Upstart Holdings: The AI-Native Lending Revolution

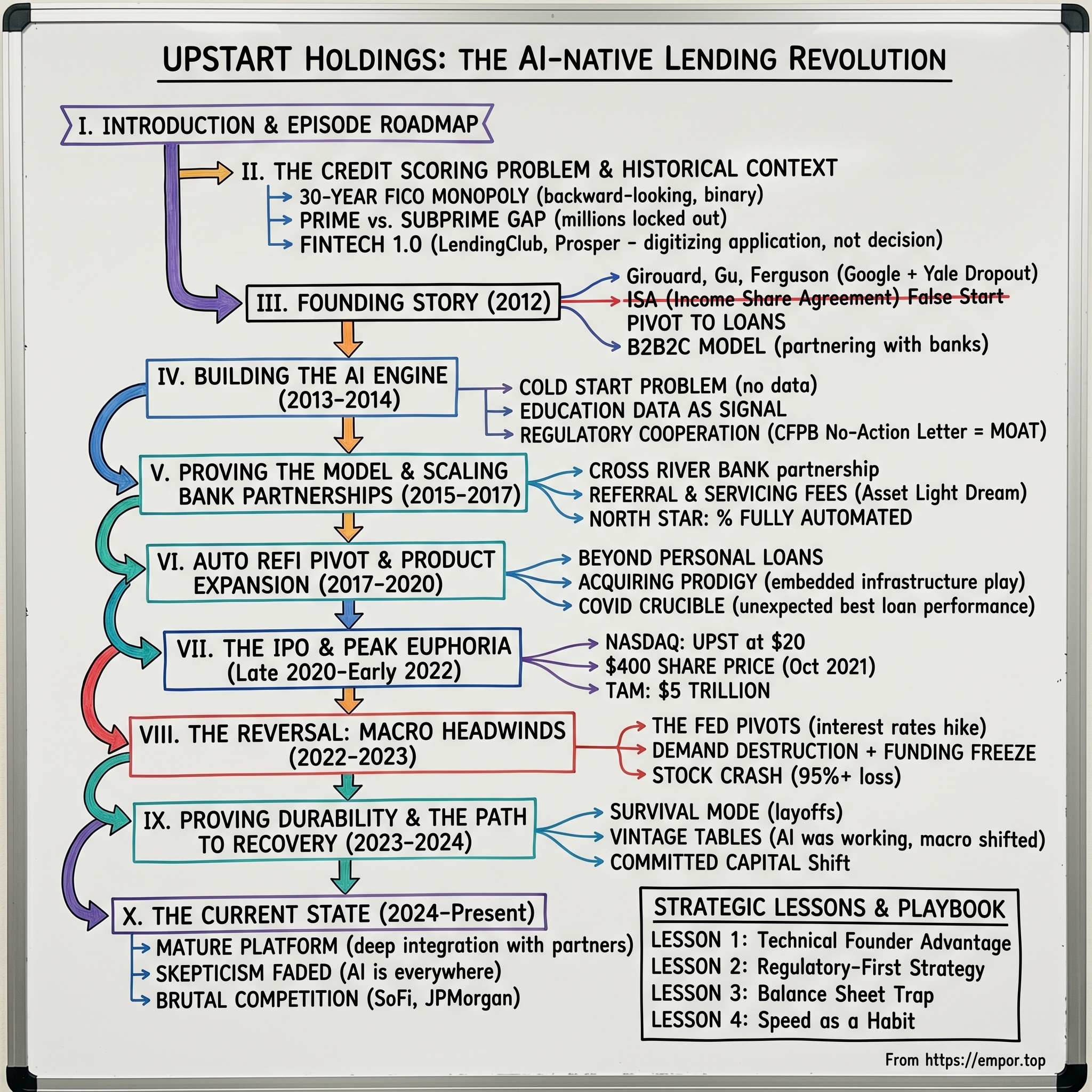

I. Introduction & Episode Roadmap

The Three Googlers and the Banker’s Paradox It is difficult to overstate how strange the pitch for Upstart sounded in 2012. You had Dave Girouard, the man who essentially built the Google Enterprise division (what we now know as Google Cloud) into a billion-dollar business, teaming up with two twenty-somethings to tell the banking industry—a sector that measures risk aversion in centuries—that their math was wrong.

The premise was audacious: the FICO score, the bedrock of the American financial system for thirty years, was a low-resolution jpeg in a 4K world. By using artificial intelligence and machine learning to analyze over 1,000 variables rather than the standard few dozen, this new company claimed it could approve more borrowers at lower rates while simultaneously lowering default risk. It sounded like alchemy.

For a brief moment in 2021, the world believed the alchemy was real. Upstart Holdings (NASDAQ: UPST) became the poster child of the "AI eating finance" thesis, rocketing from a $20 IPO to a $400 share price, commanding a market cap north of $30 billion—more than many regional banks combined. Then, gravity returned. As interest rates spiked and the easy money era of the 2020s evaporated, Upstart lost over 95% of its value, becoming a cautionary tale of what happens when a fintech platform meets a macro hurricane.

But here we are in late December 2025, and Upstart is still standing. It didn't die like many of its fintech peers. It adapted.

The Identity Crisis This deep dive is not just about a lending company. It is a case study on the fundamental identity crisis of fintech: Are you a technology company selling software (high multiples, low risk), or are you a bank in disguise (low multiples, balance sheet risk)? Upstart spent a decade trying to prove it was the former, only to be punished by the market when it was forced to act like the latter.

Over the next two hours of reading time, we will dissect one of the most volatile and fascinating business stories of the last decade. We will cover the "Google Mafia" origins, the regulatory masterclass that allowed them to operate, the euphoria of the zero-interest rate policy (ZIRP) era, and the brutal restructuring of the last three years.

Why does this story matter today? Because the promise of AI in underwriting remains the "Holy Grail" of consumer finance. If Upstart is right—if AI truly can predict risk better than a human or a scorecard—then the entire architecture of global banking is obsolete. If they are wrong, they are simply a subprime lender with better marketing. Let’s find out which one it is.

II. The Credit Scoring Problem & Historical Context

The 30-Year Monopoly To understand Upstart, you first have to understand the incumbent it was built to kill: FICO. Introduced by the Fair Isaac Corporation in 1989, the FICO score was a revolutionary technology for its time. Before FICO, getting a loan was a handshake deal based on whether the local bank manager liked your suit or knew your father. FICO standardized credit risk, creating a numerical language that allowed liquidity to flow across the country.

But by 2012, FICO had become a "step-function" technology in a continuous world. The standard credit model relies on five key factors: payment history, amounts owed, length of credit history, new credit, and credit mix. It is backward-looking by design. It tells you what someone did, not what they are capable of doing.

The "Prime" vs. "Subprime" Binary The limitations of this system created a binary world. If your score was above 680, you were "Prime" and banks fought to lend to you at 6%. If you were a 620, you were "Subprime" and your options were predatory payday lenders at 400% APR or nothing at all. There was no gradient.

Crucially, the FICO model penalized the young and the immigrants—people with "thin files." A recent college graduate from Stanford with a job offer at Google but no credit card history looked, to the FICO algorithm, exactly the same as a drifter with no income. This was the inefficiency: millions of creditworthy people were locked out of the system because the variable set (approx. 20-30 data points) was too small to see them.

Fintech 1.0: A False Dawn Following the 2008 Financial Crisis, banks retreated from consumer lending to shore up their capital reserves. This vacuum created Fintech 1.0: LendingClub, Prosper, and SoFi. These companies popularized "marketplace lending" (connecting borrowers directly to investors).

However, while Fintech 1.0 innovated on distribution (putting the loan application on a website instead of a branch), they largely didn't innovate on underwriting. Under the hood, LendingClub was still primarily using FICO bands to price risk. They were digitizing the application, not the decision. This is where the opportunity for Upstart emerged. The hypothesis wasn't to change how the user applied, but to change the brain making the decision.

III. Founding Story: Girouard, Gu & Ferguson (2012)

The Executive and the Dropouts The founding team of Upstart represents one of the most interesting archetypal mixes in Silicon Valley history: the seasoned operator and the wunderkind visionaries.

Dave Girouard was not your typical startup founder. In 2012, he was the President of Google Enterprise, managing a $1 billion P&L and thousands of employees. He was "Google royalty." He had spent a decade building the suite of tools that became Google Docs and Drive. He had everything to lose—status, unvested equity, and stability. But Girouard was obsessed with speed. He would later write a famous essay titled "Speed as a Habit," arguing that decisiveness is the primary determinant of startup success. He felt the bureaucracy of big tech slowing him down.

Then there was Paul Gu. A Peter Thiel Fellow, Gu was 20 years old, a brilliant coder who had dropped out of Yale to pursue the startup dream. He was obsessed with the inefficiency of risk pricing. He looked at his peers—smart, employable, high-earning potential—and couldn't understand why they couldn't get a credit card.

They were joined by Anna Counselman (now Anna Gu), another Google veteran who ran relentless operations and consumer experience.

The "Income Share Agreement" False Start It is a forgotten detail of history that Upstart did not start as a lending company. When they launched in 2012, the product was Income Share Agreements (ISAs). The idea was that investors would fund a young person's education or startup capital in exchange for a percentage of their future income for 10 years.

The name "Upstart" was quite literal: they were funding upstarts. They wanted to be the venture capitalists of human capital.

While intellectually elegant, the ISA model was a nightmare to scale. It required 10-year feedback loops, faced hazy regulatory definitions (was it indentured servitude? was it a loan?), and the consumer demand was tepid. Borrowers wanted money now with clear repayment terms, not complex equity-like arrangements on their own lives.

The Pivot to Loans (and the B2B2C Model) By 2014, the team made the hard decision to pivot. They realized the core technology they were building—a model to predict future income and employability—was actually a better credit model than a venture model.

But they faced a fork in the road: become a bank (Direct Lending) or become a technology partner (Platform). becoming a bank required massive capital and regulatory charters. Becoming a direct lender meant competing with banks. Girouard’s Google DNA kicked in: Google doesn’t make the websites; it organizes them. Upstart shouldn't be the bank; it should be the intelligence inside the bank. They chose the B2B2C route—partnering with banks rather than fighting them.

IV. Building the AI Engine & Getting to Product (2013-2014)

The Cold Start Problem Machine learning requires data. To train a model to predict loan defaults, you need history of loans and defaults. But Upstart hadn't made any loans. This is the classic "Cold Start Problem" of AI.

To bypass this, Paul Gu and his team built a model based on intuition and proxy data. They hypothesized that education and employment were the missing variables in FICO. If you knew an applicant graduated from nursing school (high employability, stable income) versus a volatile industry, you could price risk better.

They started originating loans on their own balance sheet (initially) to generate the training data. This was high-stakes poker. If their initial hypothesis was wrong, the company would go bust under the weight of bad loans.

Education as a Signal Upstart was the first meaningful lender to ask for your SAT score, your GPA, and your major. For a 23-year-old with no credit history, these were the only data points that mattered. The early models showed that a STEM graduate with a 3.5 GPA and no credit history was actually a safer bet than a "Prime" borrower with a high debt-to-income ratio.

The Regulatory High Wire Act This approach immediately triggered compliance alarm bells. The Equal Credit Opportunity Act (ECOA) prohibits discrimination. Banks were terrified that using "educational data" could be a proxy for race or class (disparate impact). If Upstart’s AI accidentally redlined minority borrowers because it favored certain universities, the regulators would shut them down.

Upstart’s genius was running toward the regulators. They spent years working with the Consumer Financial Protection Bureau (CFPB), effectively opening their "black box" algorithms to show that their model actually increased approval rates for minority and underserved borrowers compared to the traditional FICO model. This culminated in a "No-Action Letter" from the CFPB—a golden ticket that essentially gave them a regulatory safe harbor to experiment. This was their first true moat.

V. Proving the Model & Scaling Bank Partnerships (2015-2017)

Cross River Bank & The Hub-and-Spoke With the model showing promise (defaults were lower than predicted), Upstart needed a scalable source of capital. Enter Cross River Bank. A small New Jersey community bank that became the "plumbing" for much of the fintech wave, Cross River agreed to originate loans using Upstart's technology.

Here is how the unit economics worked: 1. A borrower comes to Upstart.com (or sees an ad). 2. Upstart’s AI assesses the risk in seconds. 3. If approved, Cross River Bank issues the loan. 4. Upstart takes a referral fee (origination fee) of 3-4% and a servicing fee. 5. Cross River Bank holds some loans but sells most to institutional investors.

This was the "Asset Light" dream. Upstart was a software company with 90% gross margins (in theory), taking no credit risk.

The Metrics of Success By 2017, the data began to compound. Upstart’s model was automating 20%, then 30%, then 40% of loans with zero human intervention. They called this metric "Percent Fully Automated." It was the North Star. Every time they removed a human underwriter, margins improved and the user experience got faster.

While competitors like LendingClub were struggling with fraud and rising defaults, Upstart’s vintage curves (the performance of loans over time) were pristine. Investors—hedge funds, credit unions, and banks—started lining up to buy the loans. The "yield chase" of the low-interest rate environment was beginning, and Upstart loans offered 8-12% yields in a world where Treasuries paid 2%.

VI. The Auto Refi Pivot & Product Expansion (2017-2020)

Beyond the Personal Loan Dave Girouard knew that personal loans were a "bug, not a feature" of the financial system. People take personal loans to consolidate credit card debt—a cyclical and somewhat limited market. To build a giant company, they needed to enter the massive asset classes: Auto and Mortgage.

The auto market is $1.5 trillion in the US alone. But it is fundamentally different from personal loans. It is secured (there is a car), it is sold at a dealership (Point of Sale), and the price is negotiated.

Acquiring Prodigy In a strategic masterstroke, Upstart didn't just build an auto loan algorithm; they bought a software company called Prodigy. Prodigy was like "Shopify for car dealerships"—software that helped dealers manage inventory and sales on iPads.

By acquiring Prodigy, Upstart inserted itself into the dealership workflow. Now, when a customer was buying a car, the dealer could click a button and get an Upstart-powered loan offer instantly. It changed Upstart from a direct-to-consumer website into an embedded infrastructure play.

The COVID Crucible Then came March 2020. As the pandemic locked down the world, credit markets froze. For a moment, it looked like the end. But then, the government stimulus kicked in. Millions of Americans used their stimulus checks to pay down debt. Savings rates skyrocketed.

Instead of a wave of defaults, Upstart saw the best loan performance in history. Simultaneously, e-commerce adoption accelerated by a decade. Banks, whose branches were closed, suddenly needed a digital lending partner. Upstart was perfectly positioned. Revenue exploded from $233 million in 2019 to run-rates implying billions. They were ready for the public markets.

VII. The IPO & Peak Euphoria (Late 2020-Early 2022)

The Debut Upstart went public in December 2020. They priced at $20 per share. By the end of the first day, they were up nearly 50%. But that was just the appetizer.

Throughout 2021, Upstart became the darling of Wall Street. In an environment where investors were hunting for "The Next Tesla" or "The Next Google," Upstart offered a compelling narrative: The AI that replaces banks.

The "Beating and Raising" Machine Quarter after quarter in 2021, Upstart didn't just beat earnings estimates; they shattered them. Revenue growth was triple-digit. Profits were real (rare for high-growth tech). They were buying back stock.

The stock chart went parabolic. From $20 to $100 to $200. In October 2021, it touched $401.49. The P/E ratio was in the hundreds, but bulls argued it was justified because the Total Addressable Market (TAM) was $5 trillion (Personal + Auto + Mortgage).

The Peak Narrative At the peak, the sentiment was that Upstart had solved credit. The "flywheel" was cited in every analyst note: More loans -> More Data -> Better AI -> Lower Rates -> More Loans. It seemed unstoppable.

However, smart observers noted a risk: The macro environment was "Goldilocks"—perfect for lending. Rates were near zero, consumers were flush with government cash, and unemployment was low. Upstart’s AI had never truly been tested in a downturn.

VIII. The Reversal: Macro Headwinds & The Crash (2022-2023)

The Fed Pivots The music stopped in early 2022. Inflation roared back, and the Federal Reserve began the most aggressive rate-hiking cycle in 40 years.

This hit Upstart with a "double whammy." 1. Demand Destruction: As rates rose, the APR Upstart had to charge borrowers jumped from 8% to 15% to 20%+. At those rates, fewer people wanted loans, and those who did were riskier. 2. Funding Freeze: This was the killer. Upstart sold its loans to credit investors. But as the Fed raised the "risk-free rate" to 5%, investors stopped buying risky consumer loans. Why buy an Upstart loan yielding 12% with default risk when you can buy a corporate bond yielding 9% with less risk?

The Balance Sheet Breach In Q1 2022, Upstart dropped a bombshell: they were holding loans on their own balance sheet because they couldn't find buyers. The market panicked. The entire "we are a tech platform, not a bank" narrative collapsed. If you hold the loans, you take the credit risk. You are a bank.

The stock crashed violently. In a single day following earnings in May 2022, the stock fell nearly 60%. It was a bloodbath.

The "Subprime" Accusation Bearish analysts piled on. They argued that Upstart wasn't using "AI"—they were just using loose underwriting to lend to subprime borrowers during a boom. As defaults began to tick up (normalizing from the artificial lows of 2021), critics claimed the model was broken.

By the end of 2022, the stock was trading in the low teens—a 97% drawdown from the peak. It was a complete round-trip.

IX. Proving Durability & The Path to Recovery (2023-2024)

Survival Mode 2023 and 2024 were the years of the "grind." Dave Girouard and the team had to shrink the company. They conducted layoffs, slashed marketing spend, and focused on one thing: proving the model works.

They released detailed "vintage tables" showing that while defaults had risen, Upstart’s model was still ranking risk correctly. The people the AI said were "risky" were defaulting at 5x the rate of the people the AI said were "safe." This proved the AI was working; the macro baseline had just shifted.

The "Committed Capital" Shift To fix the funding issue, Upstart changed its strategy. Instead of relying on fickle monthly loan buyers, they signed long-term "committed capital" deals with giants like Castlelake and Ares Management. These partners agreed to buy billions of dollars of loans over set periods, regardless of short-term market volatility. This put a floor under the business.

Auto and HELOCs While personal loans struggled, the Auto Retail business kept growing. Dealers stuck with the software. Upstart also launched Home Equity Lines of Credit (HELOCs), moving into secured lending which is more resilient in high-rate environments. By late 2024, the stock had recovered from the lows, trading in a volatile but healthier range, signaling that the market believed bankruptcy was off the table.

X. The Current State & Strategic Position (2024-Present)

December 27, 2025: The Survivor Today, Upstart is a very different company than the rocket ship of 2021. It is leaner, more disciplined, and battle-hardened. The "fair weather" fintechs are gone. Upstart remains.

The Mature Platform The platform has evolved. Upstart is no longer just a loan referral engine. It is deeply integrated into hundreds of banks and credit unions (the "partners"). These partners use Upstart’s AI to lend their own deposits to their own customers. This is the holy grail: pure SaaS revenue.

The AI Argument Wins Interestingly, the skepticism about AI in lending has largely faded by late 2025. Not because Upstart convinced everyone, but because AI has permeated every industry. The idea of not using machine learning to assess risk now seems archaic. The regulatory environment has stabilized, with the CFPB providing clearer frameworks for algorithmic fairness.

However, the competitive landscape is brutal. SoFi has built a massive bank. Affirm dominates the Point of Sale. JPMorgan and Capital One have spent billions building their own internal AI underwriting models. Upstart’s "Counter-Positioning" advantage is gone; now they must win on pure performance.

XI. Playbook: Business & Strategic Lessons

Lesson 1: The Technical Founder Advantage Upstart worked because Paul Gu approached lending as a data science problem, not a banking problem. A banker would have tried to tweak FICO. A coder tried to replace it. This "first principles" thinking is the hallmark of category-defining companies.

Lesson 2: Regulatory-First Strategy Most tech companies follow the "Uber" playbook: break the law and beg for forgiveness later. In finance, that equals jail. Upstart’s decision to embed with the CFPB early on was critical. They turned compliance into a competitive advantage (a barrier to entry for others).

Lesson 3: The Balance Sheet Trap The crash of 2022 taught a painful lesson: You cannot value a company as a tech platform if its revenue depends on capital markets liquidity. When the "spigot" of funding turns off, the tech platform stops generating revenue. Upstart has since tried to hybridize, but the market will never award it a pure SaaS multiple again until the funding is contractually guaranteed for years out.

Lesson 4: Speed as a Habit Girouard’s philosophy saved the company twice. First, in the pivot from ISAs to Loans. Second, in the rapid restructuring of 2022. Most banks take 18 months to change a credit policy. Upstart updates its model daily. In a volatile macro environment, speed is risk management.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter’s 5 Forces Analysis:

- Competitive Rivalry (HIGH): The days of being the only AI game in town are over. Big banks (JPM, Wells Fargo) have unlimited data budgets. Fintech peers (SoFi, Pagaya) are aggressive.

- Threat of New Entrants (MODERATE): Regulatory barriers are high. Building a compliant lending AI takes years of data and lawyer hours. It’s hard to just "start" a competitor today.

- Power of Suppliers (HIGH): Upstart’s "suppliers" are the capital providers (loan buyers). As seen in 2022, they have immense power. If they walk, Upstart starves.

- Power of Buyers (MODERATE): Borrowers are price sensitive. They will click on whoever gives the lowest APR. Brand loyalty in loans is non-existent.

- Threat of Substitutes (HIGH): Credit cards, Buy Now Pay Later (BNPL), and traditional bank loans are all substitutes.

Hamilton Helmer’s 7 Powers:

- Counter-Positioning (ERODED): Initially, Upstart counter-positioned against legacy banks that relied on FICO. Banks couldn't switch without cannibalizing their existing "Prime" customers. Now, banks are adopting AI, eroding this power.

- Cornered Resource (MODERATE): Their proprietary dataset—10+ years of AI loan performance across credit cycles—is a valuable resource that is hard to replicate. You can't buy this data; you have to live through the years to get it.

- Process Power (STRONG): The integration of complex AI compliance, bank reporting, and seamless UX is a process power. It is incredibly difficult for a regional bank to build this in-house.

- Network Effects (WEAK): More borrowers doesn't necessarily get Upstart better terms from banks, though more data does improve the model (Data Network Effect).

Summary: Upstart relied heavily on Counter-Positioning during its ascent. Now, its survival depends on Process Power and Cornered Resource (Data).

XIII. Bull vs. Bear Case

The Bull Case (The "Android of Lending") The Bull Case is that Upstart becomes the operating system for credit. Just as Google provides Android to every phone maker to compete with Apple, Upstart provides the AI engine to every regional bank to compete with JPMorgan. * Data Advantage: Their model has seen a crisis (COVID) and a rate shock (2022). It is battle-tested. * TAM Expansion: Auto and Home are just starting. * Efficiency: As AI improves, margins expand. They can price risk so accurately that they steal the best customers from everyone else.

The Bear Case (The "Cyclical Lender") The Bear Case is that Upstart is simply a high-beta play on the economy. * Commoditization: AI models become a commodity. Eventually, an open-source model rivals Upstart’s. * Funding Risk: They will always be at the mercy of capital markets. * Adverse Selection: The banks keep the best customers for themselves and give Upstart the "trash."

Key KPI to Track: Contribution Margin. This tells you the profitability of each loan after variable costs. If this holds up while volume grows, the Bull Case is alive.

XIV. Epilogue & What's Next

The Acquisition Target? As we look at the landscape in late 2025, one question looms: Will Upstart remain independent? For a legacy player like Capital One or even a tech giant like Apple (which has stumbled in its own lending efforts), Upstart represents a "plug-and-play" risk engine. The regulatory hard work is done. The tech is built. With a market cap that has rationalized, it is a tempting morsel.

The Future of Credit Whether Upstart wins or loses, they won the war of ideas. The era of the static, 30-variable credit score is ending. We are moving toward a world of continuous, high-fidelity risk assessment. Upstart fired the first shot in this revolution.

The question for the next decade is whether the pioneer gets to settle the new land, or if they just drew the map for the settlers coming behind them.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube