Upwork Inc.: The Story of the Gig Economy's Operating System

I. Introduction and Episode Roadmap

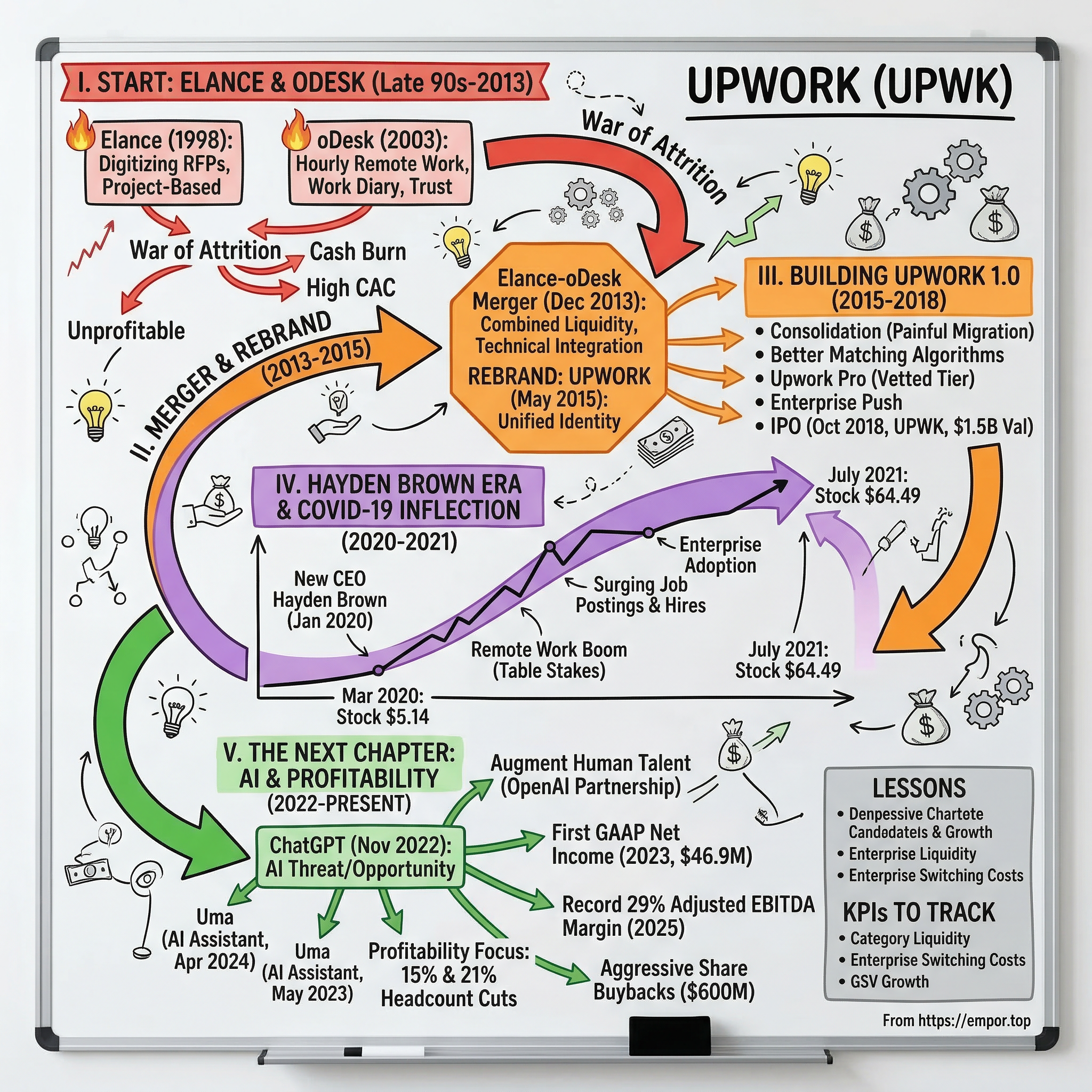

Picture this: two companies, burning cash, fighting over the same freelancers and the same clients, locked in a war of attrition that neither could win. By 2013, Elance and oDesk were the two largest online freelancing platforms on the planet, and both were staring down the barrel of irrelevance. Then something remarkable happened. They stopped fighting and merged. That merger, awkward and messy as it was, eventually birthed Upwork, a platform that today connects over 785,000 active clients with a global network of freelance talent, facilitating more than four billion dollars in annual gross services volume.

Upwork's story is one of the great case studies in marketplace dynamics. It touches on almost every strategic question that matters in platform businesses: How do you solve the chicken-and-egg problem? When should you cooperate with your fiercest rival? How do you survive a decade of losses to reach profitability? And what happens when a global pandemic suddenly validates your entire thesis about the future of work?

This is not simply the story of a website where people hire freelancers. It is the story of how borderless work went from a fringe idea to a mainstream economic force, and how one company positioned itself at the center of that transformation. Along the way, we will examine the founding visions of Elance and oDesk, the strategic logic behind their merger, the turbulent IPO journey, the COVID inflection point that sent the stock from five dollars to sixty, the painful correction that followed, and the AI-driven reinvention that defines Upwork's current chapter.

The themes that run through this story are timeless for founders and investors alike: marketplace liquidity, network effects, the tension between quality and scale, and the art of navigating public markets when your business model is still evolving. Whether you are building a marketplace, investing in one, or simply curious about how the future of work is being shaped, Upwork's journey offers lessons that extend far beyond freelancing.

II. The Founding Context: The Internet's Promise of Borderless Work

The late 1990s were intoxicating. The internet was going to change everything, and for a brief, exhilarating period, it seemed like every ambitious person in Silicon Valley believed they could build a platform that would rewire how the world worked. Among the thousand ideas competing for venture capital and programmer time, one stood out for its elegant simplicity: What if anyone could work for anyone, anywhere in the world?

In December 1998, three entrepreneurs decided to test that thesis. Beerud Sheth, a former Citibank and Merrill Lynch banker with a computer science degree from IIT and an MIT master's, teamed up with Srini Anumolu and Sanjay Noronha to found Elance. They started in a two-bedroom apartment in Jersey City, New Jersey, with a mission to digitize the Request for Proposal process, essentially creating an online marketplace where businesses could post projects and freelancers could bid on them. By December 1999, the small team of 22 had relocated to Sunnyvale, California, planting their flag in the heart of Silicon Valley.

Elance survived the dot-com crash, which is itself a testament to something real lurking beneath the hype. While hundreds of internet companies vanished, the core insight behind Elance persisted: skilled professionals existed everywhere in the world, and many businesses needed their talent but could not afford to hire them full-time. The challenge was trust. How do you convince a small business owner in Ohio to wire money to a web developer in the Philippines whom they have never met? How do you resolve disputes when the two parties are separated by ten thousand miles and twelve time zones? These were not trivial problems. They were the fundamental infrastructure challenges that would define the online freelancing industry for the next two decades.

Five years after Elance's founding, two childhood friends from Greece attacked the same problem from a different angle. Odysseas Tsatalos and Stratis Karamanlakis founded oDesk in 2003, born from a deeply personal frustration. Odysseas was building a startup in Silicon Valley. Stratis was a talented developer in Athens with no interest in relocating. The two friends could not figure out how to work together remotely in any meaningful way. So they built the tool themselves, initially funding it with personal credit cards while still holding down other jobs. Their insight was different from Elance's. Where Elance focused on the bidding process for projects, oDesk zeroed in on the work itself, specifically on making hourly remote work transparent and trustworthy. Their killer feature was the "Work Diary," a tool that took periodic screenshots of a freelancer's screen during billable hours, providing clients with real-time visibility into what was actually being done.

Gary Swart, who joined as CEO to run the business side while the founders focused on technology, became one of the most public faces of oDesk and an evangelist for the idea that remote work was not a compromise but an upgrade. He was a tireless spokesperson, appearing at conferences, writing thought-leadership pieces, and making the case that the traditional model of everyone working in the same office was not just outdated but actively wasteful. The company grew steadily through the mid-2000s, building a reputation for hourly work that complemented Elance's strength in project-based engagements.

These were, in retrospect, two separate bets on the same future. Elance bet that the transaction was the hard part, that the key challenge was matching the right freelancer with the right project and managing the commercial relationship. oDesk bet that the work itself was the hard part, that the key challenge was making remote hourly work transparent and trustworthy enough for businesses to rely on.

Both were right, and both were incomplete. But for a decade, they operated as fierce competitors, each building its own community of freelancers and clients, each struggling with the same fundamental challenges of marketplace economics. The stage was being set for a collision.

III. Building the Two-Sided Marketplace: Elance vs. oDesk

Every marketplace builder eventually confronts the same maddening paradox: you need sellers to attract buyers, but you need buyers to attract sellers. It is the classic chicken-and-egg problem, and in the early days of online freelancing, it was particularly acute. A freelancer would sign up, see few job postings, and leave. A client would post a project, receive bids from unvetted strangers, get burned on quality, and never return. Breaking through this cycle required different strategies, and Elance and oDesk took meaningfully different approaches.

Elance built its model around project-based work with a bid system. A client would post a detailed project description, set a budget, and freelancers would submit proposals competing for the work. The system was familiar to anyone who had dealt with RFPs in the corporate world. It targeted small and medium businesses initially, then began making inroads with larger enterprises. The advantage was clarity: both sides knew the scope and price upfront. The disadvantage was friction. Writing a good project brief is hard. Evaluating fifteen proposals from strangers is harder. And the bid system naturally incentivized freelancers to undercut each other on price, which created a persistent "race to the bottom" dynamic that undermined the quality of the marketplace.

oDesk took the opposite approach, building its platform around hourly work with its signature time-tracking software. The Work Diary was simultaneously oDesk's greatest innovation and its most controversial feature. Every six minutes during a billed hour, the software would capture a screenshot of the freelancer's desktop and log keyboard and mouse activity. For clients, this was revelatory: they could verify that the person they were paying was actually working. For freelancers, it felt like surveillance, a digital panopticon that reduced professional knowledge workers to monitored production units. But it worked. The transparency addressed the fundamental trust deficit that plagued remote work, and it allowed oDesk to build a reliable marketplace for ongoing hourly engagements, the kind of work that was far more valuable over time than one-off projects.

Both platforms struggled with the quality problem that plagues every open marketplace. When you allow anyone to sign up and offer services, you inevitably attract a range of skill levels that spans from brilliant to incompetent. Reviews and ratings helped, but they were imperfect signals, easily gamed and slow to accumulate. A talented developer in Bangalore with zero reviews was invisible next to a mediocre one with fifty five-star ratings from small projects. This tension between openness and quality would persist throughout the industry's evolution.

Growth in the early years came through the unglamorous channels that define most marketplace businesses: search engine optimization, content marketing, and the slow, patient work of building category liquidity. Both companies invested heavily in ranking for search terms like "hire a freelance web developer" or "find a virtual assistant." They published guides, created templates, and built content ecosystems designed to capture the long tail of search queries from businesses exploring remote hiring for the first time.

The competitive dynamics between the two were brutal. They fought for the same buyers and sellers, and the switching costs were effectively zero. A freelancer could maintain profiles on both platforms simultaneously, and clients routinely posted the same job on Elance and oDesk to see which platform delivered better candidates. This commoditized both platforms and made differentiation nearly impossible. Meanwhile, a new challenger was emerging. Fiverr launched in 2010 with a radically different model: fixed-price gigs starting at five dollars. Where Elance and oDesk built platforms for professionals, Fiverr built a marketplace for tasks. It was faster, simpler, and more accessible, and it began fragmenting the market in ways that threatened the established players.

The unit economics for both companies were punishing. Customer acquisition costs were high because marketplace businesses must acquire both sides simultaneously. Take rates, the percentage of each transaction that the platform captures, were low because aggressive competition prevented anyone from pricing aggressively. And churn was relentless: clients would find a great freelancer on the platform and then take the relationship off-platform to avoid paying fees. This "disintermediation" problem is the silent killer of marketplace businesses, and it drained revenue from both Elance and oDesk throughout their independent years.

By 2013, a decade of building and competing had produced two large but unprofitable marketplaces, each with millions of registered users, each burning cash, and each facing a competitive landscape that was fragmenting rather than consolidating. Something had to give.

IV. The Existential Crisis and The Merger

By late 2013, the math was stark. Elance and oDesk were the two largest players in online freelancing, with a combined eight million registered freelancers and two million businesses across 180 countries, generating roughly 750 million dollars in combined annual billings. And yet neither company was thriving. They were spending enormous sums acquiring users who often overlapped, building parallel infrastructure to solve the same problems, and watching new competitors chip away at their positions from every direction.

The realization came gradually, then all at once: the two companies were killing each other. Every dollar spent by oDesk to lure a freelancer from Elance was a dollar that did nothing to grow the overall market. Every feature one platform built, the other had to match, creating a treadmill of competitive investment that enriched no one. The war of attrition was producing two weakened combatants rather than a single strong winner.

The behind-the-scenes negotiations were driven by a hard-nosed assessment of the competitive landscape. Alone, each company faced a future of continued losses, constant competitive pressure, and the ever-present risk that a better-funded newcomer would leapfrog both of them. Together, they would have something genuinely powerful: the largest talent pool, the broadest category coverage, and the scale to invest in the trust, payment, and matching infrastructure that the market demanded but neither company could afford to build alone.

On December 18, 2013, the two companies announced their merger to form Elance-oDesk. The deal brought together complementary strengths: Elance's project-based model and enterprise relationships with oDesk's hourly work infrastructure and time-tracking technology. The strategic logic was sound on paper. A combined platform would have unprecedented liquidity, the ability to serve clients whether they needed project-based or hourly work, and the scale to invest properly in matching technology, payment infrastructure, and trust and safety systems.

But mergers between competitors are notoriously difficult to execute. The two companies had different cultures, different codebases, overlapping feature sets, and employees who had spent years competing against each other. Integration required painful decisions about which platform's architecture would survive, which features to keep, and how to migrate millions of users without destroying the relationships and reputations they had built on their respective platforms.

In May 2015, the combined entity took the symbolic step of rebranding as Upwork, a name that signaled a fresh start and a unified identity. The new platform launched with improved search algorithms, faster payment processing, a new mobile app, and a real-time messaging system. The rebrand was more than cosmetic. It was a declaration that the legacy platforms would eventually be phased out, which they were, with Elance finally shutting down in 2019, and that the future belonged to a single, unified marketplace.

Stephane Kasriel, who had joined the company in 2013 and risen through the ranks, became CEO and drove the integration forward. His leadership was critical during this period because the merger's success hinged on technical execution: could the company actually consolidate two platforms into one without losing the users who made those platforms valuable? The answer, delivered over several painful years of migration, was yes, but not without friction. Some freelancers lost reviews. Some clients struggled with new interfaces. The transition was messy in the way that all large-scale platform migrations are messy.

What made this merger work when so many marketplace mergers fail? Three factors stand out. First, the two companies were genuinely complementary rather than purely duplicative: Elance's project model and oDesk's hourly model served different use cases. Second, the merged entity achieved a level of marketplace liquidity that no competitor could match, creating a meaningful advantage in the one dimension that matters most for marketplace businesses. And third, the timing was right. The market for online freelancing was still early enough that consolidation could capture future growth rather than simply defending a shrinking pie. The bet was that scale plus network effects would create defensibility, and over the next several years, that bet would be tested repeatedly.

V. Building Upwork 1.0: Platform Consolidation and the IPO Journey

The years between 2015 and 2018 were defined by the unglamorous work of platform building. No flashy product launches. No viral moments. Just the slow, patient, necessary work of consolidating two legacy systems, rationalizing overlapping features, and gradually improving the experience for both sides of the marketplace. Under Kasriel's leadership, Upwork focused on three priorities: migration, matching, and moving upmarket. Each was essential. None was exciting. All were harder than they looked.

The migration from legacy Elance and oDesk platforms to the unified Upwork was a multi-year project that tested the patience of everyone involved. Millions of freelancer profiles, work histories, reviews, and payment records had to be transferred without data loss. Clients with established relationships on one platform had to be onboarded to the new system. Every migration like this risks losing users at the point of transition, the digital equivalent of asking someone to pack up their entire office and move to a new building. Upwork managed this well enough to retain its core user base, though the process was not without casualties.

Matching algorithms became a central focus, and for good reason. The platform's value proposition depends entirely on its ability to connect the right freelancer with the right client quickly. If a startup founder in Austin posts a job for a React developer and gets fifty proposals but none from qualified candidates, the platform has failed regardless of how many freelancers are registered. Early matching was rudimentary: keyword search and manual browsing. A client would type "web developer" and scroll through pages of profiles, trying to distinguish between thousands of seemingly similar options.

Upwork invested in improving its recommendation engine, using historical data on successful engagements to surface better matches. Which freelancers in this category have the highest completion rates? Which ones get rehired by the same clients? Which ones deliver on time and on budget? By feeding this data into its algorithms, Upwork could push the most reliable, most relevant freelancers to the top of search results. The goal was to reduce time-to-hire, which had historically been measured in weeks, to something closer to days or even hours.

The quality problem, inherited from both legacy platforms, demanded a new approach. Upwork introduced Upwork Pro, a vetted talent tier that screened freelancers through a combination of skills tests, portfolio review, and interviews. This was a direct response to the persistent complaint that open marketplaces are flooded with low-quality providers. By creating a curated tier within the broader marketplace, Upwork could serve clients who were willing to pay premium rates for verified quality while still maintaining the open marketplace for price-sensitive buyers.

The enterprise push was perhaps the most strategically significant move of this period. Consider the strategic logic: a small business hiring one freelancer generates a small transaction. A Fortune 500 company hiring hundreds of freelancers through an integrated platform generates massive, recurring revenue with much higher switching costs. Upwork Enterprise offered these large companies dedicated account managers, configurable contracts, intellectual property protection agreements, cost center tracking, payroll services, API access, and integrated reporting. Everything a procurement department needs to say yes.

This was a bet that the future of freelancing was not just small businesses hiring individual contractors, but large corporations building "blended workforces" that combined full-time employees with on-demand freelance talent. The enterprise segment would eventually grow to generate approximately 100 million dollars in annual revenue, validating the thesis that big companies would embrace platform-based hiring. More importantly, enterprise clients brought stability: their spending was less cyclical than small business spending, their relationships were stickier, and their lifetime value was orders of magnitude higher.

Payment infrastructure was another area of steady improvement. Upwork built global payment rails that could handle transactions in multiple currencies, process payouts to freelancers in over 180 countries, and provide the escrow services that protect both sides of a transaction. Faster payouts became a competitive advantage: freelancers care deeply about how quickly they get paid, and Upwork's investments in payment speed helped reduce the churn that plagued the platform's early years.

On October 3, 2018, Upwork made its public debut on the Nasdaq Global Select Market under the ticker UPWK. The IPO priced at fifteen dollars per share, above the expected range of twelve to fourteen dollars, a sign of strong institutional demand during the book-building process. When trading opened, the stock surged to twenty-three dollars, a more than fifty percent pop that reflected genuine excitement about the "future of work" narrative. The company raised approximately 102 million dollars from the shares it sold, while existing investors also sold shares in the offering. The underwriters, led by Citigroup, Jefferies, and RBC Capital Markets, exercised their full overallotment option, adding nearly two million additional shares to the deal. Upwork entered the public markets with a valuation of roughly 1.5 billion dollars.

Kasriel, who rang the opening bell that day, framed Upwork's mission in characteristically ambitious terms. This was not just a company going public; it was the validation of an entire category. The world's largest work marketplace was now a public company, and investors could buy a piece of the future of work. The pitch was compelling. The execution would prove more challenging.

But the post-IPO honeymoon was brief. The stock began to decline almost immediately as investors scrutinized Upwork's financials and found what they expected to find in a marketplace business at this stage: strong revenue growth but persistent losses, high customer acquisition costs, and questions about when and whether the company could achieve profitability.

The skeptics raised fair questions. Marketplace businesses often take a decade or more to reach profitability because they must invest continuously in liquidity on both sides. But public market investors, accustomed to SaaS companies with clear paths to recurring revenue and expanding margins, struggled to value a business whose economics depended on the behavior of millions of independent freelancers and the spending patterns of hundreds of thousands of clients. The stock drifted downward through 2019, falling below its IPO price and staying there.

By early 2020, the narrative had shifted from "exciting future of work play" to "unprofitable marketplace with uncertain economics." The company needed a catalyst, and it was about to get one that nobody could have predicted.

VI. The Hayden Brown Era and Strategic Pivot

When Stephane Kasriel announced in December 2019 that he would step down as CEO, the company turned to someone who knew the platform intimately. Hayden Brown had joined Upwork back in 2011, when it was still Elance, as a product manager. She had risen through a remarkable series of roles: Head of Marketplace, Chief Product Officer, Chief Marketing Officer, and Chief Marketing and Product Officer. By the time she was named President and CEO effective January 1, 2020, she had spent nearly a decade understanding the platform's strengths, weaknesses, and unrealized potential.

Brown's background shaped her approach to leadership. She studied politics at Princeton, started her career as a business analyst at McKinsey, then moved to Microsoft where she worked on online strategy and corporate strategy. A stint leading corporate development at LivePerson gave her deep experience in marketplace dynamics before she joined Upwork. Her childhood in Kathmandu, Nepal, gave her a visceral appreciation for the transformative potential of connecting global talent with global opportunity. She was not a founder-CEO driven by founding vision but an operator-CEO driven by deep institutional knowledge and a pragmatic sense of what the platform needed to do next.

Brown took over at a moment when Upwork needed a leader who understood the platform from the inside out. The company was public but underperforming. It had scale but not profitability. It had market leadership but not market confidence. Her pre-COVID strategy was focused on moving Upwork upmarket and improving the metrics that would eventually drive profitability. She pushed for better client retention, recognizing that acquiring new clients was expensive but keeping existing ones was comparatively cheap. The math was straightforward: if you spend hundreds of dollars to acquire a client who makes one small hire and never returns, you lose money. If that same client makes five hires over two years, you make a lot of money. Everything Brown did was oriented around increasing the latter scenario. She invested in improving search and discovery on the platform, making it easier for clients to find the right freelancer without wading through hundreds of profiles. She introduced "specialized profiles," which allowed freelancers to create multiple profiles showcasing different skill sets, so a designer who also did front-end development could compete effectively in both categories.

The Project Catalog was one of Brown's signature product innovations, though it would not launch in beta until October 2020, with a full global rollout in January 2021. The concept was straightforward but strategically important: create a curated marketplace of predefined, fixed-price projects that clients could browse and purchase in a few clicks.

To understand why this mattered, consider the competitive context. Fiverr had built its entire business around the idea that hiring a freelancer should be as easy as buying something on Amazon: browse, click, pay, done. Upwork's traditional model, post a job and wait for proposals, was powerful for complex engagements but felt cumbersome for simpler needs. The Project Catalog was Upwork's answer: a client could scroll through a catalog of offerings across more than 300 categories, such as "logo design package starting at 500 dollars" or "five-page website build for 2,000 dollars," and hire instantly. It added a third purchasing modality alongside Upwork's existing project-based and hourly models, addressing a gap in the platform's ability to serve quick, transactional use cases.

The beta launch was accelerated by more than a month due to strong demand, a sign that both clients and freelancers had been waiting for exactly this kind of experience.

Under Brown's leadership, the company also continued investing in the trust and payment infrastructure that underpins any marketplace. Escrow services, dispute resolution mechanisms, identity verification systems, and fraud detection tools were all improved.

These are the invisible investments that users rarely notice but that determine whether a marketplace can sustain itself over time. Think about what trust means in this context: a business owner in Chicago is about to send thousands of dollars to someone she has never met, in a country she has never visited, based on a profile and some reviews. Without the escrow system that holds funds until work is approved, without the dispute resolution process that provides recourse when things go wrong, without the identity verification that confirms the freelancer is who they claim to be, that transaction simply does not happen. A single bad experience, a freelancer who disappears after receiving payment or a client who refuses to pay for completed work, can destroy a user's trust in the platform permanently.

By early 2020, despite these improvements, Upwork was still trading below its IPO price. Revenue was growing but not fast enough to satisfy public market expectations. The company was not yet profitable. And the narrative around online freelancing, while positive in theory, had not yet captured the mainstream imagination. Upwork needed the world to believe that remote work was not a niche phenomenon but a fundamental shift in how work gets done. In March 2020, the world began to believe.

VII. COVID-19: The Inflection Point That Changed Everything

The first weeks of March 2020 were chaos. Offices shut down overnight. Millions of knowledge workers scrambled to set up home offices. Companies that had resisted remote work for years were suddenly forced to operate entirely through screens. And the stock market, in a paroxysm of fear, sold everything. Upwork's stock plunged to 5.14 dollars on March 18, 2020, its all-time low, as investors initially assumed that a global recession would devastate discretionary spending on freelancers.

They were wrong. Spectacularly, unmistakably wrong.

Within the first week, something unusual started happening in Upwork's internal dashboards. New account registrations ticked up. Then job postings surged. Then the hiring velocity metrics, which the company tracked obsessively, began climbing at a rate that nobody in the organization had ever seen. Within weeks, the platform was experiencing a surge in activity that no one had planned for and no one fully understood at first.

The initial spike came from the obvious categories: web development, design, and writing, all skill sets that businesses desperately needed as they scrambled to build digital infrastructure for a suddenly remote world. Think about what happened in those first months: a restaurant chain that had never sold food online suddenly needed an e-commerce website. A small retailer needed to set up Shopify overnight. A nonprofit needed to move its entire donor engagement process to digital channels. These companies needed websites, apps, e-commerce platforms, and content. They needed them fast. And their usual approach of hiring full-time employees was impossible when offices were closed and HR departments were in crisis mode.

But the demand went far beyond technology. New categories exploded: virtual assistance, online education support, customer service, data entry, social media management. Businesses that had never considered using a freelance platform were suddenly creating accounts and posting jobs. The pandemic did not just increase demand for existing Upwork services; it expanded the addressable market by converting entire categories of work from "must be done in person" to "can be done remotely."

The supply side matched the demand. Fifty-nine million Americans performed freelance work in 2020, representing 36 percent of the U.S. workforce, up two million from the previous year. Millions of newly unemployed workers turned to freelancing out of necessity. Others, still employed but working from home, discovered that they could pick up freelance work on the side. The combination of surging demand and expanding supply created a virtuous cycle that marketplace operators dream about but rarely experience at such velocity.

Operationally, Upwork faced the scramble that every suddenly-successful technology company knows well. Infrastructure had to be scaled to handle increased traffic. Customer support teams were overwhelmed by the volume of inquiries from first-time users who had never hired anyone online before and needed hand-holding through every step. Trust and safety systems, designed for a smaller platform, had to cope with a flood of new users, some legitimate and some looking to exploit the chaos. Fraud attempts increased alongside legitimate activity, as bad actors sensed opportunity in the confusion. The company moved quickly to scale its operations, aided by the fact that, as a remote-first company, it was better prepared for pandemic-era work than most. Upwork's own employees did not need to adjust to working from home; they had been doing it for years. That institutional comfort with remote operations became a competitive advantage during a period when many technology companies were struggling with their own remote work transitions.

The financial results told the story. Full-year 2020 revenue reached 373.6 million dollars, up 24 percent year-over-year, with marketplace revenue growing even faster at 26 percent. The fourth quarter was the strongest since the IPO, and the trajectory was clearly accelerating. Gross services volume reached 2.52 billion dollars for the year. Active clients grew to 633,000. And critically, the company's profitability improved significantly as the surge in volume spread across a cost base that did not need to grow proportionally.

What made this moment truly transformative was the realization, shared by Upwork's leadership, its customers, and the broader market, that the shift was not temporary. Remote work had gone from "nice to have" to "table stakes" in a matter of weeks, and there was no going back. A CEO who had resisted remote work for years could no longer argue it was impossible after watching her entire company operate remotely for six months. A hiring manager who had always insisted on local, in-office contractors could no longer justify that constraint after successfully managing a team of freelancers across three time zones.

Enterprise adoption accelerated dramatically as major corporations discovered that blended workforces were not just possible but often more effective and cost-efficient than traditional all-employee models. Companies began building formal programs around freelance talent acquisition, integrating Upwork into their procurement workflows, and treating external talent as a strategic resource rather than a stopgap. The conversation in corporate boardrooms shifted from "should we use freelancers?" to "how do we optimize our freelancer strategy?"

The stock market responded with enthusiasm that bordered on euphoria. From its March low of 5.14 dollars, Upwork's stock began a remarkable ascent. By the end of 2020, it was trading above 30 dollars. By February 2021, it had crossed 50 dollars. The all-time high came on July 13, 2021, when the stock reached an intraday price of 64.49 dollars, representing a more than twelve-fold increase from the pandemic low just sixteen months earlier. An investor who bought the stock at its March 2020 bottom and sold at the July 2021 peak would have made more than twelve times their money in less than a year and a half.

The "future of work" narrative captured investor imagination in a way that Upwork's management had always hoped but never achieved during its pre-pandemic years. Suddenly, Upwork was not just a freelancing website; it was a bet on the permanent transformation of the global labor market. Analysts wrote reports comparing it to the picks-and-shovels play of the remote work gold rush. Institutional investors who had ignored the stock at fifteen dollars were now buying it at fifty. The company's market capitalization swelled into the multi-billion dollar range, and for a brief, heady period, it seemed like the most obvious investment in the world.

But the nature of market narratives is that they overshoot in both directions. The euphoria priced in a future where remote freelancing would grow uninterrupted for years. Reality, as always, would prove more complicated.

Why was Upwork uniquely positioned relative to competitors? Partly scale: as the largest platform by gross services volume, it had the deepest liquidity across the most categories, meaning it could serve a wider range of client needs than any competitor. Partly breadth: while Fiverr dominated quick, cheap gigs and Toptal served only elite talent, Upwork's marketplace spanned the full spectrum, from entry-level virtual assistants to senior software architects. And partly infrastructure: a decade of investment in payment systems, dispute resolution, and compliance had created a platform that enterprises trusted in ways they did not trust newer or more narrowly focused alternatives. The pandemic did not create Upwork's advantages. It revealed them.

VIII. Navigating the Boom: Growth, Competition, and Market Dynamics

The question that hung over Upwork through 2021 and into 2022 was whether the COVID-era gains would stick. Bulls argued that remote work was a permanent structural shift and that Upwork's role as the connective tissue of the freelance economy would only grow. Bears countered that pandemic demand was artificially inflated, that companies would eventually return to traditional hiring, and that Upwork's growth would revert to pre-COVID trends.

The competitive landscape added urgency to this question. Fiverr, publicly traded since 2019 under the ticker FVRR, was growing aggressively with a gig-based model that was simpler and more consumer-friendly than Upwork's. Fiverr's brand marketing was arguably stronger, with memorable advertising campaigns that positioned freelancing as accessible and mainstream. Toptal continued to own the premium tier, accepting only the top three percent of applicants and charging accordingly. Their clients were willing to pay significantly more for the guarantee of elite talent, and Toptal's model generated higher revenue per engagement than Upwork's.

More concerning were the new entrants attacking adjacent spaces. Deel and Remote.com were building platforms for companies that wanted to hire full-time remote workers across borders, handling compliance, payroll, and benefits in ways that Upwork did not. LinkedIn, backed by Microsoft's vast resources, was quietly expanding its freelance marketplace features, leveraging a network of over 900 million professionals. And a new wave of AI-first startups, including Braintrust with its blockchain-based model, were experimenting with radically different approaches to talent matching.

Upwork's competitive response focused on its unique strengths: breadth of category coverage, depth of marketplace liquidity, and growing enterprise relationships. On the product side, the company launched several significant initiatives. Upwork Payroll helped companies manage the administrative burden of paying freelancers, handling tax forms, compliance, and regular payment schedules. Talent Scout provided human-assisted matching for enterprise clients, combining algorithmic recommendations with dedicated account managers who could curate shortlists. Project Catalog expanded rapidly across more than 300 categories, giving Upwork a direct competitive response to Fiverr's gig model.

The results through 2021 and 2022 were impressive on the surface. Revenue grew roughly 35 percent in 2021 to approximately 503 million dollars, and another 23 percent in 2022 to reach 618 million dollars. Gross services volume hit 3.55 billion dollars in 2021 and climbed to approximately 4.1 billion in 2022. Active clients peaked at over 814,000. The enterprise segment grew 39 percent year-over-year in 2022, validating the upmarket strategy.

But beneath these topline numbers, cracks were forming. The "return to office" narrative gained momentum through 2022 as major employers, from Goldman Sachs to Tesla, demanded that workers come back. While fully remote work did not disappear, the frictionless growth environment of 2020 and 2021 began to normalize. More significantly, the tech sector entered a downturn in 2022, with widespread layoffs at companies that had been among Upwork's most enthusiastic clients. When tech companies cut budgets, freelance spending was often among the first line items to go.

The stock reflected this new reality with punishing clarity. From its peak above 60 dollars in mid-2021, Upwork's stock entered a prolonged decline that accelerated through 2022. By the end of that year, it was trading below 20 dollars, erasing more than two-thirds of its value from the peak.

The market was asking a simple question: if Upwork could not sustain its COVID-era growth rates, what was the business actually worth? Growth investors who had bought the narrative of perpetual expansion were selling. Value investors were not yet convinced the business was cheap enough. And the macro environment, with rising interest rates crushing the valuations of unprofitable growth companies across the technology sector, provided no help.

The answer, it turned out, would depend on whether the company could convert revenue growth into profitability, and whether a new technological wave, artificial intelligence, would prove to be friend or foe. Both questions would define the next chapter of Upwork's story.

IX. AI and The Next Chapter: Reinventing Talent Marketplaces

When ChatGPT launched in November 2022, it sent a shockwave through every corner of the knowledge economy, and few industries felt the tremor more acutely than online freelancing. The initial reaction was fear. If artificial intelligence could write code, design logos, draft marketing copy, and build websites, what would happen to the millions of freelancers who earned their living doing exactly those things? Upwork's stock, already battered by the tech downturn, faced additional pressure as investors worried that AI represented an existential threat to the company's core marketplace.

Hayden Brown's response was swift and strategically clever. Rather than dismissing the threat or pretending AI would not affect freelancing, she leaned into it. Upwork's bet was articulated clearly: AI would augment human talent, not replace it. The nature of valuable freelance work would change, shifting toward tasks that required human judgment, creativity, and the ability to deploy AI tools effectively.

This was not mere corporate spin. There was genuine logic behind it. When AI can generate a first draft of code, the valuable skill becomes knowing which code is correct, how to integrate it into a larger system, and how to debug it when something goes wrong. When AI can produce a passable logo, the valuable skill becomes brand strategy, visual identity systems, and the design thinking that turns a logo into a brand. In this framing, Upwork's role was not diminished by AI but enhanced by it: the platform would become the place where businesses find humans who know how to use AI to get things done.

In July 2023, Upwork announced a partnership with OpenAI to connect businesses with vetted AI experts through the platform. "OpenAI Experts on Upwork" was a curated program that matched companies seeking help with AI implementation, from custom GPT development to AI strategy consulting, with freelancers who had demonstrated expertise in these tools.

It was a smart move that turned a threat narrative into an opportunity narrative. Instead of AI replacing freelancers on Upwork, Upwork became the place where companies found the humans who could help them implement AI. The framing was critical for investor perception at a time when the market was punishing any company that appeared to be on the wrong side of the AI disruption.

The most significant product launch of this era came in April 2024 with Uma, Upwork's AI-powered marketplace assistant. Built on leading large language models customized with Upwork's proprietary platform data, Uma represented the company's most ambitious attempt to use AI to improve the marketplace experience itself. For clients, Uma could draft job postings with real-time feedback, compare freelancer proposals side by side, suggest appropriate budgets based on historical data, and recommend freelancers based on more nuanced matching criteria than keyword search alone. For freelancers, Uma provided AI-assisted proposal writing, skills gap analysis, and career development suggestions.

The early results were encouraging. New clients who used Uma spent at a seven percent higher rate in their first month compared to those who did not. This was a meaningful lift in a marketplace where small improvements in conversion and engagement compound over time. A Fall 2024 release expanded Uma's capabilities further, and the company continued to invest heavily in AI across its platform.

Meanwhile, new AI-related job categories were exploding on the platform. Prompt engineering, AI model training, custom GPT development, AI integration consulting, and AI-assisted content creation all emerged as high-growth categories. In 2024, gross services volume from AI-related work grew 60 percent year-over-year, and freelancers working in AI categories earned 44 percent more per hour than their non-AI counterparts. By the fourth quarter of 2025, AI-related GSV surpassed 300 million dollars on an annualized basis, growing more than 50 percent year-over-year.

The profitability transformation that investors had been waiting for materialized during this period. In 2023, Upwork made critical decisions to restructure its cost base, including a 15 percent workforce reduction. Revenue grew 11 percent to 689 million dollars, but the bigger story was that the company achieved GAAP net income of 46.9 million dollars, its first meaningful year of profitability. In October 2024, Brown announced a further 21 percent reduction in headcount, approximately 160 positions, aimed at generating around 60 million dollars in annualized cost savings. She framed it as "flattening and streamlining" the organization.

A pivotal change to the fee structure also boosted the economics. In May 2023, Upwork replaced its tiered freelancer fee system, which had charged 20 percent on the first 500 dollars with a client, 10 percent from 500 to 10,000 dollars, and just 5 percent above that, with a flat 10 percent fee on all new contracts. Analysts estimated that the blended freelancer fee had been running at just seven to eight percent under the old structure, meaning the shift to a flat 10 percent was significantly accretive to Upwork's take rate. Combined with a 5 percent client service fee and a new per-contract fee of up to 4.95 dollars, the overall marketplace take rate improved meaningfully.

Full-year 2024 results showed the impact: revenue reached 769 million dollars, up 12 percent, with adjusted EBITDA of 167.6 million dollars, more than doubling from the prior year. GAAP net income surged to 215.6 million dollars and diluted earnings per share hit 1.52 dollars. Free cash flow reached 139 million dollars. The company that had been an unprofitable, money-losing marketplace just a few years earlier was now generating substantial cash flow.

In 2025, revenue grew more modestly to a record 787.8 million dollars, a 2 percent increase, but profitability continued to improve. Adjusted EBITDA reached a record 225.6 million dollars, representing a 29 percent margin. The company repurchased more than 9 million shares using 136 million dollars in cash, and in February 2026, the board authorized an additional 300 million dollars in share buybacks, bringing total authorizations to 600 million dollars since November 2023.

The strategic direction under Brown became clearer at the company's 2025 Investor Day, where management introduced "The New Upwork" with 2028 targets calling for GSV growth of seven to nine percent annually, revenue growth of 13 to 15 percent, and adjusted EBITDA growth of approximately 20 percent. The 2026 guidance called for GSV growth of four to six percent, revenue growth of six to eight percent, and adjusted EBITDA margins around 29 percent.

But the stock has not reflected the profitability improvement. As of early March 2026, Upwork trades around 12 dollars per share with a market capitalization of approximately 1.58 billion dollars, still well below both its 2021 peak and its IPO price. The market is saying something important: profitability is necessary but not sufficient. Revenue growth of 2 percent is not the kind of topline momentum that commands premium multiples. The question hanging over Upwork is whether the company can reignite growth through AI-powered innovation, enterprise expansion, and geographic expansion, or whether it has settled into a low-growth, moderate-margin equilibrium.

X. The Business Model Deep Dive and Unit Economics

To understand where Upwork goes from here, you need to understand how it actually makes money and what drives its economics. At its core, Upwork is a transaction-based marketplace that earns revenue as a percentage of the gross services volume flowing through its platform.

The revenue model has three layers, and understanding them is essential for anyone evaluating the business. First, freelancer service fees: since the restructuring in May 2023, a flat 10 percent on all new contracts. Before this change, the fee was tiered in a way that rewarded long-term relationships: 20 percent on the first 500 dollars earned with a given client, dropping to 10 percent between 500 and 10,000 dollars, and just 5 percent above that. The old structure was designed to encourage freelancers to build deep client relationships on the platform, but it had an unintended consequence: the most valuable relationships, where a freelancer earned tens of thousands of dollars from a single client, generated the least revenue for Upwork. The switch to a flat 10 percent was controversial among established freelancers but transformative for the company's economics.

Second, client service fees: 5 percent on each payment to a freelancer, plus a one-time fee of up to 4.95 dollars per contract. This client-side fee, introduced more recently, effectively means that both sides of the marketplace contribute to Upwork's revenue on every transaction. Third, subscription and enterprise revenue: Freelancer Plus, a premium subscription tier that provides enhanced visibility, AI-powered tools, and additional connects for bidding on jobs, and Upwork Enterprise, which charges larger fees for dedicated support, compliance tools, and integrated workforce management features.

The marketplace take rate, the total percentage of GSV that Upwork captures as revenue, is the single most important metric for understanding the business. Think of it this way: if four billion dollars in work flows through the platform and Upwork captures roughly 14 percent, that is approximately 560 million dollars in marketplace revenue. Every percentage point of take rate improvement on that base represents tens of millions of dollars of incremental revenue at essentially zero marginal cost. The fee restructuring significantly improved this number, and management's ability to sustain or expand it over time will be a key determinant of long-term profitability.

Several key performance indicators deserve attention. Gross services volume measures the total dollar value of work transacted on the platform and represents the true scale of Upwork's marketplace. Active clients, defined as those who spent money on the platform in the last twelve months, is the core demand-side health metric. In Q4 2025, this number stood at 785,000. Core clients, defined as those spending five thousand dollars or more in the past year, are even more important because they represent the higher-value, stickier relationships that drive the majority of revenue. GSV per active client, which reached 5,129 dollars in Q4 2025, up 7 percent year-over-year, reveals whether the platform is attracting deeper engagement from its existing user base.

The economics of marketplace liquidity deserve a more detailed explanation because they are central to understanding both Upwork's moat and its vulnerability. Liquidity in a marketplace context means having enough active participants on both sides that a buyer can find what they need quickly and a seller can find consistent work. Think of it like a farmer's market versus a supermarket. A farmer's market with three produce vendors might have great tomatoes but no lettuce. A supermarket has everything, and that breadth is what keeps customers coming back even when a specialty shop might have better tomatoes. Upwork's strength is being the supermarket of freelance talent.

But marketplace liquidity is not monolithic. It is category-specific. Having a million web developers does not help a client who needs a specialized biostatistician. Upwork needs critical mass in each of hundreds of skill verticals, and within each vertical, it needs geographic diversity to cover different time zones, price diversity to serve different budget levels, and quality diversity to match different complexity requirements. This is extraordinarily difficult to build and, once built, difficult for competitors to replicate. It is the source of Upwork's strongest competitive advantage. A new platform might attract top-tier AI developers, but replicating Upwork's depth across hundreds of categories, from WordPress development to legal research to voiceover work, requires years of patient investment that most startups cannot sustain.

The profitability journey tells a compelling story about marketplace maturation. In its early years, Upwork spent aggressively on both sides of the marketplace: acquiring freelancers through marketing and incentives, and acquiring clients through paid acquisition and sales teams. This is the classic marketplace playbook: subsidize growth now, extract profits later. The question was always whether "later" would actually arrive.

It did. As the marketplace achieved liquidity in its core categories, organic growth began to supplement paid acquisition, and the unit economics improved. Freelancers told other freelancers about the platform. Clients who had good experiences came back without being re-acquired. The cost restructuring of 2023 and 2024, including the workforce reductions that eliminated approximately 36 percent of the company's headcount across two rounds, accelerated the transition to profitability.

Today, Upwork generates nearly 30 percent adjusted EBITDA margins, a remarkable transformation for a company that was unprofitable as recently as 2022. Capital allocation has shifted toward share buybacks, strategic acquisitions like Bubty and the planned Ascen deal, and continued R&D investment. The company's aggressive buyback program, with 600 million dollars authorized since November 2023, signals management's belief that the stock is materially undervalued relative to the cash-generating power of the business. Whether that conviction proves justified depends on the growth trajectory over the next several years.

XI. Porter's Five Forces Analysis

Competitive Rivalry: High. The freelance marketplace space is fragmented, with meaningful competition from Fiverr, Toptal, Freelancer.com, LinkedIn, and dozens of niche platforms serving specific verticals or geographies. Switching costs for users are low on both sides: a freelancer can maintain profiles on multiple platforms simultaneously with minimal effort, and a client can post the same job across Upwork, Fiverr, and Toptal to see which delivers the best candidates. Price competition is intense, with platforms fighting over take rates and fee structures. Each time one platform adjusts its pricing, competitors must decide whether to match or differentiate. However, Upwork's estimated 61 percent share of online freelance platform revenue, roughly four times Fiverr's share, suggests that marketplace liquidity provides meaningful insulation. Being the biggest means having the best selection, which means attracting the most clients, which means attracting the most talent. That flywheel is hard to break.

Threat of New Entrants: Moderate to High. The technical barriers to building a freelance marketplace are low. Anyone with engineering talent and venture capital can build a platform. The real barrier is achieving liquidity, which requires years of patient investment in both sides of the marketplace. AI-first startups are emerging constantly, and some, like Braintrust with its blockchain-based model, are experimenting with structures that reduce fees to near zero. The barrier to entry is not building the platform; it is filling it with enough active buyers and sellers to create a self-sustaining marketplace.

Bargaining Power of Freelancers: Moderate. High-quality freelancers are Upwork's most valuable asset and its most flight-prone. Top talent has alternatives: direct client relationships, competing platforms, full-time employment, or their own agencies. The best freelancers can command rates that make platform fees feel like an unnecessary tax. However, the platform provides real value through consistent deal flow, payment security, dispute resolution, and the administrative infrastructure that many freelancers do not want to build themselves. Quality freelancers who establish strong reputations and client relationships on Upwork face real switching costs even if the financial barriers are low.

Bargaining Power of Clients: Moderate to High. Clients have abundant alternatives for finding freelance talent. They can hire directly through LinkedIn, use competing platforms, engage staffing agencies, or work with boutique consultancies. The bargaining power is particularly strong for smaller clients who use the platform sporadically. However, enterprise clients who integrate Upwork into their procurement workflows, establish pools of vetted freelancers, and build compliance frameworks around the platform face meaningful switching costs. This is one reason the enterprise segment is so strategically important: it shifts the power balance.

Threat of Substitutes: High. This is perhaps the most significant force acting on Upwork, and it comes from multiple directions simultaneously. Direct hiring through LinkedIn or Indeed substitutes for many freelance engagements, particularly for companies that need ongoing work rather than project-based help. Traditional staffing agencies and consulting firms, from Robert Half to Accenture, offer managed alternatives where the agency handles the recruiting, vetting, and management rather than the client doing it themselves on a platform. Regional platforms in emerging markets, like Workana in Latin America or Malt in Europe, serve local clients who prefer local talent.

And increasingly, AI automation threatens to replace certain categories of freelance work entirely. When a marketing manager can use ChatGPT to generate a first draft of blog posts, or when a product team can use AI to create basic UI mockups, the need to hire a freelancer for those tasks diminishes. Consider what happens to a freelance writer who charges 200 dollars per blog post when AI can produce a passable first draft in seconds. The human's role shifts from creation to editing, strategy, and quality assurance, work that is still valuable but different in nature and potentially lower in volume. The threat is not that all freelance work disappears, but that the marginal, lower-value tasks that represent a significant portion of Upwork's transaction volume get automated away, leaving a smaller market of higher-value, more complex engagements.

XII. Hamilton's 7 Powers Analysis

Scale Economies: Moderate. Upwork benefits from fixed costs in platform development, trust and safety systems, and payment infrastructure that are spread across a growing transaction base. The marginal cost of facilitating an additional transaction is essentially zero: the same algorithms, the same servers, the same compliance infrastructure can process a thousand transactions or a million. This creates natural operating leverage as the platform scales. However, these scale advantages do not create winner-take-all dynamics because the market is large enough to support multiple profitable platforms at different scale levels. Fiverr, with roughly a quarter of Upwork's revenue, remains profitable on its own scale.

Network Effects: Moderate to High. This is Upwork's strongest power, and it is worth spending time understanding what it means in practice. The two-sided network effect is textbook: more freelancers attract more clients because the selection improves, and more clients attract more freelancers because the work opportunities increase. Cross-side effects are strong and measurable. When Upwork adds another thousand iOS developers to the platform, the experience for every client looking to hire iOS developers improves: more choices, faster matches, more competitive pricing. When another hundred enterprise clients start posting jobs, every iOS developer on the platform has more opportunities. The flywheel compounds.

However, and this is the critical nuance, the network effect is fragmented by skill category and geography. Being the dominant platform for web development does not necessarily help in data science or video editing. Each category functions almost as its own sub-marketplace, and liquidity must be built separately in each one. A client hiring a web developer experiences a completely different marketplace than one hiring a patent attorney or a motion graphics designer. This fragmentation limits the global network effect and creates openings for niche competitors who can build deep liquidity in a single vertical. It also means that Upwork's competitive position varies significantly across categories, dominant in some, thin in others.

Counter-Positioning: Low. Traditional staffing firms have been slow to adapt to platform-based hiring, but they are not paralyzed. Many have invested in their own digital platforms and remote hiring capabilities. Upwork does not enjoy a business model advantage so fundamental that incumbents cannot eventually replicate it. The platform model is better for certain use cases, but staffing firms still serve important functions, particularly for longer-term, managed engagements, that Upwork has not fully addressed.

Switching Costs: Moderate. For individual freelancers and small clients, switching costs are low. A freelancer can create a profile on Fiverr in an afternoon. A client can post a job on Toptal with minimal effort. But switching costs increase meaningfully at the enterprise level. Large companies that have integrated Upwork into their procurement systems, built pools of vetted freelancers, established compliance frameworks, and trained their teams on the platform face real friction in moving to a competitor. The reputation and relationship data that freelancers accumulate on the platform also creates soft switching costs: a freelancer with hundreds of five-star reviews and a proven track record loses a significant professional asset by switching platforms.

Branding: Moderate. Upwork has strong brand recognition within the freelancing community, where it is synonymous with online freelance work. However, the brand is not premium in the way that Toptal's is, nor is it as consumer-friendly as Fiverr's. The enterprise brand has been improving, driven by dedicated sales efforts and case studies from major corporate clients. Branding matters in this market because it affects which platform a first-time client tries, but it is not a durable competitive advantage on its own.

Cornered Resource: Low. Upwork does not own its talent pool. Freelancers can work on multiple platforms simultaneously, and there is no exclusive relationship that prevents top talent from being available elsewhere. The company's data, algorithms, and matching capabilities are improving but are not proprietary in a way that competitors cannot eventually replicate. The closest thing to a cornered resource is the accumulated review and reputation data on the platform, which creates value for established freelancers that they cannot easily port elsewhere.

Process Power: Moderate. Years of operating the world's largest freelancing marketplace have given Upwork deep institutional knowledge in trust and safety, dispute resolution, payment processing, marketplace dynamics, and fraud detection. Consider the complexity: when a client in Germany disputes the quality of work delivered by a freelancer in Nigeria, Upwork must adjudicate the dispute fairly, manage the financial resolution across currencies and banking systems, and update its algorithms to prevent similar issues in the future. This kind of operational knowledge accumulates over millions of transactions and cannot be replicated quickly.

Global compliance is another dimension of process power. Managing payments across 180-plus countries with different tax and labor regulations, anti-money laundering requirements, and currency controls is extraordinarily difficult to build from scratch. But process power erodes over time as competitors learn from the market leader's playbook and invest in building their own operational capabilities.

Overall Power Assessment. Upwork's primary moat is network effects driven by marketplace liquidity, particularly at the category level. This is reinforced by moderate switching costs for enterprise clients and process power in marketplace operations. These powers are real but not insurmountable, which means that continuous innovation and execution are essential for maintaining the company's position. The company's market-leading position is defensible enough to sustain but not dominant enough to guarantee.

XIII. Bull vs. Bear Case

The Bull Case.

The structural argument for Upwork begins with a simple observation: the way work gets done is changing permanently. Remote and hybrid work arrangements are no longer experimental. They are embedded in corporate strategy at thousands of companies that will never return to fully in-office models. The overall freelance platforms market was valued at approximately 7.65 billion dollars in 2025 and is projected to reach nearly 22 billion dollars by 2031, growing at a compound annual growth rate above 16 percent. This is a secular tailwind that benefits all freelancing platforms but benefits the market leader most.

Network effects in marketplace businesses tend to strengthen over time, particularly within specific skill categories where Upwork already has dominant liquidity. As the platform reaches critical mass in more categories and geographies, the gap between Upwork and its competitors widens. Enterprise adoption remains in early innings. Only a fraction of Fortune 500 companies currently use a freelance marketplace as a formal procurement channel, and the total addressable market for enterprise contingent workforce management is vast. The recent acquisitions of Bubty and the planned acquisition of Ascen, combined with the launch of the Lifted enterprise subsidiary, position Upwork to move from a marketplace into a comprehensive workforce management platform.

AI creates new job categories faster than it destroys existing ones, at least in the near term. The explosion of AI-related work on the platform tells a compelling story: prompt engineering, AI model training, custom GPT development, and AI integration consulting did not exist as job categories three years ago. Now they represent more than 300 million dollars in annualized GSV and growing more than 50 percent annually, with AI freelancers earning 44 percent more per hour than their non-AI counterparts. If the nature of freelance work shifts from routine tasks to complex, judgment-intensive work that leverages AI tools, the average value per engagement should increase, potentially offsetting any decline in volume from automation.

International expansion, particularly in Latin America, Southeast Asia, and Africa, represents significant untapped growth. These regions are producing growing populations of skilled digital workers who need a platform to connect with global clients. Upwork's 29 percent adjusted EBITDA margins suggest a path to 20 percent-plus sustained margins as the business scales, and the aggressive share buyback program signals management's confidence in the company's intrinsic value relative to its current stock price.

The Bear Case.

The fundamental concern is that Upwork operates a commoditized marketplace with limited pricing power. Freelancers are not loyal to the platform; they go where the work is, and many maintain profiles on multiple platforms simultaneously. Clients are not locked in; they use whatever platform offers the best talent at the best price, and can switch between competitors with minimal friction. Take rates face constant pressure as competitors undercut fees to gain share. Braintrust, for example, experiments with a near-zero-fee model funded by token economics, and even traditional competitors like Fiverr adjust pricing aggressively to attract volume. If Upwork raises fees, freelancers can shift their business to lower-fee alternatives. If it lowers fees, revenue per transaction drops. This is the pricing power trap that commodity marketplaces face.

AI poses a genuine existential risk to certain freelance categories. If AI can produce adequate writing, design, or basic code for a fraction of the cost of a human freelancer, the total addressable market for those services shrinks. The optimistic view that AI creates more work than it destroys may prove true in aggregate, but the transition period could be painful for a platform whose revenue depends on transaction volume. The AI-related work categories, while growing impressively, are still a fraction of total GSV.

The competitive threat from LinkedIn deserves special attention. Microsoft's platform has a massive built-in network of more than 900 million professionals, AI capabilities through Copilot integration, and the financial resources to subsidize a freelance marketplace indefinitely. LinkedIn already has relationships with the hiring managers who post jobs and the professionals who could fulfill them. If Microsoft decides to invest seriously in freelancing, the cost of building liquidity, the single highest barrier in marketplace businesses, drops dramatically. LinkedIn would not need to acquire users from scratch; it would need only to activate existing ones.

This is the kind of competitive threat that keeps marketplace executives awake at night: an adjacent platform with an existing user base that could enter your market with lower customer acquisition costs than you face maintaining your own.

Revenue growth of 2 percent in 2025, despite record profitability, is a warning signal. The company has demonstrated impressive margin expansion, but if the topline remains anemic, there is a ceiling on how much value cost optimization can create. You can only cut costs so many times before you start cutting into the muscle that drives future growth. Freelance spending is discretionary for many businesses, and it tends to be among the first budget items cut during economic downturns. When a CFO needs to trim spending, the freelance design project is easier to cancel than a full-time employee's salary.

The quality versus quantity trade-off that has plagued the platform since the Elance and oDesk days remains unresolved. Open marketplaces attract a range of quality levels, and clients who get burned by a bad experience may never return. Meanwhile, Fiverr's active buyer count declined 10 percent in 2024, suggesting that the entire category may be facing demand headwinds, not just Upwork-specific challenges. And the market for freelance platforms may remain permanently fragmented, with no single winner achieving the kind of dominant position that drives outsized returns.

KPIs to Track. For investors monitoring Upwork's ongoing performance, two metrics matter most. First, gross services volume growth, which measures whether the overall marketplace is expanding or contracting and serves as the leading indicator of future revenue. Second, GSV per active client, which reveals whether the platform is becoming more deeply embedded in its customers' workflows or whether engagement is plateauing. Together, these two numbers tell you whether Upwork is growing the pie and increasing its share of each client's spending, the combination that drives long-term value creation.

XIV. Playbook: Lessons for Founders and Investors

On Marketplace Building. Upwork's history teaches several enduring lessons about building two-sided marketplaces.

First, category-specific liquidity matters more than overall platform size. Having millions of registered users is meaningless if a client searching for a specific skill set cannot find five qualified candidates within 24 hours. A platform could have ten million freelancers, but if only twelve of them are qualified patent illustrators, a client looking for that skill will have a poor experience. Successful marketplace builders focus on building density within individual categories rather than chasing aggregate user counts.

Second, trust and payment infrastructure are table stakes, not differentiators. The work that Elance and oDesk did to solve the trust problem, through escrow, reviews, time tracking, and dispute resolution, was necessary to create the market. Without these systems, the market for cross-border freelance work simply would not exist at scale. But once that infrastructure exists, competitors can replicate it. The long-term defensibility of a marketplace comes from liquidity and network effects, not from any single feature.

Third, the tension between quality and quantity is perpetual and has no permanent solution. Every open marketplace must constantly balance the desire to be inclusive and maximize listings with the need to maintain quality that keeps buyers coming back. Upwork's introduction of curated tiers like Upwork Pro was one approach, but the challenge resurfaces with every new category, every new cohort of freelancers, and every new competitive threat from platforms that promise higher quality through stricter screening.

Fourth, take rate optimization is both an art and a science. Upwork's shift from a tiered fee structure to a flat 10 percent was a significant moment. The old structure, which charged decreasing percentages as spending increased, was designed to reward loyalty but effectively subsidized the platform's largest and most profitable relationships. The flat fee simplified the economics and boosted revenue, but it also risked alienating the highest-value freelancers who had been paying just 5 percent. Getting this balance right is an ongoing challenge that directly affects the platform's revenue trajectory.

On Strategic Decisions. The Elance-oDesk merger stands as one of the more successful competitive mergers in marketplace history. The lesson is that sometimes the best strategic move is to stop fighting your closest competitor and combine forces. But this only works when the combined entity is genuinely stronger than either individual company, meaning there must be real synergies in technology, user bases, or market coverage, not just cost savings from eliminating duplicate functions.

Moving upmarket, from commodity freelancing to enterprise workforce management, was the right strategic response to commoditization pressure. When competition drives prices down at the low end, the winning move is often to add value at the high end. Upwork Pro and Upwork Enterprise were bets that some clients would pay premium prices for premium experiences, and the growth of the enterprise segment validated this thesis.

The COVID experience teaches a nuanced lesson about macro tailwinds. The pandemic was unambiguously good for Upwork's business, but the company's challenge afterward was distinguishing between temporary pandemic-driven demand and permanent structural shifts. Management initially treated the growth as largely structural, which contributed to over-investment in headcount and sales capacity. The subsequent layoffs and cost restructuring suggest that the structural shift was real but smaller than the pandemic peak implied. The lesson: when a macro tailwind hits, invest to capture the opportunity but maintain the discipline to adjust when the wind changes direction.

On Competitive Positioning. In marketplace businesses, the viable positions are market leader with dominant liquidity, clear number two with differentiated positioning, or niche specialist with deep expertise in a specific category. Upwork occupies the first position, Fiverr the second, and Toptal the third. Everyone else struggles.

Network effects alone are not enough to build a durable competitive advantage. They must be reinforced by switching costs, brand, and process power to create a multi-layered moat. Upwork's push into enterprise, with its higher switching costs and deeper integrations, reflects this understanding. Technology moats in marketplace businesses erode particularly fast because marketplace technology is relatively well-understood and can be replicated by well-funded competitors.

On Managing Public Markets. Upwork's IPO timing was instructive. The company went public in October 2018, before its pandemic inflection point, and spent nearly two years as a public company trading below its IPO price while investors questioned its growth trajectory and path to profitability. Had the company been able to go public in 2021, when the narrative was most favorable, it would have commanded a dramatically higher valuation. The lesson is not to time IPOs to maximum hype, which is ethically questionable, but to recognize that the public market narrative can work against you if the business has not yet reached its inflection point. Upwork spent its first two years as a public company explaining why it was not yet profitable. It would have been far better to enter public markets with profitability already achieved.

The evolution of Upwork's story from "online freelancing platform" to "future of work infrastructure" to "AI-powered talent marketplace" illustrates how public companies must continuously update their narrative to reflect both their evolving strategy and the themes that resonate with current investors. Each era of public markets has its darling themes: cloud computing, the sharing economy, remote work, AI. Companies that can authentically connect their business to the dominant theme of the moment attract capital and attention. Companies that cannot, even if their underlying business is performing well, trade at discounts. The best stories are not fabricated; they are real strategic directions articulated in language that the market can understand and value. Upwork's current challenge is demonstrating that it is an AI beneficiary rather than an AI victim, and whether the market believes that narrative will heavily influence the stock's trajectory from here.

XV. The Future: Where Does Upwork Go From Here?

Near-term priorities through 2027 center on four themes, each of which addresses a specific constraint on the company's growth.

First, AI integration will continue to deepen. Uma is only the beginning. The vision is for AI to evolve from a matching assistant into a comprehensive workflow automation layer that manages not just the hiring process but the work itself: project scoping, milestone management, quality review, and payment optimization. Imagine a future where a client describes a project to Uma, the AI drafts a detailed scope of work, identifies the three best-matched freelancers, negotiates terms, monitors progress, and processes payment upon completion. That future is closer than most people think.