Ubiquiti: The Anti-Enterprise Networking Empire

I. Introduction & Episode Roadmap

Picture this: A networking company with a $27 billion market cap, serving millions of devices worldwide, competing head-to-head with Cisco and Aruba—yet it has no sales team. No army of enterprise account executives. No 1-800 support number. No Super Bowl ads. Just a radical belief that great technology, priced aggressively and supported by passionate users, can topple industry giants.

This is Ubiquiti—a company that generated $1.903 billion in revenue in fiscal 2024 while violating nearly every rule in the enterprise technology playbook. Founded by an ex-Apple engineer who started with $30,000 in personal savings and credit card debt, Ubiquiti has become the anti-Silicon Valley success story: no venture capital, no traditional go-to-market strategy, and a founder who still owns 93% of the company.

The question isn't just how Robert Pera built this empire—it's why the entire technology industry hasn't copied his model. Is Ubiquiti a one-off anomaly, enabled by a unique moment in networking history? Or does it represent a fundamentally different way to build and scale enterprise technology companies?

Today we're diving deep into three revolutionary ideas that powered Ubiquiti's rise: First, the community-as-salesforce model that turned users into evangelists. Second, the radical vertical integration that allowed them to deliver enterprise-grade technology at consumer prices. And third, the contrarian philosophy that says the best way to serve enterprise customers might be to ignore enterprise conventions entirely.

We'll trace the journey from Pera's nights-and-weekends tinkering at Apple to a public company with a market cap that's grown 1,664% since its IPO. We'll examine how a company with no salesforce competes against armies of Cisco reps, and why traditional networking giants haven't been able to stop this bootstrap upstart. Most importantly, we'll extract the lessons for founders, investors, and anyone interested in how David can still beat Goliath in the age of tech giants.

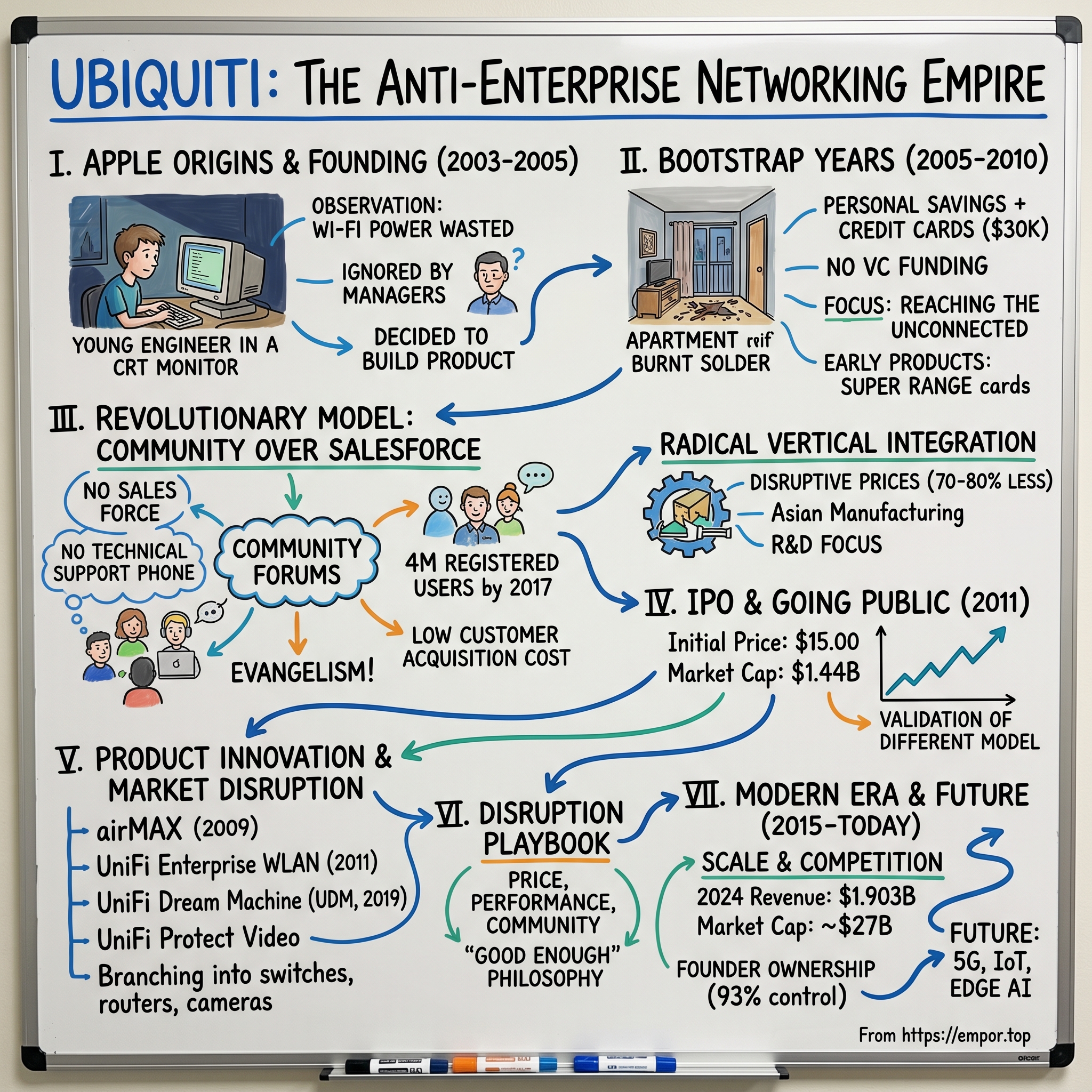

II. The Apple Origins & Founding Story

The room is dim, lit only by the glow of a CRT monitor displaying endless lines of RF test results. It's 2003, past midnight in Cupertino, and Robert Pera—26 years old, three years out of grad school—stares at data that his bosses at Apple don't want to hear about. The Wi-Fi signals from Apple's AirPort routers are transmitting at power levels 50% below FCC limits. It's like driving a Ferrari in second gear, never touching the potential that's legally allowed. He can see it plain as day: boost the power, extend the range, connect the unconnected. But Apple has bigger fish to fry—they're building iPods and planning something called an iPhone. Rural internet connectivity? Not their problem.

While testing Wi-Fi products at Apple to ensure FCC compliance, Pera discovered that the power sources Apple's devices used were significantly below regulatory limits, and believed boosting them could dramatically increase range to reach underserved areas. His managers ignored the idea, so he decided to build his own product.

This wasn't just another engineer with a side project. Robert J. Pera, born March 10, 1978, had established his first computer services company while still in high school—until a heart condition sidelined him from basketball and pushed him deeper into technology. That early company provided networking and database services to local businesses, giving him a taste of entrepreneurship that would never leave.

At the University of California, San Diego, Pera wasn't your typical engineering student. He graduated Phi Beta Kappa with a dual degree—a B.S. in Electrical Engineering and a B.A. in Japanese Language. Think about that combination for a moment: the precision of circuit design paired with the nuance of Japanese business culture. He stayed on to complete his master's in electrical engineering with an emphasis on digital communications and circuit design. During his junior year, he went to Tokyo and noticed mobile phones were way ahead of the U.S. market, deciding he wanted to work in cellular networks.

After graduation in 2002, he took a job at Apple, saying "I wanted to build products. I idolized Steve Jobs". But the reality was different from the dream. He was assigned to test Wi-Fi routers for FCC compliance—dull work, but Pera showed up early, stayed late, and shared his design ambitions with anyone who would listen. At his first annual review, his manager, who had been at Apple for decades, told him to slow down.

The irony is almost painful. Here was Apple, the company that thought different, telling an engineer to think less. During testing, Pera noticed the power sources in Apple's routers were far below FCC limits—boosting them would increase range, but Apple bosses ignored his idea.

But Pera had done his homework. Searching online, he found people in remote areas rigging routers with external amplifiers to send signals over dozens of miles—a cheap way to get Internet where traditional providers didn't reach. "This was a big market that was just starting, but nobody knew about it".

After spending a few years working on it during nights and weekends, he set out on his own and formed Ubiquiti. Actually, let's be precise about the timeline: For the next year, Pera did the bare minimum at work and spent nights and weekends in his apartment testing prototypes, ready to start his own business by early 2005. Just before leaving Apple, he got a raise and a 4-out-of-5 rating at his annual review—Apple had no idea they were about to lose an engineer who would build a $27 billion competitor.

The origin story crystallizes around a simple observation that became an obsession. Pera saw waste—wasted spectrum, wasted potential, wasted opportunity to connect millions of people. Apple saw a test engineer who needed to slow down. One company's blind spot became another company's founding vision.

What Pera understood, and what Apple missed, was that the next frontier wasn't making existing customers happier—it was reaching customers nobody else could economically serve. The teenage entrepreneur who once ran a networking company from high school had spotted a gap that the world's most innovative company couldn't see. And he was about to drive a truck through it.

III. The Bootstrap Years: Building Without Capital (2005–2010)

The apartment smells of burnt solder and instant ramen. It's March 2005, and Robert Pera's $650-per-month office in San Jose—surrounded by bail bond shops across from the courthouse—doubles as his home. He's sleeping on a cot next to prototype circuit boards, having just blown through his $30,000 in Apple stock options and maxed out his credit cards. Mr. Pera founded our Company in October 2003 and our Company began current operations in 2005. The gap between founding and operations tells a story: two years of nights and weekends while still at Apple, building prototypes in secret.

"If this doesn't work out," he remembers thinking, "I am screwed."

Pera bootstrapped the venture using approximately $30,000 of personal savings along with credit card debt. No venture capital. No angel investors. No safety net. Rather than re-up for another year, he packed up and moved into what he described as "an economical $650-per-month office" surrounded by bail bond shops across the street from the San Jose Courthouse. It would be his home for the next several months.

The contrast with typical Silicon Valley startups couldn't be starker. While his peers were raising millions in Sand Hill Road offices, Pera was hand-assembling circuit boards in what was essentially a garage startup without the garage. Bootstrap operations had no supporting infrastructure—no advisors, no board, no lawyers, no accounting support. Just an engineer with a soldering iron and a vision.

Ubiquiti's early products utilized existing Wi-Fi technology to wirelessly deliver the Internet to underserved areas (e.g., rural areas and emerging markets) lacking the infrastructure to access the Internet through traditional avenues such as phone lines and cable lines. The market opportunity was massive: billions of people worldwide had no affordable internet access. Traditional telecoms wouldn't serve them—the infrastructure costs were too high, the returns too low.

Ubiquiti Networks entered the wireless technology market in June 2005, after announcing its "Super Range" mini-PCI radio card series. The SR2 and SR5 cards were adopted by original equipment manufacturers and wireless Internet service providers. Operating at the 2.4 and 5.8 GHz bands, the "Super Range" modules used the Atheros integrated circuits. These weren't revolutionary technologies—they were existing chipsets pushed to their legal limits, packaged with custom firmware that made them actually usable.

The cards received a successful welcome and were used by many small and medium-scale Wireless Internet Service Providers worldwide. Why? Because Pera had solved a real problem. Rural WISPs needed equipment that could beam signals across miles of empty terrain. Cisco and other enterprise vendors either didn't make such products or priced them at thousands of dollars per unit. Pera's cards cost $82 to distributors.

But success brought its own challenges. However, competitors took notice and were copying his gadgets within 6 months. This wasn't just competition—it was outright theft. Chinese manufacturers were literally copying his circuit board designs, down to the component placement. To avoid further intellectual property theft, he integrated both hardware and software across a single proprietary platform. The company still combats counterfeit schemes to this day.

The early sales model was as unconventional as everything else about Ubiquiti. After Pera had left Apple, he developed a product called an embedded radio card. He peddled it at a trade show and started signing up customers. And he was apparently a good salesman, because Pera convinced customers to pay up front for it after telling them his fledgling venture had no money. Imagine that pitch: "I have no money, no company infrastructure, but I need you to pay upfront for a product from a company that barely exists." Yet it worked.

After that, Ritchie says Pera went to Taiwan and started lining up contract manufacturers. "And, literally, from that point through 2010, the company took no external capital," Ritchie says. Every dollar of growth was funded by revenue. Every product iteration was paid for by the previous product's sales.

Manufacturing was contracted to third parties in China—another controversial decision. But Pera understood something his critics didn't: by focusing solely on R&D and leveraging Asian manufacturing, he could achieve cost structures that traditional networking companies couldn't touch. A Cisco access point might cost $500; Ubiquiti could deliver similar performance for $100.

The growth was explosive. From zero revenue in 2005, the company reached $22.8 million by fiscal 2008. By 2010, revenue hit $137 million. No sales team. No marketing budget. Just products that solved real problems at prices that made sense.

But perhaps the most radical innovation wasn't technological—it was cultural. Ubiquiti didn't just sell to WISPs; it empowered them. The company's online forums became gathering places where operators shared configurations, solved problems together, and evangelized products to their peers. This wasn't customer support—it was community building.

Looking back at these bootstrap years, what's remarkable isn't just that Pera succeeded—it's that he succeeded by doing everything wrong according to conventional wisdom. No funding meant no dilution. No sales team meant no sales overhead. No traditional support meant customers had to become experts, which made them better evangelists. Every constraint became an advantage.

The boy who ran a computer services company from high school had figured out something the venture capitalists missed: sometimes the best way to build a billion-dollar company is to pretend you're still operating out of your apartment, even after you're not.

IV. The Revolutionary Business Model: Community Over Salesforce

Think of the most expensive real estate in enterprise technology: the salesperson's time. A Cisco account executive might cost $300,000 fully loaded, manage 20 accounts, and still struggle to hit quota. Now multiply that by thousands of salespeople globally. It's an army that consumes capital, creates politics, and ultimately gets passed on to customers as higher prices.

Robert Pera looked at this model and asked a heretical question: What if we just... didn't?

What makes them different from all of the other enterprise networking vendors is they employ no direct sales force or offer phone-based technical support. This wasn't a temporary bootstrap measure—it became the company's defining characteristic. No cold calls. No enterprise account managers. No solution architects doing dog-and-pony shows. Just products that sold themselves through the most powerful force in business: word of mouth.

The radical no-salesforce approach transformed every aspect of the business. Without sales overhead, Ubiquiti could price products at 70-80% less than competitors while maintaining healthy margins. Without support costs, they could invest more in R&D. Without the complexity of managing a sales organization, they could move faster and stay leaner.

But how do you actually sell enterprise equipment without salespeople? The answer was revolutionary: turn your customers into your sales force.

"Ubiquiti offers great technology at very disruptive economics and we evangelize—we sell not with salespeople but through evangelism," Pera explained. "This means that the users are operators of our technology—they form profitable businesses, they rave about it, and it spreads virally." The model was elegantly simple: build products so good and so affordable that customers couldn't help but tell others.

The community became the engine of this model. Yes, there are community forums available for support and discussions related to Ubiquiti Networks products. These forums serve as valuable platforms where users can share experiences, ask questions, and seek assistance from fellow community members. But this understates what actually happened. The forums weren't just support—they were a university, a marketplace of ideas, a place where WISPs taught each other how to build networks.

The Ubiquiti Community Forum is an excellent and resourceful place to access the wealth of knowledge from Ubiquiti Support Engineers and the entire Ubiquiti Community. R&D personnel would drop into threads, directly engaging with operators who were pushing products to their limits. Feature requests turned into firmware updates within weeks, not years. Users wrote detailed guides that became better documentation than most companies' official manuals.

The numbers tell the story of scale: By 2017, Ubiquiti's online forum had over 4M registered users. These weren't passive consumers—they were active participants in product development, testing, and evangelism. Some 2,300 distributors and interested parties worldwide have been trained in Ubiquiti products and solutions, but even this number understates the reach. Every WISP who deployed Ubiquiti gear became a de facto trainer for others in their region.

"The community is cost efficient and highly-scalable, and functions as a self-sustaining eco-system for product feedback and innovation, product support, information dissemination, and sale origination," the company noted. "It assumes the role of a sales force for Ubiquiti and in fact allows the company to function without one."

Consider what this meant for customer acquisition costs. While enterprise software companies might spend $10,000 to acquire a customer worth $50,000 in lifetime value, Ubiquiti's CAC was essentially zero. A WISP in rural Montana discovers Ubiquiti products through a forum post, deploys them successfully, then evangelizes to three other WISPs at a regional conference. Each of those WISPs does the same. The network effect compounds exponentially.

The model also created unexpected competitive advantages. Traditional vendors couldn't match Ubiquiti's prices without destroying their own business models—their existing customers would demand the same pricing. They couldn't eliminate their sales forces without alienating their channel partners. They were trapped by their own success.

But perhaps the most radical aspect wasn't what Ubiquiti didn't do—it was what this enabled them to do. "At heart, we're a software company—most of our R&D is software and most of the company is R&D, but we monetize through selling hardware," Pera explained. Without the overhead of sales and support, Ubiquiti could focus obsessively on product development.

The R&D team, consisting of 1,187 full-time equivalent employees, focuses on developing new products and versions of existing products. R&D expenses increased to $169.7 million, reflecting ongoing investment in innovation. Compare this to their sales and marketing spend: virtually nothing. The entire go-to-market strategy was essentially: build something amazing, price it aggressively, and let users discover it.

The community model also created a powerful feedback loop. The company drives brand awareness through online reviews and publications, its website, its distributors and the company's user community where customers can interface directly with R&D, marketing, and support. When thousands of operators are discussing your products daily, problems surface quickly and solutions emerge organically. It's like having thousands of unpaid product managers and QA testers.

Critics argued this model couldn't scale to enterprise. They were wrong. As Ubiquiti products proved themselves in demanding WISP deployments—often in harsh outdoor environments with zero margin for error—enterprise IT departments took notice. The same forums that served rural operators began attracting corporate IT professionals. The evangelism model worked just as well in glass towers as it did in rural fields.

The model embedded in Ubiquiti's DNA is technological leadership and products with disrupting price-performance characteristics that address customers' most critical features, without costly high-touch relationship fringe features. The model bypasses the traditional roles in sales development, marketing, and product support; and in so doing eliminates legacy inefficiencies in favor of a value-driven cost-effective and scalable model.

Looking back, what Pera built wasn't just a different sales model—it was a different relationship between company and customer. Traditional enterprise vendors saw customers as accounts to be managed. Ubiquiti saw them as partners in a movement. The difference wasn't semantic; it was fundamental. And it would power the company's rise from a $650-per-month office to a $27 billion market cap.

V. The IPO & Going Public (2011)

The conference room at UBS Investment Bank in San Francisco was tense. It was October 2011, and Robert Pera sat across from bankers who were delivering bad news: the market wasn't buying Ubiquiti's story. The original IPO range of $20-22 per share had already been cut to $15-17. Now they were recommending pricing at the absolute bottom: $15.

"Maybe we should wait," one advisor suggested. The markets were volatile, Europe was in crisis, and tech IPOs were struggling. But Pera had waited long enough. Six years of bootstrap growth. Six years of proving the model worked. It was time.

In October 2011, Ubiquiti went public, with the initial public offering of 7,038,230 shares of common stock at a price to the public of $15.00 per share. Based on the $15.00 pricing, the company will have a market capitalization of approximately $1.44 billion. The company that started with $30,000 in credit card debt was now worth over a billion dollars.

But the numbers told only part of the story. The company has grown revenue at a 106% CAGR from $22.8M in fiscal 2008 (fiscal year ends June 30) to $197.9M in fiscal 2011. Non-GAAP net income grew at a 118.8% CAGR over this period from $4.8M to $50.3M. These weren't venture-funded burn rates—this was profitable, organic growth.

The IPO structure itself was unusual. The company is selling 2.4 million shares, while shareholders are selling the remaining 4.64 million shares. Pera took the company public in 2011 and raised US$ 33.5 million in the IPO—a tiny amount by tech standards. Most of the offering was insiders cashing out small stakes. Pera himself sold nothing, maintaining his overwhelming control.

What made Ubiquiti's IPO remarkable wasn't the fundraising—it was the validation of an entirely different model. This community has over 60k members worldwide, that provide a basis for evangelism/marketing for the company. This community also provides support and training to other members within the community or new customers. Thus, the company only has a staff of 2 technical support persons, while shipping about 1 million devices per month.

Think about that ratio: 2 support staff for 1 million devices shipped monthly. Cisco probably had 2 support staff for every major account. The community model wasn't just working—it was scaling exponentially.

Wall Street struggled to understand the company. Ubiquiti's business model focuses on user experience, while delivering a product with a disruptive price/performance. They describe themselves as a software company that sells hardware. Analysts were used to evaluating companies based on sales efficiency, customer acquisition costs, and support metrics. Ubiquiti broke all their models.

The initial trading reflected this confusion. The stock opened flat, traded sideways for months. Traditional investors couldn't figure out if this was a hardware company with software margins or a software company that happened to sell hardware. The answer was neither—and both.

But for those who understood the model, the opportunity was clear. At the price range mid-point of $21, UBNT is reasonably priced at 26 times annualized earnings for the June 2011 quarter, based on expected CAGR market growth of 34%, sequential internally generated quarterly growth, and new product introductions. This wasn't a money-losing unicorn—it was a profitable company trading at reasonable multiples with explosive growth.

Since October 14, 2011, Ubiquiti's market cap has increased from $1.57B to $27.70B, an increase of 1,664.26%. That is a compound annual growth rate of 23.08%. Investors who understood the model and held have been richly rewarded.

The IPO also revealed something important about Pera's philosophy. The bulk of his wealth stems from his significant ownership of Ubiquiti Networks, where he controls around 93% of the company's stock. While other founders diluted down to single digits through funding rounds, Pera maintained iron control. This wasn't about ego—it was about alignment. When the CEO owns 93% of the company, every decision is long-term.

The public market also provided something bootstrap funding never could: currency for acquisitions and credibility with enterprise customers. Being public meant audited financials, regulatory oversight, and transparency. For conservative IT departments considering Ubiquiti products, the NASDAQ listing provided reassurance that this wasn't just another startup.

But perhaps the most important aspect of going public was what didn't change. No sudden hiring of a traditional sales force. No expensive Super Bowl ads. No pivot to enterprise software subscriptions. The same community-driven, R&D-focused model that got them to IPO would carry them forward.

Looking at the IPO in hindsight, it marked not an end but a beginning. The public markets gave Ubiquiti the platform to prove that their model could scale not just to hundreds of millions in revenue, but to billions. That a company with no salesforce could compete with Cisco. That community could replace conventional marketing. That less could indeed be more.

The bankers who pushed for the $15 price were probably right about the market timing. But they were wrong about the company's potential. That $1.44 billion market cap at IPO? It was just the first chapter in a story that would see Ubiquiti become one of the best-performing tech stocks of the decade. All while breaking every rule in the enterprise playbook.

VI. Product Innovation & Market Disruption (2009–Present)

VI. Product Innovation & Market Disruption (2009–Present)

The conference room in San Jose erupted. It was September 2009, and Pera's engineering team had just demonstrated something that shouldn't have been possible: a $79 radio delivering performance that matched Motorola's $3,000 Canopy system. They called it airMAX, and it was about to flip the wireless networking industry on its head.

airMAX, by far the most important contributor to revenues (over 60%), was introduced in September 2009. It enables wireless networking for video, voice and data. airMAX is able to support wireless network traffic for hundreds of clients per base station over long distances while maintaining low latency and high throughput. But the real innovation wasn't the technology—it was the accessibility. Suddenly, a rural ISP in Kenya could build infrastructure that rivaled what major telecoms deployed in Manhattan.

The technology solved a fundamental physics problem: how to manage hundreds of wireless connections without the chaos of collision and interference. Traditional Wi-Fi falls apart with more than a few dozen concurrent users. airMAX could handle hundreds, using a proprietary Time Division Multiple Access protocol that scheduled transmissions with military precision. WISPs could now serve entire towns from a single tower.

But Pera wasn't content with dominating rural markets. In January 2011, Ubiquiti launched UniFi, entering the enterprise WLAN market that Cisco had dominated for decades. UniFi allows WLAN managers to configure and administer a UniFi network from any web browser. No expensive controller hardware. No per-access-point licensing fees. Just download the software, run it anywhere, manage everything.

The enterprise world was skeptical. How could a company with no enterprise sales force, no professional services, no 24/7 phone support compete with Cisco Meraki or Aruba? The answer came from an unexpected place: prosumers and SMBs who were tired of paying enterprise prices for basic networking. A coffee shop didn't need Cisco's feature set—they needed reliable Wi-Fi that didn't cost a fortune.

UniFi's growth trajectory defied all conventions. By 2015, the platform was managing millions of devices globally. The UniFi Dream Machine (UDM), launched in 2019, crystallized the vision: everything you need for an UniFi network in one device. In UniFi terms, it is a UniFi OS Console, meaning it can run other UniFi software. The UDM can be a UniFi Network controller in addition to being a router, switch, and access point.

The Dream Machine was more than a product—it was a philosophy made tangible. Traditional networking required separate devices for routing, switching, wireless, and security, each with its own management interface, licensing, and support contracts. The UDM collapsed this complexity into a single $379 device that a competent IT person could deploy in minutes, not days.

It runs a full-fat edition of Ubiquiti's UniFi Network Controller software, while the integrated Advanced Security Gateway provides a business-class firewall with IDS or IPS threat protection and deep packet inspection. Features that would cost thousands in annual licenses from competitors were included free, forever. No subscriptions. No license renewals. Just buy the hardware once.

The company has since successfully branched out into other product lines such as wireless access points, security cameras, and traditional networking equipment (e.g., switches and routers). Each expansion followed the same playbook: identify a market where incumbents charge too much for too little, build a better product, price it aggressively, and let the community evangelize.

The UniFi Protect video surveillance system exemplified this approach. Traditional security camera systems required proprietary NVRs, expensive licenses per camera, and annual support contracts. UniFi Protect offered 4K cameras for under $200, free software, and no recurring fees. Small businesses that couldn't afford Axis or Hikvision enterprise systems suddenly had professional-grade surveillance.

Products and solutions are designed to reduce complexity in installation, facilitate the expansion of wireless networks, and enable high product performance at highly disruptive prices. The design philosophy was radical simplicity. Where Cisco might offer 200 configuration options, UniFi would offer 20—the ones that actually mattered. Advanced features were there for power users but hidden from those who just needed things to work.

The R&D strategy was equally unconventional. Instead of long development cycles with massive releases, Ubiquiti pushed updates constantly. The community became a real-time testing ground. Beta firmware would appear in forums, brave users would test it, problems would surface and get fixed within days. It was agile development before agile was cool.

By 2020, Ubiquiti's product portfolio spanned the entire networking stack. From long-range wireless backhauls connecting remote villages to enterprise switches powering office buildings to AI-powered security cameras, they had quietly built an empire. The company that started by pushing Wi-Fi signals further had become a full-stack networking company.

The innovation continues. Recent developments include WiFi 6E access points that push the boundaries of wireless performance, AI-driven network optimization that simplifies management, and edge computing platforms that bring processing power closer to IoT devices. Each product maintains the Ubiquiti DNA: powerful, affordable, and community-supported.

What's remarkable isn't any single product innovation—it's the consistency of execution across dozens of product lines over fifteen years. While competitors chased recurring revenue through subscriptions and locked customers into proprietary ecosystems, Ubiquiti kept building better hardware and giving away the software. It shouldn't have worked. It did.

VII. The Disruption Playbook: Price, Performance, Community

The spreadsheet made no sense. A Cisco sales engineer in 2015 stared at a competitive analysis comparing their Aironet access points to Ubiquiti's UniFi. Cisco: $1,200 per AP plus $150 annual license. UniFi: $149 per AP, no license. Same coverage. Same throughput. How was this possible?

The answer wasn't magic—it was math. Every dollar Cisco spent on sales commissions, Ubiquiti spent on R&D. Every dollar Cisco spent on marketing, Ubiquiti invested in better components. Every dollar Cisco extracted through licensing, Ubiquiti left in customers' pockets. The disruption wasn't just about technology; it was about business model arbitrage.

The company brings broadband access to the un-connected regions of the world, especially in emerging markets and rural areas. It delivers high network performance at disruptive prices, where traditional high-touch, high-cost solutions are too expensive and not easily scalable. This wasn't charity—it was strategy. By serving markets others ignored, Ubiquiti built expertise in extreme efficiency that translated to every product they touched.

Consider the unit economics. A traditional enterprise vendor might have 60% gross margins, but after sales costs (20-30%), marketing (10-15%), and support (10-15%), they're left with single-digit operating margins. Ubiquiti flipped this equation: 30-40% gross margins with virtually no sales or marketing meant 25-30% operating margins. They could sell at half the price and still be twice as profitable.

Embedded in the model is technological leadership and products with disrupting price-performance characteristics that address customers' most critical features, without costly high-touch relationship fringe features. This philosophy of "good enough" was revolutionary in enterprise technology. Ubiquiti products might not have every bell and whistle, but they had the features 90% of customers actually used—at 20% of the price.

The model bypasses the traditional roles in sales development, marketing, and product support; and in so doing eliminates legacy inefficiencies in favor of a value-driven cost-effective and scalable model. But this wasn't just cost-cutting—it was a fundamental rethinking of value creation. Instead of salespeople telling customers what they needed, the community showed each other what worked.

"At heart, we're a software company—most of our R&D is software and most of the company is R&D, but we monetize through selling hardware," Pera explained. This insight was crucial. Software has near-zero marginal cost but is hard to sell without a sales force. Hardware has real costs but sells itself. By embedding sophisticated software in affordable hardware, Ubiquiti captured software-like margins without software-like sales costs.

Manufacturing, logistics, and warehousing is contracted with third parties in China—another key to the model. While competitors built expensive factories or paid premium prices to contract manufacturers, Ubiquiti leveraged the same Chinese ecosystem that produced consumer electronics. They applied smartphone-scale economics to enterprise networking.

The community amplification effect was equally powerful. When a WISP deployed Ubiquiti gear and saved 70% versus Cisco, they didn't quietly pocket the savings—they evangelized. Forum posts detailed deployments. YouTube videos showed installations. Regional ISP conferences became Ubiquiti user groups. The cost savings were so dramatic that customers became voluntary salespeople.

Compared to traditional enterprise networking solutions, Ubiquiti provides exceptional value without recurring licensing fees. This wasn't just a pricing strategy—it was a philosophical stance. Pera believed that once you bought hardware, you owned it completely. No artificial restrictions. No features locked behind paywalls. No forced obsolescence through license expiration.

The approach created unexpected competitive moats. Traditional vendors couldn't match Ubiquiti's prices without cannibalizing their existing revenue. If Cisco offered a $150 access point, every existing customer would demand repricing. If they eliminated licensing fees, billions in recurring revenue would evaporate. They were prisoners of their own success.

The disruption extended beyond pricing to the entire customer experience. Traditional enterprise purchases involved weeks of sales meetings, proof-of-concepts, negotiations, and approvals. Ubiquiti products could be ordered online, shipped overnight, and deployed the next day. The sales cycle went from months to hours.

This speed advantage compounded. While Cisco spent six months closing a deal, a WISP using Ubiquiti had already deployed, optimized, and expanded their network. The faster iteration cycles meant Ubiquiti users were always ahead, always learning, always improving. The community's collective knowledge grew exponentially.

The model also attracted a different type of customer. Traditional enterprise vendors sold to IT departments who wanted vendor relationships, SLAs, and someone to blame when things went wrong. Ubiquiti attracted engineers who wanted to understand their networks, optimize performance, and own their infrastructure. It was the difference between renting and owning.

But perhaps the most disruptive element was sustainability. Traditional vendors needed constant revenue growth to satisfy Wall Street, driving them toward subscription models and vendor lock-in. Ubiquiti's model—profitable from day one, controlled by its founder—could optimize for long-term value over quarterly earnings. They could afford to leave money on the table because they weren't beholden to anyone except customers.

The playbook was deceptively simple: Build great products. Price them fairly. Trust the community. Repeat. No complex go-to-market strategy. No elaborate channel programs. No enterprise sales methodology. Just radical focus on product and price, with community as the amplifier.

Looking back, Ubiquiti didn't disrupt networking through superior technology—plenty of their innovations were incremental. They disrupted through business model innovation, proving that the entire edifice of enterprise sales was often unnecessary friction. In an industry obsessed with speeds and feeds, Ubiquiti's greatest innovation was subtraction.

VIII. Modern Era: Scale, Competition & Evolution (2015–Today)

The numbers were staggering. As Pera reviewed Ubiquiti's Q1 2025 results, even he seemed surprised by the acceleration. Ubiquiti revenue for the quarter ending March 31, 2025, was $0.664B, a 34.72% increase year-over-year. Ubiquiti revenue for the twelve months ending March 31, 2025, was $2.322B, a 21.43% increase year-over-year. The bootstrap startup was now generating over $2 billion annually—still with no sales team.

Ubiquiti has a market cap or net worth of $27.15 billion. The enterprise value is $27.38 billion. To put this in perspective, Ubiquiti is worth more than many traditional networking companies that have existed for decades. Juniper Networks, founded in 1996 with massive VC backing, trades at a similar valuation despite having 10 times more employees.

The modern era brought new challenges. As Ubiquiti grew, so did scrutiny. In 2021, a whistleblower accused the company of downplaying a data breach. The stock crashed 20% in a day. But what happened next was telling: the community rallied. Users shared their continued faith in the products. The stock recovered. The scandal that might have destroyed a traditional vendor barely dented Ubiquiti's momentum.

Product evolution accelerated. The UniFi ecosystem expanded beyond networking into a complete infrastructure platform. UniFi Access brought keyless entry systems. UniFi Talk introduced VoIP phones. UniFi Connect delivered high-speed fiber aggregation. Each product followed the same formula: enterprise features at prosumer prices with zero licensing fees.

Pera believes Ubiquiti is just getting started diversifying into other technologies, including pursuits into microwave backhaul, machine-to-machine networking, video surveillance, and advanced routing and switching. The vision was becoming clear: Ubiquiti wasn't just disrupting networking—they were building the infrastructure layer for the connected world.

The lean organization remained remarkably lean. The company historically maintains a lean executive team, with Mr. Pera deeply involved in operational and strategic oversight. While competitors had layers of VPs and SVPs, Ubiquiti operated more like a 200-person startup than a $2 billion company. Decisions that would take months at Cisco could be made in days at Ubiquiti.

Competition intensified from unexpected directions. Amazon entered networking with eero. Google pushed Nest WiFi. Chinese manufacturers like TP-Link moved upmarket. But Ubiquiti's position proved defensible. Consumer brands couldn't match their enterprise features. Enterprise vendors couldn't match their prices. Chinese competitors couldn't match their community.

The pandemic became an unexpected accelerant. As millions worked from home, consumer-grade networking proved inadequate. IT departments, forced to support remote work immediately, discovered UniFi's ease of deployment. Small businesses, crushed by lockdowns, needed enterprise features at survival prices. Ubiquiti was perfectly positioned for both.

In October 2012, Pera also became the owner of the Memphis Grizzlies of the National Basketball Association. The official sale of the Memphis Grizzlies to Pera was approved on October 25, 2012. The purchase price of $377 million seemed extravagant then. Today, the franchise is worth over $3 billion. Pera had applied the same contrarian thinking to basketball—buying an undervalued asset in a small market and building long-term value.

The financial performance in the modern era validated every unconventional decision. Return on equity reached absurd levels—237.68% in recent quarters. Return on invested capital hit 50.29%. These weren't software margins achieved through financial engineering—this was a hardware company generating returns that made SaaS companies jealous.

The stock price has increased by +154.51% in the last 52 weeks. The beta is 1.35, so Ubiquiti's price volatility has been higher than the market average. But long-term holders barely noticed the volatility. From the IPO price of $15 to today's $400+ per share, patient investors had seen 30x returns.

Recent innovations showed no slowdown in ambition. WiFi 7 access points pushed wireless speeds past wired connections. AI-powered cameras could identify people, vehicles, and packages without cloud processing. Edge computing appliances brought data center capabilities to branch offices. Each product pushed boundaries while maintaining the Ubiquiti formula.

The organization structure evolved but retained its core DNA. Engineering teams remained small and autonomous. The community continued driving product direction. Support stayed minimal—the forums now had millions of posts solving almost every conceivable problem. The anti-enterprise model had scaled to enterprise scale.

Manufacturing strategy sophisticated while staying lean. Multiple contract manufacturers provided redundancy. Just-in-time production minimized inventory risk. Direct-to-customer sales eliminated channel markup. The operations that started in a $650 apartment now moved billions in hardware globally.

What's most remarkable about Ubiquiti's modern era is what hasn't changed. Still no sales team. Still no licensing fees. Still the same focus on price-performance. Still the same community-first approach. While every other technology company pivoted to subscriptions and recurring revenue, Ubiquiti stayed true to its original vision.

The future roadmap suggests continued expansion. 5G infrastructure for private networks. IoT platforms for smart cities. Edge AI for autonomous systems. Each market represents billions in opportunity. Each market is currently served by expensive, complex solutions. Each market is ripe for the Ubiquiti treatment.

Looking at Ubiquiti today, you see a paradox: a $27 billion company that still operates like a startup. A hardware company with software margins. An enterprise vendor with no enterprise sales. A global corporation run like a family business. These contradictions aren't bugs—they're features. They're what happens when you ignore conventional wisdom and focus relentlessly on what actually matters: building great products that customers love at prices that make sense.

IX. Analysis & Bear vs. Bull Case

The spreadsheet glowed on the analyst's screen at Morgan Stanley. The numbers didn't fit any traditional model. Return on equity (ROE) is 237.68% and return on invested capital (ROIC) is 50.29%. These weren't typos. A hardware company was generating returns that would make Google jealous. How do you value something that breaks every rule?

Let's start with the strengths, because they're almost absurd in their magnitude. The community-driven model creates defensibility that traditional moats can't match. You can't acquire Ubiquiti's community. You can't replicate millions of forum posts. You can't manufacture the authentic evangelism of operators who've built businesses on your products. This isn't customer lock-in through contracts—it's lock-in through love.

No recurring licensing fees versus competitors isn't just a pricing advantage—it's a philosophical moat. Once the industry expects your software to be free, you can never charge for it. But competitors who've trained customers to pay annually can never stop charging without imploding their business models. Ubiquiti has essentially forced the industry into an asymmetric competition where only they can afford to compete.

The product-market fit in underserved segments created expertise that translates everywhere. By solving the hardest problems first—connecting rural Africa, enabling Arctic research stations, linking island nations—Ubiquiti built products that work anywhere. When your gear operates in the Sahara and Siberia, a climate-controlled data center is easy mode.

The capital efficiency is unprecedented. In the last 12 months, Ubiquiti had revenue of $2.32 billion and earned $549.02 million in profits. Earnings per share was $9.08. Most hardware companies barely break even. Most software companies burn cash for growth. Ubiquiti prints money while growing 20%+ annually.

But the bear case has merit. The dependence on founder-CEO is extreme. Pera owns 93% of shares and makes every major decision. What happens when he loses interest? Who succeeds someone who is simultaneously CEO, head of product, and chief engineer? The company is essentially a projection of one man's vision—brilliant but fragile.

Limited enterprise support versus traditional vendors remains a real constraint. Fortune 500 companies want someone to call at 3 AM when the network dies. They want SLAs with financial penalties. They want professional services to design and deploy. Ubiquiti offers none of this. There's a ceiling to community support, and that ceiling might be lower than the total addressable market.

Competition from both low-end and high-end is intensifying. Amazon can sell at zero margin to gain market share. Cisco can bundle networking with software and services. Chinese manufacturers can undercut on price. Ubiquiti sits in the middle—too expensive for pure price buyers, too basic for enterprise buyers, perfect for a segment that might be smaller than bulls believe.

The market dynamics tell a mixed story. The stock price has increased by +154.51% in the last 52 weeks. The beta is 1.35, so Ubiquiti's price volatility has been higher than the market average. This volatility reflects the uncertainty. One quarter's miss could crater the stock. One product recall could destroy trust. One Pera decision could change everything.

The trailing PE ratio is 49.43 and the forward PE ratio is 49.98. These are expensive multiples for a hardware company, reasonable for a software company, cheap for a high-growth SaaS business. But Ubiquiti is none of these and all of these simultaneously. Traditional valuation frameworks simply don't apply.

The regulatory risks are underappreciated. Ubiquiti manufactures in China during a trade war. They sell globally during rising nationalism. They operate with minimal compliance infrastructure during increasing regulation. Any of these could explode. The lean operation that enables efficiency also creates vulnerability.

Product complexity is growing faster than the organization. Managing dozens of product lines with minimal structure works until it doesn't. Quality issues have emerged—firmware bugs, hardware recalls, shipping delays. The community forgives because they love the company, but love has limits.

The innovation pace might be unsustainable. Ubiquiti essentially rebuilds every product category they enter. But networking is consolidating. Standards are solidifying. The opportunities for 10x improvements are diminishing. What happens when Ubiquiti can only offer 2x better instead of 10x better?

Market saturation in core segments is approaching. Most WISPs who would use Ubiquiti already do. Most SMBs aware of alternatives have already switched. Growth requires entering new markets or converting enterprise customers—both harder than the original land grab.

Yet the bull case remains compelling. The TAM expansion opportunity is massive. Private 5G, IoT infrastructure, edge computing—each market is larger than Ubiquiti's current business. The same model that disrupted WiFi could disrupt cellular, security, and computing. The playbook is proven; it just needs new stages.

The subscription revenue option remains untapped. Ubiquiti could launch optional cloud services, managed services, or premium support tomorrow and likely generate hundreds of millions in recurring revenue. They choose not to, but the option has value. It's like holding a call option on the entire SaaS business model.

The balance sheet provides enormous flexibility. With minimal debt and massive cash generation, Ubiquiti could acquire, invest, or return capital. They could weather any storm, fund any project, or pivot any direction. Few companies have such strategic flexibility.

Looking at both cases, the truth is probably in the middle. Ubiquiti isn't going to displace Cisco in the Fortune 500, but they don't need to. They're not going to maintain 200% ROE forever, but they don't need to. They're building a different kind of technology company—one that prioritizes products over process, community over convention, efficiency over expansion.

The investment case ultimately comes down to a belief about the future of technology distribution. If you believe enterprise sales forces, channel partners, and professional services remain necessary, Ubiquiti is overvalued. If you believe community, self-service, and product quality can replace traditional go-to-market, Ubiquiti might be the future.

X. Playbook: Business & Investing Lessons

The conference room at Andreessen Horowitz was silent. The partners had just heard a pitch from a founder who wanted to build "the Ubiquiti of" something—the phrase had become shorthand for bootstrap success and community-driven growth. "But can it be replicated?" asked one partner. "Or was Ubiquiti a one-time phenomenon?"

The anti-Silicon Valley model stands as perhaps the most important lesson: bootstrapping to billions isn't just possible—it might be preferable. Pera proved that consuming capital doesn't create value; building products customers want creates value. Every dollar not raised was a dollar of dilution avoided. Today, Pera's 93% stake is worth $25 billion. The VCs who never invested? They're still searching for the next Ubiquiti.

But the deeper lesson isn't about avoiding venture capital—it's about the freedom that comes from not needing it. When you're not beholden to investors demanding 10x returns, you can price products fairly. When you're not racing to the next funding round, you can think in decades. When you don't need board approval, you can make decisions in minutes. The bootstrap model wasn't just about ownership—it was about optionality.

Community as competitive advantage might be Ubiquiti's most replicable insight. Every company talks about community, but few make it central to their model. Ubiquiti proved that community isn't just marketing—it's product development, customer support, sales, and R&D rolled into one. The lesson: don't build community around your product; build your product around community.

The mechanism matters. Ubiquiti didn't just create forums and hope for the best. They had engineers actively participate. They implemented feedback quickly. They celebrated power users. They made the community feel like owners, not customers. This wasn't community management—it was community empowerment.

Vertical integration for margin and control offers another masterclass. While the tech world obsessed over asset-light models, Ubiquiti went the opposite direction. By controlling hardware design, software development, and manufacturing relationships, they captured margin at every step. They could optimize the entire stack, not just one layer. The lesson: sometimes owning more of the value chain creates more value.

But vertical integration wasn't about doing everything—it was about controlling what mattered. Ubiquiti didn't manufacture; they managed manufacturers. They didn't ship; they managed logistics. They owned the design and relationship while outsourcing the operations. It was vertical integration without the capital intensity.

The power of saying "no" to traditional enterprise sales reveals how much of enterprise technology is waste. Every salesperson eliminated freed budget for engineering. Every marketing campaign not run meant lower prices for customers. Every support call avoided meant faster product iteration. The lesson: addition by subtraction is real. What you don't do defines you as much as what you do.

This extends beyond sales. Ubiquiti said no to product complexity, offering fewer SKUs with better focus. They said no to acquisition offers that would have made Pera rich but compromised the model. They said no to Wall Street pressure for subscription revenue. Every "no" strengthened their position.

When contrarian approaches work (and when they don't) provides crucial context. Ubiquiti succeeded because they zigged when everyone zagged, but timing mattered. They entered networking when incumbents were fat and happy. They targeted customers others ignored. They built for the future (distributed work) while competitors optimized for the past (central offices). The lesson: contrarian isn't enough—you need contrarian plus correct.

The model also had natural limits. It worked in networking where products are tangible and community expertise valuable. It might not work in pure software where support expectations are higher. It might not work in regulated industries where compliance requires process. The lesson: even brilliant models have boundaries.

Capital efficiency changes everything. In the last 12 months, Ubiquiti generated $549 million in profit on $2.32 billion in revenue—24% net margins in hardware. This efficiency created a flywheel: profits funded R&D, better products attracted more customers, more customers strengthened community, stronger community reduced costs, lower costs enabled lower prices, lower prices attracted more customers. The lesson: efficiency isn't just about margins—it's about momentum.

The investing lessons are equally powerful. First, founder-led companies with significant ownership often outperform. Pera's 93% stake meant every decision optimized for long-term value. Second, companies with structural cost advantages can maintain them longer than expected. Ubiquiti's model has worked for 20 years. Third, community moats are real and undervalued by traditional analysis.

The framework for evaluation: When examining any company, ask: What are they not doing that everyone else is? How does that create advantage? Is that advantage structural or temporary? Can competitors copy it without destroying their own models? Ubiquiti scores perfectly on all counts.

For founders, the playbook is clear but challenging. Start with a real problem you deeply understand. Bootstrap as long as possible to maintain control and force efficiency. Build community from day one, not as marketing but as core strategy. Say no to conventional wisdom but yes to customer feedback. Focus relentlessly on product-market fit over fundraising-market fit.

For operators, the lessons translate. Every hire should be essential. Every process should add clear value. Every feature should matter to real users. Every price should be fair, not maximal. Every decision should consider second-order effects. Ubiquiti proved that operational excellence isn't about doing more—it's about doing less, better.

The meta-lesson might be most important: business model innovation can be more powerful than technical innovation. Ubiquiti didn't invent new networking protocols. They invented a new way to develop, sell, and support networking products. In a world obsessed with deep tech and AI, sometimes the biggest opportunity is rethinking business basics.

Looking forward, the Ubiquiti playbook will be tested by imitators and market changes. But the principles—community over sales, efficiency over growth, product over process—feel timeless. In an industry that worships complexity, Ubiquiti's radical simplicity might be the most sophisticated strategy of all.

XI. Epilogue & Final Thoughts

The Austin skyline glows orange as sunset approaches. Robert Pera, now 46, still comes to Ubiquiti's headquarters early and stays late. The company that started in a $650-per-month office has beautiful facilities now, but Pera's office remains spartan—a desk, multiple monitors, and prototype hardware scattered everywhere. He's still the chief engineer, still reading forum posts, still obsessing over antenna patterns and firmware optimization.

What Ubiquiti means for the future of enterprise technology extends far beyond networking. They've proven that the entire superstructure of enterprise sales—the armies of salespeople, the elaborate channel programs, the expensive marketing campaigns—might be unnecessary. Not just inefficient, but actively harmful to value creation. In a world where every company claims to be "customer-centric," Ubiquiti actually built a company where customers are central to everything.

The implications are staggering. If a hardware company can achieve software margins without sales teams, what else is possible? If community can replace professional support, what other orthodoxies are wrong? If bootstrapping can build billion-dollar businesses, why does venture capital exist? Ubiquiti isn't just a successful company—it's an existence proof that alternative models can work at scale.

The sustainability of the community model at scale remains the key question. Can forums and evangelism work at $5 billion in revenue? $10 billion? The evidence suggests yes, but with evolution. The community that started as WISPs sharing configuration tips has grown into a global network of IT professionals, integrators, and enthusiasts. The model scales because expertise scales—every new user potentially becomes a teacher.

But sustainability doesn't mean stasis. The community model must evolve with technology. As products become more complex, documentation must improve. As deployments grow larger, tools must become more sophisticated. As expectations rise, quality must increase. Ubiquiti seems to understand this, investing heavily in software that makes products easier to deploy and manage.

Lessons for founders crystallize around courage—the courage to ignore conventional wisdom when you know you're right. Pera could have raised venture capital, hired salespeople, and built a traditional networking company. He probably would have been successful—maybe sold to Cisco for a few hundred million. Instead, he had the courage to build something different, something that shouldn't have worked but did.

When to ignore conventional wisdom becomes clear through Ubiquiti's example: when conventional wisdom serves the industry more than customers. Enterprise sales forces don't exist because customers demand them—they exist because they've always existed. Professional services don't add value—they extract it. Licensing fees don't improve products—they improve quarterly earnings. When an industry practice benefits everyone except the end user, it's ripe for disruption.

The next decade promises new challenges and opportunities. AI and edge computing will transform networking from dumb pipes to intelligent infrastructure. Private 5G will enable new applications we can't imagine. IoT will connect billions of devices that need management. Each shift creates openings for the Ubiquiti model—complex technology that needs to be simple, expensive solutions that need to be affordable.

Ubiquiti's preparedness for these shifts seems strong. Their software-defined approach means they can adapt quickly. Their community provides real-time feedback on emerging needs. Their efficiency enables aggressive pricing in new markets. Most importantly, their independence from Wall Street means they can invest for the long term without worrying about quarterly earnings.

The deeper meaning of Ubiquiti transcends business metrics. In an era of surveillance capitalism and vendor lock-in, Ubiquiti represents something pure: a company that makes products, sells them fairly, and trusts customers to figure out the rest. No dark patterns. No forced subscriptions. No planned obsolescence. Just the radical idea that if you build great products at fair prices, everything else takes care of itself.

This philosophy feels both ancient and revolutionary. Ancient because it's how business worked before financial engineering and growth hacking. Revolutionary because it works better than modern alternatives. Ubiquiti proves that sustainable business models aren't just ethical—they're more profitable.

The personal story adds resonance. Pera, now worth over $25 billion, still drives himself to work and reads bug reports. He hasn't sold a single share since IPO. He hasn't done a single media tour. He hasn't written a book or given a TED talk. He just keeps building products. In an industry of celebrity CEOs and thought leaders, Pera's invisibility is its own statement.

What would technology look like if every company followed Ubiquiti's model? Products would be cheaper and better. Innovation would focus on customer value, not vendor lock-in. Communities would flourish around shared expertise rather than marketing messages. The entire technology industry would be more democratic, more accessible, more human.

Of course, not every company can follow this model. Some products genuinely need professional support. Some markets require traditional sales. Some innovations need venture capital to reach scale. But Ubiquiti proves that the exceptions might be rarer than we think. How many enterprise sales teams exist simply because that's how it's always been done?

As we look toward the future, Ubiquiti stands as both inspiration and challenge. Inspiration for entrepreneurs who want to build differently. Challenge to incumbents who thought their models were safe. The company that started as a nights-and-weekends project has become a $27 billion reminder that there's always another way.

The final lesson might be the simplest: focus matters more than resources. Ubiquiti had less money, fewer people, and no precedent. But they had clarity about what mattered—building great products for underserved customers at revolutionary prices. That focus, maintained for twenty years, built an empire.

In Silicon Valley's casino of venture capital and growth-at-all-costs, Ubiquiti played a different game entirely. They proved you could build a technology giant without playing by technology giant rules. They proved that community could beat capital, that efficiency could beat scale, that products could beat process.

The anti-enterprise networking empire isn't just Ubiquiti's story—it's a blueprint for anyone brave enough to build something different. In a world that insists there's only one way to build a technology company, Ubiquiti whispers: "Try another way." Sometimes, the whisper changes everything.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube