Tradeweb: The Story of Electronic Fixed Income Trading

I. Introduction & Episode Roadmap

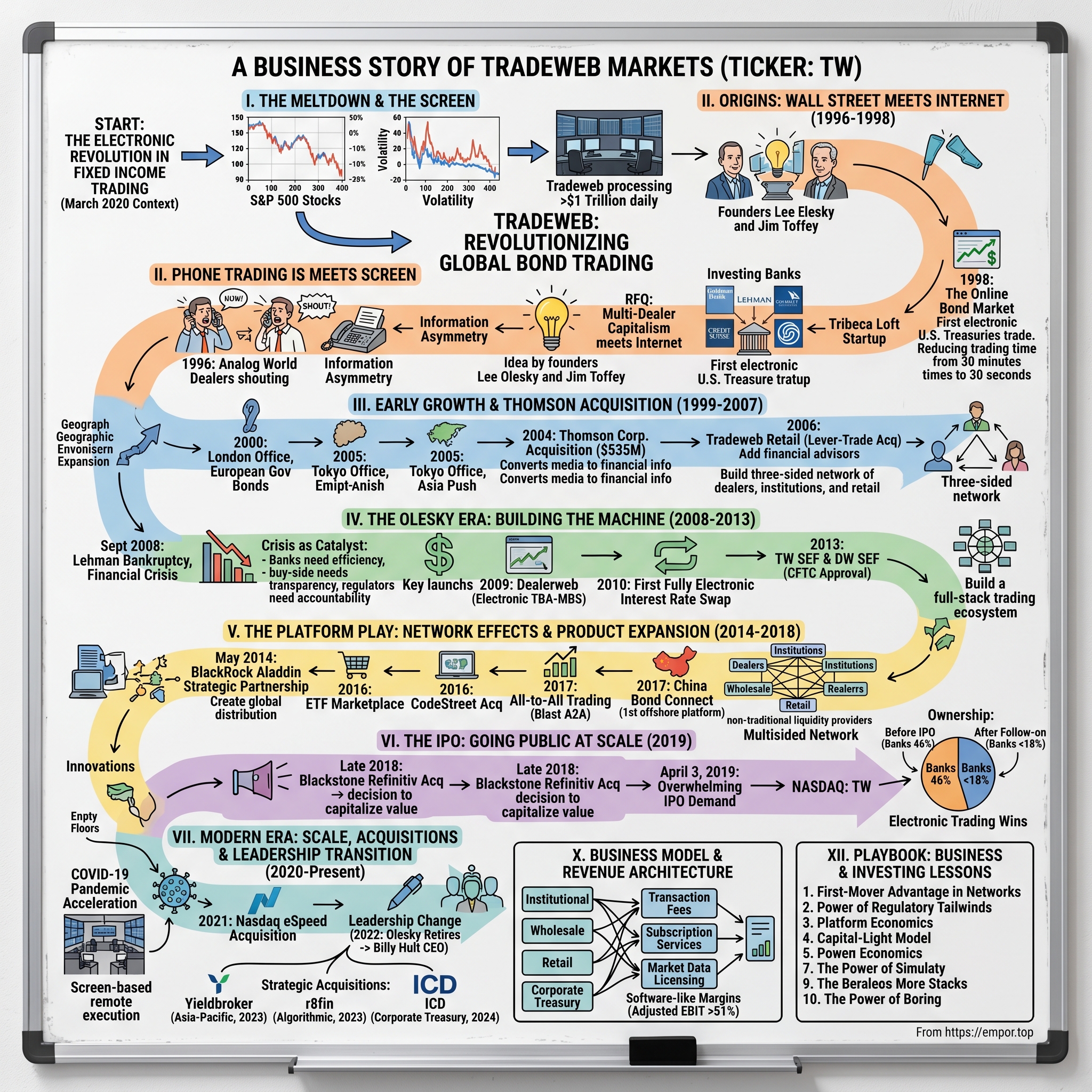

Picture this: It's March 2020, and the world's financial markets are melting down. In the span of just three weeks, the S&P 500 has crashed 34%. Treasury yields are whipsawing like penny stocks. Corporate bonds—supposedly the boring, stable part of portfolios—are experiencing price swings not seen since 2008.

But here's what's different this time: While traders in 1987 or even 2008 would have been screaming into phones and frantically faxing orders, this crisis is playing out on screens. Silent. Digital. Efficient. At the center of this electronic storm sits Tradeweb, processing over $1 trillion in daily trading volume as the world's bond markets convulse.

How did we get here? How did a startup launched in the early days of the internet—when most of Wall Street still thought email was a fad—become the dominant force in electronic bond trading?

This is the story of Tradeweb (NYSE: TW), the international financial technology company that quietly revolutionized how the world trades fixed income. Today, they build and operate electronic over-the-counter marketplaces for bonds, ETFs, and derivatives, serving everyone from Goldman Sachs to the Bank of Japan to your grandmother's pension fund. In 2020 alone, the firm's average daily trading volume across all asset classes exceeded $837 billion. That's not a typo—$837 billion per day.

What makes Tradeweb fascinating isn't just the scale—it's the journey. This is a tale of perfect timing meets relentless execution. Of how two traders saw the internet not as a threat to Wall Street's old boys' club, but as the tool that would finally crack it open. It's about first-mover advantage, network effects that compound like interest, and regulatory tailwinds that turned from gentle breezes into hurricane-force accelerants.

We'll trace the arc from those first experimental trades in 1998 to today's electronic trading behemoth. We'll explore how financial crises became catalysts for growth, how regulations meant to constrain Wall Street actually turbocharged Tradeweb's business, and how a company that started with U.S. Treasuries now touches virtually every corner of global finance.

Along the way, we'll unpack the business model that generates 50%+ operating margins, the platform dynamics that make this a winner-take-most market, and why, despite all the success, the electronification of fixed income might still be in its early innings.

Buckle up. This is going to be a ride through the plumbing of modern finance—and trust us, the plumbing is where the money flows.

II. Origins: Wall Street Meets the Internet (1996-1998)

The year is 1996. Netscape has just gone public. Amazon is selling books—just books. And if you want to buy a corporate bond, here's your workflow: You pick up the phone. You call your dealer at Goldman or Morgan Stanley. "What've you got in ten-year IBM paper?" you ask. They put you on hold, check their inventory, come back with a price. You don't like it? Call Merrill. Then Lehman. Then Bear Stearns. Each call takes five minutes. Each dealer knows you're shopping around but not what prices you're seeing. Information asymmetry is the name of the game, and the house always wins.

Into this analog world stepped Lee Olesky and Jim Toffey, two traders who had a radical thought: What if bond trading worked more like... eBay? Lee Olesky, an American financial executive and entrepreneur, co-founded Tradeweb in 1996 alongside Jim Toffey. Olesky was a lawyer by training who'd taken an unusual path to Wall Street—history degree from Tulane, law degree from George Washington, then a leap into derivatives at Credit Suisse First Boston in 1989. By 1993, he'd climbed to Chief Operating Officer for Fixed Income Americas. Toffey, his colleague at Credit Suisse, shared his vision of what bond trading could become.

The pre-internet bond market they knew was a Dickensian nightmare of inefficiency. Trading floors were noisy, energetic places, where traders yelled into phones—and at each other—as they bought and sold securities. Want to trade a corporate bond? If a trader needed to know the price on a U.S. Treasury bond, they'd have to call any number of different banks to figure out what they were quoting. It was a manual and sometimes laborious process. Each dealer had their own inventory, their own prices, their own relationships. Information was power, and the dealers held all the cards.

But Olesky and Toffey saw something different. They saw eBay launching in September 1995 and thought: Why not bonds? Lee Olesky, then at Credit Suisse First Boston, and his colleague Jim Toffey, recognized the potential of this new technology to transform the piece of the financial sector they knew best: the fixed-income market.

The revolutionary idea was elegantly simple: create a multi-dealer platform where institutional investors could request quotes (RFQ) from multiple dealers simultaneously. No more sequential phone calls. No more information asymmetry. Just send your request electronically to five, ten, fifteen dealers at once and let them compete for your business. It was capitalism meets the internet—transparent, efficient, beautiful.

Founded in 1996, with Toffey as CEO and Olesky as chairman, Tradeweb was set up as a consortium-backed venture that counted Goldman Sachs, Salomon Brothers, Lehman Brothers and Credit Suisse First Boston as its investors. This was counterintuitive genius. While the banks were the very businesses that a company like Tradeweb could ultimately supersede in the bond markets, the rationale of bringing them into the fold was clear for Olesky, who used relationships he had built up previously while at the industry group the Public Securities Association in Washington, D.C. to generate interest.

Think about the audacity of that pitch: "Hey Goldman, hey Lehman, we're building a platform that will reduce your margins by increasing price transparency. Want to invest?" But Olesky understood something fundamental about network effects—you need liquidity to attract users, and you need users to create liquidity. The banks had the inventory. They were the liquidity.

Toffey, Olesky, and the Tradeweb team—based out of a loft in New York City's Tribeca neighborhood ("the garage of New York," as Olesky called it)—devised a way for hedge funds, mutual funds, and insurance companies to be able to retrieve the prices electronically from the banks who were signed onto the platform.

Early technology challenges were immense. This was 1996—dial-up modems, Windows 95, servers that crashed if you looked at them wrong. They were trying to build real-time trading infrastructure on technology that could barely handle email. Market skepticism ran even deeper. Bond traders had built entire careers on relationships, on knowing who needed what and when. "You're going to replace my relationships with a website?" they'd scoff.

But then came 1998, and everything changed.

Tradeweb was launched in 1998, creating the first multi-dealer online trading network for U.S. Treasuries. The company went live by offering Wall Street what it originally called "The Online Bond Market". That first trade—a simple U.S. Treasury transaction—represented something profound. It wasn't just a bond changing hands; it was the first crack in a centuries-old edifice.

The platform was revolutionary for its time. The Online Bond Market may pale in comparison to the technology that Tradeweb's current offerings entail, which include an artificial intelligence pricing strategy for corporate bonds, but, for the time, it was revolutionary. An institutional investor could now see prices from multiple dealers on one screen, click to trade, and have the entire transaction documented electronically. What once took thirty minutes now took thirty seconds.

"Since our first U.S. Treasury trade in 1998, we've been developing technology to improve the markets—one milestone at a time," the company would later reflect. But in that moment, staring at screens in a Tribeca loft, Olesky and Toffey had done something that would reshape global finance: they'd made the first bond market truly electronic.

The old guard didn't know it yet, but the revolution had begun.

III. Early Growth & Thomson Acquisition (1999-2007)

By 1999, as the dot-com bubble approached its apex, Lee Olesky made a move that seemed, at first glance, like abandoning ship. He left Tradeweb—the company he'd co-founded just three years earlier—to chase another opportunity across the Atlantic.

In 1999, Olesky left Credit Suisse and relocated to London to co-found BrokerTec Global, another joint venture platform. He served as the founding CEO until BrokerTec was acquired in 2002 by ICAP plc. BrokerTec was targeting the inter-dealer market—the wholesale trading between banks themselves—while Tradeweb focused on dealer-to-customer trades. It was the same electronification playbook, different market segment.

This wasn't betrayal; it was education. Olesky was learning how to build electronic trading platforms in different contexts, different geographies, different regulatory environments. When ICAP acquired BrokerTec in 2002, Olesky had his exit—and his Harvard Business School case study in platform building. More importantly, he was ready to return home.

Following the acquisition, Olesky rejoined Tradeweb as President in 2002, but he didn't return to New York. He remained in London, where he focused on building out Tradeweb's presence in Europe. This geographic positioning was strategic—European markets were years behind the U.S. in electronic trading adoption, presenting massive growth opportunity.

Meanwhile, back at headquarters, Tradeweb was expanding its footprint methodically. In 2000, the firm opened its London office and launched marketplaces for trading European government bonds and agencies. The playbook was working: start with the most liquid, standardized products (government bonds), prove the model, then expand into more complex instruments.

Then came the deal that would transform Tradeweb from startup to institution. In 2004, Thomson Corporation—the Canadian media and information conglomerate that would later become Thomson Reuters—acquired Tradeweb for $535 million. For a company that had launched with $8 million in funding just eight years earlier, this represented a 67x return. Not bad for a pre-profit tech company in the post-bubble wreckage.

But why would Thomson, a company known for newspapers and legal databases, want a bond trading platform? The answer lay in Thomson's broader transformation strategy. They were pivoting from traditional media to financial information services, competing with Bloomberg and Reuters (which they'd later acquire). Tradeweb wasn't just a trading platform—it was a data goldmine. Every trade, every quote request, every price point flowing through the platform represented valuable market intelligence.

Under Thomson's ownership, Tradeweb accelerated its geographic expansion. Tradeweb established its Tokyo office in 2005, starting a partnership with CanDeal to launch Canadian debt securities trading. The Asia push was prescient—Japanese government bonds were the second-largest bond market globally, and electronic trading penetration was near zero.

But the real strategic coup came in 2006 with an acquisition that seemed small at the time but would prove transformative: Tradeweb Retail was established as the firm entered the retail fixed income marketplace through the acquisition of Lever-Trade. This wasn't just about serving mom-and-pop investors directly. It was about serving the thousands of financial advisors and small institutions that sat between retail and institutional—the "missing middle" of bond trading.

The retail acquisition revealed something profound about Tradeweb's strategy. While competitors fought over the biggest banks and hedge funds, Tradeweb was building a three-sided network: dealers, institutions, and now retail. Each segment reinforced the others. More retail flow meant more liquidity for dealers. More dealers meant better prices for institutions. More institutions meant more inventory for retail. Network effects squared.

By 2007, Tradeweb's value had nearly tripled. Thomson Financial announced its plans to expand electronic trading by creating a strategic partnership with nine other global dealers through Tradeweb, valuing the company at $1.55 billion. The consortium of bank investors was growing, but more importantly, they were becoming dependent on the platform. What started as a hedge—investing in potential disruption—had become critical infrastructure.

As 2007 drew to a close, Tradeweb was processing hundreds of billions in daily volume, operating across three continents, and serving everyone from central banks to retail investors. The platform that dealers once viewed with suspicion had become indispensable.

But storm clouds were gathering. Mortgage securities were starting to crack. Credit markets were seizing up. The financial system that Tradeweb had spent a decade digitizing was about to experience its greatest stress test since the Great Depression.

Nobody knew it yet, but the financial crisis about to unfold would be Tradeweb's crucible—and its catalyst.

IV. The Olesky Era: Building the Machine (2008-2013)

September 2008. Lehman Brothers—one of Tradeweb's original founding investors—files for bankruptcy. The financial world is in freefall. Credit markets are frozen. Nobody wants to trade with anybody because nobody knows who might collapse next. It's precisely the wrong time to become CEO of a trading platform.

In 2008, Olesky became CEO, taking over from co-founder Jim Toffey who departed to pursue other opportunities. Billy Hult became president. The timing seemed catastrophic. Trading volumes were cratering. Banks were hoarding capital. The very dealers who powered Tradeweb's platform were fighting for survival.

But Olesky saw something others missed: crisis creates opportunity. When markets are melting down, when counterparty risk is extreme, when nobody trusts anybody—that's exactly when you need electronic trading most. Phone calls and relationships don't work when your relationship manager just got laid off and their firm might not exist tomorrow. What works is transparent, documented, electronic execution.

"The financial crisis was our catalyst," Olesky would later explain. Banks needed efficiency—they were firing traders by the thousands and needed technology to fill the gap. The buy-side needed transparency—they couldn't afford to not know if they were getting fair prices. Regulators needed accountability—they wanted every trade documented, time-stamped, traceable.

That same year, the firm acquired brokerage firm Hilliard Farber & Co. Inc. While others were retreating, Olesky was attacking, using the crisis to acquire talent and technology at distressed prices.

The strategic masterstroke came in 2009. It launched Dealerweb, an electronic interdealer platform for to-be-announced, or forward, mortgage-backed securities (TBA-MBS). Think about the audacity of launching a mortgage trading platform in 2009, when mortgages were literally the toxic waste that had nearly destroyed the global financial system. But Olesky understood that markets don't disappear—they evolve. Someone still needed to trade mortgages, and they needed to do it more carefully, more transparently, more electronically than ever before.

Then came 2010, and with it, a glimpse of the future. It facilitated the first fully electronic, dealer-to-customer interest rate swap to be processed by a central clearing house in the U.S. This wasn't just another product launch. This was Tradeweb positioning itself for the regulatory tsunami about to hit Wall Street.

Dodd-Frank was coming. The Volcker Rule was coming. Basel III was coming. The entire regulatory framework that had governed trading since the 1930s was being rewritten, and at its heart was a simple mandate: make derivatives trading more like stock trading. Electronic. Transparent. Centrally cleared.

For most of Wall Street, Dodd-Frank was a compliance nightmare—thousands of pages of rules that would cost billions to implement. For Tradeweb, it was Christmas morning. The government was essentially mandating that trillions in derivatives trades move onto electronic platforms. Specifically, onto venues called Swap Execution Facilities (SEFs).

In 2013, the firm secured CFTC temporary approval of two wholly owned swap execution facilities (SEFs) TW SEF and DW SEF. Live SEF trading on the platforms began on October 2, 2013. This wasn't just regulatory compliance—it was regulatory capture in the best sense. Tradeweb had helped write the rules, provided the technology to implement them, and now owned the venues where they'd be executed.

But Olesky wasn't done building. In November 2013, the firm acquired BondDesk Group and rebranded the combined service Tradeweb Direct. This expanded their retail presence dramatically, adding thousands of financial advisors to the platform. The three-sided network was becoming a web, with each strand reinforcing the others.

By the end of 2013, Olesky had transformed Tradeweb from a simple dealer-to-customer platform into something far more ambitious: a full-stack trading ecosystem. They had institutional trading, wholesale trading, retail distribution. They had cash bonds, derivatives, mortgages. They had regulatory approval, technological infrastructure, and most importantly, liquidity.

The machine Olesky built during these crisis years wasn't just about surviving the financial crisis—it was about being positioned for what came next. Electronic trading was no longer optional; it was mandatory. The regulators had spoken. The economics were clear. The technology was proven.

The platform play was about to begin.

V. The Platform Play: Network Effects & Product Expansion (2014-2018)

May 2014. BlackRock's Manhattan offices. Larry Fink's team is staring at a problem: Aladdin, their risk management platform used by $20 trillion in assets globally, needs better execution capabilities. They need a partner who understands both technology and trading. They choose Tradeweb.

In May 2014, Tradeweb and BlackRock announced a strategic partnership in electronic trading in rates and derivatives markets for BlackRock's Aladdin clients. This wasn't just another partnership—it was a force multiplier. Every Aladdin user worldwide now had Tradeweb integration built in. Instant distribution to trillions in assets.

Olesky understood what Amazon had figured out with AWS: sometimes your most powerful product isn't a product at all—it's a platform that others build upon. The ecosystem strategy was elegant: make Tradeweb the pipes through which all electronic trading flows, regardless of who initiates it. In February 2016, Tradeweb launched an OTC marketplace for U.S.-listed ETFs aimed at institutional investors. This was strategic genius—ETFs were exploding in popularity, but institutional trading was still happening over the phone. Tradeweb brought electronic efficiency to yet another inefficient market.

Technology acquisitions accelerated. In March 2016, the company acquired CodeStreet LLC, a data-driven trade identification and workflow management software company. This wasn't about buying revenue—it was about acquiring the building blocks for the next generation of trading tools.

But the real revolution came in April 2017. The firm announced the launch of all-to-all trading on its U.S. institutional credit platform, enabling clients to trade with more than 130 dealers. This was paradigm-shifting. Traditionally, only dealers could provide liquidity—buy-side firms were price takers, not price makers. All-to-all changed that. Now a hedge fund could sell bonds directly to a pension fund. An insurance company could be a market maker. The old hierarchies were crumbling.

Following a successful beta period with over 140 active buy- and sell-side firms that resulted in more than $2.8 billion in inquiry volume, the platform was seeing real adoption. Tradeweb's Blast A2A solution allows clients to send a request for quote to a larger and more diverse network, also integrated with the Tradeweb Direct liquidity pool. The network effects were compounding—institutional, wholesale, and retail liquidity all feeding into one ecosystem.

The geographic expansion continued with a landmark achievement. In June 2017, it became the first offshore trading platform to connect with the China Foreign Exchange Trade System (CFETS), allowing investors outside of China to invest in the China Interbank Bond Market for the first time. China Bond Connect was huge—it opened up the world's third-largest bond market to international investors through Tradeweb's pipes.

Platform expansion accelerated into new asset classes. In May 2018, Tradeweb partnered with Plato to launch eBlock, a European cash equities block trading platform. In August 2018, it launched an RFQ platform for US equity options. Tradeweb was no longer just a bond platform—it was becoming the electronic trading layer for all of finance.

The culmination of this platform strategy came with a massive corporate transaction. Thomson Reuters sold a 55% majority stake in its Financial & Risk unit to private equity firm Blackstone Group LP on October 1, 2018, in a deal which valued the total F&R business at about $20 billion. This created Refinitiv, and with it, a new ownership structure for Tradeweb. Blackstone, the masters of financial engineering, now had a controlling stake through Refinitiv.

What had started as a multi-dealer RFQ platform for Treasuries had evolved into something far more powerful: a multi-sided network connecting dealers, institutions, retail investors, and now even non-traditional liquidity providers. Every new product, every new client type, every new geography added nodes to the network. And in networks, value grows exponentially with connections.

The platform was built. The network effects were compounding. All that remained was to take it public and let the market value what Olesky and team had created. The IPO machine was warming up.

VI. The IPO: Going Public at Scale (2019)

Late 2018. Blackstone's offices in New York. The private equity giants are running the numbers on their Refinitiv acquisition, and one asset keeps jumping off the page: Tradeweb. In a portfolio of financial data businesses, this electronic trading platform is growing faster, generating higher margins, and commanding better multiples than almost anything else they own. The decision becomes obvious—it's time to crystallize value. Refinitiv, the financial data firm co-owned by the Blackstone Group LP and Thomson Reuters Corp., had confidentially filed for an initial public offering of its Tradeweb Markets LLC business. The bond-trading platform could be worth more than $4 billion in an IPO—a valuation that would make the founding banks' original $8 million investment worth billions.

The decision to go public wasn't just about liquidity—it was about perception. The "bank-owned" perception problem was real. Buy-side clients were increasingly uncomfortable trading on a platform owned by their counterparties. Regulators were asking pointed questions about conflicts of interest. Going public would solve both problems: dilute bank ownership and create transparency through public market scrutiny.

Tradeweb tendered an IPO on April 3, 2019, announcing the pricing of its initial public offering of 40,000,000 shares of its Class A common stock at a price to the public of $27.00 per share. But here's where it gets interesting: the company had originally planned to sell just 27.3 million shares for $24 to $26 each. Demand was so overwhelming they increased the offering size to 36.25 million shares, then again to 40 million, and still priced above the range at $27.

The stock opened for trading on April 4, 2019, on the NASDAQ under ticker "TW"—and immediately exploded higher. The stock jumped more than 30% on its first day of trading in April 2019. According to Bloomberg, its offering was the best-performing IPO exceeding $1 billion for 2019.

The IPO raised $1.08 billion in gross proceeds, but the real story was what happened to the ownership structure. The net proceeds from the offering were used to purchase equity interests from certain existing bank stockholders. This wasn't dilution—it was liberation. The banks were cashing out, reducing their collective stake dramatically.

In October 2019, Tradeweb completed a follow-on offering of 17,287,878 shares of Class A Common stock at a price to the public of $40.75. Tradeweb Markets Inc. used the proceeds of $704.3 million from the offering to purchase equity interests from certain existing owners. Bank ownership fell to 17.3% after the follow-on—down from 46% before the IPO.

Public shareholders—led by large asset managers such as BlackRock, Invesco and T. Rowe Price—now held 28.7% of the company stock, while Refinitiv maintained a 54% majority stake. The buyers' list read like a who's who of fundamental investors. These weren't momentum traders or hedge funds—these were long-term holders who understood the platform dynamics, the network effects, the regulatory tailwinds.

The market validation was profound. Here was a company that had been quietly building infrastructure for two decades, largely invisible to public markets, suddenly valued at over $7 billion. The IPO wasn't just a liquidity event—it was a coming-out party for electronic trading.

Olesky had led Tradeweb from an early-stage startup with $8 million in financing to becoming one of the most successful IPOs of 2019. The lawyer-turned-trader who'd seen the future back in 1996 had built something remarkable: a platform that processed hundreds of billions daily, connected thousands of clients globally, and generated software-like margins from what was essentially financial plumbing.

What the IPO really meant was this: Electronic trading had won. The old world of phone calls and relationships wasn't dead, but it was dying. The future belonged to platforms, to networks, to those who could turn analog friction into digital efficiency. And Tradeweb, after twenty-one years of patient building, was perfectly positioned to capture that future.

The IPO proceeds would fund more acquisitions, more expansion, more technology. But more importantly, it gave Tradeweb currency—public stock to use for deals, credibility with regulators, transparency for clients. The machine Olesky had built was about to shift into a higher gear.

VII. Modern Era: Scale, Acquisitions & Leadership Transition (2020-Present)

March 2020. The world is shutting down. Trading floors—those cathedrals of capitalism with their banks of screens and Bloomberg terminals—are emptying out. Traders are scrambling to set up home offices, dragging monitors into spare bedrooms, trying to figure out how to execute billion-dollar trades from their kitchen tables.

For most of Wall Street, COVID-19 was a nightmare scenario. How do you maintain markets when nobody can get to the office? How do you execute trades when you can't tap your colleague on the shoulder? But for Tradeweb, the pandemic was an accelerant, pouring rocket fuel on trends that had been building for decades.

Throughout 2020 and 2021, as the COVID-19 pandemic prompted an increased shift to remote work, Olesky highlighted the accelerated reliance on electronic trading. "The vast majority of folks inside Tradeweb and at our clients are working remotely, and that change in environment provided an opportunity for firms like us. Having a good digital source of information and ability to execute is key."

The numbers told the story: Trading volumes exploded as central banks flooded markets with liquidity and volatility spiked. In 2020, the firm's average daily trading volume across all asset classes exceeded $837 billion. More importantly, electronic trading adoption accelerated by years in a matter of months. Firms that had resisted going electronic for decades suddenly had no choice. The phone-based traders working from home couldn't hear each other over barking dogs and Zoom calls. Electronic was the only way.

Tradeweb didn't waste the crisis. In June 2021, Tradeweb acquired Nasdaq's U.S. fixed income electronic trading platform, formerly known as eSpeed for $190 million in cash. This wasn't just any acquisition—eSpeed was the original competitor, the platform that had battled Tradeweb for supremacy in the early 2000s. Now it was being absorbed, its technology and client relationships integrated into the Tradeweb ecosystem.

But even as the company reached new heights, a changing of the guard was approaching. In February 2022, Olesky was appointed Chairman of the Board of Tradeweb and announced he would retire as CEO at the end of 2022. After fourteen years as CEO, twenty-six years since founding, Olesky was ready to pass the torch.

Billy Hult succeeded Olesky as CEO in January 2023. Hult wasn't an outsider—he'd been president since 2008, Olesky's right hand through the financial crisis, the IPO, the pandemic. The succession was seamless, deliberate, planned. This was institution-building at its finest.

Under Hult's leadership, the acquisition strategy has accelerated and expanded:

In August 2023, Tradeweb acquired Yieldbroker, an Australian trading platform, pushing deeper into Asia-Pacific markets where electronic trading penetration remained low.

In November 2023, Tradeweb announced it would acquire r8fin, a technology provider that specializes in algorithmic-based execution for U.S. Treasuries and interest rate futures. The transaction closed in January 2024. This wasn't about buying market share—it was about acquiring the next generation of trading technology, the algorithms that would automate what remained of human trading.

The biggest deal came in April 2024, when Tradeweb agreed to acquire Institutional Cash Distributors ("ICD"), an investment technology provider for corporate treasury organizations. The $785 million, all-cash transaction was completed in August 2024. ICD added an entirely new client channel—corporate treasurers managing trillions in short-term cash. Another network to integrate, another source of flow, another flywheel to spin.

Meanwhile, the ownership structure continued evolving. LSEG completed the US$27 billion purchase of Refinitiv from the two previous owners in late January 2021, and Refinitiv is now a subsidiary of LSEG. London Stock Exchange Group, one of the world's oldest financial institutions, now controlled the majority of one of its newest. The old guard owning the new guard—or was it the other way around?

The modern Tradeweb is a different beast than the startup that launched in that Tribeca loft. It processes over $1 trillion daily. It operates in 85 countries. It offers 50 products. The company that started with simple U.S. Treasury trades now touches virtually every corner of global finance.

But the core insight remains unchanged: Markets want to be electronic. Traders want transparency. Regulators want oversight. Technology wants to eat everything. And Tradeweb, now under Hult's leadership but still guided by Olesky's vision from the board, sits at the intersection of all these forces.

The COVID acceleration, the strategic acquisitions, the leadership transition—these weren't separate events but part of a continuous evolution. The company that had spent twenty-five years digitizing bond markets was now positioned for the next twenty-five: AI-powered trading, blockchain settlement, quantum computing for risk management. The future, whatever it holds, will flow through Tradeweb's pipes.

VIII. Business Model & Revenue Architecture

To understand Tradeweb's business model, forget everything you know about traditional exchanges. This isn't the New York Stock Exchange with its opening bell and trading floor. This isn't even Nasdaq with its electronic order book. Tradeweb is something different—a network orchestrator, a toll collector on the electronic highways of global finance.

The genius begins with the four client channels, each feeding the others in an intricate dance of liquidity:

Institutional Channel: This is the crown jewel. Tradeweb helps the world's leading asset managers, central banks, hedge funds and other institutional investors. These are the BlackRocks and PIMCOs of the world, moving billions with each trade. They come for the liquidity, stay for the efficiency, and pay handsomely for both.

Wholesale Channel (Dealerweb): Dealerweb serves the wholesale market—the inter-dealer trades where banks trade with each other. This is the plumbing behind the plumbing, where Goldman might sell bonds to JPMorgan, who sells to Citi, who sells to Deutsche. Every trade generates a fee.

Retail Channel (Tradeweb Direct): Tradeweb Direct serves financial advisory firms, RIAs, traders and buy-side investors. These aren't day traders on Robinhood—these are professional advisors managing wealth for millions of Americans. Smaller trades, but massive volume.

Corporate Treasury (ICD): The newest addition. ICD serves corporate treasury professionals managing the cash hoards of Fortune 500 companies. Apple's $200 billion cash pile? Microsoft's treasury operations? They need somewhere to park that money overnight, and increasingly, they're doing it through Tradeweb.

But here's where it gets interesting—the revenue model is brilliantly simple yet infinitely scalable:

Transaction Fees: The bread and butter. Every trade that crosses the platform generates a fee, typically calculated as a percentage of notional value. The beauty? The fees are tiny—often just fractions of a basis point—but when you're processing $1 trillion daily, fractions add up. The fee structure varies dramatically by product: Credit commands the highest fees per million (FPM) at $45.82, followed by Equities at $18.68, Rates at $2.29, and Money Markets at $0.52.

Think about that range—Credit generates nearly 90 times the revenue per dollar traded as Money Markets. This isn't random. It reflects the complexity, the bilateral nature of credit trading, the value Tradeweb adds in bringing transparency to opaque markets. A Treasury trade is simple, standardized, commoditized. A corporate bond trade requires price discovery, credit analysis, counterparty matching. Complexity equals margin.

Subscription Services: The recurring revenue stream Wall Street loves. Clients pay monthly or annual fees for access to the platform, regardless of trading volume. It's the gym membership model—most of the revenue comes from people who show up occasionally but pay consistently.

Market Data Licensing: Every trade generates data. Every quote request reveals demand. Every price point shows market depth. This information is gold, and Tradeweb sells it to anyone who needs to understand bond markets—hedge funds building models, academics doing research, regulators monitoring systemic risk.

The network effects make this model nearly impossible to disrupt. More than 3,000 clients connect to Tradeweb to form a global network. Each new client makes the platform more valuable for everyone else. More buyers attract more sellers. More sellers provide better prices. Better prices attract more buyers. It's a virtuous cycle that compounds like interest.

With leading offerings in government bonds, mortgage securities, municipal bonds, credit and derivatives, Tradeweb offers over 50 products in more than 85 countries across the globe. This isn't just scale—it's scope. A client might come for Treasury trading but stay for credit. Start with U.S. markets but expand to Europe. Begin with cash bonds but move to derivatives. Each product, each geography, each asset class becomes another hook, another reason not to leave.

The economics of this model are extraordinary. Once the technology platform is built, the marginal cost of each additional trade approaches zero. It costs Tradeweb essentially the same to process $1 billion in daily volume as $2 billion. The servers are running anyway. The code is already written. The connections are established.

This operating leverage shows up in the margins. Adjusted EBITDA margin reached 54.6%, with Adjusted EBIT margin at 51.2%. These are software-like margins in what most consider a financial services business. It's what happens when you digitize analog processes—you capture the efficiency gains as profit.

But perhaps the most brilliant aspect of the model is its resilience. In volatile markets, trading volumes spike as investors rebalance portfolios. In calm markets, the subscription revenue provides ballast. In growing markets, new issuance drives volume. In declining markets, flight-to-quality trading increases activity. Heads Tradeweb wins, tails they don't lose much.

The model is also naturally defensive. Switching costs are enormous—not just in technology integration but in workflow disruption. Imagine telling a trading desk they need to learn a new platform, rebuild their connections, retrain their systems. It's like asking someone to switch from QWERTY to Dvorak keyboards—theoretically possible, practically painful.

This is how you build a toll road on the information superhighway. You don't need to own the cars (the bonds) or employ the drivers (the traders). You just need to own the road everyone has to travel. And in electronic fixed income trading, increasingly, all roads lead through Tradeweb.

IX. Growth Drivers & Market Share Gains

The electronification of fixed income markets isn't a trend—it's a tectonic shift. And Tradeweb isn't just riding the wave; they're the surfboard, the wave, and increasingly, the ocean itself. The recent performance metrics tell a story of unstoppable momentum. Average daily volume (ADV) reached $2,547 billion in Q1 2025, representing a 33.7% increase year-over-year. Let that sink in—$2.5 trillion per day. That's more than the entire market cap of Apple changing hands daily through Tradeweb's servers.

Total revenue of $513.0 million for Q2 2025, representing a 26.7% increase year-over-year. This isn't just growth—it's acceleration. The company that took twenty years to reach its first billion in annual revenue now adds that much every six months.

The market share expansion story is even more compelling. The company maintained its leadership in rates trading, capturing a 23% share of the U.S. Treasury market. In Global Interest Rate Swaps, ADV increased from approximately $736 billion in Q2 2024 to $887 billion in Q2 2025, driving a 14% increase in market share. U.S. Treasuries ADV grew from $200 billion to $250 billion, resulting in a 24% market share increase.

But the real story is in the less liquid markets where Tradeweb's value proposition shines brightest. U.S. Cash Credit market share expanded by 13% for investment grade and 42% for high yield bonds. Global ETF institutional ADV surged by 62% year-over-year. These aren't mature markets gradually shifting electronic—these are markets in the midst of transformation.

The emerging markets opportunity reveals the international growth story. Emerging markets swaps, which reached an ADV of $42,562 million in the three months ending March 2025. Think about the trajectory—from essentially zero five years ago to over $40 billion daily. As these markets mature, as electronic trading becomes standard, Tradeweb is positioned as the infrastructure provider.

Regulatory tailwinds continue to blow strong. MiFID II in Europe mandates best execution reporting—impossible without electronic audit trails. Dodd-Frank in the U.S. requires derivative trades on SEFs—which Tradeweb operates. Basel III capital requirements make balance sheet expensive—driving banks toward electronic trading to maximize efficiency.

But perhaps the most powerful driver is the simplest: generational change. The traders who learned the business on phones are retiring. The new generation doesn't know a world without screens. They expect Amazon-like efficiency in everything, including bond trading. For them, calling five dealers for quotes isn't traditional—it's archaeological.

The technology moat keeps widening. Over 1,400 employees, including 400+ technologists, focused on creating diverse execution protocols. Tradeweb serves more than 3,000 clients in more than 85 countries. Each new protocol—portfolio trading, all-to-all, automated execution—adds another layer of stickiness.

The COVID-19 pandemic didn't create these trends—it revealed them. When traders were forced to work from home, when voice trading became impossible, electronic wasn't an option—it was the only option. Markets that might have taken a decade to go electronic did it in months. And once you've tasted that efficiency, there's no going back.

What we're witnessing isn't just market share gains—it's market creation. Every basis point of electronic penetration in a trillion-dollar market represents billions in new volume for Tradeweb. With most fixed income markets still less than 50% electronic, the runway stretches to the horizon.

X. Playbook: Business & Investing Lessons

After studying Tradeweb's quarter-century journey from startup to $30+ billion market cap juggernaut, several timeless lessons emerge—the kind that separate good businesses from generational compounders.

First-Mover Advantage in Network Effect Businesses

Tradeweb launched in 1998, years before competitors recognized the opportunity. But being first isn't enough—you have to be first with the right model. They didn't try to disintermediate dealers (that would have failed). Instead, they made dealers more efficient, then used that efficiency to attract buy-side clients, creating a two-sided network that compounds on itself. The lesson: In network businesses, the pioneer who survives becomes nearly impossible to displace.

The Power of Regulatory Tailwinds

Most companies fear regulation. Tradeweb embraced it. Every new rule—Dodd-Frank, MiFID II, Basel III—became a growth accelerant. Why? Because regulation typically demands transparency, documentation, and standardization—exactly what electronic platforms provide. The playbook: Find industries where regulation is increasing and position yourself as the compliance solution, not the compliance problem.

Platform Economics: Start with One Side, Then Expand

Tradeweb's genius was starting with dealer-to-customer trades, getting dealers comfortable, then expanding to dealer-to-dealer, then all-to-all. Each expansion made the platform more valuable for everyone. It's the same playbook Amazon used—start with books, win trust, then sell everything. The key insight: Don't try to boil the ocean. Dominate one use case, then expand adjacently.

Timing Technology Shifts

Tradeweb rode three major technology waves perfectly: - Internet Era (1996-2008): Moving from phones to screens - Cloud Era (2009-2019): Scaling globally without massive infrastructure - AI Era (2020-present): Automated execution, predictive analytics, intelligent routing

Each wave multiplied the value of the previous one. The lesson: Great businesses don't just adopt new technology—they're positioned to maximize each successive wave.

Building Trust in Financial Infrastructure

Tradeweb processes over $1 trillion daily. One major outage could crater trust forever. They've built that trust through two principles: gradual expansion (prove reliability in Treasuries before touching mortgages) and radical transparency (show all quotes, document everything). In infrastructure businesses, trust is your moat.

M&A Strategy: Buy Technology and Client Relationships

Look at Tradeweb's acquisitions—CodeStreet (technology), Yieldbroker (geography), ICD (new client channel), r8fin (algorithms). They're not buying revenue; they're buying capabilities and relationships that would take years to build organically. The discipline: Only acquire what accelerates your network effects.

Managing Multi-Stakeholder Complexity

Tradeweb serves dealers who compete with each other, buy-side firms who negotiate against dealers, and regulators who oversee everyone. Managing these competing interests requires Swiss-like neutrality. They've done it by making everyone better off—dealers get efficiency, buy-side gets transparency, regulators get oversight. The principle: In complex ecosystems, create win-win-win scenarios.

Capital-Light Business Model with High Margins

Adjusted EBITDA margin expanding to 54.6%, an increase of 88 basis points year-over-year. Adjusted EBIT margin improved to 51.2%, up 116 basis points from the prior year. These are software margins in a financial services wrapper. Once the platform is built, every additional trade is nearly pure profit. The insight: The best businesses have high fixed costs and near-zero marginal costs.

The Power of Boring

Tradeweb isn't sexy. Bond trading infrastructure doesn't make headlines like social media or electric vehicles. But boring businesses with mission-critical functions and high switching costs can compound for decades. As Buffett says, "Lethargy bordering on sloth remains the cornerstone of our investment style."

Creating Your Own Luck

Tradeweb seems lucky—launching just as the internet exploded, going public just before COVID accelerated electronic trading. But they created that luck by being positioned for whatever came next. They built for regulatory changes before they happened, invested in technology before it was proven, expanded internationally before it was profitable.

The meta-lesson might be the most important: Great businesses aren't built in quarters or even years—they're built over decades. Tradeweb's overnight success took twenty-five years. In an era obsessed with quick wins and growth hacks, sometimes the biggest edge is simply patience, persistence, and compound growth.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Secular Story is Just Beginning

The bulls see Tradeweb as owning the tollbooth on an increasingly busy highway. Electronic trading penetration in fixed income sits around 40% globally, compared to 95%+ in equities. Even reaching 60% penetration—highly conservative given regulatory and demographic tailwinds—represents a 50% expansion of Tradeweb's addressable market.

The network effects create winner-take-most dynamics that are only strengthening. Every new client makes the platform more valuable for existing clients. Every new product creates cross-selling opportunities. Every acquisition adds another strand to an increasingly unbreakable web. Competitors can copy features but can't replicate twenty-five years of trust, relationships, and liquidity.

The regulatory environment continues to favor electronic trading. New rules around best execution, transaction reporting, and capital requirements all push trading onto platforms. Climate disclosure requirements, ESG mandates, and systemic risk monitoring all require the kind of data that only electronic platforms can provide. Regulation isn't a headwind—it's a permanent tailwind.

International expansion opportunities remain massive. Asian fixed income markets are where U.S. markets were in 2000—dominated by voice trading, relationship-driven, opaque. As these markets mature and open up, Tradeweb's proven playbook and technology platform position them as the natural winner. China alone represents a $20 trillion bond market that's barely electronic.

Adjacent product opportunities could double the business. Commodities, foreign exchange, private credit, digital assets—all need the same market structure solutions Tradeweb provides. The company has the technology, the clients, and the credibility to expand into any asset class that needs electronic trading infrastructure.

Bear Case: The Risks Are Real

The bears point to legitimate concerns. Competition from Bloomberg, MarketAxess, and direct dealer platforms is intensifying. Bloomberg has infinite resources and captive data terminals. MarketAxess owns the high-yield space. Dealers are building their own platforms to recapture economics. The competitive moat might be narrower than it appears.

Fee compression risk looms large in mature products. U.S. Treasuries—Tradeweb's first and largest market—already trade at razor-thin margins. As products mature and commoditize, fees inevitably compress. The company needs constant innovation and new products just to maintain revenue growth.

Technology disruption risk can't be ignored. Blockchain promises peer-to-peer trading without intermediaries. DeFi protocols are experimenting with automated market making. Quantum computing could revolutionize risk management. What if the next technology wave doesn't favor incumbents?

Cyclical exposure to trading volumes creates earnings volatility. In calm markets, volumes drop. In frozen markets, nobody trades. Unlike subscription software, transaction revenue is inherently volatile. A prolonged period of low volatility could pressure growth and multiples.

Regulatory changes could alter market structure unfavorably. What if regulators decide electronic trading concentration is a systemic risk? What if they mandate interoperability between platforms? What if they cap fees? Regulation giveth, but regulation can also taketh away.

The Verdict: Structural Growth Wins

On balance, the bull case appears stronger. The secular trend toward electronification has decades to run. Network effects grow stronger over time, not weaker. The company generates 50%+ margins and throws off cash. Management has proven ability to navigate cycles and competition.

But the key insight is that Tradeweb doesn't need everything to go right. They don't need blockchain to fail or competitors to disappear. They just need fixed income markets to continue modernizing—a trend as certain as death, taxes, and technological progress.

The valuation framework for marketplace businesses suggests paying up for quality. The best marketplaces—think Visa, CME, MSCI—trade at premium multiples for decades because their economics improve over time. Tradeweb exhibits the same characteristics: network effects, pricing power, capital efficiency, secular growth.

For long-term investors, the question isn't whether Tradeweb is expensive at 40x earnings. It's whether you believe fixed income trading will be more electronic in ten years than today. If yes, Tradeweb is positioned to capture an outsized share of that transition.

The bear case risks are real but manageable. Competition has always existed. Fees have always compressed in mature products. New technologies have always threatened incumbents. Yet Tradeweb has navigated all these challenges for twenty-five years while compounding at 20%+ annually.

XII. Epilogue & "If We Were CEOs"

Billy Hult sits in the CEO chair that Lee Olesky occupied for fourteen years, inheriting a machine that processes over $2 trillion daily and generates software-like margins. But inheriting success might be harder than building it. The founder can break things; the successor must optimize without destroying what works.

Hult's priorities are already clear: technology, expansion, and platform integration. The appointment of Sherry Marcus as Tradeweb's Head of AI in May shows strategic focus. "Sherry's extensive experience and leadership will be instrumental in advancing our AI capabilities to new levels of sophistication".

If We Were CEO: The Strategic Playbook

AI and Automation Opportunities: The immediate opportunity isn't replacing traders—it's augmenting them. Build AI that predicts optimal execution timing, identifies hidden liquidity, and automates routine trades. Start with government bonds (standardized, liquid) then expand to credit (complex, relationship-driven). The goal: make every trader on the platform perform like the best trader.

Crypto/Digital Assets Strategy: Don't fight the future, embrace it carefully. Partner with established crypto exchanges for technology learning. Build infrastructure for tokenized bonds—same securities, new wrapper. Position Tradeweb as the bridge between traditional finance and DeFi, not as opposition to either. The killer app might be enabling 24/7 trading of traditional assets on blockchain rails.

China and Emerging Markets Expansion: The China Bond Connect relationship is the beachhead. Deepen it. Build local partnerships that satisfy regulatory requirements while maintaining control. Replicate the playbook in India, Brazil, Indonesia—markets with growing domestic capital pools and increasing international investment. The opportunity: be the Bloomberg of emerging market bonds.

Build vs. Buy vs. Partner Decisions: - Build: Core trading technology, AI capabilities, risk management systems - Buy: Adjacent client channels (like ICD), geographic presence (like Yieldbroker), specific technologies (like r8fin) - Partner: Blockchain experiments, cryptocurrency trading, regulatory technology

The discipline: only build what's core to competitive advantage, buy what accelerates time to market, partner where learning exceeds doing.

What Would We Do Differently?

Push harder into less liquid asset classes. Municipal bonds, emerging market debt, private credit—these markets desperately need transparency and efficiency. The less liquid the market, the more value Tradeweb adds, the higher the margins.

Create a venture arm to invest in fintech startups. Not for financial returns but for strategic intelligence. See what's coming before it arrives. Shape the future rather than react to it.

Build a true retail offering. Not through advisors but direct to sophisticated individuals. The Robinhood generation wants to trade bonds, but the infrastructure doesn't exist. Build it.

Double down on data and analytics. Trading is becoming commoditized; intelligence is becoming valuable. Transform from a transaction platform to an intelligence platform that happens to enable transactions.

Biggest Surprises from the Research

The bank ownership structure lasting so long—banks owned 46% at IPO in 2019, twenty-one years after founding. Most disruptors try to kill incumbents; Tradeweb co-opted them.

The margin resilience through cycles. Most assumed electronic trading would be a race to zero on fees. Instead, margins have expanded as scale economics dominate.

The slow pace of electronification. We're twenty-five years into the internet era, yet most bonds still trade over the phone. Cultural change happens slowly, even when the economics are obvious.

The power of boring infrastructure. Tradeweb rarely makes headlines, yet it's one of the best-performing FinTech stocks of the last decade. Sometimes the biggest opportunities hide in plain sight.

Key Lessons for Marketplace Builders

Start with the hard side of the network—usually the supply side. Tradeweb started with dealers because they had the inventory. Once you have supply, demand follows.

Solve for the ecosystem, not against it. Tradeweb made everyone better off rather than trying to disintermediate anyone. Revolution through evolution.

Trust is your ultimate moat. In financial markets, one major failure can destroy decades of credibility. Reliability trumps features.

Patience pays. Tradeweb took twenty-five years to become an overnight success. Most marketplaces fail because they try to force network effects rather than nurture them.

The platform that enables price discovery owns the market. It's not about matching buyers and sellers—it's about creating the context where fair value emerges.

Looking forward, Tradeweb's story is far from over. The company that digitized bond trading now faces the task of reimagining it for the AI age. The challenges are real—competition, technology disruption, fee pressure—but so are the opportunities.

If the last twenty-five years were about moving from analog to digital, the next twenty-five will be about moving from digital to intelligent. And Tradeweb, with its data, relationships, and platform, is positioned to lead that transition.

The lesson for investors is clear: sometimes the best investments aren't in the disruptors but in the infrastructure that enables disruption. Tradeweb isn't trying to kill Wall Street—it's trying to make Wall Street work better. And in that mission, everyone wins.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube