United Airlines Holdings: The Story of America's Aviation Survivor

I. Introduction & Episode Roadmap

Picture this: It's December 9, 2002. In a Chicago courtroom, executives from one of America's most storied airlines stand before a bankruptcy judge. United Airlines—the carrier that pioneered coast-to-coast flights, that flew presidents and celebrities, that once employed 100,000 people—is filing for Chapter 11 protection with $22.8 billion in assets and $21.2 billion in liabilities. It's the largest airline bankruptcy in history.

Fast forward to today. United Airlines Holdings, trading under the ticker UAL on Nasdaq, commands a market capitalization exceeding $35 billion. It's the world's second-largest carrier by passenger traffic, operating nearly 5,000 daily flights to 342 airports across six continents. The airline that nearly died has somehow become stronger than ever.

How did an airline born from airmail routes in 1926 survive bankruptcy, merge with its biggest rival, and emerge as a global aviation powerhouse? How did it navigate the treacherous skies of deregulation, September 11th, the Great Recession, and COVID-19 when so many competitors crashed and burned?

This is the story of survival through crisis—multiple crises, actually. It's about the Continental merger that created a giant but nearly tore the company apart from within. It's about leadership transitions that saved the airline from itself. And ultimately, it's about understanding what makes an airline succeed in an industry where most fail.

We'll trace United's journey from William Boeing's mail routes to Scott Kirby's modern fleet strategy. We'll examine how labor relations can make or break an airline, why network effects matter more than you think, and what happens when you put 80,000 employees in charge of their own company. We'll also dig into the numbers that matter for investors: revenue recovery trajectories, margin structures, and the eternal question of whether airlines can ever generate sustainable returns.

The story of United Airlines isn't just aviation history—it's a masterclass in crisis management, strategic mergers, and the raw determination required to survive in one of capitalism's most brutal industries. Let's begin where it all started: with a man, a plane, and a bag of mail.

II. Origins: Mail Routes to Modern Aviation (1926–1960s)

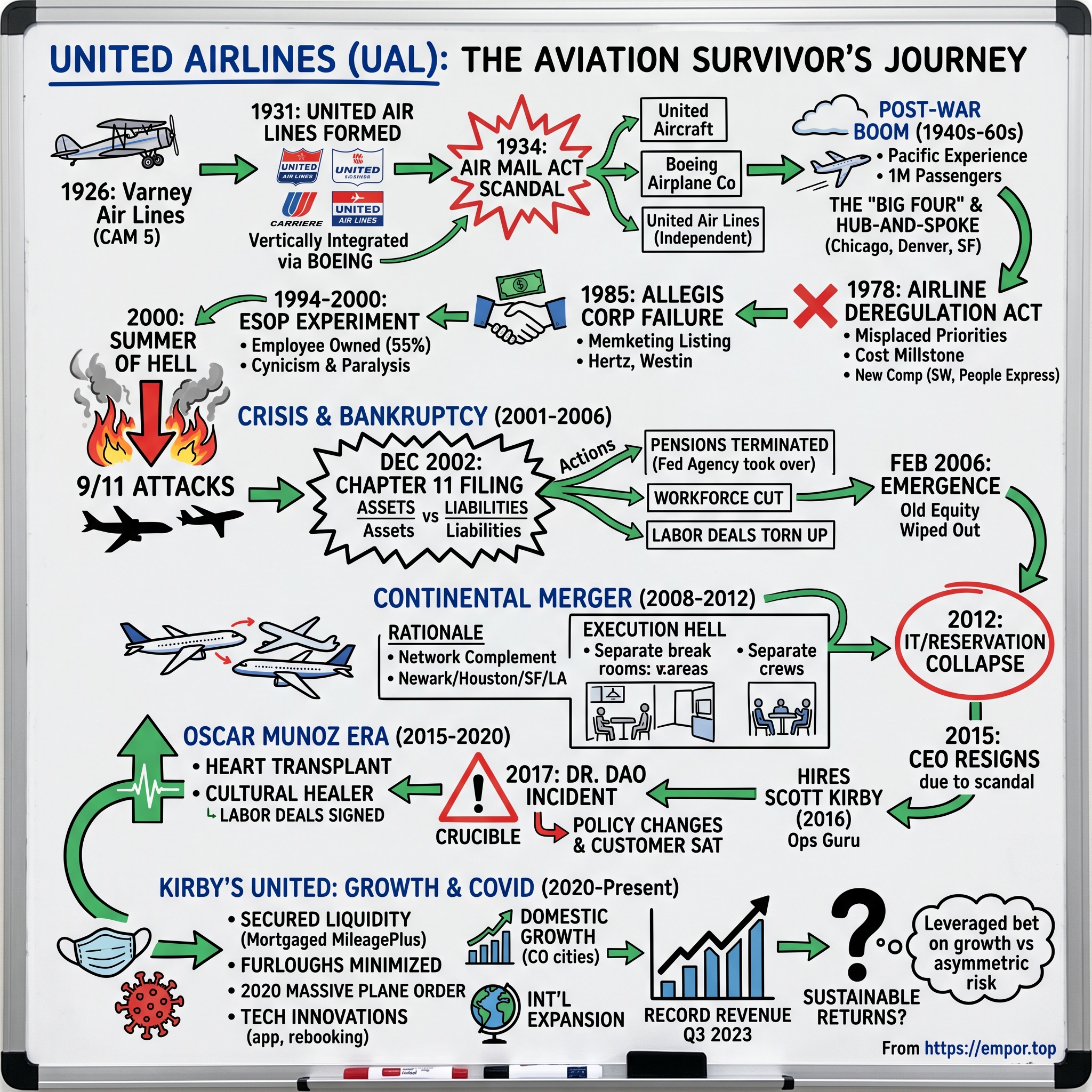

The April morning in 1926 was crisp and clear in Pasco, Washington. Walter Varney, a 37-year-old pilot and entrepreneur, climbed into his Swallow biplane carrying 200 pounds of mail. His destination: Elko, Nevada, some 400 miles away. This wasn't just another flight—it was the inaugural run of Varney Air Lines, Contract Air Mail Route #5. Varney couldn't have known that his modest mail service would evolve into a $35 billion global airline empire.

United's origin story is actually a tale of corporate assembly. In 1929, William Boeing—yes, that Boeing—was building something unprecedented: a vertically integrated aviation conglomerate called United Aircraft and Transport Corporation. He wasn't just making planes; he wanted to control every aspect of aviation from manufacturing to passenger service. Boeing acquired Varney Air Lines along with three other carriers: Boeing Air Transport, Pacific Air Transport, and National Air Transport. On July 1, 1931, these four airlines officially merged to form United Air Lines, a subsidiary of Boeing's empire.

The arrangement was brilliant—until it wasn't. In 1934, a scandal erupted that would reshape American aviation forever. President Franklin D. Roosevelt discovered that major airlines had colluded with the Postmaster General to divvy up lucrative airmail contracts. The Air Mail Act of 1934 broke up the aviation trusts, forcing Boeing's conglomerate to split into three companies: United Aircraft (later United Technologies), Boeing Airplane Company, and United Air Lines as an independent carrier.

Suddenly orphaned from its parent, United needed leadership. Enter William "Pat" Patterson, a former Wells Fargo banker who would run United for the next three decades. Patterson wasn't a pilot or an engineer—he was a businessman who understood that airlines needed to be about more than just flying planes. Under his watch, United introduced the Boeing 247 in 1933, a revolutionary all-metal monoplane that could fly coast-to-coast in under 20 hours with just seven stops. For context, the previous generation of planes took 27 hours with 14 stops. This wasn't incremental improvement; it was transformation.

World War II changed everything. United modified its fleet for military transport, flying supplies across the Pacific and training thousands of pilots for the Army Air Forces. The airline transported 200 million pounds of cargo and flew 50 million miles for the military. When peace returned in 1945, United emerged with invaluable Pacific route experience, a fleet of war-surplus aircraft, and thousands of trained personnel ready for the commercial aviation boom.

The post-war era was golden. Americans who had never flown before were suddenly taking to the skies. United capitalized brilliantly, becoming the first airline to fly one million passengers in a single year (1946) and introducing the Douglas DC-6, which could fly nonstop from coast to coast. By 1951, United was carrying more passengers than any other U.S. airline.

Patterson built United into one of the "Big Four" carriers alongside American, TWA, and Eastern. The route network became United's moat—a hub-and-spoke system centered on Chicago, Denver, and San Francisco that competitors couldn't easily replicate. By the 1960s, United was operating jets like the Boeing 720 and had placed orders for the revolutionary Boeing 747. The airline employed 35,000 people and carried 15 million passengers annually.

But success bred complacency. United had grown fat and happy under the protective umbrella of government regulation. The Civil Aeronautics Board controlled routes, set fares, and essentially guaranteed profits. Competition was genteel—airlines competed on service, not price. Flight attendants served lobster thermidor in first class. Pilots earned doctor-level salaries. Everyone made money.

This cozy arrangement was about to be blown apart. The era of deregulation was coming, and United—like every legacy carrier—was wholly unprepared for the brutal competition that would follow.

III. Deregulation Era & Early Struggles (1970s–1990s)

October 24, 1978. President Jimmy Carter signs the Airline Deregulation Act in the White House Rose Garden. For United Airlines executives watching from Chicago, it might as well have been a declaration of war. The protective walls that had sheltered the industry for forty years came crashing down overnight. Routes were now open to anyone. Prices could be set freely. The game had fundamentally changed.

United's first response was aesthetic—perhaps a telling sign of misplaced priorities. In 1973, just before deregulation hit, the airline had commissioned legendary designer Saul Bass to create a new visual identity. The result was the iconic "tulip" logo—overlapping U-shapes in red, orange, and blue that would grace United planes for the next 37 years. The tagline remained "Fly the Friendly Skies," though those skies were about to become decidedly less friendly.

The immediate post-deregulation years were chaos. Upstart carriers like People Express and Southwest Airlines began cherry-picking United's most profitable routes with rock-bottom fares. United's cost structure—built for a regulated world—was suddenly a millstone. A United pilot earned $150,000 annually while Southwest pilots made $60,000. United flight attendants had contracts guaranteeing specific meal services; Southwest didn't serve meals at all.

By 1985, United CEO Richard Ferris had a radical idea: turn United into a travel conglomerate. He acquired Hertz rental cars and Westin hotels, renaming the parent company Allegis Corporation. The vision was "door-to-door" travel services. Wall Street hated it. Corporate raider Coniston Partners accumulated shares and launched a proxy fight. Within two years, Ferris was out, the acquisitions were unwound, and United was back to just being an airline—but now wounded and distracted.

The labor situation was deteriorating fast. In 1985, United pilots went on strike for 29 days, costing the airline $92 million. Flight attendants, machinists, and pilots were constantly at war with management over pay cuts and work rules. Something had to give.

What happened next was unprecedented in corporate America. In July 1994, United employees agreed to $4.9 billion in wage and benefit concessions in exchange for 55% ownership of the company through an Employee Stock Ownership Plan (ESOP). United became the largest employee-owned company in the world. Pilots and machinists got board seats. The theory was beautiful: aligned incentives would create harmony and prosperity.

Reality was messier. The ESOP created three classes of citizens at United. Pilots and machinists were owner-employees. Flight attendants, who hadn't participated in the buyout, were just employees. Management was caught in between, trying to run an airline where labor literally owned the majority stake. Decision-making became paralyzed. When the airline needed to make strategic investments or tough cost decisions, union board members often blocked them to protect jobs.

Initially, the ESOP appeared successful. United's stock price rose from $97 in 1994 to $280 by 1997. Employees who had traded wages for stock were paper millionaires. The airline launched new international routes and ordered new aircraft. But the structure contained seeds of its own destruction. The ESOP agreement prohibited employees from selling shares until 2000, creating a ticking time bomb.

Then came the Summer of Hell. In 2000, just as the ESOP restrictions were lifting and employees could finally cash out, United's operation imploded. Contract negotiations with pilots had stalled. In response, pilots began refusing overtime and calling in sick en masse—technically legal but operationally devastating. United canceled 24,000 flights during the summer travel season. The brand damage was catastrophic. Passengers fled to competitors.

The dot-com bubble burst added fuel to the fire. Business travel—United's profit engine—evaporated as tech companies slashed travel budgets. Load factors plummeted. The stock price, which had reached $100 in early 2000, fell to $30 by year's end. Employee owners watched their nest eggs vaporize.

By September 2001, United was already in serious trouble. The airline had lost $600 million in the first half of the year. Labor relations were poisonous. The ESOP experiment had failed spectacularly—employees owned the company but couldn't agree on anything. Management was planning major restructuring.

Then, on a clear Tuesday morning, two United Airlines flights—Flight 175 and Flight 93—were hijacked and turned into weapons. The airline industry would never be the same, and United was about to enter the darkest chapter of its 75-year history.

IV. Crisis & Bankruptcy: The Darkest Chapter (2001–2006)

The images are seared into memory: United Flight 175 banking sharply before striking the South Tower at 9:03 AM. United Flight 93's passengers fighting back over Pennsylvania. In those horrific moments, United Airlines became forever linked to September 11th in ways no company would ever want.

The immediate aftermath was operational paralysis. All U.S. flights were grounded for three days. When flying resumed, passengers had vanished. Load factors dropped to 35%. Business travelers—who paid full fare for flexibility—switched to video conferencing. Leisure travelers, terrified of flying, stayed home. In the fourth quarter of 2001 alone, United lost $1.2 billion.

CEO Jim Goodwin, who had taken over in 1999, tried everything. United cut 20,000 jobs, reducing its workforce from 100,000 to 80,000. The airline parked 100 aircraft, eliminated routes, slashed executive pay. But with daily cash burn exceeding $10 million and bookings down 40%, the math was inexorable. United needed either a government bailout beyond the initial Air Transportation Stabilization Board loans, or bankruptcy protection.

In October 2002, Goodwin was forced out. The board brought in Glenn Tilton, an oil executive from Texaco with restructuring experience but zero airline knowledge. Tilton's first day was like drinking from a fire hose—union contracts he didn't understand, route networks that made no sense, a fleet mix that seemed random. But he understood bankruptcy, and that's where United was headed.

On December 9, 2002, UAL Corporation filed for Chapter 11 protection in Chicago. With $22.8 billion in assets and $21.2 billion in liabilities, it was the largest airline bankruptcy in history. Unlike a typical corporate bankruptcy where creditors fight over assets, airline bankruptcies are uniquely complex. Planes can't stop flying—that would destroy all value. Employees must keep working. Customers need confidence to buy tickets months in advance. It's like performing heart surgery while the patient runs a marathon.

Tilton's strategy was brutal but necessary: use bankruptcy to break the constraints killing United. Labor contracts were torn up and renegotiated. Aircraft leases were rejected. Unprofitable routes were eliminated. But the most controversial move involved pensions.

United had $8.3 billion in pension obligations—promises made during better times that were now unbearable. In May 2005, despite fierce union opposition and employee protests, a federal bankruptcy judge approved terminating all four employee pension plans. The Pension Benefit Guaranty Corporation, a federal agency, took over the plans but would only pay benefits up to statutory limits. Pilots expecting $125,000 annual pensions would receive $45,000. It was the largest pension default in U.S. corporate history.

The human toll was devastating. A mechanic with 30 years at United told reporters he'd lost 60% of his expected pension. Pilots who had planned retirements at 60 now flew until 65. The ESOP shares that employees had accepted instead of wages were worthless. Trust between labor and management wasn't just broken—it was incinerated.

The numbers tell the restructuring story: United's workforce shrank from 100,000 pre-9/11 to 62,000 by 2004. Annual costs were cut by $7 billion. The airline negotiated $2.5 billion in annual labor savings. Aircraft count dropped from 600 to 455. But staying in bankruptcy was expensive too—United paid $335 million in professional fees over 38 months, including $260 million to lawyers alone.

By late 2005, oil prices were spiking toward $70 per barrel, adding urgency to exit bankruptcy. Tilton needed to show the court a viable business plan. United's solution was focusing on international routes where competition was less brutal than domestic markets. The airline added flights to China, expanded in Latin America, and leveraged its Pacific network—a legacy from those World War II military routes.

On February 1, 2006, United finally emerged from bankruptcy. The old equity was wiped out—those employee ESOP shares now literally worthless paper. New stock was distributed to creditors. The airline had shed $17 billion in obligations and was technically profitable, though barely. Tilton declared victory, but everyone knew this was just survival, not success.

Almost immediately, Tilton began looking for a merger partner. The bankruptcy had bought time but hadn't solved United's fundamental problem: in a consolidated industry, United was subscale. The airline had survived its near-death experience, but it needed a transformation. That transformation would come through a merger with Continental Airlines—though the integration would prove almost as traumatic as the bankruptcy itself.

V. The Continental Merger: Creating a Giant (2008–2012)

Gordon Bethune sat in his Houston office in early 2008, studying route maps spread across his conference table. The Continental Airlines CEO had transformed his carrier from worst to first, but he knew the industry endgame: consolidate or die. His phone rang. It was Glenn Tilton from United. "Gordon, we need to talk about putting our airlines together."

The courtship between United and Continental had actually begun in 2006, barely months after United's bankruptcy exit. The strategic logic was compelling when you looked at the route maps. Continental dominated the East Coast and Latin America from its Newark and Houston hubs. United controlled the West Coast and Pacific from San Francisco and Los Angeles. Continental had a younger, more fuel-efficient fleet. United had broader international rights. On paper, it was perfect—almost no overlap, pure network expansion.

But timing killed the first attempt. In April 2008, with oil prices spiraling toward $147 per barrel and the financial crisis brewing, both airlines walked away. United turned to US Airways for merger talks instead. Continental flirted with a three-way deal involving United and US Airways. Nothing materialized. Then Lehman Brothers collapsed, credit markets froze, and everyone battened down the hatches for survival.

The financial crisis, paradoxically, made consolidation inevitable. Delta merged with Northwest in 2008, creating the world's largest airline overnight. Southwest acquired AirTran. American would eventually merge with US Airways. The industry was playing musical chairs, and whoever was left standing alone would lose.

On April 16, 2010, Jeff Smisek—who had succeeded Bethune as Continental's CEO—reopened talks with Tilton. This time, both men knew it had to happen. Secret negotiations in hotel suites, code names for Project "Broadway" (United) and "Houston" (Continental), teams of bankers running synergy models. The number crunchers projected $1.2 billion in annual synergies by combining purchasing power, eliminating redundant facilities, and optimizing the network.

May 2, 2010. The boards reached agreement: a $3.2 billion all-stock merger of equals. Except it wasn't really equal. United shareholders would own 55%, Continental 45%. The airline would keep United's name but Continental's livery and logo. Headquarters would be in Chicago, but the operational center would remain in Houston. Smisek would be CEO; Tilton would be non-executive chairman for two years then retire. It was corporate diplomacy at its finest—everyone saved face.

The regulatory approval process was revealing. The Justice Department worried about Newark, where the combined airline would control 73% of slots. United agreed to lease 36 slot pairs to Southwest. Problem solved. The EU wanted guarantees about transatlantic competition. Concessions made. On September 17, 2010, shareholders of both airlines voted overwhelmingly for the merger. The deal closed October 1, 2010, creating the world's largest airline with 87,000 employees, 1,260 aircraft, and 370 destinations.

Then reality hit like turbulence at 30,000 feet.

Merging two airlines isn't like merging two banks where you just combine computer systems. Every detail matters and conflicts. United used Boeing 747s for Pacific routes; Continental preferred Boeing 777s. United's flight attendants served Pepsi; Continental served Coke. United pilots flew Airbus A320s with different cockpit configurations than Continental's Boeing 737s. The reservation systems were incompatible—United used Apollo, Continental used SHARES.

But the real poison was cultural. United employees, brutalized by bankruptcy, were cynical and bitter. Continental employees, proud of their turnaround under Bethune, felt they were being absorbed by an inferior airline. At airports, United and Continental staff literally worked in separate break rooms. Flights were operated separately—a passenger couldn't book a United flight with a Continental crew or vice versa.

The integration disasters mounted. March 3, 2012, was supposed to be a celebration—the day Continental officially became United, marked by the last Continental flight (CO 1267 from Phoenix) landing just before midnight. Instead, that same month, United's attempt to merge reservation systems created a technological catastrophe. The cutover failed spectacularly. Passengers couldn't check in. Flights were delayed for hours. Bags were lost by the thousands. The airline's operation, already fragile from integration stress, collapsed.

Jeff Smisek tried to power through. He painted aircraft in the new livery—Continental's globe logo with United's name. He negotiated joint labor contracts, though it took years. He promised Wall Street the synergies would materialize. But five years after the merger, flight attendants still couldn't work on each other's planes. Pilots remained on separate seniority lists. The IT systems were held together with digital duct tape.

The financial results were damning. While Delta was printing money from its Northwest merger, United was struggling. Customer satisfaction scores were industry-worst. Operational reliability was abysmal. The stock price languished below $40 while Delta soared past $50. The merger of equals had become a case study in how not to integrate airlines.

By 2015, Smisek's problems went beyond integration. Federal prosecutors were investigating whether United had added a money-losing flight from Newark to Columbia, South Carolina—convenient for Port Authority Chairman David Samson's weekend home—in exchange for favorable treatment at Newark Airport. On September 8, 2015, Smisek and two lieutenants resigned immediately. The merger era was over, and United needed someone who could finally heal the wounds that bankruptcy and integration had inflicted.

VI. The Oscar Munoz Era: Cultural Transformation (2015–2020)

Oscar Munoz wasn't supposed to be CEO of United Airlines. The railroad executive from CSX was the board's outside candidate, brought in specifically because he had no airline baggage. On September 8, 2015, the same day Jeff Smisek resigned in disgrace, Munoz was named CEO. His mandate was clear: fix the culture, repair labor relations, and restore United's reputation. Thirty-eight days later, he was fighting for his life.

October 15, 2015. Munoz suffered a massive heart attack while exercising. He was rushed to Northwestern Memorial Hospital where doctors performed emergency surgery. The new CEO who was supposed to save United was now on life support, literally. The board installed General Counsel Brett Hart as acting CEO while Munoz recovered. But recovery wasn't happening—his heart was failing. On January 5, 2016, Munoz underwent a heart transplant. The airline's transformation would have to wait.

When Munoz returned to work in March 2016, he was a changed man—physically fragile but emotionally determined. His near-death experience had given him unusual clarity about what mattered. "I came back with one mission," he told employees. "We're going to make United an airline that employees are proud to work for again."

His approach was radically different from his predecessors. Where Tilton and Smisek had been imperial CEOs, Munoz was approachable. He spent his first months flying around the system, working flights as a baggage handler, sitting in crew break rooms, listening. Flight attendants told him about outdated catering equipment. Pilots complained about scheduling software. Gate agents explained why boarding was chaos. Munoz took notes on everything.

The labor breakthrough came fast. Within four months of returning from his transplant, Munoz had negotiated a five-year contract with flight attendants—ending years of stalemate. By December 2016, all major union groups had new contracts with industry-leading pay raises. The price tag was enormous—labor costs would increase by $3 billion annually. Wall Street was skeptical, but Munoz understood something his predecessors hadn't: you can't run an airline with 90,000 hostile employees.

In August 2016, Munoz made his smartest hire: Scott Kirby from American Airlines as president. Kirby was the operations genius who had made America West and then US Airways work despite their challenges. He was also the architect of American's post-merger success. Kirby immediately began fixing United's operational problems—adjusting schedules to reduce delays, improving aircraft routing, and most importantly, giving front-line employees authority to solve customer problems without calling supervisors.

Then came April 9, 2017—a date that would define Munoz's tenure.

United Express Flight 3411 from Chicago to Louisville needed four seats for crew members who had to position for another flight. Gate agents offered vouchers up to $800. No takers. The flight boarded anyway. Airlines have legal authority to remove passengers from oversold flights, but this wasn't actually oversold—United just needed the seats. Security was called. Dr. David Dao, a 69-year-old physician, refused to leave his seat.

What happened next was captured on passenger smartphones and viewed a billion times within days. Chicago Aviation Security officers dragged Dao down the aisle, his face bloodied from hitting an armrest, other passengers screaming in horror. The videos went viral globally. #BoycottUnited trended. United's stock price dropped $1.4 billion in value. Late-night comedians had a field day. It was a corporate nightmare of unprecedented proportions.

Munoz's initial response made everything worse. His first statement called Dao "disruptive and belligerent." He told employees that crew had "followed established procedures." Only after the full video emerged and public rage intensified did Munoz finally apologize properly, calling the incident "truly horrific" and accepting full responsibility.

The Dao incident became Munoz's crucible. He could have hidden behind lawyers and procedures. Instead, he used it as a catalyst for genuine change. United implemented 10 policy changes within days: passengers would never be removed for crew seating, law enforcement would only be used for safety issues, employees were empowered to offer up to $10,000 in compensation for voluntary bumping. More fundamentally, Munoz tied employee bonuses directly to customer satisfaction scores, not just operational metrics.

The transformation was measurable. United's on-time performance improved from last place to middle of the pack. Customer satisfaction scores rose steadily. Employee engagement surveys showed dramatic improvement. By 2018, United was adding capacity, launching new routes, and generating industry-leading revenue growth. The stock price climbed from $50 to $90.

But Munoz understood his limitations. He had fixed the culture but wasn't an operations expert. As the industry entered a new phase of competition and capacity growth, United needed different leadership. In December 2019, the board announced that Scott Kirby would become CEO in May 2020, with Munoz transitioning to executive chairman.

Nobody knew that within months, a virus spreading in Wuhan, China would create the worst crisis in aviation history. Kirby would inherit not the growing airline Munoz had rebuilt, but a company fighting for survival once again.

VII. Scott Kirby's United: Growth & COVID Response (2020–Present)

Scott Kirby officially became CEO of United Airlines on May 20, 2020. By any measure, it was the worst possible timing. COVID-19 had effectively shut down global aviation. United was burning $40 million in cash daily. Load factors had plummeted to 15%. The TSA was screening 100,000 passengers per day nationwide—down from 2.5 million pre-pandemic. Kirby's first CEO town hall was conducted over Zoom to 90,000 employees, most of whom were wondering if they'd still have jobs.

But Kirby had been preparing for this moment since joining United in 2016. As president under Munoz, he'd already been running day-to-day operations. He knew every route's profitability, every aircraft's configuration, every competitor's weakness. More importantly, he'd been through crisis before—at America West after 9/11, at US Airways during bankruptcy. His playbook was ready.

The first priority was survival—secure liquidity before anything else. Within weeks, Kirby had raised $20 billion through a combination of government CARES Act loans, private capital markets, and aircraft financings. He mortgaged everything—planes, routes, even United's MileagePlus loyalty program, which alone raised $6.8 billion. "We're going to have enough cash to survive even if this lasts two years," he told investors. It was a bold claim when nobody knew if passengers would ever return.

Next came the hard decisions. United cut flight capacity by 90% in April 2020. The airline parked 500 aircraft in desert storage, their windows covered with aluminum foil to protect against sun damage. International routes were suspended. But Kirby made strategic choices within the cuts. He kept cargo operations running—suddenly profitable with passenger planes grounded globally. He maintained skeleton service to key business markets, betting they'd recover first.

The workforce decisions were agonizing. United initially planned to furlough 36,000 employees when CARES Act protections expired. Kirby personally negotiated with unions, ultimately convincing pilots to accept reduced schedules that saved 2,850 jobs. Flight attendants took voluntary leaves. The final furlough number was cut to 13,000—still devastating but far less than initially feared.

While competitors retreated, Kirby saw opportunity. In June 2020, with aircraft values collapsed and manufacturers desperate, United placed a massive order: 270 Boeing 737 MAX and Airbus A321neo aircraft. The timing seemed insane—ordering planes during aviation's worst crisis. But Kirby was playing a longer game. "When demand returns, and it will return, we'll have the most modern, fuel-efficient fleet in America," he explained.

By early 2021, Kirby's domestic strategy was taking shape. Instead of just restoring pre-COVID routes, United would aggressively expand from its hubs—especially Denver, Chicago, and Houston—to secondary cities competitors had ignored. Places like Bozeman, Montana; Charleston, South Carolina; and Pensacola, Florida suddenly had nonstop United flights to multiple hubs. The goal was to capture traffic before it connected through competitor hubs.

The international strategy was even bolder. As countries reopened borders at different speeds, Kirby positioned United to pounce. The airline launched new routes to Tenerife, Palma de Mallorca, Bergen, and Marrakesh—leisure destinations Americans had discovered during COVID. United added more transatlantic flights from Newark than any competitor, becoming the largest airline across the Atlantic by 2023.

The Airbus A321XLR order in late 2023 revealed Kirby's long-term vision. This narrow-body aircraft could fly 4,700 nautical miles—enough to reach Europe from the East Coast or deep into South America. It would open routes too thin for wide-bodies but perfect for United's network strategy. The airline ordered 50 with options for more, planning routes like Newark to Northern Europe that competitors couldn't economically serve.

Technology became another differentiator under Kirby. United's app was rebuilt to handle rebooking during disruptions without calling customer service. The airline introduced ConnectionSaver, which automatically holds connecting flights for delayed passengers. Text messaging replaced gate announcements. These weren't flashy innovations, but they solved real customer pain points.

Employee relations, the foundation Munoz had rebuilt, remained strong under Kirby. In 2023, United pilots received a 40% pay increase over four years—industry-leading but necessary to avoid the disruptions plaguing other carriers. Kirby instituted "core4" metrics—on-time departures, safety, customer satisfaction, and employee engagement—with bonuses tied to all four. The message was clear: operational excellence and employee satisfaction were inseparable.

The financial results validated Kirby's strategy. United generated $12.4 billion in revenue in Q3 2023 alone—a record. Margins expanded despite higher labor costs. The stock price climbed past $50, though still lagging Delta's premium valuation. International revenue grew 30% year-over-year. Corporate travel, while not fully recovered, was returning faster to United than competitors.

But challenges remained. United's debt load from COVID survival stood at $35 billion. Boeing's delivery delays forced constant fleet plan adjustments. Climate regulations in Europe threatened international profitability. Low-cost carriers like Spirit and Frontier continued attacking United's domestic feed. The eternal airline challenge—turning a commodity service into a differentiated product—persisted.

As of early 2025, Kirby's United is a paradox: stronger than before COVID yet still fragile, growing rapidly while managing massive debt, winning back customers while facing intense competition. The airline that emerged from bankruptcy, survived a disastrous merger, and navigated COVID has proven remarkably resilient. Whether that resilience can generate sustainable returns for shareholders remains the billion-dollar question.

VIII. Playbook: Business & Strategic Lessons

The United Airlines story reads like a business school curriculum compressed into a single company. Every major strategic challenge—bankruptcy, mergers, labor relations, crisis management—has been faced and overcome (or sometimes, not overcome). The lessons are worth extracting.

Surviving Existential Crises: Bankruptcy as Reset Button

United's 2002-2006 bankruptcy offers a counterintuitive lesson: sometimes, bankruptcy is the only path to survival. Glenn Tilton used Chapter 11 not just to reduce debt but to fundamentally reset the airline's cost structure. The $8.3 billion pension termination was brutal but necessary—those obligations would have killed United within years. The key was speed and decisiveness. Airlines that lingered in bankruptcy (like Eastern) died. United ripped off the band-aid in 38 months and emerged viable, if wounded.

The COVID response under Kirby was essentially bankruptcy-without-bankruptcy. Raise massive liquidity immediately, cut capacity to match demand, negotiate with labor before crisis deepens. The playbook was similar, but executing outside bankruptcy court meant maintaining stakeholder trust—hence why Kirby communicated constantly with employees and investors during the darkest days.

The Merger Integration Paradox

The Continental merger teaches what not to do. The strategic rationale was sound—complementary networks, minimal overlap, cost synergies. But Smisek focused on the spreadsheet, not the people. Five years post-merger, employees still operated in parallel universes. The IT integration disaster of 2012 happened because nobody wanted to spend money on unsexy backend systems. The lesson: merger math is easy; merger execution is hell.

Contrast this with successful airline mergers like Delta-Northwest. Delta CEO Richard Anderson spent enormous capital on IT integration upfront, standardized fleet types quickly, and most importantly, chose one culture to dominate rather than trying to blend two. United tried to keep everyone happy and ended up with nobody happy.

Labor Relations as Competitive Advantage

The ESOP experiment of 1994-2000 proved employee ownership doesn't automatically align incentives. Giving workers equity without giving them actual decision rights created the worst of both worlds—entitled employees who couldn't actually influence strategy. When the ESOP failed, trust evaporated for a generation.

Munoz understood the inverse lesson: treat employees well not because they're owners, but because they control customer experience. His $3 billion annual labor cost increase looked expensive to Wall Street but was cheap compared to the revenue destruction from unhappy employees. Every airline CEO talks about employees being important; Munoz actually paid them accordingly and gave them decision authority.

Network Effects and Hub Economics

United's hub strategy reveals why airlines aren't just transportation companies—they're network businesses. A hub in Denver doesn't just serve Denver; it connects 200 cities through Denver. Each new spoke route adds value to every other route. This creates winner-take-all dynamics in geography. Once United dominates Chicago O'Hare, competitors can't economically challenge that dominance.

Kirby's post-COVID expansion to secondary cities exploited this dynamic brilliantly. Adding Bozeman-Denver doesn't just capture Bozeman traffic; it feeds United's entire network from Denver. Low-cost carriers can undercut United on point-to-point routes but can't replicate the network value. This is why Spirit and Frontier remain niche despite massive cost advantages.

The Commodity Trap

Airlines sell an undifferentiated product—moving humans from A to B. Attempts at differentiation (better food, wider seats, friendlier service) are instantly copied or deemed too expensive. United's "Friendly Skies" slogan meant nothing when every airline claimed friendly service. The Continental merger's Coke-versus-Pepsi debate captures the absurdity—passengers don't choose airlines based on soft drink selection.

The only sustainable differentiation is network and schedule. Business travelers pay premiums not for better service but for flexibility—multiple daily flights, easy rebooking, global connectivity. This is why United focuses on corporate contracts and loyalty programs. MileagePlus isn't just a marketing program; it's a switching cost that locks in high-value customers.

Government as Silent Partner

Every United crisis involved government intervention. The 1934 Air Mail Act created United by breaking up Boeing's empire. Deregulation in 1978 destroyed United's protected position. Post-9/11 government loans kept United alive long enough to reach bankruptcy. The CARES Act provided $8 billion during COVID. Airlines like to portray themselves as free-market enterprises, but they're really quasi-utilities that governments won't allow to fail en masse.

This creates moral hazard but also opportunity. Kirby's aggressive aircraft orders during COVID assumed government would support aviation recovery. Munoz's labor cost increases assumed regulators would allow industry consolidation to continue. Understanding government's role as both regulator and safety net is crucial for airline strategy.

Leadership During Crisis

United's CEO progression reveals different leadership for different crises. Tilton (restructuring expert) for bankruptcy. Smisek (airline veteran) for merger integration. Munoz (cultural healer) for employee relations. Kirby (operations guru) for competitive growth. Each brought specific skills for specific moments. The board's ability to recognize needed leadership styles—and change CEOs when necessary—saved United multiple times.

The most interesting contrast is Munoz versus Kirby. Munoz's heart transplant gave him unusual empathy and patience for cultural transformation. Kirby's analytical coldness allowed him to make brutal COVID decisions without hesitation. Neither could have done the other's job effectively. Great boards match leaders to moments.

IX. Analysis & Bear vs. Bull Case

Looking at United Airlines today through an investor's lens requires understanding both its remarkable recovery and the structural challenges that persist in the airline industry. The company has transformed from bankruptcy survivor to industry consolidator, yet the fundamental question remains: can airlines ever generate sustainable returns above their cost of capital?

Competitive Positioning in a Consolidated Market

The U.S. airline industry has consolidated into essentially four major players controlling 73% of domestic capacity. American Airlines, Southwest Airlines, Delta Air Lines, and United Airlines collectively account for 73% of total seat capacity in the United States. Within this oligopoly, United sits firmly in second or third position depending on the metric.

American Airlines was the leading airline in the U.S., with a domestic market share of 17.5 percent, closely followed by Delta Airlines, which had a 17.3 percent market share. United typically runs neck-and-neck with these competitors, though recent performance has been mixed. United Airlines provided returns of over 150% to investors last year, significantly outperforming Delta's still-impressive 70% returns.

The competitive dynamics have shifted dramatically post-COVID. Delta maintains its premium positioning through its American Express partnership and superior operational metrics. United under Kirby has focused on aggressive capacity expansion and international growth. American has fallen behind, struggling with network inefficiencies and product quality issues—creating opportunity for United to capture share.

Financial Performance and Metrics

United's recent financial performance shows a business hitting its stride. The company had full-year pre-tax earnings of $4.2 billion, with a pre-tax margin of 7.3%; adjusted pre-tax earnings of $4.6 billion, with an adjusted pre-tax margin of 8.1%. The company also achieved full-year diluted earnings per share of $9.45; adjusted diluted earnings per share of $10.61.

The third quarter 2024 results demonstrated improving fundamentals: The company had pre-tax earnings of $1.3 billion, with a pre-tax margin of 8.7%; adjusted pre-tax earnings of $1.4 billion, with an adjusted pre-tax margin of 9.7%. The company also achieved diluted earnings per share of $2.90; adjusted diluted earnings per share of $3.33.

Cash generation has been robust. In the quarter, the company generated $2.8 billion operating cash flow and free cash flow of $1.5 billion. This cash generation is crucial for managing United's still-elevated debt load from COVID survival financing.

Revenue trends show strength across segments. In the quarter premium revenue was up 10%, corporate revenue was up 7% and revenue from Basic Economy was up 20% year-over-year. The diversification across customer segments—from premium to basic economy—provides resilience against economic cycles.

Major Risks and Structural Challenges

The bear case for United centers on several persistent risks:

Debt Burden: United's adjusted total debt remains elevated at approximately $35 billion following COVID-era survival financing. While manageable in a growth environment, this leverage limits financial flexibility during downturns. Interest expense consumes cash that could otherwise fund growth or return to shareholders.

Fuel Price Volatility: Airlines are essentially leveraged bets on oil prices. Every $1 increase in jet fuel prices costs United hundreds of millions annually. While fuel hedging provides some protection, sustained high oil prices compress margins across the industry.

Labor Cost Inflation: The pilot shortage and strong unions have driven wage inflation well above general inflation rates. United's recent pilot contract included 40% pay increases over four years. With labor representing roughly 30% of costs, these increases directly pressure profitability.

Economic Sensitivity: Airlines are early-cycle businesses—corporate travel evaporates quickly in recessions. United generates significant revenue from business travelers who pay premium fares. A recession would disproportionately impact these high-margin customers.

Climate Regulation: European environmental regulations and potential U.S. carbon pricing could add billions in costs. Sustainable aviation fuel costs 2-3x conventional jet fuel. While necessary for long-term sustainability, the transition will be expensive.

Competition from Low-Cost Carriers: While network effects protect hub dominance, LCCs continue to cherry-pick profitable point-to-point routes. The presence of a nonstop Southwest flight lowers fares along the route by 25%, and even connecting Southwest services lower fares by 7%.

Bull Case: Network Strength and Operational Excellence

The optimistic view focuses on United's strategic positioning:

Network Value: United's hub system creates powerful network effects. Each new route adds value to every other route through connections. The recent expansion to secondary cities from major hubs strengthens this network while avoiding direct LCC competition.

International Expansion: United's Pacific network, dating back to World War II military routes, provides competitive advantage as Asia travel recovers. The transatlantic expansion from Newark has made United the largest carrier across the Atlantic. International routes face less domestic LCC competition and generate higher margins.

Fleet Modernization: The massive aircraft orders during COVID position United with one of the youngest, most fuel-efficient fleets. The Airbus A321XLR order opens new long-haul narrow-body routes competitors can't economically serve. Modern aircraft reduce fuel costs and improve reliability.

Operational Improvements: Under Kirby's leadership, United has dramatically improved operational metrics. On-time performance, customer satisfaction, and employee engagement have all increased. Technology investments in rebooking and customer service reduce friction costs.

Corporate Travel Recovery: While not at pre-COVID levels, business travel is recovering faster at United than competitors. Corporate contracts and loyalty programs create switching costs that protect market share.

The Valuation Question

Market Cap (intraday) 29.346B · Beta (5Y Monthly) 1.42 · PE Ratio (TTM) 9.09 · EPS (TTM) 9.97. At current valuations, United trades at less than 10x earnings—seemingly cheap for a company with improving operations and industry consolidation.

But airline valuations have always been depressed for good reason. The industry has destroyed more capital than it's created over its history. High capital intensity, commodity pricing, external shocks, and powerful suppliers/labor create persistent margin pressure.

The key question isn't whether United can generate profits—clearly it can. It's whether those profits can consistently exceed the cost of capital over a full cycle. History suggests skepticism is warranted.

X. Epilogue & "If We Were CEOs"

Scott Kirby stands at the helm of an airline that has defied death multiple times. United has emerged from bankruptcy, survived a catastrophic merger, navigated COVID, and is now generating record profits. The company had full-year pre-tax earnings of $4.2 billion, with a pre-tax margin of 7.3%—not spectacular by most industry standards, but remarkable for an airline.

If we were running United today, the strategic choices would be fascinating and fraught.

The Premium Paradox

The first decision point: how aggressively to chase premium revenue versus defending market share. Delta has proven that premium positioning works—their American Express partnership alone generates billions in high-margin revenue. United is playing catch-up with new business class seats and Delta One-style lounges. But this requires massive capital investment in aircraft reconfigurations, lounge construction, and service training.

The alternative is competing more directly with low-cost carriers on price. This means densifying aircraft, reducing service, and accepting lower margins in exchange for volume. It's the Southwest model, but Southwest itself is struggling with this approach as costs rise.

Our take: the premium strategy is the only sustainable path. The network carrier model only works with business travelers subsidizing leisure passengers. Without premium revenue, United becomes a high-cost commodity provider—a death sentence in this industry. The investment required is enormous, but the alternative is a race to the bottom United can't win.

Technology as Differentiator

Airlines have historically been technology laggards, running on systems from the 1960s held together with digital duct tape. The Continental merger IT disaster proved how critical—and fragile—these systems are. Today's opportunity is using technology to reduce friction in the travel experience.

United has made progress with ConnectionSaver and automated rebooking, but there's so much more potential. Dynamic pricing that actually reflects willingness to pay. Predictive maintenance that prevents delays before they happen. AI-powered customer service that doesn't require calling an agent. Seamless intermodal connections with ground transportation.

The challenge is that technology investments don't show immediate ROI. They're expensive, risky, and often invisible to customers when working properly. But they're essential for competing with tech-native entrants who will eventually target aviation.

The Sustainability Imperative

Climate change presents both the biggest threat and opportunity for airlines. The threat is obvious: flight shaming, regulatory costs, and eventually carbon pricing that could make flying prohibitively expensive. The opportunity is that the first airline to crack sustainable aviation at scale wins the future.

United has committed to net-zero emissions by 2050, but the path is unclear. Sustainable aviation fuel is expensive and scarce. Electric aircraft are decades away for long-haul routes. Hydrogen requires entirely new infrastructure. Carbon offsets are increasingly seen as greenwashing.

If we were CEO, we'd make a massive bet on one technology—probably sustainable aviation fuel—and vertically integrate. Partner with or acquire SAF producers. Guarantee purchase agreements that enable scaling. Accept lower margins temporarily to drive adoption. It's risky, but waiting for others to solve the problem ensures United becomes a victim of the solution.

Distribution Disruption

The global distribution system (GDS) oligopoly extracts billions from airlines annually. These 1960s-era systems charge airlines for the privilege of distributing their own inventory. It's as if retailers paid shopping malls for each customer who walked through the door.

Direct distribution through airline websites and apps is growing but still represents a minority of bookings. Corporate travel, United's profit engine, flows almost entirely through GDS and travel management companies that take their cut.

The bold move would be following Southwest's playbook from the 1990s—pull inventory from GDS entirely and force customers to book direct. The short-term revenue hit would be devastating, but long-term savings could be transformative. More realistically, we'd gradually shift to dynamic pricing that disadvantages GDS bookings while investing heavily in direct channel user experience.

Labor Relations as Competitive Advantage

Airlines are people businesses pretending to be technology businesses. The pilot flying the plane, the mechanic fixing it, the gate agent boarding it—these humans determine whether United succeeds or fails. Yet airline management has historically treated labor as a cost to minimize rather than an asset to optimize.

Munoz understood this, investing billions in employee satisfaction that paid off in operational improvements. But there's more to do. Profit-sharing that actually motivates. Career paths that retain talent. Technology that makes jobs easier, not obsolete. A culture that empowers front-line decisions.

The radical move would be returning to employee ownership—not the failed ESOP model, but real equity participation that aligns incentives. When a gate agent owns meaningful stock, they think differently about customer service. When pilots are owners, they optimize fuel consumption. It requires dilution and sharing control, but it could create a sustainable competitive advantage no competitor could replicate.

The Ultimate Question

As we consider United's future, the fundamental question persists: should airlines exist as independent companies at all? Or are they better as regulated utilities, government-owned enterprises, or divisions of larger conglomerates?

The industry's history suggests airlines can't generate sustainable excess returns. They're too capital intensive, too sensitive to external shocks, too commoditized. Even in today's consolidated market with disciplined capacity, margins remain single digits. The next recession, terrorist attack, or pandemic will inevitably trigger another crisis.

Perhaps the answer is accepting airlines as market-rate-of-return businesses that provide essential infrastructure. Stop chasing growth. Return cash to shareholders. Maintain steady capacity. Accept modest profitability. It's not exciting, but it might be sustainable.

Scott Kirby wouldn't accept this vision. He's building United to win—expanding internationally, modernizing the fleet, improving operations. The strategy is working today. Whether it works through the next crisis remains to be seen.

The story of United Airlines is ultimately about survival—creative, desperate, remarkable survival against odds that killed dozens of competitors. From mail routes to bankruptcy to COVID, United has endured everything aviation could throw at it. That resilience, more than any strategy or financial metric, might be the best reason to believe United will still be flying when the next crisis hits.

For investors, United represents a complex bet: on industry consolidation holding, on business travel recovering, on management execution continuing, on external shocks remaining manageable. It's not a widow-and-orphan stock. It's a leveraged play on global economic growth with asymmetric downside risk.

But for those who believe in the fundamental human desire to fly—to cross oceans in hours, to connect distant cities, to make the world smaller—United offers exposure to one of civilization's most remarkable achievements. The company that started with a mail plane in 1926 now operates a global network that would seem like magic to those early aviators.

Whether that magic can consistently generate returns above the cost of capital remains aviation's eternal question. United's next century will provide the answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube