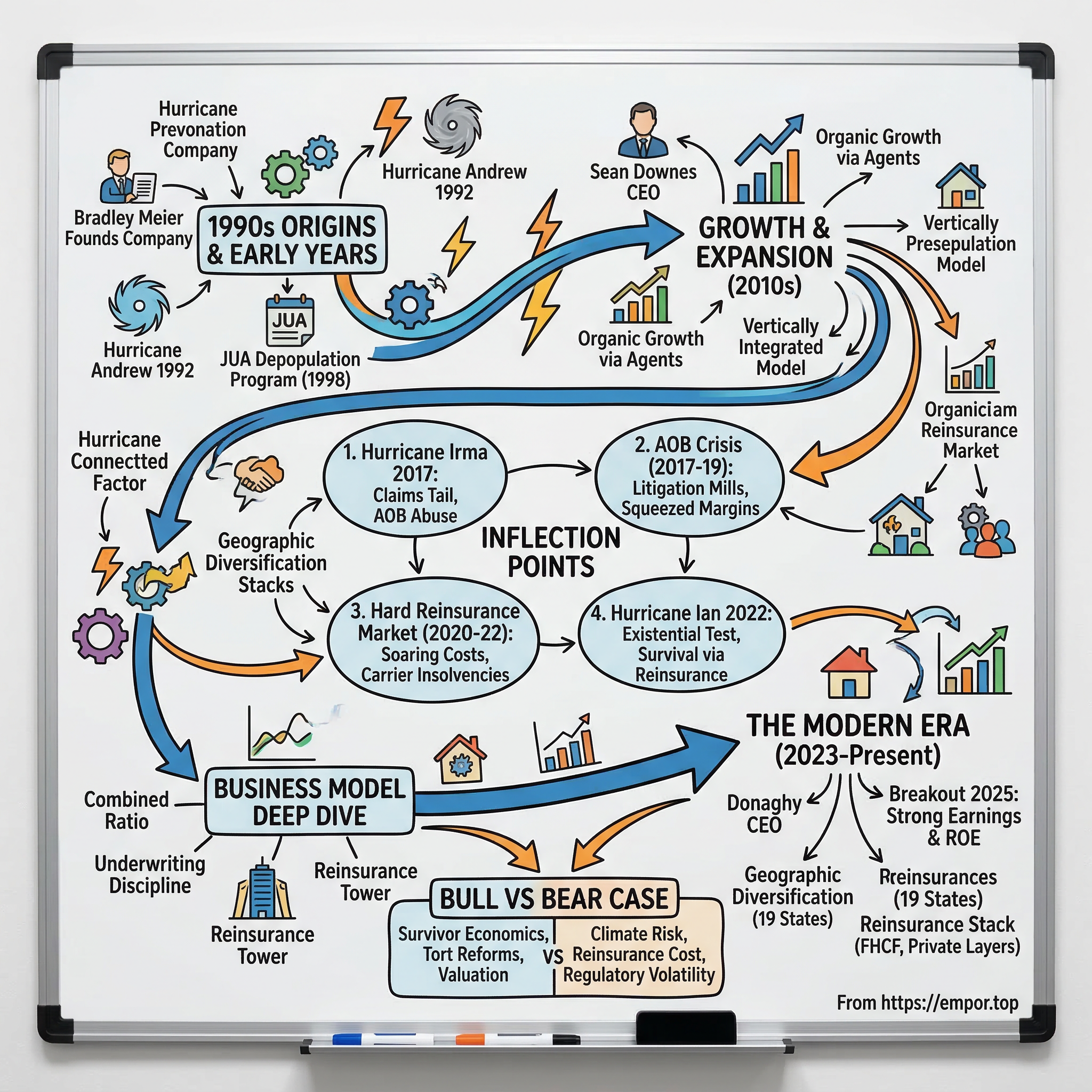

On November 12, 1990, a twenty-two-year-old Wharton graduate named Bradley Meier filed incorporation papers in Delaware for a company called Universal Heights, Inc. Meier had just completed his economics degree at the University of Pennsylvania and spotted what he believed was an underserved niche: residential property insurance in Florida, a state where rapid population growth and coastal development were creating demand that national carriers served only reluctantly.

The timing proved prescient—though not in the way Meier might have expected. Less than two years later, on August 24, 1992, Hurricane Andrew slammed into Homestead, Florida, as a Category 4 storm. The destruction was staggering: more than $15.5 billion in insured losses, a loss ratio of 1,010 percent for Florida homeowners insurance that year—meaning insurers paid out more than ten dollars in claims for every dollar of premium they had collected. Between seven and eleven property insurers became insolvent. National carriers like Allstate, State Farm, and Travelers began pulling back from the state, dropping hundreds of thousands of policies.

Andrew's devastation reshaped the Florida insurance landscape in ways that are still felt today. The state legislature created the Florida Hurricane Catastrophe Fund in 1993, a government-run reinsurance mechanism that all residential property insurers must participate in. It also established the Florida Residential Property and Casualty Joint Underwriting Association, a state-backed pool of last resort that would later be merged into Citizens Property Insurance Corporation in 2002. And crucially, the exodus of national carriers created a vacuum that dozens of small, Florida-focused startups rushed to fill. The number of domestic insurance companies in the state surged by 166 percent over the following three decades.

Universal Heights went public on December 16, 1992—just four months after Andrew—and changed its name to Universal Insurance Holdings in January 2001. But the pivotal move came in April 1997, when Meier formed the company's primary insurance subsidiary, Universal Property and Casualty Insurance Company, known as UPCIC. The new subsidiary was designed from the ground up to write homeowners coverage in hurricane country, with actuarial models, underwriting guidelines, and reinsurance structures calibrated specifically for Florida wind risk.

UPCIC's first major growth opportunity came in 1998, when it participated in the JUA depopulation program—a state-sponsored initiative that paid private insurers to assume policies from the bloated government pool, which had swelled to 940,000 policies after Andrew. Thirty-two companies participated, taking one million policies out of the JUA in exchange for $81 million in bonus payments. Universal was among them.

Here is where the company made a decision that would prove strategically consequential: after that initial 1998 takeout, UPCIC did not participate in subsequent Citizens depopulation rounds. While many Florida-only carriers became addicted to the easy growth of assuming Citizens policies—often without adequate pricing or risk selection—Universal chose to build its book organically through an independent agent network. This distinction may seem minor, but it meant that Universal's portfolio was underwritten to its own standards rather than inherited from a government pool with adverse selection problems. Several of the carriers that later went insolvent had gorged on Citizens takeout policies without properly repricing the risk.

In July 1999, a claims executive named Sean Downes joined the company from Downes and Associates, a multi-line insurance claims adjustment firm. Downes started by building out Universal's entire claims operation through a subsidiary called Universal Adjusting Corporation. His ascent was steady: COO of the claims subsidiary by 1999, COO and director of UPCIC by 2003, and senior vice president and COO of the parent company by 2005. When founder Bradley Meier resigned in February 2013 to pursue opportunities outside the homeowners insurance industry, Downes was the natural successor, stepping into the CEO role with deep operational knowledge of every corner of the business.

By 2008, Universal had also formed a second subsidiary, American Platinum Property and Casualty Insurance Company, targeting the high-value home market—properties worth more than one million dollars that fell outside UPCIC's sweet spot. The company's vertically integrated structure—with in-house underwriting through Universal Risk Advisors, in-house claims through Universal Adjusting Corporation, and in-house inspections through Universal Inspection Corporation—gave it cost control and quality oversight that many competitors, who outsourced these functions, simply could not match.

The company that emerged from the 2000s was small but purposeful: a Florida specialist with organic growth, vertically integrated operations, and a management team that had been forged in the state's uniquely hostile insurance environment. What it needed next was a stretch of calm weather to prove the model could compound value over time.

IV. The First Major Test: Hurricane Seasons and Andrew's Legacy

To understand Universal's strategic positioning, one must first understand the scar tissue that Hurricane Andrew left on the Florida insurance industry—and how that scar tissue shaped the regulatory, competitive, and reinsurance landscape that Universal would navigate for the next three decades.

Before Andrew, catastrophe modeling barely existed as a discipline. Insurers priced hurricane risk using historical averages and gut feel. One industry veteran predicted pre-Andrew that a major Miami hurricane would generate four to five billion dollars in insured losses. The actual figure was more than three times that estimate. The lesson was brutal and clarifying: the industry had been systematically underpricing Florida hurricane risk, and the tools it used to measure that risk were dangerously inadequate.

Andrew triggered a cascade of structural changes. The Florida Hurricane Catastrophe Fund provided a layer of state-backed reinsurance at below-market rates, effectively subsidizing the cost of doing business in the state. Citizens Property Insurance Corporation, created in 2002 by merging two predecessor pools, became the insurer of last resort—but with a crucial catch: if Citizens' claims exceeded its resources, it could levy assessments on virtually all property and casualty policyholders in the state, making every Floridian a backstop whether they were Citizens customers or not.

The regulatory architecture that emerged was a compromise between competing imperatives. The Office of Insurance Regulation needed to ensure rates were adequate to keep carriers solvent, but political pressure—from homeowners, real estate developers, and elected officials—pushed for rates to stay low. This tension would become a recurring theme in Universal's story, reaching its most acute expression during the insolvency wave of 2021-2022 when inadequate rate approvals were widely cited as a contributing factor.

Universal's emergence in this post-Andrew landscape was well-timed. The company was purpose-built for a market that national carriers wanted no part of. Its actuarial models reflected Florida-specific wind exposure, its underwriting guidelines incorporated roof age, construction type, and proximity to the coast, and its reinsurance tower was designed to absorb the kind of losses that had destroyed its predecessors.

The 2004 and 2005 hurricane seasons tested this architecture severely. In 2004, four major hurricanes—Charley, Frances, Ivan, and Jeanne—struck Florida within six weeks, damaging one in five homes and generating insured losses that exceeded the records set by Andrew. The following year, Hurricane Wilma hammered South Florida. These back-to-back seasons drove another wave of carrier exits and expanded Citizens' footprint, but Universal survived—a fact the company attributes to its reinsurance program and disciplined underwriting.

These back-to-back seasons also highlighted a phenomenon that would recur throughout Universal's history: the gap between initial loss estimates and ultimate loss costs. After a hurricane, the first wave of claims reflects obvious, visible damage—missing roofs, broken windows, flooded interiors. But over the following months and years, supplemental claims emerge: hidden water damage, mold remediation, roof deterioration that wasn't immediately apparent. In Florida's litigious environment, this "claims tail" could extend for years, with each reopened or supplemental claim adding to the ultimate cost. Learning to model, reserve for, and manage this tail became one of Universal's core institutional capabilities.

The experience of 2004-2005 reinforced a lesson that would become central to Universal's identity: in Florida property insurance, survival is the strategy. The carriers that failed in those seasons were not necessarily poorly managed in normal times. They simply did not have the reinsurance coverage, the capital cushion, or the operational resilience to absorb consecutive major events. Universal's willingness to spend heavily on reinsurance—even in quiet years when competitors were cutting costs by reducing coverage—was the strategic choice that differentiated it from the pack.

By the late 2000s, Universal had established itself as one of the leading writers of homeowners insurance in Florida, with a growing agent network and a reputation for paying claims promptly—a differentiator in a market where policyholders had been burned by carriers that contested or delayed payments after storms. The company's vertical integration meant that when a hurricane struck, Universal's own adjusters showed up, assessed damage under Universal's own guidelines, and processed payments through Universal's own systems. There were no handoffs to third-party vendors, no finger-pointing between the carrier and its outsourced claims operation.

This operational control would prove critical in the years ahead, as the Florida insurance market entered a period of unprecedented stress from an entirely unexpected direction: not hurricanes, but lawyers.

V. The Golden Years: Growth and Expansion (2010–2017)

The period from 2010 to 2017 was, for Florida property insurers, something close to paradise. No major hurricanes made landfall in the state. The longest such drought in modern history allowed carriers to accumulate surplus, compound book value, and attract new capital. For Universal, it was a period of aggressive but disciplined growth that transformed the company from a small regional player into Florida's largest private homeowners insurer.

Sean Downes, who became CEO in February 2013, drove the expansion with the methodical intensity of a career claims man who understood, viscerally, what happens when things go wrong. His background was not in finance or strategy—it was in adjusting claims, inspecting damage, and managing the messy reality of paying people after their homes are destroyed. That operational grounding shaped a growth philosophy that was aggressive in volume but conservative in risk selection: Universal would grow fast, but only by writing policies that met its own underwriting standards, not by bulk-importing government pool policies with unknown risk profiles.

Under his leadership, Universal grew its policy count through a network of approximately 9,300 independent agents, expanded into neighboring states—Georgia, South Carolina, North Carolina, and eventually as far north as New York and Massachusetts—and invested in proprietary technology platforms that allowed agents to quote, bind, and issue policies digitally. The company also launched Universal Direct, one of the first online distribution platforms in Florida that allowed consumers to purchase a homeowners policy entirely online—a modest but telling signal that management was thinking about distribution efficiency long before insurtech became a buzzword.

The financial results during this period were exceptional. Return on equity consistently exceeded twenty percent. The company initiated a dividend program and conducted aggressive share buybacks, returning substantial capital to shareholders. On December 3, 2013, Universal moved its listing from NYSE MKT to the New York Stock Exchange, a milestone that Downes described as reflecting "what has been a transformative year for our Company." The stock appreciated significantly as investors recognized the compounding power of a disciplined underwriter operating in a market with limited competition and growing demand.

Downes also strengthened the management bench. Jon Springer, who had reinsurance expertise from Willis Re, was appointed SVP and COO simultaneously with Downes becoming CEO, and later became President and Chief Risk Officer. Kimberly Campos, who had built the company's technology infrastructure, took on the dual role of CIO and Chief Administrative Officer. Frank Wilcox became CFO. This was a management team with deep institutional knowledge—most had been with the company for a decade or more—and their stability provided continuity through the turbulence that would follow.

But beneath the surface, risks were building that even the most sophisticated models could not fully capture. Florida's population continued to grow, with new development concentrated in exactly the coastal areas most exposed to hurricane damage. Construction costs were rising. And most ominously, a legal scheme known as Assignment of Benefits was beginning to metastasize through the state's court system, inflating claims costs in ways that had nothing to do with weather.

In July 2019, Downes transitioned to the role of Executive Chairman, and Stephen Donaghy—who had served as CIO, Chief Administrative Officer, Chief Marketing Officer, and COO in succession since 2006—became CEO. Donaghy's promotion reflected a generational transition and a recognition that the company needed a leader steeped in technology and operations for the challenges ahead. The calm years had been profitable, but they were also deceptive: the absence of major hurricanes masked the structural vulnerabilities that were about to be exposed.

For investors looking back at this period, the key insight is that Universal used the quiet years wisely. Rather than relaxing underwriting standards or chasing growth at the expense of profitability—as several competitors did—the company built surplus, strengthened its reinsurance program, diversified geographically, and invested in the operational infrastructure that would prove essential when the storms returned. The companies that treated the calm as permanent were the ones that did not survive what came next.

VI. Inflection Point #1: Hurricane Irma and The New Reality (2017)

On September 10, 2017, Hurricane Irma made landfall on the Florida Keys as a Category 4 storm, then tracked up the state's west coast, delivering hurricane-force winds to a swath of territory stretching from Naples to Jacksonville. It was the most powerful Atlantic hurricane ever recorded at the time, and for Universal—with its heavily Florida-concentrated portfolio—it represented the first true existential test of the company's reinsurance architecture.

The initial gross loss estimate was staggering: approximately $452 million. For a company with a surplus of roughly $300 million, this would have been a death sentence without reinsurance. But Universal's $2.65 billion reinsurance tower absorbed the blow. The company's net retained loss in the third quarter was approximately $37 million—painful, but manageable. Universal actually reported a net income of $10 million for Q3 2017, and full-year net income of $106.9 million with a return on equity of 25.7 percent.

The stock market initially panicked: Universal's shares dropped sharply as Irma approached Florida. But when the storm took a more westerly track than originally forecast—sparing the densely populated Miami metropolitan area from a direct hit—the stock rebounded roughly fifteen percent in a single session. The market was learning, in real time, the difference between a Florida property insurer with adequate reinsurance and one without.

But the real story of Irma was not the wind damage. It was what happened afterward. Over the following two years, Universal's gross loss estimate for Irma escalated dramatically—from the initial $452 million to over $1 billion by mid-2019, with more than 92,000 total claims received. The company ultimately acknowledged gross losses exceeding $2 billion from the single event.

What drove this explosion was not additional storm damage being discovered. It was Assignment of Benefits abuse and the litigation it spawned. Contractors and public adjusters swarmed damaged neighborhoods, persuading homeowners to sign over their insurance claim rights. The contractors would then perform work—often unnecessary or grossly inflated in cost—and when insurers disputed the charges, attorneys filed lawsuits. Under Florida's one-way attorney fee statute, even a marginal win for the plaintiff required the insurer to pay the claimant's legal fees. This asymmetry turned every disputed claim into a profitable litigation opportunity.

For Universal's management, Irma was a clarifying event. The storm itself was survivable—the reinsurance program worked exactly as designed. But the post-storm litigation environment revealed a systemic vulnerability that no amount of reinsurance could fully address: the legal system itself was being weaponized against insurers, inflating losses far beyond what the actual wind and water had caused.

The strategic response was immediate. Universal began repricing its portfolio aggressively, tightening underwriting standards, and adjusting geographic exposure to reduce concentration in the highest-risk areas. But the company also recognized that the AOB problem was not something it could solve through individual action—it required legislative reform. Universal became one of the most vocal industry advocates for changing Florida's one-way attorney fee statute and restricting the assignment of benefits, a campaign that would take five more years to succeed.

In a small but telling coda, a 2025 civil suit brought by the Florida Attorney General alleged that Universal had backdated approximately one percent of its Irma claims to increase reimbursement from the Florida Hurricane Catastrophe Fund. The company settled for a $4 million fine and withdrew roughly $30 million in disputed Cat Fund reimbursement requests. While the dollar amounts were relatively minor, the episode illustrated the intense pressure that carriers faced in the post-Irma environment—squeezed between escalating litigation costs and the temptation to maximize every available recovery mechanism.

The lesson of Irma, for Universal and for the broader market, was that hurricanes are only half the problem. The other half—arguably the more dangerous half—is the legal and regulatory environment that determines how claims are settled after the wind stops blowing.

VII. Inflection Point #2: The Assignment of Benefits Crisis (2017–2019)

If Hurricane Andrew was the event that reshaped Florida's insurance industry physically, the Assignment of Benefits crisis was the event that nearly destroyed it legally. And understanding the mechanics of this crisis is essential to understanding why so many Florida insurers failed—and why Universal survived.

An Assignment of Benefits, or AOB, is a straightforward legal concept: a policyholder transfers their right to collect insurance proceeds to a third party, typically a contractor performing repairs. In theory, it simplifies the process—the contractor fixes the roof, the insurer pays the contractor directly, and the homeowner avoids the hassle of being a middleman. In practice, it became the engine of one of the most profitable fraud schemes in American insurance history.

Here is how it worked. A water restoration company or roofing contractor would go door-to-door in a Florida neighborhood—sometimes after a storm, sometimes not—offering free inspections. The contractor would identify damage (real or imagined), persuade the homeowner to sign an AOB transferring all claim rights, and then perform work at grossly inflated prices. A typical non-AOB water damage claim might settle for $10,000. AOB claims averaged $32,000—three times the cost.

When the insurer inevitably disputed the inflated charges, the contractor's attorney would file suit. And here is where the one-way attorney fee statute turned the scam into a perpetual motion machine: if the court awarded the contractor even one dollar more than the insurer's pre-suit settlement offer, the insurer had to pay the contractor's attorney fees. If the insurer won, the contractor owed nothing. This "heads I win, tails you lose" asymmetry meant that it was almost always rational for contractors to litigate—and almost always rational for insurers to settle for inflated amounts rather than risk paying both the claim and the opposing attorney's fees.

The scale of the scheme was industrial. Entire business ecosystems emerged around AOB exploitation. Marketing companies generated leads. Contractors performed the work. Attorneys filed the lawsuits. Public adjusters facilitated the assignments. Each player took a cut, and the insurer—and ultimately the policyholder through higher premiums—paid for it all. It was, in the assessment of the Insurance Information Institute, one of the most organized and profitable insurance fraud schemes in American history.

The numbers tell a shocking story. In 2006, there were roughly 405 AOB-related lawsuits in the entire state of Florida. By 2013, that figure had exploded to over 79,000. By 2018, it reached nearly 135,000—a seventy-percent increase in just five years. The geographic concentration was extreme: Miami-Dade, Broward, and Palm Beach counties accounted for 96 percent of AOB water loss claims.

The national comparison was even more damning. According to NAIC data, Florida accounted for just over eight percent of all homeowners insurance claims opened in the United States—but more than seventy-six percent of all homeowners insurance litigation nationwide. Florida's ratio of lawsuits to claims denied was nearly twenty-eight percent, eight times higher than the next worst state, Connecticut, at 3.4 percent. These were not statistics that could be explained by weather alone. They reflected a legal system that had been systematically exploited.

For Universal, the AOB crisis hit the bottom line directly. Claims costs rose sharply even in years with no major hurricanes, compressing margins and forcing repeated rate increase filings with the OIR—which were often delayed or partially denied due to political pressure. The company invested heavily in its legal department, developing litigation strategies to fight fraudulent claims rather than simply settling. Its in-house claims operation through Alder Adjusting (the renamed Universal Adjusting Corporation) gave it an advantage: because Universal's own adjusters assessed damage from day one, the company had stronger documentation to contest inflated claims in court.

But individual company action was not enough. The scale of the problem demanded legislative intervention, and the insurance industry—Universal included—launched a sustained lobbying campaign to reform the AOB statute and the one-way attorney fee provision.

The first partial victory came in 2019, when Governor DeSantis signed HB 7065, which imposed some restrictions on AOB agreements. Citizens Property Insurance reported that premiums dropped for nearly 44,000 policyholders following this reform. A more significant step came with SB 76 in 2021, which reduced the claims filing deadline to two years, banned contractor solicitation through marketing materials, and created a new attorney fee schedule that limited inflated fee awards.

But the decisive blow came in December 2022, when the Florida legislature passed SB 2-A during a special session called by Governor DeSantis. This landmark reform eliminated the one-way attorney fee statute entirely for property insurance claims, prohibited assignment of benefits for any policy issued after January 1, 2023, tightened claims filing deadlines to one year, and reformed the bad faith litigation standard to require an adverse court judgment before a bad faith claim could proceed.

For Universal and the surviving Florida insurers, SB 2-A was the equivalent of a ceasefire in a war of attrition they were slowly losing. The litigation pipeline would take years to drain—existing cases filed before the reform would still proceed under the old rules—but the new framework fundamentally changed the economics of filing fraudulent claims. Without the one-way fee guarantee, the litigation mills that had driven the crisis lost their primary revenue model.

The AOB crisis and its resolution illustrate a broader principle: in regulated industries, the legal and political environment can be as consequential as the physical risks that the business is designed to manage. Universal survived the AOB crisis not because it had superior products or technology, but because it had the operational discipline to manage claims in-house, the financial strength to absorb inflated costs without becoming insolvent, and the strategic patience to advocate for reform while competitors collapsed around it.

VIII. Inflection Point #3: The Reinsurance Market Hardens (2020–2022)

While the AOB crisis was a uniquely Florida problem, the next challenge that confronted Universal was global in scope. Beginning in 2020 and accelerating through 2022, the worldwide reinsurance market underwent one of its most severe contractions in a generation—and for a company that depended on reinsurance as an existential shield, the consequences were immediate and painful.

The causes of the reinsurance hardening were multiple and reinforcing. Since 2017, the global reinsurance industry had absorbed roughly $650 billion in weather-related catastrophe claims, driven by a relentless sequence of major events: Hurricanes Harvey, Irma, and Maria in 2017; Hurricane Michael in 2018; devastating wildfires in California; Hurricane Ida in 2021; and severe convective storms and flooding events across the globe. Each event eroded reinsurer capital, and the cumulative effect was a supply-demand imbalance that the industry had not experienced since the aftermath of Hurricane Andrew.

COVID-era disruptions compounded the problem. Business interruption claims, supply chain inflation driving up replacement costs, and rising interest rates increased the cost of capital from roughly eight percent in 2020 to above eleven percent by early 2023. Alternative capital sources—insurance-linked securities, catastrophe bonds, and sidecars that had poured into the reinsurance market during the preceding soft cycle—pulled back as investors faced "trapped capital" from prior years' losses.

For Universal, the impact was stark. Reinsurance costs, expressed as a percentage of direct premiums earned, climbed from the mid-teens a decade earlier to 36.4 percent by 2021-2022, and peaked at 37.6 percent in the 2022-2023 treaty year. To put this in concrete terms: for every dollar of premium Universal collected from policyholders, nearly thirty-eight cents went directly to reinsurers—before the company paid a single claim, compensated a single agent, or covered a single dollar of overhead.

The strategic dilemma was acute. Universal could pass the higher reinsurance costs to customers through rate increases, but those increases required OIR approval and faced political resistance. It could reduce the scope of its reinsurance coverage, but that would increase the company's net exposure to catastrophic losses—precisely the kind of gamble that had destroyed its competitors. Or it could shrink its portfolio, reducing premium volume to match the available reinsurance capacity, but that would sacrifice the scale economies that kept its expense ratio competitive.

Universal chose a combination of all three approaches, but weighted heavily toward the first. The company filed for substantial rate increases and fought for regulatory approval, arguing that rates that did not reflect the true cost of reinsurance were a path to insolvency. It optimized its reinsurance program, negotiating multi-year contracts to lock in capacity and reduce repricing risk. And it selectively reduced exposure in the riskiest geographic areas, shedding policies in coastal zones where the reinsurance cost per policy exceeded the premium the company could charge.

Meanwhile, the insolvency wave that had begun with smaller carriers accelerated dramatically. In 2022 alone, at least six Florida property insurers were ordered into liquidation: St. Johns Insurance Company in February, Lighthouse Property Insurance in April, Southern Fidelity Insurance in June, Weston Property and Casualty in August, and FedNat Insurance in September—the last falling just days before Hurricane Ian made landfall. United Property and Casualty followed in February 2023 after Hurricane Ian pushed its actual losses to $864 million, far exceeding its $660 million reinsurance tower.

The human toll of these insolvencies was substantial. When an insurer is ordered into liquidation in Florida, its policyholders receive a cancellation notice—typically with thirty to forty-five days to find new coverage. In a market where carrier after carrier was failing, finding replacement coverage was increasingly difficult. Many policyholders were forced to turn to Citizens Property Insurance, which was legally required to offer coverage but at rates that reflected its swelling risk pool.

Each insolvency also created a cascade effect on the remaining carriers. Policyholders from failed carriers flooded into Citizens, which ballooned to more than 1.05 million policies by September 2022—double the count from two years earlier. The Florida Insurance Guaranty Association levied a 0.7 percent assessment on all property and casualty policyholders to cover the claims of insolvent carriers. And the remaining private insurers, Universal among them, faced a shrinking pool of competitors—which was simultaneously a threat (potential assessment obligations if more carriers failed) and an opportunity (pricing power and market share gains as alternatives disappeared).

Universal managed its capital conservatively during this period, suspending share buybacks and retaining more earnings to bolster its surplus. The company also maintained its A.M. Best financial strength rating, a critical signal to both policyholders and reinsurance partners that it remained a viable counterparty.

The reinsurance hardening underscored a structural vulnerability in Universal's business model: the company's single largest cost item—reinsurance—is determined by a global oligopoly of reinsurers over which Universal has limited negotiating leverage. Scale helps at the margin, but a mid-cap Florida insurer is a price-taker in a market dominated by Swiss Re, Munich Re, and a handful of Bermuda-based specialists. This supplier dependency is arguably the most important strategic constraint the company faces, and it is one that no amount of operational excellence can fully mitigate.

IX. Inflection Point #4: Hurricane Ian and The Breaking Point (2022)

On September 28, 2022, Hurricane Ian made landfall near Cayo Costa, Florida, as a Category 4 storm with sustained winds of 150 miles per hour. It crawled across the state, devastating Fort Myers, Cape Coral, Port Charlotte, and much of Southwest Florida before emerging into the Atlantic and making a second landfall in South Carolina. With estimated damages exceeding $112 billion, Ian was one of the costliest hurricanes in American history.

For Universal, the exposure was direct and substantial. The Fort Myers and Cape Coral region—ground zero for Ian's most destructive winds and storm surge—was part of the company's core territory. Within days, claims began flowing in. The initial estimate was eighteen to nineteen thousand claims; the ultimate count reached twenty-seven to thirty thousand.

The company's gross estimated loss from Ian was approximately $1 billion—a figure that would have been catastrophic without reinsurance. But Universal's $3 billion reinsurance tower, structured through multiple layers of private reinsurance, the Florida Hurricane Catastrophe Fund, and a catastrophe bond, absorbed the blow. The net catastrophe loss, after reinsurance recoveries, was approximately $36.4 million before taxes. Universal reported a net loss of $72 million for the third quarter—driven by Ian—but bounced back with a $25.1 million net profit in the fourth quarter.

The contrast with United Property and Casualty, a similarly named but very different company, was instructive and haunting. UPC had estimated its Ian losses at $660 million, within its reinsurance capacity. But when actual losses spiraled to $864 million—a two-hundred-million-dollar miss that breached the tower—the company was forced into insolvency in February 2023. Its policyholders were left scrambling for coverage. The difference between survival and failure was not a matter of luck or geography—both companies wrote in the same Florida markets, served similar customers, and faced the same storm. It was a matter of reinsurance adequacy: the thickness of the protective shield that management had chosen to purchase in advance. Universal had paid more for more coverage, and that decision—which might have seemed like an unnecessary expense in calm years—proved to be worth every penny when Ian made landfall.

HCI Group, another publicly traded Florida property insurer, reported a Q3 2022 net loss of $51.1 million but survived with its reinsurance intact. Heritage Insurance Holdings posted a $48.2 million quarterly loss but also remained solvent. The pattern was clear: carriers with adequate reinsurance towers weathered Ian; those without them did not.

Ian accelerated the competitive consolidation that had been underway for years. With FedNat already gone and UPC now joining it, the number of viable private-market alternatives for Florida homeowners had shrunk to a handful: Universal, Heritage Insurance Holdings, HCI Group, and a smattering of smaller carriers. Citizens Property Insurance, despite its mandate as insurer of last resort, was growing so rapidly that it represented a systemic risk to the state—every policy Citizens wrote was ultimately backstopped by assessments on all Florida policyholders.

For Universal, the post-Ian landscape presented a paradox. The company had just absorbed a billion-dollar gross loss and reported its first annual net loss since the financial crisis. But the competitive environment had never been more favorable. With fewer carriers competing for policies, pricing power increased dramatically. Policyholders who had been with carriers that went insolvent needed new coverage immediately, and Universal—with its intact reinsurance program, its A.M. Best rating, and its established agent network—was one of the few places they could turn.

The Florida legislature, galvanized by Ian's destruction and the insolvency crisis, responded with the emergency reforms of SB 2-A in December 2022. In addition to eliminating the one-way attorney fee and AOB provisions discussed earlier, the legislation created the Florida Optional Reinsurance Assistance program, which provided up to $1 billion in state-backed reinsurance at near-market rates—a direct response to the reinsurance cost crisis that was squeezing private carriers. The law also required Citizens to gradually bring its rates closer to actuarial soundness, making the state-backed insurer less artificially competitive with private carriers and facilitating the depopulation of its swollen portfolio.

For long-term investors, Ian and its aftermath crystallized the survivor economics at the heart of Universal's investment thesis. In a market where competitors were being eliminated by a combination of catastrophic losses, litigation abuse, and reinsurance costs, each exit widened the moat for the survivors. Universal's ability to absorb a billion-dollar gross loss, report a modest net loss for the year, and return to profitability the following quarter demonstrated both the resilience of its reinsurance program and the operational discipline that had been built over two decades.

X. The Modern Era: Strategic Repositioning (2023–Present)

The years following Hurricane Ian have been transformative for Universal Insurance Holdings. Freed from the twin burdens of AOB litigation abuse and a collapsing competitive field, the company has entered a phase of selective growth, geographic diversification, and financial performance that would have seemed improbable during the dark days of 2022.

The financial trajectory tells the story. In 2023, Universal returned to profitability with $66.8 million in net income on $1.39 billion in revenue, a combined ratio of 103.6 percent, and book value per share growth of 24.4 percent. The combined ratio was still slightly above breakeven, reflecting the lingering effects of prior-year reserves and the slow drainage of the pre-reform litigation pipeline. But the trend was unmistakably positive.

The year 2024 brought three landfalling hurricanes—Debby, Helene, and Milton—which compressed full-year net income to $58.9 million and pushed the Q4 combined ratio to 107.9 percent. But crucially, Universal's reinsurance program absorbed the impact without threatening solvency, and the company demonstrated that it could sustain profitability even in an active hurricane season.

Then came 2025—a breakout year by any measure. Benefiting from a benign hurricane season, the full effects of tort reform flowing through the loss ratio, and continued rate adequacy, Universal reported net income of $183 million, earnings per share of $6.32, and a Q4 combined ratio of 87.5 percent. The adjusted return on common equity hit 50.9 percent in the fourth quarter and 30.6 percent for the third quarter. Book value per share surged to $19.67, up 48 percent year-over-year.

These are not the financials of a company merely surviving. They are the financials of a company compounding value at an exceptional rate, benefiting from the structural advantages that come with being one of the last credible private-market players in an essential, demand-inelastic market.

Geographic diversification has accelerated meaningfully. Universal now operates in nineteen states, with 34 percent of policies and 48 percent of insured value originating outside Florida. In the fourth quarter of 2025, direct premiums written from non-Florida states grew 18.2 percent year-over-year, while Florida premiums declined 3.1 percent—a deliberate rebalancing that reduces the company's dependence on a single hurricane-exposed state. The expansion into states like New York, Pennsylvania, Massachusetts, and Minnesota provides premium diversification and, importantly, reduces the correlation between Universal's overall portfolio and any single catastrophic event.

On the reinsurance front, costs have moderated from their 2022-2023 peak of 37.6 percent of direct earned premiums to approximately 33 percent for the current treaty year—still elevated by historical standards, but meaningfully improved. For the 2025-2026 program, Universal secured a combined reinsurance tower of $2.526 billion for a single all-states event, with $352 million of multi-year coverage extending through 2026-2027. Management reported that ninety percent of the first-event catastrophe tower for the 2026 program was already placed as of the fourth quarter of 2025.

The Citizens Property Insurance depopulation has been a major structural tailwind. From a peak of approximately 1.4 million policies in October 2023, Citizens' portfolio has shrunk to roughly 385,000 policies by early 2026—a decline of more than seventy percent. In 2025 alone, more than 546,000 policies were transferred to private insurers. Universal has participated in recent depopulation rounds, absorbing policies at pricing that reflects the new, reform-era loss environment. With Citizens now recommending rate cuts for most policyholders, the glide path toward a smaller, less market-distorting state insurer appears durable.

The competitive landscape has stabilized. Heritage Insurance Holdings, HCI Group, and a handful of smaller carriers remain active in Florida, and fifteen new property insurers have entered the state since the legislative reforms. But the barriers to entry remain formidable: capital requirements, regulatory approval processes, the cost and complexity of securing reinsurance, and the institutional knowledge required to underwrite hurricane risk effectively. Universal's scale—the largest private homeowners insurer in Florida with approximately ten percent market share and over 800,000 policyholders—provides advantages in reinsurance negotiation, technology investment amortization, and regulatory relationships that are difficult for new entrants to replicate.

The monthly weighted average renewal retention rate for 2025 reached 92.5 percent—an all-time high—indicating that policyholders who have coverage with Universal are choosing to stay. In a market with limited alternatives and recent memories of carrier insolvencies, the value of a stable, rated insurer with a demonstrated track record of paying claims is difficult to overstate.

Capital allocation has shifted back toward shareholder returns. In January 2026, the board authorized a new $20 million share repurchase program, and the quarterly dividend of $0.16 per share (with periodic special dividends) provides a current yield of approximately 2.4 percent. With book value compounding at nearly fifty percent annually and the stock trading at roughly 1.7 times book value and 5.4 times 2025 earnings, the capital deployment math is increasingly favorable.

The management transition from Downes to Donaghy has also matured. Donaghy, who became CEO in July 2019, has now led the company through three of its most challenging years—the peak of the AOB crisis, Hurricane Ian, and the reinsurance hardening—and emerged with the company in its strongest financial position in history. His background in technology and operations has been reflected in the company's investments in claims automation, digital distribution, and data analytics. Downes, as Executive Chairman, provides continuity and strategic oversight while allowing Donaghy to drive day-to-day execution. This leadership structure—an operational CEO backed by a founding-era chairman—has provided both fresh energy and institutional memory during a period of extraordinary industry transformation.

XI. The Business Model Deep Dive

Universal's business model is best understood as a vertically integrated system optimized for a single purpose: writing profitable homeowners insurance in catastrophe-exposed markets while surviving the inevitable bad years.

At the top of the value chain sits underwriting—the art and science of selecting which risks to insure and at what price. Universal's underwriting philosophy is built on granular risk assessment: roof age and material, construction type, proximity to the coast, property value, historical claims frequency in the specific zip code, and the building code era under which the structure was built. Florida's statewide building code, adopted after Hurricane Andrew and significantly strengthened over subsequent updates, creates a meaningful actuarial divide between pre-2002 and post-2002 construction. Homes built to modern code standards sustain far less damage in hurricanes, and Universal's pricing reflects this distinction.

The reinsurance tower is the company's most critical strategic asset. It functions like a multi-layered shield: Universal retains the first layer of losses (its "retention"), then transfers subsequent layers to private reinsurers, the Florida Hurricane Catastrophe Fund, and catastrophe bond investors, up to a contractual maximum. For the current program year, the tower covers approximately $2.5 billion in losses from a single event. The design philosophy is conservative: the tower is sized to absorb a loss well in excess of the company's probable maximum loss from a worst-case hurricane scenario. This over-engineering is deliberate—it is the margin of safety that allowed Universal to survive Irma and Ian when competitors with thinner towers did not.

Distribution operates through two channels. The primary channel is approximately 9,300 independent agents who sell Universal policies alongside offerings from other carriers. The agent network provides geographic reach, local market knowledge, and a trusted point of contact for policyholders—particularly valuable in a state where insurance shopping is driven more by availability and claims reputation than by brand awareness. The secondary channel is Universal Direct, the company's online platform that allows consumers to purchase policies without an agent intermediary. While direct distribution offers better unit economics (no agent commission), it remains a small share of the overall book.

Claims handling is where Universal's vertical integration pays the greatest dividends. Through Alder Adjusting, the company controls the entire claims process from first notice of loss through final payment. In-house adjusters inspect damage, estimate repair costs, and process payments under consistent guidelines. This is not merely an efficiency play—it is a strategic defense against the kind of claims inflation that the AOB crisis demonstrated. When a homeowner files a claim with Universal, the company's own employee assesses the damage before any contractor is involved. This front-end control reduces the opportunity for inflated estimates and provides stronger documentation if a claim is later disputed.

The investment portfolio is managed conservatively, primarily in high-quality fixed income securities. Unlike property-casualty companies that use investment returns to subsidize underwriting losses, Universal's management has consistently emphasized underwriting profitability as the primary driver of returns. The investment portfolio generates supplemental income from the float, but it is not relied upon to offset combined ratios above one hundred percent—a discipline that distinguishes Universal from carriers that chased yield in riskier asset classes.

Customer economics are driven by retention. Acquiring a new homeowners policy—through agent commissions, marketing, and underwriting costs—is significantly more expensive than renewing an existing one. Universal's 92.5 percent retention rate means that once a policyholder is acquired, the company typically retains them for over a decade. In a market where availability is constrained and switching requires finding another carrier willing to write the risk, the friction of switching acts as a natural retention mechanism—though Universal's claims service reputation also plays a role.

The unit economics of a profitable policy illustrate why disciplined underwriting matters so much. A typical Florida homeowners policy might generate annual premium of $2,000 to $4,000. Of that, roughly a third goes to reinsurance, another fifteen to twenty percent to agent commissions and acquisition costs, and fifteen to twenty percent to operating expenses. What remains—perhaps thirty to forty cents of every premium dollar—must cover claims. In a normal year, attritional losses (non-hurricane claims like fires, water damage, and theft) might consume twenty to thirty percent of premiums, leaving a modest underwriting margin. But in a hurricane year, a single event can generate claims costs that exceed the entire annual premium multiple times over. The reinsurance tower absorbs this spike, but only if the tower was adequately sized and funded in advance.

What makes this business difficult to disrupt from the outside? The answer lies in the intersection of regulatory complexity, catastrophe risk management, and local expertise. Writing homeowners insurance in Florida requires OIR approval for rates, forms, and operations. It requires access to the Florida Hurricane Catastrophe Fund and relationships with global reinsurers. It requires decades of proprietary loss data to calibrate actuarial models. And it requires operational capabilities to handle twenty thousand or more claims simultaneously when a hurricane strikes. A technology startup with superior user experience but no reinsurance relationships, no regulatory track record, and no catastrophe modeling expertise cannot simply enter this market and compete on cost or convenience.

XII. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding Universal's competitive position requires examining both the structural forces that shape the Florida property insurance market and the sources of durable advantage—or vulnerability—that the company possesses.

Competitive Rivalry in the Florida homeowners market has shifted dramatically over the past five years. What was once an intensely competitive market with dozens of carriers fighting for share has consolidated into an oligopoly of survivors. Universal, Heritage, HCI Group, and a handful of smaller carriers compete against each other and against Citizens Property Insurance. While fifteen new entrants have arrived since the legislative reforms, most are small and building portfolios cautiously. Price competition is structurally limited by the OIR rate approval process—carriers cannot simply undercut each other with below-cost pricing because rates must be actuarially justified. Differentiation occurs primarily through claims service, agent relationships, and availability rather than price alone.

The threat of new entrants is low and declining. The capital required to enter the Florida property market is substantial—not just statutory surplus requirements, but the working capital needed to purchase a reinsurance tower that can absorb a billion-dollar-plus hurricane loss. The insolvency wave of 2021-2023 has chilled investor appetite for Florida property insurance startups. Existing players benefit from decades of proprietary loss data, established reinsurance relationships, and regulatory approval track records that new entrants cannot replicate quickly.

Supplier power—specifically reinsurance—is the most significant strategic constraint in Universal's business model. The global reinsurance market is dominated by a small number of large players, and Florida catastrophe risk is one of the most concentrated and expensive exposures to reinsure. Universal's scale provides some negotiating leverage, but it is fundamentally a price-taker in this market. The 2022-2023 reinsurance hardening, which pushed costs from the mid-teens to nearly thirty-eight percent of premiums, demonstrated how quickly supplier power can compress margins. The creation of the Florida Optional Reinsurance Assistance program and the Florida Hurricane Catastrophe Fund partially mitigate this dependency, but private reinsurance remains the dominant cost driver.

Buyer power is moderate and unusual. Florida homeowners are required to carry property insurance as a condition of their mortgage—creating inelastic demand at the aggregate level. But at the individual level, switching costs are low: homeowners policies are annual contracts, and agents can shop multiple carriers. The constraint on buyer power is availability rather than stickiness: in many Florida markets, there are so few carriers willing to write coverage that the homeowner has limited practical alternatives, even though theoretical switching costs are minimal.

Substitutes are limited. Citizens Property Insurance is the primary alternative for homeowners who cannot obtain private coverage, but Citizens is deliberately priced at or above private market rates (per the SB 2-A reforms) and carries the stigma of assessment risk. Self-insurance is an option only for the wealthiest homeowners with no mortgage. The ultimate substitute—selling a home and relocating out of hurricane-exposed areas—is a growing phenomenon, as insurance costs increasingly factor into real estate purchase decisions, but this is a slow-moving trend rather than an immediate competitive threat.

Turning to Hamilton Helmer's Seven Powers framework, Universal's competitive advantages crystallize around three pillars.

Process Power is the company's strongest source of durable advantage. Two decades of writing homeowners insurance exclusively in hurricane-exposed states has produced embedded operational knowledge that permeates every function: underwriting guidelines calibrated to Florida-specific perils, claims handling procedures refined through multiple major hurricanes, regulatory navigation skills honed through years of OIR filings, and reinsurance structuring expertise that has been tested by billion-dollar-loss events. This process knowledge is organizational rather than individual—it is embedded in systems, procedures, and institutional memory rather than residing in any single executive's expertise.

Cornered Resource provides a secondary advantage. Universal possesses proprietary loss data spanning more than twenty-five years of Florida homeowners experience, including granular information on how specific construction types, roof materials, building code eras, and geographic locations perform during hurricanes. This data is the raw input for actuarial models that determine pricing accuracy—and pricing accuracy is the single most important determinant of long-term profitability in property insurance. Regulatory relationships—the track record of rate filings, the established communication channels with OIR, the credibility built through years of compliant operations—constitute another cornered resource that new entrants cannot easily acquire.

Scale Economies provide moderate advantages. Spreading fixed costs—technology platforms, compliance infrastructure, executive management—across a larger premium base improves the expense ratio. Larger premium volume also provides somewhat better leverage in reinsurance negotiations, though this effect is limited given the power dynamics of the global reinsurance market. The most meaningful scale benefit is risk pooling: a larger, more geographically diverse portfolio produces more stable loss ratios than a concentrated one, reducing earnings volatility and capital requirements.

The remaining four powers—Network Effects, Counter-Positioning, Switching Costs, and Branding—provide minimal competitive advantage. Insurance is not a network effects business; counter-positioning opportunities are limited in a well-understood industry; switching costs for policyholders are low; and while Universal has moderate brand recognition in Florida, brand is not a primary purchase driver for homeowners insurance.

The synthesis: Universal's competitive position is built primarily on process power and cornered resources, reinforced by moderate scale advantages. Its greatest vulnerability is supplier power from the reinsurance market—a force that management can manage but cannot control.

XIII. Bull vs. Bear Case

The Bull Case

The investment thesis for Universal Insurance Holdings rests on three pillars: survivor economics, reform tailwinds, and valuation.

The survivor economics argument is straightforward. The insolvency of more than fifteen Florida property insurers between 2020 and 2023 eliminated a substantial share of the private market capacity. Universal, as the largest surviving private homeowners insurer in Florida, is a primary beneficiary of this consolidation. Policy retention at 92.5 percent indicates that existing customers are not leaving, and the depopulation of Citizens—from 1.4 million policies to roughly 385,000—provides a runway for incremental policy growth at actuarially sound pricing.

The reform tailwinds are significant and still in early innings. The elimination of one-way attorney fees and AOB abuse through SB 2-A fundamentally changed the loss ratio trajectory for Florida property insurers. Property claims lawsuits have declined substantially since the reform took effect, and the Florida property insurance market posted its first underwriting profit since 2016, according to A.M. Best. The litigation pipeline from pre-reform cases is still draining, meaning the full financial benefit of the reforms has not yet been reflected in Universal's loss ratios. As this tail liability diminishes over the next two to three years, the loss ratio should continue to improve, all else equal.

The valuation argument is compelling for those who believe the current earnings trajectory is sustainable. At a stock price of roughly $34 and 2025 earnings per share of $6.32, Universal trades at approximately 5.4 times earnings—a substantial discount to the broader property-casualty insurance sector. Book value per share of $19.67, growing at 48 percent year-over-year, provides a margin of safety. The dividend yield of approximately 2.4 percent, combined with a $20 million share repurchase authorization, suggests that management sees value in the stock at current levels.

Additional bull case catalysts include Florida's continued population growth (despite climate risks, the state added more than 300,000 residents annually in recent years), the expansion into nineteen states providing diversification and growth optionality, and the potential moderation of reinsurance costs as capital returns to the catastrophe reinsurance market.

The Bear Case

The bear case centers on the irreducible physical risk of writing property insurance in the path of Atlantic hurricanes—and the structural challenges that no amount of operational discipline can fully mitigate.

Climate change is the existential concern. Climate models project an increase in the frequency of Category 4 and 5 hurricanes, with a geographic shift toward the Gulf of Mexico and Florida peninsula. Sea-level rise amplifies storm surge damage even from weaker systems, and projected increases of 25 to 47 percent in storm surge heights by late century would dramatically increase loss severity in coastal areas. A single Hurricane Ian-scale event can consume a billion dollars of gross losses; a sequence of two or more major hurricanes in a single season could overwhelm even Universal's robust reinsurance tower.

Reinsurance cost risk is structural and ongoing. While costs have moderated from their 2022-2023 peak, they remain elevated by historical standards at approximately 33 percent of direct premiums earned. If catastrophe losses accelerate—whether from hurricanes, wildfires, or other perils—reinsurance costs could re-escalate rapidly. Universal has limited leverage in negotiations with the global reinsurance oligopoly, and there is no guarantee that the Florida Hurricane Catastrophe Fund or the FORA program will continue to provide below-market coverage indefinitely.

Regulatory and political risk is ever-present. While the current reform framework is favorable, Florida's political environment can shift. Pressure to cap rates below actuarially adequate levels, expand Citizens' mandate, or impose new regulatory burdens on private carriers could re-emerge, particularly if insurance costs become a salient political issue during election cycles.

Concentration risk remains meaningful despite diversification efforts. Seventy-two percent of 2025 direct premiums written still originated in Florida, and the company's brand, expertise, and competitive advantages are overwhelmingly Florida-centric. Expansion into other states, while strategically sound, places Universal in markets where it lacks the institutional advantages it enjoys in Florida and where it competes against larger, better-established carriers.

Finally, the sustainability of the Florida coastal property insurance model itself is uncertain. If insurance costs continue to rise—driven by climate risk, reinsurance costs, and regulatory mandates—they will increasingly affect property values in hurricane-exposed areas. At some point, the insurance cost burden could trigger a structural decline in coastal Florida real estate demand, reducing the addressable market for Universal's core product. The question of whether private insurance can remain available and affordable in hurricane country over the next two to three decades is one that neither Universal's management nor any analyst can answer with confidence.

Key Metrics to Watch

For investors tracking Universal's ongoing performance, two metrics matter above all others.

First, the combined ratio. This single number—the sum of the loss ratio and expense ratio—captures whether Universal is making money on underwriting. A combined ratio consistently below 100 percent indicates profitable underwriting; above 100 percent, the company is relying on investment income and reserve releases to generate returns. The 2025 Q4 combined ratio of 87.5 percent was exceptional, but hurricane-year quarters like Q4 2024 at 107.9 percent illustrate the volatility. The long-term average combined ratio, smoothed across hurricane and non-hurricane years, is the best indicator of the business's true earning power.

Second, reinsurance cost as a percentage of direct premiums earned. This metric captures Universal's largest and most volatile cost input—and the one over which management has the least control. The trajectory from 37.6 percent at peak to approximately 33 percent currently represents a meaningful margin improvement, but any reversal would compress earnings significantly. Monitoring this ratio provides early warning of shifts in the global catastrophe reinsurance market that directly affect Universal's profitability.

XIV. Lessons for Founders and Investors

Universal Insurance Holdings is not a venture-backed technology company, and its story does not follow the familiar Silicon Valley narrative arc of disruptive innovation, exponential growth, and winner-take-all dynamics. But it offers lessons that are arguably more durable—because they are drawn from a business that operates under constraints that most technology companies never face: irreducible physical risk, regulatory oversight, and supplier dependency.

Tail risk management is a competitive advantage, not just a compliance exercise. Universal's willingness to spend thirty-plus percent of premiums on reinsurance—even in calm years when competitors were cutting reinsurance costs to boost short-term profits—was the single most important strategic decision in the company's history. The carriers that went insolvent during Hurricane Ian did not fail because they were worse at customer service or technology. They failed because they had thinner reinsurance towers. In any business exposed to low-probability, high-impact events—from insurance to venture capital to supply chain management—the willingness to pay for protection when it seems unnecessary is what separates survivors from casualties.

Regulatory complexity can be a moat, not just a cost. Most entrepreneurs view regulation as an obstacle. Universal's experience suggests a different framing: in markets where regulatory compliance requires specialized expertise, institutional relationships, and years of track record, the regulatory burden itself becomes a barrier to entry that protects incumbents. Universal's history of OIR filings, its established relationships with regulators, and its demonstrated ability to navigate rate approvals constitute a cornered resource that new entrants cannot replicate with capital alone.

Survivor economics can generate exceptional returns. When competitors exit a market—whether through insolvency, strategic withdrawal, or regulatory pressure—the survivors inherit pricing power, market share, and customer flow that can dramatically improve returns on capital. Universal's 2025 financial performance—a fifty percent return on equity in the fourth quarter—is not the result of a brilliant new product or a disruptive innovation. It is the mathematical consequence of being one of the few remaining providers of an essential, demand-inelastic service in a market where supply has contracted sharply.

Capital allocation discipline matters most when it is hardest to practice. Universal suspended share buybacks and retained earnings during the 2021-2022 crisis, when the temptation to signal confidence through continued capital returns must have been strong. The decision to prioritize surplus preservation over shareholder distributions ensured that the company maintained its financial strength ratings and its access to reinsurance capacity—the two things that mattered most during the darkest period. Now that conditions have improved, the company has resumed buybacks and dividends from a position of strength rather than desperation.

Specialization is a double-edged sword. Universal's Florida expertise is its greatest asset and its greatest liability. The deep institutional knowledge of Florida hurricane risk, the established agent network, the regulatory relationships—these cannot be easily replicated. But they also create concentration risk that geographic diversification can only partially mitigate. The lesson is not that specialization is bad, but that specialists must be honest about the risks of concentration and manage them accordingly—through reinsurance, through diversification, and through conservative capital management.

Know what you cannot control. Universal cannot control hurricanes, climate change, or the global reinsurance market. It can control underwriting discipline, claims handling quality, regulatory compliance, and capital allocation. The company's long-term success has come from maximizing its performance on the variables it controls while building resilience against the variables it does not. This is a useful principle for any business operating in an environment with significant external risk factors.

XV. Epilogue: The Future of Florida Property Insurance

The fundamental question hanging over Universal Insurance Holdings—and the entire Florida property insurance market—is whether the current model is sustainable over the next two to three decades as climate change intensifies hurricane risk, sea levels rise, and coastal development continues.

The data so far is encouraging. Florida experienced just a one-percent average homeowners rate increase in 2024—the smallest in the nation and the lowest since 2019. Since January 2024, seventeen companies have filed for rate decreases and thirty-four have requested no increase, collectively affecting approximately 3.4 million homeowners. The state's personal property insurance market posted its first underwriting profit since 2016. These are concrete, measurable improvements that suggest the reforms are working as intended.

The optimistic scenario points to these structural reforms as proof that the political system can respond to market failures. The elimination of AOB abuse and one-way attorney fees has already produced measurable results: declining litigation, the first underwriting profit since 2016, fifteen new market entrants, and the successful depopulation of Citizens from 1.4 million policies to under 400,000. If these reforms hold—and if the Florida legislature resists future pressure to roll them back—the private market may continue to function with acceptable, if volatile, returns.

Technology offers additional reasons for optimism. Catastrophe modeling has advanced enormously since the days when Hurricane Andrew caught the industry off guard. High-resolution satellite imagery, machine learning algorithms, and real-time weather data allow insurers to model hurricane risk at the individual property level with a precision that was unimaginable a generation ago. Faster claims processing through automation reduces both costs and the opportunity for fraud. And emerging products like parametric insurance—which pays a predetermined amount based on measurable trigger events like wind speed rather than assessed damage—could reduce the claims disputes and litigation that have plagued the traditional model.

The pessimistic scenario focuses on the physics. Climate models project that the proportion of intense hurricanes will increase, and sea-level rise will amplify storm surge damage regardless of wind speed. If a major hurricane strikes the Tampa Bay metropolitan area—one of the most flood-vulnerable large cities in the world, and one that has not experienced a direct hit from a major hurricane since 1921—the losses could dwarf those from Hurricane Ian. A two-hundred-billion-dollar insured loss event would test the reinsurance tower of every Florida carrier, the capacity of the Florida Hurricane Catastrophe Fund, and the financial viability of Citizens Property Insurance simultaneously.

There is also the compounding problem of NFIP Risk Rating 2.0, which FEMA fully implemented in April 2023. Under the new methodology, flood insurance premiums are now based on individual property-specific risk rather than generalized flood zone categories. Roughly eighty percent of Florida NFIP policyholders will see increases, with nine percent eventually facing premium hikes of more than three hundred percent. When combined with rising windstorm insurance costs, the total cost of insuring a Florida coastal home is approaching levels that materially affect property values and purchase decisions. Some real estate markets are already seeing the effects: homes in high-risk coastal areas take longer to sell, and buyers are factoring insurance costs into their offering prices in ways they never did before.

At some point, the question becomes whether private insurance can remain available and affordable for Florida coastal properties—or whether the state will need a federal backstop, analogous to the National Flood Insurance Program, to ensure coverage availability. The concept of a national catastrophe insurance fund has been debated for years but faces political obstacles: states with low catastrophe exposure see no reason to subsidize Florida's hurricane risk. The alternative—managed retreat from the most vulnerable coastal areas—is politically unthinkable in a state that derives much of its economic vitality from coastal development.

Universal Insurance Holdings is positioned as well as any company can be for this uncertain future. Its reinsurance program is robust, its geographic diversification is accelerating, its regulatory relationships are deep, and its operational capabilities have been tested by multiple major hurricanes. Management has demonstrated the ability to navigate existential threats—from Hurricane Irma to the AOB crisis to Hurricane Ian—and emerge stronger each time.

But the honest assessment is that Universal's long-term trajectory depends on variables that no management team can control: the frequency and intensity of Atlantic hurricanes, the trajectory of global reinsurance costs, and the political durability of Florida's tort reforms. The company's history demonstrates that disciplined operators can survive and even thrive in the most hostile insurance environment in the United States. Whether that environment remains insurable at all, over the long term, is a question that only time—and the Atlantic hurricane seasons yet to come—can answer.

XVI. Key Metrics Summary

For ongoing monitoring of Universal Insurance Holdings, investors should focus on:

- Combined Ratio (target: sub-100% on a multi-year smoothed basis) — the definitive measure of underwriting profitability, capturing both loss experience and operational efficiency in a single number

- Reinsurance Cost as Percentage of Direct Premiums Earned (current: ~33%) — the company's largest and most volatile cost input, determined by forces largely outside management's control

These two numbers, tracked quarterly and smoothed across hurricane and non-hurricane years, provide the clearest signal of Universal's fundamental earning power and the sustainability of its business model.

XVII. Further Reading and Resources

Essential Sources:

-