United Natural Foods Inc.: America's Invisible Food Empire

I. Introduction: The Paradox of the Middleman

Picture this: you walk into a Whole Foods in Manhattan, an independent co-op in Portland, or a conventional supermarket in suburban Ohio. You fill your cart with organic almond butter, kombucha, grass-fed beef, and a bag of specialty tortilla chips from a brand you discovered on Instagram.

What you almost certainly don’t know is that a single company—one you’ve probably never heard of—likely handled a huge portion of what you just bought before it ever reached the shelf.

That company is United Natural Foods, Inc., better known as UNFI. It’s a distributor: the quiet connective tissue between thousands of brands and tens of thousands of stores. UNFI moves natural, organic, specialty, produce, conventional grocery, and non-food products across the U.S. and Canada, operating across three segments: Natural, Wholesale, and Retail.

In plain English: if a retailer needs a massive, ever-changing catalog of products delivered reliably—dry goods, refrigerated, frozen, produce, supplements, and more—UNFI is one of the biggest machines making that happen. It serves more than 30,000 locations, from natural product superstores and independent retailers to conventional supermarket chains, ecommerce providers, and foodservice customers. It also sells “value-added” help alongside the boxes: technology, data, market insights, and shelf management support.

And yet, for all that reach, UNFI is basically invisible to the people it ultimately serves. The trucks pass by unnoticed. The warehouses hum in anonymity. Shoppers debate the provenance of their quinoa without ever realizing how many hands touched it—and how much logistics it took—just to get it into the aisle.

Here’s the paradox in sharp relief. In 2025, UNFI generated $31.78 billion in revenue, up from $30.98 billion the year before. That’s an enormous river of groceries flowing through one company.

But despite all that volume, UNFI still lost money: -$118.00 million in 2025, worse than 2024. So how does a business that moves tens of billions of dollars of product, serves tens of thousands of customer locations, and employs roughly 25,000 people end up in the red?

The answer is the brutal economics of distribution. UNFI operates in one of the least glamorous, most structurally unforgiving businesses in the economy. It’s the middleman in an era obsessed with cutting out middlemen. It creates real value—aggregating supply, managing complexity, extending credit, delivering perishables with precision—but captures very little of that value. Suppliers have leverage. Retailers have leverage. UNFI gets squeezed in between, forced to run a high-stakes operation on razor-thin margins, even as players like Amazon reshape expectations for cost, speed, and control.

What follows is how a network of hippie co-ops, born out of 1970s counterculture, became a $30 billion logistics behemoth—and why that evolution may have set up an existential crisis. It’s a story of consolidation and ambition, and of what happens when the cold math of an industry refuses to bend, no matter how essential you are.

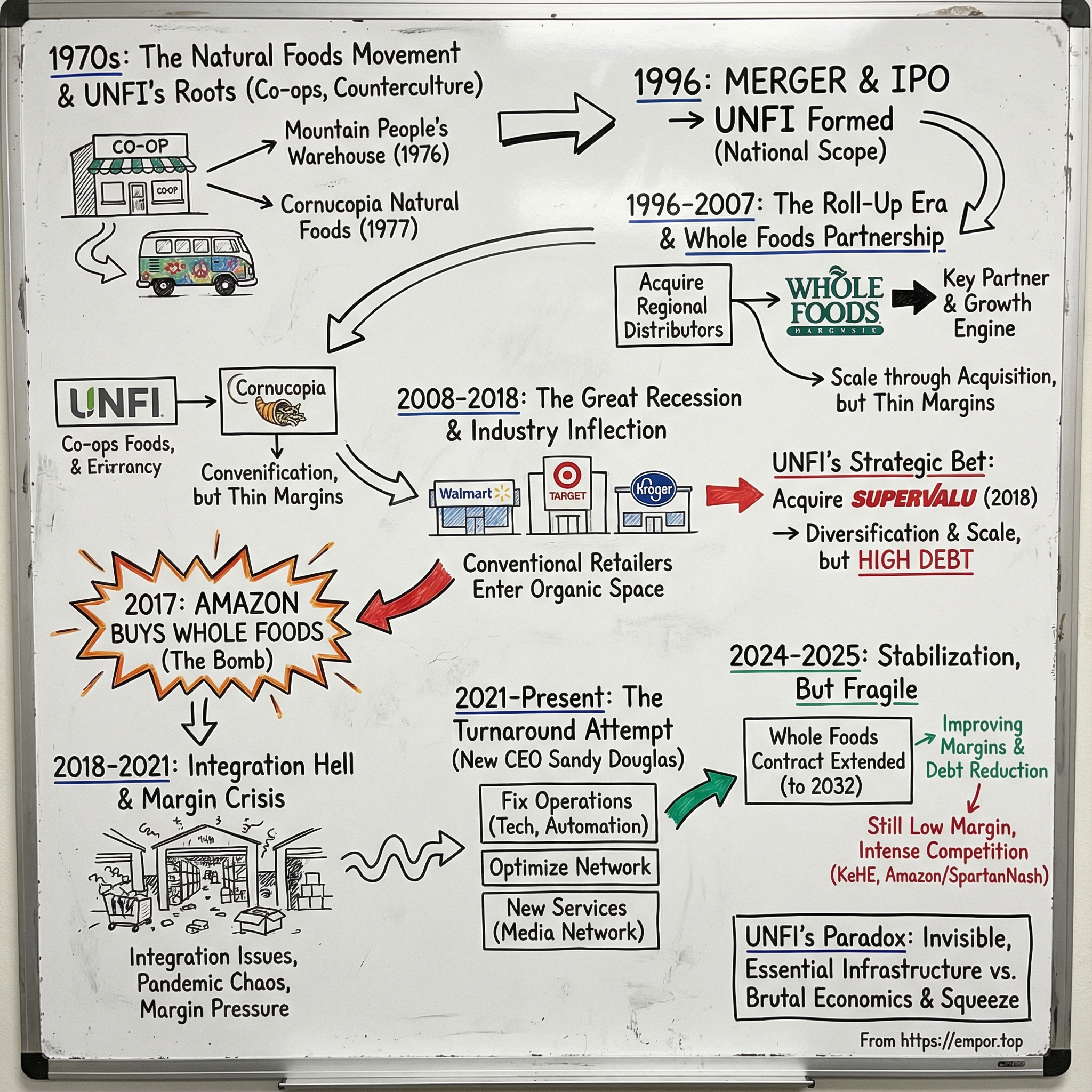

II. The Natural Foods Movement and Founding Context (1976-1995)

In America in 1976—the Bicentennial, Jimmy Carter on the campaign trail, Rocky in theaters—a quieter revolution was forming in the corners of the grocery world. Most shoppers were still filling carts at A&P or Safeway with Kraft Singles and Wonder Bread. But a small, growing group was pushing back. They wanted fewer chemicals, less processing, more transparency. They wanted organic. They wanted natural. They wanted, as the movement liked to say, food with values.

That demand created a problem: there was no real way to get this stuff to stores at scale—because the mainstream distribution system didn’t want it.

The products were niche and unfamiliar. The brands were tiny. Volumes were small, inconsistent, and hard to forecast. Many suppliers were undercapitalized, sometimes literally operating out of garages. And natural foods often meant more complexity: bulk items, supplements, refrigerated products, and shorter shelf lives. For big conventional distributors built to move pallets of Coke and boxes of Cheerios, it wasn’t worth the hassle.

So the natural foods world did what countercultures often do: it built its own parallel infrastructure.

One of the early pillars on the West Coast was Mountain People’s Warehouse, founded in 1976 by Michael Funk in Auburn, California. It operated with a cooperative spirit and served independent natural food stores and co-ops across the Western U.S. On the other side of the country, in Rhode Island, Norman A. Cloutier built Cornucopia Natural Foods. It began as a natural foods retailer in Coventry, then shifted into wholesale distribution in 1979—because if you wanted these products widely available, someone had to do the unglamorous work of warehousing, ordering, billing, and delivery.

Over time, both organizations grew—partly through organic expansion, partly by acquiring smaller regional players—riding the gradual rise in consumer interest in healthier, more “natural” options through the 1980s and early 1990s. Warehouses popped up where they had to: close enough to farms and small producers to source, close enough to co-ops and health food stores to deliver. They learned cold chain and perishables without the muscle of the mainstream giants. They extended credit to customers who didn’t have much of it. They made the whole thing work through relationships and persistence.

UNFI as we know it today didn’t truly come into existence until much later. In 1996, Mountain People’s Warehouse and Cornucopia Natural Foods merged—creating what was, at the time, the first natural products distributor with real national scope.

By then, the market had started to send signals that it might not stay on the fringe forever. Organic certification was gaining momentum. Consumer attitudes were shifting from curiosity to conviction. And by the early 1990s, Whole Foods Market was expanding—creating the first scaled, repeatable demand engine for natural and organic products.

For the regional distributors who’d spent years building a supply chain that most of corporate America dismissed, this was the inflection point. They weren’t just serving a subculture anymore. They were laying the tracks for a category about to go mainstream.

The most important takeaway from this era is cultural, not financial: UNFI’s DNA was formed in mission-driven, relationship-first commerce. That co-op ethos wasn’t a slogan—it shaped how the business operated and what it believed it was doing in the world. And as we’ll see, that heritage became both an advantage and a constraint once Wall Street scale entered the picture.

III. The Roll-Up Era: Building Through Acquisition (1996-2007)

By the mid-1990s, natural foods distribution was still a patchwork. Dozens of regional players had loyal customers and strong local relationships, but almost none had real scale. If natural and organic were going to go mainstream, someone would have to stitch that patchwork into a national network.

That stitching began in 1996, when the two companies we just met—Michael Funk’s Mountain People’s Warehouse (founded in 1976) and Norman Cloutier’s Cornucopia Natural Foods (founded in 1977)—merged to form the corporate entity United Natural Foods, Inc. They were literally on opposite coasts: Mountain People’s in California and Cornucopia in Dayville, Connecticut. Overnight, UNFI could credibly claim national reach in a category that had never really had it.

The timing mattered. The merger coincided with UNFI’s Initial Public Offering on NASDAQ in 1996, giving the company access to public-market capital. Up to that point, growth had been funded largely by the predecessor businesses themselves. The IPO changed the game: it turned a mission-driven, relationship-based distributor into a platform that could expand faster—warehouse by warehouse, region by region, competitor by competitor.

And that’s where UNFI leaned into what Wall Street and private equity would later call a roll-up strategy: buy smaller regional distributors, bolt them on, and use the growing footprint to win more business. In distribution, the logic is straightforward and relentless. More volume fills trucks. Fuller trucks make routes cheaper. Denser routes improve service and reduce per-stop costs. Bigger purchasing power brings better supplier terms. Each acquisition doesn’t just add revenue—it makes the entire machine run a little more efficiently, and makes the next deal easier to justify.

UNFI steadily broadened its footprint as more regional distributors folded into the network. In 2007, it acquired Millbrook Distribution Services, another step toward becoming the default middleman for natural and specialty products across the country.

The crown jewel of this era, though, wasn’t an acquisition. It was Whole Foods.

UNFI partnered with Whole Foods for nearly 20 years, and as Whole Foods grew from a regional chain into the national symbol of premium, health-conscious grocery shopping, UNFI scaled right alongside it. Whole Foods reportedly represented about 35 percent of UNFI’s roughly $8.5 billion in annual revenue at the time—an enormous share for a distributor. When Whole Foods grew, UNFI grew. When Whole Foods demanded more assortment, more freshness, more reliability, UNFI built the capabilities to deliver it.

But the same forces that made this period look like a clean growth story also planted the landmines UNFI would spend the next decade trying to avoid.

Customer concentration kept rising. Margins stayed thin—typically in the one to two percent range—even as revenue climbed. And the company’s co-op-and-founder DNA started running into a new reality: public shareholders don’t grade you on mission, they grade you on quarter-to-quarter performance.

By 2007, UNFI had become the clear leader in natural and specialty distribution. But in this business, “leader” doesn’t mean rich. It means you’re the best-positioned player in a structurally unforgiving industry—one where you can become essential to everyone around you, and still struggle to capture much value for yourself.

IV. The Great Recession and Industry Inflection (2008-2010)

The financial crisis of 2008–2009 changed the natural foods business in a surprising way. It didn’t kill demand. It accelerated the category’s escape velocity.

As households got more price-sensitive, the big conventional retailers realized something important: people still wanted “better-for-you” products, but they wanted them where they already shopped—and at prices that didn’t feel like a luxury. Natural and organic stopped being a fringe identity and started becoming just… groceries.

Walmart began expanding its organic assortment. Target rolled out natural and organic private-label options. Kroger invested heavily in natural foods sections. Costco turned organic into a bulk-buy staple. The very categories UNFI had spent decades nurturing were suddenly showing up everywhere, often at price points the specialty channel couldn’t touch.

For UNFI, this wasn’t just “competition.” It was a strategic fork in the road.

Option one was to stay a pure-play: keep serving natural product superstores, co-ops, and independents—loyal customers, but a smaller slice of a fast-growing market. Option two was to follow the demand into conventional retail and become a broader distributor to the mainstream chains, not just the natural aisle.

UNFI chose expansion, and on paper it made all the sense in the world. The problem was where that road led. Conventional grocery distribution made natural foods look forgiving. The customers were bigger and sharper-elbowed, and they treated logistics like a commodity to be squeezed. And the competitors—SUPERVALU, C&S, KeHE—had been fighting those margin wars for decades.

At the same time, the recession put pressure on UNFI’s existing customer base. Many independent natural retailers struggled. Some closed. Others got bought. Either way, the buyer side of the market got more concentrated, which meant more leverage sitting across the negotiating table from the distributor.

This is where the industry’s fault lines started to show. On one side: massive retailers that could demand lower prices and perfect service. On the other: smaller stores that still needed specialized help, but didn’t have the same volume to pay for it. UNFI now had to decide what it really was—a specialist, a scale player, or an uneasy mix of both.

And for anyone watching long term, the lesson was uncomfortable but clarifying: UNFI’s fate would be shaped less by clever internal execution than by the external power dynamics of grocery. In distribution, you can run a great operation and still get compressed—because the wave you’re riding matters more than how well you paddle.

V. The SUPERVALU Deal: Doubling Down on Scale (2018)

By 2018, UNFI hit a wall.

It was already a roughly $10 billion company and the clear leader in natural and specialty distribution. But the math was getting uncomfortable. The natural channel wasn’t growing fast enough to carry the next decade on its own. Whole Foods still loomed as the whale in the revenue mix, which meant one contract shift could become an existential event. And meanwhile, the real grocery volume—the kind that fills warehouses and keeps trucks running dense routes all day—still lived in conventional distribution, where UNFI was a relative lightweight.

So UNFI went shopping for scale. And it found SUPERVALU.

In July 2018, UNFI and SUPERVALU announced a definitive agreement: UNFI would acquire SUPERVALU for $32.50 per share in cash—about $2.9 billion total, including the assumption of SUPERVALU’s debt and liabilities. The deal closed a few months later, on October 22, 2018.

On paper, it was transformative. SUPERVALU was a grocery wholesaler and retailer with deep roots—it had been around since 1926, headquartered in the Minneapolis suburb of Eden Prairie, Minnesota. It brought roughly $14 billion in fiscal 2018 sales, a nationwide distribution footprint, and a customer base spanning thousands of stores. In total, SUPERVALU served 3,437 stores: 3,323 wholesale “primary stores” run by customers it supplied, plus 114 traditional retail grocery stores in continuing operations under three retail banners. It also came with a massive workforce—about 23,000 employees.

For UNFI, the strategic logic was bold, almost audacious: this wasn’t another bolt-on natural foods distributor. This was a leap from specialist to full-line wholesaler. UNFI would more than double revenue and, crucially, diversify away from its reliance on Whole Foods by inheriting a huge conventional customer base.

UNFI’s messaging captured the ambition. When it announced the deal was complete, the company said it would “take the best from both businesses to create North America’s premier food wholesaler with significant scale, reach and choices for our customers.”

Management also pitched the merger as an accelerator for UNFI’s “Build-out-the-Store” strategy—broader assortment, more categories, more customers, more suppliers. The synergy targets were sizable: run-rate cost synergies, net of reverse synergies, of more than $175 million by year three, and more than $185 million by year four.

But the way UNFI paid for it made the stakes impossible to ignore.

The transaction was primarily debt-financed. UNFI put new credit facilities in place, including a $2.1 billion asset-based revolving credit facility (with up to $1.475 billion available at closing) and a $1.950 billion senior secured first lien term loan facility. UNFI’s existing asset-based revolving facility was terminated upon close. At closing, UNFI expected leverage of about 4.7x gross debt to trailing twelve months Adjusted EBITDA, with a plan to de-lever to around 3.2x by year three and a long-term target of 2.0x to 2.5x.

And SUPERVALU didn’t come as a clean, frictionless asset.

It had been struggling through a difficult transition from retailing to wholesaling. It carried underperforming retail assets that were being sold off, operational issues like shrinking margins, and prior acquisitions still being digested. UNFI would now have to absorb all of that—while also managing its own challenges, including rising freight costs and strained warehouse capacity.

That’s what made the SUPERVALU acquisition such a defining bet. UNFI was wagering that scale and diversification would outweigh integration pain and balance-sheet risk—that becoming bigger, broader, and more “conventional” would make the business safer than staying a focused natural-foods specialist tied too tightly to one marquee customer.

It was a reasonable thesis. It was also the kind of thesis that only works if execution is near-perfect—because in distribution, there’s very little margin for error.

VI. The Amazon Bomb: Whole Foods Acquired (2017-2019)

June 16, 2017—more than a year before UNFI would sign up for the SUPERVALU bet—Amazon detonated the announcement that changed grocery overnight: it was buying Whole Foods Market for $13.7 billion in cash, at $42 a share. The deal closed on August 28, 2017, faster than many expected.

For UNFI, this wasn’t just another headline. It was an earthquake with a very specific aftershock: Whole Foods was UNFI’s single most important customer, representing roughly 35 percent of its approximately $8.5 billion in annual revenue at the time. Analysts immediately zeroed in on the obvious question: if Amazon’s superpower is logistics, why would it keep paying an outside distributor to supply its new grocery chain?

That logic hit UNFI’s stock immediately. The day Amazon announced the deal, UNFI shares fell more than 10 percent as investors priced in the nightmare scenarios. Amazon could bring distribution in-house. Or it could keep UNFI around—then squeeze it so hard on price and terms that the relationship stayed alive, but the economics didn’t.

One bearish note captured the mood bluntly: Whole Foods investors had just won big, but UNFI’s “fate” looked shaky—especially if any change-of-control provisions in UNFI’s supply agreement were triggered. Even if the contract held, the argument was simple: “Contractual obligations aside … why would the new Whole Foods need to utilize the services of an outside distribution organization when distribution is essentially the foundation of Amazon’s business?”

What steadied UNFI, at least in the near term, was that the contract didn’t vanish. UNFI’s CFO, Mike Zechmeister, told investors the parties had committed to continue their current arrangement through 2025. And in Amazon’s filings, the company disclosed it had taken on roughly $22 billion in contractually obligated future purchases—most of it tied to Whole Foods’ existing agreement with UNFI. For Amazon, famous for short-term deals and relentless pricing pressure, that kind of multi-year supplier commitment was unusual.

But while the contract stayed, the relationship changed forever.

UNFI wasn’t negotiating with a premium grocer that relied on its natural-foods expertise and infrastructure. It was now tethered to Amazon: a buyer with deep pockets, elite logistics, and a cultural reflex to push partners toward commodity pricing. The existential question shifted from “Do we keep Whole Foods?” to “At what terms—and for how long?”

Seen through that lens, the SUPERVALU acquisition looks less like ambition and more like self-preservation. If your biggest customer is suddenly owned by the most formidable operator in American commerce, diversification stops being a strategy choice. It becomes a survival requirement. Whether UNFI’s chosen escape route created a second crisis of its own would take years to find out.

VII. Integration Hell and the Margin Crisis (2018-2021)

The SUPERVALU integration was brutal. What management had sold as a synergy-rich marriage of complementary businesses quickly turned into a day-to-day operational grind. Legacy IT systems didn’t talk to each other. Warehouse processes didn’t match. Cultures collided. And when a distributor stumbles, customers feel it immediately: service levels slip, fill rates suffer, and the relationship starts to fray.

All of that would have been hard enough on its own. UNFI was also trying to pull it off while carrying the debt it had taken on to buy SUPERVALU. Even before the deal, UNFI had been wrestling with the basics of running a modern distribution network—freight costs were rising, and parts of its warehouse footprint were already stretched. After the deal, those problems didn’t disappear; they multiplied.

The financial profile deteriorated fast. Yes, revenue jumped as promised. But profitability compressed at the exact moment the company could least afford it. Leverage was roughly five times trailing EBITDA at the close, which meant the margin for error wasn’t thin—it was basically nonexistent. Interest expense soaked up cash that could have gone into systems, automation, and smoothing out the integration. And the stock, already rattled by the Amazon–Whole Foods shock, kept sliding as investors watched the risk stack up.

Then came COVID-19.

In the first months of the pandemic, UNFI looked, briefly, like a winner. Panic buying and at-home eating flooded the grocery channel with demand. Stores needed product, urgently, and distributors were suddenly mission-critical. But the sugar high didn’t last. The pandemic also delivered a relentless set of operational punches: supply chain disruptions, labor shortages, cost inflation, and constant volatility in what customers wanted and when they wanted it. It was the kind of environment that exposes every weak seam in a network—and UNFI had a lot of seams from the integration still showing.

The company’s results swung sharply as the market whipsawed. UNFI attributed the turbulence to the overall volatility and to spending tied to its transformation agenda—investments meant to improve operating performance and supply chain efficiency. But the bigger takeaway was simpler: the business was enormous, complicated, and increasingly fragile.

Because underneath the integration issues and the pandemic chaos was the industry’s fundamental problem: food distribution is structurally unforgiving.

Suppliers have power because manufacturing has consolidated—giants like Nestlé, Unilever, and Kraft Heinz can dictate terms. Retailers have power because grocery buying has consolidated—Walmart, Kroger, Albertsons, and Amazon can squeeze price and demand perfect service. And distributors sit in the middle, running warehouses, trucks, and cold chain infrastructure that everyone depends on, while capturing very little of the value they create. Layer on perishability, labor intensity, regulation, and the capital demands of facilities and fleets, and you get an industry where margins are thin in the good years and punishing the moment anything breaks.

UNFI wasn’t unique in facing that reality. But UNFI had chosen to face it with a leveraged balance sheet. Every fraction of a margin point mattered more, and every operational mistake cost more. The company didn’t have the flexibility to both invest heavily and service the debt load at the same time.

Something had to give.

VIII. The Turnaround Attempt: Transformation Under Pressure (2021-Present)

In August 2021, UNFI made the move you make when the stakes are existential: it changed the person at the top. J. Alexander “Sandy” Miller Douglas was appointed CEO and joined the board effective August 9, 2021, taking over after then-CEO Steven Spinner announced his retirement.

Douglas didn’t come up through the natural foods co-op world. His resume was built in huge, operationally complex distribution businesses—exactly the kind of muscle UNFI suddenly needed. He had most recently served as CEO of Staples, where he led a strategic transformation of its North American business-to-business distribution platform and steered the company through the COVID-19 period. Before that, he spent three decades at Coca-Cola, including running Coca-Cola North America and serving as Global Chief Customer Officer.

The message from Douglas was clear: this was no longer about simply being “the natural foods distributor.” It was about fixing the machine. UNFI’s transformation plan, he told analysts, would focus on improving the customer and supplier experience while closing “legacy integration and capability gaps” across both its digital and physical infrastructure. Under his leadership, UNFI also reshaped its organization around four service growth platforms.

The turnaround strategy centered on a few concrete moves.

First, UNFI went after its commercial structure. As part of a multi-year strategy launched in October, the company said it would restructure its commercial wholesale organization to deliver more customized value to customers and suppliers. Wholesale would be organized into two product-centered divisions: Conventional Grocery Products, and Natural, Organic, Specialty & Fresh Products. Each would have dedicated sales teams aligned to the product and service needs of the customers they serve, supported by specialists in merchandising, operations, procurement, and supplier services.

Second, technology moved from “nice to have” to core strategy. UNFI said it would deploy new robotics and automation software at its 1.15 million-square-foot distribution center in Centralia, Washington. The site would be UNFI’s first to receive Symbotic automation, bringing robotic case-pick capability as part of the broader push to modernize operations.

Third, UNFI started pruning and tightening its physical footprint. Network optimization—closing inefficient distribution centers, consolidating operations, and improving route density—became a priority. The company pointed to operational improvement initiatives and lean management routines that drove 14.5% Adjusted EBITDA growth and a $170 million improvement in free cash flow versus the prior-year quarter. Along the way, UNFI announced a pending closure of its Fort Wayne distribution center and completed the closures of its Bismarck and Billings facilities.

Then came the development that mattered most for UNFI’s long-term survival.

In May 2024, UNFI extended its partnership with Whole Foods through May 2032. The extension replaced the prior agreement that had been set to expire in September 2027, and it kept UNFI in the role of Whole Foods’ primary distributor. The market’s reaction was immediate: UNFI’s stock rose nearly 5% in early trading on the news, a real-time reminder of how central this customer remains to the story.

The extension was a watershed moment. It relieved the looming 2027 cliff and gave UNFI years of visibility it badly needed to keep transforming. But it also reinforced the defining tension in the investment case: even as UNFI worked to diversify, the Whole Foods relationship still sat at the center of its orbit—and customer concentration risk didn’t disappear just because the clock got pushed out.

IX. The Strategic Landscape: Why Distribution is Hard

To understand UNFI’s position, you first have to understand the game it’s playing. Food distribution is one of those businesses that looks huge from the outside and feels punishing on the inside, because the economics are tight at every step.

Start with the basic math. Distributors typically earn gross margins in the low teens. Out of that, they have to pay for everything that makes the system work: warehouses, trucks, drivers, fuel, refrigeration, IT, and an army of people doing the unsexy work of receiving, picking, loading, delivering, and reconciling orders. After all that, what’s left is usually a thin operating margin—often around one or two percent in good years, and less when anything goes wrong. Returns on capital tend to be similarly modest.

And if you want to see why customers care so much, look at restaurants. In foodservice, food and supply costs can be roughly a third of revenue. So a distributor isn’t a minor vendor; it can be one of the biggest levers on profitability. That means buyers negotiate like their business depends on it—because it often does.

Then there’s the capital intensity. Distribution isn’t an app you can ship and iterate. It’s concrete, steel, and cold air. Modern warehouses are enormously expensive to build and equip. Truck fleets constantly wear out and must be replaced. Cold chain infrastructure—refrigerated storage and transport for perishables—adds cost, complexity, and fragility. Automation can help, but it comes with massive upfront checks and paybacks that take years, not quarters.

Labor doesn’t make it easier. Warehouse work is hard and physically demanding. Driver turnover is a constant battle. Unionization is common. Wages rise, benefits matter, and staffing shortages show up immediately as missed deliveries and unhappy customers. Unlike software, distribution doesn’t scale cleanly. More volume generally means more people.

And hovering over everything is perishability. Food goes bad. Temperature excursions ruin loads. Recalls happen. The liability is real. Managing tens of thousands of SKUs—each with its own shelf life, storage needs, and handling rules—is a level of operational complexity most people never see when they grab a carton of yogurt off a shelf.

Now add the shadow competitor that never really leaves the room: Amazon. The threat isn’t just that Amazon might renegotiate hard. It’s that Amazon could decide it wants less middleman and more direct control—sourcing more product straight from manufacturers, streamlining the supply chain, and keeping more of the economics for itself. Ajay Jain, an analyst with Pivotal Research Group, has argued that Amazon’s drive to cut costs and pass savings to customers will eventually push it toward more direct sourcing. In his view, streamlining Whole Foods’ supply chain could mean a higher percentage of goods coming directly from manufacturers, not through a distributor like UNFI.

Meanwhile, direct-to-consumer has opened another flank. Brands that once needed distributors to reach shoppers can increasingly sell through their own sites or through newer channels like Thrive Market, subscription boxes, and meal kits. Not every product can move this way, but the direction is clear: the middleman model is being challenged from multiple angles.

So why does UNFI still exist at all?

Because it still solves real problems. Scale and route density create genuine value—aggregating shipments from thousands of suppliers and delivering them efficiently to thousands of retailers. Small and mid-sized retailers generally can’t negotiate like giants or build national logistics networks. Complexity management is hard to replicate—handling a catalog that can run to more than 40,000 SKUs across dry, refrigerated, frozen, produce, and specialty categories. Regional and local supplier access depends on relationships built over years. And distributors often provide credit, which matters more than most consumers realize.

But here’s the catch: these are reasons UNFI is useful, not reasons it’s untouchable. They support the business’s existence, but they don’t create a durable moat. And that vulnerability—essential, but easily squeezed—hangs over everything about UNFI’s strategy and its investment case.

X. Porter's Five Forces and Hamilton's Seven Powers Analysis

If you zoom out far enough, UNFI isn’t just battling competitors. It’s battling gravity. The best way to see that is to run two classic strategy lenses—Porter’s Five Forces and Hamilton Helmer’s Seven Powers—and ask a simple question: where, exactly, is UNFI supposed to make outsized money?

Threat of New Entrants: LOW

On paper, distribution is well-defended. Warehouses, fleets, cold chain, and modern tech systems require huge upfront capital. Food safety rules add compliance overhead. And the relationships—suppliers trusting you with product, retailers trusting you with their shelves—take years to build. Scale also matters: a small newcomer typically runs emptier trucks and less efficient warehouses, which means higher costs.

But there’s a caveat that matters more than all the textbook barriers: Amazon. Amazon isn’t a “new distributor” in the traditional sense, but it is a player with logistics in its bloodstream, deep pockets, and a willingness to accept ugly near-term economics. So the threat is low from typical entrants—and potentially existential from the one entrant category that doesn’t care about the usual rules.

Bargaining Power of Suppliers: MEDIUM-HIGH

Supplier power depends on who you’re talking about. In conventional grocery, manufacturing is concentrated. When giants like Nestlé, Unilever, and PepsiCo represent meaningful volume, they negotiate from strength.

UNFI has more leverage in natural and organic, where the supplier base is more fragmented and relationship-driven—UNFI’s original home turf. Private label can also provide some leverage, because owned brands give retailers an alternative to national brands. But it’s not a magic wand. In most categories, the biggest brands still have gravity.

Bargaining Power of Buyers: HIGH

This is the vice grip.

Grocery retail is concentrated, and the biggest buyers—Walmart, Kroger, Albertsons, Costco, and Amazon—have both pricing power and credible alternatives. Retailers can multi-source. They can switch. They can push costs downstream. And they can always threaten vertical integration, especially if they’re large enough to justify building their own capabilities.

The risk gets sharper when you look at UNFI’s own concentration. Moody’s has cited UNFI’s heavy reliance on its largest customer, Whole Foods, and also noted Whole Foods’ parent Amazon’s deepening relationship with SpartanNash, a UNFI competitor. Amazon also has a warrant agreement that could result in Amazon owning roughly 12%–15% of SpartanNash stock by 2027 if certain criteria are met.

Even when smaller independent retailers have less negotiating power individually, they often come with lower volumes and tighter economics—so they don’t automatically “save” the margin picture. Structurally, the buyer side is unforgiving.

Threat of Substitutes: MEDIUM-HIGH

There isn’t just one substitute; there are many, and they stack.

Brands can go direct-to-consumer and bypass traditional distribution for certain products. Retailers can self-distribute, especially at scale. Alternative channels like farmers markets, CSAs, and subscription services chip away at traditional grocery share. And adjacent giants—like foodservice distributors—can push into retail with enough investment and intent.

Competitive Rivalry: HIGH

In a business where the product is service and the service is measured in pennies, rivalry gets brutal.

UNFI fights across multiple fronts: KeHE in natural and specialty; and large-scale operators like Sysco and Performance Food Group that have the logistics muscle to expand where they choose. KeHE, UNFI’s primary natural and organic rival, is known for broad assortment and strong supplier and retailer relationships—exactly the areas where UNFI needs to defend its position.

KeHE’s network is substantial, with more than 70,000 SKUs and around 12,000 store customers, and it counts 23 of the 50 largest national food retailers among its customers. It is also employee-owned, which can create a different kind of internal alignment than a public company living quarter to quarter.

The big picture doesn’t change: differentiation is hard. One distributor’s truck pulling up to a dock looks a lot like another’s. When service levels converge, price becomes the weapon—and margins tell you how that tends to end.

Hamilton's Seven Powers Assessment:

Scale Economies: MODERATE — Scale helps: denser routes, fuller warehouses, more purchasing power, and better absorption of fixed costs like IT and overhead. But scale can also create diseconomies—more complexity, more layers, more coordination drag. And it’s not winner-take-all; multiple players can coexist.

Network Effects: MINIMAL — Adding suppliers doesn’t automatically attract retailers, and vice versa. Some data advantages can emerge from seeing what moves where, but nothing close to true platform dynamics.

Counter-Positioning: NONE — UNFI isn’t operating a business model incumbents can’t follow. If anything, UNFI is the incumbent that can be counter-positioned by Amazon and by brands that go direct.

Switching Costs: LOW-MODERATE — Retailers don’t switch distributors casually—systems, ordering habits, and operational routines create friction. Relationships matter. But in the end, distributors are substitutable enough that big buyers can credibly threaten to move.

Branding: MINIMAL — UNFI is B2B. End consumers don’t know it exists. Reputation matters inside the industry, but it’s not a durable moat the way a consumer brand can be.

Cornered Resource: NONE — No exclusive lock on suppliers at scale. No irreplaceable real estate. No proprietary technology that can’t be replicated with money and time.

Process Power: DEVELOPING — UNFI does have real operational know-how, especially in natural and specialty complexity. And it’s investing in process improvements, data, and analytics. The challenge is that process advantages in distribution are hard to keep; competitors can buy similar systems and talent if they have the capital.

Overall Assessment: UNFI is essential infrastructure without strong structural powers. It competes in a commodity-like business where both sides—suppliers and retailers—have leverage. The big strategic question is whether the transformation can create something defensible: stronger process power through technology and execution, higher switching costs through value-added services, or a defensible edge in specific categories. The hard part is that UNFI has to build that advantage while time and capital are constrained.

XI. Business Model Deep Dive and Playbook Themes

The distributor’s dilemma is easy to say and brutal to live: how do you create value for both sides of a transaction—suppliers and retailers—without ending up as the one who captures the least?

UNFI creates real value. For suppliers, it’s a gateway to more than 30,000 retail locations, plus warehousing, logistics, credit management, and a read on what’s actually moving in stores. For retailers, it’s the opposite side of the same coin: one-stop access to thousands of products, dependable delivery across dry, chilled, and frozen, support that helps decide what goes on the shelf, and help managing working capital. This is not “nice to have” stuff. It’s the operating system of modern grocery.

But value creation and value capture aren’t the same thing. In distribution, the work is essential, and the reward is often thin.

So why does food distribution attract capital anyway, if the returns are so mediocre? A few reasons. Demand is steady—people eat every day. The infrastructure is non-optional—stores can’t function without product showing up on time. The category is relatively recession-resistant. And for private equity in particular, predictable cash flows can look like something you can lever, optimize, and squeeze.

UNFI’s problem is that it’s trying to do all of that in hard mode. Its specific challenges include: - Straddling natural and conventional categories in an awkward middle—neither a pure-play specialist nor a clean full-line incumbent - Carrying the debt load from the SUPERVALU acquisition, which limits how aggressively it can invest - Customer concentration risk, with Whole Foods still central even after the extension through 2032 - A margin profile that has historically lagged peers, leaving less cushion when anything goes wrong

The playbook for what could work isn’t mysterious—but it is difficult.

One path is to lean into what UNFI has always been best at: natural and organic, where its heritage and relationships still matter. Another is to try to build real operational advantage through technology—better data, better forecasting, better automation—so the machine runs tighter than competitors’. Private label offers a different angle: instead of fighting for pennies in distribution margin, capture more economics by owning more of the product margin. And then there are adjacent services—retail support, data products, and newer efforts like media networks—that aim to make UNFI more than a truck-and-warehouse company.

As Sandy Douglas put it:

Value-added was a long-term focus of the company well before I got here. Whether it's professional and digital services or Brands+ or the UNFI Insights platform for suppliers. We recently launched the UNFI Media Network, which is very early days, but up until now, only the largest retailers really got to participate in that value stream. Having been in a CPG my whole life, I know that a diverse channel base and particularly independent retailers are so important to healthy brand growth. Our diverse customers are a tremendous brand building ecosystem for suppliers, and so why not work a media network into that customer base? Whether it's saving our customers money or helping them compete or creating new platforms, we see services as a really important component for them and a way for us to help them make some more money by adding more value.

There’s also the broader consolidation thesis: maybe this industry simply can’t support so many distributors, and scale is the only way to survive. UNFI is already the largest publicly traded player, which puts it in the center of that argument. But consolidation isn’t free. It invites antitrust scrutiny, adds operational complexity, and—if it’s funded with debt—can recreate the same balance-sheet trap UNFI has been trying to climb out of since 2018.

Which brings us to the range of possible endings. UNFI could become an acquisition target for a larger distributor or private equity. It could execute a real turnaround and slowly rebuild profitability. It could also slog forward in a long, low-return grind—or get disrupted if the industry shifts faster than it can adapt. The frustrating truth is that the outcome will hinge not just on execution, but on the evolution of grocery power dynamics—forces that sit largely outside UNFI’s control.

XII. Bull vs. Bear Case

The Bull Case:

The optimistic read is that the turnaround is no longer just a PowerPoint. UNFI rolled out a three-year business plan with clear goals: create more value for customers and suppliers, expand margins, generate more free cash flow, and keep paying down debt. Management pointed to fiscal 2024 results landing at the upper end of its outlook, and emphasized a simple but important pattern: four straight quarters of sequentially improving profitability. In a business that lives and dies on small operational edges, a streak like that matters.

The operating cadence has started to tighten, too. UNFI said its focus on lean management and “stakeholder value creation” drove meaningful Adjusted EBITDA growth and improved free cash flow versus the prior-year period. Leverage moved in the right direction as well, with net debt to Adjusted EBITDA down to 3.3x—its lowest level in the last two fiscal years.

Then there’s the category tailwind. Natural and organic demand continues to benefit from long-term health trends and shifting consumer preferences. And for thousands of small and mid-sized retailers, UNFI remains the essential infrastructure they can’t realistically replicate on their own.

Most importantly, the Whole Foods relationship—still the emotional center of this story—now runs through 2032. That extension buys UNFI time and visibility. If the company can keep improving execution, a stock priced like a chronic disappointment has room to re-rate.

UNFI also highlighted momentum in its “Supernatural” segment, which includes Whole Foods Market, with sales up 13.8% versus the same quarter a year earlier. On the back of those results, it raised its full-year outlook, projecting adjusted EPS of $0.40–$0.80 on revenue of $30.6–$31 billion, and pointed to a $170 million year-over-year improvement in free cash flow as evidence that efficiency initiatives were starting to show up where it counts.

The Bear Case:

The pessimistic read is that none of this fixes the underlying physics. Food distribution is still a squeeze play between powerful suppliers and powerful retailers, and that pressure doesn’t go away because one operator gets a little better at running warehouses.

Amazon remains the looming risk. Yes, the Whole Foods contract now extends to 2032. But renewal after that isn’t guaranteed, and the economics can always get tighter. Amazon can push for different terms, shift volumes, or pursue alternative distribution strategies if it decides more direct control is worth it.

Meanwhile, UNFI still carries meaningful debt, which limits how aggressively it can invest compared to better-capitalized competitors. Competitive threats don’t disappear either: big distributors like Sysco or US Foods could push harder into natural and specialty if they want the volume, and direct-to-consumer plus alternative channels keep nibbling at the edges of the traditional model. The SUPERVALU integration has improved, but the scars—and the complexity—haven’t fully vanished.

The core bear takeaway is harsh: retailer consolidation and brand disintermediation threaten growth and margins, while customer concentration and leverage keep the company financially fragile. Add rising compliance demands and evolving regulation, and the margin ceiling can stay low even if execution improves.

And the true nightmare scenario is still the same one investors have feared since 2017: if UNFI ever lost the Amazon/Whole Foods business without a replacement of similar scale, the equity could be wiped out.

The Realistic Case:

The middle path is that UNFI survives, but it’s never an easy story. Margins grind up slowly, debt comes down gradually, and revenue grows modestly. The stock might recover from distressed levels over time, but it’s unlikely to become a rocket ship. At some point, the most plausible “clean” ending may be consolidation—merging with a peer or being taken private by sponsors who can live with steady cash flows and modest returns. Not a growth story, not a disaster. Just a hard business.

XIII. Lessons for Founders, Operators, and Investors

UNFI’s story leaves a set of lessons that apply far beyond grocery—especially for anyone building, operating, or underwriting businesses that sit in the middle of an ecosystem.

The middleman squeeze is real. If you create value for two sides but don’t control either side, you get negotiated down from both directions. UNFI makes life easier for retailers and suppliers—aggregating demand, managing complexity, and moving product reliably—but most of the economics flow outward, not inward.

Scale isn’t always a moat. In distribution, being big can make you efficient. It doesn’t automatically make you powerful. When customers can credibly switch and your service starts to look like a commodity, size mostly turns into a high-volume version of the same margin fight.

Debt disciplines, but it also limits your options. The SUPERVALU acquisition didn’t just add warehouses and customers—it added leverage. And leverage doesn’t just raise the stakes; it narrows the playbook. UNFI spent years focused on deleveraging and stability at the same time it needed flexibility to invest, modernize, and integrate.

Customer concentration is existential risk. When a third of your revenue depends on one customer, “relationship management” becomes “single point of failure.” And when that customer is owned by Amazon, no amount of operational improvement can fully remove the vulnerability.

Mission versus margin is a real tradeoff. UNFI’s roots in co-ops and values-first commerce shaped its culture and relationships. Public markets reward something else: predictable results and expanding profitability. Living in both worlds at once creates tension, and leadership has to decide—again and again—what gets prioritized.

Transformation takes longer than you think. UNFI’s turnaround wasn’t a single program. It became a multi-year sequence of fixes, investments, and reorganizations—while the external environment kept shifting. Big, complex supply chains don’t pivot quickly, even when the need is obvious.

Industry structure can overpower good management. Execution matters, but it’s not the whole story. UNFI’s biggest constraints come from the bargaining power and consolidation on both ends of the chain. Sometimes the business is hard because the industry is hard.

Technology is necessary, but rarely sufficient. Automation, better forecasting, and data tools can tighten operations—but they’re not a permanent advantage when competitors can buy similar systems. Tech can create a lead; it doesn’t guarantee a moat.

Timing in M&A is everything. SUPERVALU brought scale and diversification, but it also arrived at the worst possible moment: high leverage, a massive integration load, and a post-Amazon Whole Foods landscape that was already rewriting the rules. In distribution, where margins leave little room for error, bad timing doesn’t just hurt—it compounds.

XIV. Recent Developments and Current State (2024-2025)

By 2024 and into 2025, the story shifted from free fall to something closer to stabilization—still fragile, still low-margin, but finally moving in the right direction.

In the third quarter of fiscal 2025, UNFI reported gross profit of $1.1 billion, up $62 million, or 6.1%, from the same quarter a year earlier. The catch is that the gross profit rate slipped to 13.4% of net sales from 13.6% the prior year. Management attributed that dip to lower product margin rates and a changing mix of business, partly offset by supplier programs and lower shrink. In other words: the machine moved more profit dollars, but the underlying pricing power still wasn’t getting materially better.

Below the gross line, though, UNFI’s operational improvements showed up more clearly. Adjusted EPS rose to $0.44 in the quarter, up from $0.10 a year earlier. Adjusted EBITDA increased to $157 million from $130 million.

The balance sheet also started to look less like a ticking clock. Total outstanding debt, net of cash, was $2.05 billion at the end of the second quarter of fiscal 2025—down $182 million from the end of the first quarter. Net debt to Adjusted EBITDA was 3.7x as of February 1, 2025. It’s not “comfortable,” but it’s meaningfully better than where UNFI had been when integration and the Amazon shock were at their worst.

Equity markets noticed. UNFI’s stock climbed to a new 52-week high of $28.3—more than tripling from its 52-week low of $8.58. Even with volatility (down 3.69% over the previous week and down 13.39% over the prior month), the shares were still up 18.75% over the last year. The message from the market was basically: UNFI isn’t out of the woods, but it no longer looks like it’s inevitably headed for the trees.

None of this means the competitive landscape got easier. If anything, UNFI’s progress raises the bar for everyone else. Rivals like KeHE Distributors, Core-Mark Holding Company, and SpartanNash face their own pressure to optimize supply chains, expand natural and organic offerings, and invest in digital capabilities.

And then there’s the relationship that still defines the entire story. The Whole Foods contract extension through 2032 buys UNFI stability and time. But Amazon’s investment in SpartanNash is a reminder that nothing in this ecosystem is ever permanently safe—especially when your biggest customer is also one of the most capable logistics operators on the planet.

XV. The Future: What Happens Next

From here, UNFI’s story doesn’t branch into a hundred paths. It really comes down to four.

Scenario 1: Successful Turnaround — The transformation finally shows up where it matters: in margins and cash. Operating margins push past the two-percent mark, leverage drops below three times EBITDA, and the stock starts trading like a steady, improving operator instead of a perpetual “fixer-upper.” This is the world where automation, network optimization, and higher-value services actually compound into a better business. Probability: 20–30%.

Scenario 2: Muddle Through — UNFI keeps its footing, but never escapes the industry’s gravity. Margins improve, but slowly. Debt comes down, but not fast enough to feel like freedom. Revenue stays roughly flat or grows modestly, and the stock grinds along without a clean rerating. In this version, the most likely “win” is eventually getting bought for a modest premium—less a triumph than an exit ramp. Probability: 40–50%.

Scenario 3: M&A Exit — A larger distributor or private equity decides UNFI’s scale is worth more in someone else’s hands than as a standalone public company. The pitch would be straightforward: stable demand, real assets, and meaningful synergies for a buyer who can integrate and cut costs. Shareholders get a one-time pop, but the long-term upside belongs to whoever writes the check. Probability: 15–20%.

Scenario 4: Disruption and Decline — The bear case turns into the plot. Amazon pulls more distribution in-house or shifts meaningful volume elsewhere, and the ripple hits other large customers, too. Revenue starts sliding, leverage stops looking manageable, and the company gets forced into restructuring—or worse. Probability: 10–15%.

Key Metrics to Watch:

If you’re tracking whether UNFI is heading toward scenario one or drifting toward scenario four, two numbers tell most of the story:

-

Adjusted EBITDA Margin — The cleanest read on whether the machine is truly getting better. It’s been running around the high-ones to roughly two percent of revenue. A sustained move higher would suggest real operational leverage. A slide back into the mid-ones would be a warning that the squeeze is tightening again.

-

Net Debt to Adjusted EBITDA Ratio — The scoreboard for financial flexibility. It has been sitting in the mid-threes depending on the quarter. A move toward three times and below would mean the balance sheet is loosening up. A move back above four times would mean the company is running out of room again.

After that, the telltales are more contextual: same-customer sales, the Supernatural segment as a proxy for Whole Foods momentum, and customer retention—because in distribution, losing volume isn’t just losing revenue. It’s losing the density that makes the whole network work.

XVI. Epilogue and Reflections

There’s a profound irony in UNFI’s story. It sits in the most essential, least celebrated part of the food system: the infrastructure that makes sure organic quinoa shows up at Whole Foods, that the independent co-op downtown can stock many of the same products as national chains, and that small suppliers can reach markets they could never reach on their own.

Walk into almost any grocery store in America and there’s a good chance UNFI touched a meaningful share of what’s on the shelves. You just don’t see it. The trucks move at night. The warehouses run in industrial parks you’ll never visit. The people—drivers, pickers, packers, and merchandisers—do the work that keeps the modern grocery machine from stalling.

And yet UNFI remains largely invisible. There’s no consumer brand halo. No emotional marketing. No “made by UNFI” label anyone looks for. Just the quiet discipline of getting the right items to the right dock doors, on time, across dry, chilled, frozen, and fresh—day after day, at scale.

The business has never been easy. Margins have always been thin. The squeeze has always been real: suppliers on one side, powerful retailers on the other. Technology keeps raising the bar, and the co-op-minded founders of the 1970s never could’ve pictured the debt, the integration complexity, and the public-market pressure their successors would inherit.

The surprising part of the story isn’t that UNFI has struggled. It’s that it’s still standing.

After the Amazon shock, the SUPERVALU integration, the margin crisis, and years of balance-sheet stress, the machine keeps running. Tens of billions in revenue. Roughly 25,000 employees. More than 30,000 customer locations served. For all the volatility on earnings calls, groceries still get delivered.

Whether UNFI ultimately becomes a great investment is still an open question. The structural challenges are real, the competitive threats are serious, and the margin for error stays slim.

But if you want to understand how commerce actually works—how products move from producers to shelves, how value gets created but not always captured, and how vital infrastructure can operate in near-total obscurity—UNFI is a case study hiding in plain sight.

The trucks will roll tonight. The warehouses will hum. Tomorrow, the shelves will be stocked. That’s the invisible empire that makes the whole thing possible.

XVII. Further Reading and Resources

Top 10 Long-Form Resources:

-

UNFI Investor Relations (ir.unfi.com) — Annual reports, 10-Ks, and quarterly filings are the cleanest source for understanding what actually happened, when it happened, and how the numbers moved.

-

"The Everything Store" by Brad Stone — The best single-volume backdrop for why Amazon changes the bargaining power in every industry it touches, grocery included.

-

Grocery Dive and Supermarket News — Two trade publications that track the grocery supply chain in real time, including UNFI’s customer moves, competitive pressure, and category shifts.

-

SUPERVALU Acquisition Analysis — 2018-era Wall Street research that captures the original bull case, the integration risks, and the leverage concerns that ended up defining the next few years.

-

IBISWorld Industry Reports — A useful, sober view of food distribution economics: why it’s big, why it’s essential, and why it’s so hard to make great returns.

-

Sysco and US Foods Investor Materials — Competitor filings and presentations that help you triangulate what “good” looks like in distribution—and how different end-markets shape margins.

-

Amazon Whole Foods Case Studies — Academic and consulting write-ups on how the acquisition reshaped grocery pricing, supply chain strategy, and the logic of vertical integration.

-

"Grocery: The Buying and Selling of Food in America" by Michael Ruhlman — A ground-level look at how grocery really works, and why the industry’s incentives often produce strange outcomes.

-

Supply Chain and Logistics Textbooks — For the mechanics: network design, route density, warehouse ops, cold chain, and why small percentage improvements matter so much at scale.

-

Hamilton Helmer's "7 Powers" — A sharp framework for asking the uncomfortable question at the heart of UNFI’s story: where is durable advantage supposed to come from in a business built on being the middle layer?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube