Unicycive Therapeutics: The "Best-in-Class" Bet on Renal Disease

I. Introduction & Episode Roadmap

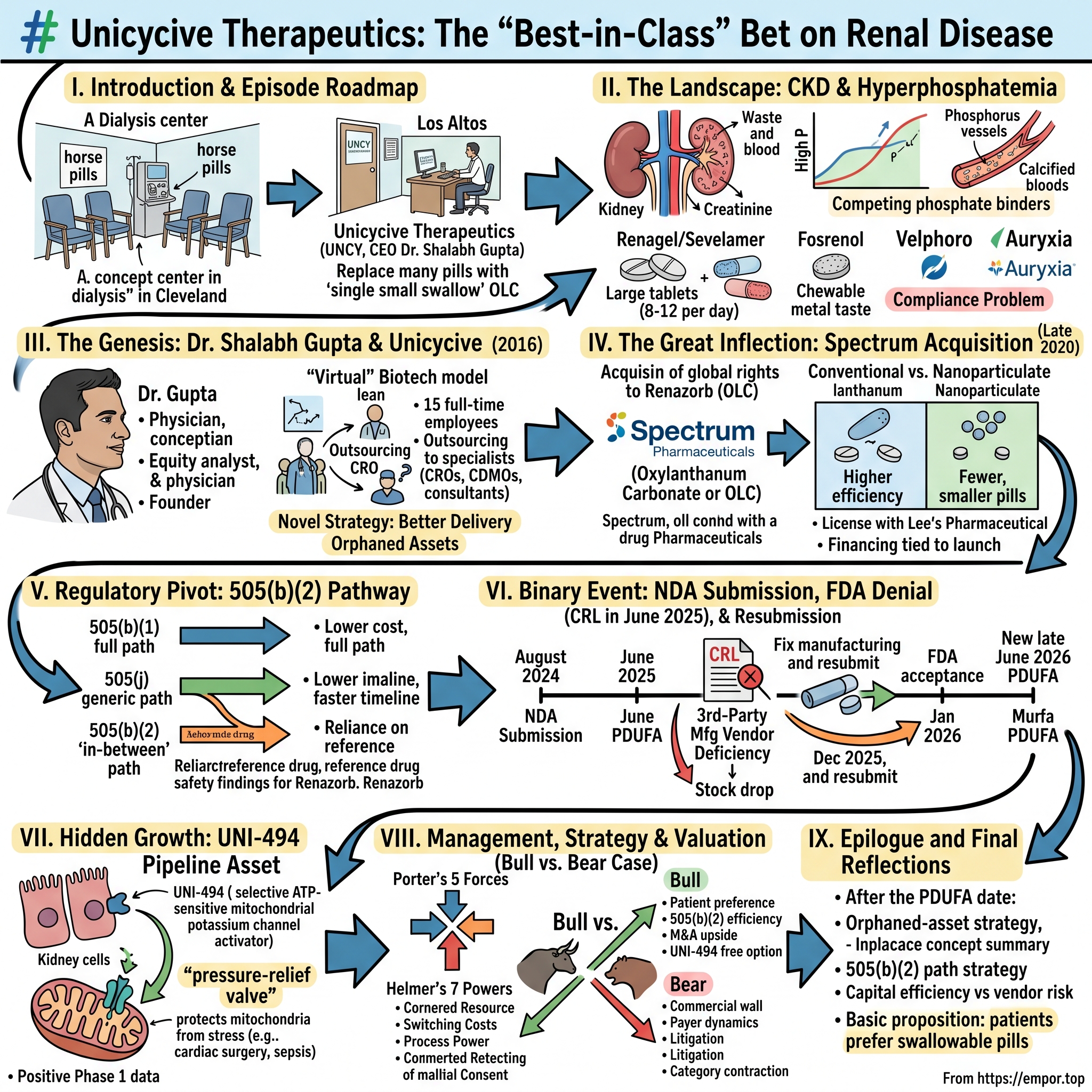

Picture a dialysis center on a Tuesday morning in suburban Cleveland. The fluorescent lights hum, the chairs recline at that familiar angle, and the patients — most of them on Medicare, most of them older than 60 — have settled in for their thrice-weekly four-hour ritual of having their blood scrubbed clean. On the rolling table next to each chair sits a small mountain of pill bottles. There is the blood-pressure pill. The diuretic. The statin. The vitamin D analog. The erythropoietin-stimulating agent. The iron supplement. The potassium binder. And then, the worst of them all by sheer volume: the phosphate binders. Chalky tablets the size of a quarter, three with every meal, every snack, every day, for the rest of life. Patients call them "horse pills." Nephrologists call them "the compliance problem." Pharmaceutical executives, for the last twenty years, have called them a multi-billion-dollar market that nobody has managed to truly fix.

Now picture a different scene: a small office park in Los Altos, California, where a company with fewer than 15 full-time employees believes it has cracked the code.1 No factories. No giant sales force. No European headquarters. Just a CEO with a stethoscope hanging behind his desk, a contract manufacturing organization halfway across the country, and a single late-stage drug candidate that could, if it clears its final regulatory hurdle, turn that pile of horse pills into a single small swallow.

That is the bet of 유니사이시브 — well, no, it is not Korean. It is Unicycive Therapeutics, NASDAQ ticker UNCY, and the bet is whether a tiny, virtual biotech can do what entire divisions inside Sanofi, Takeda, and CSL Vifor have not: deliver a meaningfully better pill to the global hyperphosphatemia market.

This is the story of how Dr. Shalabh Gupta — a Mumbai-trained physician turned Wall Street equity analyst turned biotech founder — built Unicycive on the premise that some of the most valuable assets in pharma are not sitting in the labs of the giants. They are sitting in the corners of divestiture spreadsheets, "orphaned" by strategic pivots, waiting for someone with the patience and capital discipline to push them across the finish line. It is the story of an asset called Renazorb — now formally known as Oxylanthanum Carbonate, or OLC — that Spectrum Pharmaceuticals walked away from in late 2020 as it shifted its focus to oncology, and that Unicycive picked up for a fraction of what it would cost to develop from scratch.2

It is also a story with scars. The road from "promising drug candidate" to "approved therapy" runs through the most unforgiving regulator in the world, and Unicycive learned that lesson the hard way. On June 30, 2025, the FDA issued the company a Complete Response Letter — biotech's most dreaded three letters — and the stock fell almost 30% in a single session.3 Class-action lawyers descended within weeks.4 The CEO, the CFO, and the lean management team had to spend the back half of 2025 doing the unglamorous, deeply technical work of fixing a third-party manufacturer's compliance status and resubmitting paperwork they thought they had already finished.

We are recording this on May 24, 2026, with the resubmitted NDA accepted by the FDA, a new PDUFA target action date set for late June 2026, and the company sitting on roughly $55 million in cash — enough, by management's own guidance, to run the business into 2027.5 In a month, the FDA's verdict on Oxylanthanum Carbonate will arrive. So today we trace the full arc: from the founding of the company in 2016, to the acquisition of Renazorb in 2020, to the gamble on the 505(b)(2) regulatory pathway, to the second-asset optionality of UNI-494, to the white-knuckle months of 2025, and finally to the question every long-term investor in this name has to answer: what does the day after FDA approval look like, and does the bet justify the wait?

Let's begin where every story in nephrology has to begin — with the patients, and with the pills.

II. The Landscape: The Burden of Chronic Kidney Disease

The kidney is the body's quietest organ. It does not pump like the heart, it does not breathe like the lungs, it does not think like the brain. It filters. About 180 liters of blood pass through the human kidney every day, and from that volume the organ pulls out the metabolic waste — urea, creatinine, excess electrolytes, and the one element that turns out to matter most for our story: phosphorus.

Phosphorus is essential. It builds bones, it powers the ATP molecule that runs every cell in the body, and it is in nearly every food we eat — meat, dairy, beans, nuts, sodas with phosphoric acid, and most insidiously, the phosphate additives that line ingredient labels in processed foods. In a healthy person, the kidneys excrete excess phosphorus into urine and the body keeps blood levels in a tight range, somewhere between 2.5 and 4.5 milligrams per deciliter. In a person with chronic kidney disease — and especially in the roughly 550,000 Americans whose kidneys have failed entirely and who depend on dialysis — that filter no longer works.6 Phosphorus builds up. And when it builds up, the body starts borrowing calcium from bones to neutralize it, hormones called FGF-23 and parathyroid hormone go haywire, soft tissues calcify, blood vessels stiffen into something resembling porcelain, and the patient's risk of death — from a heart attack, from a stroke, from a sudden cardiac event — climbs in a way that is hard to overstate. The clinical literature is brutal on this point. Hyperphosphatemia is not a nuisance. It is one of the strongest non-traditional predictors of mortality in the dialysis population.7

So what does the dialysis patient do? Three days a week, they sit in the chair for four hours and let a machine do the filtering. But on the other four days — and even on dialysis days, between sessions — the phosphorus from food keeps coming in. The answer, for the last two decades, has been a class of drugs called phosphate binders. They are not absorbed by the bloodstream. They sit in the gut, latch onto dietary phosphorus, and ferry it out through stool. Taken with every meal, they keep blood phosphorus in check.

The history of this market is a tour through the giants of pharma. The first widely used binder was calcium carbonate — basically antacid in disguise — but it loaded patients with so much calcium that it accelerated vascular calcification, the very thing nephrologists were trying to prevent. In 1998, Genzyme launched Renagel (sevelamer hydrochloride), a calcium-free polymer; it became a blockbuster, and after Sanofi's $20 billion acquisition of Genzyme in 2011, sevelamer continued as one of the bedrock therapies in dialysis pharmacy.8 Around the same era, Shire — and later Takeda, after Takeda's $62 billion takeover of Shire — commercialized Fosrenol (lanthanum carbonate), a rare-earth-metal-based binder so potent that, on paper, it should have dominated.9 Then came Velphoro (sucroferric oxyhydroxide), an iron-based binder developed by Vifor Pharma, which in turn became part of CSL after CSL's $11.7 billion acquisition of Vifor in 2022.10 Akebia commercialized Auryxia (ferric citrate), which had the dual benefit of binding phosphorus and treating iron deficiency anemia.

Five major branded binders. A combined commercial footprint that, at peak, exceeded $1.5 billion annually in the U.S. alone, and yet — every single nephrologist will tell you the same thing — patients hate them.

Here is why. Sevelamer's standard dose runs eight to twelve tablets per day, each tablet about the size of a multivitamin. Fosrenol's tablets are smaller, but they must be chewed — they don't dissolve in the stomach the right way otherwise — and they taste, in the words of one Reddit dialysis-patient thread, "like licking chalk soaked in metal." The iron-based binders cause GI side effects so consistently that patient discontinuation rates are notorious. The pill burden — the total number of tablets a dialysis patient swallows per day, across every prescription — averages 19 pills.11 Phosphate binders alone account for roughly half of that load.

The result is what nephrologists call the compliance gap. Studies have shown that adherence to phosphate binders is lower than to almost any other chronic medication, and that hyperphosphatemia goes uncontrolled in a majority of dialysis patients despite available therapy. The market is enormous and the unmet need is, paradoxically, equally enormous. Everyone has a drug. Nobody has a drug patients actually want to take.

That is the seam in the market that Unicycive walked into. Not "invent a new mechanism" — the mechanism works fine. Just "make the pill smaller, fewer, and easier to take." If you can do that, in a category where patients on average are still missing their phosphorus targets, you have something worth fighting for.

Hold that thought, because in 2016, in a small office in Los Altos, a doctor-turned-banker-turned-founder was about to ask exactly that question.

III. The Genesis: Dr. Shalabh Gupta and the Founding of Unicycive

Dr. Shalabh Gupta does not look or sound like the prototypical biotech CEO. He is not a PhD chemist who spun something out of MIT. He is not a serial pharma executive on his fifth job in C-suite. He is a physician — internal medicine, with a research fellowship in cardiopulmonary rehabilitation at NYU School of Medicine — who one day decided he wanted to know how money worked.12

Gupta's path bears retelling because it explains, more than anything else, how Unicycive came to exist in the form it did. He trained in medicine at Jawaharlal Institute of Postgraduate Medical Education & Research in Pondicherry, India — one of the country's elite government medical institutes, a place where the cohorts are small, the competition is brutal, and the culture leans heavily toward academic rigor.12 He moved to New York, completed his residency, served as an attending physician at NYU Medical Center, and along the way did something most physicians never do: he enrolled at NYU's Robert F. Wagner Graduate School of Public Service for a Master's in Public Administration with a concentration in Health Care Finance and Management.

That second degree was the pivot. After Wagner, Gupta crossed the river into Wall Street. He became an equity research analyst covering U.S. pharmaceutical companies at UBS Investment Bank, and later moved to Rodman & Renshaw — now HC Wainwright — to cover biotech.12 Sell-side biotech analyst is a specific kind of job. You sit in a Midtown office building, you read hundreds of clinical-trial readouts, you build NPV models for assets that may or may not exist five years later, and you learn — quickly and painfully — that the difference between a $200 million market cap biotech and a $5 billion market cap biotech is rarely the science. It is usually the strategy. Which asset to license. Which trial endpoint to choose. Which regulatory pathway to take. Which partner to bring in. Which dilution to accept.

After his time on the buy- and sell-side, Gupta did a tour at Genentech in commercial strategy, then founded Globavir, a diagnostics company that licensed technology from Stanford. By 2016, he was 40-ish, with the rare CV combining real clinical training, real Wall Street experience, real commercial pharma experience, and real founder experience. That was the year he started Unicycive.12

The founding thesis was modest, almost contrarian. Most biotech founders start with novel science — "we discovered this molecule, let's figure out what it does." Gupta started with novel strategy — "let's find molecules that already work and figure out how to deliver them better." He had spent a decade watching big pharma divest perfectly viable assets because they did not fit a strategic narrative. Velphoro had been sold from one company to another. Auryxia had been licensed and sublicensed across continents. The story of nephrology pharma was littered with assets that had clinical validation but no champion. Gupta's bet was that the right business model was not a lab; it was a scouting operation paired with a regulatory engine.

He kept Unicycive lean from day one. The team has stayed in the single digits to low teens of full-time employees for nearly a decade. The company does not own a manufacturing plant. It does not own a fill-finish line. It does not own its own clinical-trial operations infrastructure. Everything is outsourced to specialists — contract research organizations to run the trials, contract development and manufacturing organizations to make the drug, regulatory consultants to file the paperwork, and a small handful of in-house executives to coordinate the whole thing. The bet, in capital-markets language, is that R&D dollars are most valuable when spent on assets, not on overhead.

This is what the industry calls a "virtual" biotech model. Roivant, the SoftBank-backed roll-up vehicle that built a small empire of "Vant" companies around derisked assets, made the model famous. Unicycive predates much of the Roivant playbook, but it operates on the same logic: in biotech, the marginal dollar spent on a half-empty office is a dollar not spent on a Phase 3 trial.

It is worth being honest about the downside of this model, because investors who have lived through the last twelve months of Unicycive have learned it. When you do not own your own factories, you do not control your own factories. When the FDA finds a deficiency at one of your contract manufacturers — even one entirely unrelated to your drug — you bear the consequences. The CRL of June 2025, the company has insisted publicly, had nothing to do with the science of Renazorb itself. It had everything to do with the compliance status of a third-party vendor.3 In a model built on outsourcing, that vendor risk is structural, not accidental.

But for the first eight years of Unicycive's life, the leanness was the strategy and the strategy was the leanness. Now we get to the moment that turned a small team with a thesis into a small team with a product.

IV. The Great Inflection: The Spectrum Pharmaceuticals Acquisition

Every biotech has a moment when it stops being a thesis and starts being a real company. For Unicycive, that moment came in late 2020, when it signed an asset purchase agreement with Spectrum Pharmaceuticals to take over the global rights to Renazorb — what is now known as Oxylanthanum Carbonate, or OLC.2

To understand why this deal mattered, you have to understand Spectrum's position at the time. Spectrum had spent years trying to be many things — a specialty pharma in oncology, a hematology franchise, a generic injectable platform — and by 2020 the company was undergoing yet another strategic pivot, narrowing its focus toward two late-stage oncology assets, ROLONTIS and Poziotinib. Renazorb did not fit the new narrative. It was a renal asset in a portfolio trying to become an oncology asset. In the language of corporate strategy, it was orphaned.

For a small company like Unicycive, an orphaned asset inside a strategic-pivot story is a gift. You are not bidding against another buyer. You are not navigating a competitive auction. You are negotiating with a counterparty that has already decided, internally, that the asset is non-core. The terms reflected that dynamic. Under the asset purchase agreement, Unicycive acquired global rights to Renazorb and its associated patents, and Spectrum received an equity interest in Unicycive plus the right to milestone and royalty payments tied to development and commercialization.2 Compare this to what it would cost to develop a phosphate binder from scratch — somewhere north of $200 million, by industry rule of thumb — and the deal structure starts to look like a masterclass in capital discipline. No large upfront cash payment to drain the balance sheet. Equity dilution as the primary consideration. Milestone payments only if and when the drug actually generates value. Royalty payments only against real revenue.

Benchmark this against the bigger names in the binder market. Velphoro alone changed hands when CSL paid roughly $11.7 billion for the entire Vifor Pharma platform in 2022.10 Even allocating a fraction of that deal value to Velphoro, the unit economics dwarf anything Unicycive paid in 2020. Auryxia, the ferric citrate binder, has been the subject of multiple licensing and asset deals across Akebia, Keryx, and partners abroad — also at valuations vastly exceeding Unicycive's transaction. Looking at the math, Unicycive bought into the phosphate-binder market for, in effect, pennies on the dollar relative to incumbents. This is what value investors mean when they talk about "buying the seat at the table," and in biotech, the seat at the table is the IND-cleared, clinically-validated asset.

But the seat is only valuable if the asset itself is differentiated. So let's talk about the science.

Fosrenol — the existing branded lanthanum carbonate from Takeda — works. The problem is that lanthanum carbonate, in its conventional formulation, is enormous. The tablets are chewable, but they have to be chewed thoroughly, which patients hate. The total daily dose can run into several grams of material. Renazorb's proprietary nanoparticulate formulation changes the surface-area dynamics of the lanthanum. By engineering the particle size down into the nanometer range, the drug exposes vastly more reactive surface area per unit of mass. More reactive surface area means more efficient phosphate binding per gram of drug. More efficient binding per gram means smaller pills. Smaller pills mean fewer pills. Fewer pills, swallowed instead of chewed, mean — finally — a phosphate binder that might actually fit into a dialysis patient's daily life without becoming the worst part of it.

The clinical work to validate this was done with the 505(b)(2) regulatory framework in mind from the start — more on that pathway in the next section — and the pivotal study comparing Renazorb to Fosrenol completed enrollment in 2023. The pharmacokinetic and pharmacodynamic readouts supported what Unicycive needed: that this smaller, easier-to-take formulation delivers the same phosphate-lowering biology that lanthanum carbonate has been delivering for two decades.13

In the four years between the Spectrum deal and the NDA submission, Unicycive layered on additional optionality. In July 2022, the company signed an exclusive license and development agreement with Lee's Pharmaceutical Holdings, granting Renazorb rights in China, Taiwan, Hong Kong, Macau, Vietnam, Thailand, and several other Asian markets in exchange for upfront payment, milestone payments, and royalties.14 In March 2023, Unicycive announced a financing structure of up to $130 million tied to commercial launch readiness for Renazorb.15 Both of these moves were classic small-biotech blocking and tackling: monetize geographies you cannot economically serve yourself, and pre-build the capital runway you will need on the day approval comes.

The Spectrum acquisition, in retrospect, is the foundation under everything else Unicycive has done. Every strategic decision since 2020 — the 505(b)(2) gamble, the Asia license, the financing structure, the lean headcount, even the second asset UNI-494 — has been an attempt to maximize the value of the asset Gupta picked out of someone else's orphan pile. The next question was the regulatory question, and that question turned out to be the most consequential.

V. The Regulatory Pivot: The 505(b)(2) Pathway

There is a quiet provision in U.S. drug law that has, over the last two decades, become one of the most important tools in small-biotech strategy. It is called the 505(b)(2) pathway, and it is the difference, for a company like Unicycive, between trying to climb a regulatory mountain and trying to walk up the same mountain on a path someone else already cleared.16

Here is the short version, in the kind of language you would actually use at a dinner party. Under U.S. law, a New Drug Application can be filed three ways. The 505(b)(1) is the full path — invent a new molecule, run your own full safety and efficacy studies from scratch, prove the entire case top to bottom. The 505(j) is the generic path — show that your version of an existing drug is the same as the original and you get a label that exactly mirrors the brand. The 505(b)(2) is the in-between path. You bring a new product to market — a new formulation, a new dosage, a new combination — but you do not have to re-prove the basic safety and efficacy of the underlying active ingredient. Instead, you rely on the FDA's existing finding of safety and efficacy for the reference drug, and you only have to prove the parts that are actually different.

For Unicycive, this changed the economics of the entire program. Lanthanum carbonate's safety profile was established more than fifteen years ago through Shire's Fosrenol approval. The kinetics of how lanthanum binds phosphorus in the gut, the toxicology, the long-term tolerability — all of that was already in the FDA's institutional knowledge. What Unicycive had to prove was narrower and more focused: that its nanoparticulate formulation delivers the same phosphorus-binding pharmacodynamic outcome at lower pill burden, with acceptable bioequivalence on the relevant metrics.

That is a very different trial than a 505(b)(1). It is smaller. It is faster. It is dramatically cheaper. And it concentrates the risk into a much narrower clinical question, which means you either succeed cleanly or you fail cleanly — there is much less in between.

The pivotal study did succeed cleanly. In June 2023, Unicycive announced successful completion of its pivotal clinical study for Renazorb.13 The data supported the bioequivalence and pharmacodynamic case the company needed. Through the second half of 2023 and into 2024, the team worked through the manufacturing scale-up, the chemistry-manufacturing-controls package, and the formal NDA assembly. On August 14, 2024, Unicycive announced submission of the NDA to the FDA.[^17] The agency accepted it for review and set an original PDUFA target action date of June 28, 2025.

For most of the year between August 2024 and June 2025, the company traded — and was discussed by investors — as a binary event stock. The thesis was simple. If approval came on the original PDUFA date, Renazorb would launch into a market with hundreds of thousands of dialysis patients in the U.S. alone, and the company's commercial team — combined with the financing facility put in place in 2023 — would push for share against Fosrenol, Velphoro, sevelamer, and Auryxia. The valuation gap between a pre-approval small biotech and a launching-product small biotech can be enormous, and management was guiding to commercial readiness throughout 2025.

Then came the Friday before the PDUFA date.

On June 30, 2025, Unicycive announced that the FDA had issued a Complete Response Letter, declining to approve Oxylanthanum Carbonate in its current form. The CRL did not cite any clinical safety concerns. It did not cite any efficacy concerns. It did not cite preclinical issues. It cited a single deficiency tied to the compliance status of a third-party manufacturing vendor.3 The asset itself was clean. The plant that was supposed to make it commercially was not. The stock fell 29.85% to close at $4.77 that day, and within weeks securities class-action firms had filed suit, alleging that management had presented OLC as on track for approval while underrepresenting the manufacturing risk.4

This is where Unicycive's virtual-company structure cut both ways. The good news: the science was uncontaminated. There was nothing wrong with the molecule. The bad news: the company had to either wait for the third-party manufacturer to regain FDA compliance, or qualify a second manufacturing site from scratch. Either path took time. Either path cost money. And either path required the company to do something it had spent its whole life avoiding — wade deep into the operational details of a manufacturing facility it did not own.

To management's credit, they pursued both options in parallel. They engaged the FDA in a Type A meeting to align on the resubmission requirements, they accelerated qualification of a second manufacturing vendor that had already produced OLC drug product, and they pushed the original vendor to remediate. By December 29, 2025, the company announced it had resubmitted the NDA.17 On January 29, 2026, the FDA accepted the resubmission, classified it as a Class II Complete Response with a six-month review period, and set a new PDUFA target action date in late June 2026.5

If approval comes, the 505(b)(2) gamble will have paid off — but with a tax. The tax is the year of lost commercial momentum, the cash burn through 2025 and into 2026, the litigation overhang, and the credibility hit with public-market investors who do not always distinguish between "the drug failed" and "the contract factory failed." Internally, the story can be told as a vindication of the strategy: the regulatory pathway worked, the science worked, the partner choice failed and was replaceable. Externally, the question for every long-term investor is whether the company has now de-risked the manufacturing dimension well enough to clear the second PDUFA cleanly.

The next month will tell us. But while the world has been watching the Renazorb saga, a second asset has been quietly maturing in the background.

VI. "Hidden" Growth: UNI-494 and the Acute Kidney Injury Frontier

There is a category of patient that almost nobody outside nephrology and intensive care ever thinks about, and yet they sit in hospital beds in every academic medical center every single night. They have not been diagnosed with kidney disease. They do not need dialysis. They are not on phosphate binders. They are post-operative cardiac surgery patients, sepsis patients, severely dehydrated trauma patients, contrast-induced nephropathy patients, and chemotherapy patients whose kidneys, for reasons that are often poorly understood at the bedside, suddenly stop working. The clinical term for this is Acute Kidney Injury — AKI — and depending on how you measure it, it affects somewhere between 10% and 20% of hospitalized patients and a striking 50%+ of intensive-care patients.

Here is the dirty secret of nephrology in 2026: there is no approved drug therapy for AKI. The standard of care is, essentially, supportive — manage fluids, remove offending agents, dialyze if you have to, and hope the kidneys recover. The reason is that AKI is mechanistically complicated. It involves oxidative stress, mitochondrial dysfunction, inflammatory cascades, and microvascular damage all unfolding within hours. Many candidate drugs have entered trials. None has emerged with an approval label.

This is, in Unicycive's bull case, the optionality that nobody is pricing in. While the world watches the Renazorb saga, the company has been quietly advancing UNI-494, a small molecule asset that takes a completely different approach to kidney biology.

UNI-494 is what pharmacologists call a selective ATP-sensitive mitochondrial potassium channel activator.18 If that phrase made your eyes glaze over, here is the analogy. Think of the mitochondrion — the little energy-producing factory inside each cell — as a hydroelectric dam. Under normal conditions, water flows through the dam in a controlled way, producing energy efficiently. Under stress conditions — say, after a kidney is starved of oxygen during cardiac surgery — the dam gets overwhelmed, the flow becomes turbulent, and the dam starts to break down. The cell starts to die. UNI-494 acts like a pressure-relief valve. By selectively opening a specific potassium channel in the mitochondrial membrane, it lets the system depressurize, preserves the integrity of the mitochondrial machinery, and gives the kidney cell a chance to ride out the insult without dying. The technical term is "mitochondrial preconditioning" or "mitochondrial protection."

Phase 1 testing in healthy volunteers, completed in October 2024, found the drug safe and well-tolerated across single ascending doses from 10 mg to 160 mg and multiple ascending doses at 40 mg twice daily.18 The 80 mg twice-daily dose was not as well tolerated, suggesting an upper bound for the dosing range in future studies. Importantly, the pharmacokinetic profile was consistent with rapid absorption and metabolism — which is what you want for an acute, in-hospital indication where you are dosing around a known insult like cardiac surgery rather than chronically.

The strategic logic of UNI-494 inside the Unicycive portfolio is worth pausing on. Renazorb plays in a crowded market against branded incumbents who collectively spend hundreds of millions of dollars a year on nephrology sales forces. Even with a best-in-class profile, every dollar of Renazorb revenue is a dollar fought for against entrenched competition. UNI-494 plays in an empty market. There is no Fosrenol-equivalent in AKI. There is no Velphoro-equivalent. If UNI-494 reaches a positive Phase 2 readout, the asset value is not bounded by the pricing dynamics of an existing category — it is set by the unmet need of a category that has never had a drug.

Now, the caveat. Phase 1 to Phase 2 to Phase 3 in a complex, multi-mechanism indication like AKI is a long and historically punishing road. Many before UNI-494 have entered with promising preclinical data and excellent Phase 1 safety profiles, only to fail in the heterogeneous patient populations of Phase 2. The honest reading of UNI-494 today is that it is interesting optionality on a multi-year time horizon, not a near-term revenue driver. In August 2025, the company secured a new U.S. patent extending protection of UNI-494 specifically for chronic kidney disease — a quiet but meaningful sign that management is thinking about the asset as more than a one-indication play.19

For a sub-$300-million market-cap company in 2026, having a second pipeline asset with this kind of pharmacology — and this kind of unmet-need profile — is the kind of thing that matters more in the bull case than in the bear case. If Renazorb approves and launches, UNI-494 is a free option. If Renazorb stumbles, UNI-494 is the bridge to a future pipeline beyond the original Spectrum acquisition. Either way, it broadens the company's identity from "single asset binary event" to "renal-focused platform with two distinct mechanisms," which is exactly the kind of identity that potential acquirers tend to value.

Speaking of identity and acquirers, we should talk about the people running this thing.

VII. Management, Incentives, and the "Skin in the Game"

A small biotech is, more than almost any other kind of company, a bet on the people. There is no installed base of customers. There is no diversified product portfolio. There is no factory that grinds out earnings every quarter regardless of who is in the corner office. There is a thesis, a balance sheet, a regulatory pathway, and a CEO. Get the CEO wrong, and the rest of it does not matter.

We have already met Dr. Shalabh Gupta — physician, equity analyst, commercial strategist, serial founder. Inside Unicycive, he has worn the title of Founder, Chairman, and CEO since the company's formation, and the management team around him reflects the lean philosophy of the company itself.1 John Townsend, the Chief Financial Officer, has handled the capital-markets work — the public listings, the secondary offerings, the financing facilities, and now the unfortunate task of being named in the securities class-action suit alongside Gupta.4 The clinical, regulatory, and commercial heads are similarly small in number and broad in responsibility, the way they always are in companies that do not believe in headcount for its own sake.

What does the incentive structure look like? Based on the company's proxy statement, the management compensation packages are weighted heavily toward equity, with vesting and milestone triggers tied to regulatory and clinical events.20 In plain English: management gets paid the most when the company actually delivers the things the company exists to deliver — an NDA filing, an FDA approval, a clinical readout. This is the alignment story Gupta has consistently emphasized in investor presentations: significant insider ownership, equity-heavy comp, and modest cash burn on executive salaries relative to industry norms.

It is worth noting that this alignment story has been tested in a very specific way over the last twelve months. When the FDA issued the CRL in June 2025, the stock did not just fall — the equity holdings of management fell with it. Whatever criticisms one might level at the company's manufacturing oversight pre-CRL, the financial pain of the CRL was, by design, shared with management on a percentage basis. That is the structural argument for insider ownership.

The board of directors fills out the picture. Unicycive's board has historically included individuals with deep nephrology, regulatory, and capital-markets backgrounds — the kind of people who have either run drug-approval processes from the inside, or financed biotechs through the same kind of binary milestones the company is navigating now.21 In small-cap biotech, the quality of the board is often a better tell than the quality of the management team, because a strong board can replace a weak CEO but a weak board cannot save a strong company that has lost its way.

The other dimension of "skin in the game" worth talking about is capital structure discipline. Small biotechs, particularly pre-revenue ones, live and die by their ability to time capital raises. Raise too early at too low a price, and you over-dilute existing shareholders for years. Raise too late after a bad event, and you may not be able to raise at all. Unicycive's path through 2023 to 2026 has included the up-to-$130-million commercial-launch financing announced in March 2023, follow-on equity offerings, and the strategic Lee's Pharmaceutical license that brought in non-dilutive capital tied to the Asia geography.1415 As of the company's most recent disclosure — the full-year 2025 results released on March 30, 2026 — cash, cash equivalents, and marketable securities stood at approximately $54.9 million, with management guiding to a runway into 2027.5 For a company facing a PDUFA date in late June 2026, that is enough cash to absorb an approval-and-launch scenario, and enough cash to absorb a delay scenario without an emergency raise.

The 2025 P&L itself paints the picture of a late-stage biotech in the year of its CRL. Full-year R&D came in at $9.1 million, G&A at $20.4 million, and net loss for the year was $26.6 million, or $1.67 per share.5 The G&A number relative to R&D is elevated for a company at this stage, and that reflects two things: the build-out of commercial readiness functions in anticipation of launch, and the legal and consultancy overhang from the CRL and the class-action filings. Both of those, in management's narrative, are temporary expenses that normalize after approval and commercial stabilization.

Whether one believes that narrative comes down to how one weights the risks. And that is exactly what the next two sections are about.

VIII. Playbook: Porter's Five Forces and Hamilton Helmer's Seven Powers

Every Acquired episode eventually arrives at the strategy framework, and Unicycive is no exception. The reason these frameworks matter for a small biotech is that the financial statements alone do not tell you anything useful — there is no revenue, the losses are largely a function of trial design choices, and the cash position is a function of when the last raise happened. What you actually need to know is whether, in the long run, there is a moat. So let's run Unicycive through both lenses.

Starting with Hamilton Helmer's Seven Powers, the question is which of the seven actually applies. Scale economies — probably not, because a small phosphate binder is not a manufacturing-scale business. Network economies — no, drugs do not get more valuable when more people take them. Counter-positioning — only modestly, in the sense that incumbents like Takeda would have to cannibalize their own Fosrenol franchise to compete with a smaller-pill version, but a determined incumbent could in principle do it. Branding — minimal in pharma at the prescriber level, where label and clinical data drive prescribing more than brand.

That leaves three powers that are genuinely worth analyzing: Cornered Resource, Switching Costs, and Process Power.

Cornered Resource. This is the strongest power in Unicycive's case. The specific nanoparticulate formulation of lanthanum carbonate that Unicycive has developed is protected by issued patents and proprietary manufacturing know-how. A competitor cannot simply copy this formulation; they would have to invent their own approach to particle engineering, run their own pivotal study, and clear their own regulatory path. The 505(b)(2) pathway, paradoxically, makes this slightly easier for a follow-on competitor than a 505(b)(1) would have — because someone else could theoretically rely on lanthanum's existing safety data — but the specific nanoparticle work is genuinely proprietary, and the FDA's manufacturing requirements create substantial real-world friction for any would-be copier.

Switching Costs. This is where it gets nuanced. In phosphate binders, the switching costs sit not with patients but with prescribers and payers. A nephrologist who has built clinical comfort with Fosrenol over a decade does not switch lightly. Dialysis providers like 다비타 DaVita and Fresenius operate massive formularies and negotiate aggressively with manufacturers. The Medicare ESRD bundle changed the economics of dialysis-administered drugs in ways that have shifted phosphate binders into and out of the bundle over time. So the switching costs work against Unicycive on the prescriber side — but they work for Unicycive on the patient side, because once a patient has been switched to a smaller-pill regimen, they are very unlikely to want to switch back to a bigger-pill regimen. The bull case is that patient preference is so strong it pulls the prescriber along. The bear case is that prescribers are skeptical until population-level adherence data emerges, which takes years post-launch.

Process Power. Limited and probably not durable. Unicycive does not have a manufacturing process advantage — in fact, the events of 2025 are a stark illustration of the opposite. The process power, such as it is, sits in the regulatory and clinical operations expertise that Gupta and his team have accumulated over the last decade. That is real, but it is also portable, and it tends to live in individuals more than in institutional capability at this size.

Now Porter's Five Forces.

Threat of New Entrants is moderate. The barriers to entering the phosphate binder market are the same barriers Unicycive overcame — regulatory pathway, formulation IP, manufacturing capability — but they are not insurmountable. Generic versions of older binders exist. Novel mechanism candidates, particularly tenapanor (Ardelyx's XPHOZAH, a non-binder that blocks dietary phosphate absorption at the intestinal level), are already in the market and represent a real alternative for prescribers willing to switch class.

Bargaining Power of Buyers is high and getting higher. The buyers in dialysis pharma are not patients — they are integrated dialysis providers like DaVita and Fresenius, plus Medicare itself through the ESRD bundling rules. When these buyers consolidate purchasing decisions, they extract significant pricing concessions. Any new branded binder in this market enters into a price negotiation with a small number of very large counterparties. This is one of the most underappreciated risks in the Renazorb commercial story.

Bargaining Power of Suppliers is moderate. The active pharmaceutical ingredient and the contract manufacturers are not commodity inputs, and as 2025 painfully demonstrated, supplier risk in this industry can be company-defining. The remediation work and the qualification of a second manufacturing vendor are precisely the moves a company makes to reduce supplier power going forward.

Threat of Substitutes is high. SGLT2 inhibitors, originally diabetes drugs, have demonstrated significant kidney-protective benefits and are reshaping how nephrologists think about slowing CKD progression. Tenapanor — Ardelyx's XPHOZAH — represents a non-binder alternative mechanism for phosphate control. The long-term threat is not so much that Renazorb fails to take share from Fosrenol; it is that the entire phosphate-binder category gets compressed by upstream therapies that delay or reduce the need for phosphate management in the first place.

Industry Rivalry is moderate to high. The branded incumbents will not cede share gracefully, particularly Takeda with Fosrenol and CSL Vifor with Velphoro. Generic sevelamer competes on price. Auryxia competes with the iron-deficiency-anemia angle. Renazorb's wedge — the patient-preference, pill-burden story — is real but narrow.

The honest synthesis is this. Unicycive's most durable power is its Cornered Resource around the specific nanoparticulate formulation. Everything else is contingent on commercial execution, payer dynamics, and a category that is itself under threat from upstream mechanisms. That is enough to build a real business if Renazorb wins on patient preference at scale. It is not enough to build an unassailable moat. The strategic reality is that Unicycive's most likely long-term home is inside a larger renal franchise — which brings us to the bull and bear case.

IX. The Bull versus Bear Case

Let's start with the bear case, because in biotech, the bear case is always the one that demands respect first.

The bear case begins with a simple observation: a tiny company with fewer than 15 full-time employees has never, in the history of nephrology, successfully launched a phosphate binder against entrenched Big Pharma incumbents without either a partnership or an acquisition. The commercialization wall is real. To make Renazorb a meaningful franchise, Unicycive needs feet on the ground — sales reps calling on nephrology practices and dialysis centers — at a scale that the company has never operated at. Hiring a sales force is expensive, slow, and unforgiving of mistakes. The 2023 financing facility was meant to fund this, but it is not infinite, and the CRL of June 2025 burned through a year of optionality.

The bear case continues with the litigation overhang. The securities class action filed in 2025 — covering the period from March 29, 2024, through June 27, 2025, and naming Gupta and Townsend among the defendants — is unresolved.4 These cases generally settle, but they consume management time, legal fees, and credibility with public-market investors. For a company that has to spend the next eighteen months selling its narrative to potential commercial partners or acquirers, this is an unwelcome distraction.

The bear case extends into payer dynamics. Even with FDA approval, Renazorb has to win formulary placement at major dialysis providers, navigate Medicare's ESRD bundle, and price competitively against generic sevelamer. Each of these is a separate negotiation, and the leverage in each negotiation sits with the buyer. A best-in-class label does not automatically translate into best-in-class economics if the buyer says, "we love the science, here is the price we will pay."

The bear case finishes with the substitute threat. Tenapanor — Ardelyx's XPHOZAH — exists. SGLT2 inhibitors are expanding their role in CKD progression and may, over time, reduce the dialysis population itself. If you are a nephrology specialist looking at the 2030 phosphate-binder market, you have to model real category contraction risk.

Now the bull case.

The bull case begins with the patient preference logic, and on this dimension Renazorb is genuinely best-in-class. A pill that is smaller, swallowed instead of chewed, and required in lower daily counts is exactly the format that solves the compliance problem that has dogged this category for two decades. In medicine, when patients prefer one therapy over another within the same mechanistic class, market share follows — sometimes slowly, but reliably. The 505(b)(2) pathway means Unicycive does not have to prove that lanthanum works; it only has to prove that its formulation delivers lanthanum better. That is the easier of the two arguments to win in the marketplace.

The bull case continues with the asymmetry of the binary outcome. With approval expected in late June 2026, the valuation arithmetic is straightforward. Approval unlocks commercial launch, geographic expansion through partners like Lee's Pharmaceutical, and access to the financing capital that has been waiting on the sidelines for exactly this milestone. The market capitalization at approval has historically rerated meaningfully higher for similarly-positioned 505(b)(2) approvals in nephrology and beyond. The capital efficiency of the original Spectrum deal means that almost all of that incremental value accrues to existing shareholders rather than to the original asset seller.

The bull case extends into M&A optionality. Renazorb is, in the language of pharma business development, a "tuck-in" asset. A larger company with an existing nephrology sales force — think CSL Vifor, Takeda, or a private specialty pharma roll-up — could acquire Unicycive for a fraction of what it would cost to develop a comparable asset internally, plug Renazorb into an existing commercial infrastructure, and capture the patient-preference wedge without building from scratch. The most likely value-creation path for Unicycive shareholders, in many investors' eyes, is not standalone commercial success but acquisition by a strategic buyer in the first year or two post-approval. The Vifor acquisition by CSL for $11.7 billion in 2022 sets a benchmark for what the right strategic buyer is willing to pay for renal franchise positioning.10

The bull case finishes with UNI-494 as the free option. As discussed, a positive Phase 2 readout in acute kidney injury — even years from now — would put Unicycive in a category with effectively no approved competition. That is the kind of asset that strategic buyers pay disproportionately for, and it is not currently in most investors' valuation models.

Synthesizing the two, the question for the long-term investor is not whether Renazorb gets approved or not — that question will be answered in a month. The question is whether the commercial economics post-approval justify the implied valuation, and whether the second-asset optionality is sufficient to compensate for the commercial-execution risk. Reasonable people disagree on both.

A few key performance indicators for investors to track, post-approval, are worth flagging. First and most important: the script trajectory of Oxylanthanum Carbonate in the first four full quarters of commercial availability, expressed as a share of total branded phosphate-binder prescriptions. That number, more than any other, will tell you whether the patient-preference thesis is translating into prescriber behavior. Second: gross-to-net pricing, which will reveal how much Unicycive is actually getting to keep after rebates to dialysis providers and Medicare. Third: any disclosure of formulary inclusion at the major dialysis chains, because exclusion from one of the big two would put a hard ceiling on revenue regardless of patient preference. Those three indicators — script share, net pricing, and formulary placement — together capture almost everything that matters about the post-approval Renazorb story.

X. Epilogue and Final Reflections

What happens the day after the FDA gives its verdict? In one scenario, late June 2026 brings the approval letter Unicycive has been waiting nearly six years for. Press releases go out. The commercial launch plan that has been sitting in a binder since 2024 — refined, postponed, refined again — finally goes live. Nephrologists who attended company-sponsored education events in 2023 and 2024 start writing prescriptions. The Asia license to Lee's Pharmaceutical converts from option value to real value. The conversations with potential acquirers, which have probably been happening quietly for months, accelerate. Shalabh Gupta gives a victory lap interview, and the small office in Los Altos quietly begins to add the kind of staff a company actually shipping a drug needs.

In another scenario, late June brings something less clean — a second CRL, a label restriction, a post-marketing requirement that complicates the commercial pitch, or simply a delay. The bear case writes itself in that scenario, and the litigation overhang gets worse before it gets better.

The most important thing about Unicycive's story is not which scenario plays out. It is what the story has already revealed about the strategy of building biotechs in 2026. A decade ago, the default model for a renal disease company was to raise hundreds of millions in venture capital, build an internal discovery operation, run multi-year toxicology studies, and emerge with a 505(b)(1) program. Unicycive did almost the opposite. It found an asset that had already been derisked clinically and then orphaned strategically. It paid for the asset largely with equity rather than cash. It chose a regulatory pathway that compressed the development timeline. It outsourced everything that was not strategic. It kept headcount minimal until the day commercial readiness demanded otherwise. And it built a second pipeline asset, UNI-494, on the same logic — derisked science, narrow regulatory question, big addressable market.

The lessons for other small-biotech founders are obvious in retrospect and counterintuitive in real time. The orphaned-asset playbook works, but only if you have the regulatory expertise to know which orphans are real bargains and which are orphans for good reason. The virtual-company model works, but only if you understand that you are trading capital efficiency for vendor risk, and that vendor risk can detonate in the most unglamorous way imaginable — a single FDA inspection at a third-party facility you do not even own. The 505(b)(2) pathway works, but it does not absolve you of the need to do the manufacturing work correctly.

For long-term investors, the deeper lesson is about valuation in a binary-event franchise. The temptation with a company like Unicycive is to model the future as a probability tree — approval times outcome A, plus delay times outcome B — and arrive at a clean expected value. The reality is messier. The valuation in any given month is driven by the perceived odds of the next regulatory milestone, but the actual long-term value is driven by commercial execution dynamics that nobody — including management — can confidently forecast more than a year out. The honest investor is the one who acknowledges that both ends of the distribution are wider than the standard biotech model would suggest.

Will Renazorb become the new gold standard for hyperphosphatemia in chronic kidney disease? The science says it could. The strategy says Unicycive has positioned itself well. The history of the phosphate-binder market says nothing in this category is easy, and that even best-in-class products have to fight for share against incumbents with decades of nephrologist relationships. The next chapter will be written, in part, in late June 2026 when the FDA delivers its verdict. The rest will be written in the dialysis centers, the formulary committees, and the boardrooms of potential acquirers in the years that follow.

A small biotech in Los Altos. An orphaned asset from Spectrum. A 505(b)(2) gamble. A CRL that did not have to happen. A resubmission. A new PDUFA date. A second pipeline asset in an empty market. And one founder, trained as a doctor and seasoned as an analyst, betting on the most basic proposition in medicine: that patients prefer pills they can actually swallow.

That is the Unicycive story as of May 24, 2026. The next chapter starts in a month.

References

-

Management Team — Unicycive Therapeutics Investor Relations ↩↩

-

Unicycive Therapeutics Acquires Renazorb (Lanthanum Dioxycarbonate) from Spectrum Pharmaceuticals for the Treatment of Hyperphosphatemia — PR Newswire, 2020-12 ↩↩↩

-

Unicycive Therapeutics Announces Receipt of Complete Response Letter for Oxylanthanum Carbonate — GlobeNewswire, 2025-06-30 ↩↩↩

-

Unicycive Therapeutics, Inc. (UNCY) Securities Class Action Lawsuit Update — Zamansky LLC, 2025-09-30 ↩↩↩↩

-

Unicycive Therapeutics Announces FDA Acceptance of Oxylanthanum Carbonate (OLC) New Drug Application (NDA) Resubmission — GlobeNewswire, 2026-01-29 ↩↩↩↩

-

Understanding Hyperphosphatemia in CKD — American Journal of Kidney Diseases ↩

-

Nephrology Business Outlook: The Phosphate Binder Market — Healio Nephrology News, 2023-11-15 ↩

-

Sanofi Completes Acquisition of Genzyme — Sanofi Press Release, 2011-04-08 ↩

-

Takeda Completes Acquisition of Shire — Takeda Press Release, 2019-01-08 ↩

-

CSL to Buy Vifor Pharma for $11.7 Billion to Expand in Renal — Bloomberg, 2021-12-14 ↩↩↩

-

Pill Burden and Adherence in Dialysis Patients — American Journal of Kidney Diseases ↩

-

Shalabh Gupta, MD — Founder, Chairman & CEO Profile, Unicycive Therapeutics ↩↩↩↩

-

Unicycive Therapeutics Announces Successful Completion of Pivotal Clinical Study for Renazorb — GlobeNewswire, 2023-06-27 ↩↩

-

Unicycive Announces Exclusive License and Development Agreement with Lee's Pharmaceutical Holdings for Renazorb in China and Certain Other Asian Markets — GlobeNewswire, 2022-07-18 ↩↩

-

Unicycive Announces up to $130 Million Financing to Commercialize and Launch Investigational New Drug Renazorb — GlobeNewswire, 2023-03-06 ↩↩

-

Unicycive Therapeutics Announces Resubmission of New Drug Application (NDA) for Oxylanthanum Carbonate (OLC) — Unicycive Investor Relations, 2025-12-29 ↩

-

Unicycive Therapeutics Successfully Completes UNI-494 Phase 1 Study in Healthy Volunteers — GlobeNewswire, 2024-10-09 ↩↩

-

Unicycive Therapeutics Granted New U.S. Patent for UNI-494 to Treat Chronic Kidney Disease — GlobeNewswire, 2025-08-18 ↩

-

Unicycive Therapeutics Insider Ownership and Proxy Statement — SEC Schedule 14A, 2024-04-26 ↩

-

Board of Directors — Unicycive Therapeutics Investor Relations ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube