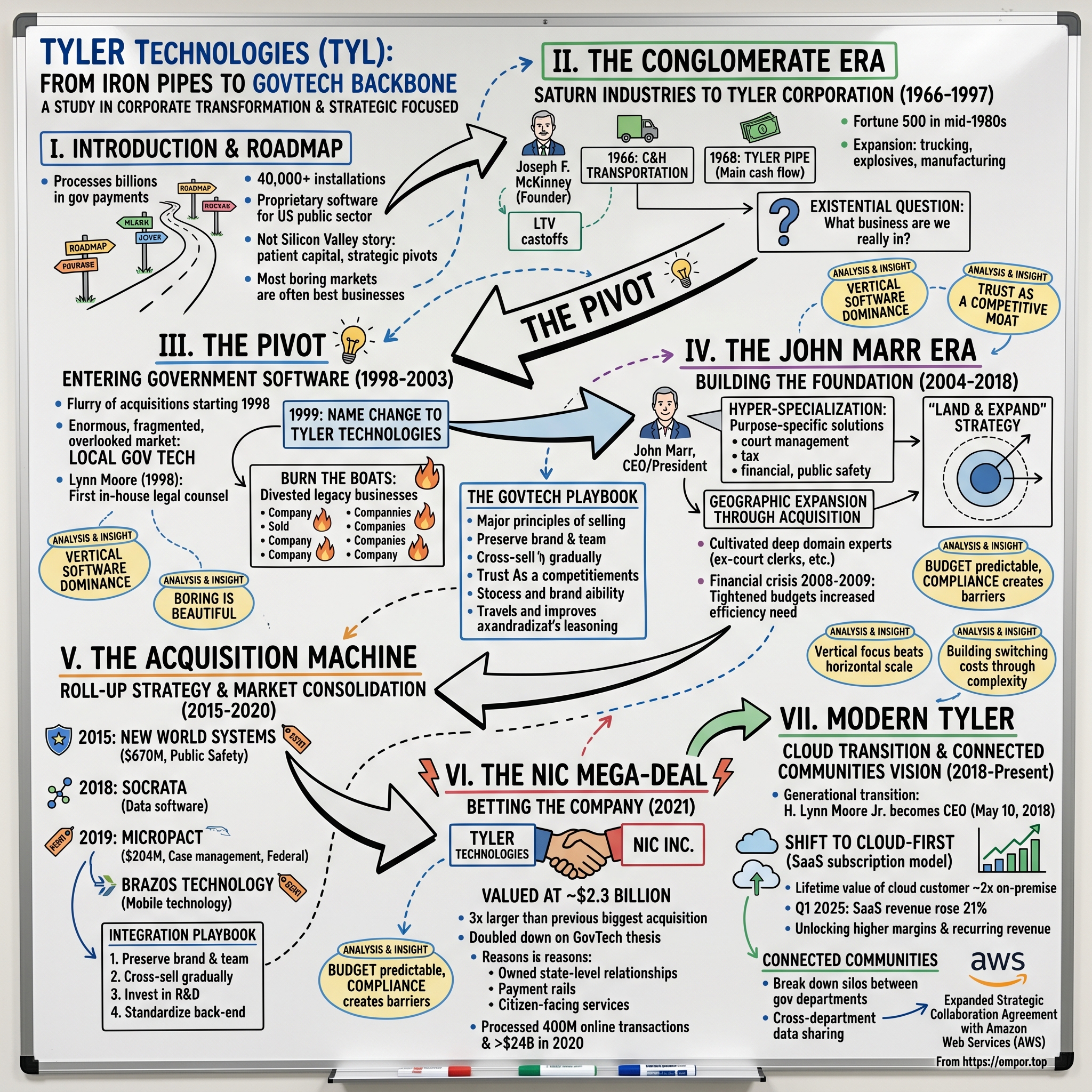

Tyler Technologies: The Unlikely Journey from Iron Pipes to America's GovTech Backbone

I. Introduction & Episode Roadmap

Picture this: A company that started by manufacturing iron pipes in the 1960s now processes billions in government payments and runs the software systems for over 40,000 installations across America's cities, counties, and courthouses. Tyler Technologies, based in Plano, Texas, is a provider of proprietary software to the United States public sector. With annual revenue for 2024 of $2.138B, a 9.53% increase from 2023, Tyler has become the unlikely backbone of American government technology.

The question that should fascinate any student of business history: How does a 1960s industrial conglomerate transform into the dominant force in government software? It's a story that defies conventional Silicon Valley narratives—no Stanford dorm rooms, no venture capital moonshots, no "move fast and break things" ethos. Instead, Tyler's journey is one of patient capital allocation, strategic pivots at precisely the right moments, and the counterintuitive insight that the most boring markets often make the best businesses.

This is the story of how Tyler Technologies went from manufacturing pipes to processing pixels, from industrial conglomerate to software powerhouse, from serving construction sites to serving constituents. It's a masterclass in corporate transformation, strategic focus, and the power of owning a vertical market that everyone else ignores.

What makes Tyler particularly fascinating for investors is its position at the intersection of several powerful trends: the digital transformation of government, the shift to cloud computing, the rise of integrated payment systems, and the increasing demand for data-driven public services. Yet unlike the high-flying tech darlings of the past decade, Tyler has built its empire by being deliberately unsexy—focusing on the mundane but mission-critical systems that keep local governments running.

II. The Conglomerate Era: Saturn Industries to Tyler Corporation (1966–1997)

The year was 1966. Lyndon Johnson was escalating the Vietnam War, The Beatles had just released "Revolver," and in Dallas, Texas, a Harvard-educated businessman named Joseph F. McKinney was about to make a move that would eventually reshape how American governments operate. But he had no idea that was where this story would lead.

Tyler Technologies was founded by Joseph F. McKinney in 1966 as Saturn Industries after buying three government companies from Ling-Temco-Vought. The deal itself was quintessentially 1960s—McKinney was acquiring castoffs from Jimmy Ling's sprawling conglomerate empire. Ling-Temco-Vought (LTV) was the Berkshire Hathaway of its day, if Berkshire had been run by someone with half of Warren Buffett's discipline and twice his appetite for debt-fueled expansion.

Combined, the three LTV companies generated $11 million in sales, the financial foundation upon which Tyler was built. But McKinney had no interest in remaining a government contractor. McKinney quickly sold the three military suppliers, wishing to avoid dependence on one customer (the U.S. government) for his business, and with the proceeds gained from the sale of the former LTV companies he acquired the first of Tyler's numerous businesses, C&H Transportation.

This move revealed McKinney's strategic DNA—he was building for stability, not moonshots. Acquired in 1966, C&H operated as a heavy-freight hauler. Unlike the companies with which McKinney had financially involved himself through Electro-Science, C&H was not a high-risk investment capable of registering either meteoric growth or catastrophic losses.

The defining moment came in 1968. In 1968, the company acquired Tyler Pipe, a manufacturer of iron pipes, which eventually became the company's main source of annual revenue. Tyler Pipe wasn't just another acquisition—it was a workhorse business with predictable cash flows and real assets. In an era when conglomerates were chasing anything that moved, McKinney had found his cash cow.

The company went public quickly. In 1969, Saturn Industries was listed on the New York Stock Exchange. Then, in a move that would prove prescient decades later, in 1970, the company changed its name to Tyler Corporation. The pipe business had become so central to the company's identity that it literally took its name.

For the next three decades, Tyler Corporation embodied the classic American industrial conglomerate playbook. McKinney, who had cut his teeth in venture capital with his Electro-Science Investors fund in the early 1960s, understood both the high-risk world of technology investing and the steady returns of industrial businesses. A Jesuit-educated, Harvard graduate, McKinney earned some of the money he used to start Tyler by recording astounding success with an investment concern he founded with another business partner in 1960. Named Electro-Science Investors, McKinney's venture capital firm invested in high-technology companies that promised high returns, but also represented high risks.

Through the 1970s and 1980s, Tyler Corporation expanded into various industrial sectors—trucking, industrial explosives, manufacturing. By the mid-1980s, it had grown into a Fortune 500 company with over $1 billion in revenue. But as the conglomerate era waned and focused strategies came into vogue, Tyler faced an existential question: What business were they really in?

The answer, surprisingly, would come not from McKinney's industrial empire, but from a completely different direction. The seeds of transformation were being planted in the late 1990s, when personal computers were becoming ubiquitous and even the most tradition-bound institutions—like local governments—were beginning to digitize.

III. The Pivot: Entering Government Software (1998–2003)

The late 1990s were a time of radical transformation in American business. Amazon was still primarily selling books, Google was a startup in a garage, and the dot-com bubble was inflating toward its spectacular burst. Meanwhile, in Texas, Tyler Corporation was about to make one of the most consequential strategic pivots in corporate history—and almost nobody noticed.

Tyler Corporation entered the government software market in 1998. This wasn't a gradual evolution; it was a deliberate, aggressive transformation. In a flurry of acquisitions starting in early 1998, Tyler began to transform itself into a software company with a clear focus on providing systems and services to the public sector.

The timing of this pivot reveals strategic brilliance. While Silicon Valley was chasing consumer eyeballs and B2B software companies were targeting Fortune 500 enterprises, Tyler saw an enormous, fragmented, and completely overlooked market: local government technology. Every county courthouse, every municipal water department, every local tax assessor's office in America was still running on paper or antiquated mainframe systems.

Enter Lynn Moore, a figure who would become central to Tyler's transformation story. He joined Tyler in 1998 as its first in-house legal counsel and was quickly named secretary to Tyler's board of directors. Moore's arrival coincided perfectly with the software pivot, and his legal expertise would prove invaluable in navigating the complex world of government contracts and the intricate acquisition strategy that would follow.

Tyler Corporation changed its name to Tyler Technologies in 1999. This wasn't just cosmetic rebranding—it was a declaration of intent. The company was shedding its industrial conglomerate skin and emerging as a technology company. But unlike the dot-com darlings of the era, Tyler was building for the long haul, targeting customers who moved slowly but, once committed, rarely switched vendors.

The early challenges were immense. Government buyers were notoriously risk-averse, procurement processes could take years, and many potential customers didn't even have IT departments. Tyler's sales team had to be part educator, part consultant, and part therapist—helping government officials understand not just what software could do, but why they needed it in the first place.

In 1997, Tyler decided to shift its focus to information technology. IFS was sold during that year and Forest City was sold in 1999. The company was burning the boats—divesting its legacy businesses to fund the transformation. This wasn't diversification; it was concentration.

By 2003, Tyler had assembled a portfolio of software companies serving various government functions—court systems, tax assessment, financial management. Each acquisition brought not just technology but also deep domain expertise and established customer relationships. The strategy was becoming clear: Tyler wouldn't build one killer app for government; it would build dozens of specialized solutions and integrate them into a comprehensive platform.

The foundation was set, but the real acceleration would come under new leadership. Tyler had successfully pivoted from pipes to pixels, but it would take a new CEO to transform it from a collection of software assets into a unified government technology powerhouse.

IV. The John Marr Era: Building the Foundation (2004–2018)

In July 2004, Tyler Technologies made a leadership change that would define its trajectory for the next decade and a half. Marr became president and CEO of Tyler in 2004, according to the company's website. John S. Marr Jr. wasn't an outsider brought in to shake things up—he was a Tyler veteran who understood both the company's history and its potential.

He was President of Munis from 1994 through July 2004 during which he developed and executed a strategy that transformed Munis from a 35-person local provider of municipal information systems to a 250-employee leader in its market. Marr had already proven he could scale a government software business; now he would do it for the entire company.

Under Marr's leadership, Tyler's strategy crystallized around a simple but powerful insight: local governments were the perfect software customers. They had complex needs, limited alternatives, long decision cycles that discouraged new entrants, and once they committed to a system, switching costs were enormous. This wasn't the "winner-take-all" dynamics of consumer internet companies; it was "winner-take-most" in thousands of micro-markets across America.

The Marr era was characterized by disciplined execution of what would become the Tyler playbook:

Hyper-specialization: Rather than building generic enterprise software and customizing it for government, Tyler built purpose-specific solutions. A court management system designed from the ground up for courts. Tax software that understood the Byzantine complexity of property assessment. Public safety systems that spoke the language of first responders.

Geographic expansion through acquisition: Tyler would identify successful regional players—companies that had built strong solutions for specific government functions but lacked the scale to expand nationally—and acquire them. But unlike typical software rollups that immediately integrated everything, Tyler often kept the brands and teams intact, preserving the domain expertise and customer relationships.

The "land and expand" strategy: Start with one department or function, prove value, then gradually expand to other areas. A city might begin with Tyler's financial system, then add utility billing, then court management, then permitting. Each new module increased switching costs and Tyler's share of wallet.

Patient capital allocation: While Silicon Valley companies were burning cash for growth, Tyler maintained consistent profitability. Marr understood that selling to government meant accepting slower growth in exchange for incredible customer retention and predictable cash flows.

The culture Marr built was distinctly non-Silicon Valley. Tyler's offices weren't filled with ping-pong tables and kombucha on tap. Instead, the company cultivated deep domain experts—former court clerks, ex-city managers, retired police chiefs—who understood their customers' challenges intimately. When a county commissioner called with a problem, they wanted to talk to someone who had walked in their shoes, not a 25-year-old with a computer science degree.

By 2010, six years into Marr's tenure, Tyler had grown revenues to over $300 million. But more importantly, the company had established itself as the trusted partner for thousands of local governments. The network effects were beginning to kick in—when a city manager moved to a new municipality, they often brought Tyler with them. When counties talked at conferences, Tyler's name came up repeatedly.

The financial crisis of 2008-2009 actually strengthened Tyler's position. As government budgets tightened, the need for efficiency increased. Manual processes that were tolerable in good times became untenable when staff was cut by 20%. Tyler's software wasn't just nice to have; it was becoming essential for governments to function with fewer resources.

John Marr's vision and direction as CEO over the past 14 years have built Tyler into the company it is today; a company sharply focused on delivering for all of its constituents - clients, shareholders and employees alike. By 2018, when Marr transitioned to Executive Chairman, Tyler had revenues exceeding $935 million and served over 15,000 installations across the country.

But Marr's greatest contribution might have been preparing his successor. He had been grooming Lynn Moore, who had been with the company since the software pivot began, to take the reins. The transition would prove seamless—and transformative.

V. The Acquisition Machine: Roll-up Strategy & Market Consolidation (2015–2020)

If the Marr era established Tyler as a major player in government software, the period from 2015 to 2020 would see the company transform into an acquisition machine that systematically consolidated the fragmented GovTech market. The all-cash deal values NIC at $2.3 billion, making it the biggest acquisition yet for Tyler, which has purchased at least 13 other government tech firms since 2015.

The acquisition spree began with a bang. Before NIC, Tyler's previous biggest acquisition was its $670 million purchase in 2015 of New World Systems, a publisher of computer-aided dispatch software. New World Systems wasn't just large—it was strategic. The company brought Tyler deep into public safety software, adding computer-aided dispatch and records management systems used by police and fire departments.

What made Tyler's acquisition strategy particularly effective was its patience and discipline. Unlike private equity rollups that slash costs and flip assets, Tyler played a longer game. The company would identify acquisition targets that met specific criteria:

Market leadership in a specific vertical: Tyler didn't buy struggling companies to turn around. It bought successful companies that dominated their niche but lacked the resources to scale nationally.

Cultural fit: The target had to share Tyler's customer-first mentality and commitment to the public sector. Companies that saw government as just another vertical wouldn't make the cut.

Technological compatibility: While Tyler didn't require immediate technical integration, the target's architecture needed to eventually work within Tyler's broader platform vision.

Tyler also made a 2018 deal to buy data software developer Socrata for nearly $150 million, and a 2019 deal to buy case management software vendor MicroPact for $204 million. The Socrata acquisition was particularly revealing of Tyler's strategic evolution. Socrata wasn't traditional enterprise software—it was a data transparency and open data platform that helped governments share information with citizens. Tyler was beginning to see beyond back-office systems to the broader digital transformation of government.

The MicroPact deal in 2019 brought Tyler into federal government for the first time in a meaningful way. MicroPact contributed $63 million to revenues in 2019. While Tyler's bread and butter remained local government, MicroPact's case management and business process automation tools opened doors in federal agencies—a market with different dynamics but enormous potential.

Tyler's acquisition spree took off in 2015 with its absorption of Brazos Technology, a manufacturer of mobile technology used in law enforcement. Each acquisition wasn't just about adding revenue; it was about completing the puzzle. Brazos brought mobile capabilities crucial for modern policing. Socrata added citizen engagement. MicroPact provided federal expertise.

The integration playbook Tyler developed during this period became a competitive advantage in itself:

Preserve the brand and team: Initially, acquired companies continued operating under their original names with their existing teams intact. This maintained customer confidence and prevented talent exodus.

Cross-sell gradually: Rather than immediately forcing customers to adopt the full Tyler suite, the company would patiently introduce complementary products over time. A city using New World's dispatch system might, two years later, add Tyler's records management system.

Invest in the product: Unlike financial buyers who might milk acquisitions for cash flow, Tyler continued investing in R&D for acquired products, often accelerating development that had been constrained by limited resources.

Standardize the back-end: While keeping customer-facing operations stable, Tyler would gradually migrate acquired companies onto common financial, HR, and IT systems, capturing cost synergies without disrupting customer relationships.

By 2020, the Plano, Texas, firm has grown to nearly 5,600 employees and more than $1 billion in annual revenue. But the biggest deal was yet to come—one that would fundamentally reshape Tyler's market position and strategic possibilities.

VI. The NIC Mega-Deal: Betting the Company (2021)

February 10, 2021. As America was still grappling with the COVID-19 pandemic, Tyler Technologies dropped a bombshell that would reshape the government technology landscape: Tyler Technologies, Inc. (NYSE: TYL) and NIC Inc. (NASDAQ: EGOV), jointly announced today that they have entered into a definitive agreement under which Tyler will acquire all outstanding shares of NIC in an all-cash transaction valued at approximately $2.3 billion.

This wasn't just another acquisition—it was a transformative bet that effectively doubled down on Tyler's government technology thesis. To understand the magnitude, consider that this deal was more than three times larger than Tyler's previous biggest acquisition. The company was putting everything on the line.

"We actually internally have had conversations at the highest level about NIC for probably 15-plus years just kind of off and on periodically," said Lynn Moore, Tyler's CEO. This revelation was stunning—Tyler had been circling NIC for more than a decade, waiting for the perfect moment to strike.

"We've watched them in the market, they're obviously a leader in the state public-sector space. A really quality company, quality leadership, a company of integrity. So we've looked at them from time to time, and really I would say going back to the summer is when we started getting really serious."

The strategic logic was compelling. NIC is a leading digital government solutions and payments company, serving more than 7,100 federal, state, and local government agencies across the nation. While Tyler dominated local government, NIC owned state-level relationships. Tyler had the software; NIC had the payment rails. Tyler focused on back-office systems; NIC excelled at citizen-facing services.

In 2020, NIC securely processed 400 million online transactions and more than $24 billion on behalf of government agencies. This wasn't just software—it was critical infrastructure for how citizens interacted with government digitally.

The deal terms revealed Tyler's confidence: NIC stockholders will receive $34.00 per share in cash, which represents a premium of approximately 22% to NIC's 30-day volume weighted average price as of February 9, 2021, and a 14% premium to the closing share price and 52-week closing high of $29.81 on February 9, 2021.

Tyler's financing approach showed both ambition and discipline. Tyler plans to fund the transaction with a combination of approximately $700m of cash on Tyler's balance sheet and new debt. Tyler has obtained financing commitments for a $1.6bn bridge facility and expects to replace the bridge facility with permanent financing prior to closing.

The integration challenges were immense. "They have a few vertical solutions, we obviously have a number of vertical solutions. It's an opportunity where we can get more solutions to government customers." But unlike Tyler's previous acquisitions, which were typically folded into existing divisions, NIC would require a different approach. Its business model—based on transaction fees rather than software licenses—was fundamentally different from Tyler's traditional approach.

The pandemic context made the deal even more significant. "The coronavirus (COVID-19) pandemic has accelerated the shift by governments to online services and electronic payments as more citizens and businesses are interacting digitally with" government. What might have been a five-year digital transformation journey for government was being compressed into months. Tyler was positioning itself to capture this acceleration.

Tyler has completed the previously announced acquisition of NIC, a leading digital government solutions and payments company that serves more than 7,100 federal, state, and local government agencies across the nation. The deal closed in April 2021, just two months after announcement—remarkably fast for a transaction of this size.

Wall Street's reaction was telling. Despite the massive price tag and debt burden, Tyler's stock rose on the announcement. Investors understood what Tyler's management had long believed: the combination of Tyler's local government dominance with NIC's state-level presence and payment capabilities created something approaching a government technology monopoly.

"It expanded (Tyler's) addressable market by giving them a strong presence in the state market, it meaningfully grew their recurring revenues, and it gave them foundational product capabilities (like payments) to build around," he told Government Technology in an email.

The NIC acquisition marked the end of one chapter and the beginning of another. Tyler was no longer just a software company selling to local government—it was becoming the operating system for digital government at all levels.

VII. Modern Tyler: Cloud Transition & Connected Communities Vision (2018–Present)

May 10, 2018, marked a generational transition at Tyler Technologies. H. Lynn Moore Jr. adds CEO to title; John S. Marr Jr. becomes Executive Chairman of the Board. John S. Marr Jr. assumes the role of executive chairman and will continue to serve as the chairman of Tyler's board.

Moore's ascension represented continuity with change. Moore joined Tyler in 1998 as general counsel and was promoted to president in January 2017. He had been with Tyler through the entire software transformation, understanding both its history and its potential future. But Moore brought a different vision—one focused on cloud transformation and what he called "Connected Communities."

The cloud transition was both an enormous opportunity and an existential challenge. Tyler had over 40,000 client installations in over 13,000 locations, the vast majority running on-premise software. Moving these installations to the cloud wasn't just a technical challenge—it was a cultural transformation for both Tyler and its government customers.

Beginning in 2019, the company shifted its approach from "cloud agnostic" to a "cloud-first," with a preference to provide its core products in both an on-premise license model and a cloud-based, or SaaS, subscription model. This wasn't just following Silicon Valley trends—Tyler had discovered something powerful: Tyler estimates that the lifetime value of a cloud customer is almost twice that of an on-premise customer.

The numbers tell the story of this transformation. In Q1 2025, SaaS revenue rose 21% year-over-year to $180.1 million, marking the 17th consecutive quarter of 20%+ growth. This wasn't gradual evolution—it was a rapid migration that defied conventional wisdom about government technology adoption.

By migrating on-premise clients to the cloud—106 flips in Q1 alone—Tyler is unlocking higher margins and recurring revenue. Flips boost contract value by 28% compared to legacy systems, while reducing costs through data center consolidation.

The cloud transition revealed Tyler's competitive moat in stark relief. Competitors couldn't simply offer cloud versions of their software and expect governments to switch. Tyler's customers trusted them with mission-critical systems—court records, tax rolls, police dispatch. The migration had to be seamless, secure, and supported by people who understood government operations.

Moore's "Connected Communities" vision went beyond just moving software to the cloud. He envisioned breaking down the silos that had traditionally separated government departments. A citizen moving to a new city shouldn't have to provide the same information to utilities, tax assessment, courts, and public safety separately. A police officer responding to a call should have access to relevant court records, building permits, and code violations.

Tyler Technologies, Inc. (NYSE: TYL) announced today an expanded eight-year Strategic Collaboration Agreement (SCA) with Amazon Web Services (AWS), with plans to further enable the growing demand for Tyler clients and public sector agencies to move to the cloud. This agreement builds upon Tyler's existing SCA with AWS, which has supported Tyler in evolving its applications in response to public sector needs.

The AWS partnership was crucial. Rather than building its own data centers, Tyler leveraged AWS's infrastructure while focusing on what it did best—understanding and serving government needs. This capital-light approach allowed Tyler to accelerate the cloud transition without massive infrastructure investments.

But 2020 brought an unexpected challenge that would test Tyler's resilience.

VIII. Product & Market Strategy: The GovTech Playbook

Tyler Technologies' product strategy reads like a masterclass in vertical software dominance. The company's public sector software includes eight categories: appraisal and tax software and services, integrated software for courts and justice agencies, data and insights services, enterprise financial software systems, planning/regulatory/maintenance software, public safety software, records/document management software, and transportation software for schools.

Each category represents not just a product line but a deep understanding of how specific government functions operate. Consider the courts and justice vertical—Tyler doesn't just provide case management software; it understands the intricate workflows of criminal cases versus civil litigation, the specific requirements of family courts versus traffic courts, the complex interactions between courts, prosecutors, public defenders, and law enforcement.

This depth creates an almost insurmountable competitive moat. A well-funded startup might build better case management software, but do they understand the specific reporting requirements for federal court statistics? Do they know how to handle the complexity of multi-jurisdictional cases? Can they integrate with the dozens of other systems a court might use? Tyler's two-decade head start in domain expertise can't be replicated with venture capital and engineering talent alone.

The pricing power this creates is remarkable. Government buyers aren't shopping for the cheapest solution—they're shopping for the solution least likely to fail. When a court system goes down, citizens can't access justice. When tax software fails, cities can't collect revenue. When dispatch systems crash, emergency response is compromised. In this context, Tyler's premium pricing isn't a barrier—it's a signal of reliability.

Tyler Technologies has achieved a 20% compound annual growth rate (CAGR) in recurring revenue since 2019, with SaaS revenue growing at 25%. The company aims to migrate 85% of its customer base to the cloud by 2030, expecting a revenue uplift of 1.7x to 1.8x.

The vertical software approach also enables powerful cross-selling dynamics. The average customer at Tyler has two to three products from us and could have eight to 10 products. Each additional product not only increases revenue per customer but dramatically increases switching costs. A city using Tyler for courts, taxes, and utilities would face an enormous project to replace even one component—replacing all three would be almost unthinkable.

The market dynamics of government software create unique advantages:

Budget cycles provide predictability: Government budgets are typically set annually, and software contracts often span multiple years. This creates highly predictable revenue streams unlike the quarterly volatility of consumer software.

Compliance creates barriers: Government software must meet countless federal, state, and local compliance requirements. Each regulation Tyler has learned to navigate becomes a barrier for new entrants.

Network effects within states: When multiple counties in a state use Tyler's tax software, they can share best practices, configurations, and even staff training. This creates powerful regional network effects.

Reference selling dominates: Government buyers rely heavily on references from peer jurisdictions. Every successful Tyler implementation becomes a sales tool for the next prospect.

The strategic positioning Tyler has achieved is remarkable. In many categories, Tyler isn't just the market leader—it's the only viable option for mid-sized governments that need enterprise-grade capabilities but can't afford custom development.

IX. Challenges & Controversies

October 2020. While the world was focused on the pandemic and the upcoming presidential election, Tyler Technologies faced a crisis that threatened to undermine decades of carefully built trust: Tyler Technologies, a Texas-based company that bills itself as the largest provider of software and technology services to the United States public sector, is battling a network intrusion that has disrupted its operations.

The ransomware attack was every government CIO's nightmare come true. Cybersecurity sources familiar with the attack told BleepingComputer that Tyler Technologies suffered an attack by the RansomExx ransomware. For a company that held critical data for thousands of government entities, this wasn't just a business disruption—it was a potential catastrophe.

The Tyler Technologies ransomware attack happened on September 23 when the threat actors breached the network of the company and managed to deploy the malware. In response, the company acted quickly and notified law enforcement, whilst also hiring a forensics firm to investigate the incident and discover the extent of the situation.

The attack revealed uncomfortable truths about the government technology ecosystem. Several readers who work in IT roles at local government systems that rely on Tyler Tech said the outage had disrupted the ability of people to pay their water bills or court payments. When Tyler's systems went down, citizens couldn't interact with their government—a stark reminder of how dependent public services had become on private technology providers.

Perhaps most controversially, Bleeping Computer has reported that Tyler Technologies has finally paid the ransom to the attackers. Tyler Technologies has finally paid the ransom to the attackers. As per their sources, the firm that fall prey to RansomEXX has paid the demanded the ransom to get the decryptor.

Tyler's response was notably opaque. The company maintained that customer data wasn't compromised, but the incident raised serious questions. If Tyler could be breached, what about smaller government technology vendors with fewer resources? The attack highlighted the cybersecurity challenges inherent in the digital transformation of government.

But ransomware wasn't Tyler's only challenge. The company's rapid growth through acquisition and the complexity of government software implementations had led to high-profile failures:

In 2014, people in Marion County, Indiana sued claiming they had been wrongfully jailed. In 2016, public defenders in Alameda County, California found dozens of people wrongfully arrested or wrongfully jailed after switching to Tyler's Odyssey Case Manager software. These weren't just software bugs—they were failures that resulted in wrongful imprisonment, the most serious consequence imaginable for a software error.

An October 2021 report from Lubbock County, Texas, cited problems with Tyler Technologies software there as well as in numerous other jurisdictions. The pattern was concerning: courts and justice agencies would implement Tyler's software, discover serious problems, and then spend years and millions of dollars trying to fix or replace the systems.

The implementation challenges revealed a fundamental tension in Tyler's business model. The company's growth depended on signing new customers and expanding within existing accounts. But government software implementations are notoriously complex, often requiring extensive customization and integration with legacy systems. The pressure to grow could conflict with the need to ensure successful implementations.

A ransomware attack vs. Tyler Technologies ($TYL) caused the government software & IT services provider to lose $1.5 million in services revenue, Tyler discloses. While the financial impact was relatively modest, the reputational damage was harder to quantify. Trust, once broken in the government market, is difficult to rebuild.

The controversies also highlighted the broader challenges of government digital transformation. Unlike private sector companies that can iterate quickly and accept some failure, government systems must work perfectly from day one. Citizens depend on these systems for essential services, and failures can have life-altering consequences.

Yet despite these challenges, Tyler's market position remained strong. The reality was that most government entities had few alternatives. The cost and risk of switching providers, especially after a failed implementation, often meant that governments would work with Tyler to fix problems rather than start over with a new vendor. This customer lock-in was both Tyler's greatest strength and its greatest responsibility.

X. Analysis & Investment Case

The bull case for Tyler Technologies rests on several powerful fundamentals that are rare in the software industry. Start with the numbers: Approximately 85% of Tyler's revenues are recurring, contributing to a nearly 27% free cash flow margin last year. In a world where investors prize predictable revenue streams, Tyler offers something approaching government bond-like certainty with equity-like returns.

The runway for growth remains substantial. Cloud migration is expected to accelerate, with increasing customer transitions through 2027 and 2028. An emphasis on government efficiency could lead to quicker system upgrades. With only a fraction of Tyler's installed base migrated to the cloud, the company has years of built-in growth just from converting existing customers to higher-value SaaS contracts.

The competitive moat appears nearly impregnable. Tyler operates in what Warren Buffett would call a "toll booth" business—once a government implements Tyler's software, the switching costs are so high that Tyler can raise prices consistently while maintaining near-perfect retention rates. The specialized nature of government software, with its complex compliance requirements and mission-critical operations, creates barriers that money alone cannot overcome.

2025 Revenue Guidance: Between $2.30 billion and $2.34 billion. 2025 Non-GAAP EPS Guidance: Between $10.90 and $11.15. The forward guidance suggests management's confidence in continued growth despite macroeconomic uncertainties.

The bear case, however, cannot be ignored. Tyler's valuation assumes flawless execution of its cloud transition while simultaneously integrating the massive NIC acquisition. History shows that technology transitions rarely go smoothly, and the complexity of government software makes mistakes particularly costly.

Cybersecurity remains an existential threat. The 2020 ransomware attack was contained, but a more serious breach could destroy decades of carefully built trust. As government systems become increasingly digital and interconnected, they become more attractive targets for both criminals and nation-state actors. Tyler must invest continuously in security while knowing that it only takes one successful attack to cause catastrophic damage.

The integration complexity of Tyler's acquired products presents ongoing challenges. With dozens of acquisitions over the years, Tyler runs multiple code bases, technologies, and architectures. While this diversity provides breadth, it also creates technical debt that becomes harder to manage over time. The promise of integrated "Connected Communities" requires these disparate systems to work together seamlessly—a technical challenge that many companies have failed to solve.

Government budget pressures could impact growth. Tyler Technologies reports limited impact from government spending fluctuations, with property taxes being the primary revenue source for local governments. While this provides some insulation, a severe recession could force governments to delay technology investments, impacting Tyler's growth trajectory.

The rise of artificial intelligence presents both opportunity and threat. Tyler Technologies plans to integrate AI into all its products this year, focusing on service delivery, decision making, and processing. However, AI could also enable new competitors to build sophisticated government software more quickly, potentially eroding Tyler's domain expertise advantage.

From a valuation perspective, Tyler trades at premium multiples reflecting its market position and growth prospects. The question for investors is whether the company can sustain its growth rates as it becomes larger and faces the law of large numbers. With annual revenue for 2024 of $2.138B, Tyler is no longer a small company that can grow through acquiring smaller competitors—it must increasingly drive organic growth.

The investment case ultimately comes down to a belief in the secular trend of government digital transformation. If you believe that American governments will continue to modernize their technology infrastructure, that citizens will demand better digital services, and that the complexity of government operations requires specialized software providers, then Tyler's dominant position makes it a compelling long-term investment. If you believe that government technology spending will face pressure, that new competitors will emerge, or that Tyler's execution will falter, then the premium valuation leaves little room for error.

XI. Lessons & Playbook Takeaways

Tyler Technologies' journey from industrial conglomerate to software monopoly offers profound lessons that challenge conventional Silicon Valley wisdom. The first and perhaps most important: boring is beautiful. While venture capitalists chased consumer unicorns and enterprise software companies targeted Fortune 500 giants, Tyler methodically built a fortress in the unsexy world of government software. The lesson? The best businesses often hide in markets that seem too small, too slow, or too boring for aggressive competitors.

The power of patient capital allocation runs through Tyler's entire history. From McKinney's original conglomerate building to Moore's current cloud transition, Tyler has consistently chosen long-term value creation over short-term metrics. They've walked away from faster-growing markets to maintain focus, accepted slower initial growth rates to ensure customer success, and invested in acquisitions that took years to fully integrate. In an era of quarterly capitalism, Tyler's decade-long time horizons stand out.

Vertical focus beats horizontal scale. Tyler could have built generic enterprise software and customized it for different industries. Instead, they went deep into government, understanding every quirk, requirement, and workflow. This depth created competitive advantages that broader players couldn't match. When Oracle or SAP occasionally competed for government contracts, they discovered that feature parity wasn't enough—success required speaking the language, understanding the culture, and navigating the unique constraints of public sector.

The acquisition integration playbook Tyler developed deserves study by any company pursuing roll-up strategies. Rather than immediately integrating acquisitions and claiming cost synergies, Tyler played a longer game. Keep the teams, preserve the brands, maintain the customer relationships, then gradually integrate the back-end while cross-selling to expand wallet share. This patient approach preserved value that hasty integration would have destroyed.

Trust as a competitive moat might be Tyler's most underappreciated advantage. In government technology, trust isn't just nice to have—it's everything. Tyler built trust through decades of successful implementations, by hiring people who understood government, by standing behind their products when problems arose. This trust couldn't be bought or built quickly; it had to be earned one customer at a time.

The importance of timing in strategic pivots cannot be overstated. Tyler's move into software in 1998 came at exactly the right moment—late enough that the technology was mature, early enough that the market was still fragmented. Their push to cloud in 2019 similarly hit the sweet spot—just as government buyers were becoming comfortable with SaaS but before competitors could establish strong positions.

Building switching costs through complexity rather than fighting it. Most software companies try to simplify their customers' operations. Tyler embraced the complexity of government, building software that understood every edge case, compliance requirement, and workflow variation. This complexity became a feature, not a bug—it made Tyler's software irreplaceable.

The power of unsexy infrastructure deserves emphasis. Tyler doesn't build the government apps citizens see; they build the systems that make government function. This infrastructure position means they're essential but invisible, embedded but not branded. It's a position that provides pricing power without attracting regulatory scrutiny or competitive attention.

For investors, Tyler demonstrates that growth and profitability aren't mutually exclusive. While Silicon Valley companies burned billions to grow, Tyler maintained consistent profitability while building market dominance. This financial discipline provided the flexibility to make strategic acquisitions without diluting shareholders or taking excessive risk.

Perhaps the most important lesson is about transformation versus disruption. Tyler didn't disrupt government; they transformed it gradually, respectfully, and profitably. They understood that revolution might make headlines, but evolution makes money. In markets where the stakes are high and failure has serious consequences, being a trusted partner beats being a disruptive innovator.

XII. Epilogue: The Future of GovTech

As we look toward the next decade of government technology, Tyler Technologies sits at the intersection of several powerful trends that will reshape how citizens interact with their governments. The question isn't whether government will continue digitizing—it's how fast, and who will capture the value.

Artificial intelligence represents both Tyler's greatest opportunity and its most existential threat. AI integration: Embedding AI into all products by 2025 to automate workflows and improve decision-making, lowering support needs. Tyler's approach—embedding AI into existing workflows rather than replacing them—reflects a deep understanding of government's risk aversion. But AI could also enable new competitors to quickly build domain expertise that took Tyler decades to accumulate.

The post-COVID acceleration of digital government services has permanently changed citizen expectations. People who can renew their passport online wonder why they must visit city hall to pay a parking ticket. This pressure for better digital services plays directly to Tyler's strengths—they have the infrastructure, the relationships, and the trust to deliver transformation at scale.

The cybersecurity imperative will only intensify. As government systems become more interconnected and hold more sensitive data, they become increasingly attractive targets. Tyler's 2020 ransomware attack was a warning shot. The company that can provide both functionality and security will own the market. Tyler's scale provides resources to invest in security that smaller competitors cannot match.

The consolidation of the GovTech market seems inevitable. With Tyler and a few other large players dominating, smaller vendors face a choice: sell to Tyler, compete in ever-smaller niches, or exit the market. This dynamic suggests Tyler's acquisition pipeline will remain robust, though antitrust scrutiny may increase as their market share grows.

The company targets a 10% to 12% CAGR in recurring revenue growth and a 30% plus operating margin by 2030. These targets suggest a maturing company transitioning from growth-at-any-cost to profitable, sustainable expansion.

The Connected Communities vision Moore articulated represents the next frontier. Breaking down silos between government departments, enabling data sharing across jurisdictions, creating seamless citizen experiences across different government touchpoints—this is the promise of digital government. Tyler's broad product portfolio and dominant market position make them uniquely positioned to deliver this integration.

Yet challenges remain. Government moves slowly, budgets are tight, and the complexity of legacy systems creates massive technical debt. Tyler must balance the need for innovation with the reality of serving customers who measure change in decades, not quarters.

The international opportunity remains largely untapped. While Tyler has some presence in Canada and other English-speaking countries, the vast global market for government software remains open. Whether Tyler can successfully export its model to countries with different government structures and regulatory requirements remains to be seen.

The broader question for investors and observers is whether Tyler's dominance is good for government innovation. Does having a near-monopoly provider accelerate transformation by providing standardization and scale? Or does it stifle innovation by reducing competitive pressure? The answer likely depends on whether Tyler continues to invest in innovation or becomes complacent in its dominant position.

As we've seen throughout Tyler's history, the company has consistently defied conventional wisdom. They've proven that boring businesses can generate exceptional returns, that patience beats speed in complex markets, and that transformation beats disruption when the stakes are high. The next chapter of Tyler's story will test whether these principles hold in an era of artificial intelligence, increasing cyber threats, and rapidly evolving citizen expectations.

What started as an industrial conglomerate making iron pipes has evolved into the digital backbone of American government. It's a transformation that would have seemed impossible in 1966, implausible in 1998, and inevitable in hindsight. Tyler Technologies hasn't just adapted to change—they've orchestrated it, one government agency at a time.

The ultimate judgment on Tyler's legacy won't be its stock price or market capitalization. It will be whether they've made government more efficient, more responsive, and more capable of serving citizens. In that sense, Tyler's story isn't just about business transformation—it's about the transformation of how democracy functions in the digital age.

For investors, entrepreneurs, and students of business strategy, Tyler Technologies offers a masterclass in patient value creation. They've shown that the best opportunities often hide in plain sight, in markets others ignore, serving customers others don't understand. They've proven that in business, as in government, evolution beats revolution, trust beats disruption, and sometimes the most profound transformations happen not with a bang, but with a quiet, persistent commitment to solving real problems for real people.

The journey from pipes to pixels is complete. The journey to connecting communities has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube