Udemy Inc.: The Democratization of Learning

I. Introduction and Episode Roadmap

Picture this: a platform hosting over 250,000 courses, serving 82 million learners across 180 countries, taught by 85,000 instructors in 75 languages. No admissions committee. No prerequisites. No ivy-covered gates. Just a search bar and a credit card. That is Udemy, the world's largest open course marketplace, and its story is one of the most fascinating case studies in what happens when Silicon Valley idealism collides with marketplace economics, Wall Street expectations, and the relentless march of artificial intelligence.

The central question of this deep dive is deceptively simple: How did a Turkish immigrant who grew up in a village with virtually no access to quality education build the world's largest teaching marketplace, and why did taking it public nearly destroy everything? The answer takes us through the golden age of MOOCs, a pricing crisis that almost tore the platform apart, an enterprise pivot that saved the business, a pandemic boom that proved fleeting, a stock collapse that humbled everyone involved, and now, a merger that may determine whether the company survives the AI age at all.

Udemy is not just an education story. It is a masterclass in two-sided marketplace dynamics, the tension between mission and margin, and the brutal reality of what happens when a hybrid business model meets public market investors who demand clean narratives. Along the way, we will explore why courses listed at two hundred dollars routinely sold for ten, why the enterprise business became the only thing keeping the lights on, and whether human-taught courses have a future when ChatGPT can tutor you for free.

Consider the arc: a four-billion-dollar IPO valuation in October 2021, an eighty-three percent stock decline by early 2026, and a pending merger with its closest rival that values the combined entity at a fraction of what the market once thought Udemy alone was worth. It is a humbling trajectory, but also one filled with genuine innovation, hard-won strategic pivots, and lessons that every founder, investor, and builder in the platform economy should study.

This is the story of Udemy, from a one-room schoolhouse in Turkey to a pending two-and-a-half-billion-dollar merger with Coursera, and every painful, exhilarating, and instructive chapter in between.

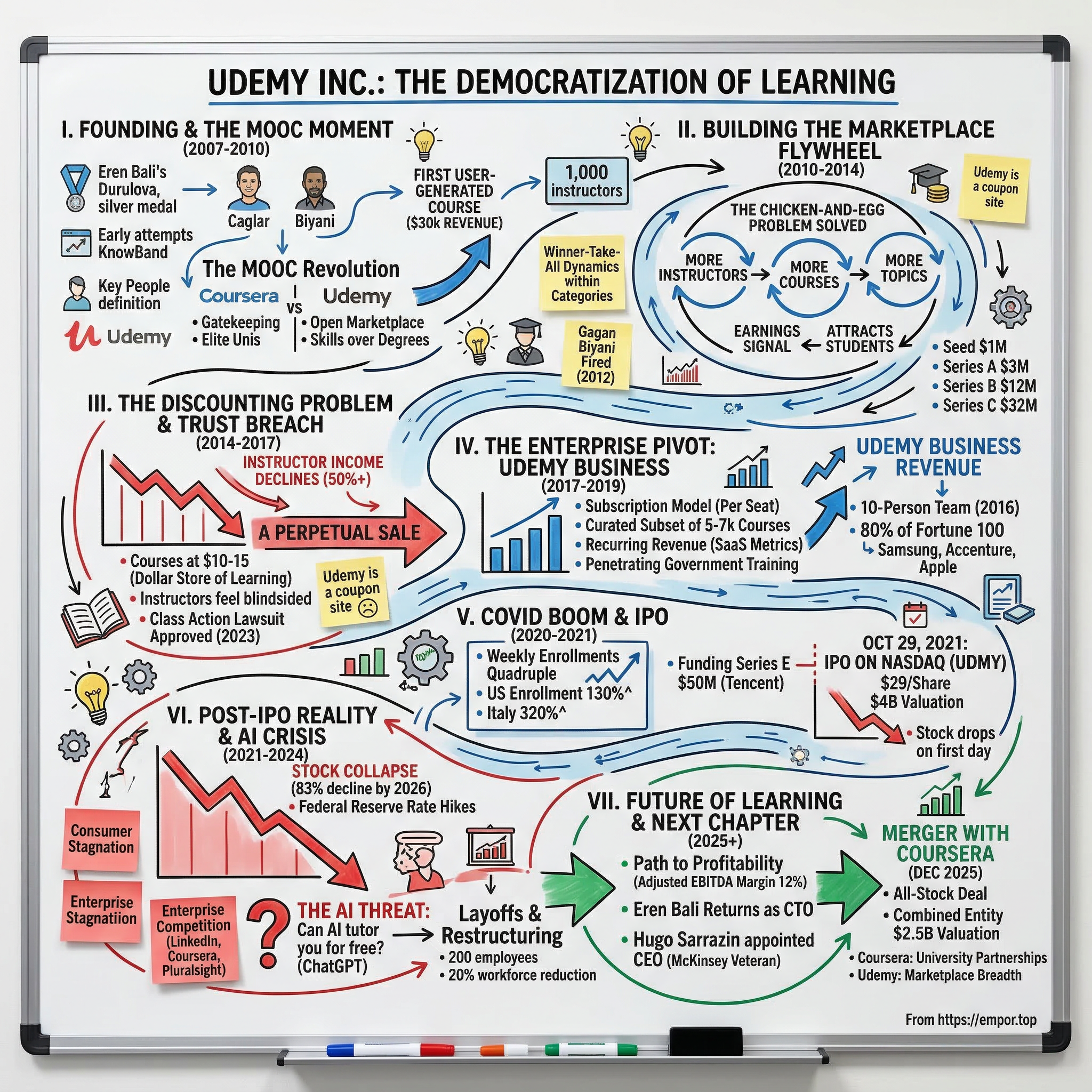

II. Founding Context and The MOOC Moment (2007-2010)

Eren Bali was born in 1984 in Durulova, a tiny apricot-farming village in Malatya province, eastern Turkey. His mother taught first through fifth grades in a single-room schoolhouse, which was, by local standards, an extraordinary educational resource. There were no bookstores, no libraries, no tutoring centers. The internet, when it eventually arrived, was Bali's window to the world. He taught himself programming and mathematics through whatever online resources he could find, and the experience left an indelible mark: he understood, viscerally, that knowledge existed in abundance, but access and structure did not.

That self-directed learning paid off spectacularly. In 2001, Bali won a silver medal at the International Mathematical Olympiad, a feat that propelled him to Middle East Technical University in Ankara, where he graduated in 2005 with a double major in computer engineering and mathematics. But the village never left him. The memory of his mother teaching every subject to every age in one room, the hours spent hunting for scraps of knowledge online, the sheer randomness of whether a kid in rural Turkey could ever learn calculus or coding—these formed the emotional bedrock of what would become Udemy.

In 2007, Bali and his childhood friend Oktay Caglar built a live virtual classroom platform while still in Turkey. It was rudimentary, ambitious, and ahead of its time. In 2008, Bali launched a livestream-based learning product called KnowBand. It went nowhere. Shortly afterward, a Silicon Valley online dating company called SpeedDate recruited Bali as an engineer, giving him his entry visa to the American tech ecosystem. Caglar eventually followed. The two of them knew they wanted to build an education platform, but they needed someone who understood the Silicon Valley growth playbook.

Enter Gagan Biyani, an Indian-American entrepreneur and UC Berkeley graduate who had written for TechCrunch and understood the mechanics of startup marketing and fundraising. Biyani became the third co-founder, bringing go-to-market savvy to Bali's technical vision and Caglar's engineering depth. Together, in early 2010, they formally incorporated Udemy—a portmanteau of "you" and "academy."

The timing was electric. Between 2010 and 2012, the MOOC revolution was reaching fever pitch. Stanford professors Sebastian Thrun and Andrew Ng launched courses that attracted hundreds of thousands of students, spawning Udacity and Coursera respectively. Sal Khan's Khan Academy was becoming a household name. The collective narrative was intoxicating: free online education would democratize knowledge, disrupt universities, and change the world. Venture capital poured in. Magazine covers were printed. The future of learning was here.

But Udemy made a fundamentally different bet. While Coursera partnered with elite universities to offer curated, accredited courses, and Udacity focused on cutting-edge technology skills taught by industry luminaries, Udemy chose the open marketplace model. Anyone could teach. Anyone could learn. The platform would be the plumbing, not the curriculum committee. This was Amazon's third-party marketplace logic applied to education—let a thousand instructors bloom and let the market sort out quality.

The distinction mattered enormously. Coursera's model required signing deals with Stanford, Yale, and the University of London. Udacity needed to recruit top-tier instructors one by one. Udemy just needed to open the doors and let people in. The trade-off was obvious: Udemy would have far more content, far more variety, and far less quality control. It was the philosophical split between gatekeeping and openness, between academic credentialing and practical skills, between polish and scale.

In February 2010, the three founders hit the fundraising trail and were rejected by more than thirty venture capital firms. Nobody believed that user-generated educational content could be good enough, or that instructors would show up in sufficient numbers. Bali and his co-founders bootstrapped development, and in May 2010, Udemy launched. Within months, a thousand instructors had created roughly two thousand courses and nearly ten thousand users had registered. The early traction was modest but real, and it caught the attention of angel investors. A seed round of one million dollars closed in August 2010, led by MHS Capital, with participation from Naval Ravikant and Dave McClure's 500 Startups.

The MOOC bubble would eventually deflate—completion rates for free online courses turned out to hover around five to fifteen percent, and universities proved far more resilient than the disruption narrative suggested. The "disruption of higher education" that venture capitalists and TED speakers had breathlessly predicted turned out to be something far more modest: a supplement to traditional education, not a replacement. But the kernel of Udemy's insight survived: there was massive, underserved demand for practical, affordable skill acquisition outside the formal education system. Not everyone wanted a degree. Many people simply wanted to learn Python, or Excel, or digital marketing, quickly and cheaply. The question was whether an open marketplace could deliver that without drowning in low-quality content, and whether the economics could ever work for instructors, students, and the platform simultaneously.

III. Building the Marketplace Flywheel (2010-2014)

Every two-sided marketplace faces the same existential challenge at birth: the chicken-and-egg problem. Without courses, students will not come. Without students, instructors will not bother creating courses. Udemy's early team solved this with a clever hack that has become startup lore. They created a course themselves—a practical, skill-based offering—that generated thirty thousand dollars in revenue within its first few weeks. This was not about the money. It was proof of concept, a signal flare to potential instructors: there is real demand here, and real money to be made.

That signal worked. The original revenue share model was generous by platform standards: instructors kept seventy percent of revenue on sales driven through Udemy's marketing channels, and even more on sales they drove themselves. For someone with expertise in web development, photography, or Excel—skills that were in enormous demand but underserved by traditional education—Udemy offered a remarkable proposition. Create a course once, upload it, and earn passive income as long as students kept enrolling. No publisher, no university, no gatekeeper.

The early course catalog was a reflection of instructor passion more than market research. Programming and web development dominated, but courses on guitar, yoga, personal finance, Photoshop, and public speaking proliferated. The breadth was the point. Udemy was not trying to be a coding bootcamp or a business school. It was trying to be the everything store for learning, and the open marketplace model meant that supply naturally flowed toward whatever topics had demand.

But openness came with a cost. Quality was wildly inconsistent. A brilliant course on Python programming might sit alongside a rambling, poorly produced lecture on the same topic. Udemy's early approach to curation was minimal—a rating and review system, plus basic content guidelines—and the platform relied heavily on market signals to surface the best courses. This created a winner-take-all dynamic within categories: once a course accumulated enough positive reviews and enrollments, it became nearly impossible for competitors to displace it, regardless of relative quality.

The funding trajectory reflected growing confidence. A three-million-dollar Series A closed in October 2011, led by Lightbank, the fund started by Groupon co-founders Eric Lefkofsky and Brad Keywell. A twelve-million-dollar Series B followed in December 2012, led by Insight Venture Partners—a relationship that would prove transformative for the company over the next decade. And in May 2014, a thirty-two-million-dollar Series C arrived from Norwest Venture Partners, with Insight and MHS Capital participating. The stated goals were broadening content, expanding internationally, and developing new product capabilities.

Behind the scenes, the founding team was fracturing. Gagan Biyani, the business-minded co-founder, was fired from Udemy in 2012—an experience he later discussed publicly, describing it as one of the most painful moments of his career. Biyani went on to advise Lyft on growth, founded and shuttered a food delivery startup called Sprig, and eventually launched Maven, a cohort-based learning platform, in 2020. His departure left Bali and Caglar running a company that was growing fast but still searching for its identity.

By 2013, Udemy crossed one million students—a milestone that validated the flywheel thesis. More instructors meant more courses, which meant more topics covered, which attracted more students, which attracted more instructors. The virtuous cycle was spinning. By the end of 2014, the platform had tens of thousands of courses and was expanding into international markets. Eren Bali stepped down as CEO that year, handing operational leadership to professional management, and would later co-found Carbon Health, a technology-enabled healthcare provider.

The flywheel was working. But underneath the impressive growth numbers, a structural problem was forming that would nearly tear the marketplace apart. The very openness that fueled Udemy's content explosion was about to collide with a pricing dynamic that no one had anticipated, turning the platform into something its founders never intended: the internet's most aggressive coupon site for education.

IV. The Discounting Problem and Marketplace Dynamics (2014-2017)

Imagine browsing Udemy in 2015. You search for a course on JavaScript. The top result shows an original price of one hundred and ninety-nine dollars, but today—lucky you—it is on sale for twelve dollars and ninety-nine cents. That is a ninety-three percent discount. You might feel like you have stumbled onto an incredible deal. But if you waited a week and checked again, the same course would be on sale again. And the week after that. And the week after that. The "original" price was fiction. The sale was permanent. And this dynamic was not limited to one course—it was the entire platform.

If this sounds familiar, it should. Department stores like J.C. Penney and Kohl's built entire business models around the same psychology: inflate the "original" price, then offer a perpetual "sale" that makes the customer feel they are getting a bargain. But when J.C. Penney's CEO Ron Johnson tried to eliminate the fake pricing and move to "everyday low prices" in 2012, sales cratered because customers had been so thoroughly conditioned to buy on discount that fair pricing felt like a rip-off. Udemy would discover the same painful truth.

How did this happen? The answer lies in the intersection of performance marketing incentives, instructor competition, and platform economics. Udemy discovered early that aggressive discounting was extraordinarily effective at driving customer acquisition. A course priced at ten to fifteen dollars had almost no purchase friction—it was an impulse buy, cheaper than lunch. The conversion rates on promotional emails and paid advertisements were dramatically higher at these price points, and the resulting customer acquisition cost was remarkably low.

Instructors, meanwhile, were caught in a prisoner's dilemma. If your competitor's course was perpetually on sale for ten dollars, pricing yours at full price was commercial suicide. So everyone listed high and discounted deep, creating a spiral that trained customers to never, ever pay full price. The platform's promotional machinery—flash sales, limited-time offers, holiday discounts, seasonal promotions—became so relentless that the actual selling price of a typical Udemy course settled into a narrow band between ten and fifteen dollars, regardless of what was listed on the course page.

The backlash was fierce. Instructors who had built their businesses around Udemy watched their per-unit revenue crater. Some reported income declines of fifty percent or more as the discounting intensified. The criticism crystallized into a devastating label: "Udemy is a coupon site." Blog posts, forum threads, and social media rants proliferated. Prominent instructors publicly denounced the platform for devaluing their work. Some left for competitors like Skillshare, or migrated to self-hosted platforms like Teachable and Thinkific, where they could set and control their own prices.

The first major trust breach had actually occurred earlier, in 2013, when Udemy unilaterally slashed the instructor revenue share on platform-driven sales from seventy percent to fifty percent. Many instructors felt blindsided by the change, which was announced without meaningful consultation. This set the tone for a relationship that would remain contentious for years: the platform controlled pricing, promotions, and discovery, while instructors supplied the content and bore the reputational cost when their courses appeared cheap or disposable.

Udemy attempted multiple fixes. In 2016, the company implemented a dramatic pricing policy overhaul that required all courses to be priced between twenty and fifty dollars, effectively banning the extreme gap between fictional list prices and perpetual sale prices. The intent was sound—restore pricing integrity and rebuild trust. The execution was a disaster. Instructors who had built marketing funnels around the high-list-low-sale model saw their strategies destroyed overnight. Instructors who had always charged fair prices were capped at fifty dollars, unable to charge premium rates for premium content. Nobody was happy.

The pricing practices eventually caught up with Udemy legally. A class action lawsuit alleged deceptive pricing—specifically, that Udemy used false reference pricing by advertising fictional original prices and running perpetual sales. In August 2023, a court granted final approval of a four-million-dollar settlement covering purchases made between August 2017 and April 2023.

But here is the counterintuitive insight that the "Udemy is a coupon site" critics missed: the discounting actually worked as a business strategy, even if it was terrible for brand perception and instructor morale. By keeping prices radically low, Udemy achieved massive customer acquisition at minimal cost. The platform crossed ten million students by 2016, and the rate of growth was accelerating. The average customer might only pay ten dollars per course, but the volume was staggering, and the customer acquisition cost was a fraction of what competitors spent.

The real business model was not about selling premium education. It was about selling accessible skill acquisition at scale, powered by a performance marketing engine that thrived on impulse purchases. Think of it less like a university bookstore and more like the dollar store of learning—not prestigious, not always high quality, but serving an enormous market of people who wanted to learn something practical without spending hundreds of dollars or committing months of their time.

The instructor economics reflected this reality in brutal terms. It was a volume game for the vast majority: seventy-five percent of instructors earned less than a thousand dollars per year. Only about one percent earned over fifty thousand dollars. But those at the top—instructors like Rob Percival in web development, who reportedly earned over two million dollars in total—demonstrated that the platform could create extraordinary outcomes for the few who cracked the code of content creation, marketing, and topic selection. The distribution was a textbook power law, and Udemy's marketplace amplified it mercilessly.

For investors thinking about Udemy's consumer business today, this period established the DNA that still defines it: a high-volume, low-price marketplace where customer loyalty is weak, brand perception is mixed, and the economics work only at massive scale. The discounting crisis was not an aberration—it was the natural outcome of Udemy's marketplace design. The company would eventually find a much more attractive business in enterprise, but the consumer segment's identity was forged in these chaotic years and has proven remarkably difficult to reshape.

V. The Enterprise Pivot: Udemy Business (2017-2019)

In 2016, when Yvonne Chen joined Udemy as VP of Marketing for its fledgling corporate training arm, the entire business unit consisted of ten people—product, engineering, sales, and marketing combined. The consumer marketplace was generating the vast majority of revenue, the discounting crisis was raging, and few inside or outside the company would have predicted that this tiny enterprise team would become the engine that kept Udemy alive through the most difficult years ahead.

The strategic logic was clear even then. The consumer marketplace was transactional and volatile, subject to the discounting dynamics that made revenue forecasting more art than science. Corporate training, by contrast, offered something that every SaaS investor loves: recurring revenue. Companies sign annual or multi-year contracts, pay per seat, and renew predictably. The global corporate learning and development market was estimated at over three hundred billion dollars, and most of it was being served by legacy learning management systems that were, to put it charitably, universally despised. Anyone who has suffered through mandatory compliance training on a clunky enterprise LMS knows the pain. Udemy saw an opportunity to bring its vast course catalog—curated down to the best five to seven thousand offerings from a library of over a hundred and fifty thousand—into the corporate environment, replacing soul-crushing compliance modules with engaging, practical skills training.

The product, initially called Udemy for Business and later rebranded to Udemy Business, was a subscription-based service. Companies paid annual per-seat licenses for their employees to access a curated subset of the marketplace catalog. The curation was critical: while the open marketplace contained everything from guitar lessons to quantum physics, the enterprise product was focused on business-relevant skills—technology, leadership, project management, data science, and professional development. A dedicated team evaluated courses for quality, relevance, and production value, creating a premium layer on top of the marketplace's open content.

The sales motion was fundamentally different from the consumer business. Instead of performance marketing and impulse purchases, enterprise deals required a dedicated sales team, multi-month procurement cycles, security reviews, integration with existing HR and LMS systems, and executive buy-in. Udemy had to build this capability from scratch, hiring enterprise sales professionals who understood how to navigate Fortune 500 procurement processes. The average contract value ranged from forty to eighty thousand dollars for large enterprise customers, with the largest deals reaching into the hundreds of thousands or millions.

The traction was remarkable. By the time of the IPO in 2021, Udemy for Business had penetrated eighty percent of Fortune 100 companies. Major clients included Samsung, Accenture, Apple, PayPal, Unilever, Pinterest, Adidas, and General Mills. The enterprise revenue trajectory told a compelling story: in 2020, Udemy Business revenue grew 103 percent year-over-year, propelled by the pandemic-driven surge in remote work and digital upskilling. In 2021, growth remained robust at 81 percent. By 2022, enterprise revenue had reached 314 million dollars—half of total company revenue—with 68 percent year-over-year growth.

Udemy also identified an underserved niche in government training. Udemy Government, serving defense agencies and federal organizations, became a meaningful segment within the enterprise business, leveraging the platform's scale and breadth to provide training that met government procurement requirements. The government sector, with its massive training budgets and mandated upskilling programs, represented a stable, high-retention customer segment that diversified the enterprise revenue base beyond the private sector.

What made the enterprise pivot particularly impressive was the speed of execution. Going from a ten-person team in 2016 to a business that would eventually generate over half a billion dollars in annual recurring revenue required building not just a sales force but an entire operational infrastructure: customer success teams to ensure adoption and renewal, content curation processes to maintain the quality bar, security and compliance capabilities to satisfy enterprise IT requirements, and analytics dashboards that gave L&D leaders visibility into employee learning activity. Each of these capabilities had to be built while the consumer marketplace continued to demand attention and investment.

The enterprise pivot created a strategic tension that would define Udemy's identity crisis for years. The consumer marketplace was the brand—it was what people thought of when they heard "Udemy." But the enterprise business was the growth engine, the margin story, and the path to financial sustainability. Every dollar and engineering hour invested in enterprise capabilities was a dollar and hour not invested in the consumer experience. Every curation decision that removed a course from the enterprise catalog had no effect on the consumer marketplace, but it highlighted the quality gap between what Udemy showed to corporations and what it showed to individual learners.

The competitive landscape was also shifting. LinkedIn Learning, born from Microsoft's twenty-six-billion-dollar acquisition of LinkedIn in 2016, had an insurmountable distribution advantage—access to LinkedIn's professional network of over a billion members. Coursera for Business brought the prestige of university partnerships into the enterprise market. Pluralsight offered deep, specialized technology training with hands-on labs. Skillsoft, the legacy incumbent, still held significant market share among large enterprises. Udemy Business was competing against all of them simultaneously, armed with breadth of content and competitive pricing but lacking the distribution advantage of LinkedIn, the credentialing power of Coursera, or the depth of Pluralsight.

The financial transformation was unmistakable, though. By 2019, enterprise bookings had reached a critical mass that fundamentally changed the revenue mix. The business was transitioning from a transactional consumer marketplace into something that looked much more like a SaaS company, with annual recurring revenue, net dollar retention metrics, and enterprise customer counts that Wall Street could understand and value. This transformation would prove essential when Udemy decided to go public—though it would also create a narrative complexity that public market investors found deeply confusing.

VI. COVID Boom and The IPO Decision (2020-2021)

In March 2020, as offices around the world shuttered and hundreds of millions of workers found themselves suddenly remote, Udemy experienced a demand surge unlike anything in its history. Weekly enrollments more than quadrupled between February and late March. Total enrollments jumped ninety-eight percent during the pandemic period. In the United States, enrollment grew 130 percent. In India, it grew 200 percent. In Italy, where lockdowns were among the earliest and most severe, enrollment surged 320 percent. Spain saw 280 percent growth. The entire world was suddenly learning online, and Udemy's vast catalog of practical, affordable courses was perfectly positioned to capture the wave.

The supply side responded in kind. The course catalog expanded from roughly 130,000 courses in 2019 to 183,000 in 2020—a sixty percent increase in a single year, as newly homebound professionals, academics, and hobbyists flooded the platform with content. Total revenue reached approximately four hundred million dollars, with consumer revenue growing forty-five percent and the enterprise business more than doubling.

The enterprise acceleration was particularly significant. Chief learning officers at large organizations suddenly needed to train entire workforces remotely, and legacy LMS systems were not built for the scale or speed required. Udemy Business became the fastest path to standing up a remote training infrastructure—a pre-built catalog of thousands of courses, accessible from any browser, with analytics dashboards that let HR teams track engagement. Companies that might have taken six months to evaluate and procure a learning platform were making decisions in weeks. The crisis compressed enterprise sales cycles and created a once-in-a-generation tailwind for digital learning adoption.

On the strength of this growth, Udemy raised a fifty-million-dollar Series E in November 2020, led by Tencent, at a pre-money valuation of 3.25 billion dollars. The round was relatively modest given the valuation, suggesting that the company was already eyeing a public offering as its next major capital event. The presence of Tencent—China's technology conglomerate with deep expertise in content platforms—added strategic credibility, even though the investment was primarily financial rather than operational.

By late 2021, the IPO window was wide open. Interest rates were still near zero, growth stocks were trading at extraordinary multiples, and edtech was riding a narrative wave. Coursera had gone public in March 2021, and its stock had initially performed well. Duolingo had listed in July 2021 to an enthusiastic reception. The market appetite for education technology companies appeared insatiable, and Udemy's combination of consumer scale and enterprise growth seemed like a compelling offering.

On October 29, 2021, Udemy went public on the Nasdaq Global Select Market at twenty-nine dollars per share—the top of its expected range—raising approximately 421 million dollars. The implied valuation was roughly four billion dollars. Morgan Stanley, J.P. Morgan, Citigroup, Bank of America Securities, Jefferies, and Truist served as underwriters. It should have been a triumphant moment for a company founded by a Turkish village kid who had been rejected by thirty venture capitalists.

Instead, the stock dropped on its first day of trading, closing at $27.50—a five percent decline that foreshadowed the pain to come. The all-time high closing price of $31.10, reached less than three weeks later on November 18, would stand as the peak that Udemy shareholders would spend years trying to reclaim and never would.

The S-1 filing revealed the fundamental tensions that Wall Street would struggle to reconcile. The company was growing fast but was not profitable. Sales and marketing expenses consumed a disproportionate share of revenue. The consumer business and enterprise business had fundamentally different economics, growth trajectories, and competitive dynamics, but they were reported as a single company. Investors were being asked to value a hybrid marketplace-SaaS business at SaaS multiples, even though the marketplace component dragged down margins and growth predictability.

The narrative problem was acute. Was Udemy a high-growth enterprise SaaS company? The enterprise metrics suggested yes—recurring revenue, strong net retention, expanding customer base. Was it a consumer marketplace? Also yes—tens of millions of users, massive course catalog, global reach. But investors want clean stories, and Udemy's story was anything but clean. The consumer business was built on aggressive discounting, had modest repeat purchase rates, and competed against free alternatives. The enterprise business was genuinely promising but still relatively small and facing formidable competitors. Putting them together created a narrative that was neither fish nor fowl—too complex for growth investors, too unprofitable for value investors, and too confusing for generalists.

The fourth inflection point had arrived. Public market scrutiny would force a strategic clarity that private markets never demanded, and the results would be painful.

VII. Post-IPO Reality and Strategic Crisis (2021-2024)

The chart tells the story with merciless efficiency. From that all-time high of $31.10 in November 2021, Udemy's stock entered a decline that would eventually wipe out more than eighty-five percent of its value. By late 2022, shares were trading below eight dollars. By 2024, the stock had fallen to the four-to-six-dollar range, representing a market capitalization of roughly seven hundred million to one billion dollars—a fraction of the four-billion-dollar IPO valuation. For investors who bought at the IPO price of twenty-nine dollars, the loss was devastating.

What went wrong was not one thing but a convergence of forces. The macro environment shifted violently against growth stocks as the Federal Reserve began raising interest rates in 2022. Edtech broadly fell out of favor as the pandemic-driven demand surge proved temporary—Chegg, 2U, and Coursera all suffered significant stock declines during the same period. The narrative that COVID would permanently accelerate the shift to online learning proved overly optimistic, at least in the near term.

Udemy's specific challenges were more structural. The consumer business stagnated and then contracted. Consumer revenue, which had been the heart of the company since its founding, peaked and began declining—from roughly three hundred and nine million dollars in 2023 to 292 million in 2024, a five percent drop. The discounting dynamics that had fueled consumer growth were now working against the company: customers had been trained to view Udemy courses as low-cost impulse purchases, making it nearly impossible to raise prices or improve unit economics without destroying volume.

Enterprise competition intensified. LinkedIn Learning's integration into the broader Microsoft and LinkedIn ecosystem gave it a distribution advantage that Udemy could not match. Coursera's university partnerships lent it a credentialing prestige that resonated with enterprise buyers concerned about training quality. Pluralsight, taken private by Vista Equity Partners in 2022 for roughly 3.5 billion dollars, could invest aggressively without public market scrutiny. The enterprise market that Udemy had helped pioneer was becoming crowded, and differentiation was increasingly difficult.

Leadership changes reflected the turbulence. Dennis Yang, who had served as CEO since Bali's departure in 2014, was succeeded by Gregg Coccari around 2020. Greg Brown, who had led the enterprise business as its President, was elevated to CEO in 2023 as the company doubled down on its enterprise-first strategy. Brown's appointment signaled a clear message: the enterprise business was the priority, and the consumer marketplace would have to adapt or accept a diminished role.

Strategic decisions under pressure followed a familiar playbook. In February 2023, Udemy laid off approximately two hundred employees—its first major reduction in force—with severance costs of eight to nine million dollars and expected annual savings of thirty to thirty-two million. Headcount fell from a peak of 1,678 employees in 2022 to 1,443 in 2023. A second, larger restructuring was announced spanning the third quarter of 2024 through the first quarter of 2025, involving a twenty percent workforce reduction, with some roles moved offshore. The expected restructuring costs were sixteen to nineteen million dollars.

The AI threat emerged as an existential question starting in late 2022 and accelerating through 2023 and 2024. ChatGPT's ability to explain concepts, answer questions, generate code, and provide personalized instruction raised a fundamental challenge: if an AI could serve as a personal tutor on virtually any topic, what was the value of pre-recorded video courses created by human instructors? The question was not hypothetical. Khan Academy launched Khanmigo, an AI-powered tutoring assistant, in 2023. Every major technology company was investing in AI-powered learning tools. The entire premise of Udemy's marketplace—that human instructors creating video content was the optimal way to deliver knowledge—was suddenly up for debate.

But the company was also bending toward profitability with notable determination. Losses peaked at 153.8 million dollars in 2022 and began narrowing rapidly. Gross margins expanded from the high fifties to sixty-three percent in 2024 and sixty-six percent in 2025. Adjusted EBITDA went from 7.8 million dollars in 2023 to forty-three million in 2024 to 95.3 million in 2025—a remarkable trajectory of margin expansion driven by cost discipline, restructuring, and the growing mix of higher-margin enterprise revenue. The third quarter of 2025 marked a milestone: Udemy reported its first GAAP-profitable quarter since the IPO, with 1.6 million dollars in net income.

In August 2024, founder Eren Bali returned to Udemy as Chief Technology Officer, leaving his CEO role at Carbon Health (where he remained as Executive Chairman). Bali's return was symbolically powerful—the founder coming home to the company he had built, now tasked with leading the AI-driven transformation of the platform's technology. He reported to CEO Greg Brown and oversaw engineering, data, and technical program management.

In March 2025, Hugo Sarrazin was appointed CEO, succeeding Greg Brown. Sarrazin brought a distinctive pedigree: twenty-seven years at McKinsey, where he had been a Senior Partner running the business technology practice in Silicon Valley, followed by a stint as President and Chief Product and Technology Officer at UKG, the human capital management software company. His appointment signaled that the board wanted someone who could drive the enterprise transformation while navigating the AI disruption with the strategic sophistication of a seasoned operator. The choice of a McKinsey veteran over a product visionary or growth-stage operator suggested that the board prioritized disciplined execution and strategic positioning over the kind of product-led innovation that might have characterized an earlier era of the company.

The leadership quartet of Sarrazin as CEO, Bali as CTO, Rob Rosenthal as President of Udemy Business, and Ramji Sundararajan as President of Consumer represented the most experienced and strategically diverse team in the company's history. Whether that team had the time and the tools to execute a transformation before the market's patience expired was the open question.

The stock, trading around five dollars by early 2026, represented an eighty-three percent decline from the IPO price. But the underlying business was dramatically healthier than the stock chart suggested—profitable on an adjusted basis, with a growing enterprise business and a leadership team focused on AI-enabled reinvention. The question was whether any of that mattered in a market that had largely written Udemy off.

VIII. The Instructor Ecosystem and Content Economics

To understand Udemy, you have to understand its instructors—not as an abstraction or a line item on an income statement, but as real people with real economic incentives that shape everything about the platform's content, quality, and competitive position.

The instructor revenue share model has been the most contentious aspect of Udemy's relationship with its content creators, evolving through several iterations that progressively shifted power toward the platform. In the earliest days, instructors received up to ninety percent of revenue on certain arrangements. That was reduced to seventy percent on Udemy-marketed sales, then slashed to fifty percent in the controversial 2013 change. The current tiered system works as follows: if an instructor drives a sale through their own coupon or referral link, they keep ninety-seven percent—a generous split that incentivizes self-promotion. But if a student finds the course through Udemy's marketplace organically, the instructor receives only thirty-seven percent. Since the majority of sales are platform-driven, most instructors operate at the lower end of this range.

The subscription model introduced yet another economic layer. For Udemy Business and the consumer subscription plan, Udemy allocates a pool of subscription revenue to instructors based on minutes consumed. This pool has been steadily shrinking: from twenty-five percent of monthly subscription revenue originally, to twenty percent in January 2024, to 17.5 percent in January 2025, with a planned reduction to fifteen percent in January 2026. As the subscription business grows relative to individual course purchases, instructors are effectively earning more in aggregate but less per unit of content consumed. The platform is capturing an ever-larger share of the value that instructors create.

The earnings distribution among instructors follows a brutal power law. Seventy-five percent of instructors earn less than one thousand dollars per year. Only about one percent earn over fifty thousand dollars—what might be considered a full-time income. The top one percent captures over half of total instructor earnings, while the bottom fifty percent shares just one percent. The S-1 filing disclosed that five percent of instructors generated seventy-one percent of paid marketplace enrollments, a concentration ratio that would alarm any economist studying platform health.

The instructors who do make serious money on Udemy have typically cracked a specific formula: choose a high-demand technical topic, produce high-quality video content, invest in marketing to build initial momentum, and benefit from the compounding effects of positive reviews and enrollment numbers that push their courses to the top of search results. Rob Percival, a web development instructor, reportedly earned over 2.8 million dollars in total Udemy earnings. Victor Bastos accumulated approximately nine hundred thousand. These are exceptional outcomes, and they create a powerful marketing narrative for Udemy's instructor recruitment—but they are wildly unrepresentative of the typical instructor experience.

The long-tail problem is the uncomfortable reality beneath the success stories. The vast majority of courses on Udemy sell almost nothing. Creating an online course requires significant effort—scripting, recording, editing, creating supplementary materials—and most instructors will never recoup that investment in monetary terms. This does not mean the courses are bad; many are excellent but simply cannot break through the discovery algorithms to reach an audience. The marketplace rewards incumbency, and once a course dominates a category, it becomes extraordinarily difficult to displace.

Quality spans an enormous spectrum. At the top end, Udemy courses are genuinely excellent—practical, well-structured, professionally produced, and regularly updated. At the bottom, they are hastily assembled cash grabs designed to capitalize on trending keywords. The open marketplace model means that Udemy cannot fully control this quality range without fundamentally changing its identity. The enterprise product solves this through curation—cherry-picking the best courses for the corporate catalog—but the consumer marketplace remains a wild frontier where buyer beware is the operating principle.

Content freshness is a persistent challenge. Technology skills change rapidly—a course on a JavaScript framework from two years ago may teach patterns that are already obsolete. Udemy encourages instructors to update their courses, but there is no mechanism to force updates, and many instructors move on to other projects once initial course creation is complete. This creates a quality decay problem that is particularly acute in the technology categories that generate the most revenue.

The platform power dynamics mirror those of other creator economies—YouTube, Amazon's third-party marketplace, app stores—where the platform controls discovery, pricing, and promotion while creators supply the content. Instructors have limited leverage individually, though top instructors can and do multi-home across platforms like Skillshare, Teachable, and their own websites. The relationship is symbiotic but asymmetric, and it generates a low-level hum of resentment that periodically erupts into public controversy.

The existential question looming over this entire ecosystem is what happens as AI improves. If ChatGPT can explain any programming concept on demand, personalized to the learner's level and learning style, what is the value of a pre-recorded video course? If AI can generate practice exercises, provide instant feedback, and adapt in real time, does the static course format become obsolete? Udemy's instructors are the company's most important asset and its most significant cost. If the asset becomes less valuable, the entire economic model unravels.

IX. Business Model Deep Dive and Unit Economics

Udemy's financial architecture is a study in contrasts. Two fundamentally different businesses—a consumer marketplace and an enterprise SaaS product—operate under one roof, sharing a content catalog but little else in terms of economics, growth dynamics, or competitive positioning.

The revenue mix tells the story of a business in transition. In 2023, enterprise revenue accounted for roughly fifty-eight percent of total revenue, and by 2024 it had reached sixty-three percent at 494.5 million dollars, with the consumer segment contributing 292.1 million. The enterprise business grew eighteen percent year-over-year in 2024, while consumer revenue declined five percent. By 2025, total revenue was essentially flat at 789.8 million dollars, with the enterprise segment continuing to grow modestly while consumer continued to shrink. The company's fortunes are now almost entirely dependent on whether the enterprise business can grow fast enough to offset consumer declines and eventually pull the overall growth rate back into positive territory.

Consumer unit economics are challenging. Customer acquisition costs are high relative to the average transaction value of ten to fifteen dollars per course purchase. Repeat purchase rates are modest—many students buy one or two courses and never return. The lifetime value of a consumer customer is limited by the low price points and the availability of free alternatives. The introduction of a consumer subscription plan (Udemy Personal) has shown promising early traction—paid subscribers reached 343,000 by the end of 2025, more than doubling year-over-year—but it remains a small portion of overall consumer revenue and its long-term retention characteristics are unproven.

Enterprise economics are substantially more attractive. The average contract value for large enterprise customers ranges from forty to eighty thousand dollars, with the largest deals reaching six or seven figures. Annual recurring revenue from the enterprise business reached approximately 520 million dollars by mid-2025. Net dollar retention—the measure of how much existing enterprise customers spend year-over-year—has ranged from ninety-three to ninety-five percent overall, and ninety-seven to ninety-nine percent for large enterprise customers. These are respectable but not exceptional SaaS metrics; world-class enterprise software companies typically achieve net retention above 120 percent, meaning their existing customers spend significantly more each year. Udemy's retention rates suggest that customers are generally staying but not dramatically expanding their usage—a "good but not great" signal that limits the compound growth potential of the enterprise base.

Gross margins have been improving steadily: from the high fifties historically to sixty-three percent in 2024 and sixty-six percent in 2025. This is lower than pure SaaS companies, which typically operate at seventy-five to eighty-five percent gross margins, because Udemy must share revenue with instructors. The instructor revenue share is effectively a cost of goods sold that scales with revenue, creating a structural ceiling on gross margins that pure software companies do not face. Think of it like a restaurant that has to pay for ingredients—no matter how efficiently you run the kitchen, the cost of the food is always there.

The operating leverage question is whether Udemy can reach twenty percent or higher operating margins as it scales. The trajectory is encouraging: adjusted EBITDA margins expanded from roughly one percent in 2023 to 5.5 percent in 2024 to twelve percent in 2025. This was driven primarily by cost cuts, restructuring, and the growing mix of higher-margin enterprise revenue. But sustaining this trajectory requires continued enterprise growth, stable instructor economics (meaning the revenue share does not need to increase to retain top instructors), and marketing efficiency improvements that have historically proven elusive in the consumer business.

The sales and marketing efficiency problem deserves particular attention. Udemy has consistently spent a high proportion of revenue on sales and marketing—necessary for driving consumer acquisition through performance marketing and for building the enterprise sales team. Bringing this ratio down while maintaining growth is the central financial challenge facing the company. In the enterprise business, the sales cycle is long and human-intensive, requiring account executives, solution engineers, and customer success managers. In the consumer business, paid acquisition competes against free alternatives and requires constant spending just to maintain baseline enrollment levels.

Comparing Udemy to its closest public competitor, Coursera, illuminates the trade-offs. Coursera's consumer gross margins are lower (twenty to twenty-five percent) because of university revenue share agreements that are more generous than Udemy's instructor payouts. But Coursera's university partnerships provide credentialing value that Udemy lacks, enabling premium pricing and different customer demographics. LinkedIn Learning, bundled into Microsoft's LinkedIn ecosystem, operates under a completely different economic model where the learning product drives engagement and retention for the broader LinkedIn platform—Microsoft does not need LinkedIn Learning to be profitable on a standalone basis, which is a structural advantage that no pure-play edtech company can match. Pluralsight, now private under Vista Equity, focused exclusively on deep technology skills with hands-on labs—a narrower market but potentially deeper moat.

One way to think about the unit economics challenge is through the lens of a restaurant analogy. A pure SaaS company is like a software restaurant where the food costs almost nothing—once the code is written, serving it to one customer or a million costs roughly the same. Udemy is more like a restaurant franchise where the ingredients (instructor content) represent a real, ongoing cost that scales with revenue. The instructor revenue share is Udemy's cost of goods sold, and unlike software costs, it cannot be engineered away through better technology or operational efficiency. This fundamental difference explains why Udemy's gross margins will likely never reach pure SaaS levels, and why investors who value the company using pure SaaS multiples will always be disappointed.

For investors evaluating Udemy's path to sustainable profitability, the math requires enterprise revenue to grow to seventy percent or more of the total mix, gross margins to stabilize in the mid-to-high sixties, and sales and marketing efficiency to improve as the enterprise customer base generates more expansion revenue relative to new logo acquisition costs. It is achievable—the trajectory points in the right direction—but it requires sustained execution in a competitive market with no room for major missteps.

X. Competitive Landscape and Market Positioning

The online learning market is one of those industries that looks enormous on paper—projected to reach 178 billion dollars by 2034, growing at nearly sixteen percent annually—but is so fragmented and competitive that no single player has achieved anything close to dominant market share. The top five platforms collectively hold only eight to ten percent of the total market, which tells you everything about both the opportunity and the challenge. It is a market where everyone can survive but nobody can dominate—the worst kind of competitive structure for generating exceptional returns.

On the consumer side, Udemy's most formidable competitor is not another edtech company—it is YouTube. Free tutorials on virtually every topic imaginable, from Python programming to watercolor painting, are available on demand with no purchase required. YouTube does not compete on production quality or structured curriculum, but it competes devastatingly on price (zero dollars) and convenience (already on every device, already habitual). Every potential Udemy customer has the option to learn for free on YouTube, and many do. Stack Overflow, GitHub documentation, and open-source communities provide additional free learning resources for the technology skills that represent Udemy's strongest category.

Among paid competitors, Skillshare operates a subscription model focused primarily on creative skills—design, illustration, photography, writing. LinkedIn Learning, included with LinkedIn Premium subscriptions, offers professionally produced courses across business, technology, and creative topics, with the massive advantage of being integrated into the world's largest professional network. CourseHero and Chegg serve adjacent markets in academic support. None of these is a direct Udemy clone, but all compete for the same fundamental resource: the learner's time and willingness to pay for structured educational content.

The fragmentation of the market is both Udemy's salvation and its curse. No single competitor has built a platform that matches Udemy across all dimensions—breadth, price, enterprise features, and global reach. But the fragmentation also means that Udemy faces different competitors in every segment: YouTube and free content in consumer, LinkedIn and Coursera in enterprise, Pluralsight in deep tech, and increasingly AI in the personalized tutoring space. Fighting a multi-front war against specialized competitors in each segment is strategically exhausting and capital-intensive.

In the enterprise market, the competitive dynamics are different and arguably more intense. LinkedIn Learning's distribution advantage is formidable—when your learning platform is integrated into the same ecosystem where employees manage their professional identities, job searches, and networking, the friction of adoption is minimal. Coursera for Business leverages university brand partnerships to offer credentialed learning paths that carry weight with both employees and employers. Pluralsight, now privately held, offers the deepest technology skills training with hands-on coding environments and skill assessments. Go1, an Australian aggregator, compiles content from multiple providers including Udemy itself, positioning as the "Spotify of learning" with the broadest content library. And legacy vendors like Skillsoft, Cornerstone OnDemand, and SAP SuccessFactors still hold significant enterprise market share through existing contracts and integrations.

Udemy's positioning in this crowded landscape is "skills marketplace for practical learning." It is not competing on credentials (that is Coursera's territory), entertainment value (that is YouTube and Skillshare), or deep technology specialization (that is Pluralsight). Udemy's value proposition is breadth, accessibility, and affordability—more courses on more topics in more languages at lower prices than anyone else. This is a legitimate competitive position, particularly in emerging markets where Udemy is often the most affordable option for quality skills training. The platform is notably strong in India, Latin America, and Southeast Asia, where the combination of massive demand for upskilling and price sensitivity aligns perfectly with Udemy's offering.

Language and localization represent both a strength and a limitation. Udemy offers courses in over seventy-five languages, but English-language content still dominates in terms of quality, depth, and instructor investment. The long tail of non-English courses is thinner and less consistently maintained, creating a quality gap that limits the platform's competitiveness in markets where English is not widely spoken.

The emerging threat that hovers over the entire landscape is AI-powered learning. ChatGPT, Claude, Gemini, and their successors can already explain concepts, answer questions, generate practice problems, and adapt explanations to individual learning styles—capabilities that overlap significantly with what Udemy courses provide. Khan Academy's Khanmigo demonstrated that AI tutoring could be effective and engaging at scale. If AI tutors continue to improve—and there is every reason to believe they will—the value proposition of pre-recorded video courses from human instructors could erode significantly. This threat applies to all online learning platforms, but Udemy is particularly vulnerable because its marketplace model relies on the assumption that human-created course content is the primary unit of value.

The content freshness challenge compounds this vulnerability. Technology skills change rapidly, and courses become outdated within months or years. Udemy's marketplace model means that updating courses is voluntary—the platform cannot force instructors to refresh content—and many courses in the catalog are stale. An AI tutor, by contrast, can draw on the latest documentation, research, and best practices in real time, never going out of date. This is not a hypothetical advantage—it is a structural one that grows more significant with each passing year.

Why has Udemy not been disrupted yet? Two reasons. First, the marketplace liquidity—250,000 courses across virtually every topic—creates a breadth of coverage that no single competitor has replicated. Second, the instructor network of 85,000 content creators represents a supply-side moat that takes years to build. But neither of these advantages is permanent. AI could generate personalized courses at scale, rendering the instructor network less essential. And if AI-native learning platforms deliver better outcomes at lower cost, marketplace liquidity becomes irrelevant—like having the world's largest VHS catalog after Netflix arrived.

XI. Porter's Five Forces Analysis

Any rigorous assessment of Udemy's competitive position requires looking beyond individual competitors to the structural forces that shape the industry's profitability and sustainability.

Threat of New Entrants: Moderate-High. The technology required to build an online course platform is commoditized. Open-source learning management systems, cloud hosting, video streaming infrastructure, and payment processing are all available as off-the-shelf components. A competent engineering team could build a functional Udemy competitor in months. What is hard—genuinely hard—is building two-sided marketplace liquidity. Getting enough instructors to create enough courses to attract enough students to attract more instructors is a cold-start problem that takes years of effort and significant capital to solve. Udemy's catalog of 250,000 courses and 82 million registered learners represents a genuine barrier to entry. But this barrier is not insurmountable, particularly for platform companies that already have large user bases (like Google, Apple, or Amazon) or AI companies that could generate content programmatically rather than relying on human instructors.

Bargaining Power of Suppliers (Instructors): Moderate. This is a split market. Top instructors—the five percent who generate seventy-one percent of enrollments—have meaningful leverage. They can multi-home across Skillshare, Teachable, their own websites, and YouTube, and their departure would hurt Udemy's catalog quality. Most instructors, however, have virtually no bargaining power. They depend on Udemy's marketplace for distribution and have no realistic alternative that offers comparable reach. The platform controls pricing, promotions, and discovery algorithms, creating a significant power asymmetry. The steady reduction in the subscription revenue pool allocated to instructors—from twenty-five percent down to a planned fifteen percent—demonstrates how the platform has used this power to progressively capture more value.

Bargaining Power of Buyers: High. On the consumer side, buyers have enormous power because the switching costs are zero and free alternatives abound. A student dissatisfied with a Udemy course can find similar content on YouTube, Google, or a competitor platform within seconds. Price sensitivity is extreme—the market has been conditioned to expect courses at ten to fifteen dollars, and any attempt to raise prices risks catastrophic volume declines. On the enterprise side, buyers are more concentrated and contracts are longer, but competitive bidding among multiple enterprise learning platforms gives procurement teams significant leverage on pricing and terms. Large enterprise customers, particularly the Fortune 500, are sophisticated buyers who benchmark providers against each other and negotiate aggressively.

Threat of Substitutes: Very High. This is arguably the most dangerous force facing Udemy. Substitutes are everywhere: free content on YouTube and the open web; formal education through universities and bootcamps; on-the-job training and mentorship programs; and, increasingly, AI tutors that can provide personalized, interactive instruction at near-zero marginal cost. The breadth and quality of free educational content available on the internet in 2026 is staggering, and it continues to grow daily. Every programming language, business concept, and creative skill that Udemy teaches has extensive free coverage elsewhere. Udemy's value-add is curation, structure, and a certificate of completion—but these are thin differentiators against the zero price point of substitutes.

Competitive Rivalry: High. The online learning market is fragmented, with multiple business models (marketplace, subscription, freemium, university-partnership, enterprise SaaS) competing for the same learner attention and corporate training budgets. Price competition is intense in the consumer market, and feature competition is fierce in the enterprise market. LinkedIn's distribution advantage, Coursera's credentialing prestige, and the emerging AI-native learning tools all create pressure from different angles. No single competitor is killing Udemy, but the cumulative competitive pressure limits pricing power, margin expansion, and growth potential.

Overall Assessment: The structural forces facing Udemy are unfavorable. High buyer power, very high substitute threat, and high competitive rivalry create an environment where sustaining attractive returns on capital is extremely difficult. The moderate barrier to entry from marketplace liquidity provides some protection, but it is not sufficient to create the kind of durable competitive advantage that generates exceptional long-term returns.

XII. Hamilton Helmer's Seven Powers Analysis

Moving from industry structure to company-specific competitive advantages, Hamilton Helmer's Seven Powers framework provides a more granular assessment of whether Udemy possesses durable sources of value that competitors cannot easily replicate.

Scale Economies: Weak. Udemy benefits from some fixed-cost leverage in platform development—the technology infrastructure that serves one million users can serve ten million without proportional cost increases. But the instructor revenue share creates a variable cost that scales with revenue, preventing the kind of dramatic operating leverage that pure software companies enjoy. The enterprise sales team requires ongoing human investment that does not scale linearly. And customer acquisition costs in the consumer business remain stubbornly high. Scale economies exist at the margins but are not strong enough to create a meaningful cost advantage over well-funded competitors.

Network Effects: Moderate. Udemy's two-sided marketplace does exhibit cross-side network effects: more instructors create more courses, which attract more students, which attract more instructors. This virtuous cycle is real and has been Udemy's primary engine of growth. But the network effects are weaker than those found in social networks or communication platforms, because learners on Udemy do not interact with each other in meaningful ways. There is no social graph, no community engagement, no viral loop. A student who loves a Python course does not generate additional enrollments through their usage in the way that a WhatsApp user generates additional installs. The network effects are enough to create modest marketplace liquidity advantages but insufficient to produce winner-take-all dynamics.

Counter-Positioning: Historical, Now Fading. In its early years, Udemy was genuinely counter-positioned against traditional education. Universities were too slow, too expensive, and too rigid. Udemy was fast, cheap, and open. Incumbents could not easily respond because adopting Udemy's model would cannibalize their own high-margin degree programs. This counter-positioning advantage was real through roughly 2015 and drove significant early growth. But it has eroded dramatically as every major educational institution, technology company, and content platform has embraced online learning. The counter-positioning advantage is essentially gone. The next wave of counter-positioning may be AI against all human-created course content—a threat that Udemy is on the wrong side of.

Switching Costs: Low (Consumer), Moderate (Enterprise). Consumer switching costs are effectively zero. A student can move from Udemy to Coursera or YouTube without losing anything of value. There is no data lock-in, no accumulated credentials that only work on Udemy, no social connections that would be severed. Enterprise switching costs are moderately higher—implementing a new learning platform requires integration work, employee retraining, content migration, and procurement cycles that create friction. But these costs are not high enough to prevent churn when a materially better alternative appears, and enterprise customers regularly evaluate competitive offerings.

Branding: Moderate. "Udemy" is a globally recognized brand associated with online learning. In brand awareness surveys, it consistently ranks among the top online learning platforms worldwide. But the brand association is mixed: affordable courses, yes, but also variable quality, heavy discounting, and a reputation as the "discount bin" of education. The brand is not prestigious (that is Coursera with its university partners), not aspirational (that is LinkedIn Learning with its professional network integration), and not beloved (that is Khan Academy with its nonprofit mission). Udemy's brand is functional—people know it, use it, and have modest expectations. This is better than no brand but insufficient to command pricing power or deep customer loyalty.

Cornered Resource: Weak. Udemy does not have exclusive relationships with its instructors, who are free to publish on competing platforms. It does not possess proprietary pedagogy or unique content. Its technology platform, while mature, is replicable. The instructor catalog of 250,000 courses is a valuable resource, but individual courses are not exclusive to Udemy, and the platform has no mechanism to prevent instructors from offering identical or similar content elsewhere.

Process Power: Weak to Moderate. Udemy has developed operational expertise in running a large-scale educational marketplace—managing instructor relationships, curating enterprise content, operating discovery and recommendation algorithms, and handling global payment processing in dozens of currencies. These processes are competent but not uniquely valuable. Nothing in Udemy's operational playbook represents the kind of deeply embedded, organizationally complex process advantage that, say, Toyota's production system or TSMC's manufacturing processes represent.

Overall Power Assessment: Udemy possesses moderate-to-weak competitive power across all seven dimensions. Its strongest asset is the marketplace network effect, but even this is insufficient to create a durable moat. The company is vulnerable to disruption from AI-native learning platforms, continued pressure from well-funded competitors like LinkedIn Learning, and the structural challenges of a market with high substitute availability and low switching costs. This does not mean Udemy cannot succeed as a business, but it does mean that exceptional long-term returns require exceptional execution in a structurally challenging environment.

XIII. Bull vs. Bear Case

The Bull Case

The most compelling argument for Udemy starts with the enterprise business. At 520 million dollars in annual recurring revenue and growing, Udemy Business serves over 17,000 enterprise customers including a majority of the Fortune 100. The net retention rate for large enterprise customers—ninety-seven to ninety-nine percent—indicates that once companies adopt the platform, they tend to stay and expand usage. As corporate learning and development budgets continue to grow, driven by the urgent need to upskill workforces for AI and digital transformation, Udemy's position as the broadest-catalog enterprise learning platform creates a meaningful competitive advantage.

The path to profitability has been proven. Adjusted EBITDA margins expanded from roughly one percent to twelve percent in just two years, and the first GAAP-profitable quarter arrived in the third quarter of 2025. The restructuring actions, while painful, have created a leaner cost structure that can generate meaningful operating leverage as enterprise revenue continues to grow. If the company can sustain mid-teens enterprise growth while holding costs relatively flat, twenty-percent-plus EBITDA margins become achievable.

The global market opportunity is genuinely massive. Skills training demand is accelerating worldwide as AI transforms job requirements across every industry. Udemy's catalog breadth—250,000 courses in 75 languages—and geographic reach—strong positions in high-growth emerging markets like India, Latin America, and Southeast Asia—provide a platform for international expansion that few competitors can match. The 291 percent surge in AI literacy demand reported in Udemy's 2024 Learning Index demonstrates that the platform is capturing real demand from the most important skills trend of the decade.

AI could enhance rather than replace the Udemy model. The company has invested in AI-powered recommendations, personalized learning paths, skills mapping for enterprises, and AI-assisted content creation tools for instructors. If AI makes existing courses more effective and personalized rather than replacing them, Udemy's vast content library becomes more valuable, not less.

The consumer subscription initiative, while early, shows promise. Paid subscribers more than doubled to 343,000 by the end of 2025, suggesting that a segment of consumers values ongoing access to the platform enough to pay recurring fees. If subscription revenue grows to represent a significant portion of the consumer business, it could transform consumer unit economics from transactional and unpredictable to recurring and stable.

Finally, the Coursera merger, announced in December 2025, creates a combined platform with over 1.5 billion dollars in revenue, expected cost synergies of 115 million dollars, and complementary strengths in marketplace content (Udemy) and university partnerships (Coursera). The merged entity would be the largest pure-play online learning company by a significant margin.

The Bear Case

The consumer business is structurally challenged and may be in permanent decline. Revenue fell five percent in 2024 and the trend has not meaningfully reversed. Free alternatives proliferate, brand perception is mixed (the "coupon site" stigma persists), switching costs are zero, and there is no obvious catalyst for consumer re-acceleration. The subscription initiative is promising but tiny relative to the overall consumer revenue base.

The enterprise market is becoming a commodity. LinkedIn Learning's distribution advantage through Microsoft's ecosystem is formidable and difficult to match. Coursera's university partnerships provide credentialing value that enterprise buyers increasingly demand. Go1's aggregation model allows companies to access Udemy content alongside content from other providers, reducing the direct relationship between Udemy and the enterprise buyer. Net dollar retention in the mid-nineties, while acceptable, suggests limited expansion revenue—enterprise customers are not dramatically increasing their spending year-over-year, which caps the compound growth potential of the installed base.

AI is an existential threat to the course format itself. The pre-recorded video course—Udemy's fundamental unit of value—may be a transitional format that is superseded by interactive, personalized AI tutoring. Every major technology company is investing billions in AI-powered education tools. If AI tutors become as good as the best human instructors (which many researchers believe is a matter of when, not if), the entire supply side of Udemy's marketplace becomes commoditized. The platform's 85,000 instructors, far from being an asset, become a cost center serving a shrinking market.

The marketplace model prevents high margins regardless of scale. Instructor revenue share is a structural cost that pure SaaS companies do not bear. Even as gross margins have expanded to sixty-six percent, they remain well below the seventy-five to eighty-five percent range typical of high-quality SaaS businesses. This margin gap limits the company's ability to invest in R&D, sales, and marketing relative to better-capitalized competitors, creating a perpetual resource disadvantage.

No strong moat exists. As the Seven Powers analysis demonstrated, Udemy's competitive advantages are moderate to weak across every dimension. The brand is not premium, switching costs are low, network effects are modest, and there are no cornered resources. In an industry with very high substitute threat and intense competitive rivalry, the absence of durable competitive advantages means that Udemy's current position is inherently fragile.

Management execution in public markets has been disappointing. From a four-billion-dollar IPO valuation to a roughly seven-hundred-million-dollar market cap represents an eighty-three percent destruction of value. While macro conditions and the broader edtech selloff contributed, the company's inability to articulate a clear, compelling narrative to Wall Street—neither pure SaaS nor pure marketplace—has been a persistent handicap.

Key Metrics to Watch

For investors tracking Udemy's ongoing performance, three KPIs matter most. First, enterprise annual recurring revenue growth rate, which measures whether the company's most important business is gaining or losing momentum—anything below ten percent growth would signal serious competitive pressure. Second, enterprise net dollar retention, particularly among large customers, which reveals whether existing clients are finding enough value to expand their usage. Third, adjusted EBITDA margin trajectory, which shows whether the path to sustainable profitability is real or an artifact of one-time cost cuts that eventually have to be reinvested.

XIV. AI, The Future of Learning, and Udemy's Next Chapter

The question that hangs over Udemy—and indeed over the entire online learning industry—is whether pre-recorded courses created by human instructors represent a durable educational format or a transitional technology that will be displaced by AI-native learning experiences. It is the right question, and the honest answer is that nobody knows yet.

The case for AI disruption is straightforward. Large language models can already explain complex concepts clearly, adapt to individual learning styles, answer follow-up questions in real time, generate practice exercises tailored to specific skill gaps, and provide feedback on student work. These capabilities overlap substantially with what a recorded video course provides, and AI does it interactively and on-demand rather than in a fixed, linear format. ChatGPT as a programming tutor is, in many contexts, already more effective than a recorded course—because it can answer the specific question you have right now, not the question the instructor anticipated when recording the course three years ago.

Udemy's AI strategy has been responsive and reasonably well-conceived, though time will tell whether it is sufficient. The company has invested in an AI Learning Assistant that provides natural-language chat grounded in course content, AI-powered skills mapping for enterprise customers, personalized learning path generation, and AI-assisted content creation tools that help instructors create microlearning content derived from existing courses. In 2025, under founder Eren Bali's technical leadership, the company accelerated its AI transformation with new hires focused on AI-powered product development and partnership ecosystems.

The shift toward skills verification represents a potentially more durable value proposition than content delivery alone. If Udemy can evolve from "we have courses" to "we can verify and certify that employees have specific skills," the platform becomes embedded in hiring workflows, performance management systems, and career development processes in ways that are harder for AI to displace. Assessments, certificates, and employer integrations create switching costs and institutional relationships that pure content delivery does not.

The strategic landscape shifted dramatically on December 17, 2025, when Coursera and Udemy announced a definitive all-stock merger agreement. Under the terms, Udemy stockholders would receive 0.800 Coursera shares for each Udemy share, valuing the combined entity at approximately 2.5 billion dollars. The merger represented a twenty-six percent premium to Udemy's thirty-day average trading price but a massive markdown from the four-billion-dollar IPO valuation. Coursera shareholders would own roughly fifty-nine percent of the combined company, with Udemy shareholders holding forty-one percent.

The strategic logic is compelling on paper. Coursera brings university partnerships, credentialing power, and a different learner demographic. Udemy brings marketplace breadth, instructor scale, and enterprise customer relationships. Combined, they would create the largest pure-play online learning platform with over 1.5 billion dollars in annual revenue and expected cost synergies of 115 million dollars within twenty-four months. Both companies' boards approved the deal unanimously, and Insight Venture Partners, Udemy's longest-standing institutional investor, committed to vote in favor.

Whether the merger succeeds—it is expected to close in the second half of 2026, pending regulatory and shareholder approval—will depend on integration execution, competitive response, and whether the combined entity can navigate the AI disruption that threatens both companies equally. Mergers of struggling companies do not always produce a stronger combined entity; sometimes they produce a larger struggling company. The 115 million dollars in expected cost synergies are achievable primarily through headcount reduction and elimination of overlapping functions, but revenue synergies—the harder and more important part—require successfully cross-selling to each other's customer bases and creating combined offerings that are more valuable than what either company provides alone.