Texas Instruments: The Semiconductor Giant's Journey

I. Introduction & Episode Roadmap

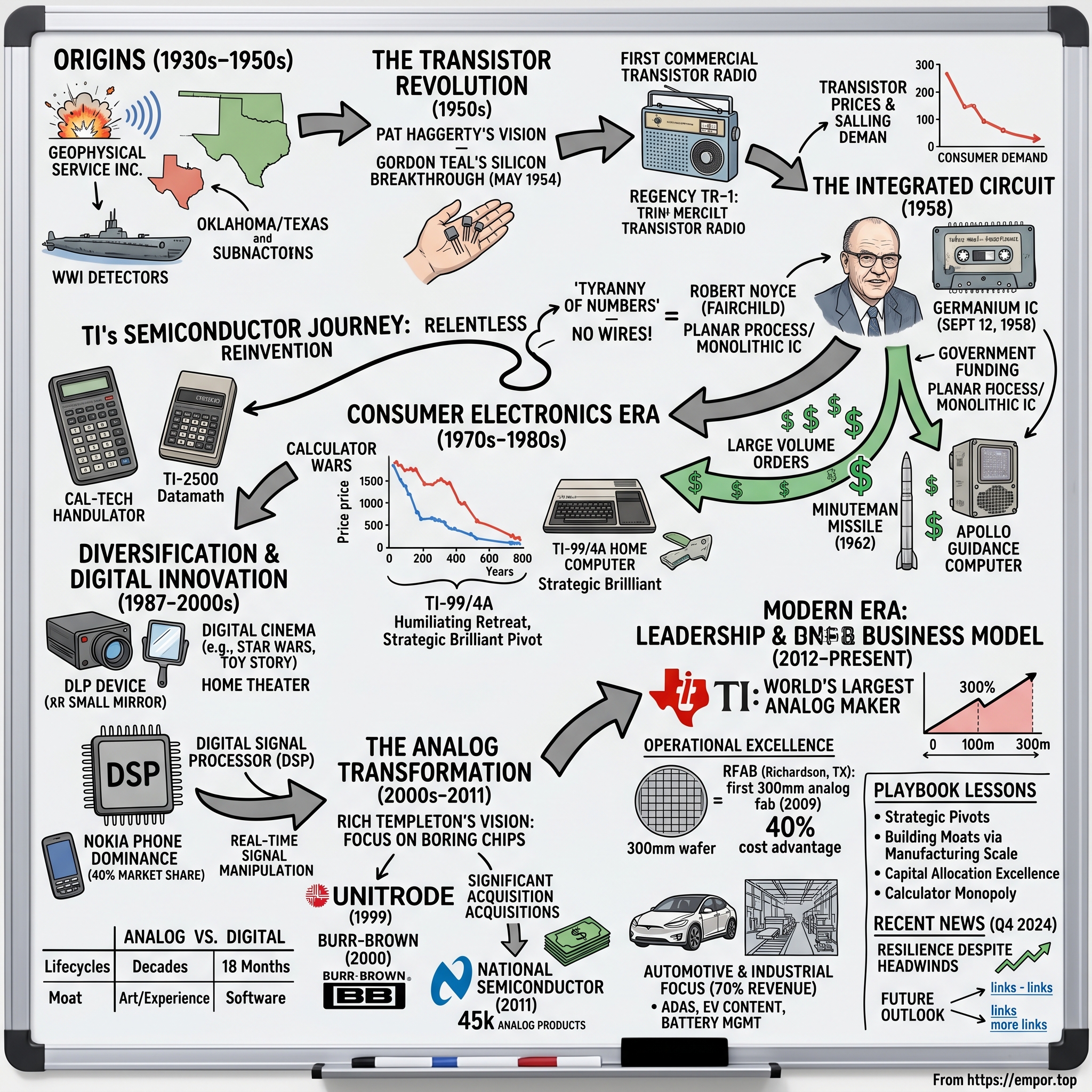

The year is 1958. In a cramped Dallas laboratory, a young engineer named Jack Kilby is working alone during the summer while his colleagues are on vacation—he hasn't earned time off yet as a new hire. With germanium transistors and other components spread across his workbench, Kilby is about to solve a problem that will fundamentally reshape human civilization: how to connect electronic components without the tangle of wires that made complex circuits impossible to manufacture reliably. His solution—the integrated circuit—would earn him a Nobel Prize and transform his employer, Texas Instruments, from an oil exploration services company into one of the most important technology companies of the 20th century.

Today, Dallas-based Texas Instruments generates over 95% of its revenue from semiconductors, with the remainder coming from those iconic graphing calculators that terrorized high school math students for generations. TI has become the world's largest maker of analog chips—the unglamorous but essential semiconductors that process real-world signals like sound, temperature, and power. While the tech press obsesses over the latest AI chips from Nvidia or Apple's newest processor, TI quietly ships billions of analog semiconductors that make modern life possible, from your car's airbag sensors to your smartphone's power management.

How did a company that started by using seismic waves to find oil deposits become the world's analog semiconductor leader? It's a story of relentless reinvention, strategic pivots that would make a management consultant weep with joy, and the kind of capital allocation discipline that Warren Buffett dreams about. From oil fields to silicon wafers, from pocket calculators to cutting-edge automotive chips, Texas Instruments has navigated every major technology transition of the past century—and emerged stronger each time.

This journey reveals three major themes that define TI's success: First, the courage to cannibalize existing businesses when technology shifts demand it. Second, the patience to build manufacturing excellence over decades when competitors chase quick profits. And third, the wisdom to focus on "boring" analog chips while others chase digital glamour—a strategy that has created one of the most defensible moats in technology.

II. Origins: From Oil Fields to Electronics (1930–1951)

The evening of December 6, 1941—one day before Pearl Harbor would thrust America into World War II—four men gathered in Dallas to sign papers that would create one of the most important technology companies of the next century. The temperature had dropped to near freezing, unusual for Dallas in early December, as Eugene McDermott, J. Erik Jonsson, Cecil H. Green, and H.B. Peacock met to purchase Geophysical Service Inc. from its parent company. None of them could have imagined that their oil exploration services company would one day become the world's dominant analog semiconductor manufacturer. But the timing of their purchase—literally on the eve of America's entry into the war—would prove fateful, forcing them to pivot from finding oil to finding submarines.

The roots of this moment stretched back to the oil fields of 1920s Oklahoma, where John Clarence Karcher had invented and patented the reflection seismograph in 1919, creating the means by which most of the world's oil reserves would be discovered. Karcher's invention was revolutionary: it used controlled explosions on the surface to beam sound waves into the earth, then recorded how those waves bounced back from underground rock formations. Like sonar for the earth's crust, it could map the salt domes and geological structures where oil accumulated—a massive improvement over the wildcatter's drill-and-pray approach.

In 1925, when Everette Lee DeGolyer learned of Karcher's experiments, he arranged a meeting that resulted in the creation of Geophysical Research Corporation as a subsidiary of Amerada Petroleum. It was at Western Electric Company that Karcher first met a young Eugene McDermott, a Brooklyn-born engineer with a master's degree from Columbia who would become his most important business partner.

By 1930, the technology had proven itself, and with DeGolyer's backing—he purchased a 50% stake for $100,000—Karcher and McDermott launched Geophysical Service Incorporated, with Karcher as president and McDermott as vice-president. They moved the company to Dallas, drawn by its central location between the oil fields of Texas, Oklahoma, and Louisiana. The early crews included future company leaders like Cecil H. Green, who began with on-the-job training as a crew chief.

The 1930s brought both growth and structural complexity. In 1938, the company split into two subsidiaries: Coronado Corporation for oil production, headed by Karcher, and Geophysical Service, Incorporated for exploration, managed by McDermott. This reorganization reflected a fundamental tension in the business—the cyclical, boom-bust nature of oil exploration services versus the steady income from actual oil production.

Then came that fateful December evening in 1941. McDermott, along with three other GSI employees—J. Erik Jonsson, Cecil H. Green, and H.B. Peacock—purchased GSI. The timing couldn't have been more dramatic. The next day, Japanese forces attacked Pearl Harbor, and suddenly these four engineers found themselves running a company whose seismic expertise would be desperately needed for an entirely different purpose.

During World War II, GSI expanded its services to include electronics for the U.S. Army, Army Signal Corps, and U.S. Navy. The company's ability to detect underground oil formations translated remarkably well to detecting underwater submarines. GSI reinvented its oil-detecting technologies to create submarine detection devices that could be loaded onto low-flying aircraft to detect magnetic waves generated by submarines below the ocean's surface. The same mathematical principles that mapped oil deposits could track enemy vessels—physics didn't care whether you were hunting petroleum or U-boats.

In November 1945, Patrick Haggerty was hired as general manager of the Laboratory and Manufacturing (L&M) division. Haggerty was no ordinary hire—he was a Navy lieutenant who had managed GSI's wartime contracts and had seen firsthand the company's potential beyond oil exploration. He brought a vision that electronics, not oil services, represented the future.

By 1951, the L&M division, with its defense contracts, was growing faster than GSI's geophysical division. The tail was wagging the dog. The four founders made a decision that would define their legacy: The company was reorganized and initially renamed General Instruments Inc. Because a firm named General Instrument already existed, the company was renamed Texas Instruments that same year.

This wasn't just a name change—it was a declaration of intent. The company that had started by listening to echoes bouncing off underground rock formations was betting its future on a technology that hadn't even been commercialized yet: the transistor. Patrick Haggerty's arrival had transformed four oil field engineers into electronics pioneers, setting the stage for Texas Instruments to ride the greatest technological wave of the 20th century.

III. The Transistor Revolution (1952–1957)

The morning of May 10, 1954, at the Institute of Radio Engineers National Conference on Airborne Electronics in Dayton, Ohio, should have been forgettable. A parade of engineers and scientists had been lamenting the sobering challenges of developing silicon transistors for hours. Scattered attendees were stifling yawns, glancing at watches, and nodding off. The consensus was clear: silicon transistors remained a laboratory curiosity, impractical for commercial production.

Then Gordon Teal of Texas Instruments stepped to the podium.

"Contrary to what my colleagues have told you about the bleak prospects for silicon transistors," he announced, "I happen to have a few of them here in my pocket." The drowsy audience snapped to attention. "Did you say you have silicon transistors in production?" asked a stupefied listener about ten rows back. "Yes, we have three types of silicon transistors in production," Teal replied, pulling several out of his pocket to the general amazement and envy of the crowd.

This theatrical moment represented the culmination of a strategic bet that Patrick Haggerty had made two years earlier. In early 1952, Texas Instruments purchased a patent license to produce germanium transistors from Western Electric, the manufacturing arm of AT&T, for $25,000. But Haggerty wasn't content to merely license technology—he wanted to lead it. Haggerty brought Gordon Teal to the company due to his expertise in growing semiconductor crystals while at Bell Telephone Laboratories.

Teal was no ordinary hire. While at Brown University, he had begun work in the laboratory of Professor Charles Kraus on the element germanium, which was then believed to be useless. Teal joined Bell Labs in 1930 and would remain employed there for 22 years. During his time there, he continued to work with germanium and silicon. When William Shockley's group at Bell Labs invented the transistor in 1947, Teal realized that substantial improvements in the device would result if it was fabricated using a single crystal, rather than the polycrystalline material then being used.

At Texas Instruments, Teal set an audacious agenda: bypass germanium entirely and go straight to silicon. This was technological heresy. Germanium was easier to work with and allowed higher-frequency operation. Silicon required temperatures above 1,000 degrees Celsius to process and was considered impossibly difficult to manufacture. But silicon had one overwhelming advantage: it could operate from -55 to 125°C, compared to germanium's 0 to 70°C range—crucial for military applications and the Texas heat.

The race was closer than anyone at the Dayton conference knew. Another company, in fact, had already fabricated a working silicon transistor a few months earlier. In January 1954, Morris Tanenbaum made one while working as a member of Shockley's research group at Bell Labs. But the world's dominant semiconductor company kept this achievement under wraps, while the Texas upstart rushed to announce it.

Working independently in April 1954, Gordon Teal at TI created the first commercial silicon transistor and tested it on April 14, 1954. The difference between Bell Labs and Texas Instruments wasn't just timing—it was philosophy. Bell Labs viewed silicon transistors as a research curiosity; TI saw them as a product.

But transistors alone don't build a business. Haggerty understood that TI needed to create demand, not just supply. His solution was audacious: build a consumer product that would showcase transistors to the world. In May 1954, Pat Haggerty, vice president of Texas Instruments, committed 10 percent of the company's revenue to the development of a brand-new mass-market consumer product, made with a not-yet-ready-for-mass-production component. He wanted it on store shelves in less than six months, in time for the holiday shopping season.

In the spring of 1954 and with a prototype in hand, TI searched out an established radio manufacturer to develop and market a radio using its transistors. TI soon partnered with the Regency Division of Industrial Development Engineering Associates (IDEA). The major radio manufacturers—RCA, Philco, Emerson—all turned them down. They were comfortable with vacuum tubes and saw no reason to change.

The engineering challenge was staggering. The original TI prototype used eight transistors; when the company met with I.D.E.A. it used six. The Regency TR-1 circuitry was refined from the TI design, reducing the number of parts, including two more expensive transistors. Although this severely reduced audio output volume, it let I.D.E.A. keep the price down to $49.95.

On 18 October 1954, Texas Instruments announced the first commercial transistorized radio. It would be available in select outlets in New York and Los Angeles beginning 1 November, with wider distribution once production ramped up. The Regency TR-1 Transistor Pocket Radio initially came in black, gray, red, and ivory.

The market response was extraordinary—and revealing. One year after the TR-1 release, sales approached 100,000 units. While the radio was praised for design aesthetics, novelty and small size, because of the cost cutting measures, the sensitivity and sound quality were behind the established vacuum tube based competitors. A review in Consumer Reports mentioned the high level of noise and instability on certain radio frequencies, and recommended against purchase.

But Haggerty didn't care about the reviews. He had achieved his real goal: demonstrating that transistors could be mass-produced for consumer products. The per-unit cost of transistors plummeted from $10-15 to under $2. More importantly, the TR-1 created a cultural phenomenon. The first transistorized consumer product, the Regency TR-1 radio, went on sale Oct. 18, 1954, and sold out almost immediately. If you owned one, you were the coolest thing on two legs.

The strategic impact extended far beyond consumer electronics. IBM CEO, Thomas J. Watson, Jr, saw transistors as the future of computers, and ordered that IBM build no more machines with tubes after June 1, 1958. But his designers had been reluctant to embrace the new technology. Watson bought and handed out numerous Regency TR-1's to set an example for IBM employees. Whenever engineers complained to Watson about the decision, he just gave them a TR-1.

By 1957, Texas Instruments' mastery of silicon transistors had created an insurmountable competitive advantage. While competitors struggled with germanium's temperature limitations and reliability issues, TI was shipping silicon transistors to the military and aerospace industries. The company that had started the decade listening to oil deposits was ending it by enabling the space race—all because Gordon Teal pulled some transistors from his pocket on a drowsy morning in Dayton.

IV. The Integrated Circuit: Jack Kilby's Nobel Prize Innovation (1958–1970s)

The summer of 1958 in Dallas was brutal—temperatures soared above 100 degrees for weeks on end. While his colleagues at Texas Instruments escaped for their two-week vacation, Jack Kilby, the new hire who hadn't earned time off yet, sat alone in the air-conditioned laboratory. As he later recalled, "I was sitting at a desk, probably staring out the window." The solitude gave him time to think about a problem that was driving the entire electronics industry mad: the "tyranny of numbers."

In the early '50s, you could design a computer that could do anything, but you couldn't build it. There were too many separate parts that had to be wired together. Just the numbers of parts and connections were too great. The common name for this problem was the tyranny of numbers. We can perceive of that device but we can't build it because the numbers are too great.

The problem was elegantly simple and maddeningly complex. Engineers could design sophisticated electronic circuits on paper, but physically building them required hand-soldering thousands of components to thousands of bits of wire. Hand-soldering thousands of components to thousands of bits of wire was expensive and time-consuming. It was also unreliable; every soldered joint was a potential source of trouble. A military computer might have 30,000 connections—each one a potential failure point. The Air Force calculated that even with 99.99% reliability per connection, complex systems would fail within hours.

Kilby's breakthrough came from a heretical thought: Why do we need the wires? If I make parts out of all of the same material, I could carve them into a block of that material and no wires. Instead of building components separately and wiring them together, why not build everything—transistors, resistors, capacitors—from the same piece of semiconductor material?

On September 12, he presented his findings to company's management, which included Mark Shepherd. He showed them a piece of germanium with an oscilloscope attached, pressed a switch, and the oscilloscope showed a continuous sine wave, proving that his integrated circuit worked. The device was ugly—a piece of germanium the size of a paper clip with protruding gold wires—but it worked. Jack Kilby successfully tests the first integrated circuit at Texas Instruments to prove that resistors and capacitors could exist on the same piece of semiconductor material. His circuit consisted of a sliver of germanium with five components linked by wires.

The executives stared at the oscilloscope's sine wave, not quite grasping that they were witnessing the birth of the modern world. Kilby's notebook entry for that day was characteristically understated: Jack Kilby recorded the successful demonstration of the first integrated circuit in his engineering notebook. Signed JS Kilby, the page in his notebook is dated Sept. 12, 1958.

Texas Instruments immediately recognized the military implications. In autumn 1958, Texas Instruments introduced the yet non-patented idea of Kilby to military customers. While most divisions rejected it as unfit to the existing concepts, the US Air Force decided that this technology complied with their molecular electronics program, and ordered production of prototype ICs, which Kilby named "functional electronic blocks".

But Kilby's invention had a fatal flaw: those gold wires. His integrated circuit wasn't truly integrated—components were carved from a single crystal but still required manual wire connections, making mass production nearly impossible. The solution would come from an unexpected place: Fairchild Semiconductor in California, where Robert Noyce was working on the same problem with a radically different approach.

Noyce had a crucial advantage: Jean Hoerni's planar process, developed in early 1959. The basis for Noyce's monolithic IC was the planar process, developed in early 1959 by Jean Hoerni. Jean Hoerni's "planar" process improved transistor reliability by creating a flat surface structure protected with an insulating silicon dioxide layer. This breakthrough allowed components to be protected under a layer of silicon dioxide—like preserving electronics in glass.

On January 23, 1959, Noyce documented his vision of the planar integrated circuit, essentially re-inventing the ideas of Kilby and Lehovec on the base of the Hoerni's planar process. But Noyce went further than Kilby. Robert Noyce then proposed interconnecting transistors on the wafer by depositing aluminum "wires" on top. Instead of hand-wiring components, Noyce would deposit aluminum connections directly onto the chip—the wires would be part of the manufacturing process itself.

Unlike Kilby's IC which had external wire connections and could not be mass-produced, Noyce's monolithic IC chip put all components on a chip of silicon and connected them with aluminum lines. This was the killer application: a truly monolithic integrated circuit that could be mass-produced using photolithography, the same technique used to print newspapers.

The patent battle that followed was epic and bitter. In July 1959 Noyce filed a patent for his conception of the integrated circuit. Texas Instruments filed a lawsuit for patent interference against Noyce and Fairchild, and the case dragged on for some years. Ten years later, long after their respective companies had cross-licensed technologies, the courts gave Kilby credit for the idea of the integrated circuit but gave Noyce the patent for his planar manufacturing process, a method for evaporating lines of conductive metal (the "wires") directly onto a silicon chip.

The real winners were the U.S. military and NASA. In October 1961, Texas Instruments built for the Air Force a demonstration "molecular computer" with a 300-bit memory. Kilby's colleague Harvey Cragon packed this computer into a volume of a little over 100 cm3, using 587 ICs to replace around 8,500 transistors and other components that would be needed to perform the equivalent function.

The Minuteman missile program became the integrated circuit's first volume customer. Many of those patents concerned improvements in IC design and manufacturing, including those for the first IC-powered experimental computer that TI built for the U.S. Air Force in 1961 and for the ICs that TI designed and delivered to the Air Force in 1962 for use in the Minuteman ballistic missile guidance system. Each Minuteman II guidance computer used 2,000 integrated circuits. The Apollo Guidance Computer would use 5,000. These military contracts did what no commercial market could: they paid premium prices for early, imperfect integrated circuits, funding the research that would drive costs down from $1,000 per circuit in 1960 to $25 by 1963.

By the late 1960s, Texas Instruments had transformed Kilby's invention into a business. The 7400 series of transistor-transistor logic chips, developed by Texas Instruments in the 1960s, popularized the use of integrated circuits in computer logic. The 7400 series became the building blocks of the digital age—standardized logic gates that engineers could use like LEGO blocks to build everything from calculators to computers.

The transformation was staggering. In 1961, a computer with the power of a smartphone would have been the size of a building and cost millions. By 1970, that same computing power fit on a chip the size of a fingernail. Gordon Moore of Fairchild (later Intel) observed that the number of transistors on a chip doubled every 18 months—Moore's Law was born, and with it, the exponential improvement that would define the next half-century of human progress.

Kilby understood the magnitude of his invention but remained remarkably humble. When he won the Nobel Prize in Physics in 2000—Noyce had died in 1990 and couldn't share it—Kilby said in his acceptance speech: "I'm pleased to have lived to see our tremendous progress. But one thing I didn't realize: I didn't think the integrated circuit would reduce the cost of electronic functions by a factor of a million. I didn't think I'd live to see the day when people had a computer in their home. But it's nice to see all these things happen."

Today, Noyce and Kilby are usually regarded as co-inventors of the integrated circuit, although Kilby was inducted into the Inventor's Hall of Fame as the inventor. But the real lesson isn't about who invented what first. It's that breakthrough innovation often requires multiple geniuses working on the same problem from different angles. Kilby showed it could be done; Noyce showed how to manufacture it at scale. Together, they gave humanity its most transformative technology—the ability to print intelligence.

V. Consumer Electronics Era: Calculators & Digital Innovation (1967–1985)

Pat Haggerty stood before his engineering team at Texas Instruments in March 1967, holding what looked like a brick with buttons. "THE FIRST CAL TECH / PRESENTED TO P. E. HAGGERTY / MARCH 29, 1967" read the inscription on the world's first handheld electronic calculator. An inscription on the front of the calculator reads: THE FIRST CAL TECH (

PRESENTED TO P. E. HAGGERTY / MARCH 29, 1967") The device weighed 2.5 pounds, displayed 12 digits on a thermal printer, and could perform four basic arithmetic functions. It ran on 150 milliwatts of power and required external power. But Haggerty saw past the limitations to the revolution it represented.

The genesis of this project stretched back to 1964, when TI engineer Jack St. Clair Kilby conceived the idea of building a miniaturized calculator on an integrated circuit chip. Kilby had already revolutionized electronics with the integrated circuit in 1958, but now he wanted to prove that ICs could transform consumer products. The project represented an enormous gamble—TI would need to compress what typically filled a desktop machine into something that could fit in a hand.

By 1970, after several years of refinement, the Cal-Tech evolved into a commercial product. The new model weighed just 45 ounces and could display up to 12 decimal digits on its LED screen. At $400 (about $3,000 in today's dollars), it was expensive but revolutionary. The TI-2500 Datamath, introduced in 1972, brought the price down to $120 and truly launched the calculator wars.

But the real breakthrough came in 1971 when TI engineer Gary Boone designed the TMS1000, the industry's first single-chip microcomputer. This 4-bit processor integrated the central processing unit, read-only memory, random access memory, and input/output support on a single chip. On September 4, 1973, Boone was awarded the first patent on a single-chip microprocessor, though Intel's 4004 had beaten TI to market by several months.

The microprocessor transformed calculators from expensive curiosities to mass-market products. By 1975, TI could sell a basic four-function calculator for under $20. The company's vertical integration—making everything from the silicon wafers to the finished products—gave it a crushing cost advantage. Competitors who had to buy TI's chips couldn't match TI's prices.

The educational calculator market became TI's fortress. In 1990, TI released the TI-81 graphing calculator, which revolutionized mathematics education. The TI-83 and TI-84 series became so entrenched in American high schools that they achieved near-monopoly status. Even today, decades after smartphones made standalone calculators technically obsolete, TI still dominates the educational calculator market with 80% market share—a testament to the power of institutional lock-in.

But TI's consumer ambitions extended far beyond calculators. In June 1978, TI introduced Speak & Spell at the Summer Consumer Electronics Show. This educational toy used TI's TMC0280 linear predictive coding speech synthesizer chip to become the first electronic device to reproduce human speech without moving parts or tape recorders. It was a sensation—children could learn spelling through an interactive, talking computer.

The home computer market beckoned next. In 1979, TI entered with the TI-99/4, featuring a 16-bit processor when most competitors used 8-bit chips. The TI-99/4A, released in 1981, became one of the best-selling home computers of the early 1980s. By late 1982, TI was shipping 5,000 computers daily from its Lubbock factory, dominating the U.S. home computer market.

Then came the price war that nearly destroyed the industry. Commodore's Jack Tramiel, determined to crush TI for undercutting his calculator business years earlier, launched a vicious price war. The Commodore VIC-20 dropped from $299 to $99; TI responded by cutting the 99/4A from $525 to $150. Both companies bled money. William Turner, TI's consumer products chief, famously quipped: "We're making money on every computer we sell—it's just that we're losing money on every computer we make."

By October 1983, TI had lost $500 million on home computers and exited the market, laying off thousands of workers. The retreat was humiliating but strategically brilliant. While competitors fought over the consumer computer market's scraps, TI pivoted to what would become far more lucrative: digital signal processors (DSPs) and analog semiconductors for industrial applications.

The DSP business, launched in 1982 with the TMS32010, would prove prescient. These specialized processors could manipulate analog signals in real-time, enabling everything from modems to digital cameras to cell phones. By the 1990s, TI commanded over 40% of the global DSP market. Every Nokia phone contained TI chips; every modem translated analog phone lines to digital signals using TI's DSPs.

This era taught TI a crucial lesson: consumer markets were fickle and brutally competitive, but the semiconductors that powered consumer devices offered steady profits with less drama. The company that had tried to be the next Apple would instead become the arms dealer to the entire electronics industry—a less glamorous but far more profitable strategy that would define its next chapter.

VI. Digital Light Processing & Technology Diversification (1987–2000s)

Larry Hornbeck sat hunched over his workbench at Texas Instruments' Central Research Laboratories in 1977, pondering an audacious question: Could he build a display using millions of tiny mirrors? The idea seemed absurd—mechanical devices couldn't possibly compete with the purely electronic cathode ray tubes that dominated displays. But Hornbeck, a Stanford-trained physicist, believed that combining mechanical engineering with semiconductor manufacturing could create something revolutionary.

Ten years and countless iterations later, in 1987, Hornbeck achieved his breakthrough: the Digital Micromirror Device (DMD). Each mirror measured just 16 micrometers square—smaller than a human red blood cell—and could tilt ±10 degrees more than 5,000 times per second. By 1987, TI invented the digital light processing device (also known as the DLP chip), which serves as the foundation for the company's DLP technology and DLP Cinema. Arrays of hundreds of thousands of these mirrors could create images by reflecting light toward or away from a projection lens.

The technology was breathtaking in its elegance. Unlike LCD displays that blocked light to create images (wasting up to 95% of the light source), DLP mirrors redirected light with almost perfect efficiency. Each mirror represented one pixel, switching between on and off states so rapidly that the human eye perceived smooth gradations of gray. Add a color wheel spinning at 120 Hz, and you had full-color video.

But finding a market proved challenging. The first DLP projectors in 1996 cost over $10,000 and competed against established LCD technology. TI needed a killer application that would justify the premium. They found it in Hollywood.

On February 2, 2000, Philippe Binant, technical manager of Digital Cinema Project at Gaumont in France, realized the first digital cinema projection in Europe with the DLP Cinema technology developed by TI. The screening of "Toy Story 2" in Paris marked the beginning of cinema's digital revolution. George Lucas used DLP projectors for "Star Wars: Episode II" in 2002, the first major film distributed digitally. By 2010, DLP powered half of all digital cinema screens worldwide.

The home theater market followed. DLP projectors offered superior contrast ratios and eliminated the "screen door effect" that plagued LCD projectors. Samsung incorporated DLP into rear-projection TVs, capturing 20% of the large-screen TV market by 2005. Today, DLP technology appears in everything from 3D printers to automotive head-up displays to spectroscopy equipment—a $2 billion annual business built on mirrors smaller than dust motes.

Parallel to DLP's development, TI was building dominance in Digital Signal Processing (DSP). The 1982 launch of the TMS32010 had created the DSP market, but the 1990s saw explosive growth as wireless communications demanded ever more sophisticated signal processing. The TMS320C6000 series, introduced in 1997, delivered 1,600 MIPS (million instructions per second) at just $25—performance that would have required a room-sized computer a decade earlier.

Nokia's rise to mobile phone dominance rode on TI's DSPs. Every GSM base station needed DSPs to handle multiple simultaneous calls. Every modem, every digital camera, every MP3 player required real-time signal processing. By 2000, TI commanded 45% of the $6 billion DSP market. The company's OMAP (Open Multimedia Applications Platform) processors powered the first smartphones, including the Nokia N95 and original Amazon Kindle.

But even as TI dominated these specialized markets, management recognized a fundamental shift occurring in semiconductors. The era of explosive growth in PCs and cell phones was ending. The future belonged to analog semiconductors—the "boring" chips that converted real-world signals into digital data and back again. Every electronic device needed dozens of analog chips for power management, signal conditioning, and interface functions.

TI's analog business in 2000 generated just $2.5 billion in revenue, placing it fifth globally behind companies like STMicroelectronics and Philips. But CEO Rich Templeton saw an opportunity. Unlike digital chips that followed Moore's Law—becoming obsolete every 18 months—analog chips had product lifecycles measured in decades. A power management chip designed in 1995 might still be selling in 2020. This longevity meant that building a broad catalog of analog products created a compounding competitive advantage.

The strategy required massive investment and patience. TI began acquiring analog specialists: Unitrode in 1999 for $1.2 billion brought power management expertise; Burr-Brown in 2000 for $7.6 billion added precision analog capabilities. Each acquisition brought not just products but customer relationships and application knowledge that took decades to build.

TI also revolutionized analog chip distribution. The company created the industry's most comprehensive online catalog, allowing engineers to search 30,000 products, download datasheets, order samples, and even simulate circuits online. This direct-to-engineer approach bypassed traditional distributors and created intimate customer relationships. An engineer who designed in a TI chip for a prototype often stuck with it through production—creating switching costs that locked in revenue for years.

By 2005, TI's analog revenue had doubled to $5 billion, making it the world's largest analog semiconductor company. The transformation from digital pioneer to analog leader was nearly complete. The company that had invented the integrated circuit and microprocessor was betting its future on chips that were fundamentally similar to those built in the 1960s—just smaller, cheaper, and more precise.

This strategic pivot would be validated dramatically with the 2011 acquisition of National Semiconductor, but already by the mid-2000s, the wisdom was apparent. While former competitors like Motorola's semiconductor division struggled and Intel poured billions into failed mobile efforts, TI quietly built an analog empire that would prove remarkably resilient through the financial crisis and beyond.

VII. The Analog Transformation & National Semiconductor Acquisition (2000–2011)

On April 4, 2011, Rich Templeton, CEO of Texas Instruments, shocked the semiconductor industry with a Monday morning announcement: TI would acquire National Semiconductor for $6.5 billion in cash—an 80% premium over National's Friday closing price. TI paid $25 per share of National Semiconductor stock, which was an 80% premium over the share price of $14.07 as of April 4, 2011, close. Analysts gasped at the price, but Templeton knew something they didn't: this deal would cement TI's transformation from a diversified technology conglomerate into the world's undisputed analog semiconductor champion.

The journey to this moment had begun a decade earlier with a simple but profound insight. In 2003, newly appointed CEO Rich Templeton gathered his leadership team and presented a contrarian vision. While Intel chased faster processors and Qualcomm built baseband chips for smartphones, Templeton saw opportunity in the unglamorous: analog semiconductors that operated in the physical world of voltage, current, and temperature rather than the digital realm of ones and zeros.

"Look at our financials," Templeton told his team. "Our analog products have 40% gross margins versus 20% for our digital baseband business. They have product lifecycles of 10-15 years versus 18 months. Customers design them in once and rarely switch. This is a beautiful business hiding inside a complicated company."

The numbers supported his thesis. While digital chips followed Moore's Law—doubling in complexity every 18 months while prices plummeted—analog chips defied this logic. A temperature sensor designed in 1995 might still sell profitably in 2010. Why? Because analog design was more art than science. Digital designers could rely on automated tools and standard cell libraries. Analog designers needed years of experience to understand how transistors behaved at different temperatures, voltages, and process variations. This expertise barrier created a moat that software couldn't cross.

TI's transformation began with targeted acquisitions. In 1999, the company acquired Unitrode for $1.2 billion, gaining power management expertise crucial for battery-powered devices. The following year, TI spent $7.6 billion on Burr-Brown, a company renowned for precision analog-to-digital converters used in industrial and medical equipment. Each acquisition brought not just products but decades of application knowledge—understanding how to solve specific customer problems that no amount of money could quickly replicate.

But acquisitions alone wouldn't suffice. TI needed to fundamentally restructure how it developed and sold analog products. The traditional semiconductor model involved designing chips for major customers like Apple or Samsung, with volumes in the millions. Analog was different—thousands of customers each buying thousands of parts. A motor controller for a German washing machine manufacturer might generate only $50,000 annually, but it would generate that for a decade with zero design changes.

TI built the industry's most extensive catalog system, eventually reaching 30,000 products. Engineers could search by specification, download datasheets, order free samples, and even simulate circuits online. This direct-to-engineer approach created a viral adoption model: an engineer prototyping a new product would naturally reach for TI parts they knew, and once designed in, switching costs made changes unlikely.

The 2008 financial crisis tested this strategy. As global semiconductor sales plummeted 25%, TI's diverse analog portfolio proved resilient. While Intel and AMD suffered as PC sales collapsed, TI's thousands of analog products across hundreds of applications provided stability. Some markets declined, others grew, but the portfolio effect smoothed the volatility.

By 2010, TI's analog business generated $6 billion in revenue with operating margins above 30%. But Templeton wanted more. After the acquisition of National Semiconductor in 2011, the company had a combined portfolio of 45,000 analog products and customer design tools. National Semiconductor, founded by Fairchild veterans in 1959, possessed complementary strengths: power management for communications infrastructure, precision amplifiers for industrial applications, and crucially, 5,000 customers that barely overlapped with TI's.

The merger math was compelling. National's $1.6 billion in revenue would make TI's analog business larger than the next three competitors combined. The combined company would have 45,000 analog products, customer relationships with virtually every electronics manufacturer globally, and the scale to invest in 300-millimeter wafer manufacturing—a technology that could reduce production costs by 40%.

On September 23, 2011, the deal closed. The deal made TI the world's largest maker of analog technology components. The companies formally merged on September 23, 2011. Integration proceeded with surgical precision. TI retained National's strongest product lines while eliminating redundancies. More importantly, TI's massive sales force—10 times larger than National's—could now sell National's products to thousands of new customers. Revenue synergies exceeded cost savings within 18 months.

The transformation was complete. The company that had pioneered digital technology—the integrated circuit, the microprocessor, the DSP—had successfully pivoted to analog. By 2011, analog semiconductors represented over 50% of TI's revenue. The baseband business that had powered Nokia phones? Sold to Ericsson. The digital television chips? Discontinued. Even the iconic DLP business, while retained, became a profitable niche rather than a growth driver.

Critics called it retreat; Templeton called it focus. While competitors scattered their resources across dozens of markets, TI concentrated on analog and embedded processing for industrial and automotive applications—markets with long product cycles, high margins, and deep competitive moats. The wisdom of this strategy would become apparent in the coming decade as TI's steady execution delivered industry-leading returns while former high-flyers stumbled.

VIII. Modern Era: Market Leadership & Business Model (2012–Present)

Inside TI's Richardson, Texas wafer fabrication plant, a robot glides silently through the clean room, carrying a single 300-millimeter silicon wafer worth more than a luxury car. This wafer, roughly the size of a medium pizza, contains over 40,000 individual analog chips—each destined for a different application, from managing the battery in a Tesla to controlling the temperature in an industrial refrigerator. This scene, replicated thousands of times daily across TI's manufacturing network, represents the culmination of a strategy that has made Texas Instruments the world's most profitable analog semiconductor company.

Dallas-based Texas Instruments generates over 95% of its revenue from semiconductors and the remainder from its well-known calculators. Texas Instruments is the world's largest maker of analog chips, which are used to process real-world signals such as sound and power. Today's Texas Instruments is radically focused compared to its conglomerate past. The company's revenue streams break down with surgical precision: As of 2016, TI is made up of four divisions: analog products, embedded processors, digital light processing, and educational technology. More specifically, Analog semiconductors generate 76.70% of total revenue, Embedded Processing contributes 16.30%, and other revenue sources including DLP and calculators account for the remaining 7%.

The market focus is equally deliberate. As of January 2021, the industrial market accounts for 41 percent of TI's annual revenue, and the automotive market accounts for 21 percent. Personal electronics represents 24%, while communications equipment and enterprise systems each contribute 6%. This diversification across thousands of customers means no single customer represents more than 10% of revenue—a stark contrast to companies like TSMC, where Apple alone drives 25% of sales.

The secret to TI's competitive advantage lies not in cutting-edge technology but in manufacturing excellence. While competitors outsource production to foundries like TSMC, TI owns and operates its fabs. The company's transition to 300-millimeter wafers represents a masterclass in operational leverage. A 300mm wafer has 2.5 times the surface area of a 200mm wafer but costs only marginally more to process. This simple geometry translates to a 40% cost advantage over competitors stuck on older equipment.

TI's RFAB facility in Richardson, Texas, which began production in 2009, was the first 300mm analog wafer fab in the industry. The company's aggressive expansion continues: new 300mm fabs in Sherman, Texas, and Lehi, Utah, will add capacity through 2030. Texas Instruments Inc (NASDAQ:TXN) received a $1.6 billion CHIPS Act grant, which will support its new 300-millimeter wafer fabs, enhancing its manufacturing capabilities. Each fab represents a $3-5 billion investment, but the returns justify the capital: gross margins consistently exceed 60%.

The breadth of TI's product portfolio creates another moat. With 80,000+ products across hundreds of categories, TI functions like the Amazon of analog chips. An engineer designing a new product can find everything needed from one supplier: power management, amplifiers, data converters, interface chips, and embedded processors. This one-stop-shop convenience creates powerful switching costs—redesigning a product to use different suppliers might save pennies per chip but cost months of engineering time.

Recent financial performance validates this strategy. Texas Instruments (TXN) reported Q4 2024 financial results with revenue of $4.01 billion, net income of $1.21 billion, and EPS of $1.30, including a 2-cent benefit not in original guidance. Revenue decreased 3% sequentially and 2% year-over-year. Despite near-term headwinds, the company's cash generation remains robust: The company's cash flow from operations reached $6.3 billion for the trailing 12 months, with free cash flow at $1.5 billion.

The capital allocation philosophy reflects confidence in the business model. Over the past year, TI invested $3.8 billion in R&D and SG&A, $4.8 billion in capital expenditures, and returned $5.7 billion to shareholders. The company increased its dividend per share by 5% in the fourth quarter, marking the 21st consecutive year of dividend increases. This balance between growth investment and shareholder returns exemplifies TI's disciplined approach.

Competition remains intense but manageable. Texas Instruments, and Analog Devices are the top 2 companies accounting for a significant share of 30% in the market. While Analog Devices offers superior performance in high-end applications, TI dominates the broad middle market where volume and cost matter more than cutting-edge specifications. Smaller competitors like Maxim (now part of Analog Devices) and NXP focus on niches, lacking TI's scale advantages.

The automotive transformation represents TI's most significant growth opportunity. Modern vehicles contain over $500 of semiconductor content, up from $100 two decades ago. Electric vehicles double this again. TI's automotive revenue has grown from virtually nothing in 2000 to 21% of total revenue today. Advanced driver assistance systems (ADAS) alone require dozens of TI chips: radar transceivers, camera serializers, LED drivers, and motor controllers.

CEO Haviv Ilan, who succeeded Rich Templeton in 2023, brings continuity to TI's strategy. A 24-year TI veteran, Ilan previously ran the analog business and understands the importance of patient capital allocation. "We've learned that the higher the ASP, and the higher the volume per socket times ASP, the more competitive the market is. It's hard to maintain margins. When you serve a $0.25 to $0.30 a socket, price is not the biggest thing. It's performance, power and feature of the part. We make good margin on this."

Looking forward, TI's guidance reflects both near-term caution and long-term confidence. For Q1 2025, TI expects revenue between $3.74-4.06 billion and EPS of $0.94-1.16. The company projects a 2025 effective tax rate of approximately 12%. The industrial and automotive markets, representing 70% of revenue, provide structural growth tailwinds as the world becomes increasingly electrified and automated.

IX. Playbook: Business & Investing Lessons

The Power of Strategic Pivots

Texas Instruments' journey from oil exploration to semiconductor dominance illustrates a masterclass in strategic evolution. The company didn't just drift between industries—each pivot was deliberate, timed to capture emerging opportunities while abandoning declining businesses before they became albatrosses. From geophysical services to military electronics (1941), from defense to transistors (1952), from consumer electronics to semiconductors (1983), and finally from digital to analog leadership (2000s)—each transformation required the courage to cannibalize existing revenue streams for future growth.

The key lesson: successful pivots aren't about chasing hot markets but leveraging existing capabilities into adjacent opportunities. TI's signal processing expertise from oil exploration translated to submarine detection, then to transistors, then to digital signal processors. Each step built on previous knowledge while moving toward higher-margin, more defensible businesses.

Building Lasting Competitive Advantages Through Manufacturing Scale

While competitors embraced the "fabless" model, outsourcing production to Asian foundries, TI doubled down on manufacturing. This contrarian bet has created an almost insurmountable competitive advantage. TI's 300mm wafer fabs provide a 40% cost advantage over competitors using 200mm technology. The $3-5 billion investment required for each fab creates a massive barrier to entry—few companies have both the capital and the volume to justify such investments.

But scale alone doesn't create advantage; it's how you deploy it. TI uses its manufacturing prowess not to win on price but to offer unmatched product breadth. The company can profitably produce chips that generate just $50,000 annually because that same fab simultaneously produces thousands of other products. Competitors focusing on high-volume products can't match this economic model.

The Analog Moat: Why "Boring" Chips Are So Valuable

Digital semiconductors grab headlines—Nvidia's AI chips, Apple's M-series processors—but analog semiconductors generate superior economic returns. Why? Three fundamental reasons:

First, longevity. A power management chip designed in 2010 might still be selling in 2030. This long product lifecycle means R&D investments amortize over decades, not quarters. Second, fragmentation. The analog market consists of thousands of niches, each too small to attract focused competition but collectively massive. Third, design complexity. Analog design remains stubbornly resistant to automation. While digital design uses standardized blocks and automated tools, analog requires understanding of real-world physics that varies with temperature, voltage, and manufacturing variations.

TI recognized these dynamics early. By focusing on "catalog" products—standardized chips solving common problems—rather than custom solutions for specific customers, TI built a library of intellectual property that compounds in value over time.

Acquisition Strategy: Buying for Technology AND Market Access

TI's acquisition track record stands out in an industry littered with failed mergers. The key differentiator: TI buys for strategic fit, not financial engineering. The Burr-Brown acquisition brought precision analog expertise TI couldn't develop internally. National Semiconductor added 5,000 customers with minimal overlap. Each deal strengthened TI's competitive position rather than just adding revenue.

Equally important is what TI doesn't do: it doesn't overpay for "transformational" deals in hot markets. While competitors spent billions chasing mobile baseband or AI accelerators, TI methodically acquired analog specialists at reasonable valuations. The National Semiconductor premium looked expensive at 80%, but the industrial logic was sound—combining portfolios created cost and revenue synergies that justified the price within two years.

Capital Allocation Excellence

TI's capital allocation framework is beautifully simple: invest to strengthen competitive advantages, return excess cash to shareholders. The company maintains R&D spending at 10-12% of revenue—enough to stay competitive but not chasing moonshots. Capital expenditure focuses on 300mm capacity that provides structural cost advantages. Everything else goes to shareholders through dividends and buybacks.

This discipline shows in the numbers. Over the past two decades, TI has returned over $50 billion to shareholders while simultaneously investing in market leadership. The company doesn't hoard cash for "strategic flexibility" or pursue ego-driven acquisitions. Management compensation aligns with free cash flow per share, ensuring leaders think like owners.

Long-term Thinking in a Cyclical Industry

Semiconductor markets are notoriously cyclical, with boom-bust patterns that destroy companies lacking financial discipline. TI's approach: build through downturns when assets are cheap, harvest during upturns when demand exceeds supply. The company added significant 300mm capacity during the 2008 financial crisis when equipment was available at distressed prices. This counter-cyclical investment created the cost structure that dominates today.

TI also maintains product availability through cycles, even when economically suboptimal. Customers know TI won't abandon products during downturns or allocation during shortages. This reliability creates customer loyalty worth far more than short-term profit optimization.

The Calculator Monopoly: A Case Study in Market Dominance

TI's graphing calculator business offers a microcosm of the company's broader strategy. Despite smartphones having superior computational capability, TI maintains 80% market share in educational calculators with gross margins exceeding 50%. How? By understanding that the customer isn't the student but the educational system. TI provides curricula, teacher training, and standardized testing compatibility that creates massive switching costs. Competitors offering better technology at lower prices fail because they're solving the wrong problem.

This same philosophy applies to industrial analog: customers don't want the best chip; they want the chip that solves their problem with minimal risk. TI's extensive application notes, reference designs, and engineering support create solutions, not just components. A purchasing manager won't risk a production line to save pennies per chip.

The meta-lesson: in B2B markets, switching costs often matter more than product superiority. Building these switching costs through ecosystem development, customer relationships, and solution completeness creates more value than pure technological innovation.

X. Analysis & Bear vs. Bull Case

Bull Case: The Compound Effect of Competitive Advantages

Texas Instruments sits at the intersection of several powerful secular trends that should drive growth for decades. The electrification of everything—from vehicles to industrial equipment to home appliances—requires ever more analog semiconductors for power management, sensor interfaces, and motor control. The global analog semiconductors market size was valued at USD 87.5 billion in 2024 and is estimated to grow at 7.4% CAGR from 2025 to 2034. The growth of analog semiconductor market is attributed to growing demand for energy efficient devices, the growth of IoT and 5G, and increasing trend towards automotive electrification.

TI's dominant market position provides unmatched competitive advantages. The latest analog semiconductor industry ranking shows that Texas instruments still holds a firm grip on the top spot with annual sales of $14.1 billion and 19% market share. Moreover, TI's 2021 analog revenue accounted for 86% of its $16.3 billion in IC sales. This leadership isn't just about size—it's about the network effects from having the broadest catalog, the most extensive customer relationships, and the deepest application expertise.

The automotive transformation alone could double TI's addressable market. Growing shift towards EVs is a major factor driving the market growth. Analog semiconductors are important for the different key functions that occur in an EV, including power management, battery charging, sensor systems, and motor control. According to IEA, the global registrations of electric cars reached to 14 million by 2023. Demand for analog components is increasing with the growth of the EV industry due to their crucial role in the development and operation of electric vehicles. With automotive currently representing just 21% of revenue, TI has substantial runway as vehicles transform into computers on wheels.

The manufacturing advantage continues to widen. TI's 300mm fabs provide a 40% cost advantage that competitors can't match without massive capital investment. With the CHIPS Act providing $1.6 billion in support, TI can accelerate capacity expansion while maintaining strong returns on capital. This scale advantage becomes more valuable as geopolitical tensions make supply chain reliability paramount.

TI's capital allocation excellence ensures shareholders capture value creation. The company's commitment to returning 100% of free cash flow to shareholders, combined with a business model that generates consistent cash through cycles, creates a compound effect. The 21-year streak of dividend increases demonstrates management's confidence in the business model's durability.

Finally, the analog market structure favors incumbents. High switching costs, long product lifecycles, and fragmented competition create a moat that strengthens over time. As TI's catalog grows and customer relationships deepen, the cost for competitors to displace TI increases exponentially.

Bear Case: Structural Challenges in a Mature Market

Despite TI's strong position, several factors could pressure future returns. The semiconductor industry's cyclical nature hasn't disappeared—it's merely been masked by pandemic-driven demand distortions. Texas Instruments annual revenue for 2024 was $15.641B, a 10.72% decline from 2023. Texas Instruments annual revenue for 2023 was $17.519B, a 12.53% decline from 2022. As inventory normalization continues, revenue could remain pressured through 2025.

China represents both opportunity and risk. With approximately 25% of revenue exposed to Chinese customers, TI faces multiple threats: domestic Chinese competitors backed by government subsidies, potential technology restrictions, and broader geopolitical tensions. Chinese analog companies like SG Micro and 3Peak are rapidly improving capabilities while offering 30-50% price discounts. In commodity analog products, patriotic purchasing preferences could erode TI's market share.

The competitive landscape is intensifying. Texas Instruments Inc (NASDAQ:TXN) reported a 2% year-over-year growth in Analog revenue after eight quarters of decline. The company is strategically emphasizing growth in the industrial and automotive markets, which now make up about 70% of its revenue. While TI has stabilized analog revenue, embedded processing continues struggling, down 18% year-over-year. Competitors like Analog Devices have consolidated (acquiring Maxim and Linear Technology) to challenge TI's scale advantages.

Technology transitions pose subtle risks. While analog semiconductors don't follow Moore's Law, system-level changes can obsolete entire product categories. Electric vehicles eliminate dozens of analog chips used in internal combustion engines. Software-defined systems reduce hardware complexity. AI at the edge might consolidate multiple analog functions into integrated solutions. TI's broad exposure means it will catch these trends, but the transition could pressure margins.

Market maturity in key segments limits growth potential. In Q4, industrial and automotive markets behaved similarly to the overall company, with some sectors like industrial automation and energy infrastructure still declining. Industrial automation, TI's largest market, faces headwinds from manufacturing reshoring (which initially reduces equipment purchases) and efficiency improvements that reduce semiconductor content. The post-pandemic boom in industrial investment may have pulled forward years of demand.

Valuation poses another challenge. At 35x trailing earnings and 8x sales, TI trades at premium multiples that assume continued execution excellence. Any stumble—whether from share loss, margin pressure, or cycle timing—could trigger multiple compression. The stock's 60% outperformance versus the SOX semiconductor index over five years has created high expectations.

Balancing the Arguments

The bull and bear cases aren't mutually exclusive—both can be simultaneously true. TI's structural advantages are real and durable, but they don't eliminate cyclical pressures or competitive threats. The company will likely continue gaining share in attractive markets while facing pressure in commoditized segments.

The key question for investors isn't whether TI is a good company—it clearly is—but whether current valuations adequately reflect both the opportunities and risks. The company's track record suggests management will navigate challenges successfully, but the margin of safety has narrowed considerably.

Smart investors might view TI like its own analog products: not exciting, but essential; not the fastest growing, but the most reliable; not cheap, but valuable. In a portfolio context, TI offers exposure to secular electrification trends with lower risk than pure-play electric vehicle or renewable energy stocks.

XI. Epilogue & "What Would We Do?"

The Future of Analog in an Increasingly Digital World

Standing at the intersection of the physical and digital worlds, analog semiconductors face a paradox: as the world becomes more digital, it needs more analog chips to interface with physical reality. Every sensor that monitors temperature, pressure, or motion requires analog-to-digital conversion. Every motor that moves, speaker that vibrates, or battery that charges needs analog control. TI's bet is simple but profound: the physical world isn't going away, and bridging atoms to bits will only become more critical.

The AI revolution, rather than threatening analog, amplifies its importance. Training large language models happens in data centers, but AI inference increasingly occurs at the edge—in cameras, automobiles, and industrial equipment. Each edge AI device requires sophisticated power management to balance performance and battery life, sensor interfaces to collect real-world data, and communication circuits to share insights. TI's embedded processors with integrated analog functionality are perfectly positioned for this edge AI explosion.

Consider autonomous vehicles: they're essentially analog sensing platforms with digital brains. Each vehicle requires dozens of radar transceivers, hundreds of power regulators, and thousands of analog components to function safely. As autonomy levels increase, so does analog content. TI's automotive revenue could triple as full autonomy deploys over the next decade.

Electric Vehicles and Renewable Energy as Growth Drivers

The energy transition represents TI's largest growth opportunity since the mobile phone revolution. Electric vehicles require 5-10x more semiconductor content than internal combustion vehicles, and most of that increase is analog: battery management systems, inverter controls, charging circuits, and thermal management. TI's broad portfolio positions it to capture value across the entire EV ecosystem, from the vehicle to the charging infrastructure to the grid connections.

Renewable energy creates similar opportunities. Every solar panel needs power optimizers and inverters. Wind turbines require sophisticated control systems to maximize efficiency. Grid-scale batteries demand precise cell balancing and thermal management. The International Energy Agency projects $2 trillion in annual clean energy investment by 2030—much of it requiring analog semiconductors that TI produces.

But the real opportunity lies in system integration. As power systems become more complex, customers increasingly want complete solutions, not just components. TI's ability to provide reference designs combining power management, sensing, and control creates competitive advantages beyond individual chip performance.

Geographic Expansion vs. Reshoring Debate

TI faces a delicate balance between accessing global growth and navigating geopolitical tensions. China remains critical—both as a market and as a competitive threat. The company's approach has been pragmatic: maintain presence to serve multinational customers manufacturing in China while avoiding dependence on Chinese domestic demand.

The reshoring trend actually benefits TI. As customers move production from Asia to North America and Europe, they often upgrade to more sophisticated automation requiring additional semiconductors. TI's U.S. manufacturing base becomes a competitive advantage as customers prioritize supply chain security over minimal cost savings.

The company's planned fab in Europe and expanded U.S. capacity provides flexibility to serve customers wherever they manufacture. This geographic diversification, while expensive, creates options valuable in an uncertain world.

What Would We Do?

If we were running Texas Instruments today, we would pursue five strategic initiatives:

First, accelerate the platform strategy. Rather than selling individual chips, we'd bundle complete solutions for specific applications—motor control for industrial robots, battery management for energy storage, sensor fusion for autonomous vehicles. This would increase switching costs and capture more value per design win.

Second, invest aggressively in compound semiconductors. While silicon dominates today's analog market, materials like gallium nitride (GaN) and silicon carbide (SiC) enable superior performance in high-power applications. TI's manufacturing expertise could create advantages in these emerging technologies before they become commoditized.

Third, build software and services layers. The highest-margin semiconductor companies increasingly monetize software and services, not just silicon. TI could offer cloud-based design tools, AI-powered optimization services, and subscription-based support that creates recurring revenue streams beyond one-time chip sales.

Fourth, pursue strategic partnerships in China rather than direct competition. Partner with local companies for commodity products while focusing TI's efforts on differentiated solutions. This would reduce political risk while maintaining market access.

Fifth, prepare for the post-Moore's Law era by investing in novel computing architectures. As digital scaling slows, hybrid analog-digital processing could provide efficiency advantages. TI's unique position spanning both domains could enable breakthrough innovations in neuromorphic computing or quantum sensing.

Final Reflections

Texas Instruments' journey from seismic sensors to semiconductor giant demonstrates that sustainable competitive advantages come not from chasing the latest technology but from patient capital allocation, operational excellence, and deep customer relationships. The company that invented the integrated circuit succeeded not by staying at the cutting edge but by mastering the fundamentals.

In an industry obsessed with the next big thing, TI proves that sometimes the best strategy is to perfect the boring basics. While competitors chase headlines with AI chips or quantum computing, TI quietly ships billions of analog semiconductors that make modern life possible. It's not glamorous, but it's enormously profitable.

The next decade will test whether TI's analog focus remains relevant as computing paradigms shift. But betting against a company that has successfully navigated every major technology transition of the past century seems unwise. More likely, TI will continue its pattern: adapting when necessary, pivoting when required, but always maintaining the discipline that has created one of the semiconductor industry's most enduring success stories.

XII. Recent News

Texas Instruments reported fourth quarter 2024 results on January 23, 2025, showing resilience despite continued market headwinds. Texas Instruments Incorporated (TI) (Nasdaq: TXN) today reported fourth quarter revenue of $4.01 billion, net income of $1.21 billion and earnings per share of $1.30. Earnings per share included a 2-cent benefit that was not in the company's original guidance. Regarding the company's performance and returns to shareholders, Haviv Ilan, TI's president and CEO, made the following comments: "Revenue decreased 3% sequentially and 2% from the same quarter a year ago.

The company's free cash flow generation remains robust despite revenue pressures. "Our cash flow from operations of $6.3 billion for the trailing 12 months again underscored the strength of our business model, the quality of our product portfolio and the benefit of 300mm production. Free cash flow for the same period was $1.5 billion. "Over the past 12 months we invested $3.8 billion in R&D and SG&A, invested $4.8 billion in capital expenditures and returned $5.7 billion to owners.

Looking ahead to the first quarter of 2025, management provided cautious guidance reflecting ongoing inventory corrections. "TI's first quarter outlook is for revenue in the range of $3.74 billion to $4.06 billion and earnings per share between $0.94 and $1.16. We now expect our 2025 effective tax rate to be about 12%."

The end market dynamics show mixed trends. Analog Revenue: Grew 2% year-over-year. Embedded Processing: Declined 18% year-over-year. The analog business has returned to growth after eight quarters of decline, validating TI's strategic focus on this segment. However, embedded processing continues to face challenges from weak industrial demand.

In a significant development for manufacturing capacity, In November 2024, Texas Instruments announced they had opened a new product distribution centre in Germany. This development intends to make 7,500 shipments daily of TI's range of analog and embedded processing semiconductors to European customers. It aims to give faster, effective, flexible, and dependable service to its clients in Europe.

The company also continues expanding its R&D footprint globally. In September 2024, Texas Instruments (TI) expanded its R&D Units in India to launch cost-effective semiconductor solutions. The strategic goal behind the expansion in its R&D is to provide cost-effective and high-quality solutions for the Indian market.

Management commentary during the Q4 earnings call provided insight into market conditions. For Q1, we expect a seasonal decline, particularly in personal electronics, which usually shows a significant drop in Q1. Automotive and industrial markets should see less pronounced declines. In Q4, industrial and automotive markets behaved similarly to the overall company, with some sectors like industrial automation and energy infrastructure still declining. In automotive, China grew but not enough to offset declines in Europe, the US, and Japan.

XIII. Links & Resources

Primary Sources: - Texas Instruments Investor Relations: investor.ti.com - Annual Reports (2015-2024): investor.ti.com/financial-information/annual-reports - Q4 2024 Earnings Release: investor.ti.com/news-releases - Historical SEC Filings: sec.gov/edgar/search

Industry Analysis: - Semiconductor Industry Association: semiconductors.org - IC Insights Analog Market Report: icinsights.com - Gartner Semiconductor Forecast: gartner.com/en/supply-chain

Historical Documentation: - "The Chip: How Two Americans Invented the Microchip and Launched a Revolution" by T.R. Reid - Computer History Museum TI Archives: computerhistory.org/collections - IEEE History Center: ethw.org/Texas_Instruments_Inc - Nobel Prize Biography of Jack Kilby: nobelprize.org/prizes/physics/2000/kilby

Books on TI and Semiconductor History:

- "Engineering the World: Stories from the First 75 Years of Texas Instruments" by Caleb Pirtle III

- "Crystal Fire: The Invention of the Transistor" by Michael Riordan and Lillian Hoddeson

- "The Man Behind the Microchip: Robert Noyce and the Invention of Silicon Valley" by Leslie Berlin

- "Direct from Dell: Strategies that Revolutionized an Industry" (mentions TI's influence)

Technical Resources: - TI Product Catalog: ti.com/products - TI Reference Designs: ti.com/reference-designs - Application Notes Archive: ti.com/lit - E2E Engineer Community: e2e.ti.com

Financial Analysis: - Morningstar: morningstar.com/stocks/xnas/txn - S&P Capital IQ - Bloomberg Terminal: TXN US Equity - FactSet

Industry Publications: - EE Times: eetimes.com - Semiconductor Engineering: semiengineering.com - Planet Analog: planetanalog.com - IEEE Spectrum: spectrum.ieee.org

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube