Travere Therapeutics: From Orphan Drug Pioneer to Rare Disease Powerhouse

The Biotech Context and the Orphan Drug Revolution

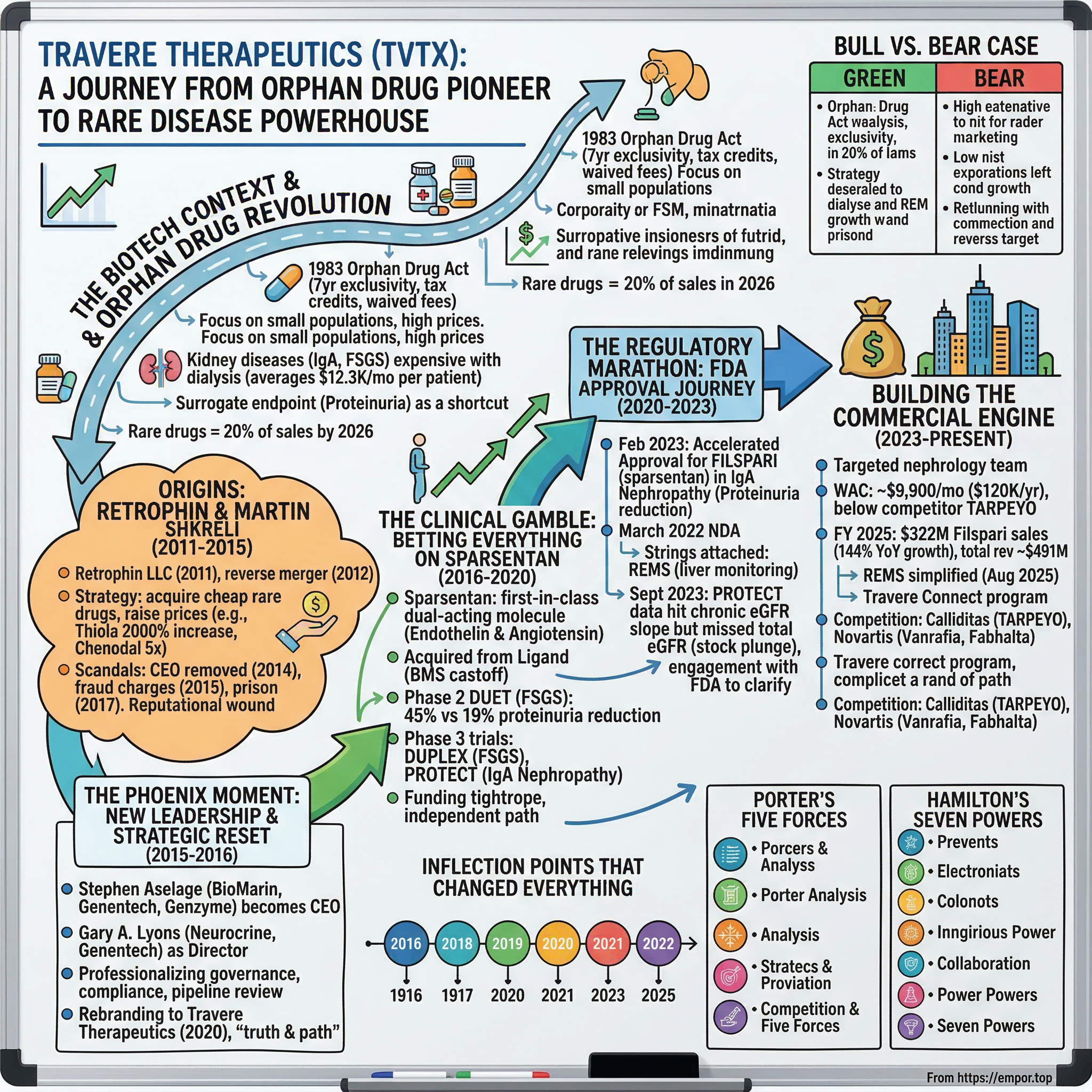

Before understanding Travere, one must understand the policy landscape that made companies like it possible. In 1983, the United States Congress passed the Orphan Drug Act, a piece of legislation that fundamentally altered the economics of pharmaceutical development. Before the Act, companies had developed a grand total of 38 drugs for rare diseases across the entire history of the FDA. The math was simply punishing: developing a drug costs hundreds of millions of dollars, and if only a few thousand patients have the disease, there is no way to recoup that investment through sales. Rare diseases were "orphaned" by the market, their patients abandoned not because of scientific impossibility but because of economic impossibility.

The Orphan Drug Act changed the equation through three powerful incentives. First, it granted seven years of market exclusivity for approved orphan drugs, meaning no competitor could sell the same drug for the same condition during that window, regardless of patent status. This created a regulatory moat distinct from and additive to patent protection. Second, it offered tax credits for clinical testing expenses, originally set at 50 percent and later reduced to 25 percent. Third, it waived FDA user fees and provided regulatory support, including closer coordination with the agency during development. A rare disease was defined as one affecting fewer than 200,000 people in the United States.

The results were transformative. By the end of 2022, the FDA had approved 882 different orphan drugs across 392 rare diseases. In 2022 alone, drugs for rare diseases represented nearly half of all novel approvals. The Act spawned an entire industry, from Genzyme's pioneering work in lysosomal storage disorders to Alexion's complement inhibitors to the modern rare disease powerhouses that populate NASDAQ. It also created an economic template that Travere would eventually exploit with precision: small patient populations, high per-patient pricing, specialized sales forces, and accelerated regulatory pathways.

The kidney disease landscape deserves special attention, because it represents both the opportunity and the challenge that define Travere's entire strategic arc. Chronic kidney disease affects approximately 37 million Americans, a silent epidemic progressing through five stages toward the grim endpoint of kidney failure. Once patients reach end-stage renal disease, they face dialysis, a treatment that consumes 9 to 15 hours per week, carries a five-year survival rate of roughly 35 to 41 percent, and costs Medicare approximately $29 billion annually for hemodialysis alone. The average monthly cost per dialysis patient runs about $12,300, with the first month spiking to over $38,000. Privately insured patients face even steeper bills: an average of $238,000 in their first year.

What makes kidney diseases particularly vexing for drug developers is the timeline. The gold-standard clinical endpoint, progression to kidney failure or sustained decline in kidney function, can take years or even decades to manifest. Running a trial long enough to capture those events requires enormous patient populations, massive budgets, and the patience of a saint. For rare kidney diseases, where the patient pool is small to begin with, the math becomes nearly impossible using traditional trial designs. This is the backdrop against which Travere placed its most consequential bet: that a surrogate endpoint, proteinuria reduction, could serve as a shortcut to approval and commercial viability.

The rare disease pharma playbook that emerged from these dynamics is distinctive and counterintuitive. Small patient populations that might seem like a liability become an asset when combined with orphan drug exclusivity and premium pricing. A drug treating 10,000 patients at $120,000 per year generates $1.2 billion in annual revenue, more than enough to justify the development costs. The specialized sales forces required are small, perhaps 50 to 100 representatives covering the nation's top nephrologists, keeping commercial costs manageable. And the patient advocacy groups that form around rare diseases become powerful allies in regulatory discussions, clinical trial recruitment, and market access. Every element of Travere's strategy, from its choice of disease targets to its pricing to its regulatory approach, flows from this playbook.

To put the kidney disease challenge in human terms, consider the typical patient journey. A young adult notices persistent foamy urine or blood in the urine after a cold. Their primary care physician orders basic blood and urine tests, which reveal elevated protein levels. The patient is referred to a nephrologist, who orders a kidney biopsy, an invasive procedure involving a long needle inserted through the back into the kidney under ultrasound guidance. The biopsy confirms one of several glomerular diseases. The nephrologist explains that treatment options are limited to blood pressure medications and, in some cases, immunosuppressive drugs with significant side effects. The patient is told to monitor their kidney function every few months and to hope for the best. For many patients, this "watch and wait" approach continues for years or decades, as kidney function slowly declines. The arrival of FILSPARI and its competitors has begun to change this calculus, but the years of therapeutic nihilism in glomerular diseases explain why patient advocacy groups became such powerful forces in regulatory discussions.

There is a myth in pharma that rare disease drugs are niche curiosities. The reality is the opposite: orphan drugs are projected to account for 20 percent of all prescription drug sales by 2026. Companies like Alexion, Vertex, and BioMarin have demonstrated that rare disease focus can produce market capitalizations rivaling those of diversified pharma companies many times their size. The economic logic is powerful: concentrated patient populations with desperate unmet need, limited competition protected by regulatory exclusivity, and premium pricing accepted by payers who recognize that even expensive drugs for rare conditions represent modest total budget impact. When the Orphan Drug Act was passed in 1983, its authors could scarcely have imagined that it would give rise to a $200 billion global industry. But that is precisely what happened, and it is the industry into which Travere was born and ultimately thrived.

Origins: Retrophin and Martin Shkreli's Shadow (2011-2015)

In March 2011, a 28-year-old hedge fund manager named Martin Shkreli formed Retrophin, LLC in Delaware. The name was a portmanteau of "recombinant dystrophin," hinting at an initial interest in muscular dystrophy, though the company's actual strategy would prove far more eclectic and opportunistic. What Shkreli had was not so much a coherent drug development vision as a financier's eye for undervalued pharmaceutical assets, a willingness to move fast and aggressively, and, as would later become devastatingly clear, a willingness to blur the lines between corporate treasury and personal hedge fund obligations.

The backstory matters because it is inextricable from Retrophin's founding. Before creating the company, Shkreli had run MSMB Capital Management, a hedge fund that became insolvent after a series of disastrous trades, including a spectacularly wrong bet against a biotech called Orexigen Therapeutics. According to later SEC filings, Shkreli created Retrophin in part "to create an asset that he might be able to use to placate his MSMB Capital investors," many of whom were furious about their losses and demanding answers. From its inception, Retrophin was entangled with Shkreli's personal financial wreckage.

The company went public in December 2012 through a reverse merger with Desert Gateway, Inc., a publicly traded shell corporation. This backdoor route to the public markets avoided the scrutiny of a traditional IPO, the underwriter due diligence, the roadshow questions from institutional investors, and the regulatory review that might have surfaced Shkreli's tangled personal finances. It was a shortcut, and like most shortcuts in public markets, it came with hidden costs that would emerge later.

Shkreli, still only 29, appeared on the Forbes 30 Under 30 list that same month, the kind of accolade that looks very different in hindsight. He was a compelling figure on the biotech conference circuit: young, brash, articulate about rare disease science, and willing to make bold predictions about drug development timelines. He cultivated a persona as a visionary who saw value where others saw neglected patients, and for a brief period, the narrative was convincing enough to attract both capital and talent.

To his credit, Shkreli's core insight about the rare disease market was sound: overlooked pharmaceutical compounds treating small patient populations could be acquired cheaply and commercialized at premium prices under the protections of the Orphan Drug Act. In February 2014, Retrophin signed an agreement to acquire Manchester Pharmaceuticals for $62.5 million, bringing in Chenodal (for a rare liver condition called cerebrotendinous xanthomatosis) and Vecamyl (for hypertension). Three months later, the company licensed Thiola, a treatment for cystinuria, a rare kidney stone disorder, from Mission Pharmacal Company. These were real drugs treating real patients, and in Shkreli's hands they became vehicles for breathtaking price increases. Thiola's price was raised approximately 2,000 percent. Chenodal's price quintupled. The playbook was simple and, to many, repugnant: acquire drugs with captive patient populations and no alternatives, then raise prices because patients had no choice.

But the drug pricing controversies, which would later explode into a national firestorm when Shkreli raised the price of Daraprim 5,000 percent at his next company, Turing Pharmaceuticals, were only the surface-level scandal at Retrophin. Beneath it, the board of directors was discovering something far worse. Shkreli had been using Retrophin as a piggy bank to settle debts from his failed hedge fund, disguising payments to former MSMB investors as "consulting fees." He granted Retrophin stock to certain recipients without shareholder-approved distribution plans. He hired private investigators using company funds. He operated what amounted to a hedge fund within the company, with commission-based incentive structures for stock trading. He traded Retrophin stock during blackout periods.

On September 30, 2014, the board removed Shkreli as CEO, replacing him with Stephen Aselage, the company's chief operating officer. Shkreli formally resigned the following month. What followed was a legal explosion. In August 2015, Retrophin sued Shkreli for $65 million, alleging breach of fiduciary duty. In December 2015, the SEC charged him with securities fraud, and the FBI arrested him at his Manhattan apartment. In August 2017, he was convicted on two counts of securities fraud and one count of conspiracy, eventually receiving a seven-year prison sentence and a $7.4 million fine. From prison, Shkreli counter-sued Retrophin directors. All lawsuits were finally settled in June 2019, with Retrophin making an undisclosed payment to Shkreli, a bitter pill for a company trying desperately to move on.

At Shkreli's fraud trial in 2017, Stephen Aselage testified as a prosecution witness, describing Shkreli as "a Pied Piper... he tells a story, sings a song." Aselage also testified that Shkreli "went on a warpath" after being removed as CEO, attempting to destabilize the company he had founded. The trial revealed a pattern of behavior that was equal parts audacious and reckless, a founder who treated a public company as an extension of his personal financial schemes. When Shkreli was eventually sentenced to seven years, it was a moment of closure for the legal system but not for the company that bore his fingerprints.

Why does this backstory matter for understanding Travere today? Because the company had to rebuild from the ashes of one of the most toxic reputations in pharmaceutical history. Every interaction with investors, regulators, physicians, and patient advocacy groups was shadowed by the Shkreli association. The institutional trust that biotech companies depend on, trust that regulators will engage in good faith, that patients will enroll in clinical trials, that payers will negotiate fairly, had been obliterated. Everything that followed at Retrophin, and later Travere, must be understood as a project of radical credibility restoration. The Shkreli era was not just a scandal; it was an existential wound that required a complete organizational transplant to survive.

The Phoenix Moment: New Leadership and Strategic Reset (2015-2016)

Stephen Aselage was not an obvious choice for corporate savior. He had been hired by Shkreli himself in October 2012 and had served as chief operating officer, which might have tainted him by association. But Aselage brought something Retrophin desperately needed: deep, legitimate rare disease expertise. Before joining Retrophin, he had spent seven years at BioMarin Pharmaceutical, one of the most respected rare disease companies in the world, where he served as executive vice president and chief business officer. At BioMarin, he had built the commercial and medical affairs functions from the ground up, launched three commercial products, and developed commercial businesses in more than 45 countries. Earlier in his career, he held leadership roles at Genentech and Genzyme, two pillars of the biotech establishment. His appointment as permanent CEO in November 2014 was the first signal that Retrophin might be more than just Shkreli's wreckage.

The board also brought in Gary A. Lyons as a director in October 2014, just weeks after Shkreli's removal. Lyons was the founding president and CEO of Neurocrine Biosciences, one of the most successful CNS-focused biotechs in the industry, and had previously held senior positions at Genentech including VP of Business Development and VP of Sales. He became Chairman of the Board in May 2016. His appointment sent a clear message to the market: this was no longer Shkreli's company. Lyons brought corporate governance credibility, operational experience from building Neurocrine from scratch, and the kind of industry reputation that reassured investors, regulators, and potential partners alike.

The culture transformation Aselage undertook was comprehensive and necessarily unglamorous. He conducted an operational review of the entire pipeline and commercial portfolio, professionalizing governance, compliance, and financial controls that had been either absent or overridden under Shkreli. He solidified the leadership team, bringing in experienced executives who would never have associated themselves with the pre-ouster company. He refocused the company's narrative from price-gouging opportunist to legitimate rare disease developer, a pivot that required not just words but sustained execution.

The most consequential strategic decision of this era had actually been set in motion before the crisis. In 2012, Retrophin had in-licensed sparsentan from Ligand Pharmaceuticals, which had itself acquired the compound through its purchase of Pharmacopeia in 2008. The molecule had originated at Bristol-Myers Squibb under the designation PS433540 and had been evaluated in Phase 2 trials for hypertension. BMS shelved it, likely because the hypertension market was already crowded with effective generics and the competitive dynamics did not justify continued investment in a novel mechanism. Ligand retained a 9 percent royalty on future sales.

When Retrophin acquired the license, someone, whether Shkreli himself or a scientific advisor, made the crucial intellectual leap: this molecule's dual mechanism, blocking both endothelin and angiotensin receptors, was more relevant to rare kidney diseases than to hypertension. In hypertension, there were dozens of cheap, effective alternatives. In FSGS and IgA nephropathy, there was nothing. The same molecule, redirected toward a different disease, transformed from a pharmaceutical also-ran into a potential first-in-class therapy. This was the bet-the-company decision, though few recognized it at the time.

Sparsentan's science was genuinely novel. It was a first-in-class dual-acting molecule that simultaneously blocked two receptors: the endothelin type A receptor and the angiotensin II type 1 receptor. To understand why this mattered, consider the existing standard of care. Patients with IgA nephropathy and FSGS were treated with ACE inhibitors or ARBs, drugs that block only the angiotensin pathway. These drugs reduce proteinuria and slow disease progression, but they address only one of several damage pathways. The endothelin system, a separate biological cascade, drives vasoconstriction within the kidney, damages podocytes (the specialized cells that form the kidney's filtration barrier), promotes inflammation, and stimulates fibrosis. By blocking both pathways with a single molecule, sparsentan offered the theoretical possibility of more comprehensive kidney protection than any existing therapy. Think of it as defending a castle not just by reinforcing the main gate but by simultaneously strengthening the walls, something no previous drug had accomplished in a single pill.

The diseases sparsentan targeted were areas of enormous unmet need. IgA nephropathy, the most common primary glomerulonephritis worldwide, affects an estimated 199,000 to 208,000 Americans. It is a cruel disease that strikes young people: 80 percent of patients are diagnosed between ages 16 and 35, with men affected at least twice as often as women. The body produces an abnormal form of immunoglobulin A that deposits in the kidney's filters, triggering inflammation and progressive scarring. Between 20 and 50 percent of patients progress to kidney failure within 20 years. Before the recent wave of approvals, there was no FDA-approved therapy specifically targeting the disease.

FSGS presented an even starker landscape. This disease, in which portions of the kidney's filtration units become scarred and hardened, is the leading glomerular cause of end-stage renal disease in the United States. It is significantly more common and more aggressive in Black patients, with incidence nearly five times higher than in White patients. For patients who do not respond to steroids and immunosuppressive drugs, the average time from onset of heavy proteinuria to kidney failure is just six to eight years. As of early 2026, there is still no FDA-approved treatment specifically for FSGS. None. Zero.

The capital situation during this period was precarious. Retrophin had limited cash runway, legal bills from the Shkreli litigation, and a stock price depressed by reputational damage. Every dollar spent on sparsentan's clinical development was a dollar not available as a cushion against failure. But the strategic logic was clear: if sparsentan worked, it would address massive unmet needs in diseases with no approved therapies, a combination that the Orphan Drug Act's incentives made potentially very lucrative. If it failed, the company was probably finished anyway.

One strategic move during this period that deserves more attention is the decision to divest non-core assets. Under Aselage and then Dube, the company sold Thiola and Chenodal, the very drugs that Shkreli had acquired and that had generated the price-gouging controversies. In February 2020, Retrophin sold Thiola to Biocodex for $170 million upfront plus up to $20 million in milestones. In March 2021, it sold Chenodal to Leadiant Biosciences. These divestitures served a dual purpose: they provided cash to fund sparsentan's clinical development, and they removed the last tangible links to the Shkreli-era business model. It was a deliberate and strategic pruning, concentrating the company's identity and resources on a single high-conviction clinical program.

In November 2020, the company completed its symbolic break from the past by changing its name from Retrophin to Travere Therapeutics. The name, pronounced "truh-veer," derives from Latin roots meaning "truth" and "path." Trading under the new ticker TVTX began on November 19, 2020. The rebranding was led by Eric Dube, a GlaxoSmithKline and ViiV Healthcare veteran who had replaced Aselage as CEO in January 2019. Dube brought 18 years of big-pharma commercial experience and a patient-centric leadership philosophy that further accelerated the cultural transformation. The name change was explicitly intended to sever the association with Shkreli, and while no rebrand can erase history, it signaled to the market that this was, in every meaningful sense, a different company.

The Clinical Gamble: Betting Everything on Sparsentan (2016-2020)

The Phase 2 DUET trial in FSGS was the first real test of whether sparsentan's dual mechanism would translate from theory to clinical reality. The study randomized 109 patients with biopsy-proven FSGS to receive sparsentan at varying doses or irbesartan, a standard ARB, at 300 milligrams daily. The primary endpoint was proteinuria reduction at eight weeks, an early readout designed to provide a preliminary signal without committing to a years-long trial. When the results were announced in September 2016 and subsequently published in the Journal of the American Society of Nephrology, they were compelling: sparsentan-treated patients achieved a 45 percent reduction in proteinuria compared to 19 percent for irbesartan. At the highest doses, the reduction was 47 percent versus 19 percent, a statistically significant difference. The FSGS Partial Remission Endpoint was achieved by 28 percent of sparsentan patients versus 9 percent on irbesartan.

These numbers may seem dry on the page, but for the nephrology community they were electric. To understand why, one must appreciate the therapeutic nihilism that had pervaded FSGS treatment for decades. Nephrologists had tried everything available, steroids, calcineurin inhibitors, rituximab, and for a large subset of patients, nothing worked. The idea that a single oral pill could reduce proteinuria by 45 percent in a disease with no approved therapy was genuinely unprecedented.

Proteinuria in FSGS is not just a biomarker; it is itself a driver of further kidney damage. Protein that escapes through damaged kidney filters is toxic to the tubular cells downstream, triggering inflammation and fibrosis in a vicious cycle where kidney damage causes protein leakage, and protein leakage causes more kidney damage. Demonstrating a 45 percent reduction versus the best available therapy suggested that sparsentan might break this cycle more effectively than anything else on the market.

The clinical endpoint challenge that confronted Travere's development team was existential. The traditional endpoint for kidney disease trials, progression to kidney failure or sustained eGFR decline, would require enormous trials running for many years. For a company with limited capital competing against the clock, this was not viable. The alternative was to seek accelerated approval based on proteinuria reduction as a surrogate endpoint, a measure "reasonably likely" to predict clinical benefit. This strategy carried regulatory risk: the FDA had never approved a drug for IgA nephropathy based on proteinuria alone, and the scientific evidence linking proteinuria reduction to long-term kidney preservation, while compelling epidemiologically, had not been validated in the context of a specific drug approval. Travere was proposing to break new ground, and if the FDA said no, the company would face years of additional development with no guarantee of survival.

The two pivotal Phase 3 trials, DUPLEX for FSGS and PROTECT for IgA nephropathy, represented the all-in moment. PROTECT enrolled 404 adults with biopsy-proven IgA nephropathy between December 2018 and May 2021, randomizing them to sparsentan 400 milligrams daily or irbesartan 300 milligrams daily. The primary endpoint was change in proteinuria at 36 weeks, with a key confirmatory endpoint of eGFR slope over 110 weeks. DUPLEX enrolled 371 patients with FSGS in a similar design.

The funding tightrope during this period was harrowing. Travere raised capital through multiple equity offerings, each one diluting existing shareholders but necessary to fund the trials. The company faced a classic biotech dilemma: too little capital risked running out of money before data readouts, while too much dilution would destroy shareholder value even if the drug succeeded. Management navigated this by timing raises around positive data milestones, when the stock price was higher and dilution was minimized.

Partnership considerations arose repeatedly. A licensing deal with a larger pharmaceutical company could have provided non-dilutive capital, but it would have meant sharing the economics of sparsentan's potential success. Travere's leadership made the deliberate choice to stay independent, a decision that would prove enormously value-creating if the drug succeeded but that amplified the risk of failure.

The COVID-19 pandemic added another layer of disruption that is easy to underestimate in retrospect. Clinical trial enrollment, which depends on patients visiting hospital-based nephrology centers for screening, biopsy confirmation, and regular monitoring visits, ground to a halt in March 2020. PROTECT had begun enrollment in December 2018 and was not fully enrolled until May 2021, a timeline that stretched well beyond original projections. Trial sites across the United States and Europe scrambled to implement remote monitoring, telemedicine visits, and home-based sample collection. For a company with limited cash reserves and trials that represented its entire future, every month of delay burned precious runway while producing no data. The team's ability to adapt operationally, maintaining trial integrity while accommodating pandemic restrictions, was a quiet but critical test of organizational capability.

The trial designs themselves reflected careful strategic thinking about regulatory expectations. PROTECT used an active comparator, irbesartan, rather than placebo. This was a bold choice: active comparator trials are harder to "win" because the control arm shows therapeutic benefit, shrinking the difference the experimental drug must demonstrate. But the FDA had signaled that any new therapy for IgA nephropathy would need to show benefit beyond the standard of care, not just beyond placebo. By designing PROTECT against the best available treatment, Travere was pre-answering the regulatory question that would determine whether sparsentan could be approved. It was a calculated gamble that paid off spectacularly when the 36-week proteinuria data showed a three-fold difference in reduction between the two arms.

The Regulatory Marathon: FDA Approval Journey (2020-2023)

On March 21, 2022, Travere submitted a New Drug Application to the FDA for sparsentan in IgA nephropathy under Subpart H, the accelerated approval pathway. The submission was based on PROTECT's 36-week data showing a 49.8 percent mean reduction in proteinuria for sparsentan versus 15.1 percent for irbesartan, a result that was statistically overwhelming. Complete proteinuria remission, defined as a urinary protein-to-creatinine ratio below 0.3, was achieved by 21 percent of sparsentan patients versus 8 percent on irbesartan. The FDA accepted the NDA in May 2022 and granted Priority Review.

On February 17, 2023, the FDA granted accelerated approval to FILSPARI for reducing proteinuria in adults with primary IgA nephropathy at risk of rapid disease progression. The announcement marked one of those rare moments in biotech where a company's entire trajectory pivots. Travere went from being a clinical-stage company with no approved products to a commercial-stage biotech with a first-in-class therapy in a disease with massive unmet need. The stock surged on the news, and the company's credibility, so painstakingly rebuilt after the Shkreli years, was validated in the most concrete way possible: an FDA stamp of approval.

It was the first and only non-immunosuppressive therapy approved for IgA nephropathy, a distinction that would become central to FILSPARI's commercial positioning. The drug became available during the week of February 27, 2023.

The approval came with strings attached. The FDA required a Risk Evaluation and Mitigation Strategy, or REMS, due to hepatotoxicity concerns. This was not unique to sparsentan; endothelin receptor antagonists as a class carry liver toxicity risk, a legacy of bosentan, an earlier ERA used for pulmonary arterial hypertension that required a boxed warning and monthly liver monitoring. Sparsentan's clinical trial data showed that liver enzyme elevations above three times the upper limit of normal occurred in approximately 2.5 percent of patients versus 2.0 percent for irbesartan, a modest difference but one the FDA took seriously. No cases of liver failure were observed in any trial. The REMS initially required monthly liver function monitoring for the first 12 months, then every three months thereafter, creating an administrative burden for physicians and patients that would become a meaningful commercial headwind.

The approval process itself was not without drama. The FDA's review of the NDA involved extensive back-and-forth about the adequacy of proteinuria as a surrogate endpoint. Historically, the agency had approved drugs for kidney diseases based on harder endpoints like eGFR decline or progression to kidney failure. Travere's regulatory affairs team, working with nephrology consultants and patient advocacy groups, built a comprehensive case that proteinuria reduction in IgA nephropathy was "reasonably likely to predict clinical benefit," the statutory standard for accelerated approval. They marshaled epidemiological data showing that higher proteinuria levels predicted worse kidney outcomes, mechanistic evidence that proteinuria itself drives tubular damage, and the practical argument that waiting for eGFR endpoints would condemn patients to years without treatment in a disease where kidneys were progressively failing. The FDA ultimately agreed, establishing a precedent that would reshape drug development for the entire glomerular disease space.

Then came September 2023, and the most dramatic stock price event in Travere's history. The PROTECT trial's 110-week confirmatory data showed that sparsentan's eGFR chronic slope, the rate at which kidney function declined, was -2.7 versus -3.8 for irbesartan, a difference of 1.1 that was statistically significant at a p-value of 0.037. But the total eGFR slope from day one to week 110 narrowly missed significance, with a p-value of 0.058. The market, focusing on the near-miss, sent Travere's stock plunging roughly 40 percent. This was a harsh overreaction: the chronic slope, which strips out the initial hemodynamic effect that makes the first few weeks look worse than the actual disease trajectory, was the more clinically meaningful measure, and it did achieve significance. But markets punish ambiguity, and the result was ambiguous enough to trigger a stampede for the exits.

The stock recovered from those depths over the following year, driven by two factors: first, nephrologists largely focused on the chronic slope data, which showed clear benefit, and continued prescribing FILSPARI; second, the company's regulatory team engaged the FDA to clarify that the confirmatory endpoint had, in fact, been met when analyzed using the pre-specified chronic slope methodology.

The full approval story vindicated Travere's science. On September 5, 2024, the FDA converted the accelerated approval to traditional approval for IgA nephropathy, confirming that FILSPARI significantly slowed kidney function decline. This was a landmark moment: it validated proteinuria as a surrogate endpoint for IgA nephropathy, establishing a regulatory precedent that would benefit the entire nephrology field. The approval was based on an updated analysis of the PROTECT data that met the confirmatory endpoint threshold.

Meanwhile, the DUPLEX trial in FSGS had produced mixed results. At 108 weeks, sparsentan showed superior proteinuria reduction, with 50 percent versus 32 percent for irbesartan, but the eGFR slope difference was not statistically significant. For FSGS, a disease with zero approved therapies, the eGFR miss would normally have been a fatal blow to the approval pathway. But a parallel scientific effort called the PARASOL project, co-sponsored by patient advocacy groups, the FDA, the Kidney Health Initiative, and the National Kidney Foundation, was working to validate proteinuria as a meaningful endpoint specifically for FSGS. PARASOL demonstrated that proteinuria reduction over 24 months was strongly associated with reduced kidney failure risk, providing the scientific framework for Travere to pursue FSGS approval based on proteinuria data rather than eGFR.

On March 17, 2025, Travere submitted a supplemental NDA for FILSPARI in FSGS. The FDA accepted it and set a PDUFA target date of January 13, 2026. In a move widely interpreted as favorable, the FDA initially scheduled an advisory committee meeting but later removed it in September 2025, suggesting the agency was satisfied with the data. However, Travere subsequently submitted additional data constituting a "major amendment," and the FDA extended the PDUFA date to April 13, 2026. As of March 2026, the decision remains pending, and it represents the single most important near-term catalyst for the company. If approved, FILSPARI would become the first and only FDA-approved treatment for FSGS.

In August 2025, the FDA approved a significant modification to the REMS program, reducing liver function monitoring from monthly to every three months from the start of treatment and removing the embryo-fetal toxicity monitoring requirement. This was a major commercial catalyst, substantially reducing the administrative burden that had been slowing physician and patient adoption. To understand why this mattered so much, consider the practical reality: under the original REMS, a patient starting FILSPARI had to visit their doctor or laboratory every single month for a year just for liver blood draws, on top of their regular nephrology appointments. For patients already managing a chronic kidney disease with its own monitoring requirements, this was a significant additional burden. Many nephrologists cited the monitoring requirement as the primary reason they hesitated to prescribe FILSPARI, even when they believed it was the right treatment for their patients. The simplified REMS removed one of the most significant barriers between the drug and the patients who needed it.

Building the Commercial Engine (2023-Present)

FILSPARI's commercial launch strategy reflected the rare disease playbook at its most disciplined. Rather than deploying a massive sales force across thousands of physicians, Travere built a targeted team of nephrology specialists covering the high-prescriber centers where IgA nephropathy and FSGS patients concentrate. In rare diseases, the top 20 percent of prescribers often account for 80 percent of prescriptions, making this focused approach both more effective and more capital-efficient than a broad-based launch.

The pricing decision was strategically astute. FILSPARI launched at a wholesale acquisition cost of approximately $9,900 per month, roughly $120,000 per year. This was deliberately positioned below Calliditas Therapeutics' TARPEYO, which treats IgA nephropathy through a different mechanism. The undercutting was not just competitive positioning; it reflected Travere's understanding that payer relations are a long game in rare diseases, and launching at a lower price point would ease formulary access and reimbursement negotiations. Gross-to-net discounts ran approximately 20 percent in 2025 and are expected to increase modestly to the mid-20 percent range in 2026. Patient assistance programs reduce copays to zero for many commercially insured patients, removing one of the most common barriers to adoption.

The commercial results have been remarkable. FILSPARI generated $322 million in US net product sales in fiscal year 2025, representing 144 percent year-over-year growth. The fourth quarter alone produced $103.3 million in FILSPARI sales, with a record 908 new patient start forms, the highest quarterly total since launch. Total company revenue reached approximately $491 million for the year.

What makes these numbers particularly impressive is the context: they were achieved with only the IgA nephropathy indication, since FSGS has not yet been approved. Each quarter showed sequential acceleration, suggesting that physician adoption was still in its early innings rather than approaching saturation. The REMS simplification in August 2025 appeared to catalyze a step-change in prescribing behavior, as physicians who had been waiting for a less burdensome monitoring regimen began initiating patients in greater numbers.

The commercial infrastructure Travere built deserves attention because it represents a capability that is difficult to replicate quickly. The company invested in a dedicated patient support program called Travere Connect, which provides insurance navigation, copay assistance, and nurse-led adherence support. In rare diseases, where patients often face complex reimbursement processes and where each patient represents significant revenue, the quality of patient support services can be as important a competitive differentiator as the drug's clinical profile. Early reports suggest that Travere Connect has achieved high patient satisfaction and strong adherence rates, though specific metrics are not publicly disclosed.

The competitive landscape has intensified significantly since FILSPARI's launch. Calliditas' TARPEYO, a targeted-release budesonide that acts as an immunosuppressive agent targeting the mucosal immune system, received full FDA approval for IgA nephropathy in December 2023 and holds a meaningful market position, with nearly one in five US IgA nephropathy patients managed on the therapy. Novartis entered the field aggressively through two routes: its $3.2 billion acquisition of Chinook Therapeutics in June 2023 brought atrasentan (now branded Vanrafia), a selective endothelin A receptor antagonist that received FDA accelerated approval for IgA nephropathy in April 2025 without a REMS requirement. Novartis also secured accelerated approval for Fabhalta (iptacopan), an oral complement Factor B inhibitor, in IgA nephropathy in August 2024. This means the IgA nephropathy market has evolved from a therapeutic desert to a multi-drug landscape in just three years, and Travere faces a Novartis armed with a three-drug kidney portfolio.

FILSPARI's key differentiator against this competition is that it is the only non-immunosuppressive approved therapy for IgA nephropathy that can be used as a chronic treatment. TARPEYO is a corticosteroid with a limited treatment duration and infection risks. Vanrafia is mechanistically closer to FILSPARI (both target the endothelin pathway), but FILSPARI's dual mechanism offers additional angiotensin receptor blockade. Fabhalta operates through complement inhibition, an entirely different pathway, and is increasingly viewed as a potential combination partner with FILSPARI rather than a pure competitor. The medical community appears to be moving toward multi-mechanism treatment approaches for IgA nephropathy, similar to the combination therapy paradigms seen in oncology and HIV.

Internationally, Travere partnered with CSL Vifor, which holds exclusive commercialization rights for sparsentan in Europe, Australia, and New Zealand. The European Commission granted conditional marketing authorization for FILSPARI in IgA nephropathy in April 2024, followed by standard full EU approval in April 2025 based on confirmatory data. Travere receives royalty revenue from CSL Vifor's European sales. Japan, where IgA nephropathy incidence is among the highest in the world at roughly 45 cases per million per year, represents a significant untapped opportunity without an announced partner or filing.

Beyond FILSPARI, Travere's pipeline includes pegtibatinase, a novel enzyme replacement therapy for classical homocystinuria, an ultra-rare metabolic disease. Classical homocystinuria is caused by a deficiency of the enzyme cystathionine beta-synthase, leading to dangerous accumulation of homocysteine in the blood. Untreated, it causes severe cardiovascular complications, skeletal abnormalities, intellectual disability, and blood clots. Current treatments are limited to dietary restrictions and vitamin supplementation, which many patients find burdensome and inadequate. Pegtibatinase offers the potential for a direct enzymatic replacement that addresses the root cause. The Phase 3 HARMONY trial had its enrollment voluntarily paused in September 2024 due to manufacturing scale-up challenges and is on track to restart enrollment in early 2026, with topline data expected later in the year. Phase 1/2 data showed a 67 percent reduction in total homocysteine, and the compound holds Breakthrough Therapy, Rare Pediatric Disease, and Fast Track designations from the FDA. While classical homocystinuria is far smaller than the IgA nephropathy or FSGS markets, the ultra-rare disease pricing model (potentially exceeding $300,000 per year) could make it a meaningful revenue contributor if approved.

The Inflection Points That Changed Everything

Every company narrative can be distilled to a handful of moments where the trajectory shifted irrevocably. For Travere, there are six.

The first was the Shkreli ouster in September 2014. This was not merely a management change; it was an existential crisis that forced a complete cultural, strategic, and reputational reset. Companies survive leadership transitions routinely. Companies survive the public imprisonment of their founder for securities fraud rarely. The fact that Retrophin emerged from this period as a functioning entity, let alone one capable of advancing a first-in-class drug through Phase 3 trials, speaks to the quality of the leadership that followed and the underlying value of the sparsentan asset.

The second was the sparsentan in-license from Ligand Pharmaceuticals in 2012. This molecule, a Bristol-Myers Squibb castoff that had been evaluated for hypertension and abandoned, would become the foundation of a multi-billion-dollar franchise. The decision to redirect it toward rare kidney diseases was the strategic insight that created all subsequent value. When Fierce Pharma later called FILSPARI "a Bristol Myers castoff turned into a unique drug for rare kidney disease," it captured the improbability of the compound's journey.

The third was the 2020 rebranding from Retrophin to Travere. Symbolic gestures in business are often dismissed as cosmetic, but this one carried real weight. The new name enabled the company to engage with physicians, patients, and partners without the conversation immediately turning to Shkreli. It was a practical necessity as much as a branding exercise.

The fourth was the positive PROTECT data that led to the February 2023 accelerated approval. This validated the science, the regulatory strategy, and the surrogate endpoint approach. It transformed Travere from a pre-revenue clinical-stage company to a commercial biotech with actual sales.

The fifth was the full FDA approval in September 2024, which validated the confirmatory data and established FILSPARI as a disease-modifying therapy, not just a proteinuria-lowering agent. This converted what had been a conditional, provisional approval into durable commercial authorization.

The sixth inflection point is still pending: the FSGS PDUFA decision on April 13, 2026. If approved, FILSPARI would become the first and only approved treatment for a disease that has had no FDA-sanctioned therapy in the entirety of the agency's existence. The addressable market would expand significantly, and Travere's narrative would shift from single-indication biotech to multi-indication rare kidney disease platform.

The arc of these inflection points tells a story of compounding transformation: from scandal-plagued to scientifically credible, from multi-asset hodgepodge to focused rare kidney disease leader, from clinical-stage to commercial-stage with two indications, from survival mode to growth mode.

What is remarkable about this sequence is that each inflection point built on the one before it in a way that was not obvious at the time. The Shkreli ouster was necessary but not sufficient for the sparsentan bet. The sparsentan bet was necessary but not sufficient for the PROTECT trial design. The PROTECT trial design was necessary but not sufficient for the accelerated approval. And the accelerated approval was necessary but not sufficient for the commercial success that has followed. At each stage, the company faced real alternatives that would have led to very different outcomes: the board could have sold Retrophin after ousting Shkreli; management could have licensed sparsentan to a larger partner; the clinical team could have designed a placebo-controlled trial that would have been easier to win but less compelling to the FDA; the regulatory team could have pursued full approval based on eGFR, delaying the launch by years. The fact that each decision was made correctly, in sequence, by a team operating under extreme pressure and with limited resources, is what separates Travere from the hundreds of biotechs that pursue similar strategies and fail.

The Science and Patient Impact Story

To truly understand what FILSPARI means, one must understand what IgA nephropathy and FSGS do to actual human beings. These are not abstractions; they are diseases that destroy lives with agonizing slowness.

IgA nephropathy typically announces itself in the most unsettling way possible: blood in the urine, often appearing during or after a common cold or throat infection. A young man in his twenties, otherwise healthy, notices red-tinged urine and visits his doctor. Blood tests show protein in the urine. A kidney biopsy, a needle inserted into the back to extract a sliver of kidney tissue, confirms the diagnosis. The doctor explains that the body's immune system is producing an abnormal form of immunoglobulin A, an antibody normally tasked with fighting infections. This malformed antibody deposits in the kidney's glomeruli, tiny filtration units, triggering chronic inflammation and progressive scarring. The news that follows is harder to absorb: there is no cure. The disease may progress slowly or rapidly, but between 20 and 50 percent of patients will reach kidney failure within two decades.

FSGS operates through a different mechanism but with similarly devastating consequences. The podocyte, a specialized cell that wraps around the kidney's capillaries like an octopus embracing a pole, is the central character. When podocytes are injured or lost, the filtration barrier crumbles, and protein floods into the urine. The body responds to the damage with scarring, which further compromises filtration in a destructive feedback loop. FSGS patients often present with massive proteinuria: foamy urine, severe swelling of the legs and face, crushing fatigue. For those who do not respond to steroids, the median time to kidney failure is six to eight years.

The endpoint of both diseases, absent effective treatment, is dialysis. Dialysis means three trips per week to a treatment center, three to five hours each session, needles inserted into a surgically created access point in the arm, blood drawn out of the body and circulated through a machine that does what the kidneys no longer can. The most common symptoms patients report are crushing fatigue (71 percent), dry skin (62 percent), insomnia (44 percent), and muscle cramps (43 percent). Many patients lose the ability to work or attend school. Depression and social isolation are endemic. The five-year survival rate is about 35 to 41 percent, worse than many common cancers.

Sparsentan's dual mechanism addresses this reality by attacking kidney damage through two pathways simultaneously. The angiotensin receptor blockade reduces pressure inside the glomerulus by dilating the blood vessel on the outflow side, the same mechanism as existing ARBs. The endothelin receptor blockade adds something no previous therapy offered: it counters the vasoconstriction, inflammation, fibrosis, and podocyte damage driven by excess endothelin-1, a powerful vasoconstrictor that is overproduced in diseased kidneys. The result, demonstrated across multiple clinical trials, is a roughly 50 percent reduction in proteinuria, approximately double what irbesartan achieves alone. In the PROTECT trial, 31 percent of patients on sparsentan achieved complete proteinuria remission at two years, compared to 11 percent on irbesartan.

What "disease-modifying" means in this context is specific and important: FILSPARI does not cure IgA nephropathy or FSGS. It does not reverse existing kidney damage. What it does is slow the rate of decline, buying patients years of kidney function they would otherwise lose. In the PROTECT trial, the chronic eGFR slope was -2.7 for sparsentan versus -3.8 for irbesartan, a difference of 1.1 milliliters per minute per year. That may sound small, but over a decade, it translates to roughly 11 additional milliliters of preserved kidney function, potentially the difference between remaining dialysis-free and beginning the grim routine of thrice-weekly blood cleansing.

An analogy may help illustrate why this matters. Think of kidney function as water in a bathtub with the drain partially open. In IgA nephropathy, the drain is open wider than normal, and the water level is steadily dropping. Standard ARBs like irbesartan partially plug the drain, slowing the loss. FILSPARI plugs the drain more effectively by addressing two separate channels through which water is escaping, the angiotensin channel and the endothelin channel. It does not refill the tub; once water is lost, it is gone. But by slowing the drain more effectively, it keeps the water level above the critical threshold, the level at which dialysis becomes necessary, for significantly longer. For a 30-year-old diagnosed with IgA nephropathy, the difference between reaching dialysis at 45 versus 55 is not a minor clinical improvement; it is a decade of normal life.

The limitations must be acknowledged alongside the promise. Not all patients respond to FILSPARI. The PROTECT trial showed that roughly 70 percent of patients did not achieve complete proteinuria remission, meaning most patients continue to have some degree of protein leakage despite treatment. The liver monitoring requirements, though reduced, remain a real consideration. And because the drug addresses the damage pathways rather than the root cause of either disease, it must be taken indefinitely, a lifelong commitment to daily medication and periodic monitoring.

Business Model and Unit Economics

Travere's financial model is a textbook illustration of rare disease economics. The basic formula is straightforward: small patient population multiplied by high per-patient pricing, funded by specialized commercial infrastructure, yielding high gross margins that can be reinvested in pipeline development.

FILSPARI's wholesale acquisition cost of approximately $120,000 per year places it in the mainstream of rare disease pricing. To a non-pharma reader, this number may seem staggering for a single pill taken once daily. But context matters enormously.

As a reference point, the median annual cost for orphan drugs across the industry is approximately $219,000, making FILSPARI actually modestly priced relative to rare disease norms. And compared to the cost of the alternative, dialysis at $150,000 or more per year with dramatically worse quality of life, the value proposition becomes clear. The small molecule format offers manufacturing advantages over biologics: synthesis is more standardized, scale-up is more predictable, and supply chain complexity is lower. These factors contribute to what are typically very high gross margins for small molecule rare disease drugs, often exceeding 80 percent once manufacturing scale is achieved.

The company's path to profitability is now clearly visible. Fiscal year 2025 saw total revenue of approximately $491 million against a net loss of only $25.5 million, implying a net margin of negative 5.2 percent. R&D spending was $206 million, declining modestly year-over-year as the clinical-stage investment shifts toward commercial execution. SG&A has increased as the company expanded its sales force and invested in FSGS launch preparations, but revenue growth has dramatically outpaced cost growth. The company exited 2025 with approximately $323 million in cash, cash equivalents, and marketable securities, providing a comfortable operating cushion.

The balance sheet carries approximately $316 million in long-term debt, resulting in an elevated debt-to-equity ratio that reflects the capital-intensive nature of clinical-stage biotech development. This debt was accumulated during the years when Travere was spending hundreds of millions on clinical trials with no offsetting revenue, a common pattern in biotech that creates a leveraged balance sheet by the time commercial revenue begins flowing.

However, with revenue now approaching $500 million annually and growing at triple-digit rates, the leverage trajectory is improving rapidly. If FILSPARI revenue continues on its current trajectory, Travere could achieve GAAP profitability in 2026 and begin generating meaningful free cash flow shortly thereafter, fundamentally changing its financial profile from net cash consumer to net cash generator.

Wall Street consensus estimates for FILSPARI peak sales range from $1.5 to $2.5 billion, depending on assumptions about FSGS approval, competitive dynamics, and international expansion. If the FSGS indication is approved and the company executes internationally through its CSL Vifor partnership and potential new collaborations, the higher end of that range becomes plausible. Rare disease companies that achieve commercial scale typically trade at significant revenue multiples because of the durability of orphan drug exclusivity, the limited competitive dynamics, and the high barriers to market entry.

The comparisons to rare disease peers are instructive. AstraZeneca acquired Alexion for $39 billion in 2021, paying roughly seven times Alexion's trailing revenue for a company with an established complement inhibitor franchise. Amgen acquired Horizon Therapeutics for $27.8 billion in 2023, at approximately five times revenue, for a portfolio anchored by Tepezza for thyroid eye disease. CSL acquired Vifor Pharma for approximately $11.7 billion in 2022, specifically to gain a nephrology commercial footprint. Merck acquired Acceleron for $11.5 billion in 2021, also at a substantial premium to revenue. These transactions established a pricing framework in which rare disease companies with established commercial franchises and growth potential command substantial premiums, typically four to eight times revenue depending on growth trajectory and competitive position.

Travere's current market capitalization of $2.6 billion, against a revenue trajectory that could reach $1 billion or more within a few years, places it in a zone where acquisition economics could be very attractive to a larger pharma company seeking to build or expand a rare disease portfolio. The CSL Vifor transaction is particularly instructive because it was driven by the acquirer's desire to build a nephrology-focused commercial platform, precisely the kind of capability that Travere has now developed. Jefferies analyst Maury Raycroft included Travere in a list of top potential acquisition targets for 2026, and the stock has reflected takeover speculation at various points.

Strategic Analysis: Porter's Five Forces

Threat of New Entrants: Moderate-High. The Orphan Drug Act's incentives cut both ways. While the seven-year market exclusivity provides a moat for approved drugs, the same incentives that attracted Travere to rare kidney diseases are attracting others. Novartis's aggressive entry through the Chinook acquisition and Fabhalta development demonstrates that large pharma is no longer ignoring this space.

However, the high cost of clinical development creates meaningful barriers. Phase 3 trials in FSGS and IgA nephropathy easily exceed $200 million, and the specialized regulatory expertise required, combined with the long timelines to approval, means that a new entrant cannot simply decide to enter this market and have a product available within a few years. The pipeline of competitors is known and visible, which provides some predictability.

Regulatory pathway clarity following FILSPARI's approval paradoxically lowers risk for followers while validating the market, creating a double-edged dynamic. Travere blazed the trail on proteinuria as a surrogate endpoint, and every subsequent IgA nephropathy drug will benefit from that precedent without bearing the risk Travere took to establish it.

Bargaining Power of Suppliers: Low-Moderate. Sparsentan is a small molecule, and contract manufacturing capacity for small molecules is broadly available. API sourcing is relatively straightforward. The primary supply chain dependency is on clinical trial sites, which require specialized nephrology expertise and access to rare disease patient populations, creating some concentration risk. But in the manufacturing dimension, Travere faces limited supplier power.

Bargaining Power of Buyers: Moderate. This is where the rare disease model shows its structural advantages and emerging vulnerabilities. Small patient populations limit payer leverage because the total budget impact of any single orphan drug is modest relative to an insurer's total spend. A health plan covering one million lives might have only 5 to 15 IgA nephropathy patients on FILSPARI, representing perhaps $600,000 to $1.8 million in annual drug spend, a rounding error in a billion-dollar pharmacy budget.

The lack of alternatives historically strengthened Travere's pricing power. The REMS program creates switching costs, as physicians and patients who have established monitoring protocols are reluctant to disrupt them. However, with TARPEYO, Vanrafia, and Fabhalta now available for IgA nephropathy, payers have increasing leverage to negotiate. Step therapy requirements, where payers mandate that patients try cheaper alternatives before accessing FILSPARI, could become a headwind. The rare disease pricing assumption that "no alternatives means unlimited pricing power" is eroding as the therapeutic landscape fills in.

Threat of Substitutes: Moderate-High. The competitive picture has transformed in just three years. Where once there were zero approved therapies for IgA nephropathy, there are now four, each with a distinct mechanism of action.

TARPEYO offers an immunosuppressive approach with demonstrated kidney function preservation, but it is a corticosteroid with time-limited dosing and infection risks that make many physicians uncomfortable with long-term use.

Vanrafia provides selective endothelin receptor antagonism without a REMS, making it potentially more convenient for both physicians and patients.

Fabhalta introduces complement inhibition, a mechanistically distinct option that targets the immune system's contribution to kidney damage rather than the hemodynamic and fibrotic pathways that FILSPARI addresses.

Each has differentiated strengths, and the emerging consensus is that combination therapy approaches may become standard, potentially positioning these drugs as complements rather than strict substitutes. But for patients who respond well to a single agent, each approved therapy is a potential substitute for the others, and physician choice will depend on individual patient characteristics, safety profiles, and insurance coverage.

Competitive Rivalry: Moderate. The IgA nephropathy market currently supports four approved therapies with distinct mechanisms, a situation that encourages physician-level competition based on mechanism selection, safety profiles, and real-world evidence. Travere's first-mover advantage provides a real but not permanent edge.

In FSGS, the competitive picture is starkly different. Travere faces no approved competition whatsoever, creating a potential monopoly position if the April 2026 PDUFA decision is favorable. No other company has a drug in late-stage development specifically for FSGS, meaning that even if competitors eventually enter the market, Travere could enjoy several years of exclusivity as the sole approved therapy.

The race across both diseases is not just for existing patients but for earlier-line therapy positioning and combination regimens, with physician relationships and real-world data generation becoming key differentiators. The company that generates the most compelling real-world evidence, showing sustained kidney function preservation in diverse patient populations, will hold a significant advantage in treatment guideline discussions and payer negotiations.

Strategic Analysis: Hamilton's Seven Powers

Scale Economies: Weak. Travere operates in niche markets with inherently limited volumes. Manufacturing scale advantages are minimal because production volumes are small. Sales force efficiency improves modestly with additional indications, since the same representatives calling on the same nephrologists can promote FILSPARI for both IgA nephropathy and FSGS. But this is incremental rather than transformative. The rare disease model is fundamentally not a scale business; it is a premium business, and the economics work not because of high volume but because of high per-unit margins.

Network Economies: Minimal. FILSPARI is a pharmaceutical product, not a platform. There are no meaningful network effects. Patient communities and physician advocacy networks create weak indirect network-like dynamics, where growing physician familiarity and growing real-world evidence make the drug more attractive over time, but these are better understood as learning curve effects than true network economies.

Counter-Positioning: Moderate, Historical. When Retrophin first redirected sparsentan toward rare kidney diseases, large pharmaceutical companies were largely uninterested in ultra-rare glomerular diseases. The patient populations were too small, the clinical trial endpoints too uncertain, and the commercial infrastructure too specialized for companies optimized around blockbuster primary care drugs.

Travere's deep specialization in nephrology allowed it to build expertise and relationships that generalist pharma companies could not easily replicate. This is the classic counter-positioning dynamic that Hamilton Helmer describes: the incumbent's business model makes it irrational for them to respond. For years, a Novartis or Roche would have looked at the IgA nephropathy market and concluded that the revenue potential did not justify the investment required for clinical development and commercial infrastructure. Travere, with lower overhead and no legacy business to protect, could make the economics work.

However, Novartis's aggressive entry through three different mechanisms, spending $3.2 billion on Chinook alone, demonstrates that this counter-positioning advantage has eroded. Once Travere proved that the market was real and that drugs could be approved, the signal-to-noise ratio improved enough for large pharma to act. Large pharma has now validated the market and is investing heavily. The counter-positioning window, perhaps seven to eight years from the sparsentan in-license to Novartis's first approval, was Travere's to exploit, and it did.

Switching Costs: Moderate-High. The REMS program creates real administrative switching costs. Physicians who have established monitoring protocols for FILSPARI, with quarterly liver function tests and patient counseling procedures, are reluctant to abandon those workflows for an alternative that may require different monitoring. Patient reluctance to change a therapy that is controlling their proteinuria is another barrier. Insurance prior authorization processes, which can take weeks to complete, create inertia once a patient is established on a therapy. The REMS modification that simplified monitoring has reduced some of this friction but has not eliminated it.

Branding: Moderate-Strong. FILSPARI's first-to-market status in IgA nephropathy and its potential first-to-market position in FSGS create powerful physician mindshare. Key opinion leaders in nephrology who participated in FILSPARI's clinical trials have become advocates for the drug, publishing papers, presenting at conferences, and educating their peers. Patient advocacy partnerships with organizations like the IgA Nephropathy Foundation and NephCure have deepened Travere's brand resonance within the patient community. The Shkreli legacy required extraordinary brand rebuilding, and the fact that the company successfully completed that transformation is itself a form of brand strength, demonstrating institutional resilience.

Cornered Resource: Moderate. Sparsentan's intellectual property protection extends through approximately 2032 to 2037 with potential extensions. The clinical trial database, including data from DUET, DUPLEX, PROTECT, and growing real-world evidence, represents an information asset that competitors cannot replicate without investing years and hundreds of millions of dollars. Key opinion leader relationships in nephrology, built over a decade of clinical collaboration, create access advantages. The regulatory precedents set with the FDA, including the validation of proteinuria as a surrogate endpoint, benefit the entire field but were established through Travere's pioneering work.

Process Power: Moderate. Travere has developed specialized capabilities in rare disease commercialization, patient support program infrastructure, and nephrology-specific regulatory affairs. These processes are the accumulated knowledge of a decade of rare kidney disease focus and provide operational advantages over less experienced entrants. However, they are ultimately replicable by well-funded competitors willing to invest the time and resources.

The overall assessment of Travere's competitive position through the Seven Powers framework reveals a company whose primary moats are its cornered resource (IP and clinical data), switching costs, and branding. These powers provide an estimated 7 to 12 years of strong protection, beyond which patent expiration and competitive advancement will erode the position. The principal vulnerability is that well-funded competitors, particularly Novartis with its multi-mechanism kidney portfolio, may develop combination therapies or next-generation compounds that offer superior efficacy or convenience.

Bull vs. Bear Case

The Bull Case

Two approved indications, with a potential third in FSGS, address significant unmet needs. The IgA nephropathy population alone includes an estimated 150,000 to 200,000 US patients, while FSGS adds roughly 40,000 diagnosed patients with no approved treatment options. First-mover advantage in both diseases provides physician mindshare and prescribing inertia that competitive entrants must overcome. The September 2024 full approval validated FILSPARI as disease-modifying, not just symptom-relieving, a distinction that matters enormously for physician confidence and payer acceptance.

The international opportunity remains largely untapped. CSL Vifor's European commercialization is in its early stages, and Japan, where IgA nephropathy prevalence is among the highest in the world, represents a significant potential market. Conservative estimates suggest that international markets could eventually contribute 50 percent or more of total FILSPARI revenue.

Label expansion opportunities include pediatric indications (IgA nephropathy and FSGS both affect children and adolescents), earlier disease stages (treating patients before proteinuria becomes severe), and potentially other proteinuric kidney diseases. Pipeline optionality through pegtibatinase for classical homocystinuria adds a second potential franchise.

FILSPARI's revenue growth of 144 percent year-over-year, approaching profitability, and a market capitalization of $2.6 billion make Travere an attractive acquisition target. Recent rare disease M&A transactions establish precedent for substantial premiums, and the company's specialized nephrology infrastructure, particularly its physician relationships and patient support programs, would be difficult and time-consuming for a larger pharma company to build from scratch.

There is also an underappreciated optionality in the FILSPARI molecule itself. Because it blocks both the endothelin and angiotensin pathways, it could potentially be studied in other proteinuric kidney diseases beyond IgA nephropathy and FSGS. Diabetic nephropathy, membranous nephropathy, and lupus nephritis all involve proteinuria as a key disease driver, and while these are larger markets with different competitive dynamics, the dual mechanism that makes sparsentan unique in rare kidney diseases could differentiate it in adjacent indications as well. No studies have been announced in these broader indications, but the scientific rationale exists, and it represents a pipeline optionality that is not reflected in most analysts' models.

The Bear Case

Competition is intensifying faster than many anticipated. Novartis now offers three mechanistically distinct options for IgA nephropathy, including Vanrafia, which targets the same endothelin pathway as FILSPARI but without a REMS requirement. The absence of a monitoring burden is a meaningful commercial advantage in a disease requiring chronic treatment. Additional agents in development, including telitacicept, povetacicept, and mezagitamab, could further fragment the market.

The patent cliff is a structural risk that every branded pharmaceutical company faces. Generic and biosimilar risk becomes relevant for FILSPARI by the early 2030s as core patents begin expiring, though orphan drug exclusivity may extend protection somewhat.

The exact timing depends on patent litigation outcomes and potential pediatric exclusivity extensions, but the window of premium pricing is finite. The liver safety signal, while manageable based on clinical trial data, creates a ceiling on physician comfort. This is particularly true for earlier-stage patients where the risk-benefit calculation is less clear, since prescribing a drug with liver monitoring requirements to a patient whose kidney function is declining slowly feels different than prescribing it to someone facing imminent dialysis.

If long-term post-marketing surveillance reveals more serious hepatotoxicity than clinical trials suggested, the commercial impact could be significant. The FDA could require a boxed warning, additional monitoring, or in an extreme scenario, market withdrawal. While no signal in the clinical data suggests this is likely, the endothelin receptor antagonist class history, including the liver problems that limited bosentan's use, means this risk cannot be dismissed entirely.

The policy environment adds another layer of uncertainty. Reimbursement pressure on rare disease drugs is a systemic trend. While individual orphan drugs have modest budget impact, the sheer number of approved orphan drugs, now numbering nearly 900, means that collectively they represent a substantial and growing share of pharmacy budgets. Payers are scrutinizing pricing more aggressively, and pharmacy benefit managers are increasingly requiring prior authorizations, step therapy, and outcomes-based contracts for rare disease drugs.

The Inflation Reduction Act's drug price negotiation provisions, while currently focused on the highest-spend Medicare Part D drugs, could eventually extend to rare disease therapies. The orphan drug exemption in the current law protects drugs with a single approved indication, but FILSPARI's approval for both IgA nephropathy and FSGS could theoretically remove this protection if the law is interpreted to apply to multi-indication orphan drugs.

The FSGS approval decision on April 13, 2026 carries meaningful binary risk. If the FDA declines approval or requires additional data, the stock would likely decline substantially, and the FSGS market opportunity would be delayed by years. The DUPLEX trial's failure to show a significant eGFR difference makes the approval pathway uncertain, dependent on the FDA's acceptance of proteinuria-based evidence informed by the PARASOL project.

There is also a "myth versus reality" tension worth addressing. The consensus narrative holds that FILSPARI's first-mover advantage is durable and that competition, while intensifying, will not significantly erode its position. The reality is more nuanced. Vanrafia's launch without a REMS requirement is a genuine competitive advantage in a disease requiring chronic treatment, and Novartis's commercial infrastructure dwarfs Travere's. The assumption that the IgA nephropathy market is "big enough for everyone" may prove true, but market share dynamics in rare diseases can shift quickly when a well-funded competitor offers a more convenient alternative. Physician inertia is real, but it cuts both ways: nephrologists who have not yet started prescribing any IgA nephropathy therapy may be equally likely to choose Vanrafia or Fabhalta as FILSPARI, particularly if those drugs require less monitoring.

What to Monitor: The Critical KPIs

For investors tracking Travere's ongoing performance, two metrics matter most.

First, quarterly new patient start forms for FILSPARI. This measures the rate at which new patients are being initiated on therapy and is the single best leading indicator of revenue growth trajectory. The Q4 2025 record of 908 new patient starts established a benchmark; sustained growth above this level would signal deepening market penetration, while deceleration could indicate competitive pressure or market saturation.

Second, the total FILSPARI prescriber base, particularly the proportion of prescriptions coming from new versus existing prescribers. Expanding the prescriber base indicates that FILSPARI is moving beyond early-adopter nephrologists into the broader physician community, a critical milestone for any rare disease drug's commercial maturation. A narrowing prescriber base, conversely, would suggest that growth depends entirely on existing physicians writing more prescriptions, a less durable foundation.

These two KPIs, new patient start forms and prescriber base breadth, together tell the story of whether FILSPARI is achieving the kind of broad-based adoption that supports sustained revenue growth, or whether it is becoming a niche product concentrated among a small number of enthusiastic prescribers. For a rare disease drug, the difference between these two trajectories can be the difference between peak sales of $1 billion and peak sales of $500 million.

Lessons for Founders, Investors, and Biotech Builders

Travere's journey offers several lessons that transcend the specifics of nephrology.

The first and most obvious is that redemption is possible in corporate life, but it is expensive. The company's transformation from Shkreli's scandal-plagued entity to a scientifically credible commercial biotech required a complete cultural reset, including new leadership, new governance, new name, new ticker, and years of patient trust-building. The cost was not just financial (legal settlements, rebranding expenses, the stock price penalty of association) but temporal. Every conversation with a potential partner, investor, or key opinion leader began with the Shkreli question for years. Biotech founders should understand that reputational damage of this magnitude can be overcome, but it demands extraordinary discipline and a willingness to invest in trust-building that generates no immediate financial return.

The second lesson is that focus wins in rare diseases. When Aselage and later Dube took over, they could have maintained Retrophin's diversified portfolio of acquired compounds. Instead, they systematically narrowed the company's focus to rare kidney diseases, eventually concentrating almost entirely on sparsentan. This focus enabled deep nephrology expertise, strong key opinion leader relationships, efficient regulatory interactions with the FDA's nephrology division, and a commercial organization purpose-built for kidney disease specialists. In an industry where many biotechs try to diversify risk by pursuing multiple therapeutic areas, Travere's concentration paid enormous dividends.

The third lesson is that regulatory strategy is as important as clinical science in biotech. Travere's decision to seek accelerated approval based on proteinuria as a surrogate endpoint was not just a tactical choice; it was a strategic bet that shaped the entire development timeline, capital requirements, and competitive positioning. If the company had been forced to demonstrate eGFR preservation as a primary endpoint in the initial filing, the trial would have been longer, more expensive, and the commercial launch would have been delayed by years, potentially allowing competitors to catch up or overtake them. The regulatory strategy enabled first-mover advantage.

The fourth lesson concerns patient advocacy. Travere's partnerships with the IgA Nephropathy Foundation and NephCure were not just corporate social responsibility exercises. These organizations helped with clinical trial recruitment, regulatory advocacy (including supporting the PARASOL initiative), market access, and physician education. In rare diseases, patient communities are small enough that advocacy organizations wield disproportionate influence, and companies that genuinely engage with them gain a competitive edge that money alone cannot buy.