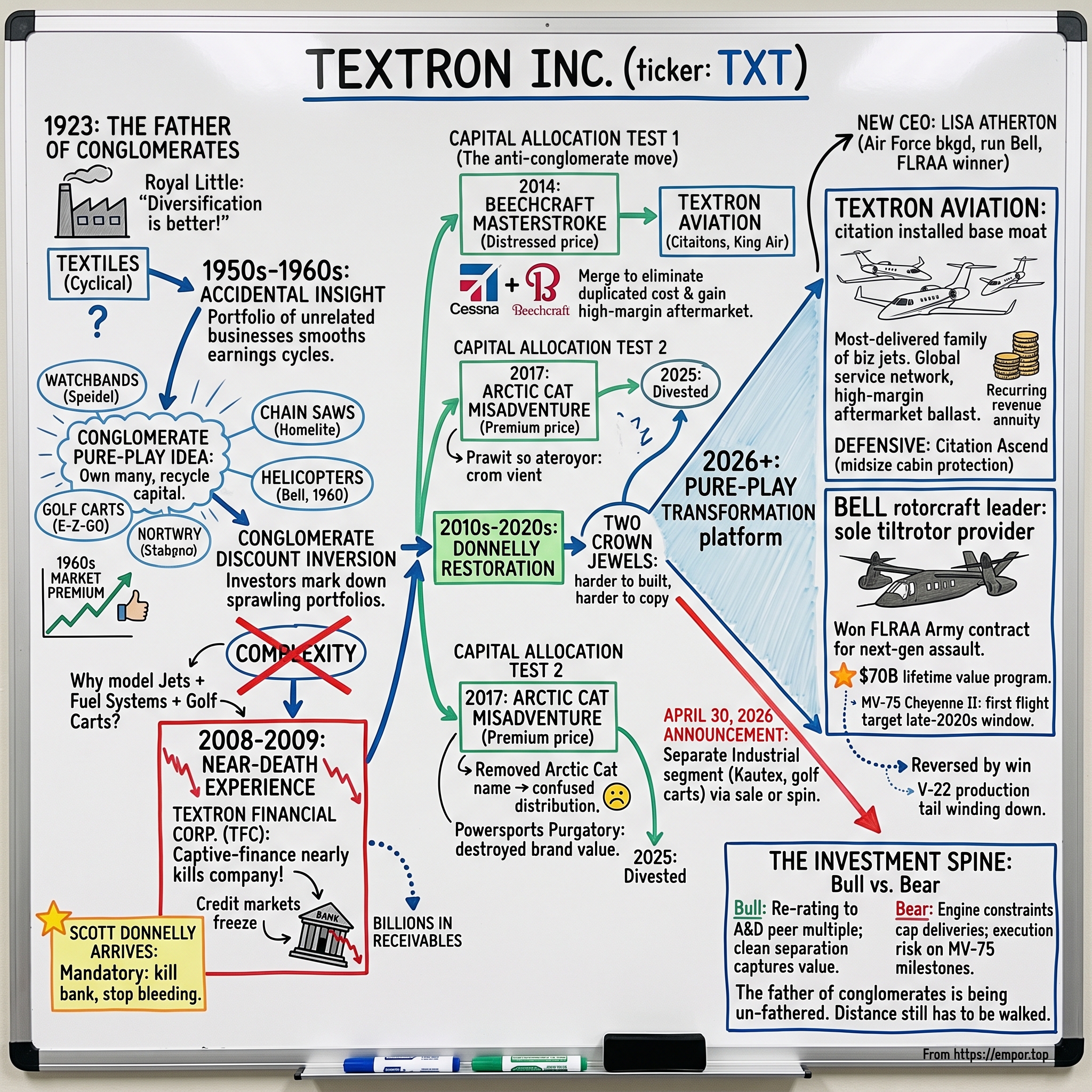

Textron: The Father of Conglomerates and the Pure-Play Transformation

I. Introduction & Episode Roadmap: The 2026 Pure-Play Catalyst

On the morning of April 30, 2026, Textron did something it had spent a hundred years refusing to do: it announced that it wanted to be simpler. Buried inside an otherwise upbeat first-quarter earnings release — revenue up 12% to $3.7 billion, adjusted earnings of $1.45 a share versus $1.28 the year before — was a single paragraph that mattered far more than the beat.1 The company said it intended to separate its Industrial segment, either by selling the businesses outright or spinning them off as a standalone public company, with the whole thing done inside 12 to 18 months. What would be left, management said, is a "pure-play Aerospace & Defense platform" built around three franchises: Textron Aviation, Bell, and Textron Systems.1

For anyone who knows the company's history, this was a genuinely strange sentence. Textron did not stumble into being a conglomerate. It invented the modern conglomerate. The company was the original template — the one that ITT, Litton, Gulf+Western, and eventually Jack Welch's General Electric all studied and copied. The whole intellectual premise of the enterprise, going back to the 1950s, was that owning many unrelated businesses was better than owning a few related ones. And now, in 2026, Textron was formally conceding the opposite: that the market would pay more for the parts than for the whole.

That concession has a name on Wall Street — the "conglomerate discount." For most of the 1960s, diversified holding companies traded at a premium, because investors believed professional managers could allocate capital across industries better than the industries could themselves. Over the following decades the logic inverted. Complexity came to be read as a place where capital goes to hide and underperform, and investors began marking down sprawling portfolios rather than up. Textron spent the 2010s and 2020s wearing that discount, its shares valued below focused aerospace and defense peers despite owning two genuinely world-class assets.

The mechanism of that discount is worth stating plainly, because it is the load-bearing assumption of the entire 2026 strategy. When a defense-and-aviation investor looks at a pure-play like General Dynamics or L3Harris, they can model it cleanly: known end markets, comparable peers, predictable capital needs. When that same investor looks at Textron, they have to underwrite jets and helicopters and plastic fuel systems and golf carts, each with its own cycle, its own competitors, and its own capital hunger. Faced with that analytical friction, the market does what markets do to complexity — it demands a higher return for holding it, which is the same thing as paying a lower price. Textron's bet is that if it removes the pieces that do not belong, the friction disappears and the price rises to meet the peers. It is a clean hypothesis. It is also, as we will see, far from guaranteed.

So the core question of this story is not whether Textron is a good company. It builds Cessna Citations, King Air turboprops, and the tiltrotor that just won the largest U.S. Army aviation contract in a generation. The question is whether a company literally founded on the idea of diversification can credibly reinvent itself as the opposite — a focused defense-and-aviation contractor — and whether a brand-new chief executive, Lisa Atherton, who took the top job on January 4, 2026, can execute a breakup that four decades of predecessors kept postponing.5

To get there, we have to travel across roughly a century of American industrial history. We will start in a Boston textile mill in 1923, where a restless entrepreneur named Royal Little began buying businesses that had nothing to do with yarn. We will walk through the 2008–2009 financial crisis, when a captive-finance arm nearly took the entire company down with it. We will benchmark two acquisitions that sit at opposite ends of the capital-allocation spectrum — the Beechcraft masterstroke of 2014 and the Arctic Cat misadventure of 2017. We will size Bell's crown jewel, a program the Army now calls the MV-75 Cheyenne II, whose lifetime value runs into the tens of billions. And we will end on the live 2026 question: what breaks the pure-play thesis, and what makes it work. Let's begin where the whole idea of "conglomeration" began.

II. The Conglomerate Pioneer: Royal Little & Textron's Genesis (1923–1980s)

Royal Little was not supposed to become a legend of American finance. He was a nephew of the chemist Arthur D. Little, he flunked out of the Massachusetts Institute of Technology, and in 1923 he founded a modest operation in Boston called Special Yarns Corporation. Textiles were, and are, a brutal business: capital-hungry, hyper-cyclical, exposed to fashion and to cheap foreign labor, and cursed with margins that vanish the moment demand softens. Little spent two decades learning that lesson the hard way, watching the same industry boom and bust with the economy.

His insight — the one that would eventually reshape corporate America — was almost accidental. If textiles alone made earnings swing violently, why be only in textiles? Why not own a portfolio of unrelated businesses whose cycles did not line up, so that when one was down another was up, smoothing the whole? And here was the financial trick underneath: Little realized that a company with lumpy but real cash flows could use debt and its own stock as currency to buy other companies, then use their cash flows to buy still more. It was a compounding machine built not on a single product but on the act of acquisition itself.

By the 1950s the renamed Textron had become the textbook definition — quite literally, in the business-school sense — of the diversified conglomerate. Little bought with an omnivorous appetite that today reads like a fever dream: Speidel, which made watchbands and gold-filled jewelry; Homelite, which made chain saws; E-Z-GO, which made golf carts; and, most consequentially, Bell Aerospace in 1960, which brought helicopters into the fold. The connective tissue between a watchband and a helicopter was not industrial logic. It was financial logic. Each business was supposed to throw off cash, require little reinvestment, and hand its surplus up to headquarters, where Little and his successors would redeploy it into the next deal.

This was the playbook that made Textron the intellectual father of a movement. Little's approach — buy cash generators, use leverage, recycle capital, tolerate no sentimental attachment to any single industry — became the blueprint for a whole generation of empire-builders. When people later spoke of Harold Geneen's ITT swallowing hundreds of companies, or of Jack Welch running GE as a portfolio to be pruned and traded, they were describing children of an idea that Royal Little had commercialized first. The conglomerate was, for a moment in the 1960s, the most admired structure in American business, and its shares carried a premium to match.

It is worth pausing on why the premium existed at all, because understanding it explains why it vanished. In the mid-twentieth century, capital markets were far less efficient than they are today. Information about individual companies was scarce, index funds did not exist, and diversifying a portfolio was genuinely hard and expensive for an ordinary investor. A conglomerate solved that problem inside a single stock: buy Textron and you owned a professionally managed basket of businesses whose ups and downs partly offset one another. Managers like Little marketed themselves as superior capital allocators — men who could pull cash out of a mature, slow-growing chainsaw business and pour it into something with a brighter future, all inside the corporate tax shield and without the friction of dividends and re-investment. For a while, investors believed it, and they paid up.

The final irony of Little's career is that he saw the end coming before most. Textron itself was eventually reshaped and pruned, and the raw acquisitive energy of the 1950s gave way, decade by decade, to a company that had to justify why any given business belonged under its roof. The chainsaws, the watchbands, the jewelry — one by one they left. What endured were the pieces with the deepest technological moats and the highest barriers to entry: the aircraft and the helicopters. In a sense, the entire arc from Little to today is the slow discovery that Textron's most valuable businesses were never the ones diversification was supposed to smooth, but the ones that were hardest to build and hardest to copy.

The premium did not last, and the reason it did not last is the quiet thesis of this entire episode. Markets eventually decided that most managers were not, in fact, better at allocating capital across unrelated industries than specialists were within their own. Diversification that was supposed to reduce risk often just reduced transparency, letting weak businesses hide inside strong ones and letting cash get spent on empire rather than returns. The premium became a discount. And Textron, the pioneer, would spend the next half-century as a case study in that inversion — first nearly destroyed by the financial machinery at the heart of the model, then slowly rebuilt around the two aerospace franchises that turned out to be the only pieces truly worth keeping. The near-destruction came first.

III. The Near-Death Experience: Subprime Aerospace and the GFC (2008–2009)

Every conglomerate eventually discovers where its hidden leverage lives. For Textron, it lived in a subsidiary that most investors barely thought about until it nearly killed the company: Textron Financial Corporation.

TFC began innocently enough, as the kind of captive finance arm that lots of industrial companies run. If you make Cessna business jets, it is convenient to also lend customers the money to buy them — financing the sale helps move the product, and the loans earn interest. But over the years TFC drifted far from that modest purpose. It grew into a sprawling finance company writing loans against commercial real estate, distribution finance, golf-course mortgages, timeshares, and other leisure and "asset-based" lending that had nothing to do with airplanes. In effect, a manufacturer of aircraft and golf carts had grown a mid-sized specialty bank on its balance sheet, funded heavily in the short-term commercial paper market.

Then came 2008. When the credit markets froze, the commercial paper that TFC relied on to roll its funding simply stopped rolling. A finance company that borrows short and lends long is only ever as solvent as the market's willingness to keep lending to it, and that willingness evaporated almost overnight. Suddenly Textron — a company most people associated with Cessnas and Bell helicopters — was staring at billions in questionable finance receivables and a funding model that had seized. The manufacturing businesses were fine. The bank bolted onto them was on fire, and the fire threatened everything.

Into that emergency walked Scott Donnelly. He arrived in July 2008 from General Electric, where he had run GE Aviation, joining Textron as executive vice president and chief operating officer — and joining, as it turned out, at almost the exact moment the crisis broke.17 By the time he was elevated to chief executive at the end of 2009, the stock had collapsed from around $60 when he walked in the door to roughly $19.17 That is not a stumble; that is the market pricing in the possibility that the company might not make it.

Donnelly's mandate was blunt: kill the bank, stop the bleeding, and drag Textron back to being a manufacturer. Management moved to exit the vast majority of Textron Financial, running off the non-core portfolios over years and absorbing painful write-downs as loans were liquidated at cents on the dollar. The company slashed its dividend to preserve cash, cut its workforce deeply, and closed facilities as it braced for a long recession in business aviation, where order books were cratering just as the finance mess peaked. It was, in every sense, a corporate near-death experience — the moment the diversification model curdled into concentrated, hidden risk.

The timing could hardly have been crueler, because the two things going wrong were the same thing wearing two masks. The finance arm imploded because credit froze; the aircraft business imploded because the same frozen credit meant no one could finance a new jet, and corporations under pressure do not buy corporate jets. Textron thus took the blow twice — once on the loans it had made, and once on the airplanes it could no longer sell. A truly diversified portfolio is supposed to protect against exactly this: when one business is down, another is up. Instead, in 2008 and 2009, Textron discovered that its "diversification" had a common thread running through it after all, and that thread was access to credit. When it snapped, everything connected to it fell at once.

There is a subtle governance lesson buried here that a skeptical investor should not miss. The finance arm had grown for years, quarter after quarter, contributing earnings that flattered the whole company and made the conglomerate look more profitable than its manufacturing operations alone. Nobody complained while the loans were performing. That is the seductive danger of a captive finance business bolted onto an industrial one: it can manufacture earnings that look like operating profit right up until the cycle turns, at which point it reveals itself as leverage. Donnelly's decision to dismantle it — accepting years of write-downs and a smaller, less impressive-looking company in exchange for durability — was the first genuine act of capital discipline in the modern Textron story, and it set the tone for everything that followed.

What makes this chapter matter for the rest of the story is the lesson Donnelly appears to have drawn from it. The finance arm had been the ultimate expression of Royal Little's original instinct — cash flows bolted onto cash flows, leverage stacked on leverage — and it had nearly destroyed the operating company underneath. The wind-down took most of a decade, but it reoriented Textron's entire strategic compass toward the two things it could actually build better than almost anyone: airplanes and rotorcraft. The rebuilding that followed would be judged not by how many businesses Textron could accumulate, but by how well it could allocate capital inside the ones that mattered. And the defining test of that discipline arrived in the form of a bankrupt competitor.

IV. The Donnelly Restoration: Portfolio Cleanup & The Beechcraft Masterstroke (2010–2016)

By 2013, Scott Donnelly had spent five years playing defense — winding down the finance arm, rebuilding the balance sheet, restoring a company that had come uncomfortably close to the edge. What he wanted was to play offense again. And the target that presented itself was almost poetically convenient: his single largest competitor in general aviation, wounded and available at a discount.

Beechcraft — the maker of the storied King Air turboprop and, through its Hawker line, a fleet of light and midsize business jets — had just emerged from Chapter 11 bankruptcy. Years of debt and a soft post-crisis market had pushed it through restructuring, and it came out the other side smaller, cleaned up, and for sale. For Donnelly, this was the rare chance to buy a direct rival not at a strategic premium but at a distressed valuation. In December 2013, Textron announced it would acquire Beech Holdings for roughly $1.4 billion in cash, and the deal closed on March 14, 2014.78

Consider the price against what it bought. Cessna and Beechcraft together had generated something on the order of $4.6 billion in revenue the year before the deal.7 Textron financed the $1.4 billion with a mix of cash on hand, $600 million of new senior notes, and a $500 million term loan — a very manageable structure for a company its size.8 In other words, Textron paid a modest, distressed multiple to fold in a competitor whose combined product line rivaled its own in scale. That is the kind of setup value investors dream about and rarely find: a big, real business bought cheap because the seller had no choice.

But the price was only half the story. The real prize was structural. Textron combined Cessna and Beechcraft into a single new segment — Textron Aviation — and in doing so it eliminated an entire layer of duplicated cost. Two competitors had been running two corporate overheads, two engineering organizations, two overlapping sales forces, and two service networks to chase the same customers. Merged, they became one. The company could consolidate factory tooling, rationalize the product lineup so its own jets no longer fought each other for the same buyer, and knit together the largest company-owned service footprint in the industry.

The most durable piece of the logic, though, was hiding in the King Air. Beechcraft's turboprop and its enormous installed base came with a high-margin, recurring aftermarket — parts, maintenance, upgrades — that keeps generating cash long after the airplane is sold and largely independent of whether new-jet demand is hot or cold. New aircraft sales are violently cyclical; they collapse in recessions and surge in booms. Aftermarket revenue is the ballast. By absorbing Beechcraft's service annuity, Textron Aviation gained a stabilizer against exactly the kind of business-jet downturn that had helped bankrupt Beechcraft in the first place. It was, in the language of capital allocation, accretive almost immediately and defensive for the long run.

There is also a competitive-dynamics angle that is easy to overlook. When Textron bought Beechcraft, it did not merely add a product line — it removed a rival from the board. In the light and midsize turboprop and jet market, the number of independent players is small, and each one that consolidates changes the balance of pricing power for everyone left standing. By folding a distressed competitor into itself rather than letting it be recapitalized and relaunched by someone else, Textron simultaneously grew its own share and denied that share to a potential new challenger. This is the quiet reason roll-ups in concentrated industries can be so lucrative: the acquirer captures not just the target's revenue, but the competitive breathing room created by the target's disappearance.

None of this was guaranteed to work, and it is worth being fair about the risks Donnelly took. Merging two proud engineering cultures, rationalizing overlapping product lines without alienating loyal owners of both brands, and consolidating factories are exactly the kinds of integration challenges that sink many industrial acquisitions. What made Beechcraft succeed where so many mergers stumble was that the logic was subtractive rather than additive — the value came from removing duplicate cost and reducing competitive overlap, both of which are far more controllable than the revenue synergies acquirers usually over-promise. Management did not have to invent growth; it had to execute discipline, and discipline was the thing this team had just spent five brutal years learning.

Weigh what this decision revealed about management. Donnelly had bought a competitor at a distressed price, integrated it to strip out cost, and used the acquired aftermarket to make the whole segment less cyclical — a near-textbook example of an industrial roll-up done for synergy rather than for size. It was the anti-conglomerate move: not diversification into something unrelated, but consolidation within a business Textron already understood cold. Had the Donnelly era ended there, the capital-allocation record would read cleanly. It did not end there. Three years later, the same management team would apply industrial logic to a consumer business it did not understand at all.

V. Powersports Purgatory: The Arctic Cat Misstep & M&A Benchmark (2017–2024)

If Beechcraft was the deal that showed what Textron did well, Arctic Cat was the deal that showed the limits of the playbook — a reminder that being good at one kind of acquisition does not make you good at all of them.

The thesis had a certain surface plausibility. Textron already owned E-Z-GO, a scaled maker of golf carts and light utility vehicles, sitting inside a division called Textron Specialized Vehicles. Powersports — snowmobiles, all-terrain vehicles, and the fast-growing category of side-by-sides — looked adjacent. Same kind of small combustion engines, same kind of dealer-distributed recreational buyer, same kind of factory. Donnelly's team reasoned that Textron's manufacturing scale and balance sheet could turn a subscale competitor into a profitable powersports platform. In January 2017 Textron agreed to buy Arctic Cat for approximately $247 million in cash, a price that represented a steep roughly 40%-plus premium to where the stock had been trading.9

Then reality asserted itself, and it did so along the exact fault lines that separate industrial products from consumer brands. The first mistake was branding. Textron moved to strip the Arctic Cat name off its ATVs and side-by-sides and sell them instead as "Textron Off Road." For a company steeped in industrial logic — where the corporate parent's name signals quality and scale — this seemed reasonable. For a powersports customer, it was heresy. Arctic Cat was a decades-old enthusiast brand with fiercely loyal riders and dealers; "Textron Off Road" meant nothing to anyone at a snowmobile dealership. The company had erased hard-won brand equity and confused its own distribution channel. By 2019 it reversed course and brought the Arctic Cat name back, but the damage to dealer trust and momentum was done.[^11]

The deeper problem was competitive, and it was one Textron had underestimated. Powersports is dominated by Polaris and by BRP, the maker of Can-Am, two focused companies that live and breathe this market, iterate their product lines aggressively, and command the dealer relationships and the R&D cadence that enthusiasts reward. Textron, running powersports as one line item inside a specialized-vehicles division inside a conglomerate, could not match that intensity. The result was predictable in hindsight: inventory that piled up, discounting that crushed margins, and a business that consumed capital and management attention while returning little of either.

The false premise was the word "adjacent." On a spreadsheet, golf carts and side-by-sides look like cousins — small engines, recreational buyers, dealer distribution. But the thing that actually determines success in enthusiast powersports is not manufacturing scale; it is brand heat, product cadence, and the emotional loyalty of a rider who identifies with a badge. Textron's core competence — building durable, functional industrial products at scale for buyers who care about total cost of ownership — is almost the opposite of what wins in a market driven by passion and identity. E-Z-GO sells to golf courses and resorts that run fleets on economics. Arctic Cat sold to individuals who tattoo the logo on their arm. Applying the fleet-economics mindset to the tattoo customer was the original sin, and no amount of balance-sheet muscle could fix a fundamental misread of what the customer was buying.

There is a useful myth-versus-reality correction here about the whole Donnelly era. The consensus story treats him as a disciplined, aerospace-focused capital allocator, and the Beechcraft deal supports that reading. But Arctic Cat is the reminder that even the disciplined version of Textron retained a residual conglomerate instinct — the belief that management skill is portable across industries, that a good operator can run anything. The market's verdict on that belief, delivered through years of a persistent conglomerate discount, was skeptical. The 2026 breakup is, in effect, management finally agreeing with the market.

Eventually, management did the disciplined thing, even if it took years. Textron wound down its powersports manufacturing and, on April 23, 2025, closed the sale of the business — including the Arctic Cat brand — to a group led by a former Arctic Cat executive tied to the Argo off-road vehicle company.[^11] Roughly eight years after buying in at a premium, Textron sold out of a business it never made work.

Put the two deals side by side and you have the cleanest possible lesson in capital allocation. Beechcraft: a competitor in a business Textron understood, bought at a distressed multiple, integrated for genuine cost and revenue synergies, defensive and accretive. Arctic Cat: a consumer brand in a business Textron did not understand, bought at a premium, mis-integrated in a way that destroyed brand value, and ultimately divested at a loss of time and capital. Same management, same industrial toolkit, opposite outcomes — because the toolkit that consolidates aerospace does not translate to lifestyle brands. That contrast is worth holding onto, because the 2026 breakup is management's argument that it has finally internalized the difference. To judge that argument, we need to understand the crown-jewel businesses Textron is choosing to keep. The larger of the two is Aviation.

VI. Inside the Core: Textron Aviation, Citations, & General Aviation Economics

Walk onto the ramp at almost any business airport in the world and start counting tails, and you will lose track of the Cessna Citations before you finish. The Citation is the most-delivered family of business jets in history — thousands upon thousands of airplanes, a fleet so large it has effectively become the default vocabulary of light and midsize corporate aviation. That installed base is not a vanity statistic. It is the foundation of the entire economic argument for Textron Aviation.

Start with scale. In 2025, Textron Aviation generated roughly $6.0 billion in revenue, up about 13%, with segment profit of $694 million, up 23% — the segment's best year on record.316 It delivered 171 Citation jets and 146 King Air and Caravan turboprops over the year, up from 151 and 127 respectively the year before, and ended 2025 with a backlog of about $7.7 billion.316 Those numbers do more than show a good year. Rising deliveries alongside a backlog that stays large tells you demand is not just present but sustained — customers are ordering faster than the factory can build, which is a healthier problem than the reverse.

Now the strategic geography. Textron does not try to be everything. It owns the light-jet market — the Citation M2, the CJ3, the CJ4 — and it is powerful in the midsize cabin with the Latitude and the long-legged Longitude. What it deliberately cedes is the ultra-long-range, ultra-premium end, the intercontinental cabins where Gulfstream and Bombardier fight over the wealthiest buyers. This is a conscious choice: Textron plays for volume and for the productive, cost-conscious core of the market rather than the trophy top. Its competitive question is not "can we build the world's fanciest jet?" but "can we defend the largest fleet in the world from being displaced?"

The answer to that question rests on two reinforcing advantages. The first is switching costs, and they are more real in aviation than in almost any consumer market. Pilots are certified to fly specific aircraft types; a corporate flight department or a fractional operator like NetJets standardizes on a fleet because commonality across tail numbers means shared training, shared maintenance procedures, and shared spare parts. To move from Citations to a rival platform is to retrain pilots and mechanics and rebuild an entire operational ecosystem — expensive, disruptive, and rarely worth it. The larger the installed base, the deeper that lock-in runs, which is precisely why fleet leadership compounds.

The second advantage is the service network. Textron runs a global web of company-owned service centers, and for an airplane owner, uptime is everything — a jet that cannot fly is a very expensive paperweight. A dense, first-party service footprint means faster parts distribution and higher availability than smaller competitors can economically match, and it generates that high-margin aftermarket cash we met in the Beechcraft chapter. To keep the midsize cabin defended, Textron is rolling out the Citation Ascend — a re-engined, updated aircraft with a flatter floor and improved range aimed squarely at protecting the most profitable slice of the lineup — with certification and first deliveries reached in late 2025.3

It is worth dwelling on why the midsize cabin matters so much to defend, because it is where Textron's economics are richest. The very light jets are a volume game with thinner margins and more price competition from below; the ultra-long-range jets are a different world Textron has chosen not to enter. The midsize segment — the Latitudes and Longitudes and the new Ascend — is the sweet spot where cabin comfort, transcontinental range, and price meet the largest pool of corporate and charter demand, and where an incumbent with the biggest fleet and the best service network can earn genuinely attractive returns. A new product like the Ascend is not a vanity launch; it is a defensive fortification of the most profitable ground Textron holds, timed to keep the midsize buyer from ever having a reason to shop a competitor.

There is a hard constraint pressing on all of this, and management has been candid about it: engines. Textron does not build its own propulsion; it buys from suppliers like Pratt & Whitney, and post-pandemic supply-chain fragility in engines and other components has repeatedly capped how fast the company can convert its backlog into delivered airplanes. On its recent calls, management has framed the bottleneck as a supplier-pacing problem rather than a demand problem — which is a genuinely better position to be in, but also one Textron cannot fully solve on its own.4 The distinction matters for how you read the backlog. A large backlog built on strong demand is an asset; a large backlog that exists only because you cannot build fast enough is a liability dressed as an asset, because it can quietly erode if impatient customers cancel or defer while they wait for engines that never arrive on schedule. So far, Textron's order book has held, but the health of that backlog — not just its size — is one of the few numbers truly worth watching. That dependency is a recurring theme, and it points us straight at the other crown jewel, where the buyer is the U.S. government and the stakes run into the tens of billions.

VII. Bell & The Crown Jewel: The $70B MV-75 Cheyenne II / FLRAA Program

For nearly a decade, the U.S. Army wrestled with a question that would decide the future of one of America's great aerospace names: what replaces the Black Hawk? The UH-60 Black Hawk had been the Army's workhorse assault helicopter since the late 1970s, and by the 2010s the service wanted something transformationally better — an aircraft that could fly roughly twice as fast and twice as far, to matter in the vast distances of the Pacific. The competition to build it, called Future Long-Range Assault Aircraft, or FLRAA, became the most important rotorcraft contest in a generation. For Bell, it was existential.

Bell's answer was the V-280 Valor, and to understand why it was radical you have to understand the tiltrotor. A conventional helicopter's rotors point straight up; they generate lift but limit forward speed. A tiltrotor's engines and rotors swivel — pointing up like a helicopter for vertical takeoff, then tilting forward like an airplane's propellers for fast, efficient cruise. Bell had spent decades mastering this notoriously difficult configuration, most famously on the V-22 Osprey. Its rival, the team of Lockheed Martin's Sikorsky and Boeing, offered the Defiant X, a compound helicopter using coaxial rotors and a pusher propeller — a fundamentally different bet on how to make a helicopter go fast.

In December 2022, the Army chose Bell.[^14] The V-280 Valor beat the Sikorsky-Boeing Defiant X to win FLRAA, a decision that instantly reset Bell's entire military future. The program's ambition is staggering in scale: it is meant to begin replacing an Army fleet of well over 2,000 Black Hawks, and across a multi-decade lifecycle of development, production, and sustainment its total value runs to roughly $70 billion — the number that underpins Bell's long-term outlook. Winning it did not just add a program; it made Bell the sole tiltrotor provider for the Army's next-generation assault fleet.

To grasp why this was existential rather than merely important, remember what Bell was before the win. Its commercial helicopter business is respectable but competes in a crowded field against Airbus Helicopters, Leonardo, and Sikorsky. Its marquee military product, the V-22 Osprey, was a mature program winding down its production tail, with the big procurement years behind it. A defense franchise whose flagship is aging and whose next act is uncertain is a franchise slowly losing relevance. FLRAA reversed that trajectory in a single afternoon. It handed Bell a multi-decade production program at the very moment its previous flagship was fading — the corporate equivalent of landing the lead role in the next franchise just as your last blockbuster leaves theaters. For a business that had spent years being the smaller sibling to Textron Aviation, it was a claim to the future.

The program then moved through its formal milestones. In August 2024 the Army approved Milestone B, authorizing the aircraft to enter the Engineering and Manufacturing Development phase, and Bell was awarded the associated EMD contract — an option worth roughly $3 billion to Bell to design, build, and test the aircraft toward production.1011 The Defense Department designated the prototype in the YMV-75 family, and in stages the aircraft acquired its full identity: the MV-75, formally named the Cheyenne II in April 2026 — "MV" for its multi-mission vertical-lift role, "75" nodding to the Army's 1775 founding, and "Cheyenne II" honoring the Cheyenne people.12 The development timeline targets first flight of the prototype in the late-2020s window, low-rate initial production toward the end of the decade, and fielding in the years after — an aggressive schedule the Army has publicly said it wants to accelerate.12

A word on why the tiltrotor bet is both Bell's moat and its risk, because the two are inseparable. Tiltrotors are hard. They are mechanically complex, they demand exquisite control software to manage the transition between vertical and forward flight, and their most famous predecessor, the V-22 Osprey, endured a long and troubled development with fatal accidents before it matured into a workhorse. That history cuts two ways for Bell. On one hand, it is the source of the cornered resource — the hard-won institutional knowledge that competitors cannot shortcut. On the other, it is a reminder that this class of aircraft has an unforgiving learning curve, and that a program can look triumphant on paper years before it proves itself in the air. The Army chose the harder, faster architecture over the more conventional compound helicopter precisely because it wanted the speed and range only a tiltrotor delivers; in doing so it also accepted the harder engineering path. Bell now has to walk it.

Here is where the investor lens matters, because a giant program win and near-term profits are not the same thing. In 2025, Bell generated about $4.3 billion in revenue, up 20%, but segment profit was $363 million — actually down slightly, by $7 million, from the prior year.3 How can revenue jump 20% while profit falls? Because early-stage development work is front-loaded with cost and thin on margin. The transition into EMD means heavy spending on engineering, tooling, and the "digital engineering" the Army demanded — the modern practice of designing and testing the aircraft in high-fidelity software before bending metal, on the theory that you "go slow to go fast," catching problems in simulation rather than in expensive physical prototypes. That investment compresses Bell's margins now in exchange for a production ramp later. Backlog tells the forward story: Bell ended 2025 at about $7.8 billion, up over $300 million, reflecting growth in both military and commercial work.3

The structure of the contract matters as much as its size, and it deserves a skeptic's attention. Development-phase defense work carries real risk of cost overruns, and how those overruns are shared between contractor and government — the difference between a cost-plus arrangement, where the government absorbs surprises, and a fixed-price one, where the contractor eats them — determines whether a schedule slip is a margin dent or a margin disaster. Bell and the Army have publicly emphasized digital engineering and disciplined risk-reduction precisely to keep the EMD phase from becoming the kind of money pit that has plagued other flagship defense programs. Whether that discipline holds through first flight and into low-rate production is the single most important operational question hanging over the entire "New Textron" thesis, because Bell is the growth engine that is supposed to justify the pure-play re-rating. A stumble here would not just hurt one segment; it would undercut the whole story.

The neutral way to hold Bell, then, is this: the program is real, the win is durable, and the sole-source position is a genuine competitive moat — but the payoff is a decade-long bet whose margins get worse before they get better, and whose value depends entirely on execution against a fixed schedule. First flight and the discipline of the EMD spend are the things to watch, not the headline $70 billion. Before we get to how management is being paid to deliver that, there is a smaller experiment worth sizing — one that shows what Textron does when a bet does not pan out.

VIII. The eAviation Experiment: Sizing the Electric Flight Speculation

Not every Textron bet is a battleship program or a billion-dollar jet franchise. In 2022, the company placed a small, speculative wager on the future of flight: it acquired Pipistrel, a pioneering Slovenian maker of light electric aircraft, and built a standalone reporting segment around it called Textron eAviation.15 The idea was to give Textron a foothold in electric and hybrid-electric aviation — the world of small electric trainers, and further out, the electric vertical-takeoff-and-landing "air taxi" dream that had captivated venture capital.

Giving it its own segment was a statement of intent. It said: this matters enough to show investors separately, to be measured on its own, to be a visible part of the story. And for a few years it was — a way for a legacy airframer to signal that it was not going to be left behind if electric propulsion reshaped the low end of aviation the way many predicted. The move also had a defensive logic. In 2021 and 2022, the eVTOL "air taxi" narrative was near its peak, with well-funded startups going public through blank-check mergers at eye-watering valuations, and there was a real fear among incumbents that a new class of electric aircraft might do to short-haul aviation what electric vehicles were doing to cars. Owning Pipistrel gave Textron a credible seat at that table for a comparatively modest outlay.

Then the numbers did the talking, and they were tiny. Textron eAviation ran at a scale that barely registered against a company doing nearly $15 billion in revenue — the segment produced only single-digit millions of dollars of revenue per quarter while posting steady operating losses, on the order of $15 million to $17 million a quarter, adding up to a full-year revenue figure in the low tens of millions against a loss in the neighborhood of $60 million-plus.15 In plain terms: it was burning meaningfully more cash than it brought in, with no near-term path to changing that, because commercial electric aviation remains capital-intensive, heavily dependent on regulatory certification, and years from real volume.

So one of Lisa Atherton's first moves as chief executive was to quietly dismantle the experiment as a standalone entity. Effective at the start of Textron's 2026 fiscal year — the very beginning of January 2026 — the eAviation segment was eliminated as a separate reporting line, with Pipistrel and the commercial electric platforms folded into Textron Aviation and the relevant unmanned and military-adjacent work absorbed elsewhere in the company.15

Read the right lesson here, because it is easy to read the wrong one. This was not Textron abandoning electric flight; the technology and the products continue inside Aviation. It was Textron declining to keep funding electric flight as a separate public segment that put a spotlight on losses without a commercial thesis to justify them. The message — consistent with the discipline the Beechcraft-versus-Arctic-Cat contrast implies management is trying to enforce — is that speculative technology belongs tucked inside a cash-generating business that can afford to nurture it patiently, not carved out as its own money-losing line. It was a small decision, but a revealing one about how the new CEO thinks. And thinking about the new CEO is where the story now lives.

IX. The Lisa Atherton Era: Carving Out Industrial & Management Alignment (Today)

On October 22, 2025, Textron's board named the person who would inherit Royal Little's hundred-year-old machine — and, it turned out, dismantle a large part of it. Lisa Atherton was appointed president and chief executive officer effective January 4, 2026, succeeding Scott Donnelly, who moved up to executive chairman.5 The handoff was not a rupture; Donnelly stayed on, and Atherton was very much an inside candidate. But her background made her a distinctive choice to lead a company pivoting toward pure-play defense.

Atherton is not a finance executive who wandered into aerospace. She is a graduate of the U.S. Air Force Academy — where she earned a degree in legal studies — served as a contracting officer in the Air Force, and spent eight years at Air Combat Command shaping requirements and budgets for the combat air forces before earning an MBA from William & Mary.[^6]6 She joined Textron in 2007, rose to run Textron Systems as its president and CEO in 2017, and then took over Bell — first as chief operating officer, then as president and CEO from April 2023 — where she was steering the FLRAA win into development.[^6] In other words, the person now leading the A&D transformation spent her career on the government side of the business and then ran the crown-jewel defense franchise. That is a deliberate signal about where the new Textron intends to point.

Which brings us to the bombshell she delivered barely four months into the job. Alongside first-quarter 2026 results on April 30, Atherton announced the intent to separate the Industrial segment — the collection of businesses that has long dragged on Textron's blended returns — within 12 to 18 months, via either a sale or a tax-free spin-off.12 Industrial is where Kautex, which makes plastic fuel systems for automakers, sits alongside Textron Specialized Vehicles and its golf carts and utility vehicles. These are decent businesses, but they are lower-margin, more cyclical in a consumer-and-auto way, and structurally different from aerospace and defense. Carving them out is the literal act of shedding the conglomerate.

On the Q1 call, analysts pushed on the mechanics, and the pushback was substantive.1 The first question was sale versus spin: a clean sale delivers cash to redeploy but crystallizes taxes and depends on a willing buyer at a good price, while a tax-free spin hands shareholders stock in a standalone company but leaves them holding the very Industrial exposure the market discounts. The second, sharper question was "stranded costs" — the centralized corporate overhead currently carried in part by Industrial, which does not vanish when Industrial leaves. If those costs strand on the remaining A&D company, the margin uplift from going pure-play is smaller than the headline suggests. Atherton's framing was that the separation creates a cleaner, higher-multiple "New Textron," but a skeptical investor is right to withhold judgment until the structure, the buyer or spin terms, and the stranded-cost math are actually on the table. Announcing a breakup is easy; capturing value from one is where these things succeed or fail.

It is fair to ask the harder governance question too: why now, and why not sooner? Kautex and the specialized-vehicles businesses have been structurally lower-margin and strategically orphaned for years — arguably since long before the Arctic Cat episode made the mismatch impossible to ignore. An activist would note that the breakup arriving within months of a CEO transition is not a coincidence; new leaders have the political capital to do the unsentimental things their predecessors avoided, and a fresh chief executive gets to be the one who unlocks value rather than the one who let it sit trapped. That does not make the move wrong — on the contrary, it is probably overdue — but it does invite scrutiny of what else, culturally, a century-old conglomerate has been slow to confront, and whether the discipline now on display is durable or merely the honeymoon energy of a new administration.

The more concrete way to test management's credibility is to look at how it is paid, because incentives reveal priorities better than press releases. Textron's long-term executive compensation is built on performance share units tied to three metrics: average return on invested capital, weighted at 50%; cumulative manufacturing cash flow, weighted at 30%; and total shareholder return relative to the S&P 500, weighted at 20%.13 This is a genuinely shareholder-friendly design — it puts capital efficiency and cash generation at the center, exactly the disciplines a former conglomerate needs. And the plan has teeth in both directions: the 2022–2024 award paid out at 122.3% of target, with ROIC and cash flow above target but relative TSR below target, meaning the stock's underperformance versus the market actually docked the payout.13 Management does not get full credit simply for operating well if the shares lag.

For 2026, the company has continued to evolve that framework, layering in operational-efficiency emphasis — including incentives around adopting AI and modern engineering tools — while retiring standalone ESG targets, per its latest proxy disclosures.14 The through-line worth holding is that pay is anchored to ROIC and cash, not to revenue or empire size — a structural rebuke of the conglomerate instinct. On capital return, Textron has been a consistent and aggressive repurchaser of its own stock, buying back on the order of a billion dollars-plus of shares annually in recent years, and management has signaled that proceeds from the Industrial separation would feed that buyback machine.3

But buybacks deserve a colder look than they usually get, because they are the place where a "disciplined" narrative most easily slips. Repurchasing shares creates value only when the stock is bought below its intrinsic worth; done indiscriminately, it merely offsets dilution or flatters per-share earnings while quietly consuming cash that might have earned more elsewhere. A company that trades at a conglomerate discount can make a genuinely good case that its own shares are cheap — that is the bullish reading of years of heavy repurchases. But the same company, if it overpays for its stock or uses buybacks to mask a lack of better ideas, is destroying value in a way that is easy to hide. The honest verdict is that Textron's repurchase record can only be judged against the prices paid and against what Industrial ultimately fetches — the two numbers that will show whether the capital discipline in the pay plan is real behavior or just a slide in a proxy. To weigh the whole enterprise, it helps to put it through a more formal strategic lens.

X. Playbook & Strategic Analysis: 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold strategic question: what, exactly, protects Textron's profits from competition? Hamilton Helmer's "7 Powers" framework is a useful scalpel here, because it forces you to name the specific mechanism rather than wave at "great products."

The clearest power is switching costs, and it lives in Aviation. We have already seen the mechanism — type ratings, fleet commonality, standardized training and maintenance — but the strategic point is that it is self-reinforcing. Every additional Citation delivered deepens the pool of pilots and mechanics trained on the platform and enlarges the parts ecosystem, which makes the next customer's decision to standardize on Cessna easier and a rival's job of dislodging them harder. This is a real, durable moat, though it is worth being honest that it protects the installed base more than it guarantees new sales, which still have to be won on price, product, and delivery against Embraer, Bombardier, and others.

The second power is a cornered resource, and it lives in Bell. Tiltrotor mastery — the accumulated engineering knowledge of building aircraft whose rotors tilt, refined over decades from the Osprey to the V-280 — is not something a competitor can simply hire or buy its way into on a program timeline. Sikorsky and Boeing bet on a different architecture and lost the FLRAA competition; that outcome left Bell as the sole tiltrotor provider for the Army's next assault aircraft. A sole-source position on a multi-decade government program is about as strong as competitive protection gets — with the important caveat that the "resource" is only as valuable as Bell's ability to execute the program, and government monopsony power sits on the other side of the table.

The third power is scale economies, and it is more moderate. Textron Aviation's global first-party service network spreads fixed costs — parts distribution, tooling, maintenance infrastructure — across the largest fleet in its categories, lowering per-aircraft cost in a way boutique competitors cannot match. It is a genuine advantage, but a bounded one; Gulfstream and Bombardier also run large networks, so scale is an edge over the small players more than over the giants.

Now run Porter's Five Forces over the "New Textron" as a pure-play A&D company, and the picture is favorable but not without pressure points. The threat of new entrants is very low — the certification barriers, capital intensity, and multi-decade customer relationships in both business aviation and military procurement are close to prohibitive. The bargaining power of buyers is mixed: the U.S. government is a powerful single buyer that can delay, restructure, or stretch programs to suit its budget, while on the commercial side large fractional operators depend on Cessna's light-to-midsize capacity in a way that balances the relationship somewhat. Rivalry is intense but structured — a handful of well-capitalized players who compete hard but rationally rather than destructively.

The force that bites hardest is the bargaining power of suppliers, and we have already met it: the engine makers. Propulsion for both jets and rotorcraft comes from a small number of suppliers — Pratt & Whitney, Honeywell, and their peers — who effectively set the pace at which Textron can deliver finished aircraft. When engines are short, Textron's backlog cannot convert to revenue no matter how strong demand is. That is a structural vulnerability no amount of moat elsewhere fully offsets, and it is the single supplier-side risk most worth watching. Substitutes, meanwhile, are a distant concern — nothing replaces a business jet or an assault tiltrotor in the relevant time horizon.

Stepping back from the frameworks, the honest synthesis is that Textron's moats are real but asymmetric across its two crown jewels. Aviation's advantage is broad and shallow-to-medium — a durable installed-base lock-in that protects a large, cyclical, competitive business but does not confer pricing dominance. Bell's advantage is narrow and deep — a near-absolute position on a single program, worth enormous value but concentrated in one customer and one execution path. A pure-play Textron is therefore a barbell: a stable, service-annuity aviation franchise on one end, and a high-variance, high-reward defense bet on the other, joined mainly by the fact that both make things that fly. Whether the market rewards that combination with a peer multiple, or continues to apply some discount for the barbell's internal tension, is precisely the question the 2026 restructuring is designed to answer. With the strategic anatomy on the table, we can finally state the investment case as a genuine two-sided argument.

XI. The Investment Spine: Bull vs. Bear Case Stress Test

Every good investment debate comes down to a clean "why win" against an equally honest "why not." For Textron in mid-2026, the two sides are unusually well-defined, because the pure-play thesis is falsifiable — it will either work or it won't, and the tells are concrete.

The bull case — why this wins from here. The core argument is a re-rating. Textron has spent years trading below focused aerospace-and-defense peers because the market applied a conglomerate discount to a portfolio that mixed jets and helicopters with fuel systems and golf carts. Remove Industrial cleanly, the argument goes, and "New Textron" is a coherent A&D company that deserves to be valued alongside the likes of General Dynamics or L3Harris — and even a partial closing of that valuation gap is worth a great deal to shareholders. Layered on top is real operating momentum: Aviation is delivering record profit on sustained demand, Bell is sitting on a multi-decade sole-source program that should transition from margin-dilutive development to production ramp, and management has a demonstrated appetite to return capital, with Industrial proceeds poised to accelerate buybacks. If those three threads hold, the story is straightforward.

The bear case — what breaks it. Start with the constraint that recurs through this entire story: engines. If Pratt & Whitney and other propulsion suppliers stay short, Aviation's backlog cannot convert, deliveries stall, and the cash-flow engine that funds everything else sputters — a bottleneck Textron cannot fix on its own timeline. Second, defense execution risk is real and specific: taking the MV-75 from digital design through prototype flight and into production is exactly the phase where costly surprises appear, and cost overruns or schedule slips on development work would pressure Bell's already-thin margins further. Third, business-jet demand is cyclical by nature; a genuine macro slowdown would cool corporate and fractional buying, and the aftermarket ballast only cushions that, it does not eliminate it. And fourth — the skeptic's favorite — the breakup itself could disappoint: stranded corporate costs could blunt the margin uplift, a soft market could force a low sale price for Industrial, and a tax-free spin would leave shareholders still holding the discounted assets. A separation announced is not a separation completed, and value is captured in the terms, not the intention.

The activist stress test sharpens the same points. A skeptical investor would ask why it took a century and a change of CEO to shed the low-return Industrial businesses; would press management on exactly how much overhead strands after the split; would scrutinize whether large buybacks are being executed at sensible prices or simply to flatter per-share metrics; and would demand that the "pure-play" premium be earned with disclosure and delivered margins, not asserted on a conference call. None of these are reasons the thesis fails — they are the conditions it must satisfy to succeed, and holding management to them is the whole job.

Which is why the disciplined way to follow this company is to ignore the noise and watch a very small number of things. First, Aviation book-to-bill and backlog — as long as orders keep pace with deliveries and the backlog holds, sustained demand is intact and the engine constraint is a timing problem rather than a demand problem; if book-to-bill slips durably below one, the demand story is cracking. Second, the MV-75 milestones and Bell's margins — a successful prototype first flight on schedule and stabilizing EMD margins would prove execution; slips and further margin erosion would prove the bear right. Third, the Industrial separation itself — the speed against the 12-to-18-month clock, the structure chosen, and above all the valuation captured and the stranded-cost math. Those three, tracked over the next several quarters, will settle the debate more honestly than any narrative. Everything else — the quarterly earnings beats, the analyst upgrades, the conference-call rhetoric about a cleaner "New Textron" — is commentary around those three facts. A patient observer who watches book-to-bill, MV-75 execution, and the terms of the Industrial exit will know how this story is going long before the market fully reprices it. And the narrative, in the end, is the point.

XII. Epilogue

There is a neat symmetry to where this story lands. A hundred years after Royal Little began buying unrelated businesses to escape the misery of the textile cycle — and in doing so invented the diversified conglomerate that a generation of American executives would imitate — his company is deliberately becoming the thing he built it not to be: focused, legible, concentrated in two industries it understands better than almost anyone. The father of conglomerates is being un-fathered, by an Air Force Academy graduate who spent her career on the government side of the defense business.

The lesson embedded in the arc is not that diversification was always wrong. For a time it genuinely smoothed earnings and compounded capital, and the near-death experience of 2008 came not from diversification itself but from letting a captive bank metastasize inside an industrial company. The lesson is narrower and more durable: in a world of specialists, sustained advantage tends to come from operational excellence and disciplined capital allocation inside businesses a management team truly understands — the Beechcraft logic — rather than from the financial engineering of assembling unrelated cash flows, or from importing an industrial playbook into a consumer market it was never built for — the Arctic Cat logic.

There is a final irony worth sitting with. The market spent decades punishing Textron for being complicated, and management spent those same decades insisting the complexity was a strength. The breakup is an admission that the market was right — that a business jet maker and a helicopter maker are worth more standing clearly on their own than hidden inside a structure that also made fuel tanks and golf carts. But admissions like this are only worth what the execution delivers. A company can announce the right strategy and still capture none of its value if the sale price is poor, the stranded costs are high, or the crown jewel it is betting on stumbles in development. The direction is finally correct; the distance still has to be walked.

Whether Textron completes that transformation on good terms is, as of July 2026, genuinely unsettled. The crown jewels are real, the incentives point the right way, and the strategic logic of the breakup is sound. But the engine constraint is real too, the largest defense program is still years from proving itself in production, and a separation is only as good as the price it fetches. What is no longer in doubt is the direction. The century-long experiment in conglomeration is being wound down, and the market is being asked to decide what a focused Textron is worth. That decision is the whole story from here.

References

-

Textron Reports First Quarter 2026 Results; Announces Intent to Separate its Industrial Segment — BusinessWire / Textron, 2026-04-30 ↩↩↩↩

-

Textron to separate Industrial segment; Q1 profit beats estimates — Reuters, 2026-04-30 ↩

-

Textron Reports Fourth Quarter 2025 Results; Announces 2026 Financial Outlook — Textron IR, 2026-01-28 ↩↩↩↩↩↩

-

Textron (TXT) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-01-28 ↩

-

Textron Announces Appointment of Lisa Atherton as President and CEO Effective January 4, 2026; Scott Donnelly Appointed Executive Chairman — Textron IR, 2025-10-22 ↩↩

-

Meet Bell CEO Lisa Atherton, Who's at the Helm of a Potential $100 Billion U.S. Army Contract — D CEO Magazine, 2024-10 ↩

-

Cessna Aircraft Parent Textron To Acquire Beechcraft for $1.4 Billion — Aviation International News, 2013-12-27 ↩↩

-

Textron Completes Acquisition of Beechcraft — Textron 8-K / SEC, 2014-03-14 ↩↩

-

Textron to Buy Arctic Cat for $247 Million — ATV.com, 2017-01-25 ↩

-

Army Approves Milestone B for Future Long Range Assault Aircraft Program — U.S. Army, 2024-08-02 ↩

-

Textron's Bell V-280 Valor Chosen as New U.S. Army Long-Range Assault Aircraft — Bell Newsroom, 2022 ↩

-

The MV-75: The Army's New Aircraft and the Future of Air Assault Warfare — Military.com, 2026-03-27 ↩↩

-

Textron Inc. 2025 Definitive Proxy Statement (Form DEF 14A) — SEC, 2025 ↩↩

-

Textron Inc. 2026 Definitive Proxy Statement (Form DEF 14A) — SEC, 2026 ↩

-

Textron Inc. First Quarter 2026 Results, Exhibit 99.1 (eAviation segment realignment) — SEC 8-K, 2026-04-30 ↩↩↩

-

Textron Aviation Posts Record 2025 Revenue and Deliveries — AeroTime, 2026-01 ↩↩

-

Last Call for Textron CEO Scott Donnelly — Corporate Jet Investor, 2025 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube