Universal Health Realty Income Trust: The Quiet Healthcare REIT

Introduction and Episode Roadmap

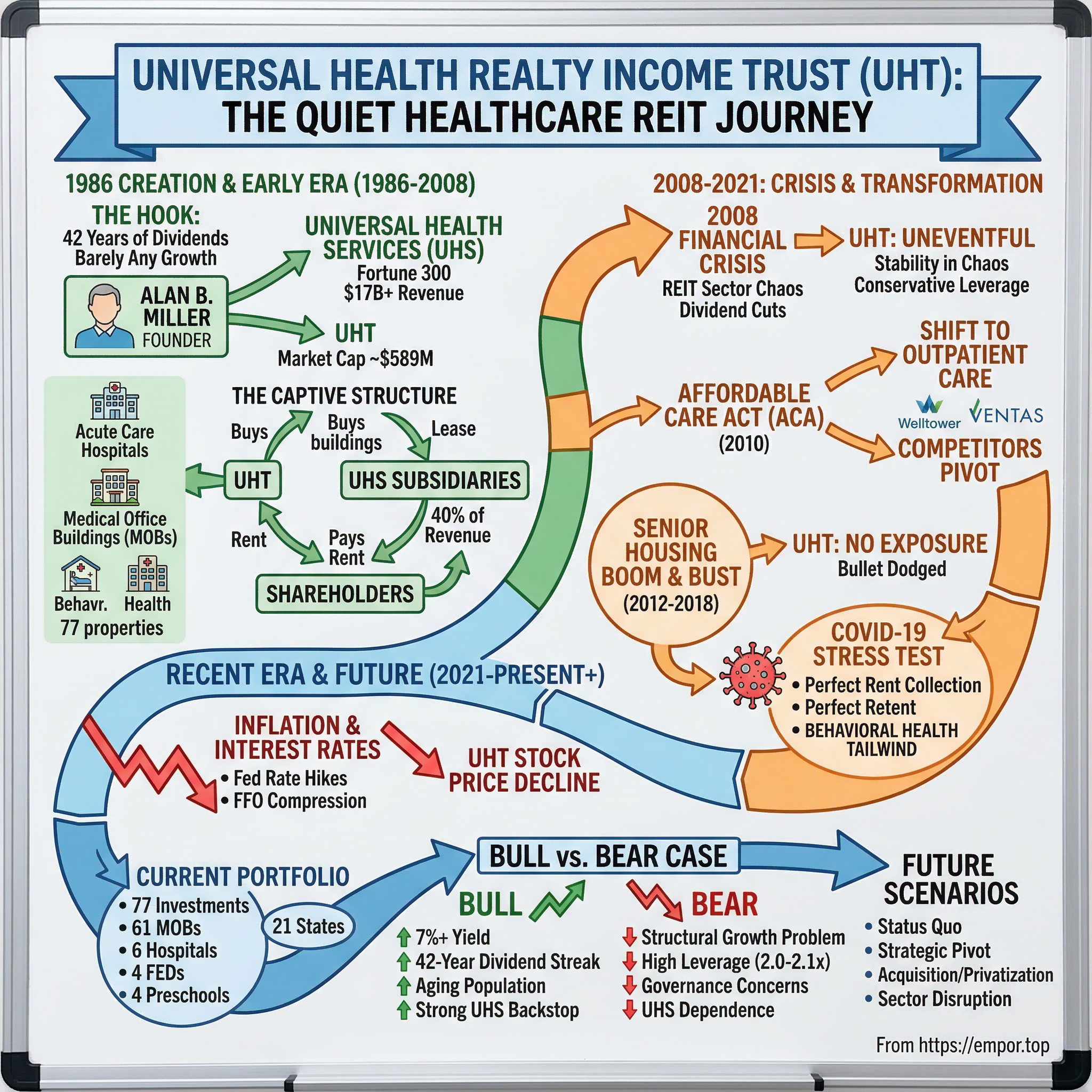

Somewhere on the New York Stock Exchange, tucked between flashier tickers and billion-dollar biotech plays, sits a real estate investment trust with a market cap of roughly $589 million. Universal Health Realty Income Trust trades under the symbol UHT, and unless you are a dividend-focused income investor with a taste for obscurity, you have almost certainly never heard of it. It owns about 77 healthcare properties across 21 states. It has paid dividends for 42 consecutive years. And it has barely grown in a decade.

That last detail is the hook. How does a REIT founded in 1986 by a hospital operator survive every healthcare crisis, every financial meltdown, every revolution in care delivery, and every interest rate cycle for four decades while remaining, by almost any measure, strategically stagnant? The answer turns out to be more interesting than the question suggests. This is not a story about growth or disruption. It is a story about strategic patience, captive relationships, and what happens when a publicly traded company functions as the real estate side hustle of a much larger enterprise.

Universal Health Realty Income Trust was created by Universal Health Services, a Fortune 300 hospital operator now generating over $17 billion in annual revenue. From day one, UHT existed to serve UHS: buying hospital buildings from its parent, leasing them back under long-term triple-net leases, and distributing the rental income to shareholders. Nearly forty years later, the structure is virtually unchanged. UHS subsidiaries still account for roughly 40 percent of UHT's consolidated revenue. All of UHT's officers are employees of a UHS subsidiary. Alan B. Miller, the man who founded both companies, still chairs UHT's board at age 88.

The themes here are ones that rarely make headlines but matter deeply to a certain kind of investor: healthcare real estate fundamentals, the peculiar economics of parent-subsidiary dynamics, the power of boring consistency, and the question of whether survival alone constitutes a strategy. While competitors like Welltower grew into a $96 billion behemoth and Ventas built a $27 billion empire, UHT just kept paying its quarterly dividend and doing essentially nothing dramatic. The most interesting thing about UHT is how determinedly uninteresting it is. And in a market obsessed with growth, disruption, and transformation, that very boredom tells us something important about what it means to endure.

The Healthcare REIT Context and UHT's Creation

Picture Washington, D.C. in the autumn of 1986. Ronald Reagan signed the Tax Reform Act that October, and among its sprawling provisions was a seemingly technical change that would reshape American real estate: REITs could now operate and manage their own properties directly, rather than farming everything out to independent contractors. Before this legislation, REITs were passive investment vehicles, essentially holding companies with severe operational restrictions. After it, they could become active businesses. The modern REIT era was born.

Alan B. Miller saw the opportunity immediately. By 1986, Miller was already one of America's most tenacious healthcare entrepreneurs. Born in 1937 in Crown Heights, Brooklyn, the son of a dry cleaning store owner and a millinery worker, he had clawed his way to the College of William and Mary on a basketball scholarship. A near-fatal car accident on the way to a game against the University of Pennsylvania ended his athletic career, but he recovered, finished his degree, and earned an MBA from Wharton. His first career was in advertising at Young and Rubicam, where he became one of the firm's youngest vice presidents and developed one of the first nationally syndicated television programs, The Galloping Gourmet with Graham Kerr. But healthcare, not advertising, would define his life.

In 1969, Miller founded American Medicorp, a pioneering hospital management company. He built it into a significant operator of private hospitals, took it public, and then watched helplessly as Humana launched a hostile takeover in 1978. Miller fought the bid furiously, forcing Humana to raise its offer from roughly $11 per share to over $27, but he could not prevent the acquisition. The experience scarred him. "He walked down the street with five associates," as one company history recounts, and immediately founded Universal Health Services. UHS started with six employees, zero revenue, and a $1 million market value. Within 18 months, it owned four hospitals and managed two more. By 1986, Miller had built a substantial and growing hospital empire, and the Tax Reform Act handed him the tools to unlock the real estate value embedded in those buildings.

The strategic rationale for creating UHT was elegant. By selling hospital properties to a newly formed REIT and leasing them back, UHS could immediately unlock capital that was tied up in bricks and mortar, redeploy that cash into operations and acquisitions, and improve its balance sheet ratios. The REIT structure added a layer of tax efficiency: as long as UHT distributed at least 90 percent of its taxable income as dividends, it would pay no federal income tax at the corporate level. The sale-leaseback model meant UHS kept operating control of its facilities while shedding the real estate from its balance sheet. It was financial engineering in the best sense, a genuine win-win for both entities.

Universal Health Realty Income Trust commenced operations on December 24, 1986, organized as a Maryland real estate investment trust. At inception, UHT acquired healthcare properties from UHS in exchange for shares. The founding structure was deliberately captive: UHT existed to serve UHS. An Advisory Agreement, renewable annually, formalized the relationship. UHS of Delaware, a wholly-owned UHS subsidiary, would serve as UHT's advisor, earning an advisory fee of 0.70 percent of average invested real estate assets. All UHT officers would be UHS employees. All major transactions between the two entities would require approval from independent trustees unaffiliated with UHS.

Healthcare real estate is fundamentally different from offices, retail, or apartments. Hospitals and medical facilities are specialized, purpose-built assets with high replacement costs, complex regulatory requirements, and limited alternative uses. You cannot easily convert a behavioral health hospital into a WeWork. Certificate-of-need laws in many states restrict who can build new facilities, creating barriers to entry. And healthcare demand is largely non-discretionary: people get sick regardless of the economic cycle. These characteristics make healthcare real estate inherently defensive but also somewhat illiquid and hard to re-tenant if a lease falls through.

While UHT was quietly establishing itself as a captive healthcare REIT in the late 1980s, the broader sector was entering a gold rush. Health Care REIT (now Welltower) had been around since the early 1970s, initially financing nursing home construction. Ventas, Healthpeak, and a constellation of smaller players would emerge through the 1990s and 2000s, pursuing aggressive acquisition strategies and diversifying into senior housing, life sciences, and medical office buildings. They raised billions, acquired thousands of properties, and built institutional-scale platforms. UHT mostly sat out this expansion. It had its parent company's buildings, its steady lease income, and its quarterly dividend. That was enough.

The First Two Decades: Steady State Strategy (1986-2008)

For the first two decades of its existence, UHT operated with the quiet rhythm of a well-maintained clock. The business model was simple and repetitive: acquire healthcare properties, primarily from UHS, lease them back under long-term triple-net leases, collect rent, pay dividends. The portfolio consisted of acute care hospitals, behavioral health facilities, and a growing collection of medical office buildings. Revenue grew slowly, from roughly $22 million in the mid-1990s to about $28 million by 2007. The company was not trying to grow fast. It was trying to be reliable.

The growth pattern told the story of UHT's constraints and its choices. While Welltower was acquiring nursing homes and senior living facilities by the hundreds, and Ventas was building a diversified healthcare real estate empire under CEO Debra Cafaro, UHT stayed heavily weighted toward UHS transactions. When UHS built or acquired a new hospital, some of those properties might flow to UHT through a sale-leaseback. When UHS did not need capital recycling, UHT's pipeline dried up. Third-party acquisitions were rare, limited by UHT's small size, higher cost of capital, and the inherent constraint of being externally managed by an entity whose primary loyalty was to UHS.

The parent-subsidiary dynamics created a peculiar equilibrium. On the benefit side, UHT had a built-in tenant with strong credit. UHS was a large, profitable hospital operator with investment-grade financial characteristics. Its leases were unconditionally guaranteed by UHS and cross-defaulted with one another, meaning that if UHS defaulted on one lease, it would trigger a default on all of them, a structure that made selective default essentially impossible. Tenants do not get much more creditworthy than that in the healthcare REIT world. On the constraint side, UHT's growth was fundamentally limited by UHS's real estate strategy. If UHS preferred to own its buildings outright, or sell them to third parties, UHT had no alternative pipeline. The captive structure provided stability at the cost of optionality.

Related-party transaction scrutiny was a persistent undercurrent. Every deal between UHT and UHS required independent trustee approval. Fair value determinations on property transfers had to withstand regulatory and shareholder scrutiny. The advisory fee, which ran about $5.5 million annually on $783 million in invested assets by 2024, was an ongoing cost that independent REITs simply did not bear. Critics pointed to the inherent conflict: Alan Miller chaired both entities, all UHT officers were UHS employees, and the people managing UHT's affairs had their primary economic allegiance to UHS. Defenders countered that the independent trustee oversight, SEC disclosure requirements, and UHS's own 5.7 percent ownership stake in UHT aligned interests sufficiently.

Through it all, the dividend kept compounding. Not spectacularly, not with double-digit growth, but with the kind of modest, clockwork consistency that appeals to a specific investor archetype. The management philosophy, to the extent one can discern it from two decades of quiet execution, was essentially: "We are not trying to be Welltower." UHT was a capital recycling vehicle for UHS and a dividend income vehicle for shareholders. Miller's influence through UHS ensured that the relationship remained stable, the leases remained in place, and the quarterly payments kept flowing. By the time the financial crisis arrived in 2008, UHT had spent 22 years proving that it could do one thing well. Whether that one thing was enough remained an open question.

The Financial Crisis: Stability in Chaos (2008-2010)

On September 15, 2008, Lehman Brothers filed for bankruptcy, and the commercial real estate world descended into chaos. Credit markets froze. Property values cratered. REITs across every sector faced margin calls, covenant breaches, and existential questions about whether they could refinance maturing debt. General Growth Properties, one of the largest mall REITs in the country, filed for bankruptcy in April 2009. Dividend cuts swept through the REIT sector like wildfire. It was the worst environment for leveraged real estate companies since the savings and loan crisis of the early 1990s.

Healthcare REITs fared better than most, but they were not immune. Ventas navigated the crisis by maintaining its acquisition discipline and conservative balance sheet, but many peers faced genuine distress. HCP, the largest healthcare REIT at the time, would eventually have to restructure its troubled relationship with Manorcare. Smaller healthcare REITs with aggressive leverage profiles found themselves locked out of capital markets at precisely the moment they needed to refinance. The crisis was a brutal stress test of business models, capital structures, and management quality.

UHT's experience during the financial crisis can be summarized in a single word: uneventful. First-half 2008 funds from operations came in at $14.8 million, essentially flat with the prior year's $14.8 million. Net income declined, largely due to non-cash items like depreciation adjustments and the absence of property sale gains, but the core business kept humming. Revenue held steady at about $29 million in 2008 and actually increased to $31.9 million in 2009. Most critically, the dividend was maintained and continued its growth streak, a feat that many larger, more diversified REITs could not match.

The advantage of UHT's boring, captive structure became apparent in crisis. Conservative leverage meant no covenant breaches and no desperate need to raise equity at fire-sale prices. Long-term triple-net leases with UHS meant no rent renegotiations, no tenant bankruptcies, and no vacancy spikes. Healthcare demand proved non-discretionary: people needed hospitals regardless of whether Lehman Brothers existed. The UHS guarantee backstopping UHT's leases provided a level of credit quality that most commercial real estate landlords could only envy. While competitors scrambled to shore up balance sheets and navigate distressed acquisition opportunities, UHT simply continued collecting rent and paying dividends.

The lesson was straightforward but easy to overlook: sometimes the best strategy in a crisis is having no exciting strategy at all. UHT did not make opportunistic acquisitions during the downturn. It did not raise capital to take advantage of distressed pricing. It did not restructure its portfolio or pursue strategic alternatives. It just kept doing what it had been doing for 22 years. For shareholders who owned UHT for income rather than capital appreciation, this was exactly what they wanted. For growth-oriented investors, it was another data point confirming that UHT was not the vehicle for them. Both conclusions were correct, and that tension would only intensify in the decade to come.

The 2010s: Healthcare Real Estate Transformation

The Affordable Care Act, signed by President Obama on March 23, 2010, reshaped American healthcare delivery in ways that are still unfolding. For healthcare real estate, the implications were profound. The law insured millions of previously uninsured Americans, creating a surge in demand for primary care, specialty services, and outpatient facilities. More fundamentally, the ACA accelerated a structural shift from fee-for-service reimbursement toward value-based care, which incentivized providers to deliver services in lower-cost outpatient settings rather than expensive inpatient hospitals. Compared with 2015, outpatient construction projects doubled across most categories: ambulatory surgery centers, immediate care facilities, and medical office buildings. The healthcare real estate playbook was being rewritten in real time.

UHT's portfolio was not ideally positioned for this transformation. Its core holdings were acute care hospitals and behavioral health facilities leased to UHS, the very inpatient assets that the ACA's incentive structures were pushing care away from. The company's growing collection of medical office buildings was better aligned with the outpatient trend, but UHT's MOB portfolio grew slowly, constrained by the same captive dynamics that limited all of its growth. Meanwhile, competitors pivoted aggressively. Healthpeak invested heavily in life sciences properties near major research universities. Welltower and Ventas poured billions into senior housing. Healthcare Realty Trust built a pure-play medical office platform. The industry was transforming, and UHT was watching from the sidelines.

The senior housing boom and bust of 2012 through 2018 was one of the defining episodes in healthcare REIT history, and UHT's absence from it tells us as much as any acquisition it could have made. The RIDEA structure, introduced in 2007 and expanded in 2009, allowed REITs to participate in the operating profits of senior housing communities rather than simply collecting rent under triple-net leases. This was catnip for yield-hungry investors in a low interest rate environment. Capital flooded into senior housing development. Construction starts soared. Welltower, Ventas, and a wave of private equity firms built and acquired assisted living and memory care communities at a frenetic pace.

By 2015, oversupply was becoming evident in markets like San Antonio, Dallas, Atlanta, and Houston. New supply kept coming even as occupancy rates declined. Brookdale Senior Living, the nation's largest senior living operator and a key partner for multiple REITs, faced persistent operating challenges. By 2016 through 2018, senior housing occupancy had collapsed enough to force dividend cuts at several healthcare REITs. Welltower and Ventas, with their massive senior housing operating portfolios, faced meaningful NOI headwinds. Healthpeak, then still trading as HCP, undertook a wrenching portfolio restructuring, spinning off its troubled skilled nursing portfolio into a separate entity called Quality Care Properties to sever its toxic relationship with Manorcare.

UHT had essentially zero exposure to senior housing during this entire period. It never chased the RIDEA yields, never leveraged up to buy assisted living communities, never hired a senior housing operating team. Was this a missed opportunity? In hindsight, it was a bullet dodged. The senior housing bust destroyed significant shareholder value at competitors that had overextended. UHT's hospital and MOB focus, boring as it was, protected the portfolio from the carnage. The captive structure that limited UHT's growth also limited its capacity for the kind of strategic overreach that burned larger peers.

On January 30, 2018, Amazon, Berkshire Hathaway, and JPMorgan Chase announced Haven, a joint venture to provide low-cost, high-quality healthcare for their combined million-plus employees. The announcement sent shockwaves through the healthcare sector. Stock prices of healthcare companies tumbled on fears that the combined might of leaders in technology and finance could disrupt the entire system. Healthcare REIT investors briefly panicked: if tech could disintermediate healthcare delivery, what would happen to the buildings? UHT's response was the institutional equivalent of a shrug. No press release, no strategic review, no panicked board meeting. Haven would quietly disband in January 2021, having accomplished essentially nothing, a $3 billion lesson in how deeply entrenched and complex the American healthcare system really is. UHT's non-reaction looked prescient in retrospect.

The growth problem, however, was real and getting harder to ignore. Through the 2010s, UHT's invested assets hovered in the $700 to $900 million range. Revenue grew from roughly $54 million in 2012, following a significant jump from acquisitions that doubled the base, to about $77 million by 2019. That was respectable growth in percentage terms but trivial in absolute dollars compared to the multi-billion-dollar portfolios assembled by peers. UHS was not spinning off many buildings, and third-party acquisition opportunities were limited by UHT's small size and higher cost of capital. The company could not compete with Welltower or Ventas on price or speed when bidding on healthcare properties. The stock traded primarily as a dividend yield play, offering a reliable income stream to investors who valued predictability over capital appreciation and who were comfortable with the related-party governance structure. The investor base self-selected accordingly: income-focused individuals, small institutions, and those who understood and accepted the captive structure. By the end of the decade, UHT had survived the ACA transformation, the senior housing bust, and the brief tech-disruption panic without changing anything material about its strategy. Whether that constituted strategic wisdom or strategic paralysis depended entirely on what you expected the company to be.

COVID-19: The Ultimate Healthcare Stress Test (2020-2021)

When COVID-19 locked down the United States in March 2020, healthcare REITs faced questions that were genuinely existential. Elective procedures, the profit engine of most hospitals, were cancelled overnight. Patient volumes cratered. Senior housing communities became ground zero for the virus, with devastating mortality rates among elderly residents and occupancy rates plummeting from the high 80s to the low 70s as families pulled loved ones out and new admissions stopped. Medical office buildings emptied as physician practices shut down or pivoted to telehealth. The entire premise of healthcare real estate, that people need physical buildings for medical care, was under siege.

The pandemic's differential impact across property types was stark. Senior housing was hardest hit, both operationally and reputationally. Skilled nursing facilities received critical support from the CARES Act's Provider Relief Fund but faced massive staffing challenges and cost surges. Medical office buildings experienced short-term disruption from elective shutdowns but recovered relatively quickly as outpatient visits resumed. Hospitals, particularly those with diversified service lines and government payor support, proved resilient. Sabra Healthcare was the first healthcare REIT to cut its dividend, reducing it by 33 percent on March 25, 2020. Welltower, New Senior Investment Group, and Diversified Healthcare Trust followed with their own cuts. The sector was in crisis.

UHT's portfolio, heavily weighted toward hospitals and behavioral health facilities leased to UHS, was positioned for relative resilience. UHS was a large, diversified hospital operator with the financial mass to weather the storm. While UHS's acute care admissions declined 14.4 percent in the second quarter of 2020 and revenue dipped modestly, the company received $417 million in CARES Act provider relief funds and over $1 billion in total government stimulus. UHS posted $944 million in annual profit for 2020, actually a 15.8 percent increase over 2019, largely supported by federal relief. As UHT's dominant tenant, UHS's survival was never in serious doubt.

Rent collection at UHT was near-perfect. Tenants representing approximately 99 percent of occupied square footage paid their rent through December 31, 2020. UHT's revenue grew modestly from $77.2 million in 2019 to $78.0 million in 2020. The dividend streak continued unbroken. While competitors were slashing payouts and scrambling to shore up balance sheets, UHT's boring, captive structure once again proved its value. The guaranteed leases with UHS, the conservative leverage, and the defensive nature of healthcare demand combined to produce what was, for UHT, a non-event.

The behavioral health dimension added an unexpected tailwind. The pandemic triggered a mental health crisis of historic proportions. Anxiety, depression, substance abuse, and suicide rates surged. UHS, as the nation's largest behavioral health operator with over 340 inpatient facilities, saw rising demand for its services. Behavioral health was one of the few healthcare segments where the pandemic actually increased utilization rather than suppressing it. For UHT, which owned behavioral health properties leased to UHS, this demand surge reinforced the value of its portfolio composition.

The telehealth explosion initially spooked healthcare real estate investors. If patients could see doctors via video, would they still need medical office buildings? The answer, it turned out, was overwhelmingly yes. Telehealth became a complement to in-person care, not a substitute. Complex examinations, procedures, diagnostics, and behavioral health interventions still required physical spaces. Medical office buildings began incorporating telehealth-ready rooms alongside traditional examination spaces, evolving to accommodate both modalities. The feared disintermediation of physical healthcare real estate never materialized.

December 2021 brought UHT's most significant transaction in years: a portfolio reshuffling with UHS. UHS's subsidiary purchased UHT's Inland Valley Campus in California for $79.6 million, while UHT acquired Aiken Regional Medical Center in South Carolina for $57.7 million and Canyon Creek Behavioral Health in Texas for $26.0 million. The net effect was roughly neutral in dollar terms but shifted UHT's portfolio from an acute care campus in high-cost California to a diversified acute care and behavioral health presence in South Carolina and Texas. It was classic UHT: a transaction with its parent company, at independently determined fair values, that reshuffled assets without dramatically changing the portfolio's character or scale. The market's broader reaction to healthcare REITs post-COVID was one of cautious revaluation. The sector recovered from its pandemic lows but remained discounted relative to pre-COVID valuations, weighed down by persistent senior housing headwinds, rising labor costs, and the shadow of what the next crisis might bring.

Recent Era: Inflation, Interest Rates, and Strategic Stasis (2021-Present)

The Federal Reserve's rate-hiking campaign, which began in March 2022 and delivered over 500 basis points of tightening at the fastest pace since the early 1980s, hit the REIT sector like a sledgehammer. The mechanics are straightforward but punishing: REITs are leveraged entities that borrow money to buy real estate and distribute most of their income as dividends. When interest rates rise, their cost of borrowing increases, their dividend yields become less attractive relative to risk-free Treasury bonds, and the present value of their future cash flows declines. Valuation compression is mechanical and often severe.

UHT was particularly vulnerable to rising rates because of its capital structure. The company's primary financing vehicle was a revolving credit facility, the kind of variable-rate debt that reprices instantly when the Fed moves. With $348.9 million outstanding on a $425 million facility and only $85 million hedged through an interest rate swap at 3.27 percent, UHT was substantially exposed to every rate increase. Interest expense climbed meaningfully: the impact was roughly $1.2 million in reduced net income in late 2023 compared to the prior year, with further pressure in 2024. FFO per share, the REIT-specific metric that strips out non-cash items, declined from $3.54 in 2022 to $3.23 in 2023 before recovering to $3.46 in 2024 and holding at $3.44 in 2025.

The stock price told the story more vividly. From its all-time high of $92.72 in February 2020, UHT declined steadily to the low $40s by early 2026, a drop of roughly 54 percent. The dividend yield, which moves inversely to the stock price, spiked above 7 percent. In normal times, a 7 percent yield on a REIT with 42 years of consecutive dividend growth would attract income investors like moths to a flame. In an environment where risk-free Treasury bills yielded over 5 percent, UHT's yield needed to be that high just to compensate for the equity risk, illiquidity, and governance concerns that came with the stock.

The current portfolio tells us what UHT actually is in 2026. The trust owns approximately 77 investments in 21 states, dominated by about 61 medical office buildings, with six hospital and behavioral health facilities, four free-standing emergency departments, four preschool and childcare centers, and a smattering of other healthcare-related properties. Medical office buildings have become the majority of the portfolio by count, though the hospital and behavioral health facilities contribute disproportionately to revenue due to their larger scale and higher rents. The geographic footprint is entirely domestic, spread across the Sun Belt and Eastern Seaboard.

The UHS relationship in 2026 remains the defining feature of UHT's existence. UHS subsidiaries directly generate about 24 percent of UHT's consolidated revenue through hospital leases, and the broader UHS-related tenancy, including MOB and FED leases to UHS affiliates, accounts for roughly 40 percent of the total. All six hospital facilities are leased to UHS subsidiaries under triple-net leases that are unconditionally guaranteed by UHS and cross-defaulted with one another. The advisory agreement with UHS of Delaware, paying 0.70 percent of invested assets, continues to be renewed annually by independent trustees. Third-party tenant diversification has progressed slowly: the 60-plus medical office buildings have brought in non-UHS tenants, but the diversification is measured rather than transformative.

Recent transactions have been modest. A $7.6 million acquisition of the McAllen Doctors' Center medical office building in 2023. A ground lease in October 2025 for Palm Beach Gardens Medical Plaza I, an estimated $34 million, 80,000-square-foot medical office building on the campus of the Alan B. Miller Medical Center, with construction beginning in February 2026. These are small deals by REIT industry standards, reflecting UHT's limited capital and selective approach. In September 2024, UHT refinanced its credit facility, extending the maturity to September 2028 with two six-month extension options. The $85 million interest rate swap, also extending through September 2028, provided partial hedging against continued rate volatility.

Management has been remarkably stable. Alan Miller, now 88, remains Chairman, President, and CEO. Charles Boyle, the CFO since 2003, and Cheryl Ramagano, who has been with the trust since the early 1990s, continue in senior vice president roles. New additions include Karla Peterson as VP of Acquisitions and Development since 2022 and Jamie Krahne as VP of Asset Management since 2025. The average management tenure of 28 years reflects continuity that borders on institutional inertia.

The fundamental question for investors is what UHT's purpose is in 2026. Is it a capital recycling vehicle for UHS? Still yes, but less active than in earlier decades. Is it an independent growth vehicle? Barely, with revenue of $99 million on invested assets of roughly $783 million and minimal acquisition activity. Is it a dividend income investment? Clearly, and this is the lens through which most shareholders view the stock. The 42-year dividend growth streak, the 7 percent yield, and the defensive healthcare portfolio make UHT a specific kind of holding for a specific kind of investor. It is not trying to be anything else.

The Business Model Deep Dive

The captive REIT structure is central to understanding UHT, so it is worth unpacking in detail. In the REIT universe, most publicly traded REITs are internally managed: they have their own employees, their own executive teams, and their own strategic autonomy. UHT is externally managed by UHS of Delaware, a wholly-owned subsidiary of its largest tenant. This means UHT literally has zero salaried employees. Every officer, every analyst, every person who makes investment decisions on UHT's behalf is on UHS's payroll. The advisory fee of 0.70 percent of average invested real estate assets, roughly $5.5 million in 2024, is the compensation UHS receives for providing these services.

This structure has direct parallels in the gaming REIT world. Gaming and Leisure Properties, or GLPI, was created in 2013 as a spin-off from Penn National Gaming. VICI Properties emerged in 2017 from Caesars Entertainment's bankruptcy. Both started as captive REITs with revenue dominated by their former parents. But here is the critical distinction: GLPI and VICI have spent the years since their formation aggressively diversifying their tenant bases, acquiring properties leased to third-party operators, and building independent platforms. After nearly four decades, UHT has not made this transition. The UHS relationship remains as central in 2026 as it was in 1986. This persistence is either a testament to the strength of the relationship or evidence of structural inability to grow beyond it.

Healthcare real estate fundamentals explain why UHT's property types present different risk and return profiles. Hospital properties are the most challenging assets in healthcare real estate. They are purpose-built, enormously expensive to construct, and nearly impossible to re-tenant. If a hospital operator leaves, the landlord is stuck with a specialized building that has limited alternative uses. This is why the UHS guarantee on UHT's hospital leases is so valuable: it essentially eliminates re-tenanting risk for UHT's most specialized assets. Behavioral health facilities share some of these characteristics but benefit from a powerful demand tailwind. The post-pandemic mental health crisis has driven sustained increases in behavioral health utilization, and UHS, as the nation's largest behavioral health operator with over 340 inpatient facilities, is the prime beneficiary. Medical office buildings are the safest play in healthcare real estate. They can accommodate multiple tenants, from individual physician practices to diagnostic labs to outpatient surgery centers. Vacancy rates for MOBs nationally stand at about 7.5 percent, far below the roughly 14 percent vacancy rate for traditional office buildings, reflecting healthcare's inelastic demand and the ongoing shift from inpatient to outpatient care.

Lease structures matter enormously for understanding the risk distribution. UHT's hospital leases with UHS are triple-net, meaning the tenant pays base rent plus property taxes, insurance, and all operating expenses. The landlord's responsibility is essentially limited to owning the building. Initial lease terms run 13 to 15 years with up to six additional five-year renewal terms, and certain leases, like the McAllen Medical Center lease, include bonus rent based on quarterly revenue comparisons to a base year. Medical office building leases are typically modified gross leases, where the tenant pays base rent covering a base year for taxes, insurance, and maintenance, with increases above the base year passed through proportionally. This is the standard structure in multi-tenant MOBs where multiple physician practices share a building.

UHT's capital allocation philosophy can be described in one word: conservative. The trust takes a selective approach to acquisitions, doing only a handful of deals per year, often with its parent company. Development activity is virtually nonexistent, with the Palm Beach Gardens Medical Plaza being a rare exception. The dividend payout ratio consistently runs at 85 to 90 percent of FFO, leaving minimal retained earnings for investment. This high payout ratio is a feature for income investors but leaves little margin for error if FFO declines.

The financial profile of UHT reveals a company in operational steady state. Revenue has grown from roughly $54 million in 2012 to about $99 million in 2025, a 13-year compound annual growth rate of less than 5 percent. FFO per share has fluctuated in a narrow band, from $3.20 in 2019 to a peak of $3.69 in 2021 before settling at $3.44 in 2025. The dividend has grown every year for 42 consecutive years, but the growth increments are tiny: about $0.04 per year, roughly a 1.5 percent annual increase. At the current stock price around $42, the trailing P/FFO ratio is approximately 12 times, a meaningful discount to larger healthcare REIT peers that trade at 15 to 20 times FFO or higher. The discount reflects the governance concerns, small size, limited growth, and liquidity constraints that define UHT's investment case.

Leverage deserves special attention because it has become a growing concern. UHT's debt-to-equity ratio stands at roughly 2.0 to 2.1 times, well above the REIT industry median of about 0.8 times. Over the past 13 years, this ratio has ranged from a low of 1.2 times to its current elevated level. The entire debt structure consists of the $425 million revolving credit facility, of which $348.9 million was drawn at the end of 2024, with only $76.1 million of available capacity. The September 2024 refinancing extended the maturity to 2028, and the $85 million interest rate swap provides partial rate protection. But the concentration of all debt in a single variable-rate facility makes UHT unusually sensitive to interest rate movements and refinancing risk compared to larger REITs with diversified debt stacks of fixed-rate bonds, term loans, and revolving facilities.

Strategic Frameworks: Porter's Five Forces and Hamilton's Seven Powers

Porter's Five Forces

Competitive rivalry in the healthcare REIT sector is moderate but heavily segmented. The major players, Welltower at $96 billion in market cap, Ventas at $27 billion, Healthpeak at $14.4 billion, compete fiercely for acquisition opportunities, tenant relationships, and investor capital. But UHT does not really compete with them. It is a captive vehicle serving UHS, operating in a category of one. Market share is irrelevant when growth is not the primary objective. When UHT does pursue third-party acquisitions, it often loses to larger, more aggressive buyers who can move faster, bid higher, and offer more attractive financing terms. The competitive dynamic is less "rivalry" and more "occasionally showing up to an auction and losing."

The threat of new entrants to the healthcare REIT space is low to moderate. The REIT structure itself is accessible, there is no patent or secret recipe, but building a meaningful healthcare real estate platform requires specialized expertise, institutional relationships, and access to capital at competitive rates. New entrants from private equity or healthcare systems creating their own REITs are rare but possible. UHT's moat, to the extent it has one, is not barriers to entry but the exclusive UHS relationship that no new entrant can replicate.

Bargaining power of suppliers, the property sellers that UHT buys from, is fragmented and market-dependent. In hot real estate markets, sellers command premium pricing. In downturns, buyers have leverage. UHT's small size limits its bargaining power relative to larger REITs that can move quickly on portfolios and offer certainty of close. Construction costs and interest rates further constrain development feasibility for small players.

Bargaining power of buyers, meaning tenants, is moderate to high in UHT's specific case because of the UHS concentration. UHS controls about 40 percent of UHT's revenue and is simultaneously UHT's advisor, its largest tenant, and the employer of all its officers. This is not a normal landlord-tenant relationship. While long-term leases with built-in escalators reduce tenant leverage once signed, the renewal and renegotiation dynamics are colored by the related-party relationship. Third-party tenants have standard bargaining power: they can negotiate terms, shop alternative locations, and make normal market-based decisions.

The threat of substitutes is moderate and evolving. Healthcare delivery is shifting toward outpatient settings, home health, and telehealth, which could theoretically reduce demand for traditional inpatient facilities. However, acute care hospitals and behavioral health facilities are harder to substitute than physician offices or routine care. Nobody does inpatient psychiatric care from their living room. Senior housing, from which UHT has minimal exposure, faces the most significant substitution threat from aging-in-place and home care alternatives. Overall, healthcare real estate demand is durable but the mix is shifting, and UHT's portfolio is positioned somewhat defensively against the most disruptive substitution trends.

The Porter's conclusion is that UHT operates in a structurally attractive industry with a unique captive position that insulates it from competitive forces but also walls it off from growth opportunities. The primary threat is not competitive intensity but strategic irrelevance, the risk that UHT becomes a permanent dividend-paying entity with no path to value creation beyond its yield.

Hamilton's Seven Powers

The Seven Powers framework, developed by Hamilton Helmer, asks a more pointed question than Porter: what gives a company durable competitive advantage that produces superior returns? Applied to UHT, the results are instructive for how sparse they are.

Scale economies do not exist at UHT. The trust manages roughly $783 million in invested assets, a fraction of what competitors deploy. Welltower manages tens of billions. There are no meaningful cost advantages from UHT's small scale. In fact, the opposite is true: its higher cost of capital relative to larger REITs with investment-grade ratings and diversified debt stacks is a scale disadvantage. General and administrative expenses as a percentage of revenue are higher for small REITs, and the advisory fee paid to UHS is an additional cost layer that internally managed REITs do not bear.

Network economies are simply inapplicable. REITs do not exhibit network effects. UHT does not become more valuable to tenants because it owns more properties. There are no interconnected tenant networks or data advantages that compound with scale.

Counter-positioning is absent. UHT is not pursuing a disruptive business model that larger competitors cannot replicate without cannibalizing their existing businesses. If anything, UHT's model is a subset of what larger REITs already do. There is no structural reason Welltower or Ventas could not replicate UHT's approach, but they have no incentive to do so at UHT's scale.

Switching costs are moderate for UHT's existing tenants but not unique to UHT. Healthcare operators face significant costs to relocate: licensing requirements, certificate-of-need laws, patient disruption, and the sheer expense of building or renovating healthcare facilities. Once a hospital is built and operational at a particular location, the tenant is effectively locked in. But this dynamic benefits all healthcare REITs, not just UHT. And UHS's switching costs are lower than those of arm's-length tenants because UHS, as a related party with intimate knowledge of UHT's financial position and strategic constraints, could theoretically refinance its real estate needs elsewhere if it chose to.

Branding provides no power. Institutional investors know UHT exists, but the company has no brand cachet that commands premium rents or attracts tenants. Healthcare operators choose landlords based on location, terms, and relationships, not brand recognition. There is no pricing power from the UHT name.

Cornered resource is UHT's single, genuine source of strategic power, and it is the UHS relationship itself. No other REIT has automatic access to UHS's real estate pipeline. UHS is a $17 billion revenue healthcare operator with over 420 facilities. When UHS decides to recycle capital through a sale-leaseback, UHT has a privileged, captive position as the buyer. This is a unique, defensible asset that provides stability, downside protection, and a built-in tenant with strong credit. However, it is also a constraint: UHT's growth is limited by UHS's real estate strategy, and the cornered resource comes with governance complexities that discount UHT's valuation. It is a durable advantage but a non-scaling one.

Process power is absent. UHT has no unique operational processes, proprietary underwriting methodologies, or embedded efficiencies that competitors cannot replicate. Property management is largely outsourced. Investment decisions follow standard REIT practices. There is no Toyota Production System equivalent hiding inside a $589 million healthcare REIT.

The Seven Powers verdict is stark: UHT possesses a single power, the cornered resource of its UHS relationship, which provides stability and downside protection but does not drive growth or expanding returns. The company is durable but strategically limited. In Helmer's framework, one power is enough to survive but not enough to compound value at rates that attract growth-oriented capital.

The synthesis of both frameworks reveals why UHT has existed for nearly 40 years without becoming a major player. It is not built to win competitively. It is built to serve UHS and provide stable income to shareholders. Porter's Five Forces show a company insulated from competitive threats but also from growth catalysts. Helmer's Seven Powers identify a single durable advantage that functions more like an anchor than a sail. The investment thesis is about yield, stability, and survivability, not transformation or disruption. For investors who seek those qualities, UHT delivers them with remarkable consistency. For everyone else, the company is a curious relic of a specific strategic logic that the market has largely moved past.

Bull vs. Bear Case and Investment Perspective

The Bull Case

Start with the dividend. Forty-two consecutive years of growth, through recessions, pandemics, interest rate spikes, and healthcare transformation. The current yield exceeds 7 percent, which in an era of expected rate normalization, looks increasingly attractive relative to declining Treasury yields. If the Federal Reserve follows through on rate cuts, UHT's stock price should benefit from the mechanical revaluation that lifts all REIT boats as risk-free rates decline.

Healthcare real estate fundamentals are sound and getting stronger. The United States is aging rapidly, with the 80-plus population growing at an accelerating pace. Healthcare spending marches toward $2 trillion. Medical office buildings nationally are running at 92.5 percent occupancy, with demand exceeding supply for 12 consecutive quarters. Construction completions for MOBs are declining to their lowest levels in a decade, tightening supply further. UHT's 61 medical office buildings sit squarely in the path of these favorable secular trends.

The UHS backstop provides a floor under UHT's value. UHS generates $17.4 billion in revenue and $1.5 billion in net income. It is not going to default on leases that represent a rounding error on its income statement. The unconditional guarantee and cross-default provisions on UHT's hospital leases make tenant credit risk essentially negligible for 40 percent of the portfolio. In a sector where Medical Properties Trust nearly imploded because its largest tenant, Steward Health Care, filed for bankruptcy, UHT's tenant quality stands out.

Behavioral health demand continues to surge. Post-pandemic awareness of mental health issues, expanded insurance coverage for behavioral health services, and reduced societal stigma are driving sustained utilization growth. UHS, as the nation's largest behavioral health operator, is the primary beneficiary, and UHT's behavioral health properties participate in that tailwind through stable, guaranteed leases.

The valuation argument is straightforward. At roughly 12 times FFO, UHT trades at a meaningful discount to healthcare REIT peers. If the market re-rates the stock toward even a modest 14 to 15 times multiple, the upside is substantial relative to the dividend income collected while waiting. The company has no complex structures, no hidden risks, and no dramatic strategic pivots to worry about. It is boring, predictable, and priced for minimal expectations.

The Bear Case

The growth problem is not just a temporary condition. It is structural. Revenue has grown at less than 5 percent annually for over a decade, and there is no visible catalyst for acceleration. UHT's captive structure limits its acquisition pipeline to whatever UHS chooses to sell, and UHS has not been an active seller in recent years. Third-party acquisition opportunities are constrained by UHT's small size and higher cost of capital. The company cannot compete with Welltower, Ventas, or even mid-size healthcare REITs on acquisitions. Without growth, the total return proposition depends entirely on the dividend yield, which must compensate shareholders for all the risks of equity ownership.

The leverage profile is concerning. A debt-to-equity ratio above 2.0 times places UHT in the bottom decile of the REIT industry. The concentration of all debt in a single revolving credit facility, with only $85 million of the $349 million balance hedged, creates significant interest rate and refinancing risk. If rates remain elevated or rise further, UHT's FFO compression continues. If credit markets tighten when the facility matures in 2028, refinancing could be expensive or difficult.

Governance concerns are not academic. Alan Miller chairs both UHT and UHS, all UHT officers are UHS employees, and the advisory fee creates an inherent misalignment between the advisor's interest in growing the asset base (which increases fees) and shareholders' interest in disciplined capital allocation. While independent trustees provide oversight, the ISS Governance QualityScore of 5 out of 10, with particularly weak audit and board scores, suggests that governance standards are below institutional investor expectations.

Healthcare disruption, while overhyped in the short term, is real in the long term. Fifty-nine medical procedures were approved for migration from inpatient to outpatient settings between 2018 and 2023. CMS continues phasing out the Inpatient Only list, shifting revenue away from hospitals. If outpatient migration accelerates, UHT's hospital properties, which generate disproportionate revenue, could face utilization pressure even with the UHS guarantee protecting against rent default.

Liquidity is a practical concern. A $589 million market cap REIT with approximately 13.8 million shares outstanding trades with limited volume and wide bid-ask spreads. Institutional ownership is thin. Getting into or out of a meaningful position is difficult without moving the stock price. This illiquidity premium should be, and apparently is, priced into the stock's discount to peers.

The existential risk is rarely discussed but worth articulating. UHT's purpose depends on UHS's willingness to continue the relationship. If UHS decided to bring its real estate in-house, sell properties to third-party REITs, or restructure the advisory agreement, UHT would lose its single competitive advantage. With Alan Miller at 88, the succession question is not hypothetical. Marc Miller, who became UHS CEO in January 2021, sits on UHT's board, but his strategic priorities for UHS may not include maintaining a $589 million side hustle REIT. The new Palm Beach Gardens Medical Plaza development suggests the relationship remains active, but the transaction volume has been modest in recent years.

Key Metrics to Track

For investors monitoring UHT's ongoing performance, three metrics matter most.

First, the percentage of revenue from UHS versus third parties. This ratio tells you whether UHT is diversifying or remaining captive. A declining UHS share signals strategic progress toward independence. A rising or stable share confirms the captive structure's persistence. Currently at roughly 40 percent UHS-related revenue, this metric has improved slowly over the decades but remains the defining characteristic of the business.

Second, FFO per share and dividend coverage. With a payout ratio running at 85 to 90 percent of FFO, there is little margin for error. If FFO per share declines due to rising interest expense, tenant issues, or portfolio stress, the dividend becomes vulnerable. The 42-year growth streak is UHT's most valuable asset, and any threat to it would trigger a significant revaluation of the stock. Watching FFO per share trends and the resulting coverage ratio is essential.

Third, debt-to-assets ratio and interest coverage. Given the elevated leverage and variable-rate debt concentration, these balance sheet metrics are the early warning system for financial stress. The September 2028 maturity on the revolving facility is the next major inflection point. How rates evolve between now and then, and what terms UHT secures on refinancing, will meaningfully impact the investment case.

What Does the Future Hold?

Four scenarios span the range of plausible outcomes for UHT over the next decade.

The first and most likely scenario is status quo forever. UHT continues as UHS's real estate side hustle, making occasional small acquisitions, collecting rent, and paying its quarterly dividend. Revenue grows at low single digits, the stock trades on yield, and the company survives another decade in quiet obscurity. This is the base case because it requires no strategic decisions, no management changes, and no external catalysts. It is the outcome that 40 years of history predict.

The second scenario involves a strategic pivot toward aggressive third-party growth. New management, perhaps following Alan Miller's eventual departure, pursues an independent growth strategy, diversifying away from UHS dependence through third-party acquisitions and development. The challenges here are significant: UHT's small size, higher cost of capital, and lack of independent infrastructure make competing with established healthcare REITs extremely difficult. Growth would require equity issuance, which would dilute existing shareholders, or increased leverage, which is already elevated. And any move toward independence risks friction with UHS, the company that literally manages UHT's affairs and employs all its officers.

The third scenario is acquisition or privatization. UHS could take UHT private, simplifying the corporate structure and eliminating the governance complexities of a public captive REIT. Another healthcare REIT could acquire UHT for its portfolio, particularly the 61 medical office buildings that are well-positioned for the outpatient care megatrend. Private equity could pursue a roll-up of small healthcare REITs. Any of these would likely require a premium to the current stock price, representing an attractive exit for long-suffering shareholders but ending the company's 40-year run as a public entity.

The fourth scenario is sector disruption. If healthcare delivery transforms rapidly enough, with outpatient care, home health, telehealth, and AI-driven diagnostics reducing the need for physical facilities, UHT's portfolio could become stranded assets. This is the tail risk scenario, unlikely in the near term given the inertia of healthcare infrastructure but worth acknowledging over a 10 to 20-year horizon. A dividend cut in this scenario would be devastating, ending the 42-year streak and triggering a severe stock price decline.

The bigger questions transcend UHT's specific situation. What role do small, captive REITs play in modern capital markets where institutional investors demand scale, liquidity, and independent governance? Is stability and survival enough in an era where the market rewards disruption and punishes stasis? Can boring compound into anything meaningful, or does it just compound into more boring?

UHT offers a partial answer. Forty years of survival, 42 years of dividend growth, and a stock that has returned meaningful income to patient shareholders, even as its price has halved from its peak. Alan Miller built two companies with radically different ambitions: UHS to grow and dominate healthcare operations, UHT to sit quietly and collect rent. Both have endured. Both have served their intended purposes. The contrast between them, one a Fortune 300 juggernaut generating $17 billion in revenue, the other a $589 million REIT that most investors have never heard of, is itself a lesson in what strategy means when you strip away the growth-at-all-costs rhetoric that dominates modern markets.

Sometimes the most interesting story is about something aggressively uninteresting. UHT is the REIT equivalent of a money market fund: unloved, unglamorous, and quietly delivering on its single, modest promise year after year. For investors who know what they own and why, that might be exactly enough.

Further Reading and Resources

Essential References

Universal Health Realty Income Trust Annual Reports and 10-K filings from 2015 through 2025 provide the most detailed portfolio, financial, and governance data, available through the SEC's EDGAR system and UHT's investor relations website.

Universal Health Services Annual Reports offer critical context on the parent company's strategy, financial health, and real estate decisions that directly affect UHT's pipeline and tenant quality.

NAREIT Healthcare REIT Reports provide industry-level data, trends, and benchmarking that contextualize UHT's performance relative to the broader healthcare REIT sector.

Green Street Advisors Healthcare REIT Research offers institutional-grade analysis including NAV estimates, cap rate trends, and sector-specific insights that are invaluable for valuation work.

CBRE Healthcare Real Estate Reports track market-level supply and demand dynamics, occupancy trends, and rental rate movements across healthcare property types.

Books for Context

Clayton Christensen's "The Innovator's Prescription" provides the intellectual framework for understanding how healthcare delivery disruption affects real estate demand, the very forces that UHT's portfolio must navigate.

William Thorndike's "The Outsiders" examines unconventional approaches to capital allocation by CEOs who generated exceptional returns. The contrast with UHT's approach, which prioritizes stability and dividend consistency over return maximization, is illuminating.

Industry and Academic Resources

The Journal of Real Estate Literature has published research on the economics of healthcare real estate that frames the supply, demand, and valuation dynamics of UHT's property types.

Academic work on related-party transactions in REITs, published in Real Estate Economics, addresses the governance concerns that are central to UHT's investment case.

CMS data on healthcare facility utilization trends provides the demand-side fundamentals that underpin the long-term viability of UHT's portfolio, particularly the migration from inpatient to outpatient care settings.

Federal Reserve reports on interest rates and REIT valuation offer the macroeconomic framework for understanding UHT's stock price movements and cost-of-capital dynamics.

Audio and Media

Alan Miller's rare interviews, primarily in healthcare industry publications and conferences, offer insight into the founding philosophy behind both UHS and UHT and the strategic rationale for maintaining the captive REIT structure for nearly four decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube