Uber: The Story of Transportation's Ultimate Disruptor

I. Introduction & Episode Roadmap

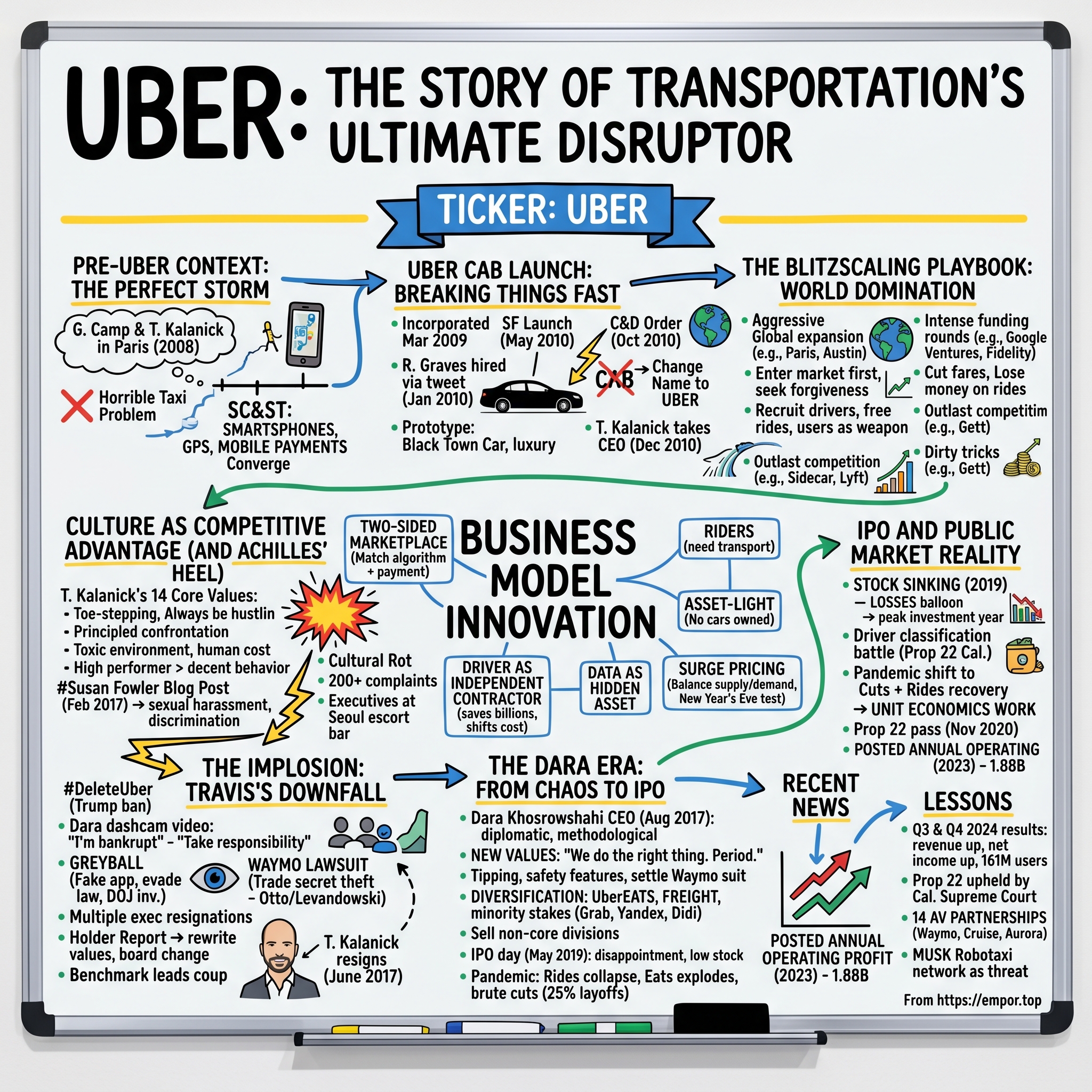

Picture this: It's 2010 in San Francisco, and you're standing on a rain-soaked street corner at 2 AM, desperately waving at yellow cabs that streak past with their lights off. Your phone battery is dying, you're soaked, and the last three taxis you flagged down told you they "don't go to that neighborhood." Then someone shows you an app—just press a button, and a black Town Car arrives in four minutes. The driver knows your name, has your destination, and payment happens invisibly. Magic.

That moment—multiplied by billions across the globe—transformed a simple app called UberCab into something far more profound: a verb, a lifestyle, and ultimately, one of the most controversial business stories of the 21st century. Today, Uber commands a market capitalization north of $150 billion, operates in over 70 countries, and has fundamentally rewired how humanity moves through cities. But the path from startup to transportation colossus reads less like a typical Silicon Valley success story and more like a Shakespearean drama—complete with coups, scandals, and redemption arcs.

How did a company that started with three cars in San Francisco become the default transportation layer for urban life? More intriguingly, how did a business built on brazenly breaking rules evolve into a public company trying to convince Wall Street it can generate sustainable profits? And perhaps most fascinatingly: What happens when the very culture that enables hypergrowth becomes an existential threat?

This is the complete Uber story—from Travis Kalanick's relentless drive to Dara Khosrowshahi's diplomatic cleanup, from regulatory battles in London to price wars in China, from the toxic "bro culture" that nearly destroyed the company to its remarkable pandemic pivot. We'll explore how Uber didn't just disrupt the taxi industry; it rewrote the social contract between companies, workers, and cities. Along the way, we'll unpack the business model innovations, the capital market dynamics, and the strategic decisions that shaped not just Uber, but the entire gig economy.

The central question we'll wrestle with: Can a company born from disruption—whose very DNA involves asking forgiveness rather than permission—build a sustainable, profitable empire? Or is Uber's story ultimately a cautionary tale about the limits of blitzscaling, the importance of culture, and the true cost of "moving fast and breaking things"?

Here's where we're headed: We'll start in 2008 Paris, where two entrepreneurs bonded over expensive taxi rides and terrible service. We'll witness the chaotic early days when cease-and-desist letters arrived faster than user signups. We'll dissect the playbook that conquered cities from New York to Nairobi. We'll go deep on the cultural implosion that toppled a founder-CEO at the height of his power. And we'll examine how a company that lost $8.5 billion in 2019 convinced investors it could become the Amazon of transportation.

Buckle up—this ride gets bumpy.

II. Pre-Uber Context: The Perfect Storm

The Uber origin story begins, improbably, at a tech conference in Paris. It's December 2008, LeWeb conference, and the global financial system is melting down. Lehman Brothers has just collapsed, unemployment is spiking, and venture capital has all but dried up. Yet in this frozen economic tundra, two serial entrepreneurs are about to stumble upon an idea that would eventually reshape urban life. Garrett Camp and Travis Kalanick were hanging out in Paris for LeWeb conference in late 2008, and their casual conversation would spawn one of the most disruptive companies in business history. Both men were successful entrepreneurs at that time—Travis had sold his file-sharing company Red Swoosh for $19 million to Akamai Technologies, and Garrett had co-founded StumbleUpon. Garrett's big idea was cracking the horrible taxi problem in San Francisco—getting stranded on the streets was familiar territory for any San Franciscan.

But to understand why this moment mattered, we need to rewind to Travis Kalanick's entrepreneurial journey—a saga of near-bankruptcies, lawsuits, and sheer stubbornness that would define Uber's DNA. While studying computer engineering at UCLA, Kalanick dropped out in 1998 to join Scour, one of the first peer-to-peer file-sharing services, which faced massive copyright infringement lawsuits and filed for bankruptcy in 2000. The lawsuits weren't small potatoes—Scour was sued for a quarter of a trillion dollars, a staggering sum that would have crushed most entrepreneurs' spirits. But Kalanick wasn't one to stay down. In 2001, he co-founded Red Swoosh with Michael Todd, calling it his "revenge business" against the entertainment industry that had killed Scour. The company's journey was a masterclass in startup hell. By August 2001, some employees had gone months without a paycheck. In September 2001, Red Swoosh used approximately $110,000 of the company's payroll tax withholdings to fund day-to-day operations. This wasn't just a cash flow problem—it was potential jail time. Todd had withheld dues to the IRS to the amount of $110,000 which is a white-collar crime and you could go to jail regardless of you knowing about it or not.

The situation deteriorated further when his co-founder Todd secretly emailed Sony Ventures, trying to get himself and the engineers hired while torpedoing the company. Kalanick kicked him out. By 2002, Red Swoosh was down to just two employees: Kalanick and one engineer. Travis worked for Red Swoosh without salary for over three years. He moved back into his parents' house, coded himself when Google poached his last engineer, and survived on a series of last-minute funding deals that always seemed to fall through at the worst possible moment.

The turning point came when Mark Cuban, after a contentious exchange on an internet forum, invested $1.8 million in 2005. In 2007, competitor Akamai Technologies acquired Red Swoosh for approximately $19 million. Kalanick made $2 million on the deal after taxes and moved to San Francisco.

This backstory matters because it explains everything about Uber's DNA. Travis Kalanick wasn't just an entrepreneur; he was a battle-scarred survivor who had stared down bankruptcy, lawsuits, IRS investigations, and betrayal. His philosophy crystallized: "Stand by your principles and be comfortable with confrontation. So few people are, so when the people with the red tape come, it becomes a negotiation."

Now back to Paris, 2008. It was a cold winter in late 2008. Garrett Camp and I were hanging out in Paris for a week at Loic and Geraldine LeMeur's LeWeb conference. Amongst the amazing food, the copious amounts of wine and inevitable nightlife crawls there were all kinds of discussions about what's next. Both men were in transition—Camp had sold StumbleUpon to eBay for $75 million and was doing "hard time" at a big company; Kalanick had just finished his tour with Akamai after the Red Swoosh acquisition.

The specific pain point that sparked Uber came from Camp's personal frustration. In 2008, San Francisco resident Garrett Camp and his friends had spent $800 on hiring private driver on New Years Eve, taking their car to several spots along the night. The cost seemed to rankle for Camp, who felt it was too much for one night's of transportation. Meanwhile, getting a regular taxi in San Francisco was its own special hell—if you could even find one willing to take you across the bridge.

The timing was perfect. Three technological forces were converging in 2008-2009 that made Uber possible: smartphones were achieving critical mass with the iPhone's explosion, GPS had become standard in every device, and mobile payments were finally viable. The infrastructure for a transportation revolution was in place; it just needed someone crazy enough to build on top of it.

The broken taxi industry provided the opening. Taxi medallions in major cities had become million-dollar monopolies, creating artificial scarcity. Service was terrible because drivers had no accountability—they could refuse rides, take circuitous routes, claim their credit card machines were "broken," and generally treat customers however they wanted. The system was ripe for disruption, but it was also protected by powerful lobbies, complex regulations, and entrenched interests. You'd have to be either naive or battle-hardened to take it on.

Garrett's big idea was cracking the horrible taxi problem in San Francisco — getting stranded on the streets of San Francisco is familiar territory for any San Franciscan. The initial concept was simple: Initially, the idea was for a timeshare limo service that could be ordered via an app. Push a button, get a ride. Camp bought the domain UberCab.com and began sketching out the concept. But this wasn't just about solving a personal inconvenience—it was about reimagining urban transportation from first principles.

The partnership between Camp and Kalanick was complementary. Camp was the visionary, the product thinker who imagined the elegant solution. Kalanick was the operator, the fighter who knew how to build companies in hostile environments. One created the dream; the other would wage the war to make it real. Neither initially wanted to run the company—but fate, as we'll see, had other plans.

III. The UberCab Launch: Breaking Things Fast

By March of 2009 Garrett started working in earnest on figuring out what this iPhone app would look like. The prototype was coming along, but it was still a side project – Garrett had spun out StumbleUpon and was now CEO again. The company officially incorporated in March 2009 with three co-founders: Garrett Camp, Travis Kalanick, and Oscar Salazar, Camp's friend from grad school who helped build the prototype. By mid-2009, Garrett began a charm offensive for ramping up Travis's involvement and by that summer Travis joined on as Uber's Chief Incubator. His job was to temporarily run the company, get the product to prototype, find a General Manager to run the operation full time and generally see Uber through its San Francisco launch. But finding the right leader proved serendipitous.

The story of Ryan Graves joining Uber has become Silicon Valley legend. On Jan 5, 2010, Ryan Graves sent a tweet to Uber co-founder Travis Kalanick suggesting himself as a potential hire for what was then a new start-up. Kalanick had tweeted: "Looking 4 entrepreneurial product mgr/biz-dev killer 4 a location-based service.. pre-launch, BIG equity, big peeps involved--ANY TIPS??" Graves, who was working for GE of all places in Chicago, simply replied: "Here's a tip. email me :)" and included his email address.

Kalanick has said that Graves, "hit the ground running," at Uber after he was hired. "From the day he got going, we spent about 15-20 hours a week working together going over product, driver on-boarding, pricing model, the whole nine. He learned the startup game fast and worked his a-- off to build the Uber team and make the San Francisco launch and subsequent growth a huge success." He became Uber's first official employee about two months later, on March 1.

By January 2010 they did their first test run in New York. We had 3 cars cruising the SOHO/Chelsea/Union Square areas and had a few people using the system. The core crew was Garrett, Travis, and Oscar Salazar. The idea was still positioned as a luxury service—press a button, get a black Town Car. No taxis, no regular cars, just high-end vehicles for people willing to pay a premium for convenience.

Ryan Graves was Uber's first chief executive officer, leading the fledgling startup in 2010 during its crucial early days. Hired personally by Travis Kalanick, Graves brought needed stability and leadership to Uber as it sought to establish itself. Though his tenure was short, barely lasting a year before Kalanick took over as CEO, Graves succeeded in growing Uber's footprint, expanding its services across multiple cities and recruiting Uber's early employees.

San Francisco launch day was May 31st, 2010 and the hair-on-fire craziness began. In the first two months after the app launched, the company went from coordinating 5 rides per night to about 50. But almost immediately, the regulatory battles began. In October 2010, the San Francisco Municipal Transportation Agency served UberCab with a cease and desist order, warning that they were in breach of regulations in the city and could face significant fines if they continued to operate as a taxicab company without appropriate permits. The order arrived on October 20th, and Ubercab remained in service under threat of penalties including up to $5,000 fee per instance of Ubercab's operation, and potentially 90 days in jail per each day the company remained in operation past the orders.

This was the defining moment—not because it threatened to kill the company, but because it proved they were onto something revolutionary. First of all, while no one likes the threat of legal action, this cease & desist is a huge validation of what UberCab is trying to do. The city of San Francisco (aka San Francisco Metro Transit Authority & the Public Utilities Commission of California) would simply not care if the company wasn't on to something. Or worse, they probably wouldn't even know about it if the service was lame. But that's not the case. There's clearly a demand for a service of this nature, and that's why the city cares.

Kalanick's response was pure Travis: Kalanick directed the company to ignore the order and continue operating, but changed the company's name from UberCab to Uber to prevent it from being accused of falsely advertising itself as a taxi company. The name change was a masterstroke—they didn't need the "Cab" part anyway. They were building something entirely new.

By December 2010, Kalanick took over as CEO from Ryan Graves, who transitioned to SVP of Global Operations. He held the position for ten months before being removed in favor of Kalanick. Camp and Graves each signed over a large portion of their shares to Kalanick when he took the CEO position, giving him a significant degree of control over the company. This wasn't a hostile takeover—it was a recognition that Uber needed a wartime CEO, and Travis Kalanick was built for war.

The early product was elegant in its simplicity but revolutionary in execution. Users opened an app, saw available cars on a map in real-time, pressed a button, and a black car arrived within minutes. The driver knew your name, had your destination, and payment happened automatically through stored credit cards. No cash, no tips, no haggling. The experience was so superior to traditional taxis that users became evangelists.

But the real innovation wasn't the technology—it was the business model audacity. Uber didn't own cars. They didn't employ drivers. They simply connected supply and demand through software and took a cut of each transaction. This asset-light approach meant they could scale infinitely without the capital requirements that had constrained transportation companies for a century.

The regulatory battles that began with that first cease-and-desist would become Uber's calling card. While competitors sought permission, Uber sought forgiveness—or more accurately, they sought to change the rules through sheer momentum. Each city they entered became a battlefield, with taxi commissions, city councils, and entrenched interests lined up against them. But Uber had a secret weapon: users who loved the service and would fight for it.

By early 2011, the company was ready to raise serious capital and expand beyond San Francisco. In February 2011, Kalanick met with Bill Gurley, an investor from venture capital firm Benchmark, and secured an $11 million investment for 20 percent of Uber (then valued at $50 million) for its Series A round of funding. The company embarked on its Series B round in late 2011, raising an additional $32 million.

But Kalanick's experiences at Scour and Red Swoosh had taught him to be paranoid about investor control. Kalanick's experiences with investors at Scour and Red Swoosh had made him wary of investors who might interfere with his control of Uber, so he ensured that the terms for these and future investments strongly favored himself and Uber. He strictly limited the amount of financial information investors could access, and the shares for new investors had a tenth of the voting power of the shares held by Kalanick, Camp, and Graves.

This structure would prove both prescient and problematic. It gave Kalanick the autonomy to move fast and break things, but it also insulated him from accountability when breaking things included breaking people. The seeds of Uber's future crisis were planted in these early structural decisions—a founder with near-absolute power, a board with limited influence, and a culture that prized growth above all else.

The transition from three cars in San Francisco to a global phenomenon was about to begin. What started as a simple solution to a taxi problem was evolving into something far more ambitious: a complete reimagining of urban transportation. And Travis Kalanick, the entrepreneur who had spent a decade failing upward, was finally in position to build an empire. The only question was whether he could do it without burning everything—including himself—to the ground.

IV. The Blitzscaling Playbook: World Domination

The numbers tell a story of unprecedented velocity. Early 2012: Uber is in a dozen cities with 50 employees, half in the field. By December 2013, the service was operating in 65 cities. Only 3 years after launching their first non-US city in Paris in December 2011, Uber was reaching a growth rate of launching a new city per day by the end of 2014. By 2015, they had achieved what seemed impossible: By 2015, it had a presence in 66 countries and over 360 cities worldwide.

The international expansion began almost accidentally. CEO Travis Kalanick was scheduled to give a keynote presentation at LeWeb, the annual European tech conference, in December 2011. When he casually mentioned that it would be great to launch Uber Paris at the conference, Mina and the rest of their team got right on board and started planning. They were set to launch in 30 days. With no prior international launch experience.

Paris was the proving ground for what would become the Uber playbook—a systematic approach to city conquest that could be replicated anywhere. Following the launch of Paris in 2012 as Ubers fifth city, and first international city, Austin Geidt was asked to put together a SWAT team of launchers that could be dropped into a city and launch it in a matter of weeks. The team developed what they called the "launch playbook"—a list of business strategies and operating guidelines that have been compiled by an internal team of about 40 employees.

The playbook was ruthlessly efficient. Step one: enter the market without asking permission. Step two: recruit drivers aggressively with guaranteed earnings and signing bonuses. Step three: flood the zone with free rides to build rider density. Step four: once you have critical mass, mobilize users as a political weapon against regulators. Step five: negotiate from a position of strength, with thousands of voters—sorry, users—demanding the service remain. The capital arms race was staggering in its intensity. In August 2013, Uber closed $258mn funding from Google Ventures which valued Uber at $3.76bn. By June 2014, Uber raised a $1.4B Series D at $18B valuation (up from $3.5B in Aug 2013) from Fidelity, Wellington, Blackrock, and Kleiner Perkins. The money wasn't for operations—it was for war.

The competition with Lyft and other upstarts like Sidecar became a brutal subsidization battle. Early 2014: Uber cuts UberX fares by up to 30% in select markets, hoping to boost demand during the winter slowdown and grow past Lyft. In 2015, Uber passengers were only paying about 40 percent of the cost of rides. By the end of 2015, Uber had raised $6.9 billion from private market investors, and Lyft had more than $1 billion in funding. Sidecar had raised about $43 million, hardly able to compete in a subsidy war.

This wasn't competition—it was economic warfare. Uber gave bonuses and other subsidies to drivers and reduced fares to passengers and lost money on every ride. "Uber intentionally sustained near-term losses that were designed to drive Sidecar out of the market while Uber acquired a dominant market position," as one lawsuit would later claim. The strategy worked: Sidecar went out of business in December 2015.

But Uber wasn't just competing on price. They pioneered dirty tricks that would become legendary in Silicon Valley. Jan 24 2014: Israeli startup Gett reports that Uber employees ordered and canceled >100 of its cars and texted drivers to switch to Uber. This was part of a broader strategy of what Kalanick called "principled confrontation"—which in practice meant anything goes.

The international expansion followed a similar playbook but with local variations. Uber calls its globalization strategy "launch playbook," a list of business strategies and operating guidelines that have been compiled by an internal team of about 40 employees. They treated each city like a startup but with the financial backing of a US company. At the end of 2014 the team were launching a new city each day and passed the 500 city milestone in a matter of years.

In China, the battle was particularly fierce. July 2014: Uber entered China after $1.2bn funding (17bn valuation). Uber's biggest competitor, Didi Kuaidi, responded by raising $3bn. Travis said that Uber was profitable in many cities globally, but that money was reinvested in its fight against Chinese player Didi. They were losing $1bn each year in the fight before eventually merging with Didi in August 2016.

The regulatory strategy was equally aggressive. Uber's strategy was generally to "seek forgiveness rather than permission". In 2014, with regards to airport pickups without a permit in California, drivers were actually told to ignore local regulations and that the company would pay for any citations. The product is so superior to the status quo that if we give people the opportunity to try it, in any place in the world where government has to be at least somewhat responsive to the people, they will demand it and defend its right to exist.

June 11 2014: London taxi drivers gridlock the city, protesting Uber. Ironically, Uber reports signups jumped 850% after the strike, a classic Streisand effect. This became the pattern everywhere—regulatory opposition became free marketing, and user outcry became political pressure.

The blitzscaling wasn't just about growth—it was about network effects and winner-take-all dynamics. Every city Uber entered made the next city easier. Every driver they recruited made the service better for riders. Every rider they acquired made driving more attractive. The flywheel spun faster and faster, powered by billions in venture capital.

Following Lyft and Sidecar into peer-to-peer ridesharing was crucial. In April 2013, after Wingz, Inc. fought to become legal and obtained the first legal ridesharing license in the world, Uber copied this model and added regular drivers instead of only black cars to the platform. This wasn't the luxury service anymore—it was transportation for everyone, subsidized by Silicon Valley's deepest pockets.

The velocity was breathtaking. Beginning of 2014: Uber has booked 200 million rides. July 2016: Uber announced that it completed 2bn trips, just 6 months after reaching 1bn rides. The company was doubling in size every six months, entering new markets daily, fighting regulators everywhere, and burning through cash at rates that would make even dot-com era companies blush.

By 2016, Uber had achieved something unprecedented: they were operating in over 450 cities across 66 countries, had raised nearly $7 billion in private capital, and had a valuation approaching $70 billion. They weren't just the biggest startup in the world—they were rewriting the rules of how companies could grow.

But this hypergrowth came with a cost that went beyond dollars. The same aggressive, win-at-all-costs culture that enabled global domination was creating toxic dynamics inside the company. The blitzscaling playbook had worked—perhaps too well. Uber had conquered the world, but in doing so, it had created enemies everywhere: regulators, competitors, drivers, and increasingly, its own employees. The stage was set for one of the most spectacular corporate culture crises in business history.

V. Culture as Competitive Advantage (and Achilles' Heel)

Culture at Uber wasn't an afterthought—it was a weapon. Travis Kalanick spent hundreds of hours huddled with senior executives drafting the company's 14 core values, before they were unveiled to employees from a stage at a 2015 employee retreat at Planet Hollywood in Las Vegas. These weren't your typical corporate platitudes about integrity and teamwork. They were a manifesto for corporate warfare.

The 14 values read like a battle cry: - Customer obsession (Start with what is best for the customer.) - Make magic (Seek breakthroughs that will stand the test of time.) - Big bold bets (Take risks and plant seeds that are five to ten years out.) - Inside out (Find the gap between popular perception and reality.) - Champion's mind-set (Put everything you have on the field to overcome adversity and get Uber over the finish line.) - Superpumped (Ryan Graves's original Twitter proclamation after Kalanick replaced him as CEO; the world is a puzzle to be solved with enthusiasm.) - Be an owner, not a renter (Revolutions are won by true believers.) - Meritocracy and toe-stepping (The best idea always wins. Don't sacrifice truth for social cohesion and don't hesitate to challenge the boss.) - Always be hustlin' - Principled confrontation

These values weren't just words on a wall—they shaped every hiring decision, every performance review, every strategic choice. "Toe-stepping" was meant to encourage employees to share their ideas regardless of their seniority or position in the company, but too often it was used as an excuse for being an asshole. "Always be hustlin'" justified 80-hour weeks and crushing anyone who stood in your way. "Principled confrontation" meant you could scream at subordinates as long as you believed you were right. The culture enabled engineering excellence but at a devastating human cost. By 2016, talented employees were leaving in droves, and those who stayed often found themselves in a toxic environment where aggression was rewarded and empathy was weakness. Corporate culture at Uber under Kalanick was grueling. Employees were expected to work nights and weekends regularly without additional compensation, and conference calls were often scheduled at all times of the night. Kalanick favored employees who were willing to do anything to advance in the company, even if it resulted in chronic infighting.

Then came February 19, 2017—the day that changed everything. Susan Fowler, a Site Reliability Engineer (SRE) at Uber, published a blog post titled "Reflecting on one very, very strange year at Uber." In it, I described a year of employment that began with a sexual proposition from my manager and only grew more demeaning and demoralizing from there. When I reported the situation, I was told by both HR and upper management that even though this was clearly sexual harassment and he was propositioning me, it was this man's first offense, and that they wouldn't feel comfortable giving him anything other than a warning and a stern talking-to. Upper management told me that he "was a high performer" (i.e. had stellar performance reviews from his superiors) and they wouldn't feel comfortable punishing him for what was probably just an innocent mistake on his part.

The blog post was devastating in its matter-of-factness. Fowler didn't rant or rage—she simply documented, with engineering precision, a year of systematic discrimination, retaliation, and gaslighting. The story was shared 22,000 times on Twitter. It racked up 6 million reads within weeks. The revelations kept coming: managers changing performance reviews to block transfers, HR lying about complaint histories, executives stealing leather jackets ordered for female employees because there weren't enough women to meet the vendor's minimum order. The cultural rot went deeper than individual harassment cases. In 2014, then-CEO Travis Kalanick, then-SVP of Business Emil Michael, and others visited a "karaoke" bar in Seoul, Korea which was staffed by "escorts." According to reports, women working at the bar wore numbered tags and sat in a circle, so men could identify their favorites. Four male Uber managers picked women out of the group, calling out their numbers, and sat with them. One of the female Uber managers in the group felt uncomfortable during this encounter and reported the event to HR at Uber about one year later, saying it made me feel horrible as a girl (seeing those girls with number tags and being called out is really degrading).

The incident only came to light in 2017 when Emil Michael called Gabi Holzwarth, Kalanick's ex-girlfriend who had been present, asking her to keep quiet about it if reporters asked. "I'm not going to lie for them," she said, describing Kalanick as "part of a class of privileged men who have been taught they can do whatever they want, and now they can."

But even more damaging than individual incidents was what they revealed about systemic dysfunction. Susan Fowler's blog post described a game-of-thrones political war raging within the ranks of upper management in the infrastructure engineering organization. It seemed like every manager was fighting their peers and attempting to undermine their direct supervisor so that they could have their direct supervisor's job. The values weren't just enabling bad behavior—they were mandating it.

The numbers told a devastating story. According to Fowler's account and subsequent investigations, Over 200 complaints of sexual harassment and gender discrimination from 2012-2017. Women made up just 15% of Uber's engineering workforce, and the percentage was falling. The company's own diversity report would later confirm these dismal statistics.

The culture wasn't just toxic—it was strategically toxic. The same aggression that helped Uber bulldoze taxi commissions was turned inward. The same disregard for rules that enabled regulatory arbitrage became disregard for basic human decency. The same "winner-take-all" mentality that drove market expansion created a zero-sum internal competition where colleagues were enemies and empathy was weakness.

Kalanick's leadership style set the tone from the top. Corporate culture at Uber under Kalanick was grueling. Employees were expected to work nights and weekends regularly without additional compensation, and conference calls were often scheduled at all times of the night. Kalanick favored employees who were willing to do anything to advance in the company, even if it resulted in chronic infighting.

The irony was that the culture was both Uber's greatest strength and its fatal flaw. It enabled the company to grow from zero to a $68 billion valuation in seven years. It attracted brilliant, aggressive, ambitious people who could execute at superhuman speed. It created a sense of mission and urgency that made the impossible possible.

But it also created an environment where Susan Fowler could be propositioned by her manager on her first day and be told by HR that nothing would be done because he was a "high performer." Where managers could openly discriminate against women and face no consequences. Where executives could visit escort bars on company trips and attempt to cover it up. Where the very people building the future of transportation couldn't get to work without fearing harassment.

The cultural debt was accumulating faster than the financial losses. And unlike subsidized rides or regulatory fines, this debt couldn't be paid with venture capital. It would require something far more difficult: acknowledging that the very values that built Uber might destroy it.

By early 2017, the company was simultaneously at its peak and on the verge of collapse. Valued at nearly $70 billion, operating in 66 countries, processing billions of rides—and hemorrhaging talent, facing multiple investigations, and becoming a symbol of everything wrong with Silicon Valley. The culture that had been designed as a competitive advantage had become an existential threat. The question was no longer whether there would be a reckoning, but whether Uber would survive it.

VI. The Business Model Innovation

Behind the cultural chaos and regulatory battles, Uber had engineered something revolutionary: a business model that turned conventional economics upside down. This wasn't just about replacing taxis with apps—it was about reimagining the fundamental mechanics of urban transportation.

The genius began with the two-sided marketplace. Traditional taxi companies owned cars, employed drivers, and served customers—a capital-intensive, operationally complex model that hadn't changed since the invention of the automobile. Uber owned nothing, employed no drivers, and yet orchestrated millions of rides daily. They weren't a transportation company; they were a matchmaking algorithm with a payment processor attached.

The marketplace dynamics were elegant in their simplicity but fiendishly complex in execution. On one side: drivers with idle cars and time to spare. On the other: riders who needed to get somewhere. Uber's job was to balance supply and demand in real-time, across thousands of micro-markets, with constantly shifting variables. Too many drivers and they'd quit from lack of earnings. Too few and riders would abandon the platform for competitors. The margin for error was razor-thin.

The take rate—Uber's cut of each ride—became the crucial lever. In the second quarter of 2025, the company had a take rate (revenue as a percentage of gross bookings) of 30.6% for mobility services and 18.8% for food delivery. But these numbers obscure a more complex reality. In the early days, Uber often took negative margins, subsidizing rides to build density. The path to profitability wasn't through individual transaction economics but through market dominance that would eventually allow pricing power.

But the real innovation—the one that would transform Uber from a clever app into an economic phenomenon—was surge pricing. When demand exceeded supply, prices would automatically increase, sometimes by 2x, 5x, even 10x normal rates. New Year's Eve 2011 was the beta test: as midnight approached and demand spiked, prices soared. Users screamed bloody murder on social media. But something fascinating happened: drivers flooded onto the platform, drawn by the higher earnings. Supply met demand. The market cleared.

Surge pricing wasn't just about revenue optimization—it was about liquidity creation. By dynamically adjusting prices, Uber could guarantee that a ride was always available, even if expensive. This reliability, even at premium prices, became a core value proposition. Better to pay $100 for a ride that exists than $20 for a taxi that never comes. The algorithm had solved a problem that had plagued transportation for a century: how to ensure supply when and where it's needed most.

The asset-light model was perhaps the most radical departure from traditional business thinking. Taxi companies spent millions on medallions, vehicles, maintenance, and insurance. Uber spent nothing. Every car on the platform was owned by someone else. Every driver was an independent contractor. The company's only assets were code, data, and brand. This meant Uber could expand to a new city with essentially zero marginal cost—just flip a switch and watch the marketplace activate.

But "asset-light" didn't mean "capital-light." The subsidization strategy required enormous amounts of cash. In 2015, Uber passengers were only paying about 40 percent of the cost of rides. The company was essentially buying market share, betting that once they achieved critical mass, network effects would create an unassailable moat. Every rider brought to the platform made it more attractive to drivers. Every driver made the service more reliable for riders. The flywheel would spin faster and faster until competition became mathematically impossible.

The driver classification battles revealed the model's fundamental tension. Drivers were the lifeblood of the platform, yet Uber insisted they weren't employees but independent contractors—free to work when they wanted, for whichever platforms they chose. This classification saved Uber billions in employment taxes, benefits, and liability. But it also meant drivers bore all the costs—gas, maintenance, depreciation, insurance—while Uber captured an increasing share of revenue.

The unit economics told a complex story. A typical UberX ride might generate $20 in gross bookings. Uber takes 25-30%, leaving $14-15 for the driver. From that, the driver pays for gas ($2-3), vehicle depreciation ($2-3), maintenance ($1), insurance ($1), leaving perhaps $7-9 in actual earnings for 30 minutes of work. Uber's $5-6 share covers payment processing ($0.50), insurance ($1), technology infrastructure ($0.50), customer support ($0.50), and maybe—eventually—profit.

But profitability at the unit level was beside the point during the growth phase. The strategy was to achieve monopolistic market share first, then optimize economics later. Uber, Lyft, Via and later Juno armed with billions of dollars in venture capital money were able to both pay drivers competitive wages and give passengers low fares via investor subsidies. In essence, the unit economics of their business model were likely negative, as Kevin Roose of the NY Times points out with a playful analogy of selling a $20 sandwich for $10.

The platform expansion strategy leveraged the core marketplace infrastructure for adjacent opportunities. UberEATS used the same driver network for food delivery. UberFREIGHT connected shippers with truckers. Uber for Business managed corporate transportation. Each new vertical could plug into the existing technology stack, payment system, and user base. The marginal cost of launching new products approached zero.

Data became the hidden asset. Every ride generated GPS traces, timing patterns, demand signals, pricing responses. Uber knew more about urban transportation patterns than any government transportation department. They could predict where demand would spike before it happened, route drivers efficiently through traffic, and price discriminately based on willingness to pay. The algorithm learned and improved with every transaction.

The network effects were powerful but not impenetrable. There is also an interesting chicken-and-egg dynamic in marketplaces such as ridesharing in which network effects are achieved through the supply side. Aggregating enough driver supply is needed for the service to be viable for riders. However, drivers are not employees and are free to use multiple services, so even though Uber has been first to many markets and has been able to achieve the critical mass of drivers needed, as soon as a competitor, such as Lyft enters, the drivers can easily sign up. In a way, Uber is doing the heavy lifting for the entire ride-hailing ecosystem.

The competitive moat turned out to be shallower than expected. Switching costs for both drivers and riders were essentially zero. Multi-homing was common—drivers worked for both Uber and Lyft, riders had both apps installed. The network effects were local, not global. Dominance in San Francisco didn't guarantee success in Shanghai. Each market was its own battlefield.

Capital became the primary weapon. By the end of 2015, Uber had raised $6.9 billion from private market investors, and Lyft had more than $1 billion in funding, according to data firm PitchBook Inc. Sidecar had raised about $43 million, hardly able to compete in a subsidy war. The model worked not because it was efficient but because Uber could raise more money than anyone else. They could lose more for longer, subsidize more aggressively, and outlast competitors who ran out of cash.

The path to profitability remained opaque even as the company grew. Uber has posted hundreds of millions or billions of dollars in losses each year from 2014 until 2022 except for 2018, when it exited from the markets in Russia, China, and Southeast Asia in exchange for stakes in rival businesses. By the end of 2022, Uber had US$32.11 billion in assets and $24.03 billion in liabilities. Uber posted annual operating profits in 2023, totaling $1.88 billion, after accumulating $31.5 billion in operating losses since 2014.

The business model innovation was undeniable. Uber had created a new category, pioneered dynamic pricing in consumer markets, and proved that asset-light platforms could achieve massive scale. They had reduced transaction costs, increased market liquidity, and made transportation more efficient. But whether this innovation could translate into sustainable profits remained an open question. The model had conquered the world, but it hadn't yet conquered basic economics.

VII. The Implosion: Travis's Downfall

The unraveling began with a hashtag. January 28, 2017: President Trump signed an executive order banning travel from seven Muslim-majority countries. Taxi drivers at JFK airport went on strike in solidarity. Uber, seeing an opportunity, turned off surge pricing at the airport. The optics were catastrophic—while others protested injustice, Uber appeared to be profiteering from it. #DeleteUber exploded across social media. In a single weekend, over 200,000 users deleted the app. Travis tried damage control, joining Trump's business advisory council to gain political leverage, but this only intensified the backlash. When he finally resigned from the council on February 2, it was too late—the narrative had been set: Uber was on the wrong side of history.

Then came the video that would define Travis Kalanick's downfall. February 5, 2017—Super Bowl Sunday. Kalanick is in the back of an UberBlack, flanked by two female companions, listening to Maroon 5 and boasting about his management philosophy: "I make sure every year is a hard year. That's kind of how I roll. I make sure every year is a hard year. If it's easy I'm not pushing hard enough."

When his companions exit, driver Fawzi Kamel seizes the moment. He's been driving for Uber since 2011, watched rates fall and standards rise. "I lost $97,000 because of you. I'm bankrupt because of you," Kamel tells Kalanick. The CEO's response would become infamous: "Some people don't like to take responsibility for their own shit. They blame everything in their life on somebody else. Good luck!"

Bloomberg published the dashcam footage on February 28. As the clip ended, Kalanick and two other executives stood in stunned silence. Kalanick seemed to understand that his behavior required some form of contrition. According to a person who was there, he literally got down on his hands and knees and began squirming on the floor. His apology email to staff that day was unprecedented: "To say that I am ashamed is an extreme understatement... I must fundamentally change as a leader and grow up. This is the first time I've been willing to admit that I need leadership help and I intend to get it."

But the hits kept coming. March 3, 2017: The New York Times broke the Greyball story. Through the use of Greyball, Uber was capable of targeting selected individuals, for example local police, with a fake version of the app that displayed fake cars that would never arrive if contacted. This was developed with the intention of evading the law where the company's practices had been deemed illegal. Greyball was deployed in countries including Belgium, the Netherlands, Germany, Spain and Denmark, with the knowledge of senior management such as Kalanick and Pierre-Dimitri Gore-Coty.

Greyball would use data collection to identify app users who were likely to be government officials and then feed them a fake version of the app with "ghost cars." When these watchdogs would try to book a ride, it would either appear that nobody was available or it would book a driver only to cancel before the "car" reached the customer. The sophistication was remarkable—Greyball mined credit card databases to identify credit cards associated with government agencies or law enforcement. It also used a technique called "geofencing" to essentially cordon off areas near city government offices so that when somebody attempted to hail a ride in those areas, Greyball would flag them. The program identified when users were opening the app several times without booking a ride and used that information along with geofencing to flag users as probably law enforcement.

The Department of Justice opened a criminal investigation. The US Department of Justice has begun a criminal investigation into Uber Technologies Inc's use of a software tool that helped its drivers evade local transportation regulators. Uber has acknowledged the software, known as 'Greyball', helped it identify and circumvent government officials who were trying to clamp down on Uber in areas where its service had not yet been approved, such as Portland, Oregon. The company prohibited the use of Greyball for this purpose shortly after the New York Times revealed its existence in March.

Then came the knockout blow: the Waymo lawsuit. February 23, 2017: Waymo took legal action against Otto and its parent company Uber for misappropriating Waymo trade secrets and infringing our patents. Recently, we uncovered evidence that Otto and Uber have taken and are using key parts of Waymo's self-driving technology. The allegations were explosive. Once inside, he downloaded 9.7 GB of Waymo's highly confidential files and trade secrets, including blueprints, design files and testing documentation. Then he connected an external drive to the laptop. Mr. Levandowski then wiped and reformatted the laptop in an attempt to erase forensic fingerprints. Beyond Mr. Levandowki's actions, we discovered that other former Waymo employees, now at Otto and Uber, downloaded additional highly confidential information pertaining to our custom-built LiDAR including supplier lists, manufacturing details and statements of work with highly technical information.

The timeline was damning. Levandowski continued to work as a technical lead on Google's self-driving car project alongside Chris Urmson, Dmitri Dolgov, and Mike Montemerlo until January 2016, when he left to launch Otto. Levandowski allegedly downloaded 9.7 GB of Waymo's confidential files before resigning to found Otto. Levandowski stated he left Google because he, "was eager to commercialize a self-driving vehicle as quickly as possible." Otto was acquired by Uber in late July 2016, at which point Levandowski assumed leadership of Uber's driverless car operation.

Uber had paid $680 million for Otto when it was just six months old—an astronomical sum that made no sense unless they were buying something more than a startup. Months before the mass download of files, Mr. Levandowski told colleagues that he had plans to "replicate" Waymo's technology at a competitor. The lawsuit wasn't just about trade secrets—it was about the future of autonomous vehicles, with billions at stake.

Each scandal reinforced the others, creating a cascading crisis of confidence. Employees were demoralized. The board was fracturing. Investors were panicking. The press smelled blood. Every day brought new revelations, new lawsuits, new hashtags. The company that had spent seven years bulldozing through obstacles suddenly found itself under siege from all directions.

March 21, 2017: Kalanick's mother died and father was seriously injured in a boating accident. Even personal tragedy couldn't pause the corporate meltdown. The board hired Eric Holder to investigate the culture. The Justice Department was investigating Greyball. The Waymo lawsuit was heading to trial. Senior executives were fleeing—the President, VP of Product, VP of Growth and VP of Engineering all resigned within weeks.

By May 2017, the situation was untenable. In May 2017 Levandowski was fired from Uber after Waymo and Google charged he had stolen trade secrets. The board, led by Benchmark's Bill Gurley, began orchestrating Kalanick's removal. They had funded his war on the taxi industry, enabled his aggressive expansion, and profited from his win-at-all-costs mentality. Now they needed a scapegoat.

June 13, 2017: The Holder Report was delivered to the board. Though never publicly released in full, the recommendations were damning—fire 20 employees, institute mandatory leadership training, rewrite the cultural values, add independent board members, limit Kalanick's responsibilities. The report confirmed what everyone knew: Uber's culture was toxic from top to bottom.

June 20, 2017: The coup was complete. Five major investors, including Benchmark, demanded Kalanick's immediate resignation in a letter titled "Moving Uber Forward." They delivered it while he was still grieving his mother's death. Faced with investor revolt and threatened with the nuclear option of going public with more damaging information, Kalanick resigned that night. "I love Uber more than anything in the world and at this difficult moment in my personal life I have accepted the investors request to step aside so that Uber can go back to building rather than be distracted with another fight," he said in a statement.

But Kalanick wasn't going quietly. He retained his board seat and significant voting control. The board battle turned into open warfare, with Benchmark suing Kalanick for fraud, seeking to strip him of his board seats. Kalanick countered by trying to pack the board with allies. The company was literally fighting itself while trying to find a new CEO. It was corporate governance at its most dysfunctional—a unicorn tearing itself apart.

VIII. The Dara Era: From Chaos to IPO

August 27, 2017: The search committee's decision stunned Silicon Valley. Not Meg Whitman, the former HP CEO who had publicly campaigned for the job. Not Jeff Immelt, the outgoing GE chief with decades of experience managing complexity. Instead, Uber's board chose Dara Khosrowshahi, the relatively unknown CEO of Expedia—a travel booking company most people forgot existed. The dark horse had won.

Khosrowshahi was everything Kalanick wasn't: diplomatic where Travis was combative, methodical where Travis was impulsive, corporate where Travis was startup. The 48-year-old Iranian-American had fled Iran as a child during the revolution, worked his way through Brown and Harvard Business School, and spent twelve years quietly building Expedia into a $72 billion travel empire. He was the adult supervision Uber desperately needed.

His first moves were symbolic but powerful. Where Kalanick had championed "Always be hustlin'" and "Toe-stepping," Khosrowshahi introduced new cultural norms: "We do the right thing. Period." "We act like owners." "We persevere." "We value ideas over hierarchy." "We make big bold bets." Gone was the combative language, replaced with corporate responsibility speak that wouldn't have been out of place at IBM.

The apology tour began immediately. Within weeks of taking over, Khosrowshahi flew to London, where Transport for London had refused to renew Uber's license, citing lack of corporate responsibility. Kalanick would have declared war; Khosrowshahi admitted mistakes. "We have got things wrong along the way," he told employees. "We must play to win, and we must also win the right way."

One of his first product decisions was allowing tipping—something drivers had begged for and Kalanick had stubbornly refused. It was a small change that sent a big message: the new Uber actually cared about drivers. He implemented new safety features like an emergency button, ride check-ins, and driver background checks. He settled the major lawsuits, including the Waymo case for 0.34% of its equity, a share which is valued at approximately $245 million.

But Khosrowshahi's biggest challenge wasn't fixing the past—it was building a future. The company was hemorrhaging a billion dollars per quarter. Competition from Lyft was intensifying. International markets were becoming battlegrounds. And looming over everything was the pressure to go public, to give early investors their long-awaited payday.

The answer was diversification. If Uber couldn't make money on rides alone, it would become something more. Uber Eats, which had launched in 2014 as a small experiment, was elevated to a core business. By 2018, Eats had generated $1.5 billion in revenue, growing 200% year-over-year. The company launched Uber Freight to connect truckers with shippers. They experimented with Uber Health for medical transportation, Uber for Business for corporate accounts, and even briefly, Uber Elevate for flying cars.

The push toward profitability meant hard choices. Khosrowshahi sold Uber's Southeast Asian operations to Grab in exchange for equity. Russia went to Yandex. China had already been surrendered to Didi. These weren't defeats—they were strategic retreats, acknowledging that Uber couldn't win everywhere and shouldn't try. Better to own a piece of a profitable competitor than to burn cash in an unwinnable war.

April 2019: Uber filed its S-1, revealing its finances to the world for the first time. The numbers were staggering. Revenue of $11.3 billion in 2018. Losses of $3.3 billion. 91 million monthly active users. 3.9 million drivers. Operations in 63 countries. The company had completed 10 billion trips and was adding a million new drivers every quarter. The scale was unprecedented—but so were the losses.

The IPO roadshow was Khosrowshahi at his diplomatic best, trying to convince Wall Street that Uber was the next Amazon, not the next Groupon. "We have size and scale that is unique, and we're going to continue to grow," he told investors. The pitch was ambitious: Uber wasn't just replacing taxis, it was replacing car ownership. The total addressable market wasn't the $100 billion taxi industry but the $12 trillion transportation industry.

But investors were skeptical. Unlike the private markets where growth was everything, public investors wanted a path to profitability. The WeWork implosion had made everyone wary of money-losing unicorns with grand visions. The trade war with China was escalating. Lyft's IPO in March had initially popped but was now trading below its offering price.

May 9, 2019: Pricing day. The company that had hoped for a $120 billion valuation, that had been valued at $76 billion in its last private round, priced at $45 per share—a $75.46 billion market cap. It was a success by any normal measure but a disappointment by Uber standards. The company raised $8.1 billion, one of the largest IPOs in US history, but it felt like a letdown.

May 10, 2019: IPO day was a disaster. The stock opened at $42, below its IPO price, and closed at $41.57—down 7.6%. It was one of the worst first-day performances for a major IPO ever. Travis Kalanick, who had shown up to the NYSE despite not being invited to ring the bell, quietly sold $547 million worth of shares that day. The symbolism was perfect: the founder cashing out as his creation stumbled into public markets.

The early months as a public company were brutal. The stock fell to $25 by November 2019, nearly half its IPO price. Every quarterly earnings report brought the same story: growing revenue, growing losses, and promises that profitability was just around the corner. Khosrowshahi compared Uber to Amazon in the early 2000s—investing heavily for long-term dominance. "We're reaching peak losses in 2019," he promised investors.

But unlike Amazon, Uber faced structural challenges. Drivers were pushing for employment classification, which would add billions in costs. Cities were imposing new regulations and fees. Competition wasn't decreasing—if anything, it was intensifying as everyone from Google to Tesla to traditional automakers invested in autonomous vehicles that could eventually eliminate Uber's need for human drivers entirely.

The Khosrowshahi era had stabilized the company, cleaned up its reputation, and gotten it public. But the fundamental question remained: Could a company built on subsidizing rides with venture capital ever actually make money? The cultural crisis was over, but the business model crisis was just beginning.

IX. The IPO and Public Market Reality

The numbers told a sobering story. From the IPO price of $45, Uber stock sank to $25.58 by November 2019—a 43% decline in six months. The company that had commanded a $120 billion private market valuation was now worth barely $60 billion in public markets. Reality had arrived with a vengeance.

Q3 2019 earnings, the company's second as a public entity, delivered the shock therapy. Revenue grew 30% to $3.8 billion—impressive for most companies, but disappointing for a supposed hypergrowth story. Worse, losses ballooned to $5.2 billion, though most of that came from stock-based compensation related to the IPO. Even excluding one-time charges, Uber lost $1.2 billion in a single quarter. At this burn rate, the company's $12.7 billion cash pile would last maybe three years.

Khosrowshahi's messaging was relentlessly optimistic, even as investors panicked. "We think 2019 will be our peak investment year," he told analysts, invoking the Amazon comparison yet again. "We've got a runway to get to adjusted EBITDA profitability by the end of 2021." The market wasn't buying it. Unlike Amazon, which had clear unit economics and was investing in infrastructure, Uber was subsidizing every ride to maintain market share against equally subsidized competitors.

The driver classification battle intensified post-IPO. September 2019: California passed AB5, essentially forcing gig companies to classify drivers as employees. The financial implications were catastrophic—adding benefits, unemployment insurance, and overtime would increase costs by 20-30%. Uber, along with Lyft and DoorDash, immediately pledged $90 million to fight the law through a ballot proposition. The company's entire business model was at stake.

Competition wasn't just coming from Lyft anymore. By late 2019, the landscape had fractured. DoorDash was attacking Uber Eats. Amazon was entering food delivery. Waymo was deploying actual self-driving cars in Phoenix. Tesla promised a robotaxi network. Traditional automakers were launching their own mobility services. The moat that Uber had spent billions building was proving to be shallow.

Then came the pandemic. March 2020: Cities locked down globally. Uber's core rides business collapsed overnight—bookings fell 75% in April. The company that had been built on urban density suddenly found its greatest strength had become its greatest vulnerability. In a single quarter, Uber lost 80% of its mobility revenue. The stock crashed to $14, down 70% from its IPO price.

But crisis, as Khosrowshahi knew from his Expedia days during 9/11, created opportunity. With millions stuck at home, food delivery exploded. Uber Eats revenue tripled year-over-year. The company made aggressive moves, acquiring Postmates for $2.65 billion and attempting to buy Grubhub (ultimately losing to Just Eat Takeaway). Within months, Eats had grown from a side business to Uber's primary revenue driver.

The company also made brutal cuts. May 2020: 6,700 employees—25% of the workforce—were laid off via a three-minute Zoom call. Khosrowshahi took no salary for the rest of the year. The company shuttered 45 offices, killed the flying car division, and sold the self-driving unit to Aurora. Every non-essential project was terminated. This wasn't growth mode anymore—it was survival mode.

But something interesting happened as cities reopened. Rides didn't just recover—they exploded. People avoiding public transit chose Uber. Labor shortages meant surge pricing became common. For the first time, the unit economics started working. Q2 2021 brought a revelation: Uber posted its first adjusted EBITDA profit of $509 million. The stock surged past $60, finally exceeding its IPO price two years later.

California's Proposition 22, the ballot measure Uber had spent $200 million supporting, passed with 58% of the vote in November 2020. Drivers would remain independent contractors but with some benefits—a hybrid model that preserved the business model while adding costs. It was expensive but existential. Without it, Uber's entire economics would have collapsed.

The path to actual profitability remained challenging. Q4 2022 saw the company post its first-ever quarterly operating profit of $60 million—twelve years after its founding. But this was through financial engineering as much as operational improvement. The company had shifted costs, cut unprofitable markets, and raised prices. The days of subsidized rides were over.

2023 brought the milestone everyone had been waiting for: full-year operating profitability. Uber posted annual operating profits in 2023, totaling $1.88 billion, after accumulating $31.5 billion in operating losses since 2014. The stock responded, reaching all-time highs above $80. But the celebration was muted. It had taken 14 years, $31 billion in cumulative losses, and the complete transformation of the business model to get there.

The public market journey revealed uncomfortable truths. Uber wasn't the winner-take-all platform investors had imagined. Network effects were local, not global. Switching costs were minimal. The service was largely commoditized. The company succeeded not through monopolistic dominance but through operational excellence, brand power, and sheer scale. It was a good business, maybe even a great one, but it wasn't the world-changing platform that would mint money like Google or Facebook.

By 2024, Uber had evolved into something nobody had predicted: a profitable, mature, diversified logistics company. The revolutionary rhetoric was gone, replaced by discussion of EBITDA margins and free cash flow. The company that had promised to make car ownership obsolete was now focused on delivering burritos profitably. It wasn't the future anyone had imagined, but it was the reality the public markets demanded.

X. Platform Evolution & Diversification

The pivot from "push a button, get a ride" to "push a button, get anything" wasn't strategic foresight—it was desperate necessity. By 2020, Uber had learned a harsh truth: ride-hailing alone would never justify the valuations or generate the returns investors demanded. The future wasn't just about moving people; it was about moving everything.

Uber Eats had started as UberFRESH in 2014, a lunchtime-only service in Santa Monica where meals were pre-loaded in cars and delivered in under ten minutes. It was Travis Kalanick's idea, born from the simple observation that Uber had cars driving around cities all day—why not fill them with food? The initial results were disastrous. Food got cold, orders were wrong, and the economics were even worse than rides. But the kernel of possibility was there.

By 2016, Eats had evolved into its modern form—a three-sided marketplace connecting restaurants, delivery drivers, and customers. The pandemic transformed it from side project to survival mechanism. When rides evaporated in March 2020, Eats exploded. Q2 2020: Eats bookings surpassed mobility for the first time. Suddenly, Uber wasn't a rides company that delivered food; it was a delivery company that also did rides.

The acquisition strategy was aggressive. Postmates for $2.65 billion brought Los Angeles dominance and merchant relationships. The failed Grubhub pursuit would have created a delivery monopoly. Cornershop for $450 million expanded grocery delivery in Latin America. Drizly for $1.1 billion added alcohol delivery. Each acquisition wasn't just about market share—it was about expanding the definition of what Uber could deliver.

The platform logic was compelling. The same drivers, the same app, the same payment infrastructure, the same customer base—but infinite use cases. Uber Connect for package delivery. Uber Health for medical transportation. Uber Direct for merchant delivery. Uber for Business managing corporate logistics. The company was becoming the connective tissue for urban commerce.

Scale advantages were finally materializing. By 2023, 150M monthly active users in 2023 opened the Uber app regularly. The customer acquisition cost, which had been astronomical during the subsidy wars, was now amortized across multiple services. A rider who ordered breakfast through Eats was more likely to take an Uber to work. Cross-selling reduced marketing costs and increased lifetime value.

The freight business, launched in 2017, represented the most ambitious expansion. The US trucking industry was $800 billion—eight times larger than ride-hailing. Uber Freight connected shippers with truckers, solving the same inefficiency problem that plagued passenger transportation. During supply chain chaos of 2021, Freight growing 64% in Q2 2021 as companies desperately sought logistics solutions.

International expansion took a different form post-IPO. Instead of fighting expensive wars, Uber took minority stakes in local champions. $3.1B Careem acquisition opening Middle East gave Uber presence from Morocco to Pakistan. Stakes in Didi (China), Grab (Southeast Asia), and Yandex (Russia) provided exposure to markets Uber could never win outright. The company learned that owning 20% of a profitable monopoly beat owning 100% of a money-losing war.

But the most intriguing evolution was happening beneath the surface—the transformation into an advertising platform. With hundreds of millions of users and detailed behavioral data, Uber could charge restaurants and merchants for promoted placement. By 2023, advertising was generating over $500 million in nearly pure-margin revenue. The company that had started as a marketplace was becoming a media company.

The autonomous vehicle strategy underwent radical surgery. After spending billions developing self-driving technology in-house, Uber sold the division to Aurora for equity in December 2020. The new approach was pragmatic: let others spend the R&D billions while Uber provided the marketplace. Partnerships with Waymo, Motional, and Aurora meant Uber would deploy autonomous vehicles without bearing development costs. The platform would remain valuable regardless of who—or what—was driving.

The super app vision, inspired by China's WeChat and Southeast Asia's Grab, guided product development. One app for all urban needs—transportation, food, groceries, packages, payments. Uber Money launched debit cards and digital wallets. Uber Pass bundled services with subscription benefits. The goal was to become so embedded in daily life that deletion became unthinkable.

By 2024, the platform had evolved beyond recognition from its 2010 origins. Mobility remained the largest business but no longer dominated. Delivery generated 35% of bookings. Freight contributed $7 billion in annual revenue. The company operated in 70 countries, processed over $130 billion in gross bookings, and facilitated over 9 billion trips annually. The numbers were staggering, but more importantly, they were finally profitable.

Yet questions remained about the platform's ultimate potential. Competition in every vertical was intense. DoorDash dominated US food delivery. Amazon threatened everything. New entrants kept emerging, funded by the same venture capital that once powered Uber. The platform had breadth but questionable depth. Users multi-homed across services, showing little loyalty. The network effects that were supposed to create winner-take-all dynamics remained frustratingly local and weak.

The evolution from ride-hailing app to global logistics platform was remarkable but incomplete. Uber had successfully diversified beyond its original business, but hadn't achieved the monopolistic dominance of true platform giants. It was profitable but not wildly so. Growing but not explosively. Valuable but not irreplaceable. The platform had evolved to survive, but whether it could evolve to truly thrive remained the billion-dollar question.

XI. Playbook: Business & Investing Lessons

The Uber story reads like a Harvard Business School case study in everything you should and shouldn't do when building a company. The lessons are profound, contradictory, and uncomfortably revealing about how modern capitalism actually works versus how we pretend it works.

Lesson 1: Blitzscaling is a double-edged sword. Reid Hoffman coined the term, but Uber perfected the practice. The strategy of prioritizing speed over efficiency, of accepting negative unit economics to achieve market dominance, worked—until it didn't. Uber achieved global scale faster than any company in history, but at a cost of $31.5 billion in cumulative losses. The lesson: Blitzscaling can build empires, but it can also build houses of cards. The key is knowing when to shift from growth to profitability before the capital runs out or the market turns.

Lesson 2: Network effects in physical markets are weaker than in digital ones. Every investor presentation claimed powerful network effects—more drivers attract more riders attract more drivers. But unlike Facebook or Google, where network effects are global and switching costs are high, Uber's network effects were hyperlocal and fragile. A rider in SF didn't care how many drivers Uber had in NYC. Both riders and drivers multi-homed across platforms. The moat everyone assumed existed was actually a shallow ditch that competitors could easily cross.

Lesson 3: Regulatory arbitrage is not a sustainable strategy. "Ask forgiveness, not permission" worked brilliantly in the early days. Uber entered markets illegally, built user bases, then used political pressure to force regulatory change. But this approach created lasting enmity with regulators, resulted in billions in fines, and established a corporate reputation that took years and massive investment to repair. The cowboys who built Uber couldn't run it at scale.

Lesson 4: Culture is strategy at scale. The same aggressive, confrontational culture that enabled Uber to bulldoze through taxi cartels also created a toxic internal environment that nearly destroyed the company. "Toe-stepping" and "principled confrontation" sound great in theory but in practice created a Lord of the Flies dynamics where politics trumped performance. The cultural debt accumulated faster than the financial losses and proved harder to restructure.

Lesson 5: Capital is a weapon, not a moat. Uber raised more private capital than any startup in history, using it as a competitive weapon to subsidize rides and destroy competitors. But capital advantage is temporary. Competitors can also raise billions. Customers captured through subsidies show no loyalty when subsidies end. The company that wins on price loses when the money runs out. Sustainable competitive advantage comes from product superiority, operational excellence, or network effects—not from having deeper pockets.

Lesson 6: The true cost of disruption is usually hidden. Uber disrupted the taxi industry, but the real costs were borne by drivers (who absorbed vehicle costs and lacked benefits), cities (who lost tax revenue and faced increased congestion), and investors (who subsidized billions in losses). The $20 Uber ride that replaced a $30 taxi ride wasn't innovation—it was venture capital temporarily repricing reality. True disruption creates value; false disruption just shifts costs to others.

Lesson 7: Founder control is critical until it's catastrophic. Travis Kalanick's iron grip on Uber—through super-voting shares and board control—enabled him to make bold bets and move fast. It also insulated him from accountability when his behavior became destructive. The same structure that enabled hypergrowth also enabled the toxic culture that nearly killed the company. The lesson: Founders need enough control to execute their vision but not so much that they become unaccountable.

Lesson 8: Timing matters more than technology. Uber's technology wasn't revolutionary—it was a dispatch algorithm and payment processor. The revolution was timing: smartphones had achieved critical mass, GPS was ubiquitous, and mobile payments were finally trusted. Had Uber launched three years earlier, it would have failed. Three years later, and someone else would have won. The lesson: Being right about the future isn't enough; you have to be right about when the future arrives.

Lesson 9: Business model innovation beats technical innovation. Uber didn't invent any new technology. They invented a new business model: the asset-light, two-sided marketplace for physical services. This model—now replicated across hundreds of verticals—was more valuable than any algorithm or patent. The company that figures out how humans and money flow through a market usually beats the company with better technology.

Lesson 10: The best investors know when to coup the founder. Benchmark's Bill Gurley made one of the greatest venture investments ever, turning $12 million into $7 billion. But his greatest contribution wasn't capital—it was orchestrating Travis's removal when the founder became a liability. Great investors don't just write checks; they know when to protect the company from its own creator.

Lesson 11: Public markets enforce discipline that private markets ignore. As a private company, Uber could lose billions while claiming future profitability. Public markets demanded actual results. The discipline of quarterly earnings, analyst scrutiny, and daily stock prices forced operational improvements that private board meetings never could. Sometimes the harsh medicine of public accountability is what unicorns need to become real businesses.

Lesson 12: Platform expansion has limits. The "Uber for X" model seemed infinitely extensible—food, packages, freight, healthcare. But each vertical had different economics, different competitive dynamics, different operational requirements. Being great at moving people didn't automatically mean being great at moving everything. Horizontal platform expansion is harder than vertical integration.

The meta-lesson is that building a transformational company requires breaking rules, but building a sustainable company requires following them. Uber succeeded by violating every norm of corporate behavior, then nearly failed for exactly the same reason. The company that emerges from this crucible—profitable, diversified, professionally managed—is successful by conventional metrics but a shadow of its revolutionary promise. Perhaps that's the ultimate lesson: The companies that change the world rarely survive in their original form. Revolution eats its children, even in Silicon Valley.

XII. Bear vs. Bull Case

The Bear Case: A Commodity Business in Disguise

The bears see Uber as the emperor with no clothes—a glorified taxi dispatcher that spent $31 billion to discover it's in a commodity business. Start with the fundamental problem: Uber provides an undifferentiated service. A ride is a ride. Whether the app is pink (Lyft), green (Grab), or black (Uber) matters little when you just need to get from A to B. This isn't like social networks where switching costs are high or search engines where quality differences are massive. It's pure commodity competition.

The moat that investors imagined—network effects, scale advantages, brand power—has proven illusory. Drivers work for multiple platforms simultaneously. Riders have multiple apps installed. Switching costs are zero. Multi-homing is standard. In any given market, Uber faces local competitors who know the terrain better and global competitors with equally deep pockets. The company's pricing power is nonexistent; raise prices 10% and watch users flee to alternatives.

Regulatory risk remains existential. The California AB5 battle was won temporarily through Proposition 22, but the war continues. Massachusetts, New York, and the EU are pushing for driver reclassification. If drivers become employees, Uber's unit economics collapse overnight. Add benefits, payroll taxes, and minimum wage guarantees, and the business model simply doesn't work. The company's entire economics depend on regulatory arbitrage that grows more tenuous each year.

The autonomous vehicle timeline keeps receding. Uber sold its self-driving division and now depends on partners like Waymo and Aurora. But if autonomous vehicles arrive at scale, what value does Uber provide? The companies that own the AVs can create their own networks. Why would Waymo need Uber when it can go direct to consumers? Uber risks being disintermediated by the very technology it claims will save it.

Competition isn't diminishing—it's intensifying. DoorDash dominates US food delivery with superior economics. Amazon is expanding into logistics. Tesla promises a robotaxi network. Every automaker is launching mobility services. Regional players like DiDi, Grab, and Ola dominate their home markets. New entrants keep emerging because the barriers to entry—building an app and recruiting drivers—are minimal. It's a perpetual price war with no end in sight.

The path to profitability required massive price increases and service cuts. The days of subsidized rides are over, but so is growth. Revenue growth is slowing to single digits in mature markets. The company is profitable only by financial engineering—cutting driver incentives, raising take rates, and eliminating unprofitable markets. This isn't sustainable growth; it's harvesting a mature business.

The Bull Case: The Infrastructure Layer for Physical World Commerce

The bulls see Uber as radically undervalued—a logistics platform that's barely scratched its potential. Start with the scale: 150 million monthly active users, presence in 70 countries, processing $130+ billion in gross bookings annually. This isn't a taxi company; it's becoming the transaction layer for the physical world, as essential as payment networks or cloud infrastructure.

Market penetration remains minimal. Even in Uber's most mature markets, ride-hailing represents less than 1% of total miles driven. In San Francisco, Uber's birthplace and most penetrated market, the company has maybe 10% transportation share. Globally, the opportunity is staggering. As urbanization accelerates and car ownership becomes increasingly expensive and impractical, Uber is positioned to capture a massive secular shift in how humans move.