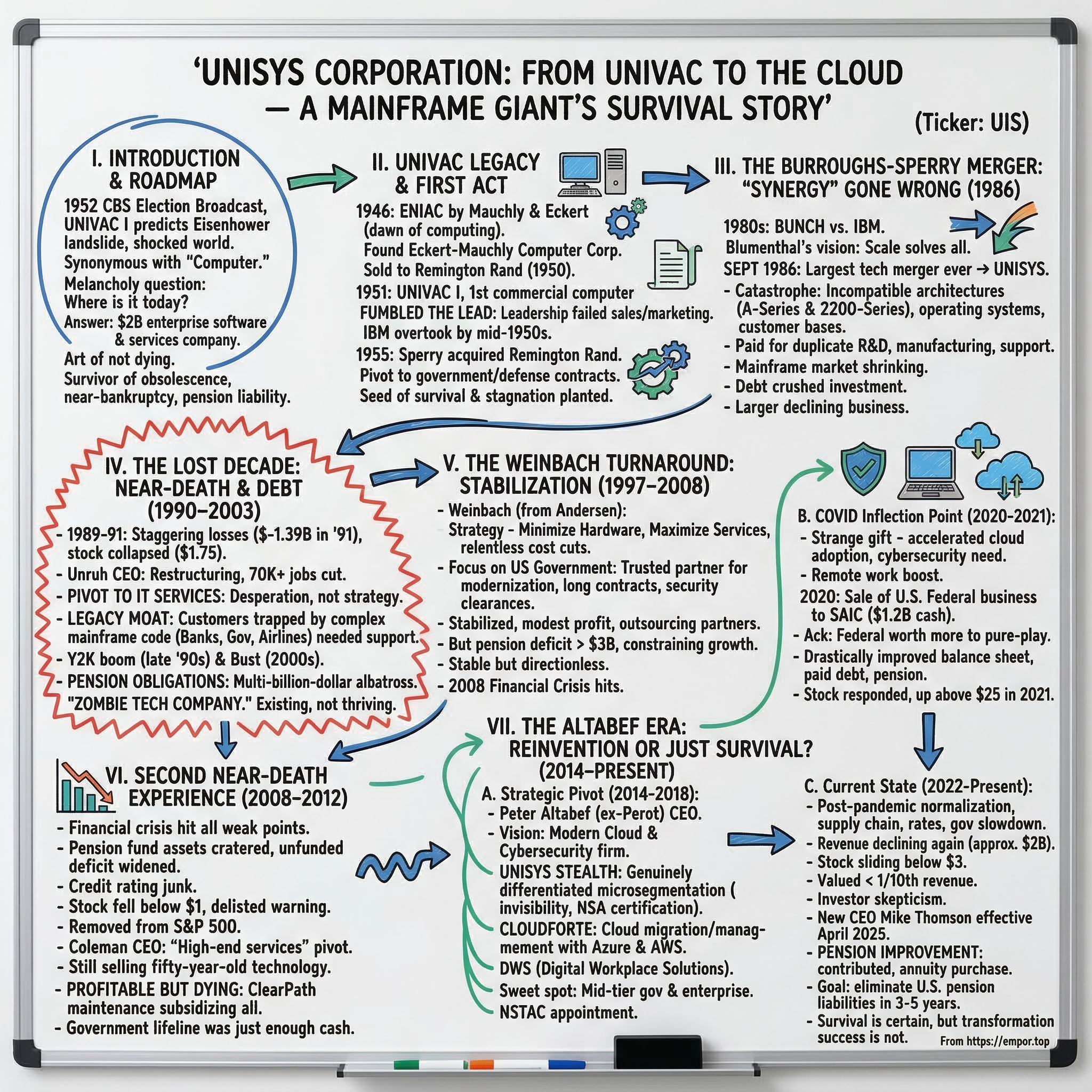

Unisys Corporation: From UNIVAC to the Cloud — A Mainframe Giant's Survival Story

I. Introduction & Episode Roadmap

On the evening of November 4, 1952, tens of millions of Americans sat glued to their television sets watching the first coast-to-coast broadcast of a presidential election. CBS News had a secret weapon that night—a room-sized machine called UNIVAC I, humming away in Philadelphia, fed punch cards of early returns from a handful of precincts. With less than seven percent of the vote counted, the machine spit out a prediction that stunned its operators: Dwight D. Eisenhower would win in a landslide, 438 electoral votes to 93 for Adlai Stevenson, at odds of 100 to 1. The prediction was so far from what every pollster in America was saying—a tight race, too close to call—that the CBS team panicked. They fudged the numbers on air, told Walter Cronkite the machine was "not ready." Only after Eisenhower's victory was confirmed, with a final Electoral College tally of 442 to 89, did CBS sheepishly admit that UNIVAC had nailed it within four electoral votes and 3.5 percent of the popular vote total. In a single evening, a computer had humiliated the entire polling industry and introduced America to the age of electronic brains.

That machine was built by the company that would eventually become Unisys Corporation—ticker symbol UIS, traded on the New York Stock Exchange. And here is the question that makes this story worth telling: the company that built the computer that predicted Eisenhower's election, the company that for a brief moment was synonymous with the word "computer" itself—where is it today?

The answer is both remarkable and melancholy. Unisys is a roughly two-billion-dollar enterprise software and services company that most people under forty have never heard of. It trades at around two dollars a share with a market capitalization hovering near $170 million—smaller than many Series C startups. Its stock, which once touched fifty dollars in 1987, has spent the better part of four decades in decline. And yet, somehow, impossibly, the company is still alive.

This is a story about the art of not dying. It is a story about what happens when a computing pioneer survives forty years past the moment its core business became obsolete. It involves one of the worst mergers in technology history, at least two brushes with bankruptcy, a pension liability that has haunted the company like a ghost for decades, and an ongoing transformation that may or may not be working. The themes are familiar to anyone who studies business history—the innovator's dilemma, the merger trap, the legacy death spiral—but rarely do you get to watch them play out across seven decades in a single company. From UNIVAC glory days through merger disaster, bankruptcy scares, and improbable reinvention, this is the Unisys story.

II. The UNIVAC Legacy and Computing's First Act

The story begins in a cramped laboratory at the University of Pennsylvania in 1946, where two engineers named John Mauchly and J. Presper Eckert completed ENIAC—the Electronic Numerical Integrator and Computer. ENIAC weighed thirty tons, occupied 1,800 square feet, and consumed enough electricity to dim the lights in an entire Philadelphia neighborhood when it was switched on. It was built for the U.S. Army to calculate artillery firing tables, and it could perform five thousand additions per second—a speed that seems laughable today but was, at the time, roughly a thousand times faster than any existing mechanical calculator. ENIAC was the dawn of electronic computing, and Mauchly and Eckert knew immediately that the technology had commercial potential far beyond military ballistics.

The two men founded the Eckert-Mauchly Computer Corporation in 1946 with the audacious goal of building a computer that businesses could actually buy and use. They had the engineering brilliance, but they lacked capital—a familiar problem for founders in any era. After burning through their initial funding, they sold the company to Remington Rand in 1950, the office equipment conglomerate best known for its typewriters and electric shavers. Under Remington Rand's sponsorship, Mauchly and Eckert completed UNIVAC I in 1951. It was the world's first commercially produced electronic digital computer, and the U.S. Census Bureau was its first customer. The machine cost roughly one million dollars—about eleven million in today's money—weighed sixteen thousand pounds, and used five thousand vacuum tubes. It could process data at speeds that made manual tabulation look like chiseling hieroglyphics into stone.

UNIVAC I became a cultural phenomenon. After the 1952 election broadcast, the name UNIVAC became synonymous with the word "computer" in the American vocabulary, much the way Xerox later meant "photocopier" and Google now means "search." For a brief, glittering moment, Remington Rand and its UNIVAC division owned the future.

But they fumbled it. The company's leadership, steeped in the culture of office equipment rather than electronic computing, failed to invest aggressively in sales, marketing, and next-generation development. They treated UNIVAC like a niche product for scientists and government statisticians rather than a platform that could transform every industry. Into that vacuum stepped a company called International Business Machines—IBM—which had been watching from the sidelines. IBM didn't have better technology, but it had something more important: a sales force of legendary discipline and aggression, deep customer relationships across corporate America, and a willingness to invest massively in the market. By the mid-1950s, IBM had overtaken UNIVAC in installations and market share. The computing pioneer had become the computing also-ran.

In 1955, Sperry Corporation acquired Remington Rand, and the UNIVAC line became part of Sperry's broader defense and electronics business. Sperry was a serious company with deep roots in military technology—it made gyroscopes, navigation systems, and radar equipment for the U.S. military—and it funneled UNIVAC's capabilities toward government and defense applications. This was a fateful decision. It kept the UNIVAC business alive and profitable through lucrative government contracts, but it also narrowed the company's focus at precisely the moment when commercial computing was exploding. While IBM was selling mainframes to banks, airlines, and insurance companies, Sperry UNIVAC was increasingly a government contractor that happened to make computers.

That government DNA—the security clearances, the long-term contracts, the deep relationships with federal agencies—would prove to be both Unisys's lifeline and its cage for the next seventy years. The seed of everything that followed, the survival and the stagnation alike, was planted in that pivot toward Washington.

III. The Burroughs-Sperry Merger: "Synergy" Gone Wrong (1986)

By the early 1980s, the mainframe industry was a battlefield dominated by a single combatant: IBM. Everyone else was scrambling for scraps. The industry had a darkly humorous name for the also-rans—the BUNCH, an acronym for Burroughs, UNIVAC, NCR, Control Data Corporation, and Honeywell. These five companies collectively held maybe twenty to twenty-five percent of the mainframe market, and each was losing ground. Meanwhile, the minicomputer revolution led by Digital Equipment Corporation and the personal computer explosion ignited by Apple and IBM's own PC division were eroding the mainframe's relevance from below. The mainframe was not quite dead yet, but you could hear the coughing.

Enter W. Michael Blumenthal, chairman and CEO of Burroughs Corporation and, improbably, the former United States Secretary of the Treasury under President Jimmy Carter. Blumenthal was a patrician figure—born in Germany, a Holocaust survivor who emigrated to the United States, educated at Princeton and Berkeley, a man of enormous intellectual confidence. He looked at the BUNCH's collective predicament and saw a solution that had the elegance of a boardroom napkin sketch: if you couldn't beat IBM alone, you would combine forces and create a number two. Scale would solve everything. Duplicate costs would be eliminated. Combined R&D budgets would produce competitive products. The whole would be greater than the sum of its parts.

In September 1986, Burroughs acquired Sperry Corporation for $4.8 billion, creating Unisys—a name coined from the words "united" and "systems." At the time, it was the largest merger in the history of the computer industry. The combined company had revenue of $10.5 billion, roughly 120,000 employees, and the self-described ambition of being the world's number-two computer company. Blumenthal became chairman and CEO. The stock market was enthusiastic. Shares traded near fifty dollars in 1987. The narrative was compelling: two legacy mainframe companies, each too small to compete with IBM, joining forces to create a credible challenger.

The reality was a catastrophe. Burroughs and Sperry were not complementary businesses that could be neatly combined—they were near-identical businesses with incompatible everything. Burroughs ran its A-Series mainframe architecture. Sperry ran its 2200-Series mainframe architecture (descended from the original UNIVAC line). The two product lines used different operating systems, different programming languages, different hardware designs, and served different customer bases that expected continued support for their specific platforms. Combining them was like merging Toyota and Honda and then trying to maintain two entirely separate car platforms, two supply chains, two dealer networks, and two engineering teams—while claiming cost savings.

The integration consumed enormous management attention and capital. Rather than choosing one platform and migrating customers (which would have been painful but rational), Unisys attempted to maintain both mainframe lines indefinitely, branding them under the ClearPath umbrella. This meant the company was paying for two full R&D pipelines, two manufacturing operations, and two support organizations—exactly the costs that the merger was supposed to eliminate. Meanwhile, the mainframe market itself was shrinking as corporate IT departments shifted spending toward minicomputers, client-server architectures, and personal computers.

By 1988-89, the warning signs were impossible to ignore. Revenue growth stalled. The debt taken on to finance the acquisition—Burroughs had borrowed heavily to buy Sperry—was crushing the company's ability to invest in new technology. And Blumenthal's grand strategic vision had a fatal flaw at its core: combining two declining businesses does not create a growth business. It creates a larger declining business with more overhead. The "synergy" that boardrooms love to invoke had turned out to be a fantasy. Unisys was about to enter the darkest period in its history.

IV. The Lost Decade: Near-Death and Debt Crisis (1990–2003)

The numbers tell the horror story with brutal clarity. In 1989, Unisys posted a net loss of $639 million. The following year, it lost another $436 million. In 1991, the loss ballooned to a staggering $1.39 billion—a figure that placed Unisys among the worst financial disasters in the history of the technology industry. In four years, the company had incinerated roughly $2.5 billion in shareholder value. The stock, which had traded near fifty dollars just three years earlier, collapsed to $1.75. Bankruptcy was no longer an abstract risk—it was a genuine possibility that management discussed behind closed doors.

The causes were cumulative and reinforcing. The mainframe market was in free fall as corporate customers migrated to cheaper, more flexible client-server computing. The merger integration had never been completed, leaving Unisys with duplicated operations and bloated costs. The debt load from the Burroughs acquisition was choking the company's cash flow. And a recession in the early 1990s hit technology spending hard, removing whatever cushion might have existed.

Blumenthal resigned in 1990, and James Unruh—a quiet, operationally focused executive who had previously worked at Memorex and Honeywell—took over as CEO. Unruh's mandate was simple: survive. He launched what he called a "draconian restructuring" that would eventually eliminate over 70,000 jobs from the company's peak headcount. Entire product lines were killed. Real estate was sold. Non-core businesses were divested. The mainframe hardware business, once the company's reason for existence, was systematically de-emphasized in favor of a pivot toward information technology services—managing, maintaining, and consulting on the very systems that Unisys and its competitors had sold.

This pivot was not born of strategic vision; it was born of desperation. But it contained a kernel of insight that would keep the company alive for decades: Unisys's customers could not easily switch away from their installed mainframe systems. Banks, government agencies, and airlines had built mission-critical applications on Burroughs and Sperry hardware over the course of twenty or thirty years. The code was deeply embedded, often poorly documented, and virtually impossible to migrate without enormous cost and risk. These customers did not love Unisys, but they needed Unisys—and they were willing to pay for ongoing maintenance, support, and consulting to keep their legacy systems running. The switching costs were, in effect, a moat—not the kind of moat that Warren Buffett celebrates, but more like a moat filled with quicksand that trapped both the company and its customers together.

By 1992, Unruh's cost-cutting had stabilized the situation. The company posted net income of $361 million on revenue of $8.7 billion—a remarkable turnaround from the brink. But the recovery was fragile, built on cost reduction rather than revenue growth. Revenue continued to decline year after year as the mainframe installed base shrank and new business proved elusive.

The late 1990s brought a temporary reprieve in the form of the Y2K consulting boom. Every company with legacy computer systems—and there were thousands—needed help ensuring that their software would not malfunction when the calendar turned from 1999 to 2000. Unisys, with its deep expertise in legacy mainframe systems, was perfectly positioned to sell Y2K remediation services. Revenue stabilized. Consulting fees flowed in. For a moment, it looked like the services pivot might work.

Then the millennium arrived, Y2K turned out to be largely a non-event, and the consulting revenue evaporated overnight. The dot-com bust followed immediately after, hammering technology spending across the board. By 2002-2003, Unisys faced a new crisis: its pension obligations. The company had accumulated massive defined-benefit pension liabilities during the era when it employed over 100,000 people, and the dot-com crash had devastated the pension fund's investment returns. The unfunded pension deficit grew into a multi-billion-dollar albatross that would distort Unisys's financials and constrain its strategic options for the next two decades.

A pattern had emerged by 2003 that would define the company for years to come. Unisys was alive, but barely. Revenue was shrinking. The balance sheet was stressed. Management was in perpetual restructuring mode. Each crisis brought a new round of layoffs, asset sales, and strategic pivots, followed by a brief stabilization, followed by the next crisis. The company had become what industry observers began calling a "zombie tech company"—not dead, but not really alive either. Just existing, sustained by the switching costs of legacy customers and the long tail of government contracts.

V. The Weinbach Turnaround: Stabilization (1997–2008)

Larry Weinbach arrived at Unisys in September 1997 with credentials that screamed "turnaround artist." He had spent thirty-six years at Arthur Andersen, rising to become chairman and CEO of Andersen Worldwide—the parent organization that oversaw both the accounting firm and its consulting arm. Weinbach understood services businesses at a molecular level. He understood consulting, outsourcing, client relationship management, and the economics of billing professionals by the hour. He was, in many ways, the ideal person to manage Unisys's transition from a hardware company to a services company.

His strategy was straightforward and unglamorous: minimize hardware, maximize services, cut costs relentlessly, and focus on the federal government. Weinbach understood that Unisys's most defensible franchise was its relationship with U.S. government agencies. Federal contracts were long-term, sticky, and carried high barriers to entry—security clearances, compliance requirements, and the sheer bureaucratic complexity of the procurement process created natural advantages for incumbents. He doubled down on this strength, positioning Unisys as a trusted partner for agencies that needed to modernize their IT infrastructure without the risk of switching to an entirely new vendor.

Under Weinbach's leadership, Unisys stabilized. Revenue stopped free-falling. The company returned to modest profitability. Outsourcing partnerships provided recurring revenue streams. The services business grew as a percentage of total revenue, even as the hardware business continued its inexorable decline.

But the pension problem loomed like a shadow over everything. By the mid-2000s, Unisys carried an unfunded pension deficit that exceeded three billion dollars. This was not an operating problem—the company's day-to-day business generated enough cash to keep the lights on—but it was a balance sheet catastrophe that frightened investors, depressed the stock price, and required significant annual cash contributions that diverted capital away from growth investments. Every strategic decision Weinbach made had to be filtered through the pension constraint. Want to acquire a complementary services company? Can't—the pension eats the cash. Want to invest heavily in new technology? Can't—the pension comes first. It was the financial equivalent of running a marathon while carrying a grand piano on your back.

When Joseph McGrath succeeded Weinbach as CEO in 2005, he inherited a company that was stable but directionless. Revenue was around $5.8 billion—down from $10.5 billion at the time of the merger—and still shrinking. The services pivot had worked in the sense that it kept the company alive, but it had not produced growth. Unisys was smaller, leaner, and more focused, but it had no compelling answer to the fundamental question: What does this company do better than anyone else?

Then the 2008 financial crisis hit, and the question became existential once again.

VI. The Second Near-Death Experience (2008–2012)

The financial crisis exposed every weakness in Unisys's foundation simultaneously. Corporate customers slashed IT spending. Government agencies faced budget sequestration. The pension fund's assets cratered as equity markets collapsed, widening the unfunded deficit to nightmarish levels. The company's credit rating was already junk; now lenders questioned whether Unisys could service its debt at all.

The stock price told the story in real time. Shares fell below five dollars in late 2008, then below two dollars in early 2009. At its nadir, the stock traded under a dollar, triggering warnings about potential delisting. Unisys was removed from the S&P 500 index—a humiliation for a company that had once been one of America's largest corporations. The market capitalization, which had been measured in billions during the merger euphoria of 1987, shrank to barely $100 million. Wall Street was pricing the company for liquidation.

J. Edward Coleman took over as CEO in October 2008, replacing McGrath amid the chaos. Coleman was an experienced technology executive—he had previously led Gateway and had deep operational expertise—but the challenge he faced was less about strategy than about survival. He launched what he called a "high-end services" pivot, attempting to move Unisys up the value chain from commodity IT outsourcing toward more specialized consulting and managed services. He sold real estate, divested non-core assets, and negotiated with the Pension Benefit Guaranty Corporation (PBGC) to manage the pension obligations.

The innovation problem, however, remained acute. In 2010, Unisys was still selling ClearPath mainframes—systems whose architecture traced directly back to the Burroughs and Sperry product lines of the 1970s. The company was, in essence, maintaining fifty-year-old technology in a world that was racing toward cloud computing, smartphones, and software-as-a-service. This was not a tenable competitive position, but it was a profitable one: the maintenance contracts on legacy ClearPath systems carried gross margins north of fifty percent, subsidizing everything else the company did. It was the classic legacy trap—the highest-margin business was the one with no future.

Coleman stabilized the company enough to avoid bankruptcy, but he could not solve the fundamental growth problem. Revenue continued to decline. The stock remained depressed. Morale within the company, which had endured decades of layoffs, restructurings, and broken promises of transformation, was dismal.

In 2012, Peter Altabef joined Unisys as President, setting the stage for the next chapter. And the question that had haunted the company since 1990—can Unisys actually transform, or will it just continue to shrink slowly?—remained unanswered. But there was one critical reason Unisys had survived when other legacy technology companies had not: government contracts. Federal agencies like the Transportation Security Administration, the Department of Homeland Security, and various defense organizations continued to rely on Unisys for mission-critical IT services. These contracts provided stable, predictable revenue that kept the company solvent during periods when its commercial business was in free fall. Combined with the switching costs embedded in its legacy installed base, the government lifeline was just enough cash, arriving just frequently enough, to keep the patient alive.

VII. The Altabef Era: Reinvention or Just Survival? (2014–Present)

A. The Strategic Pivot (2014–2018)

Peter Altabef's path to the Unisys CEO office was unconventional and, in retrospect, revealing. A Binghamton University economics graduate and University of Chicago Law School alumnus—graduating cum laude—he began his career not in technology but in law, spending eight years at the Dallas firm Hughes & Luce. There he built relationships with the Perot family, which led to a fateful pivot: in 1993, he joined Perot Systems, the IT services company founded by Ross Perot. He spent sixteen years there, rising to president and CEO in 2004 and leading the company through its $3.9 billion acquisition by Dell in 2009. After a stint running Dell Services, he became CEO of MICROS Systems, a hospitality and retail technology company, and shepherded it through its acquisition by Oracle in 2014. In other words, by the time Altabef arrived at Unisys in January 2015 as CEO, he had spent his career inside exactly the kind of mid-tier IT services companies that live in the shadow of giants—and he had twice navigated the complex process of selling such companies to larger acquirers.

Altabef's vision for Unisys was the most ambitious the company had articulated since the merger: transform from a legacy hardware and services company into a modern cloud and cybersecurity firm. The centerpiece of this strategy was a product called Unisys Stealth—and it deserves explanation, because it represented the first time in decades that Unisys had a genuinely differentiated technology offering.

Stealth is a cybersecurity software suite built around a concept called microsegmentation. Think of a traditional corporate network as a house with a strong front door but no internal walls—once an intruder gets past the perimeter, they can move freely from room to room. Microsegmentation divides the network into tiny, isolated segments, each requiring separate authentication, so that even if an attacker breaches the outer defenses, they can only access a small compartment rather than the entire network. Stealth takes this further by making unauthorized segments not merely inaccessible but actually invisible—assets protected by Stealth cannot even be detected by users who lack the proper credentials. The technology earned certification from the National Security Agency's Commercial Solutions for Classified (CSfC) program, making it the only microsegmentation product approved for protecting classified government information systems. For a company desperate for differentiation, this was meaningful.

Altabef complemented Stealth with CloudForte, a suite of cloud migration and management services built in partnership with Microsoft Azure and Amazon Web Services, designed to help enterprise customers move their workloads from legacy data centers to the cloud. He also doubled down on the federal sector, securing contracts with the TSA, Department of Homeland Security, and Department of Defense.

The challenge, of course, was competing with AWS, Microsoft, Accenture, and IBM on their turf. Unisys was bringing a knife to a gunfight in terms of scale, brand recognition, and R&D investment. But Altabef's argument was that there existed a sweet spot—mid-tier government agencies and enterprise clients that needed both legacy system expertise and modern cloud capabilities, and that were too small or too risk-averse for the hyperscalers. It was a niche strategy, but it was at least a coherent one.

In December 2016, Altabef received a notable external validation when he was appointed to the President's National Security Telecommunications Advisory Committee (NSTAC), and in 2018 he co-led the committee's Cybersecurity Moonshot initiative. These appointments gave Unisys visibility in national security circles and reinforced the company's positioning as a trusted government technology partner.

B. The COVID Inflection Point (2020–2021)

The COVID-19 pandemic, which devastated so many businesses, turned out to be a strange gift for Unisys. The overnight shift to remote work forced every organization on earth to accelerate its cloud adoption timeline by years. Companies that had been planning three-year cloud migration projects suddenly needed them done in three months. Unisys's cloud migration and digital workplace services—the businesses Altabef had been building since 2015—were suddenly in high demand.

At the same time, the explosion of remote access points made cybersecurity more critical than ever, boosting interest in Stealth's microsegmentation capabilities. The Digital Workplace Solutions business saw rapid growth as organizations needed secure, managed end-user computing environments for distributed workforces.

But Altabef also made a transformative structural move in early 2020 that reshaped the company. In February, just before the pandemic hit, Unisys announced the sale of its U.S. Federal business unit to Science Applications International Corporation (SAIC) for $1.2 billion in cash. The deal, which closed on March 16, 2020, transferred approximately 1,900 employees and roughly $689 million in annual revenue to SAIC at a multiple of thirteen times adjusted EBITDA—a significant premium to Unisys's own trading multiple. It was, in many ways, an acknowledgment that the federal IT services business, while stable, was worth more to a pure-play government contractor than to a company trying to reinvent itself.

The proceeds were used primarily to reduce debt and shore up the pension deficit, which dropped from $1.74 billion at the end of 2018 to approximately $1.14 billion on a pro forma basis. The transaction dramatically improved the balance sheet but also removed a substantial chunk of revenue, leaving the remaining Unisys smaller but theoretically better positioned for transformation.

The stock responded. From a low near ten dollars in 2019, shares climbed above twenty-five dollars in 2021. For the first time in decades, Unisys was generating positive momentum with investors. The question was whether it would last.

C. The Current State (2022–Present)

It did not last. The post-pandemic normalization brought a sharp comedown. Supply chain disruptions, rising interest rates, and a slowdown in federal IT spending hit the company from multiple directions. Revenue, which had been roughly $2.0 billion following the SAIC divestiture, began declining again. The stock price resumed its long slide, falling from the twenties into single digits and eventually below three dollars.

By the end of 2025, the picture was sobering. Full-year revenue came in at approximately $2.01 billion, down 2.9 percent year-over-year. Digital Workplace Solutions declined 2.9 percent. Cloud, Applications and Infrastructure Solutions fell 4.1 percent. Only Enterprise Computing Solutions—the legacy mainframe business—held roughly flat, buoyed by software license renewal timing. The non-GAAP operating margin reached 9.1 percent for the full year, with a strong fourth quarter at 18 percent driven by those same license renewals. Cash on the balance sheet stood at $413.9 million, and backlog grew to $3.16 billion from $2.84 billion a year earlier.

On the pension front, Unisys made significant progress. The company contributed $250 million to its U.S. pension plans and completed a group annuity purchase contract transferring approximately $320 million of pension liabilities to a third-party insurer. The unfunded deficit improved from $750 million at the end of 2024 to $448.5 million at the end of 2025—substantial progress, though still a meaningful overhang. Management has stated a goal of eliminating U.S. qualified pension liabilities within three to five years.

In a significant leadership transition, Unisys announced that Mike Thomson—who had joined the company in 2015 as Corporate Controller, risen to CFO in 2019, and become President and COO in 2021—would succeed Altabef as CEO effective April 1, 2025. Altabef remains as Chairman of the Board.

As of early 2026, the stock trades around $2.31, giving the company a market capitalization of roughly $170 million. That is less than one-tenth of its annual revenue—a valuation that reflects deep investor skepticism about whether the transformation narrative is real or simply the latest chapter in a four-decade story of decline.

VIII. The Business Model Evolution

The arc of Unisys's business model is a lesson in adaptation under duress. In its first life, from the 1950s through the 1980s, the company was fundamentally a hardware business. It designed, manufactured, and sold mainframe computers and peripherals. The economics were straightforward: high upfront capital expenditure by customers, healthy margins on hardware sales, and recurring revenue from maintenance contracts. This was the golden age, and it ended with the PC revolution.

In its second life, from roughly 1990 through 2010, Unisys reinvented itself as an IT services company. Hardware revenue shrank from the majority of the business to a minority, replaced by consulting, outsourcing, and systems integration. The company maintained the legacy mainframes it had sold to customers while also offering broader IT services—managing data centers, running help desks, integrating enterprise software. The margins were lower than hardware, but the revenue was more predictable. The essential economic engine during this period was the maintenance annuity: customers who ran mission-critical applications on ClearPath mainframes paid annual fees for support, software updates, and hardware maintenance. These contracts carried gross margins above fifty percent and provided the cash flow that subsidized everything else.

In its current incarnation, Unisys operates three reportable segments. Digital Workplace Solutions encompasses cloud-based workplace services, end-user computing management, and experience management—essentially helping organizations manage their employees' technology environments. Cloud, Applications and Infrastructure Solutions covers data center modernization, cloud migration, application development, and managed infrastructure services. Enterprise Computing Solutions is the legacy business—ClearPath mainframe software and hardware, along with associated maintenance and support.

The economic tension at the heart of the business is straightforward: the highest-margin segment, Enterprise Computing Solutions, with gross margins around 55 percent, is the one with the least growth potential. It depends on a finite and shrinking installed base of legacy mainframe customers who will eventually migrate to modern platforms. The growth segments—DWS and CA&I—carry significantly lower margins (14-20 percent) and compete in markets where Unisys faces vastly larger and better-resourced competitors. The maintenance revenue from ECS subsidizes the investment needed to grow DWS and CA&I, but that subsidy is finite. If maintenance revenue declines faster than the growth businesses can scale, the company faces a death spiral.

This dynamic explains why Unisys is difficult to value and why it trades at such a steep discount. Investors cannot easily separate the "legacy annuity" value (which is high but declining) from the "growth business" value (which is uncertain and low-margin). The result is a stock that is priced for neither scenario—neither full legacy runoff nor successful transformation—but rather for indefinite ambiguity.

The competitive position reinforces this challenge. Unisys is too small to compete head-to-head with Accenture, IBM, or AWS in cloud and consulting. It lacks the brand recognition and talent pipeline of the hyperscalers. Its most defensible competitive advantage—deep expertise in legacy mainframe systems—is a wasting asset. The niche it occupies, mid-tier government and enterprise clients with both legacy and cloud needs, is real but narrow, and it is steadily narrowing further as legacy systems are retired.

IX. Culture, Leadership, and the Survival Mentality

There is a human dimension to the Unisys story that numbers alone cannot capture. Consider what it means to work at a company that has been in crisis mode, more or less continuously, for over thirty years. Since 1990, Unisys employees have lived through at least five major restructurings, each accompanied by waves of layoffs, organizational upheaval, and existential uncertainty. The headcount has fallen from roughly 120,000 at the time of the merger to approximately 16,000 today. The psychological toll of this extended decline—the "turnaround fatigue," as organizational psychologists might call it—is difficult to overstate.

The brain drain problem is real and compounding. Top engineering talent in cloud computing, cybersecurity, and artificial intelligence gravitates toward companies with momentum, strong brands, and generous compensation—Google, Amazon, Microsoft, CrowdStrike, Palo Alto Networks. Unisys, with its legacy reputation, modest stock price, and history of instability, struggles to attract these candidates. The company's Glassdoor reviews and LinkedIn profiles tell a consistent story: dedicated long-tenured employees who believe in the mission, mixed with frustration over outdated processes, slow decision-making, and compensation that lags the market.

Then there are the mainframe engineers—a vanishing breed of specialists who maintain systems built on architectures from the 1970s. These individuals possess knowledge that is irreplaceable and non-transferable. They understand the quirks of ClearPath operating systems, the idiosyncrasies of proprietary programming languages, and the undocumented behaviors of hardware that has been running continuously for decades. When they retire—and they are retiring—their expertise leaves with them. This creates both a risk and a strange form of job security: as long as customers run ClearPath systems, someone has to maintain them, and the pool of people who can do so is shrinking faster than the installed base.

Government customer loyalty is the other side of this coin. Federal agencies stick with Unisys for reasons that go beyond switching costs. The company holds security clearances that take years to obtain. It has deep institutional knowledge of how specific agencies operate—their workflows, their compliance requirements, their bureaucratic cultures. Replacing Unisys would mean not just migrating technology but rebuilding institutional relationships. For a government procurement officer, the career risk of switching vendors and having something go wrong far outweighs the potential benefit of marginal cost savings. This inertia is Unisys's most durable asset, even if it is not the kind of competitive advantage that generates growth.

The identity crisis remains unresolved. Ask ten people at Unisys what the company is, and you may get ten different answers. A mainframe company? A services company? A security company? A cloud company? The lack of a clear, compelling identity makes it difficult to tell a coherent story to customers, investors, or prospective employees. Altabef worked hard to reposition the brand around security and cloud, but the market still sees Unisys primarily through the lens of its legacy—and in technology, perception moves slowly.

X. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding Unisys's strategic position requires a rigorous look at the competitive forces arrayed against it and the durable advantages—or lack thereof—that determine its long-term viability.

Starting with competitive rivalry: it is intense and fragmented. In IT services, Unisys competes against IBM, Accenture, DXC Technology, Cognizant, Infosys, and dozens of smaller firms. In cloud infrastructure, it faces Amazon Web Services, Microsoft Azure, and Google Cloud Platform—each of which spends more on R&D in a single quarter than Unisys's entire annual revenue. In cybersecurity, the competitive set includes CrowdStrike, Palo Alto Networks, Zscaler, and others that are purpose-built for the modern threat landscape. Unisys lacks meaningful brand strength in any of these categories. IT services have become increasingly commoditized, with pricing pressure from Indian IT firms and automation reducing the value of labor-intensive service delivery.

The threat of new entrants remains high. Cloud-native startups emerge continuously, unburdened by legacy technology and legacy cost structures. The barriers to entry in software and services are low compared to the hardware era, when building a mainframe required massive capital investment. Unisys's legacy actually works against it here—it carries costs (pension obligations, old real estate, legacy support commitments) that new entrants do not bear.

Supplier bargaining power is moderate. Unisys depends on partners like Microsoft and AWS for its modern technology stack, and these partners also compete with Unisys for the same customers. The labor market for cloud and security talent is tight, giving skilled workers significant leverage in salary negotiations—a particular challenge for a company that cannot match the compensation packages of hyperscalers and elite cybersecurity firms.

Buyer bargaining power is high and rising. Customers have more alternatives than ever. As organizations modernize their IT environments, the switching costs that once locked them into Unisys's ecosystem are declining. The exception is legacy mainframe customers, who remain effectively locked in—but this is a shrinking population.

The threat of substitutes is severe. Everything Unisys offers—cloud migration, workplace management, cybersecurity, IT consulting—can be done by larger, more capable competitors with greater scale and deeper expertise. Open-source tools, automation platforms, and artificial intelligence are reducing the need for human-delivered IT services. The build-versus-buy calculus increasingly favors either in-house teams or hyperscaler platforms over mid-tier services providers.

Turning to Hamilton Helmer's Seven Powers framework, the picture is equally challenging. Unisys possesses no meaningful scale economies—it is subscale in every market where it competes. It has no network effects; enterprise IT services and security software do not become more valuable as more customers use them. Counter-positioning, which existed briefly in the 2010s when Unisys's willingness to bridge legacy and cloud was somewhat unique, has become table stakes as every major IT services firm now offers similar capabilities.

The company's most relevant power is switching costs, but even this is declining. Legacy mainframe customers face genuinely high switching costs—they are locked into proprietary systems with decades of embedded code—and this keeps the Enterprise Computing Solutions business alive. But new cloud and security customers face low switching costs, and the legacy customer base is shrinking by natural attrition.

Brand power is weak to negative. The Unisys name carries no premium in modern technology markets and is associated with "legacy" in the minds of IT decision-makers. Cornered resources are similarly limited: expertise in legacy mainframe systems is a wasting asset, and government relationships, while valuable, are not unique to Unisys. Process power exists to a moderate degree—the company has decades of institutional knowledge in managing complex government contracts, navigating security clearance requirements, and maintaining compliance certifications—but this alone is insufficient to generate sustained competitive advantage.

The power analysis summary is sobering. Unisys's survival has depended primarily on the switching costs embedded in a declining business and on the institutional inertia of government customers. Neither of these constitutes a durable competitive advantage that can generate growth. This structural reality is reflected in the company's valuation: a market capitalization of roughly $170 million against approximately $2 billion in revenue represents a price-to-sales ratio below 0.1—a level that signals deep market skepticism about the company's future.

XI. Bull vs. Bear Case

The bull case for Unisys rests on several pillars that, while individually plausible, require near-perfect execution to translate into sustained value creation.

First, the transformation under Altabef was real in a way that previous restructurings were not. The company developed a genuinely differentiated security product in Stealth, built credible cloud capabilities through CloudForte, and restructured the balance sheet through the SAIC divestiture. The backlog growth to $3.16 billion at the end of 2025, up from $2.84 billion a year earlier, suggests that customers are signing new contracts, not just running out existing ones.

Second, the cybersecurity tailwind is powerful and secular. Government agencies and enterprises face escalating threats, and budgets for security are among the last to be cut in any downturn. Stealth's NSA certification for classified systems provides a genuine barrier to entry in a valuable niche. If the company can expand Stealth's adoption beyond its current customer base, the revenue and margin implications could be significant.

Third, the federal IT modernization wave is large and durable. The U.S. government spends billions annually on upgrading legacy technology systems, and Unisys's dual expertise in legacy and modern platforms positions it well for these contracts. The relationships and clearances built over decades cannot be replicated quickly.

Fourth, the valuation is extraordinarily compressed. At less than 0.1 times revenue, even modest improvement in growth or profitability could drive significant stock appreciation. The $413.9 million in cash on the balance sheet exceeds the market capitalization, providing a floor of sorts. This also makes the company a plausible private equity target—a buyout firm could take Unisys private, optimize the cost structure, harvest the legacy cash flows, and potentially exit at a significant profit.

The bear case, however, is at least equally compelling. The fundamental death spiral risk remains: maintenance revenue from legacy mainframe customers is declining as that installed base shrinks, and the growth businesses (DWS and CA&I) are declining as well, not growing. The 2025 results showed revenue declines across all three segments in constant currency terms. A company where all segments are contracting is not transforming—it is shrinking.

The competitive moat is, for practical purposes, nonexistent in the growth businesses. There is no clear reason why a large enterprise or government agency would choose Unisys over AWS, Microsoft, Accenture, or IBM for cloud or security services. The company lacks the scale to invest in R&D at competitive levels, the brand to attract top-tier talent, and the market presence to win against well-resourced competitors.

The pension liability, while improved, remains a meaningful drag. The $448.5 million unfunded deficit continues to require cash contributions that could otherwise fund growth investments. Management's three-to-five-year timeline for eliminating the deficit is credible but not guaranteed—another market downturn could widen the gap again.

The talent challenge is perhaps the most underappreciated risk. Cloud computing and cybersecurity are among the most competitive labor markets in the world. Unisys competes for engineers against companies that can offer significantly higher compensation, stronger brand prestige, and more compelling career trajectories. Without top-tier talent, the quality of the company's offerings will inevitably lag.

Perhaps most damning is the historical pattern. Unisys has been through multiple restructurings, each accompanied by management promises of transformation, and each ultimately producing another round of decline. At some point, the pattern becomes the prediction. Thirty-plus years of failed transformations is not definitive proof that this one will fail too—but it is substantial evidence that should give any investor pause.

The two KPIs that matter most for tracking Unisys's ongoing performance are: first, the year-over-year revenue growth rate in DWS and CA&I combined, which indicates whether the transformation is producing actual commercial traction; and second, the rate of decline in Enterprise Computing Solutions revenue, which determines how quickly the legacy subsidy is eroding. The gap between these two numbers—the speed of growth versus the speed of decay—is the single most important dynamic in the Unisys investment thesis.

XII. Key Inflection Points Summary

Seven moments determined the trajectory of Unisys, and each offers a lesson that extends beyond the company itself.

The 1986 merger was the original sin. Blumenthal's vision of creating a number-two challenger to IBM through scale was intellectually elegant and operationally disastrous. The incompatibility of the two companies' products, cultures, and systems produced not synergy but entropy—costs went up, innovation stalled, and the combined entity was weaker than either predecessor alone. The lesson is timeless: merging two declining businesses does not create a growth business.

The 1990 crisis forced the pivot to services. With losses exceeding a billion dollars and the stock trading under two dollars, Unisys had no choice but to abandon its identity as a hardware company and reinvent itself as a services provider. This pivot saved the company's life, but it was reactive rather than visionary—and the services business it built was never differentiated enough to generate sustained growth.

The Y2K boom of the late 1990s provided a temporary reprieve that masked structural decline. Revenue stabilized, consulting fees surged, and management could defer hard strategic choices. When the millennium turned and the consulting windfall evaporated, the underlying rot was still there, compounded by a growing pension crisis.

The 2008-2012 period brought the second near-death experience. The financial crisis, pension deterioration, and revenue collapse pushed the stock below one dollar and forced another round of emergency restructuring. That the company survived at all is a testament to the durability of government contracts and legacy switching costs.

Altabef's arrival in 2015 marked the most deliberate attempt at transformation in the company's history. The development of Stealth, the build-out of cloud capabilities, and the SAIC divestiture were genuine strategic moves rather than mere cost-cutting exercises. Whether they were sufficient to change the company's trajectory remains the central open question.

The COVID pandemic in 2020 accelerated digital transformation trends in ways that temporarily benefited Unisys, creating a window of growth that raised hopes for sustainable change. The stock's subsequent collapse back to pre-pandemic levels suggests the market views this as a temporary boost rather than a permanent inflection.

And the current period—from 2022 to the present—is the test. Revenue is declining again. All three segments are under pressure. A new CEO, Mike Thomson, is taking the reins. The pension deficit is shrinking but not gone. The company is smaller, leaner, and better positioned than it has been in decades—but it is also running out of time.

XIII. Lessons for Founders, Operators, and Investors

The Unisys story is a masterclass in the pathologies of corporate decline, and its lessons apply far beyond the technology industry.

The merger trap is the most vivid lesson. When Blumenthal combined Burroughs and Sperry in 1986, the strategic logic was superficially compelling: create scale, eliminate redundancy, challenge the market leader. But the logic failed because it assumed that the problem was size rather than relevance. Both companies were declining because the mainframe market was declining, and combining them created a larger entity exposed to the same structural headwind. This is a pattern that repeats across industries: companies in declining markets merge to "gain scale," only to discover that a bigger ship still sinks if the sea is draining away. The lesson for any executive considering a transformative merger: if both companies' core markets are contracting, the merger does not solve the problem—it compounds it.

The legacy dilemma is equally instructive. Unisys's highest-margin business—legacy mainframe maintenance—provided the cash flow that kept the company alive for decades. But that same cash flow also created a gravitational pull that made transformation nearly impossible. Why invest aggressively in low-margin, uncertain cloud services when you can harvest fifty-five-percent gross margins from legacy contracts? This is the innovator's dilemma in its purest form: the rational short-term decision (protect the legacy business) is the irrational long-term decision (delay the pivot until it's too late). Clayton Christensen could have written a case study about Unisys.

The cost structure lesson is stark. Unisys's pension obligations, accumulated during decades of employing over 100,000 people, created a structural cost that made transformation virtually impossible. The company was spending hundreds of millions of dollars per year servicing pension liabilities—capital that competitors were investing in R&D, acquisitions, and talent. This is an extreme case of a universal principle: fixed costs that cannot be cut become the ceiling on strategic flexibility. Any company accumulating long-term liabilities—pensions, long-term leases, guaranteed contracts—should consider the scenario in which those liabilities outlive the business that created them.

The brand lesson is often overlooked. Unisys's name carries no equity with younger generations of technologists and IT decision-makers. In an industry where talent and customer perception are everything, an unknown or negatively perceived brand is a compounding disadvantage. The company cannot charge premium prices, cannot attract top engineering talent, and cannot win competitive deals on reputation alone. For founders, this is a reminder that brand is not just a marketing asset—it is an operating asset that affects every aspect of the business.

For investors, the Unisys story is a cautionary tale about value traps. A company trading at a fraction of its revenue looks cheap on a spreadsheet. But cheapness alone is not a thesis—it is a starting point for analysis. The question is always: why is this company cheap? In Unisys's case, the answer is clear: the company has no durable competitive advantage, its highest-margin business is declining, and its growth businesses face intense competition from better-resourced rivals. These are structural problems, not cyclical ones, and they are unlikely to be resolved by new management or a new strategy. Most turnaround stories fail, and serial restructurings—Unisys is on its fifth or sixth—are a red flag, not a green light.

XIV. The Future: What Happens Next?

Projecting Unisys's future requires weighing competing scenarios, each with different implications for investors, employees, and the broader industry.

The most likely path, perhaps with a sixty percent probability, is a continuation of the slow fade. Revenue drifts downward as legacy contracts expire faster than new business replaces them. Cost-cutting maintains profitability for a time, but margins eventually compress. The company becomes progressively smaller, possibly falling below one billion dollars in annual revenue over the next five to seven years. At some point, a private equity firm or larger IT services company acquires Unisys for its government contract base, its remaining customer relationships, and its cash flows from legacy maintenance. The Unisys brand disappears into the acquirer's portfolio. This is not a dramatic ending—it is a quiet one, the kind that barely makes the headlines.

A successful transformation scenario, perhaps with a fifteen percent probability, would require the DWS and CA&I segments to achieve sustained growth, the Stealth security product to gain meaningful market share, and the legacy ECS revenue to decline more slowly than expected. Under this scenario, Unisys would reach a crossover point where new revenue exceeds declining legacy revenue, enabling the company to grow for the first time in decades. The market capitalization would expand significantly. It is possible but would require a degree of execution that the company has never demonstrated in its post-merger history.

A crisis and bankruptcy scenario, also at roughly fifteen percent probability, would be triggered by a combination of negative events: the loss of one or more major government contracts, a widening of the pension deficit due to market disruption, or a failure to refinance maturing debt. Chapter 11 reorganization or a distressed asset sale would follow. This scenario is less likely than it was in 2009 or 2012, given the improved balance sheet, but it cannot be ruled out for a company of this size and vulnerability.

Finally, a strategic acquisition by a larger IT services firm—DXC Technology, Cognizant, or similar—represents a roughly ten percent probability. Such an acquirer would be motivated by Unisys's customer base, government relationships, and maintenance revenue streams, integrating them into a larger platform where they could be supported more efficiently. This scenario might actually be the best outcome for most stakeholders, offering employees stability, customers continuity, and shareholders a premium to the current market price.

The most likely five-year outcome is that Unisys exists but in diminished form—smaller, possibly under different ownership, still managing legacy systems while attempting to stay relevant in cloud and security. Mike Thomson, taking over as CEO in April 2025, inherits both the opportunity and the burden that every Unisys CEO since 1990 has faced: the challenge of transforming a company whose past is larger than its future.

XV. Epilogue and Final Reflections

There is a paradox at the heart of the Unisys story that resists easy resolution. This is a company that traces its lineage directly to the birth of electronic computing—to ENIAC, to UNIVAC, to the machine that predicted Eisenhower's landslide. It was there at the very beginning, when computers were room-sized marvels and the idea of an electronic brain was science fiction made real. No company in the world has a longer continuous claim to computing heritage.

And yet that heritage, extraordinary as it is, has been more burden than benefit for at least forty years. Being first means nothing if you cannot adapt. Remington Rand's failure to invest in commercial computing allowed IBM to seize the market. Sperry's retreat into government work narrowed the company's horizons. The Burroughs merger compounded every existing problem while creating new ones. And the decades of decline that followed have been a slow-motion illustration of what happens when a company cannot escape the gravity of its own past.

What Unisys got right was purchasing time. The switching costs embedded in its legacy installed base, the long-term government contracts, the sheer stickiness of mission-critical mainframe systems—these factors kept the company alive through crisis after crisis, buying management the opportunity to attempt transformation. That Unisys exists at all in 2026, seventy-five years after UNIVAC I was delivered to the Census Bureau, is a remarkable feat of corporate survival.

What the company got wrong was nearly everything else. The merger strategy was wrong. The integration execution was wrong. The pace of transformation was too slow. The investments in new technology were too small. The cost structure was too heavy. The brand went unmanaged. The culture could not adapt. At nearly every strategic decision point, the company chose the conservative path—maintain both mainframe lines, protect the legacy revenue, minimize risk—and each conservative choice narrowed the range of future options.

The human story is perhaps the most poignant element. Tens of thousands of people built careers at Unisys, at Sperry, at Burroughs—people who designed mainframes, wrote code, served customers, and believed in the company's future. Many of them lived through multiple layoffs, watched colleagues lose their jobs, and experienced the creeping demoralization of working for a company that the market had written off. Some stayed for decades out of loyalty, or because their specialized skills had no market outside Unisys, or because they genuinely believed that this time, the turnaround would work. Their dedication deserves recognition, even as the outcomes have been disappointing.

The broader lesson is one that technology makes vivid but that applies to every industry: standing still is moving backward. In a world where computing power doubles every two years and new competitors emerge continuously, the only sustainable strategy is relentless adaptation. Unisys adapted—slowly, reluctantly, imperfectly—and that adaptation was enough to survive. But survival and success are different things. The company survived for forty years after its business model became obsolete. Whether that is impressive or merely sad depends on your definition of victory.

XVI. Further Reading and Resources

For those interested in exploring the Unisys story in greater depth, several resources provide valuable context and primary source material.

"The Computer: A History of the Information Machine" by Martin Campbell-Kelly and William Aspray offers an excellent account of UNIVAC's early history and the competitive dynamics that shaped the mainframe industry. For understanding why IBM's competitors struggled, Paul Carroll's "Big Blues: The Unmaking of IBM" provides essential context, as does Clayton Christensen's "The Innovator's Dilemma," which supplies the theoretical framework for understanding Unisys's failure to adapt. Michael Hiltzik's "Dealers of Lightning: Xerox PARC and the Dawn of the Computer Age" offers a parallel narrative of how computing pioneers lost their competitive positions.

The primary financial sources are Unisys's 10-K annual reports, particularly the filings from 2008, 2014, 2020, and 2024, which document the company's evolution through each major crisis and strategic pivot. The Harvard Business School case study on Unisys's pension management crisis provides a detailed examination of the pension liability challenge. Wall Street Journal archives contain contemporaneous coverage of the 1986 merger, the 1990 crisis, and the 2008-2012 near-bankruptcy that captures the drama of these events as they unfolded.

Peter Altabef's investor presentations and public interviews from 2015 through 2024 articulate the transformation vision in his own words and provide useful benchmarks for evaluating execution against stated goals. Government Accountability Office reports on TSA and DHS contracts offer an independent assessment of Unisys's government business performance. Gartner and Forrester research on the enterprise IT services market provides competitive context for understanding where Unisys fits—and where it does not—in the modern technology landscape.

SEC filings, including 10-Ks, 8-Ks, and proxy statements, remain the authoritative source for financial data, executive compensation, and risk disclosures. The Pension Benefit Guaranty Corporation's public filings document the pension negotiations that shaped the company's financial strategy during multiple crises. Competitor annual reports from IBM, DXC Technology, and Accenture provide the comparative data necessary for evaluating Unisys's relative position in the markets where it competes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube