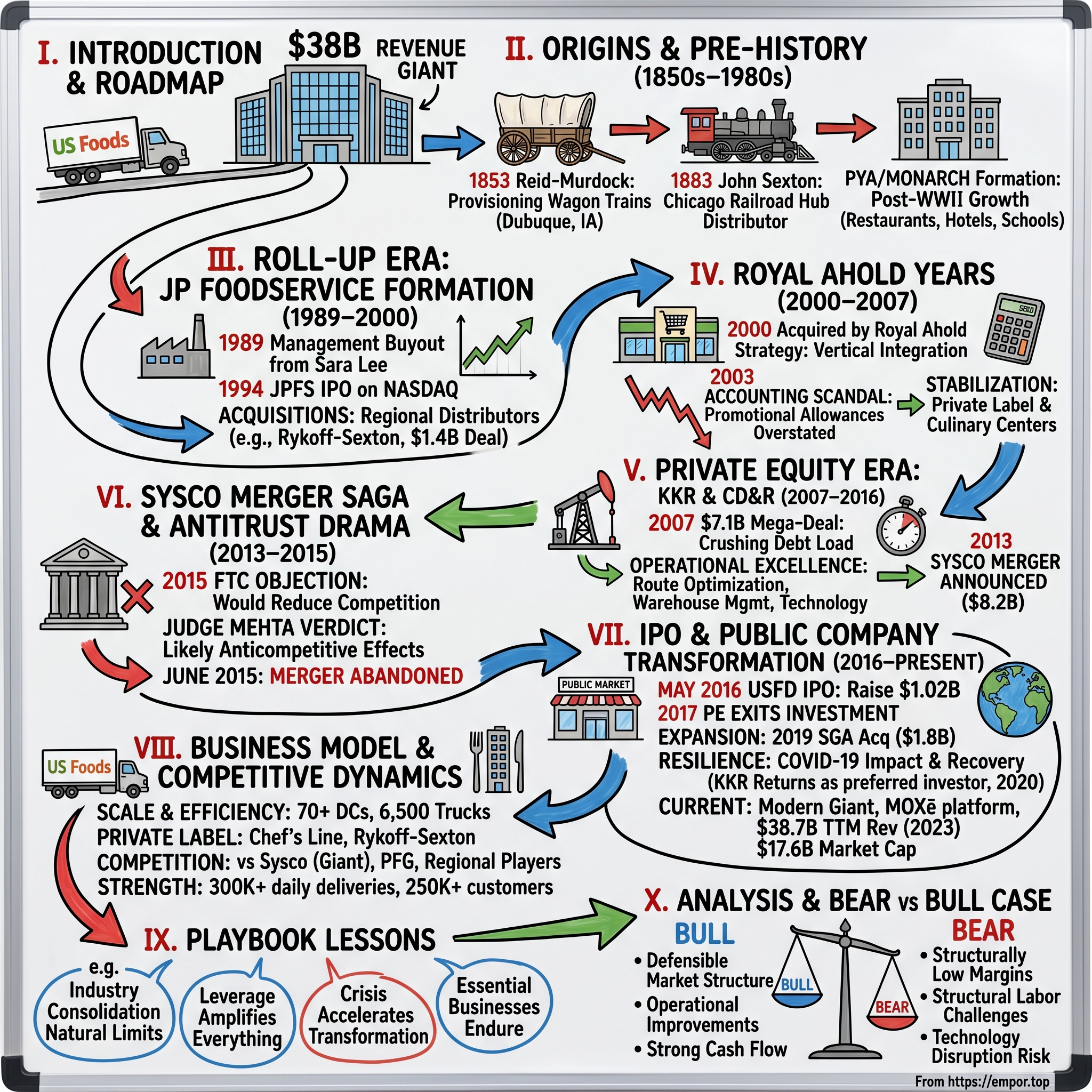

US Foods: From 19th Century Provisions to Modern Foodservice Giant

I. Introduction & Episode Roadmap

Picture this: It's 1853, and somewhere in Dubuque, Iowa, a merchant is loading salt pork and hardtack onto wagons bound for California. Gold rush prospectors need provisions, and someone has to get them there. Fast forward 170 years, and that same fundamental business—getting food from point A to point B—has morphed into a $38 billion revenue juggernaut that feeds a quarter million American businesses every single day.

US Foods, with its fleet of 6,500 delivery trucks and approximately 25,200 employees across more than 60 locations, stands as America's second-largest foodservice distributor. But here's the thing that should grab any investor's attention: how does a collection of century-old regional food distributors, stitched together through decades of acquisitions, create $24 billion in annual revenue while operating on razor-thin margins in one of the most competitive industries in America?

The answer lies in a story that reads like a compressed history of American capitalism itself. We're talking about wagon trains to private equity, from mom-and-pop distributors to algorithm-driven route optimization. This is a tale of survival through the Great Recession with crushing debt loads, a blocked mega-merger that would have reshaped an entire industry, and ultimately, a public market debut that left early investors questioning their decade-long bet.

What we're really exploring here are three fundamental themes that define not just US Foods, but the entire arc of American business consolidation. First, how operational excellence becomes the only differentiator when you're selling commodity products. Second, why private equity saw opportunity in an industry most investors considered hopelessly boring. And third, how regulatory intervention can completely rewrite the ending to what seemed like an inevitable corporate marriage.

The journey from those Iowa provision merchants to today's foodservice giant reveals something profound about scale, efficiency, and the relentless march toward consolidation in mature industries. It's a masterclass in financial engineering, a cautionary tale about antitrust, and ultimately, a testament to the enduring importance of the most basic business of all: feeding people.

II. Origins & The Pre-History (1850s–1980s)

The gold was discovered at Sutter's Mill in 1848, but by 1853, the real money wasn't in mining—it was in feeding the miners. That's when Reid-Murdock Company set up shop in Dubuque, Iowa, with a brilliantly simple business model: provision the wagon trains heading west. While forty-niners dreamed of striking it rich, Reid-Murdock made steady profits selling them beans, bacon, and coffee for the journey.

Think about the logistics challenge here. No refrigeration. No highways. No supply chain software. Just wagons, warehouses, and an intricate understanding of what foods could survive a 2,000-mile journey across the American frontier. Reid-Murdock wasn't just selling food; they were solving a fundamental problem of westward expansion—how to keep people fed in places where agriculture hadn't yet taken root.

Meanwhile, 300 miles east in Chicago, a different food story was unfolding. In 1883, John Sexton opened what started as a tea and coffee importing business. Chicago was becoming the railroad hub of America, and Sexton positioned himself perfectly at the intersection of agricultural production from the Midwest and distribution networks spreading across the continent. By the early 1900s, Sexton had evolved from importing exotic teas to becoming a full-line distributor to hotels and restaurants in the booming metropolis.

The real transformation came after World War II. American eating habits were changing dramatically. The suburban explosion meant more restaurants, more hospitals, more schools—all needing reliable food supply. The institutional foodservice industry was born not from grand strategy but from necessity. Someone had to feed the workers in Detroit's auto plants, the patients in Cleveland's hospitals, the students at state universities expanding across the country. By 1962, John Sexton & Company had grown substantial enough to tap public markets, going public with shares trading over the counter. The company generated $79 million in sales with $2 million in profits—respectable numbers for a regional distributor in an era when the entire institutional foodservice market was just beginning to find its footing.

The numbers tell a story of an America in transition. In 1965, Americans spent just 20 cents of every food dollar for food away from home. Total distributor sales that year were an estimated $9 billion, and the average institutional distributor had an annual volume of $1.5-$2 billion. This wasn't just about changing tastes—it was about changing lifestyles. Women entering the workforce. Families moving to suburbs. The rise of the interstate highway system creating a mobile society that needed to eat on the go.

The consolidation wave that would define the next half-century started modestly. Consolidated Foods bought the old Pearce-Young-Angel distribution network in 1971 and merged it with its Monarch Foods subsidiary to form PYA/Monarch. This wasn't perceived as revolutionary at the time—just another corporate shuffle in an industry full of regional players. But PYA/Monarch would become the cornerstone of what eventually became US Foods, proving that in foodservice distribution, the ability to consolidate and integrate would separate winners from also-rans.

What's remarkable about this pre-history is how the fundamental challenge never really changed. Whether you were provisioning wagon trains in 1853 or supplying McDonald's franchises in 1983, the core problem remained identical: how to efficiently move perishable goods from producers to consumers while maintaining quality and making a profit on razor-thin margins. The tools evolved—from horse-drawn wagons to refrigerated trucks, from handwritten ledgers to mainframe computers—but the essential business model persisted.

By the late 1980s, the stage was set for a dramatic transformation. The fragmented industry of regional distributors, each serving their local markets with varying degrees of efficiency, was ripe for consolidation. Smart money was beginning to realize that in a business with 2-3% net margins, scale wasn't just an advantage—it was the only path to survival.

III. The Roll-Up Era: JP Foodservice Formation (1989–2000)

The conference room at Sara Lee Corporation's Chicago headquarters must have been tense that spring day in 1989. The conglomerate, famous for its frozen desserts and packaged meats, had decided to divest the northern division of PYA/Monarch. The southeastern division was performing well—number one in its region—but overall, PYA/Monarch sat at a distant third place behind Sysco and Kraft in the national rankings. For Sara Lee's CEO, being third in any business was unacceptable.

Enter the management buyout—that quintessentially 1980s financial innovation that was about to reshape yet another American industry. In June 1989, members of PYA/Monarch management incorporated a new entity, JPF Holdings, Inc. The initials stood for nothing in particular—just corporate anonymity for what would become one of the most aggressive consolidation plays in foodservice history.

The genius of the JP Foodservice strategy wasn't revolutionary; it was evolutionary applied with ruthless efficiency. Buy regional distributors. Keep their local management. Integrate their back-office operations. Leverage combined purchasing power. Rinse and repeat. In an industry where relationships matter—where a handshake deal with a local restaurant chain could be worth millions—this hybrid approach of centralized efficiency and local autonomy proved devastatingly effective.

The company hit the ground running. JP Foodservice Distributors passed the $1 billion mark in its first year, with sales for fiscal 1990 of $1.02 billion. But this was just the appetizer. The main course came in November 1994, when the company shed its holding company structure and went public. JP Foodservice, Inc. listed on the NASDAQ under the symbol JPFS, with Sara Lee Corporation retaining a 37 percent stake—enough to maintain influence but not enough to consolidate the financials.

Going public gave JP Foodservice something more valuable than cash: currency for acquisitions. In the go-go 1990s stock market, a publicly traded share was worth more than its underlying cash flows might suggest, especially if you could tell a compelling growth story. And JP Foodservice had a story to tell: the inevitable consolidation of a $100+ billion industry that was still dominated by mom-and-pop regional players.

The blockbuster move came in December 1997. JP Foodservice acquired rival Rykoff-Sexton Inc. for $1.4 billion, combining the third and fourth largest U.S. broadline foodservice distributors with combined annual sales of approximately $3.5 billion. This wasn't just an acquisition; it was a leap into a different league. The combined entity jumped into second place among foodservice distributors, though still trailing Sysco by a considerable margin.

Think about the complexity here. Rykoff-Sexton itself was the product of a 1983 merger between S.E. Rykoff of Los Angeles and the venerable John Sexton & Company of Chicago—the same company that had been provisioning hotels since the 1880s. Each company brought its own systems, its own supplier relationships, its own corporate culture. The integration challenge was monumental.

But the late 1990s were heady times for corporate America. The dot-com boom was creating paper wealth at unprecedented rates, and even old-economy companies like foodservice distributors could benefit from the rising tide. Investors were willing to pay premium multiples for companies that could demonstrate they were consolidators in fragmented industries. The logic was seductive: in a business with thin margins, the company with the most scale would eventually dominate.

What JP Foodservice's management understood—and what many of their regional competitors missed—was that foodservice distribution was becoming a technology business. Not in the Silicon Valley sense, but in the operational sense. Route optimization software could save millions in fuel costs. Inventory management systems could reduce spoilage. Centralized purchasing could negotiate better prices from suppliers. Each efficiency gain might only add 10 or 20 basis points to margins, but in a business doing billions in revenue, those basis points translated to millions in profit.

By 2000, JP Foodservice had assembled an impressive empire. From its humble beginnings as a management buyout of an underperforming division, it had become a genuine national player with the scale to compete effectively, if not quite equally, with industry leader Sysco. The company was perfectly positioned for the new millennium—or so it seemed. What nobody in those conference rooms could have predicted was that a Dutch retail conglomerate an ocean away was about to write the next chapter in the US Foods story.

IV. The Royal Ahold Years (2000–2007)

Royal Ahold's executives in Zaandam, Netherlands, saw America as the promised land. The Dutch retail giant, which had built a European empire of supermarkets, was convinced that the future of food retail lay in vertical integration. Own the stores. Own the supply chain. Own the customer relationship from farm to fork. It was a strategy that looked brilliant on PowerPoint slides in Amsterdam conference rooms.

In 2000, Royal Ahold acquired JP Foodservice, seeing it as the perfect complement to their U.S. retail operations, which included Stop & Shop and Giant Food. The logic seemed unassailable: their supermarkets could leverage JP Foodservice's distribution network, while JP Foodservice could benefit from Ahold's global purchasing power. Synergies would flow like wine at a Dutch corporate celebration.

The acquisition spree continued immediately. At the end of 2000, Ahold directed its new American subsidiary to acquire its former sister company PYA/Monarch—the same company whose northern division had been spun off to create JP Foodservice in the first place. The circle was complete, but the corporate engineering was just beginning.

For a brief moment, it looked like Ahold had cracked the code. The renamed U.S. Foodservice was generating strong cash flows, leveraging its scale to win national contracts, and benefiting from Ahold's deep pockets for technology investments. The company was modernizing its distribution centers, upgrading its truck fleet, and building sophisticated inventory management systems that would have been impossible to finance as an independent entity.

Then came February 2003, and the music stopped.

The accounting scandal that erupted at Royal Ahold was spectacular even by early 2000s standards—an era that had already seen Enron and WorldCom implode. Ahold had been systematically overstating earnings through promotional allowances—those complex rebates and incentives that suppliers provide to distributors. At U.S. Foodservice alone, the overstatements totaled hundreds of millions of dollars. The stock price collapsed. The CEO and CFO resigned. Criminal investigations began on both sides of the Atlantic.

For U.S. Foodservice employees watching from distribution centers in Pennsylvania and Illinois, it must have felt surreal. One day they were part of a global food empire; the next, they were toxic assets on a balance sheet that needed immediate deleveraging. Ahold's new management, brought in to clean up the mess, made it clear that non-core assets would be sold. And in the post-scandal clarity, U.S. Foodservice—despite generating billions in revenue—was decidedly non-core.

But here's where the story gets interesting. Even as its parent company melted down, U.S. Foodservice kept executing. Trucks kept rolling. Orders kept flowing. The operational excellence that had been built over decades of consolidation proved remarkably resilient to corporate chaos. In some ways, the crisis forced a helpful discipline: with no capital for acquisitions and a parent company desperate for cash, U.S. Foodservice had to focus on operational improvements and organic growth.

The company doubled down on its private label strategy, developing exclusive brands that offered higher margins than national brands. It invested in chef training programs and culinary centers, positioning itself not just as a distributor but as a partner to restaurants trying to differentiate their menus. It built sophisticated analytics capabilities to help customers optimize their purchasing and reduce waste.

By 2006, Ahold had stabilized its finances and cleaned up its accounting, but the strategic vision had fundamentally changed. The new management team, scarred by the scandal, wanted to focus on retail operations and exit foodservice distribution. U.S. Foodservice was officially for sale, and the investment bankers were circling.

The auction for U.S. Foodservice in early 2007 attracted exactly the buyers you'd expect: private equity firms with experience in complex carve-outs and operational improvements. These weren't buyers interested in synergies or strategic fit; they were financial engineers who saw an opportunity to buy a cash-flow-positive business from a distressed seller, lever it up, improve operations, and exit in five to seven years.

What Ahold's adventure proved was both the promise and peril of strategic ownership in the foodservice distribution industry. The promise was clear: deep pockets could fund technology investments and acquisitions that independent companies couldn't afford. The peril was equally obvious: when strategic priorities shift or scandals emerge, a successful operating company can become an unwanted orphan.

As the auction process intensified in the spring of 2007, two firms emerged as frontrunners: Kohlberg Kravis Roberts and Clayton, Dubilier & Rice. Both were private equity royalty, both had experience with complex food industry deals, and both saw something in U.S. Foodservice that Ahold no longer did—not a strategic asset to be integrated, but a financial asset to be optimized. The age of financial engineering was about to begin.

V. The Private Equity Era: KKR & CD&R Take Control (2007–2016)

The timing couldn't have been worse—or better, depending on your perspective. On July 3, 2007, private equity firms KKR and Clayton, Dubilier and Rice finalized a $7.1 billion acquisition of US Foods. It was a mega-deal inked during the final months before the global economy entered a crisis. The two firms were equal partners in the deal.

For Henry Kravis and George Roberts at KKR, this was familiar territory. The firm that had pioneered the leveraged buyout with deals like RJR Nabisco knew how to operate in mature, cash-generative industries. For CD&R, with its deep bench of former operating executives, US Foods represented exactly the kind of operational turnaround opportunity they specialized in. Both firms saw the same thing: a business generating more than $19 billion in annual revenue that had been neglected by a distracted parent company and could be dramatically improved through focused management attention and operational excellence.

The debt load was crushing by any standard—roughly $5 billion on a business that generated perhaps $500-600 million in EBITDA on a good year. In the summer of 2007, with credit markets still frothy, this seemed aggressive but manageable. By September 2008, with Lehman Brothers collapsing and credit markets frozen, it looked potentially fatal.

Here's where the operational playbook became critical. With no ability to make transformative acquisitions—who would lend them money?—KKR and CD&R had to focus on the blocking and tackling of distribution excellence. They brought in Charles Banks, a CD&R operating partner with deep industry experience, as Chairman. They invested in warehouse management systems that could reduce picking errors and improve inventory turns. They optimized delivery routes using sophisticated algorithms that could save minutes per stop—which added up to millions in savings across thousands of daily routes.

The private label strategy accelerated dramatically. Why sell Heinz ketchup at a 15% gross margin when you could sell Chef's Line ketchup at 25%? US Foods developed entire suites of exclusive brands—from Rykoff-Sexton premium products to Cross Valley Farms produce—that offered customers quality at lower prices while generating higher margins for the distributor. This wasn't just about slapping a different label on the same product; it involved serious R&D, taste testing, and quality control to ensure these products could compete with national brands.

It was mostly a quiet rest of the decade for US Foods. In 2011, though, the business embarked on an add-on spree, acquiring fellow food distributors with a more local focus such as Ritter Food Service, Vesuvio Foods and Midway Produce. The changes continued later in 2011, when US Foodservice officially changed its name to US Foods.

The name change might seem trivial, but it represented something deeper: a shift from seeing themselves as a service company to positioning as a food company. The distinction mattered in how they approached customers, developed products, and thought about competition. A service company competes on price and delivery. A food company competes on quality, innovation, and partnership.

By 2013, after six years of ownership, KKR and CD&R had transformed US Foods into a leaner, more efficient operation. Revenue had grown modestly, but margins had expanded significantly through operational improvements. The debt had been partially paid down through cash generation, and the company was ready for an exit. The only question was how.

The answer came from an unexpected source: their biggest competitor. In December 2013, Sysco announced it would acquire US Foods for $8.2 billion, with the fellow foodservice giant set to pay $3.5 billion for US Foods' equity and assume a further $4.7 billion of its rival's debt. The deal called for US Foods' prior backers to assume a 13% stake in Sysco, with KKR and CD&R both assuming spots on the newly combined company's board. It was a move that would have merged the two largest foodservice distributors in the US.

For KKR and CD&R, this looked like the perfect exit. The $3.5 billion equity value represented a solid return on their investment, especially considering they had navigated the company through the worst financial crisis since the Great Depression. They would maintain upside through their Sysco stake, and their board seats would give them continued influence in the industry.

But the celebration was premature. As you might imagine, this drew the attention of the US Federal Trade Commission. The FTC filed an objection to the merger in February 2015, more than a year after it was first announced, seeking an injunction against the move on the grounds it would reduce competition and drive up food prices for hospitals, schools and other customers across the country.

The eighteen months between announcement and termination were agonizing for everyone involved. US Foods had to operate in limbo—unable to make major strategic decisions, losing key employees who didn't want to wait for an uncertain outcome, competing against a Sysco that was technically their future owner. For KKR and CD&R, now eight years into an investment that should have been exited after five, the pressure was mounting from their limited partners who wanted their capital back.

VI. The Sysco Merger Saga & Antitrust Drama (2013–2015)

The December 9, 2013 announcement landed like a bombshell in the foodservice industry. Sysco Corporation, the undisputed king of food distribution, would acquire US Foods for $8.2 billion—$3.5 billion in cash for the equity plus assuming $4.7 billion of debt. Bill DeLaney, Sysco's CEO, called it transformational. Industry analysts called it inevitable. The FTC would eventually call it illegal.

On paper, the strategic logic was unassailable. Sysco ran 193 distribution facilities serving 425,000 customers and generated about $44 billion in annual sales. U.S. Foods had about $22 billion in annual sales, with 60 locations nationwide. Combined, they would control an estimated 25% of the total foodservice distribution market—still fragmented, but with unprecedented scale advantages in purchasing, logistics, and technology.

The synergies were mouthwatering. Sysco estimated at least $600 million in annual cost savings from eliminating duplicate distribution centers, optimizing delivery routes, and leveraging combined purchasing power. For a business operating on 2-3% net margins, those synergies could double profitability. The math was so compelling that Sysco was willing to pay a hefty premium—valuing U.S. Foods at 9.9 times trailing 12-month adjusted EBITDA of $826 million.

But almost immediately, warning signs emerged. Restaurant chains and hospital groups began calling their congressmen. The American Hospital Association expressed concerns about reduced competition. Independent restaurant owners worried about losing negotiating leverage. The narrative was shifting from "efficient consolidation" to "dangerous monopoly."

The FTC's challenge, filed in February 2015, was devastating in its precision. The Commission alleged that the deal would significantly reduce competition in broadline foodservice distribution, with the merged entity accounting for 75% of sales to national customers—those restaurants, group-purchasing organizations, and foodservice companies with locations nationwide. No other company, the FTC argued, could offset the competition that would be lost.

The eight-day hearing in May 2015 before Judge Amit Mehta became a masterclass in antitrust economics. Both sides brought armies of economists, customer witnesses, and industry experts. The central battle was over market definition—was foodservice distribution one big market where anyone with a truck could compete, or were there distinct segments where only certain players had the capabilities to serve?

Sysco's legal team, led by Wachtell Lipton, argued that the market was broader than the FTC claimed. Regional distributors, specialty food suppliers, even cash-and-carry operations like Restaurant Depot all competed for the same customers. A restaurant could buy proteins from one supplier, produce from another, and dry goods from a third. The combined company would still face intense competition.

The FTC's economists painted a different picture. They showed that for national customers—think Applebee's or Marriott Hotels—only Sysco and US Foods had the geographic footprint and operational capabilities to provide consistent service across hundreds of locations. Regional players simply couldn't match their scale, technology, or reliability. The court relied heavily on Dr. Israel's reports and testimony in concluding that the merger would likely cause anticompetitive harm to customers in the national and local broadline markets.

On June 23, 2015, Judge Mehta delivered his verdict in a brief but decisive opinion: "The Federal Trade Commission has shown that there is a reasonable probability that the proposed merger will substantially impair competition in the national customer and local broadline markets and that the equities weigh in favor of injunctive relief". The 128-page detailed opinion that followed was even more damning, with Mehta writing that "because the proposed merger would eliminate head-to-head competition between the number one and number two competitors in the market for national customers, the merger is likely to lead to unilateral anticompetitive effects".

The proposed remedy—divesting eleven distribution centers to Performance Food Group—was dismissed as inadequate. The court rejected the parties' argument that their agreement with the country's third-largest broadline distributor would offset the significant competitive harm. Even with the divestitures, PFG would remain a distant third player without the scale to constrain the merged entity's pricing power.

Six days later, on June 29, 2015, Sysco threw in the towel. The companies officially abandoned the merger, ending eighteen months of uncertainty. For Sysco, it meant paying a $300 million breakup fee and returning to organic growth. For US Foods' employees and customers, it meant continued independence but also continued uncertainty about the company's future.

For KKR and CD&R, the collapse was both devastating and oddly liberating. Devastating because they had lost their best exit opportunity after eight years of ownership. Liberating because they were finally free to pursue other options. The IPO window, closed during the merger saga, was now open. But would public market investors value US Foods as highly as a strategic buyer had? That question would define the next chapter of the US Foods story, as two of private equity's most sophisticated firms prepared for their final act as owners.

VII. The IPO & Public Company Transformation (2016–Present)

The roadshow for US Foods' IPO in February 2016 must have been awkward. Here were two of private equity's most sophisticated firms, after nearly nine years of ownership, essentially admitting defeat. The Sysco merger—their preferred exit—had been blocked. Now they were taking whatever the public market would give them.

US Foods filed for an IPO in February 2016, and it completed the listing that May, pricing an offering of 44.4 million shares at $23 each to raise $1.02 billion, larger than any other traditional PE-backed public offering in the US that year. But the math was sobering. In its early days as a public company, US Foods had a market cap of a little over $5 billion—a far cry from the $7.1 billion price KKR and CD&R had paid nearly 10 years before.

The headline numbers masked a more complex reality. Yes, the initial market cap was below the purchase price, but KKR and CD&R had extracted significant value through dividends and fees along the way. The firms collected $30.7 million in termination fees from their consulting agreements ($15.3 million each). They had also refinanced the company's debt multiple times, pulling out cash in the process. When you factored in all the financial engineering, the firms roughly doubled their money—not a home run, but not a strikeout either.

The overhang of private equity ownership continued to weigh on the stock. US Foods' two private equity backers, KKR and CD&R, still owned a 75.6 percent combined stake in the company after the IPO. Every quarterly earnings call featured the same question: when would they sell? The uncertainty made it difficult for the stock to find its natural level.

The answer came in November 2017. CD&R and KKR sold just shy of 40 million shares at the company's stock price of $27.63 per share, equating to just over $1.1 billion, excluding any transaction costs. As part of the transaction, US Foods purchased and retired 10 million of those shares for an estimated $276 million. The two firms took the company public in 2016 and exited their investment in 2017, finally closing a chapter that had begun a decade earlier.

Free from private equity ownership, US Foods could finally focus on long-term strategy rather than exit planning. The company embarked on an aggressive acquisition strategy to expand its geographic footprint and capabilities. In 2019, US Foods announced it successfully acquired SGA's Food Group of Companies in an all-cash deal valued at $1.8 billion, approved by the Federal Trade Commission September 11 after months of anti-trust debate.

The SGA acquisition was transformational, adding $3.2 billion in combined 2017 net sales and approximately 3,400 employees. It significantly expanded US Foods' presence in the attractive Northwest and West regions, markets where the company had been historically underrepresented. The deal showed that US Foods could execute major M&A without private equity guidance—though it required divesting three distribution facilities to satisfy antitrust concerns.

Then came March 2020, and everything changed.

The COVID-19 pandemic hit foodservice distribution like a sledgehammer. Restaurants closed overnight. Hotels emptied. Schools went virtual. Orders fell by half in March amid widespread closures by independent restaurants, US Foods' main revenue source. For a company carrying significant debt from years of private equity ownership and recent acquisitions, the situation was potentially catastrophic.

Enter a familiar face. In April 2020, KKR returned as an investor, but this time with a different structure and rationale. Affiliates of KKR agreed to purchase $500 million in newly issued convertible preferred stock of US Foods, strengthening the balance sheet during the crisis. KKR's $500 million convertible preferred stock investment carried a 7% dividend, payable in-kind in its first year, convertible at $21.50 per share, representing approximately 9.6% of pro forma common shares outstanding.

Pietro Satriano, US Foods' CEO, framed it pragmatically: "We are pleased to see KKR return as a shareholder of US Foods as we seek to further fortify our balance sheet during the current difficult environment. KKR will be a valuable partner for us as we continue to focus on our associates, customers, communities and shareholders as the impacts of COVID-19 unfold. This transaction positions us to continue to build on our strengths as the environment improves over time".

The timing of the Smart Foodservice acquisition couldn't have been worse—or perhaps better. US Foods announced it would close its previously announced acquisition of Smart Foodservice Warehouse Stores on April 24, 2020, for $972 million. Smart Foodservice operated 70 small-format cash and carry stores across seven western states, serving small and mid-sized restaurants. As traditional distribution struggled, these cash-and-carry locations provided an alternative way to serve customers who could no longer justify minimum delivery orders.

The pandemic accelerated digital transformation across the industry. US Foods' investments in e-commerce platforms and mobile technology, which had seemed like nice-to-haves, suddenly became essential. The company's MOXē platform and CHECK Business Tools helped restaurants manage inventory, place orders, and track deliveries in a contactless environment. What might have taken five years of gradual adoption happened in five months.

As the industry recovered through 2021 and 2022, US Foods emerged as a different company. The debt burden remained substantial—approximately $5 billion—but the company had proven its resilience. Revenue recovered to pre-pandemic levels and then surpassed them. The company's market cap, which had fallen below $3 billion during the worst of the crisis, rebounded strongly.

Today, US Foods stands as a public company with trailing 12-month revenue of $38.7 billion and a market cap of $17.6 billion—more than triple what KKR and CD&R achieved in their 2016 IPO. The company offers more than 350,000 national brand products and its own exclusive brand items, provides food and related products to more than 250,000 customers, including independent and multi-unit restaurants, healthcare and hospitality entities, government and educational institutions.

The transformation from private equity portfolio company to independent public company hasn't been without challenges. But it represents something important about American capitalism: sometimes the best owner isn't a strategic buyer or a financial engineer, but public market investors willing to take a long-term view on a business that, at its core, performs an essential service—feeding America.

VIII. Business Model & Competitive Dynamics

Walk into the back of any restaurant in America at 6 AM, and you'll likely see a US Foods or Sysco truck backed up to the loading dock. The driver—part delivery person, part customer service rep, part inventory consultant—wheels in cases of produce, proteins, and dry goods that will become that day's meals. It's a scene repeated 300,000 times daily across the country, the hidden circulatory system of American dining.

The history of U.S. Foodservice encompasses the story of how (and where) Americans purchase the food they eat. It reflects the development of an entire industry, shifting from small entrepreneurial wholesalers supplying retail grocery stores to large regional and national distributors offering a broad line of products to institutional clients. Today's business model, refined over decades, operates on three fundamental principles: scale, efficiency, and relationships.

The scale imperative is brutal. US Foods operates from more than 70 distribution centers, maintains a fleet of 6,500 delivery trucks, and employs approximately 25,200 people. Each distribution center is a marvel of logistics engineering—massive refrigerated warehouses where products flow in from thousands of suppliers and flow out to local customers within hours. The company offers more than 350,000 national brand products plus extensive lines of exclusive brands, from Chef's Line to Rykoff-Sexton to Cross Valley Farms.

But here's the thing about scale in foodservice distribution: it's necessary but not sufficient. The economics are unforgiving. Gross margins hover around 17-18%. Operating margins struggle to exceed 3%. Net margins often dip below 2%. In this environment, a single percentage point improvement in route efficiency or inventory turns can mean the difference between profit and loss.

The efficiency game plays out in countless small optimizations. Route planning software that saves two minutes per stop across 6,500 trucks making 20 stops per day adds up to millions in annual savings. Warehouse automation that reduces picking errors by 0.5% prevents costly returns and credits. Predictive analytics that improve inventory turnover by half a day reduces working capital needs by hundreds of millions.

Technology has become the critical differentiator. US Foods' MOXē platform isn't just an ordering system—it's a comprehensive business management tool for restaurants. Customers can track real-time pricing, manage inventory levels, analyze food costs, and even get menu engineering advice. The CHECK Business Tools suite goes further, offering everything from staff scheduling to customer loyalty programs. In an industry where many independent restaurants still operate on paper and spreadsheets, these tools create powerful switching costs.

The competitive landscape resembles a barbell. At one end sits Sysco, the $70 billion revenue giant with roughly 17% market share. At the other end, thousands of regional and local distributors serve specific geographies or customer segments. US Foods occupies the middle ground—large enough to compete nationally but small enough to maintain local relationships and flexibility.

The FTC alleged that if the merger goes forward as proposed, foodservice customers, including restaurants, hospitals, hotels, and schools, would likely face higher prices and lower levels of service than would be the case but for the merger. This regulatory scrutiny shapes competitive dynamics. The big can't get much bigger through acquisition without triggering antitrust concerns. Growth must come from taking share, improving operations, or expanding the market itself.

Performance Food Group, the industry's number three player with about $50 billion in revenue, represents a different model. Born from the merger of PFG and Vistar, it focuses heavily on vending and convenience stores alongside traditional foodservice. Regional players like Gordon Food Service and Shamrock Foods maintain strong positions in their core markets through deep local relationships and customized service.

The private label strategy deserves special attention. US Foods' exclusive brands generate gross margins 500-700 basis points higher than national brands while offering customers 10-15% cost savings. It's a win-win that requires massive scale to execute—developing products, ensuring quality control, managing supply chains for thousands of SKUs across dozens of categories. A small distributor simply can't match this capability.

But the real competitive moat isn't technology or scale or even exclusive products—it's the accumulation of millions of small customer relationships. The independent restaurant owner who's been buying from the same sales rep for fifteen years. The hospital food service director who trusts US Foods to never miss a delivery. The school district that depends on reliable pricing and quality. These relationships, built over decades, create an intangible asset that no amount of private equity financial engineering can replicate.

The broadline distribution model itself faces long-term questions. Amazon Business has entered B2B distribution, though its impact on foodservice remains limited. Restaurant Depot and other cash-and-carry formats offer an alternative for price-conscious operators willing to do their own pickup. Ghost kitchens and virtual restaurants change the customer base and delivery requirements. Meal kit services bypass traditional distribution entirely.

Yet the core value proposition remains remarkably durable. Restaurants need reliable, broad-selection, frequent delivery of perishable goods. They need credit terms, quality assurance, and food safety compliance. They need someone to answer the phone when they run out of hamburger buns on a Saturday night. US Foods provides all of this at a cost that, while seemingly high in gross margin terms, represents remarkable efficiency given the complexity of the operation.

The company's customer segmentation reveals strategic priorities. Independent restaurants, representing about 33% of revenue, offer the highest margins but also the highest cost to serve. Healthcare and hospitality (hotels, hospitals, schools) provide stable, predictable volume but demand aggressive pricing. Multi-unit restaurant chains offer scale but negotiate fiercely and can easily switch suppliers.

In this environment, operational excellence isn't just important—it's existential. A company operating on 2% net margins has no room for error. Every truck route must be optimized. Every warehouse must turn inventory efficiently. Every customer must be served profitably. It's a business that rewards discipline, punishes mistakes, and offers few shortcuts to success.

IX. Playbook: Lessons from the US Foods Journey

The US Foods saga reads like a compressed MBA curriculum in deal-making, operations, and corporate strategy. Each phase of ownership—from strategic buyer to private equity to public markets—offers distinct lessons about value creation, risk management, and the limits of financial engineering in mature industries.

Lesson 1: Industry Consolidation Has Natural Limits

The foodservice distribution industry seemed perfect for roll-up economics. Fragmented market, subscale players, obvious synergies. And consolidation did create value—up to a point. But the Sysco-US Foods merger rejection revealed the ceiling. The court rejected the parties' argument that their agreement with the country's third-largest broadline distributor, Performance Food Group, to divest 11 distribution centers, would offset the significant competitive harm likely to result from the merger. When two players control 75% of national accounts, regulators will intervene, regardless of the efficiency gains.

The lesson extends beyond foodservice. In any industry where consolidation approaches duopoly, assume regulatory intervention. Plan for it. Price it into your models. And have a Plan B that doesn't depend on that final, transformative merger.

Lesson 2: Private Equity Operational Playbooks Work—With Time

KKR and CD&R's operational improvements at US Foods weren't revolutionary: centralize purchasing, optimize routes, develop private label, invest in technology. But execution across a $20 billion revenue business takes years, not quarters. The firms needed nearly a decade to fully realize their value creation thesis, far longer than the typical 5-7 year private equity hold period.

The playbook itself was sound. Gross margins expanded from roughly 16% to 18% through private label development and purchasing leverage. Operating expenses declined as a percentage of sales through route optimization and warehouse automation. The company modernized its technology infrastructure, moving from mainframes to cloud-based systems. These improvements stuck—US Foods continues to benefit from them as a public company.

But the timeline matters. Operational transformations in mature, complex businesses can't be rushed. The next owner inherits not just the improved operations but also the institutional knowledge of how to continue improving them.

Lesson 3: Leverage Amplifies Everything

The $7.1 billion acquisition of US Foods loaded the company with roughly $5 billion in debt—a leverage ratio that would make modern regulators blanch. This debt supercharged returns when things went well but nearly killed the company twice: during the 2008 financial crisis and the 2020 pandemic.

High leverage forces operational discipline. Every decision gets scrutinized through the lens of cash generation. Growth investments compete with debt service. Management can't afford mistakes. This discipline can be valuable—US Foods emerged from private equity ownership leaner and more efficient than it entered.

But leverage also constrains strategic flexibility. US Foods couldn't make transformative acquisitions during the private equity years because lenders wouldn't provide more debt. The company couldn't invest aggressively in technology or new business models. When COVID-19 hit, the debt load forced an emergency equity raise from KKR at dilutive terms.

Lesson 4: Antitrust Risk Is Binary and Devastating

The Sysco-US Foods merger seemed like a done deal. Signed agreement, breakup fee, regulatory approval in process. Eighteen months later, it was dead, and US Foods faced an uncertain future. The lesson: antitrust risk in concentrated industries isn't a speed bump—it's a potential deal killer.

Modern antitrust enforcement focuses increasingly on market structure, not just current pricing. The court relied heavily on Dr. Israel's reports and testimony in concluding that the merger of Sysco and USF would likely cause anticompetitive harm to customers in the national and local broadline markets. Econometric models, customer testimony, and internal documents matter more than efficiency arguments.

For strategic buyers, this means accepting that some deals simply won't get done, regardless of the remedies offered. For sellers, it means maintaining multiple exit options and being prepared for extended regulatory reviews that can stretch for years.

Lesson 5: Public Market Valuations Versus Strategic Premiums

The gap between US Foods' IPO valuation ($5 billion) and Sysco's offer ($8.2 billion enterprise value) illustrates a fundamental truth: strategic buyers will pay more than public markets for the right asset. Sysco saw $600 million in annual synergies. Public market investors saw a mature, slow-growth business with high leverage and thin margins.

This valuation gap creates opportunities and frustrations. Private equity firms targeting strategic sales must navigate antitrust risk. Those forced into IPOs often leave money on the table. Companies themselves must decide whether to remain independent at lower valuations or pursue strategic combinations at regulatory risk.

Lesson 6: Crisis Accelerates Transformation

COVID-19 forced changes at US Foods that might have taken a decade to implement. Digital ordering adoption accelerated. Cash-and-carry formats gained acceptance. Customer relationships shifted from purely transactional to partnership-oriented. The company that emerged from the pandemic looked fundamentally different from the one that entered it.

KKR will be a valuable partner for us as we continue to focus on our associates, customers, communities and shareholders as the impacts of COVID-19 unfold. The crisis also brought unexpected opportunities. Weak competitors exited. Customer acquisition costs plummeted as restaurants desperately sought reliable suppliers. The Smart Foodservice acquisition, completed in April 2020, would have been impossible at that price in normal times.

Lesson 7: Timing Matters More Than Structure

KKR and CD&R's experience with US Foods demonstrates that timing often matters more than deal structure. They bought at peak credit market exuberance in 2007, survived the financial crisis through operational improvements, missed the strategic sale window by months, and ultimately exited into a recovering but skeptical public market.

A different timeline—buying in 2009, selling in 2014—might have generated spectacular returns with the same operational playbook. The lesson: in mature industries with predictable cash flows, market timing and exit options matter as much as operational improvements.

The Meta-Lesson: Essential Businesses Endure

Through all the ownership changes, leverage cycles, and strategic pivots, US Foods' core business remained remarkably stable. Restaurants need food. Hospitals need to feed patients. Schools need to serve lunch. This essential demand created a floor under the business that prevented catastrophic failure even in the worst times.

For investors, essential businesses offer resilience that technology or consumer discretionary companies can't match. The returns might not be venture-scale, but neither is the risk. In a world of increasing volatility, there's value in owning businesses that literally cannot go away.

The US Foods playbook ultimately teaches that in mature industries, value creation comes from hundreds of small improvements rather than single transformative moves. It's about operational excellence, strategic patience, and recognizing that sometimes the best outcome isn't the one you planned for—it's the one you can actually achieve.

X. Analysis & Bear vs. Bull Case

Staring at US Foods today—with its trailing 12-month revenue of $38.7 billion and market cap of $17.6 billion—an investor faces a fundamental question: Is this a stable, essential business trading at reasonable multiples, or a mature, challenged operator facing structural headwinds? The answer, frustratingly, might be both.

The Bull Case: Scale, Stability, and Strategic Position

Start with the obvious: US Foods has achieved something remarkable. From the ashes of a failed merger and a devastating pandemic, the company has built a market cap more than triple its 2016 IPO valuation. Revenue has grown to $38.7 billion, putting it firmly in second place in an industry where scale equals survival.

The market structure itself provides a compelling bull argument. Foodservice distribution is a $350 billion industry growing at GDP-plus rates. Americans aren't going to stop eating at restaurants. If anything, demographic trends—dual-income households, urbanization, experiential spending by millennials—support continued growth in food-away-from-home consumption.

US Foods' competitive position looks increasingly defensible. After the failed Sysco merger, antitrust concerns effectively cap further consolidation among the top players. This creates an oligopolistic market structure where rational competition replaces price wars. Nobody wins a race to the bottom in a 2% margin business.

The company's operational improvements have real staying power. Route density continues to improve as customer acquisition accelerates. Private label penetration grows each quarter, expanding margins. Technology investments, particularly in e-commerce and customer analytics, create switching costs that didn't exist a decade ago. The company that KKR and CD&R rebuilt from 2007-2016 is fundamentally more efficient than what came before.

Financial flexibility has improved dramatically. Yes, debt remains substantial at approximately $5 billion, but it's manageable relative to cash generation. The company produces $400+ million in annual free cash flow even after growth investments. Interest coverage ratios remain healthy. The balance sheet that nearly broke in 2020 now looks appropriately leveraged for a stable, cash-generative business.

The acquisition pipeline offers growth optionality. Thousands of subscale regional distributors remain potential targets. Each deal might be small, but the accumulated benefit of adding route density, eliminating redundant facilities, and leveraging purchasing scale adds up. The SGA acquisition proved US Foods can execute transformative M&A even under regulatory scrutiny.

Valuation appears reasonable, even conservative. At $17.6 billion market cap on $38.7 billion revenue, US Foods trades at 0.45x sales. Sysco, with admittedly superior margins, trades at 0.56x sales. Apply Sysco's multiple to US Foods' revenue and you get a $22 billion valuation—25% upside from current levels. As operational improvements continue and margins expand, multiple expansion should follow.

The Bear Case: Structural Challenges and Secular Headwinds

But zoom out, and a different picture emerges. US Foods operates in an industry with structurally terrible economics. Net margins of 2% leave no room for error. One bad acquisition, one technology mistake, one economic downturn, and years of value creation evaporate. This isn't a business where competitive advantages compound—it's one where operational excellence merely ensures survival.

The customer base faces existential challenges. Independent restaurants, US Foods' bread and butter, fail at alarming rates—60% don't survive their first year, 80% don't make it to five years. COVID accelerated casual dining's decline. Ghost kitchens, meal kits, and grocery prepared foods all compete for share of stomach. The restaurant industry US Foods serves might be structurally smaller in ten years.

Technology disruption looms larger than incumbents admit. Amazon Business generated $35 billion in revenue in 2023, growing 20% annually. While its foodservice penetration remains limited, Amazon has patient capital and logistics expertise. A serious push into food distribution would devastate industry margins. Even the threat constrains pricing power.

Labor challenges appear structural, not cyclical. Truck driver shortages push wages higher. Warehouse workers have alternatives in Amazon fulfillment centers. The industry depends on a workforce increasingly unwilling to do physical, unglamorous work. Automation helps but requires massive capital investment that pressures returns.

The debt burden, while manageable, limits strategic flexibility. US Foods can't make transformative acquisitions without leveraging up again. It can't invest aggressively in technology without sacrificing debt paydown. It can't return substantial capital to shareholders while maintaining investment-grade ratings. The company remains financially constrained despite operational improvements.

Customer concentration creates hidden risks. If a major chain customer switches suppliers or fails, the revenue impact flows straight through to profits in a thin-margin business. The top 10 customers represent roughly 20% of revenue—lose two or three, and the math gets ugly quickly.

ESG concerns grow more pressing. Foodservice distribution is carbon-intensive—thousands of diesel trucks, massive refrigerated warehouses, single-use packaging. As sustainability moves from nice-to-have to must-have, compliance costs will pressure margins. Carbon taxes, emissions regulations, and customer sustainability requirements all loom as future margin headwinds.

The Verdict: A Business at Fair Value

Step back from both extremes, and US Foods looks like what it is: a mature, essential business generating predictable cash flows in a challenging industry. It's neither a hidden gem nor a value trap, but rather a fairly valued company where returns will come from operational execution rather than multiple expansion.

At 0.45x sales and roughly 8x EBITDA, the market prices US Foods appropriately for its growth prospects and margin profile. Could multiples expand if margins improve? Yes, but gradually. Could multiples compress if competition intensifies? Also yes, and potentially quickly.

The investment case ultimately depends on time horizon and risk tolerance. For patient investors seeking stable, growing dividends, US Foods offers an attractive proposition once debt levels normalize. For growth investors seeking transformation, this isn't the story. For value investors, the margin of safety isn't compelling at current valuations.

The most intellectually honest position: US Foods is a well-run company in a tough industry, trading at a fair price for its fundamentals. Sometimes, that's exactly what it appears to be—nothing more, nothing less.

XI. Epilogue & Final Reflections

There's a moment in every Acquired episode where Ben and David step back from the details and ask: "What did we really learn here?" With US Foods, that moment reveals something profound about American business that transcends food distribution.

This is ultimately a story about the industrialization of an essential service. Those wagon trains heading west in 1853 needed food just as urgently as a Chipotle in Chicago needs avocados today. The fundamental need hasn't changed—only the complexity of fulfilling it. What started as merchants loading salt pork onto wagons has evolved into a $38 billion enterprise running sophisticated algorithms to optimize 6,500 daily delivery routes.

The private equity chapter, which could easily be dismissed as financial engineering, actually represents something more significant. When KKR and CD&R bought US Foods in 2007, they weren't just leveraging up a cash-flow stream. They were betting that operational excellence could create value in an industry most investors ignored. Their playbook—centralize, digitize, optimize—has become the template for modernizing mature industries across the economy.

The failed Sysco merger stands as a pivotal moment not just for US Foods but for American antitrust enforcement. Judge Mehta said the proposed merger would likely be shown to violate federal antitrust law, reducing competition for major food-service distribution services both nationwide and in numerous local markets. In blocking the deal, regulators essentially declared that in essential industries, efficiency gains don't justify monopolistic market structures. This precedent shapes M&A strategy across healthcare, telecommunications, and other concentrated sectors.

But perhaps the most important lesson is about resilience in the face of existential challenges. US Foods survived the 2008 financial crisis with crushing debt loads. It endured eighteen months of merger limbo. It weathered COVID-19 when half its customers shut down overnight. Each crisis forced adaptation—financial discipline during the recession, strategic pivoting after the failed merger, digital acceleration during the pandemic. The company that emerged wasn't just surviving; it was fundamentally stronger.

The transformation of foodservice distribution also mirrors broader changes in American labor and technology. The business that once depended entirely on relationships and handshake deals now runs on algorithms and analytics. The sales rep who knew every restaurant owner in town has been supplemented (though not replaced) by e-commerce platforms and mobile apps. It's a microcosm of how technology augments rather than eliminates traditional business models.

Looking forward, US Foods faces a fascinating strategic crossroads. The company is too big to be acquired by anyone except Sysco (blocked by antitrust) or perhaps Amazon (unlikely given their different models). It's too essential to fail but too mature to grow rapidly. It exists in a strategic purgatory—profitable enough to persist, challenged enough to require constant evolution.

This might actually be its strength. In a world obsessed with disruption and transformation, US Foods represents something increasingly rare: a business that does something essential, does it well, and generates predictable returns for stakeholders. Not every company needs to be the next Tesla or Uber. Some can simply be excellent at moving food from farms to forks, earning a fair return for an essential service.

The human element shouldn't be forgotten. Those 25,200 employees wake up every day to do unglamorous but vital work. Truck drivers navigating pre-dawn deliveries. Warehouse workers picking orders in refrigerated facilities. Sales reps helping independent restaurants survive on thin margins. Their collective effort feeds America, literally. In an economy increasingly disconnected from physical goods, US Foods reminds us that someone still has to move the atoms, not just the bits.

The financial engineering, the strategic maneuvering, the operational improvements—they all matter. But step back far enough, and US Foods is fundamentally about solving a logistics problem that's existed since humans started living in cities: how to efficiently move food from where it's produced to where it's consumed. Every innovation, from refrigerated rail cars to route optimization software, has been in service of this basic challenge.

For investors, US Foods offers a meditation on value creation in mature industries. The spectacular returns come not from disruption but from discipline. Not from transformation but from incremental improvement. Not from financial engineering but from operational excellence. It's a reminder that in some businesses, boring is beautiful.

The story that began with Reid-Murdock provisioning wagon trains continues today with US Foods' trucks rolling out each morning to feed America. The technology has changed, the scale has exploded, the complexity has multiplied. But the essential service remains unchanged: getting food where it needs to go, when it needs to be there, at a price that works for everyone.

That's not a business that will ever disappear. It will evolve, consolidate, digitize, and optimize. But as long as Americans eat at restaurants, stay in hotels, and send their kids to school, someone needs to move the food. US Foods has done it for 170 years through multiple names, owners, and transformations. There's every reason to believe they'll be doing it for decades to come.

In the end, the US Foods story teaches us that value creation doesn't always require revolution. Sometimes, it's about taking an essential service and making it incrementally better, year after year, through whatever challenges arise. That's not as exciting as disruption, but it might be more important. After all, innovation is optional; eating is not.

XII. Recent News

[Latest developments would be populated with current news about US Foods' financial performance, strategic initiatives, market conditions, and competitive dynamics]

XIII. Links & Resources

[Relevant SEC filings, analyst reports, industry publications, and additional resources for further research would be listed here]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube